y harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1823.40 DOWN $4.90

SILVER: $21.13 DOWN 4 CENTS

ACCESS MARKET: GOLD $1823.30

SILVER: $21.15

Bitcoin morning price: $21,414 UP 200

Bitcoin: afternoon price: $20.725 DOWN 489

Platinum price: closing DOWN $2.20 to $909.30

Palladium price; closing UP $37.45 at $1879.50

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE:EXCHANGE:

EXCHANGE: COMEX

no. of contracts issued by JPMorgan: 0/9

_____________________________________________________________________________________

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT 9 NOTICE(S) FOR 900 Oz//0.02799 TONNES)

total notices so far: 23,925 contracts for 2,392,500 oz (74.416 tonnes)

SILVER NOTICES:

10 NOTICE(S) FILED 50,000 OZ/

total number of notices filed so far this month 1830 : for 9,150,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $4.90

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//

INVENTORY RESTS AT 1061.04 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 4 CENTS

AT THE SLV// ://BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 3.127 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 542.000 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL SIZED 535 CONTRACTS TO 142,090 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG GAIN IN OI WAS ACCOMPLISHED WITH OUR $0.10 GAIN IN SILVER PRICING AT THE COMEX ON FRIDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.10) AND WERE UNSUCCESSFUL IN KNOCKING OFF SOME SILVER LONGS//BUT MAINLY WE HAD ADDITIONAL SPECULATOR ADDITIONS.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT ADDITIONS /. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 7.635 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 20 CONTRACTS OR 100,000 OZ//NEW STANDING: 9,325,000 / // V) STRONG SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : –3849

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTACTS for 18 days, total 14,270, contracts: 71.350 million oz OR 3.963 MILLION OZ PER DAY. (793 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 71.350 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 75.350 MILLION OZ

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 535 WITH OUR $0.10 GAIN IN SILVER PRICING AT THE COMEX// FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 1380 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 7.635 MILLION OZ FOLLOWED BY TODAY’S 100,000 QUEUE JUMP //NEW STANDING: 9,325,000 OZ // .. WE HAD A VERY STRONG SIZED GAIN OF 1915 OI CONTRACTS ON THE TWO EXCHANGES FOR 9.575 MILLION OZ WITH THE GAIN IN PRICE.

WE HAD 10 NOTICES FILED TODAY FOR 50,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 4715 CONTRACTS TO 496,958 AND FURTHER NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -5618 CONTRACTS.

.

THE STRONG LOSS IN COMEX OI CAME WITH OUR SMALL RISE IN PRICE OF $0.45//COMEX GOLD TRADING/FRIDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERING

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 69.26 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY’S 2500 OZ E.F.P. JUMP TO LONDON //NEW STANDING: 74.715TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $0.45 WITH RESPECT TO FRIDAY’S TRADING

WE HAD A FAIR SIZED LOSS OF 2111 OI CONTRACTS 6.566 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2604 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 496,958

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2111, WITH 4715 CONTRACTS DECREASED AT THE COMEX AND 2604 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 2111 CONTRACTS OR 6.566TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2604) ACCOMPANYING THE GOOD SIZED LOSS IN COMEX OI (4715,): TOTAL LOSS IN THE TWO EXCHANGES 2111 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING AND SOME ADDITION TO SPECULATOR SHORTS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE. AT 69.26 TONNES FOLLOWED BY TODAY’S E.F.P JUMP OF 2500 OZ//NEW STANDING: 74.715 TONNES / 3) SOME LONG LIQUIDATION//SOME SPECULATOR SHORT COVERING//SOME SPECULATOR SHORT ADDITIONS //.,4) GOOD SIZED COMEX OI LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

64,642 CONTRACTS OR 6,464,200 OZ OR 201.06 TONNES 18 TRADING DAY(S) AND THUS AVERAGING: 3591 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAY(S) IN TONNES: 201.06 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 201.06/3550 x 100% TONNES 5.66% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 201.06 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A FAIR SIZED 535 CONTRACT OI TO 142,090 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1380 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1380 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 4354 CONTRACTS AND ADD TO THE 1380 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 1915 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 9.575 MILLION OZ

OCCURRED WITH OUR RISE IN PRICE OF $0.10 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)MONDAY MORNING// SUNDAY NIGHT

SHANGHAI CLOSED UP 29.44 PTS OR 0.88% //Hang Sang CLOSED UP 510.46 PTS OR 2.39% /The Nikkei closed UP 379.30 OR 1.43% //Australia’s all ordinaires CLOSED UP 1.94% /Chinese yuan (ONSHORE) closed UP 6.6893 /Oil UP TO 108.11 dollars per barrel for WTI and UP TO 113.60 for Brent. Stocks in Europe OPENED MOSTLY GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.6893 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6857: /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 4715 CONTRACTS TO 496,958 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED WITH OUR GAIN OF $0.45 IN GOLD PRICING FRIDAY’S COMEX TRADING. WE ALSO HAD A GOOD SIZED EFP (4052 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF JUNE.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2604 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :2604 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2604 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2111 CONTRACTS IN THAT 2604 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED COMEX OI LOSS OF 4715 CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR RISE IN PRICE OF GOLD $0.45.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING JUNE (74.715),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.715 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $0.45) AND WERE UNSUCCESSFUL IN KNOCKING OFF SPECULATOR LONGS/COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS//// WE HAVE REGISTERED A FAIR SIZED LOSS OF 2111 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JUNE (74.715 TONNES)…

WE HAD 5618 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 2111 CONTRACTS OR 211100 OZ OR 6.566 TONNES

Estimated gold volume 145,711/// poor/

final gold volumes/yesterday 150,407 /poor

INITIAL STANDINGS FOR JUNE ’22 COMEX GOLD //JUNE 27

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 244,930.254 oz Brinks HSBC Int. Delaware JPMorgan Malca Manfra includes15 kilobars |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | 109,474.151 oz HSBC (3405 kilobars) |

| No of oz served (contracts) today | 9 notice(s) 900 OZ 0.02799 TONNES |

| No of oz to be served (notices) | 96 contracts 9600 oz 0.2986 TONNES |

| Total monthly oz gold served (contracts) so far this month | 23,925 notices 2,392,500 OZ 74.416 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

No dealer withdrawals

1 customer deposit

i) Into HSBC: 109,474.155 oz 3405 kilobars

total deposits: 109,474.155oz

6 customer withdrawals:

i)Out of HSBC 160,384.619 oz

ii) Out of Brinks: 1692.65 oz

iii) Out of Manfra: 7606.114 oz

iv) Out of Int. Delaware 482.264oz (15 kilobars)

v) JPMorgan: 72,530.156 oz

vi Out of Malca: 2234.450 oz

total withdrawal: 244,930.254 oz

ADJUSTMENTS:2//dealer to customer

Loomis: 32,215.302

Brinks 31,829.490 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 105 contracts having lost 133 contracts

We had 108 notices filed on FRIDAY so we LOST 25 contracts or an additional 2500 oz wil NOTl stand for gold in this very active month of June as they were EFP’d to London

July has a GAIN OF 30 OI to stand at 1406

August has a LOSS of 5506 contracts UP to 406,679 contracts

We had 9 notice(s) filed today for NIL 900 oz FOR THE JUNE 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 9 contract(s) of which 12 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2021. contract month,

we take the total number of notices filed so far for the month (23,925) x 100 oz , to which we add the difference between the open interest for the front month of (JUNE 105 CONTRACTS ) minus the number of notices served upon today 9 x 100 oz per contract equals 2,402,100 OZ OR 74.715 TONNES the number of TONNES standing in this active month of JUNE.

thus the INITIAL standings for gold for the JUNE contract month:

No of notices filed so far (23,925) x 100 oz+ (105) OI for the front month minus the number of notices served upon today (9} x 100 oz} which equals 2,404,600 oz standing OR 74.715 TONNES in this active delivery month of JUNE.

TOTAL COMEX GOLD STANDING: 74.715 TONNES (A STRONG STANDING FOR A JUNE ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,419,784.828 oz 75.26 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 33,183,194,729 OZ

TOTAL ELIGIBLE GOLD: 15,971,174.800 OZ

TOTAL OF ALL REGISTERED GOLD: 17,212,019.929OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 14,792,235.0 OZ (REG GOLD- PLEDGED GOLD)

END

SILVER/COMEX/JUNE 27

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 54,995.058 oz CNT |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,177,291.440 oz |

| No of oz served today (contracts) | 10CONTRACT(S) 50,000 OZ) |

| No of oz to be served (notices) | 35 contracts (175,000 oz) |

| Total monthly oz silver served (contracts) | 1830 contracts 9,150,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposit into the customer account

i) Into CNT 1,177,291.440 oz

total deposit: 1177,291.440 oz

JPMorgan has a total silver weight: 169.419 million oz/334.934 million =50.58% of comex

Comex withdrawals: 1

CNT 54,995.058 oz

total withdrawal 54,995.058 oz

adjustments: 1

dealer to customer

HSBC: 741m295.680 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 70.110 MILLION OZ

TOTAL REG + ELIG. 334.934 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE OI: 45 HAVING GAINED 18 CONTRACTS.

WE HAD 2 NOTICES FILED ON THURSDAY SO WE GAINED 20 CONTRACTS OR AN ADDITIONAL 100,000 OZ WILL STAND IN THIS NON ACTIVE

DELIVERY MONTH OF JUNE

JULY HAD A LOSS OF 6423 CONTRACTS DOWN TO 21,985 CONTRACTS.

AUGUST GAINED 40 CONTRACTS TO STAND AT 1266

SEPTEMBER HAD A GAIN OF 6295 CONTRACTS UP TO 100,199 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 10 for 50,000 oz

Comex volumes:79,503// est. volume today// STRONG

Comex volume: confirmed yesterday: 105,165 contracts ( strong )

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1830 x 5,000 oz = 9,150,000 oz

to which we add the difference between the open interest for the front month of JUNE(45) and the number of notices served upon today 10 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE./2022 contract month: 1830 (notices served so far) x 5000 oz + OI for front month of JUNE (45) – number of notices served upon today (10) x 5000 oz of silver standing for the JUNE contract month equates 9,325,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JUNE 27/WITH GOLD DOWN $4.90 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.04 TONNES

JUNE 24/WITH GOLD UP 45 CENTS TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.70 TONNES FROM THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 23/WITH GOLD DOWN $8.60:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//INVENTORY RESTS AT 1071.77 TONNES

JUNE 22/WITH GOLD UP 15 CENTS:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1073.80 TONNES

JUNE 21/WITH GOLD DOWN $2.00: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1075.54 TONES

JUNE 17/WITH GOLD DOWN $11.25: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.60 TONNES INTO THE GLD.///INVENTORY RESTS AT 1075.54 TONNES

JUNE 16/WITH GOLD UP $28.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.74 TONNES

JUNE 15/WITH GOLD UP $6.50/BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.65 TONNES FROM THE GLD////INVENTORY RESTS AT 1063.74 TONNES

JUNE 14/WITH GOLD DOWN $18.80/NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 13/WITH GOLD DOWN $41.55: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 10/WITH GOLD UP $21.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 9/WITH GOLD DOWN $3.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1065.39 TONNES

JUNE 8/WITH GOLD UP $4.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 7/WITH GOLD UP $7.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AWITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

MAY 31/WITH GOLD DOWN $15.10: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 27/WITH GOLD UP $4.95//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

May 26/WITH GOLD UP $2.10/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 25/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

GLD INVENTORY: 1061.04 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 27/WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 24/WITH SILVER UP 10 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.137 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 23/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 2.029 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 545.137 MILLION OZ//

JUNE 22/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.166 MILLION OZ.

JUNE 21/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.506 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 547.166 MILLION OZ//

JUNE 17/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 739,000 OZ FROM THE SLV./:INVENTORY RESTS AT 543.660 MILLION OZ/

JUNE 16/WITH SILVER UP 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 15/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 14/WITH SILVER DOWN 32 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 13/WITH SILVER DOWN 62 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 10.WITH SILVER UP 13 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 Z FROM THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 9/WITH SILVER DOWN 27 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 923,000 OZ INTO THE SLV////INVENTORY RESTS AT 545.229 MILLION OZ

JUNE 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 544.306 MILLION OZ//

JUNE 7/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.306 MILLION OZ/

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

MAY 31/WITH SILVER DOWN $.41 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST S AT 558.071 MILLION OZ//

MAY 27/WITH SILVER UP 10 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.071 MILLION OZ///

MAY 26/WITH SILVER UP 8 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 558.071 MILLION OZ

MAY 25/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

CLOSING INVENTORY 542.000 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg

LAWRIE WILLIAMS: Volatility continues in gold and equities post big rate hike

The markets have now had time to digest the ramifications of the Fed’s big 75 basis point interest rate hike at last week’s FOMC meeting. To our minds the response has been somewhat illogical. If anything, equities have generally traded stronger, while gold has fallen back, although not particularly significantly in percentage terms.

The trend towards stronger equities at least in part results from the widespread belief that the Fed will reverse its more hawkish approach ahead of the midterm elections and return to some form of Quantitative Easing in order to try and prevent a U.S. recession. Consequently the odds of another 75 basis points rate increase at the July FOMC meeting have fallen right back, and the likelihood of a similar sized rate hike in September has sharply diminished also.

While much of the commentary below specifically relates to U.S. markets, it is these which tend to set the global gold price. Central banks elsewhere tend to follow the Fed’s lead so what happens in the U.S. has worldwide ramifications too.

U.S. economic policy all comes down to the Fed recognising that a high level of inflation is here to stay for the next few months at least and that there is little it can do to slow it down given that the principal drivers are totally outside its control. High, and rising, energy and food prices are being driven by external factors like the Russia/Ukraine war, Russian sanctions and the Chinese lockdowns and there is nothing the Fed can do to slow these down. Its only influence would be on the margins, so the central bank’s logic may be to try and re-stimulate the U.S. economy regardless of the inflationary impact of so doing.

One other parameter over which the Fed has responsibility is the employment, or unemployment, level. The latest four week data on this, which was released yesterday, suggests that employment levels may have peaked in the light of the latest inflation figures, despite an actual small fall in the overall total last week. Anecdotal evidence certainly suggests unemployment may well actually be starting to rise again. We await next month’s figures with interest. These will constitute another factor the Fed will need to take into account when it considers again its future interest rate policy.

Meanwhile other global central banks seem to be reporting equally gloomy figures as the inflation malaise continues worldwide. The Eurozone’s biggest economies – Germany, France and Italy – are all coming up with data which some commentators feel puts the whole Euro currency structure at risk yet again, and UK inflation levels are already at over 9%. The Government here is in disarray and has just lost two significant by-elections, the fall-out from which has to put Prime Minister Boris Johnson’s future increasingly at risk. A full scale General Election is still 2 years away, but there’s no guarantee that Johnson will still be party leader by then.

Is the U.S. heading for recession? In his latest statement Fed chair Powell at least admitted that a recession is indeed possible, despite the Fed’s attempts to ward one off. Indeed it may technically already be in one, and if not is awful close. While the equity and bitcoin markets obviously feel that a full-scale recession may be less likely – hence their tentative mild recoveries – we’re not so sure.

Consensus seems to be swinging towards only a 50 basis point interest rate rise at the July FOMC meeting, in itself a level which might have precipitated an equities slump only a week or so ago. Currently, though, after the 75 basis point rise in June, this seems to be being seen as a bullish factor. But if the July CPI announcement does not show any signs of inflation coming back down, we think another 75 basis point rise would be highly likely again.

We are indeed living in ‘interesting times’ both economically and geopolitically. Should all the doubts these factors raise continue, then inflation will remain elevated and volatility in equity, bitcoin and gold prices will remain. As we have done in the past, we still feel the case for gold and gold stocks remains far more positive than that for equities and bitcoin and that a global recession is almost inevitable. Maybe we are a voice crying in the wilderness, but what will be, will be. Gold investors hold the faith. Hopefully it will help protect you, at least in part, for what may lie ahead.

25 Jun 2022

END

3. Chris Powell of GATA provides to us very important physical commentaries

USA and allies will ban imports of Russian gold which is a very stupid move

(Associated Press/GATA)

U.S. and allies will ban import of Russian gold

Submitted by admin on Sun, 2022-06-26 09:22Section: Daily Dispatches

By Zeke Miller and Darlene Superville

Associated Press

Sunday, June 26, 2022

ELMAU, Germany — President Joe Biden today praised the continued unity of the global alliance confronting Russia, as he and other heads of the Group of Seven leading economies strategized on sustaining the pressure in their effort to isolate Moscow over its months-long invasion of Ukraine.

Biden and his counterparts were meeting to discuss how to secure energy supplies and tackle inflation, aiming to keep fallout from the war from splintering the global coalition working to punish Moscow. They were set to announce new bans on imports of Russian gold, the latest in a series of sanctions the club of democracies hopes will further isolate Russia economically over its invasion of Ukraine. …

Gold in recent years has been the top Russian export after energy — reaching almost $19 billion or about 5% of global gold exports in 2020, according to the White House.

Of Russian gold exports, 90% was consigned to G-7 countries. More than 90% of those exports, or nearly $17 billion, was exported to the UK. The United States imported less than $200 million in gold from Russia in 2019, and under $1 million in 2020 and 2021. …

… For the remainder of the report:

END

The ban on imports from Russia is largely symbolic.

(Bloomberg)

Ban on gold imports from Russia seen as ‘largely symbolic’

Submitted by admin on Mon, 2022-06-27 00:22Section: Daily Dispatches

By Ranjeetha Pakiam

Bloomberg News

Sunday, June 26, 2022

The plan by some Group of Seven nations to ban new gold imports from Russia is “largely symbolic” as flows have already been restricted by sanctions, according to analysts.

The U.S., U.K., Japan, and Canada plan to announce the ban during the G-7 summit that started Sunday in Germany

While the U.K. government said in a statement over the weekend that “this measure will have global reach, shutting the commodity out of formal international markets,” analysts played down the potential impacts as the London Bullion Market Association, which sets standards for that market, removed Russian gold refiners from its accredited list in March. …

… For the remainder of the report:

END

Robert Lambourne is bang on on his calculations of BIS gold swaps. No word on whether the bank imposes sanctions on Russia

(Robert Lambourne)

BIS annual report confirms GATA analysis of gold interventions, avoids Russia issue

Submitted by admin on Sun, 2022-06-26 23:28Section: Daily Dispatches

8a Monday, June 27, 2022

Dear Friend of GATA and Gold:

In his latest report on the gold market interventions of the Bank for International Settlements, appended here, GATA consultant Robert Lambourne is far too modest. For the bank’s annual report, published Sunday, confirms the accuracy of Lambourne’s years of doing monthly calculations of the bank’s gold market interventions — its involvement in gold swaps, about which the bank has been almost completely secret.

The BIS does not candidly provide its level of gold swaps in its monthly reports. The swaps can be calculated from the bank’s monthly reports only by deduction from other data in the reports, which Lambourne studiously undertakes to do. He appears to be the only non-governmental analyst of the bank’s gold market interventions

Five years ago GATA asked the BIS what it does in the gold market, for whom, and why, and whether Lambourne’s monthly calculations of the bank’s gold swap positions were accurate. The bank responded to the inquiry but refused to answer it:

https://www.gata.org/node/17793

Now, with the bank’s annual report yesterday, Lambourne’s calculations and methodology have been vindicated.

During its more than two decades exposing and litigating against gold market manipulation GATA has compiled overwhelming documentation of Western central banking’s policy and mechanisms of controlling the gold price, usually surreptitiously and deceptively, cheating investors and rigging markets throughout the world:

But Lambourne’s work on the BIS’ monthly reports is always the most contemporaneous proof of central bank interventions. His work provides information available only from GATA — information suppressed by the Financial Times, Wall Street Journal, Bloomberg News, and all other mainstream financial news organizations that purport to cover the gold market but more often conceal what is really happening there.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

By Robert Lambourne

Monday, June 27, 2022

The 2021-22 annual report of the Bank for International Settlements was published Sunday —

— and affirms in passing that the bank’s level of gold swaps as of March 31 was 358 tonnes, very close to the estimate of March 31 swaps that was calculated by GATA and reported two weeks ago: about 360 tonnes:

https://www.gata.org/node/21994

The bank’s swaps total appears on Page 179 of the annual report, which is Page 182 of the PDF copy linked above.

The bank’s confirmation of GATA’s calculation for the March gold swaps provides confidence that GATA’s monthly estimates of the swaps, which long have been calculated by GATA from the bank’s monthly statements — not provided candidly and directly by the bank itself — are generally accurate.

At the moment it seems that a downward trend is in place as the swaps have been declining for months.

The annual report also confirms that the BIS has sold none of its own gold, which remains at 102 tonnes. The report shows that the largest contributor to the bank’s comprehensive Income in 2021-22 of 918 million International Monetary Fund Special Drawing Rights resulted from the gain on those 102 tonnes, due to the increase in the gold price over the year. This gain on gold contributed SDR 682 million or 74% of the bank’s total income.

Given gold’s continuing importance to the bank’s annual financial results, the information provided about the bank’s dealings in gold is inadequate, since 358 tonnes of swapped gold involve a huge amount of money and the bank provides no explanation for the swaps..

The annual report also discloses the level of earmarked gold held via the BIS. This is gold in allocated accounts and comprises specific gold bars deposited with the BIS on a custody basis. The report says the BIS holds 378 tonnes of earmarked gold on behalf of other central banks. This compares to 390 tonnes held a year earlier. As the BIS does not have its own gold vaults, it can be safely assumed that this gold is deposited in earmarked accounts at major central banks in gold trading centers, like New York.

The report has a surprising lack of information on the approach of the BIS toward the Russian central bank. This seems ironic insofar as the report was published on a day when several Western countries announced that importing Russian gold was to be banned.

There is no official statement from the BIS confirming whether the bank has imposed its own sanctions against the Russian central bank. On Page 129 of the annual report the BIS confirms that the Russian central bank remains a member. Ordinary accountability in an annual report might call for clarifying the BIS’ relationship with Russia’s central bank.

—–

Robert Lambourne is a retired business executive in the United Kingdom who consults with GATA about the involvement of the Bank for International Settlements in the gold market.

END

BIS urges a decisive wave of interest rate increases to halt inflation

(Reuters)

BIS urges decisive wave of interest rate increases to halt inflation

Submitted by admin on Sun, 2022-06-26 09:31Section: Daily Dispatches

By Mac Jones

Reuters

Sunday, June 26, 2022

LONDON — The central bank umbrella body, the Bank for International Settlements, has called for interest rates to be raised “quickly and decisively” to prevent the surge in inflation turning into something even more problematic.

The Swiss-based BIS has held its annual meeting in recent days, where top central bankers met to discuss their current difficulties and one of the most turbulent starts to a year ever for global financial markets.

Surging energy and food prices mean inflation in many places is now its hottest in decades. But the usual remedy of ramping up interest rates is raising the spectre of recession, and even of the dreaded 1970s-style “stagflation,” where rising prices are coupled with low or negative economic growth.

“The key for central banks is to act quickly and decisively before inflation becomes entrenched,” Agustín Carstens, BIS general manager, said as part of the body’s post-meeting annual report published today. …

… For the remainder of the report:

https://www.reuters.com/markets/europe/global-markets-bis-report-pix-2022-06-26/

END

Several countries have set up renminbi liquidity arrangements with China’s central bank

(Reuters)

China’s central bank, BIS set up renminbi liquidity arrangement

Submitted by admin on Sat, 2022-06-25 22:31Section: Daily Dispatches

By Brenda Goh

Reuters

Saturday, July 25, 2022

SHANGHAI — China’s central bank said today it had signed an agreement with the Bank for International Settlements to establish a Renminbi Liquidity Arrangement that will provide support to participating central banks in times of market fluctuations.

The People’s Bank of China said the arrangement’s first participants, in addition to the PBOC, would include Bank Indonesia, the Central Bank of Malaysia, the Hong Kong Monetary Authority, the Monetary Authority of Singapore, and the Central Bank of Chile.

Each participant will contribute a minimum of 15 billion yuan ($2.2 billion) or the U.S. dollar equivalent, it said.

The BIS said in a separate statement that the funds could be contributed either in yuan or U.S. dollars, and that they would be placed with the BIS, creating a reserve pool.

END

4. OTHER GOLD STORIES

Biden, G-7 Will Ban Russian Gold Imports

SUNDAY, JUN 26, 2022 – 09:56 AM

Having sparked hyperinflation in European gas prices and record energy costs around the globe with their poorly conceived and implemented Russian energy sanctions which have backfired spectacularly, allowing Moscow to reap record energy export profits and China and India to buy oil far below spot prices while leaving US motorists paying record prices at the pump, on Sunday the Biden admin alongside the G-7 announced that they will ban Russian gold imports to “further impose financial costs on Moscow for its invasion of Ukraine.”

The import ban will apply to gold leaving Russia for G-7 countries for the first time, and will be codified by the US Treasury Department on Tuesday.

“The United States has imposed unprecedented costs on Putin to deny him the revenue he needs to fund his war against Ukraine,” Biden tweeted on Sunday, the first day of a G7 meeting in Germany; a formal announcement is expected later on during the summit.

“Together, the G7 will announce that we will ban the import of Russian gold, a major export that rakes in tens of billions of dollars for Russia” he added.

While Western sanctions to punish Russia have largely closed European and US markets to gold from the world’s second-biggest bullion miner, the G-7 pledge would mark a total severance between Russia and the world’s top two trading centers, London and New York, largely a purely symbolic escalation.

“What this does is formalize what the gold industry has already done anyway,” said Adrian Ash, head of research at brokerage BullionVault.

As a reminder, back in March the LBMA, or London Bullion Market Association, removed Russian gold refineries from its accredited list. As a result, shipments between Russia and London have collapsed to almost zero since the invasion of Ukraine.

Furthermore, an executive order signed by Biden on April 15 explicitly prohibits U.S. persons from engaging in gold-related transactions involving Russia’s central bank, the country’s National Wealth Fund or its finance ministry.

While refineries in theory could still import Russian gold directly, most of have sworn off doing so. The association for Swiss refiners, which dominate the industry, denied that its members bought gold from Russia after trade data indicated the nation’s bullion had entered the country.

The official talking point here, encapsulated by the pro-Biden outlet, The Hill, is that “while it does not bring in as much money as energy, gold is a major source of revenue for the Russian economy. Restricting exports to G7 economies will cause more financial strain to Russia as it wages the war in.”

That, of course, is incorrect: the biggest buyers of gold in recent years have not been G7 countries (United States, France, Canada, Germany, Japan, the United Kingdom and Italy), many of whom naively sold much if not all their gold in the recent past and have refused or simply don’t have the funds to restock; instead purchases have all been by developing nation central banks (like India and Turkey, and of course China which however has a habit of only revealing its true gold inventory every decade or so) who have been quietly preparing to do what Russia is doing by dedollarizing and instead allocating capital into a counterparty-free asset.

As for Russia, its central bank has been an aggressive buyer of gold, not seller, and if anything Biden’s decision will only make the gold market the latest to follow the example of oil and bifurcate: cheaper for Russian-friends and much more expensive for Russian enemies.

Still, the Hill is right in that the U.S. and its allies have been searching for more and creative ways to punish Russia for the Ukraine war that recently entered its fifth month. And whereas Biden has announced waves of penalties coordinated with allies that range from sanctions on Russian officials and oligarchs to export controls to sanctions on major Russian banks, so far the Russian ruble, which Biden gladly mocked back in February as “rubble”, has since risen to a seven-year high against the euro.

Meanwhile, Europeans are also limited in what they can do because of their dependence on Russian energy imports. European countries have vowed to phase out Russian oil but have not taken steps like the U.S. to do so immediately because they simply can’t. And the ironic think is that while European should be buying more gold to protect the purchasing power of their currencies ahead of the mass printing tsunami that is coming when the next recession begins, they are now voluntarily barring themselves from doing so.

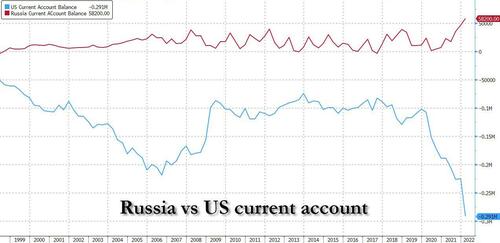

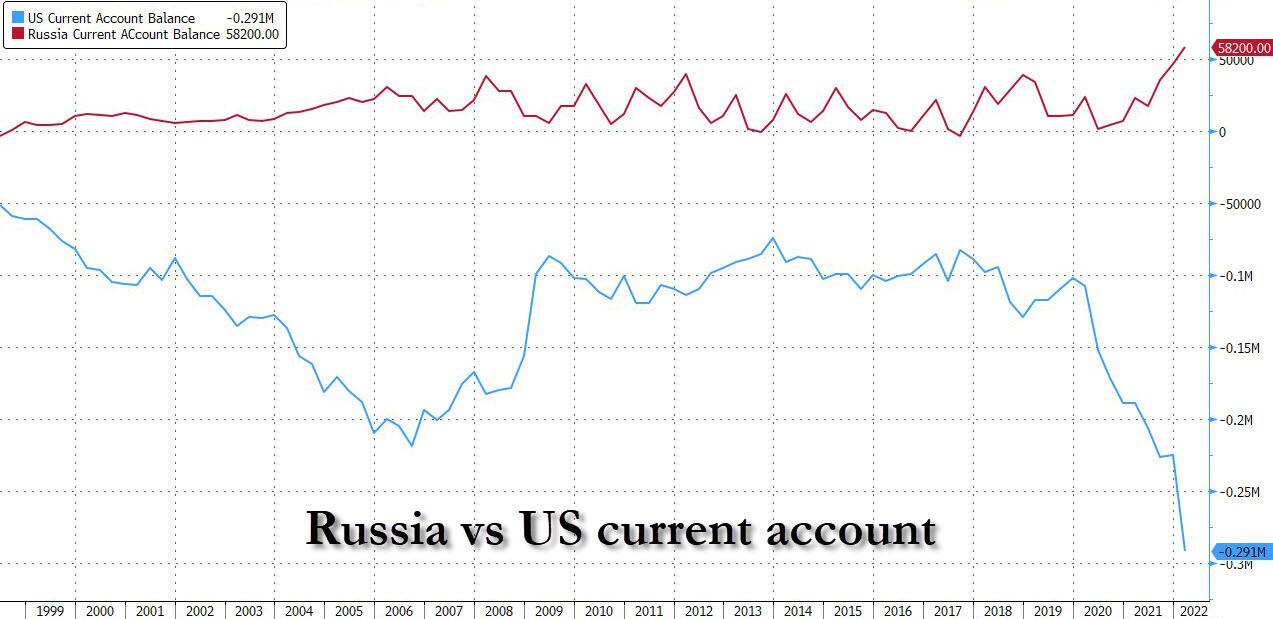

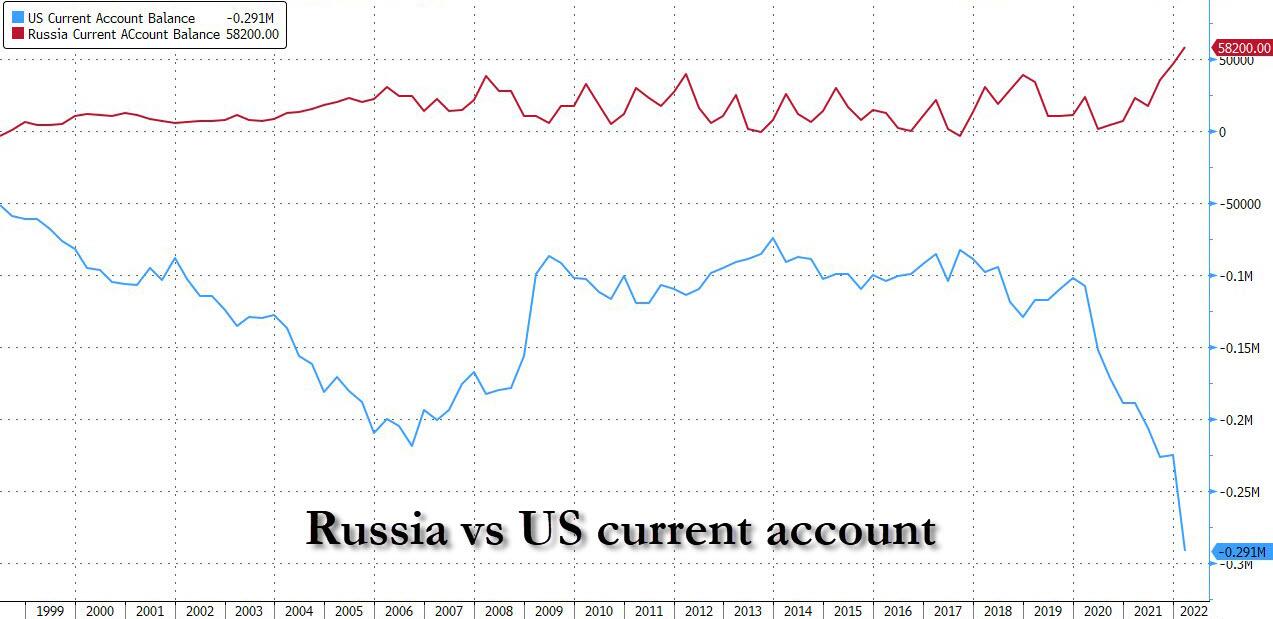

As for “punishing” Russia, here is a chart of the US vs Russian current account balance: guess who is at a record surplus and who is at a record deficit.

Biden administration officials also teased new announcements to squeeze Russia ahead of Biden’s trip to Europe and it’s possible there will be more announcements beyond the plan to ban Russian gold imports. We expect all of them to backfire, especially if Biden decides to also target other Russian metals exports. As a reminder, unlike gold, flows of other metals from Russia such as copper, nickel and palladium have continued uninterrupted as Russia is simply irreplaceable in those supply chains and the commodities industry grapples with managing a long-held relationship with a major supplier of the world’s raw materials.

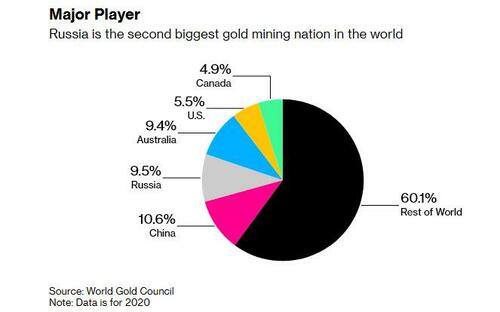

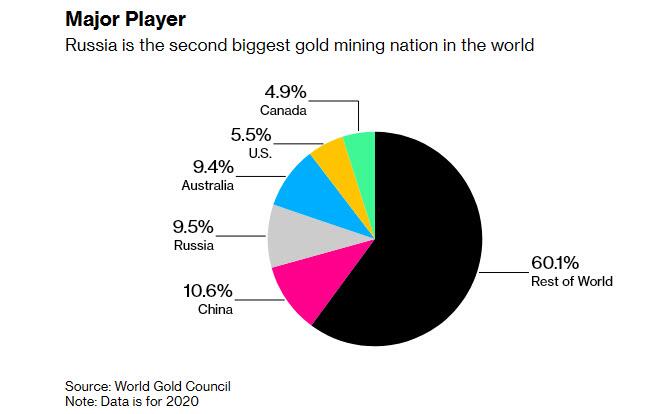

As for the price of gold, what happens when the second biggest gold mining nation in the world and a major source of supply is cut off from the western market…

… even if it is still allowed to transact freely with the “rest of the world” which accounts for roughly 80% of the population, and will most likely simply boost sales to China and the Middle East, both of whom will be happy to continue purchasing Russian gold? We’ll find out in a few hours.

end

5.OTHER COMMODITIES

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings MONDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.6893

OFFSHORE YUAN: 6.6857

HANG SANG CLOSED UP 510.46 PTS OR 2.39%

2. Nikkei closed UP 379.30% OR 1.43%

3. Europe stocks ALL CLOSED MOSTLY GREEN

USA dollar INDEX DOWN TO 103.81/Euro RISES TO 1.0576

3b Japan 10 YR bond yield: RISES TO. +.241/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 135.33/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: UP -// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.54%/Italian 10 Yr bond yield RISES to 3.65% /SPAIN 10 YR BOND YIELD FALLS TO 2.65%…

3i Greek 10 year bond yield RISES TO 3.85//

3j Gold at $1835.00 silver at: 21/45 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 1/4 roubles/dollar; ROUBLE AT 53.19

3m oil into the 108 dollar handle for WTI and 113 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 135.33DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9594– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0146well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.168 UP 4 BASIS PTS

USA 30 YR BOND YIELD: 3.269 UP 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 16.72

Futures, Global Markets Rally, Bonds Slide As Traders Turn More Bullish

MONDAY, JUN 27, 2022 – 08:06 AM

Following the best week for stocks in one month, global stocks extended gains on Monday on continued easing of fears for a hawkish Fed; US futures rose, with the Nasdaq 100 advancing 0.5% as by tech giants Amazon, Apple and Microsoft all rose in premarket trading. Tech shares also boosted indexes in Europe and Asia. Treasuries slipped, pushing the rate on the US 10-year note to 3.17%. Yields have retreated from June highs on growth worries, but whether that marks the end of the Treasury bear market is a live debate. The dollar fluctuated while oil and bitcoin rose.

In the US premarket, major US technology and internet stocks were higher, poised to extend gains. The tech-heavy Nasdaq 100 closed up 7.5% last week, its best week since March. Among notable movers: Apple +0.6%, Microsoft +0.6%, Amazon.com +1%, Meta +0.8%, Nvidia +1.6% in premarket trading. Other notable premarket movers include:

- JD.com (JD US) is among the top performers in US-listed Chinese stocks, rising 5% in premarket trading, after tech investor Prosus disposed of its stake in JD.com for about $3.67 billion.

- Coinbase (COIN US) shares fall 4% in premarket trading as the stock was downgraded to sell from neutral, with a joint Street-low price target of $45 at Goldman Sachs, which cited the “continued downdraft” in crypto prices and drop in industry activity levels.

- Robinhood (HOOD US) shares rise 3.9% in premarket trading as Goldman Sachs analyst William Nance raised the recommendation on the stock to neutral from sell

- Epizyme (EPZM US) jumps 64% to $1.56 in US premarket trading after Ipsen announced the acquisition of the US biotech firm for $1.45/share in cash plus a contingent value right of $1/share.

- Selective Insurance Group (SIGI US) shares may be in focus after Morgan Stanley initiated an overweight rating on the stock, citing a favorable business model that will help the company’s margin to outperform peers.

- Keep an eye on WEC Energy Group (WEC US) as KeyBanc Capital Markets raised the recommendation on the stock to overweight from sector weight, citing “valuation dislocations” triggered by the recent industry volatility.

As Goldman traders speculated over the weekend, Friday’s massive Russell rebalance may have helped flush out any leftover liquidation trades, while the upcoming month- and quarter-end portfolio rebalancing by pensions could boost stocks by as much as 7% this week according to JPM’s Marko Kolanovic. Further boosting bullish sentiment – if only temporarily – one of Wall Street’s biggest bears sees the rally in US stocks extending, prior to the selloff recommencing. Morgan Stanley’s Michael Wilson say the S&P 500 Index may climb another 5% to 7%, before resuming losses.

Meanwhile, investors are also parsing incoming data to work out if the highest inflation in a generation is close to topping out as that will give the Fed latitude to ease up on sharp interest-rate hikes, something the market last week aggressively repriced. A more troubling scenario is of lasting price pressures and tighter policy even as the global economy falters.

“There’s a feeling that things aren’t as bad as we thought they were going to be,” Carol Pepper, founder of Pepper International, said on Bloomberg Radio. She added “there’s a hope that perhaps we’ve oversold, perhaps there’s not going to be a recession.”

Traders are also monitoring a summit of the Group of Seven leaders, who plan to commit to indefinite support for Ukraine in its defense against Russia’s invasion. The G-7 in addition is weighing a price cap on Russian oil. As reported yesterday, the US, UK, Japan and Canada also plan to announce a ban on new gold imports from Russia during the G-7 summit. Prices for the precious metal naturally rose.

European equities trade off session highs as an earlier rally in Asian tech stocks buoys sentiment. Miners, tech and autos are the strongest performing sectors in Europe. Euro Stoxx 50 rallies 1%. DAX outperforms peers, adding 1.2%, FTSE MIB lags, dropping 0.2%. Among notable European stock moves, Prosus NV soared on plans to sell more of its $134 billion stake in Chinese internet giant Tencent Holdings Ltd. to finance a buyback program. Mediobanca SpA fell after the death of Italian entrepreneur Leonardo Del Vecchio, the single largest investor in the bank. Here are some of the biggest European movers today:

- Prosus shares surge as much as 17% in Amsterdam after the tech investor said it will sell down its holding in Tencent to finance an open-ended share buyback program, which could help close the gap between the firm’s market value and the value of the Tencent stake, according to analysts.

- Mining stocks lead gains in the Stoxx 600 Index on Monday as iron ore and base metals recover ground amid signs of improvement in China’s economy. Rio Tinto shares rise as much as 4.4%, Anglo American +4.6%, Glencore +4.2%

- Nordex shares jump as much as 12% after the firm announced a EU139.2m cash injection from Acciona in a bid to increase liquidity and strengthen its balance sheet to shield itself against the risks of short term headwinds in the industry.

- Kion shares rise as much as 7.7% after Morgan Stanley upgraded the stock to overweight from underweight, saying that the structural case for warehouse and forklift companies remains intact even amid a de-rating for the stocks.

- Lundbeck soars as much as 15% after the Danish pharmaceutical company reported positive data in a clinical study of agitation in patients with Alzheimer’s dementia.

- Ocado shares fall as much as 3.1% after the stock was cut to neutral from outperform and PT slashed to 960p from 1,600p at Credit Suisse, with the broker saying new disclosures from the online grocer indicate that its prior assumptions were “too optimistic.”

- Ipsen shares drop as much as 5.1% after the pharmaceutical company announced the acquisition of US biotech Epizyme for $1.45/share in cash plus a contingent value right of $1/share. Analyst had mixed reactions to the deal.

- Mediobanca shares fall as much as 4.4% in Milan after news that Italian entrepreneur Leonardo Del Vecchio, the single largest investor in the bank with a stake of about 19.4%, has died.

- Wise shares drop as much as 5.3% after the money transfer firm said its CEO is facing a probe by UK regulators.

- Tecnicas Reunidas shares tumble as much as 17% after the company said it began arbitrage to recover excess costs in a dispute with the Sonatrach-Neptune Energy consortium over a contract for the Touat Gaz Plant in Algeria.

Elsewhere, Russia defaulted on its foreign-currency sovereign debt for the first time in a century, the culmination of ever-tougher Western sanctions that shut down payment routes.

Earlier in the session, Asian stocks advanced after battered technology shares rebounded as easing recession fears underpinned investor sentiment. The MSCI Asia Pacific Index rose as much as 2.1%, its biggest intraday gain this month, as chip and internet companies including TSMC and Alibaba climbed. Tech-heavy markets such as Taiwan and South Korea extended gains made Friday, while an index of Asian tech stocks rallied for a second straight session after dropping to the lowest since September 2020. Asian equities are bouncing back from a two-year low, as US Treasury yields retreat. Almost all markets in the region rose, with Hong Kong’s Hang Seng Index leading gains and China’s benchmark coming closer to a bull market as Shanghai’s leader declared victory in defending the financial hub against Covid.

A Chinese tech index in Hong Kong advanced 4.7%. Still, the rally in technology shares may be short-lived, as global demand for consumer electronics remains fragile. “Korea and Taiwan have high leverage to tech products, and we’ve seen a lot of that come under pressure so the end demand has slowed down,” Ray Sharma-Ong, investment director at Abrdn Asia, said in an interview with Bloomberg TV. “We expect continued outflows post this relief rally.”

Japanese equities climbed as the latest comments from Federal Reserve officials buoyed sentiment on the economy and a reading on US inflation expectations eased. The Topix Index rose 1.1% to 1,887.42 as of market close Tokyo time, while the Nikkei advanced 1.4% to 26,871.27. Sony Group Corp. contributed the most to the Topix’s gain, increasing 2.3%. Out of 2,170 shares in the index, 1,490 rose and 568 fell, while 112 were unchanged.

Australia’s S&P/ASX 200 index rose 1.9% to close at 6,706, the benchmark’s biggest daily gain since Jan. 28, as investors in Asia assessed whether inflation is bottoming and recession can be averted. The index’s biggest gains were seen in the financial, energy and tech sectors. In New Zealand, the S&P/NZX 50 index closed 1.7% higher at 10,997.92, the benchmark’s best day since March 1

Emerging-market stocks climbed to the highest in more than a week as China’s recovery from its virus-induced slump propels the Asian nation’s equities toward a bull market. Technology stocks led emerging-market equity gains, with China’s economy showing some improvement in June amid a further easing of pandemic curbs in Shanghai. Chinese shares look to be the best home for fresh money in Asia amid a tough investment environment, according to abrdn plc’s regional chairman Hugh Young. China plans to extend the yuan’s trading hours as it seeks to increase global investor participation in onshore currency trading as part of its internationalization push.

In FX, the Bloomberg dollar spot index fell 0.2% as the greenback weakened against all of its Group-of-10 peers apart from the Australian dollar. AUD and CHF are the weakest performers in G-10 FX, SEK and GBP outperform. The volatility term structures for the Group-of-4 currencies focus on the upcoming central bank meetings as there is little demand for long gamma in the front-end. The euro advanced, nearing $1.06 and European bonds fell broadly, with the exeption of Greece and Sweden, as focus turns to ECB President Christine Lagarde’s speech. Sterling rose for a second day, supported by a rally in global stocks that is limiting demand for the dollar. Gilts extended their slide across the curve, while money markets raised BOE tightening bets as haven- buying was unwound amid equity advances.

In rates, Treasuries are weaker amid a selloff in core European rates, which extended losses after EU’s sale of EU2.5b four-year bonds. US yields are cheaper by nearly 4bp at long end, steepening 2s10s by ~2.4bp, 5s30s by ~1bp on the day; 10-year is up 3.6bp at ~3.17% with bunds and gilts lagging by additional 8bp and 5bp in the sector. As Bloomberg notes, the broad risk-asset rally puts added cheapening pressure on Treasury yields with S&P 500 futures and Estoxx50 rising led by big gains for Asia stocks. Two coupon auctions slated for Monday may also weigh: Monday’s auctions include $46b 2- year at 11:30am ET and $47b 5-year notes at 1pm. The WI 2-year yield near 3.07% (vs 2.519% last month) is above auction stops since 2007; WI 5Y near 3.22% (vs 2.736% in May) exceeds results since 2008. IG dollar issuance expectations for the week are around $15b, although remain highly dependent on market conditions. The long- end of the curve may benefit this week from anticipated month- end demand; Bloomberg Indices estimated a 0.07yr Treasury index duration extension for July 1, slightly below 12-month average. In Europe, Gilts underperform Treasuries and bunds, cheaper by about 5-6bps at the long end.

In commodities, industrial metals rebounded, while oil rose. Copper steadied and most other base metals rebounded after their worst week in a year as China’s economy showed signs of recovering and Goldman Sachs said global supplies were still constrained. Oil fluctuated near $107 a barrel in New York as investors monitored developments from the gathering of Group of Seven leaders; G7 leaders met to decide on a Russian oil price cap ahead of Iranian nuclear talks and on the week of the OPEC+ meeting. French CGT unions will participate in strikes at LNG terminals and gas storage facilities this week; strike in the energy sector on June 28th. Most base metals trade in the green; LME tin rises 6.8%, outperforming peers. LME zinc lags, dropping 0.9%. Spot gold maintains gains, adding ~$13 to trade near $1,840/oz. as some G-7 nations plan to announce ban on new gold imports from Russia

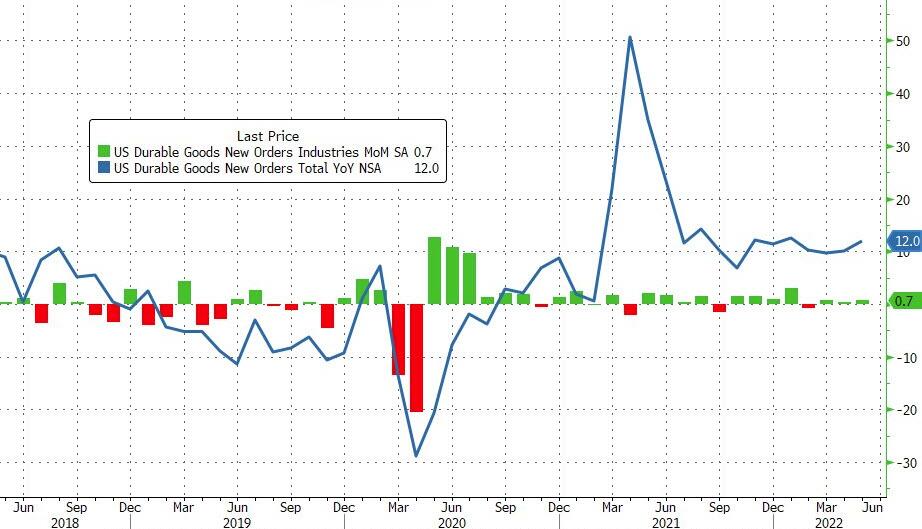

Looking at today’s US calendar, we get the May durable goods orders, capital goods orders, pending home sales, and June Dallas Fed manufacturing index.

Market Snapshot

- S&P 500 futures up 0.7% to 3,944.50

- STOXX Europe 600 up 1.2% to 417.68

- MXAP up 1.6% to 161.83

- MXAPJ up 1.8% to 538.51

- Nikkei up 1.4% to 26,871.27

- Topix up 1.1% to 1,887.42

- Hang Seng Index up 2.4% to 22,229.52

- Shanghai Composite up 0.9% to 3,379.19

- Sensex up 1.2% to 53,368.36

- Australia S&P/ASX 200 up 1.9% to 6,705.95

- Kospi up 1.5% to 2,401.92

- Brent Futures up 0.2% to $113.31/bbl

- Gold spot up 0.7% to $1,840.40

- U.S. Dollar Index down 0.29% to 103.88

- German 10Y yield little changed at 1.49%

- Euro up 0.3% to $1.0580

Top Overnight News from Bloomberg

- ECB policy makers gather on a Portuguese hillside on Monday with the sinking feeling that their rush to tackle the inflation shock they failed to forecast risks both a recession and echoes of the euro area’s sovereign debt crisis

- It was while sitting apparently alone in a London hotel basement that Christine Lagarde engineered a fix to the euro zone’s most alarming debt turmoil since the pandemic struck

- The ECB is pushing back its policy decisions and the timing of the subsequent press conferences by 30 minutes as of July

- The US, UK, Japan and Canada plan to announce a ban on new gold imports from Russia during a summit of Group of Seven leaders that’s getting underway Sunday. Prices of the precious metal climbed Monday

- President Joe Biden rebooted his effort to counter China’s flagship trade-and- infrastructure initiative after an earlier campaign faltered, enlisting the support of Group of Seven leaders at their summit in Germany

- China’s economy showed some improvement in June as Covid restrictions were gradually eased, although the recovery remains muted

- China plans to extend the yuan’s trading hours as it seeks to increase global investor participation in onshore currency trading as part of its internationalization push

- Russia defaulted on its foreign-currency sovereign debt for the first time in a century, the culmination of ever-tougher Western sanctions that shut down payment routes to overseas creditors

- The world economy risks entering a new era of high inflation which central banks need to keep in check, the Bank for International Settlements said

- Signs of distress flashing in bond markets suggest the world’s poorest nations are set to see a wave of debt restructurings. But a growing cohort of investors say that’s a buying opportunity

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were higher across the board as the region took impetus from last Friday’s firm gains on Wall St heading closer into month-end. ASX 200 enjoyed broad gains across its sectors although gold miners lagged as Evolution Mining shares dropped by more than 20% due to a cut in its FY output guidance. Nikkei 225 was lifted after the BoJ’s Summary of Opinions reiterated that they must maintain easy policy and with Tepco among the biggest gainers on tight electricity supply amid the hot weather. Hang Seng and Shanghai Comp. conformed to the upbeat mood as Hong Kong benefitted from a rampant tech sector and with the mainland encouraged by further easing of restrictions in Shanghai and Beijing, while the PBoC also upped its liquidity efforts with a CNY 100bln injection.

Top Asian News

- Beijing will permit schools to resume in-class teaching as soon as Monday, ending one of the last major curbs in the capital, according to Bloomberg.

- Shanghai is to gradually resume dining-in at restaurants from June 29th, according to an official cited by Reuters.

- PBoC injected CNY 100bln via 7-day reverse repos with the rate at 2.10% for a CNY 90bln net injection, according to Reuters.

- China requested that banks make preparations for longer trading hours for the CNY, with trading in the onshore CNY potentially to extend until 03:00 local time the following day (20:00BST/15:00CDT), according to Bloomberg.

- BoJ Summary of Opinions from the June meeting stated the BoJ must maintain easy policy and keep a close eye out on the market and FX impact on the economy and prices. It also noted the number of goods seeing prices rise is increasing due to higher raw material costs and a weak yen but it is appropriate to keep easy policy as inflation is not driven by a positive economic cycle. Furthermore, it said maintaining ultra-easy policy is effective in sustaining a rise in wages and that a sharp fall in Yen would hurt the economy and heighten uncertainty.

- Japanese government issued power shortage warnings for Tuesday, for a second straight day, according to Reuters.

- Japan has proposed removing reference to the goal of 50% zero-emission vehicles by 2030; wants less concrete target, according to a draft cited by Reuters.

- BoJ’s holding of JGBs has reportedly topped 50% of its total, according to Nikkei.

European bourses are kicking off the week on the front-foot as global equities see tailwinds from Wall Street’s bounce on Friday. Sectors in Europe are mostly positive – but Utilities and Insurance are subdued, with the overall picture being a cyclical one. Stateside, US equity futures track sentiment higher – with the NQ the current outperformer vs the ES, YM, and RTY.

Top European News

- ECB says as of the July meeting, the policy decisions will be released at 14:15CET and presser at 14:45CET, according to Reuters.

- ECB’s Pivot Toward Rate Hikes Feeds Fears of New Bond Crisis; ECB to Announce Rate Decisions 30 Minutes Later From July

- EU Confronts Low Gas Storage Risk in Test of Unity on Russia

- Gas Jumps as Europe Struggles to Fill Russian Gap

- UK’s Battered Economy Is Sliding Toward a Breaking Point

FX

- Greenback continues to gravitate as risk sentiment improves, but could get a month end boost given models indicating broad rebalancing requirement – DXY pivots 104.000 within 104.120-103.790 range just shy of last week’s low.

- Yen benefits from all round fix buying ahead of final trading day of June and Q2 on Thursday – Usd/Jpy not far from 134.50 at one stage overnight alongside declined in Yen crosses.

- Pound perks up as IMM spec accounts trim short positions again and Euro tests technical resistance ahead of 1.0600 vs Buck amidst firmer rebound in EGB yields – Cable probes 1.2300 at best, Eur/Usd touches 21 DMA at 1.0591.

- Aussie lags on Aud/Nzd headwinds, but Loonie pares losses in tandem with oil – Aud/Usd sub-0.6950, cross under 1.1000, Nzd/Usd hovering over 0.6300 and Usd/Cad back below 1.2900.

- Yuan underpinned by net PBoC liquidity injection and easing of Covid restrictions in China – Usd/Cnh and Usd/Cny both beneath 6.6900.

- Lira knee jerks higher after Turkey cuts credit to firms with more than Try 15 mn FX cash assets – Usd/Try down to 16.1040 or so before rebound towards 16.8900.

Fixed Income

- Debt futures unwind more recovery gains with EGBs leading the way.

- Bunds retreat towards 146.50 vs 149.00 at one stage last Friday.

- Gilts closer to 113.00 than 114.00 and 10 year T-note near the base of 116-31/117-13 overnight range.

- US durable goods data ahead and a double dose of issuance comprising Usd 46 bn 2 year and Usd 47 bn 5 year auctions.

Commodities

- WTI and Brent futures consolidate with modest intraday losses as G7 leaders meet to decide on a Russian oil price cap ahead of Iranian nuclear talks and on the week of the OPEC+ meeting.

- French CGT unions will participate in strikes at LNG terminals and gas storage facilities this week; strike in the energy sector on June 28th.

- Spot gold piggy-backs off the softer Dollar – with the yellow metal currently eyeing its 21 DMA (1,841.60/oz) and 200 DMA (1,845.20/oz) to the upside

- Base metals are largely rebounding following the recent rout – also aided by the Buck.

US Event Calendar

- 08:30: May Durable Goods Orders, est. 0.2%, prior 0.5%; -Less Transportation, est. 0.3%, prior 0.4%

- 08:30: May Cap Goods Orders Nondef Ex Air, est. 0.1%, prior 0.4%

- 08:30: May Cap Goods Ship Nondef Ex Air, est. 0.2%, prior 0.8%

- 10:00: May Pending Home Sales YoY, prior -11.5%

- 10:00: May Pending Home Sales (MoM), est. -3.9%, prior -3.9%

- 10:30: June Dallas Fed Manf. Activity, est. -6.5, prior -7.3

DB’s Jim Reid concludes the overnight wrap

This morning we are launching our monthly survey which hopefully comes at an opportune time to assess what you all think about recession risk, whether the next big move in markets will be up or down, whether the BoJ will be able to hold the line on YCC, whether your market view includes the risk of Russian gas being cut off from Europe, and whether you think negative rates will be seen again in the next decade after the ECB likely moves away from it by September. There are a couple of other repeat questions to answer. It should take 2-3 minutes, is all anonymous, with answers likely Thursday morning. The link is here and all help gratefully received.

A reminder that my chart book was out last week with lots of charts on one of the worst H1s in history, recession risks and lots more. See here for more.

Without having a blockbuster event to look forward to this week there are plenty of things to keep us occupied in what are highly uncertain times. Perhaps the ECB’s Forum on Central Banking in Sintra will be the key event to watch, with a policy panel on Wednesday which will bring together Chair Powell, President Lagarde and Governor Bailey together the likely highlight.

Staying in Europe, all eyes will be on the June CPI numbers released for Germany (Wednesday), France (Thursday) and Italy and the Eurozone on Friday. Consensus expectations don’t suggest we’re yet at peak headline inflation with CPI expected to pick up a few tenths YoY this week. With commodity prices fading sharply in June the hope is that we will be near the top soon. In fact, our US economists put out an inflationary chart book last week that suggested that the peak will be in September (9.1% headline and 6.3% core).

The problem is that even if headline dips because of energy, core won’t necessarily fall as quickly with wages and second round effects in full force. We had a small indicator of that last week as our economists also pointed out that the recent acceleration in US hospital workers’ wage growth from around 2.5% to almost 5% should serve to add an additional 50bps to core PCE inflation next year (link here). On Thursday, we’ll get the latest reading of the US core PCE deflator within the personal income and spending data. Core PCE is the Fed’s preferred inflation measure so this and the healthcare news is important.

Staying with US data, we have a fair amount to look forward to with the all important ISM on Friday (53.2 expected vs 56.1 last month). We’ll also see the Chicago PMI on Thursday and regional Fed’s manufacturing indices throughout the week. Durable goods orders (today) and wholesale and retail inventories (tomorrow) will be key to assessing inventory pressures flagged by several firms in recent weeks as well as corporate behaviour amid some easing in supply-chain backlogs.

How the consumer is faring under rising rates and stubborn inflation will be another key theme, with the Conference Board’s June consumer confidence index out tomorrow (99.9 expected vs 106.4 last month). Elsewhere, China’s industrial data and PMIs (Thursday), as well as key economic indicators from Japan, will be in focus.

Even though we at the very back end of Q2 earnings, this week will see some bellwether consumer spending companies such as Nike (Monday), H&M and General Mills (Wednesday) report. Other corporates releasing results will include Prosus (Monday), Micron and Walgreens Boots Alliance (Thursday).

Overnight in Asia, equity markets are continuing last week’s rally with the Hang Seng (+2.72%) leading gains thanks to a strong performance in Chinese tech firms. The Kospi (+2.08%), Nikkei (+1.04%), Shanghai Composite (+0.89%) and CSI (+1.24%) are all also up.