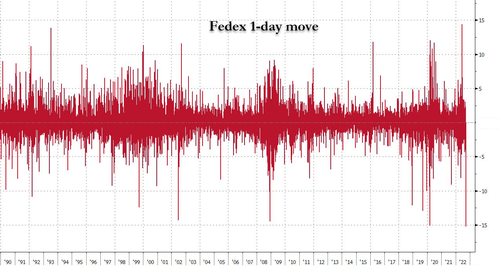

SEPT 16/GOLD CLOSED UP $5.70 TO $1674.50//SILVER CLOSED UP $0.08 TO $1937//PLATINUM WAS DOWN $2.49 TO $906.50//PALLADIUM WAS DOWN $23.40 TO $2123.10//FED EX WARNS THE WORLD THAT WE ARE IN A DEEP RECESSION AND THEY WILL NO LONGER GIVE FOREWARD GUIDANCE//DOW WAS DOWN 139.60//COVID UPDATES/DR PAUL ALEXANDER//VACCINE IMPACT/CHINES YUAN BREAKS THE 7 BARRIER AND THE BRITISH POUND AT ITS ALL TIME LOWS BREAKING 1.14//EUROPEAN/UK UPDATES ON THEIR ENERGY CRISIS//SWAMP STORIES FOR YOU TONIGHT//

323 C HSBC 237 435 H SCOTIA CAPITAL 31 624 H BOFA SECURITIES 6 657 C MORGAN STANLEY 2 661 C JP MORGAN 454 188 737 C ADVANTAGE 3 1 800 C MAREX SPEC 6 4 905 C ADM 6

total notices so far: 5333 contracts for 533,300 oz (16.587 tonnes)

SILVER NOTICES: 59 NOTICES FILED FOR 295,000 OZ/

total number of notices filed so far this month 6478 : for 32,140,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $5.70

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: //// A DEPOSIT OF 1.45 TONNES FROM THE GLD/

INVENTORY RESTS AT 962.01 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $.08

AT THE SLV// ://BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 2.58 MILION OZ INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 469.630 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A VERY STRONG SIZED 1161 CONTRACTS TO 134,504. AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.25 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.06) AND WERE SUCCESSFUL IN KNOCKING OFF SOME SPEC SILVER LONGS AS WE HAD A STRONG LOSS OF 868 CONTRACTS ON OUR TWO EXCHANGES,; WE DID HOWEVER HAVE STRONG SPECULATOR SHORT LIQUIDATIONS

WE MUST HAVE HAD: I) SOME SPECULATOR SHORT LIQUIDATIONS AND SOME SPEC SHORT ADDITIONS ////CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 205,000 OZ QUEUE JUMP / // V) STRONG SIZED COMEX OI LOSS/(//CONSIDERABLE SPEC LIQUIDATION/)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -166

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTACTS for 11 days, total 10,382 contracts: 51.910 million oz OR 4.719 MILLION OZ PER DAY. (943 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 51.910 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 51.910 MILLION OZ///

RESULT: WE HAD A VERY STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1161 WITH OUR $0.25 LOSS IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 127 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /GOOD BANKER ADDITIONS A// SOME SPEC SHORT LIQUIDATIONS AND CONSIDERABLE SPEC SHORT ADDITIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 205,000 OZ QUEUE JUMP // .. WE HAD A VERY STRONG SIZED LOSS OF 1034 OI CONTRACTS ON THE TWO EXCHANGES FOR 5.170MILLION OZ AS..THE SPECS STILL BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 59 NOTICE(S) FILED TODAY FOR 295,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 6863 CONTRACTS TO 471,278 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY:—1440 CONTRACTS.

.

THE STRONG SIZED INCREASE IN COMEX OI CAME DESPITE OUR FALL IN PRICE OF $30.20//COMEX GOLD TRADING/THURSDAY / WE MUST HAVE HAD MAJOR SPECULATOR SHORT ADDITIONS ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND /STRONG SPECULATOR SHORT ADDITIONS//CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 8.401 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 69,200 OZ //NEW STANDING 17.863 TONNES

YET ALL OF..THIS HAPPENED WITH OUR FALL IN PRICE OF $30.20 WITH RESPECT TO THURSDAY’S TRADING

WE HAD AN ATMOSPHERIC SIZED GAIN OF 15,282 OI CONTRACTS 47.53 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 8419 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 471,278

IN ESSENCE WE HAVE A GIGANTIC SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 16,722 CONTRACTS WITH 8303 CONTRACTS INCREASED AT THE COMEX AND 8419 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 16,722 CONTRACTS OR 52.012 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (8419) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (8303): TOTAL GAIN IN THE TWO EXCHANGES 15,282 CONTRACTS. WE NO DOUBT HAD 1) MAJOR SPECULATOR SHORT ADDITIONS// CONTINUED GOOD BANKER ADDITIONS//MINOR SPECULATOR SHORT COVERINGS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 8.409 TONNES FOLLOWED BY TODAY’S QUEUE. JUMP OF 69,200 oz. 3) ZERO LONG LIQUIDATION//// //.,4) STRONG SIZED COMEX OPEN INTEREST GAIN 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

29,166 CONTRACTS OR 2,916,600 OZ OR 90.72 TONNES 11 TRADING DAY(S) AND THUS AVERAGING: 2651 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAY(S) IN TONNES: 90.72 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 90.72/3550 x 100% TONNES 2.56% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 90.72 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT., FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER,FELL BY A HUGE SIZED 1161 CONTRACT OI TO 134,504 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 127 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 127 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 127 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1161 CONTRACTS AND ADD TO THE 127 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF 1034 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 5.17 MILLION OZ

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

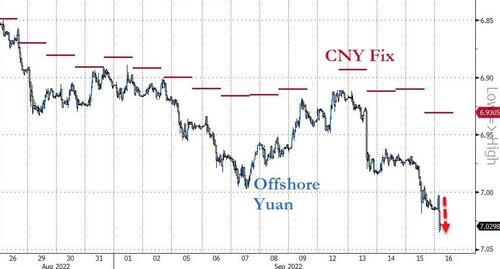

SHANGHAI CLOSED UP 73,52 PTS OR 2.30% //Hang Sang CLOSED DOWN 168.69 PTS OR 0.89% /The Nikkei closed DOWN 308.26 OR 1.11%. //Australia’s all ordinaires CLOSED DOWN 1.51% /Chinese yuan (ONSHORE) closed DOWN AT 7.0097//OFFSHORE CHINESE YUAN DOWN 7.0222// /Oil DOWN TO 85.76 dollars per barrel for WTI and BRENT AT 91.76 / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 6863 CONTRACTS TO 471,278 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS STRONG COMEX INCREASE OCCURRED DESPITE OUR HUGE FALL IN PRICE OF $30.20 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (8419 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 8419 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :8419 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 8419 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: AN ATMOSPHERIC SIZED SIZED TOTAL OF 15,282 CONTRACTS IN THAT 8419 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI GAIN OF 6863 CONTRACTS..AND THIS GIGANTIC GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR HUGE FALL IN PRICE OF GOLD $30.20. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING SEPT (17.863),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 17.863 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $30.20) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A GIGANTIC SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 15,282 CONTRACTS // COMMERCIAL LONGS HUGELY ADDED TO THE POSITIONS, AND SPECULATOR SHORTS ADDED TO THEIR POSITIONS////// WE HAVE REGISTERED AN ATMOSPHERIC SIZED GAIN OF 52.012 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR SEPT. (17.863 TONNES)…

WE HAD XXX CONTRACTS ADDED FROM COMEX TRADES. THESE WERE ADDED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 15,282 CONTRACTS OR 1,528,200 OZ OR 47.53 TONNES

Estimated gold volume 214,328/// fair//

final gold volumes/yesterday 288,236/ fair

INITIAL STANDINGS FOR SEPT ’22 COMEX GOLD //SEPT 16

Total monthly oz gold served (contracts) so far this month

5333 notices 533,300 OZ 16.587 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

2 customer withdrawals:

i) Out of Brinks: 22,698.610 oz 706 kilobars

ii) Out of JPMorgan: 16,075.500 oz (500 kilobars)

total: 38,774.110 oz

total in tonnes: 1.206 tonnes

Adjustments: 1

JPMorgan/dealer to customer: 97,571.154 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPT.

For the front month of SEPT we have an oi of 879 contracts having GAINED 492 contracts .

We had 200 notices filed on THURSDAY so we gained 692 contracts or an additional 69,200 oz

will stand for gold in this very non active delivery month of September.

October LOST 1024 contracts DOWN to 42,068

November LOST 83 contracts to stand at 234

December GAINED 7030 contracts UP to 383,036

We had 469 notice(s) filed today for 46,900 oz FOR THE SEPT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 454 notices were issued from their client or customer account. The total of all issuance by all participants equate to 469 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 188 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2022. contract month,

we take the total number of notices filed so far for the month (5333) x 100 oz , to which we add the difference between the open interest for the front month of (SEPT 879 CONTRACTS) minus the number of notices served upon today 469 x 100 oz per contract equals 574,300 OZ OR 17.863 TONNES the number of TONNES standing in this NON active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month:

No of notices filed so far (5333) x 100 oz+ (879) OI for the front month minus the number of notices served upon today (469} x 100 oz} which equals 574,300 oz standing OR 17,863 TONNES in this NON active delivery month of SEPTEMBER.

TOTAL COMEX GOLD STANDING: 17.863 TONNES (A GREAT STANDING FOR A SEPT ( NON ACTIVE) DELIVERY MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 6428 x 5,000 oz = 32,140,000 oz

to which we add the difference between the open interest for the front month of SEPT(191) and the number of notices served upon today 59 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT./2022 contract month: 6,428 (notices served so far) x 5000 oz + OI for front month of SEPT (191) – number of notices served upon today 59) x 5000 oz of silver standing for the SEPT contract month equates 32,800,000 oz. .

We have an inventory of 44.516 million oz of registered silver at the comex so Sept delivery of 32.800 MILLION OZ represents 73.68% of that category of silver.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

SEPT 13/WITH GOLD DOWN $22.85 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73ONNES FROM THE GLD////INVENTORY RESTS AT 964.91 TONNES

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

AUGUST 31.WITH GOLD DOWN $10.20:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.24 TONNES FROM THE GLD////INVENTORY RESTS AT 973.37 TONNES

AUGUST 30.WITH GOLD DOWN $12.00:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 980.61 TONNES

AUGUST 29/WITH GOLD DOWN $.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD/////INVENTORY RESTS AT 982.64 TONNES

AUGUST 26/WITH GOLD DOWN $26.60; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 25/WITH GOLD UP $9.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 18/WITH GOLD DOWN $5.25: GIGANTIC CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.78 TONNES FROM THE GLD////INVENTORY RESTS AT 985.83 TONNES

AUGUST 17/WITH GOLD DOWN $12.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 992.20 TONNES

AUGUST 16/WITH GOLD DOWN $7.85: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 993.94 TONNES

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

GLD INVENTORY: 962.01 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

SEPT 13/WITH SILVER DOWN $.31 TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.899 MILLION OZ//

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

AUGUST 31/WITH SILVER DOWN 36 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 3.087 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 465.573 MILLION OZ//

AUGUST 30/WITH SILVER DOWN 34 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 1.478 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 470.135 MILLION OZ//

AUGUST 29/WITH SILVER DOWN 7 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY A THE SLV: A WITHDRAWAL OF 2.765 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 470.135 MILLION OZ//

AUGUST 26/WITH SILVER DOWN 39 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 25/WITH SILVER UP 21 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

AUGUST 18/WITH SILVER DOWN 27 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 369,000 OZ INTO THE SLV////INVENTORY RESTS AT 485.482 MILLION OZ//

AUGUST 17/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.106 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.113 MILLION OZ//

AUGUST 16/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 486.219 MILLION OZ/

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

CLOSING INVENTORY 469.63 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

There are 435 seats in the House of Representatives (not counting nonvoting seats for D.C. and some U.S. possessions) and all of them are up for election in November. Right now, the Democrats control the House with 219 Democrats versus 211 Republicans (there are five vacancies).

It takes 218 votes to control the House. This means if the Republicans hold the seats they have and pick up just seven seats from Democrats, they will control the House.

Will this happen? The 2022 election cycle is more challenging to predict than usual because it’s the first election since the 2020 Census that the House map had redrawn to reflect population gain or loss on a state-by-state basis.

Texas gained two House seats, while Colorado, Florida, Montana, North Carolina and Oregon gained one each. The losers were California, Illinois, Michigan, New York, Ohio, Pennsylvania and West Virginia, which lost one seat each.

The new district maps favor Republicans on the whole. Another factor favoring the Republicans is that voters often turn back to the party opposing the incumbent president, either out of dissatisfaction with their presidential choice or simply to balance the scales in ways that keep any one party from becoming too powerful.

The average loss for the president’s party in a first-term midterm since 1982 was 30 seats. If that were the only information I had, my forecast would be that the Republicans would gain 30 seats this November. That would put the House at 241 Republicans and 189 Democrats, a solid 47-seat majority.

Interestingly, a RealClearPolitics forecast based on the average of numerous polls has a forecast of 219 Republicans and 182 Democrats, with 34 seats in the too-close-to-call category.

If those toss-ups were decided in the same ratio as the likely winners (55% Republican to 45% Democrat), that would sort the undecided into 19 Republicans and 15 Democrats. That would produce a final House of 238 Republicans and 197 Democrats, almost exactly the result that the historical track record predicts.

But can we go beyond statistics and polls to discern idiosyncratic factors that could push the results away from the central tendency? There are two.

The first is the trend of Hispanics and African-Americans toward Republicans and away from Democrats.

The Hispanic vote has historically been around 70% for Democrats, but recent polls show the Republicans may capture more than 50% of the Hispanic vote this time because Hispanics are trending conservative and are culturally anti-abortion, anti-crime and in favor of controlling the border.

Hispanics make up about 20% of the total population. If you shift 20% of voters by 20% in preference, that yields a 4% gain for Republicans in the overall vote. With many districts split close to 50/50, a four-point pickup is huge. We’ve already seen this dynamic with Republican gains in seats on the Texas/Mexican border that were solidly Democratic until this year.

The same trend is clear in the African-American community. They are 12% of the electorate and vote about 90% Democrat. However, recent voting results and polls show that the African-American vote could go as much as 20% for Republicans this time.

A 10% gain in a 12% community adds another 1.2% to the Republican column. Crime and the economy are the big issues for African-Americans. Combined with the Hispanic shift, this could put over five percentage points in the Republican column, enough to tip a lot of close races to Republicans.

The second trend that could push the results away from statistical tendencies is Biden’s very low approval ratings. Right now, Biden’s approval rating is 41.8% based on the average of 11 major polls. However, the polls contained in the average include some conducted as long ago as Aug. 15 (Marist) or Aug. 12 (NBC News) when Biden was riding high based on some legislative accomplishments.

The more recent polls show Biden at 38% approval (Reuters, Aug, 30). So it is likely that Biden is in a real-time downtrend back toward the 39% level he held most of the summer.

Based on these idiosyncratic variables, it seems reasonable to push the expectation of 241 Republicans and 189 Democrats to an adjusted result of 245 Republicans to 185 Democrats, a 34-seat gain for Republicans, leading to a 60-seat Republican majority.

In summary, my forecast for the 2022 midterm House result as of now is: Republicans – 245 seats, Democrats – 190 seats.

Forecasting the outcome in the Senate is both easier and harder than forecasting the House. It’s easier because there are fewer races and even fewer contests that are genuinely competitive. It’s harder because the smaller sample size makes it more difficult to use statistical methods. We have to go state by state and candidate by candidate to produce an accurate forecast.

The Senate has 100 members, two from each state. The current split is 50 Democrats/independents and 50 Republicans. Under the Constitution, the president of the Senate, Kamala Harris (the vice president), can break a tie vote.

This puts the Democrats in control of the Senate even with the 50/50 split.

There are 35 Senate seats in play this election. The Republicans are at a slight disadvantage going in because they currently hold 21 of the 35 seats being contested, whereas the Democrats only have to defend 14 seats. The good news for Republicans is that 16 of the 21 seats they are defending are rated “Solid” or “Likely” to stay Republican by The Cook Political Report.

The Democrats have nine out of 14 seats they are defending rated “Solid” or “Likely.” This means that only 10 of the 35 Senate seats in this election are truly competitive. Control of the Senate will come down to those 10. The Republicans and Democrats currently hold five of the competitive seats each.

To control the Senate, either party has to hold their five competitive seats and take one from the other party. If you lose a seat, you have to pick up another just to stay even. It’s that close.

My current best estimate is that Republicans will retain Florida, North Carolina and Ohio. Likewise, the Democrats should retain their seats in Colorado and New Hampshire. This means control of the Senate comes down to Arizona, Georgia, Nevada, Wisconsin and Pennsylvania.

If that list seems familiar it should. Those were the same five states that were hotly contested in the 2020 presidential race. All five went for Biden. Although those remaining races are all close, I rate Nevada and Georgia as wins for Republicans.

Those two wins represent a pickup of two Senate seats for Republicans since both are currently held by Democrat incumbents. I rate Arizona a win for Mark Kelly, which is a hold for the Democrats.

Wisconsin and Pennsylvania are both extremely close, but right now one would have to rate those as wins for the Democrats. That’s a pickup of two for the Democrats since both seats are currently held by Republicans.

If that forecast holds, we’re back to a 50-50 Senate. A few states would change from Democrat to Republican (Nevada and Georgia) or from Republican to Democrat (Wisconsin and Pennsylvania) but the total 50-50 split would be unchanged.

I have one other forecast: The current forecast will change. They always do when you’re still two months away.

We could see Arizona, Pennsylvania and Wisconsin tip Republican over the next two months. Georgia could remain in the Democratic column. All I can say is I’ll be watching closely and keeping you updated every step of the way.

A prudent investor would keep an above-average allocation to cash, both to withstand the volatility from potential wild cards and to profit from attractive entry points on certain assets while others are losing fortunes.

Strap in, it’s going to be a bumpy but fascinating ride.

GOLD/SILVER

END

3.Chris Powell of GATA provides to us very important physical commentaries

More central banks are engaging in gold lending and swaps and probably cannot get their physical gold back

(Central Banking Magazine/London/GATA)

More central banks engaged in gold lending and swaps last year

Submitted by admin on Thu, 2022-09-15 20:12Section: Daily Dispatches

“Ninety-nine-point-nine percent of the central bankers I know don’t even know they have gold in their vault. They don’t spend one millisecond thinking about gold during the day. It’s not on their agenda, so to think that they try to manipulate gold to suppress the gold price — forget it. They don’t even think about it.”

— Pierre Lassonde, founder and chairman emeritus of Franco-Nevada Corp., former president of Newmont Mining, and former chairman of the World Gold Council, during an interview with MineWeb in October 2013.

More Central Banks Engage in Gold Lending and Swaps

From Central Banking magazine, London Thursday, September 15, 2022

The number of central banks active in gold lending and swaps increased slightly last year, the Reserves Benchmarks 2022 reveal.

Overall, 12 (27.27%) of the 44 participating central banks said they are active in these activities. This is slightly higher than the 10 central banks engaged in these transactions among the 44 participants in last year’s study.

Additionally, just under half (47.73%) of institutions said they use derivatives for currency hedging. And over 60% resort to securities lending

end

Chris Powell

GATA

end

Your weekend reading material. This one is extremely important!!

(Alasdair Macleod)

Alasdair Macleod: Inflation is turning hyper

Submitted by admin on Thu, 2022-09-15 11:54Section: Daily Dispatches

By Alasdair Macleod GoldMoney, Toronto Thursday, September 15, 2022

Money supply took off during covid lockdowns. It is now about to take off again to pay everyone’s energy bills. But that is not all.

Demands for currency and credit to be conjured out of thin air to pay for everything will be coming thick and fast. Expectations that energy prices, including European electricity, have peaked are naïve. Putin has yet to put the winter and spring screws on Europe and the world fully. It will be surprising if global oil and natural gas prices in Europe are not significantly higher on a twelve-month view. And Europe has messed up its electricity supplies — that is where the energy costs

Bankers are trying to reduce their loan exposure to rising interest rates, undermining GDP. Besides paying for everyone’s energy bills, rescuing troubled banks, collapsing tax revenues, and difficulties in selling government debt on rising yields, governments are expected to apply economic stimulus to support both their economies and financial markets.

Furthermore, this article points to evidence as to why the expansion of central bank credit has a far greater impact on prices than contracting bank credit. The replacement of commercial bank credit by central bank credit will have a far greater inflationary impact than the deflation from bank credit alone.

Attempts to rescue the American, European, and Japanese economies by replacing commercial bank credit with central bank credit will probably be the coup de grace for fiat.

We can begin to anticipate the path to the destruction of purchasing power for all fiat currencies, not just those of Zimbabwe, Turkey, and Venezuela et al. A global hyperinflation is proving impossible to avoid. …

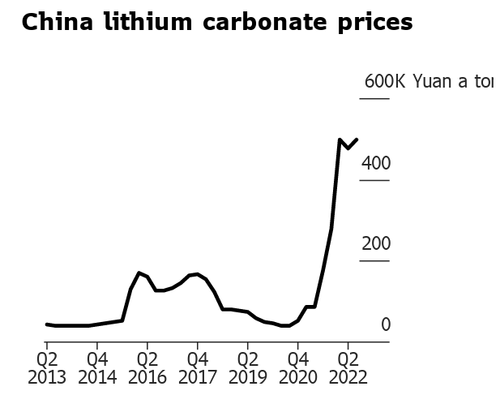

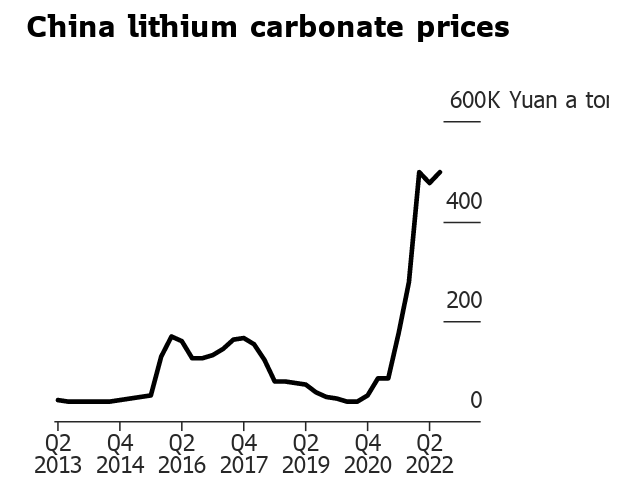

Lithium prices hit new record and thus electric vehicle affordability concerns are amounting

(zerohedge)

Lithium Prices Hit New Record As EV Affordability Concerns Mount

FRIDAY, SEP 16, 2022 – 01:44 PM

While California banned the sale of new gas-powered cars by 2035, and the Biden administration unveiled $900 million in new funding to build electric vehicle charging stations, rising lithium prices could derail the EV revolution.

The progressive view is that EVs will save the planet from catching on fire because green vehicles would eliminate the harmful carbon emissions of fossil fuel vehicles. Though a widespread rollout of EVs depends on affordability, and EVs are way more expensive than gas-powered.

Bloomberg reported lithium carbonate, a key metal in EV batteries, hit a new record high in China this week. Per ton, prices jumped to 500,500 yuan ($71,315), more than triple the price versus last year.

The global surge in lithium prices has increased the cost of EV batteries. Tesla hiked vehicle prices several times this summer (see: here) because of rising battery costs.

A steady increase in demand for global EVs combined with a recent power crunch in Sichuan province, a region that produces 20% of China’s lithium production, resulted in the disruption of output and tighter supplies, hampering an already-squeezed global market.

Research firm Rystad Energy said a second energy crisis could materialize in China this winter when heating demand soars:

“This could lead to new power shortages and hit lithium operations,” it noted, expecting lithium prices to stay elevated for the rest of the year.

Soc. Quimica & Minera de Chile SA, the world’s second-largest lithium producer, warned investors Thursday of a “very tight market” in the years ahead and sees higher prices.

The expectation that EVs would become affordable for the masses is a distant pipedream because of the high costs associated with battery production.

At least half of an EV battery includes lithium, nickel, manganese, and cobalt, four metals that have surged this past year. Also, let’s not forget China controls the world’s rare earth mineral trade…

The surge in lithium prices and other critical metals for EV batteries is a significant concern that could derail the EV revolution due to affordability concerns.

end

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.0097

OFFSHORE YUAN: 7.0222

SHANGHAI CLOSED: DOWN 73.52 PTS OR 2.30%

HANG SENG CLOSED DOWN 168.69 PTS OR 0.89%

2. Nikkei closed DOWN 308.26 PTS OR 1.11%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 109.66/Euro FALLS TO 0.9974

3b Japan 10 YR bond yield: RISES TO. +.249/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 143.02/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.766%/Italian 10 Yr bond yield FALLS to 4.05% /SPAIN 10 YR BOND YIELD RISES TO 2.92%…

3i Greek 10 year bond yield FALLS TO 4.26//

3j Gold at $1664.60 silver at: 19.00 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 26/100 roubles/dollar; ROUBLE AT 60.06//

3m oil into the 87 dollar handle for WTI and 92 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 143.02DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this .9605–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9584well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.457 UP 0 BASIS PTS

USA 30 YR BOND YIELD: 3.494 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,28

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

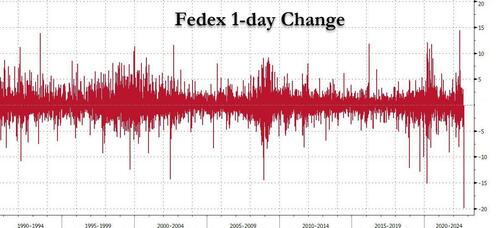

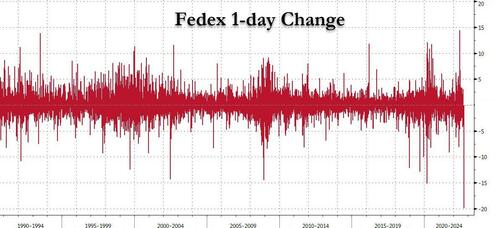

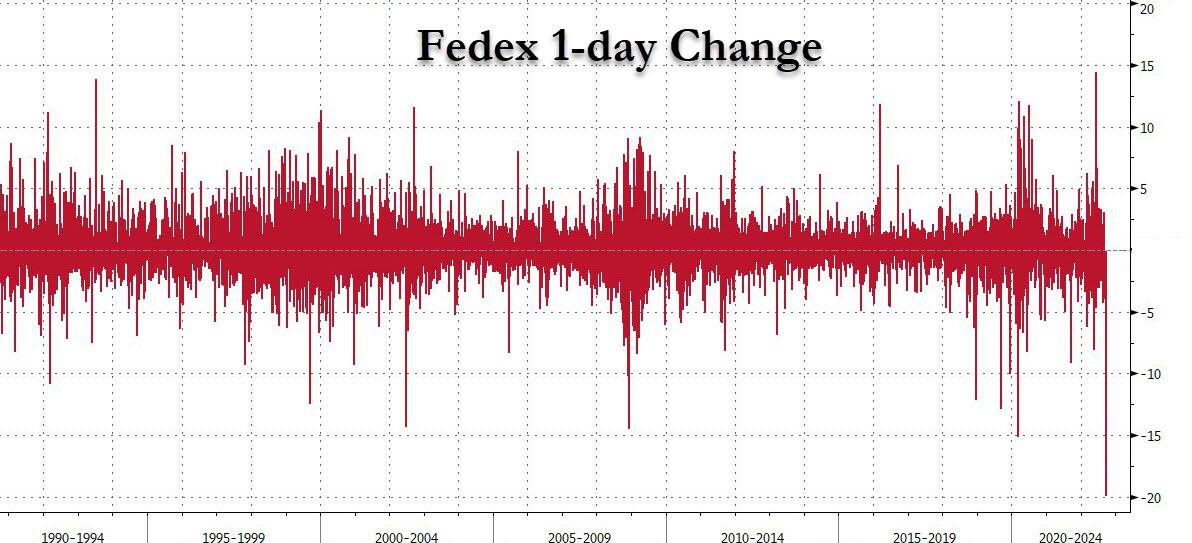

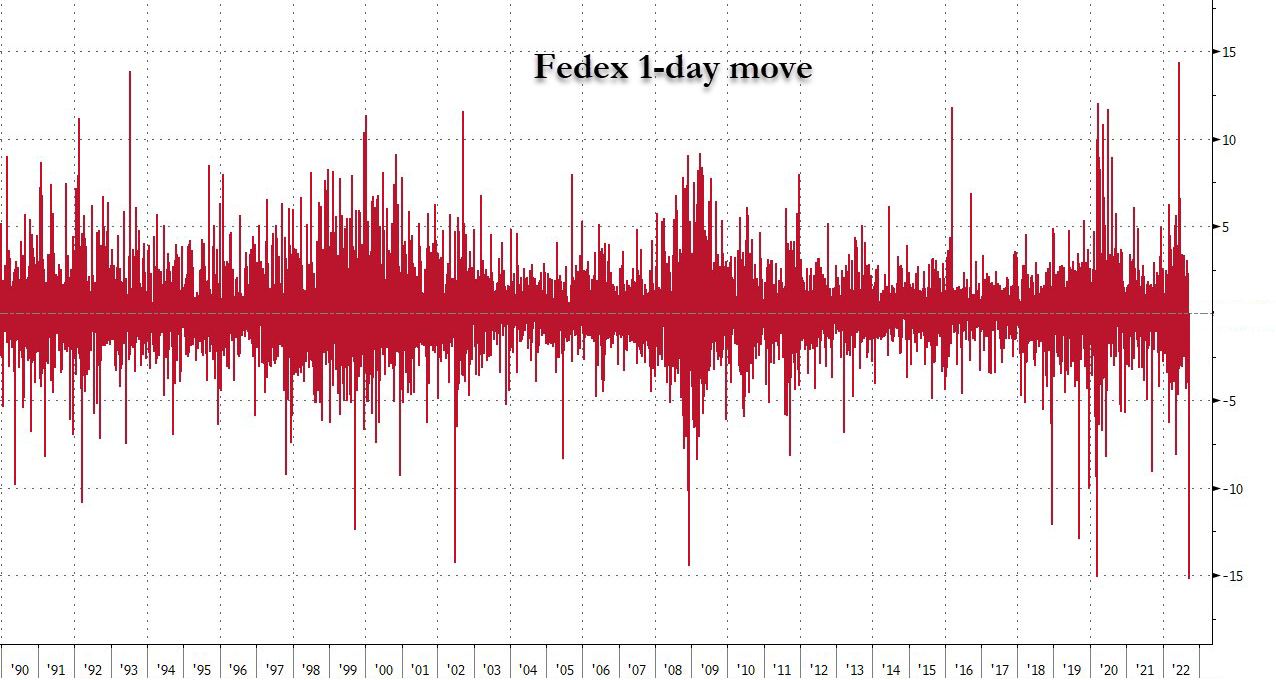

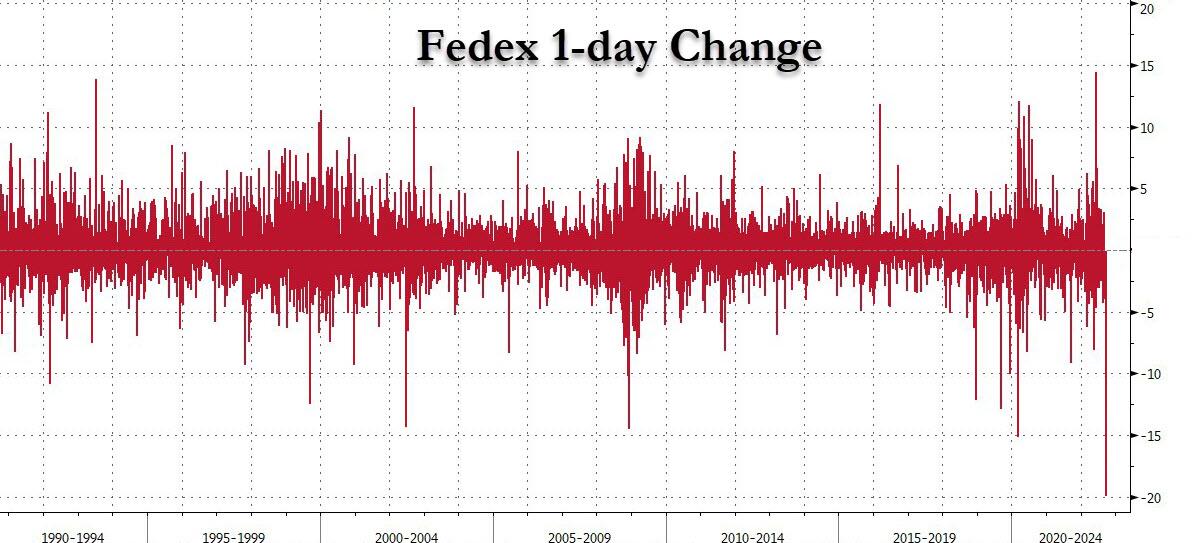

Futures Crater As Fedex Ushers In The Global Recession On $3.2 Trillion Triple Witch Day

FRIDAY, SEP 16, 2022 – 08:03 AM

Another day, another selloff, this time one driven by a catastrophic repricing by Fedex, which has plunged by the most ever this morning, down 20% and losing over $11BN in market cap…

… after pulling guidance and effectively warning that the entire world – and especially China – is in a recession. The fact that it is a $3.2 trillion opex today which guarantees even more volatility in the coming weeks…

… or that buyback blackout period begins today probably isn’t helping, and sure enough, we end the week in a mirror image to how we started it, with equities extending declines with an index of global stocks on track for the worst week since June, while the dollar continued its relentless ascent, trading back to all time highs. S&P futures were down 0.8% at 730am, dropping to the lowest level in 2 months, while Nasdaq 100 lost more than 1%, as Europe headed for a fourth day of losses, and Asian was a sea of red led by China.

In premarket trading, besides the implosion in Fedex, Uber shares slid 5.3% in US premarket trading after the ride-hailing company said it has shut down internal Slack messaging as it investigates a cybersecurity breach. Bank stocks are also lower alongside S&P 500 futures, while the US 10-year Treasury yield advances. In corporate news, Credit Suisse’s securitized products group has drawn interest from Apollo Global Management and BNP Paribas, according to people with knowledge of the matter. Here are some other big premarket movers:

FedEx (FDX US) shares plunged 20% in US premarket trading after the package delivery giant pulled its fiscal 2023 earnings forecast, triggering a raft of downgrades from analysts, including at KeyBanc and JPMorgan. Amazon (AMZN US) and UPS (UPS US) also fell.

Adobe (ADBE US) shares fall another 2.3% in premarket trading, one day after its market value shrunk by $29.5 billion on an announcement to buy software design startup Figma. More analysts slashed ratings and price targets.

Cryptocurrency- exposed stocks are likely to be active on Friday with Bitcoin dropping below $19,800 after SEC Chair Gary Gensler signaled that a feature of the network’s software could lead to tokens being considered securities by the commission.

In the US premarket trading hours, Marathon Digital (MARA US) -3.2%, Coinbase (COIN US) -2.0%, Riot Blockchain (RIOT US) -3.4%

Watch Alcoa (AA US) as Morgan Stanley upgrades the stock and several peers, noting that value begins to show within Americas metals and mining shares, but cautioning that uncertainty remains.

International Paper (IP US) slides 5.6% in US premarket trading after Jefferies downgraded the stock as well as shares in Packaging Corp of America (PKG US) to underperform in reflection of the “massive inventory glut in containerboard.” The broker stays at hold for Westrock (WRK US), noting that valuation is already depressed.

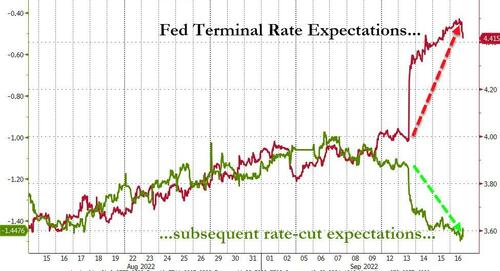

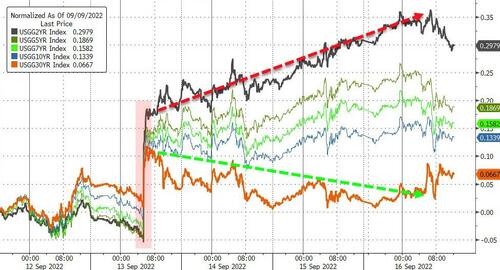

Policy-sensitive two-year Treasury yields extended a rise to the highest since 2007, deepening the curve inversion that’s seen as a recession signal. The latest US economic data painted a mixed picture for the economy that backed the view for hawkish monetary policy. Swaps traders are pricing in a 75 basis-point hike when the Federal Reserve meets next week, with some wagers appearing for a full-point move.

“Everything points to another 75 basis-point rate hike by the Fed when it meets next week. The likelihood that it will have to go ‘big’ again in November is elevated, too,” said Raphael Olszyna-Marzys, an economist at Bank J Safra Sarasin. “What’s more, its new projections should indicate that the fight against inflation will be more painful than previously acknowledged.”

Market participants will face additional volatility on Friday from the quarterly expiry event known as triple witching, with contracts for stock index futures, stock index options and stock options all expiring, while re-balancing of major equity indexes also takes place.

In Europe, the Stoxx 50 slumped 1.4%, headed for a 4th day of losses. The FTSE 100 is flat but outperforms peers, DAX lags, dropping 1.7%. Industrials, construction and autos are the worst-performing sectors as are mining stocks which as iron ore slid amid concerns over demand in China, while aluminum fell on the back of record Chinese output. European mail and parcel delivery companies took a hit in the aftermath of the Fedex warning, led by Deutsche Post AG, down as much as 7.6%. The UK’s benchmark outperformed as the British pound sank to its weakest level against the dollar since 1985.

All industry groups are in the red. Here are the biggest European movers:

Jupiter Fund Management jumps as much as 4.2% after being upgraded to neutral at UBS. Separately, the FT reported that the new CEO will restructure the company after an operational review

Krones rises as much as 1.6% on Friday, with Baader Helvea saying the company showed “huge confidence” during recent capital markets day at the Drinktec trade fair in Munich

Ariston shares soar as much as 11%, the most intraday since March 14, after the company agreed to buy 100% of Centrotec Climate Systems for EU703m in cash and ~41.42m Ariston shares

Capita shares rise as much as 9.3% amid a contract extension with Barnet Council and the sale of subsidiary Pay360 for GBP150 million to Access PaySuite

UK and EU real estate shares slip after both Goldman Sachs and JPMorgan published bearish reviews of the sector. Land Securities falls as much as 5.1% in London after being cut to sell at Goldman

European mail and parcel delivery companies take a hit, led by Deutsche Post, down to July 2020 lows, after US peer FedEx withdrew its earnings forecast on worsening business conditions

Mining stocks are among the biggest underperformers in Europe on Friday as iron ore slid amid concerns over demand in China, while aluminum fell on the back of record Chinese output

Telecom Italia shares drop to a record low after Barclays cut the carrier to underweight from equal-weight, citing a more complex investment case amid political uncertainties in Italy

Uniper plunges to its lowest level on record, with shares down as much as 16%, after people familiar with the matter said Germany is in advanced talks to take it over

Virbac falls as much as 10% after the French veterinary-products company reported 1H results that showed inflation is weighing on profit margins

Earlier in the session, Asian stocks headed for a fifth-straight weekly decline as markets remained volatile ahead of the Federal Reserve’s interest-rate decision next week, with the Xi-Putin meeting adding renewed geopolitical concerns. Stocks slumped in Japan, Hong Kong and mainland China, with little impact on sentiment from Chinese industrial-production and retail-sales data that beat expectations. The MSCI Asia Pacific Index fell as much as 1.3% on Friday, following weakness in US shares, led by technology and consumer discretionary stocks. China’s CSI 300 Index slumped the most in more than four months as the yuan weakened past 7 per dollar, offsetting upbeat August economic data, with the government ramping up stimulus to counter a slowdown. Russia’s President Vladimir Putin met with Chinese leader Xi Jinping for the first time since the war in Ukraine began, underscoring increasing risks as Beijing continues to show support for Moscow.

The Covid-Zero policy in China, a property crisis and the outcome of a US audit inspection will “keep the market in a relatively volatile state,” Laura Wang, chief China equity strategist at Morgan Stanley, said in a Bloomberg TV interview. The brokerage expects earnings growth for mainland companies “to decline to around mid-single digit” from Covid resurgence and lockdowns. India and Australia were among the region’s worst performers. Losses accelerated in afternoon trading as the dollar strengthened. Asian equities suffered a tumultuous week, falling more than 2% as risk assets took a hit from faster-than-expected US inflation, which fueled expectations for more aggressive monetary tightening by the Fed. A strong dollar and higher Treasury yields added to the headwinds. The regional stock benchmark is edging toward its lowest close since May 2020.

Japanese stocks declined as concerns of a potential global economic slowdown and higher US interest rates damped demand for risk. The Topix fell 0.6% to 1,938.56 as of the market close in Tokyo, while the Nikkei 225 declined 1.1% to 27,567.65. Keyence Corp. contributed the most to the Topix’s loss, decreasing 3.8%. Out of 2,169 stocks in the index, 589 rose and 1,501 fell, while 79 were unchanged. “The US interest rate hike will probably be 0.75 point, but there is still a strong sense of uncertainty about future hikes,” said Takeru Ogihara, a chief strategist at Asset Management One. Summers Expects Fed to Raise Rates Above 4.3% to Curb Inflation

The index for developing-nation equities fell to its lowest level in more than two years on Friday. A three-day slide has shaved $422 billion off MSCI’s EM stock index. The gauge fell as much as 1.5%, led by health care stocks. The EM equity gauge is down 5.5% this quarter, on track for a fifth consecutive drop, a record since Bloomberg began monitoring the data.

In FX, the Bloomberg Dollar Spot Index rose as the greenback strengthened against all of its Group-of-10 peers apart from the yen which is marginally up, trading at the 143/USD level. Pound at 1.13/USD, the lowest since 1985, underperforming G-10 peers.

The euro fell a first day in three, trading once again below parity against the dollar. Bunds, Italian bonds slid, putting their 10-year yields on course to climb for a seventh week as traders continued to amp up ECB tightening bets, pricing as much as 200bps of rate hikes by July. The euro volatility skew shifts higher this week and especially on longer tenors, suggesting that bearish sentiment wanes. This seems to be down to demand for topside strikes and not unwinding of shorts given move in the tails

The pound was the worst G-10 performer and fell below $1.14 for the first time since 1985. UK retail sales fell at the sharpest pace in eight months in August as a worsening cost-of-living crisis and plunging confidence forced consumers to cut back on spending. The 1.6% drop was more than three times the decline predicted by economists. Monday is a national bank holiday in the UK

The Australian dollar tumbled to the lowest level since the early days of the Covid pandemic as risk aversion swept across markets. Three-year yield touched as high as 3.44% after National Bank of Australia raised its forecast to a 50bps hike in October. Reserve Bank of Australia Governor Philip Lowe said a few hikes would be needed to tame inflation, though the case for outsized interest-rate increases has “diminished” now that the cash rate is approaching “more normal settings”

Japan’s longer-maturity bonds extended declines after Thursday’s weak 20-year auction. Japanese markets will be shut Monday and Friday next week for national holidays

Meanwhile, the offshore yuan remained on the weaker side of 7 to the dollar, even as the People’s Bank of China set the reference rate for the currency stronger-than-forecast for a 17th straight day. “While China activity showed some improvement this morning, equity investors really want to see substantial easing in China’s policies related to Covid to turn a bit more constructive,” said Chetan Seth, Asia-Pacific equity strategist at Nomura Holdings Inc. in Singapore. “That has not happened.”

In rates, the 10Y Treasury yield up 3bps to around 3.47%, gilts 10-year yield is flat at 3.16%, while bunds 10-year is also up 0.2bps at 1.79%. Treasuries remained lower after a bund-led selloff during European morning, with losses led by front-end of the curve as 2-year yields exceed Thursday’s highs, peaking near 3.92%. Further out, 5s30s breached Thursday’s low (reaching -21.1bp) to reach most inverted level since 2000. Yields are cheaper by more than 3bp across front-end of the curve with 2s10s spread flatter by ~2bp on the day; 10-year yields around 3.47%, trading broadly in line with bunds while gilts outperform by 2.5bp in the sector. US curve flattening persists as Fed rate expectations continue to grind higher; OIS markets price in a peak policy rate of around 4.5% for March 2023

In commodities, WTI and Brent are oscillating around the unchanged mark with the complex initially under pressure from the overall risk aversion. Kazakhstan energy ministry expects to stick to its oil production plans of 85.5mln tonnes this year; says Kashagan oilfield will resume output “in October at best.” Spot gold is flat after the yellow metal took out the 2021 low (USD 1,676/oz) yesterday with clean air seen below until the COVID low of USD 1,450/oz.

Bitcoin is flat around USD 19,750 whilst Ethereum remains pressured under USD 1,500.

To the day ahead now, and data releases from the US include the University of Michigan’s preliminary consumer sentiment index for September, as well as UK retail sales for August. Meanwhile from central banks, we’ll hear from ECB’s President Lagarde, as well as the ECB’s Rehn and Villeroy.

Market Snapshot

S&P 500 futures down 1.0% to 3,863.75

STOXX Europe 600 down 1.2% to 409.92

MXAP down 1.3% to 150.15

MXAPJ down 1.6% to 490.96

Nikkei down 1.1% to 27,567.65

Topix down 0.6% to 1,938.56

Hang Seng Index down 0.9% to 18,761.69

Shanghai Composite down 2.3% to 3,126.40

Sensex down 1.8% to 58,881.76

Australia S&P/ASX 200 down 1.5% to 6,739.08

Kospi down 0.8% to 2,382.78

German 10Y yield little changed at 1.78%

Euro down 0.4% to $0.9961

Gold spot down 0.5% to $1,656.63

U.S. Dollar Index up 0.34% to 110.11

Top Overnight News from Bloomberg

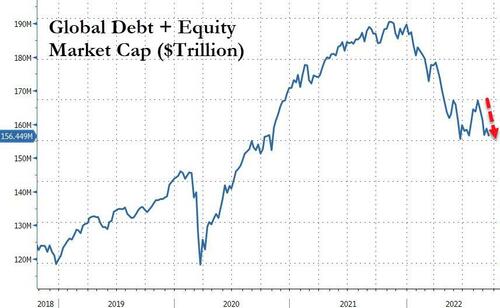

A surging dollar is now the only possible hedge for what’s turning into the biggest destruction of shareholder value since the global financial crisis

“The growing risk of recession in the euro area and the steadily increasing labor participation rate might also be factors that have kept wages in check,” European Central Bank Governing Council member Olli Rehn said in Helsinki

“The slowdown of the economy is not going to ‘take care’ of inflation on its own,” European Central Bank Vice President Luis de Guindos tells Expresso newspaper in an interview. “We need to continue the normalization of monetary policy”

The French inflation rate will peak between now and the beginning of next year near the current level, “around 6% or a little more,” Bank of France Governor Francois Villeroy de Galhau said

A shortage of high-quality assets in the euro area is keeping a lid on short- term borrowing costs, a development that could endanger the ECB’s effort to tighten financial conditions

Global equity funds saw inflows driven by US stocks in the week to Sept. 14, according to a Bank of America note, citing EPFR Global data

China has ample monetary policy room and abundant policy tools, PBOC’s monetary policy department writes in an article that reviews the country’s monetary policies in the past five years

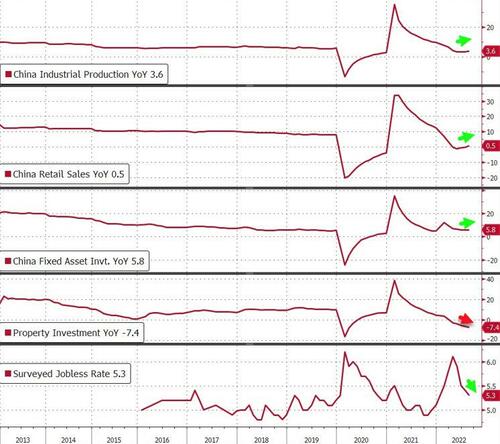

China’s economy showed signs of recovery in August. Industrial production, retail sales and fixed-asset investment all grew faster than economists expected last month. The urban jobless rate slid to 5.3%, while the youth unemployment rate fell from a record high

Japan’s increasingly incongruous policy stance aimed at securing both stable growth and inflation is adding to the likelihood of further yen losses, even as officials warn of possible intervention

India’s sovereign bonds are defying a worldwide rout, as banks and foreign funds rushed to buy the high-yielding debt in anticipation that they will be included in global indexes

Germany is taking control of Russian oil major Rosneft PJSC’s German oil refineries and is nearing a decision to take over Uniper SE and two other large gas importers as it tries to avoid a collapse of its energy industry

A more detailed look at global markets courtesy of Newsquawk

Asia stocks fell despite better-than-expected Chinese activity data as the region took its cue from the losses in the US after mixed data and as markets continued to adjust to a more aggressive Fed rate path. ASX 200 was pressured as energy and miners led the broad retreat after recent losses in commodity prices. Nikkei 225 suffered from the downbeat mood and with the 10yr JGB yield stuck at the top of the BoJ’s target. Hang Seng and Shanghai Comp conformed to the risk aversion with the latest Industrial Production and Retail Sales data failing to spur risk appetite despite both surpassing estimates.

Top Asian News

Chinese NBS said China is to coordinate economic development and COVID control, while it added that the economy continued a recovery trend in August and some factors exceeded expectations but also noted that the recovery in domestic demand still lags behind the recovery in production and that the property market faces downward pressure despite some positive changes. China’s stats bureau also commented that the economy was affected by COVID flare-ups in August but the flare-ups impact was limited and that policies to stabilise growth are gaining traction although noted that China’s economy faces more difficulties this year than in 2020.

Chinese President Xi says China’s economy remains resilient and full of potential

Japanese Finance Minister Suzuki reiterated it is important for FX to move stably reflecting economic fundamentals and that sharp FX moves are undesirable, while he is concerned about sharp, one-sided JPY weakening and they will take necessary action without ruling out any options if sharp yen moves persist.

Japan is to use JPY 3.5tln in reserve funds for economic measures, according to Kyodo News

RBA Governor Lowe said the RBA is committed to returning inflation to the 2-3% target range over time and is seeking to do this in a way that keeps the economy on an even keel, while the Board expects further increases will be required to bring inflation back to target but they are not on a pre-set path. Lowe stated that with inflation as high as it is, they need to make sure that inflation returns to target in a reasonable time and will do what is necessary to make sure that higher inflation does not become entrenched. Furthermore, Lowe said at some point will not need to hike by 50bps and they are getting closer to that point, while they will consider hiking by 25bps or 50bps at the next meeting but also stated that rates are still too low right now.

South Korean President Yoon and US President Biden are expected to discuss currency swap during a summit, according to Yonhap.

South Korean Parliament Speaker Kim says need to promptly advance South Korean and Chinese trade negotiations

Euro-bourses see the deepest losses whilst the FTSE 100 is cushioned by the slide in the Pound. European sectors are all lower and portray a clear defensive bias, with Healthcare at the top of the bunch. Stateside, US equity futures have been trundling lower with the NQ underperforming vs the ES, YM and RTY.

Top European News

No Movies. No McDonald’s. Britain Shuts for Queen’s Funeral

WHO Panel Advises Against GSK, Regeneron Drugs for Covid

AstraZeneca Gets Nod From EU for Evusheld and Respiratory Drug

Telecom Italia Falls to Record Low Amid Barclays Downgrade

Uniper Plunges to Lowest Level Ever on Nationalization Reports

Cold War Relic Threatens Plans to Ditch Russian Oil

FX

GBP extended losses in wake of significantly weaker than forecast ONS retail sales data, with Cable sliding to the lowest level since 1985.

DXY reclaimed 110.00-status as Sterling continued sliding, and now oscillates around the round figure.

JPY stands as the outperformer, as USD/JPY hold within yesterday’s extremes amid the risk aversion and recent verbal jawboning.

Chinese FX regulator says it is hard to predict short-term volatility in exchange rate, and urges companies not to bet on the exchange rate, according to state media

South Korean Authorities are reportedly suspected of “smoothing operations” in USD/KRW trading, according to Reuters citing South Korean FX dealers.

Fixed Income

Bunds have staved off pressure on 142.00 within a 142.15-143.04 range.

Gilts traded above par briefly between 104.93-105.50 extremes (+17 ticks at one stage).

10yr T-note is almost flat ahead of preliminary Michigan sentiment which will be watched closely for inflation expectations.

Commodities

WTI and Brent are oscillating around the unchanged mark with the complex initially under pressure from the overall risk aversion.

Kazakhstan energy ministry expects to stick to its oil production plans of 85.5mln tonnes this year; says Kashagan oilfield will resume output “in October at best”

Spot gold is flat after the yellow metal took out the 2021 low (USD 1,676/oz) yesterday with clean air seen below until the COVID low of USD 1,450/oz.

Base metals meanwhile are softer across the board as the Dollar remains firm, but LME nickel bucks the trend with reports via Bloomberg also suggesting LME is being sued by hedge funds, including AQR, in the London High Court

US Event Calendar

10:00: Sept. U. of Mich. Sentiment, est. 60.0, prior 58.2

10:00: Sept. U. of Mich. Current Conditions, est. 59.4, prior 58.6

10:00: Sept. U. of Mich. Expectations, est. 59.0, prior 58.0

10:00: Sept. U. of Mich. 1 Yr Inflation, est. 4.6%, prior 4.8%

10:00: Sept. U. of Mich. 5-10 Yr Inflation, est. 2.8%, prior 2.9%

16:00: July Total Net TIC Flows, prior $22.1b

16:00: July Net Foreign Security Purchases, prior $121.8b

DB’s Jim Reid concludes the overnight wrap

Two weeks after coping with a manic birthday party for two manic 5 year old twins, we repeat the whole thing this weekend as my daughter Maisie turns 7 today and has a OTT Harry Potter themed party tomorrow at our house. I have a costume which I’m hoping will be cooler than the 10ft giant inflatable diplodocus outfit I had for the twins’ party. If you don’t believe me photos are available. Many people have kindly asked how Maisie is after being diagnosed with a rare hip disease called Perthes over 12 months ago. The answer is she is coping well but still needs to be in a wheelchair until the doctors see any sign that the hip ball is regrowing. We’re crossing our fingers that there might be signs at the next scan in December. At the moment it’s still slowly disintegrating. She’s had great news this week as she’s got accepted at a very young age into a prestigious artistic swimming club. Because of her regular rehab in the pool, and a natural talent even before her condition became apparent, she is phenomenal in the water. She is a stage 7 swimmer which on average is for around 10/11 year olds and used to love gymnastics before her incapacitation. So for a sport that I’ve perhaps always previously seen as one of my least favourite, I’m now a synchronised swimming convert ahead of her first session this Sunday. I suspect I’ll stick to golf for myself though and won’t be buying the nose peg.

It was another synchronised sell off for both bonds and equities yesterday as investors moved to price in yet more rate hikes from central banks, raising market fears about a hard landing ahead. Those moves were prompted by a decent batch of US employment data, which added to the sense that the Fed could afford to keep hiking rates for the time being. But the prospect of more aggressive rate hikes proved bad news for equities, with the S&P 500 (-1.13%), its lowest level since July, more than reversing the previous day’s partial rebound that followed its worst daily performance for two years on Tuesday. In the meantime, sovereign bonds embarked on a further selloff and multiple recessionary indicators were flashing with increasing alarm, including the 2s30s Treasury yield curve that by the close was more inverted than at any time since 2000.

Before we get onto the details however, we should point out that DB’s US economists, led by Matt Luzzetti, have also revised their expectations for the Fed funds rate following the latest inflation data, and now see the terminal rate some way beyond market pricing at 4.9% in Q1 2023 (link here). Matt has been consistently the highest on the street for economists in recent months and this upgrade is now closer to the 5-6% range that David Folkerts-Landau, Peter Hooper and I said was necessary to tame inflation in our “What’s in the tails?” note (link here) back in April. Today’s UoM inflation expectations series is going to be the last important release before next week’s FOMC, especially after this week’s messy CPI data. Year-ahead inflation expectations have been edging down of late but the upside surprise in June a few hours after a blockbuster CPI beat cemented the last minute 75bps hike. With +80.5bps priced in next week, it will be interesting to see if the expectations data move pricing any closer to 75 or 100bps, and if not, whether the Fed tries to influence pricing with a leak so the meeting isn’t as “live”, or if they feel comfortable heading into the meeting with some split probability priced. While we’re on the revision path, a reminder that our 10yr Bund forecast was upgraded to 2.25% late on Wednesday. See here for more.

Against this rates higher backdrop, markets were revising their expectations in a hawkish direction following strong labour market data. In particular, the US weekly initial jobless claims for the week ending September 10 fell for a 5th consecutive week to 213k (vs. 227k expected), and the previous week was also revised down by -4k. The release added to the sense that the recent economic resilience over the late summer was proving to be more than just one data point, and it’s worth noting that the 213k reading was the lowest since May. Piling on, retail sales MoM increased 0.3% versus -0.1% expectations. As with most things macro related lately, there is a flipside, however. The core retail sales figure fell -0.3% versus expectations it would be flat, while the control group, which has outsize influence in GDP consumption tabulations, was flat MoM, versus expectations of a 0.5% expansion. Indeed, the Atlanta Fed’s GDPNow tracker downgraded 3Q GDP estimates to 0.5% from 1.3% following the print. Recession talk will only bubble up with more with revisions like that. But overall a messy set of data yesterday.

The recent inflation surprises has proven bad news for risk assets since it’s seen as giving the Fed the green light for faster rate hikes. In response, the terminal rate priced in for March 2023 rose +7.8bps yesterday to 4.46%, and that in turn led to another selloff for Treasuries. By the close, the 2yr yield was up +7.7bps to its highest level since the GFC, whilst the 10yr yield rose +4.5bps to 3.45%. In Asia the 2yr yield is up another couple of bps, with 10yr yields flat, further inverting the 2s10s curve to -44.5 bps as we go to press. Higher real yields were behind the latest moves, with the 10yr real yield crossing 1.0%, hitting a post-2018 high. And in Europe it was much the same story, with yields on 10yr bunds (+5.3bps), OATs (+3.6bps) and BTPs (+5.7bps) all moving higher as well.

Yesterday’s losses were spread across multiple asset classes, and equities took a tumble given those fears about faster rate hikes. The S&P 500 shed -1.13% as part of a broad-based decline, and the impact of higher interest rates was evident from the sectoral breakdowns, as tech stocks including the NASDAQ (-1.43%) struggled, whereas the banks in the S&P 500 advanced +1.54%. Europe experienced a similar pattern, with the STOXX 600 (-0.56%) losing ground for a third day running, in contrast to the STOXX Banks index (+1.98%) which hit a three-month high.

One more positive piece of news on the inflation side was that a deal was reached to avert an upcoming US rail strike, which would have had a significant impact on supply chains had that gone ahead. A sign of its potential impact was that even the White House was involved, with President Biden joining the meeting virtually on Wednesday evening. The news helped a number of key commodities to fall back in price, including US natural gas futures which ended the day -8.67% lower, whilst WTI oil was also down -3.82% at $85.10/bbl.

Asian equity markets are weaker again this morning, heading for a fifth consecutive weekly drop amid further weakness in US equities overnight. As I type, the CSI (-1.13%) and the Shanghai Composite (-0.97%) are trading in negative territory with stronger than expected economic data failing to boost risk sentiment. Elsewhere, the Nikkei (-1.08%), Kospi (-1.03%) and the Hang Seng (-0.55%) are also sliding. Looking ahead, stock futures in the DM world are pointing to additional losses with contracts on the S&P 500 (-0.71%), NASDAQ 100 (-0.88%) and DAX (-0.70%) all moving lower.

We have early morning data from China with retail sales standing out as it jumped +5.4% y/y in August (v/s +3.3% expected), up from +2.7% in July. The uptick in retail sales was primarily visible in the restaurant/catering sectors, an industry typically sensitive to lockdowns. Other activity series showed that industrial production grew +4.2% y/y in August, which is an improvement from July’s +3.8% increase. Also, fixed asset investment for the first eight months of the year rose by +5.8%, above the +5.5% increase forecast. However, there were some disappointing signs elsewhere as new home prices slid for the 12th consecutive month, falling -0.29% m/m in August against a -0.11% decline previously, indicating that the recently rolled-out measures failed to revive demand.

Staying on China, the People’s Bank of China (PBOC) continued its currency defense after the yuan weakened past the key level of 7 per US dollar for the first time in two years amid the relentless dollar rally. The central bank for the 17th straight day intervened while fixing the yuan 456 pips stronger than the average Bloomberg estimate to help prevent the currency’s slide.

Back to wrapping up the rest of yesterday’s data, US industrial production was down -0.2% in August (vs. unch expected), and the Philadelphia Fed’s business outlook for September fell to -9.9 (vs. 2.3 expected). However, the Empire State manufacturing survey for September rose to -1.5 (vs. -12.9 expected), rebounding from its worst month since the Covid pandemic.

To the day ahead now, and data releases from the US include the University of Michigan’s preliminary consumer sentiment index for September, as well as UK retail sales for August. Meanwhile from central banks, we’ll hear from ECB’s President Lagarde, as well as the ECB’s Rehn and Villeroy.

AND NOW NEWSQUAWK

Euro-bourses see the deepest losses whilst the FTSE 100 is cushioned by the slide in the Pound – Newsquawk US Market Open

FRIDAY, SEP 16, 2022 – 06:59 AM

Euro-bourses see the deepest losses whilst the FTSE 100 is cushioned by the slide in the Pound

GBP extended losses in wake of significantly weaker than forecast ONS retail sales data, with Cable sliding to the lowest level since 1985

10yr T-note is almost flat ahead of preliminary Michigan sentiment which will be watched closely for inflation expectations

China will impose sanctions on CEO of Raytheon Technologies (RTX) and CEO of Boeing (BA) Defense, Space & Security

Looking ahead, highlights include US University of Michigan Prelim., Quad Witching

Or why not try Newsquawk’s squawk box free for 7 days?

16th September 2022

LOOKING AHEAD

US University of Michigan Prelim., Quad Witching.

Click here for the Shanghai Cooperation Organization (SCO) Summit primer.

GEOPOLITICS

RUSSIA-UKRAINE

Russian President Putin says “We are ready to work to solve many problems in the world, the most important of which are energy and food”, via Al Jazeera.

CHINA-TAIWAN

China will impose sanctions on Gregory Hayes, CEO and chairman of Raytheon Technologies (RTX), and Ted Colbert, Boeing (BA) Defense, Space & Security president and CEO, following recent US arms sales to China’s Taiwan region, according to Chinese FM, according to Global Times.

ARMENIA-AZERBAIJAN

Kazakhstan energy ministry expects to stick to its oil production plans of 85.5mln tonnes this year; says Kashagan oilfield will resume output “in October at best”

EUROPEAN TRADE

EQUITIES

Euro-bourses see the deepest losses whilst the FTSE 100 is cushioned by the slide in the Pound

European sectors are all lower and portray a clear defensive bias, with Healthcare at the top of the bunch.

Stateside, US equity futures have been trundling lower with the NQ underperforming vs the ES, YM and RTY.

GBP extended losses in wake of significantly weaker than forecast ONS retail sales data, with Cable sliding to the lowest level since 1985.

DXY reclaimed 110.00-status as Sterling continued sliding, and now oscillates around the round figure.

JPY stands as the outperformer, as USD/JPY hold within yesterday’s extremes amid the risk aversion and recent verbal jawboning.

Chinese FX regulator says it is hard to predict short-term volatility in exchange rate, and urges companies not to bet on the exchange rate, according to state media

South Korean Authorities are reportedly suspected of “smoothing operations” in USD/KRW trading, according to Reuters citing South Korean FX dealers.

WTI and Brent are oscillating around the unchanged mark with the complex initially under pressure from the overall risk aversion.