by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1726.40 DOWN $9.40

SILVER: $19.00 DOWN 16 CENTS

ACCESS MARKET: GOLD $1726.35

SILVER: $18.94

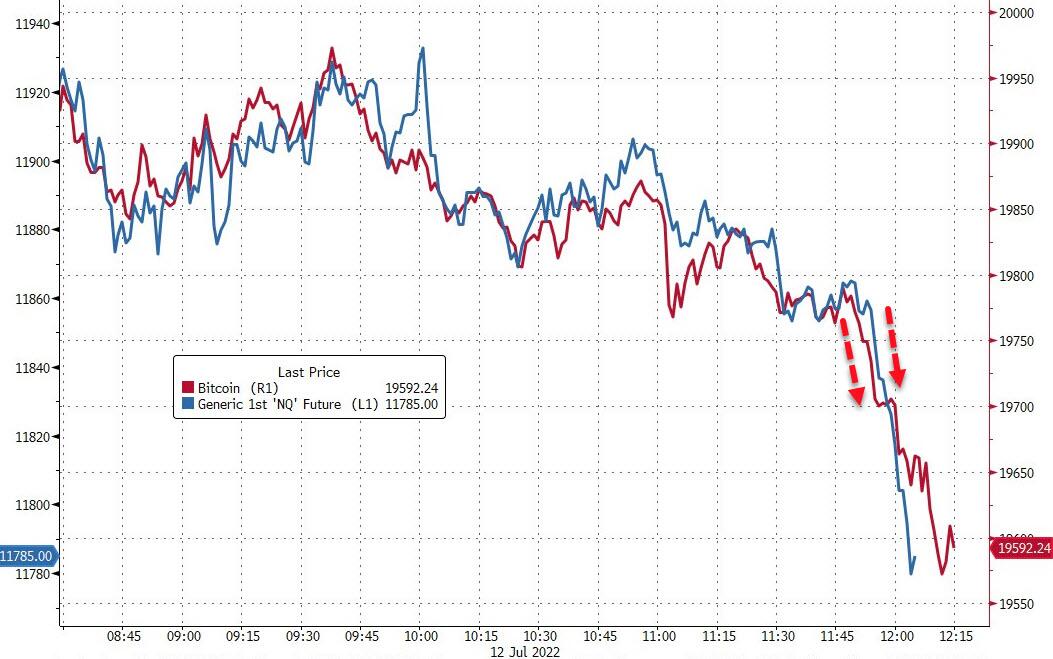

Bitcoin morning price: $19,761 DOWN 1739

Bitcoin: afternoon price: $19,560. DOWN 1940

Platinum price: closing DOWN $26.55 to $849.75

Palladium price; closing down $113.45 at $2040.50

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JULY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,730.000000000 USD

INTENT DATE: 07/11/2022 DELIVERY DATE: 07/13/2022

FIRM ORG FIRM NAME ISSUED STOPPED

323 H HSBC 5

661 C JP MORGAN 21 19

737 C ADVANTAGE 1

800 C MAREX SPEC 5

880 C CITIGROUP 3

TOTAL: 27 27

MONTH TO DATE: 3,989

no. of contracts issued by JPMorgan: 19/27

_____________________________________________________________________________________

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT 27 NOTICE(S) FOR 2700 Oz//0.0839 TONNES)

total notices so far: 3989 contracts for 398,900 oz (12.4074 tonnes)

SILVER NOTICES:

9 NOTICE(S) FILED 45,000 OZ/

total number of notices filed so far this month 2691 : for 13,455,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $9.40

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 1023.27 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 16 CENTS

AT THE SLV// ://HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 3.228 MILLION OZ FROM THE LV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 514.501 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 1206 CONTRACTS TO 141,900 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GAIN IN OI WAS ACCOMPLISHED DESPITE OUR CONSIDERABLE $0.17 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.17) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SILVER LONGS//BUT MAINLY WE HAD ADDITIONAL SPECULATOR ADDITIONS.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A POOR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.220 MILLION OZ FOLLOWED BY TODAY’S 65,000 OZ QUEUE JUMP / // V) STRONG SIZED COMEX OI GAIN

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -17

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTACTS for 7 days, total 7472 contracts: 37,360 million oz OR 5.34 MILLION OZ PER DAY. (1067 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 37.360 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 37.360 MILLION OZ

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1206 DESPITE OUR $0.17 LOSS IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE CONTRACTS: 425 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A POOR INITIAL SILVER OZ STANDING FOR JUNE. OF 15.22 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 65,000 OZ // .. WE HAD A VERY STRONG SIZED GAIN OF 1631 OI CONTRACTS ON THE TWO EXCHANGES FOR 8.155 MILLION OZ DESPITE THE LOSS IN PRICE..

WE HAD 9 NOTICES FILED TODAY FOR 45,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A HUMONGOUS SIZED 16,795 CONTRACTS TO 517,246 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: —954 CONTRACTS.

.

THE STRONG SIZED INCREASE IN COMEX OI CAME WITH OUR FALL IN PRICE OF $4.45//COMEX GOLD TRADING/MONDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR GOOD SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERING

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JULY AT 2.914 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 7300 OZ

YET ALL OF..THIS HAPPENED DESPITE OUR LOSS IN PRICE OF $4.45 WITH RESPECT TO FRIDAY’S TRADING

WE HAD AN ATMOSPHERIC SIZED GAIN OF 19,389 OI CONTRACTS 60.316 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2594 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 517,246

IN ESSENCE WE HAVE AN ATMOSPHERIC SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 19,389 CONTRACTS WITH 16,795 CONTRACTS INCREASED AT THE COMEX AND 2594 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 19,389 CONTRACTS OR 60.316 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2594) ACCOMPANYING THE HUMONGOUS SIZED GAIN IN COMEX OI (16,795,): TOTAL GAIN IN THE TWO EXCHANGES 19,389 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING AND SOME ADDITION TO SPECULATOR SHORTS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JULY. AT 2.914 TONNES FOLLOWED BY TODAY’S 7,300 OZ QUEUE JUMP 3) ZERO LONG LIQUIDATION//SOME SPECULATOR SHORT COVERING//SOME SPECULATOR SHORT ADDITIONS //.,4) STRONG SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

39,156 CONTRACTS OR 3,915,600 OZ OR 121.77 TONNES 7 TRADING DAY(S) AND THUS AVERAGING: 6093 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAY(S) IN TONNES: 121.79 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 121.79/3550 x 100% TONNES 3,43% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 2238.13 TONNES FINAL

JULY: 121.79 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JULY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 1206 CONTRACT OI TO 141,883 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 425 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 425 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE:425 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1206 CONTRACTS AND ADD TO THE 425 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A VERY STRONG SIZED GAIN OF 1631 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 8.15 MILLION OZ

OCCURRED DESPITE OUR FALL IN PRICE OF $0.17 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED DOWN 32629 PTS OR 0.97% //Hang Sang CLOSED DOWN 279.46 OR 1.32% /The Nikkei closed DOWN 475.64 OR % 1.77. //Australia’s all ordinaires CLOSED DOWN 0.08% /Chinese yuan (ONSHORE) closed DOWN 6.7214 /Oil DOWN TO 99.23 dollars per barrel for WTI and DOWN TO 102.63 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7214 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7374: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A POWERFUL SIZED 16,795 CONTRACTS TO 517,246 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS GIGANTIC COMEX INCREASE OCCURRED DESPITE OUR LOSS OF $4.45 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2594 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2594 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :2594 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2494 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: AN ATMOSPHERIC SIZED SIZED TOTAL OF 19,389 CONTRACTS IN THAT 2594 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD AN UNBELIEVABLY SIZED COMEX OI GAIN OF 16,795 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $4.45.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING JULY (14.137),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 14.137 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $4.45) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS/COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS//// WE HAVE REGISTERED AN ATMOSPHERIC SIZED GAIN OF 60.316 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR JULY (14.137 TONNES)…

WE HAD -954 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 19,389 CONTRACTS OR 1,938,900 OZ OR 60.316 TONNES

Estimated gold volume 367,491/// strong/

final gold volumes/yesterday 245,877 /fair

INITIAL STANDINGS FOR JULY ’22 COMEX GOLD //JULY 12

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 64,302.000 oz Malca |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 27 notice(s) 2700 OZ 0.0837 TONNES |

| No of oz to be served (notices) | 556 contracts 55,600 oz 1.729 TONNES |

| Total monthly oz gold served (contracts) so far this month | 3989 notices 398900 OZ 12.4074 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

1 customer withdrawals:

i) Out of Malca: 64,302.000 oz (2,000 kilobars)

total withdrawal: 64,302.000 oz

ADJUSTMENTS:1 dealer to customer

JPMorgan: 18,624.714 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 583 contracts losing 387 contracts . We had

460 notices filed on Monday so we gained a strong 73 contracts or an additional 7300 oz will stand in this non active

delivery month of July.

August has a LOSS OF 16,029 contracts down to 326,880 contracts

Sept. gained 501 contracts to 2493 contracts.

We had 27 notice(s) filed today for 2700 oz FOR THE July 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 21 notices were issued from their client or customer account. The total of all issuance by all participants equate to 27 contract(s) of which 19 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2022. contract month,

we take the total number of notices filed so far for the month (3989) x 100 oz , to which we add the difference between the open interest for the front month of (JULY 583 CONTRACTS ) minus the number of notices served upon today 27 x 100 oz per contract equals 454,500 OZ OR 14.137 TONNES the number of TONNES standing in this active month of July.

thus the INITIAL standings for gold for the JULY contract month:

No of notices filed so far (3989) x 100 oz+ (583) OI for the front month minus the number of notices served upon today (27} x 100 oz} which equals 454,500 oz standing OR 14.137 TONNES in this active delivery month of JULY.

TOTAL COMEX GOLD STANDING: 14.137 TONNES (A FAIR STANDING FOR A JULY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,443,533.842 oz 76.00 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 32,703,359.863 OZ

TOTAL ELIGIBLE GOLD: 16,121,229.199 OZ

TOTAL OF ALL REGISTERED GOLD: 16,582,130.664 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 14,138,597.0 OZ (REG GOLD- PLEDGED GOLD) 439 tonnes

END

SILVER/COMEX/JULY 12

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,110,359.190 oz Delaware Loomis |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,123,337.438 oz CNT JPMorgan |

| No of oz served today (contracts) | 9CONTRACT(S) 45,000 OZ) |

| No of oz to be served (notices) | 292 contracts (1,460,000 oz) |

| Total monthly oz silver served (contracts) | 2691 contracts 13,455,000, oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 2 deposits into the customer account

i) Into JPMorgan: 586,398.800 oz

ii) Into CNT: 536,939,678 oz

total deposit: 1,123,337.438 oz

JPMorgan has a total silver weight: 175.185 million oz/339.531 million =51.57% of comex

Comex withdrawals: 2

i) Out of Delaware: 999.300 oz

ii) Out of loomis 1,109,359.890 oz

total withdrawal 1,110,359,190 oz

adjustments: 4/dealer to customer

i) Brinks 2,092,312.540 oz

ii)HSBCL 5081.400 oz

iii) JPMorgan 2,463,373.400 oz

iv)Manfra: 801,672.886 oz

huge adjustment of 5.352 million oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 62.728 MILLION OZ

TOTAL REG + ELIG. 339.531 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JULY OI: 301 CONTRACTS HAVING LOST 32. WE HAD 45 NOTICES FILED

ON FRIDAY, SO WE GAINED 13 CONTRACTS OR AN ADDITIONAL 65,000 OZ WILL STAND FOR METAL AT THE COMEX.

AUGUST GAINED 14 CONTRACTS TO STAND AT 1104

SEPTEMBER HAD A GAIN OF 123 CONTRACTS UP TO 116,713 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 9 for 45,000 oz

Comex volumes:54,317// est. volume today// poor

Comex volume: confirmed yesterday: 41,347 contracts ( poor )

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 2691 x 5,000 oz = 13,455,000 oz

to which we add the difference between the open interest for the front month of JULY(xx) and the number of notices served upon today 9 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY./2022 contract month: 2691 (notices served so far) x 5000 oz + OI for front month of JULY (xx) – number of notices served upon today (9) x 5000 oz of silver standing for the JULY contract month equates 14,850,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JULY 12/WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESS AT 1023.27 TONNES

JULY 11/WITH GOLD DOWN $4.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWL OF 1.16 TONNES FROM THE GLD./INVENTORY RESTS AT 1023.27 TONNES

JULY 7/WITH GOLD UP $1.35: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.61 TONNES FORM THE GLD///INVENTORY REST AT 1024.43 TONNES

JULY 6/WITH GOLD DOWN $26.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 9.86 TONNES FROM THE GLD//INVENTORY REST AT 1032.04 TONNES

JULY 5/WITH GOLD DOWN $36.55//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.41 TONNES FROM THE GLD///INVENTORY RESTS AT 1041.90 TONNES

JULY 1/WITH GOLD DOWN $5.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES//INVENTORY RESTS AT 1050.31 TONNES

JUNE 30/WITH GOLD DOWN $9.20: big CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 1052.63 TONNES//

JUNE 28/WITH GOLD DOWN $3.05//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.64 TONNES FROM THE GLD///INVENTORY RESTS AT 1056.40 TONNES

JUNE 27/WITH GOLD DOWN $4.90 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.04 TONNES

JUNE 24/WITH GOLD UP 45 CENTS TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.70 TONNES FROM THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 23/WITH GOLD DOWN $8.60:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//INVENTORY RESTS AT 1071.77 TONNES

JUNE 22/WITH GOLD UP 15 CENTS:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1073.80 TONNES

JUNE 21/WITH GOLD DOWN $2.00: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1075.54 TONES

JUNE 17/WITH GOLD DOWN $11.25: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.60 TONNES INTO THE GLD.///INVENTORY RESTS AT 1075.54 TONNES

JUNE 16/WITH GOLD UP $28.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.74 TONNES

JUNE 15/WITH GOLD UP $6.50/BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.65 TONNES FROM THE GLD////INVENTORY RESTS AT 1063.74 TONNES

JUNE 14/WITH GOLD DOWN $18.80/NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 13/WITH GOLD DOWN $41.55: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 10/WITH GOLD UP $21.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 9/WITH GOLD DOWN $3.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1065.39 TONNES

JUNE 8/WITH GOLD UP $4.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 7/WITH GOLD UP $7.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

GLD INVENTORY: 1023.27 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JULY 12/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A IWTHDRAWAL OF 3.228 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 514.501 MILLION OZ//

JULY 11/WITH SILVER DOWN 17 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 5.533 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 517.729 MILLION OZ

JULY 7/WITH SILVER UP 3 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.889 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 523.262 MILLION OZ/

JULY 6/WITH SILVER UP ONE CENT: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 12.558 MILLION OZ FORM THE SLV///INVENTORY RESTS AT 528.151 MILLION OZ

JULY 5/WITH SILVER DOWN 55 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 540.709MILLION OZ//

JULY 1/WITH SILVER DOWN 61 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ//INVENTORY RESTS AT 540.709 MILLION OZ//

JUNE 30/WITH SILVER DOWN 41 CENTS : SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 738,000 OZ FROM THE SLV//INVENTORY RESTS AT 541.262 MILLION OZ//

JUNE 28/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.00 MILLION OZ..

JUNE 27/WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 24/WITH SILVER UP 10 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.137 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 23/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 2.029 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 545.137 MILLION OZ//

JUNE 22/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.166 MILLION OZ.

JUNE 21/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.506 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 547.166 MILLION OZ//

JUNE 17/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 739,000 OZ FROM THE SLV./:INVENTORY RESTS AT 543.660 MILLION OZ/

JUNE 16/WITH SILVER UP 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 15/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 14/WITH SILVER DOWN 32 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 13/WITH SILVER DOWN 62 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 10.WITH SILVER UP 13 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 Z FROM THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 9/WITH SILVER DOWN 27 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 923,000 OZ INTO THE SLV////INVENTORY RESTS AT 545.229 MILLION OZ

JUNE 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 544.306 MILLION OZ//

JUNE 7/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.306 MILLION OZ/

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

CLOSING INVENTORY 514.501 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

END

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

An excellent commentary from Mathew on gold rigging. He emphasizes that Hambro has now finally admitted to the rigging

(Mathew Piepenburg/GATA)

Matthew Piepenburg: A gold industry veteran acknowledges the market rigging

Submitted by admin on Mon, 2022-07-11 10:35Section: Daily Dispatches

10:30a ET Monday, July 11, 2022

Dear Friend of GATA and Gold:

Matterhorn Asset Management’s Matthew Piepenburg today joins the acclaim for gold industry veteran Peter Hambro’s recent declaration that the price of gold long has been suppressed with derivatives masterminded through the Bank for International Settlements, the central bank of the central banks.

Piepenburg’s commentary is headlined “Paper Gold Price Manipulation — Rigged to Fail” and it’s posted at Matterhorn’s internet site, Gold Switzerland, ere:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

Paper Gold Price Manipulation—Rigged to Fail

July 11, 2022

The current and open fraud regarding the paper gold price in the COMEX market is now as plain to see as the open desperation in the global financial system, which is unraveling in real-time all around us.

As risk assets tumble foreseeably into bear territory before a headwind of deliberately rising rates, precious metals have seen headline-making falls as well.

Below, we explain why.

Tracking the Paper Gold Price —The Standard Answer

In prior reports, we’ve noted that precious metals typically behave sympathetically when markets tank; thereafter, gold then surges north. We saw this pattern in October of 2008 and March of 2020.

Furthermore, when a Hawkish Fed pursues a temporary yet face-saving policy of rate hiking and quantitative tightening, this makes the USD the relatively stronger horse in the global currency glue factory.

And a relative rise in the USD, of course, is a headwind to gold.

Explaining the Paper Gold Price —The Rigged Answer

But let’s get to the real heart of the matter, namely: Legalized paper gold price manipulation (i.e., fraud) in the COMEX market, a topic we’ve addressed more than once, here and here.

As we’ve openly argued for years, nothing embarrasses an otherwise discredited fiat currency like a rising gold price.

As I’ve described it, rising gold prices are a middle finger to debased currencies whose declining purchasing power are the DIRECT result of the failed and drunken monetary policies (i.e., mouse-click trillions) of a central bank near you.

Or as Ronan Manly more distinctly observed: “Gold to central bankers is like sun to vampires.”

And that, folks, is precisely why the big banks (under the direction of the BIS) are deliberately (and if law school serves me correctly) as well as fraudulently manipulating the paper gold price.

Facts vs. Manipulation

In the first quarter of 2022, we saw record high purchases of ETF gold, physical gold and central bank gold. Even Goldman Sachs’ head of commodity research was targeting $2400 gold this year.

Instead, the gold price has been falling as gold demand has been rising.

Huh?

It reminds me of 2008 when mortgages were defaulting en masse yet the ABX index for sub-prime mortgages was rising.

In short, complete (and temporary) manipulations were going on behind the curtains of a few wayward banks, including Morgan Stanley.

Today’s gold behavior (i.e., surreal manipulation) is no different and no less of an insult to the natural forces of supply and demand, which central bankers have attempted to destroy for well over a decade.

But the jig will soon be up on these masters of open fraud and Wall Street socialism.

The Paper Gold Price & The Horse’s Mouth

For now, and in case you fear I’m just acting as a “gold bug” apologist, let’s go straight to the horse’s mouth and examine the confessions and facts of open price manipulation in the precious metal markets.

And I swear, you really can’t make this stuff up, it’s just that obvious and distorted.

In a recent article by Peter Hambro published by the British news site, Reaction, a 3rd generation gold insider (Petropavlovsk, Bank Hambros) made the open secret of paper gold price manipulation abundantly clear and incontrovertible.

It’s also worth adding that Mr. Hambro’s entire career was that of an heir to a banking dynasty all too familiar with the insider machinations of the London bullion markets and London Stock Exchange.

In short, when Mr. Hambro discusses gold price manipulation, it’s worth listening.

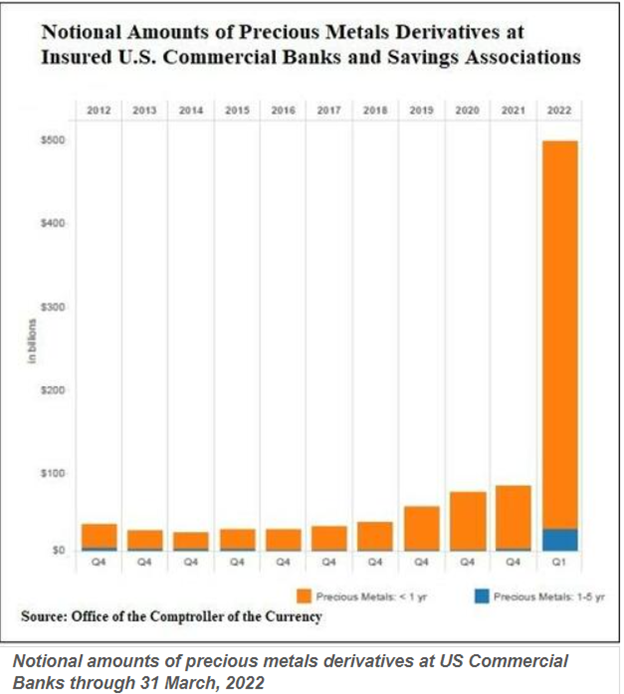

A Chart Says a Trillion+ Words

More importantly, and for those who prefer facts over human confessions or “gold bug whining,” the following chart from the U.S. Office of the Comptroller of the Currency (OCC) clearly reveals the extreme extent by which just a handful of highly pocketed (and central bank supported) banks like JP Morgan and Citi can use extreme turns of derivative-based leverage to short (i.e., keep a permanent boot to the neck of) the paper gold price:

That rising bar on the far right is nothing more than crime scene evidence.

As Hambro remarks, a long history of media and bank supported mis-information has tried to keep a lid on the desperate attempts by just a small number of BIS minion banks like JP Morgan and Citi to effectively prevent free market price discovery on the paper gold price.

Despite thousands of daily long contracts (i.e., buy orders) in the OTC forward contract markets, if just 7-8 banks wish to use massive leverage (rising bar on the right) to short the same metal, they can effectively fix the gold price via artificial manipulation of derivatives contracts, to which only a small number of banks have access.

All of this open yet legalized fraud is managed by the central-banks central bank, namely the Swiss-based Bank for International Settlements.

As Hambro states, and as taken from a recent article published by Ronan Manly:

”[s]ince 2018 the Financial Stability Desks at theworld’s central banks have followed theBank for International Settlements’ (BIS) instruction to hide the perception ofinflationby rigging the gold market.”

Hambro further observes:

“With the help of the futures markets and the connivance of the Alchemists, the bullion traders – yes, that includes me, I was Deputy Managing Director of Mocatta & Goldsmid – managed to create an unshakeable perception that ounces of gold credited to an account with a bank or bullion dealer were the same as the real thing. ‘And much easier, old chap! You don’t have to store or insure it’”.

So, there you have it: Banks acting badly, very badly.

No shocker there…

The Greenlight from Big Brother

In essence, a handful of 7-8 LBMA institutions creates an almost limitless amount of synthetic paper representing unallocated gold (i.e., gold they don’t actually own) to short the paper gold market.

Why?

Again, because the central bankers mouse-clicking and hence destroying trillions worth of sovereign currencies (since Nixon took the gold chaperone away in 1971) are utterly terrified of a neutral and relatively fixed/scarce monetary metal like gold—i.e., real money.

Indeed, gold is money, the rest is just debt and toilet paper masquerading as currency.

Furthermore, the policy makers (or central controllers) are embarrassed to confess the inflationary consequences of their absurd money printing, and nothing reveals those consequences more than a naturally rising gold price.

Solution?

Easy: Lie about inflation and rig the paper gold price with leverage, derivatives and a greenlight from the BIS, aka: “Big Brother.”

In Rigged to Fail, I revealed how central bankers rig the bond and hence stock markets. Here we are just showing you how the same bankers rig the gold price to hide a failed currency market.

And if you want to put a handsome face to the farce, here’s an unforgettable one:

What About Don’t Fight the Fed?

Of course, most of you may be angry yet not the least bit surprised to see such rigging hiding in plain sight.

And even if your eyes have been (or now are) wide open, you’re also likely to say, “great, thanks for the news, but how the heck can we (or gold) fight all the central banks?”

Fair question.

As I’ve said, even if you know about a dirty cop, there’s almost no point in fighting one, right?

The Jig (Rig) is Up

We may be a bit jaded and realistic, but that doesn’t make us naive. Gold will get the last and honest laugh over such a corrupt and dishonest “policy.”

As central banks continue to lose more and more credibility, and as investors become more and more fluent in, and aware of, the absurdity of the lies that have been sold to us for years by central bankers and MMT midgets who claim that a debt crisis can be solved with more debt, which is then paid for with trillions created out thin air, the system unwinds.

As the inevitable inflation crisis emerges from precisely such absurd “policies,” the central bankers can no longer blame the obvious and long-dated/repressed inflationary consequences of their drunken monetary policies on a virus or Putin.

Nor can they continue to peddle the lie that inflation was merely “transitory,”a fact we made clear long before Powell confessed it was not so.

Stated otherwise, more and more folks are catching on to the fraud.

The math plainly shows that expanding the broad money supply (and central bank balance sheets from $6T to $36T in just over a decade) is the real cause of the inflation in your neighborhood and the debasement in your wallet.

The First Cracks & the Last Straws

Geopolitical shifts, assassinated prime ministers, fired prime ministers, angry truck drivers, stormed capitals and Sri Lankan protestors are just the first tragic cracks in a growing social unrest driven by declining wealth and growing wealth disparity, all classic and historic symptoms and patterns of when a debt crisis leads to a political crisis, and sadly (and ultimately) more centralized controls over our markets and lives.

But as even Hambro observes, eventually the last straw breaks the back of a rigged camel, and the “straws blowing in the wind are often said to presage great tempests and I believe that {the chart above] shows just such a straw.”

Years of distorted, rigged and entirely reckless debt-and-print polices have made global economies and currencies weaker, not stronger.

The weaponized USD in the wake of the failed Putin sanctions is just further proof of how weak Western economies have become.

Dying Faith, Rising Gold

After years of profligate central bank policies, the so-called “developed economies,” which are now little more than glorified banana republics, are losing credibility, options and most importantly public faith.

This is critical.

In the end, when faith in a system ends, so does its currency.

We’ve written before how impossible it is to market time “the end of faith,” but charts like the one featured herein help to point out the rigging and hence accelerate the inevitable end to derivatives-based fraud, centralized price-fixing and, eventually, the OTC casino in particular.

Meanwhile, the current buy window for repressed precious metals is remarkable, and once central banks cripple the markets to their deflationary pain points, chaos will return, along with the inflationary money printers—all of which will send precious metals higher and fiat currencies and markets to their mean-reverting lows.

END

3. Chris Powell of GATA provides to us very important physical commentaries

There is no question that Ted Butler is right on this one: The massive shorting of silver and gold is not by the commercial banks but by speculators.

This will end very badly for them. The game will end if the commercials do not go back to the short side.

(Ted Butler)

Ted Butler: The perfect (and only) solution to shorting gold and silver

Submitted by admin on Mon, 2022-07-11 19:57Section: Daily Dispatches

7:55p ET Monday, July 11, 2022

Dear Friend of GATA and Gold:

Silver market analyst Ted Butler speculates today that the London Metals Exchange’s default on its nickel contract is prompting bullion banks to close their short positions in the monetary metals. Butler’s analysis is headlined “The Perfect (and Only) Solution” and it’s posted at GoldSeek’s companion site, SilverSeek, here:

https://silverseek.com/article/perfect-and-only-solution

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

C{Powell@GATA.org

The Perfect (and Only) Solution

Ted Butler

July 11, 2022

A new article by Reuters concerning this year’s default in nickel on the London Metals Exchange help me to crystalize some new thoughts on the recent dramatic collapse in commodity prices of all types, certainly including silver and gold. I would describe my new thoughts as being fully in line with all the major themes I’ve presented over the years, but now with a clarity I hadn’t quite anticipated. Please bear with me for a bit, as I try to tie this in with the current quite pronounced melt down in the prices of metals and other commodities.

The Reuters article didn’t provide anything really new, except to more clearly quantify the actual losses and margin calls involved when the LME rescinded and busted nickel trades on March 8. Had the trades not been busted and trading in nickel not been suspended, the margin calls due from the big nickel short (and its brokers) would have amounted to close to $20 billion on that date, an astoundingly large sum.

When a customer can’t meet a margin call due to an adverse market movement, that customer’s brokers are obligated to meet the call to the clearing house from the brokerages’ own funds. If the brokers holding the customer’s account can’t come up with enough of their own cash to satisfy the margin call, then all the other members of the clearing (guaranteeing) association are called upon to pony up the required cash to meet the margin call and keep the exchange solvent. It is the association of clearing members on every commodity exchange that guarantees the performance of all derivatives contracts and gives the exchanges their legitimacy. So large were the margin calls in nickel to the big short seller, that the exchange decided to simply cancel the trades and suspend trading, as it became obvious it would drag the LME into overall default; thereby suddenly ending 140 years of LME existence.

In order to avoid having the LME suddenly cease to exist, which would be the worst outcome possible, the exchange chose to cancel the trades and suspend trading, the next worst outcome. While I am not condoning the LME’s actions in any way, I do understand why it took the actions it did take. But nowhere in the Reuters article was it mentioned what the real problem was and how the LME failed to anticipate that problem.

Not to sound like a broken record, but the problem in LME nickel was the existence of a concentrated short position that was so large so as to endanger the entire exchange when the size of the position became obvious to all. The LME never should have allowed the nickel short position to grow as large as it got. No doubt, as the massive short position was established, its large size artificially depressed nickel prices initially, just as it caused prices to soar when it became obvious the short seller was in trouble – necessitating the busting of trades and suspension of trading. Had the LME properly performed its regulatory role, it never would have allowed the nickel short position to grow as large and concentrated as it did grow. Ignorance of the short position’s existence is hardly a legitimate defense by the LME.

As the world’s leading base metals exchange, a sudden and complete closure of the LME and the ripple effects that would have had, most likely, would have severely impacted the UK and financial systems elsewhere. On the other hand, since trading on the LME is limited to base metals, any financial system fallout would be a drop in the bucket compared to any similar problems that may arise at the CME Group, which, in addition to trading precious metals and copper, also offers trading in the widest variety of financial products, including stock and bond futures, currencies, energies, foodstuffs and grains. It would be easier to list the products that the CME doesn’t trade.

As such, the CME Group is very much a member of a highly select list of financial institutions officially considered to be systemically important, or too big to fail. Banking giants like JPMorgan, Bank of America and others, like giant asset manager BlackRock are also elite members of financial institutions considered to be systemically important. Should any of the financial institutions on this elite list ever fail, no doubt there would be serious implications for the financial system itself, both for the US and the world in general. Therefore, there’s no real comparison between the LME and the CME Group, in terms of what an actual failure of or contract default in each would mean to the financial system. In the order of financial system importance, with a higher number being more important – if the LME was a “1”, the CME would be a “100”.

That’s why, if the inadequate regulation on the LME in the case of not dealing with the concentrated short position in nickel before it was too late was serious, then any such failure by the CME, say in COMEX silver or gold, would be so much more serious. The LME defaulting was serious, but a default on the COMEX would be catastrophic for the CME and the financial system. Plus, I don’t recall hearing of any prior concerns of a massive concentrated short position in LME nickel before the default, whereas I have been screaming from the roof tops about COMEX silver having the largest concentrated short position of any commodity in real world terms for decades.

Simply put, the concentrated short position in COMEX silver and its resolution, is the most important factor, bar none, as anyone who has read any of my articles would attest. With that preamble, I would like to come full circle and further refine my take on how I see the concentrated short position in COMEX silver (and gold) getting resolved, after further digesting what occurred in LME nickel.

First, I must raise a set of circumstances so coincidental, so as to be nearly impossible to be purely coincidental. The default and busting of trades in LME nickel took place on March 8, 2022. On that same day, the price of gold hit its all-time high of $2080, while the price of silver hit $27.50, the highest it had been since June 2021. Since those price highs, gold has fallen more than $350 (17%), while silver has fallen by a much steeper $8.50 (30%).

Also, in the Commitments of Traders (COT) report for positions as of that same day, March 8, the concentrated short position of the 4 largest traders indicated a gold short position of 188,358 contracts (18.8 million oz) and a concentrated short position in silver of 54,187 contracts (271 million oz), with all the concentrated shorts held by commercial traders. As it turns out, this was the largest concentrated short position for COMEX gold since March 2020 and for silver since June 2021.

Interestingly, since March 8, the commercial-only concentrated short position in gold has fallen by more than 90,000 contracts (45%), while the true commercial-only portion of the concentrated silver short position has fallen by 23,000 contracts (42%), as of the COT report for positions held as of July 5, 2022.

My take on all this is that, while I’m not into deep conspiracies, the events of March 8, which culminated in the LME nickel default by the largest concentrated short seller, sent a powerful message to the concentrated shorts in COMEX gold and silver futures that they had better get their house in order and reduce their short positions pronto. My hundreds or thousands of allegations and complaints of concentrated short selling in COMEX silver and gold may have been brushed aside, but seeing the LME actually default due to concentrated short selling appears to have woken up the big COMEX commercial shorts. Either that, or the events of March 8 were simply some innocent coincidences.

Moreover, what I am now contending, namely, that the big commercial shorts in COMEX gold and silver have put in motion a plan to buy back and cover as many of their concentrated short positions as possible, looks to me to be the perfect and only real solution available to them. And the only way for the big commercial shorts to pull this off successfully would be to rig a market selloff of the ages – which is what we have just witnessed. Let’s face it, had the COMEX silver and gold concentrated short sellers waited too long and tried to buy on higher prices, as did the big short in LME nickel, it was likely there would have been a default on the COMEX – with much more negative fallout given the systemic importance of the CME.

In essence, the big commercial shorts on the COMEX have offloaded their short positions, largely to the managed money technical funds. As I’ve been reporting, the managed money technical funds are enjoying their best six months, performance-wise, in decades and, ironically, the money they’ve made has allowed them to take even bigger positions than otherwise. Of course, if it does turn out that the managed money traders do prevail when their current short positions are finally bought back (which assumes the commercials will sell at lower prices), then that will be confirmed in future COT reports. However, to this point, the managed money traders have never collectively made money whenever they have gone heavily short silver or gold.

At times like this in the past, when prices on a wide variety of commodities decline markedly in price due to technical fund selling, I recall suggesting the “silver disease” was spreading to other commodities. I’d define the “silver disease” as the uneconomic selling and selling short of derivatives contracts when there were no corresponding obvious signs of physical oversupply. Nothing I see indicates any sudden physical oversupply of crude oil, or grains or metals – yet prices are collapsing, as if there was physical oversupply. That’s because the managed money traders trade on price momentum, not the commodity’s actual fundamentals.

The only plausible explanation for the sudden spate of pronounced price weakness across a broad base of commodities is derivatives selling and short selling by traders motivated by price momentum. The selling is real enough in that it depresses prices, but not in the least bit economically legitimate because it’s as far from legitimate hedging as is possible. No silver miner would be looking to lock in the sharply lower prices of late. Instead, this has all the makings of a massive hoodwinking by the large commercial interests which dominate most markets in which the technical and price momentum traders operate.

I would place the blame for allowing speculative traders to massively plow onto the short side on the CFTC, because the selling was so large and purely speculative that it violates the reason why regulated futures trading exists in the first place (to allow legitimate hedging). But when the inevitable turn for higher prices occurs, the folly of the regulators allowing such large speculative selling will flip to much higher prices as the speculative short sellers rush to buy back what I consider to be their ill-advised short sales. The CFTC, essentially, abandoned the idea of legitimate speculative position limits a couple of years ago and the markets are now dealing with the aftermath of the agency’s failure.

I also can’t help but be further convinced, if my musings of the big concentrated COMEX commercial shorts getting a wake-up call as a result of the default in LME nickel are correct, that these big commercial shorts will be quite reluctant to put their heads back into the lion’s mouth by heavily shorting again. I know I have said it too many times in the past that the big shorts would stand aside and not short into future price rallies, not to acknowledge that that possibility exists – but that doesn’t take into account the default in LME nickel and what has transpired with the concentrated short positions in COMEX gold and silver since March 8. The good news is that whatever the big COMEX commercial shorts do or don’t do in the future will be recorded in future COT reports.

Therefore, the stage is set for a price explosion in silver and gold like never before. All the (former) big commercial concentrated shorts have to do to ensure the price powder keg goes off, is absolutely nothing – with nothing defined as not selling short aggressively on the next rally.

Ted Butler

July 11, 2022

END

4. OTHER GOLD COMMENTARIES

STEVE BROWN…

END

5.OTHER COMMODITIES:

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7214

OFFSHORE YUAN: 6.7374

HANG SANG CLOSED DOWN AT 279.45 PTS OR 1.37%

2. Nikkei closed DOWN 475.64 OR 1.77%

3. Europe stocks CLOSED ALL RED

USA dollar INDEX UP TO 108.07/Euro FALLS TO 1.0042

3b Japan 10 YR bond yield: RISES TO. +.239/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 136.78/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN -// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.144%/Italian 10 Yr bond yield FALLS to 3.24% /SPAIN 10 YR BOND YIELD FALLS TO 2.24%…

3i Greek 10 year bond yield FALLS TO 3.50//

3j Gold at $1736.60 silver at: 18.91 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 7/10 roubles/dollar; ROUBLE AT 58.20

3m oil into the 98 dollar handle for WTI and 102 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 136.78DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9815– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9900well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.926 DOWN 7 BASIS PTS

USA 30 YR BOND YIELD: 3.121 DOWN 6 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.37

Futures, Yields, Oil And Gold Slide As German Confidence Plummets To 2011 Lows, Euro Hits Parity

TUESDAY, JUL 12, 2022 – 07:59 AM

US index futures, global markets, Treasury yields, bitcoin and oil all fell on Tuesday as the dollar continued its relentless ascent to levels just shy of the March 2020 global crash record high…

… highlighting pervasive trader unease about the economic outlook as high inflation and a looming recession are set to unleash a catastrophic global recession coupled with a worldwide dollar shortage, now with the added boost of China’s renewed struggles with Covid. S&P and Nasdaq 100 emini futures dropped about 0.5% each having slumped as much as 0.9% earlier, as traders brace for an ugly Q2 earnings season which may provide clues on how companies are weathering inflation and recession concerns.

The US 10-year Treasury yield falls to about 2.91% amid a broad-based flight to safety; bonds also rallied in Europe. German bonds surged, sending the benchmark 10-year yield to the lowest since May, after data showed investor confidence plunged to a 2011 low.

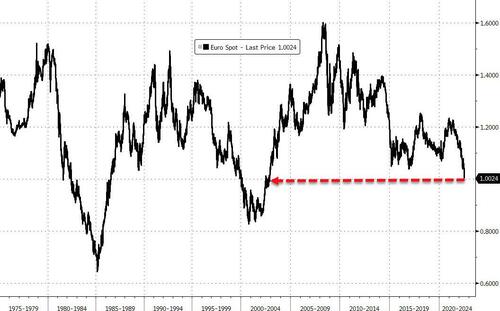

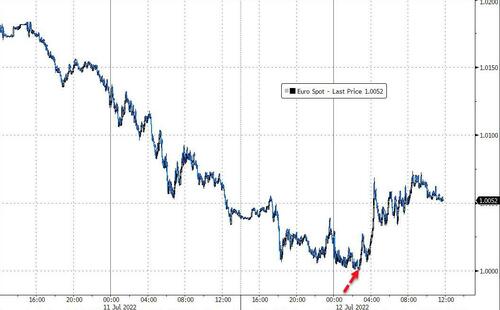

As shown above, the dollar rose just shy of record highs last seen at the height of the 2020 market panic over Covid and the yen strengthened, underlining investor caution. The euro meanwhile briefly touched parity (technically, it was 1.00003 but that’s semantics for purists who have nothing better to do) hammered by the region’s energy crisis and acute recession fears.

Dollar strength will not only “affect this quarter’s earnings, but more likely it’s going to affect the revenue generation outlook for the next couple of quarters and that, I think, is a big problem,” Kimberly Forrest, founder and chief investment officer of Bokeh Capital Partners, said on Bloomberg Radio.

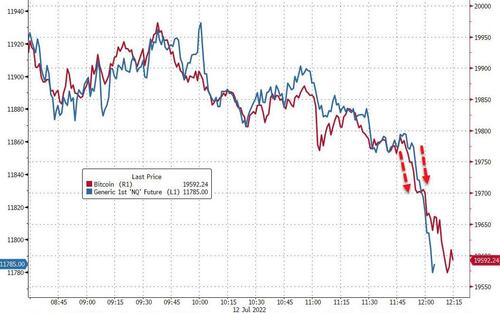

PepsiCo, one of the first major corporations to report, rose in premarket trading after lifting its revenue forecast. The soft-drinks maker said demand remained robust despite inflation, though it expected headwinds from the strong dollar. Bank stocks, meanwhile, were lower in premarket trading amid a broader slump in risk assets. Cryptocurrency stocks drop in premarket trading as Bitcoin drops below $20,000 in its fourth straight day of declines amid a stronger dollar. In corporate news, LoanDepot said it will cut about 2,000 additional staff by the end of the year. Here are the other notable premarket movers:

- Gap (GPS US) shares fall 6.4% in premarket trading after the apparel retailer fired CEO Sonia Syngal and said it expects rising costs and deepening discounts to erase this quarter’s operating profit.

- American Express (AXP US) shares are down 2.2% in premarket trading after Morgan Stanley cut the recommendation on the stock, as well as on Capital One (COF US), to equal- weight from overweight as inflation takes a larger share of household disposable incomes.

- STORE Capital (STOR US) shares fall 3.3% in premarket trading after Morgan Stanley downgrades it to underweight from equal-weight and cuts National Retail Properties (NNN US) to equal-weight from overweight, saying that US triple net REITs could see a headwind from the rising cost of capital.

- Ginkgo Bioworks (DNA US) shares are up 9% in premarket trading after exchange-traded funds managed by Cathie Wood’s Ark Investment Management bought 860,480 shares in the company.

Meanwhile, the latest Fed commentary highlighted both the central bank’s hawkishness and the risks that come with aggressive interest-rate hikes. Fed Bank of Atlanta President Raphael Bostic said the US economy can copewith higher interest rates and repeated his support for another jumbo move this month. Fed Bank of Kansas City President Esther George, who dissented last month against the central bank’s 75 basis-point rate increase, cautioned that rushing to tighten policy could backfire.

European bourses are also deep in the red. Euro Stoxx 50 falls 0.7% with the Stoxx Europe 600 sliding for a second day, though it pared the decline with utilities outperforming as EDF jumped after a report that the French government will pay a premium to take control of the electricity company. The DAX lags, dropping 0.8%. Banks, travel and autos are the worst performing sectors. German bonds surged, sending the benchmark 10-year yield to the lowest since May, after data showed investor confidence plunged to a level not seen since the sovereign debt crisis in 2011.

Asian stocks fell to a new two-year low as China’s technology shares continued to face selling pressure amid regulatory jitters and a resurgence of Covid cases in the nation. The MSCI Asia Pacific Index slipped as much as 1.5%, dragged by tech and consumer discretionary shares. The Hang Seng Tech Index fell 11% from a June high to enter a technical correction as regulatory fines for the country’s tech giants continued to damp sentiment.

In China, investors are concerned more Covid lockdowns may lie ahead as Beijing continues with a strategy of mass testing and mobility curbs. Chinese benchmarks took a hit from renewed lockdown fears from a fresh virus outbreak in Shanghai. Japan and Taiwan were among the region’s worst performing markets on lingering concerns of a global economic slowdown. Market participants are hoping that key US inflation data due Wednesday and China’s GDP figures on Friday will provide clues on the global economy’s direction. Asia’s stock benchmark has slumped 20% this year amid worries about higher interest rates and the prospect of an economic downturn. Investor sentiment continued to weaken in Asia despite remaining positive in China, said Olivier d’Assier, the head of APAC applied research at Qontigo. “Within an inflationary background, hopes of continued high profit margins in developed markets can only be balanced with fears of a margin squeeze among the developing world’s supply chain.”

In FX, the Bloomberg Dollar Spot Index rose a second day as the greenback was steady or higher against all of its Group-of-10 peers apart from the yen amid rising recession concerns. The euro fell to a low of 1.00003 per dollar but struggled to go below parity. Options traders are still preparing for life below this psychological support level. The pound lagged all of its Group-of-10 peers. UK retailers reported another drop in sales, while economists see the risk of a UK recession in the next 12 months at almost 50-50. Australian and New Zealand fell gradually. Iron ore prices sank to a seven- month low, with the demand outlook dimming on fears China may again impose strict Covid-19 curbs that hurt construction activity.

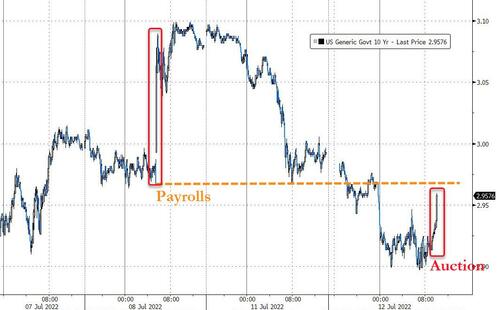

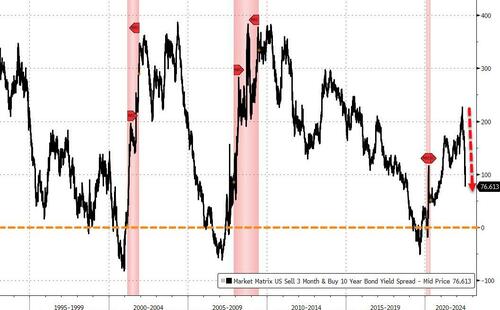

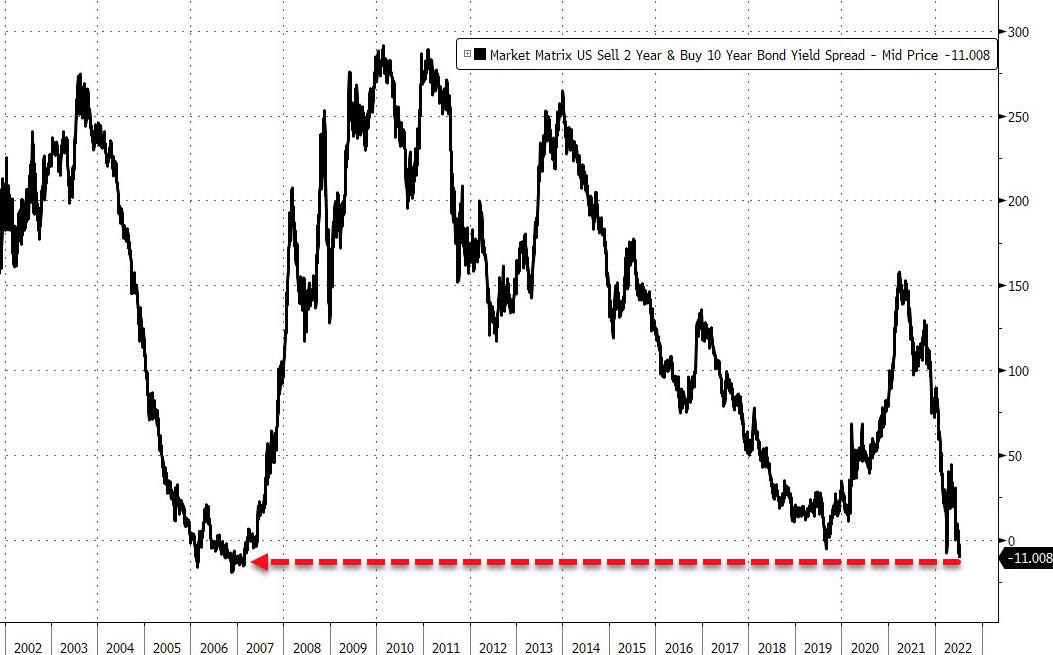

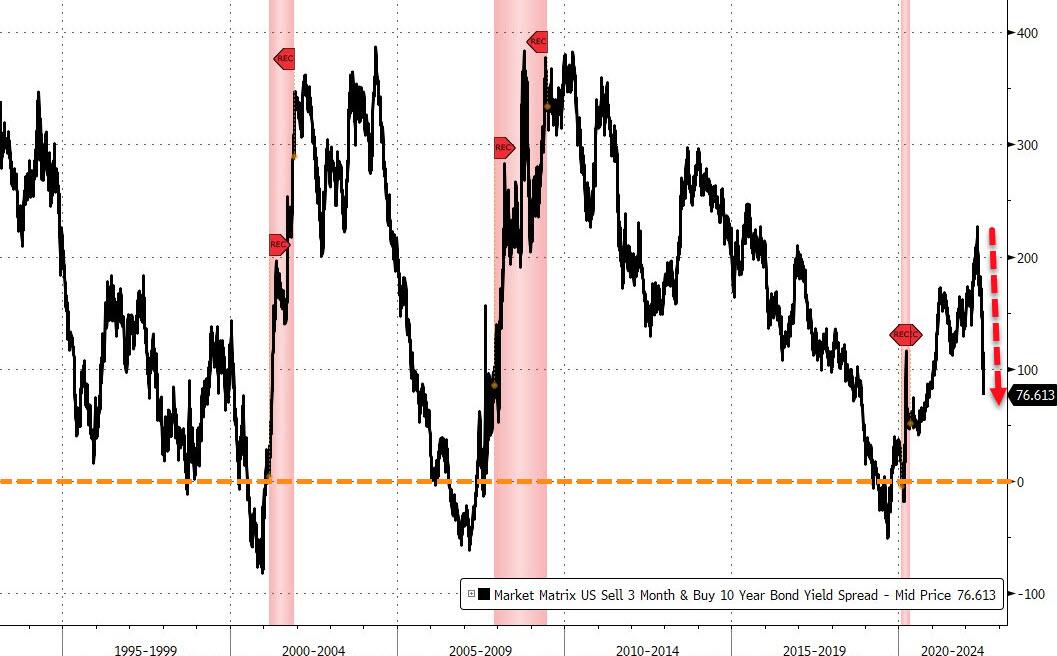

In rates, Treasuries were underpinned following gains for bunds and gilts after German ZEW expectations gauge dropped to -53.8 vs -40.5 estimate. Treasury yields richer by up to 7.5bp across intermediates, flattening 2s10s spread by 1.4bp on the day to -10.3bp, deepest inversion since 2007; German 10s outperform Treasuries by ~5bp, gilts by ~7bp. German 10-year yields dropped to lowest since May, dragging Treasury yields lower. German curve bull-flattens, richening 12-14bps across the back end. Gilts bull-steepen, with short-dated yields dropping over 15bps. Peripheral spreads widen to Germany with 10y BTP/Bund widening ~3bps to 199bps. In bond auctions we get a $33BN reopening of 10-year notes at 1pm ET follows good demand for Monday’s 3-year new issue, which stopped 0.5bp through. WI 10-year yield around 2.92% is ~11bp richer than June result, which tailed by 1.2bp.

Crude futures decline. WTI falls ~2.5% to trade near $101.60. Base metals are mixed; LME tin falls 3.1% while LME aluminum gains 0.3%. Spot gold is little changed at $1,735/oz. Spot silver loses 1.1% near $19. Bitcoin drops over 3.5% to trade back below $20,000.

Looking at the day ahead now, and data releases include the US NFIB small business optimism index for June. Central bank speakers include BoE Governor Bailey, the Fed’s Barkin and the ECB’s Villeroy. Finally, earnings releases today include PepsiCo.

Market Snapshot

- S&P 500 futures down 0.6% to 3,835.50

- STOXX Europe 600 down 0.4% to 413.46

- MXAP down 1.3% to 154.65

- MXAPJ down 1.3% to 508.44

- Nikkei down 1.8% to 26,336.66

- Topix down 1.6% to 1,883.30

- Hang Seng Index down 1.3% to 20,844.74

- Shanghai Composite down 1.0% to 3,281.47

- Sensex down 0.6% to 54,067.35

- Australia S&P/ASX 200 little changed at 6,606.28

- Kospi down 1.0% to 2,317.76

- German 10Y yield little changed at 1.16%

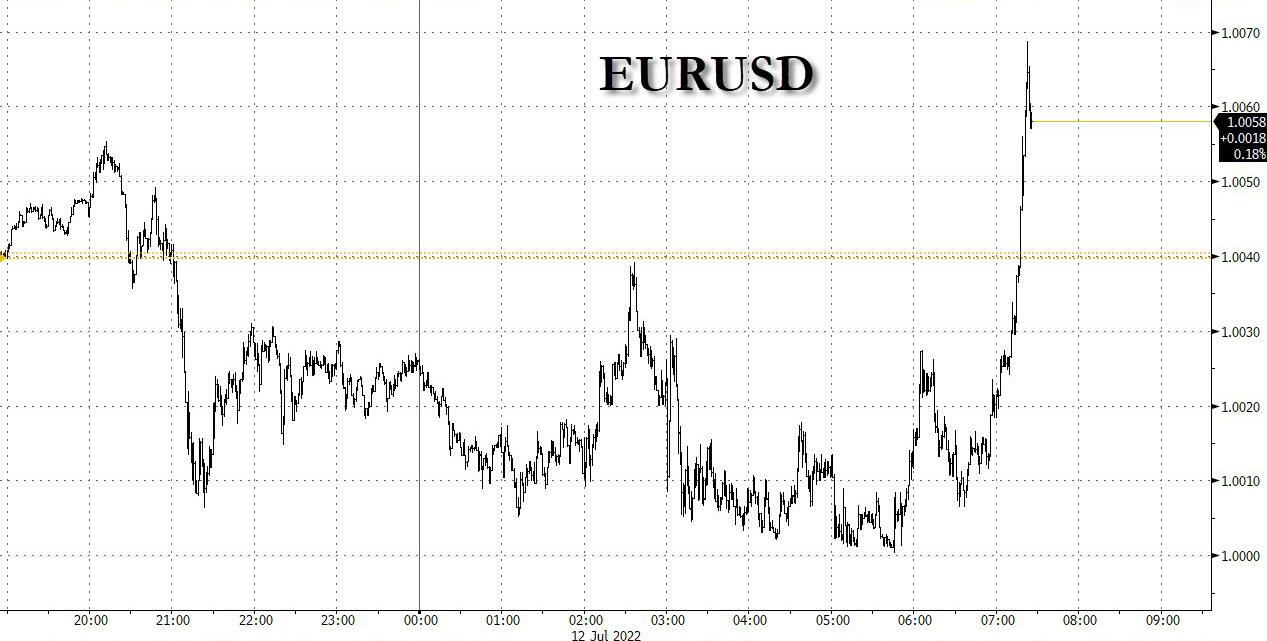

- Euro down 0.3% to $1.0008

- Brent Futures down 2.1% to $104.83/bbl

- Gold spot up 0.2% to $1,736.88

- U.S. Dollar Index up 0.43% to 108.48

Top Overnight News from Bloomnerg

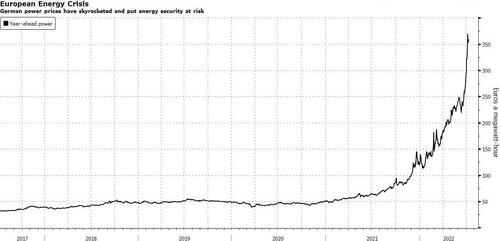

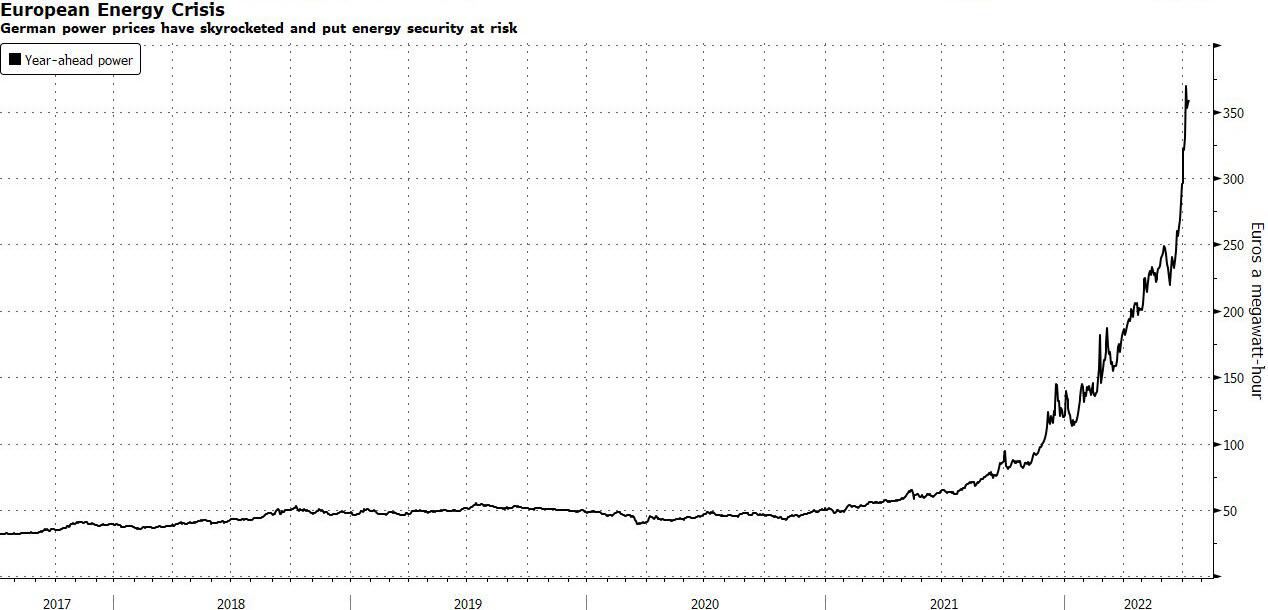

- Investor confidence in Germany’s economy slumped to the lowest since 2011 as the country faces the growing prospect of a recession and risks mount that it’s shut off from Russian energy supplies

- US Treasury Secretary Janet Yellen agreed with her Japanese counterpart Tuesday that volatile exchange rates pose a risk, and pledged to consult and cooperate as appropriate

- A global squeeze on energy supply that’s triggered crippling shortages and sent power and fuel prices surging may get worse, according to the head of the International Energy Agency

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mostly negative after the weak performance across global counterparts as China’s COVID flare-up and Europe’s energy concerns added to the headwinds for the growth outlook. ASX 200 bucked the trend with the index kept afloat by defensives although the upside was capped by weak consumer and business confidence data. Nikkei 225 underperformed as the Japanese currency attempted to compose itself from recent rapid depreciation and with automakers pressured after Toyota flagged a potential cut to its output plan citing a chip shortage and COVID impact. Hang Seng and Shanghai Comp. were lower amid the ongoing COVD concerns which overshadowed reports that China’s authorities will increase financial support for manufacturers, as well as the recent stronger than expected aggregate financing and loans data.

Top Asian News

- China is to lockdown Wugang city in Henan for 3 days due to 1 COVID case, according to Bloomberg.

- Japanese Finance Minister Suzuki said they will conduct necessary economic steps taking prices and economy into account, while he added that they are watching the FX market even more closely while working with the BoJ and will take necessary steps against the FX market with FX authorities from other nations, according to Reuters.

- Japanese Finance Minister told US Treasury Secretary Yellen that Japan is concerned about the rapid JPY weakening recently; watching currency markets with a sense of urgency; agreed to continue consulting in foreign exchange.

European bourses are pressured in a broad China-COVID driven risk move, Euro Stoxx 50 -0.5%; alongside known concerns and a dismal ZEW. Stateside, futures are lower across the board with the NQ somewhat more choppy than peers amid pronounced rate activity this morning and on PEP earnings. Back to Europe, sectors are mixed and feature IT as the laggard while Energy is green despite benchmark pricing amid outperformance in EDF.

PepsiCo Inc (PEP) Q2 2022 (USD): EPS 1.86 (exp. 1.74), Revenue 20.2bln (exp. 19.51bln). FY Revenue view 82.7bln (exp. 82.72bln)

Top European News

- UK’s Heathrow airport is imposing a capacity cap of 100k departing passengers a day, until September 11th. Beleive further action is needed now; cap means some summer journeys will be rescheduled, relocated or cancelled. Asks airline partners to stop the sale of summer tickets in order to limit the passenger impact.

- Former UK Chancellor Sunak confirmed his commitment to fiscal discipline and will stand firm on taxes until he has ‘gripped inflation’, according to FT.

- German ZEW Economic Sentiment (Jul) -53.8 vs. Exp. -38.3 (Prev. -28.0); ZEW Survey Expectations (Jul) -51.1 (Prev. -28.0)

- ZEW: current major concerns about energy supply, ECB’s announced rate hikes, restrictions in China, led to a deterioration in the outlook; economic situation significantly more negative than in previous month, experts further lower their already unfavourable forecast for the next six months.

Fixed Income

- Bonds breach recent resistance levels, with Bunds up to new July highs at 153.48 after a bleak German ZEW survey

- Gilts back on the 116.00 handle from a 115.04 Liffe low awaiting more comments from BoE Governor Bailey and 10 year T-note towards top of 119-03/118-09+ range pre-USD 33bn refunding leg

- DMO’s 2032 tap well received and German Schatz covered, but results mixed overall

FX

- Pound underperforms awaiting UK political developments as Labour Party prepares no-confidence motion against Tories; Cable on the cusp of 1.1800, while EUR/GBP rebounds over 0.8450.

- Euro prods parity vs Dollar before and after dire German ZEW survey, while DXY breaches 108.500 amidst broad Buck gains.

- Yen regroups as risk sentiment remains sour and yields retreat further, with Japan’s Finance Minister also raising concern about rapid decline, USD/JPY closer to 137.00 than 137.50+ top and Monday’s 137.75 peak.

- Loonie and Nokkie recoil alongside crude prices, but Kiwi holds up better than Aussie ahead of anticipated 50bp RBNZ rate hike on Wednesday, USD/CAD back up near 1.3050, EUR/NOK propped around 10.2600, NZD/USD holding just above 0.6100 and AUD/USD sub-0.6750.

- Yuan breaks below recent range as China’s Covid situation continues to deteriorate – USD/CNH and USD/CNY probe 6.7500 and 6.7350 respectively.

Commodities

- WTI and Brent have extended on APAC pressure as the demand-side of the equation remains sensitive to lockdowns with the OPEC MOMR and EIA STEO due.

- Currently, benchmarks are in relative proximity to their respective USD 101.06/bbl and USD 104.35/bbl lows.

- IEA’s Birol said the world is in the midst of the first energy crisis and it has not seen the worst of the energy crisis, according to Bloomberg.

- US senior official warned that a failure to implement a proposed price cap on Russian oil with the exemption of purchases below the cap, could see oil prices increase to around USD 140/bbl, while the official added that Treasury Secretary Yellen will speak to Japanese Finance Minister Suzuki on the proposed Russian oil price cap, according to Reuters.

- US Department of Energy announced a contract for 14 companies to purchase crude oil from the SPR with deliveries to take place between August 16th to September 30th, according to Reuters.

- China’s NDRC says retail prices of gasoline and diesel will be cut by CNY 360/tonne and CNY 345/tonne respectively from July 13th.

- US National Security Adviser Sullivan responded that there is a capacity for further steps that can be taken when questioned about oil output, according to Reuters.

- Spot gold is relatively resilient despite broader price action, and the yellow metal is torn between COVID-driven haven allure and the USD’s ongoing advances.

US Event Calendar

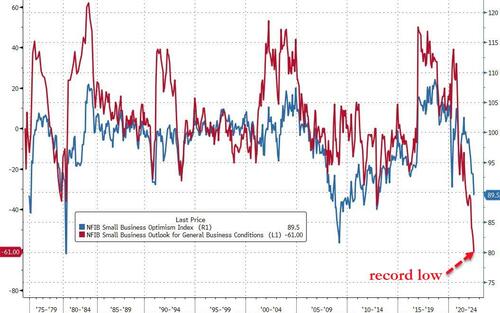

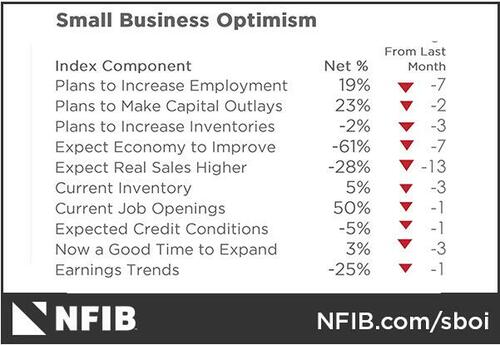

- 06:00: June SMALL BUSINESS OPTIMISM, 89.5, est. 92.5, prior 93.1

Central Banks

- 12:30: Fed’s Barkin Discusses the ‘Recession Question’

Government:

- President Biden will meet with Mexico President Andrés Manuel López Obrador at 11:15am ET

- House Jan. 6 select committee will hold a hearing on the extremists involved in the assault at 1pm ET

DB’s Jim Reid concludes the overnight wrap

It’s so hot, even at 5am, that I have two fans pointing at me as I type this. Electric ones not two people that have kindly voted for me in the II survey. Never has a commute to the office and the lure of aircon been so alluring. When we renovated 3-4 years ago we considered having some aircon fitted but decided that given the cost we would forgo that for the couple of days a year where Britain sweltered. Given that this spell looks set to last a couple of weeks I may sleep in the office, especially as the kids have now broken up and are running riot at home.

The heat may have also tired markets out after a mini rally so far in July. The last 24 hours has seen sentiment become more gloomy once again as investors looked forward to multiple data releases and earnings reports this week that’ll set the stage for some important central bank meetings over the next couple of weeks. The US CPI report will be the main highlight tomorrow, but we shouldn’t forget the start of the Q2 earnings season either, which will shed some light on how corporates are faring as the market narrative has flirted with the view that the US economy might already be in a recession. One bit of “good” news yesterday was the NY Fed’s long-run consumer inflation expectations series which showed a decent dip and helped encourage a big rally in bonds as the tug of war in the asset class continues.

More on that later but equities didn’t get that memo as they lost ground on both sides of the Atlantic yesterday with the S&P 500 shedding -1.15% by the close of trade, in what looked like a classic risk off rotation, with only Utilities and Real Estate higher, and the latter only barely up (+0.01%). Tech stocks led the declines, with the NASDAQ down by -2.26% whilst the FANG+ index of megacap tech stocks saw an even larger -4.52% decline as all 10 companies in the index lost ground. Along with a sour risk day, mega-cap shares were probably sluggish following the news over the weekend that Elon Musk would be pulling out of his Twitter deal. Small-caps were another underperformer, with the Russell 2000 down -2.11%, whereas the Dow Jones experienced a more modest -0.52% loss. Meanwhile in Europe it was much the same story, with the STOXX 600 (-0.50%) and Germany’s DAX (-1.40%) seeing decent losses of their own.

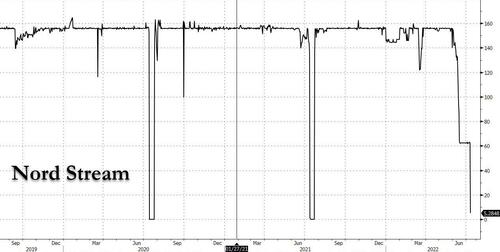

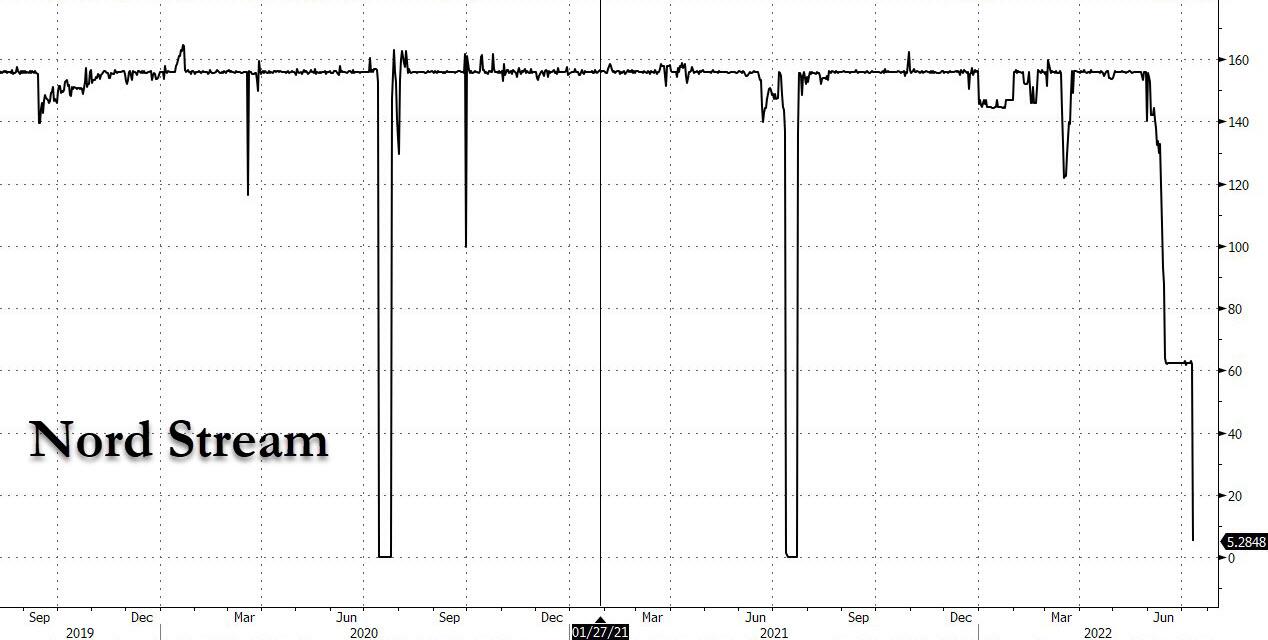

Speaking of Europe, all eyes are on what’s going to happen with the gas situation now that the Nord Stream pipeline is undergoing scheduled 10-day maintenance. European natural gas futures (-6.10%) did come down yesterday after rising for 4 consecutive weeks, thanks to the news at the very end of last week that Canada would return a turbine for the Nord Stream pipeline after their government issued a “time-limited and revocable” permit that removed it from sanctions. That said there are still significant jitters as to whether the pipeline will be turned back on again after the maintenance concludes, which meant that the Euro itself fell even closer to parity against the US Dollar. In fact, the euro closed near its weakest levels of the day at $1.0040, and has hit a fresh low of $1.0010 as we go to press as markets face up to the prospect of what a full cut-off of Russian gas would mean for the European economy. Speaking to DB’s Peter Sidorov yesterday, he tells me that the ambiguity over gas may linger as even if Russia did need this turbine part to restore stronger gas flows, the technical logistics may mean it would take an extra week or two to integrate into the pipeline. So the uncertainty may linger until early August.