by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1737.15 UP $10.55

SILVER: $19.24 UP 24 CENTS by

GOLD; $1737.15 UP $10.55

ACCESS MARKET: GOLD $1735.60

SILVER: $19.21

Bitcoin morning price: $19,758 UP 198

Bitcoin: afternoon price: $19,703. UP 253

Platinum price: closing UP $9.80 to $859.95

Palladium price; closing DOWN $62.35 at $2040.50

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JULY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,723.300000000 USD

INTENT DATE: 07/12/2022 DELIVERY DATE: 07/14/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 150

323 H HSBC 180

657 C MORGAN STANLEY 1

661 C JP MORGAN 331 272

800 C MAREX SPEC 3

880 C CITIGROUP 23

905 C ADM 2

TOTAL: 481 481

MONTH TO DATE: 4,470

no. of contracts issued by JPMorgan: 272/481

_____________________________________________________________________________________

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT 481 NOTICE(S) FOR 48,100 Oz//1.4962 TONNES)

total notices so far: 4470 contracts for 447,000 oz (13.903 tonnes)

SILVER NOTICES:

169 NOTICE(S) FILED 845,000 OZ/

total number of notices filed so far this month 2860 : for 14,300,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $10.55

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORMTHE GLD///

INVENTORY RESTS AT 1021.53 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 24 CENTS

AT THE SLV// ://NO CHANGES IN SILVER INVENTORY AT THE SLV//:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 514.501 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A FAIR SIZED CONTRACTS TO 142,259 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GAIN IN OI WAS ACCOMPLISHED DESPITE OUR $0.16 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.16) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SILVER LONGS//BUT MAINLY WE HAD ADDITIONAL SPECULATOR ADDITIONS AS WE HAD A STRONG GAIN OF 780 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A POOR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.220 MILLION OZ FOLLOWED BY TODAY’S 155,000 OZ QUEUE JUMP / // V) STRONG SIZED COMEX OI GAIN

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -119

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTACTS for 8 days, total 7757 contracts: 38.785 million oz OR 4.848 MILLION OZ PER DAY. (969 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 38.785 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 38.785 MILLION OZ

RESULT: WE HAD A FAIR SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 376 DESPITE OUR $0.16 LOSS IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 285 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A POOR INITIAL SILVER OZ STANDING FOR JUNE. OF 15.22 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 155,000 OZ // .. WE HAD A STRONG SIZED GAIN OF 661 OI CONTRACTS ON THE TWO EXCHANGES FOR 3.305 MILLION OZ DESPITE THE LOSS IN PRICE..

WE HAD 169 NOTICES FILED TODAY FOR 845,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A HUMONGOUS SIZED 26,579 CONTRACTS TO 542,493 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: —1332 CONTRACTS.

.

THE STRONG SIZED INCREASE IN COMEX OI CAME WITH OUR FALL IN PRICE OF $4.45//COMEX GOLD TRADING/TUESDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR GOOD SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERING

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JULY AT 2.914 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 45,200 OZ

YET ALL OF..THIS HAPPENED DESPITE OUR LOSS IN PRICE OF $4.45 WITH RESPECT TO TUESDAY’S TRADING

WE HAD AN ATMOSPHERIC SIZED GAIN OF 31,337 OI CONTRACTS 97.47 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6090 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 543,825

IN ESSENCE WE HAVE AN ATMOSPHERIC SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 32,669 CONTRACTS WITH 26,579 CONTRACTS INCREASED AT THE COMEX AND 6090 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 32,669 CONTRACTS OR 101.61 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (6090) ACCOMPANYING THE HUMONGOUS SIZED GAIN IN COMEX OI (25,247,): TOTAL GAIN IN THE TWO EXCHANGES 31,337 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING AND SOME ADDITION TO SPECULATOR SHORTS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JULY. AT 2.914 TONNES FOLLOWED BY TODAY’S 43,200 OZ QUEUE JUMP 3) ZERO LONG LIQUIDATION//SOME SPECULATOR SHORT COVERING//SOME SPECULATOR SHORT ADDITIONS //.,4) STRONG SIZED COMEX OPEN INTEREST GAIN 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

45,246 CONTRACTS OR 4,524,600 OZ OR 140.73 TONNES 8 TRADING DAY(S) AND THUS AVERAGING: 5655 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAY(S) IN TONNES: 140.73 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 140.73/3550 x 100% TONNES 3,97% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 2238.13 TONNES FINAL

JULY: 140.73 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JULY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A FAIR SIZED 376 CONTRACT OI TO 142,259 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 285 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 285 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE:285 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 376 CONTRACTS AND ADD TO THE 425 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 661 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 3.305 MILLION OZ

OCCURRED DESPITE OUR FALL IN PRICE OF $0.16 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 2.83 PTS OR 0.09% //Hang Sang CLOSED DOWN 46.79 OR 0.22% /The Nikkei closed UP 142.11 OR % 0.54. //Australia’s all ordinaires CLOSED UP 0.31% /Chinese yuan (ONSHORE) closed DOWN 6.7267 /Oil DOWN TO 96.48 dollars per barrel for WTI and DOWN TO 99.84 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7274 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7281: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A HUGELY POWERFUL SIZED 25,247 CONTRACTS TO 542,493 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS GIGANTIC COMEX INCREASE OCCURRED DESPITE OUR LOSS OF $4.45 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2594 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 6090 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :6090 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 6090 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: AN ATMOSPHERIC SIZED SIZED TOTAL OF 32,669 CONTRACTS IN THAT 6090 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD AN UNBELIEVABLY SIZED COMEX OI GAIN OF 25,247 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $4.45.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING JULY (14.137),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 14.137 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $4.45) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS/COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS//// WE HAVE REGISTERED AN ATMOSPHERIC SIZED GAIN OF 97.47 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR JULY (14.137 TONNES)…

WE HAD -1332 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 31,337 CONTRACTS OR 3,133,700 OZ OR 97.47 TONNES

Estimated gold volume 389,319/// strong/

final gold volumes/yesterday 373,708 /strong

INITIAL STANDINGS FOR JULY ’22 COMEX GOLD //JULY 13

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 232,924.452 oz Brinks HSBC JPMorgan Manfra .includes3523 kilobars and 2634 kilobars (Brinks and HSBC) |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 481 notice(s)48,100 OZ1.4962 TONNES |

| No of oz to be served (notices) | 507 contracts 50,700 oz1.576 TONNES |

| Total monthly oz gold served (contracts) so far this month | 4470 notices447,000 OZ13,903 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

3 customer withdrawals:

i)Out of Brinks 113,267.980 oz (3523 kilobars)

ii) Out of HSBC: 84,685.734. oz (2634 kilobars)

iii) JPMorgan: 302.30 oz

iv) out of Manfra; 34,668.438 oz

total withdrawal: 232,924.452 oz

ADJUSTMENTS:1 dealer to customer

JPMorgan: 52,759.791 oz

Manfra: 8841.140 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 988 contracts GAINED 405 contracts . We had

27 notices filed on Tuesday so we gained a HUGE 432 contracts or an additional 43,200 oz will stand in this non active

delivery month of July.

August has a LOSS OF 21,100 contracts down to 305,700 contracts

Sept. gained 5 contracts to 2498 contracts.

We had 481 notice(s) filed today for 48,100 oz FOR THE July 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 391 notices were issued from their client or customer account. The total of all issuance by all participants equate to 481 contract(s) of which 272 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2022. contract month,

we take the total number of notices filed so far for the month (4470) x 100 oz , to which we add the difference between the open interest for the front month of (JULY 988 CONTRACTS ) minus the number of notices served upon today 481 x 100 oz per contract equals 497,700 OZ OR 15.480 TONNES the number of TONNES standing in this active month of July.

thus the INITIAL standings for gold for the JULY contract month:

No of notices filed so far (4470) x 100 oz+ (988) OI for the front month minus the number of notices served upon today (481} x 100 oz} which equals 497,700 oz standing OR 15.480 TONNES in this active delivery month of JULY.

TOTAL COMEX GOLD STANDING: 15.480 TONNES (A FAIR STANDING FOR A JULY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,443,533.842 oz 76.00 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 32,470,435.411 OZ

TOTAL ELIGIBLE GOLD: 15,997,842.819 OZ

TOTAL OF ALL REGISTERED GOLD: 16,472,592.592 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 13,554,309.0 OZ (REG GOLD- PLEDGED GOLD) 421 tonnes

END

SILVER/COMEX/JULY 13

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,923,993.840 oz CNT JPMorgan Loomis Manfra |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,768,943.959 oz Brinks Delaware JPMorgan |

| No of oz served today (contracts) | 169CONTRACT(S)845,000 OZ) |

| No of oz to be served (notices) | 154 contracts (770,000 oz) |

| Total monthly oz silver served (contracts) | 2860 contracts 14,300,000oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 3 deposits into the customer account

i) Into JPMorgan: 1,744,814.200 oz

ii) Into Brinks: 20,147.700 oz

iii0 IntDelaware 3982.059

total deposit: 1,768,943.959 oz

JPMorgan has a total silver weight: 175.742 million oz/339.376 million =51.76% of comex

Comex withdrawals: 4

i) Out of CNT: 951.200 oz

ii) Out of loomis 751,708.969 oz

iii)Out of JPMorgan: 1,187,126.900 oz

iv) out of Manfra:20,147.700 oz

total withdrawal 1,923,993.860 oz

adjustments: 2/dealer to customer

i) Brinks 2,092,312.540 oz

ii)HSBCL 84,934.870 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 62.699 MILLION OZ

TOTAL REG + ELIG. 339.376 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JULY OI: 323 CONTRACTS HAVING GAINED 22 CONTRACTS HAD 9 NOTICES FILED

ON TUESDAY, SO WE GAINED 31 CONTRACTS OR AN ADDITIONAL 65,000 OZ WILL STAND FOR METAL AT THE COMEX.

AUGUST GAINED 32 CONTRACTS TO STAND AT 1136

SEPTEMBER HAD A GAIN OF 27 CONTRACTS UP TO 116,684 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 169 for 845,000 oz

Comex volumes:64.249// est. volume today// poor

Comex volume: confirmed yesterday: 57,232 contracts ( poor )

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 2860 x 5,000 oz = 14,300,000 oz

to which we add the difference between the open interest for the front month of JULY(323) and the number of notices served upon today 169 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY./2022 contract month: 2860 (notices served so far) x 5000 oz + OI for front month of JULY (323) – number of notices served upon today (169) x 5000 oz of silver standing for the JULY contract month equates 15,070,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JULY 13/WITH GOLD UP $10.55:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROMTHE GLD//INVENTORY RESTS AT 1021.53TONNES

JULY 12/WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESS AT 1023.27 TONNES

JULY 11/WITH GOLD DOWN $4.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWL OF 1.16 TONNES FROM THE GLD./INVENTORY RESTS AT 1023.27 TONNES

JULY 7/WITH GOLD UP $1.35: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.61 TONNES FORM THE GLD///INVENTORY REST AT 1024.43 TONNES

JULY 6/WITH GOLD DOWN $26.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 9.86 TONNES FROM THE GLD//INVENTORY REST AT 1032.04 TONNES

JULY 5/WITH GOLD DOWN $36.55//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.41 TONNES FROM THE GLD///INVENTORY RESTS AT 1041.90 TONNES

JULY 1/WITH GOLD DOWN $5.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES//INVENTORY RESTS AT 1050.31 TONNES

JUNE 30/WITH GOLD DOWN $9.20: big CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 1052.63 TONNES//

JUNE 28/WITH GOLD DOWN $3.05//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.64 TONNES FROM THE GLD///INVENTORY RESTS AT 1056.40 TONNES

JUNE 27/WITH GOLD DOWN $4.90 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.04 TONNES

JUNE 24/WITH GOLD UP 45 CENTS TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.70 TONNES FROM THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 23/WITH GOLD DOWN $8.60:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//INVENTORY RESTS AT 1071.77 TONNES

JUNE 22/WITH GOLD UP 15 CENTS:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1073.80 TONNES

JUNE 21/WITH GOLD DOWN $2.00: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1075.54 TONES

JUNE 17/WITH GOLD DOWN $11.25: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.60 TONNES INTO THE GLD.///INVENTORY RESTS AT 1075.54 TONNES

JUNE 16/WITH GOLD UP $28.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.74 TONNES

JUNE 15/WITH GOLD UP $6.50/BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.65 TONNES FROM THE GLD////INVENTORY RESTS AT 1063.74 TONNES

JUNE 14/WITH GOLD DOWN $18.80/NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 13/WITH GOLD DOWN $41.55: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 10/WITH GOLD UP $21.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 9/WITH GOLD DOWN $3.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1065.39 TONNES

JUNE 8/WITH GOLD UP $4.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 7/WITH GOLD UP $7.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

GLD INVENTORY: 1021.53 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JULY 13/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SV//INVENTORY RESTS AT 514,501 MILION OZ.

JULY 12/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A IWTHDRAWAL OF 3.228 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 514.501 MILLION OZ//

JULY 11/WITH SILVER DOWN 17 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 5.533 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 517.729 MILLION OZ

JULY 7/WITH SILVER UP 3 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.889 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 523.262 MILLION OZ/

JULY 6/WITH SILVER UP ONE CENT: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 12.558 MILLION OZ FORM THE SLV///INVENTORY RESTS AT 528.151 MILLION OZ

JULY 5/WITH SILVER DOWN 55 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 540.709MILLION OZ//

JULY 1/WITH SILVER DOWN 61 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ//INVENTORY RESTS AT 540.709 MILLION OZ//

JUNE 30/WITH SILVER DOWN 41 CENTS : SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 738,000 OZ FROM THE SLV//INVENTORY RESTS AT 541.262 MILLION OZ//

JUNE 28/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.00 MILLION OZ..

JUNE 27/WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 24/WITH SILVER UP 10 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.137 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 23/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 2.029 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 545.137 MILLION OZ//

JUNE 22/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.166 MILLION OZ.

JUNE 21/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.506 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 547.166 MILLION OZ//

JUNE 17/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 739,000 OZ FROM THE SLV./:INVENTORY RESTS AT 543.660 MILLION OZ/

JUNE 16/WITH SILVER UP 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 15/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 14/WITH SILVER DOWN 32 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 13/WITH SILVER DOWN 62 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 10.WITH SILVER UP 13 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 Z FROM THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 9/WITH SILVER DOWN 27 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 923,000 OZ INTO THE SLV////INVENTORY RESTS AT 545.229 MILLION OZ

JUNE 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 544.306 MILLION OZ//

JUNE 7/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.306 MILLION OZ/

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

CLOSING INVENTORY 514.501 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

END

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

END

3. Chris Powell of GATA provides to us very important physical commentaries

Hedge funds cut back trading after LME nickel chaos

Submitted by admin on Tue, 2022-07-12 10:38Section: Daily Dispatches

By Laurence Fletcher

Financial Times, London

Tuesday, July 12, 2022

Hedge funds have cut back positions in some markets that they fear could suddenly become difficult to transact in, following the London Metal Exchange’s decision to void thousands of nickel trades.

The LME’s move in March to cancel eight hours’ worth of trades has pushed a number of hedge funds to reassess the risk they face across their portfolios from human interference upending their positions.

The exchange stepped in to halt a squeeze on a short seller and protect other users from heavy losses after the price of nickel soared by 250% in just a couple of days, to $100,000 a tonne.

Its shift provoked uproar among traders, not only because many lost out on profits but also because it left them with unhedged positions in other metals markets.

Rotterdam-based quantitative hedge fund Transtrend, which trades global futures markets and manages $6.5 billion in assets, told the Financial Times that it had decided to stop trading on the LME “following the nickel debacle.” It added that this decision had led to it running smaller positions in metals than it would otherwise have held.. …

… For the remainder of the report:

https://www.ft.com/content/6c8385bf-b477-41f6-bfdc-10044f5ec0d7

END

4. OTHER GOLD COMMENTARIES

END

5.OTHER COMMODITIES:

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

“Whereabouts Unknown”: 3 Arrows Capital Founders Go MIA Amidst Crypto Firm’s Bankruptcy

TUESDAY, JUL 12, 2022 – 07:45 PM

The founders of 3 Arrows Capital have apparently made a good ole-fashioned run-for-it…

The bankrupt crypto hedge fund founders have not been cooperating in the liquidation process of the firm, according to a Bloomberg report this week. And to do one better, their whereabouts have simply been “unknown” since last Friday.

Those founders, Kyle Davies and Zhu Su, have not contacted representatives setup to help liquidate the firm by a BVI judge last week, the report says. However, lawyers for the two men have reportedly said they intend on cooperating.

A photo posted by Bloomberg this week shows the company’s headquarters seemingly abandoned….

A court hearing is set for Tuesday this week, as liquidators seek to stop the “dissipation” of the firm’s assets.

Lawyers for the liquidators said: “Here, that risk is heightened because a substantial portion of the Debtor’s assets are comprised of cash and digital assets, such as cryptocurrencies and non-fungible tokens, that are readily transferable.”

3AC has been just one of the major firms – joining names like Celsius and Voyager – that has collapsed as a result of the plunge in bitcoin. Insolvency proceedings in the BVI have started, as has a Chapter 15 bankruptcy filing in the US.

Liquidators went to Three Arrows’ office address in Singapore, which “appeared dormant”. Bloomberg reported:

“…the door was locked, computers were inactive and mail was stuffed under the door. People working in the surrounding offices said they hadn’t seen anyone enter or exit the office recently.”

Lawyers for the two men were on a Zoom call with the liquidators last week, but it was unclear if Zhu and Kyle were even on the call:

“While persons identifying themselves as “Su Zhu” and “Kyle” were present on the Zoom call, their video was turned off and they were on mute at all times with neither of them speaking despite questions being posed to them directly.

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7267

OFFSHORE YUAN: 6.7281

HANG SANG CLOSED DOWN AT 279.45 PTS OR 1.37%

2. Nikkei closed UP 142.11 OR 0.54%

3. Europe stocks CLOSED ALL RED

USA dollar INDEX DOWN TO 107.82/Euro RISES TO 1.0059

3b Japan 10 YR bond yield: FALLS TO. +.229/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 137.09/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.144%/Italian 10 Yr bond yield FALLS to 3.24% /SPAIN 10 YR BOND YIELD FALLS TO 2.24%…

3i Greek 10 year bond yield FALLS TO 3.45//

3j Gold at $1729.30 silver at: 19.00 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 5/8 roubles/dollar; ROUBLE AT 58.28

3m oil into the 96 dollar handle for WTI and 99 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 137.07DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9760– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9813well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.960 DOWN 0 BASIS PTS

USA 30 YR BOND YIELD: 3.156 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.39

Futures Grind Higher With All Eyes On Red-Hot CPI

WEDNESDAY, JUL 13, 2022 – 07:57 AM

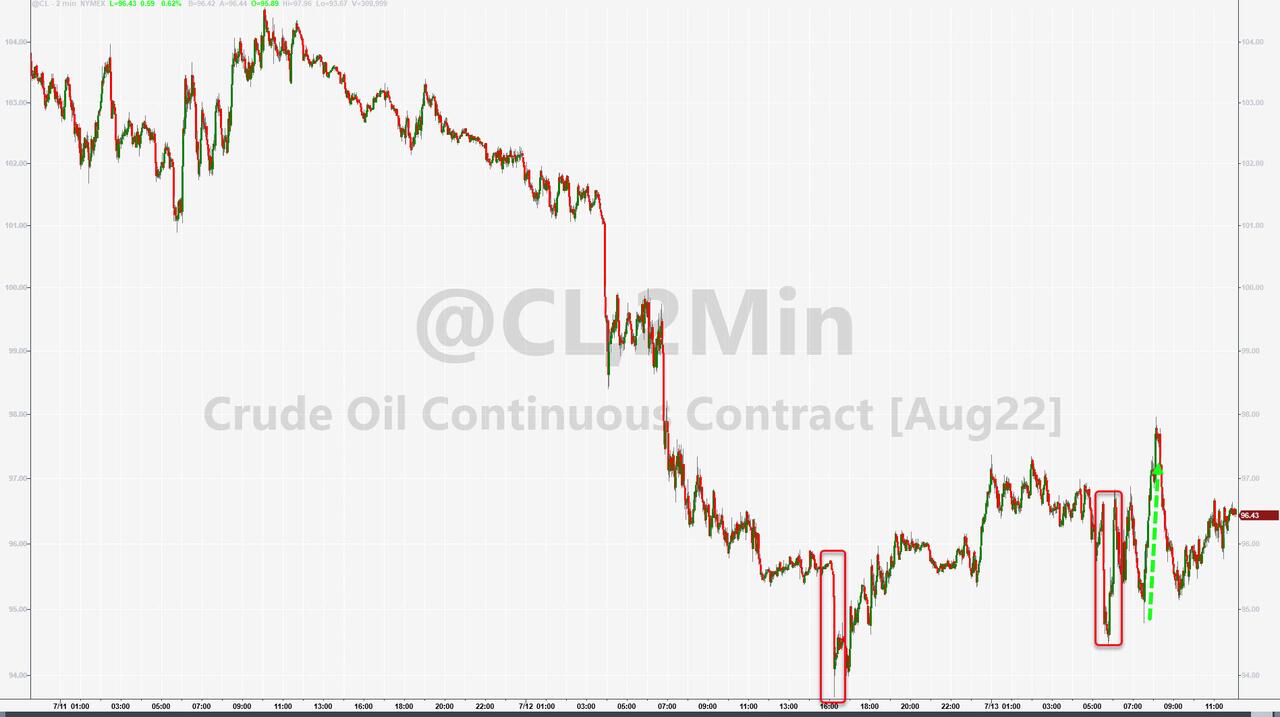

After yesterday’s last hour stock market puke prompted by a fake CPI “leak” that showed inflation rising more than double digits in June which sent spoos just over 3,800, US index futures advanced ahead of a report that will show inflation hitting a fresh four-decade high according to Bloomberg consensus which expects headline inflation to print 8.8%, ensuring another 75bps rate hike. Contracts on the S&P 500 rose 0.3% by 7:15 a.m. ET after the underlying gauge declined over the past three days. Nasdaq 100 futures were up 0.4% after the tech-heavy index shed 3% this week, reversing most of last week’s gains. The dollar dropped from a 2 year high, bitcoin rose but held below $20,000 and WTI crude oil stabilized at about $96 a barrel after a tumble.

Among notable pre-market movers, Twitter rose 1% after suing Elon Musk over his abandoned $44 billion takeover bid, accusing the billionaire of having buyer’s remorse after his fortune declined. Meanwhile, Atara Biotherapeutics tumbled 36% after the biotech firm gave an update on its multiple sclerosis therapy with Cowen strategists saying that the interim analysis of the ATA188 Phase 2 study was “inconclusive.” Here are other notable premarket movers:

- Stitch Fix (SFIX US) jumps 9.3% in premarket trading after J William Gurley, a board member and general partner at venture capital firm Benchmark, bought $5.43 million of shares in the company. Gurley’s purchase comes as the online personal-styling platform’s stock has fallen 73% this year.

- Atara Biotherapeutics (ATRA US) shares drop 41% in US premarket trading, after the biotech company gave an update on its multiple sclerosis therapy, with Cowen saying that the interim analysis of the Phase 2 study was “inconclusive” and Roth flagging potential “additional risks.”

- Humanigen (HGEN US) shares plummet as much as 76% in US premarket trading, after the biotech firm said that its Covid-19 drug trial didn’t achieve statistical significance on the primary endpoint, with Cantor Fitzgerald cutting its rating on Humanigen to neutral from overweight.

- Keep an eye on Apple (AAPL US) shares as Citi lowers its estimates for the company given cooling consumer spending trends amid macro woes and continued supply chain bottlenecks.

- Hannon Armstrong (HASI US) stocks could be active as analysts defended the climate-change investment firm after its shares slumped 19% on Tuesday. The losses followed a report from short seller Carson Block’s Muddy Waters Capital that criticized its accounting practices.

- Watch Alphabet (GOOGL US) stocks as Cowen trims 2022 Google Search and YouTube ad estimates, following checks that suggested that Search is seeing healthy demand but the business is decelerating, largely in line with expectations.

US inflation is projected to have continued to heat up in June, hitting a fresh pandemic peak. The consumer price index probably increased 8.8% from a year earlier, marking the largest jump since 1981, as discussed some banks expected a slightly softer print although others sees headline CPI rising as much as 9.0%. The consumer-price reading will be a major decisive factor for the Fed in its upcoming meeting as it decides how much further it should tighten policy to tame soaring inflation. Its hawkish policy already stoked fears the economy is heading for a recession this year.

“This is widely expected to be a really strong print,” Lauren Goodwin, economist and portfolio strategist at New York Life Investments, said on Bloomberg Television. “Even if it is not, I don’t think that changes the Fed’s perspective in a couple of weeks. We won’t have enough evidence that inflation is convincingly turning over.”

Meanwhile, the International Monetary Fund cut its growth projections for the US economy and warned that a broad-based surge in inflation poses “systemic risks” to both the country and the global economy.

Traders are also on tenterhooks for the latest corporate earnings getting underway this week and monitoring for a brewing energy crisis in Europe if Russia cuts off gas supplies in the fallout from its invasion of Ukraine. After today’s CPI, investor focus will turn to the start of the earnings season, which kicks off tomorrow with major Wall Street banks.

Meanwhile in Europe, the region’s benchmark Stoxx 600 Index fell 0.5% while the Euro Stoxx 50 slumped as much as 1.2% before roughly halving losses, amid deteriorating economic outlook. Shares of insurance companies and automakers led the drop.. FTSE 100 and FTSE MIB lag on the recovery. Autos, insurance and travel are the worst-performing sectors. Here are the biggest movers:

- Saipem shares tumble as much as 45%, extending Tuesday’s 49% slump, after only 70% of its EU2 billion rights offering was taken up by investors, signaling low confidence in the engineering company’s turnaround plan.

- Svenska Cellulosa falls as much as 4.1% and DS Smith declines 2.7% as Exane BNP downgrades its ratings on both, saying it anticipates a robust 2Q for packaging, but a correction in pulp prices.

- Bayer drops as much as 3% after a US appeals court reinstated a lawsuit by a Roundup herbicide user who claims the company failed to warn him of cancer risks.

- Galp Energia falls as much as 2.8% following its second-quarter production update, with analysts saying volumes were softer than anticipated.

- Vontobel declines as much as 6%, and EFG falls as much as 5.2% after Citi cut both to sell and kept a buy rating on Julius Baer, saying that it still sees good value in Swiss banks and prefers larger players to independents.

- Evonik falls as much as 3.9% after Barclays cut its rating to equal-weight, saying that it sees opportunities in Brenntag and Lanxess among European chemicals stocks.

- Orion gains as much as 7.9% after the pharmaceutical company raised its FY outlook after announcing it plans to work with MSD on developing and commercializing ODM-208, a drug for prostate cancer.

- Outokumpu gains as much as 6.5% after the stainless steel producer sold the majority of its Long Products business, a transaction which Jefferies and Morgan Stanley describe as positive.

- Hugo Boss rises as much as 3.1% as Jefferies says the company appears to be outperforming its luxury peers, and that expectations of continued growth, “comfortable” guidance and a successful rebrand are starting to move the market.

- Verallia gains as much as 3.3% after being initiated with a buy rating at Jefferies, which says the glass-packaging maker’s discount to peers is “unjustified.”

Earlier in the session, Asian stocks advanced, led by the region’s technology shares. The MSCI Asia Pacific Index gained as much as 0.6%, halting a two-day slide that dragged the benchmark to the lowest level in two years on Tuesday. Tech names such as TSMC, JD.com and Meituan contributed the most to the rally. Information technology was the region’s best-performing sector as the Hang Seng Tech Index bounced back after its recent drops sent the measure into a technical correction. Taiwan’s benchmark jumped nearly 3% as the government vowed to support the stock market for the first time since the early days of the pandemic. Equities posted moderate gains in South Korea and New Zealand after their central banks hiked interest rates by 50 basis points as expected. Thailand’s stock market was closed for a holiday. “Central bankers, policy makers all over the world are gonna have to pick their spots on how much inflation they’re prepared to tolerate versus how much a growth downdraft they wanna create,” Ben Powell, chief APAC investment strategist at BlackRock Investment Institute, said in a Bloomberg TV interview. In addition to today’s data on consumer prices to assess what the Federal Reserve will do next, traders are also monitoring corporate earnings results in Asia for signs of any impact from China’s lockdowns during the second quarter.

Japanese stocks advanced as investors await US data that may show inflation hit a fresh four-decade high. The Topix index rose 0.3% to 1,888.85 at the 3pm close in Tokyo, while the Nikkei 225 advanced 0.5% to 26,478.77. Recruit Holdings Co. contributed the most to the Topix’s gain, increasing 2.9%. Out of 2,170 shares in the index, 1,400 rose and 633 fell, while 137 were unchanged. “Japanese stocks will have a hard time finding a sense of direction before the US CPI announcement,” said Mitsushige Akino a senior executive officer at Ichiyoshi Asset Management.

In FX, the Bloomberg Dollar Spot Index held near its highest level in more than two years and the greenback traded mixed against its Group-of-10 peers as traders awaited US inflation data later on Wednesday for clues on the Federal Reserve’s rate trajectory. JPY and SEK are the weakest performers in G-10 FX, CHF and AUD outperform. EUR/USD stalls again, declining 6 pips shy of parity before recovering slightly. Money markets raised bets on the pace of BOE rate hikes after the UK economy grew faster than the median estimate in May to ease fears of a recession. UK GDP rose by a surprisingly robust 0.5% amid a surge in visits to doctors and holiday bookings, after an 0.2% decline in April, a figure that was revised higher. New Zealand’s dollar initially fell and then erased losses after the central bank raised interest rates by 50 basis points as economists forecast. The yen underperformed all its Group-of-10 peers amid expectations US CPI will be strong enough to keep wagers high for a continued aggressive rate-hike cycle by the Federal Reserve. Super-long sectors led drop in government bond yields after purchases by the Bank of Japan.

In rates, the 10-year Treasury yield was little changed at 2.97% after falling two basis points on Tuesday. Cash TSYs are comparatively quiet ahead of today’s CPI release. German and UK curves bear-flatten, underperforming Treasuries. Peripheral spreads widen to Germany with 10y BTP/Bund back near 200bps. Gilts and Bunds fell, underperforming Treasuries. Money markets raised bets on the pace of BOE rate hikes after the UK economy grew faster than the median estimate in May to ease fears of a recession.

In commodities, crude futures advance. WTI drifts 1.1% higher to trade near $96.90. Most base metals trade in the green; LME lead rises 1.1%, outperforming peers. LME zinc lags, dropping 0.2%. Spot gold is little changed at $1,726/oz

To the day ahead now, and data releases include the US CPI release for June, as well as UK monthly GDP for May and Euro Area industrial production for May. Otherwise from central banks, the Bank of Canada will be making their latest policy decision, and the Federal Reserve will release their Beige Book.

Market Snapshot

- S&P 500 futures up 0.2% to 3,830.50

- STOXX Europe 600 down 0.8% to 413.52

- MXAP up 0.3% to 155.40

- MXAPJ up 0.5% to 511.37

- Nikkei up 0.5% to 26,478.77

- Topix up 0.3% to 1,888.85

- Hang Seng Index down 0.2% to 20,797.95

- Shanghai Composite little changed at 3,284.29

- Sensex down 0.5% to 53,636.37

- Australia S&P/ASX 200 up 0.2% to 6,621.56

- Kospi up 0.5% to 2,328.61

- German 10Y yield little changed at 1.16%

- Euro little changed at $1.0038

- Brent Futures up 1.1% to $100.63/bbl

- Gold spot up 0.0% to $1,726.85

- U.S. Dollar Index little changed at 108.15

Top Overnight News from Bloomberg

- The planned reopening of a key Russian gas pipeline next week may be a bigger deal for the euro than the first interest-rate hike in a decade by the ECB. Both are set for July 21. While the ECB’s plans to start lifting rates have been well flagged and hence priced in by markets, there’s more doubt over whether Russia will actually restore gas flows to Europe after maintenance on the Nord Stream 1 pipeline is completed

- China will take advantage of the market-based adjustment mechanism of deposit rates and guide financial institutions to transmit the effect of falling deposit rates to their borrowers as part of efforts to lower real lending rates, Zou Lan, head of PBOC’s monetary policy department, says at a briefing

- The ECB is watching the euro-dollar exchange rate as recent lows can further stoke already record inflation, according to Governing Council member Francois Villeroy De Galhau

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mostly positive as the region shrugged off the weak lead from Wall St but with upside capped amid central bank rate hikes and ahead of upcoming key risk events including Chinese trade and US CPI data. ASX 200 traded indecisively as strength in tech was offset by losses in energy after the recent slump in oil prices. Nikkei 225 was underpinned by a weaker currency but with gains limited after a ramp-up in Tokyo COVID cases. Hang Seng and Shanghai Comp. gained but with the mainland choppy ahead of Chinese trade data, while Hong Kong tech stocks were bolstered after China approved 67 domestic games in July.

Top Asian News

- China’s Customs said foreign trade is expected to achieve stable growth and that trade growth in May and June reversed the declining trend, but noted that foreign trade faces instabilities and uncertain factors, according to Reuters.

- “Lanzhou in NW China’s Gansu Province has sealed off its 4 districts for 7 days to curb the latest COVID19 flare-up which started from last Friday and has led to 143 infections as of 10 am on Wed”, according to Global Times.

European bourses are pressured and towards the mid-point of the morning’s parameters as we await US inflation data, Euro Stoxx 50 -0.6%. Sectors, are predominently in the red with defensively-inclined names lagging though Energy outperforms and is green amid benchmark action. Stateside, futures are modestly firmer but have been choppy with pre-CPI positioning underway; ES +0.2%. Alphabet (GOOGL) said, on July 12th, that due to the hiring progress already attained, will slow the hiring process for remainder of year, via Reuters; like all Cos, not immune to economic headwinds. Kroger (KR) is launching an annual membership, provides unlimited free deliveries on orders over USD 35 and fuel discounts of up-to USD 1/gallon alongside other savings.

Top European News

- UK lawmakers are to push ahead with legislation to tear up the post-Brexit trade deal today, according to FT.

- Network Rail offered workers at two unions pay hikes in a bid to avert further crippling strikes, according to FT.

- Italy’s Salvini says the League Party is not willing to remain in the government if the 5-Star Party quits, adding that if 5-Star does not back a Thursday confidence vote, Italy should call snap elections. Subsequently, Democratic Party is unwilling to form new governments without the 5-Star Party, according to a party source cited by Reuters.

Geopolitical

- China’s military said it monitored and drove away a US destroyer which entered the South China Sea Paracel Islands, while it added that the actions of the US military seriously violated China’s sovereignty and security. Furthermore, the US military stated that USS Benfold asserted navigational rights and freedoms near the Paracel Islands consistent with international law, according to Reuters.

- US Navy says the Ronald Reagan Carrier Strike Group is operating in the South China Sea.

- Venezuela detained at least three Americans earlier this year accused of attempting to enter the country illegally, according to sources cited by Reuters.

- Iran Foreign Ministry spokesperson says results of the negotiations with Saudi Arabia have been promising, sides have an interest to continue talks. Subsequently, Iran President Raisi says it will not retreat from its ‘rightful’ stance in talks to revive the 2015 JCPOA, state TV reported.

Central Banks

- RBNZ hiked the OCR by 50bps to 2.50%, as expected, and said it remains appropriate to continue to tighten policy, while it will tighten conditions at a pace to maintain price stability and support maximum sustainable employment. RBNZ added the Committee is resolute in its commitment to ensuring price inflation returns to the 1%-3% target range and it agreed to lift the OCR to a level where it is confident consumer price inflation will settle within the target range but added that once aggregate supply and demand are more balanced, the OCR can return to a lower and more neutral level. Furthermore, the Committee agreed to maintain the approach of briskly lifting the OCR and remained comfortable with the projected path of the OCR it outlined in May, as well as noted that there are near-term upside risks to consumer prices and also medium-term downside risks to economic activity.

- BoK raised its Base Rate by 50bps to 2.25%, as expected, with the decision made unanimously. BoK stated that South Korea’s 2022 growth will moderate further from an earlier projection and inflation will remain high for some time, as well as noted that inflation will surpass the May forecast for the entire of 2022 and that core inflation is to be higher than 4% for a considerable period. Furthermore, BoK Governor Rhee said more policy tightening of 25bps looks appropriate going forward should current inflation continue for the time being and that it is reasonable to expect rates at 2.75%-3.00% by year-end.

- ECB’s Villeroy says it is not the EUR that is weak but the USD that is strong.

FX

- Greenback grinds higher ahead of US inflation data, but remains restrained, DXY back above 108.000 within 108.020-390 range.

- Aussie regroups alongside base metals and awaits labour report for further impetus; AUD/USD approaching 0.6800 vs sub-0.6750 low.

- Franc forges safe-haven gains vs Dollar and Euro, USD/CHF below 0.9800 and EUR/CHF under 0.9850.

- Kiwi somewhat deflated after RBNZ maintained half-point tightening pace, guidance and OCR path, NZD/USD capped into 0.6150.

- Sterling underpinned by above-forecast UK data and remarks from BoE Governor Bailey leaning towards bigger than 25bp hike, Cable straddling 1.1900 and EUR/GBP pivoting 100 and 200 DMAs.

- Loonie looking for a BoC boost via 75bp rate increase and hawkish guidance, USD/CAD towards the low end of 1.3050-00 band with 1.57bln option expiries rolling off at the round number.

- Yen undermined by firmer US Treasury yields pre-CPI and post-weak 10-year note the auction, USD/JPY rebounds through 137.00 again.

- Yuan pares some losses after China’s trade surplus tops consensus and PBoC pledges to up support for real economy; USD/CNH and USD/CNY testing bids and support on either side of 6.7200.

Fixed Income

- Debt fades from early EU highs irrespective of risk-off sentiment as clock ticks down to key US CPI data.

- Bunds pull up just ahead of 153.00, Gilts into 116.00 and T-note shy of 119-00.

- Italian and German supply relatively well received, but impending long bond refunding comes hot on the heels of tepid demand for 10 year issuance.

Commodities

- Crude benchmarks are bid after a concerted pick-up in the European morning that occurred without any obvious fresh fundamental driver.

- US Private Inventory Data (bbls): Crude +4.7mln (exp. -0.2mln), Gasoline +2.9mln (exp. -0.4mln), Distillates +3.2mln (exp. +1.6mln), Cushing +0.3mln.

- Libya’s Government of National Unity decided to replace the NOC chairman and board, according to a government source. NOC later announced the lifting of the force majeure on exports from the Brega and Zueitina oil terminals, while it added that negotiations were conducted to allow exports from Es Sider port and resume output at the Al Waha and Mellita fields, according to Reuters.

- Eni (ENI IM) Chair says Italy will be able to replace 50% of Russian gas flows with other sources this winter, and 80% next winter, via Reuters citing a paper.

- Hungary Foreign Minister says it could purchase up to 700 MCM of gas on the market ahead of the heating season, in addition to long-term supply deal with Russia.

- IEA OMR: 2023 demand 101.3mln BPD, +2.1mln BPD; led by strong growth in non-OECD countries. 2022 demand cut by 200k BPD, seeing a rise of 1.7mln to 99.2mln BPD

- Spot gold is modestly firmer managing to capitalise on the session’s bout of USD easing, LME Copper has benefited from the generally constructive APAC tone though participants will remain cognisant of and cautious around the China-COVID situation.

US Event Calendar

- 07:00: July MBA Mortgage Applications -1.7%, prior -5.4%

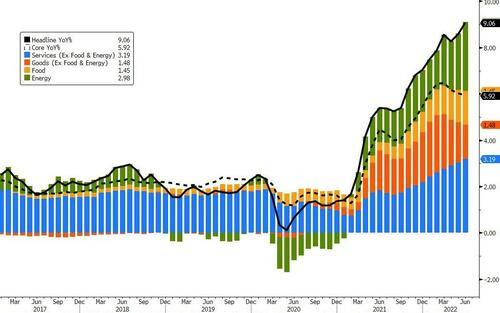

- 08:30: June CPI YoY, est. 8.8%, prior 8.6%; MoM, est. 1.1%, prior 1.0%

- 08:30: June CPI Ex Food and Energy YoY, est. 5.7%, prior 6.0%; MoM, est. 0.5%, prior 0.6%

- 08:30: June Real Avg Hourly Earning YoY, prior -3.0%, revised -2.9%

- 08:30: June Real Avg Weekly Earnings YoY, prior -3.9%, revised -4.0%

- 14:00: U.S. Federal Reserve Releases Beige Book

- 14:00: June Monthly Budget Statement, est. -$75b, prior -$174.2b

DB’s Jim Reid concludes the overnight wrap

I’m supposed to be off for the next three days with the family but given how busy things are I’m delaying two of the days until August. However I can’t escape a Theme Park outing tomorrow so I’m still doing that. I hate Theme Parks and rollercoasters with a passion. Readers might remember the last time I went I had an argument with someone who pushed in with his whole family in the queue ahead of me. I was most disgruntled at the end of a long day and vowed never to return. However my kids love them. If it were up to me my preferences would dominate and we wouldn’t go but unfortunately my selfless wife puts our kids first. Probably a good thing!!

I’ll be here now for the all important US CPI today but I’ll miss the ceremonial start of earnings season tomorrow with this week seeing a small selection of major US financials and consumer packaged goods companies reporting. My colleague Binky has just released his full preview, available here. He expects earnings to beat in the low single digits percentage region, below the long-run historical average of 5%. Earnings are likely to be 3.1% qoq along with downward revisions to forward estimates. Heading into earnings season, estimates have been revised lower for every sector but energy, which has experienced upgrades. Using a bottom-up approach, yoy EPS growth will come in at 5.7%.

Heading into CPI and earnings, after markets had climbed a wall of worry since mid-June, they seem to be losing a bit of footing again over the last few days as fears of a recession dominate again, alongside fears of aggressive rate hikes by central banks, rising Covid cases in China and the prospect of Russia cutting off Europe’s gas. This gloomy backdrop saw the S&P 500 (-0.92%) lose ground for a 3rd day running, whilst those fears of weakening demand sent Brent crude oil prices back beneath $100/bbl and also led to day two of a new fresh sizeable rally in sovereign bonds. Oil is little changed in Asia trade with Brent and WTI futures almost flat at $99.76/bbl and $95.99/bbl respectively as we go to press.

However, today’s main focus will almost certainly be on the US CPI release for June, which will set the stage for the Fed’s next decision in just two weeks’ time. Remember that it was last month’s much stronger-than-expected report that sparked a tumultuous market reaction that culminated in the Fed moving by 75bps at a single meeting for the first time since 1994, having previously only signalled a 50bps move. So any further surprises today could have a big impact. In terms of what to expect, our US economists are looking for an above-consensus monthly reading for both headline CPI (+1.3%) and core CPI (+0.6%), which in turn would take the year-on-year headline CPI up to its highest level since 1981, at +9.0%.

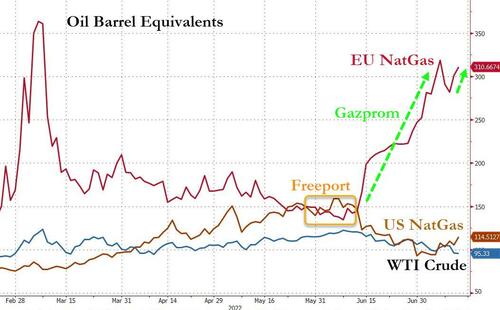

Although we’re expecting another strong inflation print today, ahead of that release there were actually growing signs of respite on the inflation front thanks to further losses amongst a number of key commodities. Brent Crude (-7.11%) and WTI (-7.93%) oil prices saw substantial losses, copper prices (-4.10%) hit a 19-month low and gold (-0.46%) hit a 9-month low. Indeed, the only major exception to that pattern was the usual suspect of European natural gas (+4.92%) which just about reversed the previous day’s decline following cuts to Norwegian capacity. Our research colleagues in Frankfurt published a detailed note yesterday on the gas supply issue (link here), where they run through 3 scenarios of how things might evolve, including what happens if Russia completely turns off the gas taps to Germany after the maintenance period that would involve gas being rationed during the winter months.

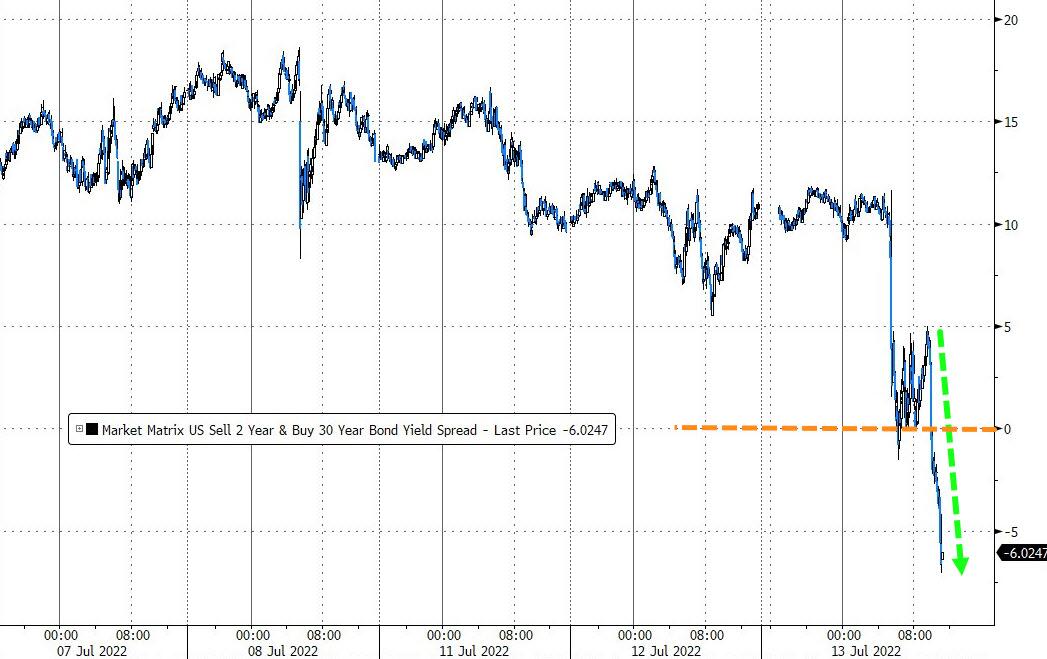

Although many will welcome the decline in those commodities mentioned above, the bad news is that the reason they’re declining is because of recession fears, and yesterday saw a number of additional recessionary indicators flash with growing alarm. One in particular is the 2s10s curve, which has inverted before every one of the last 10 US recessions, and remains near its most inverted of this cycle so far at -8.5bps after dipping below -12bps intraday. We would stress that while we are the yield curve’s biggest fan, it usually takes a minimum of three quarters from inversion to recession so we still think it may take a bit of time from the first inversion in March to confirm the almost inevitable recession.

For the 1s10s and the 2s5s curve, it was much the same story of being the most inverted so far this cycle, and the 3m10s curve reached its flattest since November 2020. And whilst the Fed have told us to focus on their preferred near-term forward spread (18m3m minus 3m), even that closed beneath 100bps for the first time so far this year at 94bps (from a peak of 270bps in early April), so these measures are all trending in the wrong direction from a recessionary standpoint.

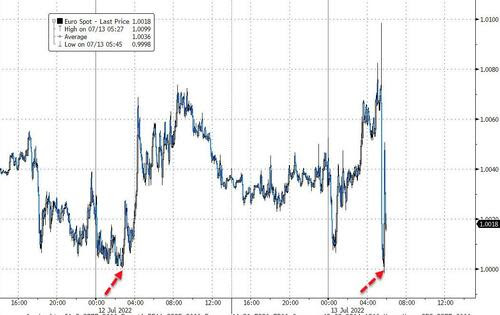

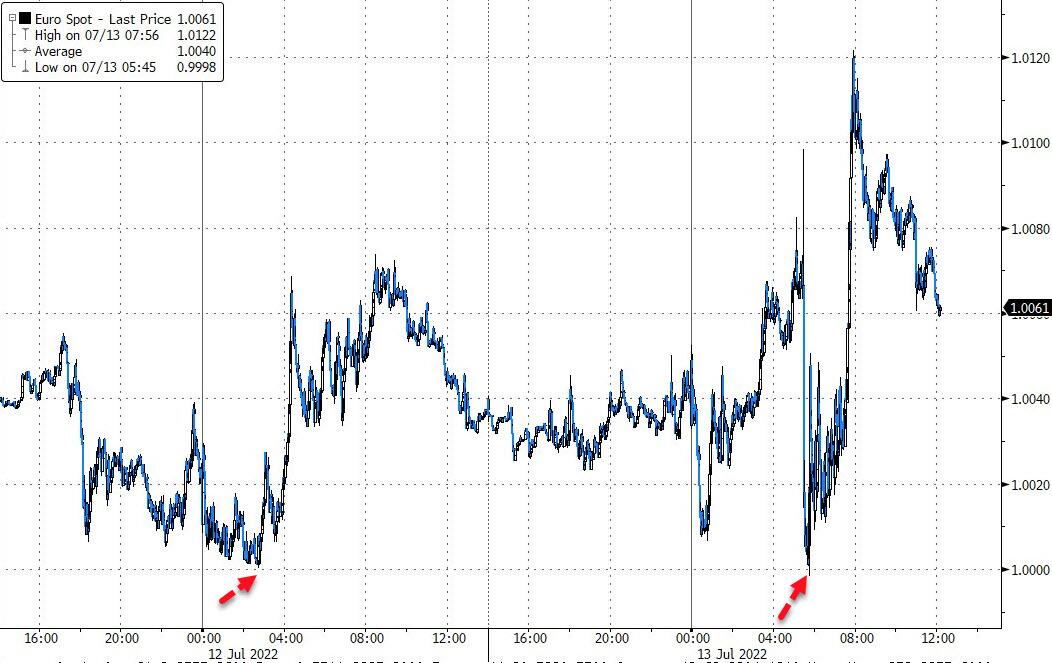

In terms of the absolute yield moves, the risk-off tone saw them move lower on both sides of the Atlantic. 10yr Treasury yields fell -2.4bps to 2.97% albeit having being as much as -9.6bps lower intraday. There was a discrete bounce in longer-dated Treasury yields following the 2bp tail in the 10yr auction. Yields are fairly stable in Asian trading. Meanwhile in Europe, those on 10yr bunds (-11.3bps), OATs (-12.8bps) and BTPs (-9.8bps) all fell back too, as concerns about the economic situation led investors to price in a less aggressive pace of monetary tightening over the coming months, particularly from the ECB. That also meant that the Euro itself moved ever closer to parity against the US Dollar yesterday, and you had to look to 5 decimal places to see that it just avoided that milestone, with an intraday low of $1.00003 during the European morning, ending the day just a hair lower versus the dollar, down -0.03% at $1.0037.

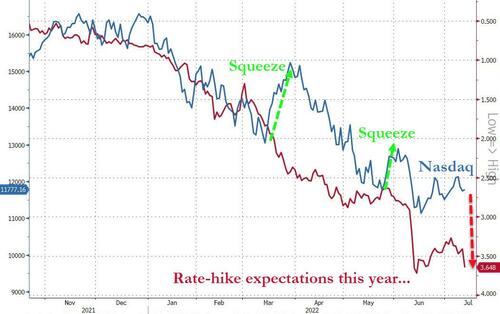

European equities staged a modest comeback from Monday’s selloff, while US equities ended lower after flirting with gains all day. The STOXX 600 gained +0.49%, with the DAX performing a touch better at +0.57%, bringing the STOXX 600 to just under flat for the week, while the DAX is still -0.84% lower on the week. The S&P 500 fell -0.92%, after trading near unchanged most of the day. Theories abounded for the late turnaround. Underlying market technicals pointed to potential algorithmic selling programs, whilst rumours spread in some circles that the CPI report was leaked and revealed a +10% print. Officials disabused us of the latter, but it nevertheless speaks to the heightened anxiety markets are trading with around inflationary data. In terms of the breakdown, energy shares (-2.03%) were the clear underperformer, but a wide-breadth of shares took a dip lower in the afternoon, sending the NASDAQ (-0.95%), FANG+ (-1.01%), and Russell 2000 (-0.22%) all lower on the day. So no clear macro driver for equities yesterday, but again, today’s CPI will be instructive about the near-term path.

Overnight in Asia equity markets are trading higher after recent losses. As I type, the Hang Seng (+0.81%) is leading gains across the region with the Kospi (+0.71%), Shanghai Composite (+0.36%), CSI (+0.26%), and the Nikkei (+0.33%) all trading up. Looking ahead, equity futures in the US point to a steady start with contracts on the S&P 500 (+0.14%) and NASDAQ 100 (+0.21%) moving higher.

Moving on to monetary policy action, the Bank of Korea (BOK) increased rates by 50bps, bringing the benchmark rate to 2.25% in order to help pullback inflation from a 24-yr high of 6%. The unprecedented rate hike size comes even as the central bank forecasts the country’s growth rate to lag “below the May forecast of 2.7%. Elsewhere, the Reserve Bank of New Zealand (RBNZ) in an expected move also increased its official cash rate (OCR) by 50bps for a third straight meeting to 2.5%.

Staying in Asia, another risk that’s been in a few headlines again is Covid. Partly this is because of the ongoing situation in China, where a steady stream of cases have been reported over recent days. But in addition to that, the US is considering whether to expand the recommendation of the second booster to all adults in light of the BA.5 omicron variant’s spread, and White House coronavirus coordinator Ashish Jha said that these discussions “have been going on for a while”. Of particular concern to officials, the BA.5 seems to evade immunity provided from prior infections.

Here in the UK, it’ll be another eventful day on the political scene as the first ballot of MPs takes place in the Conservative leadership election, which will also decide the next Prime Minister. 8 candidates will be on today’s ballot, and former Chancellor of the Exchequer Rishi Sunak is currently leading when it comes to MP’s endorsements, with yesterday seeing him gain that of Deputy PM Dominic Raab, among others. Candidates will need the support of at least 30 MPs today to progress onto the next ballot that takes place tomorrow.

There wasn’t much data yesterday, but the releases we did get only added to negative sentiment. First the German ZEW survey saw the expectations reading fall to its lowest level since the sovereign debt crisis at -53.8 (vs. -40.5 expected), whilst the current situation reading fell to -45.8 (vs. -34.5 expected). Separately, the NFIB’s small business optimism index from the US fell to 89.5 (vs. 92.5 expected).

To the day ahead now, and data releases include the US CPI release for June, as well as UK monthly GDP for May and Euro Area industrial production for May. Otherwise from central banks, the Bank of Canada will be making their latest policy decision, and the Federal Reserve will release their Beige Book.

WEDNESDAY /TUESDAY NIGHT

SHANGHAI CLOSED UP 2.83 PTS OR 0.09% //Hang Sang CLOSED DOWN 46.79 OR 0.22% /The Nikkei closed UP 142.11 OR % 0.54. //Australia’s all ordinaires CLOSED UP 0.31% /Chinese yuan (ONSHORE) closed DOWN 6.7267 /Oil DOWN TO 96.48 dollars per barrel for WTI and DOWN TO 99.84 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7274 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7281: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

3 a./NORTH KOREA/ SOUTH KOREA/

///NORTH KOREA/SOUTH KOREA/

3B JAPAN

3c CHINA

CHINA

That did not take long: China scraps firs first COVID vaccine mandate in just 48 hrs after a furious social response

(zerohedge)

Beijing Scraps China’s First COVID Vaccine Mandate In Just 48 Hours After Furious Social Response

TUESDAY, JUL 12, 2022 – 10:05 PM

On paper, the US is the land of the free and home of the brave, while China is a tyrannical, authoritarian state where individuals have no rights and where the political oligarchy always gets its way. In reality, it’s usually the opposite, especially when the people remember they are not snowflakes.

With much the US and Europe bitching and moaning but ultimately acquiescing to every incremental round of mandatory experimental mRNA-based covid vaccines (we are not even talking about those mentally unstable they/thems who demand the government strip them of their last freedom and who will be wearing a mask in their grave to signal not only their profound virtue but their willingness to lap up any amount of fecal matter shoveled by the government), a few million non-snowflake Chinese showed how it can be done.

As Bloomberg reports, last week, Beijing’s city leadership rolled out China’s first Covid-19 vaccine mandate last week. The policy made boosters mandatory for some professions, while entry to busy public venues like movie theaters and gyms was restricted to the vaccinated. Unlike Europe and the US where such mandates are now a way of life as the population is too terrified to oppose the state, in Beijing the public reacted far less snowflakily, with many residents turning to social media to declare the mandate an illegal usurpation of their rights. Beijing’s response was just as quick: Less than 48 hours after announcing the policy, the city government rescinded it.

Instead, people will be able to enter all public venues if they can simply provide a negative Covid test result that’s no older than 72 hours and have their temperature checked, an unidentified official said in an interview with state-backed Beijing Daily that was published late Thursday night. The city will continue to promote vaccination on a voluntary, informed and consent basis, the official said, something which just one year ago would have sounded like an alien world of utopian liberty to American citizens.

The policy, announced Wednesday and intended to come into effect on July 11, would have limited entry to public venues such as cinemas, museums, and theaters to only vaccinated people, and required workers in certain professions to get booster shots.

“The reversal shows the power of public opinions,” Hu Xijin, former editor-in-chief at the Communist Party-backed Global Times and an influential commentator, said on his official Weibo account. “The Chinese society is dominated by government. They timely backed up in the face of a public pushback. That means they accept the public’s view of the vaccine mandate as illegal.”A health worker takes a swab sample at a swab collection site in Beijing on July 7. Photographer: Noel Celis/AFP/Getty Images

As Bloomberg’s Adam Minter writes, while China’s authoritarians rarely back down because of public opposition, by doing so in this case, Beijing’s authorities offered a reminder of how carefully they monitor public opinion and struggle to manage it. Indeed, it’s also a reminder that at the end of the day, it’s the people who hold the power, no matter how diligently the propaganda press will try to convince the people otherwise, and no matter how armed to the teeth the state’s enforcement powers may be.

By folding to public pressure, Bloomberg notes that Beijing “inadvertently revealed that their ability to control and channel public anger isn’t absolute.” The media giant then adds that “like their counterparts in democratic countries, China’s leaders must account for populist anger. And at a time of surging Chinese nationalism, those populist currents can have damaging consequences for peace and stability in Asia and the world.”

Which is hilarious because whereas “dictatorial” China reversed on vaccine mandates in just 2 days, “democratic counterparts” can impose any amount of health experiments on the population at will and largely without objections.

And while “Democratic” nations, especially those run (for now) by so-called “Democrats” have become completely oblivious to public opinion – especially if it opposes their ruthless, authoritarian ambitions – it is the authoritarian states that actually do care: as Bloomberg notes, the internet — and especially social media — complicated both tasks, requiring huge investments in human and machine monitoring and content-generation. In 2014, the Communist Party-owned Beijing News reported that public and private Chinese entities employ more than 2 million public opinion “analysts.” Among other roles, they “collect the opinions and attitudes of netizens, organize them into reports, and submit them to decision makers.” These days, even relatively minor agencies — such as the Beijing International Horticultural Expo Coordination Bureau — purchase public opinion analysis.

Finally, as Goldman’s Rich Provorotsky writes in his morning note today, “although unlikely to change abruptly, something to watch if population’s frustration leads to a change in zero covid policy?” That assumption may soon be tested, while Beijing scrapped mandatory vaccines, Shanghai may be facing another round of lockdowns: here’s Bloomberg.

Tension is spreading through Shanghai as residents watch the Covid-19 caseload tick higher, fueling fears they’re headed back into lockdown little more than five weeks after exiting a bruising two-month ordeal.

The city reported 59 new infections for Monday, the fourth day in a row case numbers have held above 50. The sharp rise from single digits about a week ago follows the detection of the more contagious BA.5 sub-strain of the omicron variant, which has triggered two additional rounds of mass testing between Tuesday and Thursday this week across nine of the financial hub’s 16 districts, as well as other areas where cases have been found.

Bottom line: China’s strict Covid Zero approach is “once again being tested as outbreaks flare across the country amid the arrival of a sub-variant that has fueled rising caseloads elsewhere” only this time the public may be sensing that opposition to the highly unpopular government response to the Wu-flu is beyond the required tipping point and following in the footsteps of Beijing, tens of millions of Shanghai residents may soon take matters into their own hands/

end

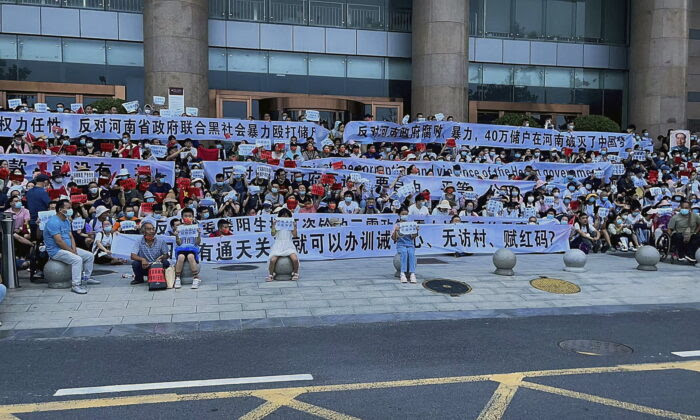

Outrage After Henan Protestors Violently Removed From Outside Bank

Inbox

| Robert Hryniak | 9:18 AM (3 minutes ago) | ||

| to |

Government does not care about people. This is a reality. Change is badly needed and in this hour of need moral authority to lead id sadly lacking as none are fit for the calling. The coming chaos will invent the changes needed more by chance that designed control. History is never linear in progression

Outrage After Henan Protestors Violently Removed From Outside Bank

A large number of Chinese bank customers protesting over frozen deposits were attacked by security forces in plainclothes in the capital of China’s central Henan Province on Sunday. It’s one of the biggest protests being suppressed in recent years.

Photos and videos of the violence that the depositors suffered have spread quickly on Chinese social media, sparking public outrage.

Since April, the funds of four rural banks in Henan and two in Anhui have been frozen by the state, resulting in about 400,000 depositors being unable to withdraw money online, involving 40 billion yuan (US$5.95 billion) in deposits. The bank customers have showed up in person in front of the banks to demand their money.

A smaller protest in May was also crushed by police. In that case, Henan authorities used a health code for preventing the spread of COVID-19 to restrict the depositors’ travel and gathering.

On Sunday, about 2,000–3,000 depositors were peacefully demonstrating in front of Zhengzhou branch of the People’s Bank of China. Many were holding banners and chanting, “Henan Bank, return my deposit!”

Along with their demands, the protestors also voiced their opposition to “the violent treatment of depositors by Henan police … the beating of depositors by the Henan provincial government in collusion with the local gangs”

MOST READ

The protestors further demanded “serious investigations into the officials who are responsible for turning the depositors’ health code red in Henan”, and the depositors also named the provincial Chinese Communist Party committee member Lou Yangsheng over the red health code incident.

Brutal Suppression

Around noon on Sunday, groups of people in plainclothes—dressed in white and black—violently dragged and beat many of the depositors up, forcefully putting them in buses with uniformed police inside sending them to multiple locations for detention.