by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1712.20 UP $7.55

SILVER: $18.92 up 25 CENTS

ACCESS MARKET:

GOLD $1709.05

SILVER: $18.70

Bitcoin morning price: $22,041 UP 1064

Bitcoin: afternoon price: $21,783. UP 806

Platinum price: closing UP $25.30 to $872.10

Palladium price; closing UP $20.45 at $1870.65

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JULY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,702.400000000 USD

INTENT DATE: 07/15/2022 DELIVERY DATE: 07/19/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 100

167 C MAREX 361

323 H HSBC 5

365 H ED&F MAN CAPITA 4

435 H SCOTIA CAPITAL 282

661 C JP MORGAN 90 119

800 C MAREX SPEC 9

TOTAL: 485 485

MONTH TO DATE: 6,922

no. of contracts issued by JPMorgan: 119/485

_____________________________________________________________________________________

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT 485 NOTICE(S) FOR 48,500 Oz//1/5085 TONNES)

total notices so far: 6922 contracts for 692,200 oz (21.530 tonnes)

SILVER NOTICES:

76 NOTICE(S) FILED 380,000 OZ/

total number of notices filed so far this month 3138 : for 15,690,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $7.55

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD///

INVENTORY RESTS AT 1014.28 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 25 CENTS

AT THE SLV// ://BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 4.995 OZ FROM THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 515.838 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 2395 CONTRACTS TO 146,693 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE LOSS IN OI WAS ACCOMPLISHED DESPITE OUR $0.31 GAIN IN SILVER PRICING AT THE COMEX ON FRIDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.31) BUT WERE SUCCESSFUL IN KNOCKING OFF SOME COMMERCIAL SILVER LONGS//BUT MAINLY WE HAD ADDITIONAL SPECULATOR ADDITIONS AS WE HAD A STRONG LOSS OF 2055 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A VERY STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A POOR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.220 MILLION OZ FOLLOWED BY TODAY’S 245,000 OZ QUEUE JUMP / // V) HUGE SIZED COMEX OI LOSS

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : +60

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTACTS for 11 days, total 10,911 contracts: 54.555 million oz OR 4.959 MILLION OZ PER DAY. (991 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 54.555 MILLION OZ

.

LAST 15 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 54.555 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2495 DESPITE OUR $0.31 GAIN IN SILVER PRICING AT THE COMEX// FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE CONTRACTS: 430 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A POOR INITIAL SILVER OZ STANDING FOR JUNE. OF 15.22 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 245,000 OZ // .. WE HAD A HUGE SIZED LOSS OF 2025 OI CONTRACTS ON THE TWO EXCHANGES FOR 10.125 MILLION OZ DESPITE THE GAIN IN PRICE..

WE HAD 76 NOTICES FILED TODAY FOR 380,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 6,241 CONTRACTS TO 546,081 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: + 182 CONTRACTS.

.

THE STRONG SIZED DECREASE IN COMEX OI CAME WITH OUR FALL IN PRICE OF $3.75//COMEX GOLD TRADING/FRIDAY / WE MUST HAVE HAD ADDITIONAL SPECULATOR SHORT ADDITION ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD SOME LONG LIQUIDATION //AND SOME SPECULATOR SHORT ADDITIONS

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JULY AT 2.914 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 69,400 OZ

YET ALL OF..THIS HAPPENED WITH OUR FALL IN PRICE OF $3.75 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A FAIR SIZED LOSS OF 3108 OI CONTRACTS 9/645 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2958 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 546,081

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3108 CONTRACTS WITH 6049 CONTRACTS DECREASED AT THE COMEX AND 2958 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 3108 CONTRACTS OR 9/645 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2958) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (6,049,): TOTAL LOSS IN THE TWO EXCHANGES 3,108 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JULY. AT 2.914 TONNES FOLLOWED BY TODAY’S 69,400 OZ QUEUE JUMP 3) SOME LONG LIQUIDATION//CONSIDERABLE SPECULATOR SHORT ADDITIONS/ //.,4) STRONG SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

61,075 CONTRACTS OR 6,107,500 OZ OR 189.96 TONNES 11 TRADING DAY(S) AND THUS AVERAGING: 5552 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAY(S) IN TONNES: 189.96 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 189.96/3550 x 100% TONNES 5.35% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 189.96 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JULY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A HUGE SIZED 2395 CONTRACT OI TO 146,633 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 430 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 430 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE:430 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2395 CONTRACTS AND ADD TO THE 430 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED LOSS OF 1965 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 9.825 MILLION OZ

OCCURRED DESPITE OUR RISE IN PRICE OF $0.31

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)MONDAY MORNING// SUNDAY NIGHT

SHANGHAI CLOSED UP 50.04 PTS OR 1.55% //Hang Sang CLOSED UP 548.46 OR 2.70% /The Nikkei closed UP 145.08 OR % 0.54. //Australia’s all ordinaires CLOSED UP 1/32% /Chinese yuan (ONSHORE) closed UP AT 6.7443 /Oil UP TO 99.81 dollars per barrel for WTI and DOWN TO 103.72 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7443 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7501: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 6,049 CONTRACTS TO 546,081 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS STRONG COMEX DECREASE OCCURRED WITH OUR FALL OF $3.75 IN GOLD PRICING FRIDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2958 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2958 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :2958 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2958 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED SIZED TOTAL OF 3,108 CONTRACTS IN THAT 2958 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI GAIN OF 6,049 CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR FALL IN PRICE OF GOLD $3.75.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING JULY (22.709),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 22.709 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $3.75) AND WERE SUCCESSFUL IN KNOCKING OFF A FEW SPECULATOR LONGS/COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS//// WE HAVE REGISTERED A FAIR SIZED LOSS OF 9.645 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR JULY (22.709 TONNES)…

WE HAD -XX CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 3,108 CONTRACTS OR 310,800 OZ OR 9.645 TONNES

Estimated gold volume 170,366/// poor/

final gold volumes/yesterday 204,724 / poor

INITIAL STANDINGS FOR JULY ’22 COMEX GOLD //JULY 18

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 1736.15 oz Manfra brinks 24 kilobars and 30 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 485 notice(s) 48,500 OZ 1.5085 TONNES |

| No of oz to be served (notices) | 377 contracts 37,700 oz 1.1726 TONNES |

| Total monthly oz gold served (contracts) so far this month | 6922 notices 692,200 OZ 21.830 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

2 customer withdrawals:

i)Out of Brinks 771.620 oz (Brinks)

ii)Out of Manfra: 964.730 oz (Manfra)

total withdrawal: 1736.15 oz

ADJUSTMENTS:2 dealer to customer

i) Malca 138,602.961 oz

ii) Manfra: 64,694.979 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 862 contracts having LOST 850 contracts . We had

1544 notices filed on Friday so we gained a WHOPPING 694 contracts or an additional 69,400 oz will stand in this non active

delivery month of July.

August has a LOSS OF 11,107 contracts down to 254,616 contracts

Sept. lost 9 contracts to 2695 contracts.

We had 485 notice(s) filed today for 48,500 oz FOR THE July 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 90 notices were issued from their client or customer account. The total of all issuance by all participants equate to 485 contract(s) of which notices were stopped (received) by j.P. Morgan dealer and 119 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2022. contract month,

we take the total number of notices filed so far for the month (6922) x 100 oz , to which we add the difference between the open interest for the front month of (JULY 862 CONTRACTS ) minus the number of notices served upon today 485 x 100 oz per contract equals 729,900 OZ OR 22.709 TONNES the number of TONNES standing in this active month of July.

thus the INITIAL standings for gold for the JULY contract month:

No of notices filed so far (6922) x 100 oz+ (862) OI for the front month minus the number of notices served upon today (485} x 100 oz} which equals 660,500 oz standing OR 22.702 TONNES in this active delivery month of JULY.

TOTAL COMEX GOLD STANDING: 22.709 TONNES (A FAIR STANDING FOR A JULY ( NON ACTIVE) DELIVERY MONTH)

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,443,533.842 oz 76.00 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 31,897,002.252 OZ

TOTAL ELIGIBLE GOLD: 15,998.217 OZ

TOTAL OF ALL REGISTERED GOLD: 15,898,190.035 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 13,454657.0 OZ (REG GOLD- PLEDGED GOLD) 421 tonnes

END

SILVER/COMEX/JULY 18

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 123,278.300 oz Delaware CNT |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 76CONTRACT(S) 585,000 OZ) |

| No of oz to be served (notices) | 162 contracts (810,000 oz) |

| Total monthly oz silver served (contracts) | 3138 contracts 15,690,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 0 deposits into the customer account

total deposit: nil oz

JPMorgan has a total silver weight: 176.916 million oz/341.826 million =51.74% of comex

Comex withdrawals:2

i) Out of CNT: 121,247.390 oz

iv) out of Delaware 2035.000

total withdrawal 123,278.300 oz

adjustments: 0/

the silver comex is in stress!

TOTAL REGISTERED SILVER: 62.196 MILLION OZ

TOTAL REG + ELIG. 341.820 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JULY OI: 238 CONTRACTS HAVING LOST42 CONTRACTS. WE HAD 91 NOTICES FILED

ON FRIDAY, SO WE GAINED 49 CONTRACTS OR AN ADDITIONAL 245,000 OZ WILL STAND FOR METAL AT THE COMEX.

AUGUST LOST 23 CONTRACTS TO STAND AT 1099

SEPTEMBER HAD A LOSS OF 2496 CONTRACTS DOWN TO 119,449 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 76 for 380,000 oz

Comex volumes:41,882// est. volume today// poor

Comex volume: confirmed yesterday: 55,134 contracts ( poor )

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 3138 x 5,000 oz = 15 690,000 oz

to which we add the difference between the open interest for the front month of JULY(238) and the number of notices served upon today 76 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY./2022 contract month: 3138 (notices served so far) x 5000 oz + OI for front month of JULY (238) – number of notices served upon today (76) x 5000 oz of silver standing for the JULY contract month equates 16,500,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JULY 18/WITH GOLD UP $7.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.28 TONNES

JULY 15/WITH GOLD DOWN $3.75:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD///INVENTORY RESTS AT 1016.89 TONNES//

JULY 14/WITH GOLD DOWN $28.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD//INVENTORY RESTS AT 1019.79 TONNES

JULY 13/WITH GOLD UP $10.55:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROMTHE GLD//INVENTORY RESTS AT 1021.53TONNES

JULY 12/WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESS AT 1023.27 TONNES

JULY 11/WITH GOLD DOWN $4.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWL OF 1.16 TONNES FROM THE GLD./INVENTORY RESTS AT 1023.27 TONNES

JULY 7/WITH GOLD UP $1.35: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.61 TONNES FORM THE GLD///INVENTORY REST AT 1024.43 TONNES

JULY 6/WITH GOLD DOWN $26.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 9.86 TONNES FROM THE GLD//INVENTORY REST AT 1032.04 TONNES

JULY 5/WITH GOLD DOWN $36.55//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.41 TONNES FROM THE GLD///INVENTORY RESTS AT 1041.90 TONNES

JULY 1/WITH GOLD DOWN $5.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES//INVENTORY RESTS AT 1050.31 TONNES

JUNE 30/WITH GOLD DOWN $9.20: big CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 1052.63 TONNES//

JUNE 28/WITH GOLD DOWN $3.05//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.64 TONNES FROM THE GLD///INVENTORY RESTS AT 1056.40 TONNES

JUNE 27/WITH GOLD DOWN $4.90 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.04 TONNES

JUNE 24/WITH GOLD UP 45 CENTS TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.70 TONNES FROM THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 23/WITH GOLD DOWN $8.60:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//INVENTORY RESTS AT 1071.77 TONNES

JUNE 22/WITH GOLD UP 15 CENTS:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1073.80 TONNES

JUNE 21/WITH GOLD DOWN $2.00: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1075.54 TONES

JUNE 17/WITH GOLD DOWN $11.25: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.60 TONNES INTO THE GLD.///INVENTORY RESTS AT 1075.54 TONNES

JUNE 16/WITH GOLD UP $28.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.74 TONNES

JUNE 15/WITH GOLD UP $6.50/BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.65 TONNES FROM THE GLD////INVENTORY RESTS AT 1063.74 TONNES

GLD INVENTORY: 1014.28 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JULY 18/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 4.995 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ.

JULY 15/WITH SILVER UP 31 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 3.226 MILLLION OZ FORM THE SLV//INVENTORY RESTS AT 510.443 MILLIONOZ//

JULY 14/WITH SILVER DOWN 88 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 OZ FROM THE SLV// //INVENTORY RESTS AT 513.671 MILLION OZ

JULY 13/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SV//INVENTORY RESTS AT 514.501 MILLION OZ.

JULY 12/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A IWTHDRAWAL OF 3.228 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 514.501 MILLION OZ//

JULY 11/WITH SILVER DOWN 17 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 5.533 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 517.729 MILLION OZ

JULY 7/WITH SILVER UP 3 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.889 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 523.262 MILLION OZ/

JULY 6/WITH SILVER UP ONE CENT: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 12.558 MILLION OZ FORM THE SLV///INVENTORY RESTS AT 528.151 MILLION OZ

JULY 5/WITH SILVER DOWN 55 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 540.709MILLION OZ//

JULY 1/WITH SILVER DOWN 61 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ//INVENTORY RESTS AT 540.709 MILLION OZ//

JUNE 30/WITH SILVER DOWN 41 CENTS : SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 738,000 OZ FROM THE SLV//INVENTORY RESTS AT 541.262 MILLION OZ//

JUNE 28/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.00 MILLION OZ..

JUNE 27/WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 24/WITH SILVER UP 10 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.137 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 23/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 2.029 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 545.137 MILLION OZ//

JUNE 22/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.166 MILLION OZ.

JUNE 21/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.506 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 547.166 MILLION OZ//

JUNE 17/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 739,000 OZ FROM THE SLV./:INVENTORY RESTS AT 543.660 MILLION OZ/

JUNE 16/WITH SILVER UP 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 15/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

CLOSING INVENTORY 515.838 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: A Tale Of Two Dollars

MONDAY, JUL 18, 2022 – 09:50 AM

The dollar has been on a tear in recent months. Just last week, the dollar index moved from 107 to 108 with an inter-week high of 109.3. The greenback also hit parity with the euro last week. The dollar is near a 20-year high compared to the European currency and a 24-year high against the Japanese yen.

And yet we have a massive devaluing of the dollar domestically. In his podcast, Peter tries to make sense of this tale of two dollars.

You can see the impact of dollar strength on import-export prices.

Export prices rose 0.7 on the month and are up 18.2% on the year – double the consumer price index. Peter noted that import prices are a better reflection of prices paid by consumers for domestically produced goods than the 9.1% CPI.

That is a real number, unlike the CPI that is a completely contrived, made-up number where you have a formula that’s reverse-engineered to come out with a lower number.”

On the flip side, import prices are much lower thanks to the power of the dollar. Nevertheless, even with dollar strength, import prices are still up 10.7% year-on-year.

It’s because the dollar is so strong that import prices are only up by 10.7% on the year. Because if the dollar wasn’t so strong, import prices would have gone up a lot more than that and that would have spilled over into the CPI. So, but for the strong dollar, we would have much higher inflation numbers than the ones we’re dealing with.”

The situation is the opposite overseas. Europeans and Japanese are paying much more for stuff they import from the US.

So, their weak currencies are exacerbating their inflation problem, whereas our strong currency is mitigating our inflation problem.”

Peter said the overall dynamics make no sense whatsoever. The US has the highest inflation in 40 years, and yet it also has the strongest dollar in 20 years. How can that be?

How can the dollar be so weak and yet be so strong at the exact same time?”

THE DYNAMICS

When you boil it all down, inflation is the loss of a currency’s purchasing power.

If our currency buys less, that means the currency is weakening. It is losing value. We need more and more dollars to buy the same quantity of goods and services.”

If the government gave everybody $1 million, we wouldn’t be richer in absolute terms. The limiting factor isn’t money. The government can print money at will. The limiting factor is always the availability of goods and services.

If the government sends everybody a check for $1 million, but the factories don’t produce any more products than they were producing before, if service providers aren’t providing any additional services than they were before, what happens? Well, the only thing that can happen is that prices have to go up so that Americans end up buying the same quantity of goods and services. They just pay $1 million more to buy them because each dollar that they have has less value. That’s basic supply and demand. As the supply of anything goes up, demand being equal, the value of that thing has to come down. So, if you double or triple the supply of dollars, the value of each dollar is going to lose a commensurate amount of value.”

That’s what’s happening in the US. It’s not so much that prices are going up. The value of the dollar is going down. There are trillions more dollars in the economy than there were a few years ago and therefore the value of each dollar is falling.

But while the dollar is losing value, it’s not been this strong in decades. It’s gaining value relative to other currencies.

That is the dichotomy. It’s a tale of two dollars. You have the domestic dollar that is weak and losing value. And then you’ve got this international dollar that is strong and is gaining value.”

The strength of the international dollar is helping Americans somewhat, but the weakness domestically is outstripping that international strength.

The question remains — why is the dollar so strong internationally when it’s so weak domestically?

During the inflationary period of the 1970s, the dollar got destroyed. It didn’t start rebounding until Paul Volker got serious about fighting inflation.

If you look at everything from a fundamental perspective, today’s inflation should be exacting an even larger toll on the value of the dollar relative to other currencies than it was back in the 70s. Yet, the opposite is happening. Inflation is actually turning into a boon for the dollar. The weaker the dollar is in America, the stronger it becomes overseas.”

Why is that? Where is all the demand for dollars coming from? Foreigners don’t need dollars to buy US products. The US is running a massive trade deficit.

The demand is coming from speculators.

Right now, the dollar is acting as an inflation hedge for everybody outside of the United States. It’s not an inflation hedge inside the United States. You can’t buy the dollar to hedge inflation if you’re an American living in the US because there’s no hedge. The dollar is losing value. … That’s not the dynamic that Europeans are looking at, or the Japanese. From their perspective, yields in the US are very positive because they’re looking at the appreciation of the US dollar.”

Keep in mind that inflation is a worldwide problem. All of the world’s central banks have expanded their money supply. For people outside the US, the dollar looks like a solution to that problem. As the old saying goes, it’s the cleanest dirty shirt in the hamper.

Ther is also a self-perpetuating dynamic in play. As foreigners buy the dollar to hedge their currency’s inflation, the dollar goes up, reinforcing the idea that it’s an inflation hedge. That suckers in more buying.

But Peter said none of this fundamentally makes sense.

The dollar is rising on the greater fool theory. Why are people buying dollars? Not because they need them to buy American products. They’re buying them because they think some greater fool is going to pay a higher price for their dollars in the future. … That can go on for only so long until ultimately the bubble pops. And that is what is going to happen to this dollar bubble. Because that’s what it is. It’s a massive reinforcing bubble where people are buying the dollar because it’s going up. And because it’s going up, people buy it.”

At some point, people will start selling dollars to get their own currencies back. Then what?

Peter said this is the primary reason the world isn’t rushing to gold. Right now, the dollar looks like a much better alternative to gold.

Right now, the dollar is stealing gold’s luster. For a while, it was bitcoin that everybody wanted instead of gold. But now it’s the dollar that everybody wants instead of gold. Eventually, people are going to figure out that they don’t want the dollar just like a lot of them figured out they don’t want bitcoin. There is ultimately going to be a rush into gold. As I’ve been saying, gold will be the last safe haven standing because it’s the only true safe haven.”

In this podcast, Peter also discusses the fact inflation is not due to “expectations,” the politics of inflation, and he explains why investors sheltering in dollars abroad are in for a rude awakening.

END

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

END

3. Chris Powell of GATA provides to us very important physical commentaries

For your interest….

Jan Nieuwenhuijs: Swiss vault renovation delays transfer of Austrian gold from London

Submitted by admin on Sun, 2022-07-17 11:44Section: Daily Dispatches

11:35a ET Sunday, July 17, 2022

Dear Friend of GATA and Gold:

Gold researcher Jan Nieuwenhuijs of Gainesville Coins writes today that Austrian gold reserves that were to have been transferred from the Bank of England in London to storage in Switzerland are still in London.

But he adds that the delay doesn’t seem to be nefarious. Rather, Nieuwenhuijs writes, the problem is that the Swiss central bank’s main gold vault is still being renovated and Switzerland’s own gold reserves have been temporarily relocated as a result.

He provides an interesting history of Switzerland’s long involvement with gold storage and refining.

His analysis is headlined “Swiss Central Bank Moved Its Gold From Berne to a Federal Bunker in Kandersteg” and it’s posted at the Gainesville Coins internet site here:

https://www.gainesvillecoins.com/blog/swiss-central-bank-moved-its-gold-mystery

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

This is interesting: Ukraine has sold more than #12 billion of its gold during its war with Russia

(Max Hunder/Reuters)

Ukraine has sold more than $12 billion of its gold during war with Russia

Submitted by admin on Sun, 2022-07-17 17:39Section: Daily Dispatches

Gold still represents the ultimate form of payment in the world. Fiat money in extremis is accepted by nobody. Gold is always accepted. — Alan Greenspan, former chairman of the Federal Reserve Board.

* * *

By Max Hunder

Reuters

Sunday, July 17, 2022

KYIV — Ukraine’s central bank has sold $12.4 billion of gold reserves since the beginning of Russia’s invasion on Feb. 24, the bank’s deputy head said on Sunday.

“We are selling (this gold) so that our importers are able to buy necessary goods for the country,” Deputy Governor Kateryna Rozhkova told national television. She said the gold was not being sold to shore up Ukraine’s hryvnia currency.

END

No question about it: the USA had already stripped Ukraine of its gold reserves

(GATA)

Has the U.S. just stripped Ukraine of its gold reserves?

Submitted by admin on Sun, 2022-07-17 19:28Section: Daily Dispatches

7:32p ET Sunday, July 17, 2022

Dear Friend of GATA and Gold:

Eight years ago as Russia seozed Crimea from Ukraine, Ukraine’s gold appeared to have been hastily shipped to the United States. Nobody in authority would deny it:

Today the Ukrainian central bank acknowledged that $12 billion of its gold reserves recently was sold under pressure of the war with Russia that began this year:

https://www.gata.org/node/22063

Since Russia began its attack on Ukraine’s non-Crimean territory in February, the United States and its allies have appropriated tens of billions of dollars in military and humanitarian aid to Ukraine. So why would Ukraine need to sell its gold reserves unless doing so was a condition of all that U.S. and European assistance, especially since the United States already had taken custody of the Ukrainian gold?

Stripping the wounded of their valuables in wartime always suggests greed or desperation — like desperation to keep the gold price down to support the U.S. dollar and other Western currencies..

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Environmentalists are providing a brick wall against a new gold rush

(WashingtonPost/GATA)

A new gold rush pits money and jobs against California’s environment

Submitted by admin on Sun, 2022-07-17 18:22 Section: Daily Dispatches

By Scott Wilson

Washington Post

Sunday, July 17, 2022

GRASS VALLEY, Calif. — Where the Sacramento Valley steepens into the Sierra Nevada, Susan Love found a home with big windows and pine-forest views. It was the house she shared happily with her husband before his death.

The surroundings, though, are changing.

There is still a lot of gold in these hills and a lot of money at stake. But across California, a strong environmental ethos and, in many historic places, an economic shift toward tourism are now sharply at odds with the resumption of gold mining, despite its promise of new jobs more than a century and a half after tens of thousands of migrants arrived to strike it rich in this state on the country’s edge.

… For the remainder of the report:

https://www.washingtonpost.com/nation/2022/07/17/california-gold-rush-environment-jobs/

END

4. OTHER GOLD COMMENTARIES

This proves that the commercials are going net long and the specs are going net short

The Commitment of Traders Report on Friday afternoon showed the following:

Silver

*The large specs increased their long positions by 97 contracts and increased their shorts by 1,838 contracts.

*The commercials increased their longs by 1,728 contracts and reduced their shorts by 282 contracts.

*The small specs reduced their longs by 747 contracts and decreased their shorts by 672 contracts.

Gold

*The large specs reduced their long positions by 16,680 contracts and increased their shorts by 10,859 contracts.

*The commercials increased their longs by 12,881 contracts and decreased their shorts by 14,916 contracts.

*The small specs increased their longs by 8,650 contracts and increased their shorts by 8,908 contracts.

END

5.OTHER COMMODITIES:

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings MONDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.7443

OFFSHORE YUAN: 6.7501

HANG SANG CLOSED UP 548.46 PTS OR 2.70%

2. Nikkei closed UP 145.03 OR 0.54%

3. Europe stocks CLOSED ALL GREEN

USA dollar INDEX DOWN TO 10./44/Euro RISES TO 1.01239

3b Japan 10 YR bond yield: FALLS TO. +.224/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 138.35/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP -// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.147%/Italian 10 Yr bond yield FALLS to 3.34% /SPAIN 10 YR BOND YIELD FALLS TO 2.30%…

3i Greek 10 year bond yield RISES TO 3.51//

3j Gold at $1713.85 silver at: 18.87 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 75/100 roubles/dollar; ROUBLE AT 56.41

3m oil into the 99 dollar handle for WTI and 103 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 137.07DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9783– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9904well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

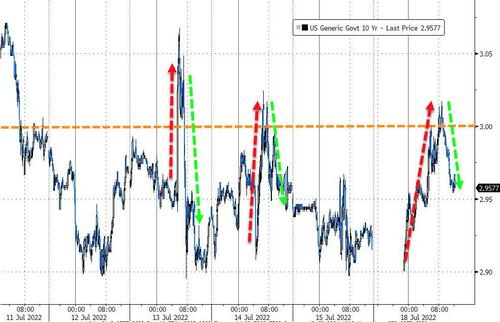

USA 10 YR BOND YIELD: 2.989 UP 6 BASIS PTS

USA 30 YR BOND YIELD: 3.096 UP 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.56

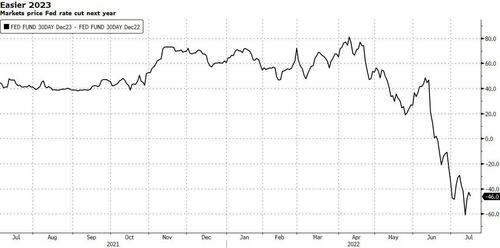

Futures Jump As Traders Scale Back Fed Hike Expectations As Economy Slumps

MONDAY, JUL 18, 2022 – 08:24 AM

US equity futures and global markets stormed higher, as the dollar extended its slide from a record high as investors scaled back bets on how aggressively the Federal Reserve will tighten policy in response to growing recession fears which Bloomberg paradoxocially interpreted as “easing recession fears.” In other words, rising risk of a recession lowers the risk of a Fed-induced recession. Lovely.

In any case, Nasdaq 100 futures rose 1.2% and contracts on the S&P 500 added 1%, with spoos trading back over 3,900 and more than 5% above June’s closing low following Friday’s strong rally on renewed hopes that the Fed will end its rate hikes and soon start cutting rates as well as end QT. West Texas Intermediate crude oil also stormed higher, undoing all recent losses and traded near $100 a barrel while the Bloomberg Dollar Spot Index slipped 0.5%, extending a retreat from a record high. The benchmark Treasury yield rose back toward 3%.

As Q2 earnings season rolls out, Goldman Sachs shares surged as much as 4% in premarket trading after the bank reported second-quarter results that were better than expected in nearly every area. Bank of America Corp.’s results were more mixed. Here are some other notable premarket movers:

- Lilium (LILM US) shares rise as much as 10% in US premarket trading on Monday after Bristow (VTOL US) secured the option to purchase 50 Lilium Jets in addition to providing maintenance services for the aircraft’s launch network in Florida, and other future U.S and European markets.

- ITHAX Acquisition (ITHX US) shares rise 32% in US premarket trading, extending gains after its holders approved the previously proposed business combination with Mondee at the EGM held on July 15, 2022.

- Cryptocurrency-exposed stocks are gaining in premarket trading after Bitcoin rose as much as 7.3% to trade above $22,000 for the first time in more than a month. Marathon Digital (MARA US) +8.8%, MicroStrategy (MSTR US) +5.1%, Coinbase (COIN US) +6.2%, Riot Blockchain (RIOT US) +7.3%, Ebang (EBON US) +2.3%

- Watch JPMorgan (JPM US) shares as Berenberg raises recommendation to hold, saying the investment bank’s shares are trading at a 20% discount to their long-run average and given the temporary nature of headwinds, downside risks to the stock “are now more limited.”

Policy makers pushed back against even bigger hikes in interest rates and fresh data showed a greater decline in US consumers’ long-term inflation expectations. That boosted odds for a 75 basis points July Fed rate hike, squashing talk of a 100 basis-point move after last week flirting with the prospect of a 100 basis-points move after data showed no let-up in stubbornly high price pressures. Yet the bullish market reaction prompted some such as Goldman to ask if the worst is now behind us.

Still, the outlook remains troubling for many investors. Gains in stock markets may prove to be short-lived as inflation pressures remain high and a recession seems increasingly likely, according to strategists at Morgan Stanley and Goldman Sachs Group Inc.

“Risk-reward at these levels has certainly improved but because we have not yet fully priced in a recession, it’s hard to say that the markets are screaming cheap,” said Anastasia Amoroso, the chief investment strategist at iCapital.

In Europe, stocks surged to the highest level in more than a month, with the Stoxx 50 jumping 1.3%, and with FTSE MIB outperforming peers, adding 1.4%, while IBEX lags, adding 0.6%. Miners, energy and banks are the strongest-performing Stoxx 600 sectors. Energy and basic resources sectors lead gains in the Stoxx 600 as oil rises after Saudi Arabia refrained from pledges to increase crude supplies, while metals rebound amid reports of China’s steps to help developers. Shell rose as much as 3.8%, TotalEnergies +2.7%, BP +3.7%, Rio Tinto +4.3%, Antofagasta +5.1%, KGHM +6.4%. Here are some of the other notable European movers today:

- GTT jumps as much as 7.5% as Societe Generale raises its price target on the LNG containment systems firm and reiterates a buy rating, as it sees the firm on the brink of its “strongest and longest period of growth” ever.

- Solvay rises as much as 5.3% after reporting preliminary results. Citi said the chemicals company reported a solid beat, driven by both volumes and prices contribution from all three segments.

- Luxury stocks including Cartier owner Richemont and UK trench-coat maker Burberry rebound after declines on Friday, with Deutsche Bank noting that there’s no underlying slowdown in consumer demand for luxury. Richemont shares rise as much as 5%, Burberry +3.8%, LVMH +1.7%

- BASF gains as much as 4.2% as Bank of America double upgrades the stock to buy from underperform, arguing that the market is overlooking the partial hedge of its oil & gas assets in Wintershall.

- Nel jumps as much as 16% after the electrolyzer firm announced a 200MW alkaline electrolyzer equipment order. Citi says the order is likely to be taken well by the market as it supports Nel’s medium-term growth outlook and is a positive sign for the trajectory of industry demand.

- Direct Line falls as much as 15% following profit guidance that was “even worse” than feared amid cost inflation, according to Jefferies, which had cut the stock to hold from buy prior to the statement Monday.

- Verbund declines as much as 7.8% after Austrian government officials suggested they’re considering a partial cap on household power bills.

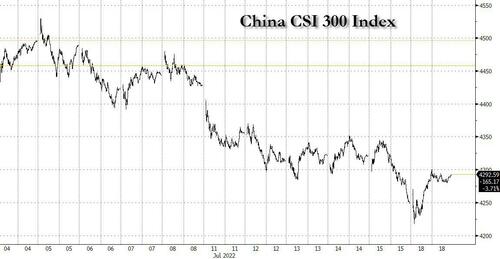

Asian stocks climbed as investors dial back expectations of aggressive tightening by the Federal Reserve while weighing China’s policy support for the ailing property sector. The MSCI Asia Pacific Index rose as much as 1.4% Monday, poised for the first gain in three days, led by financial and technology shares. Hong Kong and South Korean equities were among the top gainers in the region, while the Japanese market was closed for a holiday. Chinese shares gained after central bank Governor Yi Gang said the monetary authority will step up efforts to provide stronger economic support amid the pandemic and external headwinds. Regulators also urged banks to support developers to help stabilize the real estate market, according to another report. Asian markets took a breather as comments from two Fed officials, as well as a drop in US consumers’ long-term inflation expectations, eased fears about a super-sized interest rate hike this month. Still, ongoing Covid outbreaks in China and woes in the nation’s property sector are clouding the region’s outlook. The Asian stock benchmark is hovering near a two-year low. The Chinese central bank “doesn’t want the economy to overheat in the short term” but more policy initiatives are needed, Vikas Pershad, a fund manager at M&G Investments, said in a Bloomberg TV interview. “The slowdown in the property market is not just a small subset of mortgage payments being held back. It’s the ripple effects that go throughout the economy. And that carries through many different sectors.”

Australia’s S&P/ASX 200 index rose 1.2% to close at 6,687.10, boosted by gains across miners, banks and energy shares. A group of materials stocks rebounded as iron ore shook off losses. Whitehaven’s earnings outlook also drove optimism against the backdrop of a tightening market. In New Zealand, the S&P/NZX 50 index rose 0.4% to 11,163.63.

In FX, the Bloomberg Dollar Spot Index fell as much as 0.5%, underperforming other Group-of-10 peers; JPY and NZD are the weakest performers in G-10 FX, while GBP and SEK outperform. MXN (+0.9%) and LB (+0.8%) lead gains in EMFX. The British pound led gains.The euro rose to the highest level in a week against the dollar. The weekly fear-greed indicator hit the most bearish levels since the Greek crisis in early 2015 on Friday. The New Zealand dollar rose as much as 0.6% to $0.6201 before paring the move, after inflation accelerated more than expected in the second quarter to a fresh 32-year high, fueling bets on further aggressive tightening by the central bank,

In rates, Treasuries fell across the curve along with German bonds. US yields were cheaper by 2.5bp to 4bp across a slightly steeper curve with 2s10s, 5s30s spreads wider by 1bp and 0.5bp on the day; 10-year yields around 2.96%, cheaper by 4bp on the day while bunds underperform by additional 4bp. Italian benchmark 10-year yields surged as much as 12 basis points to 3.39%, with little sign of reconciliation among Italy’s governing coalition over the weekend. The spread between Italian and German 10-year yields rose to 223 basis points, the widest in a month, before retracing some of the move. Peripheral spreads are mixed to Germany; Italy tightens, Spain widens and Portugal widens.

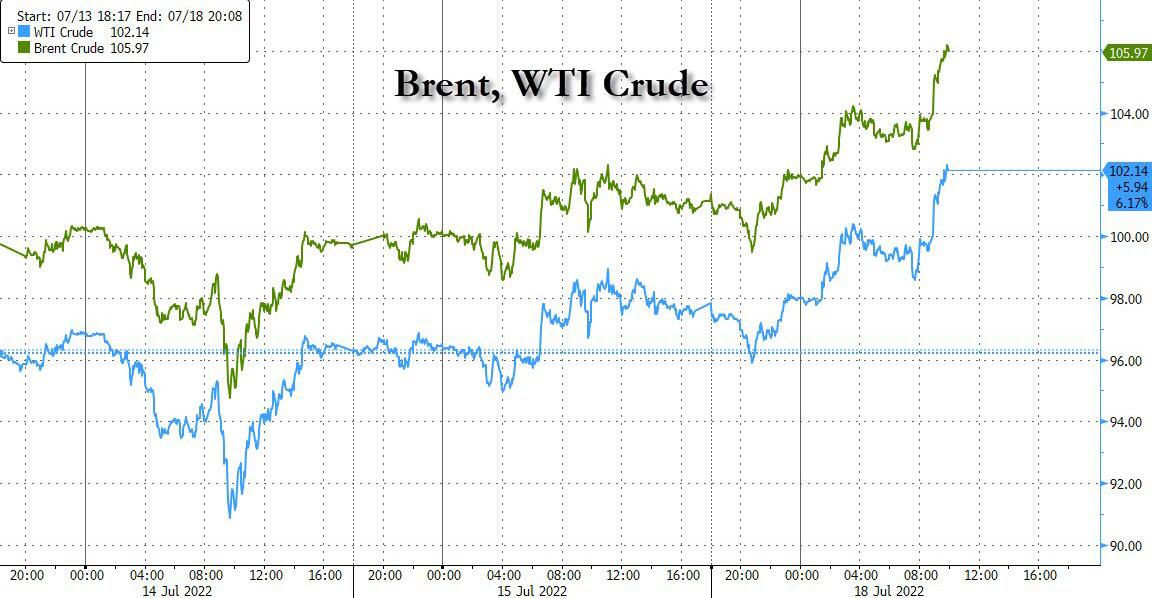

Commodities were broadly stronger after Joe Biden’s trip to the Middle East ended being a total dud and without a firm commitment from Saudi Arabia to boost crude supplies. Wheat climbed after a five-day slump and copper rallied. Crude futures advanced. as WTI drifts 1.9% higher to trade near $99.49. Brent rises 2.2% near $103.34. Most base metals trade in the green; LME nickel rises 3.3%, outperforming peers. Spot gold rises roughly $13 to trade near $1,721/oz. Spot silver gains 1.2% near $19.

US nat gas futures extended gains above the $7 level as scorching temperatures across the country boost air-conditioning demand. A heat wave in the UK and France pushed up European natural gas prices, exacerbating the region’s worst energy crunch in decades.

Separately, traders are also closely watching whether the Nord Stream pipeline from Russia will fully return to service later this week, when it ends scheduled maintenance. Moscow has already curbed supplies to the continent amid tensions related to its invasion of Ukraine: “The possibility that Russia stops, or severely reduces, their gas exports to Europe should keep markets on edge in the near-term,” Mizuho International Plc strategists Peter McCallum and Evelyne Gomez-Liechti wrote in a note to clients.

Bitcoin is bid and lifting above the $22k mark after rising above the $20K support that it has been pivoting, generally speaking, recently.

It’s a quiet start to an otherwise very busy week (with both the ECB and BOJ on deck), and we only get the NAHB Housing Market Index and the May TIC data later today. We also conclude bank earnings with BofA and Goldman reporting results premarket.

Market Snapshot

- S&P 500 futures up 1.1% to 3,907.00

- STOXX Europe 600 up 1.4% to 419.76

- MXAP up 1.4% to 156.28

- MXAPJ up 1.8% to 516.33

- Nikkei up 0.5% to 26,788.47

- Topix little changed at 1,892.50

- Hang Seng Index up 2.7% to 20,846.18

- Shanghai Composite up 1.6% to 3,278.10

- Sensex up 1.1% to 54,359.13

- Australia S&P/ASX 200 up 1.2% to 6,687.14

- Kospi up 1.9% to 2,375.25

- German 10Y yield little changed at 1.17%

- Euro up 0.5% to $1.0134

- Gold spot up 0.7% to $1,719.39

- US Dollar Index down 0.52% to 107.50

Top Overnight News from Bloomberg

- After drawing foreign capital into China’s markets for years, President Xi Jinping is now facing the risk of a nasty period of financial de-globalization. Investors point to one main reason why: Xi’s own policies

- China may allow homeowners to temporarily halt mortgage payments on stalled property projects without incurring penalties, people familiar with the matter said, as authorities race to prevent a crisis of confidence in the housing market from upending the world’s second-largest economy.

- Prime Minister Mario Draghi is under mounting pressure to reverse his pledge to resign as soon as this week and avoid throwing Italy into chaos as economic warning signs are building

- Russian Defense Minister Sergei Shoigu ordered part of his forces to focus on destroying Ukraine’s long-range missile and artillery systems during a visit to troops in occupied territory

A more detailed look at global markets courtesy of Newsquawk

APAC stocks gained with risk appetite spurred after last Friday’s firm gains on Wall St. and renewed China support pledges helped markets shrug off China’s COVID woes. ASX 200 was underpinned amid M&A activity and with Australia reinstating quarantined-support payments. Nikkei 225 was closed as Japan observed the Marine Day holiday. Hang Seng and Shanghai Comp. outperformed regional counterparts after PBoC Governor Yi pledged to increase the implementation of prudent monetary policy to provide stronger support for the real economy and with the property sector underpinned after the CBIRC asked lenders to provide credit to eligible developers so they can complete unfinished residential properties.

Top Asian News

- China reported 580 local cases on Saturday which was the highest since May 23rd. It was also reported that Shanghai said that the situation in the city remained severe. It was also reported that Shanghai is planning to conduct district-wide testing in 9 COVID-impacted districts and other smaller scope areas from Wednesday-Friday, while China’s Tianjin is also planning massive COVID tests, according to Bloomberg and Reuters.

- China is considering a mortgage grace period for home projects that have stalled, according to Bloomberg sources.

- Macau will extend its lockdown of businesses and casino closures to July 22nd, according to Reuters; subsequently, a health officials said some social activites could resume in the next week if cases drop.

- Beijing government official says no cases have been found so far in COVID tests of nearby neighborhoods, according to a media briefing.

- Chinese cyberspace regulator is to launch a two-month clean-up campaign which will focus on minors use of livestreaming, games and e-commerce platforms, according to State meida.

- US State Department approved a possible USD 108mln military sale to Taiwan, according to Reuters.

- Japanese daily COVID infection cases surpassed 110k on Saturday which was a record high, according to Jiji news agency.

- Japanese Finance Minister Suzuki reiterated sharp volatility is seen in the FX market and that they must watch moves with a strong sense of urgency, while he also noted that G20 affirmed their agreement on FX and that many countries including Japan, strongly condemned Russia’s invasion of Ukraine, according to Reuters.

- South Korean Finance Minister Choo said they are to exempt taxes on income from Korean treasury bonds to attract foreign investment, according to Reuters.

European bourses are firmer across the board in a continuation of and extension on the overnight risk tone, Euro Stoxx 50 +1.4%. Sectors are firmer across the board with the upside spearheaded by Basic Resources, Energy, and Banks – due to price action in underlying commodity prices, alongside yields. US futures are similarly bid, as we await further earnings with key names including Goldman Sachs on the docket. Delta (DAL) to buy 100 737 Max 10 Boeing (BA) craft, option for 30 additional craft. US chip firms are said to be mulling whether to oppose the CHIPS Act as it may disproportionately benefit Intel (INTC), according to Reuters sources

Top European News

- UK PM Johnson’s allies are stepping up their attacks against former Chancellor Sunak and accused him of going soft on Northern Ireland’s post-Brexit trade regime, according to FT.

- UK Foreign Secretary Truss signalled she would tighten ministerial scrutiny of the BoE if she becomes the next PM and accused the Bank of failing to tackle inflation, according to FT.

- A poll by JL Partners of more than 4,400 people found that 48% that backed the Tories in 2019 considered former Chancellor Sunak would be a good PM, while 39% thought the same of Foreign Secretary Truss and 33% thought the same of Trade Secretary Mordaunt, according to The Telegraph.

- ConservativeHome survey suggested Trade Secretary Mordaunt would lose in a head-to-head against former Chancellor Sunak (41% vs 43%) and against Foreign Secretary Truss (41% vs 48%), according to The Telegraph.

- UK Foreign Secretary Truss confirms she will not be attending Tuesday’s (July 19th) Sky News leadership debate, via Huffington Post’s Schofield; additionally, reports that former-Chancellor Sunak is pulling out of the debate.

- Italy’s League and Forza Italia parties said they can no longer govern with the 5-Star Movement which brings the government closer to collapsing ahead of a potential confidence vote on Wednesday, according to Politico.

- European Investment Bank said it will reduce road and infrastructure funding in line with its climate objectives, according to FT.

Central Banks

- Fed officials signalled they are likely to increase rates by 75bps at the July meeting and noted that although policymakers left the door open for a 100bps increase, some have simultaneously poured cold water on the idea in recent interviews and comments, according to WSJ.

- RBNZ announced a new standing repurchase facility which will permit eligible counterparties to lend NZD through the standing repurchase facility from July 20th and will be remunerated at the OCR -15bps, while the RBNZ will deliver to counterparty nominal New Zealand government bonds as collateral in exchange for depositing NZD, according to Reuters.

- PBoC Governor Yi said China’s economy faces downward pressure due to COVID and external shocks, while he added that the central bank will increase the implementation of prudent monetary policy to provide stronger support for the real economy, according to a PBoC statement cited by Reuters.

- HKMA said they need to regulate decentralised finance platforms sooner rather than later, while RBA Governor Lowe commented that it is likely better for retail digital currency tokens to be issued by regulated private sector companies than central banks, according to Reuters.

- SNB intends to increase rates by at least 50bp (from the current -0.25%) at the September gathering, in the scenaro of further inflation upside a 75bp move could occur, according to sources via Schweiz am Wochenende.

- BoE’s Saunders says he will not announce today how he will vote at the August meeting; believes that the tightening cycle has “some way to go”, the cost of not tightening promptly enough would be relatively high at present.

- Czech central bank’s Dedek said it is appropriate today to use FX intervention to prevent the crown from weakening and the aim is not to strengthen the currency, while he added that they are far from the point they would start to feel reserves are getting dangerously low, according to Lidove Noviny.

FX

- Sterling takes advantage of Buck’s demise even before hawkish commentary from BoE’s Saunders, Cable closer to 1.2000 than 1.1850, DXY nearer 107.000 than 108.00.

- Aussie underpinned by rebound in iron ore ahead of RBA minutes, AUD/USD approaching 0.6850 from sub-0.6800 overnight low.

- Euro probes 1.0150 vs Greenback ahead of Thursday’s ECB meeting and expected 25 bp hike.

- Loonie supported by recovery in WTI and BoC Governor Macklem flagging Canadian CPI on 8% handle next week, USD/CAD below 1.3000.

- Kiwi capped after stronger than forecast NZ inflation data as RBNZ announces standing repo for loans 15 bp below OCR to start on July 20th, NZD/USD hovering under 0.6200 and AUD/NZD cross above 1.1050.

- Franc lags irrespective of reporting suggesting SNB to hike at least half point again in September as weekly Swiss sight deposits at domestic bank increase, USD/CHF pivots 0.9750.

- Lira lurches further in wake of Turkish budget balance turning from surplus to deficit, USD/TRY testing 17.5000 offers and semi-psychological resistance.

Commodities

- WTI and Brent have been moving higher with the broader risk tone and after the Biden-Saudi meeting with attention, for the complex, looking to the next OPEC+ gathering.

- Saudi Arabia’s Crown Prince MBS said adopting unrealistic policies toward energy sources will lead to inflation and he called on Iran to cooperate with the region, according to Reuters. Saudi’s Crown Prince also said that they have an immediate capacity to increase production to 12mln bpd and with investments, production can go to 13mln bpd after which the kingdom will not have any additional capacity to increase production.

- Saudi Foreign Minister said that they listen to their partners and friends across the world especially consumer countries but added that at the end of the day, OPEC+ follows the market situation and will supply energy as needed, according to Bloomberg.

- US senior envoy for energy security Hochstein said he expects gas prices to decline further towards USD 4/gallon and is confident there will be a few more steps in the coming weeks from OPEC in terms of oil supply, according to Reuters.

- Energy Intel’s Bakr stated that we are in a situation where capacity is limited which is why the UAE and Saudi Arabia want to remain cautious about how and when it is used.

- Top German energy regulator said natgas inventories are nearly 65% full but not enough to get through the winter without Russian gas, according to Bild am Sonntag.

- Libya’s Oil Minister said Libya has resumed oil exports, according to Al Jazeera. It was also reported that the NOC said its board will not cooperate with any illegal dismissal decisions made by an outgoing administration.

- South Africa’s largest fuel producer Sasol declared a force majeure on the supply of petroleum products due to delays in deliveries of crude to the Natref refinery, while the outage means all refineries in the country are shut, according to Bloomberg.

- Iran set August Iranian light crude price to Asia at Oman/Dubai + USD 8.90/bbl, according to Reuters sources.

- Spot gold is bid as the USD pulls-bacl but is yet to breach USD 1725/oz in relatively limited European newsflow. Base metals bid after strong overnight performance.

US Event Calendar

- 10:00: July NAHB Housing Market Index, est. 65, prior 67

- 16:00: May Total Net TIC Flows, prior $1.3b

DB’s Jim Reid concludes the overnight wrap

It could be a record week here in the UK with temperatures possibly hitting 40 degrees for the first time ever today or tomorrow! While the warm weather has been pleasant of late, I can’t wait until Wednesday when it cools down a bit. The coolest I was this weekend was going to a cinema on Saturday night with aircon to see Top Gun Maverick. However that was an incredibly stressful film. I’m not really a fan of action movies but that was edge of the seat stuff and very well done. Looking forward to the third part of the trilogy in 2058.

Back to 2022, and with the Fed now on their FOMC blackout period and a lighter US week for data (ex-housing), Q2 US earnings and all things European will be at the forefront of market attention this week with the highlight being the ECB’s likely first rate hike since 2011 on Thursday. Gas flows from Russia after maintenance on the Nord Stream pipeline ends the same day will also be a big focus with the EU expected to detail energy contingency plans the day before. We’ll also get a decision from the BoJ on Thursday too. Global preliminary July PMIs for the US, Japan and key European economies will come out on Friday.

Going through some of these themes in more detail now. The ECB meeting on Thursday will likely deliver a +25bps hike, the first rate increase since 2011. Our European economists preview the upcoming meeting here. Their updated call retains the 2% terminal rate forecast but the hiking cycle is expected to be split. The first phase has hikes of +25bp, +50bp, +50bp and +25bp in July, September, October and December. By end-2022, the deposit rate will be 1%, helping to balance inflation and growth risks before the anticipated recession forces a pause. The second phase in H1 2024 is now expected to have four +25bp hikes and push rates into moderately above neutral territory. The ECB’s decision comes as Europe is grappling with significant concerns about the energy supply, a euro that has reached parity against the dollar for the first time since 2002, and inflation at an all-time high of 8.6%. If that’s not enough, it also comes alongside a recent widening in peripheral sovereign bond spreads and an Italian government possibly on the brink of collapse. We should know more on Wednesday when Draghi addresses lawmakers in Rome, however things are escalating quickly. The Five Star Movement (the second largest in the coalition) effectively abstained in a confidence motion in the Senate, triggering the current crisis. This weekend the party have met and don’t seem to be dialling down the rhetoric with leader Conte blaming Draghi for the impasse. Meanwhile the centre-right block are saying the coalition pact has been broken and that they won’t now rule in a coalition with Five Star. Probabilities of a snap election are certainly going up.

With this unfolding, the details of the anti-fragmentation tool will be highly sought after at the ECB meeting and our economics team reviews the key features of the new tool – size, target, conditionality and sterilisation method – in the same preview note mentioned above. The ECB will also release its Euro area bank lending survey tomorrow and the Survey of Professional Forecasters on Friday.

Another event that will keep investors on edge that day is the end of the Nord Stream pipeline’s scheduled maintenance period. Fears that Russia will keep the taps closed have roiled markets in recent weeks and the EU is expected to detail contingency plans on Wednesday. Although the NS1 maintenance period ends on Thursday, it’s possible that there will be ambiguity on supply for a while. Whatever Russia’s plans for supply through the autumn and winter, we may not fully see it in the next few days and weeks. Part of that might be politics and part of it may be operational as the turbine repair may take a while to be fully integrated, or at least that could be the claim. So we may get a few clues from Friday but it is unlikely we’ll know all the answers. See my one-sided devil’s advocate view in Thursday’s CoTD here on why it’s not in Putin’s interest to completely cut off the supply of gas.

Also on Thursday, the next policy decision from the BoJ will be due. Our chief Japan economist previews the meeting here. While he expects no change in the current monetary stance and forward guidance on policy rates, the BoJ’s Outlook Report is expected to show a downgrade in its growth forecast for FY2022 and an increase in its inflation forecast. The national CPI print will be due the next day and our economist expects core inflation (ex. fresh food) to climb to 2.2% YoY (+2.1% in May) and core-core inflation (ex. fresh food and energy) to 0.9% (+0.8% in May). Small fry in a western context but relatively strong for Japan.

Back to the data and US housing market indicators will be in focus this week, after the June CPI report showed the fastest monthly gains since 1986 for primary rents and 1990 for owners’ equivalent rent. In terms of data, we have July’s NAHB Housing Market Index (today), followed by June housing starts, building permits (tomorrow) and existing home sales (Wednesday).

In European data, the UK will be in focus with June CPI, RPI, PPI and May’s house price index due on Wednesday, preceded by labour market data tomorrow. Also released tomorrow will be July’s consumer confidence for the Eurozone, followed by a similar gauge and June retail sales for the UK on Friday.

In terms of earnings, after key US banks started reporting last week, we will get more insight into the state of the economy and consumer spending from Goldman Sachs, Bank of America (today) and American Express (Friday). Amid a mixed-bag performance for commodities in recent weeks, results from Halliburton (tomorrow), Baker Hughes (Wednesday), Schlumberger and NextEra (Friday) will be in focus. Earnings of consumer-oriented companies will be highly anticipated as well, including Johnson & Johnson (tomorrow), United Airlines, Tesla (Wednesday) and American Airlines (Thursday). In tech, key reporting corporates will include IBM (today), Netflix (tomorrow), ASML (Wednesday), SAP (Thursday) and Twitter (Friday). Other corporate earnings reports will feature Lockheed Martin (tomorrow), AT&T, Blackstone (Thursday) and Verizon (Friday).

Asian equity markets are higher at start of the week after gains on Wall Street on Friday. As I type, the Hang Seng (+2.45%) is leading the way followed by the Kospi (+1.80%), Shanghai Composite (+1.49%) and the CSI (+1.00%). Elsewhere, markets in Japan are closed today for the Marine Day Holiday. Outside of Asia, stock futures in the DMs are pointing to additional gains with contracts on the S&P 500 (+0.43%), NASDAQ 100 (+0.75%) and DAX (+0.37%) all climbing.

Early morning data showed that New Zealand’s consumer price index (+7.3% y/y) climbed to a 32-year high in the June 2022 quarter (v/s +7.1% expected) and speeding up from a +6.9% gain in the first quarter, mainly due to rising prices for construction and rentals for housing.

Looking back on another wild week in markets now. The highlight was inflation. The US CPI report came out on Wednesday, where headline yoy inflation bumped up to 9.1%, its highest since 1981. Indeed, each of the headline/core/MoM/YoY measures surpassed expectations. The following day showed producers were also feeling the heat, with final demand PPI measures beating expectations, with the crucial health care component portending an increase in upcoming PCE prints, the Fed’s preferred inflation measure.

The prints drove speculation the Fed would deliver a super-charged 100bp hike at the July meeting, but Fed officials threw water on that pricing at the end of the week, signaling a preference for a second consecutive 75bp hike. Nevertheless, the yield curve moved to its most inverted of the cycle, ending the week at -21.3bps, as expected Fed tightening was brought forward, and the resulting landing was expected to get that much harder. All told, 2yr yields increased +1.5bps (-1.2bps Friday) and 10yr yields fell -16.5bps (-4.4bps Friday). While stocks experienced a bump on the easier policy expectations (75 not 100) from Fed speakers at the end of the week, the S&P 500 climbing +1.92% Friday, the index fell the other four days and ended the week -0.93% lower. Tech underperformed with the NASDAQ falling -1.57%, staging a +1.79% recovery of its own on Friday.

US earnings season kicked off, with major US financials disappointing, as major money center banks signaled they would likely need to optimise their balance sheets to increase capital ratios over the near-term. A realisation that had JPMorgan temporarily suspending share buybacks.

Along with their own inflationary worries, Europe is also facing down political and energy crises. The attempted resignation of Prime Minister Draghi, and subsequent rejection by President Mattarella, injected yet more turmoil into European asset pricing. 10yr BTPs widened 19.4bps versus bunds (+6.5bps Friday), to 212bps, their widest levels since the ECB has floated a new anti-fragmentation tool. Heading into this week’s ECB meeting, pricing currently is at +29.0bps, a smidge higher than the week prior, so some chance the ECB will kick off the hiking cycle with a 50bp hike. 10yr bunds were 21.2bps lower (-4.5bps Friday), giving swirling risk on the continent. Speaking of European natural gas, prices managed to fall -8.23% (-8.84% Friday) following news that Canada would deliver the necessary turbine to restore gas flows from Russia back to the continent, but prices traded in a more than 20% range over the week, showing the anxiety that still dominates the situation. Elsewhere, brent crude fell below $100/bbl intraweek for the first time since mid-April, ultimately falling -5.50% on the week (+2.08% Friday) to $101.16/bbl as global growth fears grip markets.

i)MONDAY MORNING// SUNDAY NIGHT

SHANGHAI CLOSED UP 50.04 PTS OR 1.55% //Hang Sang CLOSED UP 548.46 OR 2.70% /The Nikkei closed UP 145.08 OR % 0.54. //Australia’s all ordinaires CLOSED UP 1/32% /Chinese yuan (ONSHORE) closed UP AT 6.7443 /Oil UP TO 99.81 dollars per barrel for WTI and DOWN TO 103.72 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7443 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7501: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

3 a./NORTH KOREA/ SOUTH KOREA/

///NORTH KOREA/SOUTH KOREA/

3B JAPAN

3c CHINA

CHINA

Beijing panics as they try and halt mortgage boycott!!

Beijing Panics, Scrambles To Halt Mortgage Boycott By “Urging” Banks To Rush Developer Loans

MONDAY, JUL 18, 2022 – 01:50 PM