by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1728.90 UP $14.45

SILVER: $18.71 DOWN 10 CENTS

ACCESS MARKET:

GOLD $1727.15

SILVER: $18.62

Bitcoin morning price: $23,043 UP 488

Bitcoin: afternoon price: $23,074. UP 457

Platinum price: closing UP $5.35 to $880.30

Palladium price; closing UP $123.80 at $2012.95

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JULY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,712.700000000 USD

INTENT DATE: 07/21/2022 DELIVERY DATE: 07/25/2022

FIRM ORG FIRM NAME ISSUED STOPPED

363 H WELLS FARGO SEC 30

624 H BOFA SECURITIES 256

657 C MORGAN STANLEY 6

661 C JP MORGAN 292

TOTAL: 292 292

MONTH TO DATE: 9,519

no. of contracts issued by JPMorgan: 292/292

_____________________________________________________________________________________

NUMBER OF NOTICES FILED FOR JULY CONTRACT: 292 NOTICES FOR 29,200 OZ //0.9082 TONNES

total notices so far: 9519 contracts for 951,900 oz (29.608 tonnes)

SILVER NOTICES:

47 NOTICES FILED FOR 235,000 OZ/

total number of notices filed so far this month 3405 : for 17,025,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $17.45

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD:

TONNES FROM THE GLD///

INVENTORY RESTS AT 1005.87 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 10 CENTS

AT THE SLV// ://NO CHANGES IN SILVER INVENTORY AT THE SLV//:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 500.484 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GOOD SIZED 710 CONTRACTS TO 145,595 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GOOD LOSS IN OI WAS ACCOMPLISHED WITH OUR TINY $0.05 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.05) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY COMMERCIAL SILVER LONGS//BUT MAINLY WE HAD ADDITIONAL SPECULATOR ADDITIONS AS WE HAD A STRONG GAIN OF 937 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A POOR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.220 MILLION OZ FOLLOWED BY TODAY’S 270,000 OZ QUEUE JUMP / // V) GOOD SIZED COMEX OI LOSS

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -46

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTACTS for 15 days, total 13,508 contracts: 67.540 million oz OR 4.502 MILLION OZ PER DAY. (901 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 67.54 MILLION OZ

.

LAST 15 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 67.54 MILLION OZ

RESULT: WE HAD A GOOD SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 710 DESPITE OUR $0.05 GAIN IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 1601 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A POOR INITIAL SILVER OZ STANDING FOR JUNE. OF 15.22 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 270,000 OZ // .. WE HAD A VERY STRONG SIZED GAIN OF 937 OI CONTRACTS ON THE TWO EXCHANGES FOR 4.455 MILLION OZ WITH THE GAIN IN PRICE..

WE HAD 47 NOTICES FILED TODAY FOR 235,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 9671 CONTRACTS TO 518,984 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -44 CONTRACTS.

.

THE STRONG SIZED DECREASE IN COMEX OI CAME DESPITE OUR RISE IN PRICE OF $11.40//COMEX GOLD TRADING/THURSDAY / WE MUST HAVE HAD ADDITIONAL SPECULATOR SHORT ADDITION ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //AND SOME SPECULATOR SHORT ADDITIONS

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JULY AT 2.914 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 17,500 OZ

YET ALL OF..THIS HAPPENED WITH OUR STRONG RISE IN PRICE OF $11.40 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A VERY TINY SIZED GAIN OF 108 OI CONTRACTS 0.3359 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 9779 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 518,984

IN ESSENCE WE HAVE A VERY TINY SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 108 CONTRACTS WITH 9671 CONTRACTS DECREASED AT THE COMEX AND9779 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 108 CONTRACTS OR 0.3359 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (9779) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (9,571): TOTAL GAIN IN THE TWO EXCHANGES 10,324 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JULY. AT 2.914 TONNES FOLLOWED BY TODAY’S 17,500 OZ QUEUE JUMP 3) ZERO LONG LIQUIDATION//CONSIDERABLE SPECULATOR SHORT ADDITIONS/ //.,4) STRONG SIZED COMEX OPEN INTEREST LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

98,062 CONTRACTS OR 9,806,200 OZ OR 305.01 TONNES 15 TRADING DAY(S) AND THUS AVERAGING: 6305 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15 TRADING DAY(S) IN TONNES: 305.01 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 305.01/3550 x 100% TONNES 8.59% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 305.01 TONNES (HUGE INCREASE FROM JUNE//WILL CLOSE IN ON THE RECORD EFP ISSUANCE IN MARCH 22)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JULY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 710 CONTRACT OI TO 145,595 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1601 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 1601 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE:1601 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 664 CONTRACTS AND ADD TO THE 1601 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 891 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 4.455 MILLION OZ

OCCURRED WITH OUR SMALL RISE IN PRICE OF $0.05

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED DOWN 2.03 PTS OR 0.06% //Hang Sang CLOSED UP 34.51 OR 0.17% /The Nikkei closed UP 111.66 OR % 0.40. //Australia’s all ordinaires CLOSED DOWN 0.09% /Chinese yuan (ONSHORE) closed UP AT 6.7583//OFF SHORE CHINESE YUAN UP 7.613// /Oil DOWN TO 95.41 dollars per barrel for WTI and BRENT AT 103.13// SHANGHAI CLOSED DOWN 2.03 PTS OR 0.06% //Hang Sang CLOSED UP 34.51 OR 0.17% /The Nikkei closed UP 111.66 OR % 0.40. //Australia’s all ordinaires CLOSED DOWN 0.09% / Stocks in Europe OPENED ALL GREEN ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONG AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 9,627 CONTRACTS TO 519,028 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS STRONG COMEX INCREASE OCCURRED DESPITE OUR RISE OF $11.40 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (6455 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 9627 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :9627 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 9627 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY TINY SIZED SIZED TOTAL OF 152 CONTRACTS IN THAT 9779 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 9627 CONTRACTS..AND THIS SMALL GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR STRONG RISE IN PRICE OF GOLD $ 11.40.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING JULY (29.645),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.645 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $11.40) AND WERE UNSUCCESSFUL IN KNOCKING OFF SOME SPECULATOR LONGS/COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS//// WE HAVE REGISTERED A VERY TINY SIZED GAIN OF 0.4778 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR JULY (29.645 TONNES)…

WE HAD -XX CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 132 CONTRACTS OR 13200 OZ OR 0.4728 TONNES

Estimated gold volume 254,786/// fair/

final gold volumes/yesterday 317,644 / good

INITIAL STANDINGS FOR JULY ’22 COMEX GOLD //JULY 22

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 160,112,481oz Brinks Malca Manfra |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | NIL oz |

| No of oz served (contracts) today | 292 notice(s) 29,200 OZ 0.9082 TONNES |

| No of oz to be served (notices) | 12 contracts 1200 oz 0.0373 TONNES |

| Total monthly oz gold served (contracts) so far this month | 9519 notices 951900 OZ 29.608 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

No dealer withdrawals

Customer deposits: 0

total deposits: NIL oz

3 customer withdrawals:

i)Out of Brinks 128.61 oz (4 kilobar)

ii)Out of Manfra: 21,380.03 oz (665 KILOBARS)

iii) Out of Malca: 138,602.961 oz

total withdrawal: 160.111.681 oz (4.98 tonnes)

ADJUSTMENTS:3 dealer to customer

Brinks: 76,680.135 oz

JPMorgan: 4630.911 oz

Malca: 2797.137 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 304 contracts having GAINED 162 contracts . We had

13 notices filed on Thursday so we GAINED a strong 175 contracts or an additional 17,500 oz will stand in this non active

delivery month of July.

August has a LOSS OF 28,579 contracts down to 187,913 contracts

Sept. gained 99 contracts to 2878 contracts.

We had 292 notice(s) filed today for 29200 oz FOR THE July 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 292 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 292 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2022. contract month,

we take the total number of notices filed so far for the month (9519) x 100 oz , to which we add the difference between the open interest for the front month of (JULY 304 CONTRACTS ) minus the number of notices served upon today 292 x 100 oz per contract equals 953,100 OZ OR 29.645 TONNES the number of TONNES standing in this active month of July.

thus the INITIAL standings for gold for the JULY contract month:

No of notices filed so far (9519) x 100 oz+ (304) OI for the front month minus the number of notices served upon today (292} x 100 oz} which equals 953,100 oz standing OR 29.645 TONNES in this active delivery month of JULY.

TOTAL COMEX GOLD STANDING: 29.645 TONNES (A FAIR STANDING FOR A JULY ( NON ACTIVE) DELIVERY MONTH)

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,443,533.842 oz 76.00 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 31,173,271.582 OZ

TOTAL REGISTERED GOLD: 15,873,034.587 OZ

TOTAL OF ALL ELIGIBLE GOLD: 15,300,736.995 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 13,538,186.0 OZ (REG GOLD- PLEDGED GOLD) 421 tonnes

END

SILVER/COMEX/JULY 22

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,579,769.080 oz CNT Delaware JPMorgan Loomis |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,158,871.160 oz JPM Loomis |

| No of oz served today (contracts) | 47 CONTRACT(S) 235,000 OZ) |

| No of oz to be served (notices) | 183 contracts (915,000 oz) |

| Total monthly oz silver served (contracts) | 3405 contracts 17,025,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) Into Delaware 2004.061 oz

total deposit: 2004.061 oz

JPMorgan has a total silver weight: 177.063 million oz/341.926 million =51.79% of comex

Comex withdrawals:0

adjustments: 1/dealer to customer

JPMorgan: 312,407.190 oz

customer to Dealer: HSBC: 889,917.620 oz

two: customer to dealer

a) Brinks 55,536.920 oz

b) HSBC 8937.110 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 60.044 MILLION OZ

TOTAL REG + ELIG. 341.926 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JULY OI: 230 CONTRACTS HAVING LOST 31 CONTRACTS. WE HAD 85 NOTICES FILED

ON THURSDAY, SO WE GAINED 54 CONTRACTS OR AN ADDITIONAL 270,000 OZ WILL STAND FOR METAL AT THE COMEX.

AUGUST LOST 40 CONTRACTS TO STAND AT 983

SEPTEMBER HAD A LOSS OF 663 CONTRACTS UP TO 117,185

CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 47 for 235,000 oz

Comex volumes:43,714// est. volume today// poor

Comex volume: confirmed yesterday: 60,290 contracts ( poor )

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 3405 x 5,000 oz = 17 025,000 oz

to which we add the difference between the open interest for the front month of JULY(230) and the number of notices served upon today 47 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY./2022 contract month: 3405 (notices served so far) x 5000 oz + OI for front month of JULY (230) – number of notices served upon today (47) x 5000 oz of silver standing for the JULY contract month equates 17,940,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JULY 22/WITH GOLD UP $17.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 21/WITH GOLD UP $11.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.101 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.87 TONNES

JULY 20/WITH GOLD DOWN $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1009.06 TONNES

JULY 19/WITH GOLD DOWN $.35 :BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.22 TONNES FROM THE GLD//INVENTORY RESTS AT 1009.06 TONNES

JULY 18/WITH GOLD UP $7.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.28 TONNES

JULY 15/WITH GOLD DOWN $3.75:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD///INVENTORY RESTS AT 1016.89 TONNES//

JULY 14/WITH GOLD DOWN $28.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD//INVENTORY RESTS AT 1019.79 TONNES

JULY 13/WITH GOLD UP $10.55:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROMTHE GLD//INVENTORY RESTS AT 1021.53TONNES

JULY 12/WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESS AT 1023.27 TONNES

JULY 11/WITH GOLD DOWN $4.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWL OF 1.16 TONNES FROM THE GLD./INVENTORY RESTS AT 1023.27 TONNES

JULY 7/WITH GOLD UP $1.35: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.61 TONNES FORM THE GLD///INVENTORY REST AT 1024.43 TONNES

JULY 6/WITH GOLD DOWN $26.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 9.86 TONNES FROM THE GLD//INVENTORY REST AT 1032.04 TONNES

JULY 5/WITH GOLD DOWN $36.55//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.41 TONNES FROM THE GLD///INVENTORY RESTS AT 1041.90 TONNES

JULY 1/WITH GOLD DOWN $5.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES//INVENTORY RESTS AT 1050.31 TONNES

JUNE 30/WITH GOLD DOWN $9.20: big CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 1052.63 TONNES//

JUNE 28/WITH GOLD DOWN $3.05//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.64 TONNES FROM THE GLD///INVENTORY RESTS AT 1056.40 TONNES

JUNE 27/WITH GOLD DOWN $4.90 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.04 TONNES

JUNE 24/WITH GOLD UP 45 CENTS TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.70 TONNES FROM THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 23/WITH GOLD DOWN $8.60:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//INVENTORY RESTS AT 1071.77 TONNES

JUNE 22/WITH GOLD UP 15 CENTS:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1073.80 TONNES

GLD INVENTORY: 1005.87 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JULY 22/WITH SILVER DOWN 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 500.484 MILLION OZ//

JULY 21/WITH SILVER UP 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.19 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 500.484MILLION OZ/

JULY 20/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 8.253 MILLION OZ FORM THE SLV/INVENTORY RESTS AT 507.585 MILLION OZ//

JULY 19/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ//

JULY 18/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 4.995 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ.

JULY 15/WITH SILVER UP 31 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 3.226 MILLION OZ FORM THE SLV//INVENTORY RESTS AT 510.443 MILLIONOZ//

JULY 14/WITH SILVER DOWN 88 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 OZ FROM THE SLV// //INVENTORY RESTS AT 513.671 MILLION OZ

JULY 13/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SV//INVENTORY RESTS AT 514.501 MILLION OZ.

JULY 12/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.228 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 514.501 MILLION OZ//

JULY 11/WITH SILVER DOWN 17 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 5.533 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 517.729 MILLION OZ

JULY 7/WITH SILVER UP 3 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.889 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 523.262 MILLION OZ/

JULY 6/WITH SILVER UP ONE CENT: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 12.558 MILLION OZ FORM THE SLV///INVENTORY RESTS AT 528.151 MILLION OZ

JULY 5/WITH SILVER DOWN 55 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 540.709MILLION OZ//

JULY 1/WITH SILVER DOWN 61 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ//INVENTORY RESTS AT 540.709 MILLION OZ//

JUNE 30/WITH SILVER DOWN 41 CENTS : SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 738,000 OZ FROM THE SLV//INVENTORY RESTS AT 541.262 MILLION OZ//

JUNE 28/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.00 MILLION OZ..

JUNE 27/WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 24/WITH SILVER UP 10 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.137 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 23/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 2.029 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 545.137 MILLION OZ//

JUNE 22/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.166 MILLION OZ.

CLOSING INVENTORY 500.484 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

END

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

3. Chris Powell of GATA provides to us very important physical commentaries

Your weekend reading material.

A must read

(Courtesy Alasdair Macleod/GATA)

Alasdair Macleod: Gold and the coming recession

Submitted by admin on Thu, 2022-07-21 19:27Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, July 21, 2022

We are now seeing the initial stages of a currency, credit, and banking crisis develop. Driving it are an inflation of prices, contraction of bank credit, and a pathological fear of recession. One can imagine that the major central banks almost wish a mild recession upon us so that they can keep interest rates suppressed and bond yields low.

The key to understanding the course of events is that the cycle of bank credit is turning down, and this time the factors driving contraction are greater than anything we have experienced since the 1930s, and possibly in all modern monetary history.

This article joins the dots between inflation and recession and puts the relationship between money (that is only gold), currencies, credit, and commodity prices into the proper perspective. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/gold-and-the-upcoming-recession

4. OTHER GOLD/SILVER COMMENTARIES

RONAN MANLY/BULLION STAR:

Despite Manipulating Precious Metals Prices, JPMorgan Is Still At The Heart Of The LBMA, SBMA, & COMEX

FRIDAY, JUL 22, 2022 – 07:20 AM

Submitted by Ronan Manly, BullionStar.com

With a group of former JP Morgan precious metals traders currently on criminal trial in front of a federal jury in Chicago, accused of engaging in a racketeering conspiracy involving precious metals price manipulation, commodities fraud and trade spoofing, while another group of their colleagues have already pleaded guilty, now is a good time to ask how the bank JP Morgan is still considered fit and proper to not only continue to trade in the precious metals markets, but to continue to literally dominate the entire precious metals industry in London, Singapore and New York, with the support of the London Bullion Market Association (LBMA), the Singapore Bullion Market Association (SBMA) and the CME Group (operator of the COMEX and NYMEX).

While JP Morgan made a deferred prosecution deal with the US Department of Justice (DoJ) and Commodity Futures Trade Commission (CFTC) in 2020 and admitted wrongdoing for the criminal conduct of numerous JP Morgan traders and sales personnel on the bank’s precious metals desk located in London, Singapore, and New York, while paying US$ 920 million in the form of a criminal monetary penalty, criminal disgorgement, and victim compensation in relation to this criminal precious metals scheme, the LBMA and SBMA and CME Group (owner of COMEX), as you will see below, continue to not only welcome the proven criminal bank JP Morgan with open arms, but to allow JP Morgan to operate at the highest levels of each organisation.

Ongoing Trial of Nowak & Co

The current criminal trial, which kicked off on Friday 8 July 2022, with the US DoJ and CFTC as prosecution, accuses Michael Nowak (former head of JP Morgan’s precious metals trading desk), Gregg Smith (former JP Morgan precious metals trader) and Jeffery Ruffo (former JP Morgan precious metals salesman) of being involved in a criminal enterprise that entered and cancelled thousands of fake precious metals futures orders (deceptive orders) for gold, silver, platinum and palladium futures contracts traded on COMEX and NYMEX between March 2008 and August 2016 in order to manipulate precious metals prices as well as manipulate barrier options based on the futures prices.

A fourth former JP Morgan precious metals trader, Christopher Jordan, who left JP Morgan in December 2009, is also accused of similar crimes by the DoJ and will be tried separately.

The Nowak – Smith – Ruffo trail is being presided over by Edmond E. Chang, United States District Judge. Unbelievably (or maybe not), Nowak’s defense lawyer in the trial is none other than David Meister, who from 2010 – 2013 was the CFTC’s Director of Enforcement, and who was at the CFTC during the chairmanship of Gary Gensler during which time the CFTC did a 5 year investigation into precious metals price manipulation, and then shut down the investigation claiming it had found no evidence of manipulation. That could explain why Meister is called “the Gensler Whisperer” by lawyer profile experts Chambers.

At the time the indictment of Nowak, Smith and Jordan was unsealed in September 2019, US Assistant Attorney General Brian A. Benczkowski at the DoJ said:

“The defendants and others allegedly engaged in a massive, multiyear scheme to manipulate the market for precious metals futures contracts and defraud market participants.”

In the current trial of Nowak, Smith and Ruffo, the US Government is calling two other former JP Morgan precious metals traders as witnesses for the prosecution, namely John Edmonds, Christian Trunz, and one colleague of Gregg Smith’s who worked with him at Bear Stearns, namely Corey Flaum.

Edmonds and Trunz have already pleaded guilty to their roles in the JP Morgan criminal scheme, and Flaum has already pleaded guilty to manipulating precious metals prices via COMEX futures between 2007 and 2016.

As of the time of writing, John Edmonds, Corey Flaum and Christian Trunz have all just testified to the federal jury in the Nowak – Smith – Ruffo trial. See here for Edmonds testimony, here for Flaum’s testimony, and here for Trunz’s testimony. The earlier guilty pleas of Edmonds, Trunz and Flaum were as follows:

On 9 October 2018, John Edmonds pleaded guilty to “commodities fraud and a spoofing conspiracy in connection with his participation in fraudulent and deceptive trading activity in the precious metals futures contracts markets”.

Edmonds admitted that:

“from approximately 2009 through 2015, he conspired with other precious metals traders at the Bank to manipulate the markets for gold, silver, platinum and palladium futures contracts traded on the COMEX and NYMEX.”

Notably, Edmonds also:

“admitted that he learned this deceptive trading strategy from more senior traders at the Bank, and he personally deployed this strategy hundreds of times with the knowledge and consent of his immediate supervisors.”

On 25 July 2019, Corey Flaum (who worked with Gregg Smith at Bear Sterns before Smith moved to JP Morgan) pleaded guilty to attempted commodities price manipulation and admitted that:

“between approximately June 2007 and July 2016, [he] placed thousands of orders to manipulate the prices of gold, silver, platinum and palladium futures contracts traded on COMEX and NYMEX.”

Corey Flaum worked at Bear Stearns from 2006 until 2008, and then worked at Scotia Capital from 2010 until 2016.

On 20 August 2019, Christian Trunz, “a former precious metals trader at the London, Singapore and New York offices of JP Morgan” pleaded guilty to conspiracy and spoofing charges. Trunz also admitted that:

“between approximately July 2007 and August 2016, [he] placed thousands of orders that he did not intend to execute for gold, silver, platinum and palladium futures contracts traded on the NYMEX and COMEX).”

Notably, the DoJ says that Trunz admitted that he:

“learned to spoof from more senior traders, and spoofed with the knowledge and consent of his supervisors.”

Trunz is interesting in that he worked at various times in all three locations that JP Morgan’s global trading desk spans, i.e. London, Singapore and New York.

The guilty please of Edmonds, Flaum and Trunz over 2018 – 2019 then allowed the US Department of Justice to move forward with its indictment of Michael Nowak, Gregg Smith and Christopher Jordan, an indictment which was filed on 22 August 2019, and then unsealed on 16 September 2019. In fact, the Nowak – Smith – Jordan indictment was filed only 2 days after Trunz had pleaded guilty.

In its indictment statement of Nowak, Smith and Jordan, the US DoJ said that:

“between approximately May 2008 and August 2016, the defendants [Nowak, Smith and Jordan] and their co-conspirators were members of JP Morgan’s global precious metals trading desk in New York, London and Singapore with varying degrees of seniority and supervisory responsibility over others on the desk.

As it relates to the RICO conspiracy, the defendants and their co-conspirators were allegedly members of an enterprise – namely, the precious metals desk at JP Morgan – and conducted the affairs of the desk through a pattern of racketeering activity, specifically, wire fraud affecting a financial institution and bank fraud.

The indictment alleges that the defendants engaged in widespread spoofing, market manipulation and fraud while working on the precious metals desk at JP Morgan through the placement of orders they intended to cancel before execution (Deceptive Orders) in an effort to create liquidity and drive prices toward orders they wanted to execute on the opposite side of the market.

In thousands of sequences, the defendants and their co-conspirators allegedly placed Deceptive Orders for gold, silver, platinum and palladium futures contracts traded on the NYMEX and COMEX.”

On 14 November 2019, the US DoJ then filed a superseding indictment, which added Jeffery Ruffo to the racketeering conspiracy, along with Nowak, Smith and Jordan.

Then on 29 September 2020, the DoJ announced a bombshell, namely that JP Morgan had agreed to a Deferred Prosecution Agreement (DPA) with the DoJ, specifically that JP Morgan had:

“entered into a resolution with the Department of Justice to resolve criminal charges related to …tens of thousands of episodes of unlawful trading in the markets for precious metals futures contracts” and agreed to “pay over $920 million in a criminal monetary penalty, criminal disgorgement, and victim compensation”.

In the DoJ statement from 29 September 2020, Assistant Director William F. Sweeney Jr of the FBI’s New York Field Office said that”

“For nearly a decade, a significant number of JP Morgan traders and sales personnel openly disregarded U.S. laws that serve to protect against illegal activity in the marketplace.”

“According to admissions and court documents, between approximately March 2008 and August 2016, numerous traders and sales personnel on JPMorgan’s precious metals desk located in New York, London, and Singapore engaged in a scheme to defraud in connection with the purchase and sale of gold, silver, platinum, and palladium futures contracts (collectively, precious metals futures contracts) that traded on the COMEX and NYMEX.”

In the Deferred Prosecution Agreement (DPA), “JPMorgan” was defined as “JP Morgan and its subsidiaries JPMorgan Chase Bank, N.A. (JPMC), and J.P. Morgan Securities LLC (JPMS) and their subsidiaries and affiliates, and their officers, directors, employees and agents.”

The DoJ statement from 2020 also referred to the next stage of the investigation, saying that the DOJ “obtained a superseding indictment” against Nowak, Smith, Jordan and Ruffo which charges them “for their alleged participation in a racketeering conspiracy and other federal crimes in connection with the manipulation of the precious metals futures contracts markets”.

Which illustrates nicely for those who might not know that the ongoing trial of Nowak, Smith and Ruffo in July 2022 is part of the same criminal investigation which JP Morgan bought its way out of for US$ 920 million in 2020.

Which brings us right back to the central question, a.k.a. the elephant in the room, which is, given that JPMorgan’s precious metals desk located in New York, London, and Singapore was manipulating the prices of gold, silver, platinum and palladium for more than 8 years between 2008 to 2016, then why is JP Morgan still even allowed near the precious metals markets in London, Singapore and New York, let alone allowed to dominate these markets with the blessing of the organizations which administer these markets, namely the LBMA and SBMA and COMEX?

* * *

London – JP Morgan and the LBMA

Let’s take a look at what I mean. Despite its criminal activities and precious metals price manipulation, JP Morgan is still one of the most powerful members of the London Bullion Market Association (LBMA) and one of the most dominant banks active in the London gold and silver and platinum and palladium markets.

Despite its crimes and manipulations, there are currently (as of July 2022) three JP Morgan entities that are members of the LBMA. These entities are JP Morgan Chase Bank which is a Market making member of the LBMA, JP Morgan Securities Plc which is a full member of the LBMA, and JP Morgan AG (Germany) which is also a full member of the LBMA.

JP Morgan Chase Bank NA (London branch) is also one of 16 direct participants in the daily LBMA Gold Price auctions, auctions which set a gold price which is used daily in everything from ETF valuations, to mine sales contracts, to valuing billions of dollars of derivatives contracts, such as swaps and options.

Similarly, JP Morgan Chase Bank NA (London branch) is also one of 13 direct participants in the daily LBMA Silver Price auctions.

But there’s more, JP Morgan is one of only 4 members of London Precious Metals Clearing Limited (LPMCL) , a private company which runs the entire paper precious metals clearing system in London. In fact, JP Morgan was one of the founding members of LPMCL in 2001. See the BullionStar article here for background.

There are 2 current active directors of LPMCL from JP Morgan, namely Mark Amlin and Andrew Lovell.

In fact, LPMCL’s correspondence address is at the LBMA’s headquarters at 7th Floor, 62 Threadneedle Street in the City of London, i.e. the LBMA and LPMCL share the same office!

In precious metals vaulting, JP Morgan is also one of the 3 bank custodians which operate a vault in the LBMA London market (the other vault custodians which are the banks HSBC and ICBC Standard). The security operators Brinks, Malca Amit and Loomis also run LBMA vaults in London.

This previously secret JP Morgan vault is located under a JP Morgan building between Carmelite Street and John Carpenter Street in the City of London, as explained in February 2013 here.

JP Morgan Chase Bank is also a market making member of the London Platinum and Palladium Market (LPPM). In addition, J P Morgan Securities plc and J P Morgan SE are associate Members of the LPPM.

But wait. There is even more. JP Morgan is also active on a number of LBMA committees. There is one JP Morgan representative, Andrew Lovell, on the LBMA’s Physical Committee. This committee “is responsible for monitoring, developing and protecting the Good Delivery List”. There is also one JP Morgan representative, Declan McKeever, on the LBMA Regulatory Affairs Committee.

The LBMA also runs a few other working groups, one of which is the deliciously titled “LBMA Financial Crime Working Group.” Presumably JP Morgan is not in this group, but there again, perhaps they actually run it, and use the forum to share their practical experience, such as precious metals trade spoofing and fraud, with the rest of the members.

But the icing on the cake has to be that on the day when the US DoJ unsealed its indictment against JP Morgan’s global precious metals desk head Michael Nowak on 16 September 2019, Nowak was still a board member of the LBMA. See BullionStar article “LBMA Board Member & JP Morgan Managing Director Charged with Rigging Precious Metals” from 17 September 2019.

You can’t make this up. Then a few days after the DoJ’s 16 September 2019 announcement, the LBMA was no longer able to keep its head buried in the sand and was forced to remove Nowak from the LBMA Board. See BullionStar article “LBMA Removes JP Morgan’s Michael Nowak from the LBMA Board” from 20 September 2019.

So why is a bank whose precious metals traders manipulated prices for over 8 years, and in the words of the US DoJ, defrauded customers through “thousands of instances of unlawful trades” that “openly disregarded U.S. laws that serve to protect against illegal activity in the marketplace” still allowed to be a member of the LBMA and to practically dominate the London precious metals markets?

Everything that JP Morgan’s precious metals traders did from 2008 to 2016 while manipulating the prices of gold and silver and platinum and palladium is in breach of the principles of the Financial Services Authority handbook such as Principle 1 (Integrity), Principle 2 (Due skill, Care and Diligence), Principle 5 (Market Conduct), as well as in breach of the LBMA code of conduct in the form of the Bullion Market annex of the Non-Investment Products (NIPs) code which the LBMA was involved in drawing up, and which was in force before it was replaced by the LBMA Global Precious Metals Code in 2017. A copy of the NIPs code can be seen here – the-non-investment-products-code.

In essence, Why have the LBMA and the LPPM not kicked JP Morgan out of their associations? Has the LBMA no moral compass or ethics? Additionally, why does the Bank of England observer on the LBMA Board, Andrew Grice, not call for JP Morgan to be immediately ejected from the London Bullion Market Association (LBMA) and the London Platinum and Palladium Market (LPPM) and permanently banned from trading, clearing and vaulting gold, silver, platinum and palladium in London?

Perhaps it has something to do with the fact that, through Morgan Guaranty Trust Company of New York, JP Morgan was one of the 6 founding members of the London Bullion Market Association (LBMA) in November 1987.

If you look at the 1987 Memorandum of Association of the LBMA, you will even see that it is signed by Guy Field of JP Morgan, who was at the time global head of the JP Morgan bullion department, and who became the founding vice chairman of the LBMA. See also BullionStar article here about the LBMA’s founding.

So is the LBMA merely a cartel front for JP Morgan and its fellow bullion banks to control the global precious metals markets with JP Morgan pulling the strings?

Singapore – JP Morgan and the SBMA

Speaking of the founding members of bullion market associations, most people do not realize that the tentacles of the JP Morgan octopus stretch even to Singapore, where, the Singapore Bullion Market Association (SBMA) was … wait for it… co-founded by JP Morgan in 1993. I kid you not.

Specifically, the Singapore Bullion Market Association (SBMA) was founded by Tim Gardiner of JP Morgan and Kerr Cruikshank of the World Gold Council (aka the World Paper Gold Council).

Tim Gardiner of JP Morgan was even the founding chairman of the SBMA. Here’s a video of Tim Gardiner actually confirming these facts.

Current SBMA CEO, Albert Cheng also confirms these facts in a SBMA article from 5 June 2019 where he says:

“In 1993, the Singapore government announced the implementation of the Goods & Services Tax (GST) scheme to all business transactions. In response, JP Morgan and the World Gold Council felt it was necessary to form an industry forum of bullion market participants to lobby the government for concessions for gold trading businesses dealing in physical transactions, hence the birth of SBMA.”

Fast forward to more recent times, and in March 2018, Gordon Cheung, who was previously a managing director of Bear Sterns and an executive director of JP Morgan, was appointed as deputy director of the SBMA.

Right now, JP Morgan representatives are also on the SBMA management committee. A JP Morgan South East Asia (SEA) Ltd managing director, Amar Singh, is currently a member of the SBMA’s management committee . Prior to Singh, Stephen Jani, a managing director of JP Morgan Global Commodities, was the JP Morgan member of the SBMA management committee from 2017 to 2019.

And prior to Jani, the JP Morgan representative on the SBMA management committee was Harshika Patel, another managing Director of JP Morgan Global Commodities. Patel was also on the SBMA’s Public Affairs Committee (PAC) at that time.

Currently, JP Morgan SEA Ltd is also on the SBMA Good Delivery List committee.

In fact, JP Morgan is in the most prestigious membership category of the SBMA, namely a Category 1 member. Apart from JP Morgan, only one other bank, ICBC Standard Singapore branch, is a category 1 member of the SBMA. Not surprisingly the World Gold Council (the other co-founder of the SBMA) got a free pass to also be defined as a category 1 member of the SBMA.

To qualify as Category 1 bank members of the SBMA –

“Category 1 Members which are banks and financial institutions must satisfy the “Fit and Proper” criteria specified in the MAS “Guidelines on Fit and Proper Criteria” (FSG-G01) as may be amended from time to time and have a track record in the bullion industry for a period of at least 3 years. “

MAS is the Monetary Authority of Singapore. So what are the MAS Fit and Proper criteria for banks?

According to the MAS document titled “Guidelines on Fit and Proper Criteria” which apply to ‘Relevant Persons’ (i.e. all financial entities including banks):

“2. MAS expects a relevant person to be competent, honest, to have integrity and to be of sound financial standing….This also underpins our requirements that the relevant person performs the activities regulated under the relevant legislation efficiently, honestly, fairly and acts in the best interests of its or his stakeholders and customers.”

“8 The criteria for considering whether a relevant person is fit and proper include but are not limited to the following:

(a) honesty, integrity and reputation;

(b) competence and capability; (c) financial soundness”

“13 Honesty, Integrity and Reputation

The factors set out in the following paragraphs are relevant to the assessment of the honesty, integrity and reputation of a relevant person. The factors include but are not limited to whether the relevant person:

(c) has been censured, disciplined, suspended or refused membership or registration by MAS or any other regulatory authority, an operator of a market, trade repository or clearing facility, any professional body or government agency, whether in Singapore or elsewhere;

(e) has been the subject of any proceedings of a disciplinary or criminal nature or has been notified of any potential proceedings or of any investigation which might lead to those proceedings, under any law in any jurisdiction;

(g) has had any judgment (in particular, that associated with a finding of fraud, misrepresentation or dishonesty) entered against the relevant person in any civil proceedings or is a party to any pending proceedings which may lead to such a judgment, under any law in any jurisdiction;

(h) has accepted civil liability for fraud or misrepresentation under any law in any jurisdiction;

Based on it’s own extensive criteria of “Fit and Proper”, JP Morgan fails all of these tests, where “for nearly a decade” between March 2008 and August 2016, as the US Department of Justice stated, ”a significant number of JP Morgan traders and sales personnel” from “JPMorgan’s precious metals desk located in New York, London, and Singapore” engaged in “racketeering activity” through a “criminal enterprise”, and engaged in “widespread spoofing, market manipulation and fraud” and engaged in “a scheme to defraud in connection with the purchase and sale of gold, silver, platinum, and palladium futures contracts (collectively, precious metals futures contracts) that traded on the COMEX and NYMEX.”

So why has Singapore’s MAS not acted against JP Morgan? And why does the Singapore Bullion Market Association (SBMA), knowing that JP Morgan rigged precious metals prices and conducted fraud for over 8 years while paying $920 million in a deferred prosecuted agreement with the US DoJ and the US CFTC, still allow JP Morgan to be a member of the SBMA, let alone still allow JP Morgan representatives on to the SBMA Management Committee? Enquiring minds would like to know.

USA – JP Morgan and COMEX

Finally, let’s go back to the commodity futures exchanges on which the criminal activities of JP Morgan have been proven to have taken place – the Commodity Exchange (COMEX) and the New York Mercantile Exchange (NYMEX). Surely the owners and governors of COMEX and NYMEX have kicked out JP Morgan from continuing to operate on their exchanges?

Wrong!

Despite during 2020 admitting criminal wrongdoing and paying a criminal monetary penalty of US $ 920 million to the DoJ and CFTC for engaging “in a scheme to defraud in connection with the purchase and sale of gold, silver, platinum, and palladium futures contracts (collectively, precious metals futures contracts) that traded on the New York Mercantile Exchange Inc. (NYMEX) and Commodity Exchange Inc. (COMEX), which are commodities exchanges operated by the CME Group, Inc”, JP Morgan is still one of the largest traders of COMEX precious metals futures contracts.

JP Morgan is also a COMEX approved depository (vault storage provider) for the storage of gold, silver, platinum and palladium used in the settlement of COMEX futures contracts.

Not only that, but the JP Morgan vault in New York holds the largest amounts of gold, silver, platinum and palladium listed on the COMEX inventory reports, compared to any other COMEX approved vault.

JP Morgan’s COMEX vault is located in the 5th basement level (basement B5) under 1 Chase Manhattan Plaza (across the street from the New York Federal Reserve’s gold vault at 33 Liberty Street). As explained in March 2013.

Through JP Morgan Securities LLC, JP Morgan is also one of the largest clearing firms of COMEX and NYMEX and an authorized clearing member of COMEX and NYMEX.

In addition, JP Morgan (along with Citibank) together hold 90% of all gold and other precious metals derivatives held by all US banks. See here for discussion.

Why has the COMEX Board of Governors not disciplined and expelled JP Morgan from any and all involvement in COMEX, let alone allowing JP Morgan to continue to be one of the largest traders and clearers on COMEX and the largest approved vault operator of a COMEX vault?

After all, there is an entire section in the By-Laws of COMEX covering Disciplinary proceedings, specifically Article 8. See here.

Also, why did the CME “Market Surveillance” team, which is “responsible for protecting the economic functioning of exchange markets by ensuring the markets are free from manipulation” by “detecting, deterring, and preventing market manipulation”, never pick up on JP Morgan’s 8 years of criminal manipulation of COMEX gold, silver, platinum and palladium futures prices?

Now that the US Department of Justice has done so, why has CME Group (owner of the COMEX and NYMEX) not prohibited JP Morgan from operating on the COMEX and NYMEX given that JP Morgan broke all the rules in its criminal manipulation of gold and silver and platinum and palladium futures contracts on COMEX and NYMEX over an 8 year period?

This article has drawn together the various pieces of the investigation into JP Morgan’s precious metals manipulation in New York and London and Singapore, and the prosecutions and deferred prosecutions so far, as well as the ongoing trial of Nowak & Co, so as to then show that JP Morgan is still not only active in the precious metals markets in these financial centers, but actually still at the heart of the LBMA and the SBMA and the COMEX, where in all 3 cases it is welcomed with open arms.

The latest revelations from the current Chicago federal trial of Michael Nowak, Gregg Smith and Jeffery Ruffo are startling. According to Smith’s colleague at JP Morgan, Christian Trunz, who gave evidence to the jury on 19 July 2022,

“Gregg Smith clicked his computer mouse so rapidly to place and cancel bogus gold and silver orders for Bear Stearns Cos. and later JPMorgan Chase & Co. that his colleagues would joke that he needed to put ice on his fingers to cool them down afterward, or that he must be double-jointed.”

Since JP Morgan’s global precious metals trading desk spans the 3 locations of New York, London, and Singapore, it’s reasonable to assume that it employs a follow the sun model, in which case the trade book of the desk would be carried around the clock between the 3 locations. If that is the case, the trading teams in London and Singapore would know the trades of JP Morgan’s New York traders. So this begs the question, what are the UK’s Financial Conduct Authority (FCA) and Singapore’s Monetary Authority (MAS) going to do if or when Nowak, Smith, Ruffo and Jordan are found guilty? Open up investigations of their own into the London and Singapore arms of JP Morgan’s global precious metals trading desk?

And how will the LBMA, SBMA and COMEX react if or when the next batch of JP Morgan precious metals traders are found guilty? Will it continue to be business as usual? The answer unfortunately is probably yes.

* * *

This article was originally published on the BullionStar.com website under the same title “Despite manipulating precious metals prices, JP Morgan is still at the heart of the LBMA, SBMA and COMEX”.

END

5.OTHER COMMODITIES: EGGS

Egg Prices Sky-High As Breakfast Inflation Pressures American Households

FRIDAY, JUL 22, 2022 – 01:40 PM

It’s no secret that breakfast food is more expensive than a year ago, yet another sign of how the cost-of-living crisis squeezes American household budgets.

According to the Bureau of Labor Statistics, the Consumer Price Index shows food at home prices climbed 10.4% in June over the past year.

Breakfast is supposed to be the most affordable meal of the day — but as we’ve explained (read: here & here), soaring prices for coffee, milk, sugar, wheat, oats, eggs, and orange juice have transformed breakfast into a costly meal.

Focusing on eggs, once considered the cheapest source of protein, has seen wholesale prices for a dozen large eggs more than triple in one year.

As if inflation wasn’t enough, one of the worst-ever bird flu outbreaks resulted in the death of more than 30 million commercial and wild birds, reducing egg production capacity.

The good news is that Cal-Maine Foods, Inc., the largest US fresh egg producer, said in a recent earnings statement the bird flu outbreak appears to be waning as no infections have been reported in its flocks since early June.

With inflation broad-based, June’s overall CPI print was hotter than expected at 9.1%, up half a percentage point from last month and the highest since 1981. Looking at this in another way to capture economic distress felt by everyday people is the “misery index” — which combines US labor force participation with CPI – hasn’t been this high since the stagflationary period more than four decades ago.

Last Friday, disappointing retail sales sparked some concern that consumers are tapped out.

Meanwhile, the White House, through President Biden’s Twitter account, called the latest inflation figures “not acceptable.” They noted consumers had saved 40 cents per gallon over the past month. Despite the savings at the pump, Biden’s polling data has yet to reverse from record lows.

Americans are waking up to the lies the Biden administration pushed about “transitory” inflation and how they openly lied this entire time.

Combine skyrocketing breakfast costs with elevated gas prices at the pump; no wonder consumers are miserable. People will vote with their empty wallets come November’s midterm elections.

END

COMMODITIES IN GENERAL/

END

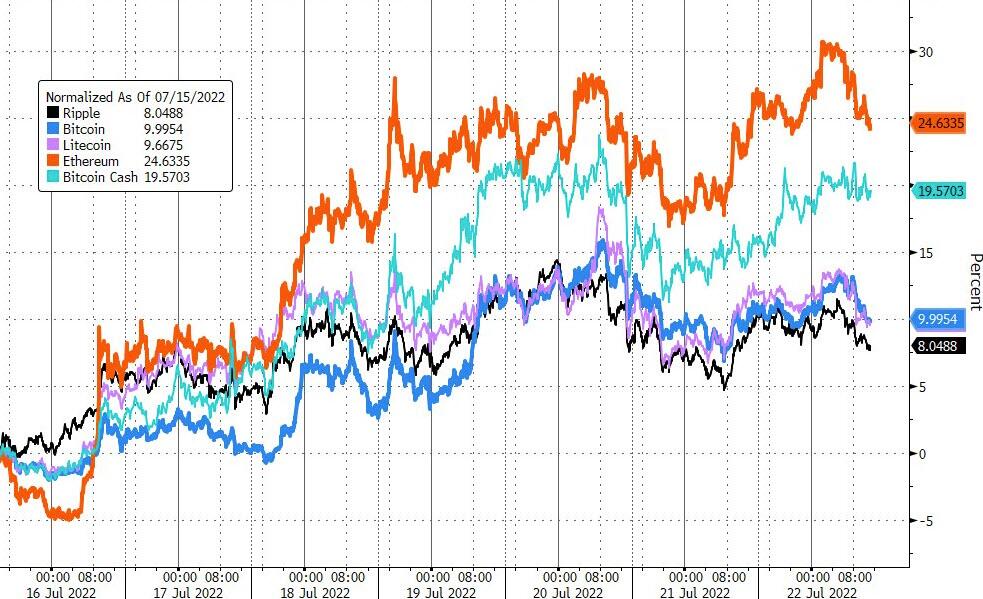

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.7583

OFFSHORE YUAN: 6.7613

HANG SANG CLOSED UP 34.51 PTS OR 0.17%

2. Nikkei closed UP 111.66 OR 0.40%

3. Europe stocks CLOSED ALL GREEN

USA dollar INDEX DOWN TO 106,80/Euro FALLS TO 1.0178

3b Japan 10 YR bond yield: FALLS TO. +.213/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 136.88/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP -// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.045%/Italian 10 Yr bond yield RISES to 3.40% /SPAIN 10 YR BOND YIELD FALLS TO 2.27%…

3i Greek 10 year bond yield FALLS TO 3.28//

3j Gold at $1725.60 silver at: 18.83 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 1/100 roubles/dollar; ROUBLE AT 57.73

3m oil into the 95 dollar handle for WTI and 103 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 136.88DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9649– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9819well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

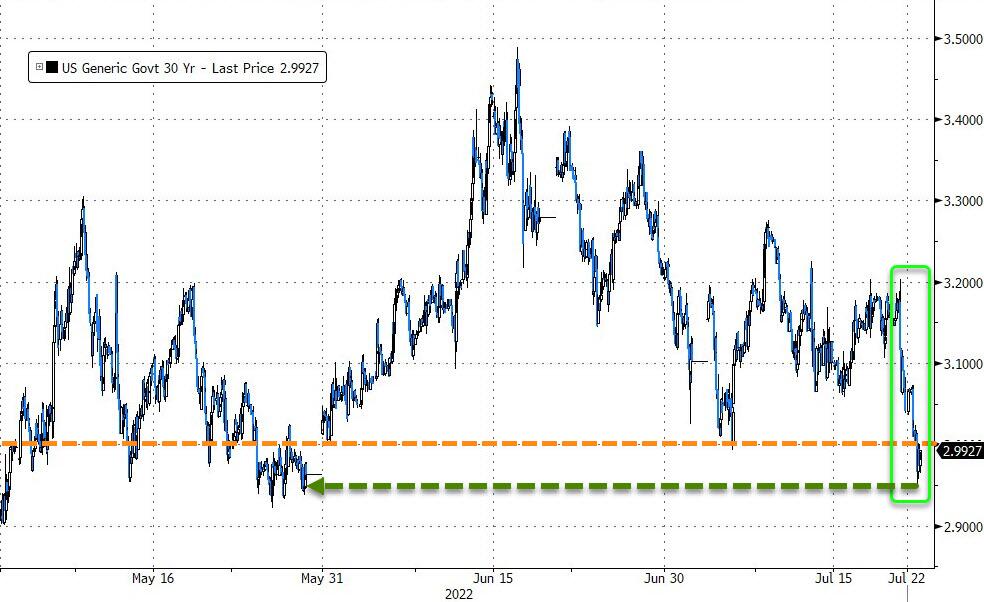

USA 10 YR BOND YIELD: 2.801 DOWN 11 BASIS PTS

USA 30 YR BOND YIELD: 3.008 DOWN 7 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.76

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

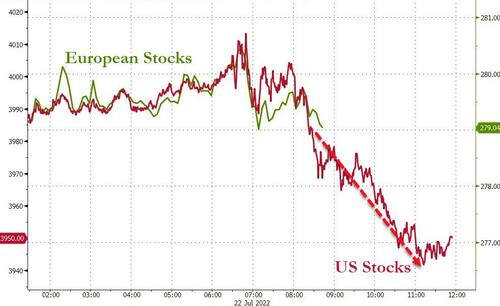

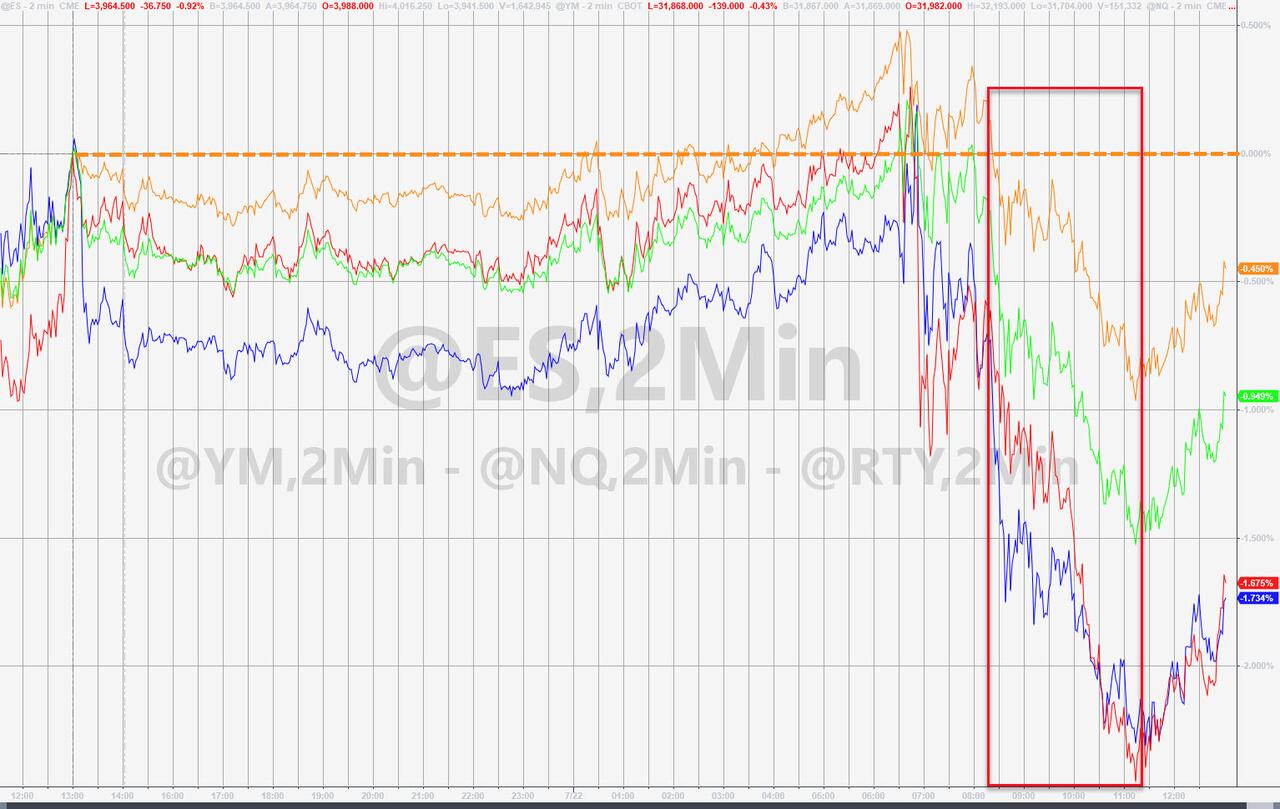

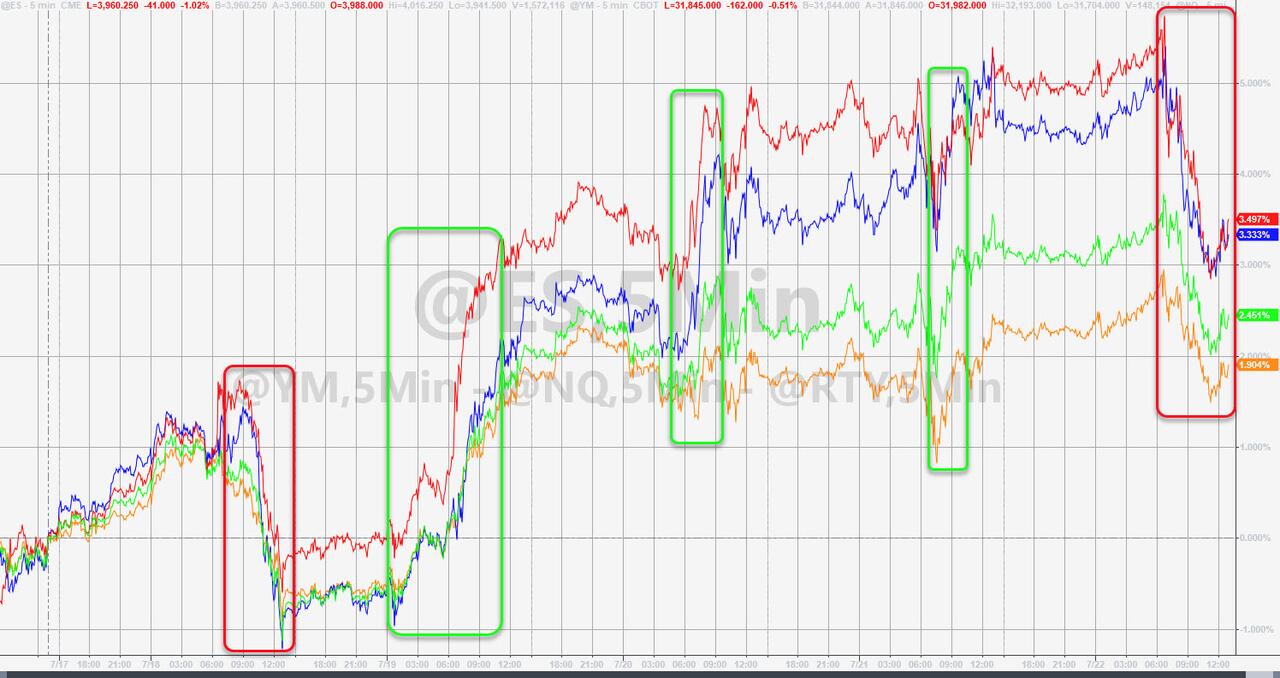

Futures Rally Fizzles After Volley Of Disappointing Earnings And Economic News

FRIDAY, JUL 22, 2022 – 07:59 AM

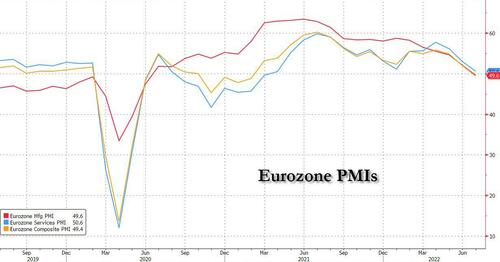

US futures were flat (bouncing off session lows), and a rally in tech stocks reversed after three days of gains as recessionary PMI data out of Europe and disappointing results from COF, CRSR, SAM, SIVB, STX and others raised concerns about sliding corporate profits amid slowing economic growth. Contracts on the Nasdaq 100 were down 0.5% as 7:30am in New York, while S&P futures ticked 0.3% lower, but are on pace to close the week more than 3% higher after solid rallies in the past two days.

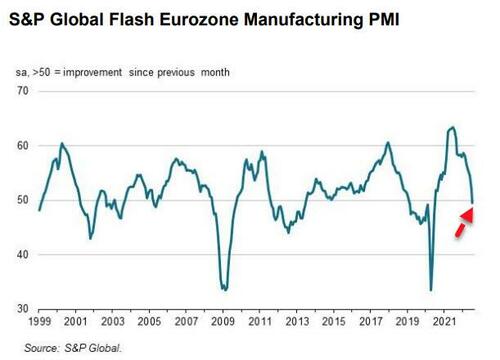

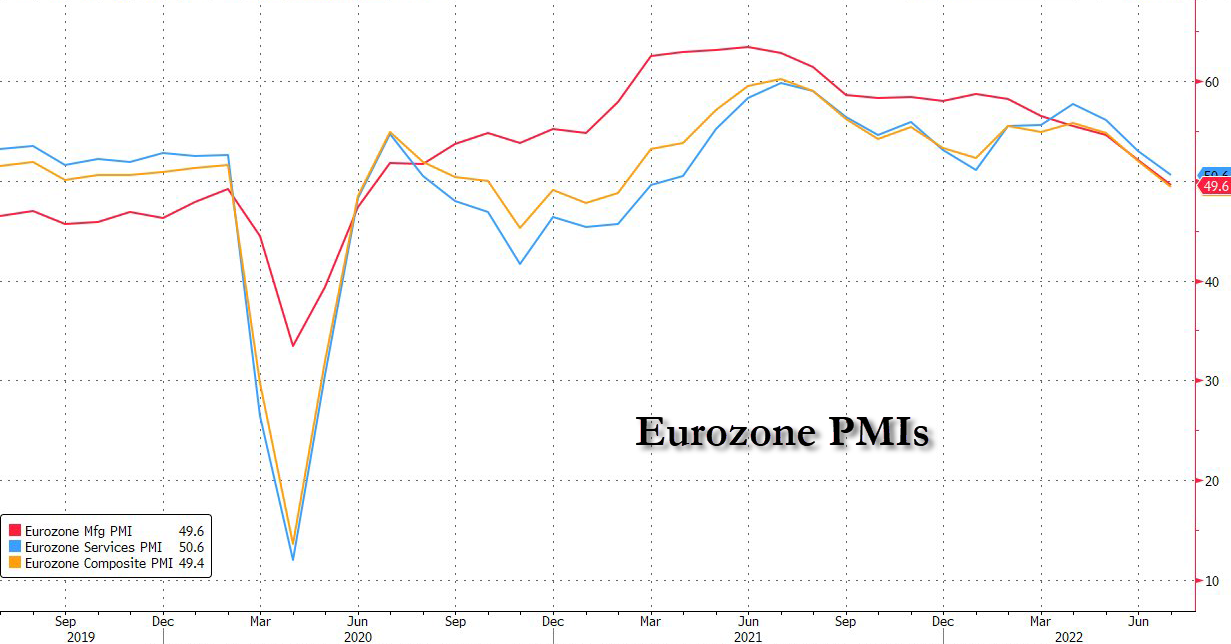

Europe’s Stoxx 600 Index added 0.5%, poised for a weekly advance as investors shrugged off worries about the economic outlook prompted by the worst Euro Area PMI data which dropped to a 17-month low in July, dipping beneath the level that signals a contraction, and confirming Europe has entered a recession. The downturn was driven by worsening output among manufacturers and a near-stalling of service-sector growth. Economists had expected a mild expansion.

Despite the dismal European economic data, global stocks remain on course for their best week in a month, paring this year’s equity market rout to about 18% amid speculation that the world is headed for a recession which will force central banks to end their tightening earlier than expected. Earnings have been a mixed bag so far in Q2, with the scandal-plagued Twitter due to report results later.

“Q2 earnings were seemingly not as bad as feared,” Mizuho International Plc strategists Peter McCallum and Evelyne Gomez-Liechti wrote in a note to clients. “That said, tech giants announced spending cuts and a hiring slowdown. Consumer firms lowered this year’s guidance.”

In premarket trading, Snap shares plunged 28% as the company reported missed its already slashed guidance and removed guidance, roiled partly by a major slowdown in ad spending. Other social media-linked stocks, including Facebook-owner Meta Platforms, Google-parent Alphabet and Twitter, also fell. Meanwhile, Seagate Technology shares are down 13% in premarket trading, after the computer hardware and storage company issued a weak forecast for the current period. Intuitive Surgical shares plunged 12% in US premarket trading after the company’s second-quarter profit and revenue both missed the average analyst estimate. At least four analysts cut their PTs on the surgical systems maker, noting the capital concerns and macro headwinds that weighed on the performance. Verizon slumped more than 2% after the company slashed its FY adj EPS range from $5.40-$5.55 to $5.10-$5.25.It wasn’t all bad news: American Express jumped after reporting that spending on its network soared, leading the firm to raise its forecast for full-year revenue.

“The Snap results came as a warning for other Big Tech names that rely on ad revenue,” said Ipek Ozkardeskaya, senior analyst at Swissquote. “The results could reverse appetite for at least a couple of them, including Google and Meta before the closing bell.”

These technology heavyweights, which led the rally in US stocks following the pandemic-driven slump in early 2020, have been among the biggest decliners this year as the Federal Reserve began an aggressive cycle of interest rate increases. The tech sector has been particularly vulnerable as higher rates mean a bigger discount for the present value of future profits, hurting growth shares with the highest valuations. With the Fed expected to announce another hike at its meeting next week, focus has been on the second-quarter earnings season for clues on how companies are holding up amid surging inflation and a possible looming recession.

In Europe, the Euro Stoxx 50 rose 0.5%. IBEX outperforms peers, adding 0.6%, FTSE 100 is flat but underperforms peers. Travel, real estate and utilities are the strongest performing Stoxx 600 sectors. Here are some of the biggest European movers today:

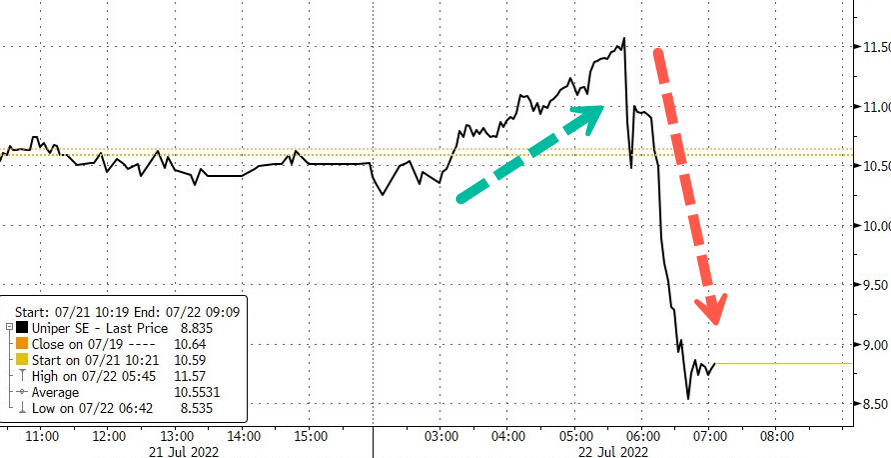

- Uniper shares were volatile after Germany confirmed the rescue package for the utility. The shares pared earlier gains of as much as 11% to briefly turn negative. Majority-owner Fortum rose as much as 13%.

- Delivery Hero shares surge as much as 21%, the most since December 2019, after lifting full-year adjusted Ebitda margin target.

- Beazley shares jump as much as 13% to the highest in more than two years after an upgrade to profit guidance driven by cyber insurance.

- Sinch shares jump as much as 15% following a volatile run for the cloud messaging platform firm, with Handelsbanken saying its recent results contained few positive surprises but that there are good operational signs.

- Stora Enso shares fall as much as 9.8%, the most since May, after a quarterly update analysts say looks somewhat soft, with a miss on earnings for the Finnish packaging and forestry group.

- Lonza shares fall as much as 3.4% after it reported 1H results. While noting the Swiss company is a “structural long- term growth story,” the lack of an upgrade to 2022 outlook may leave some disappointed, Jefferies says.

- Aston Martin shares fall as much as 13%, paring the gains of the past week, as Jefferies says the announced boost to the company’s capital structure leaves open questions, with the stock likely to remain “volatile” in coming weeks.

- Temenos shares drop as much as 7.7%. 2Q results missed estimates and analysts anticipate investors may be skeptical that the software firm will be able to hits its confirmed FY guidance.

- Electrolux Professional shares fall as much as 6.5%, after component shortages eroded the appliance manufacturer’s margins in the second quarter.

Earlier in the session, Asian stocks headed for the biggest weekly gain in four months as renewed optimism in Chinese technology shares helped offset downbeat sentiment triggered by a disappointing earnings report by Snap Inc. The MSCI Asia Pacific Index was poised for a slight gain Friday, maintaining a weekly rally of more than 3%. Shares in Hong Kong edged higher, with a gauge tracking China’s technology sector posting a three-day gain, while Japanese stocks also gained. Investors are looking anew at China’s tech sector after Beijing wrapped up a year-long probe into ride-hailing giant Didi Global Inc., which was fined $1.2 billion. Sentiment has improved as US chipmaker stocks staged a stunning rebound on evidence that supply-chain issues are easing and demand is growing.

Asian stocks are up less than 1% so far this month after slumping almost 7% in June, the market’s worst month in over two years, as traders pared expectations of aggressive monetary tightening by the US Federal Reserve and as the dollar softened. “Recession risks have definitely risen in the developed markets, but one of the bright spots that we’re seeing is really in places like Asia ex-Japan, where a lot of economies are still continuing to reopen pretty strongly,” Clara Cheong, global market strategist at JPMorgan Asset Management, told Bloomberg TV. Expectations China will rebound in the second half should “help to bolster Chinese equity markets and the broader Asia ex-Japan region,” Cheong said.

Japanese equities erased earlier losses as investors assessed US earnings results amid economic uncertainty. The Topix index rose 0.3% to 1,955.97 as of the market close in Tokyo, while the Nikkei 225 advanced 0.4% to 27,914.66. Keyence Corp. contributed the most to the Topix’s gain, increasing 3%. Out of 2,170 shares in the index, 1,147 rose and 865 fell, while 158 were unchanged. “Strong US markets were a supporting factor for Japanese stocks today,” said Masahiro Ichikawa, chief market strategist at Mitsui DS Asset Management

Key stock gauges in India completed their best weekly performance since early-February 2021 as foreign funds turned buyers. The S&P BSE Sensex rose 0.7% to 56,072.23 in Mumbai, taking its weekly gain to 4.3%. The NSE Nifty 50 Index also rose 0.7% Friday. Nine of the 19 sectoral indexes compiled by BSE Ltd. advanced, led by a gauge of lenders. Foreigners net-bought more than $1 billion of local stocks this week through July 20, after 15 straight weeks of net selling. Read: After $30 Billion Exodus, Global Money Trickles Back Into India The decline in crude oil prices and rebound in foreign inflows helped the Sensex to close above 56,000, Amol Athawale, vice president at Kotak Securities, wrote in a note. “The fear of aggressive rate hikes by both the US Fed and RBI seems to be moderating, which is giving investors some room to lap up stocks of companies with good fundamentals,” Athawale said. In earnings, Reliance Industries Ltd., India’s biggest company by market value, is scheduled to announce results later Friday. Infosys, Kotak Mahindra Bank and ICICI Bank are due to report their results over the weekend.

In FX, the euro turned lower, pushing the Bloomberg Dollar Index to only its second daily advance this week after flash PMI data in France, Germany and the euro zone as a whole disappointed. The euro dropped as much as 1% to $1.0130. UK readings were in line with expectations. CAD and CHF are the strongest performers in G-10 FX, EUR and DKK underperform.

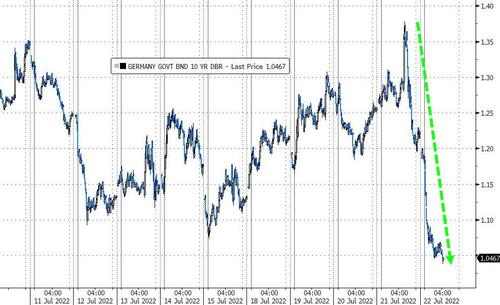

In rates, Treasuries were richer across the curve, following wider rally seen in bunds after flash PMI data in France, Germany and the eurozone as a whole disappointed and entered contraction territory. US yields richer by up to 6.5bp across 5-year sector, tightening the 2s5s30s fly byb 6.5bp on the day, adding to Thursday’s belly-led gains. US 10-year yields around 2.82%, richer by 5.5bp on the day with bunds outperforming by ~10bp in the sector. Three-month dollar Libor -1.67bp at 2.76629%. IG dollar issuance slate empty so far; Thursday saw a quiet session for issuance, following a rush of deals seen at the start of the week.

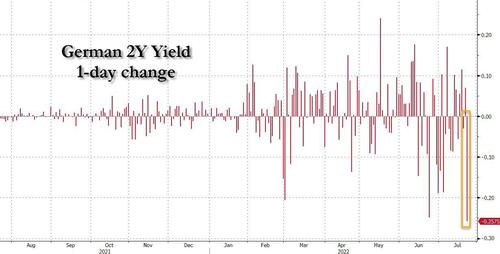

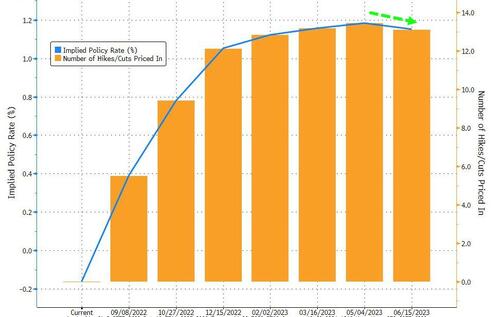

European bonds also rallied, led by the short-end, with 2-year German bond yields falling as much as 25 basis points to 0.42%, its biggest plunge since 2008 on expectations a recession is now unevitable; money markets traders no longer fully price in a 50-basis-point ECB hike in September. Peripheral spreads are mixed to Germany; Italy tightens, Spain and Portugal widen.

In commodities, crude futures dropped 2% erasing an earlier gain after the catastrophic european economic data. Most base metals trade in the green; LME aluminum rises 1.5%, outperforming peers. LME tin lags, dropping 0.9% Spot gold is little changed at $1,718/oz

Bitcoin remains bid and has eclipsed the USD 23.5k mark at best, though this was brief and it has since waned marginally.

Looking to the day ahead, and the main data highlight will be the global flash PMIs for July. Otherwise, we’ll hear from the ECB’s Villeroy. Earnings releases include Verizon Communications, NextEra Energy, American Express and Twitter.

Market Snapshot

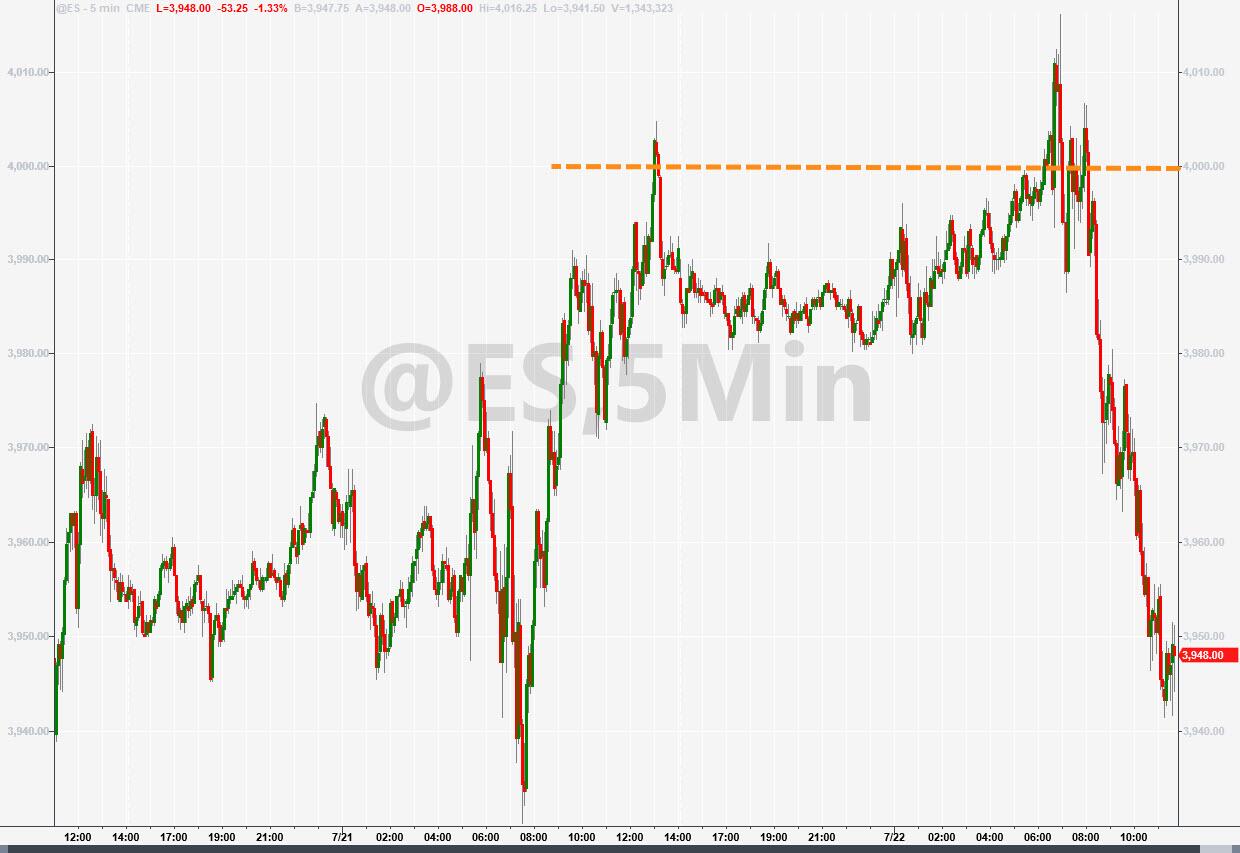

- S&P 500 futures down 0.3% to 3,987.25

- STOXX Europe 600 up 0.3% to 425.79

- MXAP up 0.2% to 159.10

- MXAPJ little changed at 521.40

- Nikkei up 0.4% to 27,914.66

- Topix up 0.3% to 1,955.97

- Hang Seng Index up 0.2% to 20,609.14

- Shanghai Composite little changed at 3,269.97

- Sensex up 0.7% to 56,083.03

- Australia S&P/ASX 200 little changed at 6,791.50

- Kospi down 0.7% to 2,393.14

- German 10Y yield little changed at 1.07%

- Euro down 0.7% to $1.0157

- Gold spot up 0.0% to $1,719.20

- U.S. Dollar Index up 0.21% to 107.14

Top Overnight News from Bloomberg

- Private-sector activity in the euro area unexpectedly shrank for the first time since the pandemic lockdowns of early 2021, adding to signs that a recession might be on the horizon. A survey of purchasing managers by S&P Global dropped to a 17- month low in July, dipping beneath the level that signals contraction.

- US social-media giants shed nearly $47 billion in market value in extended trading Thursday, as disappointing revenue from Snap Inc. raised concerns about the outlook for online advertising.

- Former President Donald Trump ignored pleas to call off the mob storming the US Capitol and remained publicly silent as he watched the violence unfold on television from his personal dining room off the Oval Office, according to evidence and testimony to the committee investigating last year’s insurrection.

- US equity futures fell Friday and Asian stocks wavered after disappointment over technology earnings stoked worries about the economic outlook and took some of the shine off this week’s global equity rebound.

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mostly higher after the gains in the US but with upside capped by lingering growth concerns. ASX 200 was rangebound near the 6,800 level after PMI data slowed but remained in expansion territory. Nikkei 225 was kept afloat after the recent dovish affirmations from the BoJ and Governor Kuroda but with gains limited amid the COVID situation and with Core Inflation rising by its fastest pace in 7 years. Hang Seng and Shanghai Comp. were mixed amid earnings releases and with suggestions that President Biden could temporarily reduce China tariffs in response to supply chain disruptions and rising inflation.

Top Asian News

- US Democrat Rep. Ami Bera said President Biden could opt for a “temporary reduction” of Trump-era tariffs on China in response to supply chain disruptions and rising inflation, according to Nikkei.

- Hong Kong Faces First Prime Rate Hike Since 2018 on Hawkish Fed

- South Korea Restores Military Drills Once Reduced to Help Trump

- China Says Japan ‘Shall Pay’ If It Handles Fukushima Water Wrong

- Russia Rises With China in Latest Japan Threat Assessment

- UK Politicians Voice Concern Over HSBC China Communist Committee

- Inflation to Drive RBI’s Rate Action Rather Than Rupee, DBS Says

European bourses are resilient despite Flash PMIs for June moving into contractionary territory, with the regions upside perhaps derived from potential less-hawkish ECB implications. Stateside, futures are subdued but have been fairly contained after late Wall St. action and ahead of further key earnings. Sectors are mostly in the green and feature upside in Real Estate and Travel while Banks, Resources and Autos lag.

Top European News