by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1721.05 DOWN $7.85

SILVER: $18.47 DOWN 24 CENTS

ACCESS MARKET:

GOLD $1719.65

SILVER: $18.44

We are now entering options expiry for Comex (tomorrow) and OTC/LBMA (Friday)

Bitcoin morning price: $21,998 DOWN 1076

Bitcoin: afternoon price: $21,605. DOWN 1469

Platinum price: closing UP $4.00 to $884.30

Palladium price; closing DONW $2.45 at $2010.50

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JULY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,727.100000000 USD

INTENT DATE: 07/22/2022 DELIVERY DATE: 07/26/2022

FIRM ORG FIRM NAME ISSUED STOPPED

363 H WELLS FARGO SEC 15

661 C JP MORGAN 20 45

690 C ABN AMRO 10

TOTAL: 45 45

MONTH TO DATE: 9,564

no. of contracts issued by JPMorgan: 45/45

_____________________________________________________________________________________

NUMBER OF NOTICES FILED FOR JULY CONTRACT: 45 NOTICES FOR 4500 OZ //1.399 TONNES

total notices so far: 956,400 contracts for 956,400 oz (29.748 tonnes)

SILVER NOTICES:

186 NOTICES FILED FOR 930,000 OZ/

total number of notices filed so far this month 3591 : for 17,955,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $7.85

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD:

TONNES FROM THE GLD///

INVENTORY RESTS AT 1005.87 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 24 CENTS

AT THE SLV// ://HUGE CHANGES IN SILVER INVENTORY AT THE SLV//:A WITHDRAWAL OF 1.383 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 499.101 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 1511 CONTRACTS TO 147,106 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE HUGE GAIN IN OI WAS ACCOMPLISHED DESPITE OUR $0.10 LOSS IN SILVER PRICING AT THE COMEX ON FRIDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.10) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY COMMERCIAL SILVER LONGS//BUT MAINLY WE HAD ADDITIONAL SPECULATOR ADDITIONS AS WE HAD A GIGANTIC GAIN OF 3151 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GIGANTIC ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A POOR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.220 MILLION OZ FOLLOWED BY TODAY’S 250,000 OZ QUEUE JUMP / // V) HUGE SIZED COMEX OI GAIN

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -28

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTACTS for 16 days, total 15,120 contracts: 75.600 million oz OR 4.725 MILLION OZ PER DAY. (945 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 75.6 MILLION OZ

.

LAST 15 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 75.60 MILLION OZ ( LOOKS LIKE ANOTHER LOW ISSUANCE MONTH FOR SILVER)

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1511 DESPITE OUR $0.10 LOSS IN SILVER PRICING AT THE COMEX// FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 1612 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER ADDITIONS ////// HUGE SPECULATOR SHORT ADDITIONS// WE HAVE A POOR INITIAL SILVER OZ STANDING FOR JUNE. OF 15.22 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 250,000 OZ // .. WE HAD AN ATMOSPHERIC SIZED GAIN OF 3123 OI CONTRACTS ON THE TWO EXCHANGES FOR 15.615 MILLION OZ DESPITE THE LOSS IN PRICE..

WE HAD 186 NOTICES FILED TODAY FOR 930,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A VERY STRONG SIZED 9,585 CONTRACTS TO 509,399 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: +485 CONTRACTS.

.

THE STRONG SIZED DECREASE IN COMEX OI CAME DESPITE OUR RISE IN PRICE OF $14.45//COMEX GOLD TRADING/FRIDAY / WE MUST HAVE HAD ADDITIONAL SPECULATOR SHORT ADDITION ACCOMPANYING OUR GOOD SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //AND HUGE SPECULATOR SHORT ADDITIONS//HUGE ADDITIONS TO OUR BANKER LONGS!!

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JULY AT 2.914 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 5,500 OZ

YET ALL OF..THIS HAPPENED WITH OUR STRONG RISE IN PRICE OF $14.45 WITH RESPECT TO FRIDAY’S TRADING

WE HAD A STRONG SIZED LOSS OF 5568 OI CONTRACTS 17.318 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4017 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 509,399

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5568 CONTRACTS WITH 9585 CONTRACTS DECREASED AT THE COMEX AND 4017 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 5568 CONTRACTS OR 17.318 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4017) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (9,585): TOTAL LOSS IN THE TWO EXCHANGES 5568 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT ADDITIONS//STRONG BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JULY. AT 2.914 TONNES FOLLOWED BY TODAY’S 5,000 OZ QUEUE JUMP 3) ZERO LONG LIQUIDATION//HUGE SPECULATOR SHORT COVERINGS/ //.,4) STRONG SIZED COMEX OPEN INTEREST LOSS 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

102,079 CONTRACTS OR 10,207,900 OZ OR 317.50 TONNES 16 TRADING DAY(S) AND THUS AVERAGING: 6380 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES: 317.50 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 317.50/3550 x 100% TONNES 8.96% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 317.50 TONNES (HUGE INCREASE FROM JUNE//WILL CLOSE IN ON THE RECORD EFP ISSUANCE IN MARCH 22//SURPASSED PREVIOUS RECORD HIGH NOV 21)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JULY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GIGANTIC SIZED 1511 CONTRACT OI TO 147,106 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1612 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 1612 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE:1612 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1511 CONTRACTS AND ADD TO THE 1612 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN ATMOSPHERIC SIZED GAIN OF 3123 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 15.615 MILLION OZ

OCCURRED DESPITE OUR FALL IN PRICE OF $0.10

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)MONDAY MORNING// SUNDAY NIGHT

SHANGHAI CLOSED DOWN 19.59 PTS OR 0.60% //Hang Sang CLOSED DOWN 46.20 OR 0.22% /The Nikkei closed DOWN 215.41 OR % 0.77. //Australia’s all ordinaires CLOSED DOWN 0.08% /Chinese yuan (ONSHORE) closed UP AT 6.7455//OFF SHORE CHINESE YUAN UP 6.7520// /Oil UP TO 95.80 dollars per barrel for WTI and BRENT AT 104.26// SHANGHAI CLOSED DOWN 19.59 PTS OR 0.60% //Hang Sang CLOSED DOWN 46.20 OR 0.22% /The Nikkei closed DOWN 215.41 OR % 0.77. //Australia’s all ordinaires CLOSED DOWN 0.08% / Stocks in Europe OPENED ALL GREEN ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A VERY STRONG SIZED 9,585 CONTRACTS TO 509.389 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS STRONG COMEX DECREASE OCCURRED DESPITE OUR RISE OF $14.45 IN GOLD PRICING FRIDAY’S COMEX TRADING. WE ALSO HAD A GOOD SIZED EFP (4,017 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY.. THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4017 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :4017 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4017 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED SIZED TOTAL OF 5568 CONTRACTS IN THAT 4017 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 9,585 CONTRACTS..AND THIS STRONG LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR GOOD SIZED RISE IN PRICE OF GOLD $ 14.45. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING JULY (29.800),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.800 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $14.45) AND WERE UNSUCCESSFUL IN KNOCKING OFF SOME SPECULATOR LONGS/COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO COVER TO THEIR POSITIONS//// WE HAVE REGISTERED A STRONG SIZED LOSS OF 17.318 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR JULY (29.800 TONNES)…

WE HAD +484 CONTRACTS ADDED TO COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 5568 CONTRACTS OR 556,800 OZ OR 17.318 TONNES

Estimated gold volume 219,298/// poor/

final gold volumes/yesterday 284,565 / fair

INITIAL STANDINGS FOR JULY ’22 COMEX GOLD //JULY 25

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 69,639.071oz JPMorgan Manfra 2166 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | 16,979.280 oz Brinks (525 kilobars) |

| No of oz served (contracts) today | 45 notice(s) 4500 OZ 1.399 TONNES |

| No of oz to be served (notices) | 17 contracts 1700 oz 0.05287 TONNES |

| Total monthly oz gold served (contracts) so far this month | 9564 notices 956400 OZ 29.748 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

No dealer withdrawals

Customer deposits: 1

i) Into Brinks: 16,879.280 oz (525 kilobars)

total deposits: 16,879.280 oz

2 customer withdrawals:

i)Out of JPM 52,759.791 oz (1641 kilobar)

ii)Out of Manfra: 16,879.280oz (525 KILOBARS)

total withdrawals: 69,639.071 oz(2166 kilobars)

ADJUSTMENTS:3 dealer to customer

Int Delaware: 11,601.160 oz

JPMorgan: 118,097.916 oz

Manfra: 244,600.956 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 62 contracts having LOST 242 contracts . We had

292 notices filed on Friday so we GAINED a strong 50 contracts or an additional 5000 oz will stand in this non active

delivery month of July.

August has a LOSS OF 31,161 contracts down to 156,709 contracts. We have 4 more reading days before first day notice. Looks like we will have a strong August standing for gold (JULY 29/22..FIRST DAY NOTICE)

Sept. gained 95 contracts to 2973 contracts.

We had 45 notice(s) filed today for 4500 oz FOR THE July 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 20 notices were issued from their client or customer account. The total of all issuance by all participants equate to 45 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 45 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2022. contract month,

we take the total number of notices filed so far for the month (9564) x 100 oz , to which we add the difference between the open interest for the front month of (JULY 62 CONTRACTS ) minus the number of notices served upon today 45 x 100 oz per contract equals 958,100 OZ OR 29.800 TONNES the number of TONNES standing in this active month of July.

thus the INITIAL standings for gold for the JULY contract month:

No of notices filed so far (9564) x 100 oz+ (62) OI for the front month minus the number of notices served upon today (45} x 100 oz} which equals 958,100 oz standing OR 29.645 TONNES in this active delivery month of JULY.

TOTAL COMEX GOLD STANDING: 29.800 TONNES (A FAIR STANDING FOR A JULY ( NON ACTIVE) DELIVERY MONTH)

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,443,533.842 oz 76.00 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 31,173,271.582 OZ

TOTAL REGISTERED GOLD: 15,498,734.555 OZ (48,20 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 15,622,277.236 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 13,178,744.0 OZ (REG GOLD- PLEDGED GOLD) 409.9 tonnes

END

SILVER/COMEX/JULY 22

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 973,786.862 oz CNT Delaware JPMorgan Brinks |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 190,759.160 oz Delaware CNT |

| No of oz served today (contracts) | 186 CONTRACT(S) 930,000 OZ) |

| No of oz to be served (notices) | 0 contracts (0,000 oz) |

| Total monthly oz silver served (contracts) | 3591 contracts 17,955,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 2 deposits into the customer account

i) Into Delaware 189,798.360 oz

ii) Into CNT: 960.80 oz

total deposit: 190,759.160 oz

JPMorgan has a total silver weight: 176.177 million oz/341.145 million =51.62% of comex

Comex withdrawals:4

i) Out of Brinks: 6788.120 oz

ii) 72,241.943 oz

iii) Out of Delaware 4988.299 oz

iv) Out of jPMorgan 889,768.000 0z

adjustments: 2/dealer to customer

CNT: 14,423.563 oz

Manfra: 474,205.304 oz

customer to Dealer: JPMorgan 44,551.400 oz

and Loomis: 4745.80 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 59.633 MILLION OZ

TOTAL REG + ELIG. 341.141 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JULY OI: 233 CONTRACTS HAVING GAINED 3 CONTRACTS. WE HAD 47 NOTICES FILED

ON FRIDAY, SO WE GAINED 50 CONTRACTS OR AN ADDITIONAL 250,000 OZ WILL STAND FOR METAL AT THE COMEX.

AUGUST LOST 25 CONTRACTS TO STAND AT 958

SEPTEMBER HAD A GAIN OF 1381 CONTRACTS DOWN TO 118,520

CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 186 for 230,000 oz

Comex volumes:43,456// est. volume today// poor

Comex volume: confirmed yesterday: 50,180 contracts ( poor )

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 3591 x 5,000 oz = 17 955,000 oz

to which we add the difference between the open interest for the front month of JULY(233) and the number of notices served upon today 186 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY./2022 contract month: 3591 (notices served so far) x 5000 oz + OI for front month of JULY (233) – number of notices served upon today (186) x 5000 oz of silver standing for the JULY contract month equates 18,190,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JULY 25/WITH GOLD DOWN $7.85: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 1005.87 TONNES

JULY 22/WITH GOLD UP $17.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 21/WITH GOLD UP $11.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.101 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.87 TONNES

JULY 20/WITH GOLD DOWN $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1009.06 TONNES

JULY 19/WITH GOLD DOWN $.35 :BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.22 TONNES FROM THE GLD//INVENTORY RESTS AT 1009.06 TONNES

JULY 18/WITH GOLD UP $7.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.28 TONNES

JULY 15/WITH GOLD DOWN $3.75:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD///INVENTORY RESTS AT 1016.89 TONNES//

JULY 14/WITH GOLD DOWN $28.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD//INVENTORY RESTS AT 1019.79 TONNES

JULY 13/WITH GOLD UP $10.55:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROMTHE GLD//INVENTORY RESTS AT 1021.53TONNES

JULY 12/WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESS AT 1023.27 TONNES

JULY 11/WITH GOLD DOWN $4.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWL OF 1.16 TONNES FROM THE GLD./INVENTORY RESTS AT 1023.27 TONNES

JULY 7/WITH GOLD UP $1.35: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.61 TONNES FORM THE GLD///INVENTORY REST AT 1024.43 TONNES

JULY 6/WITH GOLD DOWN $26.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 9.86 TONNES FROM THE GLD//INVENTORY REST AT 1032.04 TONNES

JULY 5/WITH GOLD DOWN $36.55//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.41 TONNES FROM THE GLD///INVENTORY RESTS AT 1041.90 TONNES

JULY 1/WITH GOLD DOWN $5.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES//INVENTORY RESTS AT 1050.31 TONNES

JUNE 30/WITH GOLD DOWN $9.20: big CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 1052.63 TONNES//

JUNE 28/WITH GOLD DOWN $3.05//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.64 TONNES FROM THE GLD///INVENTORY RESTS AT 1056.40 TONNES

JUNE 27/WITH GOLD DOWN $4.90 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.04 TONNES

JUNE 24/WITH GOLD UP 45 CENTS TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.70 TONNES FROM THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 23/WITH GOLD DOWN $8.60:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//INVENTORY RESTS AT 1071.77 TONNES

JUNE 22/WITH GOLD UP 15 CENTS:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1073.80 TONNES

GLD INVENTORY: 1005.87 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JULY 25/WITH SILVER DOWN 24 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.383 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 499.101 MILLION OZ//

JULY 22/WITH SILVER DOWN 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 500.484 MILLION OZ//

JULY 21/WITH SILVER UP 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.19 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 500.484MILLION OZ/

JULY 20/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 8.253 MILLION OZ FORM THE SLV/INVENTORY RESTS AT 507.585 MILLION OZ//

JULY 19/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ//

JULY 18/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 4.995 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ.

JULY 15/WITH SILVER UP 31 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 3.226 MILLION OZ FORM THE SLV//INVENTORY RESTS AT 510.443 MILLIONOZ//

JULY 14/WITH SILVER DOWN 88 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 OZ FROM THE SLV// //INVENTORY RESTS AT 513.671 MILLION OZ

JULY 13/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SV//INVENTORY RESTS AT 514.501 MILLION OZ.

JULY 12/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.228 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 514.501 MILLION OZ//

JULY 11/WITH SILVER DOWN 17 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 5.533 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 517.729 MILLION OZ

JULY 7/WITH SILVER UP 3 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.889 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 523.262 MILLION OZ/

JULY 6/WITH SILVER UP ONE CENT: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 12.558 MILLION OZ FORM THE SLV///INVENTORY RESTS AT 528.151 MILLION OZ

JULY 5/WITH SILVER DOWN 55 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 540.709MILLION OZ//

JULY 1/WITH SILVER DOWN 61 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ//INVENTORY RESTS AT 540.709 MILLION OZ//

JUNE 30/WITH SILVER DOWN 41 CENTS : SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 738,000 OZ FROM THE SLV//INVENTORY RESTS AT 541.262 MILLION OZ//

JUNE 28/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.00 MILLION OZ..

JUNE 27/WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 24/WITH SILVER UP 10 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.137 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 23/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 2.029 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 545.137 MILLION OZ//

JUNE 22/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.166 MILLION OZ.

CLOSING INVENTORY 499.101 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: It’s Getting Harder To Deny Recession Reality

MONDAY, JUL 25, 2022 – 10:20 AM

It’s getting harder and harder for recession deniers to justify their optimism. And some people seem to be waking up to that reality.

Late last week, we got more economic data and corporate earning news that proves the economic optimism that’s been bandied about for months is unfounded.

Weekly first-time jobless claims rose for the third consecutive week, hitting 251,000. This was higher than projected and it’s the highest level of jobless claims since last October.

The Philadelphia Fed Manufacturing Index for July also came out. The consensus was for 0.4, up from June’s -3.3 print. Instead, the number came in at -12.3. That was 50% below the low end of the consensus. Meanwhile, the employment index declined 9 points to 19.4. That was its lowest reading since May 2021.

The leading economic indicator index for June fell 0.8% in June off a May number revised lower to down 0.6%. It was the fourth straight monthly decline in that index.

The composite PMI index fell to 47.5 in July from 52.3 in June, hitting a 26-month low. The PMI services index fell even lower to 47. Anything below 50 is supposed to indicate a recession. Peter said the big drop in the service sector was particularly troubling.

When you have a 47 on the services index, you know the US economy is in recession because the service sector is what everybody looks to to power the economy.”

Peter said this data really should surprise people because it’s nothing new.

This should be obvious, but people have been in denial about the weakness in the economy. So, as all this weak economic data continues to come out, more and more of the recession deniers are going to have to throw in the towel and accept reality — including all of the recession deniers at the Federal Reserve.”

The Atlanta Fed continues to project a second straight month of negative GDP growth in the second quarter. Currently, it projects a -1.6% decline. It will release one more projection before the actual numbers come out. Peter said he thinks it will be around -2. That would indicate the second quarter was actually weaker than Q1.

After we got the negative GDP print in the first quarter, the mainstream blew it off, asserting that it was just an outlier.

When we end up with an even weaker number for the second quarter, that really throws a bunch of cold water in the face of the idea that we have a strong economy. And given how weak the Q3 data already is… We don’t have a lot of July data yet, but it’s starting to come in and what we’ve seen is pretty ugly. And it makes a lot of sense that the third quarter would be even weaker than the first two because interest rates are going to be a lot higher in the third quarter than they were back then. Next week, the Fed is set to raise interest rates 75 basis points. We’re going to be up to 2.25 to 2.5%. If we were in recession when interest rates were 0.5%, 1%, 1.5%, think about how much worse that recession is going to be when interest rates are higher.”

In this podcast, Peter also talks about the first ECB rate hike in 11 years, a possible top in the dollar, a possible bottom in gold, and the pain tech companies are feeling as advertisers flee.

END

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

Rickards: Fed’s Cure May Be Worse Than The Disease

SUNDAY, JUL 24, 2022 – 12:30 PM

Authored by James Rickards via DailyReckoning.com,

Right now, it’s basically a case of the Fed versus the economy. You might say, “Wait a second. Isn’t the Fed supposed to help the economy?”

Well, not exactly. They may want to help the economy, but helping the economy actually isn’t job one. Job one is helping the banks. The Fed was essentially created to prop up the banking system and prevent bank runs.

Everything else it tries to accomplish, such as price stability and maximum employment, comes second.

So it’s not clear that the Fed’s always aligned with the best interests of the economy. People don’t realize that, but it’s important to keep in mind.

Everyone knows the Fed’s raising interest rates right now. But which rates? The rate that the Fed actually raises is called the fed funds target rate. And what is that?

That’s the rate at which banks lend to each other to meet their reserve requirements on an overnight basis. Fed funds are amounts that banks lend to each other to meet overnight reserve requirements.

It’s an extremely short-term rate. The Fed targets that rate as a way to control the money supply and perhaps tweak inflation or achieve other economic goals.

The Fed Is Targeting a Rate That No Longer Exists

I don’t want to get into the mechanics of the banking system, but here’s the essential point I want to make:

There hasn’t been a real fed funds market for about 12 or 13 years, ever since the Fed began flooding the system with money during the Great Financial Crisis. Today, reserves are close to an all-time high.

In other words, the banks have excess reserves. Their actual reserves are multiple trillions of dollars in excess of the requirement. So there is no shortage of reserves.

There’s no overnight lending for reserve requirements, because all the banks have excess reserves.

So the Fed is targeting a rate that doesn’t exist anymore. Why are they doing it?

Banks aren’t lending to each other, but they are lending to the Fed in the form of excess reserves. Those are deposits at the Fed, which the Fed pays interest on. So in a sense, the interest on excess reserves is a modern substitute for the old fed funds rate.

But this money is basically sterilized. It stays within the banking system without making its way into the real economy. That’s why all the QE the Fed engaged in after 2008 never led to consumer price inflation.

The inflation we’re seeing today has nothing to do with QE (more on that in a minute). Now people say the Fed’s raising interest rates. But it’s not that simple.

The Fed Has Limited Influence Over Long-Term Rates

The Fed really only controls that overnight rate. It doesn’t have that type of control over longer-term interest rates like those on the 10-year Treasury note, for example.

The Fed can target 10-year note rates to some extent with quantitative easing or quantitative tightening, through buying and selling them in the market. They can move the rate around a little bit, but that influence is limited.

The market for 10-year Treasuries is much, much larger than the Fed. It’s the deepest and most liquid market in the world.

So the Fed’s really targeting one minor rate, the overnight rate. It’s a really narrow target.

They don’t control long-term interest rates directly, nor do they have the capacity to do so.

So how does raising the fed funds rate reduce inflation?

The Supply Side

There are two major sources of inflation. There’s the supply side and there’s the demand side. Either one of them can drive inflation, but they’re very, very different in terms of how they work.

The supply side, as the name implies, comes from input. The supply just isn’t there. Farm prices are going up because fertilizer prices are going up, partly because of the war in Ukraine. Oil prices are going up because there’s a global shortage, and there’s disruption in supply chains.

Actually, I need to refine my comments about oil shortages. Rising gasoline prices don’t have all that much to do with the oil supply. There’s not a shortage of oil, but in the United States, there’s a shortage of refining capacity.

You don’t put crude oil in your gas tank, you put gasoline in your gas tank, or diesel, or jet fuel, which is basically kerosene. All of it has to be refined, and that’s where the bottleneck is.

Raising Rates Won’t Plant Crops or Increase Oil Production

So there are increasing shortages in some of the refined products, and that also accounts for today’s extremely high prices. And transportation costs go into the prices of everything.

So what can the Fed do about that? Nothing. Does the Fed drill for oil? Does the Fed run a farm? Does the Fed drive a truck? Does the Fed pilot a cargo vessel across the Pacific or load freight at the Port of Los Angeles?

No, they don’t do any of those things, and so they can’t fix that part of the problem. Raising interest rates has no impact on the supply side shortages we’re seeing. And that’s where the inflation’s coming from.

Since the Fed has misdiagnosed the disease, they are applying the wrong medicine. Tight money won’t solve a supply shock. Until the supply shortages are fixed, higher prices will continue. But tight money will hurt consumers, increase the savings rate and raise mortgage interest rates, which hurts housing.

The Demand Side

Then there’s demand-side inflation, called demand-pull inflation. That’s when people build inflation into their day-to-day behavior, when they think inflation’s here to stay.

They say, “Well, I was thinking of buying a new refrigerator. Better go get it today because the price is going up.”

The same logic applies to buying a new car, a new house, etc. The motivation to buy now accelerates demand because consumers think the price will only go up. These expectations can take on a life of their own and feed on themselves as people rush to the stores.

Supply can’t keep up, which is a recipe for higher prices. We’re not there yet. We’re not at the demand-pull side, but we’re dangerously close.

Are you running right out today to go buy a new refrigerator because you fear the price is going up? Probably not. You’re certainly aware of price increases; you see them at the pump and at the grocery store. But at least so far, that part of the behavior has not changed very much.

The Cure May Be Worse Than the Disease

Here’s the point: The Fed can’t create supply but it can destroy demand. If they raise interest rates enough, mortgage rates will rise and monthly payments with them. People will stop buying houses and credit card balances will rise because they’re paying higher interest. Financing starts to dry up, which spreads throughout the economy.

So the Fed can destroy demand, but only at the cost of the economy. It’s one thing if the inflation is coming from the demand side, but it’s not. It’s coming from the supply side, and the Fed can’t do anything about that.

They can destroy enough demand to maybe bring inflation down, but only by destroying the economy.

And that’s the point. The idea that the Fed can squash inflation without squashing the economy is false.

I’m afraid we’re going to find that out the hard way.

end

LAWRIE WILLIAMS: Is nothing sacred nowadays? Probably not!

China has always been adept at playing the long game, and Russia has been following in its footsteps. Both nations have used the decades now of détente with the West to put themselves in a dominant position in terms of the supply of certain key metals, minerals, and strategic manufactured items that they virtually have a stranglehold on the supply of many products that are absolutely key to the economies and national security of potential competitor nations. In short, these still totalitarian states are taking one of the worst aspects of capitalism and using mass production and low pricing to drive competing businesses out of several key strategic markets.

This has been brought to global notice by the Russian invasion of Ukraine and the reaction of nearly all European nations in condemning it with the imposition of economic sanctions on Russia. Yet Russia holds virtually all of them economic hostage to the potential threat of cutting off their key energy source – nearly all European nations are enormously dependent on the supply of Russian oil and natural gas through a complex network of overland pipelines.

Russia would obviously like to sow dissent among the Europeans through threats to limit, or cut off, supplies, although the situation is not that simple. But if an all- out war with NATO were to develop no doubt supplies would be cut immediately. At the moment Russia needs the revenue from its oil and gas sales to finance its Ukraine war so a somewhat uneasy situation is currently in place as European nations desperately try to source alternate supplies and Russia looks for alternate markets, and the oil and gas continues to flow, with reducing delivery rates probably balanced in revenue terms by rising prices.

As for China it has long cornered the market for a number of absolutely key strategic metals and minerals, and where its domestic mines are not dominant it has sought to buy control of overseas mines which fit this criterion. For example, of the list of 35 metals and minerals deemed strategically critical by the U.S. , China is the dominant supplier of 21 of these. Most other western nations find themselves in a similar position.

But it is not only the supply of metals and minerals which is a current cause for concern. China is also a leader in certain aspects of technology, particularly in the communications and computing sphere. Indeed many U.S. technological products are now manufactured in China and there is a huge fear, possibly unfounded, that U.S. and allied security protocols may have been breached and accessed accordingly. Hence the recent actions taken against Huawei over its technology and equipment being used in new 5G communications systems, despite denials by the company and the Chinese government. Who believes government denials nowadays?

So what has all the above got to do with precious metals prices going forward? Absolutely everything we would suggest. It presages an era of global economic instability and tensions the like of which we have probably not seen for decades. Indeed not since the eras which led up to massive global conflicts. Let us hope and pray that the end game this time around is not something similar.

Such global geopolitical and economic instability, or the contemplation of such, tends to drive wealth into protective assets, and gold is probably the one that has best stood the test of time in this respect. Forget bitcoin, while some equities may do OK in such conditions but others may be decimated, and the choice between potential winners and losers tends to be a real gamble.

The worse the situation we find ourselves in the higher these ‘safe haven’ asset prices may rise – so be careful what you wish for. But we see the potential for the escalation of the war in Europe as decidedly worrying, as is that of China flexing its military muscles over Taiwan, particularly if the latter’s principal ally, the U.S., also becomes embroiled in a European conflict. Can its military fight successfully concurrent conflicts on opposite sides of the world simultaneously?

Hopefully all the above possibilities will remain theoretical only. But the very fact that they are even in the mind’s eye may well provide a continuing stimulus to the global gold price and drive it to new heights, But as long as no real actual military escalation occurs, price rises should remain under reasonable control and still continue to disappoint the out-and-out gold mega-bulls.

25 Jul 2022

3. Chris Powell of GATA provides to us very important physical commentaries

Cambone confesses when at Kitco gold rigging was a prohibited subject.

a good read..

(courtesy Chris Powell/GATA)

Stansberry’s Cambone confesses: Gold market rigging was prohibited subject

Submitted by admin on Sat, 2022-07-23 09:24Section: Daily Dispatches

9:35a ET Saturday, July 23, 2022

Dear Friend of GATA and Gold:

This week’s Stansberry Research interview by Daniela Cambone of Mark Yaxley of bullion dealer Strategic Wealth Preservation is far more notable for what Cambone herself says than for anything said by Yaxley.

Cambone notes that lately much news has been produced by the trial of former JPMorgan Chase gold and silver traders on federal charges of market rigging. Then she tells Yaxley:

“Back in the day, you remember when we started in the industry, the talk of gold manipulation was really … like, you couldn’t talk about it. It was like an underground thing. You were seen as a conspiracy person if you did speak about it, and now it’s really like it’s almost out in the open. Yes, banks were spoofing the prices.”

Yes, gold and silver market manipulation was all around them and financial journalists heard about it but none of them dared to attempt actual journalism by investigating it.

So it would be even more interesting if someone interviewed Cambone herself to discover exactly who at Kitco News directed her not to discuss the issue in her many years of doing interviews there, and to discover who seems to have renewed those instructions to Kitco’s current staff members.

But Cambone also leaves a mistaken impression here. For while the gold and silver sector now may be fully aware of the longstanding rigging of its markets, the government policy behind that rigging, which goes far beyond the Morgan traders who have been convicted and those who are now on trial, still can’t be addressed by mainstream financial news organizations and most monetary metals market analysts — nor by nearly all gold and silver mining companies themselves.

If Cambone really wants to make amends for her years of aiding gold and silver price suppression and the cheating of the investors who relied on her, she might consider interviewing a few of her bigshot friends in the industry about the extensive documentation of government gold price suppression policy, as compiled by GATA here —

— reviewing the documents one by one and asking the bigshots what they think about them after their years of denial that anything improper was going on. Their squirming would be enlightening for investors, and fun to watch.

Yaxley did make a couple of excellent points — first, that because because of its comprehensive misconduct in the gold and silver markets, JPMorgan Chase should be kicked out of the industry worldwide, even though the bank is so dominant that it would be hard to replace; and second, that premiums on gold and silver coins are causing prices to be much higher than futures prices.

Cambone’s interview with Yaxley, including her flippant confession, is 17 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Patrick Heller: Is gold’s price manipulated. Spoiler alert: yes

(Patrick Heller)

Patrick Heller: Is gold’s price manipulated?

Submitted by admin on Fri, 2022-07-22 10:18Section: Daily Dispatches

By Patrick Heller

Numismatic News

Stevens Point, Wisconsin

Thursday, July 21, 2022

Is the price of gold, and possibly silver, manipulated? The available evidence answers “yes” as it applies to decades past. The pattern strongly suggests that it is still happening today.

Overall, the manipulation has been to suppress the price of gold, where the suppression of silver’s price is one tactic employed to achieve a lower gold price.

In my column two weeks ago, I pointed out that a significant amount of trading in the gold market is not transparent. That provides the opportunity to manipulate the price of gold. But the important questions to answer are: Who has the legal authority, the financial clout, and the monetary incentive to want to suppress the price of gold?

The answer to all three of these questions is the U.S. government. …

… For the remainder of the analysis:

https://www.numismaticnews.net/coin-market/is-golds-price-manipulated

END

(Chris Powell)

Another financial writer omits intervention when explaining gold’s counterintuitive performance

Submitted by admin on Fri, 2022-07-22 10:07Section: Daily Dispatches

Friday, July 22, 2022

Dan Weil

MarketWatch, New York

Dear Dan (if I may):

In response to your commentary today at MarketWatch on the counterintuitive failure of the gold price to reflect the explosion of inflation worldwide —

https://www.thestreet.com/markets/commodities/gold/gold-stalls-while-inflation-surges-what-gives

— please let me call to your attention a better and more documented explanation than any offered by your commentary: the decades-long policy of largely surreptitious intervention against gold by governments and central banks, especially the U.S. government.

A summary of this documentation and its objectives can be found at the internet site of my organization, the Gold Anti-Trust Action Committee, here:

We realize that this is a sensitive subject and that governments and their agents among investment banks may bring powerful pressure on news organizations to stay away from it. Any news organization acknowledging the issue risks its advertising from these banks. But I urge you to look into it anyway, because the financial world is really not as it seems and gold pricing cannot be fairly reported without accounting for intervention.

With good wishes.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

Manchester, Connecticut

END

4. OTHER GOLD/SILVER COMMENTARIES

END

5.OTHER COMMODITIES: EGGS

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings MONDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.7455

OFFSHORE YUAN: 6.7520

HANG SANG CLOSED DOWN 46.20 PTS OR 0.22%

2. Nikkei closed DOWN 215.41 OR 0.77%

3. Europe stocks CLOSED ALL GREEN

USA dollar INDEX DOWN TO 106,21/Euro RISES TO 1.0248

3b Japan 10 YR bond yield: FALLS TO. +.200/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 136.46/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: UP -// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.045%/Italian 10 Yr bond yield RISES to 3.40% /SPAIN 10 YR BOND YIELD FALLS TO 2.27%…

3i Greek 10 year bond yield FALLS TO 3.07//

3j Gold at $1727.30 silver at: 18.62 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 35/100 roubles/dollar; ROUBLE AT 57.64

3m oil into the 95 dollar handle for WTI and 104 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 136.46DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9637– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9870well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.81 UP 3 BASIS PTS

USA 30 YR BOND YIELD: 3.052 UP 6 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.85

Overnight: Newsquawk and Zero hedge:

FIRST, NEWSQUAWK

Sentiment supported amid USD-downside and Kremlin commentary, US 2yr ahead – Newsquawk US Market Open

MONDAY, JUL 25, 2022 – 06:45 AM

- European bourses are firmer across the board as the initially cautious tone amid soft-Ifo and weekend developments dissipated amid USD-downside and constructive Kremlin remarks

- US futures also modestly bid into the busiest Q2 earnings week and pre-FOMC

- USD is under pressure on the risk tone with EUR underpinned by Kazaks despite Ifo while antipodeans lead the way

- Core debt has seen pronounced two-way action amid the above factors; currently, modestly softer with US yields steeper pre-2yr

- Crude began on the backfoot but has benefited from the Kremlin re. Nord Stream with Ags bid after Odessa strikes

- Looking ahead, highlights include US National Activity Index, US Dallas Fed, and supply from the US.

As of 11:15BST/06:15ET

For the full report and more content like this check out Newsquawk

Try a 14 day trial with Newsquawk and hear breaking trading news as it happens.

LOOKING AHEAD

- US National Activity Index, US Dallas Fed, supply from the US.

- Click here for the Week Ahead preview

GEOPOLITICS

RUSSIA-UKRAINE

- The Ukrainian port of Odesa was hit by a series of Russian missile strikes, according to Sky News. Russian Defence Minister said a Ukrainian warship and US-supplied anti-ship missiles were destroyed in the Odesa port attack, according to Reuters.

- US Secretary of State Blinken said Russia breached the grain deal commitments with the attack on Odesa port, via Reuters.

- Russian Kremlin says Odessa port strikes were strikes on military targets, won’t affect grain exports.

- Russian Kremlin says the repaired turbine delivered from Canada will soon be installed at Nord Stream 1, still equipment to be repaired which Siemens Energy (ENR GY) is aware of.

- EU countries are reportedly attempting to water down the Commission’s plans to cut gas demand by 15% from next month, according to the FT citing sources and a draft proposal. One proposal suggests compulsory targets should take into account each state’s dependency on Russian gas and storage. Plans will be discussed on Monday before an emergency Energy Ministers’ meeting on Tuesday, according to the FT.

- White House Defense Department spokesman said the US DoD is making preliminary explorations into the feasibility of potentially providing fighter jets for Ukraine, and said providing jets to Ukraine is not something that would be executed in the near term, according to Reuters.

- Ukraine President Zelensky said roughly 10mln tonnes of last year’s grain harvest will be exported after the deal is signed with Russia, according to Reuters.

- Ukrainian Presidential Advisor said if its ports are open, then Ukraine could transfer 60mln tonnes of grain over 8-9 months, but it will take 20-24 months to export the same amount if ports do not work, via Reuters.

- Siemens (SIE GY) on Sunday transferred a Canadian export license to Gazprom that allows turbines for the Nord Stream gas pipeline to be repaired and transported. The pipeline part may be en route to Russia by midweek but there is no guarantee that the arrival of the turbine will boost gas flows, according to Bloomberg.

OTHER

- French President Macron expressed disappointment to his Iranian counterpart about the lack of progress in nuclear talks, according to the Elysee Palace cited by Reuters.

- Turkish Foreign Ministry has summoned Sweden to convey a “strong reaction” over “terrorist propaganda” in Sweden, according to Reuters. This comes in the context of Sweden’s NATO ascension

- China has strengthened its warning to the US about House Speaker Pelosi’s visit to Taiwan, according to the FT. Sources suggest private rhetoric in China suggested a possible military response. Note, this is in-fitting with rhetoric seen via Global Times last week.

- US Deputy Secretary of State Sherman and US Ambassador to Australia Kennedy plan to visit the Solomon Islands next month, according to Reuters sources. Note, China has recently signed a new security agreement with the Solomon Islands, which caused concern among officials in the US, Australia and New Zealand.

- South Korean and US defence chiefs will be holding talks this week to discuss security on the Korean Peninsula and deterrence against evolving North Korean threats, according to Yonhap.

EUROPEAN TRADE

CENTRAL BANKS

- ECB’s Lagarde said the ECB will raise rates for as long as it takes to bring inflation back to target, according to an interview via Funke Mediengruppe.

- ECB’s Nagel said it is better to start with a bigger hike and is confident that ECB’s TPI would survive legal challenges, according to Handelsblatt. He added that future rate hikes are to depend on data, and we still see positive growth in 2022 and 2023. He said TPI is to be used in exceptional circumstances.

- ECB’s Holzmann said the ECB may accept a “light recession” if the outlook for CPI rises, according to an interview via ORF. Holzmann said the ECB is to consider the economic situation before another big hike and said economic growth is slowing and that has brought in caution.

- ECB’s Kazaks says large interest rate hikes may not be over; too weak EUR is a “problem”. The hike in September needs to be quite “significant” and should be open to larger hikes.

- BoJ’s Takata (new member) says the BoJ is able to keep monetary policy easy, but are facing new challenges such as dwindling bank margin and impact on market function.

- BoJ’s Tamura (new member) says Japan may soon see positive cycle commence, with wages increasing with inflation. If this occurred, exit from easy policy would become focus of discussions.

EQUITIES

- European bourses are firmer across the board as the initially cautious tone amid soft-Ifo and weekend developments dissipated amid USD-downside and constructive Kremlin remarks; Euro Stoxx 50 +0.3%.

- US futures are modestly firmer, ES +0.5%, as we kick off the busiest week of earnings for Q2 and in the run-up to the FOMC.

- Tesla (TSLA) discloses a USD 170mln impairment loss resulting from changes to the carrying value of Bitcoin during H1 (ending June 30th). Increases FY22-24 CapEx to USD 6-8bln/yr (prev. 5-7bln).

- Click here for more detail.

FX

- DXY down again ahead of the Fed on Wednesday as risk appetite recovers broadly, index slips further from 107.00 to 106.240.

- Euro underpinned by hawkish ECB commentary and supportive Russian gas supply vibe to the extent that bleak German Ifo survey findings are shrugged off, USD/USD probes 1.0250 where hefty option expiry interest sits (1.86bln).

- Aussie derives traction from spike in iron ore prices, AUD/USD through 0.6950 and towards circa 1bln option expiries at 0.7000 strike.

- Franc and Yen underperform as bond yields rebound firmly from recent lows, USD/CHF around 0.9625 and USD/JPY 136.00+ vs Friday lows of 0.9600 and 135.57.

- Yuan welcomes PBoC notice of recovery in support of cultural and tourism sectors plus reports of Chinese real estate fund, USD/CNH and USD/CNY both sub-6.7500 compared to highs at 7.7667 and 6.7577 respectively.

- Lira laments deterioration in Turkish manufacturing confidence, USD/TRY just shy of 17.8400.

- Click here for more detail.

Notable FX Expiries, NY Cut:

- Click here for more detail.

FIXED INCOME

- Debt futures flip then flop in choppy fashion amidst hawkish ECB rhetoric and encouraging news from Russia on EU gas supplies.

- Bunds rebound to 154.86 before retreat to 153.78, Gilts recoil from 117.48 to 117.02 and 10 year T-note within a 120-02+/119-21 range

- Downbeat German Ifo survey and mixed UK CBI industrial orders vs business optimism largely ignored

- 2 year note supply looms and may be interesting as a gauge of investor demand ahead of the Fed

- Click here for more detail.

COMMODITIES

- Crude benchmarks began the session on the back foot, amidst the generally cautious APAC mode where participants were digesting multiple updates including Russia/Ukraine, Nord Stream, China/US and reiterations from Biden.

- However, a seeming USD-driven move lifted the benchmarks back towards session highs amid a concerted risk move following Kremlin commentary.

- US President Biden said gasoline prices are still too high and is working to make sure gasoline prices move with oil prices and said companies should use profits to boost output, according to Reuters.

- LME will not ban Nornickel’s metal as the Russian firm is not under UK sanctions, according to Reuters sources.

- Chicago wheat, corn and soybean futures rose at the open, possibly on the back of reports that the Ukrainian port of Odessa was hit by Russian missiles less than 24 hours after the signing of the grains agreement in Turkey.

- Malaysia’s Commodities Minister said crude palm oil prices are likely to remain weak for most of Q3 2022 as Jakarta lifts the exports levy; but prices are expected to be higher in Q4 amid the resumption of Indonesia’s palm oil export levy, via Reuters.

- Spot gold has found support from the declining USD, lifting to USD 1733.70/oz, though upside is capped by the broader risk tone with the yellow metal yet to test Friday’s USD 1738.99/oz best.

- Click here for more detail.

NOTABLE EUROPEAN HEADLINES

- Italy’s far-right Brothers of Italy party is reportedly struggling to find ministerial candidates, according to The Times.

- A survey by DIHK of 3,500 firms in Germany found that 16% are scaling back production or partially pausing business operations amid high energy prices, via Reuters.

- Fitch affirmed Hungary at “BBB”; outlook Stable; affirmed Ireland at “AA”; outlook stable.

NOTABLE US HEADLINES

- US President Biden’s physician said the president’s COVID symptoms continue to improve significantly, according to Reuters.

- Google (GOOG) co-founder Brin reportedly told his advisers to sell his personal investments in Tesla (TSLA) CEO Musk’s companies in recent months after learning that he had a brief affair with his wife, according to WSJ. Elon Musk denied the report, via Twitter.

- Click here for the US Early Morning note.

DATA RECAP

- German Ifo Business Climate New (Jul) 88.6 vs. Exp. 90.2 (Prev. 92.3, Rev. 92.2); Current Conditions New (Jul) 97.7 vs. Exp. 98.0 (Prev. 99.3, Rev. 99.4); Expectations New (Jul) 80.3 vs. Exp. 83.0 (Prev. 85.8, Rev. 85.5)

- UK CBI Trends – Orders (Jul) 8 (Prev. 18.0).

CRYPTO

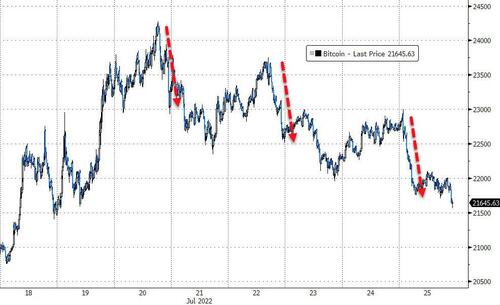

- Bitcoin remains under pressure and is yet to convincingly reclaims the USD 22k mark, after slipping to USD 21.75k overnight.

APAC TRADE

- APAC stocks traded mostly lower with the tech sector in the region hit following the Stateside sectoral performance.

- ASX 200 saw the gains in its Metals & Mining sector offset by a selloff in Tech.

- Nikkei 225 underperformed following the JPY strength seen on Friday, whilst the KOSPI outpaced peers.

- Hang Seng was lower following reports China is said to be mulling categorising US-listed Chinese firms into three groups based on the sensitivity of data held by the firms, but the property sector outperformed amid reports that China is planning to set up a real estate fund.

- Shanghai Comp was also softer but monkeypox-related stocks soared after the WHO declared monkeypox a global health emergency.

NOTABLE APAC HEADLINES

- China is reportedly imposing COVID “closed loops” on major Shenzhen companies which include Foxconn (2354 TW), BYD (1211 HK), CNOOC (0833 HK) and Huawei (002502 SZ), via Bloomberg.

- China is said to be mulling categorising US-listed Chinese firms into three groups based on the sensitivity of data held by the firms, according to FT sources.

- Neither the EU nor China believes that conditions are ripe for the implementation of the China-EU Comprehensive Investment Agreement, according to Chinese sources cited by SGH Macro.

- China reportedly plans to set up a real estate fund worth up to USD 44bln, according to REDD cited by Reuters.

- Hong Kong is reportedly planning to cut hotel quarantine times, according to Sing Tao Daily.

- The Sakurajima volcano on Japan’s western major island of Kyushu has erupted with the alert level raised to 5 – the highest, according to Sky News. No damage has been reported but volcanic stones could be seen raining down up to 1.5 miles away from the site, according to NHK.

- China’s securities regulator said in a statement it has not researched a plan for a three-tiered system to help Chinese companies avoid US delisting, according to CNBC.

i)MONDAY MORNING// SUNDAY NIGHT

SHANGHAI CLOSED DOWN 19.59 PTS OR 0.60% //Hang Sang CLOSED DOWN 46.20 OR 0.22% /The Nikkei closed DOWN 215.41 OR % 0.77. //Australia’s all ordinaires CLOSED DOWN 0.08% /Chinese yuan (ONSHORE) closed UP AT 6.7455//OFF SHORE CHINESE YUAN UP 6.7520// /Oil UP TO 95.80 dollars per barrel for WTI and BRENT AT 104.26// SHANGHAI CLOSED DOWN 19.59 PTS OR 0.60% //Hang Sang CLOSED DOWN 46.20 OR 0.22% /The Nikkei closed DOWN 215.41 OR % 0.77. //Australia’s all ordinaires CLOSED DOWN 0.08% / Stocks in Europe OPENED ALL GREEN ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

3 a./NORTH KOREA/ SOUTH KOREA/

///NORTH KOREA/SOUTH KOREA/

3B JAPAN

3c CHINA

CHINA/Sunday

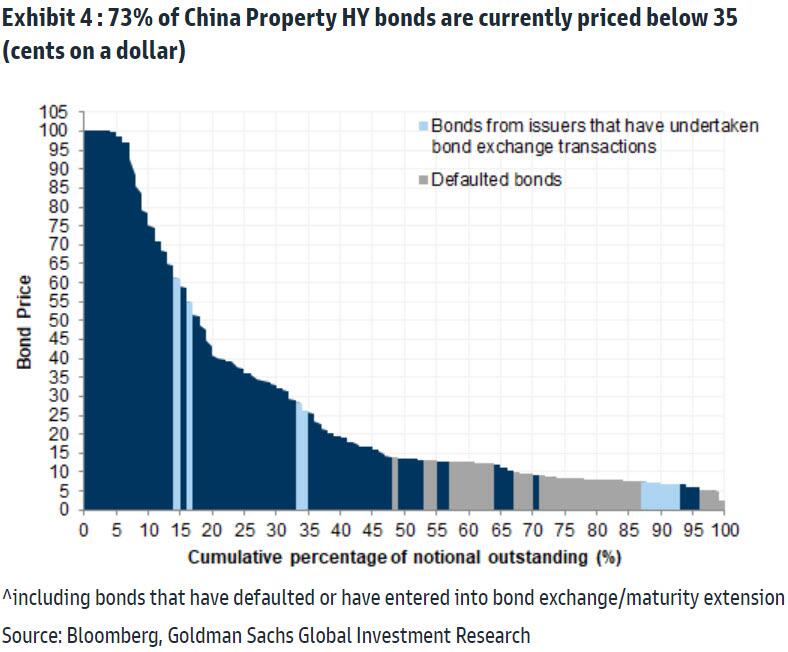

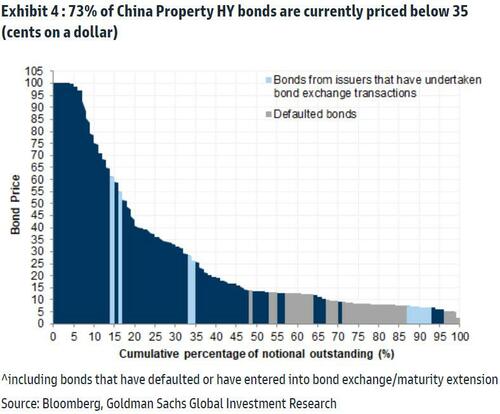

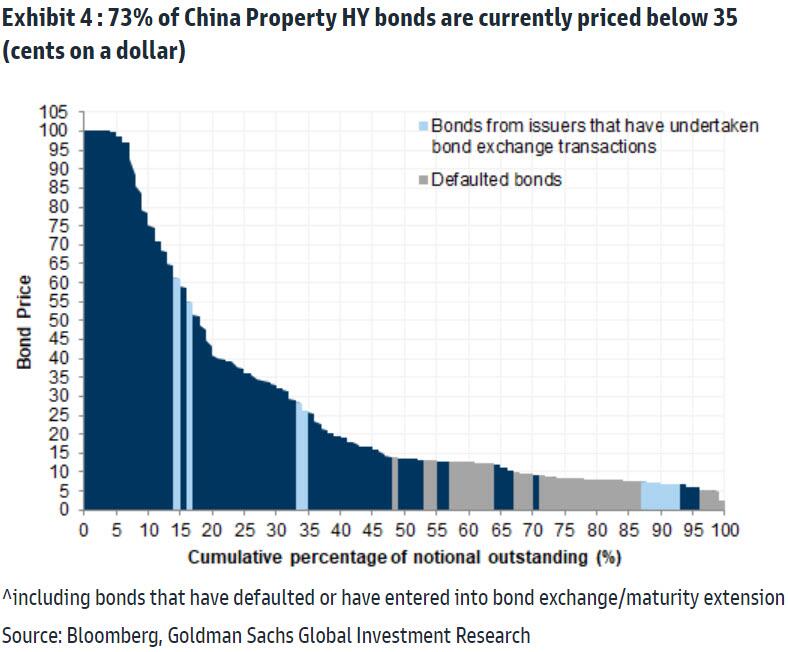

Chinese property continues to cause major problems for China. Most of Chinese property junk bonds are now trading below 35 cents

(Xie/Bloomberg)

Most Chinese Property Junk Bonds Are Trading Below 35 Cents

SUNDAY, JUL 24, 2022 – 09:45 PM

By Ye Xie, Bloomberg Markets Live commentator and reporter

1. China’s mortgage-boycott problem is still growing. More homebuyers halted payments on unfinished apartments, affecting at least 319 projects, up from 235 a week ago, according to Capital Economics. By all accounts, the situation is still manageable. Most economists estimate that the affected loans make up about 1%-2% of China’s $5.8 trillion in mortgages.

But the problem is that Beijing has yet to break the vicious circle in the housing market. The boycotts undermine confidence of new homebuyers, which reduces the cash flow of troubled developers and causes more of the type of construction delays that motivated the boycotts in the first place.

Already, the top 100 private developers, which account for more than a third of the projects under construction, are experiencing liquidity risks, according to Goldman Sachs. Reflecting this risk, about 73% of China’s high-yield property bonds are trading below 35 cents on the dollar, a level deemed as distressed by Goldman’s analysts. Left unsolved, it could quickly create problems in the banking system.

What’s the solution? Policy makers are considering remedies, including allowing a grace period for mortgage payments of affected homeowners. Bank of America’s economists led by Helen Qiao expect local governments and state-owned enterprises to step in to complete the unfinished projects. But they also warn that it may take time to resolve the issue, and governments of lower-tier cities may not have sufficient funds to come to the rescue.

2. The housing troubles and sporadic Covid outbreaks took momentum out of the economic rebound. The consensus 2022 GDP forecast in a Bloomberg survey has declined to 4%, and a number of economists, including at Bloomberg Economics, only see a growth rate of 3%. The outperformance of Chinese stocks since last month also has faded.

In response to the latest housing drama, the PBOC kept liquidity abundant, with interbank borrowing costs dropping below 1.5% for the first time since December 2020. Meanwhile, traders took advantage of the cheap funding to build leverage in the bond market, sending the overnight repo trading volume to records almost on a daily basis.

3. Recession risks keep rising as central banks tighten monetary policy. A survey of purchasing managers by S&P Global on Friday showed activities in both the euro zone and US contracted. The ECB ended eight years of negative interest rates with a 50bp hike last week. The Fed is expected to raise rates by 75 bps this week for a second consecutive meeting. But traders are betting that the Fed will slow down the rate increases afterward and wrap the tightening campaign by December.

END

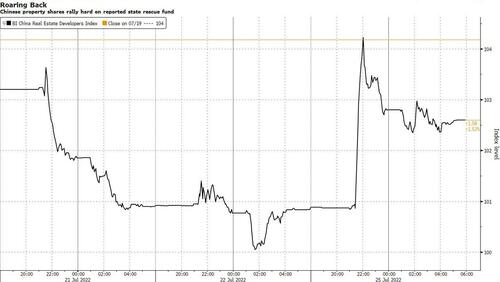

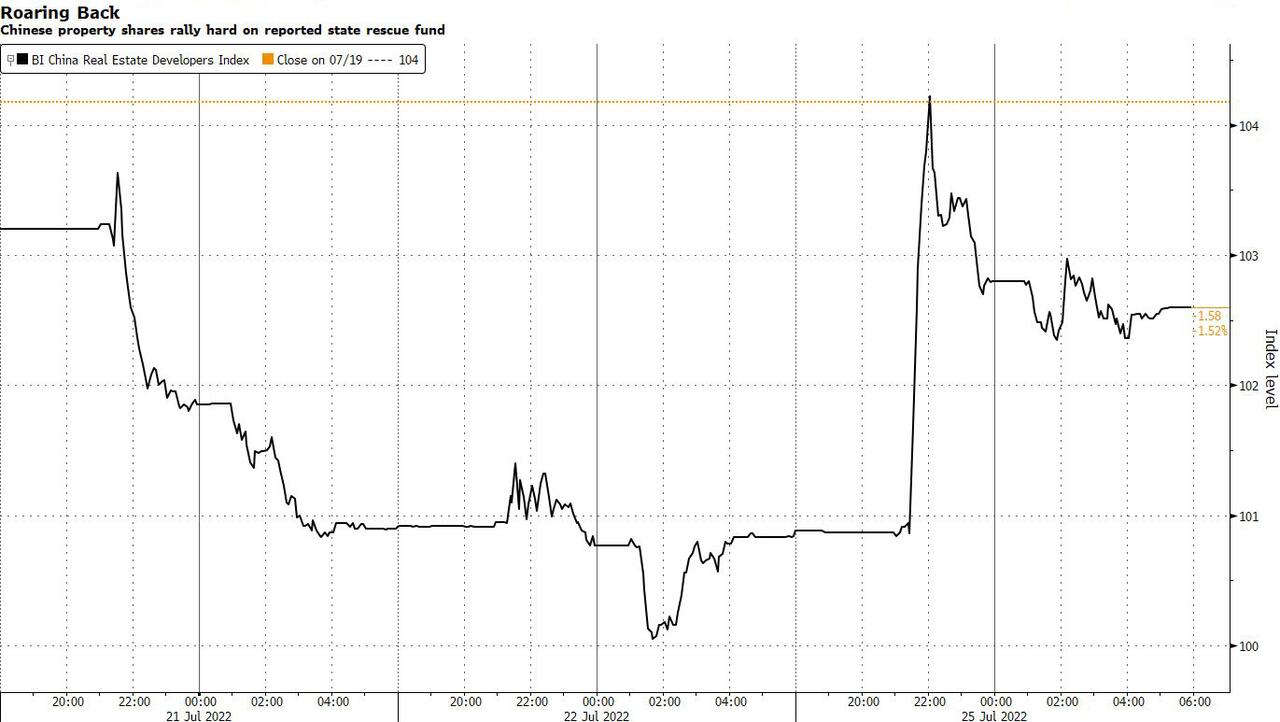

Monday: China cracks: the mortgage boycott prompts the government to launch a multi billion property rescue fund

(zerohedge)

Beijing Cracks: Mortgage Boycott Prompts China To Launch Multi-Billion Property Rescue Fund

MONDAY, JUL 25, 2022 – 08:47 AM

With Chinese property sentiment sinking from bad to worse amid the growing mortgage boycott – which for now remains contained affecting about 1%-2% of China’s $5.8 trillion in mortgages. but spreading rapidly – and Goldman observing over the weekend that over 70% of Chinese property junk bonds (as there are virtually no investment grade bonds left in China real estate) are trading below 35 cents…

… on Monday, Chinese property stocks and dollar bonds rallied sharply after a reported move by Beijing to establish a fund to support developers fueled optimism about a turnaround for the struggling sector. A Bloomberg Intelligence index of the country’s real estate firms jumped 1.7%, the most in a week…

… while China’s high-yield dollar notes, predominately issued by developers, rose at least 1 cent on the dollar, according to credit traders, with a Bloomberg gauge tracking the sector set for the longest winning streak in two months.

The catalyst for the mood reversal was a report by REDD that China’s State Council has approved a plan to set up a fund to support 12 developers and a few new distressed real estate firms nominated by local authorities. If confirmed, the move would mark one of the most direct measures yet taken by Beijing to salvage a sector roiled by massive defaults, slumping sales and a widening boycott on bank loans.

According to REDD, the fund secured 50 billion yuan ($7.4 billion) from China Construction Bank Corp. and a 30 billion yuan relending facility from the People’s Bank of China, and can be upsized to between 200 billion yuan and 300 billion yuan, it added.

“The mortgage boycott is effectively forcing Beijing to ease credit conditions for developers,” said Amy Xie Patrick, a portfolio manager at Pendal Group Ltd. “The real estate fund, if confirmed, is a stronger initiative compared to previously guiding state banks to lend to property developers, but it won’t be enough to solve the problem unless it can be capitalized by a blank check from the Chinese government,” she said.

Bloomberg was first to report some aspects of the plan last week, revealing that regulators have asked China Construction Bank, the nation’s largest mortgage lender, to explore a pilot program to set up a fund with selected local governments to purchase projects under construction that have yet to find buyers, with the aim of converting them into apartments for long-term rentals.

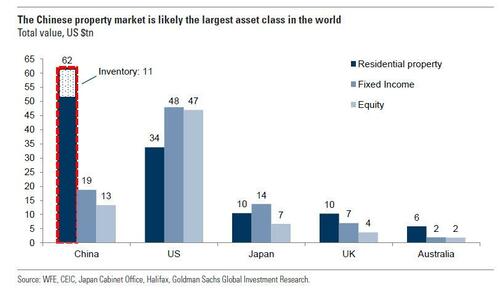

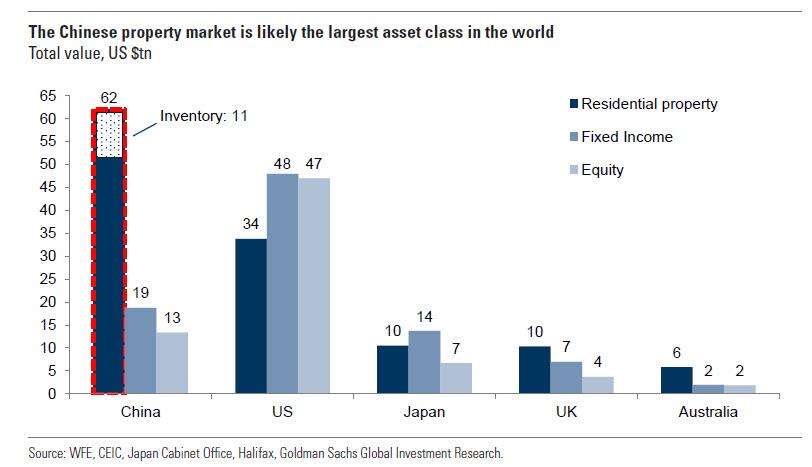

The reported plan for the state fund offers the latest indication of growing ease among policymakers over a deepening housing bust that threatens both financial and social stability, as it sends shock waves through China’s 400-million-strong middle class and upends the belief that real estate is a surefire way to build wealth. As a reminder, Goldman last year calculated that the Chinese property market is the world’s biggest asset; needless to say, a crash here would lead to an unprecedented global deflationary shockwave.

In response to the news, property developers surged: Guangzhou R&F Properties Co. gained 5.7%, with Country Garden Holdings Co. was up 4.5%. In the credit market, dollar bonds of investment-grade Chinese developers jumped in tandem with their junk peers, led by China Vanke and Longfor Group Holdings. In the credit market, dollar bonds of investment-grade Chinese developers jumped in tandem with their junk peers, led by China Vanke Co. and Longfor Group Holdings.

Of course, as Jim Chanos was quick to point, the current iteration of the rescue fund is a drop in the bucket…

… and as Bloomberg notes, the 12 developers expected to benefit from the fund rescue have a combined short-term debt of 742 billion yuan, UBS analysts calculated. The number would swell to 4.05 trillion yuan when taking into account the amount owed to homebuyers and suppliers, they added.

In other words, now that Beijing has cracked and is willing to backstop housing, this is just the start and UBS agrees: despite the fund’s limited size, “clearly the government is signaling it wants to restore homebuyers’ confidence and encourage them to start purchasing houses again,” said Steve Wong, an analyst at Essence International Financial Holdings Ltd. “Setting up a fund is more feasible since a broad-based easing for the sector is unlikely.”

end

4/EUROPEAN AFFAIRS//UK AFFAIRS/

/GERMANY//GAZPROM//RUSSIA//GERMANY/EU//update

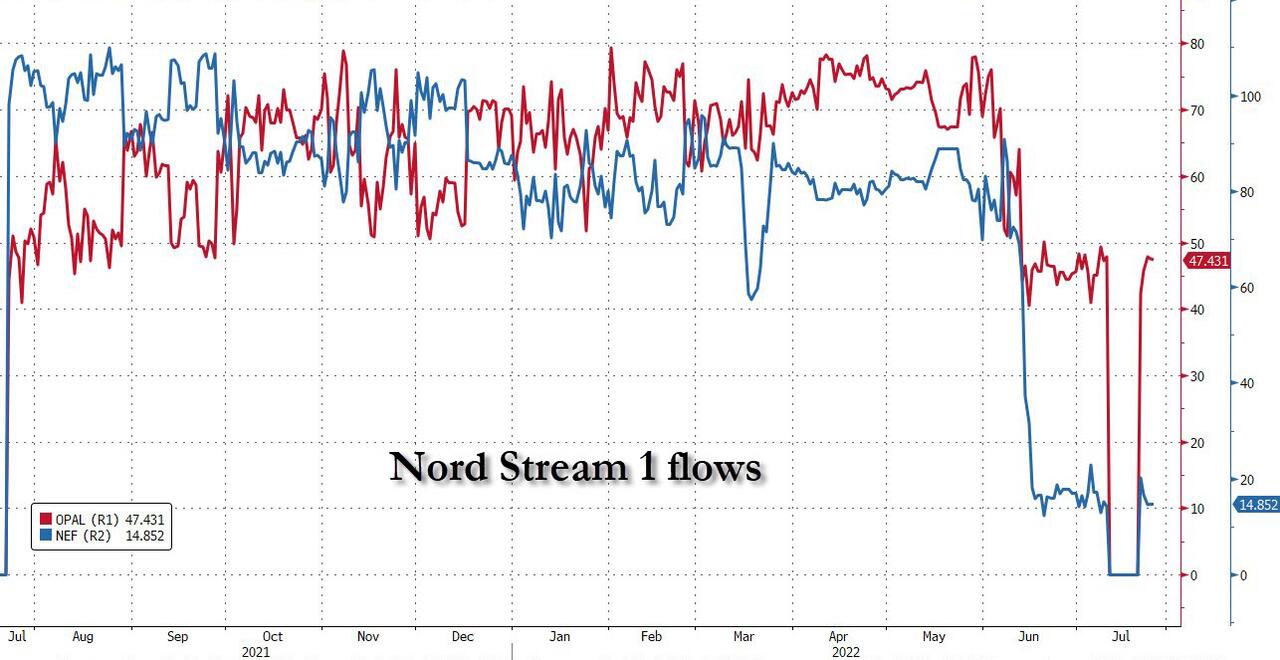

Putin ties a rope around the neck of Germany as Gazprom unexpectedly halts more transmission through Nordstream 1, cuts flows in half. European gas prices soar

(zerohedge)

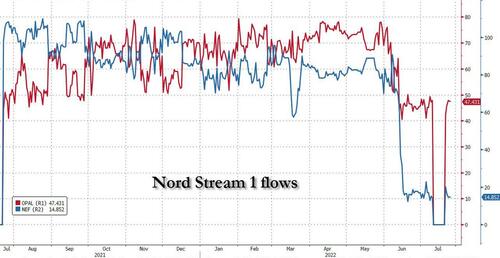

Putin Turns The Screws: Gazprom Unexpectedly Halts Another Nord Stream Turbine Cutting Flows In Half; European Gas Prices Soar

MONDAY, JUL 25, 2022 – 10:53 AM

Europeans, and especially Germans, breathed a sigh of relief last Thursday when amid fears that Moscow would not restart flows along the Nord Stream 1 pipeline after its 10 day maintenance period, Putin turned the gas back on, if just to its pre-maintenance peak level of about 40% of maximum capacity.

Alas Europe’s muted celebration were not meant to last, and with many speculating that Russia was just waiting for the right opportunity to turn the screws on Germany, both literally and metaphorically, that’s precisely what happened moments ago when shortly after Siemens finally delivered transport documents for the controversial Nord Stream turbine that had been stuck in Canada for weeks, Gazprom unexpectedly announced it would halt one more Nord Stream turbine at its Portovaya compressor station from July 27, “taking into account the technical conditions of the engine,” the Russian company says in a statement.

This means that as had been whispered much of last week, gas flows from Portovaya will drop to as much as 33 million cubic meters per day from 7am Moscow time on July 27, which means flows along NS1 will decline by half, from 40% of capacity to just 20%.

- GERMAN NETWORK REGULATOR HEAD: NORD STREAM 1 GAS NOMINATIONS HALVED FOR TUESDAY

According to Bloomberg energy expert Javier Blas, with “Nord Stream 1 flowing at just 20% of capacity from July 27, Germany will NOT have enough natural gas to make it throughout the whole winter **unless big demand reductions are implemented**. Berlin will need to activate stage 3 of its gas.”

Translation: unless Putin changes his mind, Germany is facing not just a freezing winter, but a bitter recession.

In kneejerk response, European (TTF) nat gas prices spiked 10% and are likely to keep rising as Putin just assured that – all else equal – a recession Germany is now inevitable, and yet since commodity prices will continue to rise, the ECB remains helpless: it can’t cut rates without sending inflation even higher, but it can’t keep hiking with Europe now in a recession.