by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1719.45 DOWN $1.60

SILVER: $18.63 UP 16 CENTS

ACCESS MARKET:

GOLD $1717.40

SILVER: $18.63

We are now entering options expiry for Comex (tomorrow) and OTC/LBMA (Friday)

Bitcoin morning price: $21,097 DOWN 508

Bitcoin: afternoon price: $21,605. DOWN 1469

Platinum price: closing DOWN $4.40 to $879.90

Palladium price; closing UP $5.00 at $2015.50

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JULY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,719.000000000 USD

INTENT DATE: 07/25/2022 DELIVERY DATE: 07/27/2022

FIRM ORG FIRM NAME ISSUED STOPPED

657 C MORGAN STANLEY 1

661 C JP MORGAN 13 41

732 C RBC CAP MARKETS 21

905 C ADM 6

TOTAL: 41 41

MONTH TO DATE: 9,605

no. of contracts issued by JPMorgan: 41/41

_____________________________________________________________________________________

GOLD: NUMBER OF NOTICES FILED FOR JULY CONTRACT: 41 NOTICES FOR 4100 OZ //0.1275 TONNES

total notices so far: 9605 contracts for 960,500 oz (29.875 tonnes)

SILVER NOTICES:

383 NOTICES FILED FOR 1,915,000 OZ/

total number of notices filed so far this month 3974 : for 19.870,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $1.60

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD

INVENTORY RESTS AT 1005.29 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 16 CENTS

AT THE SLV// ://HUGE CHANGES IN SILVER INVENTORY AT THE SLV//:A WITHDRAWAL OF 3.504 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 495.597 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 2114 CONTRACTS TO 149,220 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE HUGE GAIN IN OI WAS ACCOMPLISHED DESPITE OUR $0.24 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.24) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY COMMERCIAL SILVER LONGS//BUT MAINLY WE HAD ADDITIONAL SPECULATOR ADDITIONS AS WE HAD A GIGANTIC GAIN OF 2707 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A POOR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.220 MILLION OZ FOLLOWED BY TODAY’S 1,735,000 OZ QUEUE JUMP / // V) HUGE SIZED COMEX OI GAIN

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -16

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTACTS for 17 days, total 15,697 contracts: 78.485 million oz OR 4.616 MILLION OZ PER DAY. (923 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 78.485 MILLION OZ

.

LAST 15 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 78.485 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2114 DESPITE OUR $0.24 LOSS IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE CONTRACTS: 577 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER ADDITIONS ////// HUGE SPECULATOR SHORT ADDITIONS// WE HAVE A POOR INITIAL SILVER OZ STANDING FOR JUNE. OF 15.22 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 1,735,000 OZ // .. WE HAD AN ATMOSPHERIC SIZED GAIN OF 2707 OI CONTRACTS ON THE TWO EXCHANGES FOR 13.535 MILLION OZ DESPITE THE LOSS IN PRICE..

WE HAD 41 NOTICES FILED TODAY FOR 1,915,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A VERY STRONG SIZED 6664 CONTRACTS TO 491,736 AND further from THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: 973 CONTRACTS.

.

THE STRONG SIZED DECREASE IN COMEX OI CAME DESPITE OUR FALL IN PRICE OF $7.85//COMEX GOLD TRADING/MONDAY / WE MUST HAVE HAD ADDITIONAL SPECULATOR SHORT ADDITION ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //AND HUGE SPECULATOR SHORT ADDITIONS//HUGE ADDITIONS TO OUR BANKER LONGS!!

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JULY AT 2.914 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 6100 OZ

YET ALL OF..THIS HAPPENED WITH OUR FALL IN PRICE OF $7.85 WITH RESPECT TO FRIDAY’S TRADING

WE HAD A SMALL SIZED LOSS OF 168 OI CONTRACTS 0.5132 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6496 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 502,738

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 168 CONTRACTS WITH 6661 CONTRACTS DECREASED AT THE COMEX AND 6496 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 168 CONTRACTS OR 0.5132 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (6496) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (6661): TOTAL LOSS IN THE TWO EXCHANGES 165 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT ADDITIONS//STRONG BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JULY. AT 2.914 TONNES FOLLOWED BY TODAY’S 6,100 OZ QUEUE JUMP 3) ZERO LONG LIQUIDATION//SOME SPECULATOR SHORT COVERINGS/ //.,4) STRONG SIZED COMEX OPEN INTEREST LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

108,575 CONTRACTS OR 10,857,500 OZ OR 337.71 TONNES 17 TRADING DAY(S) AND THUS AVERAGING: 6386 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAY(S) IN TONNES: 337.71 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 337.71/3550 x 100% TONNES 8.52% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 337.71 TONNES (HUGE INCREASE FROM JUNE//WILL CLOSE IN ON THE RECORD EFP ISSUANCE IN MARCH 22//SURPASSED PREVIOUS RECORD HIGH NOV 21)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JULY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GIGANTIC SIZED 2114 CONTRACT OI TO 149,220 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 577 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 577 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 577 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2114 CONTRACTS AND ADD TO THE 577 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN ATMOSPHERIC SIZED GAIN OF 2691 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 13.455 MILLION OZ

OCCURRED DESPITE OUR FALL IN PRICE OF $0.24

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED UP 27.05 PTS OR 0.83% //Hang Sang CLOSED UP 342.94 OR 1,07% /The Nikkei closed DOWN 44.04 OR % 0.16. //Australia’s all ordinaires CLOSED UP 0.27% /Chinese yuan (ONSHORE) closed DOWN AT 6.7607//OFF SHORE CHINESE YUAN UP 6.7653// /Oil UP TO 98.34 dollars per barrel for WTI and BRENT AT 106.71// SHANGHAI CLOSED UP 27.05 PTS OR 0.83% //Hang Sang CLOSED UP 342.94 OR 1.07% /The Nikkei closed DOWN 44.04 OR % 0.16. //Australia’s all ordinaires CLOSED UP 0.27% / Stocks in Europe OPENED MOSTLY RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 6661 CONTRACTS TO 502,738 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS STRONG COMEX DECREASE OCCURRED DESPITE OUR FALL OF $7.85 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (6496 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 6496 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :6496 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 6496 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED SIZED TOTAL OF 165 CONTRACTS IN THAT 6496 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 6661 CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR GOOD SIZED FALL IN PRICE OF GOLD $ 7.85. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING JULY (29.987),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $7.85) BUT WERE UNSUCCESSFUL IN KNOCKING OFF SOME SPECULATOR LONGS/COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO COVER TO THEIR POSITIONS//// WE HAVE REGISTERED A SMALL SIZED LOSS OF 0.5132 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR JULY (29.987 TONNES)…

WE HAD -973 CONTRACTS ADDED TO COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 165 CONTRACTS OR 16,500 OZ OR 0.5132 TONNES

Estimated gold volume 228,118/// poor/

final gold volumes/yesterday 245,115 / fair

INITIAL STANDINGS FOR JULY ’22 COMEX GOLD //JULY 26

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 158,808.967oz Brinks HSBC Manfra 938 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | 50,762.574 oz Brinks |

| No of oz served (contracts) today | 41 notice(s) 4100 OZ 0,1275 TONNES |

| No of oz to be served (notices) | 36 contracts 3600 oz 0.1119 TONNES |

| Total monthly oz gold served (contracts) so far this month | 9605 notices 960,500 OZ 29.875 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

No dealer withdrawals

Customer deposits: 1

i) Into Brinks: 50,762.574 oz

total deposits: 50,762.574 oz

3 customer withdrawals:

i)Out of Brinks 72,406.490 oz

ii) Out of HSBC: 30,157.638 oz (938 kilobars)

iii)Out of Manfra: 50,762.574 oz

total withdrawals: 158,808.967 oz (4.93 tonnes)

ADJUSTMENTS:2 dealer to customer

Brinks: 13,792.226

JPMorgan: 33,105.985 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 77 contracts having GAINED 15 contracts . We had

45 notices filed on Monday so we GAINED a strong 61 contracts or an additional 6100 oz will stand in this non active

delivery month of July.

August has a LOSS OF 36,066 contracts down to 120,643 contracts. We have 3 more reading days before first day notice. Looks like we will have a strong August standing for gold (JULY 29/22..FIRST DAY NOTICE)

Sept. gained161 contracts to 3134 contracts.

We had 41 notice(s) filed today for 4100 oz FOR THE July 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 13 notices were issued from their client or customer account. The total of all issuance by all participants equate to 41 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 45 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2022. contract month,

we take the total number of notices filed so far for the month (9605) x 100 oz , to which we add the difference between the open interest for the front month of (JULY 77 CONTRACTS ) minus the number of notices served upon today 41 x 100 oz per contract equals 964,100 OZ OR 29.987 TONNES the number of TONNES standing in this active month of July.

thus the INITIAL standings for gold for the JULY contract month:

No of notices filed so far (9605) x 100 oz+ (77) OI for the front month minus the number of notices served upon today (45} x 100 oz} which equals 958,100 oz standing OR 29.987 TONNES in this active delivery month of JULY.

TOTAL COMEX GOLD STANDING: 29.987 TONNES (A FAIR STANDING FOR A JULY ( NON ACTIVE) DELIVERY MONTH)

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,443,533.842 oz 76.00 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 31,012,965.398 OZ

TOTAL REGISTERED GOLD: 15,451,836.344 OZ (48,06 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 15,561,129.054 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 13,008,303.0 OZ (REG GOLD- PLEDGED GOLD) 404.6 tonnes

END

SILVER/COMEX/JULY 26

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 3,330,259.329 oz CNT Delaware JPMorgan Brinks Loomis Manfra |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 383 CONTRACT(S) 19,870,000 OZ) |

| No of oz to be served (notices) | 11 contracts (55,000 oz) |

| Total monthly oz silver served (contracts) | 3974 contracts 19,870,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 0 deposits into the customer account

total deposit: nil oz

JPMorgan has a total silver weight: 175.149 million oz/337.508 million =51.88% of comex

Comex withdrawals:6

i) Out of Brinks: 602,026.800 oz

ii) Out of CNT: 400,433.879 oz

iii) Out of Delaware 999.760 oz

iv) Out of jPMorgan 717,682.900 0z

v) Out of Loomis: 1,108,606.990 oz

vi) Out of Manfra: 500,508.900 oz

adjustments: 1 customer to dealer//HSBC: 53,289.990 oz

2. removal of 306,543.000 oz from JPMorgan eligible

the silver comex is in stress!

TOTAL REGISTERED SILVER: 59.686 MILLION OZ

TOTAL REG + ELIG. 337.508 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JULY OI: 394 CONTRACTS HAVING GAINED 161 CONTRACTS. WE HAD 186 NOTICES FILED

ON MONDAY, SO WE GAINED 347 CONTRACTS OR AN ADDITIONAL 1,735,000 OZ WILL STAND FOR METAL AT THE COMEX.

AUGUST LOST 22 CONTRACTS TO STAND AT 936

SEPTEMBER HAD A GAIN OF 810 CONTRACTS DOWN TO 119,330

CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 186 for 230,000 oz

Comex volumes:42,939// est. volume today// poor

Comex volume: confirmed yesterday: 46,521 contracts ( poor )

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 3974 x 5,000 oz = 19,870,000 oz

to which we add the difference between the open interest for the front month of JULY(394) and the number of notices served upon today 383 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY./2022 contract month: 3974 (notices served so far) x 5000 oz + OI for front month of JULY (394) – number of notices served upon today (383) x 5000 oz of silver standing for the JULY contract month equates 19,925,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JULY 26/WITH GOLD DOWN $1.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.29 TONNES

JULY 25/WITH GOLD DOWN $7.85: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 1005.87 TONNES

JULY 22/WITH GOLD UP $17.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 21/WITH GOLD UP $11.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.101 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.87 TONNES

JULY 20/WITH GOLD DOWN $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1009.06 TONNES

JULY 19/WITH GOLD DOWN $.35 :BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.22 TONNES FROM THE GLD//INVENTORY RESTS AT 1009.06 TONNES

JULY 18/WITH GOLD UP $7.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.28 TONNES

JULY 15/WITH GOLD DOWN $3.75:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD///INVENTORY RESTS AT 1016.89 TONNES//

JULY 14/WITH GOLD DOWN $28.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD//INVENTORY RESTS AT 1019.79 TONNES

JULY 13/WITH GOLD UP $10.55:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD//INVENTORY RESTS AT 1021.53TONNES

JULY 12/WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESS AT 1023.27 TONNES

JULY 11/WITH GOLD DOWN $4.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD./INVENTORY RESTS AT 1023.27 TONNES

JULY 7/WITH GOLD UP $1.35: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.61 TONNES FORM THE GLD///INVENTORY REST AT 1024.43 TONNES

JULY 6/WITH GOLD DOWN $26.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 9.86 TONNES FROM THE GLD//INVENTORY REST AT 1032.04 TONNES

JULY 5/WITH GOLD DOWN $36.55//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.41 TONNES FROM THE GLD///INVENTORY RESTS AT 1041.90 TONNES

JULY 1/WITH GOLD DOWN $5.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES//INVENTORY RESTS AT 1050.31 TONNES

JUNE 30/WITH GOLD DOWN $9.20: big CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 1052.63 TONNES//

JUNE 28/WITH GOLD DOWN $3.05//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.64 TONNES FROM THE GLD///INVENTORY RESTS AT 1056.40 TONNES

JUNE 27/WITH GOLD DOWN $4.90 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.04 TONNES

JUNE 24/WITH GOLD UP 45 CENTS TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.70 TONNES FROM THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 23/WITH GOLD DOWN $8.60:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//INVENTORY RESTS AT 1071.77 TONNES

JUNE 22/WITH GOLD UP 15 CENTS:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1073.80 TONNES

GLD INVENTORY: 1005.29 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JULY 26/WITH SILVER UP 16 CENTS: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.504 MILLION OZ FROM THE SLV//: //INVENTORY RESTS AT 495.597 MILLION OZ//

JULY 25/WITH SILVER DOWN 24 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.383 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 499.101 MILLION OZ//

JULY 22/WITH SILVER DOWN 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 500.484 MILLION OZ//

JULY 21/WITH SILVER UP 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.19 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 500.484MILLION OZ/

JULY 20/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 8.253 MILLION OZ FORM THE SLV/INVENTORY RESTS AT 507.585 MILLION OZ//

JULY 19/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ//

JULY 18/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 4.995 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ.

JULY 15/WITH SILVER UP 31 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 3.226 MILLION OZ FORM THE SLV//INVENTORY RESTS AT 510.443 MILLIONOZ//

JULY 14/WITH SILVER DOWN 88 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 OZ FROM THE SLV// //INVENTORY RESTS AT 513.671 MILLION OZ

JULY 13/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SV//INVENTORY RESTS AT 514.501 MILLION OZ.

JULY 12/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.228 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 514.501 MILLION OZ//

JULY 11/WITH SILVER DOWN 17 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 5.533 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 517.729 MILLION OZ

JULY 7/WITH SILVER UP 3 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.889 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 523.262 MILLION OZ/

JULY 6/WITH SILVER UP ONE CENT: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 12.558 MILLION OZ FORM THE SLV///INVENTORY RESTS AT 528.151 MILLION OZ

JULY 5/WITH SILVER DOWN 55 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 540.709MILLION OZ//

JULY 1/WITH SILVER DOWN 61 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ//INVENTORY RESTS AT 540.709 MILLION OZ//

JUNE 30/WITH SILVER DOWN 41 CENTS : SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 738,000 OZ FROM THE SLV//INVENTORY RESTS AT 541.262 MILLION OZ//

JUNE 28/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.00 MILLION OZ..

JUNE 27/WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 24/WITH SILVER UP 10 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.137 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 23/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 2.029 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 545.137 MILLION OZ//

JUNE 22/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.166 MILLION OZ.

CLOSING INVENTORY 495.597 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

END

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

Federal Data Show JPMorgan Chase Is, By Far, the Riskiest Bank in the U.S.

By Pam Martens and Russ Martens: July 26, 2022

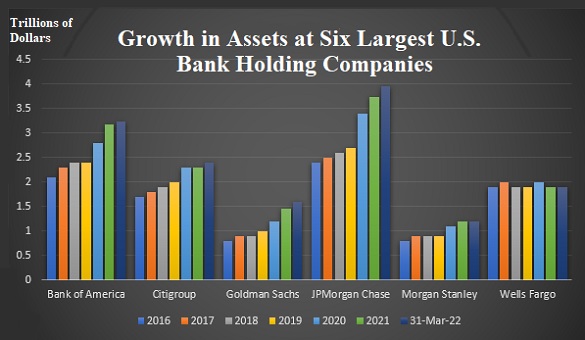

The long-tenured Chairman and CEO of JPMorgan Chase, Jamie Dimon, likes to use the phrase “fortress balance sheet,” when talking about his bank to Congress or shareholders. But the data stored at its federal regulators show that the bank is, by far, the most systemically dangerous bank in the United States. And, despite its high risk profile, neither Congress nor federal regulators have restricted its growth. Its assets have soared by 65 percent since the end of 2016 and stood at $3.95 trillion as of March 31, making it the largest bank in the United States.

Making this situation even more dangerous, the bank has admitted to five criminal felony counts over the past eight years and a multitude of civil crimes and multi-billion dollar fines — all during the tenure of Dimon. Neither Congress nor federal regulators nor the Justice Department that brought those felony counts has demanded that Dimon be replaced. The Board of Directors of the bank has been equally obsequious toward Dimon, awarding him a $50 million bonus after the bank admitted to its fourth and fifth felony counts for “tens of thousands” of trades that rigged the precious metals and U.S. Treasury markets.

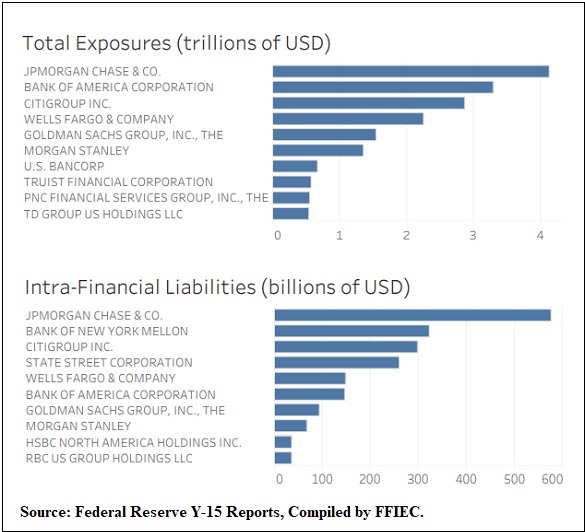

Our data comes from the National Information Center, a repository of bank data collected by the Federal Reserve. It is part of the Federal Financial Institutions Examination Council (FFIEC), which was created by federal legislation to create uniformity in the examination of U.S. financial institutions by the various banking regulators.

Each year the National Information Center creates a graphic profile of banks measured by 12 systemic risk indicators. The data used to create these graphics come from the “Systemic Risk Report” or form FR Y-15 that banks are required to file with the Federal Reserve. To measure the systemic risk that a particular bank poses to the stability of the U.S. financial system, the data is broken down into five categories of system risk: size, interconnectedness, substitutability, complexity, and cross-jurisdictional activity. Those measurements consist of 12 pieces of financial information that banks have to provide on their Y-15 forms.

The most recent data is for the period ending December 31, 2020. It indicates that in 8 out of 12 measurements – or two-thirds of all systemic risk measurements – JPMorgan Chase ranks at the top for having the riskiest footprint among its peer banks.

One of the 12 financial metrics is based on the Intra- Financial System Liabilities of each bank. This shows how much money a particular bank has at risk at other banks by using inputs such as how much of its funds it has on deposit with, or has been lent to, other financial institutions; the unused portion of any credit lines it has committed to other financial institutions; and its holdings of debt, equity, commercial paper, etc. of other financial institutions. The idea is to understand the interconnectivity of systemically- risky megabanks and whether one distressed megabank could cause a daisy-chain of contagion with other megabanks — such as the contagion caused by Citigroup and Lehman Brothers in 2008.

JPMorgan Chase’s footprint for Intra-Financial System Liabilities is huge. The 2020 data show that JPMorgan Chase has $577 billion exposure in that category. That’s an increase of $182 billion over what it showed in that category in 2019 – a startling increase of 46 percent in one year.

Equally unnerving, JPMorgan Chase ranks number one in the instruments that played a major role in blowing up Wall Street in 2008 – OTC (Over-the-Counter) derivatives. These are private contracts between two parties and lack the transparency or protections of being traded on an exchange. This means if the counterparty defaults and the exposure is large enough, it could put a federally-insured bank at risk. This is not a hypothetical scenario. The giant insurer, AIG, blew itself up in 2008 because it was holding tens of billions of dollars in OTC derivative contracts for the biggest banks on Wall Street, on which it could not pay its obligations. The U.S. government was forced to nationalize AIG and paid more than $90 billion to the banks for their AIG derivative contracts and securities lending obligations. According to the data, JPMorgan Chase has the largest exposure to OTC derivatives, with $44.38 trillion exposure.

The Dodd-Frank financial reform legislation of 2010 was hyped as ending the hubris of OTC derivatives. It was supposed to force these vehicles into the sunlight of exchanges and central clearinghouses. But that hasn’t happened. Corporate business media is simply declining to report on it. According to the Office of the Comptroller of the Currency, the federal regulator of national banks, as of March 31, 2022, only “43.4 percent of banks’ derivative holdings were centrally cleared.” (See page 13 at this link.) That statistic comes 12 years after Dodd-Frank was signed into law, showing just how lax federal regulators have been in enforcing the congressional intent of the law.

Adding to the systemic dangers of JPMorgan, it is a pivotal cog in the U.S. payments system. The bank was responsible for $510 trillion of the U.S. payments system in 2020 – a 51 percent increase over its size in that category in 2019. The $510 trillion is more than the next three largest banks in that category combined: Bank of New York Mellon at $194.23 trillion; Citigroup at $176.57 trillion; and Bank of America at $138.34 trillion.

And despite Dimon perpetually bragging about the bank’s “fortress balance sheet,” the Federal Reserve has yet to explain why a unit of JPMorgan Chase (J.P. Morgan Securities) needed to secretly borrow a cumulative $2.59 trillion in repo loans from the Fed in the last quarter of 2019 – long before the first case of COVID-19 appeared in the U.S. (See chart below.)

The Senate Banking Committee has told Wall Street On Parade that it will be scheduling its annual hearing with Wall Street CEOs before the year is out. The Committee needs to stop using Wells Fargo as a convenient punching bag and focus on the dangerous elephant in the room – JPMorgan Chase. (By the way, Wells Fargo did not rank number one in even one of the 12 systemic risk categories.)

-END-

end

3. Chris Powell of GATA provides to us very important physical commentaries

How novel: Zimbabwe goes for gold coins to fight high inflation

(Washington Post)

Zimbabwe goes for the gold (coins) to fight high inflation

Submitted by admin on Mon, 2022-07-25 22:28Section: Daily Dispatches

By Lesley Wroughton

The Washington Post

Monday, July 25, 2022

With inflation soaring in Zimbabwe and the country’s currency in free fall as people abandon it for the U.S. dollar, the government of President Emmerson Mnangagwa is fighting back with a novel strategy: gold coins.

Starting Monday, Zimbabwe is selling one-ounce, 22-carat gold coins bearing an image of Victoria Falls, its world-famous natural wonder. Each has a serial number, comes with a certificate and will be sold at a price “based on the prevailing international price of gold and the cost of production,” the central bank said in its announcement on July 4.

The coins will be tradable both in Zimbabwe and overseas, the bank said, and can be exchanged for cash. The goal is to reduce the quantity of Zimbabwe dollars in circulation to eventually restore that currency’s value.

What’s unknown is whether the approach has any real chance of success.

While gold is traditionally the ideal hedge against inflation and general economic uncertainty, no country has previously tried to tackle a weakening currency by selling gold coins. “In that sense, it is unusual,” said Carlos Caceres, the International Monetary Fund’s representative to Zimbabwe.

And with gold trading at $1,710 per troy ounce late last week, institutional investors may be the coins’ principal buyers.

“No ordinary person will be able to afford it,” said Prosper Chitambara, a senior researcher at the Labor and Economic Development Research Institute of Zimbabwe. “Right now, Zimbabweans are living hand-to-mouth.”…

… For the remainder of the report:

https://www.washingtonpost.com/world/2022/07/25/zimbabwe-gold-coin-inflation/

END

END

4. OTHER GOLD/SILVER COMMENTARIES

JPMorgan Spoofing Trial May End Without Defendants’ Testimony

July 25, 2022, 6:45 PM

Chicago jury hears from first defense witness on Monday

Attorneys signal defendants won’t take to the stand themselves

Two former JPMorgan Chase & Co. gold traders and a salesman on the bank’s precious metals desk signaled they won’t take the stand at a trial where they’re charged with conspiring to use spoof trades to manipulate prices for years…

END

5.OTHER COMMODITIES: WHEAT

Wheat prices jump after Russian missiles hit Odessa, a major port for exporting wheat from Ukraine

(zerohedge)

Wheat Prices Jump After Russian Missiles Hit Odessa

TUESDAY, JUL 26, 2022 – 02:45 AM

Wheat prices soared Monday after Russia attacked the Black Sea trade port in Odessa, Ukraine, on Saturday. The strike comes less than one day after Ukraine and Russia brokered an export deal — mediated by Turkey — to export millions of tons of grains.

On Friday, officials from the U.N., Turkey, Russia, and Ukraine signed an agreement to reopen three ports, including Odessa, the country’s largest port. It’s a move heralded by these officials to alleviate a global food crisis.

Kremlin spokesman Dmitry Peskov insisted the weekend missile attack is “in no way related to infrastructure used for the export of grain.”

Meanwhile, Ukraine Infrastructure Minister Vasyl Shkurakov said the deal should come into effect in days and the first shipment later this week.

Chicago wheat futures jumped 4.6% and traded 1.9% higher as of 1230 ET. Prices slid 10% in the days leading to the signing of the export deal.

“Wheat futures jumped after Russia struck Odessa’s sea port, sparking doubt over its commitment to free Ukrainian grain exports. Moscow said it hit a “military infrastructure facility,” Goldman Sach’s John Flood wrote in a note Monday.

Wall Street firms are saying the “attack on last Saturday is raising doubts about the resumption of the port activity in appropriate conditions,” Agritel said in a note to clients.

“The market will inevitably remain very nervous in the event of new bombings or doubts about the concrete implementation of this resumption of export activity,” Agritel continued.

“It is thought to be unlikely that much will move from Ukraine right away as the infrastructure internally and at the ports needs to be rebuilt,” Jack Scoville, an analyst at Price Futures Group Inc, wrote.

Ukraine will press ahead with reopening Odessa as traders monitor grain flows from the port, watching for signs of how quickly volumes come online and determining the next move for wheat prices.

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7607

OFFSHORE YUAN: 6.7653

HANG SANG CLOSED UP 342.94 PTS OR 1.67%

2. Nikkei closed DOWN 44.04 OR 0.16%

3. Europe stocks CLOSED MOSTLY RED EXCEPT LONDON

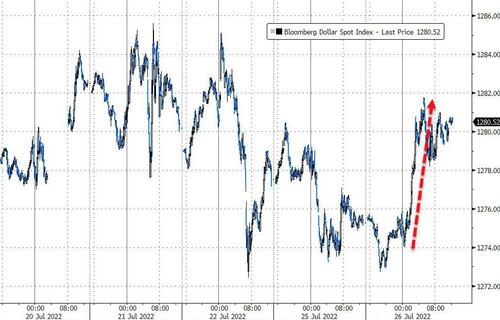

USA dollar INDEX UP TO 106,97/Euro FALLS TO 1.0137

3b Japan 10 YR bond yield: FALLS TO. +.200/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 136.70/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

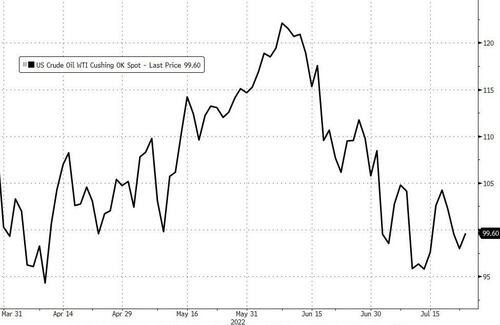

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.045%/Italian 10 Yr bond yield RISES to 3.40% /SPAIN 10 YR BOND YIELD FALLS TO 2.27%…

3i Greek 10 year bond yield FALLS TO 2.987//

3j Gold at $1716.80 silver at: 18.45 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 74/100 roubles/dollar; ROUBLE AT 58.85

3m oil into the 98 dollar handle for WTI and 106 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 136.70DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9657– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9783well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

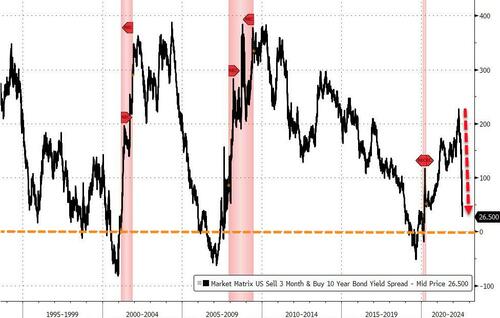

USA 10 YR BOND YIELD: 2.765 DOWN 3 BASIS PTS

USA 30 YR BOND YIELD: 2.999 DOWN 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.85

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Fizzle As Walmart Warning Batters Bear Market Rally

TUESDAY, JUL 26, 2022 – 08:09 AM

US stock futures dropped as investors braced for Wednesday’s Federal Reserve meeting, while Walmart’s surprise profit warning fueled concerns about the strength of US consumer spending. A barrage of earnings including notable misses by the likes of GM and a 3M guidance cut, did not help the mood. Contracts on the S&P 500 and the Nasdaq 100 were each down 0.4% by 7:45am in New York. European stocks rose driven by energy stocks amid a fresh surge in gas prices following Russia warnings of an imminent halving in NS1 shipments even as European Union countries reached a political agreement to cut their gas use. The dollar jumped and 10Y yields tumbled below 2.75% as a recession looks inevitable, no matter how Biden defines it.

In premarket trading, Alibaba Group jumped 5.1% after the Chinese e-commerce giant said it will seek a primary listing in Hong Kong, boosting other US-listed Chinese stocks with it. Cryptocurrency-exposed stocks were lower as Bitcoin sank to a one-week low, denting hopes for a sustained rebound. Coinbase fell 4% in premarket trading after a Bloomberg News report that the cryptocurrency company is facing a US probe into whether it improperly let Americans trade digital assets that should have been registered as securities. Shares of US big-box retailers and e-commerce peers fell in US premarket trading on Tuesday, after Walmart again cut its quarterly and full-year profit guidance just weeks ahead of its earnings report, raising new questions about the damage from surging inflation to consumers’ spending ability. The shares slid as much as 9.8% in US premarket trading. In premarket trading, Target shares drop as much as 4.9%, Costco Wholesale -2.8%; watch Best Buy shares for later in the session

Online retailers also fall amid broader worries over the sector, Amazon -3.8%, Etsy -4.1%, EBay -0.6%, Shopify -6% after a PT cut at Citi; also watch Wayfair and Chewy. Here are some other notable pre-market movers:

- Shopify (SHOP US) shares fall as much as 6% in US premarket trading, as Citi cuts its price target on the e- commerce platform provider amid fresh economic headwinds.

- Cryptocurrency-exposed stocks are lower in US premarket trading as Bitcoin sank to a one-week low on Tuesday. The group is also pressured after a Bloomberg News report about the US Securities and Exchange Commission probing Coinbase over cryptocurrency listings.

- Alibaba (BABA US) shares jump 5.1% in US premarket trading after the Chinese e-commerce giant said it will seek a primary listing in Hong Kong, boosting other US-listed Chinese stocks higher with it.

- F5 (FFIV US) shares rise 7.8% in premarket trading on Tuesday, after the communications equipment company forecast better-than-expected adjusted earnings for the fourth- quarter.

- Koss Corp. (KOSS US) shares fall as much as 18% in US premarket trading, setting the headphones maker on track to trim part of the 43% surge it posted the previous session after reaching a deal with Apple in an AirPods patent infringement case.

- NXP Semiconductors (NXPI US) shares are down 1.2% in US premarket trading even as the company issued a strong forecast for the current quarter driven by demand for components used in automobiles. Analysts note that while supply is improving, demand continues to outstrip it.

- Aaron’s Co (AAN US) shares fell as much as 35% in postmarket trading on Monday as its revenue and earnings guidance cut shows the pressures facing the furniture and appliances retailer, with analysts anticipating that macro headwinds will continue to weigh

Meanwhile, investors are bracing for a flurry of earnings this week to gauge the ability of corporates to overcome supply constraints and soaring prices, just as the S&P 500 is on a course for its best month since October. A barrage of reports from GE, GM, 3M, RTX, MCD And UPS painted a mixed picture, with GE and 3M rising post-results while GM and UPS drop.

“There is still scope in the second half of this year, and maybe even early next year, for earnings disappointment,” said Paul Jackson, Invesco’s global head of asset allocation research, in a Bloomberg TV interview. “There’s still probably a delayed reaction for earnings, and then you have a layer on top of that, the margins squeeze that’s coming through higher raw material costs and in some sectors higher labor costs.”

Coca Cola Inc., McDonald’s Corp. and Mondelez International Inc. are among companies reporting earnings before the market open, while Texas Instruments Inc., Visa Inc., Microsoft Corp. and Alphabet Inc. will report after hours. These results “could really define an earnings season which, up until now, has been pretty resilient given the backdrop,” said Russ Mould, investment director at AJ Bell.

Tomorrow we also get the highlight of the week when the Fed is strongly expected to hike rates by 75 basis-points with many speculating that the Fed will have to inflict much more pain on the Biden economy to get inflation under control.

“For the time being, the Fed and other major central banks look much more concerned about the risk of inflation expectations becoming unanchored than high risk weighing on growth,” Valentine Ainouz, deputy head of developed markets research at Amundi, said in a Bloomberg TV interview. “Maybe in some months we will have a pivot toward growth, but this is not the mood right now, the mood now is fighting inflation.”

Markets are underestimating the risks of persisting inflation, which is likely to keep central banks hawkish for longer, according to Goldman Sachs strategists. Investors appear to be more optimistic on the central bank put, given that in past cycles the policy makers made a dovish pivot when growth slowed, strategists led by Cecilia Mariotti wrote in a note.

“The Fed’s main enemy is inflation, and it’s desperate to prevent expectations of sustained inflation from taking hold,” said Frédéric Leroux, a member of Carmignac’s strategic investment committee. “The recession that the Fed will probably provoke by its current monetary tightening is an avatar that it can withstand. In fact, it’s not beyond the realms of possibility that the central bank wants a recession, given the bearish effects it would have on prices.”

For Katerina Simonetti, an adviser at Morgan Stanley Private Wealth Management, the litany of risks exposes the vulnerability of the 6% rebound in global shares from June lows.

“This is most likely a bear market rally and there are significant risks still facing this market,” she said on Bloomberg Television. “We’re probably going to be seeing a lot of choppiness and potentially some further declines in the market before the year end.”

European shares edged higher, led by the FTSE 100 which climbed on rising oil and metal prices. Currencies are mostly steady and yields dipped ahead of the Fed meeting tomorrow. Euro Stoxx 50 is little changed. FTSE 100 adds 0.8%, FTSE MIB lags, dropping 0.4%. European energy and mining stocks outperform while retailers, autos and telecoms are the worst performing Stoxx 600 sectors. Here are some of the biggest European movers today:

- UBS shares drop as much as 7.2% after reporting 2Q results that missed expectations. Underlying pretax profit was about 10% below consensus with analysts pointing to a charge in Corporate Center.

- Eutelsat shares fall as much as 14%, extending yesterday’s losses, after the French satellite operator and OneWeb are set to combine in an all-share deal valuing its UK rival at $3.4 billion.

- Uniper drops for a fourth day, with shares down as much as 12.6% as a further supply reduction from Russia’s Gazprom helped send gas prices higher.

- Kesko shares fall as much as 7.6% after the Finnish consumer retail group published its latest earnings, which included declining margins in its Building & Technical retail segment in an otherwise solid report, Kepler Cheuvreux writes.

- Veolia shares fall as much as 4.4% as the stock was reinstated with an underweight rating at JPMorgan, with the broker bearish on the impact the French water and waste management group will face from Europe’s energy crisis.

- European retailers slump after Walmart cut its profit outlook, raising new questions about the resilience of consumer spending with inflation at a four-decade high. Zalando declines as much as -6.9%, Ahold -3.7%, Marks & Spencer -5.2%

- Unilever shares gain as much as 3.2% after the consumer-goods company reported 2Q sales that topped market expectations. Analysts found the sales beat reassuring, though noted the company had maintained its margin outlook for the year.

- Energy and mining shares are among best-performing groups in the Stoxx Europe 600 index on Tuesday as oil and metals rallied amid a decline in the dollar and signs of tightness in some commodity markets. Shell gains as much as 2.7%, BP +2.4%, Equinor +5.6%; Glencore +3%, Anglo American +3.3%

Earlier in the session, Asian stocks edged higher, rebounding from Monday’s decline, helped by a rally in Alibaba Group and other Chinese tech shares. The MSCI Asia Pacific Index advanced as much as 0.4%. Alibaba was the biggest contributor to the gauge’s gains after saying it will seek a primary listing, a move that would allow it to seek inclusion in the Stock Connect link with the Shanghai and Shenzhen exchanges. Sector-wise, consumer discretionary and financials were the top performers. Stocks in China gained despite a resurgence of Covid-19 infections that could threaten the operations of industry giants including BYD and Huawei Technologies, while Hong Kong’s equity benchmark was the best performer in the region. Investors are gearing up for a week of earnings releases from some of the biggest tech companies in the US, with the Fed’s meeting also in focus for further insights on the pace and quantum of rate increases. The MSCI Asiagauge jumped 3.6% last week.

“Despite the slew of data pointing to ongoing growth slowdown, markets seem to have been accustomed to such narrative lately, riding on expectations that growth risks have been priced to a large extent,” Jun Rong Yeap, a market strategist at IG Asia, wrote in a note. “That will clearly be put to the test to a greater extent this week with a series of big tech earnings, Fed’s policy guidance, along with key US inflation and consumer sentiment data ahead,” he wrote.

Key stock gauges in India declined ahead of the anticipated interest rate hike by the US Federal Reserve. The S&P BSE Sensex fell 0.9% to 55,268.49 in Mumbai, while the NSE Nifty 50 Index declined by a similar measure. The 30-member Sensex had 21 stocks trading lower. A gauge of information technology companies fell the most among the 19 sectoral indexes compiled by BSE Ltd., all of which declined. Software exporters Infosys and Tata Consultancy Services slipped as investors assessed global recession risks and increasing margin pressure on Indian technology companies. The Fed is expected to hike interest rates by 75 basis points on Wednesday to tame four-decade high inflation.

In FX, the dollar climbed, snapping three days of losses, as traders brace for a widely expected 75 basis points Fed rate rise on Wednesday, part of campaign to tackle inflation.The Japanese yen was little changed at 136.58 per dollar. Sterling fell, erasing gains after touching a three-week high against a broadly sluggish US dollar; still, it’s clinging on to $1.20, leading traders to watch if it can see out the month above key psychological levels.

In rates, treasuries are underpinned by rally in bunds amid concerns about European gas supply. Gains led by belly of the curve, eroding concession ahead of 5-year auction at 1pm New York time. US yields are richer by 2bp-4bp across the curve with the 10Y yield dropping to 2.75%, and a belly-led advance steepening 5s30s spread by 1.7bp; 2s5s30s fly drops 3.7bp on the day onto tightest levels since March ahead of 5- year sale. The final coupon auction cycle of May-July quarter continues with $46b 5-year note sale, following Monday’s solid 2-year auction. WI 5-year yield around 2.84% is ~43bp richer than June result, a 3.5bp tail. European peripheral spreads are mixed to Germany; Italy widens, Spain and Portugal tightens. Bunds advanced for a fifth day, the longest run since August as focus remains on gas supply concerns.

In commodities, crude futures rose for the 2nd day: WTI drifts 2.1% higher to trade near $98.74. Brent rises 1.8% near $107.07. Most base metals trade in the green; LME copper rises 2.8%. Spot gold rises roughly $4 to trade near $1,724/oz. Spot silver gains 1.1% near $19.

Todays’s economic data slate includes May FHFA house price index, S&P Case-Shiller house prices (9am), July Richmond Fed manufacturing index, consumer confidence, June new home sales (10am); this week also includes durable goods orders, 2Q GDP, personal income/spending (includes PCE deflator), MNI Chicago PMI and University of Michigan sentiment.

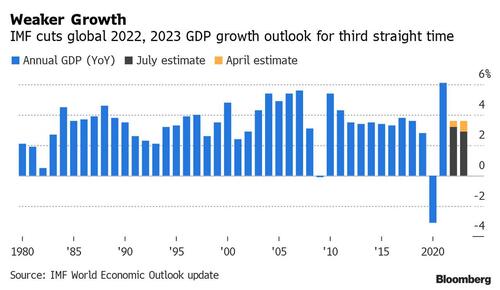

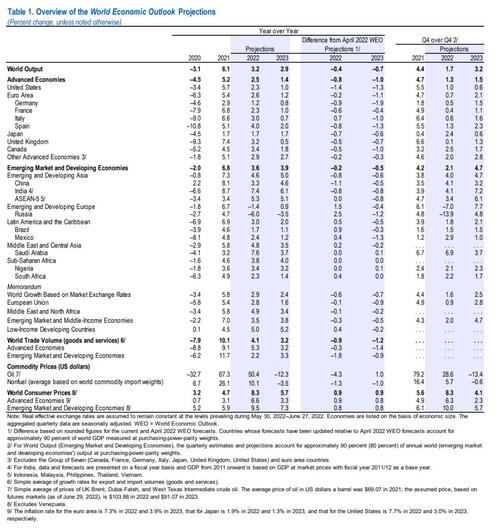

In terms of today we have the US July Conference Board consumer confidence index, Richmond Fed manufacturing index, June new home sales, and the May FHFA house price index. As discussed above EU energy ministers meet. Earnings is in full bloom with Microsoft, Alphabet, Visa, LVMH, Coca-Cola, McDonald’s, UPS, Texas Instruments, Raytheon Technologies, Unilever, Mondelez, 3M, General Electric, UBS, General Motors, ADM, Chipotle, and Deutsche Boerse all reporting. Elsewhere the IMF release their economic outlook update. Last but by no means least the FOMC start their crucial two-day meeting.

Market snapshot

- S&P 500 futures down 0.2% to 3,960.50

- STOXX Europe 600 up 0.1% to 426.79

- MXAP up 0.3% to 159.28

- MXAPJ up 0.5% to 522.24

- Nikkei down 0.2% to 27,655.21

- Topix little changed at 1,943.17

- Hang Seng Index up 1.7% to 20,905.88

- Shanghai Composite up 0.8% to 3,277.44

- Sensex down 0.7% to 55,385.81

- Australia S&P/ASX 200 up 0.3% to 6,807.27

- Kospi up 0.4% to 2,412.96

- German 10Y yield little changed at 0.98%

- Euro little changed at $1.0215

- Gold spot up 0.2% to $1,723.33

- U.S. Dollar Index little changed at 106.50

Top Overnight News from Bloomberg

- UBS Group AG’s investment bank disappointed in the second quarter as global deal activity collapsed and the trading business struggled to keep pace with Wall Street peers.

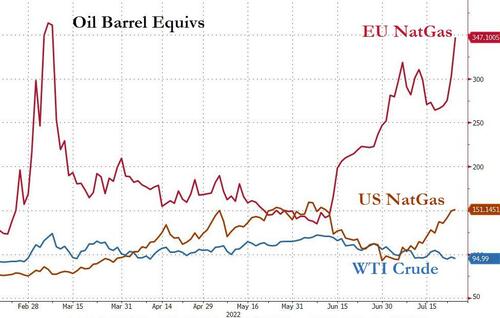

- European natural gas prices surged to the highest level in more than four months, as the region braces for a further reduction in Russian supply that could severely dent efforts to keep the lights on and homes warm this winter.

- Alibaba Group Holding Ltd. will seek a primary listing in Hong Kong, entrenching the financial hub’s status as an alternative to US markets and paving the way for investors in China to directly buy shares of the country’s most prominent e-commerce company for the first time.

- Coinbase Global Inc. is facing a US probe into whether it improperly let Americans trade digital assets that should have been registered as securities, according to three people familiar with the matter.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks took their cue from Wall Street and eventually traded mostly higher, albeit some with mild gains, after seeing mixed trade in the early hours until the Chinese open. ASX 200 was supported by its energy and mining sectors as underlying oil and metals prices rose, Nikkei 225 moved back toward the 27.5k mark to the downside amid currency dynamics whilst the KOSPI was kept afloat after Q2 GDP topped expectations. Hang Seng overlooked reports that Hong Kong may have to downgrade its annual growth forecast and surged amid a boost from Alibaba rising almost 4% as it plans for a primary listing in Hong Kong, which would make it eligible for the Stock Connect programme and allow mainland Chinese investors to trade Co. shares, in turn helping increase liquidity. Shanghai Comp posted modest gains, but the upside was capped as Shanghai added 10 high and medium-risk areas subject to lockdown.

Top Asian News

- Shanghai adds 10 high and medium-risk areas subject to lockdown, according to Bloomberg.

- Alibaba (9988 HK/BABA) is pursuing a primary listing on the Hong Kong exchange, expected to occur before the end of 2022; Co. will become a dual primary listed Co. on HKEX and NYSE.

- Hong Kong may have to downgrade its annual growth forecast in August for the second time in three months, according to SCMP citing the finance chief.

- PBoC set USD/CNY mid-point at 6.7483 vs exp. 6.7490 (prev. 6. 7543).

- PBoC injected CNY 5bln via 7-day reverse repos with the maintained rate of 2.10% for a net drain of CNY 2bln

European bourses are under modest pressure, Euro Stoxx 50 -0.4%, in what has been a limited session of newsflow ahead of the EU energy update and US earnings; though, strength in commodities is lifting the FTSE 100 +0.5%. However, further pressure has been seen in wake of most recent Kremlin related commentary, with the Nord Stream 1 turbine yet to be installed. Stateside, US futures are dented to the tune of crica. 5/10s of a percent; but, fairly rangebound (ex-above Kremlin related moves) overall pre-earnings and Wednesday’s FOMC.

Top European News

- Porsche IPO, Software Fix: What Awaits VW’s New CEO

- European Oil and Mining Stocks Outperform Amid Commodity Gains

- Hedging Bond Trades Is Getting Harder in UK’s Volatile Markets

- Rolls-Royce Names Ex-BP Executive as CEO to Succeed East

- Beijing Denounces Truss Vow to Crack Down on China Firms in UK

- UBS CEO Hamers Signals Worst Over for Asia Deleveraging

Central Banks

- RBNZ Governor Orr says in addition to remit review, RBNZ will also review recent performance in conducting monetary policy; will assess inflation and employment outcomes relative to targets, via Reuters.

- CNB’s Frait says policy is already quite restrictive, won’t rule out a hike now or in the near time. Temporary FX interventions are normal in situations of shock to balance of payments, via Reuters.

FX

- Aussie fades after probing Fib resistance vs Greenback and Loonie following oil powered rise to best levels since mid-June, AUD/USD back under 0.6950 from 0.6983, USD/CAD above 1.2880 from sub-1.2820.

- Dollar regains poise otherwise in choppy, cautious trade pre-FOMC, DXY rebounds firmly from 106.190 surpassing Monday high of 106.890 to 107.10+.

- Yen and Franc find some traction from pronounced bounce in bonds and reversion to bull-flattening, USD/CHF and USD/JPY hold below/above 0.9650 and 136.50 respectively.

- Euro undermined by ongoing Russian gas supply jitters ahead of Extraordinary Energy Summit, EUR/USD retreats from 1.0250 to circa 1.0140.

- Pound pulls up after narrowly missing 1.2100 vs Buck, Cable now below 1.2000, albeit still relatively comfortably above a series of recent descending lows.

Fixed Income

- Bonds back in bull-flattening mode as Bunds front run latest leg higher.

- 10 year German benchmark reaches 155.90 and peaks not seen since late May, while yield breaches 1% with more conviction.

- Gilts and T-notes lag within 117-6935 and 120-04/119-24 respective ranges ahead of the Fed tomorrow and BoE next week.

- BTPs off lest levels and lag periphery peers amidst short term and linker supply.

Commodities

- Dutch TTF continues to lift with the August contract in proximity to EUR 200 as Nord Stream 1 is set to be curtailed tomorrow; however, the EU has agreed on a deal to reduce gas use.

- Crude benchmarks are bid and drawing impetus from the referenced factors and EU divisions, though the magnitude of the move is more modest in nature vs TTF.

- EU nations agree to reduce gas use for next winter.; only Hungary voted against approval of mandatory gas rationing if Russia shuts off the taps, France24 reports. Reminder, press conferences are expected at 12:30BST/07:30ET and 15:00BST/10:00ET.

- EU energy chief Simson says Europe has to be prepared for supply cuts from Russia at any moment, expects to have a deal today in curbing gas demand.

- Libyan oil minister says oil production is 1.1mln BPD.

- China is to lower retail prices of gasoline and diesel by CNY 300 and CNY 290/tonne respectively as of July 27th.

- Spot gold is little changed overall and moving at the whim of the USD while base metals remain bid in a continuation of APAC trade.

Crypto

- Coinbase (COIN) faces SEC probe over crypto listings, according to Bloomberg sources.

- US House lawmakers are reportedly delaying consideration of a bipartisan bill to regulate stablecoins, according to WSJ citing sources, pushing back consideration of the measure until after Congress’ August break.

US Event Calendar

- 09:00: May FHFA House Price Index MoM, est. 1.5%, prior 1.6%

- 09:00: May S&P/CS 20 City MoM SA, est. 1.50%, prior 1.77%

- 09:00: May S&P CS Composite-20 YoY, est. 20.60%, prior 21.23%

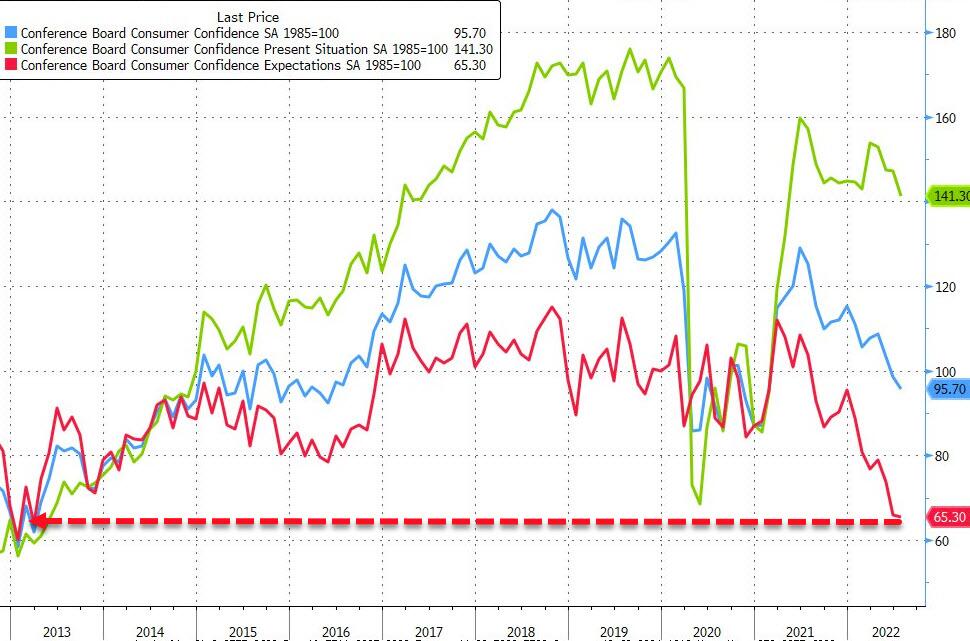

- 10:00: July Conf. Board Consumer Confidence, est. 97.0, prior 98.7

- Expectations, prior 66.4

- Present Situation, prior 147.1

- 10:00: July Richmond Fed Index, est. -14, prior -11

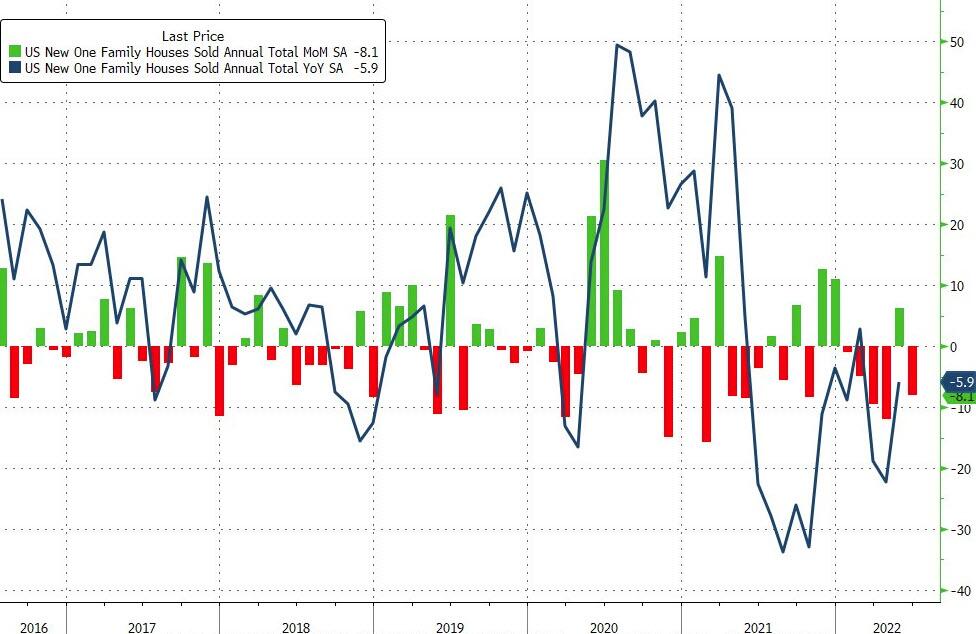

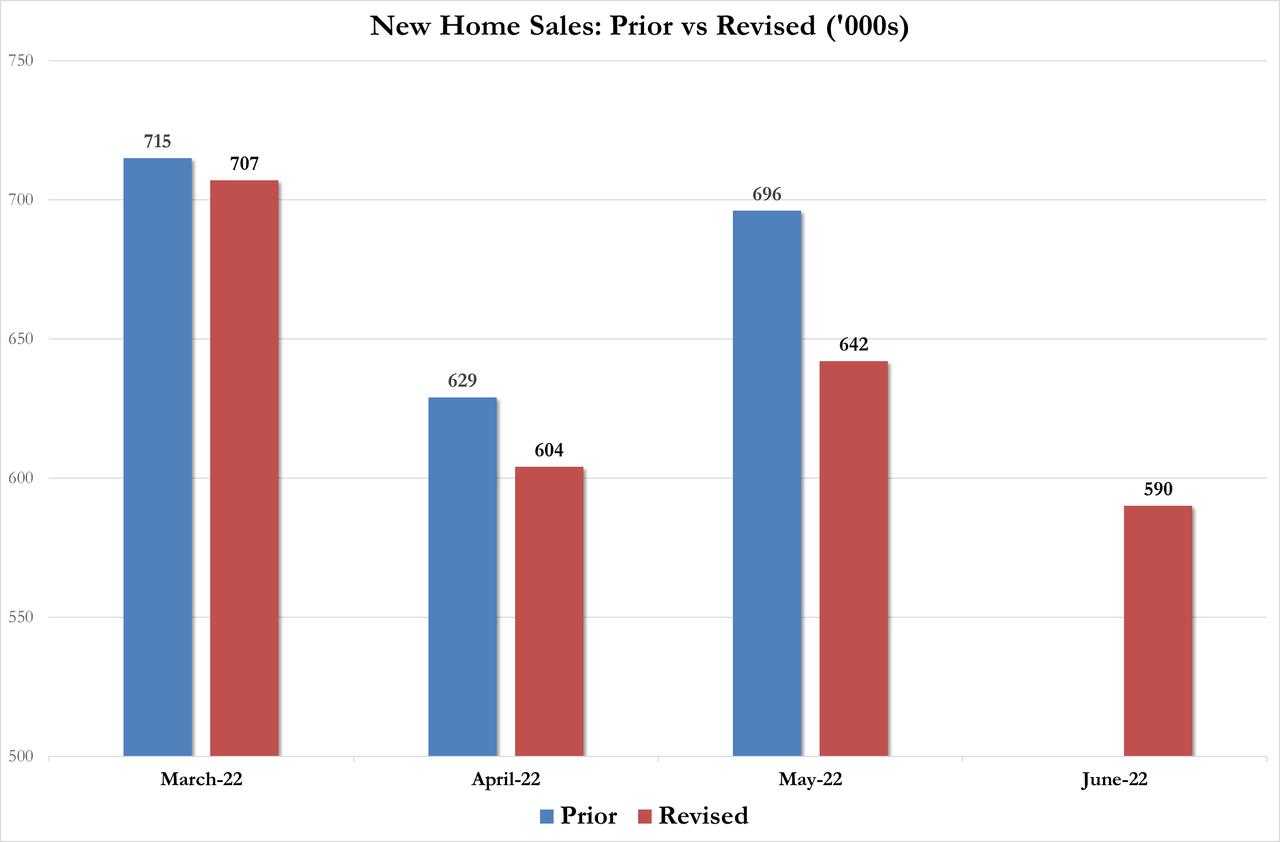

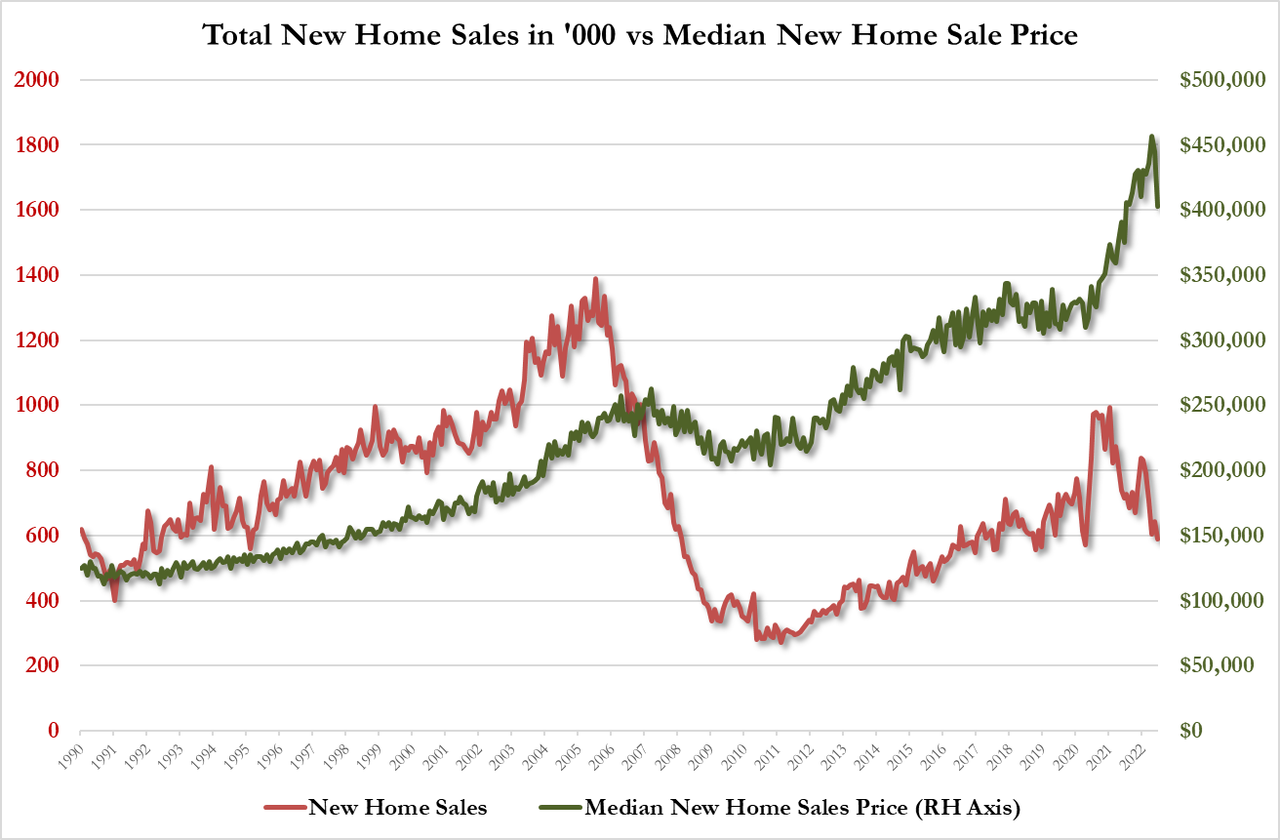

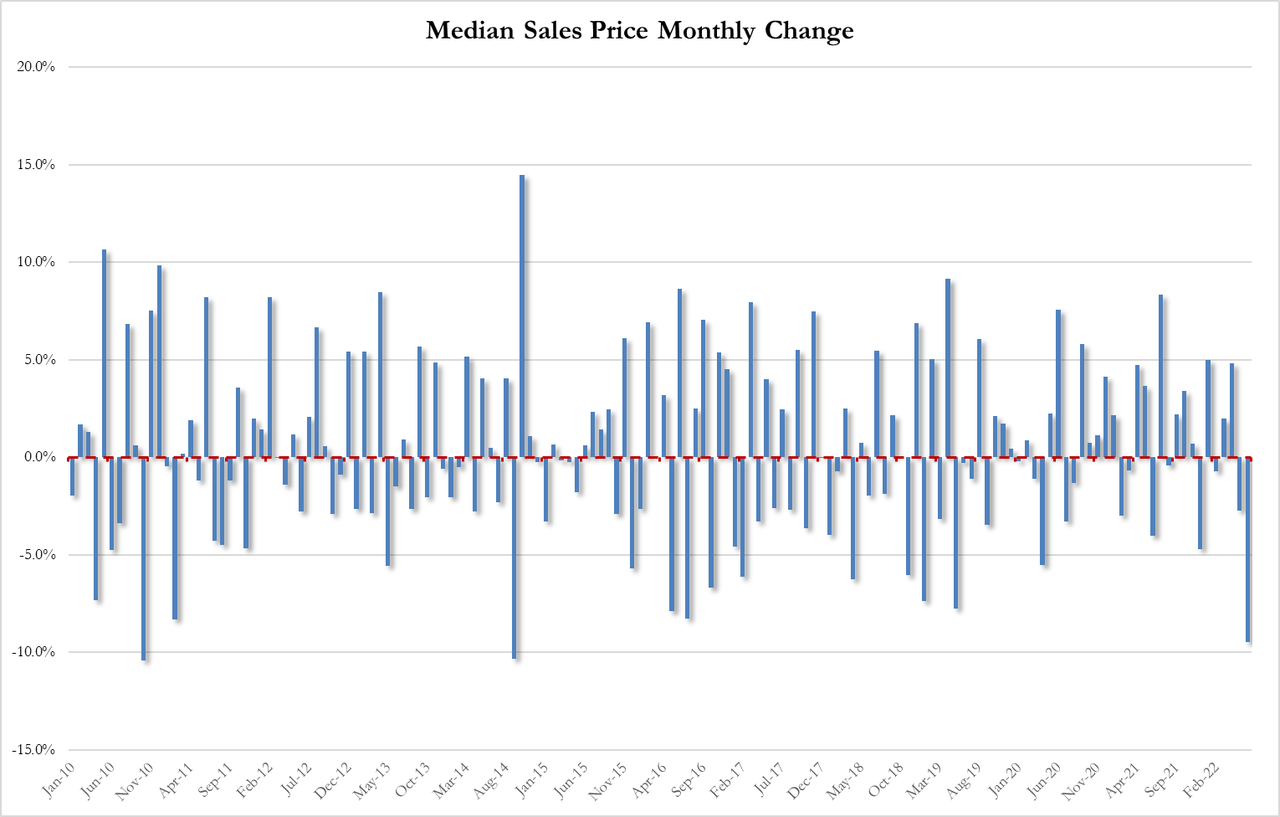

- 10:00: June New Home Sales MoM, est. -5.4%, prior 10.7%

- June New Home Sales, est. 658,000, prior 696,000

DB’s Jim Reid concludes the overnight wrap

10 years ago today Draghi uttered the seminal lines “whatever it takes” when referring to keeping Europe together when ECB President. It clearly worked but a decade later, Europe is again facing testing times, still partly because of Italy but also because of inflation and an energy crisis that has flared up again over the last 24 hours.

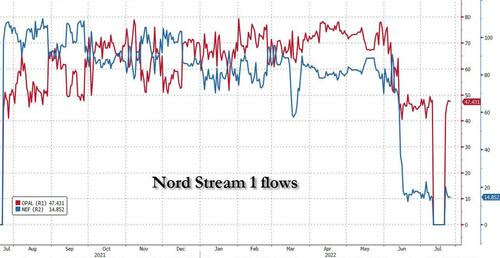

Indeed in yesterday’s EMR we discussed how this week was all about the US (FOMC and likely technical recession confirmation) but that we needed to watch the gas flows as Putin had suggested late last week that if the turbine didn’t make it back to Russia by early this week gas flows could be cut back from 40% capacity to 20% due to works being required on another turbine. The news flow yesterday was originally more positive as documentation between Siemens and Gazprom seemed to indicate that the repaired turbine issue was getting closer to being finalised. However the day turned late in the European session as Gazprom announced that another turbine will go out of service at 7am tomorrow for maintenance and gas would indeed be cut back to 20%. We can’t say we weren’t warned I suppose. It’s a bit confusing as to whether this will be a short restriction of supply while the repaired turbine makes its way back online or whether the paperwork will never quite be resolved, and we live with only 20% supplies for a considerable time. Siemens and the German government have said that there is no reason for transportation of the repaired turbine not to start back on its final leg to Russia.

Peter Sidorov has published a review of the latest news here and what it means for the economy over winter in an overnight blog. Peter says that from reading the Russian version of the latest statement from Gazprom, they are looking for clearer guarantees on future sanctions exemptions for maintenance of NS1 and related issues. This will likely be hard to achieve and the Russians will know this. So it appears like Russian politics will be in control here for now.

As we mentioned last week, at 40% capacity Germany could make it through the winter even if some light rationing was needed. At 20% you would likely need some notable rationing unless they cut gas exports which would be a very delicate thing to do politically. Gas futures rallied around 10% on the news, closing a touch under that. EU energy minister meet today to discuss the ongoing crisis and potentially revise the rationing plans laid out by the EC last week. The potentially forced 15% reduction that all member states would have to adhere to was very unpopular amongst several members. Expect lots of carve-outs and compromises to appear if a plan that can progress is agreed upon.

The biggest market impact to yesterday’s gas move (outside of gas itself of course) was in bonds, with bunds falling -6bps into the close after an earlier sell-off in bonds. 10yr Bunds closed c.-1bps lower. There wasn’t any major move in spreads though as Italy tightened a basis point to bunds. European equities dipped on the news but mostly stayed in positive territory with the exception of the DAX (-0.33%). The Stoxx 600 closed +0.13%.

The US is certainly taking an interest in Europe’s problems at the moment (Gas and Italy) but it generally then moves on and marches to its own beat. 10yr Treasuries still climbed c.+5bps, even if they were 4bps off the days highs. This morning in Asia, yields on are around -1bps lower, trading at 2.786%, as we go to press. US equities generally held onto gains with the S&P 500 (+0.13%) but with the NASDAQ (-0.43%) dipping ahead of a huge week of tech earnings. We have Microsoft and Alphabet after the bell today followed by Meta tomorrow and Apple and Amazon on Thursday. So that’s over $7.5 trillion of market cap here alone at stake over the next couple of days although with these 5 stocks being down between around -13% (Apple) YTD to around -50% (Meta), with the other three down around -20 to -25%, this figure would have been closer to $10 trillion at the start of the year. Elsewhere in earnings land, we have GM, NXP Semiconductors, Raytheon Technologies, Coca-Cola, McDonald’s, Unilever and Mondelez reporting today amongst others. So plenty to keep an eye on today and for the rest of the week on the reporting front.

Back to US equities and Energy was the main winner (+3.71%) as Oil rose c.+2% yesterday and is up another +1.25% this morning ahead of some big oil majors reporting this week. Consumer Discretionary (-0.85%) was the weakest, likely on the bubbling recession fears. After the bell Walmart cut their outlook for Q2 and FY 23 and with it their equity fell -9.94% in after hours. As a result US futures are down with contracts on the S&P 500 (-0.28%) and NASDAQ 100 (-0.40%) edging lower this morning.

Asian equity markets have been fluctuating this morning and are still mostly higher with the Hang Seng (+1.60%) leading gains after Alibaba rose as much as +4.80% as it announced that it will be applying for a primary listing on the Hong Kong Stock Exchange. If completed, Alibaba will become a dual-primary listed company in Hong Kong and New York. The move is expected to happen by year-end. Over in mainland China, the Shanghai Composite (+0.81%) and the CSI (+0.96%) are climbing, reversing their previous session declines whilst the Nikkei (-0.06%) is fractionally lower this morning. Elsewhere, the Kospi (+0.12%) is edging up as South Korea’s Q2 growth rose +0.7% q/q (v/s +0.4% expected), faster than the +0.6% growth in the first quarter.

Data yesterday wasn’t top tier but both Chicago and Dallas Fed activity indices were slightly weaker than expected. The German IFO was slightly weaker too (88.6 vs 90.1 expected) but it was hard to upstage the poor PMIs from last Friday which set the tone for a major rally in bunds at the back end of last week. Its remarkable that after an initial spike to 0.765% for 2 year Bunds after the ECB, they dipped to 0.35% a day later after first the TPI wobbles and then the weak PMIs, and to around 0.4% at the close last night.

In terms of today we have the US July Conference Board consumer confidence index, Richmond Fed manufacturing index, June new home sales, and the May FHFA house price index. As discussed above EU energy ministers meet. Earnings is in full bloom with Microsoft, Alphabet, Visa, LVMH, Coca-Cola, McDonald’s, UPS, Texas Instruments, Raytheon Technologies, Unilever, Mondelez, 3M, General Electric, UBS, General Motors, ADM, Chipotle, and Deutsche Boerse all reporting. Elsewhere the IMF release their economic outlook update. Last but by no means least the FOMC start their crucial two-day meeting.

END

AND NOW NEWSQUAWK

Sentiment sours amid Kremlin updates, EU Energy deal & US-earnings in focus – Newsquawk US Market Open

TUESDAY, JUL 26, 2022 – 06:50 AM

- European bourses and US futures spent much of the morning under modest pressure, with the US in particular fairly rangebound pre-earnings & Wednesday’s FOMC.

- However, further pressure has been seen in wake of the most recent Kremlin-related commentary, with the Nord Stream 1 turbine yet to be installed.

- Dutch TTF & Crude benchmarks bid ahead of further Nord Stream 1 curtailments, though, the upside waned as the EU agrees on an emergency energy deal for the winter

- DXY continues to climb amid the above newsflow/narrative, pressuring peers while core debt climbs and US yields flatten modestly.

- Looking ahead, highlights include US Monthly Home Prices, US Consumer Confidence, US Richmond Fed, IMF Short-term Forecasts, the EU’s Energy Summit pressers and, supply from the US.

- Earnings from Alphabet, Microsoft, McDonald’s, Visa, UPS, LVMH, Michelin, UniCredit, and many more.

As of 11:20BST/06:20ET

For the full report and more content like this check out Newsquawk

Try a 14 day trial with Newsquawk and hear breaking trading news as it happens.

LOOKING AHEAD

- US Monthly Home Prices, US Consumer Confidence, US Richmond Fed, IMF Short-term Forecasts, the EU’s Energy Summit pressers and, supply from the US.

- Earnings from Alphabet, Microsoft, McDonald’s, Visa, UPS, LVMH, Michelin, UniCredit, and many more.

- Click here for the Week Ahead preview

GEOPOLITICS

- EU member states have agreed an emergency plan to reduce the bloc’s gas consumption in a bid to soften the impact of a potential total stoppage in Russian gas supplies, DPA has learned.

- Ukrainian Infrastructure Minister says we will stop grain exports if we detect any Russian threats in the Black Sea, via Al Jazeera.

- Kremlin says turbine for Nord Stream 1 pipeline is on its way after maintenance, still not been installed, via Reuters.

- Explosions were reported in the countryside of Odessa province, southern Ukraine, according to an Al Jazeera correspondent.

EUROPEAN TRADE

CENTRAL BANKS

- RBNZ Governor Orr says in addition to remit review, RBNZ will also review recent performance in conducting monetary policy; will assess inflation and employment outcomes relative to targets, via Reuters.

- CNB’s Frait says policy is already quite restrictive, won’t rule out a hike now or in the near time. Temporary FX interventions are normal in situations of shock to balance of payments, via Reuters.

EQUITIES

- European bourses are under modest pressure, Euro Stoxx 50 -0.4%, in what has been a limited session of newsflow ahead of the EU energy update and US earnings; though, strength in commodities is lifting the FTSE 100 +0.5%.

- However, further pressure has been seen in wake of most recent Kremlin related commentary, with the Nord Stream 1 turbine yet to be installed.

- Stateside, US futures are dented to the tune of crica. 5/10s of a percent; but, fairly rangebound (ex-above Kremlin related moves) overall pre-earnings and Wednesday’s FOMC.

- United Parcel Service Inc (UPS) Q2 2022 (USD): EPS 3.35 (exp. 3.16), Revenue 24.8bln (exp. 24.62bln)

- General Motors Co (GM) Q2 2022 (USD): EPS 1.14 (exp. 1.30), Revenue 35.8bln (exp. 34.52bln). FY EPS view 6.50-7.50 (exp. 6.89).

- Click here for more detail.

FX

- Aussie fades after probing Fib resistance vs Greenback and Loonie following oil powered rise to best levels since mid-June, AUD/USD back under 0.6950 from 0.6983, USD/CAD above 1.2880 from sub-1.2820.

- Dollar regains poise otherwise in choppy, cautious trade pre-FOMC, DXY rebounds firmly from 106.190 surpassing Monday high of 106.890 to 107.10+.

- Yen and Franc find some traction from pronounced bounce in bonds and reversion to bull-flattening, USD/CHF and USD/JPY hold below/above 0.9650 and 136.50 respectively.

- Euro undermined by ongoing Russian gas supply jitters ahead of Extraordinary Energy Summit, EUR/USD retreats from 1.0250 to circa 1.0140.

- Pound pulls up after narrowly missing 1.2100 vs Buck, Cable now below 1.2000, albeit still relatively comfortably above a series of recent descending lows.

- Click here for more detail.

Notable FX Expiries, NY Cut:

- Click here for more detail.

FIXED INCOME

- Bonds back in bull-flattening mode as Bunds front run latest leg higher.

- 10 year German benchmark reaches 155.90 and peaks not seen since late May, while yield breaches 1% with more conviction.

- Gilts and T-notes lag within 117-6935 and 120-04/119-24 respective ranges ahead of the Fed tomorrow and BoE next week.

- BTPs off lest levels and lag periphery peers amidst short term and linker supply.

- Click here for more detail.

COMMODITIES

- Dutch TTF continues to lift with the August contract in proximity to EUR 200 as Nord Stream 1 is set to be curtailed tomorrow; however, the EU has agreed on a deal to reduce gas use.

- Crude benchmarks are bid and drawing impetus from the referenced factors and EU divisions, though the magnitude of the move is more modest in nature vs TTF.

- EU nations agree to reduce gas use for next winter.; only Hungary voted against approval of mandatory gas rationing if Russia shuts off the taps, France24 reports. Reminder, press conferences are expected at 12:30BST/07:30ET and 15:00BST/10:00ET.