in Uncategorized · Leave a comment·Edit

GOLD; $1721.25 UP $1.80

SILVER: $18.67 UP 4 CENTS

ACCESS MARKET:

GOLD $1734.40

SILVER: $19.11

We are now entering options expiry for Comex (tomorrow) and OTC/LBMA (Friday)

Bitcoin morning price: $21,291 DOWN 314

Bitcoin: afternoon price: $22,880. UP 1270

Platinum price: closing UP $4.40 to $889.10

Palladium price; closing DOWN $5.15 at $2010.75

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JULY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,717.700000000 USD

INTENT DATE: 07/26/2022 DELIVERY DATE: 07/28/2022

FIRM ORG FIRM NAME ISSUED STOPPED

JPMorgan stopped 30/30

661 C JP MORGAN 30

690 C ABN AMRO 29

905 C ADM 1

TOTAL: 30 30

MONTH TO DATE: 9,635

_____________________________________________________________________________________

GOLD: NUMBER OF NOTICES FILED FOR JULY CONTRACT:

30 NOTICES FOR 3000 OZ //0.0933 TONNES

total notices so far: 9635 contracts for 963,500 oz (29.968 tonnes)

SILVER NOTICES:

34 NOTICES FILED FOR 170000 OZ/

total number of notices filed so far this month 4008 : for 20,040,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $1.80

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGE IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 1005.29 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 4 CENTS

AT THE SLV// ://HUGE CHANGES IN SILVER INVENTORY AT THE SLV//:A WITHDRAWAL OF 11.479 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 484.118 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 1436 CONTRACTS TO 147,784 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE HUGE GAIN IN OI WAS ACCOMPLISHED DESPITE OUR $0.16 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.16) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY COMMERCIAL SILVER LONGS//BUT MAINLY WE HAD ADDITIONAL SPECULATOR ADDITIONS AS WE HAD A HUGE LOSS OF 1217 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A POOR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.220 MILLION OZ FOLLOWED BY TODAY’S 445,000 OZ QUEUE JUMP / // V) HUGE SIZED COMEX OI LOSS

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -17

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTACTS for 18 days, total 15,897 contracts: 79.485 million oz OR 4.416 MILLION OZ PER DAY. (884 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 79.485 MILLION OZ

.

LAST 15 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 79.485 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1436 DESPITE OUR $0.16 GAIN IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 200 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER ADDITIONS ////// HUGE SPECULATOR SHORT ADDITIONS// WE HAVE A POOR INITIAL SILVER OZ STANDING FOR JULY. OF 15.22 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 445,000 OZ // .. WE HAD A HUGE SIZED LOSS OF 1236 OI CONTRACTS ON THE TWO EXCHANGES FOR 6.180 MILLION OZ DESPITE THE GAIN IN PRICE..THE SPECS ARE GOING TO THE SLAUGHTER HOUSE.

WE HAD 34 NOTICES FILED TODAY FOR 170000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A HUGE SIZED 15,223 CONTRACTS TO 487,515 AND further from THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -949 CONTRACTS.

.

THE STRONG SIZED DECREASE IN COMEX OI CAME DESPITE OUR TINY FALL IN PRICE OF $1.60//COMEX GOLD TRADING/TUESDAY / WE MUST HAVE HAD ADDITIONAL SPECULATOR SHORT ADDITIONS ACCOMPANYING OUR GOOD SIZED EXCHANGE FOR PHYSICAL ISSUANCE.//WE HAD INITIATION OF SPREADER LIQUIDATION WHICH TOOK CARE OF ALL OF THE FALL AT COMEX.. WE HAD ZERO LONG LIQUIDATION //AND HUGE SPECULATOR SHORT ADDITIONS//HUGE ADDITIONS TO OUR BANKER LONGS!! THE COMEX IS ONE BIG FARCE

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JULY AT 2.914 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 0 OZ

YET ALL OF..THIS HAPPENED WITH OUR TINY FALL IN PRICE OF $1.60 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A HUGE SIZED LOSS OF 10,939 OI CONTRACTS 34.024 PAPER TONNES) ON OUR TWO EXCHANGES..WITH ALL THE LOSS DUE TO SPREADER LIQUIDATION

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4284 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 487,515

IN ESSENCE WE HAVE A HUGE SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,939 CONTRACTS WITH 15,223 CONTRACTS DECREASED AT THE COMEX AND 4284 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 11,888 CONTRACTS OR 36.976 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4284) ACCOMPANYING THE GIGANTIC SIZED LOSS IN COMEX OI (15,223): TOTAL LOSS IN THE TWO EXCHANGES 10,939 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT ADDITIONS//STRONG BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JULY. AT 2.914 TONNES FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP 3) ZERO LONG LIQUIDATION AS ALL OF THE COMEX LOSS WAS DUE TO SPREADER LIQUIDATION////SOME SPECULATOR SHORT COVERINGS/ //.,4) HUGE SIZED COMEX OPEN INTEREST LOSS 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

112,859 CONTRACTS OR 11,285,900 OZ OR 351.03 TONNES 18 TRADING DAY(S) AND THUS AVERAGING: 6269 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAY(S) IN TONNES: 351.03 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 351.03/3550 x 100% TONNES 9.88% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 351.03 TONNES (HUGE INCREASE FROM JUNE//WILL CLOSE IN ON THE RECORD EFP ISSUANCE IN MARCH 22//SURPASSED PREVIOUS RECORD HIGH NOV 21)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JULY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A GIGANTIC SIZED 1436 CONTRACT OI TO 147,801 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 200 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 200 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 200 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1436 CONTRACTS AND ADD TO THE 200 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED LOSS OF 1236 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 6.180 MILLION OZ

OCCURRED DESPITE OUR RISE IN PRICE OF $0.16

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED DOWN 1.68 PTS OR 0.05% //Hang Sang CLOSED DOWN 235.84 OR 1,13% /The Nikkei closed UP 60.54 OR % 0.22. //Australia’s all ordinaires CLOSED UP 0.18% /Chinese yuan (ONSHORE) closed UP AT 6.7512//OFF SHORE CHINESE YUAN UP 6.7480// /Oil DOWN TO 96.12 dollars per barrel for WTI and BRENT AT 105.42// SHANGHAI CLOSED DOWN 1.68 PTS OR 0.05% //Hang Sang CLOSED DOWN 235.84 OR 1.13% /The Nikkei closed UP 60.54 OR % 0.22. //Australia’s all ordinaires CLOSED UP 0.18% / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GIGANTIC SIZED 15,223 CONTRACTS TO 487,515 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS STRONG COMEX DECREASE OCCURRED DESPITE OUR SMALL FALL OF $1.60 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A GOOD SIZED EFP (4284 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4284 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :4284 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4284 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A HUGE SIZED SIZED TOTAL OF 11,888 CONTRACTS IN THAT 4284 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 15,223 CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR TINY SIZED FALL IN PRICE OF GOLD $ 1.60. TODAY, WAS THE INITIATION OF SPREADER LIQUIDATION. WE ARE NOW ALSO WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS IS AN ABSOLUTE FARCE

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING JULY (29.987),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $1.60) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AND COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO COVER TO THEIR POSITIONS////ALL THE COMEX LOSS WAS DUE TO SPREADER LIQUIDATION// WE HAVE REGISTERED A STRONG SIZED LOSS OF 36.976 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR JULY (29.987 TONNES)…

WE HAD -949 CONTRACTS ADDED TO COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 10,939 CONTRACTS OR 1,093,900 OZ OR 34.024 TONNES

Estimated gold volume 214,534/// poor/

final gold volumes/yesterday 246,463 / fair

INITIAL STANDINGS FOR JULY ’22 COMEX GOLD //JULY 27

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 120,395.031oz Brinks JPMorgan Loomis Manfra 46 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 30 notice(s) 3000 OZ 0.0933 TONNES |

| No of oz to be served (notices) | 6 contracts 600 oz 0.0186 TONNES |

| Total monthly oz gold served (contracts) so far this month | 9635 notices 963,500 OZ 29.968 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

No dealer withdrawals

Customer deposits: 0

i) out of Brinks: 16,464.870 oz

ii) out of JPMorgan: 102,386.913 oz

iii) out of Loomis: 1446.795 oz (45 kilobars)

iv)out of Manfra: 96.453 oz 1 kilobar

total deposits: 0 oz

4 customer withdrawals:

i) out of Brinks: 16,464.870 oz

ii) out of JPMorgan: 102,386.913 oz

iii) out of Loomis: 1446.795 oz (45 kilobars)

iv)out of Manfra: 96.453 oz 1 kilobar

total withdrawals: 120,395.031 oz

ADJUSTMENTS:none

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 36 contracts having LOST 41 contracts . We had

41 notices filed on Monday so we GAINED 0 contracts or an additional NIL oz will stand in this non active

delivery month of July.

August has a LOSS OF 41,811 contracts down to 78,832 contracts. We have 2 more reading days before first day notice. Looks like we will have a strong August standing for gold (JULY 29/22..FIRST DAY NOTICE)

Sept. gained 238 contracts to 3372 contracts.

We had 30 notice(s) filed today for 3000 oz FOR THE July 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 30 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 30 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2022. contract month,

we take the total number of notices filed so far for the month (9635) x 100 oz , to which we add the difference between the open interest for the front month of (JULY 36 CONTRACTS ) minus the number of notices served upon today 30 x 100 oz per contract equals 964,100 OZ OR 29.987 TONNES the number of TONNES standing in this active month of July.

thus the INITIAL standings for gold for the JULY contract month:

No of notices filed so far (9635) x 100 oz+ (36) OI for the front month minus the number of notices served upon today (30} x 100 oz} which equals 958,100 oz standing OR 29.987 TONNES in this active delivery month of JULY.

TOTAL COMEX GOLD STANDING: 29.987 TONNES (A FAIR STANDING FOR A JULY ( NON ACTIVE) DELIVERY MONTH)

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,443,533.842 oz 76.00 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 30,892.570.364 OZ 960.88

TOTAL REGISTERED GOLD: 15,451,836.344 OZ (480.6 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 15,440,734.023 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 13,008,303.0 OZ (REG GOLD- PLEDGED GOLD) 404.6 tonnes

END

SILVER/COMEX/JULY 27

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 717,256.682 oz CNT Delaware JPMorgan Brinks |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 802,768.630 oz Delaware JPMorgan |

| No of oz served today (contracts) | 34 CONTRACT(S) 170,000 OZ) |

| No of oz to be served (notices) | 66 contracts (330,000 oz) |

| Total monthly oz silver served (contracts) | 4008 contracts 20,040,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 2 deposits into the customer account

i) Into Delaware 178,981.730 oz

ii) Into JPMorgan: 623,776.900 oz

total deposit: 802,768.630 oz

JPMorgan has a total silver weight: 175.168 million oz/337.594 million =51.89% of comex

Comex withdrawals:4

i) Out of Brinks: 9489.510 oz

ii) Out of CNT: 100,085.238 oz

iii) Out of Delaware 2999.934 oz

iv) Out of jPMorgan 601,682.000 0z

total: 717,256.682 oz

adjustments: 2//dealer to customer

JPMorgan 1,932,366.380 oz

and

Manfra: 14,422.600 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 57.787 MILLION OZ

TOTAL REG + ELIG. 337.594 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JULY OI: 100 CONTRACTS HAVING LOST 294 CONTRACTS. WE HAD 383 NOTICES FILED

ON TUESDAY, SO WE GAINED 89 CONTRACTS OR AN ADDITIONAL 445,000 OZ WILL STAND FOR METAL AT THE COMEX.

AUGUST LOST 62 CONTRACTS TO STAND AT 874

SEPTEMBER HAD A LOSS OF 2404 CONTRACTS DOWN TO 116,926

CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 34 for 170,000 oz

Comex volumes:47,665// est. volume today// poor

Comex volume: confirmed yesterday: 45,822 contracts ( poor )

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 4008 x 5,000 oz = 20,040,000 oz

to which we add the difference between the open interest for the front month of JULY(100) and the number of notices served upon today 34 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY./2022 contract month: 4008 (notices served so far) x 5000 oz + OI for front month of JULY (100) – number of notices served upon today (34) x 5000 oz of silver standing for the JULY contract month equates 20,370,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JULY 27.//WITH GOLD UP $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 26/WITH GOLD DOWN $1.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.29 TONNES

JULY 25/WITH GOLD DOWN $7.85: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 1005.87 TONNES

JULY 22/WITH GOLD UP $17.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 21/WITH GOLD UP $11.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.101 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.87 TONNES

JULY 20/WITH GOLD DOWN $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1009.06 TONNES

JULY 19/WITH GOLD DOWN $.35 :BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.22 TONNES FROM THE GLD//INVENTORY RESTS AT 1009.06 TONNES

JULY 18/WITH GOLD UP $7.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.28 TONNES

JULY 15/WITH GOLD DOWN $3.75:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD///INVENTORY RESTS AT 1016.89 TONNES//

JULY 14/WITH GOLD DOWN $28.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD//INVENTORY RESTS AT 1019.79 TONNES

JULY 13/WITH GOLD UP $10.55:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD//INVENTORY RESTS AT 1021.53TONNES

JULY 12/WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESS AT 1023.27 TONNES

JULY 11/WITH GOLD DOWN $4.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD./INVENTORY RESTS AT 1023.27 TONNES

JULY 7/WITH GOLD UP $1.35: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.61 TONNES FORM THE GLD///INVENTORY REST AT 1024.43 TONNES

JULY 6/WITH GOLD DOWN $26.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 9.86 TONNES FROM THE GLD//INVENTORY REST AT 1032.04 TONNES

JULY 5/WITH GOLD DOWN $36.55//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.41 TONNES FROM THE GLD///INVENTORY RESTS AT 1041.90 TONNES

JULY 1/WITH GOLD DOWN $5.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES//INVENTORY RESTS AT 1050.31 TONNES

JUNE 30/WITH GOLD DOWN $9.20: big CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 1052.63 TONNES//

JUNE 28/WITH GOLD DOWN $3.05//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.64 TONNES FROM THE GLD///INVENTORY RESTS AT 1056.40 TONNES

JUNE 27/WITH GOLD DOWN $4.90 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.04 TONNES

JUNE 24/WITH GOLD UP 45 CENTS TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.70 TONNES FROM THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 23/WITH GOLD DOWN $8.60:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//INVENTORY RESTS AT 1071.77 TONNES

JUNE 22/WITH GOLD UP 15 CENTS:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1073.80 TONNES

GLD INVENTORY: 1005.29 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JULY 27/.WITH SILVER UP 4 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL 11.479 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 484.118MILLION OZ//

JULY 26/WITH SILVER UP 16 CENTS: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.504 MILLION OZ FROM THE SLV//: //INVENTORY RESTS AT 495.597 MILLION OZ//

JULY 25/WITH SILVER DOWN 24 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.383 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 499.101 MILLION OZ//

JULY 22/WITH SILVER DOWN 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 500.484 MILLION OZ//

JULY 21/WITH SILVER UP 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.19 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 500.484MILLION OZ/

JULY 20/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 8.253 MILLION OZ FORM THE SLV/INVENTORY RESTS AT 507.585 MILLION OZ//

JULY 19/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ//

JULY 18/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 4.995 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ.

JULY 15/WITH SILVER UP 31 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 3.226 MILLION OZ FORM THE SLV//INVENTORY RESTS AT 510.443 MILLIONOZ//

JULY 14/WITH SILVER DOWN 88 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 OZ FROM THE SLV// //INVENTORY RESTS AT 513.671 MILLION OZ

JULY 13/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SV//INVENTORY RESTS AT 514.501 MILLION OZ.

JULY 12/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.228 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 514.501 MILLION OZ//

JULY 11/WITH SILVER DOWN 17 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 5.533 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 517.729 MILLION OZ

JULY 7/WITH SILVER UP 3 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.889 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 523.262 MILLION OZ/

JULY 6/WITH SILVER UP ONE CENT: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 12.558 MILLION OZ FORM THE SLV///INVENTORY RESTS AT 528.151 MILLION OZ

JULY 5/WITH SILVER DOWN 55 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 540.709MILLION OZ//

JULY 1/WITH SILVER DOWN 61 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ//INVENTORY RESTS AT 540.709 MILLION OZ//

JUNE 30/WITH SILVER DOWN 41 CENTS : SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 738,000 OZ FROM THE SLV//INVENTORY RESTS AT 541.262 MILLION OZ//

JUNE 28/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.00 MILLION OZ..

JUNE 27/WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 24/WITH SILVER UP 10 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.137 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 23/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 2.029 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 545.137 MILLION OZ//

JUNE 22/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.166 MILLION OZ.

CLOSING INVENTORY 484.118 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: The White House Recession Denial

WEDNESDAY, JUL 27, 2022 – 10:10 AM

The economic data indicates that the US economy is already in a recession. The Biden administration wants you to think otherwise, and the White House has come up with an interesting way to deny the recession reality. Just change the definition of a recession.

Peter Schiff appeared on the Ingraham Angle with Lauren Ingraham to talk about this White House spin.

The common definition of a recession is two consecutive quarters of negative GDP growth. In the first quarter of 2022, GDP came in at -1.6 percent. The Atlanta Fed projects another -1.6% decline in Q2. That would mean we’re in a recession now, and we have been all year. But White House spokespeople and Treasury Secretary Janet Yellen are quick to remind us that this is not the “technical” definition of a recession.

Technicalities notwithstanding, Ingraham points out that the last 10 times the economy experienced two consecutive quarters of negative GDP growth were technically defined as recessions. She called the Biden administration’s wordplay “a perfect distillation of modern leftism.”

When you’re losing, just change the rules of the game, then declare victory.”

Peter pointed out that the government already changed the definition of inflation from “an expansion of the money supply” to “prices going up.”

So, they may as well change the definition of recession. Because for my entire career, recession has been described by two quarters of negative GDP growth. And we’ve got that.”

During her interview on Meet the Press, Yellen said a recession wasn’t two quarters of negative GDP. She said it was a broad-based economic slowdown. Peter said that’s exactly what we’ve got.

The auto industry is in recession. The housing industry is in recession. Retail is in recession. Advertising is in recession. So many unrelated segments of the economy are in recession — how you can’t say this is a broad-based slowdown — it doesn’t make any sense. And in fact, it’s going to get a lot worse in the third quarter and then probably the fourth quarter as well.”

Ingraham noted that the White House and others denying a recession hang their hats on the tight labor market. But even that is looking shaky. As Peter said, we’ve seen three straight weeks of increasing first-time jobless claims, and they’re at the highest level since October last year.

Meanwhile, if you look at that last job report, even though we added about 400,000 jobs in the establishment survey, the household survey lost about that many jobs. But if you actually look at the jobs, almost all of these new jobs were for people who already had jobs. These were people taking second and third jobs because they’re struggling to pay the bills. And you have a lot of retirees who are being forced back into the workforce because inflation has eviscerated their incomes, and now they have no choice but to go to work. So, these are not jobs that people want. These are jobs that people are forced to take because the economy is so weak.”

Peter also pointed out that employment is a lagging indicator.

I think we’re going to see mass layoffs in the third and fourth quarters of this year as employers start to react to the reality of recession by laying off workers.”

As Ingraham said, next the White House will have to redefine the word layoffs.

END

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

end

3. Chris Powell of GATA provides to us very important physical commentaries

(Courtesy Chris Powell/GATA)

When buying gold or silver, please consider the dealers who support GATA

Submitted by admin on Tue, 2022-07-26 23:10Section: Daily Dispatches

1110p ET Tuesday, July 26, 2022

Dear Friend of GATA and Gold:

Being the only forms of money without counterparty risk, at least when held directly by their owners, gold and silver are often seen as the foundation of a sound investment portfolio.

This principle was put into graphic format by the U.S. economist John Exter, who served as the Federal Reserve Bank of New York’s vice president in charge of international banking and precious metals operations, as well as a member of the Federal Reserve’s Board of Governors, long before suppressing the gold price became the Fed’s primary objective.

In Exter’s inverted pyramid of financial asset risk, gold is the ultimate asset, with all other assets posing greater risk to their owners:

But you can do more than protect yourself when you buy gold and the other monetary metal, silver. You can also help GATA fight the price suppression we long have been exposing, documenting, and sometimes litigating against:

That is you can buy metal from dealers who support GATA and have been recommended by our supporters over the years.

A list of those dealers is included with every GATA Dispatch and is posted at GATA’s internet site here:

So please give them a chance to meet your investment needs.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Craig Hemke at Sprott believes that after looking at inverest rates, concludes that the Fed will have to stop raising interest rates long before they come close to the official inflation rate

(Craig Hemke/Sprott/GATA)

Craig Hemke at Sprott Money: Putting the stag in stagflation

Submitted by admin on Tue, 2022-07-26 22:56Section: Daily Dispatches

10:56p ET Tuesday, July 26, 2022

Dear Friend of GATA and Gold:

The TF Metals Report’s Craig Hemke, writing tonight at Sprott Money, looks at bond prices and concludes that the Federal Reserve will have to stop raising interest rates long before they come close to the official inflation rate. That, Hemke concludes, means stagflation and resumption of uptrends for gold and silver.

Hemke’s analysis is headlined “Putting the Stag in Staflation” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/blog/Putting-The-Stag-in-Stagflation-Craig-Hemke-July-26-2022

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

4. OTHER GOLD/SILVER COMMENTARIES

For your interest…

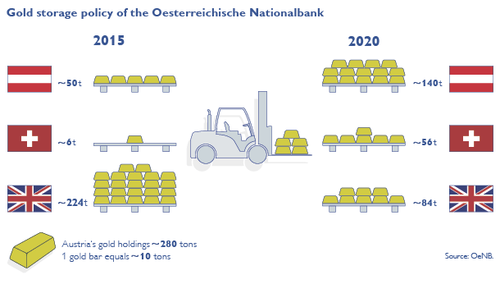

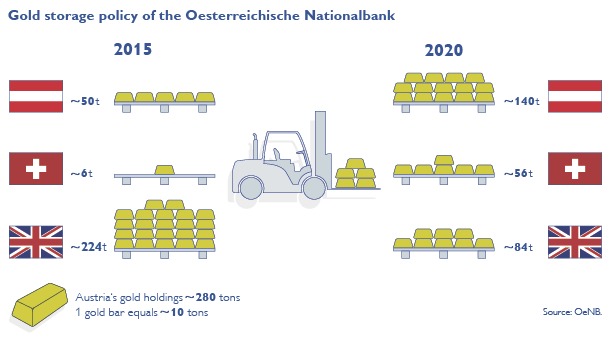

Why Austria’s Monetary Gold Transfer To Switzerland Is Delayed

WEDNESDAY, JUL 27, 2022 – 05:00 AM

By Jan Nieuwenhuijs of Gainesville Coins

In my first article on this topic I wrote the Austrian central bank (OeNB) had implemented a new gold storage concept in 2015, because the national court of audit (Rechnungshof, RH hereafter) found it was storing too much gold in London at the Bank of England (BOE). OeNB planned to repatriate 90 tonnes from BOE, and transfer 50 tonnes from London to Switzerland. Within five years (by 2020) the new storage concept should have materialized.

In 2018, ahead of schedule, the gold had arrived in Austria. However, the shipment to Switzerland hasn’t arrived until this day.

First, the problem isn’t in London. There hasn’t been any problem for OeNB withdrawing 90 tonnes to repatriate, so there is little reason to think another 50 tonnes couldn’t be taken out. Austria is politically on good footing with the U.K., unlike Venezuela which has been blocked from repatriating in recent years.

Second, in two documents by RH—one from 2015 and another from 2018—there is evidence OeNB was already storing gold at the Swiss central bank (SNB), and wanted to add 50 tonnes to the same depository. As discussed in my second article on this topic, the renovation of the Swiss central bank’s vault was planned to be completed in 2018, but is taking several years longer than excepted. This is why OeNB was forced to postpone the shipment. Let’s have a look at the evidence.

In both documents (RH1 and RH2 hereafter) the actual names of many banks, institutions and depositories are replaced by code names. Although, there is sufficient information disclosed to decipher who’s who. For example, in table 4 in RH1 it shows that by late 2013 the central bank of Finland (BOF) held 7% of its gold at “depository C in Switzerland.” On its website we read BOF holds 7% of its gold at SNB. Other cross checks confirm “depository C in Switzerland” must be SNB. An often mentioned “institution in Switzerland” must be the Bank for International Settlements (BIS). And so forth.

Connecting the Dots

By 2014 OeNB had closed all accounts with commercial banks and its metal at the BIS in Switzerland was allocated. The gold previously held at Swiss commercial banks was moved to OeNB’s account at SNB.

From RH1 (page 48):

In 2013, OeNB closed the gold deposits held at two Swiss commercial banks (depositories A and B), in which a total of approximately seven tonnes of gold … were stored and opened a gold deposit for these approximately seven tonnes … at depository C in Switzerland [SNB]….

From RH1 (page 60):

Implemented as per December 31, 2013: The physical stocks, which were stored at commercial banks, were finally entirely liquidated … due to risk considerations.

…

A metal account of approximately 14.3 tonnes held at the institution in Switzerland [BIS] … was converted into physical stock as of January 30, 2014.

Since 2014 OeNB’s gold is spread over four vaults, and it wants to keep it like that.

From RH2 (page 19):

The court of audit found that, since 2014, OeNB had kept its physical gold holdings in its own vaults, at the Austrian Mint, at a depository in England [BOE] and a depository in Switzerland [SNB]. In its new storage concept OeNB did not envisage using any other depositories in the coming years.

OeNB can physically hold gold at four vaults (OeNB, Austrian Mint, BOE, SNB) and the BIS, because the BIS has no vaults of its own but uses the custodial services of BOE, SNB, and the Federal Reserve Bank of New York.

Attentive readers might have noted that in 2015 OeNB disclosed to have ~6 tonnes stored in Switzerland, which is less than 14.3 tonnes with the BIS at SNB plus ~7 tonnes at SNB directly. The explanation is a location swap executed by the BIS (from SNB to BOE) on the same day the metal was allocated.

From RH1 (page 53):

As of January 30, 2014, OeNB had the delivery claims recorded in the account held at the institution in Switzerland [BIS] transferred to a bar deposit account of the institution at the depository in England [BOE] ….

After the swap OeNB held “approximately seven tonnes of gold” at SNB. Roughly in line with ~6 tonnes. The counterparty of the swap that moved metal from BOE to SNB is unknown to me.

RH is mainly concerned about spreading the gold geographically and for OeNB being able to audit it. Other points of attention are the custodian’s duties of care and liability, ownership rights, insurance, the transmission of stock lists and agreements regarding deliveries. In RH1 (page 74) it states, “the most comprehensive agreement was the one with depository C in Switzerland [SNB].” Although, as early as 2013, auditing access was limited.

From RH2 (page 19):

In its letter of May 8, 2013, the depository in Switzerland [SNB] informed the OeNB that in general it would be able to access OeNB’s stored gold but pointed out that there would be restrictions in this regard until 2018. … In response to an inquiry by OeNB during the follow-up review by the court of audit in February 2017, the depository in Switzerland confirmed … that OeNB would have normal access to the depository as of 2019.

Apparently SNB started moving out the gold from Bundesplatz 1 in Berne to the federal bunker near Kandersteg in 2013 whereby access to the vault was restricted. The dates on which the restrictions would be lifted more or less fit SNB’s projections as mentioned in its annual reports. In 2018 SNB first disclosed the renovation wad delayed until 2021. In 2019 completion was set for 2022, and in 2021 it was moved further back to 2024.

Aside from stagnating on site auditing, OeNB had to wait for shipping 50 tonnes from London to SNB’s vault in Berne due to the renovation, RH concludes in 2015.

From RH1 (page 19):

By concluding an agreement with depository C in Switzerland [SNB], for up to 50 tonnes of gold, the depositories were spread out, which was intended to reduce the concentration risk at the depository in England [BOE]. However, this reduction was severely limited due to external circumstances that OeNB could not influence. Up until the beginning of 2019, a maximum of around seven tons of gold could initially be stored at this storage facility in Switzerland due to renovation work.

Other parts in RH1 also mention renovation work at depository C in Switzerland (SNB) as the reason an additional 50 tonnes couldn’t be shipped immediately.

Conclusion

More often than not speculation has the upper hand in the gold blogosphere. In 2013 many commentators (including me) were disgruntled by the pace with which the German central bank (BuBa) announced to repatriate gold from New York: 300 tonnes in 7 years. Eventually, it became clear BuBa wanted to upgrade the bars not adhering to LBMA Good Delivery standards. When it completed repatriating ahead of schedule in 2017, the Financial Times wrote 55 tonnes had been routed through Switzerland, “where two smelters remoulded the bullion,” before it went to Frankfurt.

There is also an explanation for the delay in OeNB’s shipment from London to Switzerland. Likely, OeNB needed time to check and weigh the 90 tonnes coming home from London. In any case, it knew the shipment to SNB had to wait a few years and so the decision was made to implement the new storage concept by 2020. But then the renovation took longer than anticipated and OeNB had to adapt.

I will write one final article on this topic, when OeNB’s gold has finally arrived in Berne.

END

Worth repeating

(Alasdair Macleod)

Gold & The Upcoming Recession

WEDNESDAY, JUL 27, 2022 – 07:20 AM

Authored by Alasdair Macleod via GoldMoney.com,

We are now seeing the initial stages of a currency, credit, and banking crisis develop.

Driving it are an inflation of prices, contraction of bank credit and a pathological fear of recession.

One can imagine that the major central banks almost wish a mild recession upon us so that they can keep interest rates suppressed and bond yields low.

The key to understanding the course of events is that the cycle of bank credit is turning down, and this time the factors driving contraction are greater than anything we have experienced since the 1930s, and possibly in all modern monetary history.

This article joins the dots between inflation and recession and puts the relationship between money (that is only gold), currencies, credit, and commodity prices into their proper perspective.

The bank credit downturn…

It is increasingly obvious that the economic cost of sanctioning Russia is immense, and there’s now growing evidence of all major economies facing a downturn in economic activity. And we don’t have to rely on GDP forecasts to know why. Intuitively, if food and energy shortages impact us all, higher prices for these items alone will affect our spending on less important items and services.

That’s reasonable enough for sensible citizens. But financial analysts insist on quantifying it with their models. Their principal measure is the total value of all recorded transactions, comprised of GDP. They proceed seemingly unaware of the difference between the value of economic activity to the advancement of the human condition, which can’t be measured, and a meaningless total comprised of only currency and credit, which can. Consequently, all they end up recording is changes in the quantity of currency and credit deployed in the economy.

Of course, there is a broad point that if the quantity of currency and credit contracts, GDP falls. And if it is severe, economic activity tends to fall as well. But to equate the two to the point that a variation of less than a per cent or so from modelled forecasts means anything is nonsense. A proper assessment of the economic condition gets lost.

Instead, an awareness of the role of bank credit is called for. Banks create credit, which feeds into the GDP total when they are optimistic about the outlook for lending. And when they deem the outlook to be deteriorating, they withdraw credit which reduces the GDP total. It leads to a repetitive cycle of boom and bust. We are now entering a period where, at the margin, banks are trying to reduce their exposure to credit going sour. Therefore, GDP will contract And we can assess where it will contract. It really is that simple.

The best thing to do is to stand back and let the excesses of lending and the support for malinvestments wash themselves out of the system. The last time this was done was the brief but very sharp recession of 1920—1921 in the US. The government of the day understood it was not its business to intervene, and anyway, it was not capable of improving thngs.

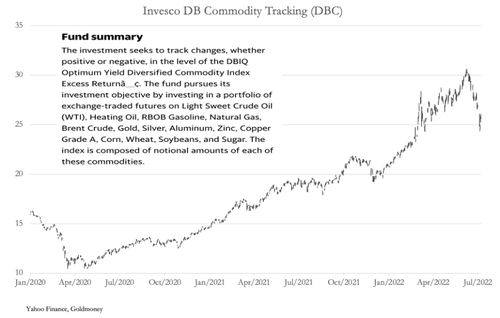

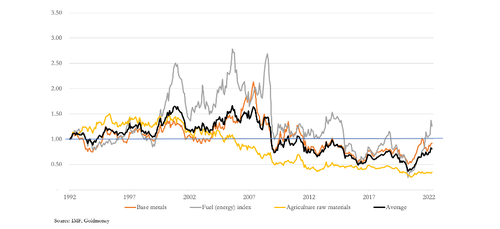

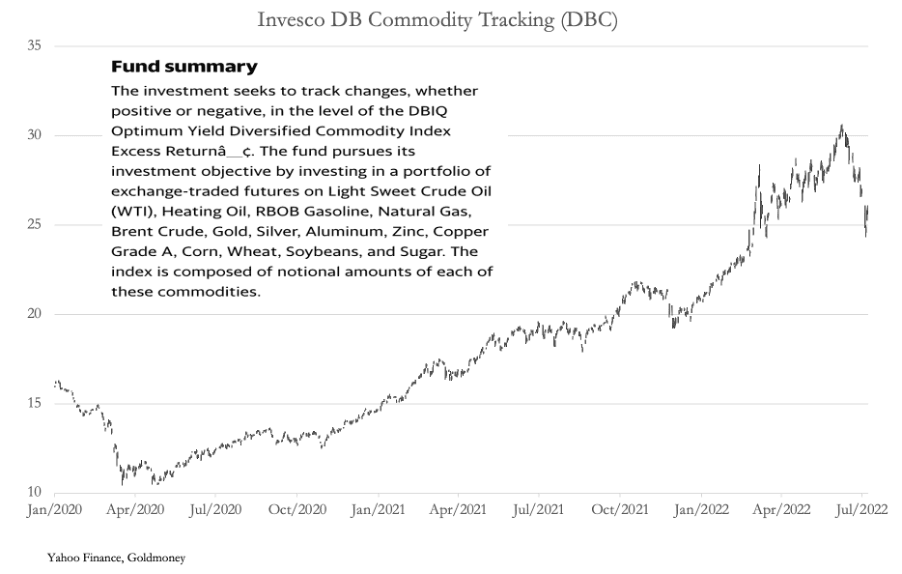

But increasingly since, monetary policy has become run by central banks which steer their economies through rear view mirrors, reacting to information rather than anticipating. But even if they could anticipate economic trends they lack the commercial nous to manage it. Instead, their stock reaction to declining GDP will be to “stimulate”. Not only do they have a mandate to maintain full employment, but they have a Keynesian belief that a decline in GDP is entirely due to falling demand. Falling demand, they say, leads to lower prices, so the inflation figures in the CPI will fall. Producer prices will fall. All commodity prices will fall. The chart below feeds this line of hopeful thinking.

This basket of commodities has fallen in value by 17% in a month. Panic over. Even wheat and soya prices have fallen. Dr Copper is down. Grasping at these straws, central banks are undoubtedly relieved that inflation might be turning transient after all.

Or so they think. There is no doubt that we are experiencing enormous price volatility. If it was entirely due to consumers deciding not to spend because prices are too high for them, that is one thing. But if it is because banks are withdrawing credit, the consequences are materially different.

A central bank’s concern to maintain consumer spending might discourage banks from contracting credit for consumers, at least initially. Furthermore, their risk models show that while individually consumers using credit are often high risk the magic of securitisation turns these risks collectively into low risk. It becomes a numbers game. So, credit card and other consumer faced lending divisions with very high credit margins are not the first to be targeted. And anyway, that would put the bank’s executives at odds with the central bank.

Instead, in the initial stages of a credit downturn, banks withdraw credit principally from business borrowers who use overdraft facilities. A business that frequently resorts to overdraft facilities is high risk in any bank’s assessment. Weaker businesses are first to succumb to the credit downturn for this reason. Other early victims of credit contraction are financial speculators because their collateral is easily realised. We have seen the decline of US stock indices so far being accompanied by a $200bn reduction in margin lending. There’s still much more to go.

As the economist Irving Fisher pointed out in the 1930s, calling in loans to reduce bank credit can become a self-feeding destruction of value. The bit he failed to understand is that in a serious downturn it can’t be helped, because it is the other side of earlier credit expansion, and it is the unwinding of unsound lending. Both an understanding of what drives periodic contractions of bank credit and the empirical evidence that it has repeated in one form or another approximately every decade since records began, inform us that it should not be stopped but allowed to proceed. Compare the brief 1920—1921 slump in the US with the prolonged 1930s slump, the latter managed by first Presidents Herbert Hoover and then Franklin Roosevelt.

We should also know from understanding that bank credit is a cycle, that the height of the recent expansionary phase measured by the ratio of total bank balance sheet assets to their shareholders’ capital indicates the likely severity of the subsequent credit contraction. It reflects deposit liabilities to a bank’s customers relative to its shareholders assets. Traditionally, asset to equity ratios of more than eight to ten times were deemed risky. Some major banks, particularly in the EU and Japan, are now at over twenty times. While the US banks are less geared, the systemic risks to them from other national banking systems in this financially interconnected world are the highest they have ever been.

For the immediate future we can discern two things. First is that production of goods and services is likely to be more limited than consumption due to an absence of bank credit, knocking on the head the Keynesian misconception that it is a problem of insufficient demand. That is just an initial phase. And following it, the contraction of bank credit can be expected to become more severe, as banks draw their horns in to protect their shareholders from an Irving Fisher style slump. In this subsequent second phase both producers and consumers will face enormous financial difficulties.

Without aggressive intervention by central banks, the correction from excessive over-lending taking bank balance sheets beyond dangerous levels of leverage will simply fuel a GDP slump. Central banks will intervene, not just to deliver on the full employment mandate, but to finance government budget deficits which will soar under these developing circumstances.

Prices in a slump

The last real slump, when the forces driving bank credit contraction were arguably less severe, was in the 1930s following the Wall Street crash. At that time, the dollar and sterling, together the world’s major international currencies, were both on gold standards. Prices of commodities, raw materials and agricultural products collapsed, effectively measured in gold through these two currencies. The political strains led to Britain abandoning its bullion standard in 1932, and the US gold coin standard was suspended for US citizens in 1933, followed by a 40% dollar-devaluation in January 1934.

The effect of the collapse of bank credit was to make circulating media in dollars and sterling scarce, thereby raising their purchasing power. To this extent, gold’s purchasing power also rose, because it was tied to the currencies. While gold gave credibility to the dollar and sterling, it was the contraction of bank credit that drove the slump in prices, while gold got the blame.

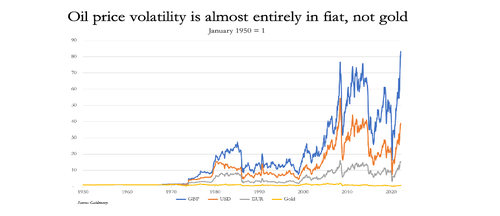

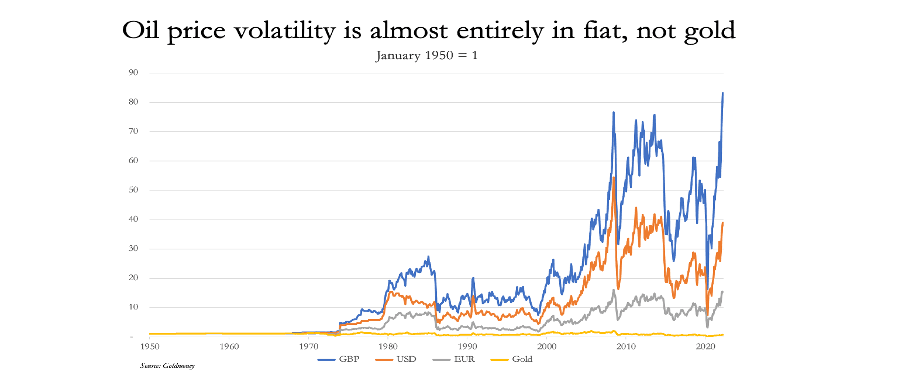

We know that priced in gold, over time commodity, raw materials, and agricultural product prices are remarkably stable. Disruption in the price relationship does not come from gold. The following chart of the WTI oil price rebased to 1950 illustrates prices in sterling, dollars, and euros where there are huge variations in prices. Contrast that with gold (the yellow line), where the price today is down about 30% from 1950 with minimal volatility along the way.

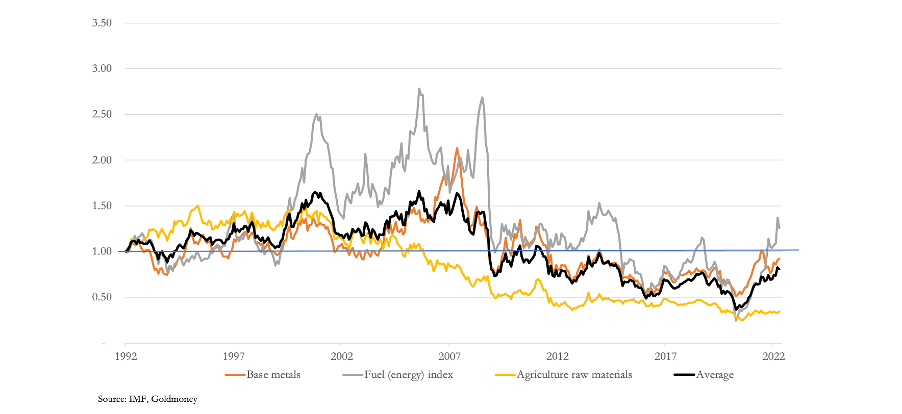

Our next chart makes the point with base metals, fuel and non-cyclical agriculture raw materials all rebased in gold.

Since 1992, which is the earliest common date we have for these series, an unweighted average gold value for them has fallen a net 19% (the black line). Fuel has been the most volatile at up to 2.5 times the 1992 price, but from the previous chart we can see that it was up a net 12 times in US dollars in 2007/08 from 1992. Priced in gold, the relatively little volatility we see in these commodity groups is as close as we can get to free market values in sound money. And even then, we know that gold prices are manipulated in the markets. We can also assume that the origin of this volatility does not come from gold, but from the violent price changes in fiat currencies, their interest rates, and their distortions with respect to demand for commodities.

These findings overturn conventional opinions on price formation. The evidence is that it is not true that fiat currencies are purely objective in their relationship with commodity prices. Forecasters of commodity prices incorrectly assume there is no change from the currency side. But clearly, the fluctuations overwhelmingly emanate from the currencies themselves.

This brings us to the likely effect of an economic slump on prices. Initially in our analysis, we will assume there is little change in the public’s desire to hold fiat currencies relative to the range of commodities and consumer goods. That being the case, we can see that it will be variations in the quantity of currency and credit in circulation driving prices. A contraction in this quantity will tend to lower prices. And Keynesian economists might conclude that precious metals being commodities will also fall in price against fiat currencies, given that fiat currencies are no longer tied to gold.

The flaw in this argument is that there are indeed other factors involved, and the consequences for the quantity of currency and credit in a slump must be taken into account. Irrespective of changes in monetary policy, in socialised economies government budget deficits soar and will need financing by expansion of the currency if bank credit is not forthcoming. In other words, despite the tendency for banks to contract bank credit to the private sector and even if central banks do not amend monetary policies, it will be more than offset by an expansion of currency passed into the economy through the government’s books.

Furthermore, under these circumstances monetary policy will change as well. Following the initial withdrawal of overdraft credit from businesses and bank loans for financial speculation, there is likely to be a softening of consumer demand as lending standards tighten and financial insecurity for consumers escalates. Central banks will notice the tendency for the withdrawal of bank credit to lead to a slump in consumer demand. They will almost certainly reduce interest rates and reintroduce quantitative easing to replace contracting bank credit to stimulate flagging economic activity. They have eased and stimulated in every bank credit cycle at this point since the 1930s, and there’s no reason to think they will do otherwise today.

An increase in currency and credit, not emanating from the commercial banks but from the central bank, with increasing budget deficits will continue to debase the currency in gold terms. The currency will also be debased against commodities. But with some volatility imparted from the currency side, we can see that the general relationship between commodities and gold can be expected to remain intact.

A systemic failure is on the cards

All this assumes that within the context of the bank credit cycle there is not a significant systemic failure. Given that the forces behind credit contraction today are greater than any time since the 1930s, and possibly for all modern monetary history, that is a vain hope. Last week I pointed out the looming catastrophe for the euro system and the euro. A similar tale can be told about the Japanese yen. And sterling is just a poor man’s version of the dollar without its hegemony status.

In the event of a systemic crisis, the role of central banks will be to underwrite their entire commercial banking system. The consequences of letting Lehman go bankrupt on the last cycle of bank credit contraction did not serve as a warning to profligate bankers. Instead, it had us all staring into a systemic abyss, and that mistake will not be repeated. In a systemic crisis today, it will take unprecedented currency and credit creation by the central banks to save the financial world. And it’s that debasement that will end up collapsing fiat currencies.

Meanwhile, we can expect central banks to milk the transitory inflation story for all its worth. Forget the CPI rising at 8%+ they will say. It will soon return to the 2% target as recession bites. But that’s another excuse to ease policy. It might buy just a little more time before the crisis hits. But don’t bank on it.

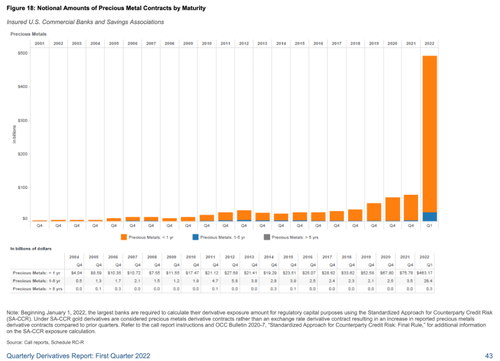

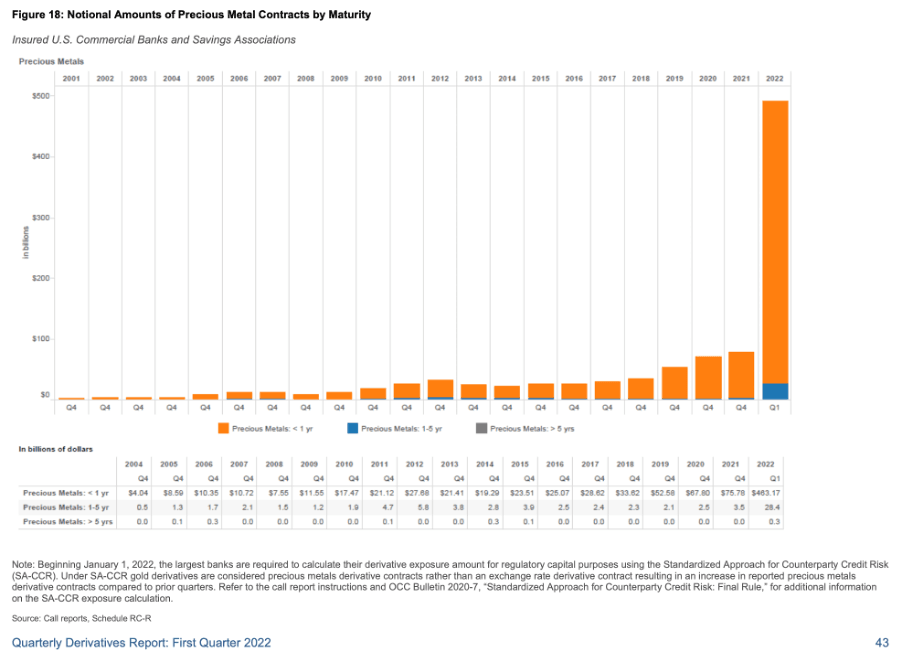

Manipulation becomes official

Earlier this month, three JPMorgan Chase traders faced a federal trial in Chicago, accused of masterminding a massive eight-year scheme to manipulate international markets for precious metals by spoofing, including gold and silver. JPMorgan had already been fined $920m in 2020.

Coincidently, Peter Hambro who was a gold trader in London in the early days of the derivatives market described how the bullion banks created unallocated gold accounts. One of Hambros’ more interesting comments was about the role of the authorities:

“Disinformation for many years has kept the lid on this tinderbox and since 2018 the Financial Stability Desks at the world’s central banks have followed the Bank of International Settlements’ instruction to hide the perception of inflation by rigging the gold market.”

Perhaps it’s not too great a leap of the imagination to suggest that the three JPMorgan Chase traders facing criminal charges in Chicago are being hung out to dry, when all they were doing the BIS’s and other central banks’ bidding.

What appears to have got Hambro commenting was a chart released by the US Office of the Comptroller of the Currency in its quarterly derivatives report, replicated with notes below.

Over the previous quarter, 2022 Q1 shows a 520% increase in precious metal derivatives over 2021 Q4. As the note explains, this is due to a reclassification of gold derivatives from exchange rates to precious metals. What it does not say is that the effect is to increase the supervisory factor from 4% to 18%. The following definition of supervisory factors is taken from the OCC’s Bulletin 2020-7:

“The Basel Committee standard uses supervisory factors that reflect the volatilities observed in the derivatives markets during the financial crisis. The supervisory factors reflect the potential variability of the primary risk factor of the derivative contract over a one-year horizon.”

In the context of this article, the reason for the reclassification of legal money (for that is gold) from exchange rate derivatives to commodities is that after significant back-testing they found gold correlated more with commodities than currencies. Bravo! That is what the earlier charts in this article, of the steadiness of commodity prices over time measured in gold, point out. The mistake made by regulators is to think price volatility is in commodities, when in fact it is in fiat currencies. What they should be doing is giving gold a zero supervisory factor, commodities a 4% factor, and currencies 18%. But as Peter Hambro points out, the BIS, which supervises Basel banking regulations, has run a secret campaign with the major central banks to suppress the price of gold.

While the manipulators at the BIS might think that declassifying gold from currency is a further nail in gold’s coffin, the measure could backfire. Following this ruling, to maintain substantial derivative positions chews up balance sheet, and bank treasurers are likely to seek restraint on outstanding positions, given their mandate to reduce balance sheet leverage. This observation is a segway to another consideration.

The markets for over the counter and regulated derivatives have increased along with the financialisation of banking activities since the mid-eighties. For nearly forty years, the dollar has acted as the backbone of financialisation with the big New York banks acting as its recycler. Two events are calling an end to this period. First, the long-term decline of interest rates has come to an end as the purchasing power of the dollar declines at an accelerating pace. And secondly, sanctions against Russia have backfired badly on dollar hegemony. If anything, it heralds a new era of Asian currencies reflecting, or being tied to commodities. Indeed, a trade settlement currency for the Eurasian Economic Union (EAEU) with a major commodity element in it is planned. It may not see the light of day, but commodities, not financial activities, are central to pan-Asian trade and the dollar’s successors are likely to reflect it.

Even Saudi Arabia has shown interest in aligning with the BRICS group, which in turn is aligning with the Shanghai Cooperation Organisation, which has in its membership all the EAEU nations. Saudi Arabia is important, because it was the Kingdom’s agreement with President Nixon which created the petrodollar. So, Mohammed bin Salman who now rules the kingdom politically, appears to be turning his back on the Nixon agreement to only accept payment in dollars for oil. That is the death knell for the petrodollar.

And then there are the balance sheet considerations in the financially centric banking system. Rising interest rates are collapsing the availability of bank credit for maintaining the bull market in stock and bond prices. Just as a long-term bull market on the back of an enduring decline in interest rates has driven the expansion of derivatives, the end of that bull market is bound to lead to a contraction. And as commercial bank treasurers prioritise balance sheet reductions, those having a high supervisory factor, such as precious metal and commodity derivatives will attract their attention.

The BIS scheme for suppressing gold prices will be unwound while global currency debasement accelerates. It looks like a double-whammy is about to undermine global fiat currency world credibility. For now, it is the dollar that reflects the upcoming storm, like the weird fall in sea levels ahead of a tsunami. The collapse in the yen, euro, and pound, together with an increasing list of minor currencies collapsing, is like an approaching tsunami, when the sea level initially drops.

The same happened in the last bank credit crisis, when Lehman failed, and every other US bank was rescued by the Fed. There was an initial flight into the dollar which saw gold prices fall. The problem facing risk-averse Keynesian-educated investors is their accounting of profits and losses is in fiat currencies. They must sell risky investments for cash in their currencies of account. And internationally, that is predominantly dollars which is why the dollar is usually a safe haven in the initial stages of a systemic crisis.

After the initial rush, dollars and other currencies are then sold for real money, which is and always has been gold.

END

JPMorgan Spoofing Trial May End Without Defendants’ Testimony

July 25, 2022, 6:45 PM

Chicago jury hears from first defense witness on Monday

Attorneys signal defendants won’t take to the stand themselves

Two former JPMorgan Chase & Co. gold traders and a salesman on the bank’s precious metals desk signaled they won’t take the stand at a trial where they’re charged with conspiring to use spoof trades to manipulate prices for years…

END

5.OTHER COMMODITIES: WHEAT

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7512

OFFSHORE YUAN: 6.7480

HANG SANG CLOSED DOWN 235.84 PTS OR 1.13%

2. Nikkei closed UP 60.54 OR 0.22%

3. Europe stocks CLOSED ALL IN THE GREEN

USA dollar INDEX DOWN TO 106,74/Euro RISES TO 1.0163

3b Japan 10 YR bond yield: FALLS TO. +.199/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 136.74/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: UP -// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.045%/Italian 10 Yr bond yield RISES to 3.40% /SPAIN 10 YR BOND YIELD FALLS TO 2.27%…

3i Greek 10 year bond yield RISES TO 3.05//

3j Gold at $1720.10 silver at: 18.76 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 1 AND 00/100 roubles/dollar; ROUBLE AT 59.56

3m oil into the 96 dollar handle for WTI and 105 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 136.71DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9616– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9714well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

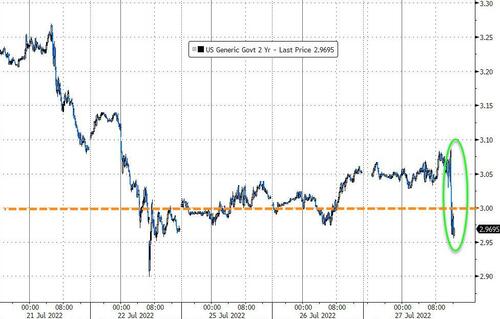

USA 10 YR BOND YIELD: 2.799 UP 1 BASIS PTS

USA 30 YR BOND YIELD: 3.027 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.92

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Bounce On Tech Optimism As Fed Looms

WEDNESDAY, JUL 27, 2022 – 08:00 AM

Global markets and US equity futures got a strong boost on Tuesday from reassuring big tech reports including Microsoft, Texas Instruments and Google, which delivered double-digit revenue growth reversing the doom and gloom from other reporters. Microsoft assuaged fears that the strong dollar and a weakening economy would hurt sales while Alphabet posted advertising revenue that surpassed analysts’ expectations amid an industry slowdown. Credit Suisse CEO Thomas Gottstein will to be replaced by asset-management head Ulrich Koerner next week after the Swiss bank posted its third straight quarterly loss and its worst trading first half in decades. All of that, of course, pales ahead of the day’s main event Later today, the Federal Reserve is expected to increase its benchmark interest rate by three quarters of a percentage point.

Nasdaq 100 contracts led gains rising 1.3% and reversing much of Tuesday’s plunge. S&P futures rose 0.8% alongside European stocks which also rose, with the banking sector up even as Credit Suisse Group AG posted a larger-than-expected loss, Deutsche Bank AG warned on costs, and the outlook on Italy’s sovereign debt ranking was lowered by S&P. The dollar and Treasury yields slipped, while oil and European natural gas prices extended gains.

In premarket trading, major technology and internet stocks were higher after both Microsoft and Google-parent Alphabet reported double- digit quarterly revenue growth amid tough macro conditions. Microsoft shares rose 4.3% after the software company said it expects double- digit sales growth for the fiscal year 2023. While quarterly revenue was weaker than expected, Barclays analysts say the report shows resilience despite a number of headwinds. Fellow tech giant Alphabet shares also rise 4% in premarket trading after the Google parent reported its 2Q revenue in line with Wall Street expectations. Analysts said the results were better than feared, but noted that “macro uncertainty remains high.” Here are some other notable premarket movers:

- Alphabet Inc (GOOGL) Q2 2022 (USD): EPS 1.21 (exp. 1.29), Revenue 69.70bln (exp. 70.04bln).Google advertising 56.29bln, (exp. 55.91bln). CFO said FX impact to be even greater in the current Q, according to CNBC. (Newswires/CNBC) +3.5% in the pre-market

- Microsoft Corp (MSFT) Q4 2022 (USD): EPS 2.23 (exp. 2.29/2.29 GAAP), Revenue 51.9bln (exp. 52.45bln). Intelligent Cloud revenue 20.91bln (exp. 21.07bln). Guides FY23 revenue double digits sales growth, FY23 FX impact of 4-points decrease in revenue growth, via its conference call. (Newswires) +3.8% in the pre-market

- Visa Inc (V) Q3 2022 (USD): Adj. EPS 1.98 (exp. 1.74/1.73 GAAP), Revenue 7.3bln (exp. 7.06bln). (Newswires) Co. seeing no evidence of a pullback in consumer spending. Unch. in the pre-market

- Twitter (TWTR) said it significantly slowed hiring in Q2 2022; in 2021 and H1 2022, macro factors had a negative impact on, and may negative impact in future periods, such as advertising revenue. Twitter is to hold shareholder vote on Musk deal on September 13th at 18:00BEST/13:00EDT, according to CNBC. (Newswires/CNBC)

- PayPal (PYPL US) shares jump as much as 6.5% premarket, following a report that activist investor Elliott is building a stake in the payments firm. Results from peer Visa also boost sentiment.

- Cryptocurrency-exposed stocks are higher in premarket trading as Bitcoin rebounds along with US stock futures after Alphabet, Microsoft and Texas Instruments results spur hopes that the technology sector can manage a slow economy. Coinbase (COIN US) +4.9%, Marathon Digital (MARA US) +7.6%, Riot Blockchain (RIOT US) +5.5%, Ebang (EBON US) +12%

- ObsEva (OBSV US) shares slump 75% in premarket trading after the biopharmaceutical company said it plans to initiate a corporate restructuring given the commercial landscape and potential additional capital is needed to fund the completion of the linzagolix clinical development program.

- Enphase Energy (ENPH US) shares surged as much as 12% in premarket trading as analysts hiked their price targets on the solar energy equipment maker, with brokers saying its results and guidance for the 3Q were robust and exceeded expectations thanks to strong demand.

- Texas Instruments (TXN US) shares rose 2.8% in postmarket trading on Tuesday after issuing a bullish forecast for the current quarter. Analysts note that the company exceeded its “overly conservative” estimates as lockdowns eased in China.

- Teva Pharmaceuticals shares jump as much as 16% in Tel Aviv, the most since May 2020, after the Israeli company said it had struck a deal with US state and local governments to pay more than $4 billion to settle thousands of lawsuits. US-listed ADRs also gain 16% in premarket trading.

The mood remains edgy ahead of a much-anticipated Fed interest-rate increase – part of a global wave of monetary tightening to quell inflation that’s stoking concerns about a worldwide economic slowdown. Investors are also bracing for the busiest reporting day of the season, where Meta may sour the mood after the bell with a slowdown in ad spending. Qualcomm will give investors a view into a smartphone market that’s losing steam. Boeing, Ford and Kraft are also due.

That said, US company earnings are providing a sliver of hope — more than three-quarters of firms that have reported so far either beat or met expectations. But there are doubts about how long they can weather economic challenges. Top-tier firms including Apple, Amazon and Mastercard will report tomorrow, on what will be a $9.4 trillion day in the US and Europe. Last but not least tomorrow the US will report the first estimate of Q2 GDP which is expected to print negative confirming a US technical recession. “Inflation is hurting companies and the question is whether these policy rate hikes are going to do anything to alleviate the pain,” Quadratic Capital Management founder Nancy Davis said on Bloomberg Television.

Elsewhere, President Joe Biden will speak with Chinese leader Xi Jinping on Thursday amid fresh tensions over Taiwan. The White House is also considering whether to lift some tariffs on Chinese imports to stem inflation.

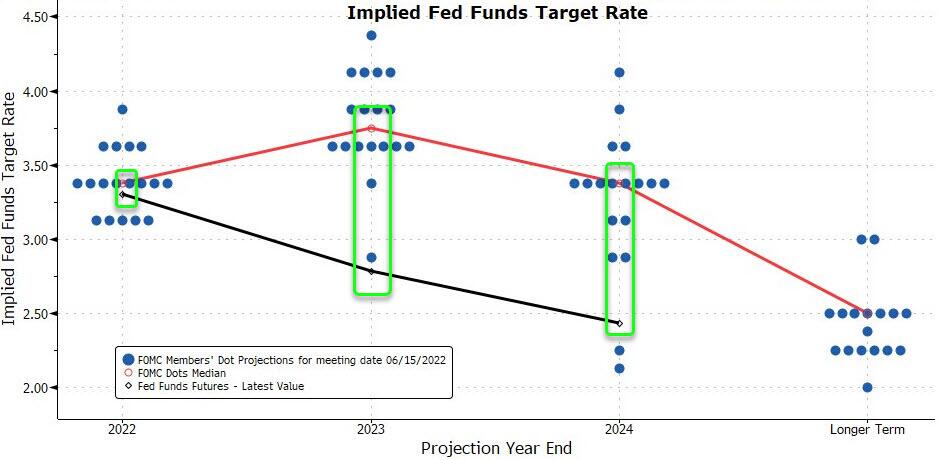

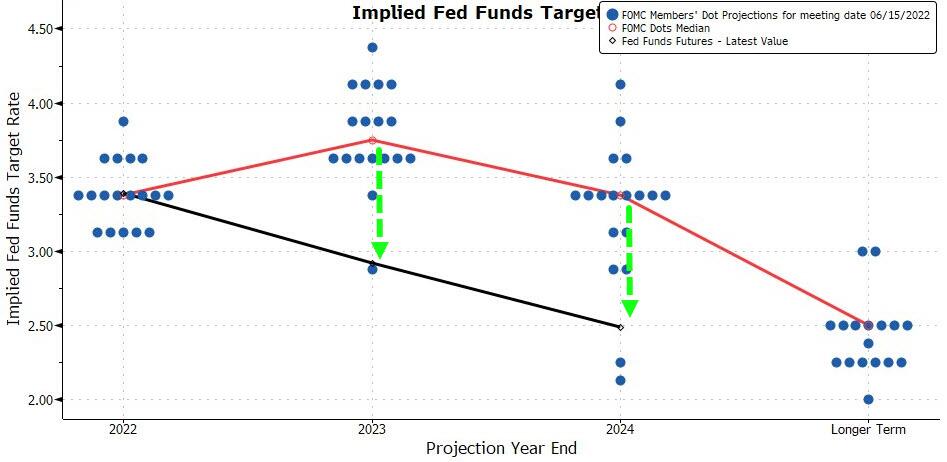

And speaking of the Fed, the swaps market currently prices in around 77bp of rate hikes for today’s Fed decision and combined additional 183bp by the December FOMC meeting. The projected 75 basis-point Fed move to tackle price pressures would cement the steepest two-month rise in rates since the 1980s. The key question is whether Chair Jerome Powell’s policy signals validate or refute scaled-back bets projecting a 3.4% peak fed funds rate around year-end and cuts in 2023 to shore up an economy at risk of recession.

“The Fed hasn’t even gotten to neutral yet,” Jason England, global bonds portfolio manager at Janus Henderson Investors, said on Bloomberg Television. “For them to start easing already or for them to start seeing eases priced in is, I think, a little premature.”

In any case, Powell is expected to acknowledge that downside risks to growth have increased and reiterate the Fed’s commitment to controlling inflation. A full FOMC preview can be found here.

“The risk is that Powell starts to set markets up for a move back to a default position of 50bp moves, though we can see little reason for the Fed to lose the optionality of going 75bp when there is significant news that they may have to react to between this and the next meeting,” according to RBC Capital Markets strategist Adam Cole. Meanwhile, the ECB will deliver only 50 basis points of additional interest rate increases this year as the euro zone succumbs to a recession in the fourth quarter, according to JPMorgan.

In Europe, the Stoxx 50 rose 0.6% with travel, personal care and tech are the strongest performing sectors. Credit Suisse shares gained as the bank replaced its embattled chief executive officer and said it would embark on a new turnaround plan just nine months after the last one, while Deutsche Bank fell after it scrapped an efficiency target for the year and warned a key profitability goal was getting harder to reach. Here are the most notable European movers:

- UniCredit shares jumped as much as 7.4% after what Jefferies said was a “bumper” quarter, with new 2022 profit guidance about 10% above consensus. The lender reported net income for 2Q that doubled analyst expectations.

- Reckitt shares jump as much as 6.7%, after the consumer-goods company reported 2Q sales that beat estimates and raised its outlook for the year.

- Worldline shares jump as much as 15% after the payment firm’s 2Q revenue and margin beat expectations, with strength driven by the in- focus merchant services arm, according to analysts.

- Holcim shares climb as much as 5.9% after it reported 2Q sales that beat the average estimate, with analysts highlighting the building materials company’s success in raising prices.