by harveyorgan · in Uncategorized · Leave a comment·Edit

in Uncategorized · Leave a comment·Edit

ACCESS MARKET:

GOLD $1766.50

SILVER: $20.36

Bitcoin morning price: $23,833 UP 6

Bitcoin: afternoon price: $23,874. UP 47

Platinum price: closing UP $8.85 to $899.10

Palladium price; closing up $35.90 at $2130.1-

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: AUGUST 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,750.300000000 USD

INTENT DATE: 07/28/2022 DELIVERY DATE: 08/01/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 390 810

072 H GOLDMAN 2086

104 C MIZUHO 626

118 C MACQUARIE FUT 266

132 C SG AMERICAS 40 4

167 C MAREX 546

190 H BMO CAPITAL 1620

323 C HSBC 910

357 C WEDBUSH 11

363 H WELLS FARGO SEC 508

365 C ED&F MAN CAPITA 6

365 H ED&F MAN CAPITA 1

523 C INTERACTIVE BRO 5

624 H BOFA SECURITIES 1962

657 C MORGAN STANLEY 6240

661 C JP MORGAN 2036 5787

661 H JP MORGAN 117

685 C RJ OBRIEN 18

686 C STONEX FINANCIA 1 58

686 H STONEX FINANCIA 81

690 C ABN AMRO 21 205

DLV615-T CME CLEARING

BUSINESS DATE: 07/28/2022 DAILY DELIVERY NOTICES RUN DATE: 07/28/2022

PRODUCT GROUP: METALS RUN TIME: 20:41:57

709 C BARCLAYS 3912

732 C RBC CAP MARKETS 2765 13

737 C ADVANTAGE 1

800 C MAREX SPEC 43

880 C CITIGROUP 502

880 H CITIGROUP 1876

905 C ADM 11 190

TOTAL: 16,834 16,834

MONTH TO DATE: 16,834

JPMorgan stopped 5787/16,834

_____________________________________________________________________________________

GOLD: NUMBER OF NOTICES FILED FOR AUGUST CONTRACT:

16,834 NOTICES FOR 1,683400 OZ //52.360 TONNES

total notices so far: 16,834 contracts for 1,683,400 oz (52.360 tonnes)

SILVER NOTICES:

669 NOTICES FILED FOR 3,345,000 OZ/

total number of notices filed so far this month 669 : for 3,345,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $12,50

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGE IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 1005.29 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 30 CENTS

AT THE SLV// ://HUGE CHANGES IN SILVER INVENTORY AT THE SLV//:A WITHDRAWAL OF 0.461 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 483.118 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 4490 CONTRACTS TO 143,598 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE HUGE LOSS IN OI WAS ACCOMPLISHED DESPITE OUR HUGE $1.24 GAIN IN SILVER PRICING AT THE COMEX ON THDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $1.24) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY COMMERCIAL SILVER LONGS// WE HAD HUGE SPECULATOR LIQUIDATIONS AS WE HAD A HUGE LOSS OF 3238 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT LIQUIDATIONS//HUGE BANKER OI COMEX GAIN /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A FAIR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ / // V) GIGANTIC SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: +53

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTACTS for 20 days, total 17,422 contracts: 87.110 million oz OR 4.05 MILLION OZ PER DAY. (871 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 87.110 MILLION OZ

.

LAST 15 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4490 DESPITE OUR $1.24 GAIN IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 1305 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER ADDITIONS ////// HUGE SPECULATOR SHORT LIQUIDATION// WE HAVE A POOR INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ // .. WE HAD A HUGE SIZED LOSS OF 3185 OI CONTRACTS ON THE TWO EXCHANGES FOR 15.93 MILLION OZ AS..THE SPECS WERE SENT TO THE SLAUGHTER HOUSE.

WE HAD 669 NOTICES FILED TODAY FOR 3,345,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 3,193 CONTRACTS TO 485,668 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -799 CONTRACTS.

.

THE GOOD SIZED INCREASE IN COMEX OI CAME DESPITE OUR HUGE RISE IN PRICE OF $31.25//COMEX GOLD TRADING/THURSDAY / WE MUST HAVE HAD ADDITIONAL SPECULATOR SHORT SHORT COVERINGS ACCOMPANYING OUR GOOD SIZED EXCHANGE FOR PHYSICAL ISSUANCE.//WE HAD OUR CONCLUSION OF SPREADER LIQUIDATION WHICH TOOK CARE OF MUCH OF THE COMEX OI.. WE HAD ZERO LONG LIQUIDATION //AND HUGE SPECULATOR SHORT COVERINGS//HUGE ADDITIONS TO OUR BANKER LONGS!! THE COMEX IS ONE BIG FARCE

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR AUGUST AT 99.272 TONNES ON FIRST DAY NOTICE

YET ALL OF..THIS HAPPENED WITH OUR HUGE RISE IN PRICE OF $31.25 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 7986 OI CONTRACTS 24.840 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4743 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 4865,668

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7986 CONTRACTS WITH 3193 CONTRACTS INCREASED AT THE COMEX AND 4743 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 8735 CONTRACTS OR 27.169 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4743) ACCOMPANYING THE GOOD SIZED GAIN IN COMEX OI (3,193): TOTAL GAIN IN THE TWO EXCHANGES 7986 CONTRACTS. WE NO DOUBT HAD 1) HUGE SPECULATOR SHORT COVERINGS//STRONG BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR AUGUST. AT 99.272 TONNES 3) ZERO LONG LIQUIDATION AND THE CONCLUSION OF SPREADER LIQUIDATION///// //.,4) GOOD SIZED COMEX OPEN INTEREST GAIN 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST :

121,665 CONTRACTS OR 12166,500 OZ OR 378,43 TONNES 20 TRADING DAY(S) AND THUS AVERAGING: 6083 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAY(S) IN TONNES: 378.43 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 378.43/3550 x 100% TONNES 10.67% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JULY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A GIGANTIC SIZED 4490 CONTRACT OI TO 143,598 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1305 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 1305 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1305 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 4490 CONTRACTS AND ADD TO THE 1305 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED LOSS OF 3185 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 15.93 MILLION OZ

OCCURRED DESPITE OUR RISE IN PRICE OF $1.24

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED DOWN 29.34 PTS OR 0.89% //Hang Sang CLOSED DOWN 466.17 OR 2.26% /The Nikkei closed UP 13.84 OR % 0.05. //Australia’s all ordinaires CLOSED UP 0.81% /Chinese yuan (ONSHORE) closed UP AT 6.7355//OFFSHORE CHINESE YUAN UP 6.7343// /Oil DOWN TO 98.77 dollars per barrel for WTI and BRENT AT 103.98// SHANGHAI CLOSED DOWN 29.34 PTS OR 0.89% //Hang Sang CLOSED DOWN 466.17 OR 2.26% /The Nikkei closed DOWN 13.84 OR % 0.05. //Australia’s all ordinaries CLOSED UP 0.81% / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GOOD SIZED 3193 CONTRACTS TO 485,668 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS GOOD COMEX INCREASE OCCURRED DESPITE OUR HUGE RISE OF $31.25 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A GOOD SIZED EFP (4743 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF AUGUST.. THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4743 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :4743 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4743 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED SIZED TOTAL OF 7986 CONTRACTS IN THAT 4743 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED COMEX OI GAIN OF 3193 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR HUGE SIZED GAIN IN PRICE OF GOLD $ 31.25. TODAY, WITNESSED THE CONCLUSION OF SPREADER LIQUIDATION. WE ALSO ARE WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS IS AN ABSOLUTE FARCE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING AUGUST (99.228),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:99.228 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $31.25) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AND COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO COVER TO THEIR POSITIONS////// WE HAVE REGISTERED A STRONG SIZED GAIN OF 27.169 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR AUGUST (99.228 TONNES)…

WE HAD -799 CONTRACTS ADDED TO COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 7986 CONTRACTS OR 798600 OZ OR 24.84 TONNES

Estimated gold volume 140,374/// poor/

final gold volumes/yesterday 253,702 / fair

INITIAL STANDINGS FOR AUGUST ’22 COMEX GOLD //JULY 29

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 302,674.161oz Brinks JPMorgan HSBC Manfra Malca Int. Delaware 3300 kilobars (HSBC) |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 16,834 notice(s) 1,683,400 OZ 52.360 TONNES |

| No of oz to be served (notices) | 15,068 contracts 1,506,800 oz 46.86 TONNES |

| Total monthly oz gold served (contracts) so far this month | 16,834 notices 1,683,400 OZ 52.360 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

No dealer withdrawals

Customer deposits: 0

total deposits: 0 oz

6 customer withdrawals:

i) out of Brinks: 227.712 oz

ii) out of JPMorgan: 165,385.911 oz

iv)out of Manfra: 1,791,431 oz

v) Out of Malca: 17,569.647 oz

total withdrawals: 302,674.161 oz (9.4 tonnes)

ADJUSTMENTS: dealer to customer/Malca

16,498.670

and manfra: 14,892.276 oz

customer to dealer: Manfra 383.812 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 31,916 contracts having LOST 11,812 contracts .

Thus by definition, the initial amount of gold that will stand for this active month of August is as follows:

31,902notices x 100 oz per notice = 3,190,200 oz or 99.228 tonnes

Sept. gained 71 contracts to 3902 contracts.

October gained 5429 contracts up to 39,117

We had 16,834 notice(s) filed today for 1,683,400 oz FOR THE AUGUST 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 2036 notices were issued from their client or customer account. The total of all issuance by all participants equate to 16,834 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 5787 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2022. contract month,

we take the total number of notices filed so far for the month (16,834) x 100 oz , to which we add the difference between the open interest for the front month of (AUGUST 31,902 CONTRACTS ) minus the number of notices served upon today 16,834 x 100 oz per contract equals 3,190,200 OZ OR 99.228 TONNES the number of TONNES standing in this active month of AUGUST.

thus the INITIAL standings for gold for the AUGUST contract month:

No of notices filed so far (16,834) x 100 oz+ (31,902) OI for the front month minus the number of notices served upon today (16.834} x 100 oz} which equals 3,190,200 oz standing OR 99.228 TONNES in this active delivery month of August.

TOTAL COMEX GOLD STANDING: 99.228 TONNES (A HUGE STANDING FOR AUGUST ( ACTIVE) DELIVERY MONTH)

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,360,873,921 oz 73.43 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 30,332,431.006 OZ

TOTAL REGISTERED GOLD: 15,404,287.310 OZ (479.14 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 14,928,143.296 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 13,004,341.0 OZ (REG GOLD- PLEDGED GOLD) 404.6 tonnes

END

SILVER/COMEX/JULY 29

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 738,530.160 oz Brinks HSBC JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 901,274.480 oz Delaware JPMorgan |

| No of oz served today (contracts) | 669 CONTRACT(S) 3,345,000 OZ) |

| No of oz to be served (notices) | 102 contracts (510,000 oz) |

| Total monthly oz silver served (contracts) | 669 contracts 3,345,,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 0 deposits into the customer account

total deposit: nil oz

JPMorgan has a total silver weight: 174.508 million oz/336.758 million =51.81% of comex

Comex withdrawals:3

i) Out of JPM: 594,745.300 oz

ii) Out of Loomis: 342,868.510 oz

iii) Out of Manfra: 60,568.800 oz

total: 998,182.610 oz

adjustments: 1//dealer to customer

JPMorgan: 269,943.06 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 55.452 MILLION OZ

TOTAL REG + ELIG. 336.758 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF AUGUST OI: 771 CONTRACTS HAVING LOST 58 CONTRACTS.

THUS BY DEFINITION, THE INITIAL AMOUNT OF SILVER STANDING IN THIS NON ACTIVE DELIVERY MONTH OF AUGUST IS AS FOLLOWS:

771 NOTICES X 5,000 OZ PER NOTICE = 3,855,000

SEPTEMBER HAD A LOSS OF 5423 CONTRACTS DOWN TO 109,563

CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 669 for 3,345,000 oz

Comex volumes:62,618// est. volume today// fair

Comex volume: confirmed yesterday: 92,999 contracts ( very good )

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 669 x 5,000 oz = 3,345,000 oz

to which we add the difference between the open interest for the front month of AUGUST(771) and the number of notices served upon today 669 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST./2022 contract month: 669 (notices served so far) x 5000 oz + OI for front month of AUGUST (771) – number of notices served upon today (669) x 5000 oz of silver standing for the AUGUST contract month equates 3,855,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JULY 29//WITH GOLD UP $12.50; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1005.29 TONNES

JULY 28/WITH GOLD UP $31.25; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 27.//WITH GOLD UP $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 26/WITH GOLD DOWN $1.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.29 TONNES

JULY 25/WITH GOLD DOWN $7.85: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 1005.87 TONNES

JULY 22/WITH GOLD UP $17.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 21/WITH GOLD UP $11.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.101 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.87 TONNES

JULY 20/WITH GOLD DOWN $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1009.06 TONNES

JULY 19/WITH GOLD DOWN $.35 :BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.22 TONNES FROM THE GLD//INVENTORY RESTS AT 1009.06 TONNES

JULY 18/WITH GOLD UP $7.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.28 TONNES

JULY 15/WITH GOLD DOWN $3.75:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD///INVENTORY RESTS AT 1016.89 TONNES//

JULY 14/WITH GOLD DOWN $28.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD//INVENTORY RESTS AT 1019.79 TONNES

JULY 13/WITH GOLD UP $10.55:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD//INVENTORY RESTS AT 1021.53TONNES

JULY 12/WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESS AT 1023.27 TONNES

JULY 11/WITH GOLD DOWN $4.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD./INVENTORY RESTS AT 1023.27 TONNES

JULY 7/WITH GOLD UP $1.35: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.61 TONNES FORM THE GLD///INVENTORY REST AT 1024.43 TONNES

JULY 6/WITH GOLD DOWN $26.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 9.86 TONNES FROM THE GLD//INVENTORY REST AT 1032.04 TONNES

JULY 5/WITH GOLD DOWN $36.55//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.41 TONNES FROM THE GLD///INVENTORY RESTS AT 1041.90 TONNES

JULY 1/WITH GOLD DOWN $5.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES//INVENTORY RESTS AT 1050.31 TONNES

JUNE 30/WITH GOLD DOWN $9.20: big CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 1052.63 TONNES//

JUNE 28/WITH GOLD DOWN $3.05//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.64 TONNES FROM THE GLD///INVENTORY RESTS AT 1056.40 TONNES

JUNE 27/WITH GOLD DOWN $4.90 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.04 TONNES

JUNE 24/WITH GOLD UP 45 CENTS TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.70 TONNES FROM THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 23/WITH GOLD DOWN $8.60:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//INVENTORY RESTS AT 1071.77 TONNES

JUNE 22/WITH GOLD UP 15 CENTS:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1073.80 TONNES

GLD INVENTORY: 1005.29 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JULY 29/WITH SILVER UP 30 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 461,000 OZ FROM THE SLV..//INVENTORY RESTS AT 483.657 MILLION OZ/

JULY 28/WITH SILVER UP $1.24 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 484.118 MILLION OZ/

JULY 27/.WITH SILVER UP 4 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL 11.479 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 484.118MILLION OZ//

JULY 26/WITH SILVER UP 16 CENTS: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.504 MILLION OZ FROM THE SLV//: //INVENTORY RESTS AT 495.597 MILLION OZ//

JULY 25/WITH SILVER DOWN 24 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.383 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 499.101 MILLION OZ//

JULY 22/WITH SILVER DOWN 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 500.484 MILLION OZ//

JULY 21/WITH SILVER UP 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.19 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 500.484MILLION OZ/

JULY 20/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 8.253 MILLION OZ FORM THE SLV/INVENTORY RESTS AT 507.585 MILLION OZ//

JULY 19/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ//

JULY 18/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 4.995 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ.

JULY 15/WITH SILVER UP 31 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 3.226 MILLION OZ FORM THE SLV//INVENTORY RESTS AT 510.443 MILLIONOZ//

JULY 14/WITH SILVER DOWN 88 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 OZ FROM THE SLV// //INVENTORY RESTS AT 513.671 MILLION OZ

JULY 13/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SV//INVENTORY RESTS AT 514.501 MILLION OZ.

JULY 12/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.228 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 514.501 MILLION OZ//

JULY 11/WITH SILVER DOWN 17 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 5.533 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 517.729 MILLION OZ

JULY 7/WITH SILVER UP 3 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.889 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 523.262 MILLION OZ/

JULY 6/WITH SILVER UP ONE CENT: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 12.558 MILLION OZ FORM THE SLV///INVENTORY RESTS AT 528.151 MILLION OZ

JULY 5/WITH SILVER DOWN 55 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 540.709MILLION OZ//

JULY 1/WITH SILVER DOWN 61 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ//INVENTORY RESTS AT 540.709 MILLION OZ//

JUNE 30/WITH SILVER DOWN 41 CENTS : SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 738,000 OZ FROM THE SLV//INVENTORY RESTS AT 541.262 MILLION OZ//

JUNE 28/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.00 MILLION OZ..

JUNE 27/WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 24/WITH SILVER UP 10 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.137 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 23/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 2.029 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 545.137 MILLION OZ//

JUNE 22/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.166 MILLION OZ.

CLOSING INVENTORY 483.657 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

3.Chris Powell of GATA provides to us very important physical commentaries

Your weekend reading material

(courtesy Alasdair Macleod)

Alasdair Macleod: Challenges for the new prime minister

Submitted by admin on Thu, 2022-07-28 11:34Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, July 28, 2022

Britain’s next prime minister must address two overriding problems: London is at the centre of an evolving financial and currency crisis brought forward by a change in interest rate trends; and the reality of emerging Asian superpowers must be accommodated instead of attacked.

This article starts by examining the economic challenges the next prime minister faces domestically. Are the two candidates equipped with a strategy to improve the nation’s economic prospects, and why can we expect them to succeed where others have failed?

It is unlikely that either candidate is aware that there has been a fundamental shift in the direction of interest rates, the consequences of which are undermining debt mountains everywhere. The problem is particularly acute for the euro system. As well as for other major currencies, London operates as the clearing centre for transactions between the Eurozone’s commercial banks. If the euro system fails, London’s survival as a financial centre could be jeopardised.

The other major challenge is geopolitical. Being tied into America’s five-eyes intelligence network, coupled with policies to remove fossil fuels as sources of energy Britain is condemned to falling behind the Asian superpowers, and sacrificing trading relationships with which her true interests must surely lie. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/challenges-for-the-new-prime-minister

END

An excellent commentary from Chris Powell of GATA concerning how gold mined in West Africa is now being used to increase wealth of its citizens

by staying in their country.

(Chris Powell/GATA)

Gold yet may awaken the rich countries insisting on being poor

Submitted by admin on Fri, 2022-07-29 00:15Section: Daily Dispatches

12:27a ET Friday, July 29, 2022

Dear Friend of GATA and Gold:

You may recall that your secretary/treasurer long has lamented “the rich countries insisting on being poor,” the still-developing countries with large gold resources and even large gold production that nevertheless have declined to incorporate the metal into their monetary systems but instead have remained the slaves of the developed world and its more sophisticated — and exploitive — monetary systems.

Almost miraculously, some Nigerians have just set out to do something about it comprehensively.– to build what they call a “gold value chain” in the gold treasure house of west Africa — really, a gold economy in which metal mined locally is turned into not just jewelry locally but also local savings of wealth through a digitized system of gold ownership in which metal credits can be converted to gold coins and bars at local banks.

The enterprise, called Sanu, a west African word for gold, has been started by Kian Smith Trade & Co. Ltd. in Lagos, which operates a gold refinery and other businesses. Sanu has created an internet application that allows the purchase of small amounts of gold and silver that can be redeemed for metal in LBMA-certified products at bank branches not only in Nigeria but also London and Dubai. All metal purchases via Sanu are made on a fully allocated basis — no fractional-reserve gold banking here, as in London and New York.

Sabu’s objective is to help the people of west Africa invest and save in their region’s own natural wealth and protect themselves with a local form of money against the notorious inflation of developing-country currencies.

Will African governments facilitate this or permit it to be successful for long, insofar as demand for gold is sure to reduce demand for African government currencies? That is a critical question, but African governments recently have shown some recognition of gold’s enduring monetary properties and the strength gold can bring to their currencies. Ghana lately has been acquiring domestically produced gold for its central bank reserves, and Zimbabwe has just begun experimenting with gold coinage redeemable at its central bank.

A crucial insight about Sanu’s objective was offered this week in an interview with the Lagos newspaper This Day by the executive vice chairman of the Kian Smith refinery, Nere Emiko:

We really believe that we have the product that gives gold to the people. Everywhere we’ve gone in the last few years people keep asking: ‘This gold you say you are refining, that you’re selling — where is it?’ The same thing is actually happening for Burkina Faso, which is No. 2 in west Africa after Ghana for gold production. Believe it or not, but most people in Burkina Faso have never seen gold. Yet Burkina Faso has several airstrips dedicated to daily evacuation of gold.

So a lot of what you find happening in our region is there are wealth and mineral resources that we are producing but can’t access, and this is a way of now giving Nigerians, west Africans, and anyone in Africa the opportunity to access gold.

Apart from jewelry, it is almost impossible to access gold refined to international standards in our local currencies. We have done all the work now to give the people access to gold in the small retail quantities they want, empowering women and giving gold to the people.

What happens when the people of gold-producing developing countries start seeing the metal they mine functioning as savings and money in their daily lives, an alternative not only to their local currencies but also to their current inflation hedge, the U.S. dollar?

They may become independent and sovereign in a very practical sense — a danger to the imperial powers of the West. But then those imperial powers, already tied up with the war in Ukraine, can’t invade everybody.

Sanu’s internet site explains its operation:

Recent Nigerian television news interviews about it can be viewed at YouTube here:

Something similar should be attempted in Central and South America, other gold-producing regions full of rich countries insisting on being poor.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

4. OTHER GOLD/SILVER COMMENTARIES

JPMorgan’s gold ‘boss’ led group plot to spoof prices, jury told

Bloomberg News | July 28, 2022 | 1:43 pm Intelligence USA Gold

JPMorgan not leaving physical commodities: report

Michael Nowak was “the boss” of a plot at JPMorgan Chase & Co. to manipulate gold and silver prices and worked with the top trader and salesman on the bank’s precious metals desk to “spoof” markets with bogus buy and sell orders, a federal prosecutor told jurors in Chicago.

“For years, executives at one of the world’s largest banks conspired to manipulate the markets for precious metals,” Matthew Sullivan, an attorney in the US Department of Justice, said Thursday during closing arguments in the trial of Nowak, Gregg Smith and Jeffrey Ruffo. “All three worked together toward the same goal: earning profits for the precious-metals desk by spoofing.”

Prosecutors are wrapping up the biggest criminal case by the US in its crackdown on market manipulation following the global financial crisis. Nowak and Smith are charged with racketeering conspiracy as well as conspiring to commit price manipulation, wire fraud, commodities fraud and spoofing from 2008 to 2016. Ruffo is charged with racketeering and conspiracy. They face years in prison if convicted.

Over the past three weeks, government witnesses described how Nowak, who ran the desk, and Smith, its chief gold trader, routinely placed huge buy and sell orders they never intended to execute. It was part of their strategy to push prices in the direction that would profit the bank, said two former JPMorgan traders who agreed to cooperate after pleading guilty. Ruffo encouraged the practice to benefit his hedge fund clients, they said.

JPMorgan, one of the most influential banks in the precious-metals market, already has paid $920 million to settle Justice Department spoofing allegations against it.

‘Power and influence’

“The defendants had power and influence, and together they abused their positions and rigged the precious metals markets for their own gain,” Sullivan said. “They did it by spoofing, which put simply is a lie to make money by tricking other people in the market.”

Defense lawyers are scheduled to make their case to jurors later Thursday and on Friday, after which the case will go to the jury. Over the course of the trial, they’ve argued that all the alleged spoof orders were legitimate. They say there are other explanations for entering large orders to buy and sell futures contracts at the same time on behalf of clients or to provide market pricing, not to fool rivals with bogus spoof trades.

Sullivan described Nowak as “the boss” of the operation as managing director of the precious-metals business, overseeing JPMorgan’s trading and vaults around the world. The prosecutor cited several examples of Nowak’s trading records showing he placed big buy or sell orders that were quickly canceled after he executed smaller orders on the opposite side of the market.

Two junior members of the JPMorgan team, Christian Trunz and John Edmonds, testified for the government that this pattern was part of a trading strategy they learned from Nowak and Smith and was a routine way they all operated for years.

“Mr. Trunz and Mr. Edmonds gave you an insider’s account of the criminal activity that took place while they worked side by side with the defendants on the desk, watching and learning from them,” Sullivan told the jury. “They described what they saw and what they heard on the desk.”

Nowak lied to regulators about his trading because he knew his spoofing was wrong, and encouraged Trunz to do the same by not cooperating with prosecutors after Edmonds had agreed to plead guilty, Sullivan said.

“The heat was on,” Sullivan said. “The conspiracy’s secrets were now in the open.”

Trunz had described an encounter with Nowak, who he considered a close friend and mentor, in which the executive “pressured Mr. Trunz” to stick with the false narrative that all their orders were placed with the intent to trade, Sullivan said. Nowak told him, “You’re not going to turn around and plea now, are you?” according to Trunz, who said he interpreted that as a directive to lie.

The government also presented trading records for Smith, who was relied upon to handle most of the big buy and sell orders from JPMorgan clients Ruffo dealt with, including Moore Capital Management and Tudor Capital Corp. Trunz had described Smith as an expert spoofer, and that Ruffo encouraged him to use the tactic to keep his clients happy.

“They did this to get better prices for Jeff Ruffo’s big hedge fund clients,” Sullivan said. “Better prices meant more money for the desk and for themselves.”

The case is US v. Smith et al, 19-cr-00669, US District Court, Northern District of Illinois (Chicago)

end

Andrew Maguire from the vault:

https://kinesis.money/live-from-the-vault/

end

5.OTHER COMMODITIES: WHEAT

END

COMMODITIES IN GENERAL/

END

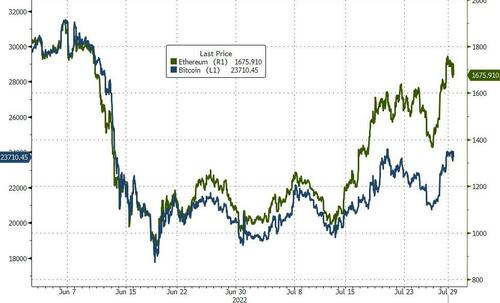

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.7355

OFFSHORE YUAN: 6.7343

HANG SENG CLOSED DOWN 466.17 PTS OR 2.26%

2. Nikkei closed DOWN 13.84 OR 0.05%

3. Europe stocks CLOSED ALL GREEN

USA dollar INDEX DOWN TO 105,76/Euro RISES TO 1.0225

3b Japan 10 YR bond yield: FALLS TO. +.181/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 133.36/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP -// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +0.8855%/Italian 10 Yr bond yield RISES to 3.24% /SPAIN 10 YR BOND YIELD FALLS TO 2.01%…

3i Greek 10 year bond yield RISES TO 3.007//

3j Gold at $1760.60 silver at: 20.00 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 33/100 roubles/dollar; ROUBLE AT 62.14

3m oil into the 98 dollar handle for WTI and 103 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 133.36DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9534– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9746well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.695 UP 2 BASIS PTS

USA 30 YR BOND YIELD: 3.052 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.84

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Surge Propelled By Stellar Tech, Energy Earnings

FRIDAY, JUL 29, 2022 – 08:16 AM

US and European stock were set for their best month since November 2020 following blowout earnings from the likes of Amazon and Apple last night, and record profits from energy giants Exxon and Chevron this morning, boosted by expectations of shallower Federal Reserve monetary tightening now that the US is technically in a recession. S&P futures rose 0.6% following yesterday’s meltup while Nasdaq 100 futures rose more than 1% after US stocks hit a seven-week high Thursday, as record underinvested hedge funds are forced to chase the move higher now that most downside catalysts (peak inflation, hawkish Fed, earnings disappointment) have been eliminated. The dollar was flat, and 10Y yields rose slightly to 2.70% after plunging as low as 2.65% yesterday after the Q2 GDP print confirmed news of the unofficial US recession.

In premarket trading, Amazon soared as much as 13% in premarket trading on Friday, after the e-commerce giant reported better-than-expected 2Q results and gave an upbeat forecast. Apple rose 2.8% after the iPhone maker reported third-quarter revenue that was stronger than expected. US energy giants Exxon and Chevron both rose sharply higher in premarket trading after reporting record profits for Q2. here are some other notable premarket movers:

- Roku (ROKU US) tumbles 26% after the video-streaming platform company issued a 3Q revenue forecast and reported 2Q results that were weaker than expected, citing a slowdown in TV advertising spending.

- Intel (INTC US) slumps 9.4% after the chip manufacturer reported lower-than-expected 2Q earnings and cut its full-year forecasts

- US-listed Chinese stocks fall in premarket trading, following Asian peers lower, amid a lack of new stimulus policies from China’s top leadership.

- Avantor Inc. (AVTR US) analysts pointed to several factors weighing on the life sciences firm’s results, including its exposure to the European market, forex and Covid. Avantor’s shares slid 11% in US postmarket trading on Thursday.

- Dexcom Inc. (DXCM US) shares slumped as much as 18% in premarket trading, with analysts pointing to disappointing US growth and a delay to the US launch of the medical device maker’s G7 glucose- monitoring system used by people with diabetes. Analysts said the reaction was overdone and a buying opportunity given the growth outlook.

- Edwards Life (EW US) down after posting second- quarter results below analyst expectations, as hospital staff shortages and FX headwinds weigh on the medical technology company’s growth.

Global shares are set for a second weekly advance, paring this year’s rout. The risk is that the recent bout of optimism eventually gets a reality check if inflation stays stubbornly elevated, leaving interest rates higher than investors would like amid an economic downturn.

“At some point, the Fed will pivot policy and that should be better for risk markets, but in the meantime, they’re so bent on quelling inflation that we prefer not to buy the dip here,” Thomas Taw, head of APAC iShares Investment Strategy at BlackRock Inc., said on Bloomberg Radio.

Elsewhere, a call between US President Joe Biden and China’s Xi Jinping underlined bilateral tension even as the leaders sought an in-person meeting.

European stocks also rallied into the month-end after positive earnings buoyed sentiment. The Euro Stoxx 600 rose 0.9%, with Italy’s. FTSE MIB outperforms peers, adding 1.6%, FTSE 100 lags, adding 0.6%. Construction, retailers and consumer products are the strongest performing sectors. The banking sector outperformed after a slate of better-than-expected results from Banco Bilbao Vizcaya Argentaria SA, Standard Chartered Plc and BNP Paribas SA. Hermes International rose about 6% after joining LVMH and Kering SA in posting strong results, showing the luxury consumer is resilient so far to high inflation and worries over a potential economic downturn. Here are some other notable European movers:

- NatWest shares surge as much as 9.5% after the UK lender reported second-quarter earnings that beat estimates, also announcing a special dividend with analysts seeing consensus upgrades ahead.

- Allfunds jumps as much as 14%, most since May, after reporting adjusted Ebitda ahead of Morgan Stanley’s expectations and providing a “reassuring outlook.”

- Zalando rises as much as 8.7% alongside other European ecommerce stocks following blowout results from US giant Amazon, which sent its shares surging in premarket trading.

- Hermes climbs as much as 9.6% to an almost 6-month high after the maker of Kelly handbags reported what Bernstein called a “very strong” beat, with 2Q sales almost 9% ahead.

- L’Oreal jumps as much as 5.2% after it reported 2Q like-for-like sales that beat estimates, with Jefferies calling the performance “another quarter of gravity- defying growth.”

- Fluidra gains as much as 12%, the most intraday since October 2020, despite a guidance cut as analysts remain optimistic on longer-term prospects.

- Kion rises as much as 9.6%, the most since March, bouncing after a post-results decline in the prior session. UBS said it’s positive on the forklift maker’s outlook.

- Signify slumps as much as 11% after reporting 2Q Ebita below consensus and flagging margin headwinds, which Citi expects will lead to low-single-digit downgrades to full-year estimates.

- AstraZeneca slides as much as 3.1% on its latest earnings, which exceeded estimates. Analysts say the beat, however, was fueled by one-time items.

- EssilorLuxottica dips as much as 5.1% after the eyewear firm reported interim results. Jefferies noted the “understandably circumspect” tone of the company’s near-term outlook.

- Fresenius Medical Care declines as much as 5.7%, extending Thursday’s 14% fall, as the market continued to digest the guidance downgrade. JPMorgan cut its price target by more than 50%.

- AMS-Osram shares fall as much as 9.7% after its new guidance consensus estimates, with the chipmaker saying production volumes were hit by increasingly unfavorable end markets.

Euro-zone GDP rose by more than three times the amount economists expected, putting it on a firmer footing as surging inflation and a possible Russian energy cutoff threaten to tip it into a recession. On the other hand, inflation in the region soared to another all-time high, supporting calls for the European Central Bank to follow up its first interest-rate hike since 2011 with another big move.

The tone was more somber in Asia, hampered by a tumble in Chinese tech shares that dragged Hong Kong toward a correction of more than 10% from a June high. Asian stocks slumped as losses in Chinese equities offset gains in the rest of the region, after the nation’s Politburo refrained from announcing new stimulus. The MSCI Asia Pacific Index swung between small gains and losses on Friday. Alibaba and Tencent were among the biggest drags, countering gains in heavyweights including TSMC and Reliance Industries. The Hang Seng Index entered a technical correction, while a gauge of Hong Kong’s tech shares tumbled close to 5%. Sentiment was damped by Chinese leaders’ downbeat assessment of growth and the lack of new measures to boost the economy from a highly anticipated Politburo meeting. Shares of Alibaba tumbled after a report said that Jack Ma was planning to give up control of his fintech unit Ant Group, ahead of the tech giant’s earnings report next week.

“We were kind of looking for more policy” from the Chinese government before the National Party Congress later this year, Thomas Taw, head of APAC iShares Investment Strategy at BlackRock Inc., said on Bloomberg Radio. “I think the offshore, foreign sentiment towards China is very, very bearish at the moment.” Investors are also monitoring the latest corporate results while keeping an eye on the property crisis and Covid situation in China. Major overseas earnings before the Asian open were a mixed bag, with strong reports from Apple and Amazon while Intel disappointed. The key Asian stock gauge is still on track for its biggest monthly gain so far in 2022. While stocks in Hong Kong and mainland China are set for a monthly loss, the region’s other markets such as India, Japan and South Korea are poised for their best months of the year.

Japanese stocks dipped in afternoon trading as the yen resumed strengthening against the dollar. The Topix fell 0.4% to close at 1,940.31, while the Nikkei was down 0.1% to 27,801.64. Still the Nikkei closed July with a 5.3% gain, its best month since November 2020. The yen rose 0.9% to around 133 per dollar, pushing its three-day advance to 2.8%. Yen Advances to Level That Threatens This Year’s Big FX Short Keyence Corp. contributed the most to the Topix decline, decreasing 2.8% after it missed earnings expectations. Out of 2,170 shares in the index, 601 rose and 1,469 fell, while 100 were unchanged.

In FX, the Bloomberg dollar spot index falls 0.3%. GBP and CAD are the weakest performers in G-10 FX, JPY continues to outperform, trading at 133.11/USD.

In fixed income, Treasuries were cheaper across the curve with losses led by the long-end, where yields are higher by around 4bp. Wider losses seen across bunds and gilts, weighing on Treasuries as ECB rate-hike premium is added in after a mix of CPI and GDP data out of Eurozone. US 10-year yields around 2.70%, cheaper by 2bp on the day and outperforming bunds and gilts by 3.5bp and 4.5bp in the sector; long-end led losses steepens 2s10s, 5s30s spreads each by around 2bp on the day. IG issuance slate empty so far; four names priced $5.1b Thursday, paying 15bp in concessions on order books that were 3 times oversubscribed.

WTI trades within Thursday’s range, adding 2.1% to trade around $98. Spot gold rises roughly $8 to trade close to $1,765/oz. Most base metals trade in the green; LME zinc rises 3.9%, outperforming peers.

Looking to the day ahead, data includes the employment cost index, PCE, income, and spending data in the US, Tokyo CPI, consumer confidence, jobless rate, retail sales, industrial production, and starts in Japan, CPI and GDP in France, GDP in Germany, and GDP in Canada. It’s another full slate of earnings which will include Sony, Exxon, Procter & Gamble, Chevron, AbbVie, AstraZeneca, Colgate-Palmolive, BNP Paribas, Eni, Intesa Sanpaolo, LyondellBasell, Engie, BBVA, NatWest, and Citrix.

Market Snapshot

S&P 500 futures up 0.7% to 4,103.00

Gold spot up 0.4% to $1,763.27

U.S. Dollar Index down 0.36% to 105.97

Top Overnight News from Bloomberg

- Euro-zone inflation climbed to another all-time high, supporting calls for the European Central Bank to follow up its first interest-rate hike since 2011 with another big move

- The euro-zone economy expanded by more than three times the amount economists expected, putting it on a firmer footing as surging inflation and a possible Russian energy cutoff threaten to tip it into a recession

- Stocks in Europe and the US are set for their biggest monthly advance since November 2020 on positive earnings and expectations of shallower Federal Reserve monetary tightening

- China’s top leadership is committing to ample liquidity as the nation contends with a slowdown. So far, a lot of that cash is sitting in the financial system instead of being transmitted to the real economy

- Biden, Xi Plan In-Person Meet as Taiwan Tensions Intensify

- Amazon, Apple Poised to Add $230 Billion After Resilient Results

- Citigroup Drops Some Clients to Boost Trading Returns

- Credit Suisse Woes Spread to Singapore With $800 Million Trial

- Bitcoin and Ether Are on Track for Their Best Month Since 2021

- Russia Is Wiring Dollars to Turkey for $20 Billion Nuclear Plant

- Alibaba Slumps as Traders Assess Earnings Risk, Ant Report

- BofA Says Too Soon for Bull Rally as Investors Pile Into Stocks

- Singapore, New York Tie for Highest First Half Rental Growth

- Morgan Stanley Hires Shen as Head of China Onshore Equities

- Alito Mocks Foreign Leaders Who Attacked His Abortion Opinion

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed despite the positive lead from Wall Street, with Chinese markets lagging. ASX 200 was lifted by gold names amid the recent rise in the precious metal. Nikkei 225 saw mild gains throughout the session but eventually fell into the red amid notable JPY strength, whilst Nissan shares fell over 4% at one point after earnings. KOSPI was propelled by its Telecom sector, with Financials and Industrials also aiding. Hang Seng slipped over 2% with Alibaba shedding 6% after WSJ reported that Jack Ma intends to relinquish control of Ant Group. Headlines pointed out the Hang Seng index has fallen 10% from its June peak. Shanghai Comp held a negative bias as traders reacted to the Biden-Xi call, which included no rollback of Trump-era tariffs. Selling thereafter resumed following downbeat commentary from China’s MOFCOM, suggesting the outlook for H2 trade growth is not optimistic.

Top Asian News

- China’s Commerce Ministry said China’s foreign trade faces higher risks; the outlook for China’s H2 trade growth is not optimistic, via Bloomberg. MOFCOM said they will study targeted measures for foreign trade, and will step up support for export credit insurance in H2 and expand imports actively and ensure domestic commodity supply, via Reuters.

- China’s Commerce Ministry official said foundation for consumption recovery is not solid yet, more efforts needed to boost consumption, via Reuters.

- Japanese government decided to tap JPY 257bln in budget reserves to help with rising oil and broader inflation, according to the MoF.

- PBoC injected CNY 2bln via 7-day reverse repos with the maintained rate of 2.10% for a net drain of CNY 1bln and for a weekly drain of CNY 12bln

- PBoC set USD/CNY mid-point at 6.7437 vs exp. 6.7414 (prev. 6.7411)

- Japan’s Finance Minister Suzuki provides no comment on day-to-day FX moves, closely watching moves with a sense of urgency while working with the BoJ; Japan’s MOF said it did not intervene in FX in the June 29th to July 27th period.

European bourses are firmer across the board, Euro Stoxx 50 +0.9%, and are set to post their best monthly performance since Nov’20. Stateside, the NQ continues to outperform, +1.2%, amid after-market earnings from AMZN and AAPL; US PCE Price Index ahead.

Top European News

- Germany Stagnates as Rest of Europe Beats Estimates: GDP Update

- UK June Mortgage Approvals Fall to 24-Month Low of 63.7k

- Ukraine Latest: Lavrov in No Rush to Respond to Blinken Request

- Amundi Defies Gloom Among Managers With $1.8-Billion Inflows

- Biden, Xi Plan In-Person Meet as Taiwan Tensions Intensify

FX

- Yen recovery momentum gathers pace and extends beyond Dollar pairing to JPY crosses, USD/JPY slides over 2 big figures to test 132.50, EUR/JPY down to 137.56 from 137.32.

- DXY loses grip of 106.000 post-negative US GDP print and looking for support from PCE, ECI and/or Chicago PMI.

- Euro fades again irrespective of some encouraging Eurozone data and option expiry interest may be capping, EUR/USD tops out just over 1.0250 yet again and circa 3bln rolling off between 1.2045-50.

- Rand underpinned by Gold gains and Lira holds above 18.0000 as Turkish trade deficit narrows and Russia transfers funds for a nuclear facility.

- Sterling fades amidst mixed BoE consumer credit and housing metrics, Cable sub-1.2150 vs 1.2245 at best and EUR/GBP probing 0.8400 vs low around 0.8346 yesterday.

Fixed Income

- Marked debt retracement following run of even more pronounced recovery gains.

- Bunds fade just shy of 158.00 again and retreat to 156.21, Gilts reverse around 100 ticks from 118.36 and T-note to 120-21+ from 121-08 at best.

- Stronger than expected Eurozone data also in the mix along with buoyant risk sentiment and firm oil.

- Bonds braced for busy pm agenda comprising US PCE, ECI and Chicago PMI.

Commodities

- WTI Sep’22 and Brent Oct’22 are posting gains in excess of 2.0% on the session but remain capped by USD 100/bbl and 105/bbl respectively.

- Dutch TTF Sep’22 has pulled back to modestly below the EUR 200/mWh mark, but remains bid after several sessions of pronounced price action.

- Spot gold is relatively contained and resides just above the unchanged mark but continues to be dictated by the USD with the JPY-induced pressure lifting the yellow metal briefly overnight.

- Saudi Energy Minister and Russian Deputy PM Novak met in Riyadh and discussion cooperation between the two nations, according to Twitter, via Reuters.

Biden-Xi Call

- Senior US admin official said US President Biden and China’s President Xi discussed face-to-face meeting and directed teams to follow up; did not discuss any potential lifting of US tariffs on Chinese products.

- White House said presidents Biden and Xi discussed a range of issues important to bilateral relationship and other regional/global issues.

- Senior US admin official said Biden and Xi had a ‘direct and honest’ discussion on Taiwan. They discussed areas of cooperation including climate change, health security and counter-narcotics. Biden brought up the long-standing concerns on human rights. Macroeconomic coordination between China and US is of great importance. Biden explained to Xi his core concerns about China’s economic practices.

- China President Xi told US President Biden that the US should abide by the One China principle, and act in line with its words, according to State Media. On the Taiwan issue, Xi told Biden that ‘those who play with fire will get burned’. Xi told Biden that China fiercely opposes Taiwan independence and the interference of external forces

- US President Biden told China President Xi that the US stance on One China policy remains unchanged, according to China’s Global Times.

Central Banks

- BoJ Summary of Opinions (Jul meeting): achieving the price stability target in a stable manner is difficult given developments in the output gap and inflation expectations. The recent resurgence of COVID-19 is extremely rapid, and it is necessary to examine how this will affect financial positions, mainly of small and medium-sized firms. The Bank needs to closely monitor the impact that the recent increase in its Japanese government bond (JGB) purchases to contain upward pressure on interest rates has on the functioning of the JGB market.

- ECB’s de Guindos says EUR depreciation has been one of the factors behind high inflation, main factor that guides decisions is the evolution of inflation.

- HKMA buys around HKD 9.656bln from the market to defend the peg.

US Event Calendar

- 08:30: 2Q Employment Cost Index, est. 1.2%, prior 1.4%

- 08:30: June Personal Income, est. 0.5%, prior 0.5%

- June Personal Spending, est. 0.9%, prior 0.2%

- June Real Personal Spending, est. 0%, prior -0.4%

- June PCE Deflator MoM, est. 0.9%, prior 0.6%; PCE Deflator YoY, est. 6.8%, prior 6.3%

- June PCE Core Deflator MoM, est. 0.5%, prior 0.3%; Core Deflator YoY, est. 4.7%, prior 4.7%

- 09:45: July MNI Chicago PMI, est. 55.0, prior 56.0

- 10:00: July U. of Mich. Sentiment, est. 51.1, prior 51.1;

- Expectations, est. 47.5, prior 47.3

- Current Conditions, est. 57.1, prior 57.1

- 1 Yr Inflation, est. 5.2%, prior 5.2%; 5-10 Yr Inflation, est. 2.8%, prior 2.8%

DB’s Jim Reid concludes the overnight wrap

Morning from sunny Frankfurt. Today we wave goodbye to July which after the worst first half returns since 1788 in treasuries and 1962 for the S&P 500, is set to launch us into a very strong start to H2. A reminder that in a chart of the day I did back in June, it showed that the worst 5 H1s for equities all saw a big H2 rebound. However there are five long months to go before we can relax.

The key questions from the last 24 hours were 1) Did the Fed pivot on Wednesday? And 2) Is the US in a recession? Treasury markets continued to think the answer to both was yes, which boosted risk sentiment by further capping how far the market thinks the Fed can go. Meanwhile, Presidents Biden and Xi held a phone call, the markets continued to digest the Inflation Reduction Act, the US did see it’s second successive quarter of negative growth, German CPI beat expectations and Amazon and Apple impressed the market with earnings after the bell.

The main macro driver continued to be the interpretation of the July FOMC. Specifically, that the Chair said at some point in the future it may be appropriate to slow the pace of tightening and that he and the Committee paid heed to slowing activity data (more below). The current interpretation being that factors other than inflation were seeping into the Fed’s reaction function. Global yields rallied hard yesterday. 2yr yields were -13.6bps lower at 2.86% while 10yr Treasuries were -10.9bps lower at 2.68%, their lowest since early April. Notably, real yields drove the decline, falling -13.1bps (-26.2bps lower over the last two days, their largest two-day decline since the invasion in early March), suggesting easier expected policy without an impact on inflation, with breakevens up a modest +2.1bps. This is a market believing the Fed will be forced into a pivot, and that slowing activity figures will soon translate into lower inflation. This morning in Asia, yields on 10yr USTs (-1.80 bps) are extending their decline, trading at 2.66% as I type.

Europe outpaced the US with 2yr bunds -18.7bps lower at 0.22%, their lowest since mid-May. 10yr bunds were -11.8bps lower and OATs fell -13.4bps. 10yr BTPs outperformed on the perceived shift in policy tone, down -14.9bps.

Regular readers will know we are skeptical things will work out as the market is increasingly pricing in. Real policy rates remain deeply in negative territory despite the Fed believing they are at neutral. Furthermore, policy works on long and variable lags, not only is 5 months (the amount of time until the market is pricing cuts) a very short amount of time for today’s tightening to bring inflation back from 9%, but the very reaction we’re witnessing in markets means financial conditions have actually eased since the June FOMC meeting. So the Fed has instituted back-to-back 75bp hikes and financial conditions haven’t gotten any tighter. DB research has been putting out a number of pieces addressing this of late. Matt Luzzetti and Peter Hooper put out a piece yesterday showing that the Fed is historically more cautious about cutting rates when core PCE is above 4% (see here), while Tim Wessel on my team showed that markets overestimate how large those cuts will be ahead of time when inflation is that high (see here). However, one needs to be wary of summer seasonals, where August is usually the strongest month of the year, when deciding whether to fight the move now or wait until September.

Adding to the yield rally justification, advanced US GDP came in at -0.9% in 2Q, that is in negative territory for a second straight quarter. This has driven much hand-wringing about whether or not the US is currently in a recession. We won’t know for a while if the NBER officially calls this a recession, as the growth data will undergo plenty of revisions before we have a final number. Further, the NBER actually doesn’t use GDP as one of their indicators for defining recessions, funnily enough, instead amalgamating personal income, payrolls, real PCE, retail sales, household survey employment, and industrial production (which eventually wind up looking a whole lot like GDP). Some of those underlying figures still look quite strong even if the headline GDP figure is not. In the end, whether or not the NBER decides in the future that we are in recession today is almost beside the point: markets will continue to trade based on their perception of the Fed’s responsiveness to slowing activity weighed against runaway inflation.

On that note, the overwhelming perception over the last two days is that slowing activity, will become increasingly more important for policy going forward. This drove risk assets higher for a second straight day across the Atlantic. The S&P 500 increased +1.21% with all but one sector higher, while the NASDAQ was up +1.08%, bringing them +11.06% and +14.24% higher since terminal rates first fell from above 4% in mid-June. In Europe, the STOXX 600 climbed +1.09%, while the DAX and CAC increased +0.88% and +1.30%, respectively.

On the earnings front, Mastercard said that card spending and use of its payments infrastructure have picked up in a big way amidst runaway inflation, pushing the company’s revenue forecast for the year higher. Hard to see how inflation slows if consumers are spending like that.

After the close Apple and Amazon reported earnings on the stronger side of what we’ve seen for mega-caps so far, with both releases containing optimism around supply chains and consumer spending. Apple’s revenues and earnings figures beat street estimates, despite supply chain disruptions from China covid lockdowns, on the back of stronger-than-expected iPhone and iPad sales, with shares rising around +3% after hours. Amazon shares rose more than +12% in after hours trading after beating revenue estimates and revising forecasts higher. While hiring appears to be slowing, Amazon also looks to be unwinding storage capacity, again another sign that supply chain pressures may be easing, while cutting costs.

We got more international data on the great slower activity versus high inflation dichotomy, with German CPI increasing +0.9% MoM versus expectations of +0.6%, bringing YoY to +7.5% versus +7.4% expectations. The EU harmonised measures also beat expectations, climbing +0.8% MoM versus +0.4% expectations while YoY ticked up to +8.5% versus +8.1% expectations.

Asian equity markets are mixed this morning with the Hang Seng (-2.19%) sharply lower and with the Shanghai Composite (-0.71%) and CSI (-1.02%) also slipping on rising expectations of China’s economic growth outlook remaining subdued in H2 after yesterday’s high-level Communist Party meeting omitted its full-year GDP growth target and will instead strive to achieve the best results for the economy this year. Elsewhere, the Nikkei (+0.46%) and the Kospi (+0.43%) are trading in positive territory and more matching western markets.

Talking of which, stock futures in the US are pointing to a strong start with contracts on the S&P 500 (+0.57%) and NASDAQ 100 (+1.21%) both higher on the positive earnings from Amazon and Apple.

Early morning data showed that Japan’s industrial output jumped +8.9% m/m in June (v/s +4.2% expected) posting the biggest one-month gain in nine years as disruptions due to China’s COVID-19 curbs eased. It followed a -7.5% drop last month. But retail sales (-1.4% m/m) unexpectedly contracted in June (v/s +0.2% expected) after an upwardly revised +0.7% increase in May. Separately, July Tokyo CPI advanced to +2.5% y/y in July (v/s +2.4% expected, +2.3% in June) on the back of a hike in utility prices. Meanwhile, labour market conditions in the nation remained relatively healthy as the jobless rate stayed at 2.6% in June (v/s 2.5% market consensus) albeit the job-to-applicants ratio improved to 1.27 in June (v/s 1.25 expected) from 1.24 in May.

Elsewhere, Presidents Biden and Xi had a two-hour phone call. The call covered foreign policy issues surrounding Taiwan and Ukraine. The two leaders reportedly covered areas of mutual cooperation, as well, including using their economic might to prevent a global recession and tasking aides to follow up on climate and healthy security issues. Aides have been tasked with setting up a face to face meeting which seems an impressive development even with the tensions there obviously are between the two sides.

To the day ahead, data includes the employment cost index, PCE, income, and spending data in the US, Tokyo CPI, consumer confidence, jobless rate, retail sales, industrial production, and starts in Japan, CPI and GDP in France, GDP in Germany, and GDP in Canada. It’s another full slate of earnings which will include Sony, Exxon, Procter & Gamble, Chevron, AbbVie, AstraZeneca, Colgate-Palmolive, BNP Paribas, Eni, Intesa Sanpaolo, LyondellBasell, Engie, BBVA, NatWest, and Citrix.

END

AND NOW NEWSQUAWK

NQ continues to outperform post AAPL & AMZN, while JPY dictates FX – Newsquawk US Market Open

FRIDAY, JUL 29, 2022 – 06:49 AM

- European bourses are firmer across the board, Euro Stoxx 50 +0.9%, and are set to post their best monthly performance since Nov’20.

- NQ continues to outperform, +1.2%, amid after-market earnings from AMZN and AAPL

- DXY attempts to recoup from JPY-induced pressure after USD/JPY dropped to 132.50; EUR fades despite hot-CPI and strong GDP data

- Crude is bid while TTF relinquishes EUR 200 mark; Saudi-Russia talks and Lavrov looking into a call with US’ Blinken

- Marked pull-back in core debt but still notably bid for the week as a whole with a busy afternoon docket ahead

- US President Biden and China’s President Xi discussed face-to-face meeting and directed teams to follow up; did not discuss any potential lifting of US tariffs on Chinese products.

- Looking ahead, highlights include US Jun PCE, US Chicago PMI, and Canadian GDP. Earnings from Exxon Mobil, Phillips 66, AbbVie, and more.

For the full report and more content like this check out Newsquawk

Try a 14 day trial with Newsquawk and hear breaking trading news as it happens.

As of 11:20BST/06:20ET

LOOKING AHEAD

- US Jun PCE, US Chicago PMI, Canadian GDP.

- Earnings from Exxon Mobil, Phillips 66, AbbVie, and more.

- Click here for the Week Ahead preview

GEOPOLITICS

BIDEN-XI CALL

- Senior US admin official said US President Biden and China’s President Xi discussed face-to-face meeting and directed teams to follow up; did not discuss any potential lifting of US tariffs on Chinese products.

- White House said presidents Biden and Xi discussed a range of issues important to bilateral relationship and other regional/global issues.

- Senior US admin official said Biden and Xi had a ‘direct and honest’ discussion on Taiwan. They discussed areas of cooperation including climate change, health security and counter-narcotics. Biden brought up the long-standing concerns on human rights. Macroeconomic coordination between China and US is of great importance. Biden explained to Xi his core concerns about China’s economic practices.

- China President Xi told US President Biden that the US should abide by the One China principle, and act in line with its words, according to State Media. On the Taiwan issue, Xi told Biden that ‘those who play with fire will get burned’. Xi told Biden that China fiercely opposes Taiwan independence and the interference of external forces

- US President Biden told China President Xi that the US stance on One China policy remains unchanged, according to China’s Global Times.

RUSSIA-UKRAINE

- Russian Kremlin, when asked on the West pushing Ukraine to negotiate says it does not see the possibility for talks.

- Russian Foreign Minister Lavrov says will soon propose a date for a call with US Secretary of State Blinken; interested in Blinken’s proposals regarding the export of Russian grain.

- US State Department said Russia has acknowledged the request for Blinken-Lavrov call but said there is no update on when they will speak, and added the US continues to expect that Blinken-Lavrov will have an opportunity to speak in the coming days.

- Russia is reportedly transferring USDs to Turkey for a USD 20bln nuclear facility, according to Bloomberg.

EUROPEAN TRADE

CENTRAL BANKS