by harveyorgan · in Uncategorized · Leave a comment·Edit

in Uncategorized · Leave a comment·Edit

GOLD; $1773.70 UP $3.70

SILVER: $20.17 DOWN 21 CENTS

ACCESS MARKET:

GOLD $1761.45

SILVER: $20.00

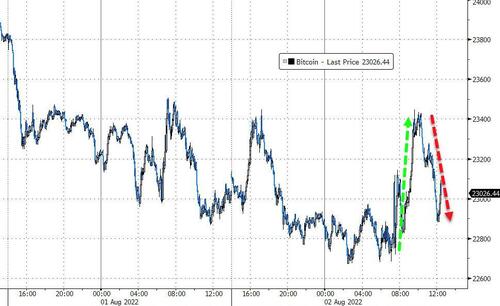

Bitcoin morning price: $22,886 DOWN 103

Bitcoin: afternoon price: $23,040. UP 51

Platinum price: closing UP $4.05 to $911.30

Palladium price; closing DOWN $122.05 at $2074.70

END

I am going to take a one day break. So I will not be doing a commentary tomorrow Wednesday, August 3

I will resume on Thursday. However I will record all comex data and this will be up to date by Thursday.

Harvey

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: AUGUST 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,769.000000000 USD

INTENT DATE: 08/01/2022 DELIVERY DATE: 08/03/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 521 169

072 H GOLDMAN 444

104 C MIZUHO 500 133

118 C MACQUARIE FUT 57

132 C SG AMERICAS 4 71

167 C MAREX 111

190 H BMO CAPITAL 109

357 C WEDBUSH 2

624 C BOFA SECURITIES 438

624 H BOFA SECURITIES 437

661 C JP MORGAN 1873 1229

661 H JP MORGAN 24

685 C RJ OBRIEN 20 3

686 C STONEX FINANCIA 1 9

686 H STONEX FINANCIA 16

690 C ABN AMRO 30 41

732 C RBC CAP MARKETS 3

800 C MAREX SPEC 31 33

880 C CITIGROUP 95

880 H CITIGROUP 397

905 C ADM 39

TOTAL: 3,420 3,420

MONTH TO DATE: 25,355

JPMorgan stopped 1229/3420

_____________________________________________________________________________________

GOLD: NUMBER OF NOTICES FILED FOR AUGUST CONTRACT:

5,101 NOTICES FOR 3420 OZ //10.6326 TONNES

total notices so far: 25,355 contracts for 2,535,500 oz (78.864 tonnes)

SILVER NOTICES:

28 NOTICES FILED FOR 140,000 OZ/

total number of notices filed so far this month 707 : for 3,535,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $3.70

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES OF GOLD FROM THE GLD

INVENTORY RESTS AT 1002.97 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 21 CENTS

AT THE SLV// ://HUGE CHANGES IN SILVER INVENTORY AT THE SLV//:A WITHDRAWAL OF 3.504 MILLION OZ FROM THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 487.161 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 3611 CONTRACTS TO 135,312 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE HUGE LOSS IN OI WAS ACCOMPLISHED DESPITE OUR STRONG $0.17 GAIN IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.17) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY COMMERCIAL SILVER LONGS// WE HAD HUGE SPECULATOR LIQUIDATIONS AS WE HAD A HUGE LOSS OF 2811 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT LIQUIDATIONS//HUGE BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A FAIR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 165,000 OZ QUEUE JUMP / // V) GIGANTIC SIZED COMEX OI LOSS/(SPEC LIQUIDATION)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -10

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTACTS for 2 days, total 2050 contracts: 10.250 million oz OR 5.125 MILLION OZ PER DAY. (1025 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 10.250 MILLION OZ

.

LAST 16 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 10.250 MILLION OZ

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3621 DESPITE OUR $0.17 GAIN IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 800 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER ADDITIONS ////// HUGE SPECULATOR SHORT LIQUIDATION// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 165,000 OZ QUEUE JUMP // .. WE HAD A HUGE SIZED LOSS OF 2821 OI CONTRACTS ON THE TWO EXCHANGES FOR 14.105 MILLION OZ AS..THE SPECS WERE SENT TO THE SLAUGHTER HOUSE.

WE HAD 28 NOTICES FILED TODAY FOR 140,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GOOD SIZED 4068 CONTRACTS TO 462,770 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -37 CONTRACTS.

.

THE GOOD SIZED DECREASE IN COMEX OI CAME DESPITE OUR RISE IN PRICE OF $5.75//COMEX GOLD TRADING/MONDAY / WE MUST HAVE HAD ADDITIONAL SPECULATOR SHORT SHORT COVERINGS ACCOMPANYING OUR SMALL SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND HUGE SPECULATOR SHORT COVERINGS//HUGE ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR AUGUST AT 97.291 TONNES ON FIRST DAY NOTICE

YET ALL OF..THIS HAPPENED WITH OUR RISE IN PRICE OF $5.75 WITH RESPECT TO FRIDAY’S TRADING

WE HAD A FAIR SIZED LOSS OF 3164 OI CONTRACTS 9.841 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 904 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 462,770

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3,164 CONTRACTS WITH 4,068 CONTRACTS DECREASED AT THE COMEX AND 904 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 3127 CONTRACTS OR 9.726 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (904) ACCOMPANYING THE GOOD SIZED LOSS IN COMEX OI (4068): TOTAL LOSS IN THE TWO EXCHANGES 3164 CONTRACTS. WE NO DOUBT HAD 1) HUGE SPECULATOR SHORT COVERINGS//STRONG BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR AUGUST. AT 99.272 TONNES FOLLOWED BY TODAY’S EFP JUMP TO LONDON OF 1,100 oz. (THESE OZ WILL EVENTUALLY FIND THEIR WAY BACK TO THE COMEX AS BANKERS SCOUR THE PLANET FOR BADLY NEEDED GOLD!! 3) ZERO LONG LIQUIDATION//// //.,4) GOOD SIZED COMEX OPEN INTEREST LOSS 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST :

2265 CONTRACTS OR 226,500 OZ OR 7,045 TONNES 2 TRADING DAY(S) AND THUS AVERAGING: 1133 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAY(S) IN TONNES: 7.045 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 7.045/3550 x 100% TONNES 0.197% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 7.045 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF SEPT., FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A GIGANTIC SIZED 3621 CONTRACT OI TO 135,312 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1250 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 800 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 800 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 3621 CONTRACTS AND ADD TO THE 800 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED LOSS OF 2821 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 14.105 MILLION OZ

OCCURRED DESPITE OUR RISE IN PRICE OF $0.17

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED DOWN 73.69 PTS OR 2.26% //Hang Sang CLOSED DOWN 476.63 OR 2.26% /The Nikkei closed DOWN 398.67 OR % 1.72. //Australia’s all ordinaires CLOSED UP 0.05% /Chinese yuan (ONSHORE) closed DOWN AT 67586//OFFSHORE CHINESE YUAN DOWN 6.7707// /Oil DOWN TO 94.19 dollars per barrel for WTI and BRENT AT 100.68// SHANGHAI CLOSED DOWN 73.69 PTS OR 2.26% //Hang Sang CLOSED DOWN 476.63 OR 2.36% /The Nikkei closed DOWN 398.67 OR % 1.72. //Australia’s all ordinaries CLOSED UP 0.05% / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 4068 CONTRACTS TO 462,770 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS GOOD COMEX DECREASE OCCURRED DESPITE OUR RISE OF $5.75 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A SMALL SIZED EFP (904 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF AUGUST.. THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 904 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :904 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 904 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED SIZED TOTAL OF 3164 CONTRACTS IN THAT 904 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED COMEX OI LOSS OF 4068 CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR STRONG SIZED GAIN IN PRICE OF GOLD $ 5.75. . WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS IS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING AUGUST (97.287),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:97.287 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $5.75) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS // COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO COVER TO THEIR POSITIONS////// WE HAVE REGISTERED A FAIR SIZED LOSS OF 9,726 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR AUGUST (97.287 TONNES)…

WE HAD -37 CONTRACTS SUBTRACTED TO COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 3164 CONTRACTS OR 316,400 OZ OR 9.841 TONNES

Estimated gold volume 170,848/// poor/

final gold volumes/yesterday 144,999 / poor

INITIAL STANDINGS FOR AUGUST ’22 COMEX GOLD //AUGUST 2

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 194,418.105oz JPMorgan Loomis 1600 kilobars (HSBC) |

| Deposit to the Dealer Inventory in oz | 1999.94 OZ Delaware |

| Deposits to the Customer Inventory, in oz | 384.485 oz Brinks |

| No of oz served (contracts) today | 3420 notice(s) 342,000 OZ 10.6322 TONNES |

| No of oz to be served (notices) | 5923 contracts 592,300 oz 18.241 TONNES |

| Total monthly oz gold served (contracts) so far this month | 25,355 notices 2,535,500 OZ 78.864TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 1

i) Into the dealer Delaware: 1.999.94 oz

total dealer deposit: 1999.94 oz

No dealer withdrawals

Customer deposits: 0

total deposits: 0 oz

2 customer withdrawals:

i) out of Loomis: 34,464.872oz

ii) out of JPMorgan: 159,953.233 oz

total withdrawal: 194,418.105 oz (6.04 tonnes)

Adjustments: customer to dealer: JPMorgan 139,877.158 oz

customer to dealer Brinks: 93,077.145 oz

and: Manfra: 64,678.933 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 9343 contracts having LOST 511 contracts .

We had 5101 notices served upon yesterday so we lost a very tiny 10 contracts (1000 oz) as these guys were EFP’d to London where they will turn around and

take gold from the Comex at T + 2.

Sept. gained 77 contracts to 3974 contracts.

October gained 539 contracts up to 39,533

We had 3420 notice(s) filed today for 342,000 oz FOR THE AUGUST 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 1873 notices were issued from their client or customer account. The total of all issuance by all participants equate to 3420 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 1229 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2022. contract month,

we take the total number of notices filed so far for the month (25,355) x 100 oz , to which we add the difference between the open interest for the front month of (AUGUST 9343 CONTRACTS ) minus the number of notices served upon today 3420 x 100 oz per contract equals 3,127,800 OZ OR 97.287 TONNES the number of TONNES standing in this active month of AUGUST.

thus the INITIAL standings for gold for the AUGUST contract month:

No of notices filed so far (25,355) x 100 oz+ (9343) OI for the front month minus the number of notices served upon today (3420} x 100 oz} which equals 3,127,800 oz standing OR 97.287 TONNES in this active delivery month of August.

TOTAL COMEX GOLD STANDING: 97.287 TONNES (A HUGE STANDING FOR AUGUST ( ACTIVE) DELIVERY MONTH)

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,320,459.814oz 72,17 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 30,049,842.972 OZ

TOTAL REGISTERED GOLD: 15,248,246.109 OZ (474.77 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 14,801,595.863 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 12,927,789.0 OZ (REG GOLD- PLEDGED GOLD) 402.1 tonnes

END

SILVER/COMEX/AUGUST 2

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,307,609.966 oz CNT HSBC Loomis Manfra |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 83,064.300 oz CNT |

| No of oz served today (contracts) | 28 CONTRACT(S) 140,000 OZ) |

| No of oz to be served (notices) | 105 contracts (525,000 oz) |

| Total monthly oz silver served (contracts) | 707 contracts 3,535,500 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have1 deposits into the customer account

i) Into CNT: 83,064.300 oz

total deposit: 83,064.300 oz

JPMorgan has a total silver weight: 175.113 million oz/335.549 million =52.20% of comex

Comex withdrawals: 4

i) Out of HSBC 601,294.800 oz

ii) out of CNT: 137,276.591 0z

iii0 Out of Loomis: 64,372.750 oz

iv) Out of Manfra: 504,665.825 oz

total: 1,307,609.966 oz

adjustments: 1// customer to dealer

Manfra 62,272.264 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 55.525 MILLION OZ

TOTAL REG + ELIG. 335.549 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR AUGUST

silver open interest data:

FRONT MONTH OF AUGUST OI: 133 CONTRACTS HAVING GAINED 23 CONTRACTS. WE HAD 10 NOTICES FILED ON MONDAY

SO WE GAINED 33 CONTRACTS OR AN ADDITIONAL 165,000 OZ OF SILVER WILL STAND FOR DELIVERY. THE AMOUNT STANDING

WILL NOW INCREASE ON A DAILY BASIS AS BANKERS SCOUR THE PLANET FOR BADLY NEEDED SILVER.

SEPTEMBER HAD A LOSS OF 5347 CONTRACTS DOWN TO 99,811

CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 28 for 140,000 oz

Comex volumes:69,159// est. volume today// good

Comex volume: confirmed yesterday: 64,327 contracts ( good )

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 707 x 5,000 oz = 3,535,500 oz

to which we add the difference between the open interest for the front month of AUGUST(133) and the number of notices served upon today 28 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST./2022 contract month: 707 (notices served so far) x 5000 oz + OI for front month of AUGUST (133) – number of notices served upon today (28) x 5000 oz of silver standing for the AUGUST contract month equates 4.060,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

AUGUST 2/WITH GOLD UP $3.70; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD//INVENTORY RESTS AT 1002.97 TONNES//

AUGUST 1/WITH GOLD UP $5.75: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 29//WITH GOLD UP $12.50; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1005.29 TONNES

JULY 28/WITH GOLD UP $31.25; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 27.//WITH GOLD UP $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 26/WITH GOLD DOWN $1.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.29 TONNES

JULY 25/WITH GOLD DOWN $7.85: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 1005.87 TONNES

JULY 22/WITH GOLD UP $17.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 21/WITH GOLD UP $11.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.101 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.87 TONNES

JULY 20/WITH GOLD DOWN $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1009.06 TONNES

JULY 19/WITH GOLD DOWN $.35 :BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.22 TONNES FROM THE GLD//INVENTORY RESTS AT 1009.06 TONNES

JULY 18/WITH GOLD UP $7.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.28 TONNES

JULY 15/WITH GOLD DOWN $3.75:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD///INVENTORY RESTS AT 1016.89 TONNES//

JULY 14/WITH GOLD DOWN $28.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD//INVENTORY RESTS AT 1019.79 TONNES

JULY 13/WITH GOLD UP $10.55:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD//INVENTORY RESTS AT 1021.53TONNES

JULY 12/WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESS AT 1023.27 TONNES

JULY 11/WITH GOLD DOWN $4.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD./INVENTORY RESTS AT 1023.27 TONNES

JULY 7/WITH GOLD UP $1.35: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.61 TONNES FORM THE GLD///INVENTORY REST AT 1024.43 TONNES

JULY 6/WITH GOLD DOWN $26.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 9.86 TONNES FROM THE GLD//INVENTORY REST AT 1032.04 TONNES

JULY 5/WITH GOLD DOWN $36.55//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.41 TONNES FROM THE GLD///INVENTORY RESTS AT 1041.90 TONNES

JULY 1/WITH GOLD DOWN $5.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES//INVENTORY RESTS AT 1050.31 TONNES

JUNE 30/WITH GOLD DOWN $9.20: big CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 1052.63 TONNES//

JUNE 28/WITH GOLD DOWN $3.05//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.64 TONNES FROM THE GLD///INVENTORY RESTS AT 1056.40 TONNES

JUNE 27/WITH GOLD DOWN $4.90 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.04 TONNES

JUNE 24/WITH GOLD UP 45 CENTS TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.70 TONNES FROM THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 23/WITH GOLD DOWN $8.60:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//INVENTORY RESTS AT 1071.77 TONNES

JUNE 22/WITH GOLD UP 15 CENTS:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1073.80 TONNES

GLD INVENTORY: 1002.97 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 2/WITH SILVER DOWN 21 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.504 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.161 MILLION OZ//

AUGUST 1/WITH SILVER UP 17 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE GLD: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 483.657 MILLION OZ//

JULY 29/WITH SILVER UP 30 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 461,000 OZ FROM THE SLV..//INVENTORY RESTS AT 483.657 MILLION OZ/

JULY 28/WITH SILVER UP $1.24 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 484.118 MILLION OZ/

JULY 27/.WITH SILVER UP 4 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL 11.479 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 484.118MILLION OZ//

JULY 26/WITH SILVER UP 16 CENTS: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.504 MILLION OZ FROM THE SLV//: //INVENTORY RESTS AT 495.597 MILLION OZ//

JULY 25/WITH SILVER DOWN 24 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.383 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 499.101 MILLION OZ//

JULY 22/WITH SILVER DOWN 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 500.484 MILLION OZ//

JULY 21/WITH SILVER UP 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.19 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 500.484MILLION OZ/

JULY 20/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 8.253 MILLION OZ FORM THE SLV/INVENTORY RESTS AT 507.585 MILLION OZ//

JULY 19/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ//

JULY 18/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 4.995 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ.

JULY 15/WITH SILVER UP 31 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 3.226 MILLION OZ FORM THE SLV//INVENTORY RESTS AT 510.443 MILLIONOZ//

JULY 14/WITH SILVER DOWN 88 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 OZ FROM THE SLV// //INVENTORY RESTS AT 513.671 MILLION OZ

JULY 13/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SV//INVENTORY RESTS AT 514.501 MILLION OZ.

JULY 12/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.228 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 514.501 MILLION OZ//

JULY 11/WITH SILVER DOWN 17 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 5.533 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 517.729 MILLION OZ

JULY 7/WITH SILVER UP 3 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.889 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 523.262 MILLION OZ/

JULY 6/WITH SILVER UP ONE CENT: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 12.558 MILLION OZ FORM THE SLV///INVENTORY RESTS AT 528.151 MILLION OZ

JULY 5/WITH SILVER DOWN 55 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 540.709MILLION OZ//

JULY 1/WITH SILVER DOWN 61 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ//INVENTORY RESTS AT 540.709 MILLION OZ//

JUNE 30/WITH SILVER DOWN 41 CENTS : SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 738,000 OZ FROM THE SLV//INVENTORY RESTS AT 541.262 MILLION OZ//

JUNE 28/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.00 MILLION OZ..

JUNE 27/WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 24/WITH SILVER UP 10 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.137 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 23/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 2.029 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 545.137 MILLION OZ//

JUNE 22/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.166 MILLION OZ.

CLOSING INVENTORY 487.161 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: The ‘Inflation Reduction Act’ Will Do The Exact Opposite

TUESDAY, AUG 02, 2022 – 01:20 PM

Congress passed a bill to prop up the US semiconductor industry last week and is now considering a new spending plan dubbed the “Inflation Reduction Act.” On his podcast, Peter Schiff talked about the Democrats’ legislative agenda and concluded that the “Inflation Reduction Act” will do the exact opposite.

Last Thursday, the House passed the Chips Act, a law that will subsidize the domestic computer chip industry by handing out roughly $52 billion in government subsidies for the US production of semiconductors. Peter called the bill “completely unconstitutional.”

There is nothing in the US Constitution that authorized the US government to pick winners and losers, and to decide to invest taxpayer money in particular businesses and hand over that money to industries like the computer chip industry.”

Politicians call this kind of handout “an investment.” Peter said he doesn’t see how you can call it that.

There’s no return to the taxpayer. It’s simply a grant. The US government is giving $50 billion to private companies.”

It’s really just another example of government central planning. And it never works. As Peter said, capital needs to be allocated in the private sector.

If computer chips are viable, which of course they are, and if they’re necessary, then there will be a profit associated with producing those chips. And because private investors are incentivized by profits to make investments, there will be private sector investment in this industry if that is, in fact, what the country needs. And so the government needs to stay out of it. This is not an example of capitalism. This is an example of socialism. And this is going to fail.”

And of course, the federal government doesn’t have $50 billion.

It is going to have to borrow it. It is going to have to run larger deficits. How are these deficits going to be financed? Well, they’re likely going to be financed by the Fed through the printing of money. Even though the Fed is still claiming it is going to shrink its balance sheet, it’s going to end up expanding its balance sheet. But even if the Fed doesn’t finance the deficits, they have to be financed somehow, which means other private sector investment is going to get crowded out to make this government investment possible.”

If the government is crowding out other private investments, it should be clear that this government program is not the best use for that money. The highest and best use would be a function of the free market.

So, if the free market doesn’t want to do something, but politicians want to force it to happen anyway, it’s because it’s not the best use of the capital.”

At a time the government should be cutting spending to reduce deficits and help fight raging inflation, it is doing the exact opposite.

Peter Schiff called the “Inflation Reduction Act” the most ironic of all. He also noted that there should be a law requiring “truth in legislating.”

Whenever they title a bill something, the opposite is achieved. For example, if they pass the ‘Tax Simplification Act,’ it means taxes are going to get a lot more complicated. They passed the ‘Patriot Act.’ It was probably one of the most unpatriotic pieces of legislation ever passed. The same will hold true for the ‘Inflation Reduction Act.’ The Inflation Reduction Act will increase inflation.”

Why?

Because the bill doesn’t do anything except spend more money.

The only act that the government could pass to reduce inflation would be to reduce government spending. They need to cut government spending. That is not what this act is doing.”

The proposed spending bill does include tax increases on corporations and closes some other tax “loopholes.” But even if the tax hikes lowered deficits – which they won’t – taxes on corporations limit supply, not demand.

They result in less capital investment and reduce the supply of goods or services available to buy. That puts more upward pressure on prices. The only way that the government can fight inflation with tax hikes is if those tax hikes are targeted on the middle class. Because the tax hikes have to reduce demand, not supply. The way you reduce demand is you increase taxes on the people who would have spent the money on consumer goods and services.”

When you tax the rich, it doesn’t tend to significantly alter their spending. It reduces their saving and investing.

Peter said anybody who says the “Inflation Reduction Act” will reduce inflation because it will reduce the budget deficit is wrong.

These tax hikes will have no effect on inflation other than to make it worse because they will limit supply.”

Peter said he isn’t advocating tax hikes on the middle class. He would prefer the government to fight inflation by cutting spending.

But that’s not on the table. The only thing that the Democrats have put on the table is tax hikes. And I’m pointing out that the only tax hikes that will work in reducing inflation would be tax hikes on the middle class and the poor. But again, the best way to tackle inflation is through spending cuts.”

In this podcast, Peter also talked about the current recession that the government and Fed deny is upon us, the weak labor market, and the market reaction to the GDP news.

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

3.Chris Powell of GATA provides to us very important physical commentaries

Gold investors are in a bind over Russian bars held in Europe

(Reuters)

Gold investors are in a bind over bars from tarnished Russia

Submitted by admin on Mon, 2022-08-01 10:05Section: Daily Dispatches

By Peter Hobson

Reuters

Monday, August 1, 2022

LONDON — Some investors want Russian gold off their books but it’s not that easy to remove.

A de-facto ban on Russian bullion minted after Moscow’s invasion of Ukraine — instigated by the London market in early March — does not apply to hundreds of tonnes of gold that have been sitting in commercial vaults since before the conflict started.

Fund managers looking to sell the metal to avoid the deepening reputational risk of holding assets linked to Russia in their portfolios could trigger a costly scramble to replace it with non-Russian gold, according to bankers and investors.

“This would serve only to damage investors. It doesn’t damage the (Russian) regime,” said Christopher Mellor at Invesco, whose fund has around 265 tonnes of gold, 35 tonnes of it produced in Russia with a market value of around $2 billion.

The dilemma facing investors reflects Russia’s heft in the global bullion trade and its hub, the London market, where gold worth around $50 billion changes hands daily in private deals. …

… For the remainder of the report:

END

Zimbabwe has success in selling gold coins and this prompts a second offering

(Bloomberg/GATA)

Success of first Zimbabwe gold coin sale prompts second offering

Submitted by admin on Mon, 2022-08-01 11:24Section: Daily Dispatches

By Ray Ndlovu

Bloomberg News

Monday, August 1, 2022

Zimbabwe’s central bank will offer 2,000 more gold coins to the public, a week after an initial sale saw “favorable uptake.”

The bank sold 1,500 gold coins during the first week of their release into the market, Governor John Mangudya said today in an emailed statement. They are sold in local and foreign currencies by banks and approved dealers in the country.

The authorities introduced the so-called Mosi-oa-Tunya coins last month to ease demand for U.S. dollars as a store of value, after a collapse of the Zimbabwe dollar. It has lost more than two-thirds of its value against the greenback this year, spawning annual inflation of 257% in July. …

… For the remainder of the report:

end

4. OTHER GOLD/SILVER COMMENTARIES

end

end

5.OTHER COMMODITIES: WHEAT//GRAINS/DIESEL

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

end

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7586

OFFSHORE YUAN: 6.7707

HANG SENG CLOSED DOWN 476.63 PTS OR 2.36%

2. Nikkei closed DOWN 398.67 OR 1.72%

3. Europe stocks CLOSED ALL RED

USA dollar INDEX UP TO 105,43/Euro FALLS TO 1.0234

3b Japan 10 YR bond yield: FALLS TO. +.169/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 131.03/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN -// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +0.819%/Italian 10 Yr bond yield RISES to 3.05% /SPAIN 10 YR BOND YIELD FALLS TO 1.89%…

3i Greek 10 year bond yield FALLS TO 2.880//

3j Gold at $1778.95 silver at: 20.44 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 13/100 roubles/dollar; ROUBLE AT 60.30

3m oil into the 94 dollar handle for WTI and 100 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 131.03DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9522– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9743well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.559 DOWN 5 BASIS PTS

USA 30 YR BOND YIELD: 2.887 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.96

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

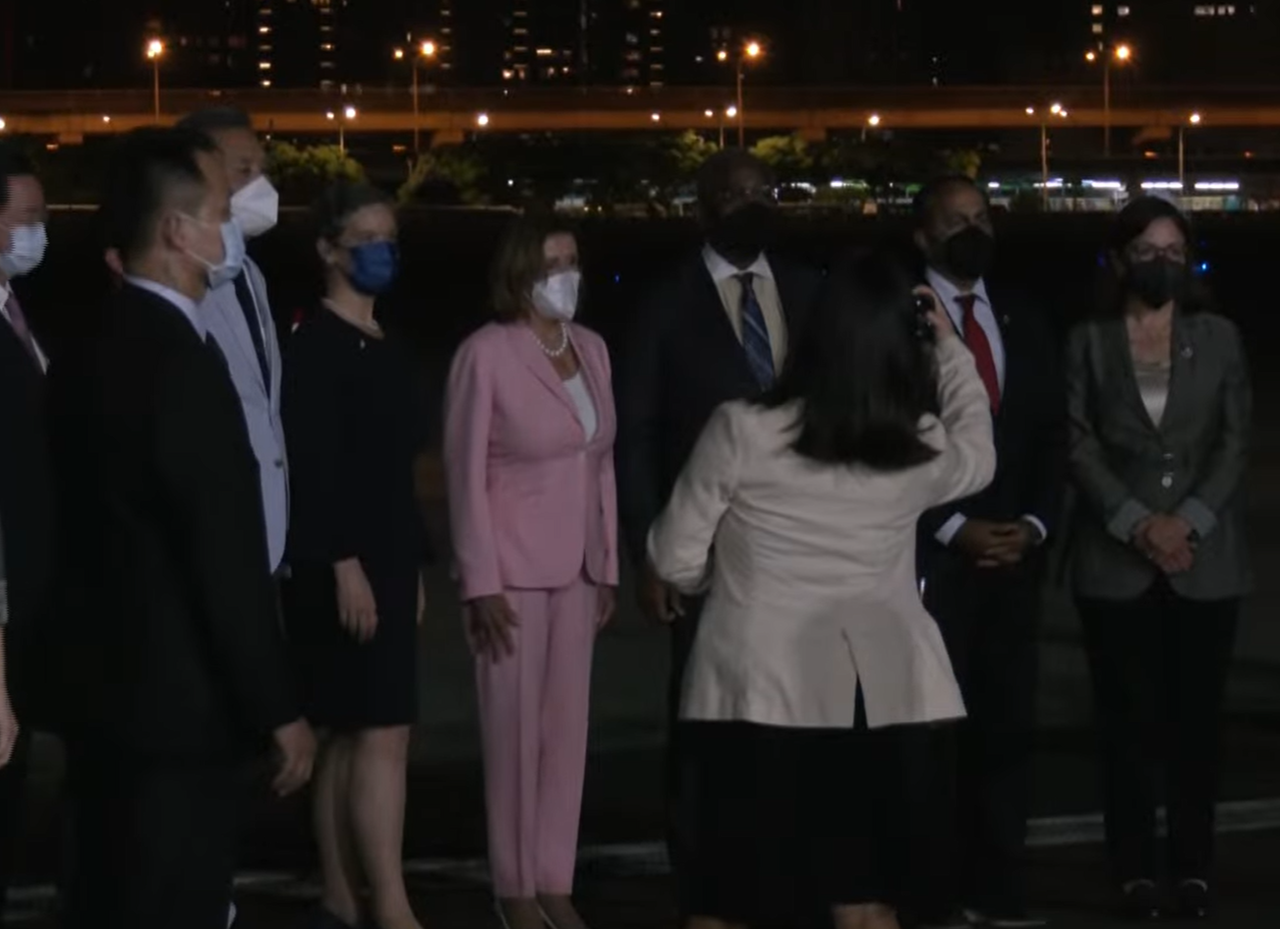

Global Markets Slump With Terrified Traders Tracking Pelosi’s Next Move

TUESDAY, AUG 02, 2022 – 08:05 AM

Forget inflation, stagflation, recession, depression, earnings, Biden locked up in the basement with covid, and everything else: today’s it all about whether Nancy Pelosi will start World War 3 when she lands in Taiwan in 3 hours.

US stocks were set for a second day of declines as investors hunkered down over the imminent (military) response by China to Pelosi’s Taiwan planned visit to Taiwan, along with the risks from weakening economic growth amid hawkish central bank policy. Nasdaq 100 contracts were down 0.7% by 7:30a.m. in New York, while S&P 500 futures fell 0.6% having fallen as much as 1% earlier. 10Y yields are down to 2.55% after hitting 2.51% earlier, while both the dollar and gold are higher.

Elsewhere around the world, Europe’s Stoxx 600 fell 0.6%, with energy among the few industries bucking the trend after BP hiked its dividend and accelerated share buybacks to the fastest pace yet after profits surged. Asian stocks slid the most in three weeks, with some of the steepest falls in Hong Kong, China and Taiwan.

Among notable movers in premarket trading, Pinterest shares jumped 19% after the social-media company reported second-quarter sales and user figures that beat analysts’ estimates, and activist investor Elliott Investment Management confirmed a major stake in the company. US-listed Chinese stocks were on track to fall for a fourth day, which would mark the group’s longest streak of losses since late-June, amid the rising geopolitical tensions. In premarket trading, bank stocks are lower amid rising tensions between the US and China. S&P 500 futures are also lower, falling as much as 0.9%, while the 10-year Treasury yield falls to 2.56%. Cowen Inc. shares gained as much as 7.5% after Toronto-Dominion Bank agreed to buy the US brokerage for $1.3 billion in cash. Meanwhile, KKR’s distributable earnings fell 9% during the second quarter as the alternative-asset manager saw fewer deal exits amid tough market conditions. Here are some other notable premarket movers:

- Activision Blizzard (ATVI US Equity) falls 0.6% though analysts are positive on the company’s plans to roll out new video game titles after it reported adjusted second-quarter revenue that beat expectations. While the $68.7 billion Microsoft takeover deal remains a focus point, the company is building out a “robust” pipeline, Jefferies said.

- Arista Networks (ANET US) analysts said that the cloud networking company’s results were “impressive,” especially given supply-chain constraints, with a couple of brokers nudging their targets higher. Arista’s shares rose more than 5% in US after-hours trading on Monday after the company’s revenue guidance for the third quarter beat the average analyst estimate.

- Avis Budget (CAR US) saw a “big beat” on low Americas fleet costs and strong performance for its international segment, Morgan Stanley says. The rental-car firm’s shares rose 5.5% in US after-hours trading on Monday, after second-quarter profit and revenue beat the average analyst estimate.

- Snowflake (SNOW US) falls 5.3% after being cut at BTIG to neutral from buy, citing field checks that show a potential slowdown in product revenue growth in the coming quarters.

- Clarus Corp. (CLAR US) should continue to see “outsized demand” from the “mega-trend” of people seeking the great outdoors, Jefferies says, after the sports gear manufacturer reported second-quarter sales that beat estimates. Clarus’s shares climbed 9% in US postmarket trading on Monday.

- Cryptocurrency-exposed stocks are lower in US premarket trading as Bitcoin falls for the third consecutive session as global markets and cryptocurrencies remain pressured over deepening US-China tension. Coinbase (COIN US) falls 2.3% while Marathon Digital (MARA US) drops 3.3%.

- Transocean (RIG US) rises 18% in US premarket trading after 2Q Ebitda beat estimates, with other positives including a new contract and a 2-year extension of a revolver.

- US-listed Chinese stocks are on track to fall for a fourth day, which would mark the group’s longest streak of losses since end-of-June, amid geopolitical tensions related to House Speaker Nancy Pelosi’s expected visit to Taiwan. Alibaba (BABA) falls 2.5% and Baidu (BIDU US) dips 2.7%

- ZoomInfo Technologies analysts were positive on the software firm’s raised guidance and improved margins, with Piper Sandler saying the firm is “in a class of its own.” The shares rose more than 11% in US after-hours trading, after closing at $37.73.

Pelosi is expected to land in Taiwan on Tuesday, the highest-ranking American politician to visit the island in 25 years, a little after 10pm local time evening in defiance of Chinese threats. China, which regards Taiwan as part of its territory, has vowed an unspecified military response to a visit that risks sparking a crisis between the world’s biggest economies. “There is no way people will want to put on risk right now with this potential boiling point,” said Neil Campling, head of tech, media and telecom research at Mirabaud Securities. The potential ramifications of Pelosi’s planned visit “are huge.”

The growing tensions are the latest addition to a myriad of challenges facing equity investors going into the second half of the year. Fears of a US recession as the Federal Reserve tightens policy to tame soaring inflation have weighed on risk assets. US manufacturing activity continued to cool in July, with the data highlighting softer demand for merchandise as the economy struggles for momentum. In the off chance we avoid world war, there will be a shallow recession that could start by the end of the year, according to Rupert Thompson, chief investment officer at Kingswood Holdings. Meanwhile, the market is too optimistic about the path of monetary policy and “the risk is the Fed goes further than the markets are building in in terms of hiking,” Thompson said in an interview with Bloomberg Television.

Goldman Sachs strategists also said it was too soon for stock markets to fade the risks of a recession on expectations of a pivot in the Fed’s hawkish policy. On the other hand, JPMorgan strategists said the outlook for US equities is improving for the second half of the year on attractive valuations and as the peak in investor hawkishness has likely passed.

“Although the activity outlook remains challenging, we believe that the risk-reward for equities is looking more attractive as we move through the second half,” JPMorgan’s Marko Kolanovic wrote in a note dated Aug. 1. “The phase of bad data being interpreted as good is gaining traction, while the call of peak Federal Reserve hawkishness, peak yields and peak inflation is playing out.”

Markets are also bracing for commentary on the US interest-rate outlook from Chicago Fed President Charles Evans and St. Louis Fed President James Bullard.

In Europe, tech, financial services and travel are the worst-performing sectors. Euro Stoxx 50 falls 0.8%. FTSE 100 is flat but outperforms peers. Here are some of the biggest European movers today:

- BP shares rise as much as 4.8% on earnings. The oil major’s quarterly results look strong with an earnings beat, dividend hike and increased buyback all positives, analysts say.

- OCI rises as much as 8.6%, the most since March, on its latest earnings. Analysts say the results are ahead of expectations and the fertilizer firm’s short-term outlook remains robust.

- Maersk shares rise as much as 3.7% after the Danish shipping giant boosted its underlying Ebit forecast for the full year. Analysts note the boosted guidance is significantly above consensus estimates.

- Greggs shares rise as much as 4% after the UK bakery chain reported an increase in 1H sales. The 1H results are “solid,” while the start to 2H is “robust,” according to Goodbody.

- Delivery Hero shares gain as much as 3.8%. The stock is upgraded to overweight from neutral at JPMorgan, which said many of the negatives that have weighed on the firm are starting to turn.

- Rotork gains as much as 4%, the most since June 24, after beating analyst expectations for 1H 2022. Shore Capital says the company shows “good momentum” in the report.

- Credit Suisse shares decline as much as 6.4% after its senior debt was downgraded by Moody’s, and its credit outlook cut by S&P, while Vontobel lowered the PT following “disappointing” 2Q earnings.

- Travis Perkins shares drop as much as 11%, the most since March 2020. Citi says the builders’ merchant’s results are “slightly weaker than expected,” with RBC noting shortfalls in sales and Ebita.

- DSM shares drop by as much as 4.9% as Citi notes weak free cash flow after company reported adjusted Ebitda for the second quarter up 5.3% with FY22 guidance unchanged.

- UK homebuilders fall after house prices in the country posted their smallest increase in at least a year, indicating that the property market is starting to cool, with Crest Nichols dropping as much as 5.2%.

- Wind-turbine stocks fall in Europe after Spain’s Siemens Gamesa cut sales and margin guidance, with Siemens Energy dropping as much as 6.1%, with Vestas Wind Systems down as much as 4.7%.

Earlier in the session, Asian stocks fell as traders braced for a potential escalation of US-China tensions given a possible visit by US House Speaker Nancy Pelosi to Taiwan. The MSCI Asia Pacific Index dropped as much as 1.4%, poised for its worst day in five weeks. All sectors, barring real estate, were lower with chipmaker TSMC and China’s tech stocks among the biggest drags on the regional measure. Pelosi is expected to arrive in Taipei late on Tuesday. Beijing regards Taiwan as part of its territory and has promised “grave consequences” for her trip. Benchmarks in Hong Kong, China and Taiwan were among the laggards in Asia, slipping at least 1.4% each. Japan’s Topix declined as the yen received a boost from safe-haven demand.

“I do expect a negative feedback loop into China-related equities especially those related to the semiconductor and technology sectors as Pelosi’s potential visit to Taiwan is likely to harden the current frosty US-China tech war,” said Kelvin Wong, analyst at CMC Markets (Singapore). Pelosi’s controversial trip is souring a nascent revival in risk appetite in the region that saw the MSCI Asia gauge rise in July to cap its best month this year. China’s economic slowdown continues to weigh on sentiment, as authorities said this year’s economic growth target of “around 5.5%” should serve as a guidance rather than a hard target.

Japanese equities fell as the yen soared to a two month high over concerns of US-China tensions escalating with US House Speaker Nancy Pelosi expected to visit Taiwan on Tuesday. The Topix fell 1.8% to 1,925.49 as of the market close, while the Nikkei declined 1.4% to 27,594.73. Toyota Motor Corp. contributed the most to the Topix Index decline, decreasing 2.6%. Out of 2,170 shares in the index, 227 rose and 1,903 fell, while 40 were unchanged. Pelosi would become the highest-ranking American politician to visit Taiwan in 25 years. China views the island as its territory and has warned of consequences if the trip takes place. “The relationship between the US and China was just about to enter into a period of review, with a move from the US to reduce China tariffs,” said Ikuo Mitsui a fund manager at Aizawa Securities. That could change now as a result of Pelosi’s visit, he added

Meanwhile, Australia’s S&P/ASX 200 index erased an earlier loss of as much as 0.7% to close 0.1% higher after the Reserve Bank’s widely-expected half-percentage point lift of the cash rate to 1.85%. The index wiped out a loss of as much as 0.7% in early trade. The RBA’s statement was “not as hawkish as anticipated and the lower growth forecast suggests the RBA is aware of both the domestic and international drags on the economy,” said Kerry Craig, global market strategist at JPMorgan. “We expect the RBA will continue to push interest rates back to a neutral level this year given the successive upgrades to the inflation outlook, but 2023 looks to be a much less eventful year for the RBA,” Craig said. Banks and consumer discretionary advanced to boost the index, while miners and energy shares declined. In New Zealand, the S&P/NZX 50 index rose less than 0.1% to 11,532.46.

Indian stock indexes are on course to claw back this year’s losses on steady buying by foreigners. The S&P BSE Sensex closed little changed at 58,136.36 in Mumbai, after falling as much as 0.6% earlier in the day. The measure is now just 0.2% away from turning positive for the year. The NSE Nifty Index too is a few ticks away from moving into the green. Nine of the BSE Ltd.’s 19 sector sub-indexes advanced on Tuesday, led by power and utilities companies. Foreigners bought local shares worth $836.2 million in July, after pulling out a record $33 billion from the Indian equity market since October. July was the first month of net equity purchases by foreign institutional investors, after nine months of outflows. Still, “choppiness would remain high due to the upcoming RBI policy meet outcome and prevailing earnings season,” Ajit Mishra, vice-president for research at Religare Broking Ltd. wrote in a note. “Participants should continue with the buy-on-dips approach.” The Reserve Bank of India is widely expected to raise interest rates for a third straight time on Friday. Of the 33 Nifty companies that have reported results so far, 18 have beaten the consensus view while 15 have trailed. Of the 30 shares in the Sensex index, 16 rose, while 14 fell. IndusInd Bank and Asian Paints were among the key gainers on the Sensex, while Tech Mahindra Ltd. and mortgage lender Housing Development Finance Corp were prominent decliners.

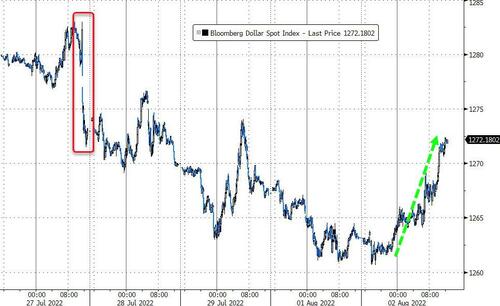

In FX, the Bloomberg dollar spot index rises 0.1%. JPY and CAD are the strongest performers in G-10 FX, NOK and AUD underperforms, after Australia’s central bank hiked rates by 50 basis-points for a third straight month and signaled policy flexibility. USD/JPY dropped as much as 0.9% to 130.41, the lowest since June 3, in the longest streak of daily losses since April 2021. Leveraged accounts are adding to short positions on the pair ahead of Pelosi’s visit, Asia-based FX traders said.

In rates, treasuries extended Monday’s rally in early Asia session as 10-year yields dropped as low as 2.514% amid escalating US-China tension over Taiwan. Treasury yields were richer by up to 5bp across long-end of the curve, where 20-year sector continues to outperform ahead of Wednesday’s quarterly refunding announcement, expected to make extra cutbacks to the tenor. US 10-year yields off lows of the day around 2.55%, lagging bunds by 4bp and gilts by 4.5bp. US stock futures slumped given risk adverse backdrop, adding support into Treasuries while bunds outperform as traders scale back ECB rate hike expectations. The yield on the two-year German note, among the most sensitive to rate hikes, fell as low as 0.17%, its lowest since May 16. Gilts also gained across the curve. Bund curve bull-steepens with 2s10s widening ~2 bps. Gilt and Treasury curves mostly bull-flatten. Australian bonds soared after RBA delivered a third- straight 50bp rate hike as expected, but gave itself wriggle room to slow the pace of tightening in the coming months.

In commodities, WTI trades within Monday’s range, falling 0.6% to trade around $93, while Brent falls below $100. Spot gold is little changed at $1,779/oz. Base metals are mixed; LME nickel falls 2% while LME zinc gains 0.6%.

Bitcoin remains under modest pressure and has incrementally lost the USD 23k mark, but remains comfortably above last-week’s USD 20.6k trough.

Looking to the day ahead now and there is a relatively short list of economic indicators to watch, including June JOLTS report and total vehicle sales (July) for the US, UK’s July Nationwide house price index and July PMI for Canada. Given the apparent uncertainty about the direction of the Fed in markets, many will be awaiting Fed’s Bullard, Mester and Evans, who will speak throughout the day. And in corporate earnings, it will be a busy day featuring results from BP, Caterpillar, Ferrari, Marriott, KKR, Uber, S&P Global, Occidental Petroleum, Electronic Arts, Gilead Sciences, Advanced Micro Devices, Starbucks, Airbnb, PayPal, Marathon Petroleum.

Market Snapshot

- S&P 500 futures down 0.6% to 4,096.50

- STOXX Europe 600 down 0.5% to 435.13

- MXAP down 1.3% to 159.73

- MXAPJ down 1.3% to 516.82

- Nikkei down 1.4% to 27,594.73

- Topix down 1.8% to 1,925.49

- Hang Seng Index down 2.4% to 19,689.21

- Shanghai Composite down 2.3% to 3,186.27

- Sensex little changed at 58,120.97

- Australia S&P/ASX 200 little changed at 6,998.05

- Kospi down 0.5% to 2,439.62

- German 10Y yield little changed at 0.74%

- Euro down 0.3% to $1.0231

- Brent Futures down 0.6% to $99.44/bbl

- Gold spot down 0.1% to $1,770.93

- U.S. Dollar Index up 0.15% to 105.61

Top Overnight News from Bloomberg

- Oil Steadies Before OPEC+ as Traders Weigh Up Market Tightness

- China Slaps Export Ban on 100 Taiwan Brands Before Pelosi Visit

- Pozsar Says L-Shaped Recession Is Needed to Conquer Inflation

- Pelosi’s Taiwan Trip Raises Angst in Global Financial Markets

- Taiwan Risk Joins Long List of Reasons to Shun China Stocks

- Biden Says Strike in Kabul Killed a Planner of 9/11 Attacks

- Biden Team Tries to Blunt China Rage as Pelosi Heads for Taiwan

- The Best and Worst Airlines for Flight Cancellations

- GOP Plans to Deploy Obscure Rule as Weapon Against Spending Bill

- US to Stop TSMC, Intel From Adding Advanced Chip Fabs in China

- US Anti-Terrorism Operation in Afghanistan Kills Al-Qaeda Leader

- They Quit Goldman’s Star Trading Team, Then It Raised Alarms

- Sinema’s Silence on Manchin’s Deal Keeps Everyone Guessing

- Manchin Side-Deal Seeks to Advance Mountain Valley Pipeline

A more detailed look at global markets courtesy of Newsquawk

APAC stocks followed suit to the weak performance across global counterparts as tensions simmered amid Pelosi’s potential visit to Taiwan. ASX 200 was initially pressured ahead of the RBA rate decision where the central bank hiked by 50bp, as expected, although most of the losses in the index were pared amid a lack of any hawkish surprises in the statement and after the central bank noted it was not on a pre-set path. Nikkei 225 declined amid a slew of earnings and continued unwinding of the JPY depreciation. Hang Seng and Shanghai Comp underperformed due to the ongoing US-China tensions after reports that House Speaker Pelosi will arrive in Taiwan late on Tuesday despite the military threats by China, while losses in Hong Kong were exacerbated by weakness in tech and it was also reported that Chinese leaders said the GDP goal is guidance and not a hard target which doesn’t provide much confidence in China’s economy.

Top Asian News

- Tourism Jump to Power Thai GDP Growth to Five-Year High in 2023

- China in Longest Streak of Liquidity Withdrawals Since February

- Singapore Says Can Tame Wild Power Market Without State Control

- India’s Zomato Appoints Four CEOs, to Change Name to Eternal

- Taiwan Tensions Raise Risks in One of Busiest Shipping Lanes

- Japan Trading Giants Book $1.7 Billion Russian LNG Impairment

- Japan Proposes Record Minimum Wage Hike as Inflation Hits

European bourses are pressured as the general tone remains tentative ahead of Pelosi’s visit to Taiwan, Euro Stoxx 50 -0.9%; note, FTSE 100 -0.1% notably outperforms following earnings from BP +3.0%. As such, the Energy sector bucks the trend which has the majority in the red and a defensive bias in-play. Stateside, futures are similarly downbeat and have been drifting lower amid the incremental updates to Pelosi and her possible Taiwan arrival time of circa. 14:30BST/09:30ET; ES -1.0%. Apple (AAPL) files final pricing term sheet for four-part notes offering of up to USD 5.5bln, according to a filing.

Top European News

- Ukraine Sees Slow Return of Grain Exports as World Watches

- Ruble Boosts Raiffeisen’s Russian Unit Despite Credit Halt

- DSM 2Q Adj. Ebitda Up; Jefferies Sees ‘Muted’ Reaction

- Credit Suisse Hit by More Rating Downgrades After CEO Reboot

- Man Group Sees Assets Decline for First Time in Two Years

- Exodus of Young Germans From Family Nest Is Getting Ever Bigger

FX

- Yen extends winning streak through yet more key levels vs Buck and irrespective of general Greenback recovery on heightened US-China tensions over Taiwan

- USD/JPY breaches support around 131.35 and probes 130.50 before stalling, but remains sub-131.00 even though the DXY hovers above 105.500 within a 105.030-710 range.

- Aussie undermined by risk aversion and no hawkish shift by RBA after latest 50bp hike; AUD/USD nearer 0.6900 having climbed to within a few pips of 0.7050 on Monday.

- Kiwi holds up better with AUD/NZD tailwind awaiting NZ jobs data, NZD/USD hovering just under 0.6300 and cross closer to 1.1000 than 1.1100.

- Euro and Pound wane after falling fractionally short of round number levels vs Dollar, EUR/USD back under 1.0250 vs 1.0294 at best, Cable pivoting 1.2200 from 1.2293 yesterday.

- Loonie and Franc rangy after return from Canadian and Swiss market holidays, USD/CAD straddling 1.2850 and USD/CHF rotating around 0.9500.

- Yuan off lows after slightly firmer PBoC midpoint fix, but awaiting repercussions of Pelosi trip given Chinese warnings about strong reprisals, USD/CNH circa 6.7700 and USD/CNY just below 6.7600 vs 6.7950+ and 6.7800+ respectively.

- South Africa’s Eskom says due to a shortage of generation capacity, Stage Two loadshedding could be implemented at short notice between 16:00-00:00 over the next three days.

Fixed Income

- Taiwan-related risk aversion keeps bonds afloat ahead of relatively light pm agenda before a trio of Fed speakers.

- Bunds hold above 159.00 within 159.70-158.57 range, Gilts around 119.50 between 119.70-20 parameters and T-note nearer 122-02 peak than 121-17+ trough.

- UK 2032 supply comfortably twice oversubscribed irrespective of little concession.

Commodities

- WTI Sept and Brent Oct futures trade with both contracts under the USD 100/bbl mark as the participants juggle a myriad of major factors, incl. the JTC commencing shortly.

- Spot gold is stable and just below the 50-DMA at USD 1793/oz while base metals succumb to the broader tone.

- A source with knowledge of last month’s meeting between President Biden and Saudi King Salman said the Saudis will push OPEC+ to increase oil production at their meeting on Wednesday and that the Saudi King made the assurance to President Biden during their face-to-face meeting July 16th, according to Fox Business’s Lawrence.

- US Senator Manchin “secured a commitment” from President Biden, Senate Majority Leader Schumer and House Speaker Pelosi for completion of the Mountain Valley Pipeline, according to 13NEWS.

US Event Calendar

- July Wards Total Vehicle Sales, est. 13.4m, prior 13m

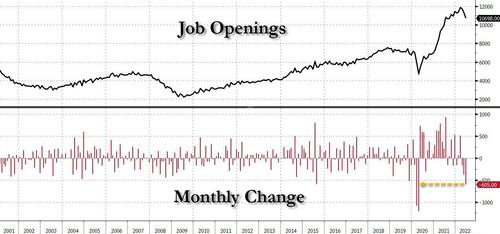

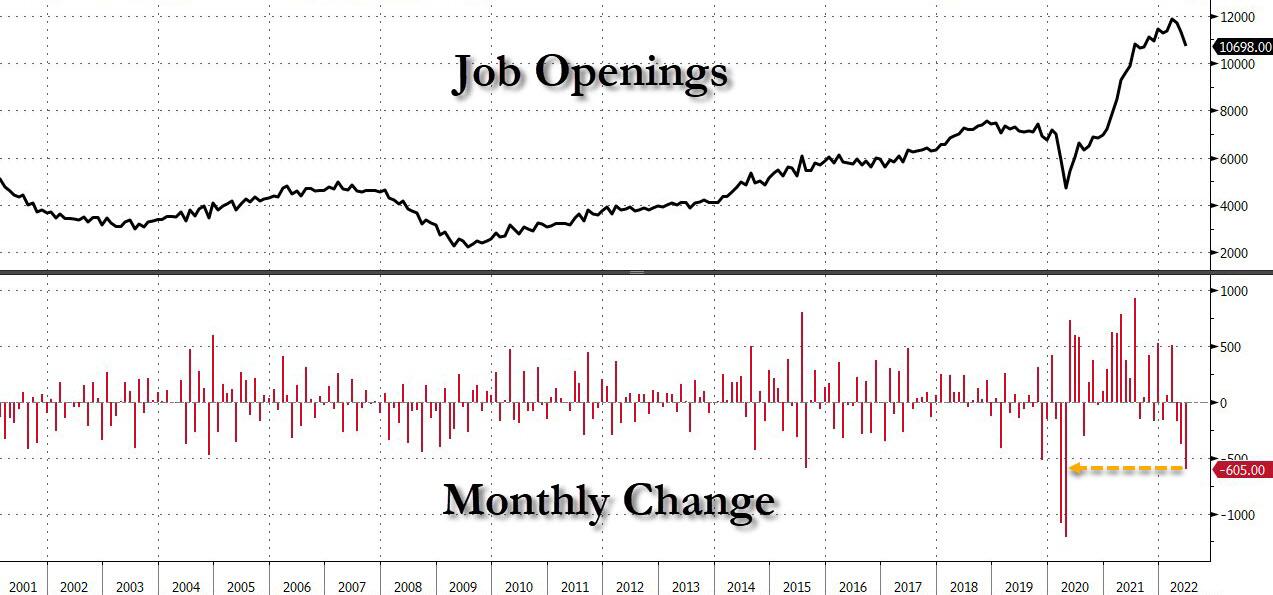

- 10:00: June JOLTs Job Openings, est. 11m, prior 11.3m

- 10:00: Fed’s Evans Hosts Media Breakfast

- 11:00: NY Fed Releases 2Q Household Debt and Credit Report

- 13:00: Fed’s Mester Takes Part in Washington Post Live Event

- 18:45: Fed’s Bullard Speaks to the Money Marketeers

DB’s Jim Reid concludes the overnight wrap

In thin markets, US House Speaker Nancy Pelosi’s visit to Taiwan today for meetings tomorrow (as part of her tour of Asia) could be the main event. She’s scheduled to land tonight local time which will be mid-morning US time. She’ll be the highest ranking US politician to visit in 25 years. Expect some reaction from the Chinese and markets to be nervous. Meanwhile to dial back rising tensions, the White House has urged China to refrain from an aggressive response as speaker Pelosi’s visit does not change the US position toward the island.

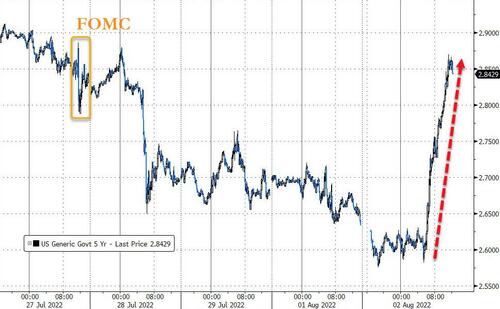

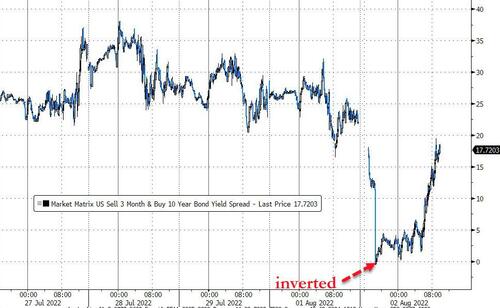

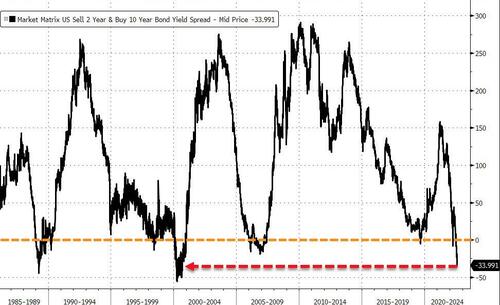

As the headline confirming her visit was going ahead broke, 10 year US Treasuries immediately fell a handful of basis point from 2.69% (opened at 2.665%) and continued falling to around 2.58% as Europe retired for the day, roughly where it closed (-6.8bps). Breakevens led most of the move. 2 year notes actually held in which inverted the curve a further -6.12bps and to the lowest this cycle at -30.84bps. Remember that August is the best month of the year for fixed income (see my CoTD last week here for more on this) so the month has started off in line with the textbook. This morning 10yr USTs yields have dipped another -3bps to 2.55%, some 14bps lower than when Pelosi stopover was first confirmed 18 hours ago. 2yr yields have slightly out-performed with the curve just back below -30bps again.

Lower yields initially helped to lift equities yesterday, with the Nasdaq being up more than a percent at one point before falling with the rest of the market and closing -0.18%. The S&P 500 was -0.28% and dragged lower by energy (-2.17%). The latter came as crude prices moved substantially lower, with WTI losing -4.91% and Brent (-3.97%) dipping below $100 per barrel as well. Growth concerns, partly due to the weekend and yesterday’s data from China, and partly due to the US risk off yesterday, were mainly to blame. These worries filtered through other commodities as well, including industrial metals and agriculture. For the latter, Ukraine’s first grain shipment since the war began was a contributing factor. European gas was a standout, notching a +5.2% gain as the relentless march continues.

In an overall risk-off market, staples (+1.21%) were the only sector meaningfully advancing on the day, followed by discretionary (+0.51%) stocks. Meanwhile, real estate (-0.90%), financials (-0.89%) and materials (-0.82%) dragged the index lower. Although yesterday’s earnings stack was light, today’s line up includes BP, Starbucks, Airbnb and PayPal.

Asian equity markets opened sharply lower this morning on the fresh geopolitical tensions between the US and China over Taiwan. Across the region, the Hang Seng (-2.96%) is leading losses after yesterday’s data showed that Hong Kong slipped into a technical recession as Q2 GDP shrank by -1.4%, contracting for the second consecutive quarter as global headwinds mount. Mainland China stocks are also sliding with the Shanghai Composite (-2.90%) and CSI (-2.33%) trading deep in the red whilst the Nikkei (-1.59%) is also in negative territory. Elsewhere, the Kospi (-0.77%) is also weak in early trade. Outside of Asia, DMs stock futures point to a lower restart with contracts on the S&P 500 (-0.38%), NASDAQ 100 (-0.40%) and DAX (-0.50%) all turning lower.

As we go to print, the RBA board has raised rates by another 50 basis points to 1.85%. Their economic forecasts seem to have been lowered and they have now said monetary policy is “not on a pre-set path” which some are already interpreting as possibly meaning 25bps instead of 50bps at the next meeting. Aussie 10yr yields dropped 7-8bps on the announcement and 10bps on the day.

Back to yesterday, and the important US ISM index, on balance, painted a slightly more comforting picture than it could have been – although the index slowed to the lowest since June 2020. The headline came in above the median estimate on Bloomberg (52.8 vs 52.0). We did see a second month in a row of below-50 score for new orders, but a fall in prices paid from 78.5 to 60.0, the lowest since August 2020, offered some respite to fears about price pressures. Similarly, a rise in the employment gauge from 47.3 to 49.9, beating estimates, was also a positive. The manufacturing PMI was revised down a tenth from the preliminary reading which didn’t move the needle. JOLTS today will be on my radar given it’s been the best measure of US labour market tightness over the past year or so. Also Fed hawks Mester (lunchtime US) and Bullard (after the closing bell) will be speaking today.

Turning to Europe, price action across sovereign bond markets was driven by dovish repricing of ECB’s monetary policy, in contrast to the US where the front end held up. A cloudier growth outlook from yesterday’s European data releases helped drive yields lower – retail sales in Germany unexpectedly contracted in June (-1.6% vs estimates of +0.3%) and Italy’s manufacturing PMI slipped below 50 (48.5 vs 49.0 expected). So Bund yields fell -3.8bps, similar to OATs (-3.1bps). The decline was more pronounced in peripheral yields and spreads, with BTPs (-12.9bps) in particular dropping below 3% for the first time since May of this year, perhaps on further follow through from last week’s story that the far right party leading the polls aren’t planning to break EU budget rules. Spreads have recovered the lost ground from Draghi’s resignation announcement now. Weaker economic data overpowered the effect of lower yields and sent European stocks faded into the close after being higher most of the day with the STOXX 600 eventually declining -0.19%. The Italian market outperformed (+0.11%) for the reasons discussed above.

Early this morning, data showed that South Korea’s July CPI inflation rate rose to +6.3% y/y, hitting its highest level since November 1998 (v/s +6.0% in June), in line with the market consensus. The strong inflation data comes as the Bank of Korea (BOK) mulls further interest rate hikes at its next policy meeting on August 25.

To the day ahead now and there is a relatively short list of economic indicators to watch, including June JOLTS report and total vehicle sales (July) for the US, UK’s July Nationwide house price index and July PMI for Canada. Given the apparent uncertainty about the direction of the Fed in markets, many will be awaiting Fed’s Bullard, Mester and Evans, who will speak throughout the day. And in corporate earnings, it will be a busy day featuring results from BP, Caterpillar, Ferrari, Marriott, KKR, Uber, S&P Global, Occidental Petroleum, Electronic Arts, Gilead Sciences, Advanced Micro Devices, Starbucks, Airbnb, PayPal, Marathon Petroleum.

END

AND NOW NEWSQUAWK

Tentative trade as we await Pelosi’s arrival in Taiwan, Fed speak features – Newsquawk US Market Open

TUESDAY, AUG 02, 2022 – 06:40 AM

- European bourses are pressured as the general tone remains tentative ahead of Pelosi’s visit to Taiwan, Euro Stoxx 50 -0.9%; note, FTSE 100 -0.1% notably outperforms following earnings from BP +3.0%.

- Stateside, futures are similarly downbeat and have been drifting lower amid the incremental updates to Pelosi and her possible Taiwan arrival time of circa. 14:30BST/09:30ET; ES -1.0%.

- DXY lifts as activity currencies wane on the above risk tone alongside JPY extending its winning streak; AUD slips post 50bp hike

- Core fixed income is underpinned pre-Pelosi and Fed speak while UK issuance was twice over-subscribed

- Going into JTC, FBN source says Saudi will push OPEC+ to increase oil production at Wednesday’s gathering

- Looking ahead, highlights include Canadian Manufacturing PMI, New Zealand Unemployment, US NY Fed Household Debt & Credit Report, Speeches from Fed’s Bullard, Evans & Mester. Earnings from Uniper, PayPal, Gilead, Uber & Starbucks.

As of 11:05BST/06:05ET

For the full report and more content like this check out Newsquawk.

Try a 14 day trial with Newsquawk and hear breaking trading news as it happens.

LOOKING AHEAD

- Canadian Manufacturing PMI, New Zealand Unemployment, US NY Fed Household Debt & Credit Report, Speeches from Fed’s Bullard, Evans & Mester. Earnings from Uniper, PayPal, Gilead, Uber & Starbucks.

- Click here for the Week Ahead preview

TAIWAN/PELOSI

- Click here for newsquawk analysis on the subject.

- Several Chinese warplanes flew close to the median line of the Taiwan Strait on Tuesday morning and several Chinese warships have stayed close to the median line of the Taiwan Strait since Monday, according to a source briefed on the matter cited by Reuters. It was also reported that Taiwan’s Defence Ministry reinforced its combat alertness level from Tuesday morning to Thursday noon, according to the official Central News Agency citing sources.

- Global Times’ Hu Xijin says “Based on what I know, in response to Pelosi’s possible visit to Taiwan, Beijing has formulated a series of countermeasures, including military actions.”

- China’s Foreign Ministry says their position on US House Speaker Pelosi’s potential Taiwan visit is clear, will take all necessary measures to preserve interests.

- The plane (SPAR19) likely carrying the delegation of US House Speaker Pelosi is in the air, having departed Kuala Lumpur. It is taking a route around the Philippines to Taiwan. Sources suggest this is designed to minimize the security risks, according to CNN’s Rogin. Follows FlightRadar24 showing the craft in-flight earlier, no confirmation that Pelosi is onboard or as to its destination/flight path.

- SET News expects US House Speaker Pelosi in Taipei at 21:30 local time (14:30BST/09:30EDT).

- “Both of aircraft carriers of the PLA Navy have reportedly moved out from their homeports respectively amid Pelosi’s possible visit to the island of Taiwan, which media reported could happen Tuesday evening.”, according to Global Times.

- Xiamen Air in East China’s Fujian Province announced on Tuesday the adjustment of some of its flights due to flow control, via Global Times. Geographically, the Fujian province is in close proximity to Taiwan

- PLA’s Eastern Theater Command conducts live-fire drills in East China Sea, practicing subjects such as air defense, anti-reconnaissance, missile defense, and long-range sea strikes, via CCTV.

GEOPOLITICS