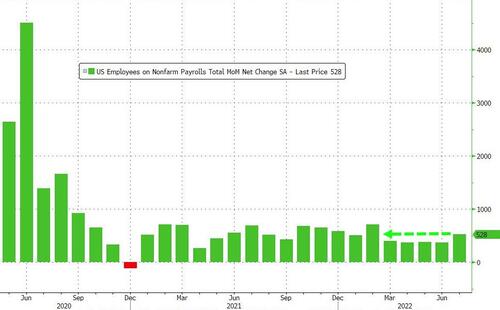

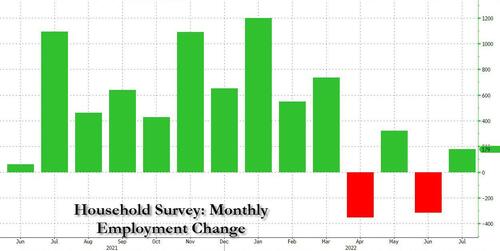

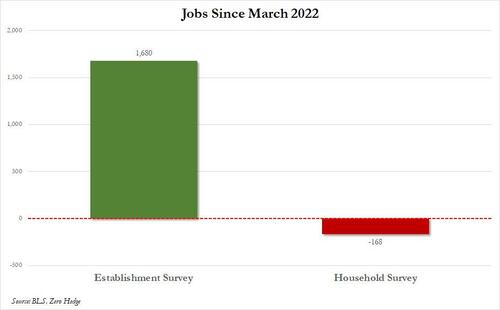

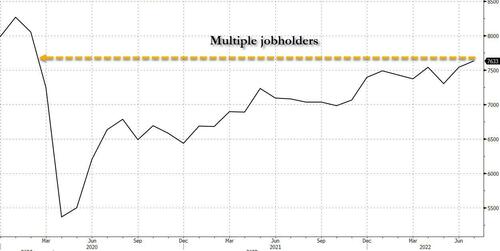

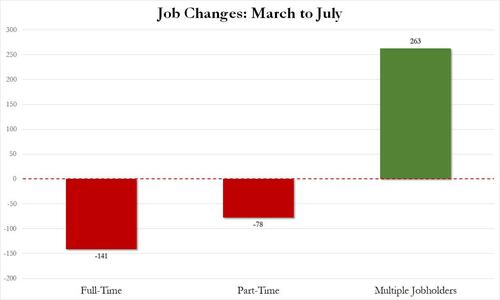

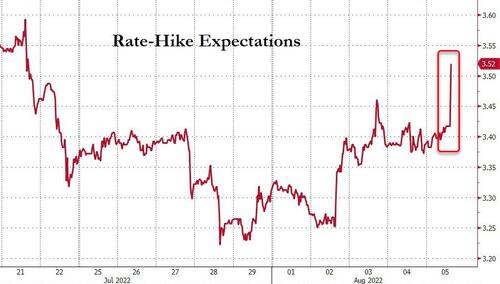

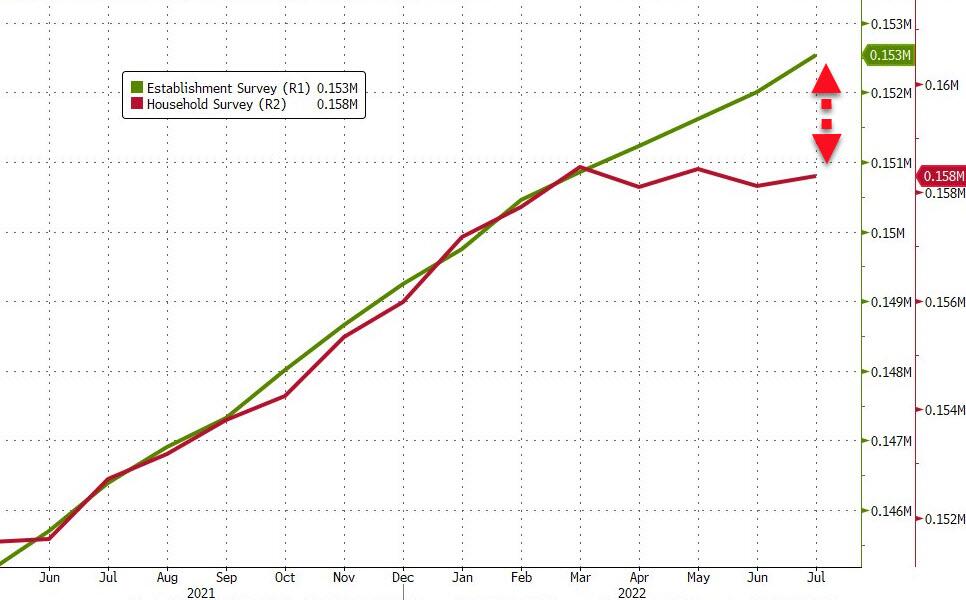

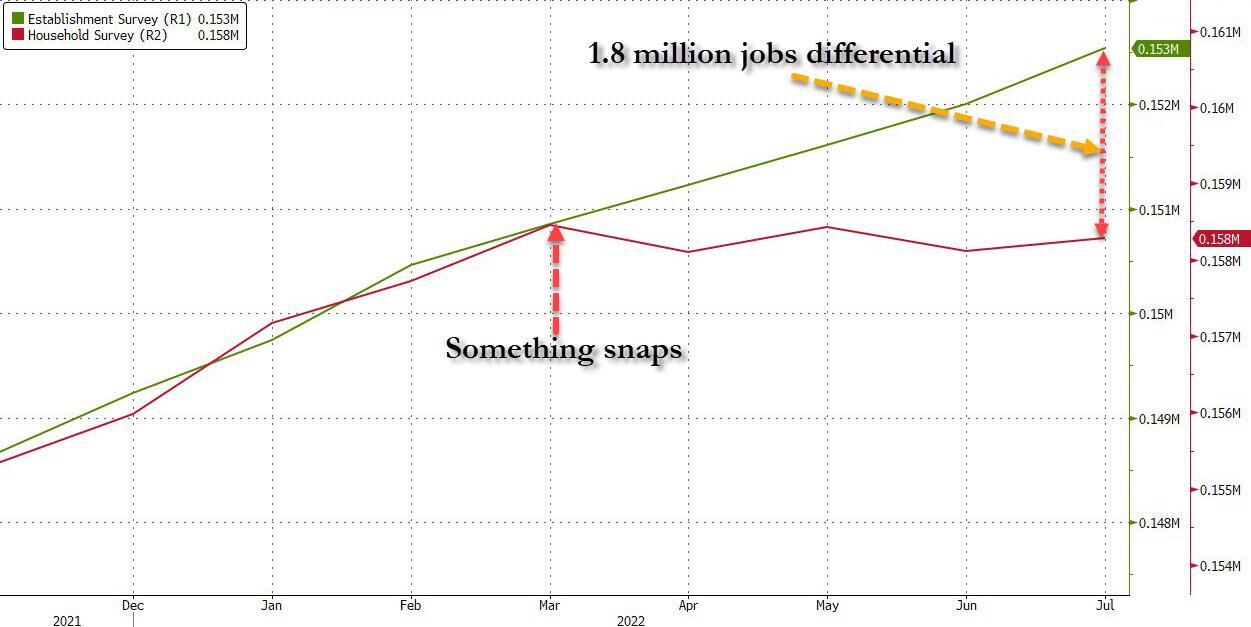

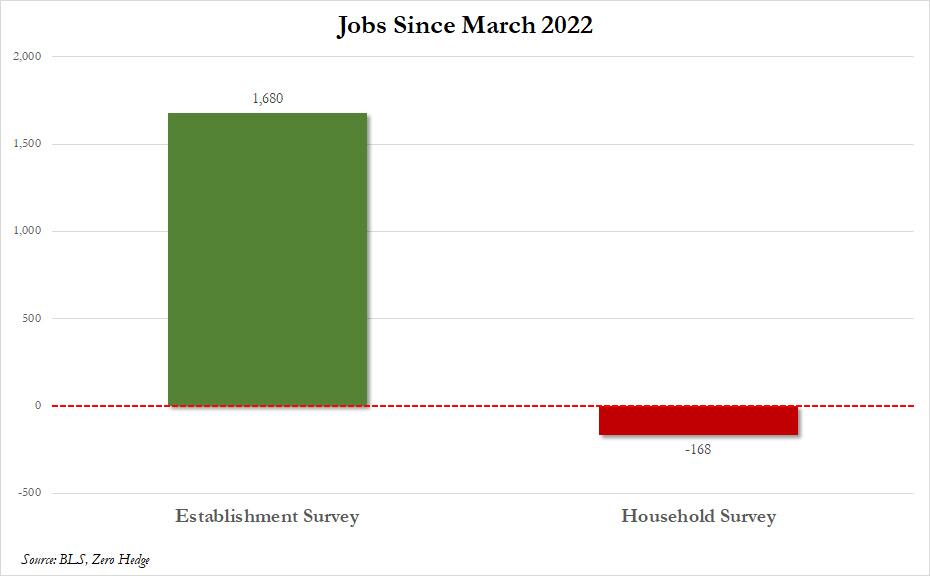

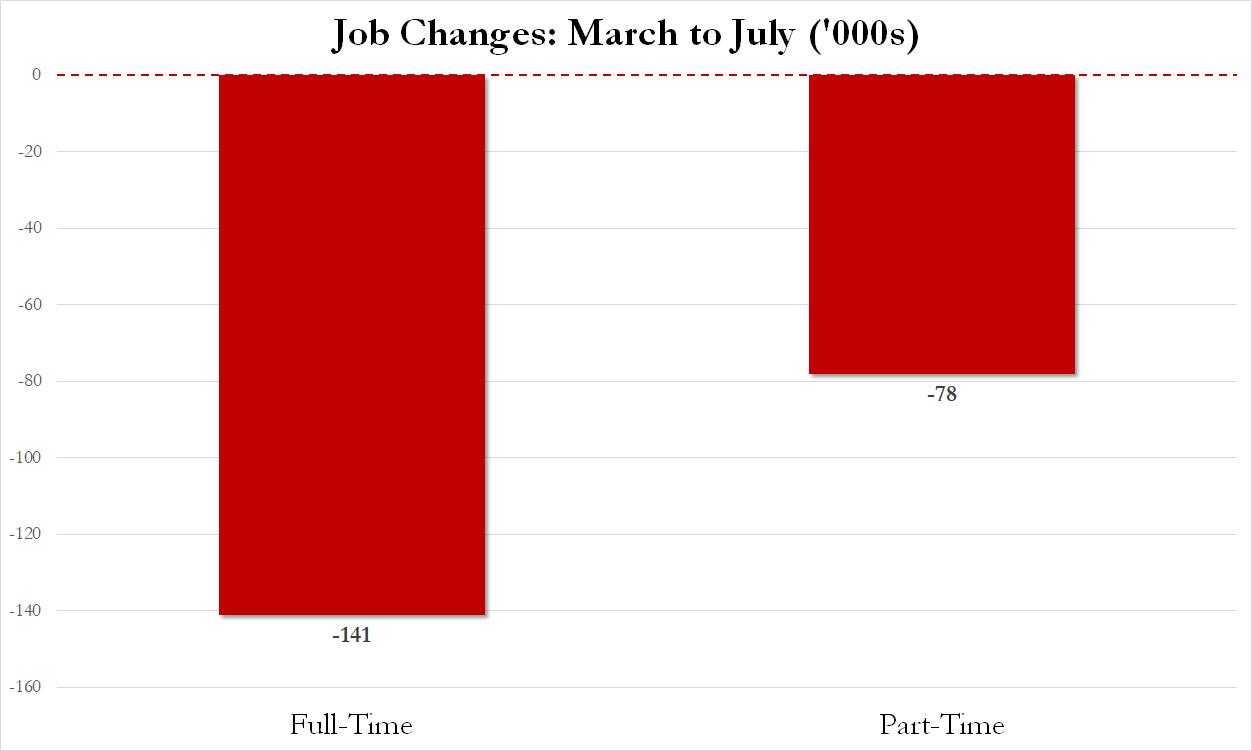

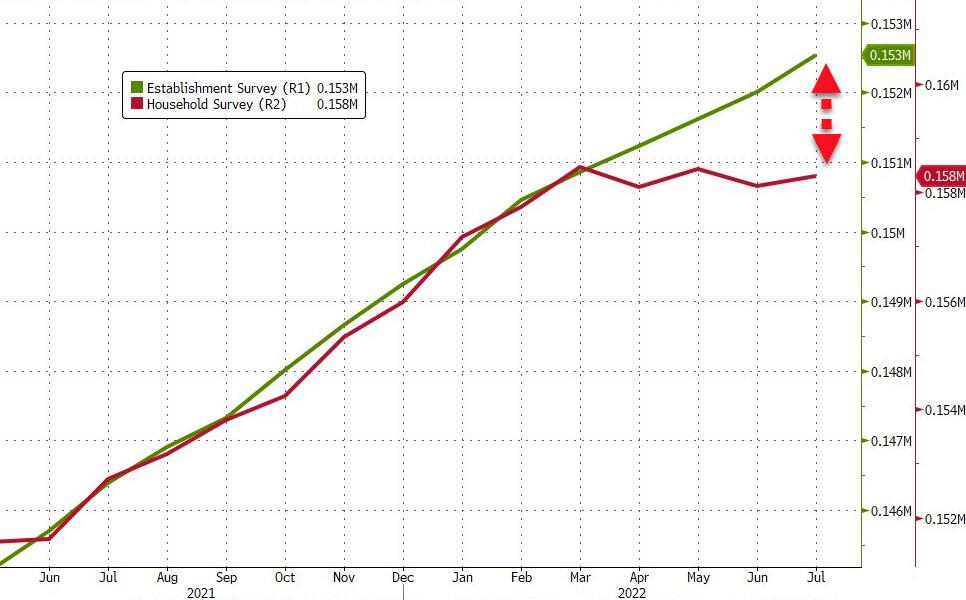

AUGUST 5/GOLD CLOSED DOWN $14.25 TO $1775.50 AFTER A PHONY JOBS REPORT//SILVER CLOSED DOWN 28 CENTS TO $19.86//PLATINUM UNCHANGED AT $931.30//PALLADIUM UP $50.80 TO $2129.25//BIDEN ADMINISTRATION AT IT AGAIN FALSIFYING A MEGA 500,000 +JOB GAIN//THE REAL STORY BEHIND THE ESTABLISHMENT REPORT AND THE HOUSEHOLD SURVEY REPORT ON THE JOB CREATION//COVID UPDATES/VACCINE INJURY REPORT//DR PAUL ALEXANDER//VACCINE IMPACT//COMMENTARY BY JAN N. (KOOS JANSEN) ON HOW TURKEY IS FALSIFYING THEIR FOREIGN EXCHANGE/GOLD RESERVES//

072 C GOLDMAN 87 072 H GOLDMAN 230 104 C MIZUHO 69 118 C MACQUARIE FUT 29 132 C SG AMERICAS 118 167 C MAREX 58 190 H BMO CAPITAL 57 323 H HSBC 1650 624 H BOFA SECURITIES 172 661 C JP MORGAN 623 661 H JP MORGAN 13 685 C RJ OBRIEN 1 686 C STONEX FINANCIA 3 690 C ABN AMRO 8 732 C RBC CAP MARKETS 2 800 C MAREX SPEC 6 26 880 C CITIGROUP 90 30 880 H CITIGROUP 206 905 C ADM 14

GOLD: NUMBER OF NOTICES FILED FOR AUGUST CONTRACT:

1746 NOTICES FOR 174600 OZ //5.430 TONNES

total notices so far: 27,752 contracts for 2,775,200 oz (86.320 tonnes)

SILVER NOTICES:

8 NOTICES FILED FOR 40,000 OZ/

total number of notices filed so far this month 790 : for 3,950,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $14.25

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A SMALL WITHDRAWAL OF 0.33 TONNES OF GOLD FROM THE GLD

INVENTORY RESTS AT 1000.32 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 28 CENTS

AT THE SLV// ://HUGE CHANGES IN SILVER INVENTORY AT THE SLV//:A WITHDRAWAL OF 0.922 MILLION OZ FROM THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 485.712 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 2256 CONTRACTS TO 137,747 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG GAIN IN OI WAS ACCOMPLISHED WITH OUR $0.21 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.21) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY COMMERCIAL SILVER LONGS//. HOWEVER WE HAD SOME SPECULATOR LIQUIDATIONS AS WE HAD A STRONG GAIN OF 2529 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD: I) HUGE SPECULATOR SHORT LIQUIDATIONS//HUGE BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A FAIR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 10,000 OZ QUEUE JUMP / // V) STRONG SIZED COMEX OI GAIN/(SPEC LIQUIDATION)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -28

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTACTS for 5 days, total 2751 contracts: 13.755 million oz OR 2.71 MILLION OZ PER DAY. (550 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 13.755 MILLION OZ

.

LAST 16 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 13.755 MILLION OZ

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2256 WITH OUR $0.21 GAIN IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 245 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER ADDITIONS ////// HUGE SPECULATOR SHORT LIQUIDATION// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 10,000 OZ QUEUE JUMP // .. WE HAD A HUGE SIZED GAIN OF 2501 OI CONTRACTS ON THE TWO EXCHANGES FOR 12.505 MILLION OZ AS..THE SPECS STILL BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 8 NOTICES FILED TODAY FOR 40,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 2179 CONTRACTS TO 461,339 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -355 CONTRACTS.

.

THE FAIR SIZED INCREASE IN COMEX OI CAME WITH OUR RISE IN PRICE OF $29.00//COMEX GOLD TRADING/THURSDAY / WE MUST HAVE HAD ADDITIONAL SPECULATOR SHORT SHORT COVERINGS ACCOMPANYING OUR SMALL SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND HUGE SPECULATOR SHORT COVERINGS//HUGE ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR AUGUST AT 97.02 TONNES ON FIRST DAY NOTICE

YET ALL OF..THIS HAPPENED WITH OUR RISE IN PRICE OF $29.00 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 7784 OI CONTRACTS 24.21 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5605 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 461,339

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7784 CONTRACTS WITH 2179 CONTRACTS INCREASED AT THE COMEX AND 5605 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 8139 CONTRACTS OR 25.315 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5605) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (2179): TOTAL GAIN IN THE TWO EXCHANGES 7784 CONTRACTS. WE NO DOUBT HAD 1) HUGE SPECULATOR SHORT COVERINGS//STRONG BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR AUGUST. AT 99.272 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 5900 oz. 3) ZERO LONG LIQUIDATION//// //.,4) FAIR SIZED COMEX OPEN INTEREST GAIN 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST :

12,491 CONTRACTS OR 1,249,100 OZ OR 38,852 TONNES 5 TRADING DAY(S) AND THUS AVERAGING: 2498 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAY(S) IN TONNES: 38.852 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 38.852/3550 x 100% TONNES 1.09% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 38.852 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF SEPT., FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A HUGE SIZED 2256 CONTRACT OI TO 137,719 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 245 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 245 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 245 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2256 CONTRACTS AND ADD TO THE 245 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 2501 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 12.505 MILLION OZ

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED UP 37.99 PTS OR 1.19% //Hang Seng CLOSED UP 27.90 OR 0.04% /The Nikkei closed UP 243.07 OR % 0.87. //Australia’s all ordinaires CLOSED UP 0.59% /Chinese yuan (ONSHORE) closed UP AT 6.7519//OFFSHORE CHINESE YUAN UP 6.7507// /Oil DOWN TO 88.29 dollars per barrel for WTI and BRENT AT 93.76// SHANGHAI CLOSED UP 37.99 PTS OR 1.19% //Hang Sang CLOSED UP 27.90 OR 0.04% /The Nikkei closed UP 243.67 OR % 0.87. //Australia’s all ordinaries CLOSED UP 0.59% / Stocks in Europe OPENED MOSTLY RED. ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 2179 CONTRACTS TO 461,339 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS FAIR COMEX INCREASE OCCURRED DESPITE OUR STRONG RISE OF $29.00 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (5605 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF AUGUST.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 5605 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :5605 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5605 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED SIZED TOTAL OF 8139 CONTRACTS IN THAT5605 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 2534 CONTRACTS..AND THIS SMALLISH GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR HUGE RISE IN PRICE OF GOLD $ 29.00. . WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING AUGUST (97.02),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:97.02 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $29.00) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS // COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO COVER TO THEIR POSITIONS////// WE HAVE REGISTERED A STRONG SIZED GAIN OF 7784 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR AUGUST (97.02 TONNES)…

WE HAD -355 CONTRACTS SUBTRACTED TO COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 7784 CONTRACTS OR 778,400 OZ OR 24.21 TONNES

Estimated gold volume 170,446/// poor/

final gold volumes/yesterday 169,237 / poor

INITIAL STANDINGS FOR AUGUST ’22 COMEX GOLD //AUGUST 5

Total monthly oz gold served (contracts) so far this month

27,752 notices 2,775,200 OZ 86.320 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 2

i) Into Brinks: 35,494.704 oz (1104 KILOBARS)

ii) Into Delaware 2314.872 oz (720 kilobars)

total deposits: 37,809.576 oz

2 customer withdrawals:

i) out of Brinks: 66,093.381 oz

ii) Out of manfra; 73,362.070 oz

total: 139,455.407 oz

total in tonnes:4.33 tonnes

Adjustments: dealer to customer

Brinks 84,495.557 oz

JPmorgan: 24,588.795 oz

Loomis: 5,883.633 oz

Malca 166,863.690 oz

Manfra 15,629.307 oz

customer to dealer: hsbc 69,186.686 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 5188 contracts having LOST 444 contracts .

We had 503 notices served upon yesterday so we gained 59 contracts or an additional 5900 oz will stand for delivery in this very active month of August.

From this point on, we will now add to the amount of gold standing at the comex until the end of the month.

Sept. lost 582 contracts to 3028 contracts.

October GAINED 56 contracts UP to 40,363

We had 1746 notice(s) filed today for 174,600 oz FOR THE AUGUST 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1742 contract(s) of which 13 notices were stopped (received) by j.P. Morgan dealer and 623 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2022. contract month,

we take the total number of notices filed so far for the month (27,752) x 100 oz , to which we add the difference between the open interest for the front month of (AUGUST 5188 CONTRACTS ) minus the number of notices served upon today 1746 x 100 oz per contract equals 3,119,400 OZ OR 97.02 TONNES the number of TONNES standing in this active month of AUGUST.

thus the INITIAL standings for gold for the AUGUST contract month:

No of notices filed so far (27,752) x 100 oz+ (5188) OI for the front month minus the number of notices served upon today (1746} x 100 oz} which equals 3,119,400 oz standing OR 97.02 TONNES in this active delivery month of August.

TOTAL COMEX GOLD STANDING: 97.020 TONNES (A HUGE STANDING FOR AUGUST ( ACTIVE) DELIVERY MONTH)

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 790 x 5,000 oz = 3,950,000 oz

to which we add the difference between the open interest for the front month of AUGUST(104) and the number of notices served upon today 8 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST./2022 contract month: 790 (notices served so far) x 5000 oz + OI for front month of AUGUST (104) – number of notices served upon today (8) x 5000 oz of silver standing for the AUGUST contract month equates 4,430,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

AUGUST 5/WITH GOLD DOWN $14.25: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .33 TONNES FROM THE GLD////INVENTORY RESTS AT 1000.32 TONNES

AUGUST 4 WITH GOLD UP $29.00 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES FROM THE GLD///INVENTORY REST AT 1000.65 TONNES

AUGUST 2/WITH GOLD UP $3.70; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD//INVENTORY RESTS AT 1002.97 TONNES//

AUGUST 1/WITH GOLD UP $5.75: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 29//WITH GOLD UP $12.50; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1005.29 TONNES

JULY 28/WITH GOLD UP $31.25; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 27.//WITH GOLD UP $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 26/WITH GOLD DOWN $1.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.29 TONNES

JULY 25/WITH GOLD DOWN $7.85: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 1005.87 TONNES

JULY 22/WITH GOLD UP $17.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 21/WITH GOLD UP $11.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.101 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.87 TONNES

JULY 20/WITH GOLD DOWN $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1009.06 TONNES

JULY 19/WITH GOLD DOWN $.35 :BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.22 TONNES FROM THE GLD//INVENTORY RESTS AT 1009.06 TONNES

JULY 18/WITH GOLD UP $7.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.28 TONNES

JULY 15/WITH GOLD DOWN $3.75:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD///INVENTORY RESTS AT 1016.89 TONNES//

JULY 14/WITH GOLD DOWN $28.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD//INVENTORY RESTS AT 1019.79 TONNES

JULY 13/WITH GOLD UP $10.55:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD//INVENTORY RESTS AT 1021.53TONNES

JULY 12/WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESS AT 1023.27 TONNES

JULY 11/WITH GOLD DOWN $4.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD./INVENTORY RESTS AT 1023.27 TONNES

JULY 7/WITH GOLD UP $1.35: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.61 TONNES FORM THE GLD///INVENTORY REST AT 1024.43 TONNES

JULY 6/WITH GOLD DOWN $26.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 9.86 TONNES FROM THE GLD//INVENTORY REST AT 1032.04 TONNES

JULY 5/WITH GOLD DOWN $36.55//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.41 TONNES FROM THE GLD///INVENTORY RESTS AT 1041.90 TONNES

JULY 1/WITH GOLD DOWN $5.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES//INVENTORY RESTS AT 1050.31 TONNES

JUNE 30/WITH GOLD DOWN $9.20: big CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 1052.63 TONNES//

JUNE 28/WITH GOLD DOWN $3.05//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.64 TONNES FROM THE GLD///INVENTORY RESTS AT 1056.40 TONNES

JUNE 27/WITH GOLD DOWN $4.90 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.04 TONNES

JUNE 24/WITH GOLD UP 45 CENTS TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.70 TONNES FROM THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 23/WITH GOLD DOWN $8.60:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//INVENTORY RESTS AT 1071.77 TONNES

JUNE 22/WITH GOLD UP 15 CENTS:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1073.80 TONNES

GLD INVENTORY: 1000.32 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 5/WITH SILVER DOWN 28 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 922,000 OZ FROM THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 4 WITH SILVER UP 21 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 527,000 OZ FROM THE SLV////INVENTORY RESTS AT 486.634 MILLION OZ

AUGUST 2/WITH SILVER DOWN 21 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.504 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.161 MILLION OZ//

AUGUST 1/WITH SILVER UP 17 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE GLD: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 483.657 MILLION OZ//

JULY 29/WITH SILVER UP 30 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 461,000 OZ FROM THE SLV..//INVENTORY RESTS AT 483.657 MILLION OZ/

JULY 28/WITH SILVER UP $1.24 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 484.118 MILLION OZ/

JULY 27/.WITH SILVER UP 4 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL 11.479 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 484.118MILLION OZ//

JULY 26/WITH SILVER UP 16 CENTS: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.504 MILLION OZ FROM THE SLV//: //INVENTORY RESTS AT 495.597 MILLION OZ//

JULY 25/WITH SILVER DOWN 24 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.383 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 499.101 MILLION OZ//

JULY 22/WITH SILVER DOWN 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 500.484 MILLION OZ//

JULY 21/WITH SILVER UP 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.19 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 500.484MILLION OZ/

JULY 20/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 8.253 MILLION OZ FORM THE SLV/INVENTORY RESTS AT 507.585 MILLION OZ//

JULY 19/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ//

JULY 18/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 4.995 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ.

JULY 15/WITH SILVER UP 31 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 3.226 MILLION OZ FORM THE SLV//INVENTORY RESTS AT 510.443 MILLIONOZ//

JULY 14/WITH SILVER DOWN 88 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 OZ FROM THE SLV// //INVENTORY RESTS AT 513.671 MILLION OZ

JULY 13/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SV//INVENTORY RESTS AT 514.501 MILLION OZ.

JULY 12/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.228 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 514.501 MILLION OZ//

JULY 11/WITH SILVER DOWN 17 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 5.533 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 517.729 MILLION OZ

JULY 7/WITH SILVER UP 3 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.889 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 523.262 MILLION OZ/

JULY 6/WITH SILVER UP ONE CENT: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 12.558 MILLION OZ FORM THE SLV///INVENTORY RESTS AT 528.151 MILLION OZ

JULY 5/WITH SILVER DOWN 55 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 540.709MILLION OZ//

JULY 1/WITH SILVER DOWN 61 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ//INVENTORY RESTS AT 540.709 MILLION OZ//

JUNE 30/WITH SILVER DOWN 41 CENTS : SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 738,000 OZ FROM THE SLV//INVENTORY RESTS AT 541.262 MILLION OZ//

JUNE 28/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.00 MILLION OZ..

JUNE 27/WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 24/WITH SILVER UP 10 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.137 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 23/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 2.029 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 545.137 MILLION OZ//

JUNE 22/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.166 MILLION OZ.

CLOSING INVENTORY 485.712 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

3.Chris Powell of GATA provides to us very important physical commentaries

Alasdair Macleod: Is bank credit friend or foe?

Submitted by admin on Thu, 2022-08-04 11:48Section: Daily Dispatches

By Alasdair Macleod GoldMoney, Toronto Thursday, August 4, 2022

Advocates of sound money place much of the blame for inflation on bank credit. Do away with the creation of bank credit, they say, and the destructive cycle of boom and bust will be cured. But is this solution practical, and is it the real inflation problem?

It may be an inconvenient fact, but commodity prices prove to be far more volatile under a fiat currency regime than they ever where under sound money and fluctuations in bank credit.

Understanding bank credit possesses a new urgency, given that this cycle of its expansion appears to be ending and the fiat world is heading for a periodic credit contraction. This article details how bank credit is created, how it has evolved and its role in fostering economic progress. We look at the alternative of banks of deposit, their history, and their practicality as a replacement for banking as we know it today.

We must be clear that there is a difference between cycles of bank credit, which so long as they are moderate can be tolerated, and state-induced inflation of the currency, which can be expected to lead to a permanent loss of a fiat currency’s purchasing power. In this context, are proposals to do away with bank credit taking a sledgehammer to crack the wrong nut?

On this subject, the Keynesian and Austrian economists disagree fundamentally. The conclusion of this article is that bank credit is economically beneficial, but it is state intervention in one form or another which has made it not just a driving force for economic progress, but unnecessarily destructive as well. …

As a serious investor, you’re well aware of the unique challenges presented by today’s markets.

— Central banks — led by the Federal Reserve — intent to fight off rising inflation with rate hikes.

— The markets responding with massive selloffs, sending a clear message to the Fed to lay off.

Inflation remaining at 1970s levels, and the U.S. economy hurtling toward recession. …

— … while the Fed itself is running head-long into today’s towering debt loads, the insurmountable obstacle blocking their rate-hike campaign.

With all this and more going on, many investors are caught like deer in the headlights, unsure of which way to turn.

But a few others are quietly confident, taking comfort in one unassailable fact:

The New Orleans Conference will be back in full force Wednesday through Saturday, October 12-15.

And this is why I’m writing you now: We’ve opened registration for this year’s New Orleans Investment Conference, and it may be the most eagerly awaited event in our 48-year history.

There are a number of reasons for the excitement.

First, we’ll finally be “back” after a three-year absence due to the Covid pandemic.

Yes, we hosted our first in-person event last year, but many of our exhibiting companies and friends from around the world weren’t able to travel and join us. Still, it was an extraordinary gathering, seeping with intellectual energy from our attendees and value from our elite speakers.

Now that everyone will be able to join us, we’re going to blow the doors off with this year’s New Orleans Conference.

Our phones have been ringing and our email inboxes bursting with inquiries from across the globe.

This event is not to be missed!

Second, the fundamentals and technicals are lined up perfectly for the precious metals, commodity, and mining stock opportunities that the New Orleans Conference is renowned for offering.

— Inflation has surged to 1970s levels, and real rates are more negative than at any time since the 1940s.

— The Fed is dead-set on the most aggressive monetary tightening in decades, with enormous repercussions now being felt in every investment sector.

— But with an enormous federal debt today — three times its level in 2008 — the Fed is powerless to fight inflation.

— The next big development comes when the Fed is forced to retreat from its rate hikes.

— When the Fed wavers, specific investment sectors are going to explode higher.

What does it all mean?

It means you’re now facing tremendous risks and opportunities — and you have to be prepared for what’s coming.

Third, we have lined up an extraordinary roster of speakers, drawing heavily on the wildly popular experts from last year, with many more still to come.

Consider who has told us they’re coming to talk to you so far:

James Grant. Jim Rickards. George Gammon. Danielle DiMartino Booth. Tavi Costa. Peter Boockvar. Jim Iuorio. Dave Collum. Lawrence Lepard. Doug Casey. Jon Najarian and Marc LoPresti. Dominic Frisby. Adam Taggart. Bob Prechter. Adrian Day. Mark Skousen. Mary Anne and Pam Aden. Steven Hochberg. The Real Estate Guys. Brent Cook. Thom Calandra. Chris Powell. Dana Samuelson. Gary Alexander. Albert Lu. Mike Larson. Nick Hodge. Lobo Tiggre. Omar Ayales.

…and, of course, yours truly.

Again, there’s much more to come — we’re still in the midst of planning this year’s event, and I’ve got some big surprises in store.

But even at this early date, one thing seems certain: New Orleans 2022 is going to be a blockbuster!

I urge you to secure your place for New Orleans 2022.

I don’t remember an investment event as eagerly awaited as this one.

Everything — the years spent mired in the pandemic, the macro-economic setup, the geopolitical uncertainty, the teetering stock markets, soaring inflation, a looming generational commodities bull market, and the Fed’s upcoming retreat on monetary tightening — make New Orleans 2022 a must-attend event.

I fully expect our entire hotel room block to sell out this year, so you’ll have to act soon to make sure you’ll get in.

By registering now, you’ll not only save up to $400 from the full registration fee — you’ll also guarantee your place.

Submitted by admin on Thu, 2022-08-04 09:37Section: Daily Dispatches

From the Swiss Broadcasting Corp., Bern Wednesday, August 3, 2022

Switzerland, a major global hub for gold, has followed the European Union in banning imports of Russian gold as part of new sanctions due to the war in Ukraine.

“The new measures primarily concern a ban on buying, importing, or transporting gold and gold products from Russia. Services in connection with these goods are also prohibited,” the economics ministry wrote on Wednesday.

The decision is in line with the ban on Russian gold made by the EU on July 21, the ministry said, and implements “the most urgent measures in terms of time and substance” taken by Brussels. Until now only exports of gold from Switzerland to Russia had been banned.

The potential impact of the new sanctions on Swiss refineries is unclear. Following the invasion of Ukraine in February, imports from Russia have been largely avoided for ethical reasons. Moreover, since March 7 trade of bullion produced by Russian refineries has not been possible in Switzerland, due to a decision by the leading London Bullion Market Association. …

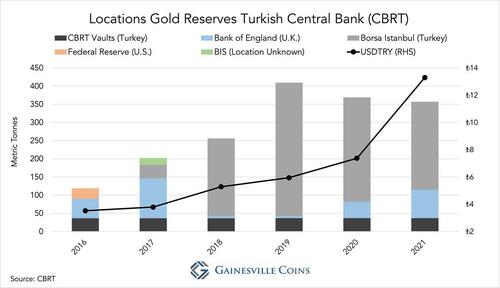

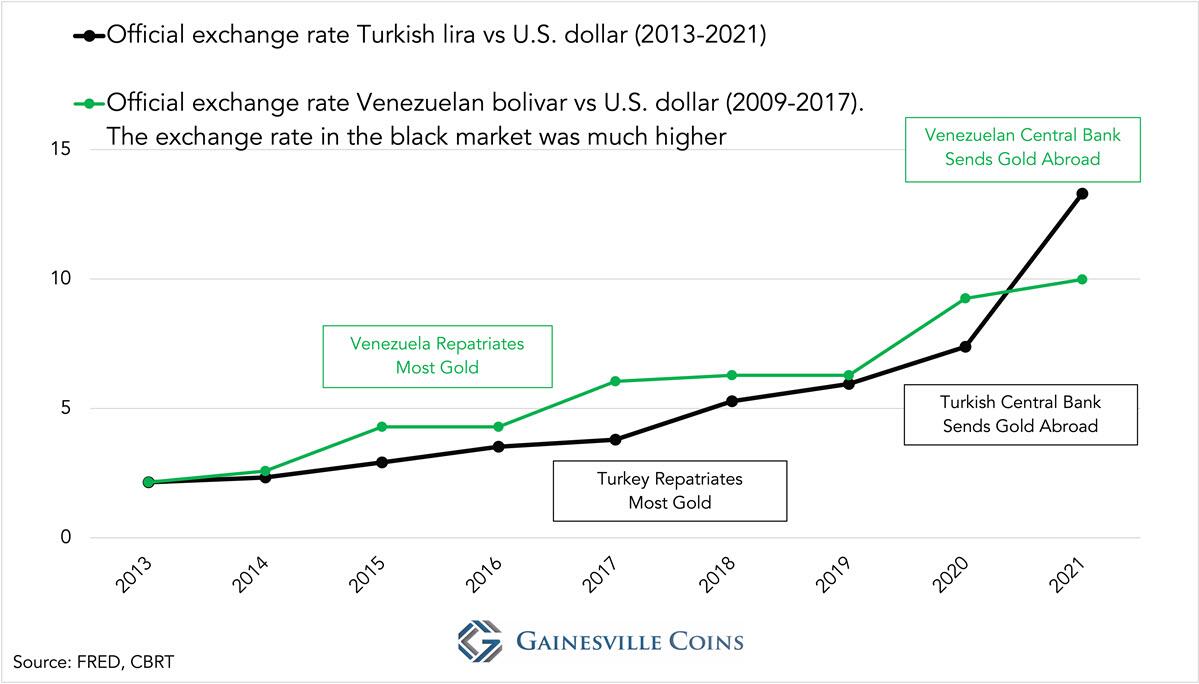

This is a very important commentary which we brought to your attention yesterday. Jan N. describes how the market misinterprets the amount of gold actually

held clear by Turkey. Erdogan uses swaps and it is highly likely that they are down to less than 300 tonnes. Also it has been reported that their net foreign exchanges reserves

are negative

(Jan N. //(Koos Jansen)//Gainsville coins)

In Desperate Need Of FX, Turkish Central Bank Sends Gold To London

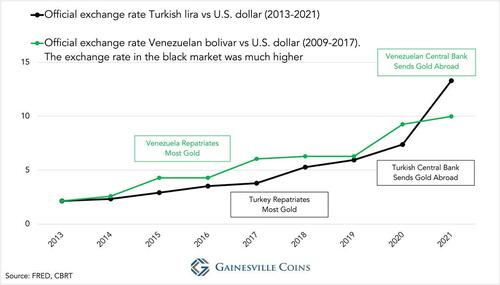

After having repatriated 104 tonnes from the Bank of England (BOE) in 2018, the Central Bank of Turkey (CBRT) has been sending gold back to London in 2020 and 2021. Amid economic turmoil that’s weakening the Turkish lira, CBRT is likely using its gold at BOE as collateral for foreign exchange (FX) loans. Turkey’s situation is reminiscent of Venezuela several years ago.

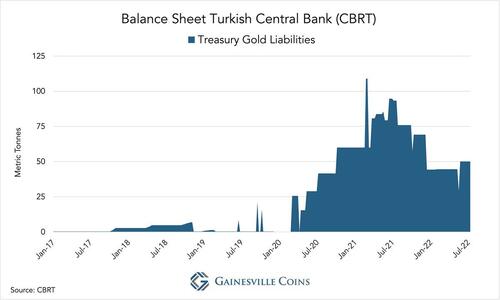

Computing Turkey’s net gold reserves is complicated, because since 2011 CBRT and the Turkish Treasury have launched several schemes to borrow gold, which all show up on the central bank’s balance sheet. Simplified, what I have done is take the tonnage “owned by the central bank” in CBRT’s annual report—this excludes gold submitted by banks for reserve requirements and the Treasury’s gold—and subtracted outstanding Turkish lira for gold swaps*.

The World Gold Council (WGC) computes Turkish net gold reserves differently. My estimate for Turkey’s net gold reserves on December 31, 2021, is 354 tonnes, roughly 300 tonnes less than what the IMF reports, while the WGC discloses 394 tonnes. A more detailed discussion on this topic can be found in the Appendix.

*A swap in this article refers to a spot sale (for example, selling gold for dollars) that is unwound by a forward transaction (buying gold with dollars) for a slightly higher price reflecting an interest rate. A swap can also be viewed as a collateralized loan (borrowing dollars with gold as collateral).

Sending Back Repatriated Gold

In 2017 and 2018 CBRT repatriated all its gold from the Federal Reserve Bank of New York (FRBNY) and the Bank for International Settlements (BIS), and all but 6 tonnes from BOE, according to its annual reports. All the repatriated gold was moved into the vaults of Borsa Istanbul. CBRT is highly influenced by Turkish President Erdogan, who has strained ties with the West. The central bank prefers to store gold on its own soil, preventing rivals from having leverage in disputes.

Yet in 2020 CBRT began shipping gold back from Turkey to London, which is one of the most liquid gold markets globally. At the end of 2021 CBRT was holding 78 tonnes at the BOE. Possibly, it wants to hold gold in London for an emergency sale. More likely the gold is being swapped for FX to defend the lira or make international payments.

Turkey’s economy is in dire straits. Consumer price inflation is at 80% and the Turkish lira has lost 90% of its value versus the U.S. dollar in less than 14 years. The currency crisis is eating into Turkey’s FX reserves.

In turn, President Erdogan doesn’t believe in raising interest rates to stop the lira from plummeting in value. He thinks higher interest rates will fuel inflation, instead of the other way around. On the first of January of this year, it took 13 Turkish liras to buy 1 U.S. dollar; at the time of writing, it takes 18 liras. This will not end well if Erdogan continues to control CBRT and assumes inflation will magically disappear by itself.

Conclusion

There is intense pressure on CBRT’s international reserves—gold, FX, and SDRs. My estimate for CBRT’s net gold holdings is at most 354 tonnes (end 2021) but can be significantly lower if some of it has been swapped for FX in London. In case all CBRT’s gold at BOE is on swap, 78 tonnes must be deducted from the total (354 – 78 = 276). When Turkey can’t unwind the swap by buying back their gold, the collateral is lost.

After Turkish foreign exchange reserves dropped to a multi-decade low over the summer, some gold holdings are believed to have been mobilized to support the lira and/or repay international debt.

It could be this quote refers to gold for FX swaps by CBRT in London.

According to this website by two Turkish economists, CBRT’s net international reserves were negative in 2021, when taking into account all (on and off balance sheet) FX liabilities. More recently Reuters reported Turkey’s net international reserves are negative. If true—I haven’t been able to calculate CBRT’s net FX reserves myself—this means that Turkey won’t be able to pay its international debt obligations, even it sells all its gold and SDRs. Only an emergency loan by the IMF or a miracle can save it.

Appendix

The following explains how I have computed Turkey’s net gold reserves.

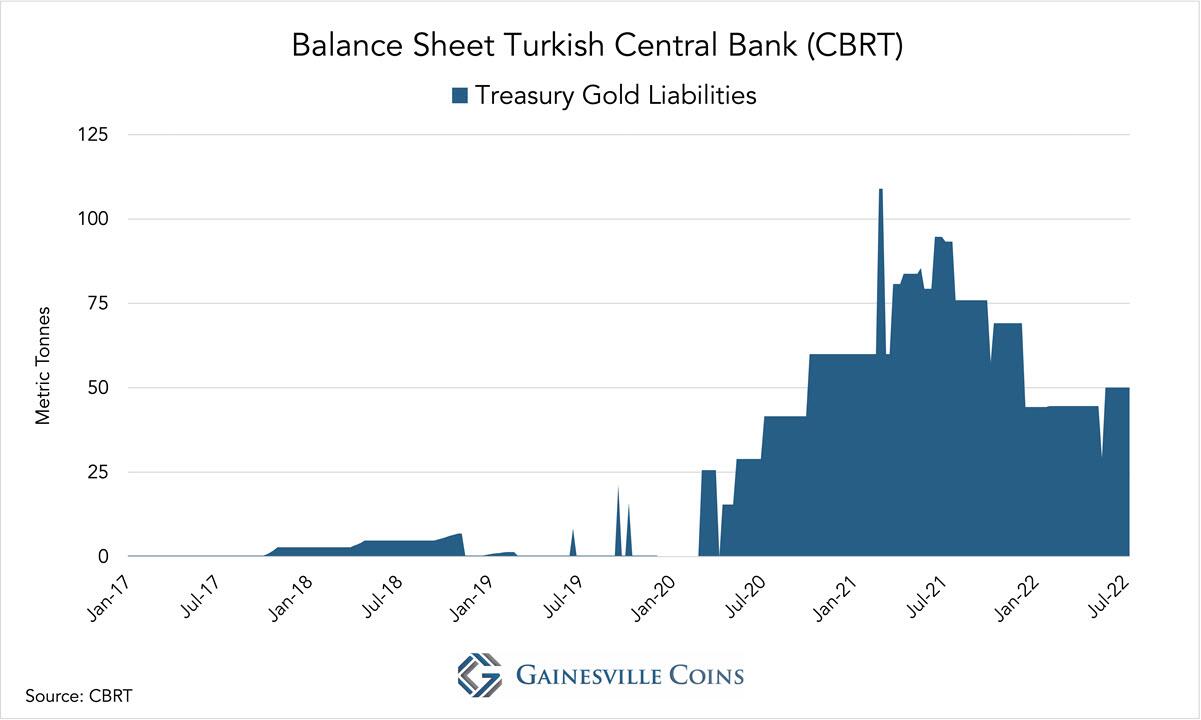

Starting in 2011, CBRT allowed commercial banks to fulfill their lira reserve requirements partly in gold. The aim was to attract physical gold from “under-the-mattress” into the financial system, which banks would use for reserve requirements (RR), freeing up lira liquidity. Gold QE, if you will. The scheme was modestly successful, because most of the gold submitted for RR by banks was borrowed in London. This facility is called the Reserve Option Mechanism (ROM).

In 2018, the Turkish Treasury began issuing gold bonds. The gold borrowed is transferred to CBRT’s balance sheet, and thus increases CBRT’s gross gold reserves and gold liabilities to the Treasury. Issuing of gold bonds has intensified, as measured by CBRT’s gold liabilities to the Treasury. See the chart below.

As mentioned earlier, my starting point in calculating CBRT’s net gold reserves has been the tonnage “owned by the central bank” in the annual reports. Cross checks confirm this amount excludes gold in the ROM facility and the Treasury’s gold on CBRT balance sheet. Subsequently, I have subtracted the total amount of gold swaps outstanding from the total. The result is my estimate for Turkey’s net gold reserves.

For those interested, here is a paper by the World Gold Council on how they measure Turkey’s net gold reserves.

end

5.OTHER COMMODITIES: WHEAT//GRAINS/DIESEL

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

end

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.7519

OFFSHORE YUAN: 6.7504

HANG SENG CLOSED UP 27.90 PTS OR 0.46%

2. Nikkei closed UP 243.67 OR 0.87%

3. Europe stocks CLOSED MOSTLY RED

USA dollar INDEX UP TO 105726/Euro FALLS TO 1.0235

3b Japan 10 YR bond yield: FALLS TO. +.169/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 133.09/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: UP -// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +0.819%/Italian 10 Yr bond yield RISES to 3.05% /SPAIN 10 YR BOND YIELD FALLS TO 1.89%…

3i Greek 10 year bond yield FALLS TO 2.95//

3j Gold at $1787.50 silver at: 20.11 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 19/100 roubles/dollar; ROUBLE AT 60.53

3m oil into the 88 dollar handle for WTI and 93 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 133.09DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9557– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9782well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.694 UP 2 BASIS PTS

USA 30 YR BOND YIELD: 2.969 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.97

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

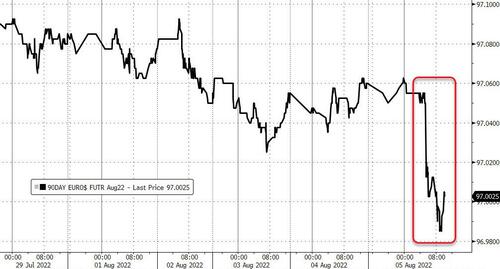

Futures Flat Ahead Of Much-Anticipated Jobs Report

FRIDAY, AUG 05, 2022 – 07:39 AM

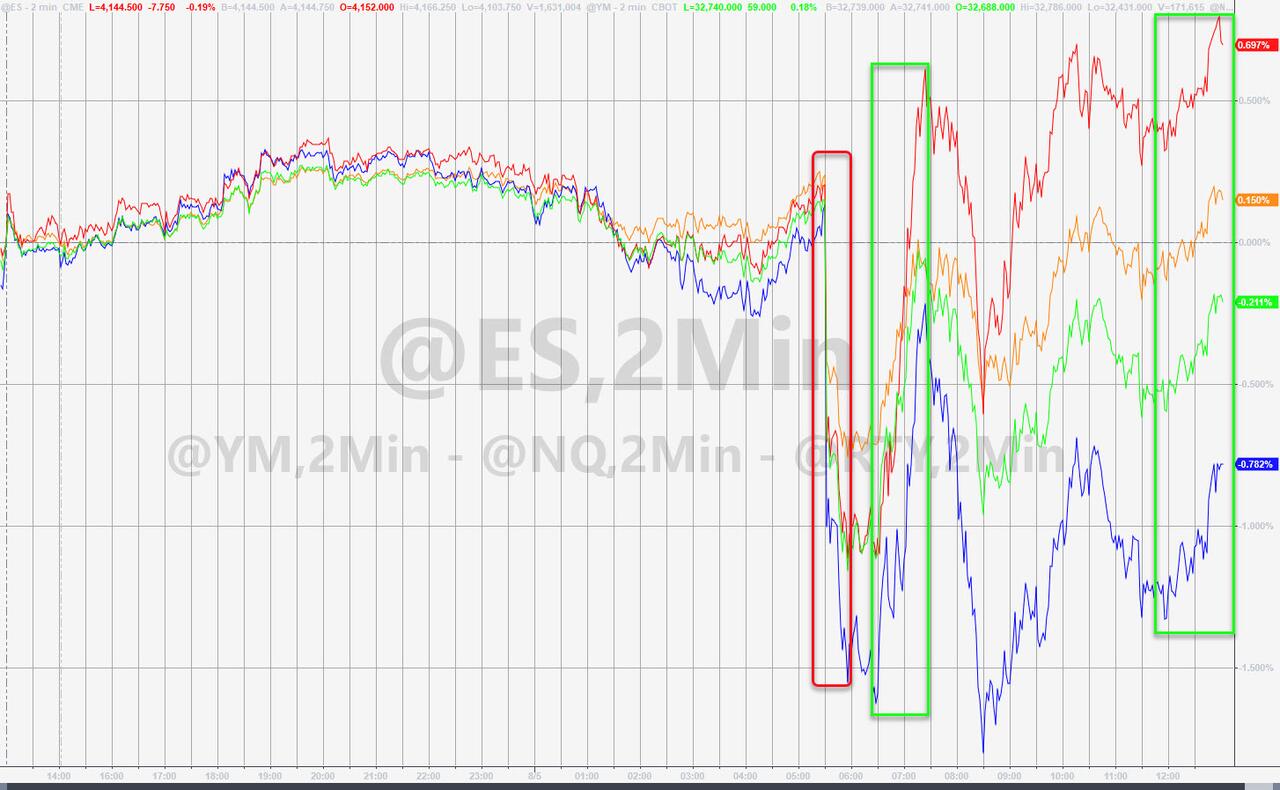

Markets are muted this morning with US equity futures paring back modest gains, ahead of the much-anticipated US jobs report later Friday. S&P 500, Nasdaq 100 and Dow Jones futures are little changed as sentiment gets hit after China imposed sanctions against Pelosi and would halt military talks with the US over Pelosi trip, while European stocks slipped after a stronger Asian session. The Nasdaq has stopped just short of a 20% rebound from its June low that would meet the technical definition of a bull market. The dollar and Treasuries were steady. Oil and gold slipped and Bitcoin recouped much of yesterday’s losses.

In premarket trading, US-listed Chinese stocks slipped after China said it would cancel climate and military talks with US, as part of a countermeasure package following House Speaker Nancy Pelosi’s trip to Taiwan. Among Chinese internet stocks lower were Alibaba -3.3% as investors continue to digest earnings; Nio -1%, Baidu -0.8%, Pinduoduo -2%, JD.com -1.9%, NetEase -1.8%, Li Auto -1.5%, XPeng -1.8%, Bilibili -1.6%. Here are some of the biggest U.S. premarket movers today:

Warner BrosDiscovery (WBD US) shares slump 11% in premarket trading after the media company reported a net loss and sales for the second quarter that missed the average analyst estimate. The recently merged media giant recorded about $4 billion in charges related to the deal, including amortization and restructuring expenses, wiping out profits.

Virgin Galactic (SPCE US) shares tumbled 13% in premarket trading after the space tourism company announced another delay to the launch of their commercial service, pushing it back to the second quarter of 2023.

Amgen (AMGN US) delivered a solid set of results and the biotech giant’s acquisition of autoimmune disease drug maker Chemocentryx looks to make sense, analysts say.

Kellogg (K US) raised to neutral from underweight at Piper Sandler with the broker saying a “way-too-early” sum-of-the-parts assessment of the cereal giant ahead of its planned split suggests it is fairly valued.

Block (SQ US) shares fall 6.5% in premarket trading after gross payment volume for the second quarter missed the average analyst estimate. Analysts noted signs of slowdown in the Cash App business in July.

Yelp (YELP US) boosted its full-year outlook on the back of better-than-expected 2Q sales, adjusted Ebitda and margin, prompting Evercore ISI and Baird to raise price targets. Analysts say the online review company’s new products are bearing fruit, with demand from advertisers still robust despite macro risks.

DoorDash (DASH US) shares jumped 13% in premarket trading, after the food delivery company reported stronger-than-expected second-quarter results. Analysts were optimistic about the “stickiness” of the company’s product and noted that demand seems to be holding up despite inflationary and macro pressures.

Cloudflare (NET US) shares soared as much as 23% in US premarket trading as analysts hiked their targets on the software company, highlighting that the firm was able to keep growing in a tough macroeconomic environment. Cloudflare also boosted its revenue guidance for the full year.

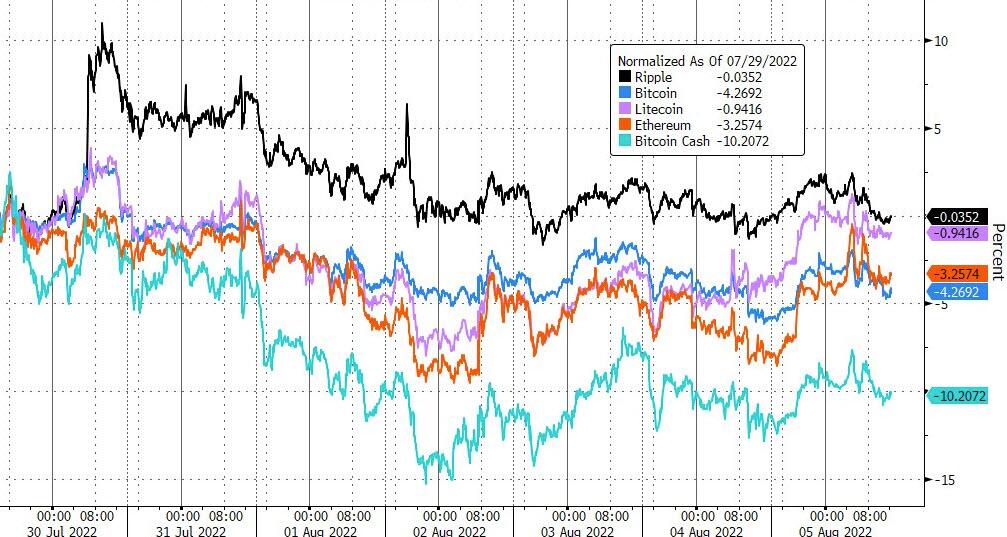

Cryptocurrency-exposed stocks are gaining in premarket trading after Bitcoin rose as much as 4% to trade above $23,000. On Thursday, BlackRock partnered with Coinbase to make it easier for institutional investors to manage and trade Bitcoin.

Doximity’s (DOCS US) guidance cut will provide fuel to bears on the online healthcare platform, analysts say. Shares in the firm fell 14% in after-hours trading on Thursday following its results.

Twilio (TWLO US) shares drop 7.9% in US premarket trading after the software firm’s guidance and margins disappointed, with questions over the latter metric ongoing, analysts say.

Ventas (VTR US) reported strong revenue growth in its second-quarter earnings, as expense pressure weighs on third-quarter guidance. Analysts retain a positive long-term outlook on the stock, as an aging population drives demand for Ventas’ senior housing portfolio. .

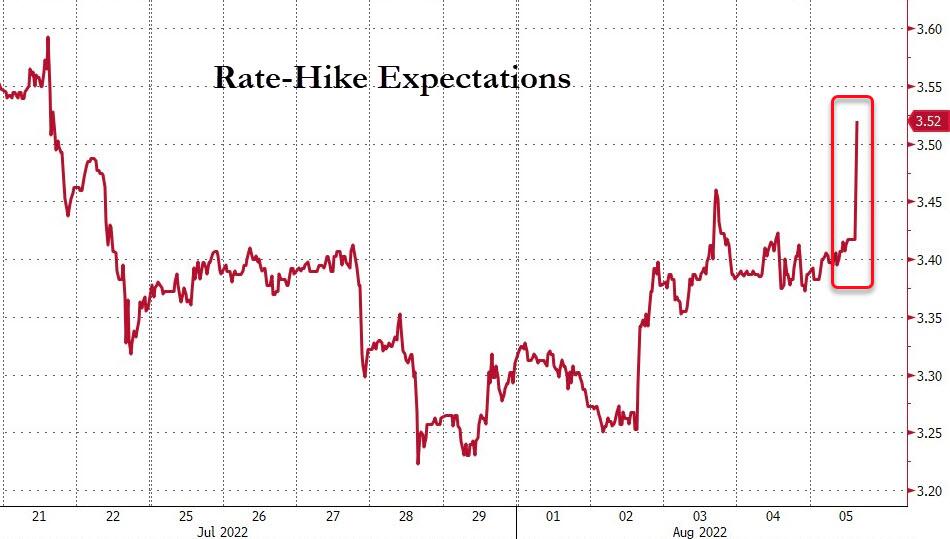

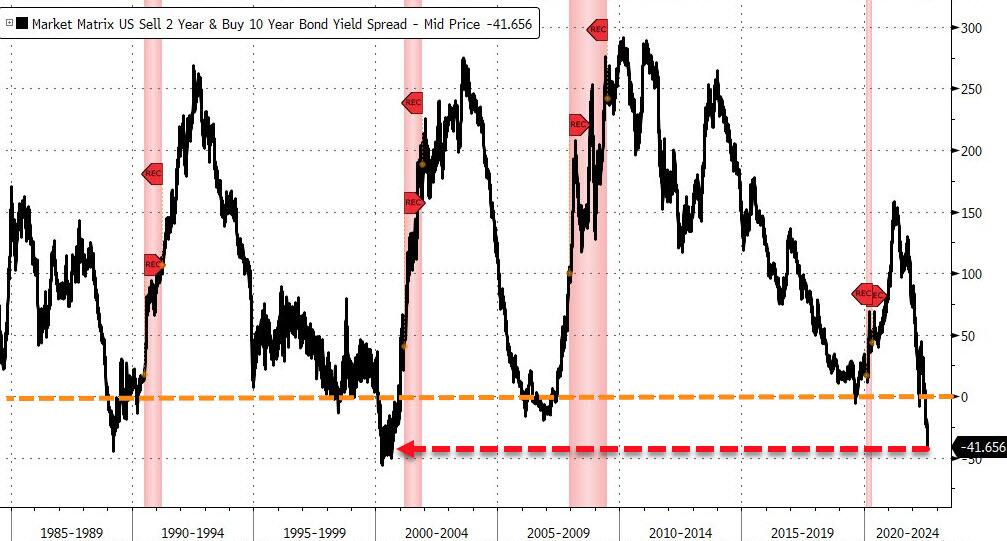

A global equity index is set for a third weekly advance and near a two-month peak in a recovery from bear-market lows, helped by resilient US company profits. The durability of the bounce remains in doubt as central banks around the world speed up rate hikes, and the inversion between two-year and 10-year yields remains near the deepest since 2000, harkening imminent recession.

The stock rally is being fed by speculation that runaway inflation may have peaked and the Fed can temper interest-rate increases. With US payrolls Friday data a closely-monitored Fed indicator, an above-expectation reading could provoke a negative reaction by traders because it would be seen as emboldening the US central bank to press on with outsized hikes.

“The equity market in the last month has managed to turn both hawkish and dovish data into a reason for cheer, which obviously is rather self-serving and unsustainable in the medium term,” said James Athey, investment director at Abrdn. “I would continue to be a seller of equity strength given my view that the path for the economy most certainly remains down.”

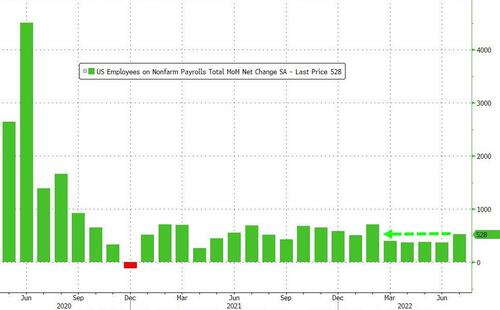

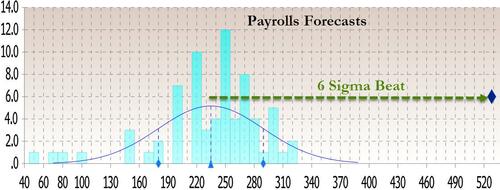

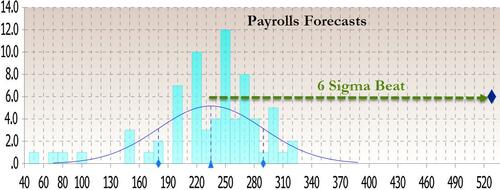

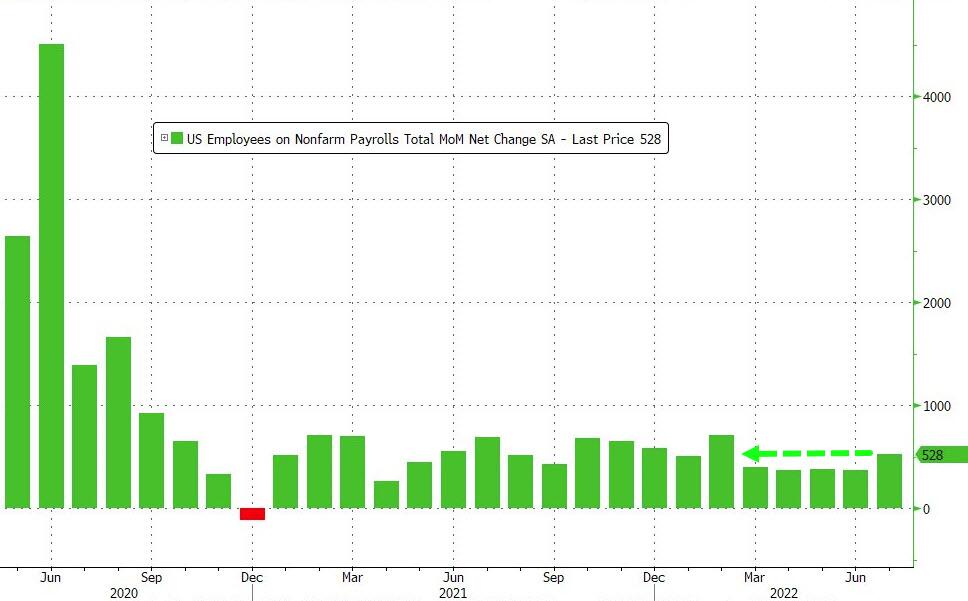

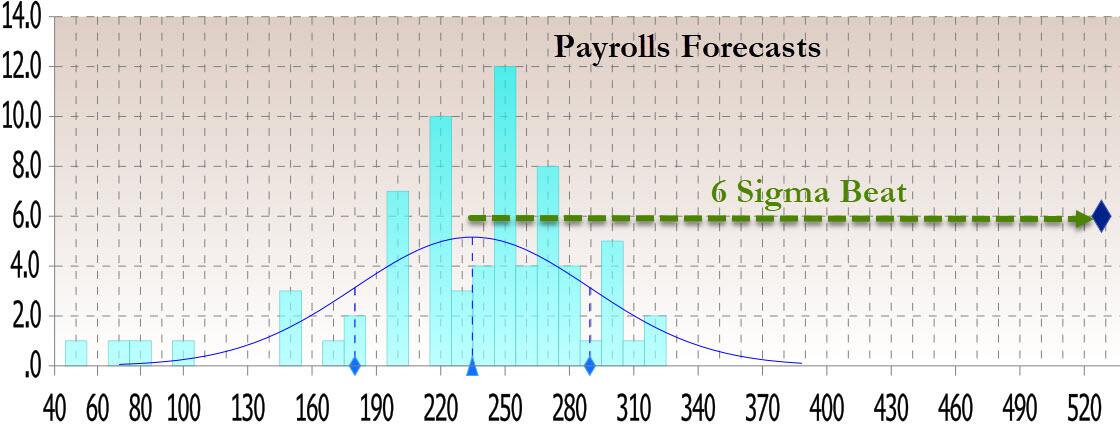

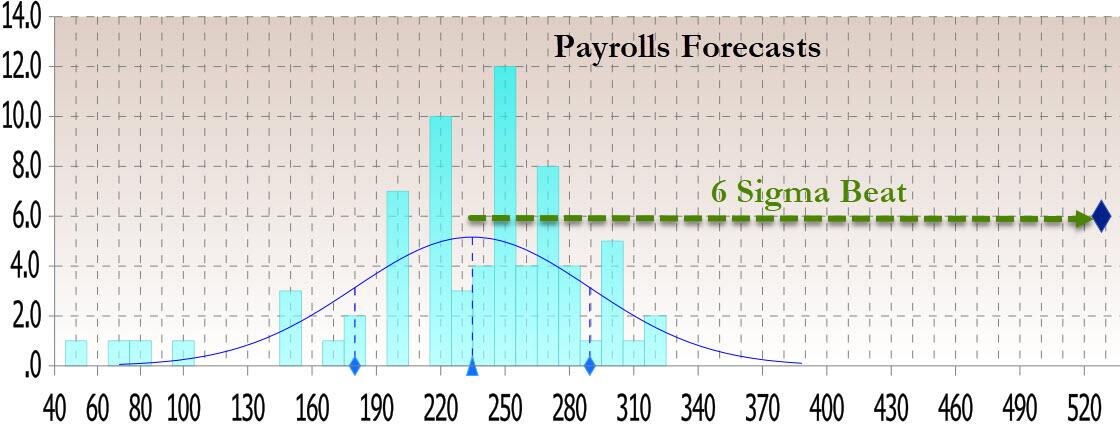

Looking at today’s main event, the July payrolls report at 8:30am ET is expected by economists to show job creation slowed from past year’s pace to 250k, with crowd- sourced whisper number currently 225k; unemployment rate expected to remain at 3.6%. Goldman goes even farther and predicts that a negative print would lead to a powerful stock rally: according to Goldman flow trader John Flood “we are firmly in a BAD is GOOD and vice versa tape right now.” He adds that whereas Goldman estimates a +225k headline print (vs +372 prior and +250k consensus). In this context:

The market “will get hit hard (-200bps) on a print north of 372k (>prior reading) as sooner than expected “fed pivot” convos will quickly be shelved.”

On the other hand, “a relatively inline print (150k – 300k) mkt wont react to as traders will sit on hands and wait for CPI.”

Finally, “if jobs are lost and we get a negative print, tape will rally 100+bps as FOMO/COVER chase will (remain) on w/ early 2023 rate cut discussions gaining more momentum.”

In Europe, the Stoxx 50 index fell 0.3%. DAX is flat but outperforms peers, CAC 40 lags, dropping 0.4%. Media, energy and consumer products are the worst-performing sectors. Here are the top European movers:

WPP shares fall as much as 7.3%, the most since May, despite the advertising agency raising full-year sales guidance. While the company surpassed consensus estimates on organic revenue growth in the first half, Goldman Sachs says the magnitude of the beat is smaller than peers.

London Stock Exchange shares rise as much as 2% to an almost four-month high, after the financial information company reported interim results and announced a £750m share buyback.

Hargreaves Lansdown shares gain as much as 5.7%, the most since March, as its reported pretax for the full year fell below analysts estimates.

Vestas Wind Systems rises as much as 5.5% after US Democratic senators agreed on a revised version of an ambitious tax and climate bill.

Pets at Home shares gain as much as 4% to the highest intraday since April 6, after the UK retailer reported 1Q like-for-like sales growth of 6%, beating RBC’s estimate of 3%.

Rheinmetall shares fall as much as 6.9% after the defense and auto manufacturer published 2Q earnings and confirmed its lowered FY sales outlook reported last week.

Deutsche Post rises as much as 6.5%, the most in more than four months, after the company reported Ebit in the second quarter that beat analysts estimates and confirmed its 2022 guidance.

Bpost shares rise as much as 9.2% to the highest level since Jan. 26 after what KBC says were a “very good set of result.”

Pirelli gains as much as 6.4%, the most intraday since March 9, after the tiremaker reported 2Q results ahead of expectations and raised its guidance for revenue and net cash generation, with Oddo BHF noting the new outlook should reassure.

Earlier in the session, Asian stocks rose, boosted by a rally in Taiwan and gains in the region’s technology shares. The MSCI Asia Pacific Index climbed as much as 0.9%, with TSMC and Sony among the biggest contributors to its advance. Tech was also the best-performing sector on the gauge, followed by materials. Taiwan’s equity benchmark was the biggest gainer in the region, jumping 2.3%. Semiconductor and shipping stocks climbed, helping the Taiwan Stock Exchange Weighted Index recoup all the losses fueled by US House Speaker Nancy Pelosi’s visit to the island earlier this week. That’s even as China likely fired missiles over Taiwan for the first time during its biggest military drills around the island in decades.

Investors will continue to assess the ongoing corporate-earnings season and the Fed’s monetary-tightening path. US payrolls data on Friday is the next key data point for global markets; Cleveland Federal Reserve Bank President Loretta Mester reiterated Thursday the US central bank’s determination to quell inflation. “A recession with the rising inflation rates is not going to be a constructive environment for the stock market. So I still regard this as a bear-market rally,” Jeffrey Halley, senior market analyst at Oanda Asia Pacific, said in an interview with Bloomberg TV. Stock gauges in Japan and South Korea also rose, helped by positive earnings reports. China’s Alibaba Group Holding Ltd. posted better results than many investors feared, avoiding a sharp sales contraction. Still, the stock slumped in Hong Kong after rallying for two days ahead of the earnings report.

Australia’s S&P/ASX 200 rose 0.6% to close at 7,015.60, driven by mining and health shares. The benchmark climbed for a third consecutive week, up 1%. Lithium stocks extended their rally on Friday as industry executives said they were inundated by bankers and brokers at the Diggers & Dealers Mining Forum this week, talking up deals to secure some of the estimated $42 billion worth of investment needed for metal producers to meet their goals. Meanwhile, Australia’s central bank lifted its inflation and wage growth forecasts while predicting unemployment will remain under 4% through mid-2024, underscoring the need for even tighter monetary policy. In New Zealand, the S&P/NZX 50 index fell 0.1% to 11,728.47.

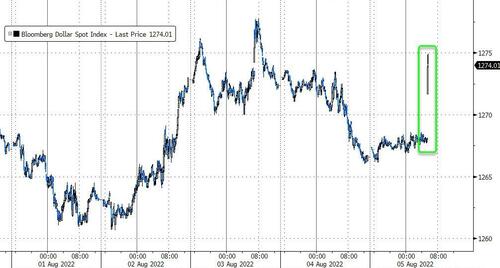

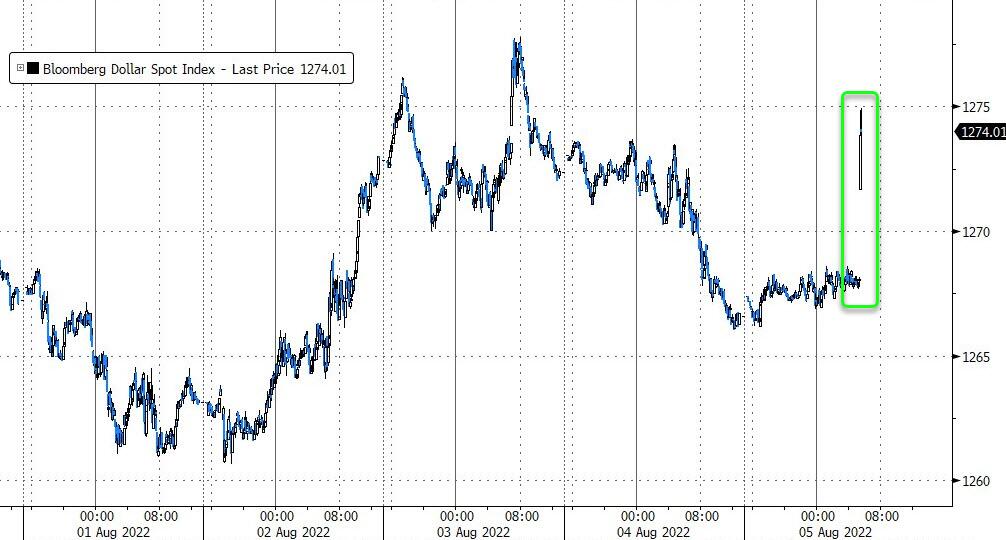

In FX, the Bloomberg Dollar Spot Index rose 0.1% in quiet trading, snapping a two-day decline. CHF and NZD are the strongest performers in G-10 FX, SEK and AUD underperform. The euro eased as much as 0.3% to 1.0219, weighed by weaker European share prices, while the yen slipped as traders unwound a recent streak of bullish bets on the currency

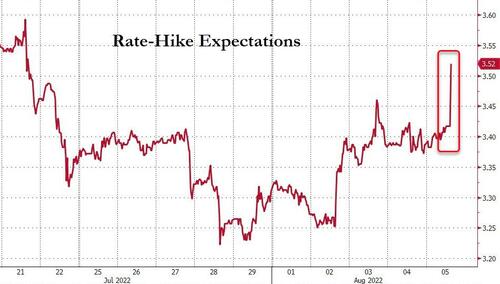

In rates, the Treasury yield curve was barely changed, with two-year yields rising 1.9 basis points higher to 3.06%. In Thursday’s US trading session two- and 10-year yields ended down 2 basis points while the 2s10s spread remained about 37.6bps in inversion. US yields are cheaper by as much as 2bp across front-end of the curve with spreads broadly within 1bp of Thursday’s closing levels; 10-year yields around 2.70%, cheaper by 1bp on the day and outperforming bunds and gilts by ~2bp each. European bonds eased, with the two-year German Schatz yield rising 2 basis points to 0.36%, while the 10-year Bund yield rose 3.1 basis points to 0.83%. Gilt curve bull-flattens with 2s10s widening 2.5bps after BOE’s Huw Pill cautioned against assuming a 50-bps hike in September. Short-end bunds decline, with the yield on the 2-year up about 2 bps.

WTI trades within Thursday’s range at around $88. Spot gold falls roughly $4 to trade at ~$1,787/oz. Most base metals trade in the green; LME nickel rises 1.8%, outperforming peers. LME lead lags, dropping 0.1%.

In today’s docket of economic data, the payrolls report in the US will be in the spotlight with June consumer credit out later in the day. In Europe, we will get June industrial production for Germany, France and Italy and Q2 private sector payrolls, wages and June trade balance for France. In central banks, speakers will include Fed’s Barkin and BoE’s Pill.

Market Snapshot

S&P 500 futures little changed at 4,154.00

STOXX Europe 600 down 0.2% to 438.32

MXAP up 0.8% to 161.72

MXAPJ up 0.9% to 527.30

Nikkei up 0.9% to 28,175.87

Topix up 0.9% to 1,947.17

Hang Seng Index up 0.1% to 20,201.94

Shanghai Composite up 1.2% to 3,227.03

Sensex up 0.2% to 58,442.88

Australia S&P/ASX 200 up 0.6% to 7,015.56

Kospi up 0.7% to 2,490.80

German 10Y yield little changed at 0.82%

Euro down 0.2% to $1.0227

Gold spot down 0.2% to $1,787.20

U.S. Dollar Index up 0.24% to 105.95

Top Overnight News from Bloomberg

Stocks in Europe and US equity futures struggled for direction as investors brace for the monthly US jobs report that’s likely to enliven the recession debate. The dollar rebounded from two days of declines.

China announced it would halt cooperation with the US in a number of areas following US House Speaker Nancy Pelosi’s trip to the US, including working-level talks on climate change and defense.

Bond giant Pacific Investment Management Co. saw outside clients pull money for a second straight quarter amid a global bond selloff.

Investors have resumed shunning global stocks in favor of bonds, according to Bank of America Corp. strategists, who say the time is right to step back from US equities after the strong rally in July.

German power prices rose to a record as utilities are increasingly reducing electricity output in western Europe because of the hot weather.

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks traded mostly positive but with gains capped amid geopolitical and growth slowdown concerns, while markets also await the upcoming US NFP jobs report. ASX 200 was lifted by strength in mining stocks after gains in underlying metal prices although the energy sector lagged due to the recent oil pressure. Nikkei 225 surpassed 28k after stronger-than-expected Household Spending and firmer wage growth. Hang Seng and Shanghai Comp lacked firm direction with Hong Kong stocks indecisive after Alibaba failed to replicate the strength in its ADRs post-earnings and with sentiment clouded by geopolitical risks

Top Asian News

Hong Kong to Announce Hotel Quarantine Cut as Soon as Monday

Japan’s Kishida to Reshuffle Cabinet as Soon as Aug. 10: NHK

Seazen Says It’s Wired Funds for $200m Dollar Bond Due Aug. 8

Indonesia’s GDP Surprise May Not Be Enough to Sway BI to Hike

SpaceX Rocket Launches South Korea’s First Mission to the Moon

Copper and Zinc Push Higher on Tightening Supply Backdrops

European bourses are under modest pressure in wake of China taking countermeasures against “Pelosi’s invasion of Taiwan”, Euro Stoxx 50 -0.4%. However, as we await the key US Labour Market print (newsquawkperformance is fairly contained overall preview available) before next week’s CPI. Currently US futures are lower by circa. 0.1% in narrow ranges amid thin summer conditions and a limited European schedule.

Top European News

German Power Climbs to Record as Plants Start to Buckle in Heat

UK House Prices Fall for First Time in a Year as Crisis Bites

Solvency II Plans Open Door to UK Insurance Buyback Bonanza

Italian Industry Output Slumps as Election Uncertainty Mounts

Vestas Surges as US Tax and Climate Bill Passes Major Hurdle

WPP Shares Drop After Outlook Upgrade Fails to Live up to Peers

FX

DXY trades on a firmer footing and tested 106.00 as China announced sanctions against House Speaker Pelosi; CNH saw some weakness.

EUR and GBP are posting mild losses vs the Buck, but the EUR sees slightly more of a downside bias vs the GBP

Activity currencies hold a mild downside against the Buck, with more pronounced losses seen as reports of Chinese sanctions against Pelosi dented sentiment.

Haven FX have climbed up the G10 ranks following the deterioration in sentiment.

Fixed Income

Pre-BoE core consolidation has dissipated and the flattening bias is back in play, albeit, only incrementally so with NFP ahead.

Bunds are towards the mid point of a relatively contained 60 tick range which is capped by nearby support/resistance.

OATs are in-fitting directionally but at the lower-end of ranges ahead of Fitch’s review of France; currently, AA Negative

Commodities

Crude benchmarks are under pressure amid the mentioned countermeasures taken by China and also as Taiwan reports no/limited ships/aircraft impact from China drills

WTI and Brent lower by circa. USD 0.20/bbl and towards the bottom-end of the session’s parameters.

China’s market regulator recently carried out investigations in Shanxi, Inner Mongolia and Shaanxi, 3 major coal-producing provinces, to further supervise and regulate thermal coal prices. 18 coal companies were suspected of bidding up coal prices, accord.

Spot gold is softer and incrementally losing its allure as the USD picks up while remain mixed

US Event Calendar

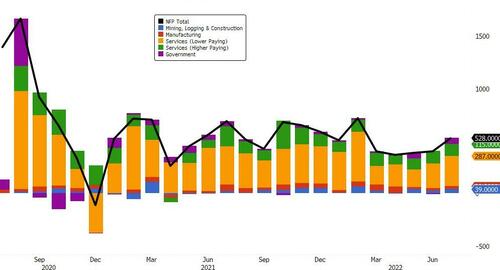

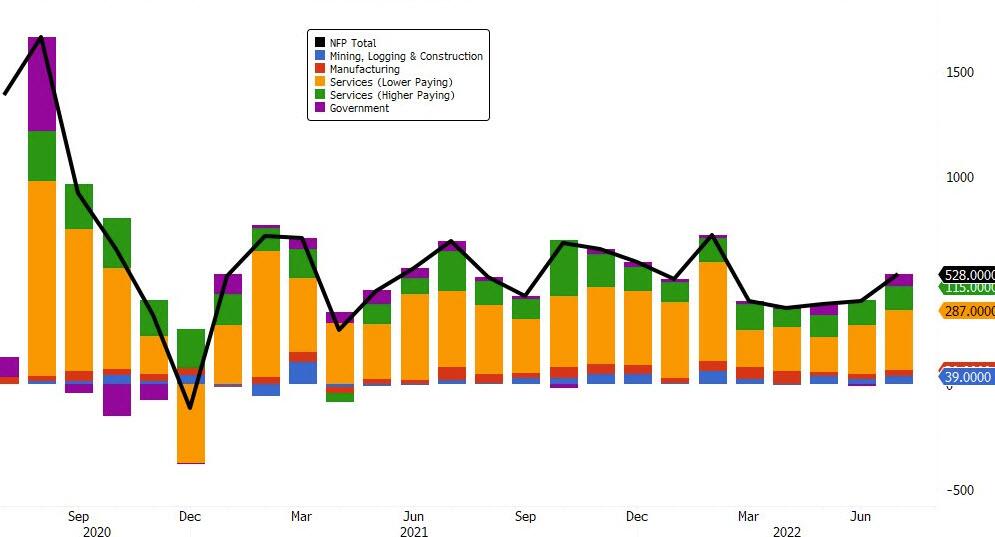

08:30: July Change in Nonfarm Payrolls, est. 250,000, prior 372,000

Change in Private Payrolls, est. 230,000, prior 381,000

Change in Manufact. Payrolls, est. 20,000, prior 29,000

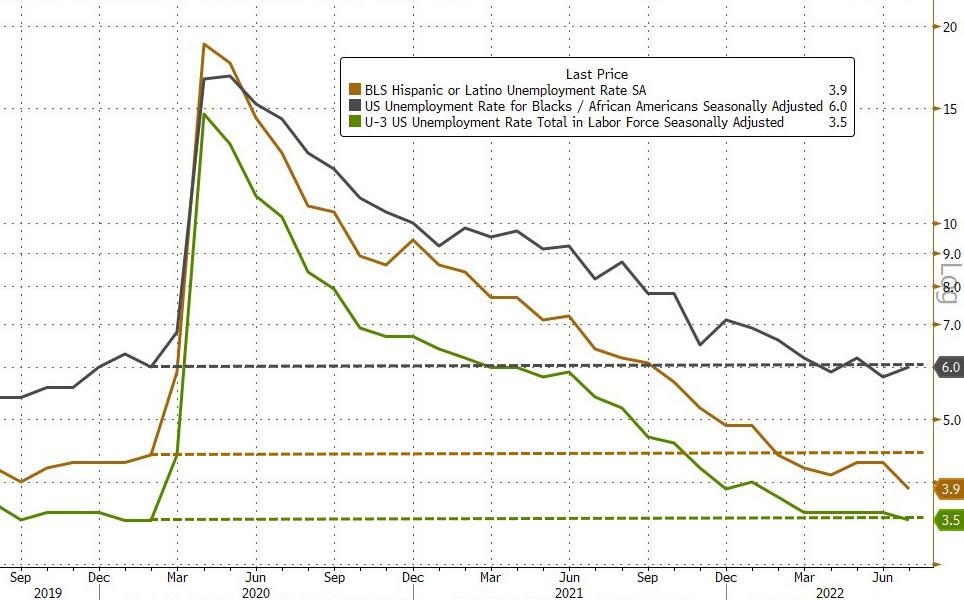

July Unemployment Rate, est. 3.6%, prior 3.6%

Underemployment Rate, prior 6.7%

Labor Force Participation Rate, est. 62.2%, prior 62.2%

Average Hourly Earnings MoM, est. 0.3%, prior 0.3%; Average Hourly Earnings YoY, est. 4.9%, prior 5.1%

July Average Weekly Hours All Emplo, est. 34.5, prior 34.5

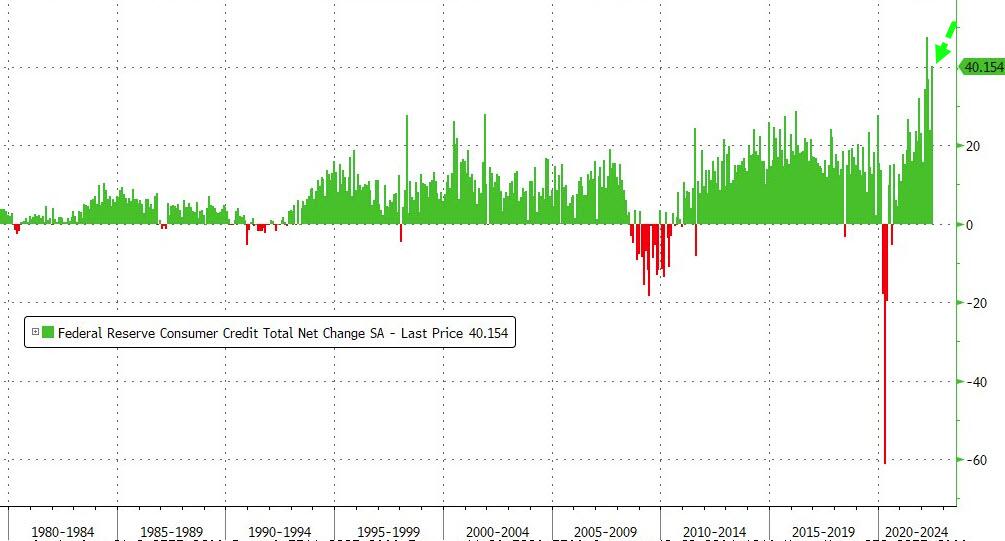

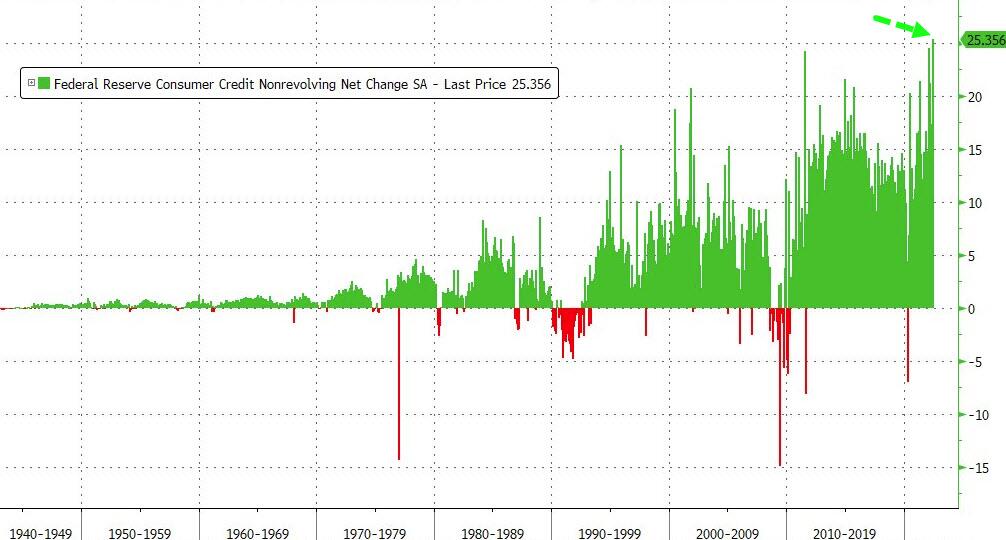

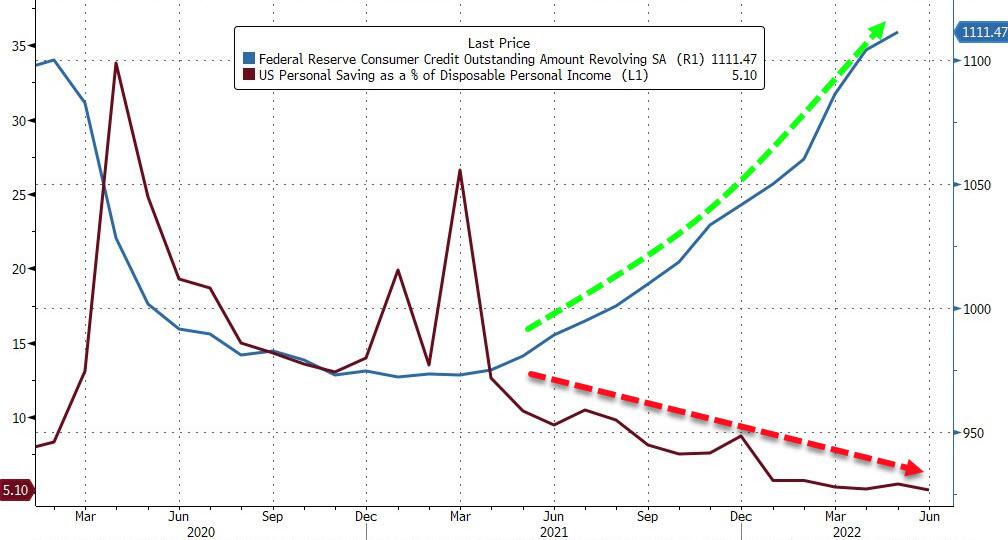

15:00: June Consumer Credit, est. $27b, prior $22.3b

DB’s Jim Reid concludes the overnight wrap

Welcome to another payrolls Friday which after a week of better US data on balance, probably isn’t set up with the market as worried as it could have been. There will be some concerns that continuing claims picked up last week (as released yesterday) but it’s fair to say the market is probably going into today’s print less worried about it than it was at the start of the week.

Yesterday was in truth the dullest day of the month so far after three action packed days even with a well flagged 50bps hike, but with a five quarter recession call, from the BoE being the obvious highlight.

US yields did rally across the curve but the moves were much smaller than we’ve seen earlier this week. The 2yr (-2.2bps) eased a touch more than the 10yr (-1.7bps). This came alongside hawkish comments from Cleveland Fed’s President Mester who stuck with her preference for rates to get above 4%, but now potentially preferring to frontload the hikes relative to her view in June’s summary of economic projections. The next edition is due at the September FOMC.

It was a mixed-bag day for the S&P 500 (-0.08%). Energy (-3.60%) continued to be the worst performing sector amid gloom in oil, with WTI losing -2.78% and trading below $90 per barrel and Brent (-3.25%) also down, but it was among 3 other sectors to finish the day lower including staples (-0.79%) and healthcare (-0.49%), while discretionary (+0.54%) and IT (+0.42%) drove the index higher as earnings took over given the lack of a significant macro driver.

Earnings also largely pulled the Nasdaq (+0.41%) ahead of other benchmarks as well, as the Dow Jones declined by -0.26%. Alibaba’s (+1.88%) revenue beat and a fairly optimistic take on consumer trends earlier in the session helped. Other notable movements on the day included Coinbase (+10%), which surged after news it is to partner with BlackRock to improve Bitcoin trading for institutions. But with 423 members of the S&P 500 now reported earnings for this season, the results-driven stories may fade in the coming days.

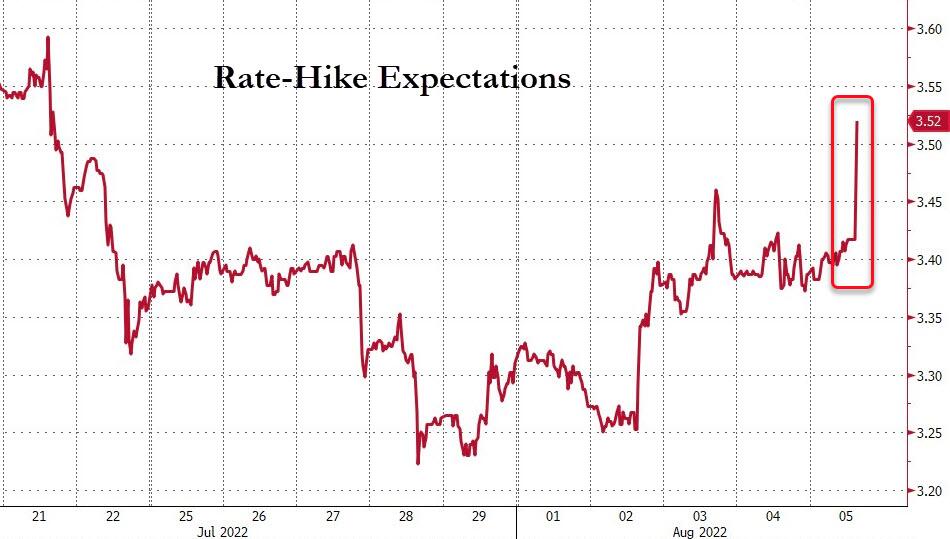

As mentioned at the top there was some disappointment from the claims numbers in the US which impacted sentiment a touch. While initial claims came in line with the median Bloomberg estimate of 260k, the upside surprise in continuing claims (1416k vs 1385k expected) were notable and remember that our US economists have pointed out that this series is a better gauge when it comes to forecasting imminent recessions. This fly in the job’s market soup comes after several Fed speakers have highlighted the continued tightness in the labour market this week, and with the ISM employment gauges surprising on the upside. So this puts today’s payrolls report solidly top of mind for markets from both a growth and monetary policy perspective. Our US economists expect a 250k print, down from 372k in June but enough to tip the unemployment rate lower to 3.5% from 3.6%. Consensus is also at 250k.

Some softness in yields and risk assets also started around the time of the BoE’s meeting yesterday that brought a fairly gloomy set of economic projections along with the widely expected +50bps hike, the largest since 1995, and a potential roadmap for active QT. Our UK economists review the meeting here and point to three key takeaways – inflation risks outweighed growth concerns, there is less reliance on medium-run projections and fairly unconstrained forward guidance. Our economics team continue to see +50bps in September and +25bps in November, marking a peak of 2.5% for the Bank Rate.

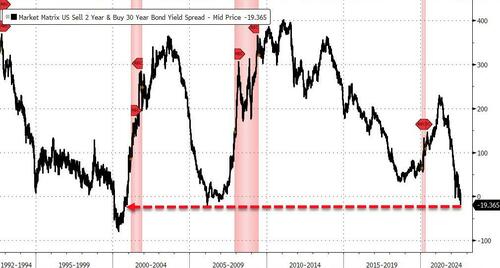

Briefly diving into the forecasts that dominated the headlines, the projections showed expectations of a prolonged contraction starting Q4 this year, with a -2.2% GDP decrease between then and Q2-24. So five quarters of recession predicted. What on earth would happen if the Fed predicted that? Inflation expectations also got a notable uptick of +200bps, and is now projected to peak at 13% in Q4 this year. While that was quite a mix for investors to digest, as our UK economists point out the Bank explicitly underscored it would assign less weight to more uncertain projections these days. That also further emphasises the importance of the next prime minister’s (results on September 5th) fiscal policy. 2s10s briefly inverted for the first time since 2019 as markets got on board with the recession story. The 2yr dropped by roughly -20bps from session’s highs at one point before closing only marginally lower (-0.5bps). The long end declined a bit more, with the 10y closing at -2.4bps, and the 2s10s finishing the day at 10bps, down -1.9bps. Nevertheless, breakevens surged by +6.2bps and the pound saw a U-turn from a nearly -1% loss in the aftermath of the meeting, recovering nearly to the level it held in early European trading.

The rest of major European bond markets also saw a rally for yields but more catching up to the late previous night US rally than anything else, with those for Bunds (-7.2bps), OATs (-8.6bps) and BTPs (-8.2bps) all lower. Falling yields supported equities in the region, as the STOXX 600 (+0.18%) was propelled by materials (+1.22%), helped by Glencore’s results, IT (+1.07%) and discretionary (+0.96%) stocks. Energy (-1.34%) and real estate (-1.18%) were the main outliers on the downside and 66% of index’s members finished the day higher.

Over in Asia, stock markets are trading higher this morning as markets appear to be unfazed by China’s military drills around Taiwan. As I type, the Kospi (+0.81%) is leading gains in early trade with the Nikkei (+0.71%) not far behind. Elsewhere, the Shanghai Composite (+0.28%) and the CSI (+0.37%) are also in positive territory whilst the Hang Seng (+0.06%) is swinging between gains and losses. Meanwhile, oil futures are slightly higher and reversing earlier losses as we go to print.

Looking ahead, equity futures in the US point to further gains with contracts on the S&P 500 (+0.24%), and the NASDAQ 100 (+0.30%) higher.

Early morning data showed that Japan’s household spending (+3.5% y/y) increased for the first time in four months in June (v/s +1.5% expected) and compared to a -0.5% decline in May. Separate data showed that real wages in Japan (-0.4% y/y) slipped for the third straight month in June (v/s -1.3% expected) as consumer prices advanced faster than nominal wages (+2.2% y/y, +1.9% consensus) which recorded its strongest growth in four years.

Elsewhere, the Reserve Bank of Australia (RBA) in its monetary statement this morning upgraded its inflation and wage growth forecasts while predicting the nation’s unemployment rate would fall further by the end of this year. The central bank in its statement revealed that it sees headline inflation reaching 7.75% by the end of 2022 and assumes the key interest rate will reach 3% by December from 1.85% at present and then “decline a little” by end-2024. Additionally, it estimates the jobless rate will reach 3.25% from the 3.75% forecasted earlier in May.

In today’s docket of economic data, the payrolls report in the US will be in the spotlight with June consumer credit out later in the day. In Europe, we will get June industrial production for Germany, France and Italy and Q2 private sector payrolls, wages and June trade balance for France. In central banks, speakers will include Fed’s Barkin and BoE’s Pill.

END

AND NOW NEWSQUAWK

Modest/fleeting risk-off amid China countermeasures pre-NFP – Newsquawk US Market Open

FRIDAY, AUG 05, 2022 – 06:54 AM

European bourses are under modest pressure in wake of China taking countermeasures against “Pelosi’s invasion of Taiwan”, Euro Stoxx 50 -0.4%.

However, performance is fairly contained overall as we await the key US Labour Market print (newsquawk preview available) before next week’s CPI.

DXY is firmer on the China update with activity currencies pressured and havens deriving modest upside.

Core debt is relatively steady with a modest flattening bias back in play; OATs in focus ahead of Fitch’s review

Crude benchmarks are under pressure amid the mentioned countermeasures taken by China and also as Taiwan reports no/limited ships/aircraft impact from China drills

Looking ahead, highlights include US & Canadian Labour Market Reports; BoE’s Pill & Fed’s Barkin.

As of 11:25BST/06:25ET

For the full report and more content like this check out Newsquawk.

Try a 14 day trial with Newsquawk and hear breaking trading news as it happens.

LOOKING AHEAD

US & Canadian Labour Market Reports; BoE’s Pill & Fed’s Barkin.

Ukraine is calling for the Black Sea grain deal to extend to other products, according to FT; subsequently, Russian Kremlin says a solution to the problems, in reference to Turkey’s proposed extension of a grain deal to metals, can only be attained if it is linked to the removal of restrictions on Russian metal producers, via Reuters.

TAIWAN

Chinese Foreign Ministry says it will sanction US House Speaker Pelosi over her visit to Taiwan; adding that, Pelosi’s Taiwan visit seriously interfered with China’s internal affairs and trampled on the One-China principle.

Chinese Foreign Ministry says it will take more counter-measures over House Speaker Pelosi’s trip to Taiwan. China announces eight measures, click here for details.

Taiwanese Transportation Ministry says no ships altered plans to enter or leave ports on Thursday and there is little impact on airport traffic following Chinese military drills, via Reuters.

US House Speaker Pelosi said they had positive meetings in Taiwan about security and governance and that they said from the start that representation is not about changing the status quo, while she added that China will not isolate Taiwan by preventing them from travelling there, according to Reuters.

White House’s Kirby said the US urges China not to overreact and to bring down tensions, while the US is watching China’s exercises near Japan ‘very, very closely’. Kirby also said the US condemns China launching missiles near Taiwan and expects China to continue to react in the coming days, while he added the US is prepared and that Beijing’s actions are a significant escalation in its attempt to change the status quo.

Taiwan’s Premier said the “evil neighbour” next door is showing off her power at our door and that China is arbitrarily destroying the world’s most frequently used waterway with military drills, while Taiwan’s Premier added that China’s actions are being condemned by the world.

Taiwan’s Defence Ministry said multiple Chinese navy ships and air force aircraft crossed the Taiwan Strait median line on Friday morning, while it added China’s actions are provocative and that the military principle is ‘no escalation, no triggering of incident’, according to Reuters.

Around 20 Chinese military aircraft briefly cross the Taiwan median line on Friday morning, according to a Taiwan source via Reuters.

White House summoned the Chinese ambassador yesterday to condemn the nation for escalating actions against Taiwan following the visit by House Speaker Pelosi, according to the Washington Post,

OTHER

North Korea tested explosive devices and began digging new tunnels at its Punggye-ri nuclear test site, which “paves the way for additional nuclear tests” according to Nikkei citing a UN draft report.

“There has been no discussion in Vienna between IAEA and Iran this week. And that none planned at this point”, according to WSJ’s Norman citing sources.

EUROPEAN TRADE

EQUITIES

European bourses are under modest pressure in wake of China taking countermeasures against “Pelosi’s invasion of Taiwan”, Euro Stoxx 50 -0.4%.

However, performance is fairly contained overall as we await the key US Labour Market print (newsquawk preview available) before next week’s CPI.

Currently, US futures lower by circa. 0.1% in narrow ranges amid thin summer conditions and a limited European schedule.

DXY trades on a firmer footing and tested 106.00 as China announced sanctions against House Speaker Pelosi; CNH saw some weakness.

EUR and GBP are posting mild losses vs the Buck, but the EUR sees slightly more of a downside bias vs the GBP.

Activity currencies hold a mild downside against the Buck, with more pronounced losses seen as reports of Chinese sanctions against Pelosi dented sentiment.

Haven FX have climbed up the G10 ranks following the deterioration in sentiment.

Crude benchmarks are under pressure amid the mentioned countermeasures taken by China and also as Taiwan reports no/limited ships/aircraft impact from China drills

WTI and Brent lower by circa. USD 0.20/bbl and towards the bottom-end of the session’s parameters.

China’s market regulator recently carried out investigations in Shanxi, Inner Mongolia and Shaanxi, 3 major coal-producing provinces, to further supervise and regulate thermal coal prices. 18 coal companies were suspected of bidding up coal prices, accord.

Spot gold is softer and incrementally losing its allure as the USD picks up while base metals remain mixed.

BoE Chief Economist Pill says the MPC is targeting the more persistent elements of inflation, BoE is aiming to be flexible and should not assume that September will be a 50bps hike. If inflation returns to 2%, nominal rates will be broadly at that level, via BBG TV.

NOTABLE US HEADLINES

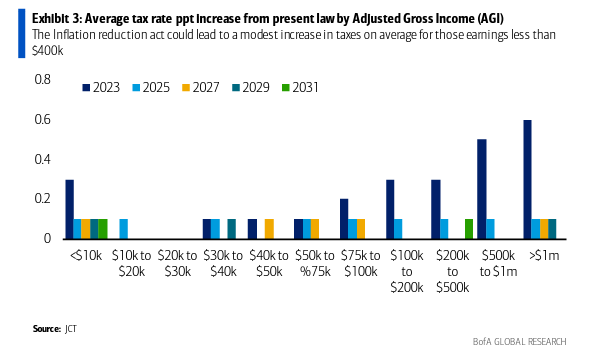

US Senator Sinema agreed to move forward on Senate tax and climate bill in which she agreed to remove the carried interest tax provision, protect manufacturing and boost the clean energy economy in the Senate’s budget reconciliation legislation. Furthermore, Senate Majority Leader Schumer said the final version of the reconciliation bill will be published on Saturday and that the agreement preserves major components of the inflation reduction act.

Bitcoin is firmer and once again back above the USD 23k mark in what has been a fairly choppy week within narrow ranges of less than USD 2k thus far.

APAC TRADE

APAC stocks traded mostly positive but with gains capped amid geopolitical and growth slowdown concerns, while markets also await the upcoming US NFP jobs report.

ASX 200 was lifted by strength in mining stocks after gains in underlying metal prices although the energy sector lagged due to the recent oil pressure.

Nikkei 225 surpassed 28k after stronger-than-expected Household Spending and firmer wage growth.

Hang Seng and Shanghai Comp lacked firm direction with Hong Kong stocks indecisive after Alibaba failed to replicate the strength in its ADRs post-earnings and with sentiment clouded by geopolitical risks.

NOTABLE APAC HEADLINES

Chinese Premier Li said China can ‘live with’ slightly lower growth if inflation remains below 3.5%, according to SCMP

ASEAN Foreign Ministers’ communique stated that they underscored the importance of maintaining unity and centrality, while they reaffirmed shared commitment to maintaining and promoting peace, security and stability in the region. They also reiterated their commitment to keeping markets open for trade and investment, as well as refraining from imposing unnecessary non-tariff measures to ensure supply chain connectivity.