Uncategorized · Leave a comment·Edit

GOLD; $1782.85.30 DOWN $16.45

SILVER: $20.35 DOWN 38 CENTS

ACCESS MARKET:

GOLD $1779.50

SILVER: $20.31

Bitcoin morning price: $24,225 UP 59

Bitcoin: afternoon price: $24,070. DOWN 155

Platinum price closing DOWN $23.40 AT$938.25

Palladium price; closing DOWN $72.60 at $2154.80

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: AUGUST 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,798.600000000 USD

INTENT DATE: 08/12/2022 DELIVERY DATE: 08/16/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 333 10

072 H GOLDMAN 27

104 C MIZUHO 7

118 C MACQUARIE FUT 60

132 C SG AMERICAS 81

167 C MAREX 6

190 H BMO CAPITAL 6

323 H HSBC 1

624 H BOFA SECURITIES 58

657 C MORGAN STANLEY 14

661 C JP MORGAN 140

661 H JP MORGAN 2

685 C RJ OBRIEN 9

686 C STONEX FINANCIA 1

690 C ABN AMRO 5

737 C ADVANTAGE 6 4

800 C MAREX SPEC 30 11

880 C CITIGROUP 25 3

880 H CITIGROUP 24

905 C ADM 19

TOTAL: 441 441

MONTH TO DATE: 32,466

JPMorgan stopped: 140/441

_____________________________________________________________________________________

GOLD: NUMBER OF NOTICES FILED FOR AUGUST CONTRACT:

441 NOTICES FOR 44,100 OZ //1.3716 TONNES

total notices so far: 32,466 contracts for 3,24,6600 oz (100.982 tonnes)

SILVER NOTICES:

0 NOTICES FILED FOR 0 OZ/

total number of notices filed so far this month 827 : for 4,135,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $16.45

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD.

INVENTORY RESTS AT 995.97 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN $0.38 CENTS

AT THE SLV// ://A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 1.152 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 486.219 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GOOD SIZED 641 CONTRACTS TO 148,006 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE HUMONGOUS GAIN IN OI WAS ACCOMPLISHED DESPITE OUR $0.46 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.46) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY COMMERCIAL SILVER LONGS//. HOWEVER WE CONTINUE TO HAVE SOME SPECULATOR LIQUIDATIONS AS WE HAD A GIGANTIC GAIN OF 5557 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT LIQUIDATIONS//HUGE BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A FAIR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 35,000 OZ QUEUE JUMP / // V) FAIR SIZED COMEX OI LOSS/(//HUGE SPEC LIQUIDATION)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -22

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTACTS for 11 days, total 6286 contracts: 31.430 million oz OR 2.857 MILLION OZ PER DAY. (623 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 31.43 MILLION OZ

.

LAST 16 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 31.43 MILLION OZ (A LOT LESS THAN NORMAL//THE CROOKS ARE SCARED TO ISSUE MORE EFP’S)

RESULT: WE HAD A GOOD SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 604 DESPITE OUR $0.34 GAIN IN SILVER PRICING AT THE COMEX// FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE CONTRACTS: 300 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER ADDITIONS AND SPEC SHORT LIQUIDATIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 35,000 OZ QUEUE JUMP // .. WE HAD A SMALL SIZED LOSS OF 341 OI CONTRACTS ON THE TWO EXCHANGES FOR 1.705 MILLION OZ AS..THE SPECS STILL BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 0 NOTICE(S) FILED TODAY FOR 0 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 951 CONTRACTS TO 458,923 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: — 272 CONTRACTS.

.

THE SMALL SIZED INCREASE IN COMEX OI CAME WITH OUR RISE IN PRICE OF $7.65//COMEX GOLD TRADING/FRIDAY / WE MUST HAVE HAD ADDITIONAL SPECULATOR SHORT SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND STRONG SPECULATOR SHORT COVERINGS//STRONG ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR AUGUST AT 98.367 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 11,400 OZ//NEW STANDING 103.390 TONNES

YET ALL OF..THIS HAPPENED WITH OUR RISE IN PRICE OF $7.65 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 3812 OI CONTRACTS 11.852 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2861 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 458,933

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3812 CONTRACTS WITH 951 CONTRACTS INCREASED AT THE COMEX AND 2861 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 4084 CONTRACTS OR 112.702 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2861) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (951): TOTAL GAIN IN THE TWO EXCHANGES 3812 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERINGS//GOOD BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR AUGUST. AT 99.272 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 11,400 oz. 3) ZERO/ LONG LIQUIDATION//// //.,4) SMALL SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST :

26,206 CONTRACTS OR 2,620,600 OZ OR 81.51 TONNES 11 TRADING DAY(S) AND THUS AVERAGING: 2382 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAY(S) IN TONNES: 81.51 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 81.51/3550 x 100% TONNES 2.29% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 81.51 TONNES (DRAMATICALLY FALLING AGAIN)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF SEPT., FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A GOOD SIZED 641 CONTRACT OI TO 148,006 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 300 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 300 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 300 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 604 CONTRACTS AND ADD TO THE 50 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED LOSS OF 341 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 1.705 MILLION OZ

OCCURRED DESPITE OUR RISE IN PRICE OF $0.34

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)MONDAY MORNING// SUNDAY NIGHT

SHANGHAI CLOSED DOWN 0.80 PTS OR 0.02% //Hang Sang CLOSED DOWN 134.76 OR 0.67% /The Nikkei closed UP 324.80 OR % 1.14. //Australia’s all ordinaires CLOSED UP 0.48% /Chinese yuan (ONSHORE) closed DOWN AT 6.7701//OFFSHORE CHINESE YUAN DOWN 6.7842// /Oil DOWN TO 87.62 dollars per barrel for WTI and BRENT AT 93.18// / Stocks in Europe OPENED ALL MIXED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 951 CONTRACTS TO 458,923 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR RISE OF $7.65 IN GOLD PRICING FRIDAY’S COMEX TRADING. WE ALSO HAD A GOOD SIZED EFP (3822 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF AUGUST.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2861 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :2861 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2861 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED SIZED TOTAL OF 3812 CONTRACTS IN THAT 2861 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED COMEX OI GAIN OF 3812 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR RISE IN PRICE OF GOLD $ 7.65. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING AUGUST (103.390),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:103.390 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $7.65) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS // COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO COVER TO THEIR POSITIONS////// WE HAVE REGISTERED A GOOD SIZED GAIN OF 11.852 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR AUGUST (103.390 TONNES)…

WE HAD –272 CONTRACTS ADDED TO COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3812 CONTRACTS OR 381,200 OZ OR 11.852 TONNES

Estimated gold volume 134,871/// poor/

final gold volumes/yesterday 127,304/ poor

INITIAL STANDINGS FOR AUGUST ’22 COMEX GOLD //AUGUST 15

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 315,983.595 oz Brinks JPMorgan Malca 519 kilobars Manfra |

| Deposit to the Dealer Inventory in oz | 32,118.849 OZ 999 kilobars |

| Deposits to the Customer Inventory, in oz | 32.151 oz Brinks 1 kilobar |

| No of oz served (contracts) today | 441 notice(s) 44,100 OZ 10.4199 TONNES |

| No of oz to be served (notices) | 776 contracts 77,600 oz 2.417 TONNES |

| Total monthly oz gold served (contracts) so far this month | 32,466 notices 3,246,600 OZ 99.611 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 1

Into Brinks 32,118.849 oz 999 kilobars

total dealer deposit: 32118.849 oz

No dealer withdrawals

Customer deposits: 1

i) Into Brinks 32.151 oz (1 kilobars)

total deposits:32.151 oz

3 customer withdrawals:

i) out of HSBC 20,445.673 oz

ii) Out of JPM: 17,509.972 oz

iii) Out of Malca: 166,863.690 oz (519 kilobars)

iv) Out of Manfra 111,164.240 oz

ii) Out of JPM ; 20,183.213oz

total: 315,983.595 oz

total in tonnes: 9.82 tonnes

Adjustments: dealer to customer //2

Malca 204.23 oz

Brinks 96.453 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 1217 contracts having LOST 3236 contracts .

We had 3350 notices served upon yesterday so we gained a STRONG 114 contracts or an additional 11,400 oz will stand for delivery in this very active month of August.

.As promised, from this point on, we will now add to the amount of gold standing at the comex until the end of the month.

Sept. LOST 101 contracts to 3627 contracts.

October LOST 163 contracts DOWN to 38,767

We had 441 notice(s) filed today for 44,100 oz FOR THE AUGUST 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 441 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 140 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2022. contract month,

we take the total number of notices filed so far for the month (32,466) x 100 oz , to which we add the difference between the open interest for the front month of (AUGUST 1217 CONTRACTS ) minus the number of notices served upon today 441 x 100 oz per contract equals 3,324,200 OZ OR 103.390 TONNES the number of TONNES standing in this active month of AUGUST.

thus the INITIAL standings for gold for the AUGUST contract month:

No of notices filed so far (32,466) x 100 oz+ (1217) OI for the front month minus the number of notices served upon today (441} x 100 oz} which equals 3,324,200 oz standing OR 103.042 TONNES in this active delivery month of August.

TOTAL COMEX GOLD STANDING: 103.390 TONNES (A HUGE STANDING FOR AUGUST ( ACTIVE) DELIVERY MONTH)

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,318,414,091 oz 72.11 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 29,000,953,997 OZ

TOTAL REGISTERED GOLD: 14,511,706.272 OZ (451,37 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 14,889,227.725 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 12,193,292.0 OZ (REG GOLD- PLEDGED GOLD) 379.26 tonnes//rapidly declining

END

SILVER/COMEX/AUGUST 15

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 763,184.978 oz CNT Delaware JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 211,181.774 oz Delaware |

| No of oz served today (contracts) | 0 CONTRACT(S) nil OZ) |

| No of oz to be served (notices) | 117 contracts (585,000 oz) |

| Total monthly oz silver served (contracts) | 827 contracts 4,135,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) Into Delaware 211,181.774 oz

total deposit: 211,181.774 oz

JPMorgan has a total silver weight: 173.985 million oz/332.856 million =52.26% of comex

Comex withdrawals: 3

i) out of CNT 164,525.588 oz

ii) Out of Delaware 2000.00 oz

iii) Out of JPMorgan: 596,659.3900 oz

total: 763,184.978 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 55.234 MILLION OZ

TOTAL REG + ELIG. 332.856 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR AUGUST

silver open interest data:

FRONT MONTH OF AUGUST OI: 117 CONTRACTS HAVING GAINED 5 CONTRACTS. WE HAD 2 NOTICES FILED ON THURSDAY

SO WE GAINED 7 CONTRACTS OR AN ADDITIONAL 35,000 OZ OF SILVER WILL STAND FOR DELIVERY. THE AMOUNT STANDING

WILL NOW INCREASE//(OR REMAIN CONSTANT) ON A DAILY BASIS AS BANKERS SCOUR THE PLANET FOR BADLY NEEDED SILVER.

SEPTEMBER HAD A LOSS OF 2647 CONTRACTS DOWN TO 66,022

OCTOBER GAINED 7 CONTRACTS TO STAND AT 97

CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes:60,079// est. volume today// good

Comex volume: confirmed yesterday: 53,206 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 827 x 5,000 oz = 4,135,000 oz

to which we add the difference between the open interest for the front month of AUGUST(117) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST./2022 contract month: 827 (notices served so far) x 5000 oz + OI for front month of AUGUST (117) – number of notices served upon today (0) x 5000 oz of silver standing for the AUGUST contract month equates 4,720,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

AUGUST 10//WITH GOLD UP $2.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES

AUGUST 9/WITH GOLD UP $6.70: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES.

AUGUST 8/WITH GOLD UP $13.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FORM THE GLD//INVENTORY RESTS AT 999.16 TONNES

AUGUST 5/WITH GOLD DOWN $14.25: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .33 TONNES FROM THE GLD////INVENTORY RESTS AT 1000.32 TONNES

AUGUST 4 WITH GOLD UP $29.00 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES FROM THE GLD///INVENTORY REST AT 1000.65 TONNES

AUGUST 2/WITH GOLD UP $3.70; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD//INVENTORY RESTS AT 1002.97 TONNES//

AUGUST 1/WITH GOLD UP $5.75: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 29//WITH GOLD UP $12.50; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1005.29 TONNES

JULY 28/WITH GOLD UP $31.25; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 27.//WITH GOLD UP $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 26/WITH GOLD DOWN $1.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.29 TONNES

JULY 25/WITH GOLD DOWN $7.85: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 1005.87 TONNES

JULY 22/WITH GOLD UP $17.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 21/WITH GOLD UP $11.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.101 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.87 TONNES

JULY 20/WITH GOLD DOWN $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1009.06 TONNES

JULY 19/WITH GOLD DOWN $.35 :BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.22 TONNES FROM THE GLD//INVENTORY RESTS AT 1009.06 TONNES

JULY 18/WITH GOLD UP $7.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.28 TONNES

JULY 15/WITH GOLD DOWN $3.75:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD///INVENTORY RESTS AT 1016.89 TONNES//

JULY 14/WITH GOLD DOWN $28.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD//INVENTORY RESTS AT 1019.79 TONNES

JULY 13/WITH GOLD UP $10.55:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD//INVENTORY RESTS AT 1021.53TONNES

JULY 12/WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESS AT 1023.27 TONNES

GLD INVENTORY: 995.97 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 10/WITH SILVER UP 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 9/WITH SILVER DOWN 25 CENTS TODAY: TWO CHANGES IN SILVER INVENTORY AT THE SLV: FIRST: A DEPOSIT OF 461,000 OZ INTO THE SLV AND THEN A WITHDRAWAL OF 1.014 MILLION OZ..//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 8/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 5/WITH SILVER DOWN 28 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 922,000 OZ FROM THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 4 WITH SILVER UP 21 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 527,000 OZ FROM THE SLV////INVENTORY RESTS AT 486.634 MILLION OZ

AUGUST 2/WITH SILVER DOWN 21 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.504 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.161 MILLION OZ//

AUGUST 1/WITH SILVER UP 17 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE GLD: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 483.657 MILLION OZ//

JULY 29/WITH SILVER UP 30 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 461,000 OZ FROM THE SLV..//INVENTORY RESTS AT 483.657 MILLION OZ/

JULY 28/WITH SILVER UP $1.24 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 484.118 MILLION OZ/

JULY 27/.WITH SILVER UP 4 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL 11.479 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 484.118MILLION OZ//

JULY 26/WITH SILVER UP 16 CENTS: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.504 MILLION OZ FROM THE SLV//: //INVENTORY RESTS AT 495.597 MILLION OZ//

JULY 25/WITH SILVER DOWN 24 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.383 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 499.101 MILLION OZ//

JULY 22/WITH SILVER DOWN 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 500.484 MILLION OZ//

JULY 21/WITH SILVER UP 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.19 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 500.484MILLION OZ/

JULY 20/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 8.253 MILLION OZ FORM THE SLV/INVENTORY RESTS AT 507.585 MILLION OZ//

JULY 19/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ//

JULY 18/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 4.995 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ.

JULY 15/WITH SILVER UP 31 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 3.226 MILLION OZ FORM THE SLV//INVENTORY RESTS AT 510.443 MILLIONOZ//

JULY 14/WITH SILVER DOWN 88 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 OZ FROM THE SLV// //INVENTORY RESTS AT 513.671 MILLION OZ

JULY 13/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SV//INVENTORY RESTS AT 514.501 MILLION OZ.

JULY 12/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.228 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 514.501 MILLION OZ//

CLOSING INVENTORY 486.219 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

LAWRIE WILLIAMS: Gold breaches $1,800 but falls back yet again

Depending on how one analyses them, the latest U.S. Consumer Price Index (CPI) and Producer Price Index (PPI) figures, which were announced on Wednesday and Thursday, were either encouraging, if one looked at the year-on-year headline comparisons, or non-committal to continuing disturbing if one looked at the core figures. Headline y-o-y CPI came down to 8.5% in July, the same as in May, but well below the shock 9.1% recorded in June. Likewise the PPI also fell by 0.5% in July compared with June, but worryingly, if one strips out the volatile fuel and food elements the underlying core trend was flat to positive and with the possibility that there could yet be further strain on food and energy prices. With no end yet in sight to the Ukraine war we look likely to see higher than acceptable inflation levels for some time to come yet. Certainly the Fed’s target level of 2% inflation seems far, far away.

However, the levelling down of the headline figure did prompt the equity markets to generate some enthusiasm with the general opinion that the Fed may yet consequently tend to be rather less aggressive in its interest rate raising programme. Thus equity prices, which had already received a boost from the previous week’s well above expectation employment figures, continued on an upwards path.

We would offer a word or two of caution here for equity investors. Inflation certainly has not yet gone away as can be seen from the continuing high core inflation figures. Indeed core inflation may still be on the up. There is some continuing evidence, though, that energy prices are coming down – for example the latest oil price quote is US$90.21/barrel, down from well over $100 only just over a week ago, but oil prices can fluctuate and the reduction may not last, given continuing global supply uncertainties around Russian oil exports due to the Ukraine war.

The rise in equity prices was largely because of the feeling in the U.S. that the lower headline inflation levels may cause the Fed to be less aggressive in its interest rate raising programme at next month’s FOMC meeting. While the CME’s Fedwatch Tool participants just about agree, they currently only put the odds at 56.5:43.5 for a 50 basis point increase rather than a 75 basis point one – hardly a huge vote of confidence for a lower rate rise. However the FOMC meeting is five weeks away yet and there will be another CPI and PPI data announcement before then, so there is plenty of time for expectations to change and be re- assessed.

As for gold and silver prices, both advanced well following the inflation data announcements and the market expectations of a less aggressive Fed. The gold price ended the week above $1,800 again, after failing to hold that level a couple of times in intra-day price movement during the week. Silver did even better in percentage terms ending the week at $20.87, up almost 3% on the day. The Gold:Silver Ratio came out at a respectable 86.44 after spending recent time in the 90s. However these higher prices were not sustained in Asian and early European trade this morning and came down quite sharply so far. It will be interesting to see what U.S. markets make of the situation when they trade as they remain the principal global price drivers.

We do have faith in the gold price in particular moving forward between now and the year-end and we feel that a $1,900, or even a $2,000, price is yet achievable. The silver price does tend to follow gold upwards, often in a more exaggerated manner, although its upwards path could yet be slightly hindered by its principal demand areas nowadays being in the industrial sector and these could suffer if a serious recession strikes. Much of the world seems to be in one already and the U.S. is in denial, although is already in a technical recession as defined by two successive quarters of shrinking GDP.

15 Aug 2022

3.Chris Powell of GATA provides to us very important physical commentaries

Nine in 10 Bank of England staffers get bonuses as inflation soars

Submitted by admin on Sun, 2022-08-14 19:12Section: Daily Dispatches

By Laura Onita

The Telegraph, London

Sunday, August 14, 2022

Nine in 10 employees at the Bank of England were handed bonuses last year even as inflation soared beyond its 2% target.

A total of 4,263 workers, accounting for about 90% of its workforce, received a bonus last year, disclosures show. The highest payouts were between L15,000 and L20,000, with 34 members of staff getting rewards in this range.

More than 300 employees received a bonus between L10,000 and L15,000 and 1,733 were awarded between L5,000 and L10,000. In total, the central bank spent L23 million on variable compensation last year.

The disclosures are likely to heighten scrutiny of the central bank and leave it open to accusations of rewarding failure. Inflation has soared to a 40-year high over the last year, crossing the Bank’s 2% target in May 2021 and hitting 9.4% in June.

July’s data, due on Wednesday, is expected to show price rises accelerated to 9.8% and Threadneedle Street expects inflation to peak above 13% later this year. …

… For the remainder of the report:

end

A good read.

(Bloomberg/GATA)

How the U.S. toppled the world’s most powerful gold trader

Submitted by admin on Sun, 2022-08-14 11:22Section: Daily Dispatches

Except that the world’s most powerful gold traders are really the U.S Treasury Department, the Federal Reserve, and the Bank for International Settlements, for which JPMorgan Chase long has been executing trades.

* * *

How the U.S. Toppled the World’s Most Powerful Gold Trader

Eddie Spence, Joe Deaux, and Tom Schoenberg

Bloomberg News

via Yahoo News, Sunnyvale, California

Sunday, August 14, 2022

In December 2018 a man in his early 30s was intercepted on arrival at the Fort Lauderdale airport and taken to a room where two FBI agents sat waiting.

The target was scared and already on high alert — one of his associates had recently admitted to crimes he knew he had also committed. Christian Trunz wasn’t a terrorist or a drug trafficker but a mid-level trader of precious metals returning from his honeymoon.

Crucially, he was also a longstanding employee of JPMorgan Chase & Co., the biggest bullion bank.

The FBI’s airport ambush described by Trunz was a crucial step in the pursuit by U.S. prosecutors of JPMorgan’s precious metals desk, leading up to last week’s climax — the conviction on 13 counts of the man who was once the most powerful figure in the gold market, the desk’s former global head, Michael Nowak.

Watched with a mix of fascination and horror by precious metals traders around the world, the case has shone a light on how JPMorgan’s traders — including Nowak and the bank’s long-time lead gold trader Gregg Smith — for years allegedly manipulated markets by placing bogus orders designed to wrongfoot other market participants, principally algorithmic traders whose high-speed activity became a major source of frustration.

Nowak has become one of the most senior bankers to be convicted in the United States since the financial crisis and faces the prospect of decades in prison, although it could be far less. …

… For the remainder of the report:

https://finance.yahoo.com/news/us-toppled-world-most-powerful-123040880.html

END

A must view

(Andrew Maguire/Kinesis)

Spoofing trial indicated that JPMorgan traded gold for central banks, Maguire says

Submitted by admin on Fri, 2022-08-12 22:23Section: Daily Dispatches

10:28p ET Friday, August 12, 2022

Dear Friend of GATA and Gold:

Evidence in the trial of the former JPMorgan traders convicted of gold market manipulation this week indicated that the bank long has been trading the monetary metal for central banks and the Bank for International Settlements, London metals trader Andrew Maguire says in this week’s “Live from the Vault” program from Kinesis Money.

Maguire cites Bloomberg News reporting about the “spoofing” trial, highlighted in a GATA Dispatch on July 31 — https://gata.org/node/22108 — which said: “Another set of important clients” of JPMorgan “were central banks, which trade gold for their reserves and are among the biggest players in the bullion market. At least 10 central banks held their metal in vaults run by JPMorgan in 2010, according to documents disclosed in court.”

Maguire construes this to mean that the “spoofing” of which the Morgan traders were convicted probably was coordinated with knowledge of central bank trading plans.

Noting GATA consultant Robert Lambourne’s reporting on the rapid decline in the gold swap positions held by the BIS —https://gata.org/node/22127 — Maguire adds that the bank, the gold broker for major central banks, is bringing itself into compliance with the recent “Basel III” rules restricting “unallocated” or “paper” gold positions, positions not fully backed by gold itself or equally strong collateral. These positions, creating a vast, imaginary supply of gold, backstopped by central banks, long have been the primary mechanisms of gold price suppression

Maguire sees central banks transitioning steadily from short to long gold and estimates that the BIS itself will have extricated itself from gold liabilities and be profiting from higher gold prices by the end of the year.

Maguire’s comments on “Live from the Vault” come in a 43-minute interview with Shane Morand of Kinesis Money that can be seen at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

4. OTHER GOLD/SILVER COMMENTARIES

Ep.86 Live from the Vault

The BIS, the Bullion Banks & the Basel III price reset!

In this week’s Live from the Vault, Andrew Maguire exposes the race major world banks are in to discreetly exit decades of accrued, loaned-out short bets against gold and silver, as Basel III reforms bring the precious metals market closer to an inflection point.

With the recent JP Morgan spoofing scandal adding empirical weight to Andrew’s insider reports, the London whistleblower drills even deeper into the industrial scale of market manipulation across elitist players.

end

5.OTHER COMMODITIES: EGGS

end

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

end

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings MONDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7701

OFFSHORE YUAN: 6.7847

HANG SENG CLOSED DOWN 134.76 PTS OR 0.67%

2. Nikkei closed UP 324.80 OR 1.14%

3. Europe stocks CLOSED ALL MIXED

USA dollar INDEX UP TO 106.12/Euro FALLS TO 1.0199

3b Japan 10 YR bond yield: FALLS TO. +.185/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 133.12/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +0.947%/Italian 10 Yr bond yield FALLS to 3.04% /SPAIN 10 YR BOND YIELD FALLS TO 1.99%…

3i Greek 10 year bond yield RISES TO 3.21//

3j Gold at $1774.75 silver at: 20.23 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 0/100 roubles/dollar; ROUBLE AT 61.61

3m oil into the 87 dollar handle for WTI and 93 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 133.32DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9456– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9643well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.829 DOWN 2 BASIS PTS

USA 30 YR BOND YIELD: 3.108 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.96

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Global economy looks wounded

(zerohedge)

Futures Slide, Oil Tumbles After Dismal Chinese Data

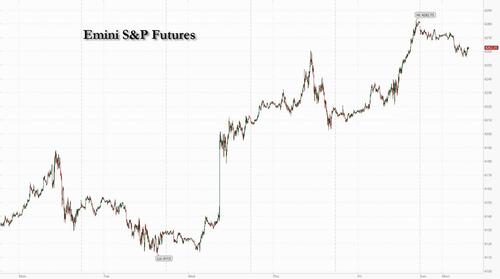

MONDAY, AUG 15, 2022 – 07:51 AM

US equity futures stocks were mixed and commodities from oil to iron ore tumbled as the latest round of terrible data from China further clouded the outlook for the global economy, an unexpected rate cut from the PBOC notwithstanding. Contracts on both the S&P 500 and Nasdaq 100 were lower by about 0.5% follows gains last week that sent the tech-heavy index up 22% from June to the highest since April, suggesting a four-week stocks rally – the longest since November 2020 – may stall at least until the $13Bn in daily buying from systematic funds and buybacks kicks in.

Europe’s equity benchmark advanced about 0.2%, as corporate news buoyed healthcare stocks while miners and carmakers declined. Asian stocks added less than 0.1% and emerging-market stocks dropped. The dollar jumped as the Euro and yuan tumbled, crude oil plunged, the downside accelerating after Iran’s foreign minister said that a “basis exists for signing an agreement “in the very near future” to revive the 2015 nuclear deal. After hitting $25K, a bout of aggressive shorting and dollar strength sent bitcoin back to $24K.

In premarket trading on Monday, tech giants including Apple Inc. and Amazon.com declined, alongside the broader tech sector as growth fears reemerged. US-listed Chinese electric-vehicle makers slid in premarket trading Monday after Li Auto (LI US) forecast revenue for the third quarter that fell short of analysts’ estimates.

- Cisco Systems (CSCO US) traded 0.6% lower after Citi says the company is losing market share as supply chain issues hurt the network gear maker more than its peers.

- Lufax (LU US) shares rose as much as 3.5% amid a report that the Chinese fintech firm is planning to file for a listing in Hong Kong as soon as the second half of the year.

- PlayAGS (AGS US) shares gained 7.5% to $8.08 after the company said it got a non-binding indication of interest valued at $10 a share in cash.

- UNITY Biotechnology (UBX US) shares rose 15% after Citigroup analyst Yigal Nochomovitz (buy) said the data for UBX1325 in in patients with diabetic macular edema were better than expected.

- Illinois Tool Works (ITW US) was downgraded to sell from hold at Deutsche Bank, which struggles to sees the equipment manufacturer’s valuation as justified.

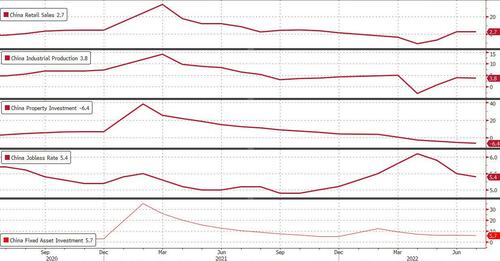

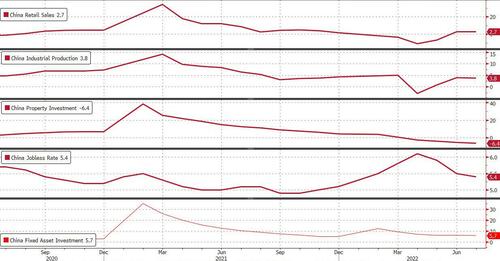

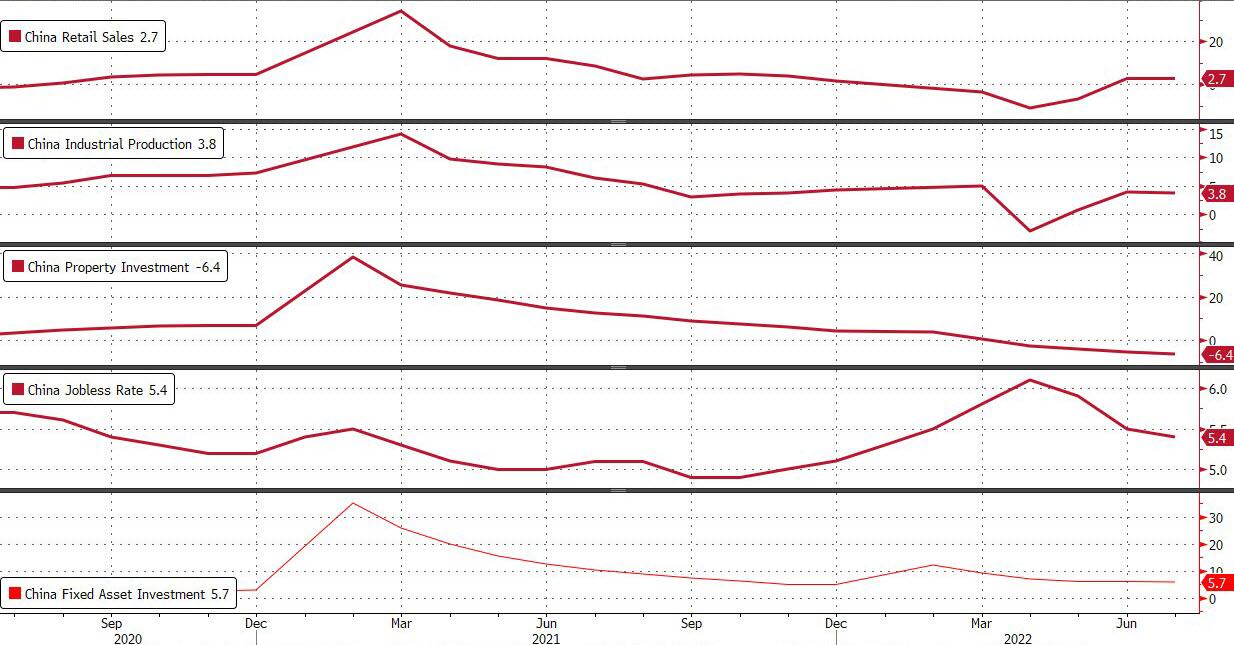

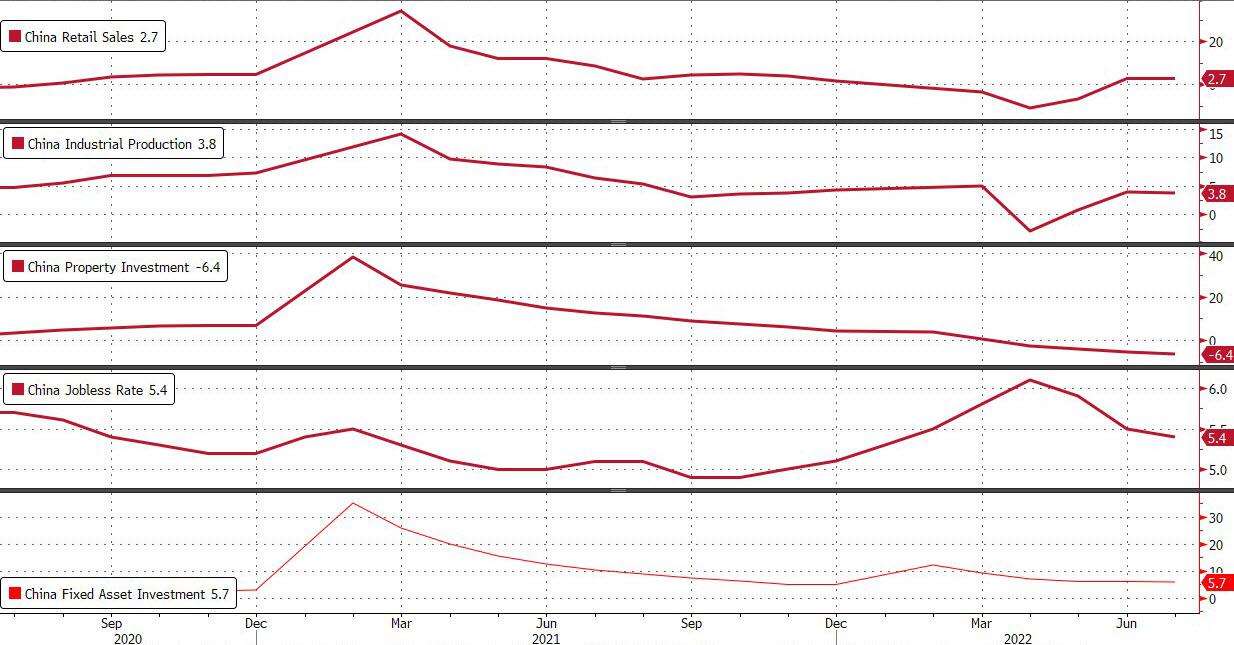

Equity markets in recent weeks have been propelled higher by signs of slowing price pressures, which stirred hopes of a shift by the Fed to less aggressive rate hikes. But China’s faltering economy shows many hurdles still lie ahead for a near-13% rebound in global stocks from June bear-market lows. Sentiment took a hit after Chinese retail sales, industrial output and investment all slowed and missed economist estimates in July. An unexpected cut to the nation’s interest rates is unlikely to turn things around as a worsening property slump and coronavirus lockdowns continue to weigh on the economy.

“Bad data from China also weighs on recession worries for the rest of the world,” said Ipek Ozkardeskaya, a senior analyst at Swissquote. “It’s too early to uncork the champagne, and call the end of the market selloff,” especially as the Fed continues to warn that inflation is still high, she said.

Equities have been rallying as data pointed to softer US inflation, bolstering bets of a pivot by Federal Reserve policy makers before the economy dives into a significant recession. While there is a thin calender of Fed speakers before the conference in Jackson Hole later this month, investors will be assessing minutes from the last Federal Open Market Committee meeting that are due on Wednesday.

In the ongoing feud between Wall Street permabulls and bears, Morgan Stanley’s Michael Wilson reiterated his weekly mantra that the sharp rally since June is just a pause in the bear market, predicting that share prices will be pulled down in the second half of the year as profits weaken, interest rates keep rising and the economy slows. On the other side, strategists at JPMorgan also unleashed their weekly dose of unicorns and rainbows, saying the rally could continue.

European stocks softened since a stronger open, with energy and basic resources weighing on market. Health care, construction and chemicals are the strongest-performing sectors. The risk of a euro-area recession has reached the highest level since November 2020, according to economists polled by Bloomberg. Here are some of the biggest European movers today:

- HelloFresh shares jump as much as 10%, the most since May, after the meal-kit maker confirmed results published in a preliminary report on July 20 and reiterated its full-year outlook

- Encavis rises as much as 5.4% after the renewable energy company confirmed preliminary 2Q results and a guidance raise for FY22, which were originally reported earlier this month

- RS Group climbs as much as 7.1% after The Times noted “growing speculation” that the company is preparing to bolster its defenses in the event of a takeover approach

- Henkel gains as much as 1.5% after the firm posted a 1H beat and guidance raise, which Jefferies says was due to the company’s strong pricing and a managed impact on volume

- Nordex swings between gains and losses after mixed results. While the company confirmed its FY22 guidance, the top- line was weaker-than-expected amid higher costs, analysts said

- Phoenix Group drops as much as 1.2%, reversing initial gains, after reporting interim results that Citi said contained few surprises

- GSK and Haleon fall, extending recent losses amid concerns over possible litigation risks related to antacid drug Zantac. Morgan Stanley says “considerable uncertainty” surrounds the litigation

- Treatt tumbles as much as 34% after cutting FY estimates. Peel Hunt said the update was disappointing in the short-term, and cut its price target on the stock to a Street low

Earlier in the session, Asian equities eked out gains with Japanese stocks giving a boost, while investors weighed China’s unexpected policy rate cut against disappointing economic data. The MSCI Asia Pacific Index was up less than 0.1% erasing the bulk of its 0.6% rise driven by health care and tech shares. Japan’s Nikkei 225 led gains in the region, with the benchmark turning positive for the year helped by a weaker yen and continued stimulus by Bank of Japan. China stocks turned lower after retail sales, industrial output and investment all missed estimates, erasing a gain caused by the country’s central bank lowering the rate on its one-year policy loans. The undershoot in data highlighted the growing toll of the nation’s Covid restrictions, casting a pall over the market’s outlook. Hong Kong shares were the worst performers in Asia. “The cuts by themselves may not be material enough to stimulate the economy given monetary policy is increasingly loosing its teeth in China – but on the margin – I feel this is positive for Chinese stocks,” said Chetan Seth, Asia Pacific equity strategist at Nomura Holdings.

The MSCI Asia gauge is trading close to a two-month high after capping its fourth weekly advance, with further gains dependent on the ongoing earnings season and whether global appetite can further improve. Still, China’s economic slowdown, worsened by virus curbs and a property crisis, and the Fed’s tightening trajectory continue to be bugbears for investors. Thai stocks rose even after data showed the domestic economy grew at a slower pace than economists estimated last quarter. India and South Korea were closed for holidays on Monday.

In Australia, the S&P/ASX 200 index rose 0.5% to close at 7,064.30, with materials and real estate stocks contributing the most to its move. Core Lithium was the top performer after an update on its exploration activities in the Northern Territory. Beach Energy was the biggest decliner after its FY underlying profit missed estimates. In New Zealand, the S&P/NZX 50 index rose 0.5% to 11,789.03

In FX, the Bloomberg Dollar Spot Index jumped about 0.5%, gaining for a second day as the currency climbed against all of its Group-of-10 peers except the yen amid demand for havens. Euro falls to week’s low versus USD, the Chinese yuan also slumped after the latest terrible economic data. Australian and New Zealand dollars slid after China’s central bank unexpectedly cut a key policy interest rate for the first time since January as it ramped up support for an economy struggling to recover from Covid lockdowns and a property downturn. Separately, China’s retail sales for July undershot estimates, as did industrial production. The yuan slumped and China’s benchmark 10-year China bond yield slid to the lowest since May 2020. Iron ore, copper and other metals declined. The yen held up against the dollar in thin summer trading, with traders waiting to see if US yields can vault higher on the back of aggressive Federal Reserve rate hikes. Japanese government bonds were mixed.

In rates, Treasuries were narrowly mixed with the curve slightly flatter; gains led by 20-year sector where yields are richer by around ~1bp on the day. Bunds, gilts both outperform vs Treasuries amid thin liquidity with Assumption Day holiday observed in many parts of Europe. 10-year TSY yields were around 2.83%, slightly richer and underperforming bunds and gilts in the sector by ~3bp; curves slightly flatter although spreads broadly remain within 1bp of Friday’s close. Italian bonds twist flattened, while bunds advanced and the German curve bull flattened. Treasury moves were small and the curve twist flattened slightly. IG dollar issuance slate empty so far; this week’s Treasury coupon auctions include 20-year new issue Wednesday and 30-year TIPS reopening Thursday. The latest CFTC positioning data shows hedge funds were aggressive net sellers of 10-year note contracts over the week.

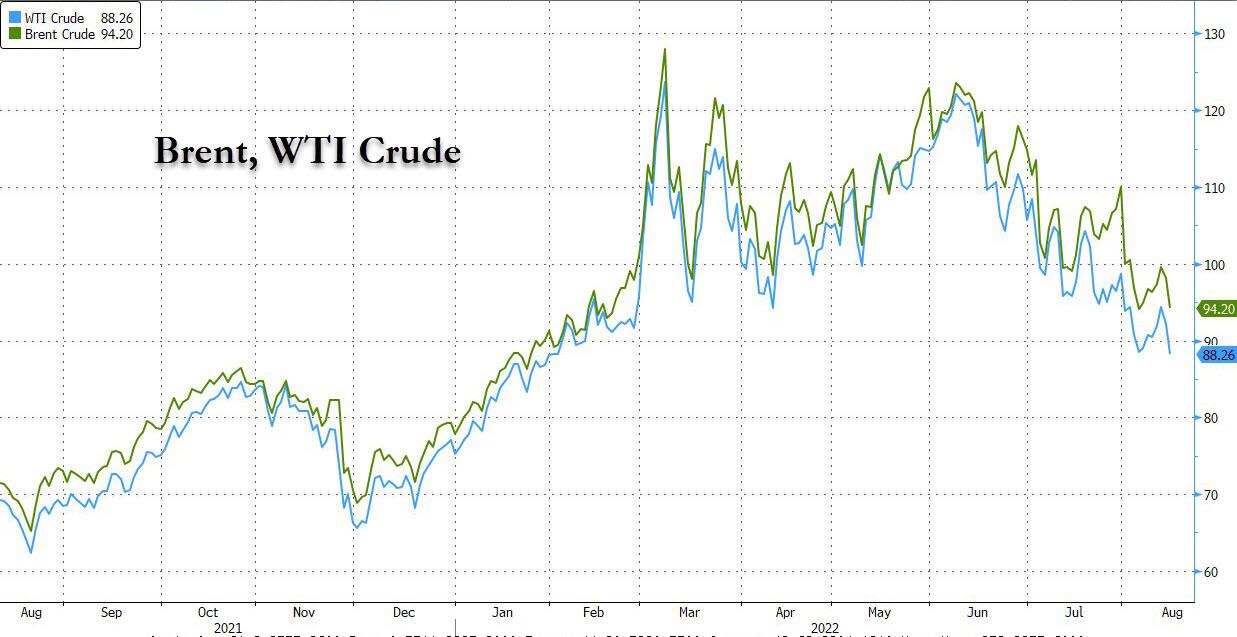

In commodities, WTI drifts 3.5% lower to trade around $88. Spot gold falls roughly $20 to trade near $1,782/oz. Spot silver loses 2% near $20. Most base metals trade in the red; LME nickel falls 4.6%, underperforming peers.

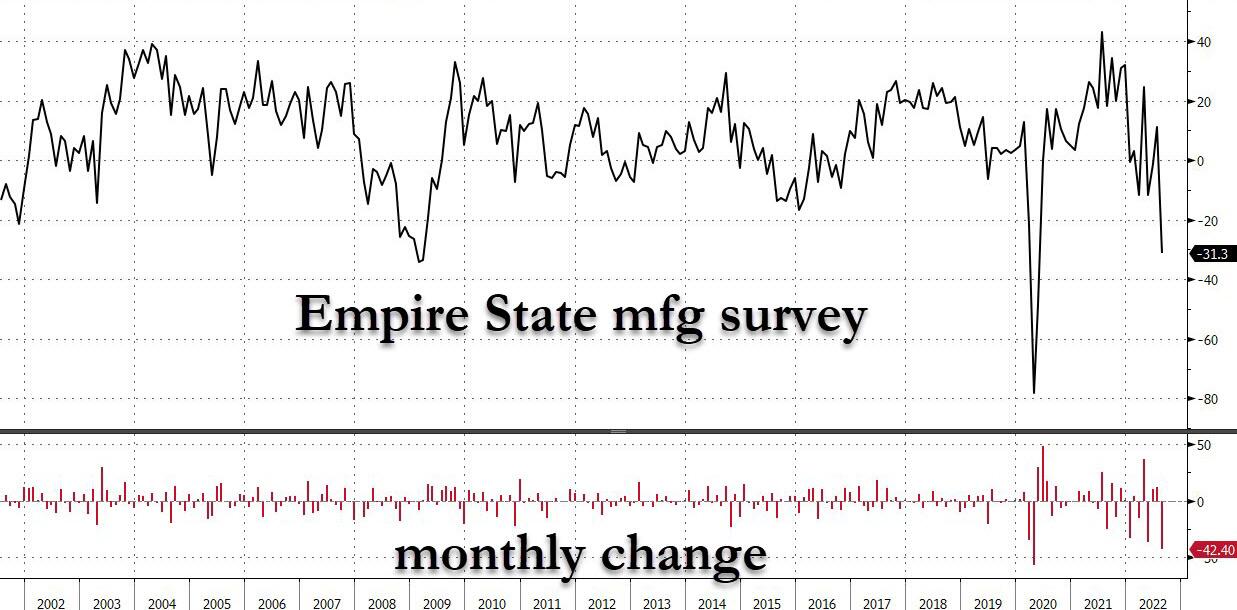

US economic data slate includes August Empire manufacturing (8:30am), NAHB housing market index (10am) and June TIC flows (4pm); industrial production, retail sales and FOMC meeting minutes are ahead this week

Market Snapshot

- S&P 500 futures down 0.4% to 4,263.25

- STOXX Europe 600 up 0.3% to 442.36

- German 10Y yield little changed at 0.96%

- MXAP up 0.1% to 163.32

- MXAPJ down 0.3% to 529.88

- Nikkei up 1.1% to 28,871.78

- Topix up 0.6% to 1,984.96

- Hang Seng Index down 0.7% to 20,040.86

- Shanghai Composite little changed at 3,276.09

- Sensex up 0.2% to 59,462.78

- Australia S&P/ASX 200 up 0.5% to 7,064.34

- Kospi up 0.2% to 2,527.94

- Euro down 0.3% to $1.0229

- Gold spot down 0.9% to $1,786.91

- U.S. Dollar Index up 0.32% to 105.97

Top Overnight News from Bloomberg

- Fund managers are warning the market is turning complacent over the outlook for inflation in Europe, where the prospect of recession has stoked the appeal of sheltering in bonds

- Hedge funds have turned bearish on the dollar for the first time in a year in a wager the US currency’s best days may be over

- Russian President Vladimir Putin offered to expand relations with North Korea, reaching out to his neighbor as the Kremlin scours the globe for weapons for its war in Ukraine

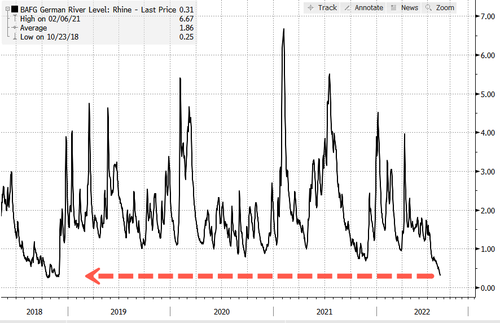

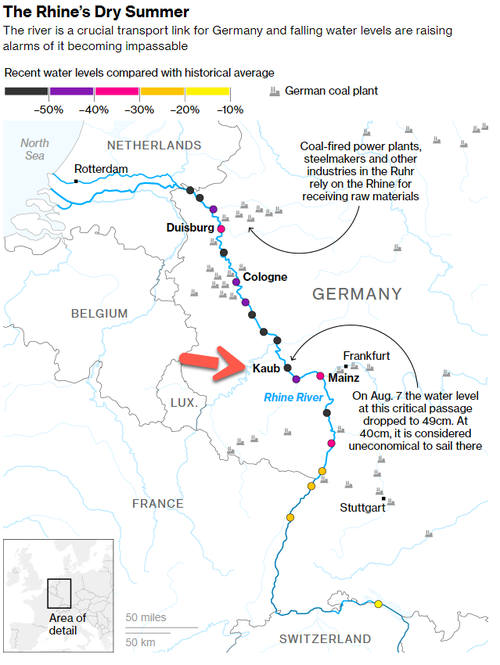

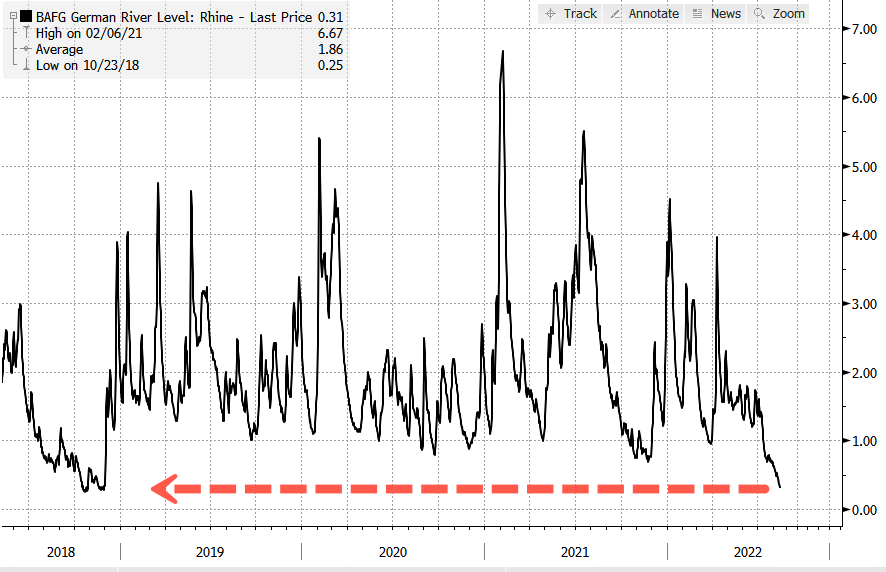

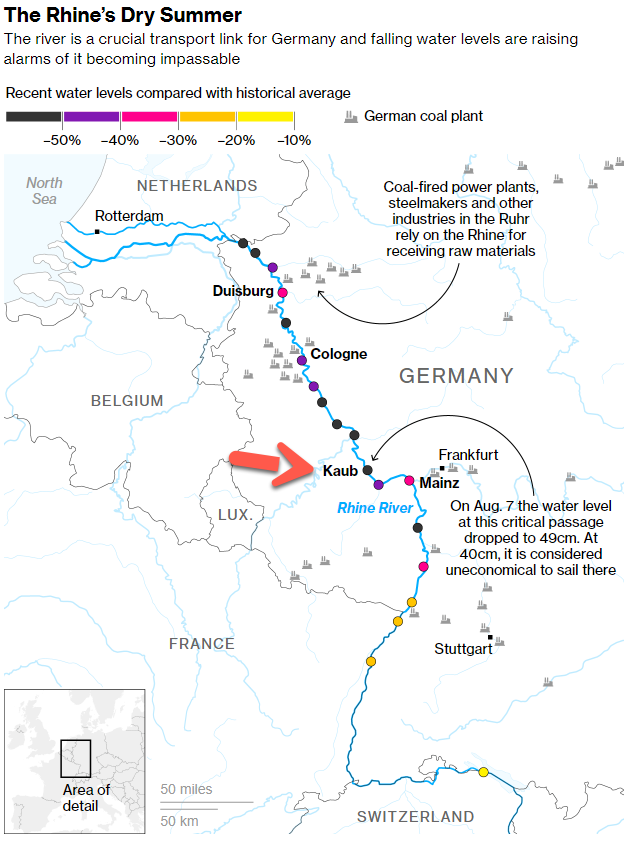

- The Rhine River’s water level continued to decline, hitting a new threshold as a climate crisis exacerbates Europe’s energy-supply crunch

A more detailed look at global markets courtesy of Newsquawk

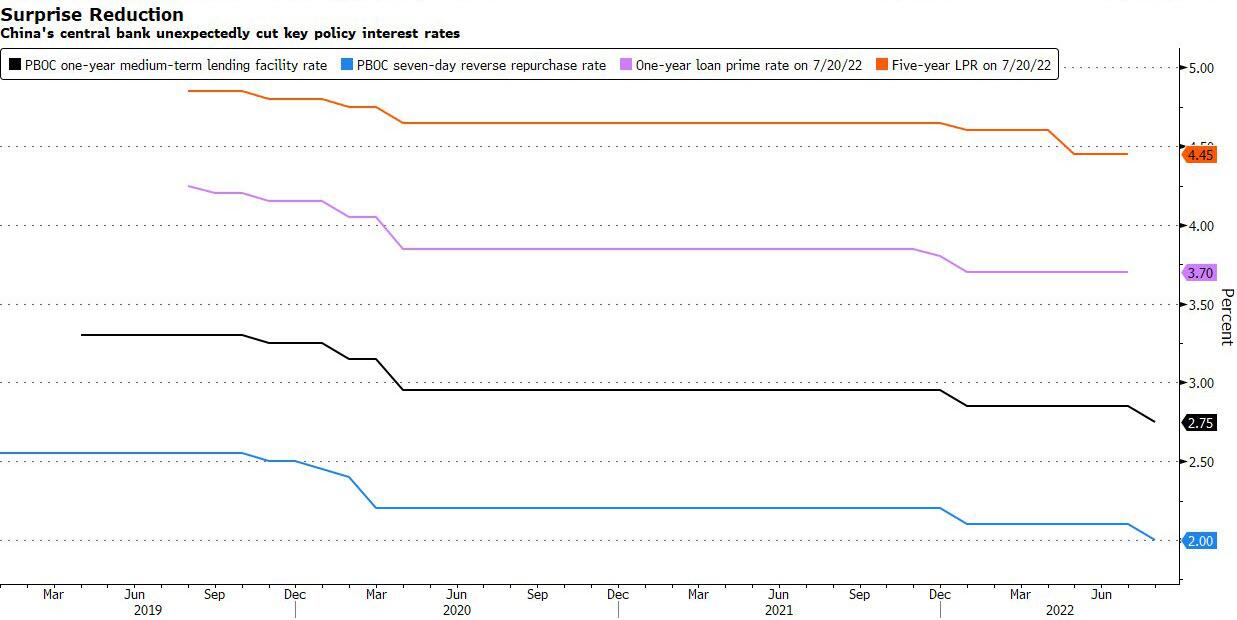

Asia-Pacific stocks were mixed with markets focused on China, as the PBoC’s surprise 10bps rate cuts to its 1-year MLF rate and 7-day Reverse Repo was overshadowed by the latest activity data from China in which both Industrial Production and Retail Sales fell short of market expectations. ASX 200 was positive with upside led by tech and miners amid a busy schedule of earnings this week and with Bluescope Steel firmly higher after its FY net more than doubled. Nikkei 225 outperformed and was unfazed by the Japanese GDP data for Q2 which printed weaker-than-expected but returned to expansion territory. Hang Seng and Shanghai Comp swung between gains and losses with early support after the PBoC delivered surprise 10bps rate cuts for the 1-year MLF and 7-day Reverse Repo rates, although Chinese stocks then slipped back into the red after disappointing Chinese activity data

Top Asian News

- PBoC injected CNY 400bln vs CNY 600bln maturing via 1-year MLF with the rate cut by 10bps to 2.75% (exp. 2.85%), while it conducted CNY 2bln of 7-day reverse repos with the rate cut by 10bps to 2.10%.

- China’s local COVID-19 cases topped 2,000 on Friday despite the recent tighter restrictions and lockdowns, according to Bloomberg.

- Shanghai extended the weekly COVID-19 testing requirement until end-September, although it was also reported that Shanghai announced primary schools, middle schools, kindergartens and nurseries will be permitted to reopen on September 1st, according to a statement cited by Reuters.

- China’s stats bureau said China’s economy continued a recovery trend in July but the foundation for a recovery is not solid and said the momentum of China’s economic recovery slowed in July, while it added that the economy remains resilient despite facing difficulties and they expect China’s economy to continue to recover, according to Reuters.

- “Rivers in multiple provinces, regions across China have dried up due to persistently high temperature and far below average amount of rainfall, posing threat to drinking water resources and agriculture productions”, according to Global Times.

- China’s Sichuan province order industrial plants to shut down between Aug 15-20th to ensure residential power supply, according to a document cited by Reuters.

Major bourses in Europe kicked off the session with modest broad-based gains before trimming gains amid a cautious tone. US equity futures have been subdued since the resumption of trade following the gains on Wall Street on Friday, and with retailers such as Walmart set to round off the Q2 earnings season whilst FOMC minutes are due on Wednesday. Regional sectors are now mixed (vs mostly positive at the open), with the theme more of a defensive one as Healthcare, Personal Goods, Food & Beverages, and Utilities among the top performers German gas levy set at 2.419cents/kWh, via Trading Hub Europe. Additionally, German Finance Ministry spokesperson said there is no response yet from the EU commission on the proposed VAT exemption for gas levy. Panasonic (6752 JT) is to boost its EV battery output for Tesla (TSLA) by 10%, according to Nikkei.

Top European News

- BoE Governor Bailey told Chancellor Zahawi that he would be “open to a review” of the Bank’s mandate, following Liz Truss’s criticism of its approach to inflation, according to The Telegraph.

- Reuters poll showed 30 out of 51 economists expect the BoE to hike rates by 50bps to 2.25% next month and the remaining 21 economists expect a 25bps increase.

- UK Treasury plans a government-backed lending scheme for suppliers which would reduce energy bills for households by an extra GBP 400 this winter, according to The Times.

- Two of the biggest UK energy suppliers are calling for a special fund that would allow the industry to freeze customers’ bills for two years and spread the cost of the gas-price crisis over a decade or more, according to The Times. It was also reported that UK energy suppliers called for the UK government to scrap levies and charges on bills, according to FT.

- SAS Shares Jump as Apollo Provides $700 Million Loan to Airline

- Russia Opens Trading to Some Foreign Investors

- Turkey Budget Remains in Deficit on Increased Spending in July

FX

- Dollar back in favour as safe haven with Yuan down on disappointing Chinese data and unexpected PBoC easing, DXY up to 106.340 from 105.540 low, USD/CNH tops 6.7850 and USD/CNY through 6.7700 from 6.7410 midpoint fix.

- Yen holds up better than others irrespective of sub-forecast Japanese GDP, USD/JPY mostly sub-133.50.

- High beta and commodity currencies hit hardest, while Euro, Franc and Sterling also retreat vs Greenback

- NZD/USD sub-0.6400, AUD/USD under 0.7050, USD/CAD over 1.2900, EUR/USD below 1.0200, USD/CHF 0.9460 and Cable close to 1.2050.

- Norwegian Crown undermined by slide in Brent to extent that wider trade surplus shrugged off, but Turkish Lira unable to benefit from cheaper oil as budget deficit blows out, EUR/NOK nearer 9.9000 than 9.9800, UDY/TRY nearer 18.0000 than 17.9000.

Fixed Income

- Bonds bounce strongly from early lows amidst China-related risk aversion and holiday-thinned turnover.

- Bunds top 156.00 from just above round number below, Gilts reach 116.66 from 115.94 and T-note nearer 119-16 top than 119-04+ bottom.

- UK STIRs contracts underperform as poll predicts another 50bp BoE hike before reversion to 25bp and then pause.

Commodities

- Crude markets have been selling off since the start of European trade alongside constructive developments on the Iranian Nuclear deal front.

- The firmer Dollar has hit the metals market – spot gold back under USD 1,800/oz, LME copper has been extending on losses back under USD 8,000/t.

- Saudi Aramco’s CEO said they are working to increase production from multiple energy sources and they will invest in the reliable energy and petrochemicals that the world needs, while he added that global oil demand is healthy in which he expects the recovery in oil demand to continue for the rest of the decade and said that global spare capacity is under 2mln bpd and declining fast. Saudi Aramco’s CEO also stated that Saudi oil production capacity increase will come gradually with a limited increase in 2024 and in 2025 they should go to 12.3mln bpd, as well as noted that they are confident in their ability to ramp up to 12mln bpd whenever there is a call from the government or Energy Ministry, according to Reuters.

- Ukrainian state gas transit operator said Gazprom booked transit capacity of 41.82mcm for August 15th (prev. 40.81mcm on August 14th), according to Reuters.

- Iran set September Iranian light crude prices to Asia at Oman/Dubai + USD 9.50/bbl, according to the National Iranian Oil Company.

- The damaged pipeline at the Louisiana port has been repaired, according to a port spokesman cited by Reuters.

- Germany’s top network regulator warned that Germany must cut gas use by 20% to avoid winter rationing, according to FT.

US Event Calendar

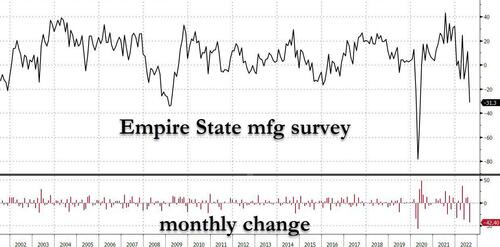

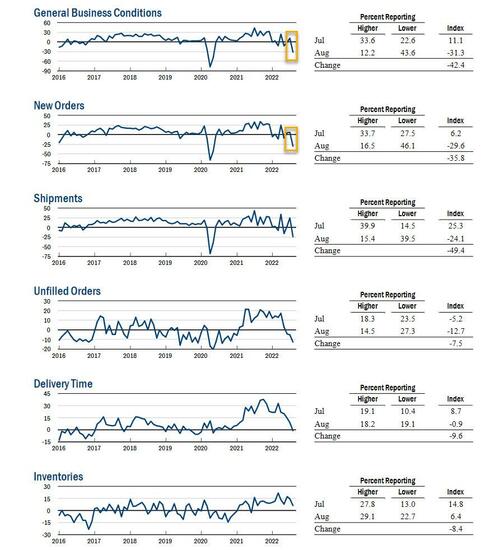

- 08:30: Aug. Empire Manufacturing, est. 5.0, prior 11.1

- 10:00: Aug. NAHB Housing Market Index, est. 55, prior 55

- 16:00: June Total Net TIC Flows, prior $182.5b; June Net Foreign Security Purchases, prior $155.3b

DB’s Henry Allen concludes the overnight wrap

Whilst the global economy looks to be heading towards a very difficult winter ahead, for markets the summer rally has shown few signs of abating. Indeed, the MSCI World Index has now advanced for 4 weeks running for the first time this calendar year, and the S&P 500 has recovered by a significant +16.5% in less than two months.

That run of gains has been turbocharged over the last couple of weeks by a number of good news stories that have fed into a narrative about whether we might have seen “peak inflation” now, raising hopes that central banks might not need to be as aggressive as feared about raising rates. We’ve raised questions about whether this optimism can hold, not least given Fed officials themselves are discussing a much more hawkish path for rates than what markets are pricing in, but for now there’s been little sign of a reversal, even as an increasing number of recessionary signals like the 2s10s Treasury curve have been flashing with growing alarm.

Overnight in Asia however, we’ve seen a slight loss of momentum after Chinese economic data for July came in weaker than expected. Industrial production was up by +3.8% on a year-on-year basis (vs. +4.3% expected), whilst retail sales were up +2.7% year-on-year (vs. +4.9% expected). In turn, that’s prompted the central bank to cut their one-year policy loan rate by -10bps to 2.75%, and yields on 10yr Chinese government debt are down -6.3bps this morning to 2.68%. Equity markets have also lost momentum, with the Shanghai Comp (-0.06%) and the CSI 300 (-0.07%) seeing modest declines, unlike elsewhere in Asia, where the Nikkei (+1.15%) and the Kospi (+0.16%) have both advanced this morning. In fact, that advance for the Nikkei puts it at a 7-month high, and back in positive territory on a YTD basis.

Looking forward now, the week ahead is a quieter one on the market calendar as we await the traditional late summer gathering of central bankers at Jackson Hole next week. However, we do have a few events to watch out for, including the expected signing by President Biden of the Inflation Reduction Act, which passed the House of Representatives on Friday by a margin of 220-207 following its earlier tie-breaking path through the Senate. The legislation includes funds for clean energy provisions, a 15% minimum tax for corporations with more than $1bn in revenue, and a 1% excise tax on stock buybacks. It also offers a political win for the Biden administration ahead of the mid-term elections in early November, and if you look at FiveThirtyEight’s average then President Biden’s approval rating is now running at its highest in a couple of months now, at 40.3%.

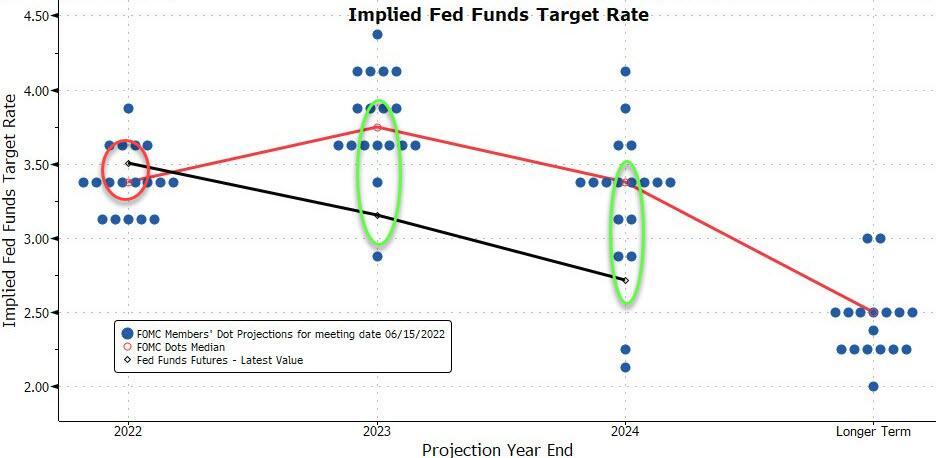

On the central bank side, we don’t have much in the way of decisions or speakers over the week ahead, which will mean this Wednesday’s release of the FOMC minutes from July will take on added importance. That meeting saw the Fed hike rates by 75bps again, following up their similar move in June, but investors interpreted the meeting in a dovish light as they latched onto comments that the Fed would move away from 75bp moves “at some point”. However, officials then moved to push back on that dovish interpretation, and by the close on Friday futures were almost evenly split between whether the Fed would hike by 75bps for a third time or whether they’ll step down to a 50bps pace. Our US economists write that these minutes could well provide some clues about how officials are likely to determine whether a downshift in the pace of rate hikes is warranted, and these signals from the minutes and other Fedspeak will become more important as the Fed moves towards greater data dependency when making decisions.

Staying on the US, the week ahead will also see an increasing amount of hard data for July come out. What we’ve had so far from the jobs report and the CPI has been very positive for markets, with investors growing more hopeful about a soft landing after more than half a million jobs were added and inflation came in beneath expectations. But in terms of what’s still ahead, we’ve got retail sales on Wednesday, where our economists expect that headlines sales should be boosted by the rebound in unit motor vehicle sales last month, as well as industrial production, housing starts and building permits on Tuesday. Also keep an eye out for the weekly initial jobless claims on Thursday, which have been on a fairly consistent path higher over recent months. Furthermore, our US economists have previously found that an 11.5% rise in the 4-week moving average of continuing claims relative to the minimum over the past year provides the most accurate recession signal. So a further move higher this week would only add to the recessionary signals we’ve seen like the 2s10s curve that’s been moving deeper into inversion territory over recent weeks.

On the inflation front, the week ahead will also bring us a number of countries’ CPI releases. One of them will be the UK, where our economist expects headline CPI to have risen to 9.8% in July, which would be its fastest pace in four decades. Meanwhile in Japan, our economist expects that core inflation excluding fresh food should rise to +2.4%, the highest since late-2014. Finally in Canada, the consensus expects that CPI will fall back from its multi-decade high of +8.1% in June to +7.6% in July, echoing what we saw in the US where year-on-year inflation has now begun to fall back from its June peak.

When it comes to earnings, this week will see the current season continue to wind down, with 455 of the S&P 500 having already reported results by now. However, we’ll still get a number of US retailers including Walmart (Tuesday) and Target (Wednesday). Both have cut their profit forecasts over the last couple of months, so it’ll be interesting to see what their earnings have to tell us about the strength of the US consumer right now.

Recapping last week now, it was yet another positive one for risk assets, with the S&P 500 (+3.26%) gaining for a 4th week running for the first time since November. It was a similar pattern across the major global indices, with the STOXX 600 (+1.18%) and the Nikkei (+1.32%) both moving higher as well. Small-cap stocks were a particular beneficiary, with the Russell 2000 seeing a +4.93% advance, but the moves were fairly broad-based, and the S&P 500 now stands “only” -10.20% lower on a YTD basis.

A key driver behind that optimism were the weaker-than-expected US CPI and PPI inflation readings last week. That led to a growing belief that the Fed might not hike by 75bps again at their next meeting in September, with the hike priced in by futures coming down from 69.0bps to 62.2bps by the end of the week. However, at the same time we saw the rate priced in by end-2023 move higher again as Fed officials struck a more hawkish tone on the future policy path than markets were already pricing, sending the December-2023 implied rate up from 3.08% to 3.20%. In turn, that sent government bond yields higher, with those on the 10yr Treasury up by +0.4bps to 2.83%, whilst those on 10yr bunds rose +3.2bps to 0.99%.

Finally, a major area of continuing concern was the European energy situation. Natural gas futures rose by +4.99% over the week to €206 per megawatt-hour, having been trading around €80 as recently as early June. Power prices for next year have also continued to make significant gains, with French power for 2023 up +14.64% on the week to €617 per megawatt-hour, which also marked its 9th consecutive weekly rise. German power was also up by +13.16% to a record €460 per megawatt-hour.

END

AND NOW NEWSQUAWK

Crude curtailed amid Iranian nuclear developments, DXY bid and Yuan soft – Newsquawk US Market Open

MONDAY, AUG 15, 2022 – 06:46 AM

- Major bourses in Europe kicked off the session with modest broad-based gains before trimming gains amid a cautious tone; stateside performance more subdued

- Crude benchmarks under pronounced pressure amid constructive Iranian nuclear deal updates; Iran to update before end of session

- DXY has been picking up to the detriment of peers across the board as the tone turns more cautions, Antipodeans lag amid poor China data

- Yuan hit on data and unexpected PBoC action

- Rhine river down to 32cm at Kaub with similar issues reported in China and the Sichuan province to shut industry to ensure power supply

- Looking ahead, highlights include US NY Fed Manufacturing, Speech from Fed’s Waller.

For the full report and more content like this check out Newsquawk.

Try a 14 day trial with Newsquawk and hear breaking trading news as it happens.

As of 11:15BST/06:15ET

LOOKING AHEAD

- US NY Fed Manufacturing, Speech from Fed’s Waller.

- Click here for the Week Ahead preview.

GEOPOLITICS

RUSSIA-UKRAINE

- Russian Defence Ministry said their forces have taken full control of Pisky village in Ukraine’s Donetsk region and have destroyed an ammo depo and HIMARS rocket system near Kramatorsk, according to Interfax. However, the Ukrainian military later stated that fierce fighting continues at Pisky village.

- Russian Foreign Ministry warned that the possible seizure of Russian assets by the US in favour of Ukraine will complete the destruction of Russia-US relations, while it was reported late on Friday that Russia told the US that diplomatic relations would be badly damaged and could even be broken off if Russia is declared a state sponsor of terrorism, according to TASS.

- US Secretary of State Blinken said that they are concerned about reports of British, Swedish and Croatian nationals being charged by illegitimate authorities in Eastern Ukraine, while he also said that Russia and its proxies have an obligation to respect international humanitarian law including the rights and protections afforded to prisoners of war.

- Several major Wall Street banks have begun offering facilitating trades in Russian debt after guidelines from the Treasury last month that allowed US holders to wind down their positions, according to Reuters

- “Russian forces have suggested a ceasefire around the embattled Zaporizhzhya nuclear power plant in southern Ukraine”, according to dpa.

CHINA-TAIWAN

- A delegation of US lawmakers led by Democratic Senator Markey arrived in Taiwan on Sunday and are said to have sought to reaffirm US support for Taiwan, as well as encourage stability and peace across the Taiwan Strait.

- China’s PLA Eastern Theater Command is likely to conduct strong and powerful military operations in the waters and airspaces around Taiwan as a countermeasure to the latest US lawmakers’ visit to Taiwan, according to Global Times.

- Taiwan said 13 Chinese air force planes crossed the Taiwan Strait median line on Saturday and 11 PLA aircraft crossed the median line or entered Taiwan’s air defence identification zone on Sunday, according to Reuters.

IRAN

- Iran says we have to let go on some nuclear demand to gain others; Iran to inform the EU of its response to a nuclear deal text tonight, via Bloomberg; says there is a plan B if talks fail, response will be made by midnight tonight, via Reuters. Further nuclear talks will be needed if the US refuses to show flexibility. Deal can be concluded if the US agrees to three remaining issues. Newsflow which saw a pronounced extension of pressure in crude, WTI Sep’22 and Brent Oct’22 to fresh session lows circa. USD 3/bbl below the morning’s initial pricing.

- Iranian Foreign Minister says “We exchange messages with Washington on three issues, and we have informed them of our readiness for compromise”, via Al Jazeera and a failure to revive the deal would not be the end of the world, via Reuters/Al Jazeera.

- Prior to this, an Iranian Foreign Ministry spokesperson says significant progress was made in the last round of talks held in Vienna. Consultations over the EU draft are ongoing. Ground is prepared for an agreement, provided Iran’s red lines are met, via Tehran Times. An update which sent crude to fresh session lows in an immediate reaction

For reference, earlier in the session reports included:

- Tehran Times journalist tweets “My hearings: Through a Qatari mediation, Iran has accepted the EU proposal, and an agreement will soon be signed.”.

- Russia’s chief negotiator in Iranian nuclear talks Ulyanov said an agreement may be reached as early as next week but added that “If amendments, objections appear it is difficult to project further developments now. We have to wait for the beginning of next week”, according to TASS.

- The terms of the EU’s Iranian Nuclear deal draft “make it sound like the Biden administration is prepared to make greater concessions”, according to Politico.

OTHER

- Israel was reported to have conducted an attack on targets in the vicinity of Syria’s port city of Tartous. Furthermore, explosions were heard and Syrian air defences confronted the “hostile targets” over Tartous, while the Syrian military said three military men were killed and three others were injured following the attack, according to Reuters.

- Author Salman Rushdie was stabbed several times on Friday at a conference near Buffalo New York and was rushed to hospital, while a Hezbollah official said the group does not know anything about the attack and VICE World News separately reported that the suspect had been in contact with Iran’s Revolutionary Guard.

- EU called for Serbia and Kosovo abandon their war rhetoric as the EU and NATO prepare to hold crisis talks with the rivals this week in an effort to avoid fresh conflict in the Balkans, according to FT.

- Russian President Putin told North Korean leader Kim in a letter that Russia and North Korea will expand bilateral ties, according to KCNA.

EUROPEAN TRADE

EQUITIES

- Major bourses in Europe kicked off the session with modest broad-based gains before trimming gains amid a cautious tone.