by harveyorgan · in Uncategorized · Leave a comment·Edit

Uncategorized · Leave a comment·Edit

GOLD; $1775.00 DOWN $7.85

SILVER: $20.13 DOWN 22 CENTS

ACCESS MARKET:

GOLD $1776.00

SILVER: $20.14

Bitcoin morning price: $24,036 DOWN 34

Bitcoin: afternoon price: $23,992. DOWN 78

Platinum price closing DOWN $0.65 AT$937.60

Palladium price; closing DOWN $0 at $2154.80

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: AUGUST 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,781.400000000 USD

INTENT DATE: 08/15/2022 DELIVERY DATE: 08/17/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 H GOLDMAN 2

118 C MACQUARIE FUT 3

132 C SG AMERICAS 4

624 H BOFA SECURITIES 3

661 C JP MORGAN 7

737 C ADVANTAGE 10

800 C MAREX SPEC 11 1

880 H CITIGROUP 2

905 C ADM 1

TOTAL: 22 22

MONTH TO DATE: 32,488

JPMorgan stopped: 7/22

_____________________________________________________________________________________

GOLD: NUMBER OF NOTICES FILED FOR AUGUST CONTRACT:

22 NOTICES FOR 2200 OZ //0.0684 TONNES

total notices so far: 32,488 contracts for 3,248,800 oz (101.051 tonnes)

SILVER NOTICES:

0 NOTICES FILED FOR 0 OZ/

total number of notices filed so far this month 827 : for 4,135,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $7.85

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD.

INVENTORY RESTS AT 993.94 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN $0.22 CENTS

AT THE SLV// ://A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 1.152 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 486.219 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 1287 CONTRACTS TO 146,719. AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG LOSS IN OI WAS ACCOMPLISHED WITH OUR $0.38 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.38) AND WERE UNSUCCESSFUL IN KNOCKING OFF SOME SPEC SILVER LONGS/ WE HAD A STRONG LOSS OF 928 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

I) SOME SPECULATOR SHORT LIQUIDATIONS//CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A FAIR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 60,000 OZ QUEUE JUMP / // V) STRONG SIZED COMEX OI LOSS/(//SOME SPEC LIQUIDATION)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -92

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTACTS for 12 days, total 6550 contracts: 32.750 million oz OR 2.729 MILLION OZ PER DAY. (545 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 32.75 MILLION OZ

.

LAST 16 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 31.43 MILLION OZ (A LOT LESS THAN NORMAL//THE CROOKS ARE SCARED TO ISSUE MORE EFP’S)

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1287 WITH OUR $0.38 LOSS IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 264 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /SOME BANKER ADDITIONS AND SOME SPEC SHORT LIQUIDATIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 60,000 OZ QUEUE JUMP // .. WE HAD A STRONG SIZED LOSS OF 1023 OI CONTRACTS ON THE TWO EXCHANGES FOR 5.115 MILLION OZ AS..THE SPECS STILL BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 0 NOTICE(S) FILED TODAY FOR 0 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GOOD SIZED 3277 CONTRACTS TO 455,656 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY:+ 172 CONTRACTS.

.

THE GOOD SIZED DECREASE IN COMEX OI CAME WITH OUR FALL IN PRICE OF $16.45//COMEX GOLD TRADING/MONDAY / WE MUST HAVE HAD ADDITIONAL SPECULATOR SHORT SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD SOME LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERINGS//CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR AUGUST AT 98.367 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 1300 OZ//NEW STANDING 103.437 TONNES

YET ALL OF..THIS HAPPENED WITH OUR FALL IN PRICE OF $16.45 WITH RESPECT TO MONDAY’S TRADING

WE HAD A FAIR SIZED LOSS OF 1565 OI CONTRACTS 4.867 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1712 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 455,656

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1565 CONTRACTS WITH 3277 CONTRACTS DECREASED AT THE COMEX AND 1712 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 1737 CONTRACTS OR 5.402 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1712) ACCOMPANYING THE GOOD SIZED LOSS IN COMEX OI (3277): TOTAL LOSS IN THE TWO EXCHANGES 1565 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR AUGUST. AT 99.272 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 1300 oz. 3) SOME/ LONG LIQUIDATION//// //.,4) GOOD SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST :

27,918 CONTRACTS OR 2,791,800 OZ OR 86.83 TONNES 12 TRADING DAY(S) AND THUS AVERAGING: 2326 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES: 86.83 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 86.83/3550 x 100% TONNES 2.45% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 86.83 TONNES (DRAMATICALLY FALLING AGAIN)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF SEPT., FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 1287 CONTRACT OI TO 146,719 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 264 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 264 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 264 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1287 CONTRACTS AND ADD TO THE 264 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF 1023 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 5.115 MILLION OZ

OCCURRED WITH OUR FALL IN PRICE OF $0.38

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED UP 1.80 PTS OR 0.05% //Hang Sang CLOSED DOWN 210.34 OR 1.05% /The Nikkei closed DOWN 2.87 OR % 0.01. //Australia’s all ordinaires CLOSED UP 0.50% /Chinese yuan (ONSHORE) closed DOWN AT 6.7882//OFFSHORE CHINESE YUAN DOWN 6.8088// /Oil UP TO 90.07 dollars per barrel for WTI and BRENT AT 95.39// / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 3277 CONTRACTS TO 455,656 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED WITH OUR FALL OF $16.45 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (1712 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF AUGUST.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1712 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :1712 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1712 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED SIZED TOTAL OF 1565 CONTRACTS IN THAT 1712 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED COMEX OI LOSS OF 3449 CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR STRONG FALL IN PRICE OF GOLD $ 16.45. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING AUGUST (103.437),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:103.437 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $16.45) AND WERE SUCCESSFUL IN KNOCKING OFF SOME SPECULATOR LONGS // COMMERCIAL LONGS ADDED TO THE POSITIONS, BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS////// WE HAVE REGISTERED A FAIR SIZED LOSS OF 4.867 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR AUGUST (103.437 TONNES)…

WE HAD +172 CONTRACTS ADDED TO COMEX TRADES. THESE WERE ADDED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 1565 CONTRACTS OR 156,500 OZ OR 4.867 TONNES

Estimated gold volume 90,858/// extremely poor/

final gold volumes/yesterday 145,199/ poor

INITIAL STANDINGS FOR AUGUST ’22 COMEX GOLD //AUGUST 16

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 265,494.458 oz Brinks HSBC 2,000 kilobars JPMorgan |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 22 notice(s) 2200 OZ 10.4199 TONNES |

| No of oz to be served (notices) | 767 contracts 76700 oz 2.385 TONNES |

| Total monthly oz gold served (contracts) so far this month | 32,488 notices 3,248,800 OZ 101.051 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

3 customer withdrawals:

i) out of HSBC 96,453.000 oz 2, 000 kilobars

ii) Out of JPM: 167,435.688 oz

iii) Out of Brinks: 1605.77 oz

total: 265,494.458 oz

total in tonnes: 8.25 tonnes

Adjustments: dealer to customer //2

JPMorgan 5594.274 oz

Manfra: 98.244 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 789 contracts having LOST 428 contracts .

We had 441 notices served upon yesterday so we gained a STRONG 13 contracts or an additional 1300 oz will stand for delivery in this very active month of August.

.As promised, from this point on, we will now add to the amount of gold standing at the comex until the end of the month.

Sept. GAINED 32 contracts to 3659 contracts.

October GAINED 416 contracts UP to 39,183

We had 22 notice(s) filed today for 2200 oz FOR THE AUGUST 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 22 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 7 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2022. contract month,

we take the total number of notices filed so far for the month (32,488) x 100 oz , to which we add the difference between the open interest for the front month of (AUGUST 789 CONTRACTS ) minus the number of notices served upon today 22 x 100 oz per contract equals 3,325,500 OZ OR 103.437 TONNES the number of TONNES standing in this active month of AUGUST.

thus the INITIAL standings for gold for the AUGUST contract month:

No of notices filed so far (32,488) x 100 oz+ (789) OI for the front month minus the number of notices served upon today (22} x 100 oz} which equals 3,325,500 oz standing OR 103.437 TONNES in this active delivery month of August.

TOTAL COMEX GOLD STANDING: 103.437 TONNES (A HUGE STANDING FOR AUGUST ( ACTIVE) DELIVERY MONTH)

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,318,414,091 oz 72.11 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 28,735,439.539 OZ

TOTAL REGISTERED GOLD: 14,506,013.757 OZ (451,18 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 14,229,425.782 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 11,911,011.0 OZ (REG GOLD- PLEDGED GOLD) 370.48 tonnes//rapidly declining

END

SILVER/COMEX/AUGUST 16

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,124,981.813 oz CNT Brinks JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,198,870.480 oz CNT JPMorgan |

| No of oz served today (contracts) | 0 CONTRACT(S) nil OZ) |

| No of oz to be served (notices) | 129 contracts (645,000 oz) |

| Total monthly oz silver served (contracts) | 827 contracts 4,135,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 2 deposits into the customer account

i) Into CNT: 600,786.780 oz

ii) Into JPMorgan: 598,083.720 oz

total deposit: 1198,870.480 oz oz

JPMorgan has a total silver weight: 173.929 million oz/333.029 million =52.22% of comex

Comex withdrawals: 3

i) out of CNT 162,886,343 oz

ii) Out of Brinks 267,546.976 oz

iii) Out of JPMorgan: 594,548.500 oz

total: 1,124,981.813 oz

adjustments: 1 dealer to customer

Manfra 227,008.421 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 55.027 MILLION OZ

TOTAL REG + ELIG. 333.029 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR AUGUST

silver open interest data:

FRONT MONTH OF AUGUST OI: 129 CONTRACTS HAVING GAINED 12 CONTRACTS. WE HAD 0 NOTICES FILED ON MONDAY

SO WE GAINED 12 CONTRACTS OR AN ADDITIONAL 60,000 OZ OF SILVER WILL STAND FOR DELIVERY. THE AMOUNT STANDING

WILL NOW INCREASE//(OR REMAIN CONSTANT) ON A DAILY BASIS AS BANKERS SCOUR THE PLANET FOR BADLY NEEDED SILVER.

SEPTEMBER HAD A LOSS OF 2975 CONTRACTS DOWN TO 63,047

OCTOBER GAINED 9 CONTRACTS TO STAND AT 106

CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes:49,365// est. volume today// fair

Comex volume: confirmed yesterday: 63,763 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 827 x 5,000 oz = 4,135,000 oz

to which we add the difference between the open interest for the front month of AUGUST(129) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST./2022 contract month: 827 (notices served so far) x 5000 oz + OI for front month of AUGUST (129) – number of notices served upon today (0) x 5000 oz of silver standing for the AUGUST contract month equates 4,780,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

AUGUST 16/WITH GOLD DOWN $7.85: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 993.94 TONNES

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

AUGUST 10//WITH GOLD UP $2.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES

AUGUST 9/WITH GOLD UP $6.70: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES.

AUGUST 8/WITH GOLD UP $13.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FORM THE GLD//INVENTORY RESTS AT 999.16 TONNES

AUGUST 5/WITH GOLD DOWN $14.25: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .33 TONNES FROM THE GLD////INVENTORY RESTS AT 1000.32 TONNES

AUGUST 4 WITH GOLD UP $29.00 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES FROM THE GLD///INVENTORY REST AT 1000.65 TONNES

AUGUST 2/WITH GOLD UP $3.70; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD//INVENTORY RESTS AT 1002.97 TONNES//

AUGUST 1/WITH GOLD UP $5.75: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 29//WITH GOLD UP $12.50; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1005.29 TONNES

JULY 28/WITH GOLD UP $31.25; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 27.//WITH GOLD UP $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 26/WITH GOLD DOWN $1.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.29 TONNES

JULY 25/WITH GOLD DOWN $7.85: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 1005.87 TONNES

JULY 22/WITH GOLD UP $17.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 21/WITH GOLD UP $11.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.101 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.87 TONNES

JULY 20/WITH GOLD DOWN $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1009.06 TONNES

JULY 19/WITH GOLD DOWN $.35 :BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.22 TONNES FROM THE GLD//INVENTORY RESTS AT 1009.06 TONNES

JULY 18/WITH GOLD UP $7.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.28 TONNES

JULY 15/WITH GOLD DOWN $3.75:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD///INVENTORY RESTS AT 1016.89 TONNES//

JULY 14/WITH GOLD DOWN $28.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD//INVENTORY RESTS AT 1019.79 TONNES

JULY 13/WITH GOLD UP $10.55:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD//INVENTORY RESTS AT 1021.53TONNES

JULY 12/WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESS AT 1023.27 TONNES

GLD INVENTORY: 995.97 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 16/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 486.219 MILLION OZ/

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 10/WITH SILVER UP 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 9/WITH SILVER DOWN 25 CENTS TODAY: TWO CHANGES IN SILVER INVENTORY AT THE SLV: FIRST: A DEPOSIT OF 461,000 OZ INTO THE SLV AND THEN A WITHDRAWAL OF 1.014 MILLION OZ..//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 8/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 5/WITH SILVER DOWN 28 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 922,000 OZ FROM THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 4 WITH SILVER UP 21 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 527,000 OZ FROM THE SLV////INVENTORY RESTS AT 486.634 MILLION OZ

AUGUST 2/WITH SILVER DOWN 21 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.504 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.161 MILLION OZ//

AUGUST 1/WITH SILVER UP 17 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE GLD: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 483.657 MILLION OZ//

JULY 29/WITH SILVER UP 30 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 461,000 OZ FROM THE SLV..//INVENTORY RESTS AT 483.657 MILLION OZ/

JULY 28/WITH SILVER UP $1.24 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 484.118 MILLION OZ/

JULY 27/.WITH SILVER UP 4 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL 11.479 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 484.118MILLION OZ//

JULY 26/WITH SILVER UP 16 CENTS: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.504 MILLION OZ FROM THE SLV//: //INVENTORY RESTS AT 495.597 MILLION OZ//

JULY 25/WITH SILVER DOWN 24 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.383 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 499.101 MILLION OZ//

JULY 22/WITH SILVER DOWN 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 500.484 MILLION OZ//

JULY 21/WITH SILVER UP 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.19 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 500.484MILLION OZ/

JULY 20/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 8.253 MILLION OZ FORM THE SLV/INVENTORY RESTS AT 507.585 MILLION OZ//

JULY 19/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ//

JULY 18/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 4.995 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ.

JULY 15/WITH SILVER UP 31 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 3.226 MILLION OZ FORM THE SLV//INVENTORY RESTS AT 510.443 MILLIONOZ//

JULY 14/WITH SILVER DOWN 88 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 OZ FROM THE SLV// //INVENTORY RESTS AT 513.671 MILLION OZ

JULY 13/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SV//INVENTORY RESTS AT 514.501 MILLION OZ.

JULY 12/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.228 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 514.501 MILLION OZ//

CLOSING INVENTORY 486.219 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

3.Chris Powell of GATA provides to us very important physical commentaries

END

4. OTHER GOLD/SILVER COMMENTARIES

This is good!

Russia Proposes New Standard To Compete With RIGGED London Bullion Market Association (LBMA)

BY CAPITALIST EXPLOITS

TUESDAY, AUG 16, 2022 – 7:50

A NEW FINANCIAL INFRASTRUCTURE

I’ve just finished a report on this (if you are a Capitalist Exploits subscriber then it will be in your hands shortly), but I’ll touch on this here.

Russia proposes a new international standard for trading in precious metals: the Moscow World Standard (MWS) which will become an alternative to the London Bullion Market Association (LBMA) which systematically manipulates precious metals markets to depress prices. According to Russia’s Finance Ministry, this new, independent international structure is necessary for “normalizing the functioning of the precious metals sector” and its creation is “critically important.”

“The basis of this new structure will be a new, specialized international precious metals brokerage headquartered in Moscow, which will rely on the MWS. Also proposed is a committee for fixing precious metals prices composed of central banks and largest banks of countries that are members of the Eurasian Economic Union (Armenia, Belarus, Kazakhstan, Kyrgyzstan and Russia) that currently have a presence on the precious metals market.

According to the Russian Finance Ministry, precious metals prices will be fixed either in the national currencies of key member-countries or using new monetary units used in international trade—for instance, the new BRICS currency proposed by Putin.

The Finance Ministry wants to make membership in this organization attractive to all market participants, especially China, India, Venezuela, Peru and other South American countries, as well as Africa. It aims to swiftly destroy the monopoly of LBMA and to provide for stable development of the precious metals sector.

In essence, Russia proposes to create a market for gold, platinum, etc., which will be regulated by countries that control the resources for these metals. This would be, simply put, a revolution. On the basis of this new market, it intends to further the system of bilateral trade in national currencies that specifically excludes dollars, euros and pounds.

And now, some statistics on the world gold supply. The production share of the US and other hostile nations* produce a grand total of 22% of the world’s gold. Eurasian Economic Union, BRICS and Africa, together, produce 57%—already a controlling share. Now add Peru and Venezuela, and the number goes up to 62%.

To put it in the plainest terms possible, Russia is colluding with a number of other countries to exclude the dollar, the euro and the pound from the system of international settlements, starting with precious metals but not necessarily stopping there. These countries control a lion’s share of gold production. For starters, Russia has fixed the price of gold in rubles at 5000₽/g, which works out to $2,447.17 per troy ounce. This compares rather favorably to the current LBMA fix of $1737.84. The days of LBMA’s ability to drive down gold prices using paper gold manipulation appear be running out.

What now?

Capital controls, that’s what. The smart money will flee to this. How long do we have?

I don’t know, but what’s that old saying from Willy Waggledagger?

Willy Waggledagger makes a great point!

Despite having a mullet, Willy has a very good point.

The proposed currency system is going to be backed by commodities, and the BRICs cannot be a system that is under the control of the LME. Remember when we wrote about the fiasco of the cancellation of $4bn of nickel trades and how the LME did so to bail out the CCP?

Good ol’ Cliffy was livid, but you know what. Even though he’s a titan in the industry, he couldn’t swing any changes.

Hedge fund titan Clifford Asness leads trader fury after LME cancels $4bn in nickel trades

Cancelling the trades helped Tsingshan Holding Group. The China-based stainless steel producer is estimated to have lost $8bn on its short position. Because the LME cancelled trades, Tsingshan losses are potentially less severe than if the trades had stood. The holding group’s chair, Xiang Guangda, is reportedly still holding short positions on nickel.

Now if Cliff couldn’t swing changes… and he’s a billionaire, then what hope do we have?

Anyway, the point is that when the LME did that they destroyed their credibility and trust. The only question in my mind was, at the time, what replaces it and where. Well, I think we now have the answer.

Remember, the UN/NATO Western crowd are championing “you’ll own nothing and be happy.”

If you can’t own precious metals then what is the point of backing a currency with them?

The answer is none.

Which allows me to conclude that the BRICs are not going to sanction the ownership of precious metals.

The West? Hmm, well I can certainly see the teleprompter telling sleepy Joe that by owning precious metals you’re “funding Putin’s war” or some hogwash like that.

Like I said, I’ve put more thought into this particular topic and more and you’ll be able to read all about it when it hits your inbox soon.

Cheers,

Chris MacIntosh – Capitalist exploits and Glenorchy Capital Macro Fund Manager

I write a premium newsletter called Insider for our paying subscribers. We also publish a couple of premium articles (pulled from Insider) on Zerohedge, which you just read. You can cut to the chase and get good exposure to our idea’s and strategies by signing up to the freebie newsletter. It’s a summary, and really saves time for you.

Just hop on over to this page and enter your email, then you’ll be set.

Contributor posts published on Zero Hedge do not necessarily represent the views and opinions of Zero Hedge, and are not selected, edited or screened by Zero Hedge editors.

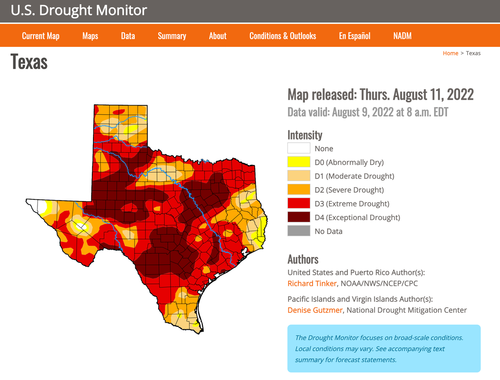

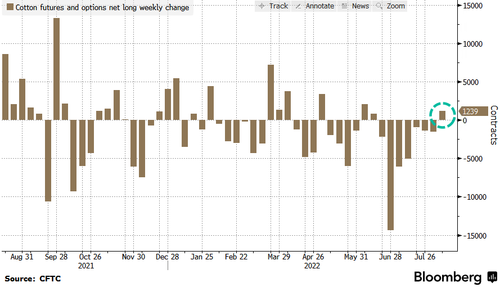

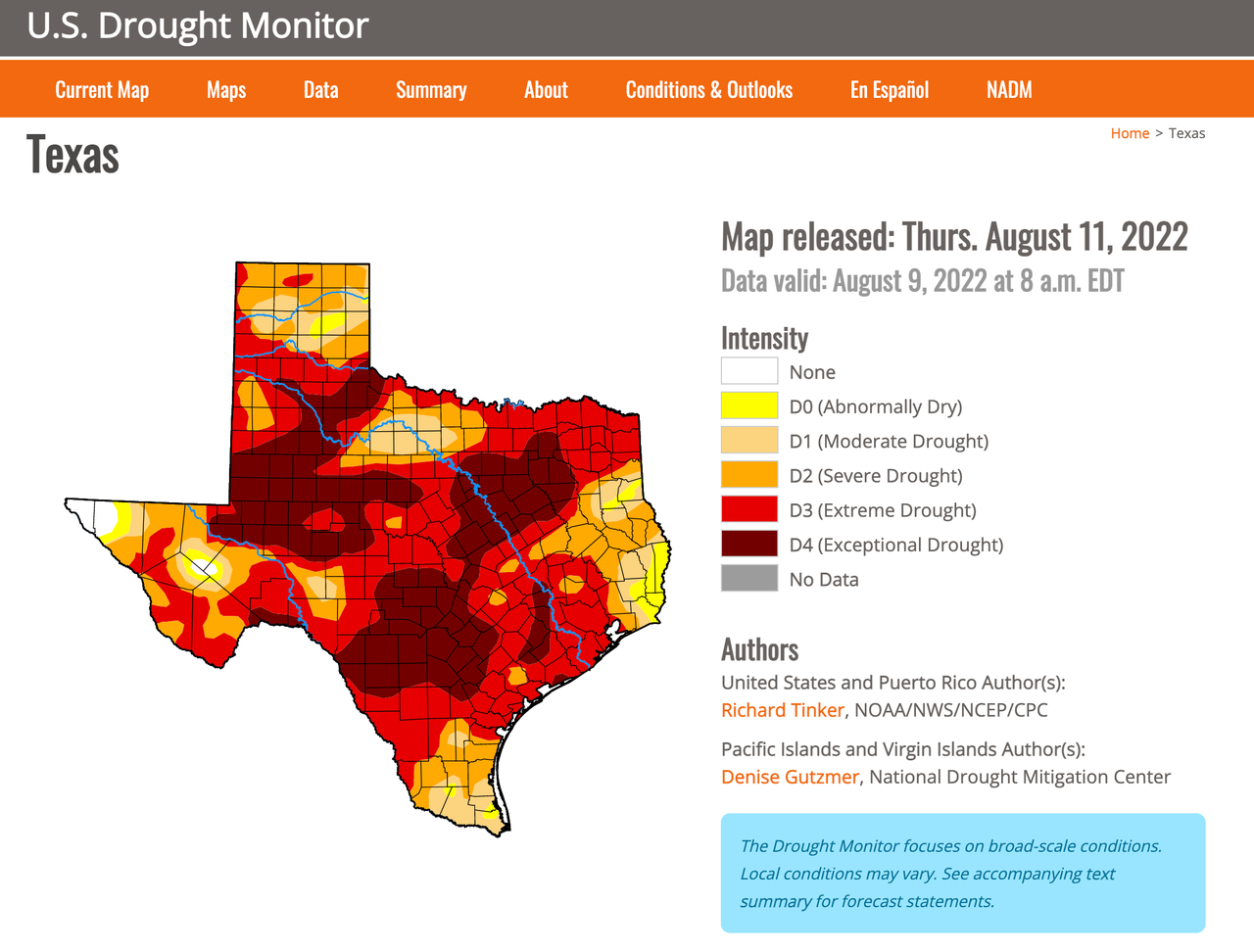

5.OTHER COMMODITIES: USA/COTTON

Cotton prices soar due to the drought in Texas. A massive crop estimate cut by the uSDA

“Worst I’ve Ever Seen”: Cotton Prices Soar After Historic USDA Cut Amid Megadrought

TUESDAY, AUG 16, 2022 – 06:55 AM

US cotton prices continued to surge above the boom days of 2010-11 after a massive crop estimate cut by the USDA, shocking Wall Street analysts and traders, due primarily to a megadrought scorching farmland of Texas, according to Bloomberg.

Futures in New York for December delivery were up 4.5% to $1.1359 a pound and up more than 21% this month.

“I don’t think you can put a top on prices right now,” Louis Barbera, the managing partner for VLM Commodities, told Bloomberg.

“I have been going to Texas for more than ten years, and this is by far the absolute worst I have ever seen, said Barbera.

What Barbera is referring to is the drought situation in Texas. The long stretches of triple-digit temperatures and limited rainfall this summer have turned vast amounts of farmland to dust, hurting cotton farmers in the South Plains of West Texas.

Last Friday, the USDA’s bigger-than-expected cut to domestic cotton crop stunned many on Wall Street. Crop output plunged to 12.57 million bales, the lowest in a decade. The cut also pushed down the US from the world’s third-largest producer to the world’s fourth.

Barbera said the western Texas region (around Lubbock and Lamesa), the epicenter of America’s cotton-growing belt, has “literally nothing” in fields that are just desert sand. He said fields that had drip irrigation were harvestable, but ones that weren’t weren’t salvageable.

“If cotton is not readily available from other sources, the scarcity of supply from the US could support prices globally, said Jon Devine, supply-chain economist for research Cotton Inc.

“The market has struggled to find the balance between the weakened demand environment and limited exportable supply in recent months. The conflict between these two influences makes it difficult to discern a clear direction for prices and suggests continued volatility,” Devine continued.

Supporting prices are bullish bets by money managers turning positive for the first time since June as prices rally.

Louis Rose, director at Rose Commodity Group, said the USDA’s cut to US output is “shocking” and comes at a time of the highest consumer inflation in decades.

end

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

end

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7882

OFFSHORE YUAN: 6.8088

HANG SENG CLOSED DOWN 210.34 PTS OR 1.05%

2. Nikkei closed DOWN 2.87 OR 0.01%

3. Europe stocks CLOSED ALL GREEN

USA dollar INDEX UP TO 106.82/Euro FALLS TO 1.0127

3b Japan 10 YR bond yield: FALLS TO. +.165/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 134.46/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +0.923%/Italian 10 Yr bond yield RISES to 3.06% /SPAIN 10 YR BOND YIELD RISES TO 2.05%…

3i Greek 10 year bond yield RISES TO 3.23//

3j Gold at $1775.85 silver at: 20.11 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 4/100 roubles/dollar; ROUBLE AT 61.27

3m oil into the 90 dollar handle for WTI and 95 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 134.46DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9502– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9623well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.806 UP 2 BASIS PTS

USA 30 YR BOND YIELD: 3.098 UP 0 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.96

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Reverse Early Losses As Walmart Beat Sparks Relief Buying

TUESDAY, AUG 16, 2022 – 08:20 AM

US stock futures drifted modestly lower after hitting a 4-month high just above 4,300 during Monday’s session, boosted by solid earnings and a guidance boost from Walmart, as attention turned back to lingering worries about the path of economic growth, how long until the NBER admits the US is in a recession and how Fed policy ties the room together. Contracts on the Nasdaq 100 and the S&P 500 were down less than 0.1% by 7:45 a.m. ET.

Gains in technology stocks on Monday spurred the broader benchmark equity index to its highest since May, with investors shrugging off terrible Chinese economic data. Crude oil reversed some of its recent sharp losses amid economic headwinds that clouded the demand outlook and prospects for an increase in supply. The greenback settled higher after fluctuating between gains and losses, while bitcoin traded above $24K. Chinese stocks listed in the US declined in premarket trading after a Reuters report that Tencent would liquidate its $24BN stake in Meituan to appease Beijing, sparking concerns it would do the same to its other investments.

Among notable movers in premarket trading, Snowflake fell 3.5% after Tiger Global Management cut its position in the software firm for the first time in eight quarters, according to latest 13F filings. Chinese stocks listed in New York fell in premarket trading following the Tencent report. Pinduoduo Inc. lost 4%, while JD.com Inc. declined 2.2%. Zoom Video Communications slid 3% after Citigroup Inc. downgraded its recommendation on the stock to sell from neutral, seeing “new hurdles to sustaining growth.” Here are some other notable premarket movers:

- Big-box retailers gain in premarket trading after Walmart said it sees a full-year adjusted EPS decline of 9% to 11% — less steep than its previous projection for a decline of 11% to 13% — following a stronger-than-expected earnings report for the second quarter.

- Zoom VideoCommunications (ZM US) down 3% in pre-market trading as Citi cuts its recommendation on the stock to sell from neutral, saying it sees “new hurdles to sustaining growth,” including growing competition from services like Microsoft Teams and macro-related pressures hitting customers.

- Bird Global (BRDS US) shares drop 6.4% in premarket trading after the electric vehicle company on Aug. 15 posted second-quarter results that showed a wider net loss than the same period a year earlier.

- Chinese stocks in US fall in premarket trading following a report that Tencent plans to sell all or much of its stake in food delivery company Meituan, in an effort to appease Beijing and lock in profits.

- Alibaba (BABA US) -2.2%, Nio (NIO US) -1%, Baidu (BIDU US) -1.8%

- Compass (COMP US) analysts at Barclays and Morgan Stanley cut their price targets on the real estate brokerage after it reduced its full-year guidance and announced plans to cut costs. The shares plunged 12% in US postmarket trading on Monday.

- Ginkgo Bioworks (DNA US) shares jump as much as 23% in US premarket trading after the cell programming platform operator’s revenue for the second quarter beat estimates.

- Snowflake (SNOW US) drops 3.5% in premarket trading after Tiger Global Management cut its position in the software firm for the first time in eight quarters, according to latest 13F filings.

“The lack of clear direction is driving the markets up and down,” Ipek Ozkardeskaya, a senior analyst at Swissquote Bank, wrote in a note. “Yesterday’s data softens the case for the continuation of the steep recovery, and throws the foundation of a period of consolidation, and perhaps a downside correction.”

A sharp drop in New York state manufacturing, the second-worst reading since 2001, along with the longest streak of declines since 2007 in homebuilder sentiment, sparked another round of “bad news is good news” and boosted hopes that the Fed may slow interest-rate hikes. However, it was soon outweighed by fears of a recession and belief among some traders the Fed could still press ahead with its tightening irrespective of a slowdown.

US stocks have been rallying since mid-June on optimism that corporate earnings are holding up even with higher prices and weakening consumer sentiment. The market also has gotten a boost from speculation that the Fed will slow the pace of interest rate increases after cooler-than-expected inflation data. While some strategists, especially those at JPMorgan, suggest the rebound could extend until the end of the year as investors turn less bearish, others including Michael Wilson at Morgan Stanley have said disappointing earnings are likely to spark another selloff in stocks.

As a result of the recent frenzied positional rally, four weeks of gains have pushed more than 90% of S&P 500 members above their 50-day moving averages. That’s been a good omen in the past, with stocks showing gains of 5.7% on average in the following three months and rising 18% in the 12 months after the signal. Negative returns have been a rare exception, with stocks falling only twice. “While this is not a necessary condition for the end of the bear market, it would increase our confidence that a rally back to the old highs will come before a return to the June lows,” Jeff Buchbinder, a strategist at LPL Financial, wrote in a note on Monday.

On the other hand, Skylar Montgomery Koning, senior global macro strategist at TS Lombard, said the bar for the Fed to stop its hiking cycle was high. “The market is betting not only that inflation comes down to a level that the Fed is comfortable with, but that the Fed reaction is timely,” she said on Bloomberg Television. “It may take until we get a 75-basis point hike in September or the new set of dot projections, and that may have to be what makes the market narrative shift.”

- European bourses are firmer across the board after a relatively constructive APAC handover, the Euro Stoxx 50 rising +0.4%, though off best levels post-ZEW. IBEX outperforms, adding 1.1%. Miners, telecoms and utilities are the strongest performing sectors. Here are some of the biggest European movers today:

- Delivery Hero shares jump as much as 14% after the firm projected 7% q/q growth in gross merchandise value in 3Q, in- line with expectations and putting the firm on track to meet its FY targets

- Glencore and other European miners outperform the broader market after BHP posted its highest ever FY profit and said it will push ahead with growth options

- Philips rises as much as 3.6% after its CEO Frans van Houten said he would step down in October, with the current head of the company’s Connected Care division, Roy Jakobs, taking over

- Watches of Switzerland jumps as much as 7.1%, reaching the highest since June 7, after the watchmaker published a first-quarter trading update. Analysts found the update to be solid

- Jyske Bank gains as much as 9.1% after the Danish lender reported 2Q pretax profit that topped Citigroup’s estimate by more than 20%, with Citi noting provisions came in well above expectations

- DFDS climbs as much as 8.7% after the Danish logistics company published 2Q results that beat consensus estimates and boosted its FY22 revenue forecast, RBC writes in a note

- Pandora drops as much as 8%, the most in more than three months, after the jewelery maker reported Ebit before significant items that missed the average analyst estimate

- Sonova and other European hearing aid makers lead losses on the Stoxx 600 after the firm and Danish peer Demant cut their guidance, with analysts flagging negative consensus revisions

- Straumann plunges as much as 14%, the most intraday since May 2020, after the oral care company announced 1H results and reaffirmed its guidance for the year

- Hemnet falls as much as 16% after the Swedish property ad company offered 8 million shares at SEK147 a share in a secondary offering announced on Monday after markets closed

- Hargreaves Lansdown declines as much as 1.8% after Credit Suisse downgraded its recommendation to neutral from outperform due to the personal investment firm’s valuation

Earlier in the session, Asian equities fell as investors weighed growth risks in the region against the probability of a slower pace of US interest-rate increases. The MSCI Asia Pacific Index declined as much as 0.4%, and is poised to snap a four-day winning streak. Hong Kong shares fell the most, with Meituan among the biggest drags on the regional gauge after Reuters reported that Tencent intends to sell all or much of its $24 billion stake in the food-delivery giant to appease Beijing. Across Asia, energy shares slid as oil prices fell on rapidly cooling US manufacturing that followed weaker-than-expected Chinese data Monday — offsetting gains in materials and utilities shares. After improving sentiment pushed up the region’s stocks for four straight weeks, markets are looking ahead to minutes of the Federal Reserve’s latest policy meeting due Wednesday for hints on its rate-hike trajectory. Closer to home, China’s surprise interest-rate cut on Monday did little to allay concerns over the property sector and the broader slowdown from Covid restrictions. Economists and state media are calling for additional stimulus, which could aid a rally in Chinese stocks and Asian peers.

“While the downside surprises across the economic calendar suggested that growth conditions have clearly worsened, market participants seem willing to ride on optimism” that the Fed may shift to a looser policy stance sooner with easing inflation, Jun Rong Yeap, market strategist at IG Asia said in a note. Japan’s benchmarks dropped while gauges in the Philippines, Malaysia and India rose. Indonesian shares were higher after President Joko Widodo said in his annual budget speech that he aims to narrow next year’s deficit to below 3% of gross domestic product for the first time since 2019.

Japanese stocks edged lower as investors remained on the lookout for signs of an economic slowdown in the US and China. The Topix Index fell 0.2% to 1,981.96 at the market close in Tokyo, while the Nikkei 225 was virtually unchanged at 28,868.91. SoftBank Group Corp. contributed the most to the Topix’s decline, decreasing 2.6% after Elliot Management sold off almost all of its position in the company. Out of 2,170 stocks in the index, 908 rose and 1,138 fell, while 124 were unchanged.

Australia’s S&P/ASX 200 index rose 0.6% to close at 7,105.40, its highest level since June 8. BHP, the largest-weighted stock in the benchmark, was among the top performers Tuesday after its full-year profit exceeded analysts’ expectations. Challenger slumped after announcing a strategic review of Challenger Bank. In New Zealand, the S&P/NZX 50 index rose 0.5% to 11,847.15.

In FX, the Bloomberg Dollar Spot Index advanced a third day as the greenback was steady to higher against all of its Group-of-10 peers. The euro touched an almost two-week low of $1.0125 after German ZEW expecations index came in lower than forecast. Aussie recovered a loss after the Reserve Bank’s August minutes failed to bolster bearish views, only to resume its slide in the European session. Australia’s central bank signaled further interest-rate increases would come in the period ahead, while restating it will be guided by incoming economic data and the inflation outlook. The yen was steady in the Asian session only to slip in the European session. China’s onshore yuan fell to the lowest since May, tracking Monday’s losses in the offshore unit. The nation’s central bank didn’t push back strongly against the currency weakness through its daily reference rate on Tuesday but traders are watching if its stance would change in case the yuan selloff deepens. USD/CNY rose as much as 0.3% to 6.7978, the highest since May 16; USD/CNH falls 0.1% to 6.8113 after surging 1.2% on Monday

In rates, Treasuries were mixed, pivoting around a near unchanged 10-year sector with the curve flatter as long-end outperforms. Bunds and gilts underperform with the latter following stronger-than-forecast UK wage figures for June. US yields cheaper by up to 2bp across front-end and richer by 1.5bp in long-end of the curve — 2s10s, 5s30s spreads subsequently flatter by 1.7bp and 2.7bp on the day; 10-year yields around 2.79% and near unchanged, outperforming both bunds and gilts by over 1bp.

European bonds fall, with the yield on German 10-year up about 2bps, while gilts 10-year yield rises ~3bps following stronger-than-forecast UK wage figures for June. . Both are trading within Monday’s range. Peripheral spreads are mixed to Germany; Italy and Spain widen, Portugal tightens. Italian 10-year yield rises ~7bps to 3.04%. Australian and New Zealand bonds extended opening gains amid concerns over economic growth. Japanese government bonds rallied as a smooth five-year auction and concerns over global economic slowdown encouraged buying.

In commodities, WTI traded within Monday’s range when crude futures fell around 5% over the previous two sessions. Besides economic worries, investors are also facing the prospect of rising supply as demand moderates. Libya is pumping more and Iran is edging closer to reviving a nuclear deal that will likely see higher crude flows. On Tuesday, oil reversed recent losses however, and rose more than 1% to over $90 as the prospect of an “imminent” Iranian deal once again faded; Iran responded to the EU’s draft nuclear deal and expects a response in the next two days, according to a source cited by ISNA. It was also reported that an adviser to the Iranian negotiating delegation told Al-Jazeera they are not far from an agreement and chances of reaching a nuclear deal are very high. Iran’s response to the draft EU JCPOA text will probably fail to satisfy Western parties, particularly the US, according to Iran International; Iran wants further provisions around economic guarantees above the one-year exemption reportedly being offered. Elsewhere, spot gold falls roughly $4 to around $1,775/oz. Base metals are mixed; LME tin falls 1% while LME zinc gains 1.9%.

Looking to the day ahead, data releases from the US include July’s industrial production, capacity utilization, housing starts and building permits. In the UK, there’s unemployment for June, Germany has the ZEW survey for August and Canada has July’s CPI. Elsewhere, we’ll get earnings releases from Walmart and Home Depot.

Market Snapshot

- S&P 500 futures little changed at 4,295.50

- STOXX Europe 600 up 0.4% to 443.91

- MXAP down 0.3% to 163.03

- MXAPJ little changed at 529.75

- Nikkei little changed at 28,868.91

- Topix down 0.2% to 1,981.96

- Hang Seng Index down 1.0% to 19,830.52

- Shanghai Composite little changed at 3,277.89

- Sensex up 0.5% to 59,751.63

- Australia S&P/ASX 200 up 0.6% to 7,105.39

- Kospi up 0.2% to 2,533.52

- German 10Y yield little changed at 0.91%

- Euro down 0.2% to $1.0140

- Gold spot down 0.3% to $1,774.93

- U.S. Dollar Index up 0.18% to 106.74

Top Overnight News from Bloomberg

- Tencent-Backed Giants Dive on Report of $24 Billion Meituan Sale

- Oil Extends Losses on Global Slowdown and Chance of More Supply

- Babylon Said to Mull Take-Private Not Long After SPAC Deal

- Chipmakers’ Pandemic Boom Turns to Bust as Recession Looms

- Apple Lays Off Recruiters as Part of Its Slowdown in Hiring

- FAA Warns of Monday Evening Delays at NYC Area Airports

- Wong Says Singapore Must Compromise Over Law on Sex Between Men

- ‘Broken’ Barclays ETN Soars to 33% Premium With Issuance Halted

- Trump Executive Weisselberg in Plea Talks to Resolve Tax Case

- US Congress Pushes Biden Toward Risky Confrontation With China

- Twitter Must Give Musk Data, Documents From Ex-Product Head

- Next Singapore PM Warns US, China May ‘Sleepwalk Into Conflict’

- Apple Sets Return-to-Office Deadline of Sept. 5 After Delays

- Tiger Global, Yale Cut Stocks Last Quarter as Markets Tumbled

- Druckenmiller Sold Big Tech in Bear Market as Soros Dove Back In

- A Century of Fed Crises Holds Secrets to Fight Future Recession

- Compass Stock Slumps as CEO Reffkin Plots Out More Cost Cuts

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mostly positive as the region followed suit to the gains on Wall Street but with upside limited as economic slowdown concerns lingered. ASX 200 traded higher amid a deluge of earnings and with the index led by the mining sector including BHP shares after the industry giant reported a record FY underlying net and dividend. Nikkei 225 lacked direction amid the absence of any major fresh macro drivers and alongside a choppy currency. Hang Seng and Shanghai Comp were initially kept afloat by support-related optimism with developers encouraged after reports that China is considering issuing government-guaranteed bonds to provide liquidity to certain developers, while PBoC-backed press noted that China needs additional policy stimulus to increase economic growth. However, the Hang Seng later pulled back ahead of the European open to slip below 20k.

Top Asian News

- China’s NDRC said macro policies should be strong, reasonable and moderate in expanding demand actively, while it will roll out practical measures to support starting up businesses and job employment, according to Reuters.

- PBoC-backed Financial News front page report stated that China needs additional policy stimulus to increase economic growth, while Securities Times suggested the recent surprise PBoC rate cut could be the first in a series of measures to stabilise growth.

- China is to consider issuing government-guaranteed bonds to provide liquidity to certain developers.

- RBA Minutes from the August 2nd meeting stated the board expects to take further steps in the process of normalising monetary conditions in the months ahead, but is not on a pre-set path and seeks to do this in a way that keeps the economy on an even keel. The minutes also reiterated that members agreed it was appropriate to continue the process of normalising monetary conditions and that inflation was expected to peak later in 2022 and then decline back to the top of the 2%-3% range by the end of 2024.

- Australian Bureau of Statistics will begin publishing a monthly CPI indicator with the first publication on October 26th to coincide with the release of the quarterly CPI data, while it added that quarterly CPI will continue to be the key measure of inflation.

- China is reportedly to enhance policy to increase new births, will boost housing support for those with additional children, via Bloomberg.

European bourses are firmer across the board after a relatively constructive APAC handover, Euro Stoxx 50 +0.4%, though off best levels post-ZEW. US futures are in contained ranges and pivoting the unchanged mark at this point in time, ES -0.2%; HD and WMT in focus. Home Depot Inc (HD) Q1 2023 (USD): EPS 5.05 (exp. 4.94), Revenue 43.79 (exp. 43.36bln); confirms FY22 guidance.

Top European News

- Delivery Hero Sees Path to 2023 Profit Powered by Asia Unit

- Pandora Sells Lab-Grown Diamonds in US as Mined Ones Dropped

- UK Real Wages are Falling at Their Fastest Pace on Record: Chart

- Hearing Aid Makers Plunge After Sonova, Demant Cut Guidance

- DFDS Gains on Guidance Upgrade; RBC Sees Future Growth Potential

- Turkey Limits Resales of Newly Bought Cars by Dealers

FX

- DXY breaches last week’s peak as Treasury yields rebound and Yuan weakens further amidst Chinese growth concerns, index up to 106.860 vs 106.810 on August 8, USD/CNY and USD/CNH approach 6.8000 and 6.8200 respectively.

- Euro stumbles after unexpected deterioration in German ZEW economic sentiment and Pound slips following mixed UK jobs and wage data, EUR/USD down to 1.0125 and Cable low 1.2000 area.

- Yen and Franc retreat as risk sentiment improves and bonds back off, USD/JPY tops 134.00 and USD/CHF above 0.9500.

- Kiwi cautious ahead of RBNZ, but Aussie holds up better post-RBA minutes flagging more hikes, NZD/USD eyes bids into 0.6300 and AUD/USD hovers just under 0.7000.

- Loonie underpinned awaiting Canadian CPI as crude prices stabilise to a degree, USD/CAD straddles 1.2900.

Fixed Income

- Debt futures retreat further from Monday’s lofty levels in corrective price action and as broad risk sentiment improves.

- Bunds down to 156.07 having been closer to 157.00, Gilts to 116.52 vs 116.99 earlier and 117+ yesterday, T-notes to 119-19 from almost 120-00.

- UK 2029 and German 2027 supply snapped up amidst given some yield concession.

Commodities

- Crude benchmarks pressure, but off worst levels and well within yesterday’s ranges, as the EU receives Iran’s response to the JCPOA draft.

- Initial indications are that a deal is in reach, though, caveats/unknowns remain in focus – particularly the US’ response.

- EIA said US oil output from top shale regions in September is due to increase to the highest since March 2020, according to Reuters.

- Iran sets September Iranian light crude OSP to Asia at Oman/Dubai + USD 9.50/bbl, via Reuters.

- Major European zinc smelter (Nyrstar Budel) reportedly to shut due to elevated energy costs, via Bloomberg; will shut as of September 1st.

- Spot gold under modest pressure as the USD lifts, but still near the 50-DMA while base metals recoup from Monday’s data-driven pressure.

US Event Calendar

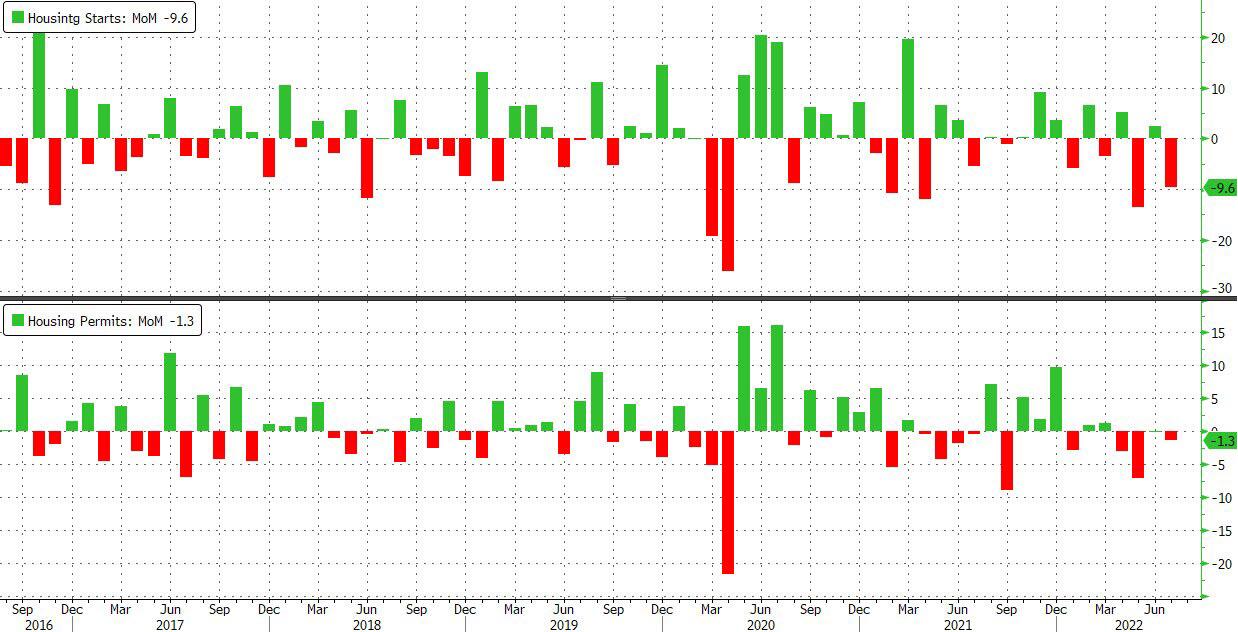

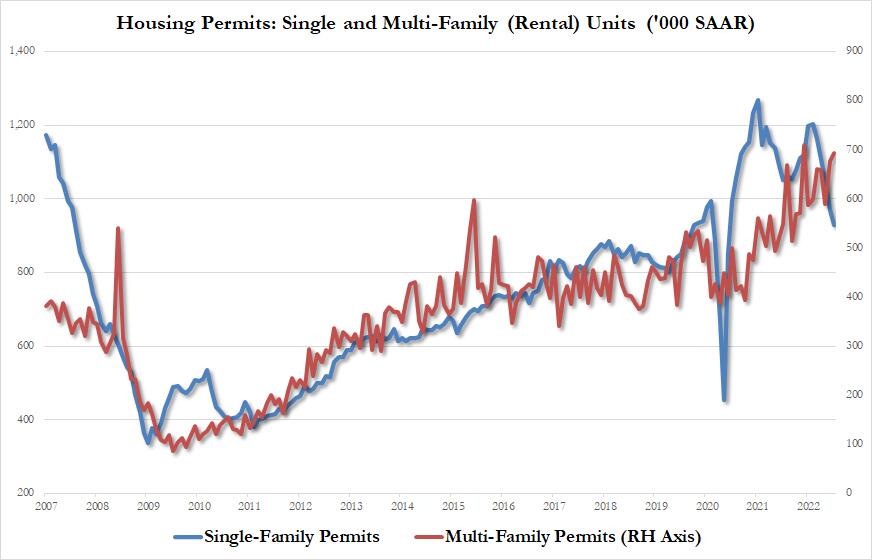

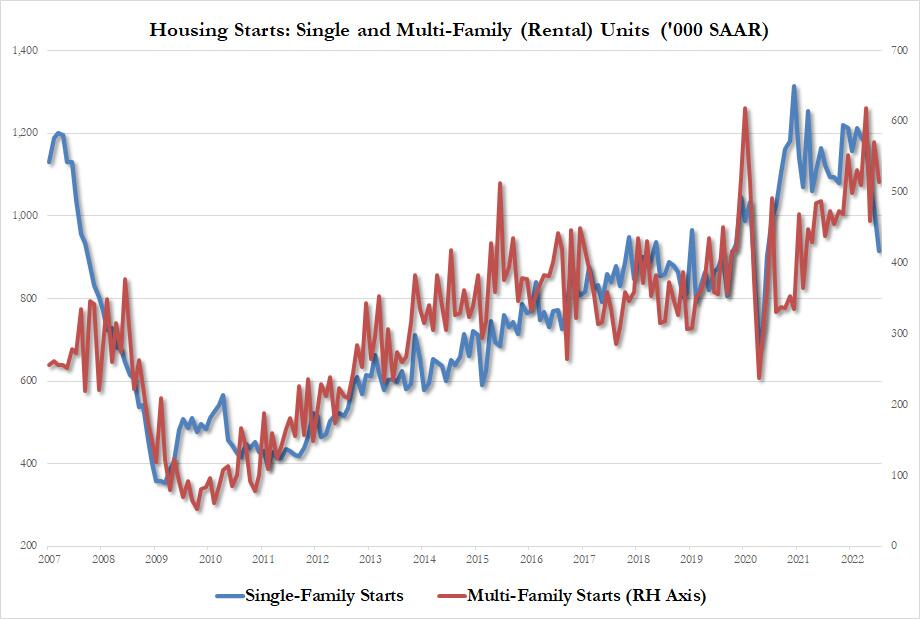

- 08:30: July Housing Starts, est. 1.53m, prior 1.56m

- July Housing Starts MoM, est. -2.0%, prior -2.0%

- July Building Permits, est. 1.64m, prior 1.69m, revised 1.7m

- July Building Permits MoM, est. -3.3%, prior -0.6%, revised 0.1%

- 09:15: July Industrial Production MoM, est. 0.3%, prior -0.2%

- July Capacity Utilization, est. 80.2%, prior 80.0%

- July Manufacturing (SIC) Production, est. 0.3%, prior -0.5%

DB’s Henry Allen concludes the overnight wrap

Here in the UK we’ve had quite a historic weather spell recently. Last month was the driest July in England since 1935, and a new record temperature just above 40°C was also recorded. But as this dry spell finally comes to an end, there are now weather warnings about thunderstorms over the coming days. My wife and I discovered this to our cost on our evening walk yesterday, when we hadn’t packed an umbrella and got soaked. One thing I hadn’t realised until watching the news the other day was that healthy grass actually absorbs water much quicker than parched grass – I had assumed like humans that the grass that’s been without water for days would drink it up rapidly. So while I’m not paid to give you my bad hunches on how weather works, the risk now is that the water just runs off the hard ground and leads to flooding. Let’s hope we can catch a break from this in the days ahead.

Markets were also struggling to catch a break yesterday thanks to a succession of disappointing data releases that brought the risks of a recession back into focus. That marks a shift in the dominant narrative over the last couple of weeks, when there had actually been a small but growing hope that central banks might be able to execute a soft landing, not least after the much stronger-than-expected US jobs report for July. But ultimately, a number of leading indicators are still moving in the wrong direction, and yesterday’s releases served as a reminder that hard landings have historically been the norm when starting from a position as unfavourable as the present one.

In terms of the specifics of those data releases, the more negative tone was set from the outset by the Chinese data we mentioned in yesterday’s edition, which showed that retail sales and industrial production for July had been weaker than expected by the consensus. But we then also got the Empire State manufacturing survey for August, which plunged to -31.3 (vs. 5.0 expected), thus also marking its worst performance since the GFC apart from April and May 2020 during the Covid lockdowns. Lastly, we then had the NAHB’s housing market index for August, which similarly fell to its lowest level since May 2020 at 49 (vs. 54 expected). That marked its 8th consecutive move lower, which comes against the backdrop of one of the most aggressive Fed tightening cycles in decades, with housing one of the most sensitive sectors to rate hikes.

Growing fears of a slowdown led to a decent risk-off move across multiple asset classes, but one of the places that was most evident was in oil prices, where both Brent crude (-3.11%) and WTI (-2.91%) underwent sizeable declines on the day. In fact on an intraday basis, Brent crude traded at $92.78 per barrel at its lows, which exactly matches its previous intraday low on August 5, and prior to that you’ve got to go back before Russia’s invasion of Ukraine in late February for the last time that oil prices were trading lower. That decline in oil prices was offered further support by the latest developments on the Iran nuclear deal, where Iran sent its response to the European Union’s proposed text to revive the deal. While the specific contents of the response are unknown, it’s been reported by the semi-official Iranian Students’ News Agency that Iran expects a response back from the EU within the next two days, so there could be tangible progress this week. Furthermore, Iran’s foreign minister said that an agreement with the US could be reached in the coming days. That trend towards weaker oil prices has continued this morning as well, with Brent crude down a further -0.87% at $94.27/bbl, and WTI down -0.62% at $88.86/bbl.

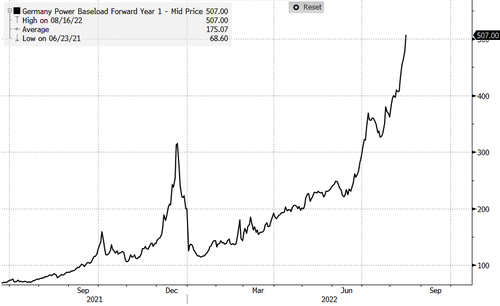

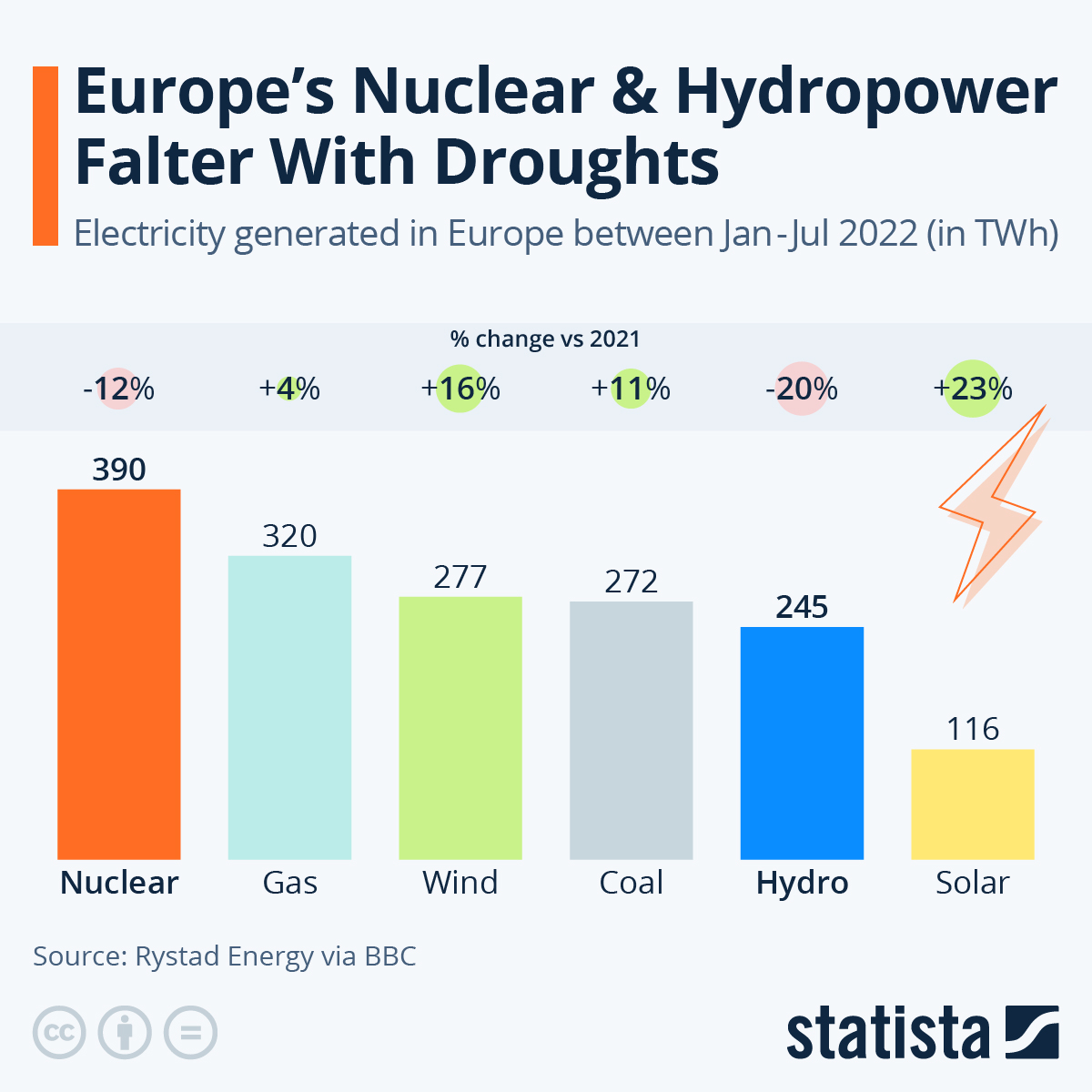

Whilst oil prices fell back yesterday, the seemingly inexorable move higher in European natural gas continued, with futures up +6.79% on the day to €220 per megawatt-hour, which is just shy of their March peak at €227. Prices have been bolstered by the latest European heatwave, which has seen rivers dry up and caused issues with fuel transportation, further compounding the continent’s existing woes on the energy side. That gloomy backdrop saw Germany’s government announce a levy of an extra 2.419 euro cents per kilowatt hour for natural gas, which comes as policymakers are hoping that measures to reduce demand will help the continent get through the winter. Meanwhile, German and French power prices for next year rose to fresh records yesterday, rising +3.67% and +3.24% respectively.

In light of the decline in oil prices and the more general risk-off tone, sovereign bonds rallied on both sides of the Atlantic yesterday, and yields on 10yr Treasuries came down -4.3bps to 2.79%. Inflation breakevens led the bulk of that decline amidst the moves lower in commodity prices, with the 10yr breakeven down by -2.9bps, whilst the 2s10s curve (+2.1bps) remained firmly in inversion territory at -40.0bps, even as it underwent a modest steepening. For Europe there were even larger declines in yields yesterday, with those on 10yr bunds (-8.8bps), OATs (-8.1bps) and BTPs (-6.5bps) all moving lower on the day, which came as investors moved to price in a less aggressive ECB hiking cycle over the coming months, with the June 2023 implied rate down by -9.9bps on the day. In overnight trading, yields on 10yr USTs (-0.9bps) have posted a further decline to 2.78% as we write.

One asset class that didn’t fit this pattern so well were equities yesterday, as they pared back their earlier losses to move higher on the day, building on a run of 4 consecutive weekly moves higher. In the US, the S&P had opened -0.54% lower, but reversed course to end the session up +0.40%, which brings its advances from its recent low in mid-June to more than +17% now. It was a fairly broad-based advance across sectors, and the NASDAQ posted a similar +0.62% gain as well, whilst in Europe, the STOXX 600 (+0.34%) also strengthened in the afternoon to post a 4th consecutive daily advance.

Those moves in US and European equities have been echoed in Asia this morning, with the Hang Seng (+0.12%), Shanghai Composite (+0.24%), CSI (+0.13%) and the Kospi (+0.31%) all edging higher in early trade. The main exception is the Nikkei (-0.08%), which has lost ground modestly after reaching a 7-month high in the previous session. That said, there are signs that equities may be losing momentum as well this morning, with futures on the S&P 500 (-0.12%) and the NASDAQ 100 (-0.12%) both pointing lower following their strong run of gains recently.

To the day ahead now, and data releases from the US include July’s industrial production, capacity utilisation, housing starts and building permits. In the UK, there’s unemployment for June, Germany has the ZEW survey for August and Canada has July’s CPI. Elsewhere, we’ll get earnings releases from Walmart and Home Depot.

(zerohedge)

END

AND NOW NEWSQUAWK

Equities firmer though curtailed post-ZEW, crude under pressure on JCPOA – Newsquawk US Market Open

TUESDAY, AUG 16, 2022 – 06:47 AM

- European bourses are firmer across the board after a relatively constructive APAC handover, Euro Stoxx 50 +0.4%, though off best levels post-ZEW.

- US futures are in contained ranges and pivoting the unchanged mark at this point in time, ES -0.2%; HD and WMT in focus.

- DXY has breached last week’s peak to the detriment of peers across the board, with EUR downside exacerbating this amid data.

- Core fixed benchmarks have seen a pullback from Monday’s best levels while UK and German supply was well received.

- Crude benchmarks pressure, but off worst levels and well within yesterday’s ranges, as the EU receives Iran’s response to the JCPOA draft.

- Looking ahead, US Building Permits/Housing Starts, Industrial Production. Earnings from Walmart.

As of 11:20BST/06:20ET

For the full report and more content like this check out Newsquawk.

Try a 14 day trial with Newsquawk and hear breaking trading news as it happens.

LOOKING AHEAD

- US Building Permits/Housing Starts, Industrial Production. Earnings from Walmart.

- Click here for the Week Ahead preview.

GEOPOLITICS

CHINA-TAIWAN

- China’s Taiwan Affairs Office sanctioned seven Taiwanese officials for supporting Taiwan independence, according to state media. Taiwan’s Foreign Ministry later stated regarding China’s sanctions and stated that they cannot accept threats, while President Tsai separately commented that peace and stability of the Taiwan Strait are critical to the stability of the global supply chain of high-tech products, according to Reuters.

RUSSIA-UKRAINE

- Russian diplomat said it is too dangerous for the IAEA mission to go through Kyiv to visit the Zaporizhzhia nuclear power station and that the IAEA mission cannot deal with the demilitarisation of the plant, according to Reuters.

- Russian Defence Ministry says that Sweden and Finland joining NATO will mean that the nation reviews its defence approaches, via Reuters.

IRAN

- Iran responded to the EU’s draft nuclear deal and expects a response in the next two days, according to a source cited by ISNA. It was also reported that an adviser to the Iranian negotiating delegation told Al-Jazeera they are not far from an agreement and chances of reaching a nuclear deal are very high.

- Iran’s response to the draft EU JCPOA text will probably fail to satisfy Western parties, particularly the US, according to Iran International; Iran wants further provisions around economic guarantees above the one-year exemption reportedly being offered. Adding that Iran has reportedly accepted the safeguarding proposal.

- EU says it consulting with the US on a way ahead for the Iranian nuclear deal.

- Senior Iranian official says Iran’s response to the European proposal is realistic and professional and includes important observations to secure its interests, according to Al Jazeera.

EUROPEAN TRADE

EQUITIES

- European bourses are firmer across the board after a relatively constructive APAC handover, Euro Stoxx 50 +0.4%, though off best levels post-ZEW.

- US futures are in contained ranges and pivoting the unchanged mark at this point in time, ES -0.2%; HD and WMT in focus.

- Home Depot Inc (HD) Q1 2023 (USD): EPS 5.05 (exp. 4.94), Revenue 43.79 (exp. 43.36bln); confirms FY22 guidance.

- Click here for more detail.

FX

- DXY breaches last week’s peak as Treasury yields rebound and Yuan weakens further amidst Chinese growth concerns, index up to 106.860 vs 106.810 on August 8, USD/CNY and USD/CNH approach 6.8000 and 6.8200 respectively.

- Euro stumbles after unexpected deterioration in German ZEW economic sentiment and Pound slips following mixed UK jobs and wage data, EUR/USD down to 1.0125 and Cable low 1.2000 area.

- Yen and Franc retreat as risk sentiment improves and bonds back off, USD/JPY tops 134.00 and USD/CHF above 0.9500.

- Kiwi cautious ahead of RBNZ, but Aussie holds up better post-RBA minutes flagging more hikes, NZD/USD eyes bids into 0.6300 and AUD/USD hovers just under 0.7000.

- Loonie underpinned awaiting Canadian CPI as crude prices stabilise to a degree, USD/CAD straddles 1.2900.

- Click herefor more detail.

Notable FX Expiries, NY Cut:

- Click here for more detail.

FIXED INCOME

- Debt futures retreat further from Monday’s lofty levels in corrective price action and as broad risk sentiment improves.

- Bunds down to 156.07 having been closer to 157.00, Gilts to 116.52 vs 116.99 earlier and 117+ yesterday, T-notes to 119-19 from almost 120-00.

- UK 2029 and German 2027 supply snapped up amidst given some yield concession.

- Click here for more detail.

COMMODITIES

- Crude benchmarks pressure, but off worst levels and well within yesterday’s ranges, as the EU receives Iran’s response to the JCPOA draft.

- Initial indications are that a deal is in reach, though, caveats/unknowns remain in focus – particularly the US’ response.

- EIA said US oil output from top shale regions in September is due to increase to the highest since March 2020, according to Reuters.

- Iran sets September Iranian light crude OSP to Asia at Oman/Dubai + USD 9.50/bbl, via Reuters.

- Major European zinc smelter (Nyrstar Budel) reportedly to shut due to elevated energy costs, via Bloomberg; will shut as of September 1st.

- Spot gold under modest pressure as the USD lifts, but still near the 50-DMA while base metals recoup from Monday’s data-driven pressure.

- Click here for more detail.

NOTABLE HEADLINES

- Czech central banker Frait says the current level of rates at 7% already creates restrictive monetary conditions.

- NBP’s Wnorowski says rates could peak between 6-7%.

NOTABLE DATA

- UK ILO Unemployment Rate (Jun) 3.8% vs. Exp. 3.8% (Prev. 3.8%); Claimant Count Unemployment Change (Jul) -10.5k (Prev. -20.0k)

- Average Week Earnings 3M YY (Jun) 5.1% vs. Exp. 4.5% (Prev. 6.2%); (Ex-Bonus) (Jun) 4.7% vs. Exp. 4.5% (Prev. 4.3%)