by harveyorgan · in Uncategorized · Leave a comment·Edit

Uncategorized · Leave a comment·Edit

GOLD; $1763.00 DOWN $12.00

SILVER: $19.81 DOWN 32 CENTS

ACCESS MARKET:

GOLD $1762.40

SILVER: $19.80

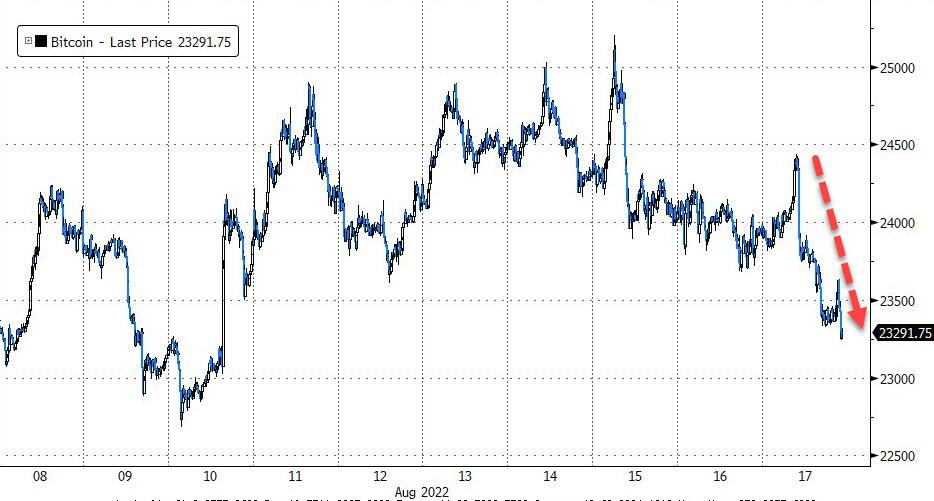

Bitcoin morning price: $23,758 DOWN 234

Bitcoin: afternoon price: $23,291. DOWN 701

Platinum price closing DOWN $11.00 AT$926.60

Palladium price; closing DOWN $16.15 at $2138.65

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: AUGUST 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,773.200000000 USD

INTENT DATE: 08/16/2022 DELIVERY DATE: 08/18/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 H GOLDMAN 2

132 C SG AMERICAS 13

624 H BOFA SECURITIES 8

657 C MORGAN STANLEY 16

661 C JP MORGAN 6

800 C MAREX SPEC 1 1

880 H CITIGROUP 1

905 C ADM 14

TOTAL: 31 31

MONTH TO DATE: 32,519

JPMorgan stopped: 6/31

_____________________________________________________________________________________

GOLD: NUMBER OF NOTICES FILED FOR AUGUST CONTRACT:

31 NOTICES FOR 3100 OZ //0.09642 TONNES

total notices so far: 32,519 contracts for 3,251,900 oz (101.147 tonnes)

SILVER NOTICES:

96 NOTICES FILED FOR 480,000 OZ/

total number of notices filed so far this month 923 : for 4,615,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $12.00

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD.

INVENTORY RESTS AT 993.94 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN $0.32 CENTS

AT THE SLV// ://A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 1.106 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 485.113 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 2405 CONTRACTS TO 144,314. AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG LOSS IN OI WAS ACCOMPLISHED WITH OUR $0.22 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.22) AND WERE SOMEWHAT SUCCESSFUL IN KNOCKING OFF SOME SPEC SILVER LONGS AS WE HAD A STRONG LOSS OF 1878 CONTRACTS ON OUR TWO EXCHANGES. HOWEVER WE HAD A SOME LIQUIDATION OF SPECULATOR SHORTS.

WE MUST HAVE HAD:

I) SOME SPECULATOR SHORT LIQUIDATIONS//CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A ZERO ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A FAIR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 95,000 OZ QUEUE JUMP / // V) GIGANTIC SIZED COMEX OI LOSS/(//SOME SPEC LIQUIDATION)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -535

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTACTS for 13 days, total 6550 contracts: 32.750 million oz OR 2.729 MILLION OZ PER DAY. (467 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 32.75 MILLION OZ

.

LAST 16 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 31.43 MILLION OZ (A LOT LESS THAN NORMAL//THE CROOKS ARE SCARED TO ISSUE MORE EFP’S)

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2405 WITH OUR $0.22 LOSS IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A ZERO SIZED EFP ISSUANCE CONTRACTS: 0 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /SOME BANKER ADDITIONS AND SOME SPEC SHORT LIQUIDATIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 95,000 OZ QUEUE JUMP // .. WE HAD A STRONG SIZED LOSS OF 2405 OI CONTRACTS ON THE TWO EXCHANGES FOR 12.025 MILLION OZ AS..THE SPECS STILL BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 96 NOTICE(S) FILED TODAY FOR 480,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 1626 CONTRACTS TO 453,960 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY:–70 CONTRACTS.

.

THE FAIR SIZED DECREASE IN COMEX OI CAME WITH OUR FALL IN PRICE OF $16.45//COMEX GOLD TRADING/TUESDAY / WE MUST HAVE HAD ADDITIONAL SPECULATOR SHORT SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERINGS//CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR AUGUST AT 98.367 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 19300 OZ//NEW STANDING 104.037 TONNES

YET ALL OF..THIS HAPPENED WITH OUR FALL IN PRICE OF $16.45 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 1346 OI CONTRACTS 4.186 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3042 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 453,960

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1346 CONTRACTS WITH 1626 CONTRACTS DECREASED AT THE COMEX AND 3042 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1346 CONTRACTS OR 4.186 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3042) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (1696): TOTAL GAIN IN THE TWO EXCHANGES 1346 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR AUGUST. AT 99.272 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 19300 oz. 3) ZERO/ LONG LIQUIDATION//// //.,4) FAIR SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST :

30,960 CONTRACTS OR 3,096,000 OZ OR 96.30 TONNES 13 TRADING DAY(S) AND THUS AVERAGING: 2326 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAY(S) IN TONNES: 96.30 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 96.30/3550 x 100% TONNES 2.70% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 96.30 TONNES (DRAMATICALLY FALLING AGAIN)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF SEPT., FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A GIGANTIC SIZED 2495 CONTRACT OI TO 144,314 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 0 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2405 CONTRACTS AND ADD TO THE 0 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF 2405 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 12.025 MILLION OZ

OCCURRED WITH OUR FALL IN PRICE OF $0.22

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 14.64 PTS OR 0.45% //Hang Sang CLOSED UP 91.93 OR 0.46% /The Nikkei closed UP 353.86 OR % 1.23. //Australia’s all ordinaires CLOSED UP 0.26% /Chinese yuan (ONSHORE) closed DOWN AT 6.7794//OFFSHORE CHINESE YUAN DOWN 6.7966// /Oil DOWN TO 86.40 dollars per barrel for WTI and BRENT AT 91939// / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1696 CONTRACTS TO 453,960 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED WITH OUR FALL OF $7.85 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (3042 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF AUGUST.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3042 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :3042 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3042 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED SIZED TOTAL OF 1346 CONTRACTS IN THAT 3042 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 1696 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR STRONG FALL IN PRICE OF GOLD $ 16.45. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING AUGUST (104.037),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.037 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $16.45) AND WERE SUCCESSFUL IN KNOCKING OFF SOME SPECULATOR LONGS // COMMERCIAL LONGS ADDED TO THE POSITIONS, BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS////// WE HAVE REGISTERED A FAIR SIZED LOSS OF 4.186 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR AUGUST (104.037 TONNES)…

WE HAD –70 CONTRACTS ADDED TO COMEX TRADES. THESE WERE ADDED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 1346 CONTRACTS OR 134,600 OZ OR 4.186 TONNES

Estimated gold volume 126,180/// extremely poor/

final gold volumes/yesterday 100,614/extremely poor

INITIAL STANDINGS FOR AUGUST ’22 COMEX GOLD //AUGUST 17

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 64,653.041 oz Brinks Manfra |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | 32,079.431 oz Brinks, HSBC |

| No of oz served (contracts) today | 31 notice(s) 3100 OZ 0.09642 TONNES |

| No of oz to be served (notices) | 929 contracts 92,900 oz 2.089 TONNES |

| Total monthly oz gold served (contracts) so far this month | 32,519 notices 3,251,900 OZ 101.147 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 2

i) Into Brinks: 98.241 oz

ii) Into HSBC: 31,981.190 oz

total deposits 32,079.431 oz

2 customer withdrawals:

i) Out of Manfra 98.241 oz

ii) Out of Brinks 64,554.800 oz

total: 64,653.041 oz

total in tonnes: 2.01 tonnes

Adjustments: dealer to customer //1

Brinks: 578.718 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 960 contracts having GAINED 171 contracts .

We had 22 notices served upon yesterday so we gained a HUMONGOUS 193 contracts or an additional 19300 oz will stand for delivery in this very active month of August.

.As promised, from this point on, we will now add to the amount of gold standing at the comex until the end of the month.

Sept. LOST 31 contracts to 3628 contracts.

October GAINED 132 contracts UP to 39,315

We had 31 notice(s) filed today for 3100 oz FOR THE AUGUST 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 31 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 6 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2022. contract month,

we take the total number of notices filed so far for the month (32,519) x 100 oz , to which we add the difference between the open interest for the front month of (AUGUST 960 CONTRACTS ) minus the number of notices served upon today 31 x 100 oz per contract equals 3,344,800 OZ OR 104.037 TONNES the number of TONNES standing in this active month of AUGUST.

thus the INITIAL standings for gold for the AUGUST contract month:

No of notices filed so far (32,519) x 100 oz+ (960) OI for the front month minus the number of notices served upon today (31} x 100 oz} which equals 3,344,800 oz standing OR 104.037 TONNES in this active delivery month of August.

TOTAL COMEX GOLD STANDING: 104.037 TONNES (A HUGE STANDING FOR AUGUST ( ACTIVE) DELIVERY MONTH)

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,318,414,091 oz 72.11 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 28,702,865.929 OZ

TOTAL REGISTERED GOLD: 14,505,435.039 OZ (451,18 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 14,197,430.890 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 12,187,021.0 OZ (REG GOLD- PLEDGED GOLD) 379.06 tonnes//rapidly declining

END

SILVER/COMEX/AUGUST 17

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 583,880.900 oz Delaware Brinks JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 159,475.740 oz Loomis |

| No of oz served today (contracts) | 96 CONTRACT(S) 480,000 OZ) |

| No of oz to be served (notices) | 52 contracts (260,000 oz) |

| Total monthly oz silver served (contracts) | 923 contracts 4,615,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) Into Loomis: 159,475.740 0z

total deposit: 159,475.740 oz

JPMorgan has a total silver weight: 173.408 million oz/332.605 million =52.13% of comex

Comex withdrawals: 3

i) Out of Brinks 1951.000 oz

ii) Out of JPMorgan: 580,932.700 oz

iii) out of Delaware: 997.200 oz

total: 583,880.900 oz

adjustments: 1 customer to dealer

HSBC: 451,088.200 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 55.478 MILLION OZ

TOTAL REG + ELIG. 332.605 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR AUGUST

silver open interest data:

FRONT MONTH OF AUGUST OI: 148 CONTRACTS HAVING GAINED 19 CONTRACTS. WE HAD 0 NOTICES FILED ON TUESDAY

SO WE GAINED 19 CONTRACTS OR AN ADDITIONAL 95,000 OZ OF SILVER WILL STAND FOR DELIVERY. THE AMOUNT STANDING

WILL NOW INCREASE//(OR REMAIN CONSTANT) ON A DAILY BASIS AS BANKERS SCOUR THE PLANET FOR BADLY NEEDED SILVER.

SEPTEMBER HAD A LOSS OF 4819 CONTRACTS DOWN TO 58,228

OCTOBER GAINED 8 CONTRACTS TO STAND AT 114

CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 96 for 480,000 oz

Comex volumes:53,774// est. volume today// fair

Comex volume: confirmed yesterday: 52,184 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 923 x 5,000 oz = 4,615,000 oz

to which we add the difference between the open interest for the front month of AUGUST(148) and the number of notices served upon today 96 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST./2022 contract month: 923 (notices served so far) x 5000 oz + OI for front month of AUGUST (148) – number of notices served upon today (96) x 5000 oz of silver standing for the AUGUST contract month equates 4,875,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

AUGUST 17/WITH GOLD DOWN $12.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 992.20 TONNES

AUGUST 16/WITH GOLD DOWN $7.85: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 993.94 TONNES

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

AUGUST 10//WITH GOLD UP $2.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES

AUGUST 9/WITH GOLD UP $6.70: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES.

AUGUST 8/WITH GOLD UP $13.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FORM THE GLD//INVENTORY RESTS AT 999.16 TONNES

AUGUST 5/WITH GOLD DOWN $14.25: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .33 TONNES FROM THE GLD////INVENTORY RESTS AT 1000.32 TONNES

AUGUST 4 WITH GOLD UP $29.00 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES FROM THE GLD///INVENTORY REST AT 1000.65 TONNES

AUGUST 2/WITH GOLD UP $3.70; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD//INVENTORY RESTS AT 1002.97 TONNES//

AUGUST 1/WITH GOLD UP $5.75: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 29//WITH GOLD UP $12.50; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1005.29 TONNES

JULY 28/WITH GOLD UP $31.25; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 27.//WITH GOLD UP $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 26/WITH GOLD DOWN $1.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.29 TONNES

JULY 25/WITH GOLD DOWN $7.85: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 1005.87 TONNES

JULY 22/WITH GOLD UP $17.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 21/WITH GOLD UP $11.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.101 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.87 TONNES

JULY 20/WITH GOLD DOWN $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1009.06 TONNES

JULY 19/WITH GOLD DOWN $.35 :BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.22 TONNES FROM THE GLD//INVENTORY RESTS AT 1009.06 TONNES

JULY 18/WITH GOLD UP $7.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.28 TONNES

JULY 15/WITH GOLD DOWN $3.75:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD///INVENTORY RESTS AT 1016.89 TONNES//

JULY 14/WITH GOLD DOWN $28.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD//INVENTORY RESTS AT 1019.79 TONNES

JULY 13/WITH GOLD UP $10.55:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD//INVENTORY RESTS AT 1021.53TONNES

JULY 12/WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESS AT 1023.27 TONNES

GLD INVENTORY: 992.20 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 17/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.106 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.113 MILLION OZ//

AUGUST 16/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 486.219 MILLION OZ/

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 10/WITH SILVER UP 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 9/WITH SILVER DOWN 25 CENTS TODAY: TWO CHANGES IN SILVER INVENTORY AT THE SLV: FIRST: A DEPOSIT OF 461,000 OZ INTO THE SLV AND THEN A WITHDRAWAL OF 1.014 MILLION OZ..//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 8/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 5/WITH SILVER DOWN 28 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 922,000 OZ FROM THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 4 WITH SILVER UP 21 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 527,000 OZ FROM THE SLV////INVENTORY RESTS AT 486.634 MILLION OZ

AUGUST 2/WITH SILVER DOWN 21 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.504 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.161 MILLION OZ//

AUGUST 1/WITH SILVER UP 17 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE GLD: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 483.657 MILLION OZ//

JULY 29/WITH SILVER UP 30 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 461,000 OZ FROM THE SLV..//INVENTORY RESTS AT 483.657 MILLION OZ/

JULY 28/WITH SILVER UP $1.24 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 484.118 MILLION OZ/

JULY 27/.WITH SILVER UP 4 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL 11.479 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 484.118MILLION OZ//

JULY 26/WITH SILVER UP 16 CENTS: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.504 MILLION OZ FROM THE SLV//: //INVENTORY RESTS AT 495.597 MILLION OZ//

JULY 25/WITH SILVER DOWN 24 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.383 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 499.101 MILLION OZ//

JULY 22/WITH SILVER DOWN 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 500.484 MILLION OZ//

JULY 21/WITH SILVER UP 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.19 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 500.484MILLION OZ/

JULY 20/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 8.253 MILLION OZ FORM THE SLV/INVENTORY RESTS AT 507.585 MILLION OZ//

JULY 19/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ//

JULY 18/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 4.995 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ.

JULY 15/WITH SILVER UP 31 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 3.226 MILLION OZ FORM THE SLV//INVENTORY RESTS AT 510.443 MILLIONOZ//

JULY 14/WITH SILVER DOWN 88 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 OZ FROM THE SLV// //INVENTORY RESTS AT 513.671 MILLION OZ

JULY 13/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SV//INVENTORY RESTS AT 514.501 MILLION OZ.

JULY 12/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.228 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 514.501 MILLION OZ//

CLOSING INVENTORY 485.113 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff Pans Joe Biden’s Unwarranted Inflation Victory Lap

WEDNESDAY, AUG 17, 2022 – 07:20 AM

Peter Schiff appeared on the Newsmax Saturday Report along with former Rep. Peter King (R-NY) to talk about President Joe Biden’s unwarranted inflation victory lap.

The CPI for July came in slightly cooler than June’s sizzling 9.1%. But even at 8.5%, CPI remains near 40-year highs. But Biden focused on the unchanged month-on-month CPI to declare victory over inflation and claimed he’s building “an economy that works for everyone.”

Host Rita Cosby kicked off the interview by asking Rep. King his views on funding for 87,000 IRS agents in the “Inflation Reduction Act.” King said the spending in the bill will be bad enough and that it will cause “long-term consequences,” but the beefed-up IRS will cause even more damage. He warned the agency will be weaponized to go after political opponents.

Peter Schiff went a step further and said he doesn’t even think the US should have an income tax.

I think the government should fund itself with excise taxes. I don’t think subjecting Americans to these types of audits is the type of country that the founding fathers envisioned when they created this republic.”

Schiff also said he doesn’t think the IRS will use its new manpower to go after billionaires and millionaires.

They can avoid taxes legally. It’s the middle class, it’s small business owners, it’s people who are self-employed — that’s who’s in the IRS crosshairs. And their going to be hit not only with huge tax bills, but interest and penalties that will actually exceed what they owed in taxes.”

CBO analysis of the “Inflation Reduction Act” found that it would collect some $20 billion from people making under $400,000 per year. That breaks a Democrat promise not to raise taxes on people making less than $400K. But Schiff said it’s worse than that.

The inflation tax hits hardest those who earn the least. The fact that Biden is doing a victory dance, I want to throw a flag for taunting.”

Schiff pointed out that while gasoline prices fell last month, driving CPI lower, food prices went up, along with costs in a lot of other categories.

So, it wasn’t a good month. It was another bad month for consumers. It was just masked by a temporary drop in gasoline prices for one month.”

Rep. King wrapped up the interview, saying Biden is “going against reality.” He also pointed out that even though the president can’t control everything in the economy, “the wounds we suffered today are all self-inflicted by Joe Biden.”

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

3.Chris Powell of GATA provides to us very important physical commentaries

A good read

(Craig Hemke/GATA)

Craig Hemke at Sprott Money: The convicted criminals of JPMorgan

Submitted by admin on Tue, 2022-08-16 21:07Section: Daily Dispatches

9:25p ET Tuesday, August 16, 2022

Dear Friend of GATA and Gold:

Writing tonight at Sprott Money, Craig Hemke of the TF Metals Report notes the inability of the U.S. Commodity Futures Trading Commission to discover the manipulation of the gold and silver markets for which the U.S. Justice Department just achieved conviction of two former traders at bullion bank JPMorganChase.

Hemke adds that one of those former traders, Michael Nowak, was on the Board of Directors of the London Bullion Market Association until he was indicted — whereupon he hired as his criminal defense lawyer the former head of the CFTC’s ineffectual enforcement division, David Meister.

It’s called “regulatory capture” and embodies the comprehensive corruption of the U.S. governemt’s so-called financial regulators.

Hemke’s analysis is headlined “The Convicted Criminals of JPMorgan” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/blog/The-Convicted-Criminals-of-JP-Morgan-Craig-Hemke-August-16-2022

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

This is a very important read: Russian finance minister wants to break the LBMA monopoly on gold by creating a new international standard , the Moscow World Standard

by using physical gold to fix prices. This is where we are heading

(Vzglyad/Institute for Social Economic and Political Studies/Moscow/GATA)

Russian government plans to ‘break the LBMA monopoly’ on gold

Submitted by admin on Tue, 2022-08-16 11:30Section: Daily Dispatches

Treasury Proposes to Create Alternative to the London Precious Metals Standard

From Vzglyad

Institute for Socio-Economic and Political Studies, Moscow

Thursday, July 28, 2022

Via Google Translator

https://vz.ru/amp/news/2022/7/28/1169741.html

A new international standard for the precious metals market, the Moscow World Standard (MWS), should be created to become an alternative to the standard of the London Bullion Market Association (LBMA), the Russian Finance Ministry said.

A letter from the Ministry of Finance to industry participants says that “an independent international infrastructure” is needed to “normalize the functioning of the precious metals industry.”

According to the department, it is “critically necessary” to create it, RIA Novosti reports.

It is proposed to “place a specialized international precious metals exchange headquartered in Moscow” using the “new international standard MWS” as the “basis of the structure.” It is also proposed to establish a Price Fixing Committee. Subject to the application of the MWS standard, it will include the central banks and the largest banks of the Eurasian Economic Union countries represented in the precious metals market.

According to the Russian department, it is necessary to “bet on fixing prices in the national currencies of the key member countries, or on new units of international settlements, such as the new unit of settlements proposed by the president of Russia within the member countries of the BRICS organization.”

The Ministry of Finance wants to make membership in this organization attractive to all foreign market participants, especially China, India, and Venezuela, Peru, and other countries of South America, as well as Africa. The agency expects that such a move will quickly break the LBMA monopoly and ensure the stable development of the industry.

Recall that the Council of the European Union approved the seventh package of anti-Russian sanctions, including a partial embargo on gold, blacklisting 55 individuals and legal entities, expanding the list of dual-use goods prohibited from import. The largest producer of primary silver and the second-largest gold producer in Russia, Polymetal, is exploring the possibility of selling Russian assets.

END

4. OTHER GOLD/SILVER COMMENTARIES

5.OTHER COMMODITIES: USA/COTTON

end

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

end

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7794

OFFSHORE YUAN: 6.7966

HANG SENG CLOSED UP 91.93 PTS OR 0.46%

2. Nikkei closed UP 353.86 OR 1.23%

3. Europe stocks CLOSED ALL RED

USA dollar INDEX UP TO 106.66/Euro FALLS TO 1.0160

3b Japan 10 YR bond yield: RISES TO. +.183/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 135.15/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.105%/Italian 10 Yr bond yield RISES to 3.331% /SPAIN 10 YR BOND YIELD RISES TO 2.24%…

3i Greek 10 year bond yield RISES TO 3.495//

3j Gold at $1769.10 silver at: 19.85 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 60/100 roubles/dollar; ROUBLE AT 60.31

3m oil into the 86 dollar handle for WTI and 91 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 135.15DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9532– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9684well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.893 UP 7 BASIS PTS

USA 30 YR BOND YIELD: 3.148 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.96

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

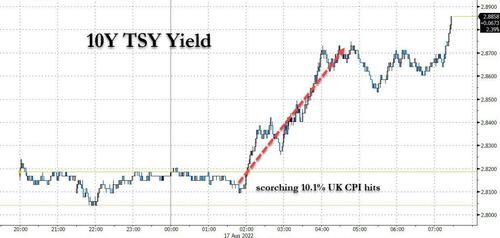

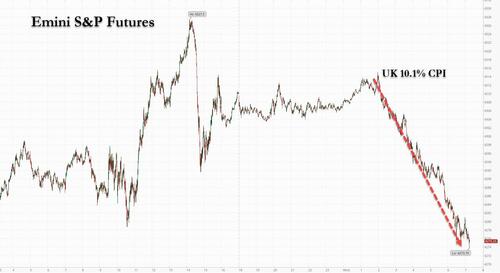

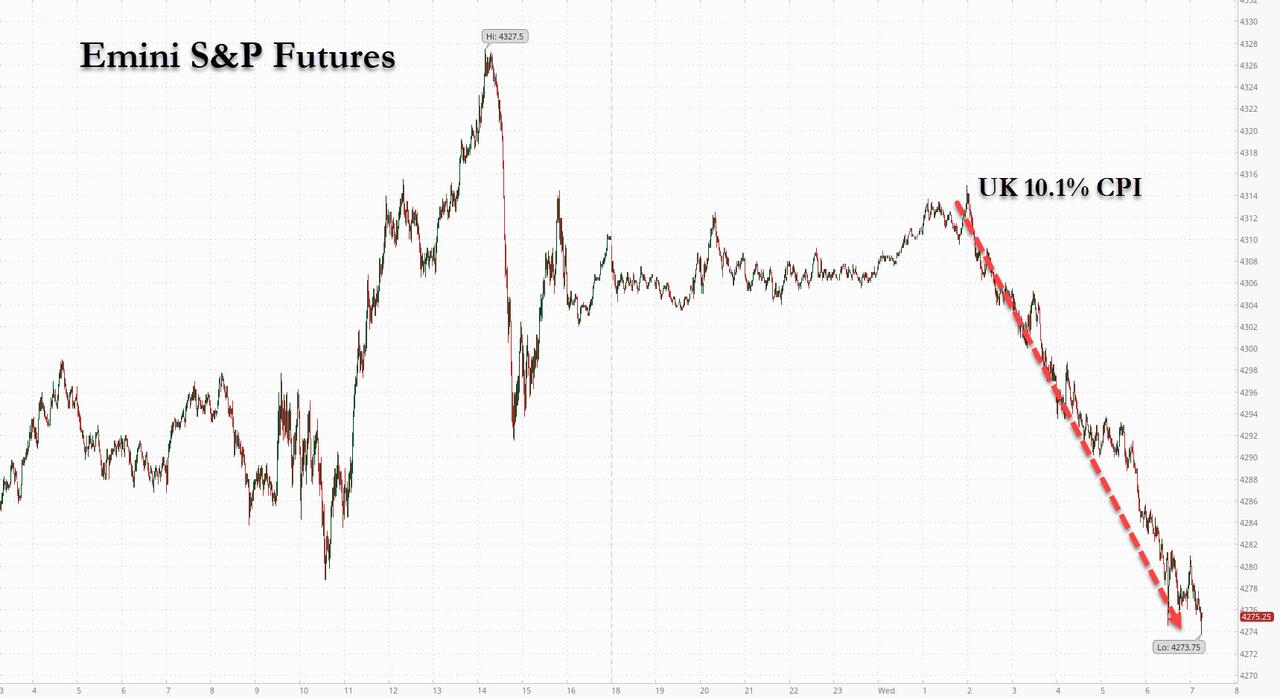

Futures Tumble After UK Double-Digit Inflation Shock Sparks Surge In Yields

WEDNESDAY, AUG 17, 2022 – 07:55 AM

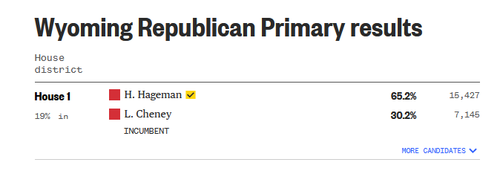

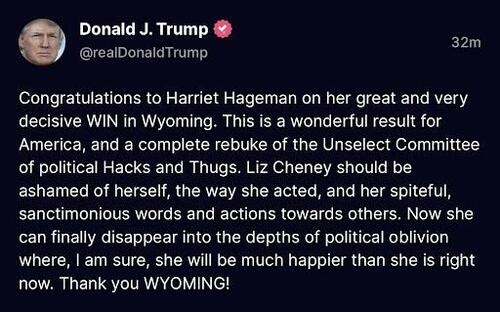

Futures were grinding gingerly higher, perhaps celebrating the end of the Cheney family’s presence in Congress, and looked set to re-test Michael Hartnett bearish target of 4,328 on the S&P (which marked the peak of yesterday’s meltup before a waterfall slide lower when spoos got to within half a point of the bogey), when algos and the few remaining carbon-based traders got a stark reminder that central banks will keep hammering risk assets after the UK reported a blistering CPI print, which at a double digit 10.1% was not only higher than the highest forecast, but was the highest in 40 years.

The print appeared to shock markets out of their month-long levitating complacency, and yields – both in the UK and the US – spiked…

… and with yields surging, futures had no choice but to notice and after trading at session highs just before the UK CPI print, they have since tumbled more than 40 points and were last down 0.85% or 37 points to 4,271.

Nasdaq 100 futures retreated 0.9% signaling a selloff in technology names will continue. The dollar rose as investors awaited the minutes of the Fed’s last policy meeting for clues on policy makers’ sensitivity to weaker economic data.

In US premarket trading, retail giant Target slumped 4% after reporting earnings that missed expectations despite still predicting a rebound. Applied Materials and PayPal dropped at least 1.3%. Tech stocks are the forefront of the growing pessimism over equity valuations on the back of Fed rate increases. The S&P 500 had posted a small gain on Tuesday, aided by earnings reports from retailers Walmart Inc. and Home Depot. Here are some of the other biggest U.S. movers today:

- Manchester United (MANU US) rises as much as 17% in US premarket trading before trimming most of the gains, after Tesla CEO Elon Musk said he was buying the English football club but later added that he was joking.

- Hill International (HIL US) shares rise 61% in premarket trading hours after it announced Global Infrastructure Solutions will commence an all-cash tender offer for $2.85/share in cash, representing a premium of 63% to the last closing price.

- BioNTech (BNTX US) was initiated with a market perform recommendation at Cowen, which expects demand for Covid-19 vaccines to mirror annual flu trends as the pandemic enters its endemic phase.

- Bed Bath & Beyond (BBBY US) shares surge 20% in premarket trading, putting the stock on track for its sixth day of gains. The home-goods company has helped reinvigorate a wave of meme stock buying

- Agilent (A US) saw its price target boosted at brokers as analysts say the scientific testing equipment maker’s results were strong thanks to growth in biopharma and a recovery in China, while the company’s guidance was on the conservative side. Shares rose .

- Jefferies initiated coverage of Waldencast Plc (WALD US) class A with a buy recommendation as analyst Stephanie Wissink sees 29% upside potential.

- Sea Ltd. (SE US) ADRs slipped as much as 2.1% in US premarket trading, extending Tuesday’s declines, as Morgan Stanley cut its PT on expectations of slowing growth at the Shopee owner’s e-commerce business in the third quarter.

- Weber (WEBR US) downgraded to sell from neutral at Citi, which says there are too many concerns to remain on the sidelines, including a decline in point-of-sale traffic and macro factors like inflation weighing on consumer demand

In the past two months, US stocks rallied on signs of peaking inflation and an earnings-reporting season that saw four out of five companies meeting or beating estimates. Boosted by relentless systematic (CTA) buying and retail-driven short squeezes, as well as a surge in buybacks, stocks recovered more than 50% of the bear market retracement. Yet, continuing rate hikes and the likelihood of a recession in the world’s largest economy are weighing on sentiment. Meanwhile, concern is growing that Fed rate setters will remain focused on the fight against inflation rather than supporting growth.

“We expect the FOMC minutes to have a hawkish tilt,” Carol Kong, strategist at Commonwealth Bank of Australia Ltd., wrote in a note. “We would not be surprised if the minutes show the FOMC considered a 100 basis-point increase in July.”

In Europe, the Stoxx 600 fell after a strong start amid signs the continent’s energy crisis is worsening. Benchmark natural-gas futures jumped as much as 5.1% on expectations the hot weather will boost demand for cooling. In the UK, consumer-price growth jumped to 10.1%, sending gilts tumbling. Real estate, retailers and miners are the worst performing sectors. The Stoxx 600 Real Estate Index declined 2%, making it the worst-performing sector in the wider European market, as focus turned to UK inflation that soared to double digits for the first time in four decades and also to today’s FOMC minutes. German and Swedish names almost exclusively account for the 10 biggest decliners. TAG Immobilien drops 5.4%, Wallenstam is down 4.7%, Castellum falls 4% and LEG Immobilien declines 3.3%. The sector tumbles on rising bond yields, with 10y Bund yield up 11bps, and dwindling demand for Swedish real estate amid rising rates.

Earlier on Wednesday, stocks rose in Asia amid speculation that China may deploy more stimulus to shore up its ailing economy while Japanese exporters were boosted by a weaker yen. After a string of weak data driven by a property-sector slump and Covid curbs, China’s Premier Li Keqiang asked local officials from six key provinces that account for 40% of the economy to bolster pro-growth measures. The MSCI Asia Pacific Index advanced as much as 0.8%, with consumer-discretionary and industrial stocks such as Japanese automakers Toyota and Honda among the leaders on Wednesday. The benchmark Topix erased its year-to-date loss. Chinese food-delivery platform Meituan also rebounded after dropping more than 9% in the previous session on a Reuters report that Tencent may divest its stake in the firm. Chinese stocks erased declines early in the day, as investors hoped for more economic stimulus after a surprise rate cut on Monday failed to excite the market. Premier Li Keqiang has asked local officials from six key provinces that account for about 40% of the country’s economy to bolster pro-growth measures.

“I believe policymakers have the tools to prevent a hard landing if needed,” Kristina Hooper, chief global market strategist at Invesco, said in a note. “I find investors are overly pessimistic about Chinese stocks — which means there is the potential for positive surprise.” Asia’s stock benchmark is trading at mid-June levels as traders attempt to determine the trajectory of interest-rate hikes and economic growth globally — as well as the impact of China’s property crisis and Covid policies. Meanwhile, minutes of the US Federal Reserve’s July policy meeting, out later Wednesday, will be carefully parsed. New Zealand stocks closed little changed as the country’s central bank raised interest rates by a half percentage point for a fourth-straight meeting. Australia’s S&P/ASX 200 index rose 0.3% to close at 7,127.70, supported by materials and consumer discretionary stocks. South Korea’s benchmark missed out on the rally across Asian equities, as losses by large-cap exporters weighed on the measure

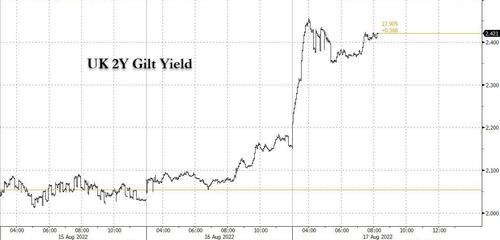

In FX, the Bloomberg Dollar Spot Index rose as the dollar gained versus most of its Group-of-10 peers. The pound was the best G-10 performer while gilts slumped, led by the short end and sending 2-year yields to their highest level since 2008, after UK inflation accelerated more than expected in July. The yield curve inverted the most since the financial crisis as traders ratcheted up bets on BOE rate hikes in money markets, wagering on 200 more basis points of hikes by May. The euro traded in a narrow range against the dollar while the region’s bonds slumped, led by the front end. Scandinavian currencies recovered some early European session losses while the aussie, kiwi and yen extended their slide in thin trading. EUR/NOK one-day volatility touched a 15.12% high before paring ahead of Norges Bank’s meeting Thursday where it may have to raise rates by a bigger margin than indicated in June given Norway’s inflation exceeded forecasts for a fourth straight month, hitting a new 34-year high. Consumer sentiment in Norway fell to the lowest level since data began in 1992, according to Finance Norway. New Zealand’s dollar and bond yields both rose in response to the Reserve Bank hiking rates by 50bps, while flagging concern about labor market pressures and consequent wage inflation; the currency subsequently gave up gains in early European trading. The Aussie slumped after data showing the nation’s wages advanced at less than half the pace of inflation in the three months through June, backing the Reserve Bank’s move to give itself more flexibility on interest rates.

In rates, treasuries held losses incurred during European morning as gilt yields climbed after UK inflation rose more than forecast. US 10-year around 2.87% is 6.5bp cheaper on the day vs ~13bp for UK 10-year; UK curve aggressively bear-flattened following inflation data, with long-end yields rising about 10bp. Front-end UK yields remain cheaper by ~20bp, off session highs, leading a global government bond selloff. US yields are higher on the day by by 4bp-7bp; focal points of US session are 20-year bond auction and FOMC minutes release an hour later. Treasury auctions resume with $15b 20-year bond sale at 1pm ET; WI 20-year yield at around 3.35% is ~7bp richer than July’s sale, which stopped 2.7bp through the WI level.

In commodities, oil fluctuated between gains and losses, and was in sight of a more than six-month low — reflecting lingering worries about a tough economic outlook amid high inflation and tightening monetary policy. Spot gold is little changed at $1,774/oz

Looking at the day ahead, the FOMC minutes from July will be the main highlight, and the other central bank speaker will be Fed Governor Bowman. Otherwise, earnings releases include Target, Lowe’s and Cisco Systems, and data releases include US retail sales and UK CPI for July.

Market Snapshot

- S&P 500 futures down 0.3% to 4,293.00

- STOXX Europe 600 little changed at 443.30

- MXAP up 0.5% to 163.48

- MXAPJ up 0.2% to 530.38

- Nikkei up 1.2% to 29,222.77

- Topix up 1.3% to 2,006.99

- Hang Seng Index up 0.5% to 19,922.45

- Shanghai Composite up 0.4% to 3,292.53

- Sensex up 0.5% to 60,168.83

- Australia S&P/ASX 200 up 0.3% to 7,127.68

- Kospi down 0.7% to 2,516.47

- German 10Y yield little changed at 1.06%

- Euro little changed at $1.0178

- Gold spot down 0.0% to $1,775.21

- U.S. Dollar Index little changed at 106.50

Top Overnight News from Bloomberg

- More market prognosticators are alighting on the idea of benchmark Treasury yields sliding to 2% if the US succumbs to a recession. That’s an out-of-consensus call, compared with Bloomberg estimates of about a 3% level by the end of this year and similar levels through 2023. But it’s a sign of how growth worries are forcing a rethink in some quarters

- The euro-area economy grew slightly less than initially estimated in the second quarter as signs continue to emerge that momentum is unraveling. Output rose 0.6% from the previous three months between April and June, compared with a preliminary reading of 0.7%, Eurostat said Wednesday

- Egypt became a prime destination for hot money by tethering its currency and boasting the world’s highest interest rates when adjusted for inflation

- Norway’s $1.3 trillion sovereign wealth fund, the world’s largest, posted its biggest loss since the pandemic as rate hikes, surging inflation and Russia’s invasion of Ukraine spurred volatility. It lost an equivalent of $174 billion in the six months through June, or 14.4%

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks just about shrugged off the choppy lead from the US where markets were tentative amid mixed data signals and strong retailer earnings, but with gains capped overnight ahead of the FOMC Minutes and as participants digested another 50bps rate hike by the RBNZ. ASX 200 swung between gains and losses with the index indecisive amid a slew of earnings and with strength in the consumer sectors offset by underperformance in tech, energy and healthcare. Nikkei 225 climbed above the 29,000 level with the index unfazed by mixed data releases in which Machinery Orders disappointed although both Exports and Imports topped forecasts. Hang Seng and Shanghai Comp were somewhat varied with Hong Kong led higher by tech amid plenty of attention on Meituan after reports its largest shareholder Tencent could reduce all or the bulk of its shares in the Co. which a Tencent executive later refuted, while the mainland was less decisive amid headwinds from the ongoing COVID situation and with power restrictions disrupting activity in Sichuan, although reports also noted that Chinese Premier Li told top provincial officials that they must have a sense of urgency to consolidate the economic recovery and reiterated to step up macro policies.

Top Asian News

- RBNZ hiked the OCR by 50bps to 3.00%, as expected, while it stated that conditions need to continue to tighten and they agreed that maintaining the current pace of tightening remains the best means. RBNZ also agreed that further increases in the OCR were required to meet the remit objective and that domestic inflationary pressures had increased since May. Furthermore, the RBNZ raised its projections for the OCR and inflation with the OCR seen at 3.69% in Dec. 2022 (prev. 3.41%) and at 4.1% for both Sept. 2023 and Dec. 2023 (prev. 3.95%), while it sees annual CPI at 4.1% by Sept. 2023 (prev. 3.0%).

- RBNZ Governor Orr stated at the press conference that they are not forecasting a recession but expected below-potential growth amid subdued consumer spending. Governor Orr also stated that they did not discuss a 75bps rate hike today and that 50bps moves have been orderly and sufficient, while he added that getting rates to 4% would buy comfort for the policy committee and that a Cash Rate of around 4% is unambiguously above neutral and sufficient to meet the inflation mandate.

- Chongqing, China is to curb power use for eight days for industry.

- China’s Infrastructure Boom Gets Swamped by Property Woes

- Tencent 2Q Revenue Misses Estimates

- Hong Kong Denies Democracy Advocates Security Law Jury Trial

- UN Expert Says Xinjiang Forced Labor Claims ‘Reasonable’

- Singapore’s COE Category B Bidding Hits New Record

- Delayed Deals Add to Floundering Singapore IPO Market: ECM Watch

European bourses have dipped from initial mixed/flat performance and are modestly into negative territory, Euro Stoxx 50 -0.5%. Stateside, futures are under similar pressure awaiting fresh corporate updates and the July FOMC Minutes, ES -0.6%. Fresh drivers relatively limited throughout the session with known themes in play and focus on upcoming risk events; stocks also suffering on further hawkish yield action. Lowe’s Companies Inc (LOW) Q1 2023 (USD): EPS 4.68 (exp. 4.58), Revenue 27.47 (exp. 28.12bln); expect FY22 total & comp. sales at bottom-end of outlook range, Operating Income and Diluted EPS at top-end. Target Corp (TGT) Q1 2023 (USD): EPS 0.39 (exp. 0.72), Revenue 26.0bln (exp. 26.04bln); current trends support prior guidance.

Top European News

- German Gas to Last Less Than 3 Months if Russia Cuts Supply

- European Gas Surges Again as Higher Demand Compounds Supply Pain

- Entain Falls; Citi Views Fine Negatively but Notes Steps by Firm

- UK Inflation Hits Double Digits for the First Time in 40 Years

- Crypto.com Receives Registration as UK Cryptoasset Provider

FX

- Greenback underpinned ahead of US retail sales data and FOMC minutes, DXY holds tight around 106.500.

- Pound pegged back after spike in wake of stronger than expected UK inflation metrics, Cable hovers circa 1.2100 after fade into 1.2150.

- Kiwi retreats following knee jerk rise on the back of hawkish RBNZ hike, NZD/USD near 0.6300 from 0.6380+ overnight peak.

- Aussie undermined by marginally softer than anticipated wage prices and lower RBA tightening bets in response, AUD/USD well under 0.7000 vs 0.7026 at one stage.

- Yen weaker as yield differentials widen again, but Euro cushioned by more pronounced EGB reversal vs USTs, USD/JPY probes 21 DMA just below 135.00, EUR/USD bounces from around 1.0150 towards 1.0200.

- Loonie and Nokkie soft amidst latest slippage in oil, USD/CAD closer to 1.2900 than 1.2800, EUR/NOK nudging 9.8600 within 9.8215-9.8740 range.

Fixed Income

- Debt retracement ongoing and gathering pace ahead of Wednesday’s key risk events.

- Bunds now closer to 154.00 than 156.00 and 157.00 only yesterday, Gilts not far from 114.50 vs almost 116.00 and 117.00+ earlier this week and T-note sub-119-00 vs 119-31 at best on Monday.

- Sonia strip hit hardest as markets price in aggressive BoE hikes in response to UK inflation data toppy already elevated expectations.

Commodities

- Crude benchmarks are currently little changed overall, having recovered from a bout of initial pressure; newsflow thin awaiting fresh JCPOA developments

- Spot gold is little changed overall but with a slight negative bias as the USD remains resilient and outpaces the yellow metal as the haven of choice.

- Aluminium is the clear outperformer amid updates from Norsk Hydro that they are shutting production at their Slovalco site (175k/T year) by end-September, due to elevated energy prices.

- OPEC Sec Gen says he sees a likelihood of an oil-supply squeeze this year, open for dialogue with the US. Still bullish on oil demand for 2022. Too soon to call the outcome of the September 5th gathering. Spare capacity at around the 2-3mln BPD mark, “running on thin ice”.

- US Private Inventory Data (bbls): Crude -0.4mln (exp. -0.3mln), Cushing +0.3mln, Gasoline -4.5mln (exp. -1.1mln), Distillates -0.8mln (exp. +0.4mln).

- Shell (SHEL LN) announced it is to shut its Gulf of Mexico Odyssey and Delta crude pipelines for two weeks in September for maintenance, according to Reuters.

- Uniper (UN01 GY) says the energy supply situation in Europe is far from easing and gas supply in winter remains “extremely challenging”.

- China sets the second batch of the 2022 rare earth mining output quota at 109.2k/T, via Industry Ministry; smelting/separation quota 104.8k/T.

Geopolitics

- China’s military is to partake in a military exercise in Russia, their participation has nothing to do with the international situation.

- Taiwan’s Defence Ministry says they have detected 21 Chinese aircraft and five ships around Taiwan on Wednesday, via Reuters.

- Iran is calling on the US to free jailed Iranian’s, says they are prepared for prisoner swaps, via Fars.

US Event Calendar

- 07:00: Aug. MBA Mortgage Applications, prior 0.2%

- 08:30: July Retail Sales Advance MoM, est. 0.1%, prior 1.0%

- 08:30: July Retail Sales Ex Auto MoM, est. -0.1%, prior 1.0%

- 08:30: July Retail Sales Control Group, est. 0.6%, prior 0.8%

- 10:00: June Business Inventories, est. 1.4%, prior 1.4%

- 14:00: July FOMC Meeting Minutes

DB’s Tim Wessel concludes the overnight wrap

Starting in Europe, where the looming energy crisis remains at the forefront. An update from our team, who just published the fourth edition of their indispensable gas monitor (link here), where they note the surprisingly fast rebuild of German gas storage, driven by reductions in industrial activity, reduces the risk that rationing may become reality this winter. Many more insights within, so do read the full piece for analysis spanning scenarios. Keep in mind, that while gas may be available, it is set to come at a higher clearing price, which manifest itself in markets yesterday where European natural gas futures rose a further +2.64% to €226 per megawatt-hour, just shy of their closing record at €227 in March. But, that’s still well beneath their intraday high from March, where at one point they traded at €345. Further, one-year German power futures increased +6.30%, breaching €500 for the first time, closing at €507. Germany is weighing consumer relief measures in light of climbing consumer prices and also announced that planned nuclear facility closures would be “temporarily” postponed.

The upward energy price pressure and attenuated (albeit, not eliminated) risk of rationing pushed European sovereign yields higher. 10yr German bunds climbed +7.1bps to 0.97%, while 10yr OATs kept the pace, increasing +7.4bps. 10yr BTPs increased +15.9bps, widening sovereign spreads, while high yield crossover spreads widened +10.2bps in the credit space.

Equities were resilient, however, with the STOXX 600 posting a +0.16% gain after flitting around a narrow range all day. Regional indices were also robust to climbing energy prices, with the DAX up +0.68% and the CAC +0.34% higher. In the States the S&P 500 registered a modest +0.19% gain, with the NASDAQ mirroring the index, falling -0.19%. Retail shares drove the S&P on the day, with the two consumer sectors both gaining more than +1%, following strong earnings reports from Wal Mart and Home Depot.

Treasury yields also climbed, but the story was the further flattening in the curve. 2yr yields were +7.5bps higher while 10yr yields managed to increase just +1.6bps, leaving 2s10s at its second most negative close of the cycle at -46bps. 10yr yields are another basis point higher this morning. A hodgepodge of data painted a mixed picture. Housing permits beat expectations (+1674k vs. +1640k) while starts (+1446k vs. +1527k) fell to their slowest pace since February 2021. However, under the hood, even permits weren’t necessarily as strong as first glance, as single family permits fell -4.3% with gains in multifamily pushing the aggregate higher. Indeed, year-over-year, single family permits have now fallen -11.7% while multifamily permits are +23.5% higher. So the single family housing market continues to feel the impact of Fed tightening. Meanwhile, industrial production climbed +0.6% month-over-month (vs. +0.3%), with capacity utilization hitting its highest level since 2008 at 80.3%.

Drifting north of the border, Canadian inflation slowed to 7.6% YoY in July in line with estimates, while the average of core measures climbed to a record 5.3%. Bank of Canada Governor Macklem penned an opinion piece saying that while it looks like inflation may have peaked, “the bad news is that inflation will likely remain too high for some time.” In turn, Canadian OIS rates by December climbed +16.2bps.

In other data, the expectations component of the German ZEW survey fell to -55.3, its lowest level since October 2008 at the depths of the GFC. In the UK, regular pay (excluding bonuses) fell by -3.0% in real terms over the year to April-June 2022, its fastest decline on record.

On the Iranian nuclear deal, EU negotiators reportedly found Iran’s response constructive, though Iran still had some concerns. Notably, Iran is looking for guarantees that if a future US administration withdraws from the JCPOA the US will “have to pay a price”, seeking insulation from the vagaries of representative democracy.

Asian equity markets are trading higher after Wall Street’s solid performance overnight. The Nikkei (+0.76%) is leading gains across the region with the Hang Seng (+0.57%), the Shanghai Composite (+0.23%) and the CSI (+0.51%) all rebounding from its opening losses this morning. US futures are struggling to gain traction this morning with the S&P 500 (-0.02%) and NASDAQ 100 (-0.09%) trading just below flat.

The Reserve Bank of New Zealand lifted its official cash rate (OCR) for the fourth consecutive time by an expected +50bps to 3%, a seven-year high, while bringing forward the estimate of future rate increases. The central bank expects the OCR will reach 3.69% at the end of this year and expects it to peak at 4.1% in March 2023, higher and sooner than previously forecast.

Early morning data coming out from Japan showed that exports rose +19.0% y/y in July (v/s +17.6% expected) posting 17 straight months of gains while imports advanced +47.2% (v/s +45.5% expected) driven by global fuel inflation and a weakening yen. With the imports outweighing exports, the nation reported trade deficit for the 14th consecutive month, swelling to -2.13 trillion yen in July (v/s -1.91 trillion yen expected) compared to a revised deficit of -1.95 trillion yen in June.

In terms of the day ahead, the FOMC minutes from July will be the main highlight, and the other central bank speaker will be Fed Governor Bowman. Otherwise, earnings releases include Target, Lowe’s and Cisco Systems, and data releases include US retail sales and UK CPI for July.

END

AND NOW NEWSQUAWK

Debt retracement continues and DXY firmer with Retail Sales & Minutes due – Newsquawk US Market Open

WEDNESDAY, AUG 17, 2022 – 06:54 AM

- European bourses have dipped from initial mixed/flat performance and are modestly into negative territory, Euro Stoxx 50 -0.5%.

- Stateside, futures are under similar pressure awaiting fresh corporate updates (LOW & TGT thus far) and the July FOMC Minutes, ES -0.6%.

- USD bid but off best with Retail Sales and Minutes ahead, GBP pulls back from initial post-CPI gains, JPY hit on differentials

- Debt retracement continues as yields climb while Sonia drops on further hawkish pricing after UK data

- Crude benchmarks little changed overall awaiting JCPOA developments

- Gold is softer as USD is the haven of choice currently, Aluminium outperforms at Slovalco to close amid elevated energy costs

- Looking ahead, highlights include US Retail Sales, Business Inventories, FOMC Minutes, Supply from the US, and Earnings from Cisco.

As of 11:25BST/06:25ET

For the full report and more content like this check out Newsquawk.

Try a 14 day trial with Newsquawk and hear breaking trading news as it happens.

LOOKING AHEAD

- US Retail Sales, Business Inventories, FOMC Minutes, Supply from the US, Earnings from Cisco.

- Click here for the Week Ahead preview.

GEOPOLITICS

- China’s military is to partake in a military exercise in Russia, their participation has nothing to do with the international situation.

- Taiwan’s Defence Ministry says they have detected 21 Chinese aircraft and five ships around Taiwan on Wednesday, via Reuters.

- Iran is calling on the US to free jailed Iranian’s, says they are prepared for prisoner swaps, via Fars.

EUROPEAN TRADE

EQUITIES

- European bourses have dipped from initial mixed/flat performance and are modestly into negative territory, Euro Stoxx 50 -0.5%.

- Stateside, futures are under similar pressure awaiting fresh corporate updates and the July FOMC Minutes, ES -0.6%.

- Fresh drivers relatively limited throughout the session with known themes in play and focus on upcoming risk events; stocks also suffering on further hawkish yield action.

- Lowe’s Companies Inc (LOW) Q1 2023 (USD): EPS 4.68 (exp. 4.58), Revenue 27.47 (exp. 28.12bln); expect FY22 total & comp. sales at bottom-end of outlook range, Operating Income and Diluted EPS at top-end.

- Target Corp (TGT) Q1 2023 (USD): EPS 0.39 (exp. 0.72), Revenue 26.0bln (exp. 26.04bln); current trends support prior guidance.

- Click here for more detail.

FX

- Greenback underpinned ahead of US retail sales data and FOMC minutes, DXY holds tight around 106.500.

- Pound pegged back after spike in wake of stronger than expected UK inflation metrics, Cable hovers circa 1.2100 after fade into 1.2150.

- Kiwi retreats following knee jerk rise on the back of hawkish RBNZ hike, NZD/USD near 0.6300 from 0.6380+ overnight peak.

- Aussie undermined by marginally softer than anticipated wage prices and lower RBA tightening bets in response, AUD/USD well under 0.7000 vs 0.7026 at one stage.

- Yen weaker as yield differentials widen again, but Euro cushioned by more pronounced EGB reversal vs USTs, USD/JPY probes 21 DMA just below 135.00, EUR/USD bounces from around 1.0150 towards 1.0200.

- Loonie and Nokkie soft amidst latest slippage in oil, USD/CAD closer to 1.2900 than 1.2800, EUR/NOK nudging 9.8600 within 9.8215-9.8740 range.

- Click herefor more detail.

Notable FX Expiries, NY Cut:

- Click here for more detail.

FIXED INCOME

- Debt retracement ongoing and gathering pace ahead of Wednesday’s key risk events.

- Bunds now closer to 154.00 than 156.00 and 157.00 only yesterday, Gilts not far from 114.50 vs almost 116.00 and 117.00+ earlier this week and T-note sub-119-00 vs 119-31 at best on Monday.

- Sonia strip hit hardest as markets price in aggressive BoE hikes in response to UK inflation data toppy already elevated expectations.

- Click here for more detail.

COMMODITIES

- Crude benchmarks are currently little changed overall, having recovered from a bout of initial pressure; newsflow thin awaiting fresh JCPOA developments

- Spot gold is little changed overall but with a slight negative bias as the USD remains resilient and outpaces the yellow metal as the haven of choice.

- Aluminium is the clear outperformer amid updates from Norsk Hydro that they are shutting production at their Slovalco site (175k/T year) by end-September, due to elevated energy prices.

- OPEC Sec Gen says he sees a likelihood of an oil-supply squeeze this year, open for dialogue with the US. Still bullish on oil demand for 2022. Too soon to call the outcome of the September 5th gathering. Spare capacity at around the 2-3mln BPD mark, “running on thin ice”.

- US Private Inventory Data (bbls): Crude -0.4mln (exp. -0.3mln), Cushing +0.3mln, Gasoline -4.5mln (exp. -1.1mln), Distillates -0.8mln (exp. +0.4mln).

- Shell (SHEL LN) announced it is to shut its Gulf of Mexico Odyssey and Delta crude pipelines for two weeks in September for maintenance, according to Reuters.

- Uniper (UN01 GY) says the energy supply situation in Europe is far from easing and gas supply in winter remains “extremely challenging”.

- China sets the second batch of the 2022 rare earth mining output quota at 109.2k/T, via Industry Ministry; smelting/separation quota 104.8k/T.

- Click here for more detail.

NOTABLE HEADLINES

- UK Foreign Minister Truss has commenced formal dispute proceedings against the EU, accusing the bloc of a “clear breach” of the post-Brexit trade agreement, according to the Telegraph.

NOTABLE DATA

- UK CPI YY (Jul) 10.1% vs. Exp. 9.8% (Prev. 9.4%); 0.6% vs. Exp. 0.4% (Prev. 0.8%)

- UK Core CPI YY (Jul) 6.2% vs. Exp. 5.9% (Prev. 5.8%); (Jul) 0.3% vs. Exp. 0.2% (Prev. 0.4%)

- UK ONS House Prices (Jun) +7.8% vs. prev. +12.8%

NOTABLE US HEADLINES

- US President Biden signed the USD 750bln health care, tax and climate bill known as the Inflation Reduction Act into law, according to CNN.

APAC TRADE

- APAC stocks just about shrugged off the choppy lead from the US where markets were tentative amid mixed data signals and strong retailer earnings, but with gains capped overnight ahead of the FOMC Minutes and as participants digested another 50bps rate hike by the RBNZ.

- ASX 200 swung between gains and losses with the index indecisive amid a slew of earnings and with strength in the consumer sectors offset by underperformance in tech, energy and healthcare.

- Nikkei 225 climbed above the 29,000 level with the index unfazed by mixed data releases in which Machinery Orders disappointed although both Exports and Imports topped forecasts.

- Hang Seng and Shanghai Comp were somewhat varied with Hong Kong led higher by tech amid plenty of attention on Meituan after reports its largest shareholder Tencent could reduce all or the bulk of its shares in the Co. which a Tencent executive later refuted, while the mainland was less decisive amid headwinds from the ongoing COVID situation and with power restrictions disrupting activity in Sichuan, although reports also noted that Chinese Premier Li told top provincial officials that they must have a sense of urgency to consolidate the economic recovery and reiterated to step up macro policies.

NOTABLE APAC HEADLINES

- RBNZ hiked the OCR by 50bps to 3.00%, as expected, while it stated that conditions need to continue to tighten and they agreed that maintaining the current pace of tightening remains the best means. RBNZ also agreed that further increases in the OCR were required to meet the remit objective and that domestic inflationary pressures had increased since May. Furthermore, the RBNZ raised its projections for the OCR and inflation with the OCR seen at 3.69% in Dec. 2022 (prev. 3.41%) and at 4.1% for both Sept. 2023 and Dec. 2023 (prev. 3.95%), while it sees annual CPI at 4.1% by Sept. 2023 (prev. 3.0%).

- RBNZ Governor Orr stated at the press conference that they are not forecasting a recession but expected below-potential growth amid subdued consumer spending. Governor Orr also stated that they did not discuss a 75bps rate hike today and that 50bps moves have been orderly and sufficient, while he added that getting rates to 4% would buy comfort for the policy committee and that a Cash Rate of around 4% is unambiguously above neutral and sufficient to meet the inflation mandate.

- Chongqing, China is to curb power use for eight days for industry.

DATA RECAP

- Japanese Trade Balance Total Yen (Jul) -1436.8B vs. Exp. -1405.0B (Prev. -1383.8B, Rev. -1398.5B)

- Japanese Exports YY (Jul) 19.0% vs. Exp. 18.2% (Prev. 19.4%, Rev. 19.3%)

- Japanese Imports YY (Jul) 47.2% vs. Exp. 45.7% (Prev. 46.1%)

- Japanese Machinery Orders MM (Jun) 0.9% vs. Exp. 1.3% (Prev. -5.6%)

- Japanese Machinery Orders YY (Jun) 6.5% vs. Exp. 7.5% (Prev. 7.4%)

- Australian Wage Price Index QQ (Q2) 0.7% vs. Exp. 0.8% (Prev. 0.7%)

- Australian Wage Price Index YY (Q2) 2.6% vs. Exp. 2.7% (Prev. 2.4%)

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 14.64 PTS OR 0.45% //Hang Sang CLOSED UP 91.93 OR 0.46% /The Nikkei closed UP 353.86 OR % 1.23. //Australia’s all ordinaires CLOSED UP 0.26% /Chinese yuan (ONSHORE) closed DOWN AT 6.7794//OFFSHORE CHINESE YUAN DOWN 6.7966// /Oil DOWN TO 86.40 dollars per barrel for WTI and BRENT AT 91939// / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

3 a./NORTH KOREA/ SOUTH KOREA/

///NORTH KOREA/SOUTH KOREA/

3B JAPAN

.

end

3c CHINA

CHINA//

Chinese factories ration electricity as the heatwave disrupts its hydropower generation

(zerohedge)

Chinese Factories Ration Electricity As Heatwave Disrupts Hydropower Generation

TUESDAY, AUG 16, 2022 – 07:20 PM

China’s worst heatwave in decades is curbing hydropower generation in one of the country’s most populous provinces. Local authorities requested some factories in southwestern China to halt production to conserve electricity, adding to the financial pressures of an already rapidly slowing economy.

Sichuan province has more than 80 million inhabitants and is home to a major manufacturing hub. The Washington Post said some factories had suspended production on request by the government due to high temperatures and drought, leading to declining water flows through local hydropower reservoirs.

Jin Xiandong, a spokesman for the National Development and Reform Commission, said on Tuesday that China has to increase coal-fired power output because of waning hydropower output.

China’s inland Sichuan province is a major manufacturing hub that produces consumer goods from electronics, furniture, and food. Also, it’s home to the world’s largest crystalline silicon solar cell producer.

China Securities Journal said Foxconn’s plant in Sichuan that produces Apple products, such as iPads and Macs, wouldn’t be significantly impacted by power rationings.