Uncategorized · Leave a comment·Edit

Uncategorized · Leave a comment·Edit

GOLD; $1737.60 DOWN $20.60

SILVER: $18.85 DOWN 39 CENTS

ACCESS MARKET:

GOLD $1738.10

SILVER: $18.90

Bitcoin morning price: $21,170 DOWN 457

Bitcoin: afternoon price: $20,671 DOWN 956

Platinum price closing DOWN $18.34 AT $868.15

Palladium price; closing DOWN $12.45 at $2122.75

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: AUGUST 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,757.700000000 USD

INTENT DATE: 08/25/2022 DELIVERY DATE: 08/29/2022

FIRM ORG FIRM NAME ISSUED STOPPED

624 H BOFA SECURITIES 1

661 C JP MORGAN 32

690 C ABN AMRO 87

732 C RBC CAP MARKETS 1

905 C ADM 4

991 H CME 57

TOTAL: 91 91

MONTH TO DATE: 33,684

JPMorgan stopped: 32/91

_____________________________________________________________________________________

GOLD: NUMBER OF NOTICES FILED FOR AUGUST CONTRACT:

91 NOTICES FOR 9100 OZ //0.2830 TONNES

total notices so far: 33,684 contracts for 3,368,400 oz (104.771 tonnes)

SILVER NOTICES: 22 NOTICES FILED FOR 110,000 OZ/

total number of notices filed so far this month 1049 : for 5,245,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $20.60

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 984.38 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $.21

AT THE SLV// ://NO CHANGES IN SILVER INVENTORY AT THE SLV//:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 472.900 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 3600 CONTRACTS TO 137,108. AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GIGANTIC LOSS IN OI WAS ACCOMPLISHED DESPITE OUR $0.21 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.21) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC SILVER LONGS AS WE HAD A STRONG LOSS OF 2697 CONTRACTS ON OUR TWO EXCHANGES, WITH ALL OF THAT LOSS DUE TO SPREADER LIQUIDATION AND SOME SPECULATOR LIQUIDATION.

WE MUST HAVE HAD:

I) SOME SPECULATOR SHORT LIQUIDATIONS AND COMMENCEMENT OF SPREADER LIQUIDATION////CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUEUE JUMP / // V) GIGANTIC SIZED COMEX OI LOSS/(//SOME SPEC LIQUIDATION//SPREADER LIQUIDATION)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -6

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTACTS for 20 days, total 11,385 contracts: 56.925 million oz OR 2.850 MILLION OZ PER DAY. (569 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 56.925 MILLION OZ

.

LAST 16 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 56.925 MILLION OZ (A LOT LESS THAN NORMAL//THE CROOKS ARE SCARED TO ISSUE MORE EFP’S)

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3600 DESPITE OUR $0.21 GAIN IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 897 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /SOME BANKER ADDITIONS A// SOME SPEC SHORT LIQUIDATIONS BUT STRONG SPREADER LIQUIDATION /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUEUE JUMP // .. WE HAD A GIGANTIC SIZED LOSS OF 2697 OI CONTRACTS ON THE TWO EXCHANGES FOR 13.485 MILLION OZ AS..THE SPECS STILL BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 22 NOTICE(S) FILED TODAY FOR 110,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 2593 CONTRACTS TO 457,023 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY:–1360 CONTRACTS.

.

THE FAIR SIZED DECREASE IN COMEX OI CAME DESPITE OUR RISE IN PRICE OF $9.70//COMEX GOLD TRADING/THURSDAY / WE MUST HAVE HAD ADDITIONAL SPECULATOR SHORT SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND CONSIDERABLE SPECULATOR SHORT COVERINGS//CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR AUGUST AT 98.367 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 2200 OZ //NEW STANDING 105.179 TONNES

YET ALL OF..THIS HAPPENED WITH OUR RISE IN PRICE OF $9.70 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A SMALL SIZED LOSS OF 111 OI CONTRACTS 0.34 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2452 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 457,023

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 111 CONTRACTS WITH 2593 CONTRACTS DECREASED AT THE COMEX AND 2482 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 111 CONTRACTS OR 0.34 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2482) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (2593): TOTAL LOSS IN THE TWO EXCHANGES 111 CONTRACTS. WE NO DOUBT HAD 1) CONSIDERABLE SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR AUGUST. AT 99.272 TONNES FOLLOWED BY TODAY’S E.F.P. JUMP OF 2200 oz. 3) ZERO LONG LIQUIDATION//// //.,4) SMALL SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST :

52,161 CONTRACTS OR 5,216,100 OZ OR 162.24 TONNES 20 TRADING DAY(S) AND THUS AVERAGING: 2608 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAY(S) IN TONNES: 162.24 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 162.24/3550 x 100% TONNES 4.56% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 162.24 TONNES (DRAMATICALLY FALLING AGAIN)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF SEPT., FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A GIGANTIC SIZED 3600 CONTRACT OI TO 137,109 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 897 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 897 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 897 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 3600 CONTRACTS AND ADD TO THE 897 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF 27003 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 13.515 MILLION OZ

OCCURRED WITH OUR GAIN IN PRICE OF $0.21

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

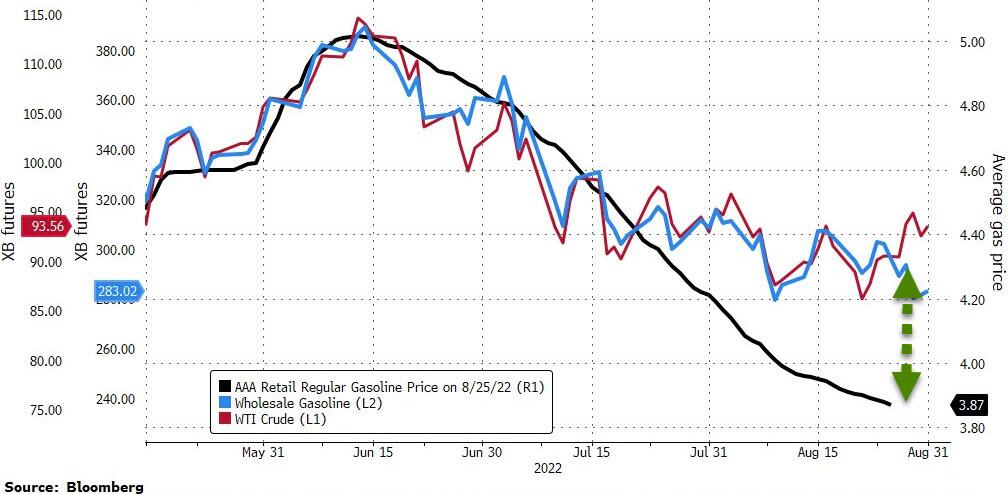

SHANGHAI CLOSED UP 10.02 PTS OR 0.31% //Hang Sang CLOSED UP 201.66 OR 1,01% /The Nikkei closed UP 162.37 OR % 0.57. //Australia’s all ordinaires CLOSED UP 0.74% /Chinese yuan (ONSHORE) closed DOWN AT 6.8627//OFFSHORE CHINESE YUAN DOWN 6.8674// /Oil DOWN TO 93.68 dollars per barrel for WTI and BRENT AT 100.63// / Stocks in Europe OPENED MOSTLY ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 2593 CONTRACTS TO 457,023 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED WITH OUR RISE OF $9.70 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2482 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF AUGUST.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2482 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :2482 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2482 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED SIZED TOTAL OF 111 CONTRACTS IN THAT 2482 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 2593 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR STRONG RISE IN PRICE OF GOLD $ 9.70. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING AUGUST (105.179),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:105.179 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $9.70) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A SMALL SIZED TOTAL GAIN ON OUR TWO EXCHANGES // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS////// WE HAVE REGISTERED A SMALL SIZED LOSS OF 0.34 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR AUGUST (105.179 TONNES)…

WE HAD -1360 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE ADDED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 111 CONTRACTS OR 11100 OZ OR 0.34 TONNES

Estimated gold volume 172,274/// extremely poor/

final gold volumes/yesterday 124,731/extremely poor

INITIAL STANDINGS FOR AUGUST ’22 COMEX GOLD //AUGUST 26

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 65,680.066 oz Brinks HSBC Manfra |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 91 notice(s) 9100 OZ 0.2830 TONNES |

| No of oz to be served (notices) | 131 contracts 13100 oz 0.4074 TONNES |

| Total monthly oz gold served (contracts) so far this month | 33,684 notices 3,368,400 OZ 104.711 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

3 customer withdrawals:

i) Out of Brinks 11,989.759 oz

ii) Out of HSBC: 300.178 oz

iii) OUT OF MANFRA: 53,390.129 oz

total: 65,680.066 oz

total in tonnes: 2.04 tonnes

Adjustments: dealer to customer //3

i) Brinks 96,605.935 oz

ii) HSBC: 6,534.034 oz

iii) Manfra: 4675.731 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 222 contracts having LOST 342 contracts .

We had 320 notices served upon yesterday so we LOST 22 contracts or an additional 2200 oz will NOT stand for delivery in this very active month of August as they were EFP’d over to London.

Sept. lost 150 contracts to 2871 contracts.

October lost 1752 contracts up to 38,787

We had 91 notice(s) filed today for 9,100 oz FOR THE AUGUST 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 91 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 32 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2022. contract month,

we take the total number of notices filed so far for the month (33,684) x 100 oz , to which we add the difference between the open interest for the front month of (AUGUST 222 CONTRACTS ) minus the number of notices served upon today 91 x 100 oz per contract equals 3,381,500 OZ OR 105.179 TONNES the number of TONNES standing in this active month of AUGUST.

thus the INITIAL standings for gold for the AUGUST contract month:

No of notices filed so far (33,684) x 100 oz+ (222) OI for the front month minus the number of notices served upon today (91} x 100 oz} which equals 3,381,500 oz standing OR 105.179 TONNES in this active delivery month of August.

TOTAL COMEX GOLD STANDING: 105.179 TONNES (A HUGE STANDING FOR AUGUST ( ACTIVE) DELIVERY MONTH)

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,344,669.896 oz 72.92 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 28,386,338.315 OZ

TOTAL REGISTERED GOLD: 13,724,316,329 OZ (426.87 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 14,622,021.980 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 11,379,647. OZ (REG GOLD- PLEDGED GOLD) 353.95 tonnes//rapidly declining

END

SILVER/COMEX/AUGUST 26

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,307,727.224 oz CNT JPMorgan Brinks Loomis |

| Deposits to the Dealer Inventory | 9659.627 OZ Delaware |

| Deposits to the Customer Inventory | 254,263.767oz |

| No of oz served today (contracts) | 22CONTRACT(S) 110,000 OZ) |

| No of oz to be served (notices) | 53 contracts (265,000 oz) |

| Total monthly oz silver served (contracts) | 1049 contracts 5,245,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

i)Into Delaware: 9659.627 oz

total dealer deposits: 9,659.627 oz oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) Into Delaware 254,263.767 oz

total deposit: nil oz

JPMorgan has a total silver weight: 170.388 million oz/329.784 million =51.66% of comex

Comex withdrawals:3

i) Out of CNT: 100,043.780 oz

ii) Out of JPMorgan: 597,548.130 oz

iii) Out of Brinks: 9942.880 oz

iv) Out of Loomis: 600,192.434 oz

total: 1,307,727.224 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 52.025 MILLION OZ

TOTAL REG + ELIG. 329,784 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR AUGUST

silver open interest data:

FRONT MONTH OF AUGUST OI: 75 CONTRACTS HAVING LOST 2 CONTRACTS. WE HAD 3 NOTICES FILED ON THURSDAY

SO WE GAINED 1 CONTRACTS OR AN ADDITIONAL 5,000 OZ OF SILVER WILL STAND FOR DELIVERY. THE AMOUNT STANDING

WILL NOW INCREASE//(OR REMAIN CONSTANT) ON A DAILY BASIS AS BANKERS SCOUR THE PLANET FOR BADLY NEEDED SILVER.

SEPTEMBER HAD A LOSS OF 10,605 CONTRACTS DOWN TO 21,364

OCTOBER GAINED 110 CONTRACTS TO STAND AT 453

CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 22 for 110,000 oz

Comex volumes:90,289// est. volume today// very good

Comex volume: confirmed yesterday: 74,989 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 1049 x 5,000 oz = 5,245,000 oz

to which we add the difference between the open interest for the front month of AUGUST(75) and the number of notices served upon today 22 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST./2022 contract month: 1049 (notices served so far) x 5000 oz + OI for front month of AUGUST (75) – number of notices served upon today (22) x 5000 oz of silver standing for the AUGUST contract month equates 5,510,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

AUGUST 26/WITH GOLD DOWN $26.60; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 25/WITH GOLD UP $9.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 18/WITH GOLD DOWN $5.25: GIGANTIC CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.78 TONNES FROM THE GLD////INVENTORY RESTS AT 985.83 TONNES

AUGUST 17/WITH GOLD DOWN $12.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 992.20 TONNES

AUGUST 16/WITH GOLD DOWN $7.85: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 993.94 TONNES

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

AUGUST 10//WITH GOLD UP $2.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES

AUGUST 9/WITH GOLD UP $6.70: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES.

AUGUST 8/WITH GOLD UP $13.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FORM THE GLD//INVENTORY RESTS AT 999.16 TONNES

AUGUST 5/WITH GOLD DOWN $14.25: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .33 TONNES FROM THE GLD////INVENTORY RESTS AT 1000.32 TONNES

AUGUST 4 WITH GOLD UP $29.00 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES FROM THE GLD///INVENTORY REST AT 1000.65 TONNES

AUGUST 2/WITH GOLD UP $3.70; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD//INVENTORY RESTS AT 1002.97 TONNES//

AUGUST 1/WITH GOLD UP $5.75: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 29//WITH GOLD UP $12.50; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1005.29 TONNES

JULY 28/WITH GOLD UP $31.25; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 27.//WITH GOLD UP $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 26/WITH GOLD DOWN $1.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.29 TONNES

JULY 25/WITH GOLD DOWN $7.85: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 1005.87 TONNES

JULY 22/WITH GOLD UP $17.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 21/WITH GOLD UP $11.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.101 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.87 TONNES

JULY 20/WITH GOLD DOWN $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1009.06 TONNES

JULY 19/WITH GOLD DOWN $.35 :BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.22 TONNES FROM THE GLD//INVENTORY RESTS AT 1009.06 TONNES

GLD INVENTORY: 984.38 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 26/WITH SILVER DOWN 39 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 25/WITH SILVER UP 21 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

AUGUST 18/WITH SILVER DOWN 27 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 369,000 OZ INTO THE SLV////INVENTORY RESTS AT 485.482 MILLION OZ//

AUGUST 17/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.106 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.113 MILLION OZ//

AUGUST 16/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 486.219 MILLION OZ/

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 10/WITH SILVER UP 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 9/WITH SILVER DOWN 25 CENTS TODAY: TWO CHANGES IN SILVER INVENTORY AT THE SLV: FIRST: A DEPOSIT OF 461,000 OZ INTO THE SLV AND THEN A WITHDRAWAL OF 1.014 MILLION OZ..//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 8/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 5/WITH SILVER DOWN 28 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 922,000 OZ FROM THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 4 WITH SILVER UP 21 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 527,000 OZ FROM THE SLV////INVENTORY RESTS AT 486.634 MILLION OZ

AUGUST 2/WITH SILVER DOWN 21 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.504 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.161 MILLION OZ//

AUGUST 1/WITH SILVER UP 17 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE GLD: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 483.657 MILLION OZ//

JULY 29/WITH SILVER UP 30 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 461,000 OZ FROM THE SLV..//INVENTORY RESTS AT 483.657 MILLION OZ/

JULY 28/WITH SILVER UP $1.24 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 484.118 MILLION OZ/

JULY 27/.WITH SILVER UP 4 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL 11.479 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 484.118MILLION OZ//

JULY 26/WITH SILVER UP 16 CENTS: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.504 MILLION OZ FROM THE SLV//: //INVENTORY RESTS AT 495.597 MILLION OZ//

JULY 25/WITH SILVER DOWN 24 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.383 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 499.101 MILLION OZ//

JULY 22/WITH SILVER DOWN 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 500.484 MILLION OZ//

JULY 21/WITH SILVER UP 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.19 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 500.484MILLION OZ/

JULY 20/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 8.253 MILLION OZ FORM THE SLV/INVENTORY RESTS AT 507.585 MILLION OZ//

JULY 19/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ//

CLOSING INVENTORY 472.900 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

Money Does Matter: The End Of The Gold Standard Led To A Lower Standard Of Living

FRIDAY, AUG 26, 2022 – 04:25 PM

Authored by André Marques via The Mises Institute,

On August 15, 1971, Richard Nixon announced that the US dollar (USD) would no longer be redeemable in gold. This was supposed to be temporary. And yet, fifty-one years later, here we are. The gold standard was gradually destroyed in the twentieth century.

Now people are experiencing the consequences: less purchasing power, more economic cycles, and a weaker economy.

In the chapter 4 of his book What Has Government Done to Our Money?, Murray Rothbard goes over the steps the government took to end the gold standard over the twentieth century, from the end of the classical gold standard to the closing of the gold window in 1971.

The Classical Gold Standard (1815–1914)

The classical gold standard tended to prevent the government from running budget deficits and going into debt, as it could not easily create inflation. In 1913, the Federal Reserve (Fed) was born. When the US entered the World War I, US dollars were printed at an excess of the gold reserves. At this point, the US got off the classical gold standard and this money printing contributed to the depression of 1920–21.

The Gold Exchange Standard (1926–31)

In this regime, the USD and the pound sterling (GBP) were the two currencies of reference (“key currencies”). The US went back to the classical gold standard (converting USD into gold). GBP and other currencies were not convertible into gold (except for large bars). The Great Britain converted GBP to USD and the other European countries converted their currencies to GBP. So, the Great Britain inflated GBP and the other European countries did the same with their respective currencies (a “pyramiding” of GBP on USD and of other European currencies on GBP). Consequently, as Rothbard stated:

Britain and Europe were permitted to inflate unchecked, and British deficits could pile up unrestrained by the market discipline of the gold standard…. Britain was able to induce the United States to inflate dollars so as not to lose many dollar reserves or gold to the United States. As sterling balances piled up in France, the United States, and elsewhere, the slightest loss of confidence in the … inflationary structure was bound to lead to general collapse. This is precisely what happened in 1931; the failure of inflated banks throughout Europe, and the attempt of “hard money” France to cash in its sterling balances for gold, led Britain to go off the gold standard completely. Britain was soon followed by the other countries of Europe.

Fluctuating Fiat Currencies (1931–45)

In 1933–34 the US abandoned the classical gold standard once again. The USD was defined as 1/35 of an ounce of gold and only foreign governments and central banks could convert it into gold. So, there was a certain link to gold, but the US was in a floating exchange rate regime. As Rothbard stated, by cutting the ties to gold, this regime

leave[s] the absolute control of each national currency in the hands of its … government [which can] allow its currency to fluctuate freely with respect to all other fiat currencies … [The flaw] is to hand total control of the money supply to [the government], and then to … expect that it will refrain from using that power.

the disastrous experience of … the 1930s world of fiat paper and economic warfare, led the United States authorities to [aim] the restoration of a viable international monetary order

Bretton Woods and the New Gold Exchange Standard (1945–68)

Thus, enter the Bretton Woods system (conceived and implemented by the US at a conference in Bretton Woods, New Hampshire in 1944, and ratified by the US Congress in 1945). It was similar to the gold exchange standard, but with the USD being the only “key currency,” priced at $35 an ounce of gold and being redeemable in gold only by foreign governments and central banks.

However, this system eventually met its end. The US inflated the USD (“pyramided” it on its gold reserves), and other governments held USD as their reserves and “pyramided” their currencies on those dollars. And throughout the 1960s, the US constantly inflated the dollar in absolute terms and relative to Europe and Japan. This decade was marked by the “War on Poverty,” the Vietnam War, and space programs.

To finance all this, the US started running large budget deficits, with the Fed monetizing the debt (expanding the money supply). However, the Western European countries that had adopted more solid monetary policies (Western Germany, Switzerland, France and Italy), started to oppose the obligation to accumulate dollars. Europe began to redeem dollars in gold, and the Bretton Woods system began to collapse in 1968 (ending in 1971, when Nixon suspended the redemption of the USD in gold).

The Closing of the Gold Window and the Rise of the Floating Exchange Rate Regime (1971–?)

In order to keep the redemption of the USD in gold, the US government had two options:

- Cut spending and taxes to reduce the budget deficit. The supply of money would decrease, and the USD would appreciate, which would allow prices to fall to levels that would be consistent with an ounce of gold at $35 and restore demand for the currency.

- Dollar devaluation. This would mean that the price of an ounce of gold would have to rise to a level that would be consistent with the supply of USD and the higher prices for goods and services. But this would require the government to reduce the budget deficit to prevent future devaluations.

Both options were inconvenient for the government. Thus, in February 1973, after two devaluations of the USD that raised the price of an ounce of gold to $42.22, the closing of the gold window became permanent. Therefore, the USD returned to the floating exchange rate regime (as in 1931–45, but with no link to gold).

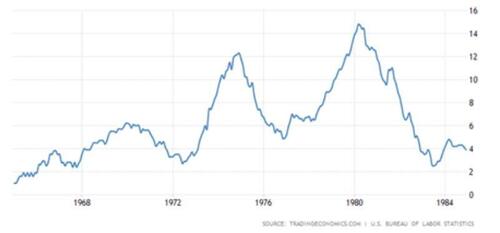

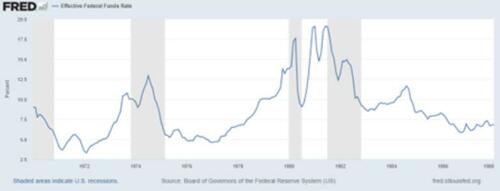

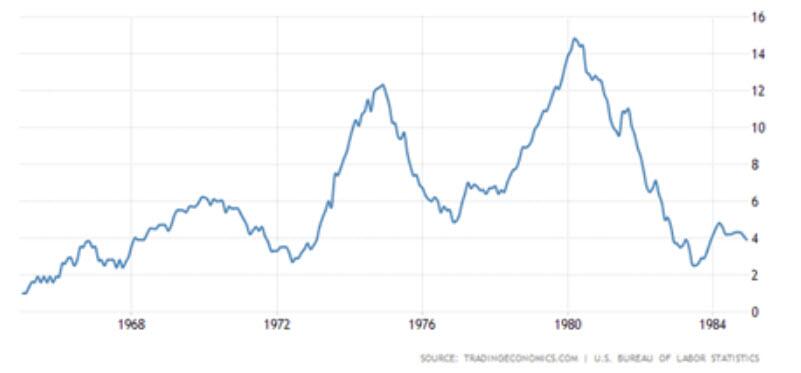

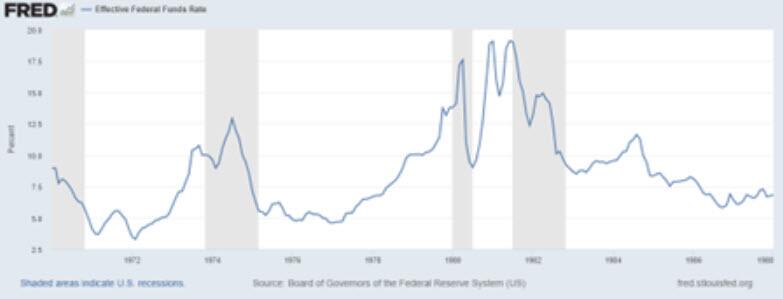

As a result, the USD devalued and the 1970s were marked by stagflation. In 1980, the price of an ounce of gold was $850. The price of oil rose from just under $3 a barrel in 1970 to just under $40 in 1980. The Consumer Price Index (CPI) was over 14 percent in 1980 (chart 1). It was only in the early 1980s that the CPI began to decline, when Paul Volcker, Fed chairman at the time, raised the federal funds rate to almost 20 percent (chart 2).

Chart 1: Consumer Price Index (1965–85)

Source: Trading Economics; author’s own elaboration.

Chart 2: Federal Funds Rate (1970–88)

Source: FRED; author’s own elaboration.

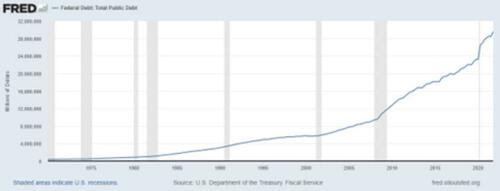

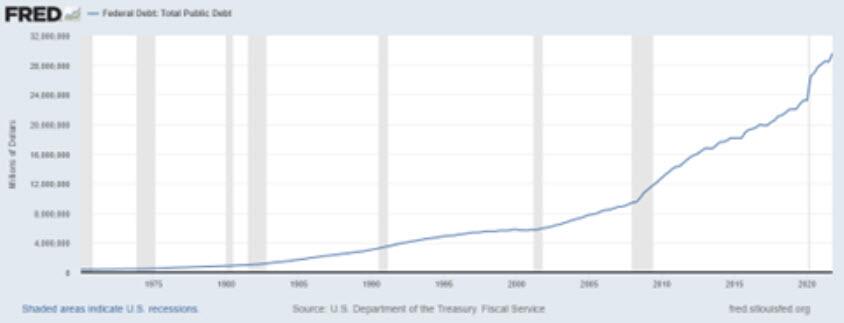

However, in 1980, the US federal debt was “only” $930.2 billion (chart 3). Thus, it was possible to significantly increase interest rates without causing major impacts on the economy. Today, the federal debt is above $30.5 trillion. The Fed can’t raise rates without crashing the economy. The US has gone from being the world’s biggest creditor in the early 1970s to the world’s biggest debtor today (the US has more debt than all other governments in the world combined).

Chart 3: Federal Debt for the United States (1970–2021)

Source: FRED; author’s own elaboration.

As the federal funds rate rose, the USD appreciated and there was a restoration of confidence in the currency. This (along with the fact that the US dollar was already the currency in which oil and other commodities were priced) allowed the USD to remain the main world reserve currency. And this, along with the fact that the USD has been unbacked since 1971, has allowed the US to inflate it over time, destroying its value. As of August 3, 2022, the ounce of gold costs $1765:

Chart 4: Price of Gold (In US Dollars)

Price of 1 Kg – 1Kg = 2.20462 Pounds (Left Axis); Price of an Ounce (Right Axis).

Source: goldprice.org; author’s own elaboration.

Conclusion

The consequences of the end of the gold standard began to be felt in the 1970s.

The devaluation of the USD substantially reduced Americans’ real wages.

Before 1970, usually only one member of a family was able to support it.

From the 1970s onwards, this began to change to the point where today this is only possible for wealthier people. Despite all the technological advancements, the standard of living today is lower than in the 1950s and the 1960s, as today, in order to live and to buy things they want or need, people need to work a lot more (and even go into debt).

If the USD had not been devalued since 1913 (or even if it had been appreciated, which is what tends to occur when there is no monetary expansion), the standard of living would be much higher today.

END

3.Chris Powell of GATA provides to us very important physical commentaries

This is a must read: SLV is in a massive physical short position and thus the reason for silver price being under

pressure. It cannot be resolved unless the price escalates considerably.

(Butler/GATA)

Ted Butler: Why silver went down when it should have gone up

Submitted by admin on Thu, 2022-08-25 13:36Section: Daily Dispatches

By Ted Butler

Butler Research, Jupiter, Florida

via SilverSeek.com

https://www.butlerresearch.com/

Two weeks ago it looked to me like silver was about to take off, following months of sharp price declines, yet we experienced the worst selloff in a couple of years.

Most puzzling was the cause of the sharp price declines. It didn’t appear to reside in Comex futures positioning. It was something else entirely. I’ve been (quite literally) agonizing over what was behind this completely unexpected selloff to no avail, almost to the point of questioning my sanity, until a simple question from Jim Cook, president of Investment Rarities, appeared to provide the answer.

Jim asked if the highly-counterintuitive selloff I was moaning about could be related to the short position in the exchange-traded fund SLV, and my head nearly exploded because it was so obvious that I couldn’t conceive why I hadn’t thought of it.

Talk about being too close to the trees to see the forest. I had been so preoccupied with the excessive short position in SLV that I failed to make the most obvious connection.

Simply put, the most plausible explanation for the selloff in silver this week was the short position in SLV that I have been writing about.

The excessive short position in SLV is the explanations for the truly putrid price performance in silver over the past two weeks.

What makes the short position in SLV such a big deal is that the most plausible reason for its existence is a wholesale shortage in silver of thousand-ounce bars. …

… For the remainder of the analysis:

end

Why Silver Went down When It Should Have Gone Up

August 22, 2022

Ted Butler

Two weeks ago, it looked to me like silver was about to take off, following months of sharp price declines, yet we experienced the worst selloff in a couple of years. Most puzzling was the cause of the sharp price declines. It didn’t appear to reside in COMEX futures positioning. It was something else entirely. I’ve been (quite literally) agonizing over what was behind this completely unexpected selloff to no avail, almost to the point of questioning my sanity, until a simple question from Jim Cook, president of Investment Rarities, appeared to provide the answer. Jim asked if the highly-counterintuitive selloff I was moaning about could be related to the short position in SLV and my head nearly exploded because it was so obvious that I couldn’t conceive why I hadn’t thought of it. Talk about being too close to the trees to see the forest. I had been so pre-occupied with the excessive short position in SLV that I failed to make the most obvious connection.

Simply put, the most plausible explanation for the selloff in silver this week was the short position in SLV that I have been writing about. The excessive short position in SLV is the explanations for the truly putrid price performance in silver over the past two weeks. What makes the short position in SLV such a big deal is that the most plausible reason for its existence is a wholesale shortage in silver of 1000 oz bars. The short position exists because there is not sufficient physical silver available for deposit, as is required by the prospectus. The only reason for an AP (Authorized Participant) to short shares of SLV at a time of extremely low silver prices and low levels of commercial shorting on the COMEX is the lack of availability of physical silver to deposit for newly created shares.

So how do those short in the SLV get out of their short position? Prices have been rigged lower on the COMEX to make it easier for whoever is short SLV to buy back short positions in SLV on lower prices. Shorting more shares would have only dug their hole deeper. The only way the big short sellers in SLV could rig prices lower was by using the crooked and illegal price mechanism of rigging prices lower on the COMEX, so that the shorted shares of SLV could be bought back. In fact, there was no other way. For the big short sellers in SLV, to simply buy back shares without using the COMEX price mechanism to rig prices lower would have sent silver prices soaring – the very last thing the big SLV short sellers would desire. I can’t explain how I didn’t see this until Cook asked me the question – but better late than never.

The biggest question, of course, is where the heck are the regulators while this is going on? I have put the SEC on notice (and have received confirmations that my complaints were received), but, obviously, this is very much a matter for the CFTC and the CME Group, as well and I’ll send them this article as I have all along. The issues I’m raising are substantive and documented and every bit the big deal I claim them to be. Yet, nothing ever seems to be the done by the regulators.

What I have described is nothing less than the existence of a profound physical shortage in wholesale quantities of silver that is much closer to hitting the proverbial fan that anyone can imagine. While I wouldn’t attempt to try and pinpoint when the turn up may come, it seems impossible that silver prices, regardless of where they may go in the short run, will not be substantially higher in the not-too-distant future. I have always made it a practice not to underestimate the treachery and cunning of the commercial shorts on the COMEX and now in SLV, and this latest manipulative episode in the shorted shares in SLV only prove these crooks are relentless. That said, a physical silver shortage appears to be close at hand and based upon what has transpired, any other conclusion seems far-fetched. One thing of which I’m increasingly certain is that whenever the real move higher in silver gets initiated, it won’t be of the two steps forward, one step back variety. Instead, we go straightaway and with no looking back.

Ted Butler

August 22, 2022

end

Your weekend reading material

(Alasdair Macleod/GATA)

Alasdair Macleod: Living with contracting bank credit

Submitted by admin on Thu, 2022-08-25 14:21Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, August 25, 2022

In this article we look at the consequences of contracting bank credit on the economy, financial markets, and commodities. It is a developing global condition.

Why is bank credit on the verge of a substantial contraction?

The starting point is record bank balance sheet leverage in the Eurozone and Japan, high bank leverage rates elsewhere, and a sea change in the interest rate environment. In short, instead of being greedy for profits, senior bankers are now growing scared of risk and of their exposure to it.

The effect on the non-financial economy will be to cause nominal GDP to slump because every transaction that makes up GDP is settled through credit — nearly all of it is bank credit. Contracting bank credit will simply drive GDP into the ground.

But bank credit also drives financial activities, its long-term expansion having driven bond yields down, equities up, and expanding derivative markets to a $700 trillion monster. A credit contraction undermines financial asset values and associated derivative markets. This article looks at the inadequacies of Basel III regulations in this context.

Every 10 years or so there is a banking crisis because of bankers attempting to reduce lending risk. Fourteen years since the Lehman failure, this cycle’s downturn is now overdue.

The indications are that the cycle of bank credit contraction is just beginning…

… For the remainder of the analysis :

https://www.goldmoney.com/research/living-with-contracting-bank-credit?gmrefcode=gata

end

4. OTHER GOLD/SILVER COMMENTARIES

Ep.88 Live from the Vault

Russia weaponizes gold – LBMA under siege!

In this week’s Live from the Vault, Andrew Maguire highlights the possible implications of Russia’s plan to create its own international standard for the precious metals market by establishing a local LBMA-competing brand.

With global investors growing frustrated over the unnatural capping of the gold and silver prices, the London wholesaler provides further evidence of the COMEX’s broken pricing mechanism.

-END-

*SHOCKING Letter from US Mint Director

Just got a shocking letter (attached) from US Mint Director Ventris Gibson claiming…

“This year, we significantly increased production quantities of one of our most popular coins, the American Eagle One Ounce Silver Dollar, which will lead to broader availability to our customers!”

WOW! How is producing Silver Eagles at 25% of the Mint’s full year capacity “increasing production quantities?”

In 2015 the US Mint produced 47M Silver Eagles and 8 months into 2022 they’ve only made 12 Million!!

Must be another secret part of the “Inflation Reduction Act!”

Luckily, there are good people calling them out on their lies:

end

Very important read:

Could new Russia metals exchange have an impact on gold prices?

By Indrabati Lahiri

Capital-com

Russia has just announced a new precious metals exchange called the Moscow World Standard

Russia has recently proposed its own precious metals exchange, provisionally called the Moscow World Standard (MWS), which is expected to join the ranks of other world- class metals exchanges. This plan has been long in the making, with the country specifically highlighting that it wants this exchange to be an alternative to the London Bullion Market Association (LBMA).

Over the last few months, Russia has become increasingly insistent that the LBMA has engaged in artificial practices by manipulating the precious metals market and keeping prices low. This in turn, is seen as having a negative impact on precious metal exporters. These accusations have also become stronger since the LBMA banned Russian precious metals such as gold, platinum and palladium as part of the international Russia-Ukraine sanctions.

Russia is one of the biggest producers of gold worldwide

What do we know about the proposed Moscow World Standard so far?

Although seen as a kind of retaliatory gesture towards the LBMA, according to the Russian Finance Ministry, this move is key for “normalizing the functioning of the precious metals sector.” The exchange will be based on a special global precious metals brokerage, which will have headquarters in Moscow and will rely on the Moscow World Standard.

There is also likely to be a committee which will have major financial institutions and central banks from ex-USSR countries such as Armenia, Kyrgyztan, Belarus and Kazakhstan, which along with Russia, form the key Eurasian Economic Union.

The current plan is to peg precious metal prices to either one of the national currencies of the countries in the union or create an entirely new currency, inspired by the proposed BRICS currency. This will be used for international trade, smoothening processes outside the union.

Apart from that, Russia is also trying to get other major gold producing and consuming countries, such as Venezuela, China, India and Peru to support this new exchange. India has recently announced its own precious metals exchange, known as the India International Bullion Exchange (IIBX), to compete with the LBMA as well, reportedly unhappy with the latter’s methods of practice too.

According to Indian Prime Minister, Narendra Modi, the IIBX will “empower India to gain its rightful place in the global bullion market and serve the global value chain with integrity and quality.”

Investors speculate that Russia and India have started a movement, which could potentially sweep up other major gold and precious metals producing countries as well, inspiring them to open up their own exchanges soon too. This will go a long way in distributing the power of traditional metal exchnages a little more evenly throughout the world.

end

5.OTHER COMMODITIES:

COMMODITIES IN GENERAL/COAL

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.8627

OFFSHORE YUAN: 6.8674

HANG SENG CLOSED UP 201.66 PTS OR 1.01%

2. Nikkei closed UP 162.37 OR 0.57%

3. Europe stocks CLOSED MOSTLY RED

USA dollar INDEX DOWN TO 108.37/Euro RISES TO 0.9989

3b Japan 10 YR bond yield: FALLS TO. +.215/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 137.02/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.341%/Italian 10 Yr bond yield RISES to 3.64% /SPAIN 10 YR BOND YIELD RISES TO 2.53%…

3i Greek 10 year bond yield RISES TO 3.91//

3j Gold at $1745.00 silver at: 19.23 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 14/100 roubles/dollar; ROUBLE AT 60.00//

3m oil into the 93 dollar handle for WTI and 100 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 136.39DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 9645– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9635well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.071 UP 5 BASIS PTS

USA 30 YR BOND YIELD: 3.281 UP 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,18

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

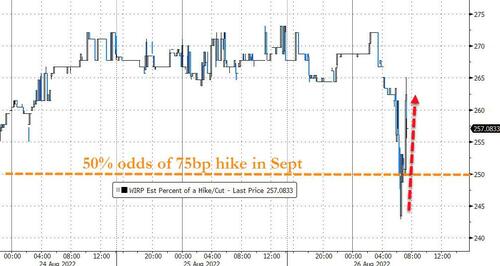

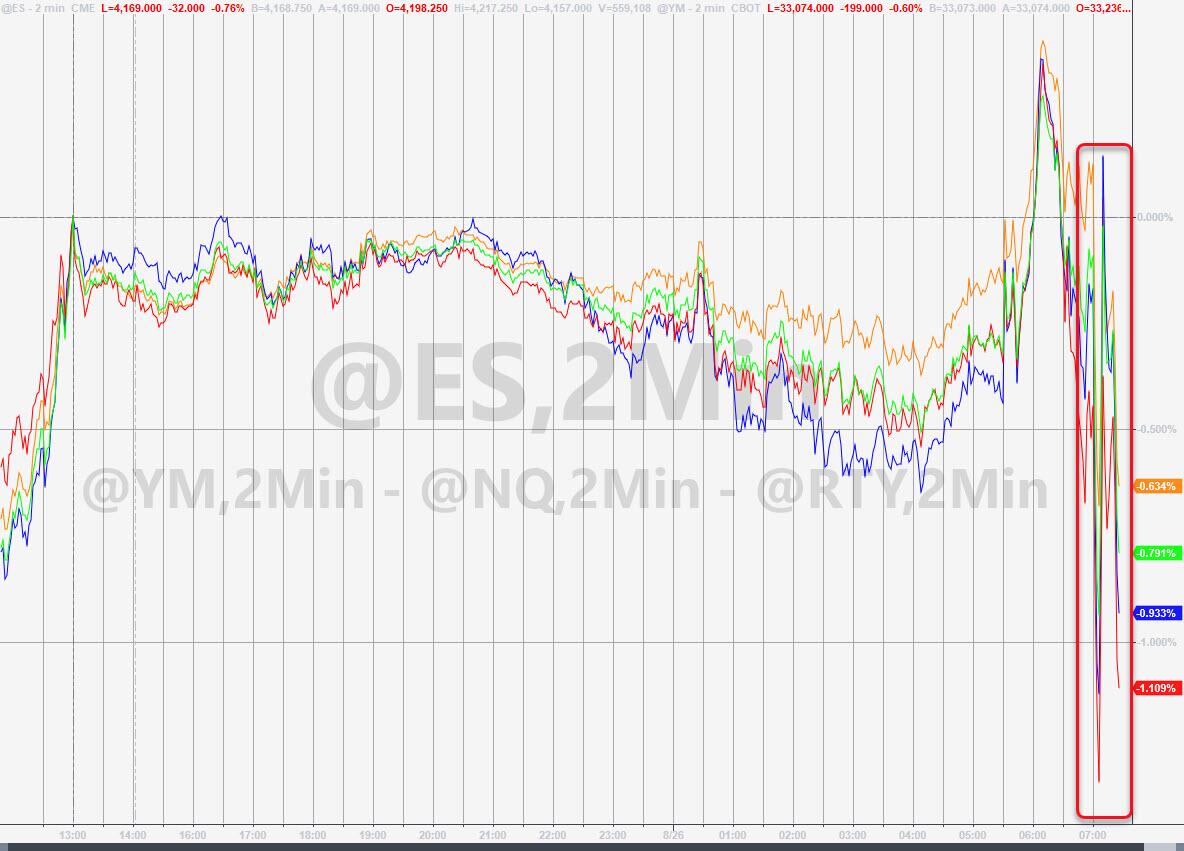

Futures Drift Lower Ahead Of Action Jackson Hawk-nado

FRIDAY, AUG 26, 2022 – 07:47 AM

The day we’ve all been waiting for has finally arrived as Jerome Powell prepares for his keynote hawknado speech at the

“Action Jackson” Hole.

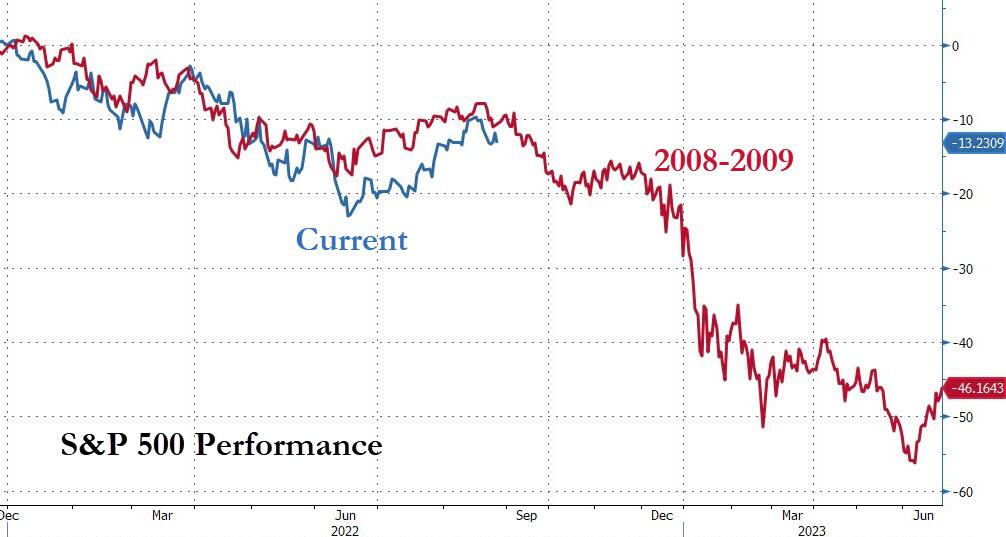

After yesterday’s unexpected last hour rally, US stock futures dropped and interest rates rose as jittery investor nerves took hold before Federal Reserve Chair Jerome Powell’s much-anticipated (hawkish) speech at the Jackson Hole symposium. S&P futures dropped 0.4% in a subdued session, while Nasdaq 100 futures fell 0.5% as of 7:15 a.m. ET. Both underlying indexes jumped Thursday, paring losses from earlier in the week, as bond yields dropped. Still, the benchmark S&P 500 is set for its second straight weekly decline as Fed policy makers sounded more hawkish about their outlook on rate hikes, even amid growing fears of a recession.

Among notable movers in premarket trading, Affirm Holdings Inc. slumped after the payments company gave a revenue forecast for 2023 that missed the average analyst estimate. Shares of Dell Technologies also fell more than 4% following bearish remarks from the PC maker about the business environment for the second half. Other notable premarket movers:

- Farfetch (FTCH US) rises 16% in premarket trading after the company posted a 2Q revenue beat, with analysts highlighting strong growth prospects for 2023 and resilient core results.

- Gap (GPS US) gains 8% in premarket trading after the apparel retailer reported a surprise profit and improving sales trends.

- Workday (WDAY US) rises 11% in premarket trading after the application software company reported second-quarter results that beat expectations and reiterated its forecast for the year.

- Marvell Technology (MRVL US) fell 1.4% in postmarket trading. The firm’s softer guidance is disappointing, with weakness in some key growth areas, analysts said.

- Ulta Beauty’s (ULTA US) quarterly results beat on most metrics, prompting price-target raises for the beauty products retailer. The shares rose 3% in postmarket trading.

Of course, today’s main event is Powell’s speech scheduled for 10 a.m. Washington time, where the Fed chair is expected to restate the central bank’s resolve to keep tightening policy to fight elevated inflation. Mark Haefele, chief investment officer at UBS Global Wealth Management, said the stakes are high for what Powell signals today as inflation will likely drive the trajectory of stocks over the next year. “If the Fed’s incremental rate hikes are effective at cooling today’s rampant inflation, Powell could lead to market upside over the course of the next year,” Haefele wrote. “But if the Fed, or the market misjudge the direction and drivers of inflation, outcomes for investors would likely be much worse.”

“The reality is that the Fed will want to be sure that inflation is falling at a sustainable enough pace before it signals any sort of dovish shift or pivot,” said Michael Hewson, chief market analyst at CMC Markets UK. “This puts Powell in the rather tricky position of having to let markets down gently.”

As Oanda’s Craig Erlam writes, there is “no doubt Powell will have chosen his words very carefully today, all too aware of the consequences of even the smallest deviation in his intended message. It’s a little ridiculous that markets put so much weight on such things but that is the situation we are in and I expect the Fed Chair will be very clear in the message he wants to send. The difficulty for Powell stems from the fact that there’s the message investors desperately want to hear and the one they’ve repeatedly ignored since the July Fed meeting.”

Erlam adds that the “dovish pivot” played nicely into the hands of the perma-bulls that have waited impatiently for the stock market to recover this year. Despite policymakers’ best efforts, “attempts to correct this narrative have been brushed aside and the view today is that Powell may try to address this in a more forceful and convincing way.” But, “if he fails or gives the slightest impression that there is any substance to the dovish pivot narrative, we could see yields slip and stock markets end the week on a high. That could come intentionally, or otherwise, but investors will be clinging to his every word for even the slightest hint. Especially in light of the recent inflation reading. No pressure.”

Duration and rate-sensitive tech stocks will be in particular focus in the aftermath of the J-Hole conclave after leading the sharp recovery in US stocks since mid-June. Higher interest rates mean a bigger DCF discount, hurting growth stocks with the highest valuations, including technology, and boosting cheap or so-called value shares. As Bloomberg notes, market watchers will be cautious about further gains for the sector after the technology-heavy Nasdaq 100 rallied more than 20% from its June low, making valuations more expensive again. In the week to Aug. 24, technology funds saw the biggest outflows since November 2021, according to a note from Bank of America Corp. citing EPFR Global Data.

European equities tracked US futures, and turned negative after gaining in early trading. The Stoxx Europe 600 Index dropped 0.4% giving up earlier gains of as much as 0.5%. Miners and banks outperformed, while media stocks were laggards. Media, travel and food & beverages lag while miners, banks and autos outperform. The summer rally in European shares has run into concerns that the Fed will continue raising rates to tame inflation despite fears of an economic slump. The main regional benchmark is set for a second week of losses. Here are some of the biggest European movers today:

- SKF shares rise as much as 7.2% after activist investment firm Cevian Capital boosted its stake in the Swedish industrial group. Analysts say the firm could be on the verge of meaningful change

- European mining companies are the best-performing group in Stoxx 600 benchmark on Friday, as iron ore gained. Base metals also edged higher amid China’s efforts to stimulate its economy

- GSK, Sanofi and Haleon shares all gain as Citi opens positive catalyst watches on GSK and Sanofi following a tentative ruling that could mean the settlement on Zantac is significantly lower than expected

- Micro Focus International shares rise as much as 94% after Canada’s OpenText agrees to buy the UK software firm for 532p/share, implying an enterprise value of about $6b

- Molecular Partners rises as much as 8.6% after the biotech reported 2Q results that came in line with expectations. RBC says the firm has a strong cash position, which remains the key financial metric

- SFS shares are up as much as 6%, most since December 2021, after the company reported a sales beat, with analysts welcoming the new margin guidance, saying it represents upside to consensus estimates

- Eurocommercial Properties shares gain as much as 7.4%, the most intraday since March 29, after the real estate investment firm reported better- than-expected net property income

- RELX shares dip 3.7% and Wolters Kluwer shares drop 2.5% and drag on the Stoxx 600 Media index, with Citi flagging negative sentiment for the media groups from US Open Access plans

- Lundbergforetagen slides, falling as much as 3.3%, as Handelsbanken warns of the risk that the Swedish property investment firm’s net asset value (NAV) discount could increase still further

- H&M shares drop as much as 2.1% as price targets are cut at at least three more brokers, with analysts bearish on the outlook for the Swedish fast- fashion retailer amid a weaker consumer environment

Earlier in the session, Asian stocks advanced for a second day, as technology stocks gained ahead of Federal Reserve Chair Jerome Powell’s speech at Jackson Hole. The MSCI Asia Pacific Index climbed 0.4%, trimming gains later in the day as US futures slipped. TSMC and Samsung were among the biggest boosts as global chipmakers rallied, while Alibaba and peers climbed after reports of talks to avoid delistings of Chinese stocks in New York. Australia stocks were among the biggest gainers, with the benchmark gauge up 0.8%. Investors will monitor Powell’s remarks later Friday for clues on the path of the Fed’s interest rate hikes ahead of its September meeting. Recent comments by Fed officials have indicated the US central bank may focus on taming high inflation, triggering a selloff in equities earlier this week. Read: Fed’s Jackson Hole Conference Is Underway: Here’s What to Expect “To some degree, we are expecting Chair Powell may well push back against the ideas that we should expect the dovish pivot any time soon,” Audrey Goh, an investment strategist at Standard Chartered Bank SG, said in an interview with Bloomberg TV. “Whether this rally will extend, I think the key is really the dollar. We really need to see a weak dollar for risk assets to sustain recovery,” she said. Friday’s advance following a jump in the previous session has helped the MSCI’s Asian stock benchmark finish the week almost flat. The gauge had slumped earlier in the week amid concerns that the Fed may ramp up its hawkishness and mixed corporate earnings. The gauge is down 17% this year, underperforming global peers on steep losses in Chinese shares

Japanese stocks tracked gains in US peers as investors weighed comments from Federal Reserve officials which signaled a resolve to tighten further to tame inflation. The Topix rose 0.2% to close at 1,979.59, while the Nikkei advanced 0.6% to 28,641.38. Sony Group Corp. contributed the most to the Topix gain, increasing 1% as the company said it will increase PlayStation 5 console prices in certain countries. Out of 2,170 stocks in the index, 1,053 rose and 969 fell, while 148 were unchanged. St. Louis Fed chief James Bullard said officials should act quickly and lift their policy benchmark to a 3.75% to 4% range by year end. Bullard spoke to CNBC in Jackson Hole, where Fed Chair Jerome Powell is due to make a speech Friday. “For Japan stocks the remarks will have a different aspect depending on the industry, with a more hawkish tone favorable for export-related stocks as interest rates rise and the yen will weaken,” said Tomo Kinoshita, a global market strategist at Invesco Asset Management. But, “overall, of course the more dovish the more favorable it will be for the markets.”

Australia’s S&P/ASX 200 index rose 0.8% to close at 7,104.10, boosted by banks and mining shares. Soaring profits unveiled by Australian miners this week were a beacon of light amid the gloom dominating economic headlines. The benchmark erased 0.2% this week, snapping five weeks of gains, in the lead up to Federal Reserve Chair Jerome Powell’s speech at Jackson Hole on Friday. Investors will monitor Powell’s remarks for clues on the path of the Fed’s interest rate hikes ahead of its September meeting. In New Zealand, the S&P/NZX 50 index fell 0.2% to 11,608.29

Stocks in India rose in line with Asian peers on Friday as Kotak Mahindra Bank and Larsen & Toubro gained. The key equity gauges still posted their first weekly drops since mid-July, with investors remaining cautious ahead of the US Federal Reserve’s commentary about monetary-policy outlook. The S&P BSE Sensex rose 0.1% to 58,833.87 in Mumbai, paring its weekly loss to 1.4%. The NSE Nifty 50 Index climbed 0.2% on Friday. Among the 30 members on the Sensex, 19 gained and 11 fell. The gauge on Thursday took a surprise dive in the last hour of trade due to the expiry of the monthly derivative contracts. Much of the advance in Indian stocks since June have been driven by purchases by foreign investors. However, the inflows moderated this week on risk-aversion ahead of Fed Chair Jerome Powell’s speech at the Jackson Hole symposium on Friday, which will help investors gauge the future course of rate hikes by the US central bank. Foreign investors have purchased $110m of Indian stocks this week through Aug. 24, compared with net buying of more than $1 billion for preceding three weeks.

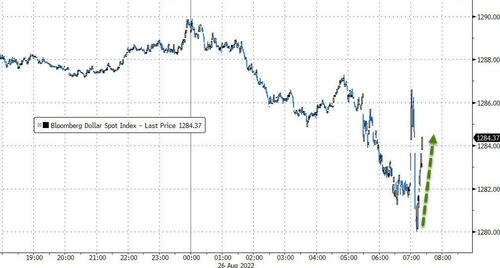

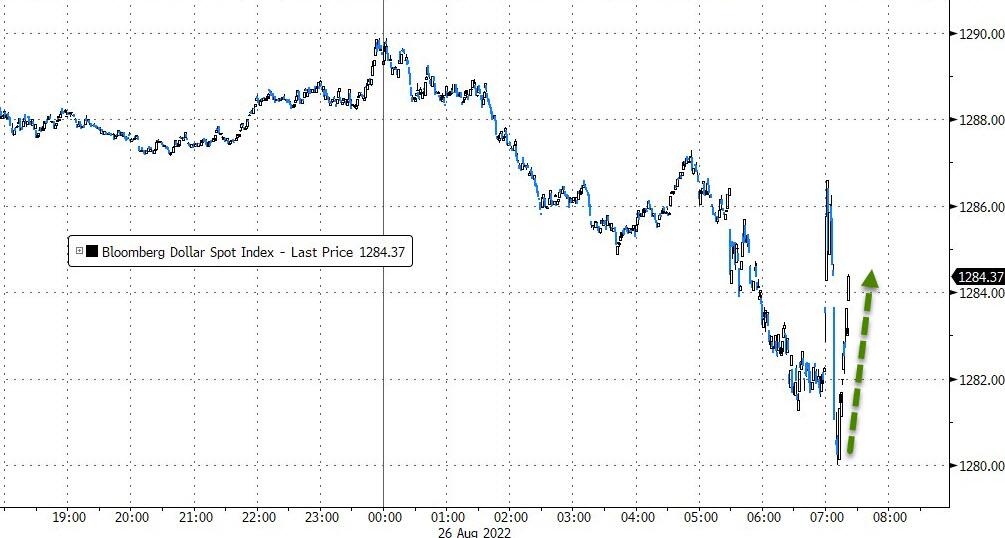

In FX, the greenback pared gains against most of its Group-of-10 currencies. DKK and EUR are the strongest performers in G-10 FX, NZD and GBP underperform. The Bloomberg Dollar Spot Index little changed after rising 0.3% earlier. As Powell delivers the much anticipated speech, “markets may find enough reason to push their peak rate pricing closer to the 4.0% mark today, which should ultimately offer some support to the dollar,” Francesco Pesole, a strategist at ING Groep NV wrote in a note.

Australian and New Zealand dollars fell the most among G-10 currencies as they were sold by fast money funds in last minute positioning ahead of Powell’s speech, according to Asia-based FX traders. “The Fed has been pretty clear in its messaging so I would be surprised if Powell suddenly changed direction or threw something else into the mix,” said Darren Langer, co-head of Australian fixed income at Yarra Capital

- EUR/GBP up 0.3%; GBP/USD down 0.1%. The pound fell as much as 0.5% after the UK energy regulator raised the caps on energy prices, a move likely to escalate inflationary pressures

- NZD/USD fell 0.3% to 0.621. The Reserve Bank of New Zealand Governor Adrian Orr forecast sharply slower economic growth to constrain demand and tamp down inflation while suggesting the central bank may be nearing the end of its aggressive hiking cycle

- AUD/USD dropped 0.1% to 0.6955 after falling as much as 0.4%

- USD/JPY rose 0.3% to 136.886

In rates, Treasuries were lower led by intermediates, re-steepening 2s10s spread back toward middle of Thursday’s range. Bunds and more notably gilts outperform Treasuries, while S&P 500 futures are also under pressure with European stocks. US 10-year yield 3.07% is cheaper by 5bp on the day, underperforming bunds by ~1bp, gilts by ~5bp; 2s10s is steeper by ~4bp with front-end Treasuries only marginally cheaper on the day. Bunds 10-year yield up about 2 bps to 1.33%, while gilts appear relatively muted in comparison as 10-year yield is unchanged at 2.61. IG dollar issuance slate empty so far, and just $1.3b of new supply has been seen this week. Three-month dollar Libor +2.64bp to 3.06957%.

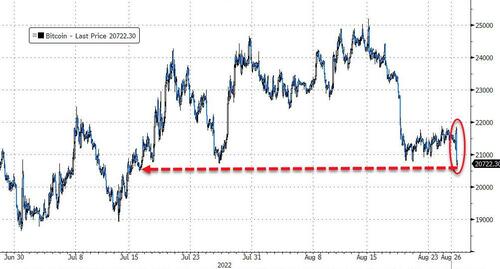

In commodities, WTI trades within Thursday’s range, adding 0.6% to around $93. Most base metals are in the green; LME nickel rises 1.6%, outperforming peers. Spot gold falls roughly $6 to trade near $1,752/oz. Bitcoin and ethereum both slumped, going back to levels last ween on Wednesday.

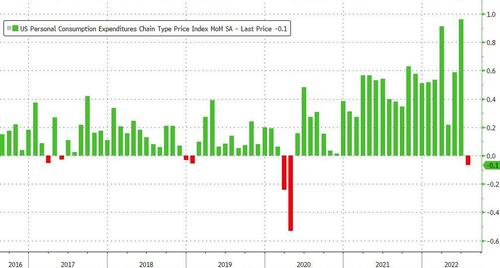

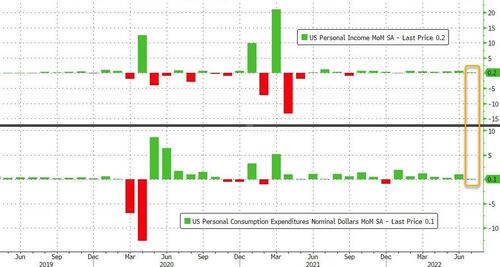

To the day ahead now, the main highlight will be Fed Chair Powell’s speech at Jackson Hole. Otherwise, data releases from the US include July’s personal income and personal spending, along with the University of Michigan’s final consumer sentiment index for August. From Europe, there’s the GfK consumer confidence index from Germany for September, as well as consumer confidence readings from France and Italy too for August.

Market Snapshot

- S&P 500 futures down 0.3% to 4,190.00

- STOXX Europe 600 little changed at 433.05

- MXAP up 0.4% to 160.81

- MXAPJ up 0.5% to 525.76

- Nikkei up 0.6% to 28,641.38

- Topix up 0.2% to 1,979.59

- Hang Seng Index up 1.0% to 20,170.04

- Shanghai Composite down 0.3% to 3,236.22

- Sensex up 0.4% to 59,023.37

- Australia S&P/ASX 200 up 0.8% to 7,104.06

- Kospi up 0.2% to 2,481.03

- German 10Y yield little changed at 1.34%

- Euro little changed at $0.9978

- Brent Futures up 0.9% to $100.20/bbl

- Brent Futures up 0.9% to $100.21/bbl

- Gold spot down 0.4% to $1,751.78

- U.S. Dollar Index little changed at 108.54

Top Overnight News from Bloomberg

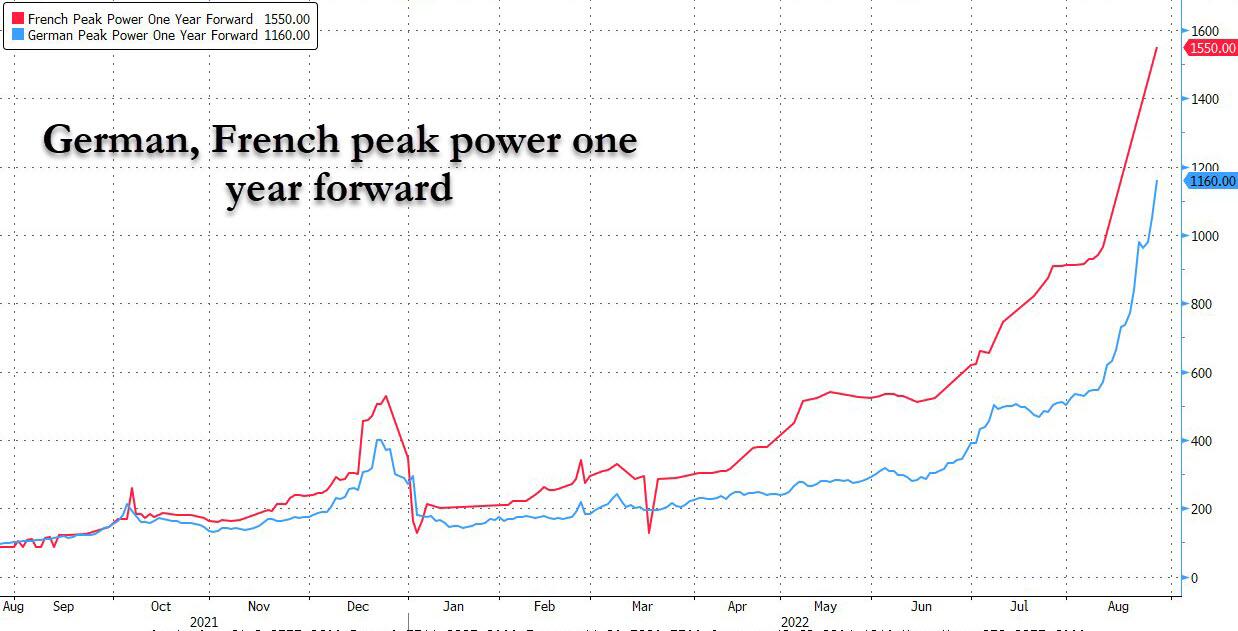

- From canceling Friday night trips to the pub to pushing back soccer practice, global investors are pulling out all the stops to ensure they’re ready for the most important gathering of central bankers this year.

- China is using China Aerospace Science and Industry Corp to ship millions of barrels of Venezuelan oil despite US sanctions, Reuters reports, citing three unidentified people and tanker tracking data

- Europeans are taking colder showers, offices are turning down thermostats and stores are dimming lights to avoid blackouts and freezing homes this winter in the fallout from Russia’s war in Ukraine

- The cost of French power jumped to a fresh record as its nuclear fleet faces further outages going into what’s set to be a very expensive winter. UK households will pay almost triple the price to heat their homes this winter compared with a year ago

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks took impetus from Wall St where stocks eventually shrugged off the initial choppy mood and ramped up heading into the close with outperformance in the Nasdaq amid a lower yield environment. ASX 200 was underpinned amid a slew of earnings releases and with the consumer-related sectors leading the gains after Australia’s largest retailer Wesfarmers reported a 9% increase in revenue. Nikkei 225 gained from the open with the index unfazed by firm Tokyo CPI data which printed its fastest pace of increase since 2014, as this is seen as unlikely to trigger an adjustment of BoJ policy. Hang Seng and Shanghai Comp conformed to the constructive mood as participants digested a slew of earnings results including PetroChina’s record profit and with tech stocks buoyed after delisting concerns were soothed by reports that China and the US are nearing a deal regarding company audits.

Top Asian News

- US suspended 26 US flights by Chinese carriers after China’s COVID action limited some US flights, according to the DOT cited by Reuters.

- Chinese state planner official says domestic inflation is likely to quicken slightly later in 2022 and early next year.

- China has asked some US-listed Chinese companies and their audit firms to make preparations for American inspections in Hong Kong, according to Reuters sources.

- Chinese Financial Regulators have informally told lenders to make more loans, and raise some banks’ loan quotas and loan-growth requirements, according to Reuters sources.

European bourses are currently contained, Euro Stoxx 50 -0.2%, as initial price action eased with catalyst thin pre-Powell. Stateside, futures are under modest pressure, ES -0.4%, and the NQ -0.6% lags slightly given modest yield upside. US Chip software producer Synopsys is set to expand into Vietnam amid the Chinese tech war, according to the Nikkei. Panasonic (6752 JT) says they are considering various EV battery business strategies, nothing decided yet.

Top European News

- Ofgem UK Energy Price Cap – Q4 2022 (GBP): Default 3549 (prev. 1971, exp. 3582), +80.06%; Standard Credit 3764 (prev. 2100), +79.2%; Prepayment Meter 3641 (prev. 2017), +80.5%.

- UK Tory leadership frontrunner Truss is considering plans to invoke Article 16 regarding the Northern Ireland Protocol within days if she becomes the next PM, according to government insiders cited by FT.

- UK Tory leadership frontrunner Truss has reportedly been meeting with the business secretary and her prospective chancellor regarding a significant support package to help with energy bills, according to The Times citing sources.

- German Economy Ministry spokesperson says they are looking at changes to the gas levy.

FX

- DXY fades earlier gains but trades within a 108.25-75 range throughout the morning.

- EUR outperforms and has been resilient as EUR/USD sees large OpEx above parity.

- GBP, AUD, CHF, and CAD are all relatively flat vs the Buck, whilst NZD and JPY lag.

Fixed Income

- Despite fairly pronounced ranges, over 100 ticks in Bunds, the general tone is tentative with benchmarks within WTD parameters.

- USTs are pressured, with yields elevated and the curve bear-steepening but, again, well within recent ranges.

- SONIA strip takes a slight dovish skew, though Gilts unfased, following the as-expected Ofgem cap announcement.

Commodities

- WTI and Brent October contracts are consolidating following yesterday’s slide in prices.

- Spot gold resides around USD 1,750/oz after dipping under its 10 DMA (USD 1,756.60/oz)

- Base metals are mixed but copper prices remain supported and reside around USD 8,250/t.

- UAE is supportive of the latest statement from Saudi Arabia on crude markets, via Reuters citing sources.

- Four ships loaded with grain are leaving Ukrainian ports and another five ships are arriving for loading, according to Al Jazeera citing the Turkish Defense Ministry.

US Event Calendar

- 08:30: July Personal Income, est. 0.6%, prior 0.6%

- July Personal Spending, est. 0.5%, prior 1.1%

- July Real Personal Spending, est. 0.4%, prior 0.1%

- 08:30: July PCE Deflator MoM, est. 0%, prior 1.0%; PCE Deflator YoY, est. 6.4%, prior 6.8%

- 08:30: July PCE Core Deflator MoM, est. 0.2%, prior 0.6%; PCE Core Deflator YoY, est. 4.7%, prior 4.8%

- 08:30: July Retail Inventories MoM, est. 1.2%, prior 2.0%

- July Wholesale Inventories MoM, est. 1.4%, prior 1.8%

- 08:30: July Advance Goods Trade Balance, est. -$98.5b, prior -$98.2b, revised – $98.6b

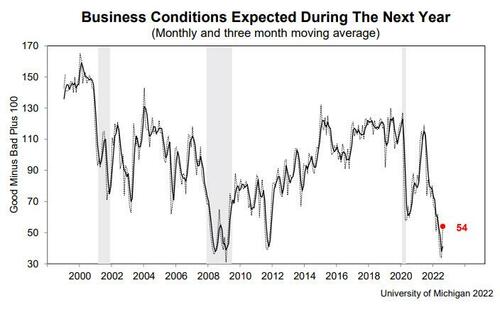

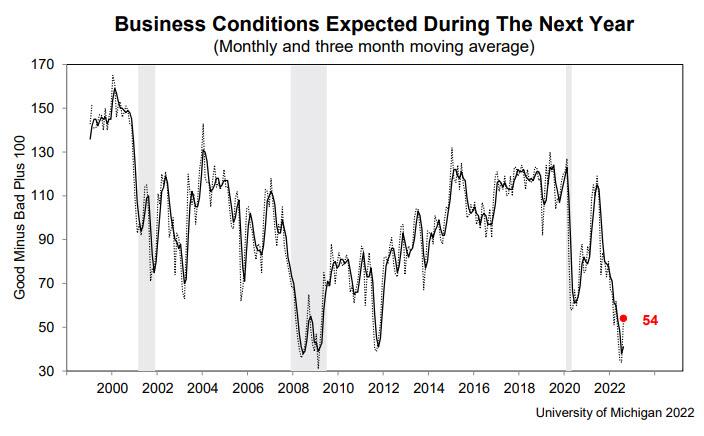

- 10:00: Aug. U. of Mich. Sentiment, est. 55.4, prior 55.1

- Aug. U. of Mich. Expectations, est. 55.0, prior 54.9

- Aug. U. of Mich. Current Conditions, est. 55.6, prior 55.5

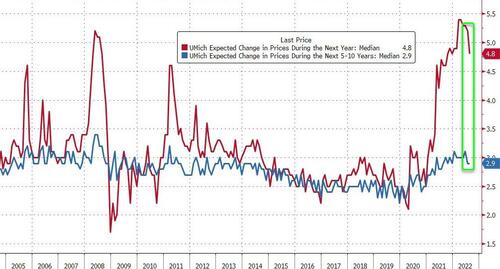

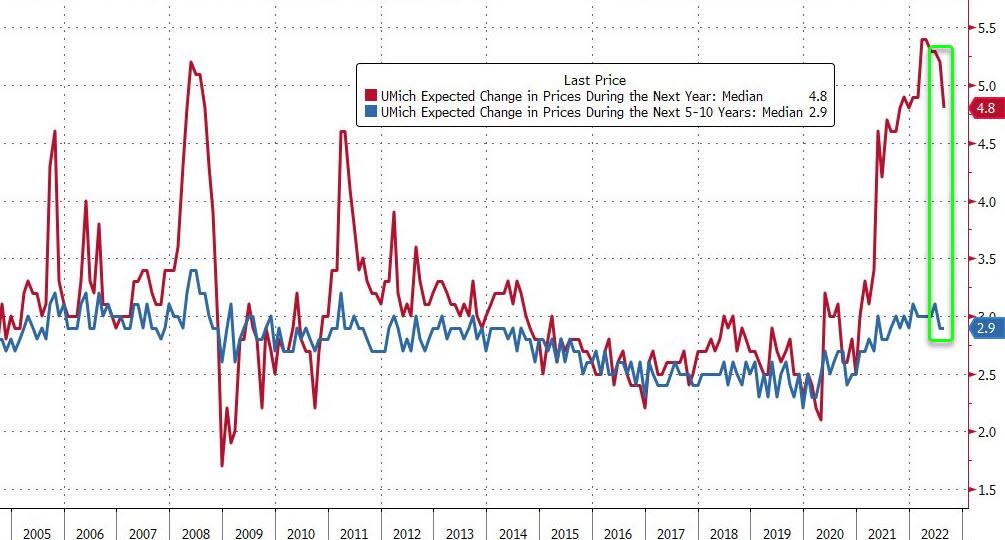

- Aug. U. of Mich. 1 Yr Inflation, est. 5.0%, prior 5.0%; 5-10 Yr Inflation, est. 3.0%, prior 3.0%

DB’s Jim Reid concludes the overnight wrap