Uncategorized · Leave a comment·Edit

Uncategorized · Leave a comment·Edit

GOLD; $1758.20 UP $9.70

SILVER: $19.24 up 21 CENTS

ACCESS MARKET:

GOLD $1758.20

SILVER: $19.25

Bitcoin morning price: $21,710 UP 169

Bitcoin: afternoon price: $21,627 up 86

Platinum price closing up $9.19 AT $886.49

Palladium price; closing UP $114.60 at $2135.20

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: AUGUST 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,747.800000000 USD

INTENT DATE: 08/24/2022 DELIVERY DATE: 08/26/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 1

132 C SG AMERICAS 1

435 H SCOTIA CAPITAL 1

624 H BOFA SECURITIES 263

661 C JP MORGAN 315

685 C RJ OBRIEN 2

690 C ABN AMRO 42

905 C ADM 15

TOTAL: 320 320

MONTH TO DATE: 33,593

JPMorgan stopped: 315/320

_____________________________________________________________________________________

GOLD: NUMBER OF NOTICES FILED FOR AUGUST CONTRACT:

320 NOTICES FOR 32,000 OZ //0.9953 TONNES

total notices so far: 33,593 contracts for 3,359,300 oz (104.488 tonnes)

SILVER NOTICES: 3 NOTICES FILED FOR 15,000 OZ/

total number of notices filed so far this month 1024 : for 5,120,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $9.70

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 984.38 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $.21

AT THE SLV// ://A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 472.900 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 3659 CONTRACTS TO 140,688. AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GIGANTIC LOSS IN OI WAS ACCOMPLISHED WITH OUR SMALL $0.12 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.12) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC SILVER LONGS AS WE HAD A STRONG LOSS OF 3030 CONTRACTS ON OUR TWO EXCHANGES, WITH ALL OF THAT LOSS DUE TO MASSIVE LIQUIDATION OF SPECULATOR SHORTS.

WE MUST HAVE HAD:

I) MASSIVE SPECULATOR SHORT LIQUIDATIONS//CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 120,000 OZ QUEUE JUMP / // V) GIGANTIC SIZED COMEX OI LOSS/(//MASSIVE SPEC LIQUIDATION)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -329

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTACTS for 19 days, total 10,488 contracts: 52.440 million oz OR 2.760 MILLION OZ PER DAY. (552 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 52.440 MILLION OZ

.

LAST 16 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 52.440 MILLION OZ (A LOT LESS THAN NORMAL//THE CROOKS ARE SCARED TO ISSUE MORE EFP’S)

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3659 DESPITE OUR SMALL $0.12 LOSS IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE CONTRACTS: 300 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /SOME BANKER ADDITIONS AND CONSIDERABLE SPEC SHORT LIQUIDATIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 120,000 OZ QUEUE JUMP // .. WE HAD A GIGANTIC SIZED LOSS OF 3359 OI CONTRACTS ON THE TWO EXCHANGES FOR 16.795 MILLION OZ AS..THE SPECS STILL BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 3 NOTICE(S) FILED TODAY FOR 15,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 1854 CONTRACTS TO 459,616 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY:–329 CONTRACTS.

.

THE FAIR SIZED INCREASE IN COMEX OI CAME WITH OUR RISE IN PRICE OF $0.50//COMEX GOLD TRADING/WEDNESDAY / WE MUST HAVE HAD ADDITIONAL SPECULATOR SHORT SHORT COVERINGS ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND CONSIDERABLE SPECULATOR SHORT COVERINGS//CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR AUGUST AT 98.367 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 4200 OZ //NEW STANDING 105.247 TONNES

YET ALL OF..THIS HAPPENED WITH OUR RISE IN PRICE OF $0.50 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 2204 OI CONTRACTS 6.855 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 350 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 459,616

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2204 CONTRACTS WITH 1854 CONTRACTS INCREASED AT THE COMEX AND 350 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2204 CONTRACTS OR 6.855 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (350) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (1854): TOTAL GAIN IN THE TWO EXCHANGES 2204 CONTRACTS. WE NO DOUBT HAD 1) CONSIDERABLE SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR AUGUST. AT 99.272 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 4200 oz. 3) ZERO LONG LIQUIDATION//// //.,4) FAIR SIZED COMEX OPEN INTEREST GAIN 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST :

49,679 CONTRACTS OR 4,967,900 OZ OR 154.523 TONNES 19 TRADING DAY(S) AND THUS AVERAGING: 2615 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAY(S) IN TONNES: 154.523 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 154.523/3550 x 100% TONNES 4.37% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 154.523 TONNES (DRAMATICALLY FALLING AGAIN)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF SEPT., FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A GIGANTIC SIZED 3659 CONTRACT OI TO 140,698 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 300 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 300 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 300 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 3659 CONTRACTS AND ADD TO THE 300 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF 3359 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 16.795 MILLION OZ

OCCURRED WITH OUR SMALL DECLINE IN PRICE OF $0.12

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED UP 31.05 PTS OR 0.97% //Hang Sang CLOSED UP 699.64 OR 3.63% /The Nikkei closed UP 165.54 OR % 0.58. //Australia’s all ordinaires CLOSED UP 0.69% /Chinese yuan (ONSHORE) closed UP AT 6.8523//OFFSHORE CHINESE YUAN UP 6.8576// /Oil UP TO 95.20 dollars per barrel for WTI and BRENT AT 101.80// / Stocks in Europe OPENED MOSTLY ALL GREEN. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 1854 CONTRACTS TO 459,616 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED WITH OUR RISE OF $0.50 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A SMALL SIZED EFP (350 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF AUGUST.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 350 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :350 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 350 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED SIZED TOTAL OF 2204 CONTRACTS IN THAT 350 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 1854 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR RISE IN PRICE OF GOLD $ 0.50. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING AUGUST (105.247),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:105.247 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $0.50) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A FAIR SIZED TOTAL GAIN ON OUR TWO EXCHANGES // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS////// WE HAVE REGISTERED A GOOD SIZED GAIN OF 6.855 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR AUGUST (105.247 TONNES)…

WE HAD -329 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE ADDED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3073 CONTRACTS OR 307,300 OZ OR 9.558 TONNES

Estimated gold volume 114,713/// extremely poor/

final gold volumes/yesterday 120,501/extremely poor

INITIAL STANDINGS FOR AUGUST ’22 COMEX GOLD //AUGUST 25

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 233,736.253 oz Brinks HSBC |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 320 notice(s) 32000 OZ 0.9953 TONNES |

| No of oz to be served (notices) | 244 contracts 24400 oz 0.7589 TONNES |

| Total monthly oz gold served (contracts) so far this month | 33,593 notices 3,359,300 OZ 104.488 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

2 customer withdrawals:

i) Out of Brinks 189,530.145 oz (5895 kilobars)

ii) Out of HSBC: 44,206.108 oz

total: 233,736.253 oz

total in tonnes: 7.27 tonnes

Adjustments: dealer to customer //0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 564 contracts having GAINED 26 contracts .

We had 16 notices served upon yesterday so we GAINED 42 contracts or an additional 4200 oz will stand for delivery in this very active month of August

Sept. lost 32 contracts to 3021 contracts.

October gained 144 contracts up to 40,539

We had 320 notice(s) filed today for 32,000 oz FOR THE AUGUST 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 320 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 315 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2022. contract month,

we take the total number of notices filed so far for the month (33,593) x 100 oz , to which we add the difference between the open interest for the front month of (AUGUST 564 CONTRACTS ) minus the number of notices served upon today 320 x 100 oz per contract equals 3,383,700 OZ OR 105.247 TONNES the number of TONNES standing in this active month of AUGUST.

thus the INITIAL standings for gold for the AUGUST contract month:

No of notices filed so far (33,593) x 100 oz+ (564) OI for the front month minus the number of notices served upon today (320} x 100 oz} which equals 3,383,700 oz standing OR 105.247 TONNES in this active delivery month of August.

TOTAL COMEX GOLD STANDING: 105.247 TONNES (A HUGE STANDING FOR AUGUST ( ACTIVE) DELIVERY MONTH)

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,344,669.896 oz 72.92 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 28,452,018.381 OZ

TOTAL REGISTERED GOLD: 13,832,132.027 OZ (430.23 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 14,619,886.352 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 11,487,463. OZ (REG GOLD- PLEDGED GOLD) 368.05 tonnes//rapidly declining

END

SILVER/COMEX/AUGUST 25

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,124,437.210 oz CNT JPMorgan Brinks |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 3CONTRACT(S) 15,000 OZ) |

| No of oz to be served (notices) | 74 contracts (370,000 oz) |

| Total monthly oz silver served (contracts) | 1027 contracts 5,135,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 0 deposits into the customer account

total deposit: nil oz

JPMorgan has a total silver weight: 170.985 million oz/330.828 million =51.69% of comex

Comex withdrawals:32

i) Out of CNT: 1,891.740 oz

ii) Out of JPMorgan: 585,547.470 oz

iii) Out of Brinks: 536,998.000 oz

total: 1,124,437.210 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 52.015 MILLION OZ

TOTAL REG + ELIG. 330.828 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR AUGUST

silver open interest data:

FRONT MONTH OF AUGUST OI: 77 CONTRACTS HAVING LOST 21 CONTRACTS. WE HAD 45 NOTICES FILED ON WEDNESDAY

SO WE GAINED 24 CONTRACTS OR AN ADDITIONAL 120,000 OZ OF SILVER WILL STAND FOR DELIVERY. THE AMOUNT STANDING

WILL NOW INCREASE//(OR REMAIN CONSTANT) ON A DAILY BASIS AS BANKERS SCOUR THE PLANET FOR BADLY NEEDED SILVER.

SEPTEMBER HAD A LOSS OF 8614 CONTRACTS DOWN TO 32,169

OCTOBER GAINED 49 CONTRACTS TO STAND AT 343

CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 3 for 15,000 oz

Comex volumes:70,597// est. volume today// good

Comex volume: confirmed yesterday: 64,885 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 1027 x 5,000 oz = 5,135,000 oz

to which we add the difference between the open interest for the front month of AUGUST(77) and the number of notices served upon today 3 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST./2022 contract month: 1027 (notices served so far) x 5000 oz + OI for front month of AUGUST (77) – number of notices served upon today (3) x 5000 oz of silver standing for the AUGUST contract month equates 5,505,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

AUGUST 25/WITH GOLD UP $9.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 18/WITH GOLD DOWN $5.25: GIGANTIC CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.78 TONNES FROM THE GLD////INVENTORY RESTS AT 985.83 TONNES

AUGUST 17/WITH GOLD DOWN $12.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 992.20 TONNES

AUGUST 16/WITH GOLD DOWN $7.85: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 993.94 TONNES

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

AUGUST 10//WITH GOLD UP $2.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES

AUGUST 9/WITH GOLD UP $6.70: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES.

AUGUST 8/WITH GOLD UP $13.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FORM THE GLD//INVENTORY RESTS AT 999.16 TONNES

AUGUST 5/WITH GOLD DOWN $14.25: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .33 TONNES FROM THE GLD////INVENTORY RESTS AT 1000.32 TONNES

AUGUST 4 WITH GOLD UP $29.00 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES FROM THE GLD///INVENTORY REST AT 1000.65 TONNES

AUGUST 2/WITH GOLD UP $3.70; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD//INVENTORY RESTS AT 1002.97 TONNES//

AUGUST 1/WITH GOLD UP $5.75: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 29//WITH GOLD UP $12.50; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1005.29 TONNES

JULY 28/WITH GOLD UP $31.25; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 27.//WITH GOLD UP $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 26/WITH GOLD DOWN $1.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.29 TONNES

JULY 25/WITH GOLD DOWN $7.85: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 1005.87 TONNES

JULY 22/WITH GOLD UP $17.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 21/WITH GOLD UP $11.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.101 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.87 TONNES

JULY 20/WITH GOLD DOWN $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1009.06 TONNES

JULY 19/WITH GOLD DOWN $.35 :BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.22 TONNES FROM THE GLD//INVENTORY RESTS AT 1009.06 TONNES

GLD INVENTORY: 984.38 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 25/WITH SILVER UP 21 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

AUGUST 18/WITH SILVER DOWN 27 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 369,000 OZ INTO THE SLV////INVENTORY RESTS AT 485.482 MILLION OZ//

AUGUST 17/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.106 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.113 MILLION OZ//

AUGUST 16/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 486.219 MILLION OZ/

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 10/WITH SILVER UP 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 9/WITH SILVER DOWN 25 CENTS TODAY: TWO CHANGES IN SILVER INVENTORY AT THE SLV: FIRST: A DEPOSIT OF 461,000 OZ INTO THE SLV AND THEN A WITHDRAWAL OF 1.014 MILLION OZ..//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 8/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 5/WITH SILVER DOWN 28 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 922,000 OZ FROM THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 4 WITH SILVER UP 21 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 527,000 OZ FROM THE SLV////INVENTORY RESTS AT 486.634 MILLION OZ

AUGUST 2/WITH SILVER DOWN 21 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.504 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.161 MILLION OZ//

AUGUST 1/WITH SILVER UP 17 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE GLD: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 483.657 MILLION OZ//

JULY 29/WITH SILVER UP 30 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 461,000 OZ FROM THE SLV..//INVENTORY RESTS AT 483.657 MILLION OZ/

JULY 28/WITH SILVER UP $1.24 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 484.118 MILLION OZ/

JULY 27/.WITH SILVER UP 4 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL 11.479 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 484.118MILLION OZ//

JULY 26/WITH SILVER UP 16 CENTS: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.504 MILLION OZ FROM THE SLV//: //INVENTORY RESTS AT 495.597 MILLION OZ//

JULY 25/WITH SILVER DOWN 24 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.383 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 499.101 MILLION OZ//

JULY 22/WITH SILVER DOWN 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 500.484 MILLION OZ//

JULY 21/WITH SILVER UP 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.19 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 500.484MILLION OZ/

JULY 20/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 8.253 MILLION OZ FORM THE SLV/INVENTORY RESTS AT 507.585 MILLION OZ//

JULY 19/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ//

CLOSING INVENTORY 472.900 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

Into The Black Hole – Six Months Of War With No End In Sight

THURSDAY, AUG 25, 2022 – 07:20 AM

Authored by James Rickards cia DailyReckoning.com,

The war in Ukraine has been dragging on for six months with no end in sight.

Russia is slowly and systematically advancing, while the Ukrainian military is being ground down in the Donbas region of eastern Ukraine.

On balance, Russia is winning the war, although progress is slow.

Russia will next likely move to take Odesa, a strategically key Black Sea port. Russia has staged missile attacks on Odesa in recent days. If Russia ultimately takes Odesa, it removes Ukraine’s access to the sea, effectively rendering it completely landlocked.

But there don’t appear to be any plans for an imminent Russian attack on Odesa. At any rate, a negotiated peace settlement is nowhere in sight. Neither side will accept the other’s demands.

Meanwhile, a car bomb killed the daughter of “Putin’s brain” this past weekend near Moscow. Alexander Dugin is an ardent Russian nationalist whose thinking is said to have influenced Putin. His daughter was killed in the blast, although many suspect he was the intended target.

Russia blames Ukraine for the attack, which Ukraine denies. How Russia responds remains to be seen.

What’s the Endgame?

As the war drags on with no end in sight, there’s also no end in sight to the flow of U.S. aid to Ukraine. It’s an open-ended commitment with no clearly defined objective.

Both the Democratic and Republican parties support the spending, except for a minority who are vilified as Putin stooges and apologists.

Supporters talk about standing up for democracy, but Ukraine is a corrupt oligarchy that’s just about as corrupt as Russia. It’s far from a model democracy.

But the aid’s for a good cause, they say. We’re helping defeat aggression and assisting a weaker nation stand up against a much stronger attacker.

Well, that’s fine, but there’s little to no oversight to supervise the transfers. Where’s the U.S. aid to Ukraine going?

The aid is being stolen off the top or diverted to corrupt officials. Goods are often stolen and resold on the black market. Weapons are also sold on the black market. In all, very limited amounts of aid are actually going to the war effort.

Massive Corruption

One Ukrainian volunteer fighting in the Donbas has said:

In Ukraine, people cheat each other even in war. I’ve watched the medical supplies donated to us being taken away. The cars that drove us to our position were stolen. And we have not been replaced with new soldiers in three months, though we should have been relieved three times by now…

If I had known how much deception there was in this army, and how everything would be for us, I never would have joined. I want to go home, but if I flee, I face prison.

Here’s what a Ukrainian journalist has to say:

The corruption related to the war aid is shocking. The weapons are stolen, the humanitarian aid is stolen and we have no idea where the billions sent to this country have gone.

Of course, your tax money is paying for this swindle.

Wartime Sacrifice?

Here’s an idea of where at least some of the billions have gone. Last month, the Ukrainian parliament voted to give itself a 70% pay raise, while the army is collapsing and the Ukrainian people are suffering.

So much for wartime sacrifice. Moreover, Western admirers of Ukrainian president Zelenskyy have praised him as a modern Winston Churchill, defyingly resisting an evil aggressor.

But Zelenskyy is no Churchill.

He’s succeeded in presenting himself as a strong wartime leader, standing up to the big, bad Putin. But in reality, he’s a corrupt oligarch with millions of dollars hidden offshore. His acting skills have enhanced his propaganda efforts, but it doesn’t take much training to see how phony he is.

Innocent civilians, including women and children, are dying under his failed leadership and inability to come to terms with Putin before the invasion began.

The True U.S. Objective in Ukraine

But the same journalist who complained about the widespread corruption has figured out the real U.S. strategy in Ukraine:

It is obvious that the U.S. doesn’t want Ukraine to win the war. They only want to make Russia weak. No one will win this war, but the countries the U.S. is using like a playground will lose.

That’s exactly right. The U.S. has no vital interest in Ukraine worth going to war over. Its real aim is to weaken Russia through a protracted war in Ukraine. The longer it drags on, the better, no matter how many Ukrainians have to die in the process.

In other words, the U.S. is willing to fight Russia to the last Ukrainian.

That may sound overly cynical, but it really isn’t. It’s just an objective assessment based upon the facts on the ground. But don’t take my word for it.

As Defense Secretary Lloyd Austin has said, “We want to see Russia weakened to the degree that it can’t do the kinds of things that it has done in invading Ukraine.”

Sanctions Are a Complete Failure

Meanwhile, the sanctions regime against Russia has proven to be a complete failure. Sanctions have had zero impact on Russian advances on the battlefield and Russian goals in Ukraine. In fact, Putin has run rings around the sanctions.

Instead of the ruble collapsing, it has strengthened in the face of Western sanctions. And boycotting Russian exports of oil and natural gas was pointless because Russia just sold the same energy to China and India instead of Europe. It’s a world market, after all.

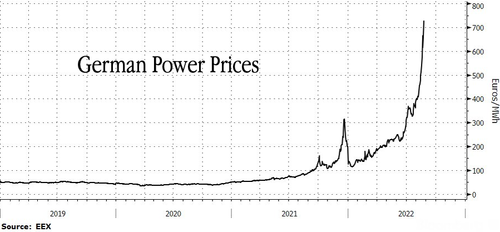

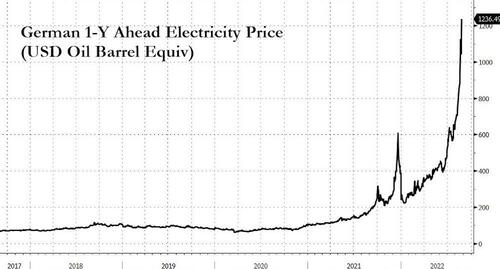

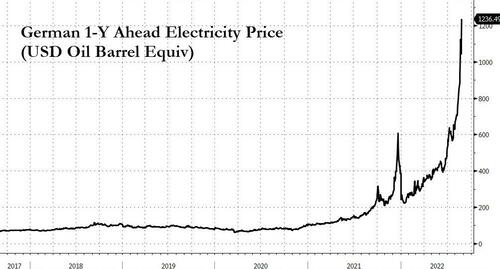

European countries like Germany are so dependent on Russian energy that they’re facing severe shortages and a bleak winter without it. Germany faces a catastrophic winter in which factories will have to be closed, homes will have to reduce heat to 50 F and hot showers may be a thing of the past.

It’s all because Germany made a political decision to side with the climate alarmists and Greens

despite the lack of scientific evidence supporting their claims. They became utterly dependent on Russia as a result.

When reality collides with ideology, reality wins every time. Now Germany will pay the price. Meanwhile, global food shortages and possibly famine are real possibilities this winter because Ukrainian and Russian grain won’t be delivered.

The tragedy is that all of this could have been prevented had the U.S. and NATO guaranteed Russia that Ukraine would never be invited into the alliance. That’s not a defense of Putin’s invasion, by the way, which I condemn. It’s just reality.

Now the world is living with the results.

END

LAWRIE WILLIAMS: Gold on the rise as Fedwatch tool moves in favour of 75 bps increase

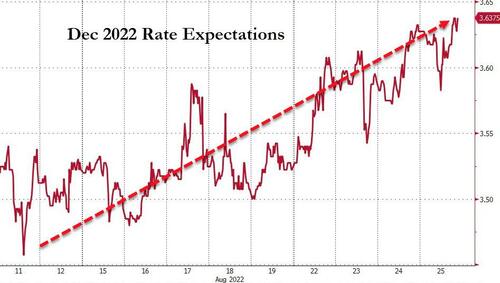

We recently commented on the volatile nature of the Chicago Mercantile Exchange’s Fedwatch Tool which analyses market sentiment on what the Fed’s most likely rate increase will be at the next FOMC meeting – still nearly a month away. This is a great day-to-day pointer to market sentiment on the state of the U.S. economy, and thus on short term market movements in all sectors that are dependent on such perceptions.

Over the past couple of days this has moved from favouring, only marginally, a 50 basis point rate increase being imposed at the September meeting to today’s 56.5:43.5 likelihood of the higher 75 basis point rise forthcoming. Of course this ratio is likely to be changed one way, or the other, by the latest U.S. GDP data, which has come out today, the Personal Consumption Expenditure (PCE) index data out tomorrow and analysis of Fed chair Jerome Powell’s address to the Jackson Hole Economic Symposium, also tomorrow. We could thus see some sharp movements in the Fedwatch forecasts by the weekend.

But of course the actual FOMC meeting does not take place until September 20th – 21st, allowing ample time for other relevant data, both economic and geopolitical, to affect the final rate increase decisions. Not least among these will be the next U.S. Consumer Price Index (CPI) data release due out on September 13th which will give us some idea if the Fed’s relatively aggressive interest rate raising policies so far are having any effect on inflation at all – and even if overall inflation appears to be easing the conclusions may still be inconclusive given that one of the biggest inflationary elements, the oil price, has been moderating on influences entirely outside Fed involvement. A worrying factor here is that it seems to be picking up slowly again, albeit still remaining well below recent peaks. Analysis of the core inflation figure, which excludes the biggest variables of energy and food prices, may thus give a better indication of the true state of affairs

There is a theory among some well-respected analysts that the Fed will not be too displeased if the U.S. economy is indeed seen to be seen either already in recession, or heading there, and will possibly give this likelihood something of a boost by raising rates by the higher 75 basis points which will have a negative impact on corporate performance. Hence the latest movements in the Fedwatch tool. This would depress equity prices and could give the dollar index a further leg up. What this might do to precious metals prices is a little more uncertain.

In theory a stronger dollar would tend to signify a weaker gold price in dollar terms but this is not always the case as the safe haven aspects of gold also tend to come into play with such Fed moves suggesting a continuing worry about the inflationary impact on the U.S. economy. Gold is sometimes viewed as an inflation hedge so it could also benefit. Certainly its early performance today in European markets was positive, although that could also have been due to a slightly weakening dollar. As trade has progressed in the U.S. this morning the price has slipped although is still up on yesterday’s close, with U.S. jobless claims falling a little, contrary to expectations and the GDP figure confirming a small Q2 contraction.

The markets will take a little time to digest this, but will largely be waiting on Powell’s Jackson Hole address and the new PCE data figure, before it draws any new conclusions. But the FOMC meeting is still 27 days away leaving plenty of time, and relevant data release announcements, to influence sentiment in the meantime. Interesting times ahead as the summer holiday period draws to a close and market makers and influencers are all back at their desks!

25 Aug 2022

3.Chris Powell of GATA provides to us very important physical commentaries

Quite a story: Ghana allows Chinese state mining operation Shaanzi Mining company steal and murder local residents

(Syndey Morning Herald)

Ghana lets Chinese gold mining company murder local residents, steal from adjacent mine

Submitted by admin on Wed, 2022-08-24 22:37Section: Daily Dispatches

Blood Gold: In Africa’s Gold Country an Australian Firm

Is Embroiled in a Bitter and Deadly $395 Million Dispute

By Eryk Bagshaw and Edward Adeti

Sydney Morning Herald

Thursday, August 25, 2022

The tunnel runs 150 metres underground. Inside, Australian mining manager Andrew Head is trudging through mud and muck. He only has a headlight to guide him as the temperature in this dark pit in western Africa hits 45 degrees.

The tunnel has gold running through its veins. Head, a rugged 48-year-old, father-of-three from Sydney’s northern suburbs is searching for gaps in the wall.

“It’s 100% humidity. There is water leaking everywhere and you’re wading all the time in human faeces,” he says. “It’s like a scene from ‘Raiders of the Lost Ark.'”

Two companies bought access to this barren patch of earth in Talensi, northern Ghana, in 2008 and 2014. Now one of them is hitting paydirt while the other is crying foul play.

Separated by 2½ kilometres of rock, rubble, and poverty above ground, the mines stand opposite each other. One is an Australian exploration mine run by Cassius Mining Ltd. The other is a Chinese state-linked mine run by the Shaanxi Mining Co.

Both came here to make their fortune by tapping into the rich veins of gold that run through this ancient terrain but competition soon turned to suspicion and hostility. Now they are involved in a bitter dispute over claims of trespass, theft, and the deaths of more than a dozen miners. …

… For the remainder of the report:

https://www.smh.com.au/interactive/2022/blood-gold/index.html

END

A must read: Pritchard states that the Fed wants to crush stock markets to get inflation under control

(Ambrose Evans Pritchard)

Ambrose Evans-Pritchard: Fed wants to crush stock markets, so ignore it at your peril

Submitted by admin on Wed, 2022-08-24 22:55Section: Daily Dispatches

By Ambrose Evans-Pritchard

The Telegraph, London

Wednesday, August 24, 2022

Beware the wrath of the U.S. Federal Reserve at this week’s conclave of central bankers in Jackson Hole, Wyoming. The Fed is determined to break Wall Street’s torrid and unwelcome rally, a bear-trap variant if ever there was one.

The presidents of the Richmond, St Louis, and San Francisco Federal Reserve Banks have scorched the ground in different ways over recent days, either warning that the Federal Open Market Committee is itching to raise rates by a further 75 basis points next month, or that the Fed will not hesitate to lurch into monetary overkill and inflict a deliberate recession if need be.

Even the ultra-dovish president of the Minneapolis Fed is breathing fire.

It would be extraordinary if Chairman Jay Powell did anything other than endorse this declaration of muscular intent at the Grand Tetons on Friday.

The Fed is openly irritated that markets have jumped the gun. It thinks investors have misunderstood the unscripted comments by Powell last month — easily misunderstood, it has to be said — as evidence of an early “pivot” in the interest rate cycle and a licence for fresh excess in tech stocks and frothy asset markets across the world. …

… For the remainder of the analysis:

There is every sign that the Fed actively wishes to crater equity prices in order to restrain demand through the wealth effect. It wishes to push up junk yield spreads and restore some Schumpeterian discipline to corporate finance. It wishes to tighten financial conditions as a mechanism for choking inflation. It is a “tug of war” between the Fed and the markets, says Krishna Guha from Evercore ISI.

The institution is willing to let the dollar index (DXY) vault to a 20-year high and tighten the tourniquet for emerging markets. It intends to accelerate the pace of quantitative tightening (QT) in September with $95bn of monthly bond sales. It intends to drain liquidity from the world’s dollarised financial system, and the rest of us can drop dead. Fight this Fed if you dare.

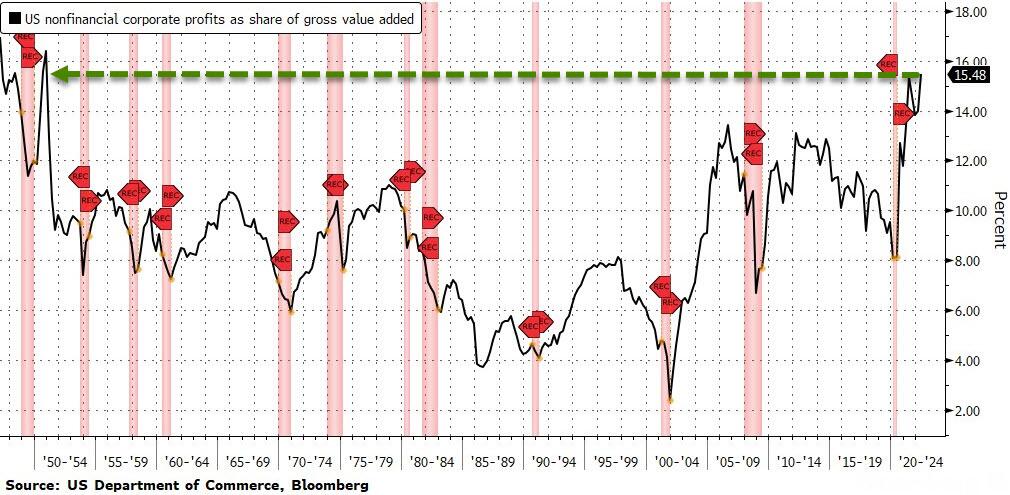

Bulls retort that US corporate profits have defied dire predictions. Earnings muddled through in the second quarter, although they fell by 4pc (year-on-year) sans energy, and revisions are coming in thick and fast. Factset says most S&P 500 companies that have spoken so far are issuing negative guidance for this quarter.

There is another catch. The next downturn will be different from past episodes. Companies are going to hoard labour to avoid the sort of reopening shortages we have seen since the end of the pandemic. “It’s what we always used to see in Japan in the 1980s and 1990s: consumption holds up better in the recession, but profits take the strain and collapse,” Albert Edwards from Societe Generale.

Furthermore, the equity rebound from mid-June to mid-August – 14pc for the S&P 500, 22pc for the Nasdaq, 7pc for the FTSE 100 – has been fuelled in part by what CrossBorderCapital calls the “Fed’s QT summer lull”.

This was caused by a quirk in the market for mortgage bonds held by the Fed. The effect will be overwhelmed once QT begins in earnest next month. That is when the real trouble begins. The Fed has repeatedly been caught off guard before by the potent effects of bond sales, chiefly because it disregards the quantity of money effect.

The Fed laid out its theory in a paper in June: the house model equates $2.5 trillion of QT to nothing more than two quarter point rate rises. This is contestable in monetary theory and empirically false if you live in the real world of the markets. If the Fed really thinks that $2.5 trillion of QT is little more than background noise, there is going to be blood on Wall Street and world bourses.

In essence, investors have been betting that US inflation has already peaked, that the Fed will soon roll over (whatever it says), and that the US economy remains in rude good health. This glorious combination opens the way for another leg of the bull market.

You can certainly paint such a rosy scenario. The US economy added over half a million jobs in July. If the US has one foot in recession, it is an odd sort of recession.

But be careful. The headline non-farm payrolls figure is a lagging indicator. “It is at odds with a rather impressive list of data. Could it be that payrolls are right and everything else is wrong?” said Tom Porcelli, a former New York Fed official now at RBC Capital.

Measures that catch turning points earlier are ominous. Weekly initial claims – unemployment filings – have been climbing since March. Full-time employment has dropped by 150,000 since then under the “household survey” measure. A string of industrial surveys have been dire. The New York Fed’s manufacturing index (Empire State) has collapsed to 2008 levels.

Yes, inflation is looking better behaved. The headline rate dropped from 9.1pc in June to 8.5pc in July, and was slightly negative on a month-to-month basis. This was not just because of falling oil and commodity prices. Clothing is in deflation too.

But, again, be careful. Inflation may fall too fast for comfort. The US money supply figures have swung from boom to bust. Over the last three months M1 money has contracted in absolute terms, and has been falling at a double-digit annual pace in real terms. If this does not lead to recession this winter, it will be a miracle.

The greatest danger is the behaviour of the Fed itself. The institution seems not to have learned any theoretical lesson from what has gone wrong. It clings to its old model. It persists in ridiculing money data. It is therefore in the process of repeating the mistake it made two years ago when it generated today’s inflation, but this time in the opposite deflationary direction through monetary overkill.

Never overlook the emotional element in central banking. Last year’s gathering at Jackson Hole saw much self-congratulation among the global monetary fraternity. Had they not printed their way through Covid with daring and panache? Had they not saved civilisation?

Mr Powell insisted then that there were no signs of “broad inflationary pressures” and that any jump in prices would prove “transient”. He stressed that inflation expectations remained “anchored” – as indeed they were, further evidence of the uselessness of that monetary lodestar.

A year later, the historical verdict is brutal. The 2021 forum was a humiliating fiasco: the requital for New Keynesian hubris, and the end of the superstar central banker as a Jupiterian deity.

Mr Powell and his colleagues are now on a mission to redeem themselves and prove that they can conquer inflation after all. Zeal is a dangerous thing. That is why I fear the Jackson Hole of 2022.

-END-

end

4. OTHER GOLD/SILVER COMMENTARIES

-END-

A very important read.

5.OTHER COMMODITIES: COFFEE

Could Poor Coffee Harvests Send Prices Even Higher?

WEDNESDAY, AUG 24, 2022 – 05:20 PM

Coffee prices have been in a tight trading pattern for much of this year and at the highest levels since the commodity boom a decade ago. Poor harvest outlooks and tighter global supplies could send prices even higher.

Let’s first examine the world’s largest coffee exporter, Brazil — its top producing areas of Parana, Sao Paulo, and Minas Gerais are expected to produce poor harvests because of drought and frost. This means global supplies will tighten further, resulting in what could be even more coffee inflation for US consumers.

“Very dry weather over Brazil’s major arabica-growing regions during the second half of August added to drier-than-normal conditions the region has seen” due to the La Nina weather phenomenon, the Hightower Report said. – Bloomberg

Meanwhile, adverse weather conditions have hurt coffee production in neighboring Colombia, another major producer. Producers in Honduras, Guatemala, Nicaragua, and Costa Rica also show crop stress signs.

Across the world, in Vietnam, the second-largest coffee producer and top supplier of robusta, stockpiles will be halved by the end of September versus a year ago, according to the median estimate in a Bloomberg survey of traders.

Dwindling reserves and poor global harvest outlooks come as demand increases. The International Coffee Organization stated global demand would outpace supply for the second consecutive year. At the same time, Fitch Solutions said bean stocks in Intercontinental Exchange warehouses are at their lowest point this century.

We noted last year that Caribou Coffee Co. stockpiled extra beans in late 2021.

Rabobank’s Carlos Mera warned in February that coffee prices might ‘soar out of control‘ due to dwindling stockpiles.

So far, Arabica coffee futures have been range bound since the beginning of the year after a 180% run-up from the early days of the pandemic.

The tight trading range between $2-2.50 per pound suggests a big move is coming — and if poor harvests continue in top producing countries with outsized global demand, this may imply prices could head higher.

end

COMMODITIES IN GENERAL/COAL

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.8523

OFFSHORE YUAN: 6.8576

HANG SENG CLOSED UP 699.64 PTS OR 3.63%

2. Nikkei closed DOWN 165.54 OR 0.58%

3. Europe stocks CLOSED ALL GREEN

USA dollar INDEX DOWN TO 108.22/Euro RISES TO 0.9986

3b Japan 10 YR bond yield: RISES TO. +.224/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 136.39/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP -// OFF- SHORE: UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.338%/Italian 10 Yr bond yield FALLS to 3.55% /SPAIN 10 YR BOND YIELD FALLS TO 2.51%…

3i Greek 10 year bond yield FALLS TO 3.90//

3j Gold at $1762.50 silver at: 19.31 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 9/100 roubles/dollar; ROUBLE AT 59.79//

3m oil into the 95 dollar handle for WTI and 101 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 136.39DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 9634– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9621well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

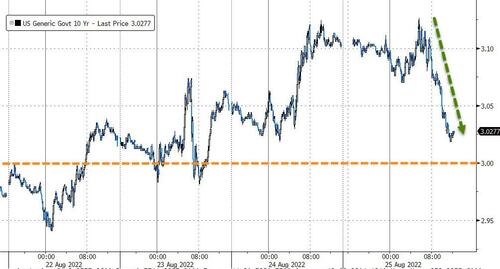

USA 10 YR BOND YIELD: 3.091 DOWN 2 BASIS PTS

USA 30 YR BOND YIELD: 3.298 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,16

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Jump As China Adds Fresh 1 Trillion Yuan Stimulus, But J-Hole Jitters Dominate

THURSDAY, AUG 25, 2022 – 08:04 AM

Futures jumped overnight after China revealed its latest massive stimulus (which however is still woefully insufficient to prop up the country’s crashing housing sector) steadied nerves in the nervous wait for Fed Chair Jerome Powell’s key speech at 8am tomorrow.

Shortly after 2am ET, China stepped up its economic stimulus with a further 1 trillion yuan ($146 billion) of funding largely focused on infrastructure spending, support that analysts quickly agreed won’t go far enough to counter the damage from repeated Covid lockdowns and a property market slump. The State Council, China’s Cabinet, outlined a 19-point policy package on Wednesday, including another 300 billion yuan that state policy banks can invest in infrastructure projects, on top of 300 billion yuan already announced at the end of June. Local governments will be allocated 500 billion yuan of special bonds from previously unused quotas. However, as has been the case for the past 2 years with Beijing’s drip-drip stimulus, economists were downbeat on the measures, while financial markets were muted. The yield on 10-year government bonds rose 2 basis points to 2.65%. China’s CSI 300 Index of stocks rose as much as 0.6% before paring gains to trade up 0.3% as of 2:28 p.m. local time. A similar reaction was observed in US futures which initially spiked by nearly 30 points, reaching a high of 4187.5 before fading most of the gains; emini futures traded +0.6%, or 25 points higher, at 7:30am ET, while Nasdaq futures were up 0.85%. Emerging-market stocks also rallied the most in two weeks on the Chinese stimulus news, only to see gains fade. Treasury yields and a dollar gauge dipped, while the crypto space rose on China’s stimulus.

The Chinese-inspired gains failed to stick as traders expect markets to remain volatile as they look to Powell’s comments due Friday at the Jackson Hole meeting for clues on the pace of US monetary tightening. Fed officials in the run-up to Jackson Hole have been clear they see more monetary tightening ahead, a message that’s eroded a bounce in stocks and bonds from mid-June troughs. The tension in markets is whether those assets will continue to head back toward the lows of the year.

“Powell is likely to push back on premature expectations of a dovish pivot, reiterating the focus on the fight against high inflation,” said Silvia Dall’Angelo, a senior economist at Federated Hermes Ltd. “Whether markets take him seriously amid an increasingly gloomy outlook for the global economy is yet to be seen.”

In premarket trading, Chinese stocks in the US rallied amid recent positivity over Beijing boosting stimulus with a further 1 trillion yuan of funding, and as the country takes measures to shore up its currency. Tesla shares rose 2% as the electric-vehicle maker’s 3-for-1 stock split takes effect, confirming US markets remain dominated by idiots. Snowflake shares soared ~17% in premarket trading after the infrastructure software company reported second-quarter revenue that beat expectations and raised its full-year forecast for product revenue. On the other end, Nvidia shares slide ~4% in premarket trading after the chipmaker, which preannounced a month ago and gave a dire forecast, did it again and gave a third- quarter revenue forecast that was below expectations as demand for chips used in gaming computers slipped. Other notable premarket movers:

- Salesforce (CRM US) shares are down 6.6% in premarket trading after the application- software company reported second-quarter results that beat expectations but lowered its full-year forecast. Analysts note that the company’s forecast is being hit by FX headwinds and delays in closing large deals.

- Teladoc Health (TDOC US) shares climb 5% in premarket trading after Amazon says it will close its primary care and telehealth service by the end of the year.

- Bed Bath & Beyond (BBBY US) shares rose as much as 6% in US premarket trading before turning lower. The fluctuation follows a report that the home furnishings retailer is nearing a $375 million loan deal with Sixth Street Partners.

- Kinetik (KNTK US) initiated with an equal-weight recommendation and Street-high price target at Morgan Stanley, which says the midstream services company offers an “attractively positioned set of Permian midstream assets run by a growth-oriented management team.”

- NetApp (NTAP US) shares were up ~4% in extended trading after the computer hardware company reported first-quarter results that beat expectations and affirmed its forecast. Analysts note the company continues to see broad-based demand strength, despite supply challenges and FX headwinds.

In Europe, the Stoxx 50 rose 0.3%, paring an earlier advance amid mixed economic data from the region’s biggest economy. Energy and basic resources stocks were the biggest gainers, with retailers underperforming. Sovereign bonds across Europe gained led by short-end bonds. IBEX outperforms, adding 0.6%, FTSE MIB lags, adding 0.1%. In fixed income, short-end bonds lead the move. Here are some of the biggest European movers today:

- Harbour Energy shares jump as much as 13%, the most since November 2020, as analysts applaud an increased buyback and strong cash flows. Jefferies says 1H results “beat on all metrics”

- Ambu rises as much as 11% on its latest earnings, which were in-line with figures released on Aug. 3. Handelsbanken sees a “no drama” report and DNB highlights a positive free cash flow

- Rentokil gains as much as 2.7% after JPMorgan put the pest control company on a positive catalyst watch as the closing date for the Terminix acquisition nears

- Hunting rises as much as 19% after the company posted better-than-expected profitability, while the outlook for the rest of 2022 and 2023 is positive

- Yara gains as much as 2.8% as Citi flags rising demand for fertilizers. Yara earlier said it would cut production, citing record gas prices

- Tessenderlo climbs as much as 8.1% to a level last seen in April after the Belgian chemicals company raised annual guidance again and said it sees adjusted Ebitda for the year rising 15% to 20%

- Komax rises as much as 5% after Credit Suisse raises the wire processing machines maker to outperform, seeing its recent merger with Schleuniger as highly- accretive

- Elekta falls as much as 11% after the firm presented its latest earnings. Jefferies noted a “disappointing” drop in order intake, while Handelsbanken flags a soft outlook

- Baloise drops as much as 7.6%, hitting the lowest since March, after the Swiss financial services firm reported solid, “yet unspectacular” results, according to Vontobel

- Daetwyler falls as much as 6.3%, the most since May, as Credit Suisse cut its price target on the rubber components and seals maker following its results in the prior session

- Grafton declines as much as 5.4% after reporting 1H profit that missed expectations. The company said the weakness was due to hot weather in the UK and less construction activity

Earlier in the session, Asian stocks rebounded strongly after a five-day loss to head for their biggest advance since the end of May, boosted by a late surge in Hong Kong shares. The MSCI Asia Pacific Index climbed as much as 1.6% late in the Asian day, with Hong Kong-listed Chinese tech stocks like Alibaba and Tencent being the biggest contributors to its gain. The gauge’s increase earlier in the session was driven by export-heavy markets like Korea and Taiwan as the dollar weakened. The Hang Seng Index surged 3.6%, the most since April 29, leading the late regional rebound that some traders attributed to short-covering ahead of a key speech by Federal Reserve Chair Jerome Powell at the Jackson Hole conference. The morning trading session in Hong Kong was suspended due to a tropical storm warning. The amount of bearish bets against Hong Kong stocks rose to levels that could trigger a surge in share prices as traders rush to close out their positions, according to quantitative analysts at Morgan Stanley. A gauge of Chinese tech names listed in the financial hub soared 6%. It is still down about 25% this year. Markets have been edgy ahead of Powell’s speech, with the MSCI Asia gauge losing 3.1% in the last five sessions.

Thursday’s move looks like “pre-positioning,” said Justin Tang, the head of Asian research at United First Partners. “Investors are taking positions on expectations” of a less hawkish commentary from Powell, he said. Chinese stocks on the mainland also rose as the nation stepped up measures to bolster growth with a further 1 trillion yuan ($146 billion) of stimulus. South Korean shares gained on foreign buying even after the nation’s central bank raised its key interest rate by 25 basis points, while Taiwanese stocks also climbed. “It may be a combination of risk-on sentiment across the region heading into Jackson Hole and the China support measures,” said Marvin Chen, a strategist with Bloomberg Intelligence. “Growth, tech and offshore-listed China stocks are leading gains suggesting that Fed meeting may be playing a bigger role in the late-day move.”

Japanese equities advanced, with the Nikkei 225 posting its first gain in six sessions, as the market looked ahead to remarks Friday from Fed Chair Jerome Powell at the Jackson Hole meeting. The Nikkei rose 0.6% to close at 28,479.01, while the Topix added 0.5% to 1,976.60. Daiichi Sankyo Co. contributed the most to the Topix gain, increasing 4.6%. Out of 2,170 shares in the index, 1,445 rose and 597 fell, while 128 were unchanged. “Investors will continue to take a wait-and-see stance until after the speech by Chairman Powell scheduled for the 26th,” said Takashi Ito, a senior strategist at Nomura Securities. “After a round of buying, there is a possibility that there will be a small drop.”

Australia,’s S&P/ASX 200 index rose 0.7% to close at 7,048.10, driven by gains in banks and mining shares. The materials sub-gauge rallied to its highest level since June 16, amid advances in iron ore prices. Uranium company Paladin was the top performer, surging after Japan said it is planning a dramatic shift back to nuclear power more than a decade on from the Fukushima disaster. City Chic was the biggest decliner after it flagged an uncertain outlook. In New Zealand, the S&P/NZX 50 index fell 0.2% to 11,627.14

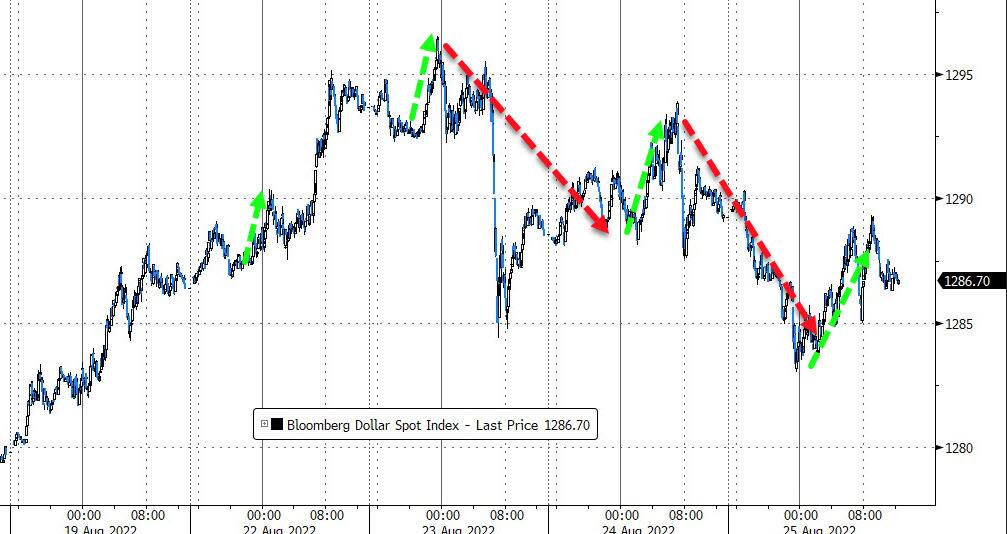

In FX, the Bloomberg Dollar Spot Index fell as the greenback weakened against all of its Group-of-10 peers. The Aussie led G-10 gains, jumping as much as 1.1% against the greenback as traders turned more optimistic after China announced fresh economic stimulus with a further $146 billion of funding largely focused on infrastructure spending. Australia’s dollar outperformed the kiwi after New Zealand reported disappointing retail sales data. The euro rose to briefly trade above parity against the dollar. Germany’s economy proved more resilient than initially thought in the second quarter, growing 0.1% despite surging inflation and the war in Ukraine; the initial reading was 0%. Separately, German Aug. Ifo business confidence came in at 88.5 vs est. 86.8. The gauge of business expectations for the next six months inched down to 80.3 from 80.4, but better than forecast 79.0. Yen rose on flows-driven trade amid a decline in US yields and general dollar weakness during Asian hours

In rates, Treasury futures were off session highs into the early US session, although yields remained richer by 1bp-2bp across the curve, following wider gains across UK gilts where 10s rally as much as 7bp on the day. US 10-year yields around 3.09%, richer by ~1bp on the day with bunds and gilts outperforming by 2bp and 5bp in the sector; curves steady with gains seen across maturities. US auctions conclude with 7-year note sale at 1pm New York time. European bonds advanced in a rally that was led by Italian bonds. Gilts outperform USTs and bunds; gilts 2-year yields drop ~10bps to 2.81%. USTs push higher, led by the belly. Bunds 2-year yield down about 5.5bps to 0.85%. Peripheral spreads tighten to Germany with 10y BTP/Bund narrowing 5.1bps to 225.7bps. Benchmark 10-year JGB yield climbed to its highest in more than a month. The yield on China’s 10-year government bonds rises the most since June 27 after the State Council outlined a 19-point policy package to stimulate the economy. The 10-year yield advanced 3bps to 2.66% while the 30-year note yield gained 3bps to 3.14%.

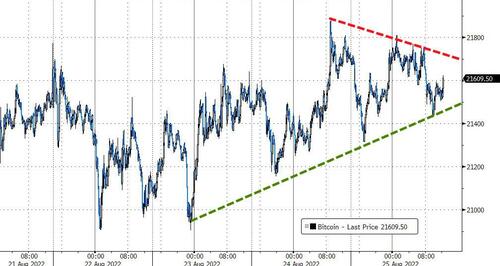

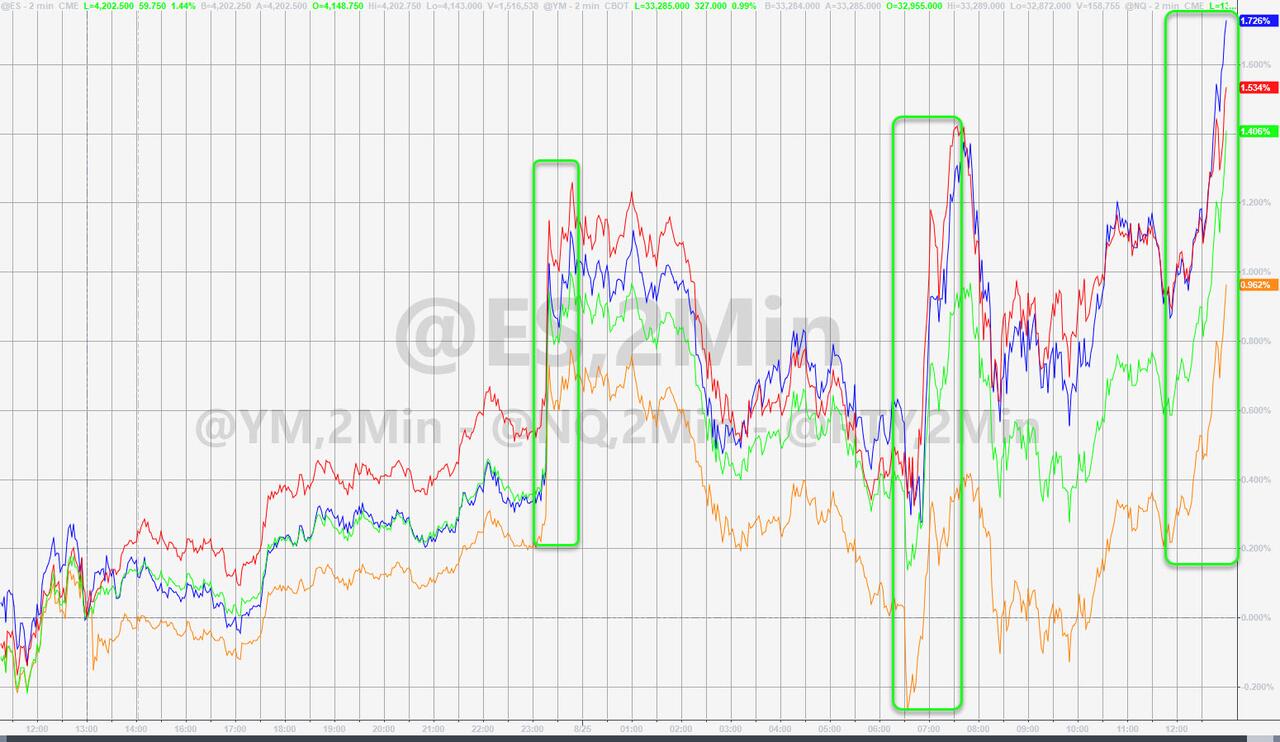

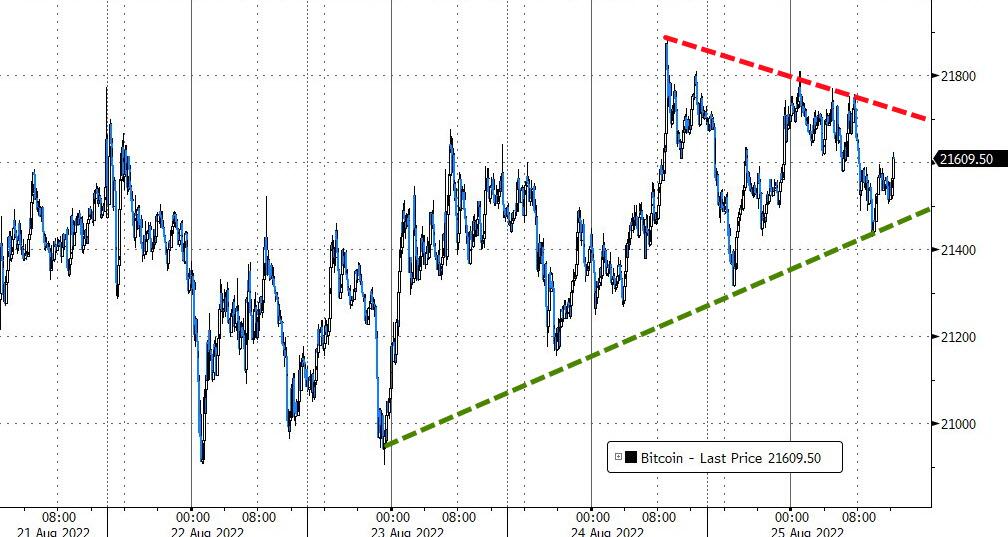

Bitcoin is essentially unchanged but closer to the top-end of circa. USD 500 parameters that reside well within the USD 21k area.

WTI jerked drifts 0.4% higher to around $95 after the WSJ reported that the OPEC president is open to cutting oil production. Most base metals trade in the green; LME copper rises 1.4%, outperforming peers. Spot gold rises roughly $13 to trade near $1,764/oz. Natural gas has surged to fresh highs, intensifying an energy crisis that threatens the euro-area economy and hence the global outlook.

Looking at the day ahead, data releases from the US include the weekly initial jobless claims, the second estimate of Q2 GDP and the Kansas City Fed’s manufacturing activity in index. In Germany there’s also the Ifo Institute’s business climate indicator for August. Otherwise from central banks, we’ll get the account of the ECB’s July meeting.

Market Snapshot

- S&P 500 futures up 0.9% to 4,179.50

- STOXX Europe 600 up 0.7% to 435.05

- MXAP up 1.6% to 160.34

- MXAPJ up 2.0% to 523.18

- Nikkei up 0.6% to 28,479.01

- Topix up 0.5% to 1,976.60

- Hang Seng Index up 3.6% to 19,968.38

- Shanghai Composite up 1.0% to 3,246.25

- Sensex up 0.5% to 59,385.35

- Australia S&P/ASX 200 up 0.7% to 7,048.13

- Kospi up 1.2% to 2,477.26

- German 10Y yield little changed at 1.35%

- Euro up 0.4% to $1.0004

- Gold spot up 0.8% to $1,765.17

- U.S. Dollar Index down 0.45% to 108.18

Top overnight news from Bloomberg

- China stepped up its economic stimulus with a further 1 trillion yuan ($146 billion) of funding largely focused on infrastructure spending, support that likely won’t go far enough to counter the damage from repeated Covid lockdowns and a property market slump

- As the countdown to the Jackson Hole symposium begins, an abrupt shift has taken place in the options market. When trading got underway in Asia on Thursday, investors had to pay more for options which benefit when dollar-yen rises. Just a few hours later, the premium had shifted in favor of options that benefit when the currency pair falls

- European natural gas extended its blistering rally as the worst supply crunch in decades boosts pressure on politicians to do more to rescue industries and households. Benchmark futures jumped as much as 8.1%, after closing at a record on Wednesday

- The good news is that Ukraine’s crucial grain is leaving its ports again. The bad news is that farmland lost to the war and weak local prices are threatening its next wheat harvest

- Climate change is having a “clear impact” on inflation in the euro area, ECB President Christine Lagarde said in an interview

- The current state of the economy and prices doesn’t allow the Bank of Japan’s easing bias to be shifted to neutral, board member Toyoaki Nakamura tells reporters

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks took impetus from the positive handover from Wall St but with gains capped as attention remained on the looming Jackson Hole Symposium. ASX 200 was led higher by commodity stocks after the recent upside in energy and precious metals. Nikkei 225 was underpinned as the government mulled a further loosening of COVID rules and is expected to extend local travel incentives through next month. Shanghai Comp was initially choppy amid the absence of Stock Connect flows after morning trade in Hong Kong was cancelled, although the mood gradually improved with Hong Kong opening for the afternoon session after the storm signal 8 was dropped and following the recent support pledges by China.

Top Asian News

- Chinese Industry Ministry says will accelerate research and development of new types of batteries including sodium-ion batters and hydrogen energy storage batteries; will improve supply capabilities of key resources including lithium, nickel, cobalt and platinum.

- Some of China’s sate-backed financial firms are said to be pushing back on calls to support the Chinese property sector amid the exposure risk on their balance sheets, according to sources cited by Reuters.

- BoK hiked its base rate by 25bps to 2.50%, as expected, with the decision unanimous. BoK said inflation will remain high for the time being and export growth is to slow, while Governor Rhee said strong inflation could last longer than previously seen. Furthermore, Rhee noted that policies will continue to be inflation-focused for a while and said there will be no change in the 25bps rate increase stance for the foreseeable future.

- China Human Resources Ministry official said they will focus on expanding jobs and will promote fiscal, monetary and industrial policies to support job market stabilisation, according to Reuters.

European bourses are essentially unchanged, Euro Stoxx 50 -0.1%, as an initial pronounced foray higher around the cash open that occurred without driver has dissipated since. Fresh drivers have been slim with the German Ifo release sparking a brief extension on initial gains of circa. 50 points in Euro Stoxx 50, for instance. Stateside, futures remain modestly firmer but are similarly off best levels, ES +0.5%, ahead of Jackson Hole beginning today (Powell on Friday).

Top European News

- ECB’s Lagarde says “we can no longer rely exclusively on the projections provided by our models – they have repeatedly had to be revised upwards over these past two years.”.

- Private Jet Shortage Hits English Football’s Pre-Match Prep

- Veolia Must Sell 3 Businesses to Complete Suez Deal, UK Says

- Germany Aug. IFO Business Confidence Index 88.5; Est. 86.8

- London’s Stock Market Misery Grows as Delistings Add to IPO Woes

Commodities

- WTI and Brent October contracts consolidated in the early hours following a session of gains yesterday.

- Spot gold is edging higher in tandem with the decline in the Dollar, with the yellow metal approaching its 50 and 21 DMAs.

- Base metal futures are mostly firmer amid the softer Dollar, with 3M LME copper making its way further above USD 8,000/t.

- Caspian Pipeline Consortium says the SPM-3 inspection has completed, mooring point is fine to work, via Reuters.

- Italian government to update emergency plan for gas next week; will not announce gas rationing plan for now, according to Reuters citing government sources; to include tougher measures in case of further cut or stop of Russian gas flows.

- German Network Regulator VP says is on right track with gas storage but more must be done; will reach 85% storage by October 1st

Fixed Income

- Core benchmarks have derived a pronounced upward bias, despite pronounced pressure alongside initial equity strength and post-Ifo.

- Pressure which has dissipated and given way to modest across the board strength with Bunds eyeing 151.00, Gilts above 111.00 and USTs firmer by 4 ticks.

- Yield dynamics are mixed and are modestly off earlier WTD peaks given the above action, US 7yr due,

Central Banks

- ECB’s Lagarde says “we can no longer rely exclusively on the projections provided by our models – they have repeatedly had to be revised upwards over these past two years.”.

- BoJ Board Member Nakamura says JPY has weakened significantly so far this year, high volatility has had big impact on Japan’s economy; premature to tweak the BoJ’s dovish guidance now, there are pros and cons to soft JPY, therefore will watch carefully but there is not much the BoJ can do as moves are driven by changes in US economy.

- South Korean Presidential Office says closely monitoring forex markets, will take timely measures to stabilise the market.

- Fed’s Bostic (2024 Voter) says he has not decided whether a 50bp or 75bp increase is appropriate in September, at this point it is a coin toss, via WSJ. Key employment and inflation reports are due prior to the meeting, if data remains strong and inflation clearly doesn’t soften then it may make the case for another 75bp move. Too soon to say the inflation surge has peaked, some hopeful signs. Cautioned that expectations the Fed could reverse course in short-order and reduce rates fairly soon is misguided. Upbeat on the economic outlook.

US Event Calendar

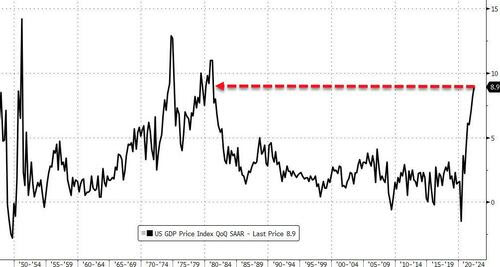

- 08:30: 2Q GDP Annualized QoQ, est. -0.7%, prior -0.9%

- Personal Consumption, est. 1.5%, prior 1.0%

- GDP Price Index, est. 8.7%, prior 8.7%

- PCE Core QoQ, est. 4.4%, prior 4.4%

- 08:30: Aug. Initial Jobless Claims, est. 252,000, prior 250,000

- Continuing Claims, est. 1.44m, prior 1.44m

- 11:00: Aug. Kansas City Fed Manf. Activity, est. 10, prior 13

DB’s Jim Reid concludes the overnight wrap