SEPT 2/GOLD CLOSED UP $7.00 TO $1711.40//SILVER WAS UP 13 CENTS TO $17.99//PLATINUM WAS UP $4.55 TO $837.00/PALLADIUM WAS UP $23.00 TO $2030.00//COVID UPDATS//DR PAUL ALEXANDER//VACCINE INJURIES//VICTOR DASVIS HANSON ON LONG COVID, A MUST READ//RUSSIA HALTS AGAIN NORDSTREAM ONE FOR AN INDEFINITE PERIOD AND NO DOUBT PAYING BACK THE EU FOR THE NEW OIL PRICE CAPS//RUSSIA RESPONS TO EUROPES PRICE CAP BY REFUSING TO SHIP COUNTRIES WHO ENDORSE THE PLAN: MARKETS TUMBLED ON THE NEWS//USA JOB REPORTS ANOTHER PHONEY WITH DETAILS OUTLINED!!//CHINA’S REAL ESTATE MESS OUTLINED AS ONE OF THE BIGGEST DEVELOPER STATES THE COUNTRY IS NOW IN A DEPRESSION//USA FACTORY ORDERS FALTER BADLY/BIDEN’S SHOCKING SPEECH LAST NIGHT OFFERING GRAVE WARNINGS TO THE REPUBLICAN “MAGA SUPPORTERS”: LOOKS LIKE WE ARE HEADING INTO A CIVIL WAR//SWAMP STORIES FOR YOU TONIGHT//

118 C MACQUARIE FUT 49 132 C SG AMERICAS 51 435 H SCOTIA CAPITAL 56 657 C MORGAN STANLEY 9 661 C JP MORGAN 67 306 690 C ABN AMRO 17 709 C BARCLAYS 382 737 C ADVANTAGE 6 14 800 C MAREX SPEC 14 6 905 C ADM 50 11

GOLD: NUMBER OF NOTICES FILED FOR AUGUST CONTRACT:

519 NOTICES FOR 51,900 OZ //1.6143 TONNES

total notices so far: 1810 contracts for 181,000 oz (5.6298 tonnes)

SILVER NOTICES: 101 NOTICES FILED FOR 505,000 OZ/

total number of notices filed so far this month 5702 : for 28,510,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $7.00

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.29 TONNES FROM THE GLD//

INVENTORY RESTS AT 973.08 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $.13

AT THE SLV// ://BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 1.567 MILLION OZ FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 467.140 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GOOD SIZED 670 CONTRACTS TO 137,593. AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE HUGE LOSS IN OI WAS ACCOMPLISHED WITH OUR $0.58 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.58) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC SILVER LONGS AS WE HAD A HUGE GAIN OF 1687 CONTRACTS ON OUR TWO EXCHANGES,; WE HAD MINOR SPECULATOR LIQUIDATION.

WE MUST HAVE HAD: I) SOME//MINOR SPECULATOR SHORT LIQUIDATIONS ////CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 265,000 OZ QUEUE JUMP / // V) STRONG SIZED COMEX OI GAIN/(//MINOR SPEC LIQUIDATION/)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -49

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTACTS for 2 days, total 3442 contracts: 17.210 million oz OR 8.605 MILLION OZ PER DAY. (1721 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 17.210 MILLION OZ

.

LAST 16 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 17.210 MILLION OZ///

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 621 DESPITE OUR $0.58 LOSS IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 1017 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /SOME BANKER ADDITIONS A// MINOR SPEC SHORT LIQUIDATIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 265,000 OZ QUEUE JUMP // .. WE HAD A HUGE SIZED GAIN OF 1687 OI CONTRACTS ON THE TWO EXCHANGES FOR 8.435 MILLION OZ AS..THE SPECS STILL BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 101 NOTICE(S) FILED TODAY FOR 505,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 4837 CONTRACTS TO 464,244 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY:–1020 CONTRACTS.

.

THE FAIR SIZED INCREASE IN COMEX OI CAME DESPITE OUR STRONG FALL IN PRICE OF $26.70//COMEX GOLD TRADING/THURSDAY / WE MUST HAVE HAD MINOR SPECULATOR SHORT SHORT COVERINGS ACCOMPANYING OUR SMALL SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND SOME/MINOR SPECULATOR SHORT COVERINGS//CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR AUGUST AT 8.401 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S GIGANTIC JUMP OF 39,400 OZ //NEW STANDING 9.7667 TONNES

YET ALL OF..THIS HAPPENED DESPITE OUR FALL IN PRICE OF $26.70 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 8572 OI CONTRACTS 26.66 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 3735 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 464,244

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8572 CONTRACTS WITH 4837 CONTRACTS INCREASED AT THE COMEX AND 3735 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 8572 CONTRACTS OR 26.66 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3735) ACCOMPANYING THE GOOD SIZED GAIN IN COMEX OI (4837): TOTAL GAIN IN THE TWO EXCHANGES 8572 CONTRACTS. WE NO DOUBT HAD 1) MINOR SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 99.272 TONNES FOLLOWED BY TODAY’S QUEUE. JUMP OF 39,400 oz. 3) ZERO LONG LIQUIDATION//// //.,4) GOOD SIZED COMEX OPEN INTEREST GAIN 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST :

6635 CONTRACTS OR 663,500 OZ OR 20.63 TONNES 2 TRADING DAY(S) AND THUS AVERAGING: 3318 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAY(S) IN TONNES: 20.63 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 20.63/3550 x 100% TONNES 0.59% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 20.63 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT., FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 621 CONTRACT OI TO 137,593 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1017 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 1017 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1017 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 621 CONTRACTS AND ADD TO THE 1017 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 1638 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 8.190 MILLION OZ

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED UP 1.50 PTS OR 0.05% //Hang Sang CLOSED DOWN 145.22 OR 0.74% /The Nikkei closed DOWN 10.63 OR .04%. //Australia’s all ordinaires CLOSED DOWN 0.33% /Chinese yuan (ONSHORE) closed DOWN AT 6.9082//OFFSHORE CHINESE YUAN DOWN 6.9153// /Oil DOWN TO 88.08 dollars per barrel for WTI and BRENT AT 93.97 / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GOOD SIZED 4837 CONTRACTS TO 464,244 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR FALL OF $26.70 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (3735 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF AUGUST.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3735 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :3735 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3735 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED SIZED TOTAL OF 8572 CONTRACTS IN THAT 3735 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI GAIN OF 4837 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR STRONG FALL IN PRICE OF GOLD $ 26.70. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING SEPT (10.992),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 10.992 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $26.70) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A STRONG SIZED TOTAL GAIN ON OUR TWO EXCHANGES // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS////// WE HAVE REGISTERED A STRONG SIZED GAIN OF 26.66 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR AUGUST (10.992 TONNES)…

WE HAD -1020 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 8572 CONTRACTS OR 857200 OZ OR 26.66 TONNES

Estimated gold volume 197,122/// poor/

final gold volumes/yesterday 190,092/ poor

INITIAL STANDINGS FOR SEPT ’22 COMEX GOLD //SEPT 2

Total monthly oz gold served (contracts) so far this month

1810 notices 181,000 OZ 5.6298 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

1 customer withdrawals:

i) Out of Brinks 2788.099 oz

total: 2788.099 oz

total in tonnes: 0.0867 tonnes

Adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPT.

For the front month of SEPT we have an oi of 2243 contracts having LOST493 contracts .

We had 887 notices filed yesterday so we gained a whopping 394 contracts or an additional 39,400 oz

will stand for gold in this very non active delivery month of September.

October GAINED 2042 contracts UP to 41,231

November GAINED 6 contracts to stand at 6

December gained 2667 contracts UP to 380,131.

We had 519 notice(s) filed today for 51900 oz FOR THE SEPT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 519 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 306 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2022. contract month,

we take the total number of notices filed so far for the month (1810) x 100 oz , to which we add the difference between the open interest for the front month of (SEPT 2243 CONTRACTS ) minus the number of notices served upon today 519 x 100 oz per contract equals 353,400 OZ OR 10.992 TONNES the number of TONNES standing in this NON active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month:

No of notices filed so far 1810) x 100 oz+ (2243) OI for the front month minus the number of notices served upon today (519} x 100 oz} which equals 353,400 oz standing OR 10.992 TONNES in this NON active delivery month of SEPTEMBER.

TOTAL COMEX GOLD STANDING: 10.992 TONNES (A GREAT STANDING FOR A SEPT ( NON ACTIVE) DELIVERY MONTH)

VERY UNUSUAL THAT ON DAY 2 AND DAY 3 WE HAD A HUGE QUEUE JUMP. (NORMALLY AN EFP JUMP//REDUCTION IN GOLD STANDING ON BOTH DAYS)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 5702 x 5,000 oz = 28,510,000 oz

to which we add the difference between the open interest for the front month of SEPT(425) and the number of notices served upon today 101 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST./2022 contract month: 5,702 (notices served so far) x 5000 oz + OI for front month of SEPT (425) – number of notices served upon today (101) x 5000 oz of silver standing for the SEPT contract month equates 30,130,000 oz. .

We have an inventory of 50 million oz of registered silver at the comex so Sept delivery of 30.13 represents 60.26% of that category of silver.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

AUGUST 31.WITH GOLD DOWN $10.20:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.24 TONNES FROM THE GLD////INVENTORY RESTS AT 973.37 TONNES

AUGUST 30.WITH GOLD DOWN $12.00:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 980.61 TONNES

AUGUST 29/WITH GOLD DOWN $.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD/////INVENTORY RESTS AT 982.64 TONNES

AUGUST 26/WITH GOLD DOWN $26.60; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 25/WITH GOLD UP $9.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 18/WITH GOLD DOWN $5.25: GIGANTIC CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.78 TONNES FROM THE GLD////INVENTORY RESTS AT 985.83 TONNES

AUGUST 17/WITH GOLD DOWN $12.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 992.20 TONNES

AUGUST 16/WITH GOLD DOWN $7.85: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 993.94 TONNES

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

AUGUST 10//WITH GOLD UP $2.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES

AUGUST 9/WITH GOLD UP $6.70: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES.

AUGUST 8/WITH GOLD UP $13.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FORM THE GLD//INVENTORY RESTS AT 999.16 TONNES

AUGUST 5/WITH GOLD DOWN $14.25: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .33 TONNES FROM THE GLD////INVENTORY RESTS AT 1000.32 TONNES

AUGUST 4 WITH GOLD UP $29.00 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES FROM THE GLD///INVENTORY REST AT 1000.65 TONNES

AUGUST 2/WITH GOLD UP $3.70; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD//INVENTORY RESTS AT 1002.97 TONNES//

AUGUST 1/WITH GOLD UP $5.75: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1005.87 TONNES

GLD INVENTORY: 973.08 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

AUGUST 31/WITH SILVER DOWN 36 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 3.087 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 465.573 MILLION OZ//

AUGUST 30/WITH SILVER DOWN 34 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 1.478 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 470.135 MILLION OZ//

AUGUST 29/WITH SILVER DOWN 7 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY A THE SLV: A WITHDRAWAL OF 2.765 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 470.135 MILLION OZ//

AUGUST 26/WITH SILVER DOWN 39 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 25/WITH SILVER UP 21 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

AUGUST 18/WITH SILVER DOWN 27 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 369,000 OZ INTO THE SLV////INVENTORY RESTS AT 485.482 MILLION OZ//

AUGUST 17/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.106 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.113 MILLION OZ//

AUGUST 16/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 486.219 MILLION OZ/

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 10/WITH SILVER UP 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 9/WITH SILVER DOWN 25 CENTS TODAY: TWO CHANGES IN SILVER INVENTORY AT THE SLV: FIRST: A DEPOSIT OF 461,000 OZ INTO THE SLV AND THEN A WITHDRAWAL OF 1.014 MILLION OZ..//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 8/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 5/WITH SILVER DOWN 28 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 922,000 OZ FROM THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 4 WITH SILVER UP 21 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 527,000 OZ FROM THE SLV////INVENTORY RESTS AT 486.634 MILLION OZ

AUGUST 2/WITH SILVER DOWN 21 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.504 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.161 MILLION OZ//

AUGUST 1/WITH SILVER UP 17 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE GLD: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 483.657 MILLION OZ//

CLOSING INVENTORY 467.140 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Millions Of Americans Face Eviction In Coming Months

The economy is fine, so we’re told. There is no recession, so we’re told. The Federal Reserve has everything under control, so we’re told. Meanwhile, 3.8 million Americans say they could face eviction in the next two months.

It doesn’t sound like everything is fine.

The median rent in the US eclipsed $2,000 per month in June for the first time ever. It’s another symptom of rampant inflation burning through the US economy.

While the CPI cooled slightly in July, shelter costs rose another 0.5% month-on-month. On a yearly basis, shelter costs have spiked by 5.7%, according to government numbers. And the CPI drastically understates the cost of housing. Actual rents have increased more than 15% in the last 12 months, according to data compiled by Zillow.

With rents skyrocketing, households representing 8.5 million people are behind on their rent, according to the Census Bureau. Of those, 3.8 million say they are somewhat or very likely to be evicted within the next two months.

According to Yahoo Finance, “The combination of soaring inflation, the end of most eviction moratoriums and rental assistance payments and an extremely low vacancy rate has pushed rents up — and many renters out.”

Nearly half of all renters experienced rent hikes in the past 12 months, according to Census Bureau data. Eleven percent have seen rent increases of over $250 per month.

To make ends meet, people are turning to credit cards and loans, raiding savings, selling assets, and dipping into retirement funds. According to the Census Bureau, 57% of renters said they were forced to resort to one of these desperate measures to keep up with their rent.

This dovetails with the skyrocketing levels of household debt. Americans added another $40.1 billion to their debt load in June alone. That represented a 10.5% year-on-year increase. Credit card balances increased by $46 billion in the second quarter of this year. Over the last year, credit card debt has exploded by 13%, the biggest increase in over 20 years.

According to Yahoo Finance, the Fed’s efforts to stem inflation are adding to the pain. With mortgage rates rising, renters who were hoping to buy homes have been priced out of the market.

Eviction levels are already rising. According to Princeton University’s Eviction Lab, evictions were 52% above average in Tampa, 90% above average in Houston, and 94% above average in Minneapolis-St. Paul this month.

This is yet another sign that the economy isn’t as strong as the powers that be would like you to believe.

Despite the fact that private sector economic activity has dropped to the lowest levels since early in the COVID lockdowns, the housing market is tanking, and the economy has charted two straight months of negative GDP growth, the mainstream keeps pointing to the strong labor market. But if the labor market is so strong, why are so many people facing eviction?

Peter Schiff has said the labor market isn’t nearly as robust as people think. There may be plenty of jobs, but real wages are falling. “I don’t care about how many jobs are being created. What I’m looking at is: are the workers getting pay raises or are they suffering pay cuts? Because in a strong labor market, you get a raise,” Schiff said.

It’s clear; a strong labor market or not, a lot of Americans are struggling. And it appears a large number may soon find themselves on the streets.

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

GOLD/SILVER

END

3.Chris Powell of GATA provides to us very important physical commentaries

A very important commentary: Russia changes its strategy. It will no longer accumulate any euros or dollars but purchase friendly foreign exchange. This is done to slow the ruble’s rise. The goal to stop uSA hegemony on the usa of the dollar.

(Bloomberg)//GATA

Russia considers big purchases of ‘friendly’ foreign exchange to slow ruble’s rise

Submitted by admin on Thu, 2022-09-01 11:27Section: Daily Dispatches

Isn’t the “friendliest” currency that old yellow metal?

From Bloomberg News

Thursday, September 1, 2022

Russia is considering a plan to buy as much as $70 billion in yuan and other “friendly” currencies this year to slow the ruble’s surge, before shifting to a longer-term strategy of selling its holdings of the Chinese currency to fund investment.

The plan won initial support at a special “strategic” planning meeting of top government and central bank officials including Governor Elvira Nabiullina on Aug. 30, according to people familiar with the deliberations who spoke on condition of anonymity to discuss matters that aren’t public.

The proposal represents a shift from more than a decade of economic policy built around accumulating savings in dollars and euros as the Kremlin overhauls its strategy amid sweeping sanctions imposed by the United States and its allies over Vladimir Putin’s invasion of Ukraine. …

Russian ‘De-Dollarization’ Escalates: Begins “Strategic” Plan To Buy Billions In “Friendly” Currencies

THURSDAY, SEP 01, 2022 – 09:40 PM

Ever since March 2018, when Moscow dumped practically all of its US Treasury holdings, Russia has been at the forefront of a global process of ‘de-dollarization’. Practically speaking, reducing the nation’s dependence on the global hegemon’s control of payments and thus everything else.

China joined the fight more recently but has been increasing its gold reserves while reducing its US Treasury reserves quite consistently for over two years.

Of course, all of that ‘normal’ process has been thrown into chaos since Putin invaded Ukraine with sanctions, bans, and virtue-signaling by Washington curb-stomping the freedoms of many so-called ‘friendly’ nations to Russia (and some un-friendly who simply prefer to feed/heat/cool their citizenry than fall in line).

Since the invasion, the ‘Ruble is rubble’ narrative has been crushed after initial weakness in the Russian currency reversed to massive strength amid soaring energy prices (and energy-for-Rubles agreements)…

All of which brings us to a stunning new report from Bloomberg that Russia is considering a plan to buy as much as $70 billion in yuan and other “friendly” currencies this year to slow the ruble’s surge.

“In the new situation, accumulating liquid foreign exchange reserves for future crises is extremely difficult and not expedient,” a presentation on the proposal prepared for the meeting said.

For years, the Kremlin contained spending and saved hundreds of billions in dollars, euros and other foreign currencies as a cushion to insulate the economy from the ups and downs of oil prices.

“The frozen $300 billion were of no help to Russia; on the contrary, they became a vulnerability and a symbol of missed opportunities,” the presentation said, in a rare official admission of the true impact of sanctions.

Bloomberg saw a copy of the document, which isn’t public, and the people familiar with the meeting confirmed its authenticity. The government and central bank didn’t immediately respond to requests for comment on the plan.

According to people familiar with the deliberations who spoke on condition of anonymity to discuss matters that aren’t public, the plan won initial support at a special “strategic” planning meeting of top government and central bank officials including Governor Elvira Nabiullina on Aug. 30.

With earnings from exports of oil and gas flooding in and driving the current account surplus to a record this year and pushing the ruble higher, the proposal calls for spending 4.4 trillion rubles ($70 billion) to buy the currencies of “friendly” countries, mostly yuan…which it has been gathering for a couple of years…

Alexander Isakov, Bloomberg’s Russia economist noted that “the purchases will help Russia cap unprecedented real-exchange-rate strength, which is hurting exporters and the budget’s commodity revenues. For neutral countries, these purchases will bring some support for local currencies, help fix their current account issues and help fund commodity imports.”

So, as CFR senior fellow Brad Setser notes, the Russian Central Bank could become the first big central bank to hold the bulk of its reserves in emerging market currencies.

Currencies of ‘friendly’ currencies like offshore Yuan, Turkish Lira, and India’s Rupee all caught a bid on the report earlier in the day.

As Ruchir Sharma recently noted, reflecting on the false security many are getting from seeing a strong dollar, the impact of US sanctions on Russia is demonstrating how much influence the US wields over a dollar-driven world, inspiring many countries to speed up their search for options. It’s possible that the next step is not towards a single reserve currency, but to currency blocs.

Setser adds that “the real lesson of Russia isn’t about the dollar (or euro). It is that excess reserve holdings of all G-7 currencies may not be as strategically valuable as thought.“

As Banque de France noted in a July article, recent geopolitical tensions have put the hegemonic role of the dollar, and its potential demise, back into the spotlight. Looking at a new long run measure of global currency competition over two centuries, no global currency leader has been able to sustain such a large lead over its competitors for such a prolonged period.

Remember, nothing lasts forever…

Since the 15th century, the last five global empires have issued the world’s reserve currency – the one most often used by other countries – for 94 years on average. The dollar has held reserve status for more than 100 years, so its reign is already older than most.

end

4. OTHER GOLD/SILVER COMMENTARIES

-END-

.

end

5.OTHER COMMODITIES:

COMMODITIES IN GENERAL/COAL

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.9082

OFFSHORE YUAN: 6.9153

HANG SENG CLOSED DOWN 145.22 PTS OR 0.74%

2. Nikkei closed DOWN 10.63 OR 0.64%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 109.30/Euro RISES TO 0.9994

3b Japan 10 YR bond yield: RISES TO. +.235/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 140.41/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.585%/Italian 10 Yr bond yield RISES to 3.95% /SPAIN 10 YR BOND YIELD RISES TO 2.78%…

3i Greek 10 year bond yield RISES TO 4.23//

3j Gold at $1706.25 silver at: 17.95 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 5/100 roubles/dollar; ROUBLE AT 60.36//

3m oil into the 88 dollar handle for WTI and 93 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 140.41DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 9827–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9823well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.252 DOWN 1 BASIS PTS

USA 30 YR BOND YIELD: 3.370 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,22

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

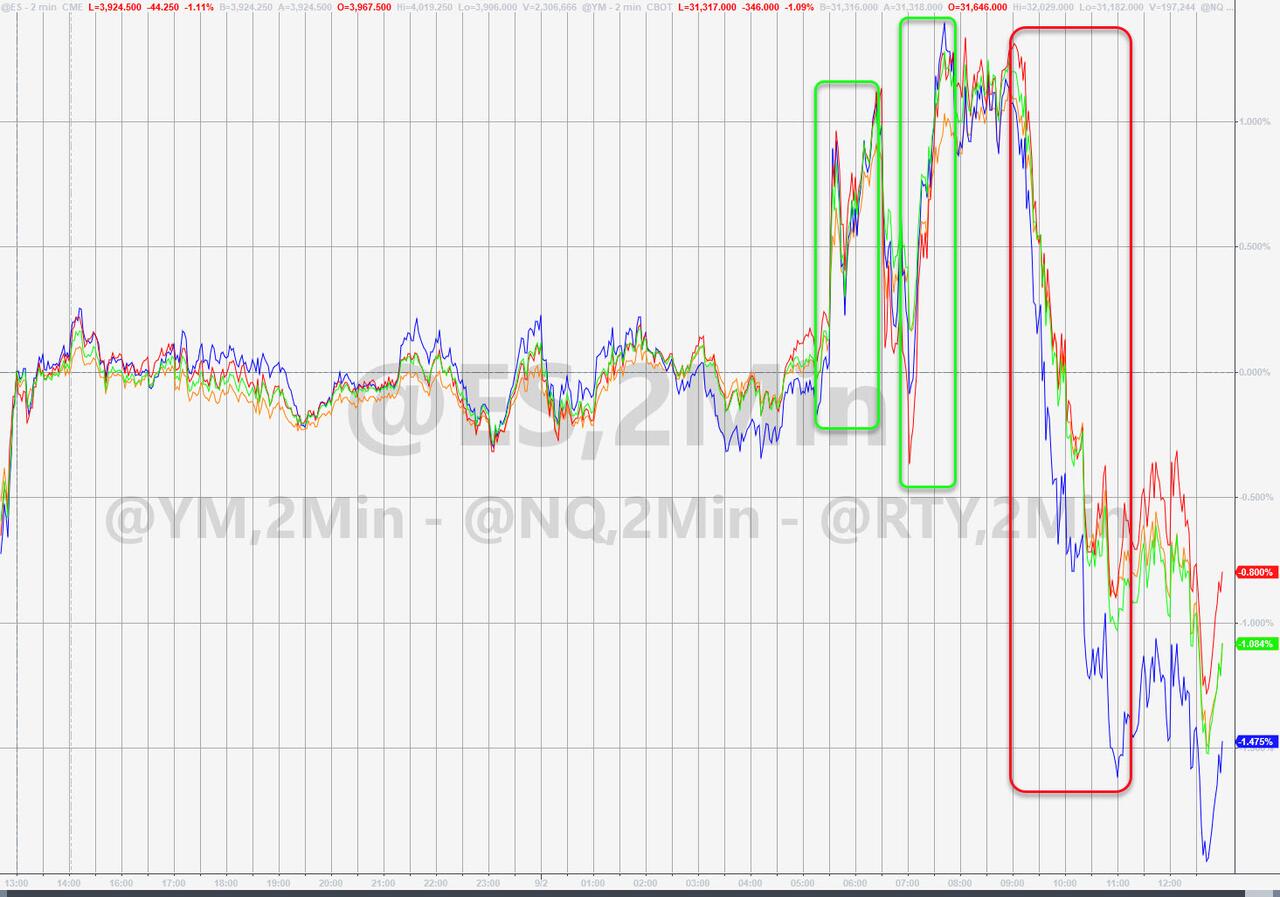

Futures Flat In Muted End To Turbulent Week With All Eyes On Payrolls

FRIDAY, SEP 02, 2022 – 07:52 AM

US futures dropped on Friday, ending a third straight week of declines, as investors eyed a key jobs report that will be pivotal for this month’s Fed rate hike decision. S&P futures fell 0.2% at 730 a.m. ET, with the underlying cash index down 2.2% this week. Nasdaq 100 futures fell 0.3%, with the tech-heavy index down 2.6% in the previous four days. The dollar index slipped from a record high and the euro strengthened. 10Y yield traded slightly lower, at 3.25%, following yesterday’s spike.

In pre-market trading, Lululemon jumped 10% after raising its full-year outlook. Meanwhile, Bed Bath & Beyond fell as much as 6%, putting the home-goods retailer on track for a weekly loss following its survival plan earlier in the week. Analysts raise PTs on the stock, though some flag higher inventory levels as a note of bearishness. Here are other notable movers:

Procept BioRobotics (PRCT US) initiated at overweight by Wells Fargo, highlighting the potential of the company’s AquaBeam Robotic System, a therapy for prostate gland enlargement

JPMorgan cuts its ratings on Dow and LyondellBasell (LYB US) to neutral from overweight, saying the petrochemicals companies are “probably not the best places to put new money to work.”

Shares in Addentax (ATXG US), a Chinese garment-maker, drop as much as 40% in US premarket trading, set to extend yesterday’s 95% plunge into a second day.

US semiconductor- related stocks could be active on Friday after Broadcom gave a robust sales forecast for the current quarter, calming worries that spending on infrastructure is slowing

The outlook for stocks has soured since mid-August after traders ramped up bets that the Fed will continue its aggressive monetary tightening, hurting the economy in the process. The S&P 500 has erased $2 trillion in market capitalization in the past five days, and has given up half of its gains made in the summer rally. Meanwhile, tech stocks have succumbed to rising rates, which are a headwind to the expensive growth sector.

“We don’t have a lot of reasons to be bullish in this type of environment for the next couple of weeks and months,” Meera Pandit, global market strategist at JPMorgan Asset Management, said on Bloomberg Television. “Yet when we think about the longer term perspective and the longer term investor, these are the types of level that can be fruitful in the long run.”

US stocks had outflows of $6.1 billion in the week to Aug. 31 – the biggest exodus in 10 weeks – according to a Bank of America’s Michael Hartnett, adding that investors expect “fast inflation shock, slow recession shock” as nominal growth continues to be boosted by surging consumer prices, fiscal stimulus, large household savings and the impact of the war in Ukraine.

Next up on investor minds is the August jobs report in under an hour, which is expected to show healthy payrolls growth following a stronger-than-expected US manufacturing report. This is how Goldman traders framed what to expect (full preview here): “we are still in a bad is good and vice versa set up for US stocks as Fed has made it clear that they want to see some froth exit the labor market in tandem with cooling inflation: i) Strong print here will clearly make 75bps much more likely on 9/21; ii) Inline print of 300k(ish) will keep pressure on this tape…anything close to last month’s shocking print of 528k would lead to real risk unwind into the wknd (I think at least a 200bp sell off). iii) Sweet spot for stocks tomorrow is a 0 – 100k headline reading…should get a 100+bp rally for S&P in this scenario after this recent drawdown. If we happen to get a negative number an even sharper rally”, and the pivot will be right back on the Q1 calendar.

“The risk of having another additional 75-basis-points hike is high and also to have a big rally on the real rates” depending on the outcome of the jobs report, said Claudia Panseri, a global equity strategist at UBS Global Wealth Management. “Volatility in the equity market will remain quite high until the picture on inflation becomes more clear than it is right now,” she told Bloomberg Television.

In Europe, the Euro 50 rose 0.9%, with Germany’s DAX outperforming peers, adding 1.5%, IBEX lags, rising 0.2%. Autos, financial services and energy are the strongest-performing sectors. Here are the biggest Europen movers:

Nokia shares are up as much as 1.4% on Friday, adding to a weekly gain and outperforming the wider markets decline as the communications company will join the Euro Stoxx 50 benchmark

Ashmore shares gain as much as 5.5%, reversing a small decline at the open, with Panmure Gordon upgrading the emerging markets fund manager to buy from hold following its FY results

Smith & Nephew rises as much as 4.9%, extending a weekly gain. RBC says investors are viewing stock’s “historically low valuation” against orthopedic peers as a “buying opportunity.”

Segro and Tritax Big Box gain 2.5% and 2.2%, respectively, after Shore Capital upgrades the REITs, saying downside risks for Segro are “fairly priced,” and the risk- reward balance for Tritax is more even

UK homebuilders fall and are among the worst performers in the Stoxx 600 after HSBC cut its ratings on seven stocks, saying the UK is on the “cusp of a housing downturn”

Sectra shares are down as much as 6.6% after the Swedish medical technology company presented its latest earnings, which included a drop in operating profit

Alliance Pharma falls as much 11%, most since July, as the UK’s competition watchdog seeks to disqualify seven of the firm’s directors, including CEO Peter Butterfield

Proximus falls to fresh record low, declining as much as 4.3% after Morgan Stanley resumes at underweight in note citing structural market headwinds and an unsupportive valuation

Kofola CeskoSlovensko shares drop 2.5% after rising costs prompted the Czech producer of soft beverages to reduce its dividend proposal and rein in guidance

Compleo Charging Solutions falls as much as 4% after Berenberg downgrades to hold and lowers its price target by 80%, citing resignation of the company’s co-founder Checrallah Kachouh

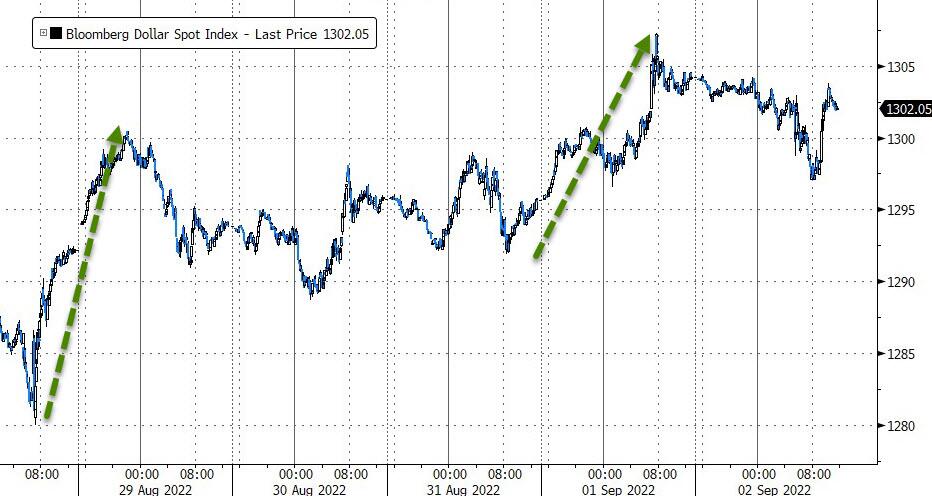

Earlier in the session, Asian stocks fell, on course for their worst week in more than two months, as the dollar hit a new high amid worries about the Federal Reserve’s aggressive rate-hike path and as lockdowns continued in China. The MSCI Asia Pacific Index declined as much as 0.7%, set for a weekly loss of nearly 4%. TSMC and other tech stocks contributed the most to the benchmark’s drop as Treasury yields climbed, sending the Bloomberg Dollar Spot Index to a record high. Equity gauges in Hong Kong led declines in the region, dragged by the banking and tech sectors. Meanwhile, shares in Japan fell as the yen slipped to a 24-year-low against the dollar. Fresh lockdowns in China are also weighing on sentiment, putting the Asian stock benchmark on track for its third-straight weekly decline. The sell-off reflects broad concerns of an economic slowdown amid weaker manufacturing data in the region’s major tech exporters.

“Dollar momentum sees no sign of breaking,” Saxo Capital Markets strategists including Redmond Wong wrote in a note. “Fresh Covid lockdowns in China, in particular, the full lockdown of Chengdu and extended restriction in Shenzhen, have caused some demand concerns.” Investors will keep a keen eye on the US August jobs report due later Friday to gauge the Fed’s next move in its September meeting. While weak sentiment has kept Asian shares hovering near their two-year lows, hedge-fund giant Man Group said Asian stocks are set to outshine peers next year. The investment firm is betting on defensive stocks in India and Southeast Asia, Andrew Swan, Man GLG’s head of Asia ex-Japan equities, said in an interview

Japanese stocks fell as investors awaited key US employment figures and assessed the yen’s decline to a 24-year low against the dollar. The Topix Index dropped 0.3% to 1,930.17 as of the market close in Tokyo, while the Nikkei 225 was virtually unchanged at 27,650.84. Sony Group contributed the most to the Topix’s decline, decreasing 1.1%. Out of 2,169 stocks in the index, 738 rose and 1,307 fell, while 124 were unchanged. “The US jobs report won’t be very positive no matter what’s out,” said Tatsushi Maeno, a senior strategist at Okasan Asset Management. “If it’s strong, the FOMC will lean toward a 0.75% rate hike and on the other hand, if it’s weak, there could be talk of a recession.”

India’s benchmark equities index closed slightly higher, after swinging between gains and losses several times throughout the session, as investors tried to gauge the impact of the US Federal Reserve’s hawkish stance in a week marked by volatility. The S&P BSE Sensex rose 0.1% to 58,803.33 in Mumbai, but ended lower for a second consecutive week. The NSE Nifty 50 Index was little change on Friday. Housing Development Finance Corp and HDFC Bank provided the biggest support to the Sensex, which saw 19 of its 30 member stocks ending lower. Thirteen of the 19 sector indexes compiled by BSE Ltd. declined, led by a measure of oil and gas companies. “The effect of Jackson Hole is still revolving across financial markets, with a soaring dollar and falling equities as the main themes,” Prashanth Tapse, an analyst at Mehta Securities, wrote in a note.

In FX, the greenback fell against all of its Group-of-10 peers except the yen. The euro rose a fourth day in five against the greenback, to edge above parity. The pound languished near the lowest since March 2020 versus the dollar. Investors awaited the results of a vote to choose the country’s next prime minister on Monday, with expected winner Liz Truss aiming to cut taxes and increase borrowing. The Norwegian krone outperformed, and rebounded from a six-week low versus the greenback, amid a recovery in oil prices before an OPEC+ meeting on supply at which Saudi Arabia could push for output cuts. The yen weakened past 140 per dollar after a slight rally in Asian trading faded.

In rates, treasuries were little changed while European bonds slipped. The 10-year Treasury yield held steady near 3.26%; while gilts 10-year yield is up 2.6bps around 2.90% and bunds 10-year yield is up 2bps to 1.58%.

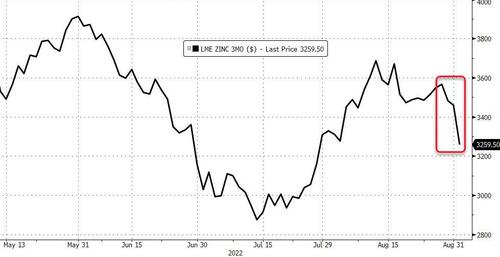

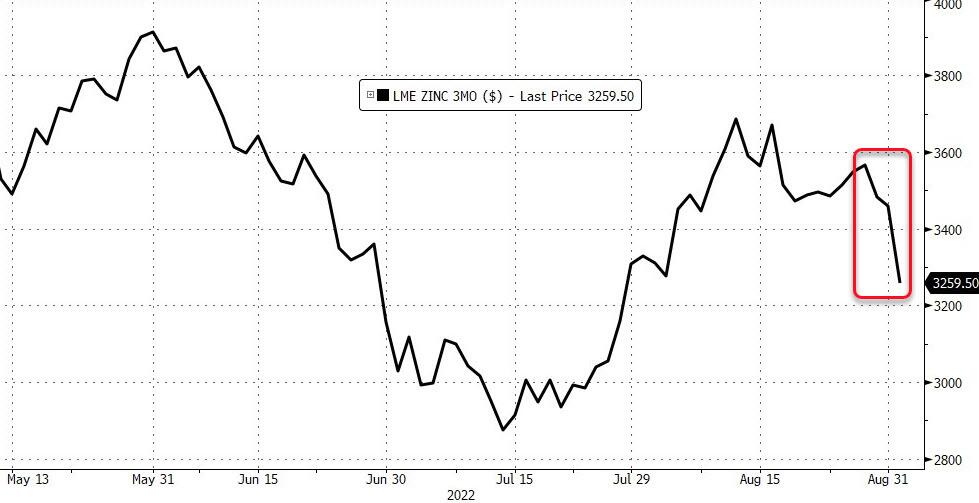

In commodities, WTI crude futures rebound 3% to around $89, within Thursday’s range; oil pared gains after news that the Group of Seven most industrialized countries is poised to agree to introduce a price cap for global purchases of Russian oil, while Russia looks set to resume gas supplies through its key pipeline. Gold rose $6 to around $1,704. Meanwhile, zinc headed for its biggest weekly loss in over a decade on concern Chinese demand will be hamstrung by new virus restrictions.

Bitcoin has reclaimed the USD 20k mark but the upward move is yet to gain any real traction amid the broader contained price action.

Looking to the day ahead now, the main highlight will be the US jobs report for August. Otherwise on the data side, there’s US factory orders for July and Euro Area PPI for July.

Market Snapshot

S&P 500 futures little changed at 3,969.25

Gold spot up 0.4% to $1,704.52

MXAP down 0.5% to 154.28

MXAPJ down 0.5% to 506.44

Nikkei little changed at 27,650.84

Topix down 0.3% to 1,930.17

Hang Seng Index down 0.7% to 19,452.09

Shanghai Composite little changed at 3,186.48

Sensex up 0.4% to 59,025.66

Australia S&P/ASX 200 down 0.2% to 6,828.71

Kospi down 0.3% to 2,409.41

STOXX Europe 600 up 0.7% to 410.47

German 10Y yield little changed at 1.58%

Euro up 0.3% to $0.9980

U.S. Dollar Index down 0.25% to 109.42

Top Overnight News from Bloomberg

Under pressure from central bankers determined to quash inflation even at the cost of a recession, global bonds slumped into their first bear market in a generation. The Bloomberg Global Aggregate Total Return Index of government and investment-grade corporate bonds has fallen more than 20% from its 2021 peak, the biggest drawdown since its inception in 1990

The ECB remains behind the curve on tackling record euro- zone inflation and will have to act more forcefully than previously envisaged to wrest control of prices, according to a survey of economists

Consumers’ expectations for inflation in three years rose to 3% in July from 2.8% in June, European Central Bank says in statement summarizing the results of its monthly survey.

Russia looks set to resume gas supplies through its key pipeline to Europe, a relief for markets even as fears persist about more halts this winter. Grid data indicate that flows will resume on Saturday at 20% of capacity as planned

German exports and imports both fell in July as surging prices and the war in Ukraine threaten to send Europe’s largest economy into a recession. The trade surplus shrank to 5.4 billion euros ($5.4 billion) from 6.2 billion euros in June, as exports dropped by 2.1% and imports by 1.5%

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were indecisive with price action relatively rangebound after the mixed lead from the US and with the region lacking firm commitment as participants await the upcoming US NFP jobs data. ASX 200 was lacklustre as earnings releases quietened and with strength in financials offset by losses across the commodity-related sectors. Nikkei 225 traded subdued amid underperformance in large industrials although losses in the index were stemmed by retailers after several reported strong August sales. Hang Seng and Shanghai Comp were mixed as Hong Kong underperformed amid notable losses in developers and with the mainland choppy but ultimately kept afloat after the PBoC recently cut rates on its Standing Lending Facility by 10bps from August 15th and after several officials pledged measures.

Top Asian News

PBoC official Ruan said monetary policy is to further improve cross-cyclical adjustments and maintain stable and moderate credit development, while they will keep liquidity reasonably ample. PBoC will also better coordinate structural and aggregate policy tools but will avoid flood-like stimulus and keep prices stable. Furthermore, the PBoC said China has not taken excessive monetary policy stimulus since the pandemic, leaving room for subsequent policy adjustments and that balanced consumer prices also create favourable conditions for monetary policy adjustments, according to Reuters.

PBoC adviser Wang said banks need to increase financial support for infrastructure and that infrastructure is restricted by local government debt levels, while Wang added that they need to ensure property companies’ financing needs are met, according to Reuters.

China’s securities regulator official said they will promote new legislation for overseas listings and will implement the China-US audit agreement, as well as continue strengthening communication with foreign institutional investors, according to Reuters.

China’s banking regulator official said they will steadily resolve the risks faced by small and medium-sized financial institutions, while they will improve monitoring and disposal of debt risks of large companies, according to Reuters.

Japanese Finance Minister Suzuki said it is important for currencies to move stably reflecting economic fundamentals, while he noted that recent FX moves are big and they will take appropriate action on FX if necessary. Suzuki also stated that they are watching FX with a sense of urgency and will brief the media after the G7 finance ministers meeting tonight.

European bourses are firmer across the board as hawkish yield action in the EZ has eased from yesterday’s recent peaks, Euro Stoxx 50 +0.8%. Stateside, futures are contained and flat with all focus on the NFP report. Alphabet’s Google (GOOG) is planning to accept the use of third-party payment services on its smartphone app in national such as Japan and India but not the US, according to the Nikkei

Top European News

British Chambers of Commerce said the UK is already in the midst of a recession and it expects the UK economy to decline for two more periods following the contraction in Q2, while it also sees inflation to reach 14% later this year

EU warned UK Foreign Secretary Truss against triggering Article 16 and said they will refuse to engage in serious talks on reforms to the post-Brexit deal unless she takes the “loaded gun” of unilateral legislation off the table

German Economy Gets Another Growth Warning as Trade Volumes Drop

Russian Gas Link Set to Restart as Traders Weigh Further Halts

ECB Says Consumers Now See Inflation in Three Years at 3%

A Hot Jobs Report Could Send Bitcoin to $15,000, Hedge Fund Says

Citi Favors Bets on 75Bps Hikes at Each of Next Two ECB Meetings

FX

DXY’s overnight pullback has picked up pace in early European hours.

The EUR stands as the best performer alongside reports that Nord Stream 1 flows are expected to resume on Saturday.

Non-US dollars are all modestly firmer to varying degrees, whilst JPY fails to benefit from the dollar weakness.

Yuan shrugged off another notably firmer-than-expected CNY fixing overnight.

Fixed Income

Comparably contained session overall thus far though Bunds are holding at the lower end of a 85 tick range in limited newsflow pre-NFP.

Currently, the Bund low is circa. 10 ticks above 147.00, with yesterday’s 146.78 trough in focus and then 145.97/87 thereafter.

Gilts and USTs are very similar thus far in that both benchmarks are essentially unchanged.

Commodities

WTI Oct and Brent Nov futures are firmer on the day amid a softer Dollar and narrowing prospects of an imminent Iranian Nuclear deal.

Spot gold edges higher as the Dollar remains weak, with the yellow metal back on a 1,700/oz+.

Base metals are mixed LME copper softer around the USD 7,500/t.

US Event Calendar

08:30: Aug. Change in Nonfarm Payrolls, est. 298,000, prior 528,000

Change in Private Payrolls, est. 300,000, prior 471,000

Change in Manufact. Payrolls, est. 15,000, prior 30,000

Unemployment Rate, est. 3.5%, prior 3.5%

Labor Force Participation Rate, est. 62.2%, prior 62.1%

Underemployment Rate, prior 6.7%

Average Hourly Earnings YoY, est. 5.3%, prior 5.2%

Average Hourly Earnings MoM, est. 0.4%, prior 0.5%

Average Weekly Hours All Emplo, est. 34.6, prior 34.6

10:00: July Durable Goods Orders, est. 0%, prior 0%; July -Less Transportation, est. 0.3%, prior 0.3%

10:00: July Factory Orders, est. 0.2%, prior 2.0%

10:00: July Cap Goods Orders Nondef Ex Air, prior 0.4%

10:00: July Factory Orders Ex Trans, est. 0.4%, prior 1.4%

DB’s Jim Reid concludes the overnight wrap

If I’m not here on Monday it’s not impossible that I’ve been eaten by a snake or a small crocodile, or poisoned by a tarantula. For our twins’ 5th birthday party this weekend we’ve hired a professional reptile handler to come round and show 30-40 overexcitable kids some interesting animals. If I’m not eaten or bitten I’m a bit worried he won’t do the full register on the way out and I’ll be left with a huge lizard hiding in my bed. All I can say is that for my 5th birthday party we just had pin the tail on the donkey and a few stale sandwiches. Life was so much simpler then.

Markets are pretty complicated at the moment with investors not being quite able to decide whether the newsflow was bad or good yesterday for risk assets. We went to both extremes with the US rallying back into positive territory by the close (S&P 500 +0.30% having been -1.23% just after Europe logged off). As the US starts it’s day a bit later we’ll have a fresh payroll print to throw into the mix which could be the swing factor between 50 and 75bps at the September Fed meeting.

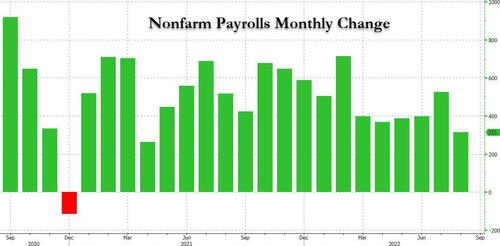

Last month’s strong print ratcheted up expectations that the Fed could hike by 75bps for a third meeting in a row, and markets are still pricing that as the more likely outcome than 50bps, with futures now pricing in +67.7bps worth of hikes. In terms of what to expect today, our US economists are looking for +300k growth in nonfarm payrolls, which should be enough to keep the unemployment rate at its current 3.5%.

Ahead of that, the US labour market data we got yesterday was pretty good, continuing the run of decent releases over recent days. Initial jobless claims for the week through August 27 unexpectedly fell back to 232k (vs. 248k expected), and the previous week was also revised down by -6k. That’s the third week in a row that the jobless claims have fallen, marking a change from the mostly upward trend we’ve seen since late March. On top of that, the ISM manufacturing release also surpassed expectations, remaining at 52.8 (vs. 51.9 expected), with the employment component at a 5-month high of 54.2 (vs. 49.5 expected).

Treasuries lost significant ground on the day, even before the data, with the 2yr yield rising +1bps to hit another post-2007 high of 3.50%, whilst the 10yr yield rose +6bps to 3.25%. The moves were driven by higher real yields across the curve, with the 5yr real yield hitting a 3-year high of 0.849%. It was a similar story in Europe too, where yields on 10yr bunds (+2.2bps), OATs (+2.5bps) and BTPs (+3.3bps) rose. Those European moves came as investors grew increasingly confident that the ECB would hike by 75bps at some point this year, which was aided by the latest data that showed Euro Area unemployment fell to a new low of 6.6% in July. That’s the lowest level since the single currency’s formation, and means that the latest data is showing that the Euro Area simultaneously has the highest inflation and the lowest unemployment of its existence.

As discussed at the top, US equities turned round late in the session with the Nasdaq nearly making it back into the green (-0.26%) as well as the S&P after being -2.28% at 6pm London time. This was too late to save the European session as the STOXX 600 (-1.80%) took a significant hit. Sentiment was pretty downbeat from the outset after the lockdown of the Chinese city of Chengdu (population 21m) risked further disruption to supply chains and global economic demand. That said, the energy situation continued to develop in a positive direction, with German power prices for next year coming down by a further -9.11% to €523.40 per megawatt-hour. In fact they have halved since their intraday peak on Monday when they hit €1050, which just shows how amazingly volatile this market is right now. The EU is considering various interventions to deal with the current turmoil, including price caps and windfall taxes, and Commission President Von der Leyen is set to outline the measures in her State of the Union address on September 14.

Staying on commodities, the decline in oil prices continued yesterday thanks to fears of further Chinese lockdowns and hawkish central banks. Brent crude was down -4.28% to $92.36/bbl, which is a substantial decline since its closing level on Monday of $105.09/bbl. As we go to print, crude oil prices are showing some recovery with Brent futures +1.91% higher at $94.12/bbl. There was a similar negative pattern among industrial metals, with copper (-2.96%) down for a 5th day running on the back of those same fears about demand. Meanwhile in the precious metal space, gold (-0.79%) slipped below $1700/oz, while hitting its lowest since July intraday as markets priced higher interest rates, thus raising the opportunity cost of holding a non-interest-bearing asset.

Over in the FX space, a number of new milestones were reached yesterday, most notably a rise in the dollar index (+0.91%) to levels not seen since 2002. The greenback was supported yesterday by the strong data that added to expectations the Fed would keep hiking into next year, although the reverse picture was that the Euro fell back beneath parity against the dollar, and the Japanese yen fell to 140 per dollar for the first time since 1998. In Asia’ morning trade, the Japanese yen further weakened, touching 140.26 per US dollar. Here in the UK, sterling also fell just beneath the $1.15 mark in trading for the first time since March 2020.

In Asia this morning, the Nikkei (-0.21%), the Hang Seng (-0.58%), and the CSI (-0.20%) are trading lower with the Shanghai Composite (+0.28%) bucking the trend. Elsewhere, the Kospi (+0.04%) is struggling to gain traction after South Korea’s headline inflation slowed after six months of accelerating (more below).

Moving ahead, US stock futures are fairly flat with contracts on the S&P 500 (-0.08%) and NASDAQ 100 (-0.04%) treading water.

Early morning data showed that Korea’s inflation eased to +5.7% y/y in August (v/s +6.1% expected) from +6.3% in July as energy prices eased. MoM prices dropped -0.1% in August (v/s +0.3% expected) after rising +0.5% in the prior month thus providing some comfort to the Bank of Korea (BoK) in its yearlong tightening cycle.

Rounding off yesterday’s data, there was plenty to digest from the global manufacturing PMIs, although they mostly confirmed the picture from the flash readings we’d already got. In the Euro Area, the reading came in at 49.6 (vs. flash 49.7), and the US had a 51.5 reading (vs. flash 51.3). The UK had a stronger revision up to 47.3 (vs. flash 46), but it was still in contractionary territory and the lowest since May 2020. Elsewhere, German retail sales grew by +1.9% (vs. -0.1% expected).

To the day ahead now, and the main highlight will be the US jobs report for August. Otherwise on the data side, there’s US factory orders for July and Euro Area PPI for July.

AND NOW NEWSQUAWK

USTs steady and DXY back towards 109.00 pre-NFP – Newsquawk US Market Open

FRIDAY, SEP 02, 2022 – 06:38 AM

European bourses are firmer across the board as hawkish yield action in the EZ has eased from yesterday’s recent peaks, Euro Stoxx 50 +0.8%.

Stateside, futures are contained and flat with all focus on the NFP report.

DXY continues to pullback from its approach of 110.00, now around 109.10 to the benefit of peers ex-JPY

Comparably contained session overall thus far though Bunds are holding at the lower end of a 85 tick range in limited newsflow pre-NFP; USTs Unch.

WTI Oct and Brent Nov futures are firmer on the day amid a softer Dollar and narrowing prospects of an imminent Iranian Nuclear deal.

Looking ahead, highlights include US NFP & Factory Orders.

As of 11:10BST/06:10ET

For the full report and more content like this check out Newsquawk.

Try a 14 day trial with Newsquawk and hear breaking trading news as it happens.

Russian President Putin said Ukraine is an anti-Russian enclave that is threatening Russia and that Russia is unbowed by western sanctions, according to FT.

“The Russian Embassy in Washington reacted to a message about the proposal of the US authorities to set a price ceiling for Russian oil, saying that Moscow would not supply fuel on non-market terms”, according to Interfax.

European G7 Official says, regarding a potential Russian oil price cap, that a deal is likely but it is unclear how much detail will be provided, via Reuters; however, other officials have said that China and India have expressed interest in purchasing Russian oil at an even lower price, in line with the cap.

Russia’s Kremlin will stop selling oil to countries which support price caps for Russian oil; will ship oil to countries which act in accordance with market rules.

G7 finance ministers set to announce deal on Russian oil price cap this afternoon, officials tell FT; cap would be effective in line with the EU’s embargoes on Russian oil imports.

Ukraine President Zelenskiy says the nation is ready to raise electricity exports to EU nations, even despite all difficulties, Ukraine can meet 8% of Italy’s consumption.

Two inspectors from the IAEA are to stay at the Zaporizhia nuclear plant on a permanent basis, according to a Russian official cited by Ria.

Russia’s Kremlin says only one turbine is operational at the Nord Stream 1 gas pipeline station, reliability of the system is under threat.

CHINA-TAIWAN

Taiwan’s Premier commented regarding the recent shooting down of a drone in which he said that they will do the most appropriate thing for the protection of Taiwan and that they repeatedly warned about encroaching on their doorstep. Furthermore, he said China should exercise restraint and not trigger incidents, as well as noted that Taiwan will not provoke, according to Reuters.

IRAN

Iran sent a constructive response to US proposals aimed at reviving the nuclear deal in which Iran’s response was aimed at finalising negotiations, according to state media cited by Reuters. However, it was later reported that the US said the latest Iran response regarding the nuclear deal is not constructive, according to AFP.

European diplomat says the Iranian response to US comments on the draft JCPOA look “negative and not reasonable”, another source adds the reply does “not look good at all“, via Iran International English.

EU official says Iran’s response was “a disappointing response when we could have closed, and definitely an unreasonable one.”, according to WSJ’s Norman.

Adviser to the Iranian negotiating delegation say “an agreement could be signed within days, as the matter is not complicated, and this depends on the American position”, via Al Jazeera.

OTHER

South Korean national security adviser said South Korea, Japan and the US agreed there will be no soft response in the event of a North Korean nuclear test and they agreed to jointly respond to acts disturbing global supply chains, according to Yonhap.

North Korea accused the newly appointed U.N. special rapporteur on its human rights situation of being a “puppet” of the US, according to Yonhap.

EUROPEAN TRADE

EQUITIES

European bourses are firmer across the board as hawkish yield action in the EZ has eased from yesterday’s recent peaks, Euro Stoxx 50 +0.8%.

Stateside, futures are contained and flat with all focus on the NFP report.

Alphabet’s Google (GOOG) is planning to accept the use of third-party payment services on its smartphone app in national such as Japan and India but not the US, according to the Nikkei

British Chambers of Commerce said the UK is already in the midst of a recession and it expects the UK economy to decline for two more periods following the contraction in Q2, while it also sees inflation to reach 14% later this year, according to Bloomberg.

EU warned UK Foreign Secretary Truss against triggering Article 16 and said they will refuse to engage in serious talks on reforms to the post-Brexit deal unless she takes the “loaded gun” of unilateral legislation off the table, according to FT.

NOTABLE DATA

EU Producer Prices YY (Jul) 37.9% vs. Exp. 35.8% (Prev. 35.8%, Rev. 36.0%); MM (Jul) 4.0% vs. Exp. 2.5% (Prev. 1.1%, Rev. 1.3%)

NOTABLE US HEADLINES

Fed’s Bostic (2024 voter) said the Fed has work to do regarding inflation and is a long way from 2%, while he added that the Fed has got to get the economy to slow down. Bostic also commented that the balance sheet is to be increasingly MBS concentrated and the Fed may have to sell MBS from its balance sheet, according to Bloomberg.

Bitcoin has reclaimed the USD 20k mark but the upward move is yet to gain any real traction amid the broader contained price action.

APAC TRADE

APAC stocks were indecisive with price action relatively rangebound after the mixed lead from the US and with the region lacking firm commitment as participants await the upcoming US NFP jobs data.

ASX 200 was lacklustre as earnings releases quietened and with strength in financials offset by losses across the commodity-related sectors.

Nikkei 225 traded subdued amid underperformance in large industrials although losses in the index were stemmed by retailers after several reported strong August sales.

Hang Seng and Shanghai Comp were mixed as Hong Kong underperformed amid notable losses in developers and with the mainland choppy but ultimately kept afloat after the PBoC recently cut rates on its Standing Lending Facility by 10bps from August 15th and after several officials pledged measures.

NOTABLE APAC HEADLINES

PBoC set USD/CNY mid-point at 6.8917 vs exp. 6.9202 (prev. 6.8821).

PBoC official Ruan said monetary policy is to further improve cross-cyclical adjustments and maintain stable and moderate credit development, while they will keep liquidity reasonably ample. PBoC will also better coordinate structural and aggregate policy tools but will avoid flood-like stimulus and keep prices stable. Furthermore, the PBoC said China has not taken excessive monetary policy stimulus since the pandemic, leaving room for subsequent policy adjustments and that balanced consumer prices also create favourable conditions for monetary policy adjustments, according to Reuters.

PBoC adviser Wang said banks need to increase financial support for infrastructure and that infrastructure is restricted by local government debt levels, while Wang added that they need to ensure property companies’ financing needs are met, according to Reuters.

China’s securities regulator official said they will promote new legislation for overseas listings and will implement the China-US audit agreement, as well as continue strengthening communication with foreign institutional investors, according to Reuters.

China’s banking regulator official said they will steadily resolve the risks faced by small and medium-sized financial institutions, while they will improve monitoring and disposal of debt risks of large companies, according to Reuters.

Japanese Finance Minister Suzuki said it is important for currencies to move stably reflecting economic fundamentals, while he noted that recent FX moves are big and they will take appropriate action on FX if necessary. Suzuki also stated that they are watching FX with a sense of urgency and will brief the media after the G7 finance ministers meeting tonight.

DATA RECAP

Korea (Republic of) CPI Growth MM (Aug) -0.1% vs. Exp. 0.3% (Prev. 0.5%); YY (Aug) 5.7% vs. Exp. 6.1% (Prev. 6.3%)

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED UP 1.50 PTS OR 0.05% //Hang Sang CLOSED DOWN 145.22 OR 0.74% /The Nikkei closed DOWN 10.63 OR .04%. //Australia’s all ordinaires CLOSED DOWN 0.33% /Chinese yuan (ONSHORE) closed DOWN AT 6.9082//OFFSHORE CHINESE YUAN DOWN 6.9153// /Oil DOWN TO 88.08 dollars per barrel for WTI and BRENT AT 93.97 / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

3 a./NORTH KOREA/ SOUTH KOREA/

///NORTH KOREA/SOUTH KOREA/

3B JAPAN

end

3c CHINA

CHINA/

A super typhoon (equivalent to a category 4 to 5 hurricane) barrels towards China and directly in shipping lanes. This will probably disrupt shipping of goods

(zerohedge)

.

Super Typhoon Barrels Towards China, Major Shipping Lanes In Path

THURSDAY, SEP 01, 2022 – 07:00 PM

Super Typhoon Hinnamnor is barreling towards China’s coastal provinces, Japan, and South Korea as it traverses the South China Sea in the western Pacific Ocean.

The United States Naval Meteorology and Oceanography Command has labeled Hinnamnor a “super typhoon” — since it has surpassed winds of at least 150 mph. For US readers, the storm is equivalent to a Category 4/5 in the Atlantic basin.

As of Thursday, Hinnamnor was located 143 miles east of Japan’s Okinawa, as per the Hong Kong Observatory, with wind speeds above 159 mph, gusting to 195 mph, according to The Weather Channel.

According to Taiwan News, the rapid intensification of Hinnamnor is because it absorbed a tropical system, Tropical Depression TD14. Also, warm tropical waters and mild winds allowed the system to develop into a super typhoon.

In response to the system’s path, China activated the lowest tier of its four-level emergency response system in eight provinces and municipalities, including Shanghai and Zhejiang. The system is expected to move into the East China Sea over the weekend.

Even though Hinnamnor could lose strength in the coming days, its forecasted path could be very disruptive to international supply chains — already under pressure as zero-Covid policies shutter a major manufacturing hub on Thursday. Ports, such as the ones in Shanghai, could be in the storm’s path by the late weekend or early Monday. The storm could impact parts of South Korea and Japan by late Monday or early Tuesday. These are are known for some of the largest containerized shipping ports in the world.

All eyes this weekend are on Hinnamnor’s path as it is expected to threaten countries such as Japan, China, and South Korea.

end

Another top developer in China (Garden Holdings Co) warns that the property crisis has slid the country into a severe depression. Real estate in China is 27% of their GDP

(zerohedge)

China’s Top Developer Warns Property Crisis Has “Slid Rapidly Into Severe Depression”

THURSDAY, SEP 01, 2022 – 11:00 PM

China hit an ominous milestone this week as one of the largest property developers reported a 96% profit drop, blaming a “severe depression” in the real estate market where “only the fittest can survive,” reported WSJ.

Garden Holdings Co.’s first-half earnings crashed the most since its 2007 listing in Hong Kong as the housing market crisis worsened. It said preliminary net profit collapsed from $2 billion to just $88 million in the first six months.

Alarm is spreading in China as the once robust property market is at risk of collapse. The Guangdong-based company warned demand is slipping and property values are sliding:

“All these exert mounting pressure on all participants in the property market, which has slid rapidly into severe depression. The harsh business environment in which only the fittest can survive means even higher requirements for businesses’ competitive strength.”