by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1668.80 DOWN $30.20

SILVER: $19.29 DOWN $0.25

ACCESS MARKET:

GOLD $1664.50

SILVER: $19.17

Bitcoin morning price: $20,139 UP 335

Bitcoin: afternoon price: $19,752 DOWN 57

Platinum price closing UP $0.24 AT $908.99

Palladium price; closing DOWN $23.25 at $2146.50

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,696.500000000 USD

INTENT DATE: 09/14/2022 DELIVERY DATE: 09/16/2022

FIRM ORG FIRM NAME ISSUED STOPPED

323 C HSBC 48

435 H SCOTIA CAPITAL 63

624 H BOFA SECURITIES 13

657 C MORGAN STANLEY 6

661 C JP MORGAN 156 60

737 C ADVANTAGE 12 3

800 C MAREX SPEC 32 6

905 C ADM 1

TOTAL: 200 200

MONTH TO DATE: 4,864

JPMorgan stopped: 267/775

_____________________________________________________________________________________

GOLD: NUMBER OF NOTICES FILED FOR SEPT CONTRACT:

200 NOTICES FOR 20,000 OZ //0.622 TONNES

total notices so far: 4864 contracts for 486,400 oz (15.129 tonnes)

SILVER NOTICES: 42 NOTICES FILED FOR 210,000 OZ/

total number of notices filed so far this month 6369 : for 31,845,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $30.20

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: //// A WITHDRAWAL OF 2.35 TONNES FROM THE GLD/

INVENTORY RESTS AT 960.56 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN $.25

AT THE SLV// ://BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 1.151 MILION OZ INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 467.050 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL SIZED 135 CONTRACTS TO 135,665. AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.06 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.06) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC SILVER LONGS AS WE HAD A STRONG GAIN OF 1045 CONTRACTS ON OUR TWO EXCHANGES,; WE DID HAVE SOME MINOR SPECULATOR LIQUIDATION.(SHORT COVERING)

WE MUST HAVE HAD:

I) SOME MINOR/ SPECULATOR SHORT LIQUIDATIONS ////CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 165,000 OZ QUEUE JUMP / // V) SMALL SIZED COMEX OI GAIN/(//SOME SPEC LIQUIDATION/)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -17

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTACTS for 10 days, total 10,255 contracts: 51.275 million oz OR 5.1275 MILLION OZ PER DAY. (1026 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 51.275 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 51.275 MILLION OZ///

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 135 WITH OUR $0.06 GAIN IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 893 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /GOOD BANKER ADDITIONS A// MINOR SPEC SHORT LIQUIDATIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 165,000 OZ QUEUE JUMP // .. WE HAD A STRONG SIZED GAIN OF 1028 OI CONTRACTS ON THE TWO EXCHANGES FOR 5.140MILLION OZ AS..THE SPECS STILL BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 42 NOTICE(S) FILED TODAY FOR 210,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 741 CONTRACTS TO 464,415 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY:—976 CONTRACTS.

.

THE SMALL SIZED INCREASE IN COMEX OI CAME DESPITE OUR FALL IN PRICE OF $7.70//COMEX GOLD TRADING/WEDNESDAY / WE MUST HAVE HAD MINOR SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND /STRONG SPECULATOR SHORT ADDITIONS//CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 8.401 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 36,980 OZ //NEW STANDING 15.7107 TONNES

YET ALL OF..THIS HAPPENED WITH OUR FALL IN PRICE OF $7.70 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 3302 OI CONTRACTS 10.27 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2511 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 464M415

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3302 CONTRACTS WITH 741 CONTRACTS INCREASED AT THE COMEX AND 2511 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3302 CONTRACTS OR 10.270 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2511) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (741): TOTAL GAIN IN THE TWO EXCHANGES 3302 CONTRACTS. WE NO DOUBT HAD 1) MINOR SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS//STRONG SPECULATOR SHORT ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 8.409 TONNES FOLLOWED BY TODAY’S QUEUE. JUMP OF 36,980 oz. 3) ZERO LONG LIQUIDATION//// //.,4) FAIR SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

20,747 CONTRACTS OR 2,074,700 OZ OR 64.53 TONNES 10 TRADING DAY(S) AND THUS AVERAGING: 2075 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10 TRADING DAY(S) IN TONNES: 64.53 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 64.53/3550 x 100% TONNES 1.83% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 64.53 TONNES (MUCH LESS ISSUANCE THIS MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT., FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER,ROSE BY A SMALL SIZED 135 CONTRACT OI TO 135,665 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 893 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 893 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 893 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 135 CONTRACTS AND ADD TO THE 893 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 1028 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 5.140 MILLION OZ

OCCURRED WITH OUR GAIN IN PRICE OF $0.06

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 37.62 PTS OR 1.16% //Hang Sang CLOSED UP 83.28 PTS OR 0.44% /The Nikkei closed UP 57.29 OR 0.21%. //Australia’s all ordinaries CLOSED UP 0.15% /Chinese yuan (ONSHORE) closed DOWN AT 6.9909//OFFSHORE CHINESE YUAN DOWN 6.9999// /Oil UP TO 87,08 dollars per barrel for WTI and BRENT AT 92.93 / Stocks in Europe OPENED MOSTLY GREEN. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 741 CONTRACTS TO 464,415 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS FAIR COMEX INCREASE OCCURRED DESPITE OUR STRONG FALL IN PRICE OF $7.70 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2511 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2511 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :2511 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2511 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED SIZED TOTAL OF 3302 CONTRACTS IN THAT 2511 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 741 CONTRACTS..AND THIS GOOD GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR STRONG FALL IN PRICE OF GOLD $7.70. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING SEPT (15.7107),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 15.7107 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $7.70) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A GOOD SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 3302 CONTRACTS // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS ADDED TO THEIR POSITIONS////// WE HAVE REGISTERED A SMALL SIZED GAIN OF 10.27 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR SEPT. (15.7107 TONNES)…

WE HAD 976 CONTRACTS ADDED FROM COMEX TRADES. THESE WERE ADDED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3302 CONTRACTS OR 330200 OZ OR 10.27 TONNES

Estimated gold volume 261,841/// fair//raid/

final gold volumes/yesterday 182,353/ poor

INITIAL STANDINGS FOR SEPT ’22 COMEX GOLD //SEPT 15

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 49,928.792 oz Brinks HSBC JPMorgan includes one kilobar |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 1999.900 oz Delaware |

| No of oz served (contracts) today | 200 notice(s) 20,000 OZ 0.622 TONNES |

| No of oz to be served (notices) | 187 contracts 18,700 oz 0.5816TONNES |

| Total monthly oz gold served (contracts) so far this month | 4864 notices 486,400 OZ 15.129 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

3 customer withdrawals:

i) Out of Brinks: 32.151 oz one kilobar

ii) Out of HSBC: 9648.678 oz

iii) Out of jPMorgan 40,247.963 oz

total: 49,928.792 oz

total in tonnes: 1.55 tonnes

Adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPT.

For the front month of SEPT we have an oi of 387 contracts having LOST 406 contracts .

We had 775 notices filed on WEDNESDAY so we gained 369 contracts or an additional 36,900 oz

will stand for gold in this very non active delivery month of September.

October LOST 53 contracts DOWN to 43,092

November GAINED 128 contracts to stand at 317

December GAINED 773 contracts UP to 376,006

We had 200 notice(s) filed today for 20,000 oz FOR THE SEPT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 156 notices were issued from their client or customer account. The total of all issuance by all participants equate to 200 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 60 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2022. contract month,

we take the total number of notices filed so far for the month (4864) x 100 oz , to which we add the difference between the open interest for the front month of (SEPT 387 CONTRACTS) minus the number of notices served upon today 200 x 100 oz per contract equals 505,100 OZ OR 15.7107 TONNES the number of TONNES standing in this NON active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month:

No of notices filed so far (4864) x 100 oz+ (387) OI for the front month minus the number of notices served upon today (200} x 100 oz} which equals 505,100 oz standing OR 15.7107 TONNES in this NON active delivery month of SEPTEMBER.

TOTAL COMEX GOLD STANDING: 15.7107 TONNES (A GREAT STANDING FOR A SEPT ( NON ACTIVE) DELIVERY MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,422,430.376 oz 75.34 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 27,170,221.801 OZ

TOTAL REGISTERED GOLD: 13,379,878.715 OZ (416.17 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 13,790,343.080 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,957.448. OZ (REG GOLD- PLEDGED GOLD) 340.82 tonnes//rapidly declining

END

SILVER/COMEX/SEPT 15

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2,324,980.731oz BRINKS Delaware Loomis JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 535,868.762 oz HSBC |

| No of oz served today (contracts) | 42 CONTRACT(S) 210,000 OZ) |

| No of oz to be served (notices) | 150 contracts (750,000 oz) |

| Total monthly oz silver served (contracts) | 6369 contracts 31,845,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i)Into HSBC 535,868.762 oz

total deposit: 535,868.762 oz

JPMorgan has a total silver weight: 166.361 million oz/320.341million =51.92% of comex

Comex withdrawals: 4

i) Out of Loomis: 1,401,953.699 oz

ii) Out of jPMorgan: 904,654.520 oz

iii) Out of Brinks 16,405.820 oz

iv) Out of Delaware 1966.693 oz

total: 2,324,980.731 oz

adjustments: 2//dealer to customer

Brinks 195,248.320 oz

and

Delaware: 19,984.281 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 45.688 MILLION OZ

TOTAL REG + ELIG. 320.341 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF SEPT OI: 192 CONTRACTS HAVING GAINED 10 CONTRACTS. WE HAD

23 CONTRACTS SERVED ON WEDNESDAY SO WE GAINED 33 CONTRACTS OR AN ADDITIONAL

165,000 OZ WILL STAND FOR METAL IN THIS VERY ACTIVE MONTH OF SEPT.

WE WILL GAIN IN TOTAL SILVER STANDING EACH TRADING DAY UNTIL THE END OF THE MONTH

(CONTINUAL QUEUE JUMPING BY OUR BANKERS SEARCHING FOR SILVER METAL)

OCTOBER LOST 15 CONTRACTS TO STAND AT 552 CONTACTS.

NOVEMBER GAINED 7 CONTRACTS TO STAND AT 54

DECEMBER SAW A LOSS OF 351 CONTRACTS DOWN TO 120,775

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 42 for 210,000 oz

Comex volumes:74,106// est. volume today// good

Comex volume: confirmed yesterday: 86,127 contracts ( good)

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 6369 x 5,000 oz = 31,845,000 oz

to which we add the difference between the open interest for the front month of SEPT(192) and the number of notices served upon today 42 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT./2022 contract month: 6,369 (notices served so far) x 5000 oz + OI for front month of SEPT (192) – number of notices served upon today (42) x 5000 oz of silver standing for the SEPT contract month equates 32,595,000 oz. .

We have an inventory of 45.688 million oz of registered silver at the comex so Sept delivery of 32.595 MILLION OZ represents 71.34% of that category of silver.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:24,471// est. volume today// extremely poor

Comex volume: confirmed yesterday: 50,223contracts ( poor)

END

GLD AND SLV INVENTORY LEVELS

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

SEPT 13/WITH GOLD DOWN $22.85 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73ONNES FROM THE GLD////INVENTORY RESTS AT 964.91 TONNES

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

AUGUST 31.WITH GOLD DOWN $10.20:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.24 TONNES FROM THE GLD////INVENTORY RESTS AT 973.37 TONNES

AUGUST 30.WITH GOLD DOWN $12.00:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 980.61 TONNES

AUGUST 29/WITH GOLD DOWN $.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD/////INVENTORY RESTS AT 982.64 TONNES

AUGUST 26/WITH GOLD DOWN $26.60; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 25/WITH GOLD UP $9.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 18/WITH GOLD DOWN $5.25: GIGANTIC CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.78 TONNES FROM THE GLD////INVENTORY RESTS AT 985.83 TONNES

AUGUST 17/WITH GOLD DOWN $12.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 992.20 TONNES

AUGUST 16/WITH GOLD DOWN $7.85: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 993.94 TONNES

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

GLD INVENTORY: 960.56 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

SEPT 13/WITH SILVER DOWN $.31 TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.899 MILLION OZ//

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

AUGUST 31/WITH SILVER DOWN 36 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 3.087 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 465.573 MILLION OZ//

AUGUST 30/WITH SILVER DOWN 34 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 1.478 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 470.135 MILLION OZ//

AUGUST 29/WITH SILVER DOWN 7 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY A THE SLV: A WITHDRAWAL OF 2.765 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 470.135 MILLION OZ//

AUGUST 26/WITH SILVER DOWN 39 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 25/WITH SILVER UP 21 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

AUGUST 18/WITH SILVER DOWN 27 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 369,000 OZ INTO THE SLV////INVENTORY RESTS AT 485.482 MILLION OZ//

AUGUST 17/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.106 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.113 MILLION OZ//

AUGUST 16/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 486.219 MILLION OZ/

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

CLOSING INVENTORY 467.050 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

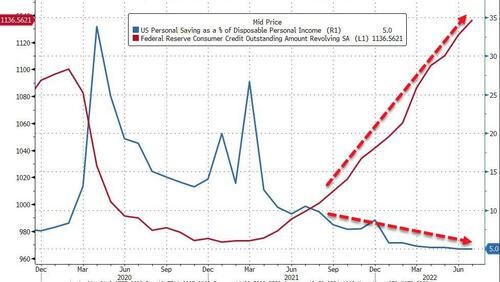

Americans Continue To Pile On More And More Debt

THURSDAY, SEP 15, 2022 – 08:48 AM

American consumers continue to cope with rising prices and prop up the sagging economy using their credit cards.

Total consumer debt rose another $23.8 billion in July to a record $4.644 trillion, according to the latest data from the Federal Reserve.

On an annual basis, consumer debt rose by 6.2%, moderating somewhat from the last few months as the CPI cooled thanks to a drop in energy prices.

The Federal Reserve consumer debt figures include credit card debt, student loans, and auto loans, but do not factor in mortgage debt. When you include mortgages, US consumers are buried under more than $16.2 trillion in debt.

Consumer credit grew by an average of $30 billion per month through the first seven months of the year.

Americans are burning up their plastic in order to make ends meet. Revolving credit, primarily reflecting credit card debt, rose by another $10.9 billion, an 11.6% annual increase. To put that into perspective, the annual increase in 2019, prior to the pandemic was 3.6%. It’s pretty clear that with stimulus money long gone, Americans have turned to plastic in order to make ends meet as prices continue to skyrocket.

Revolving debt now stands at $1.137 trillion – above the pre-pandemic record.

Americans, by and large, kept their credit cards in their wallets and paid down balances at the height of the pandemic in 2020. This is typical consumer behavior during an economic downturn and the trend was even more pronounced with pandemic stimulus checks. Credit card balances were over $1 trillion when the pandemic began. They fell below that level in 2020 with an 11.2% drop. We saw small upticks in credit card balances in February and March of last year as the recovery began, with a sharp drop in April as another round of stimulus checks rolled out. But Americans started borrowing in earnest again in May 2021. Since then, we’ve seen a steady increase in consumer debt.

Not only are credit card balances growing; consumers are trying to find ways to borrow even more. According to Fed data, Americans opened 233 million new credit card accounts in the second quarter of this year. That was the largest number of new accounts opened in a single quarter since 2008 – the beginning of the Great Recession.

Aggregate limits on credit card accounts increased by $100 billion in Q2 and now stand at $4.22 trillion. That reflects the largest increase in more than 10 years.

Meanwhile, average credit card interest rates have eclipsed the record high of 17.87% set in April 2019. The average annual percentage rates (APR) currently stand at 18.03%. That’s up from 17.5% just a month ago.

The central bank is expected to push rates up another 75 basis points during its September meeting.

This is bad news for Americans depending on credit to pay their bills. With interest rates rising, Americans are paying higher and higher interest charges every month with minimum payments rising. With every Federal Reserve interest rate increase, the cost of borrowing will go up more, putting a further squeeze on American consumers.

Non-revolving credit charted a healthy jump in July, increasing by $12.9 billion, an 4.4% year-on-year jump. This includes auto loans and student loans. Total non-revolving credit now stands at $3.508 trillion.

For months, the mainstream has told us the massive growth in debt was a sign of economic health. Last month, MarketWatch reported, “How much credit households use is seen as a good window into the strength of the economy. Consumers tend to borrow more when times are good and cut back when the economy is weak.” Meanwhile. Fed chair Jerome Powell keeps telling us that “households are in very strong financial shape.” With the growth in debt moderating somewhat (although still high) does this mean the economy is getting shaky?

You probably won’t hear that narrative from the mainstream. But any slowdown in spending is bad news for an economy that relies on people buying stuff. Of course, the slowing of the debt increase likely just reflects slightly lower energy prices in July and not any real change in consumer spending.

The bottom line is that Americans continue to borrow at an excessive rate because they don’t have any other way to make ends meet. People don’t run up their Visa balance month after month to buy groceries when they are in “very strong” financial shape. The stimulus checks are long gone. Savings are being depleted. The average person has no choice but to pull out the plastic. Of course, this is not a sustainable trajectory. A credit card has this inconvenient thing called a limit.

end

Peter Schiff: The Fed Won’t Bend This Inflation Curve

THURSDAY, SEP 15, 2022 – 12:01 PM

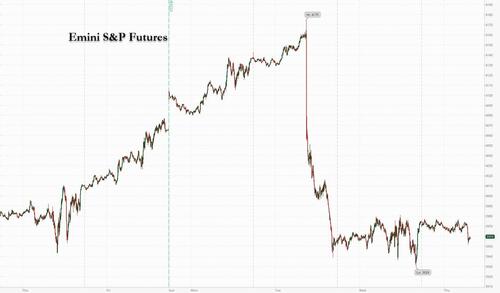

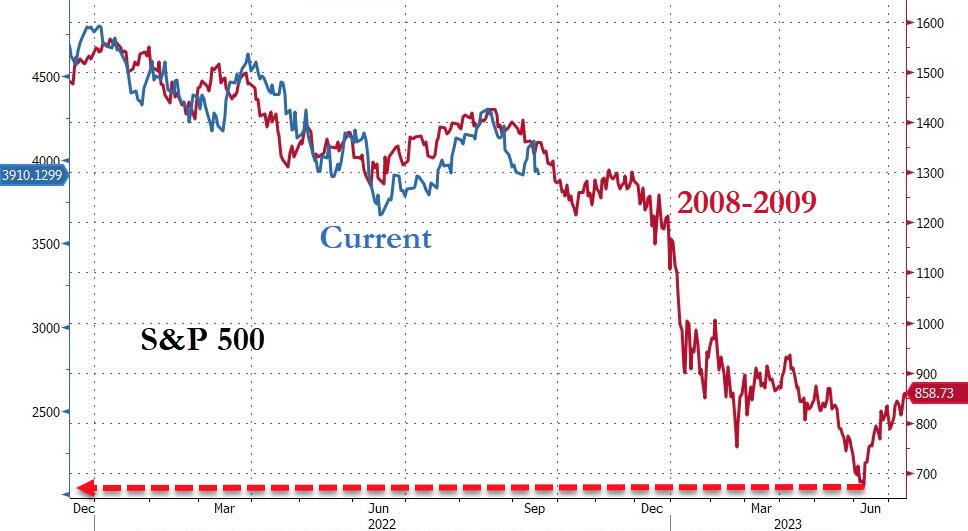

The CPI data for August came in hotter than expected, sparking the biggest market crash since the 2020 COVID lockdowns. The price of gold also dropped on the news in anticipation of the Federal Reserve taking interest rates higher. Peter Schiff talked about the inflation news on his podcast and said investors need to get gold now before the entry point rises a lot higher. Because at some point the markets are going to figure the Fed can’t bend this inflation curve.

After the CPI data came out, stocks plunged. The Dow Jones fell by over 1,276 points. It was the seventh-biggest drop (based on points) in history. Other stock market indices charted similar declines. The NASDAQ fell 5.16%.

As Peter noted, gold also fell, but not nearly as much as stocks. The yellow metal was off about 1.3%. But gold did manage to close above $1,700, although it traded below that level interday.

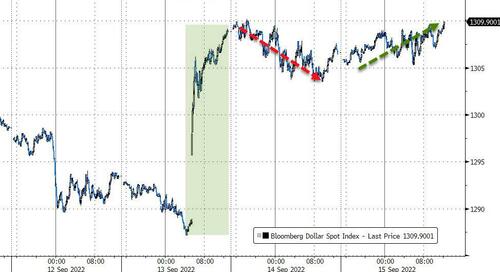

The dollar index charted a huge swing, moving from 107.68 prior to the CPI data and then rallying to close at 109.9. Peter said it was one of the biggest moves in the dollar he’s seen.

The markets were preparing for a softer CPI. Everybody was under the impression that inflation had peaked and that it was coming down, and that when we got validation that inflation was coming down by the August CPI, that would take a lot of pressure off the Fed — that it wouldn’t have to raise rates as much because the inflation problem was solved. That’s one of the reasons the dollar sold off. It’s one of the reasons gold and silver rallied. In fact, it’s one of the reasons the stock market had been rallying, because the Fed was going to be taken out of the game. Maybe not completely sidelined, but at least it was going to tone down its rhetoric and maybe not raise rates as much as people thought. But now that we got this hotter than expected number, people think the Fed is going to raise rates more than they thought.”

Peter said the markets still don’t understand that even if the Fed hikes by 100 basis points at the September meeting, it will not bend the inflation curve.

I don’t know why everybody continues to be surprised when the inflation numbers come out worse than expected. They assume that what the Fed is doing is going to work. It’s not going to work. The people who think it is don’t understand the nature of the problem.”

The numbers indicate that Fed can’t win this inflation fight. Part of the solution is positive real interest rates. If you look at all of the Fed tightening cycles since 1973, the central bank has never stopped tightening before the Fed funds rate was higher than the CPI.

As long as we have interest rates below the inflation rate, even if they’re higher, they’re still negative, and negative interest rates put upward pressure on inflation. You can’t fight inflation with negative interest rates. It’s like saying, ‘I’m going to fight this fire by pouring gasoline on it. It’s just that I’m only going to pour a little bit of gasoline, not as much gasoline as I was pouring on before.’”

Clearly, the fire will keep getting bigger.

But the markets don’t seem to get this. Otherwise, they wouldn’t be selling gold into rising inflation.

After all, gold is an inflation hedge. And if investors expect more inflation, they’re going to hedge with gold. And if you expect inflation to continue, gold is going to discount that future inflation into the present, and it’s going to be reflected in the current price of gold.”

The question is when will those expectations change?

How many more months can the CPI come out hotter than expected and investors still believe that inflation is going to go away? How many more rate hikes do we need that are ineffective at reducing inflation before investors figure out that it’s not going to work? And of course, how many rate hikes will the Fed be able to get away with without crashing the stock market? Without crashing the real estate market? Without causing a financial crisis?”

And if the Fed keeps pushing that envelope until it rips, will the Fed continue to hike rates? Or will the Fed pivot when it anticipates or acknowledges the next crisis?

As long as it pivots at all, that means inflation is going to run out of control. And if it is, the dollar needs to go way down and gold needs to go way up.”

Peter said he doesn’t personally think the Fed will get away with very many more rate hikes.

He pointed out that gold didn’t fall all that much given the plunge in stocks. In fact, gold didn’t even close on the lows.

Maybe that’s some indication that investors are beginning to question that narrative. They haven’t completely figured it out yet, but some of the selling may in fact have been exhausted.”

Peter said at some point there will be divergence and gold will start rising when inflation is worse than expected. The dollar will fall. And the long end of the bond market will start getting beat up.

If you’re waiting for a sign, some indication that everything is about to blow up, that’s what you should look for. You should look for a reaction in the bond market and the currency market and the precious metals market that is opposite of the reaction that we’ve been having.”

Peter said you shouldn’t wait for that signal to position yourself.

I think it’s possible that by the time we get that signal, it could be a much worse entry position than the one we have right now. Because the markets can start anticipating that signal before we actually get it. I know it’s going to happen eventually. But when it does happen, that’s when you’ll know the end has finally begun. But before it does, take advantage of other investors’ misunderstanding of what’s going on by increasing your exposure to both gold and silver, and gold and silver mining stocks.”

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

LAWRIE WILLIAMS: Above expectation CPI raises prospects of 1% FOMC rate rise

Well the August Consumer Price Index (CPI) inflation figure has come in at an above expectation 8.3% increase year-on-year but the Producer Price index (PPI) came in marginally lower year-on-year at 8.7% – lower than expected. But in both cases month –on-month core inflation rates rose sharply prompting prior expectations of a Fed 75 basis point rate rise over a 50 basis point one to switch to a likelihood of a 75 basis point increase over a 100 basis point one to 72:28 in the CME group’s Fedwatch Tool.

As a consequence markets all fell sharply as the likelihood of a looming U.S. recession, as we have been warning all along, grew ever closer. Indeed as we have expressed beforehand we may already be in one as the technical parameters for a recession of two successive quarters of negative GDP growth have already occurred.

The Dow has fallen around 1,400 points over the past couple of days and still appears to be falling. Bitcoin is down well over $2,000 over a similar period and the gold price is off around $35 – a much smaller fall in percentage terms than equities or bitcoin, demonstrating that precious metals tend to be a far safer investment in such times of economic meltdown.

Where does this leave the Fed? Fed chair Powell, and some of his colleagues, have reiterated in recent speeches that the Fed ‘will do what it takes’ to bring inflation down, even if it impinges negatively on some of the Fed’s other priorities of keeping employment levels as high as possible. This could well involve raising interest rates higher and faster than the markets had previously been expecting, and one thus can’t rule out a year-end rate of 4.5% or thereabouts which is definitely higher than had previously been anticipated and certainly, if implemented, could easily tip the U.S. economy into recession, if it were not there already,

One should expect the threat of higher U.S. interest rates to raise the dollar index on the international currency markets which would be a continuing negative factor for gold. However, the ever increasing likelihood that the U.S. economy is heading for recession may be acting as a counter to this and so far dollar strength seems to have been muted.

Ukraine’s recent apparent successes in recapturing some ground from the seemingly impregnable Russian advance has been leading some to suggest that the conflict there is entering a new phase which could lead to a Ukraine victory and a defeat for Putin. In our view this is an extremely dangerous assumption and could lead to Putin employing ever more dangerous weaponry and tactics to regain the military advantage. He is not known for backing down. If this should happen and Russia, for example, starts to use tactical nuclear weapons, who knows where that could lead, It could lead to a huge surge in safe haven assets prices, but equities and bitcoin could be left out in the cold. Hopefully such an eventuality is beyond the pale even for President Putin, but who knows what a wounded bear is capable of?

14 Sep 2022

GOLD/SILVER

END

3.Chris Powell of GATA provides to us very important physical commentaries

Suriname is fighting to give more rights to indigenous

(Lyons/Epinosa/GATA)

Can two new bills reshape indigenous rights and illegal gold mining in Suriname?

Submitted by admin on Wed, 2022-09-14 20:10Section: Daily Dispatches

By Charles Lyons and Charlie Espinosa

Mongabay.com, Menlo Park, California

Wednesday, September 14, 2022

“We’ve been fighting the government of Suriname for almost 25 years, for recognition of our land rights,” says Jupta Itoewaki, a leader of the Indigenous Wayana people. “The government and leaders don’t feel like they need to consult us.”

Itoewaki has long been at the forefront of a battle to win legal standing for Indigenous and tribal groups, who make up about a quarter of the population of Suriname, the smallest country in South America. Along with Guyana and French Guiana, Suriname is the only Amazonian country or territory not to have ratified Convention 169, a 1989 treaty from the International Labour Organization that legally recognizes Indigenous and tribal peoples’ right to self-determination.

Such rights have not been recognized despite rulings in 2006, 2007, and 2015 by the Inter-American Human Rights Court against Suriname for violating the rights of Indigenous groups.

And as Indigenous activists in Suriname recently pointed out, even the United Nations continues to fail to be sensitive to the issue.

On a trip to the country in July, U.N. Secretary-General António Guterres celebrated Suriname’s record of preserving its forests, calling the country an example for the rest of the world.

Two associations of tribal and Indigenous leaders, VIDS and KAMPOS, sent a letter to Guterres and the U.N. reminding them that Suriname’s environmental and human rights records have been far from the best and pleading for legislation to defend their rights. …

… For the remainder of the report:

END

This is terrific: Money Metals Exchange is growing fast and it is now building a huge 40,000 sq foot facility

(MME/GATA)

Money Metals Exchange builds largest gold and silver depository in western U.S.

Submitted by admin on Wed, 2022-09-14 20:24Section: Daily Dispatches

From Money Metals News Service, Eagle, Idaho

Wednesday, September 14, 2022

EAGLE, Idaho — Money Metals Exchange, a nationally focused precious metals company, announced today it is breaking ground on a 40,000-square-foot vaulting and fulfillment facility in Idaho.

The $21 million facility will be the largest private depository of its kind in the western United States. It could be expanded to 60,000 square feet.

“The overwhelming growth in demand for physical gold and silver as financial insurance combined with the great pricing, customer service, and content offered by Money Metals have led to dramatic growth in our business since 2019,” said Money Metals Exchange President Stefan Gleason.

“Americans are waking up to the risks we all face from growing attacks on our freedom and financial security, combined with a runaway inflation situation fueled by debt-funded government spending and Federal Reserve monetary debasement.”

The nationally acclaimed metals dealer has outgrown its existing facility, constructed in 2014, with its employee count rising from 25 to nearly 100 during the past three years.

Money Metals now ships more than 40,000 gold and silver orders across America each month, with thousands of other investors choosing to securely store their precious metals in individually segregated accounts at the Money Metals Depository. …

… For the remainder of the announcement:

END

Unbelievable: Biden funnels billions to the Taliban in Afghanistan via the BIS

(New York Sun/GATA)

New York Sun: Biden will funnel billions to Taliban via BIS

Submitted by admin on Wed, 2022-09-14 20:46Section: Daily Dispatches

The Folly of Biden’s ‘Afghan Fund’

From The New York Sun

Wednesday, September 14, 2022

Not since Robert Strange McNamara used the World Bank to steer funds backed by American taxpayers to the North Vietnamese has there been as outrageous a move as President Biden’s decision to set aside billions of dollars to fund Afghanistan in the Taliban era.

Mr. Biden’s démarche, which involves a new Swiss-based entity called “The Afghan Fund,” defies credulity by vowing to aid the Afghan people without propping up the Taliban regime.

Mr. Biden insists that the money, some $3.5 billion, will not go to the Taliban. He claims that the funds will “be used for the benefit of the people of Afghanistan while keeping them out of the hands of the Taliban,” a Treasury statement today notes.

This runs contrary to a basic rule of economics, the fungibility of money. Aid sent to the Afghan people relieves pressure on the Taliban, enabling them to prioritize their murderous intentions.

Yet the “Taliban are not a part of the Afghan Fund,” Mr. Biden blithely contends, “and robust safeguards have been put in place to prevent the funds from being used for illicit activity.” Such assurances are the rationalizations of the appeasement-minded, among them the deputy State secretary, Wendy Sherman, who vows that the billions will “improve economic stability for the people of Afghanistan while continuing to hold the Taliban accountable.”

It should reassure no one concerned about the ethics of this plan that the new “Afghan Fund” will operate out of that haven for transparency in financial transactions, Switzerland. The money in question, currently on deposit at the New York Fed, will now migrate into an account with the Bank for International Settlements, and the White House promises “an external auditor will monitor and audit the Afghan Fund as required by Swiss law.” …

… For the remainder of the commentary:

https://www.nysun.com/article/the-folly-of-bidens-afghan-fund

end

4. OTHER GOLD/SILVER COMMENTARIES

.

end

5.OTHER COMMODITIES: RICE

The Stage Is Being Set For A Massive Global Rice Shortage

THURSDAY, SEP 15, 2022 – 04:20 PM

Authored by Michael Snyder via The Economic Collapse blog,

This wasn’t supposed to happen. For months, I have been writing article after article about the rapidly growing global food crisis, but even though drought is devastating so many other crops all over the planet I thought that there would be plenty of rice in 2023. Unfortunately, I was wrong. As you will see below, some of the biggest rice producers in the entire world are being hit really hard, and rice production is going to be way below expectations this year. Of course rice is one of the primary staples that poor nations depend upon, and so this is a really big deal. If there is a serious shortage of rice in 2023, that is going to have enormous implications for all of us.

An announcement that India just made should be front page news all over the globe right now.

India usually accounts for over 40 percent of all worldwide rice shipments, but now they have placed severe restrictions on all future exports this year…

India banned exports of broken rice and imposed a 20% duty on exports of various grades of rice on Thursday as the world’s biggest exporter of the grain tries to augment supplies and calm local prices after below-average monsoon rainfall curtailed planting.

India exports rice to more than 150 countries, and any reduction in its shipments would increase upward pressure on food prices, which are already rising because of drought, heat-waves and Russia’s invasion of Ukraine.

Did you catch that last sentence?

150 different nations depend on rice from India.

So where are they going to get their rice?

Normally, India exports more rice than the next four largest exporters combined…

India’s rice exports touched a record 21.5 million tons in 2021, more than the combined shipments of the world’s next four biggest exporters of the grain: Thailand, Vietnam, Pakistan and the United States.

Europe certainly isn’t going to make up the difference.

Italy is the biggest rice producer in the European Union, and it is being projected that rice production in that nation will be down about 30 percent this year due to the endless drought that Europe is currently experiencing…

The unfavorable weather has already taken a serious toll on the rice industry. Estimates say farmers are expecting to lose around 30 percent of their yields this year, and the industry has already hemorrhaged around $3 billion as a result of the drought. Many of the most stricken fields are in the regions of Lombardy and Piedmont, which together produce around 90 percent of Italy’s rice.

Rice production is going to be way down in the United States as well.

California usually produces about 20 percent of all U.S. rice, but this year a severe lack of water for agricultural purposes is making things exceedingly difficult for rice growers in the state…

Rice farmers in Colusa County, 60 miles north of Sacramento, received 18% of the federal water shipments to which they are entitled, far less than normal and too little for many to grow the crop at all.

“Even in a drought, rice farmers have been able to get a fairly high percentage of the water they had rights to,” said Tim Johnson, chief executive of the California Rice Commission. “Now they are experiencing drought at a level they’ve never seen before.”

What we are witnessing is truly unprecedented.

I know that this may be hard to believe, but it is being reported that “about 300,000 out of the 550,000 acres committed to rice growing in California will go without harvest” in 2022. The following comes from Zero Hedge…

New satellite imagery shows a large swath of California’s rice fields has been left barren without harvest as fears of a ‘mini dust bowl’ emerge due to diminishing water supplies.

Kurt Richter, a third-generation rice farmer in Colusa, the rice capital of California, told San Francisco Chronicle that fields upon fields of the grain have already transformed into a “wasteland.”

A report via the US Department of Agriculture shows about 300,000 out of the 550,000 acres committed to rice growing in California will go without harvest. This could potentially drive up sushi prices nationwide because most of the rice produced in the state is for just that.

Of course many other crops are being hit extremely hard as well.

California normally produces approximately a third of our vegetables and about two-thirds of our fruits and nuts, and the lack of production this year is already starting to show up on our store shelves…

High temperatures in the Western U.S. are hitting the produce industry, damaging crops, shrinking shipments, and leaving fewer leafy greens and fruits on supermarket shelves.

A California grower said some of his lettuce leaves are turning brown and melting in the fields because of crop diseases intensified by the high temperatures. In Pennsylvania, a retailer said its stores went a week without having strawberries to sell. A New York distributor has substituted honeydew melons for watermelons, which have become scarce.

Supermarkets say they are giving less shelf space to products with weather-induced discolorations, bruises or burns. Stores are cutting prices on poor-quality items to avoid getting stuck with them, and increasingly receiving products from Canada, Florida, New Jersey and Ohio instead of California, long the go-to source for U.S. grocers.

This crisis is only going to get worse in the months ahead.

I have been encouraging my readers to get prepared for a very long time, and I hope that you have taken that advice.

All over the planet, agricultural production is going to be way below original projections this year. For example, just check out what is happening to olive oil production in Spain…

In July, temperatures broke records to top 40 degrees Celsius (104.5 degrees Fahrenheit) across parts of France, Spain, Italy and Portugal. By early August, sweltering heat and a lack of rainfall had pushed almost two-thirds of land in the European Union into drought conditions, according to the European Drought Observatory.

Olive oil producers have been hit hard. Kyle Holland, a pricing analyst for oilseeds and grains at Mintec, a commodities data company, expects a “dramatic reduction” of between 33% and 38% in Spain’s olive oil harvest that begins in October.

Spain is the world’s biggest producer of olive oil, accounting for more than two-fifths of global supply last year, according to the International Olive Council. Greece, Italy and Portugal are also major producers.

For a lot more data points on the rapidly growing global food crisis, please see my previous article entitled “A List Of 33 Things We Know About The Coming Food Shortages”.

None of us have ever faced anything like this.

The food that will not be harvested in the months ahead will not be on our store shelves in 2023.

Food prices are going to rise to absolutely ridiculous levels, and the head of the UN is already warning of “multiple famines” next year.

This is not a drill. Food shortages really are coming, and our world will be changing in wild and unpredictable ways.

END

end

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.9909

OFFSHORE YUAN: 6.9999

SHANGHAI CLOSED: DOWN 37.62 PTS OR 1.16%

HANG SENG CLOSED UP 83.28 PTS OR 0.44%

2. Nikkei closed UP 57.29 PTS OR 0.21%

3. Europe stocks SO FAR: MOSTLY GREEN

USA dollar INDEX DOWN TO 109.35/Euro RISES TO 0.9988

3b Japan 10 YR bond yield: FALLS TO. +.248/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 143.35/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.743%/Italian 10 Yr bond yield RISES to 4.08% /SPAIN 10 YR BOND YIELD FALLS TO 2.89%…

3i Greek 10 year bond yield FALLS TO 4.23//

3j Gold at $1685.80 silver at: 19.37 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 25/100 roubles/dollar; ROUBLE AT 59.64//

3m oil into the 87 dollar handle for WTI and 92 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 143.33DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this .9562– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9552well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.453 UP 4 BASIS PTS

USA 30 YR BOND YIELD: 3.503 UP 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,27

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Fall, Yields Rise Ahead Of Econ Data Onslaught

THURSDAY, SEP 15, 2022 – 07:54 AM

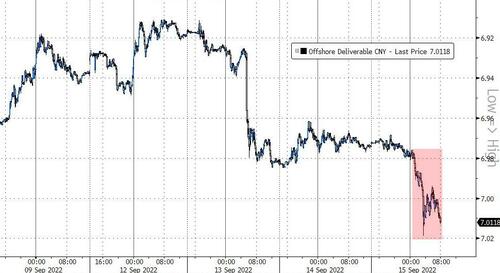

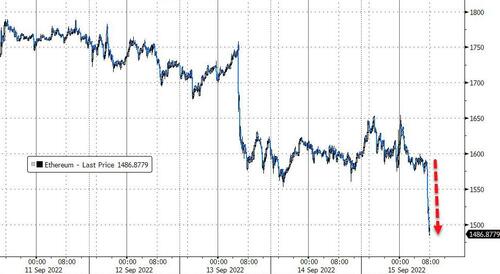

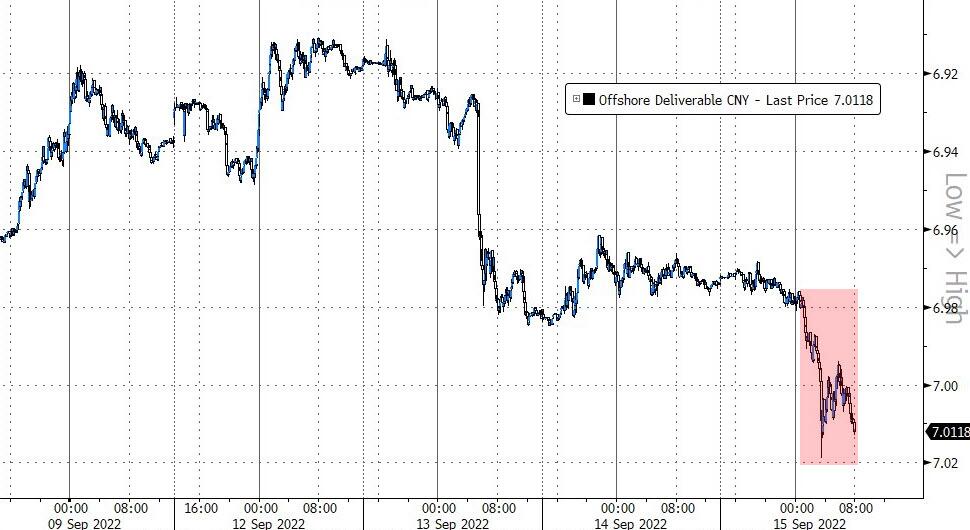

Extremely illiquid US equity futures (top of book depth is between $1-2MM) dropped after trading flat for much of the overnight session, ahead of a packed data slate today including retail sales, industrial production and capacity utilisation for August, the Empire State manufacturing survey and the Philadelphia Fed business outlook for September, and the weekly initial jobless claims, as Treasury and Bund yield rose after Russian energy supplier Gazprom warned that nearly full EU gas inventories can’t guarantee a safe winter with money markets raise tightening wagers, pricing as much as 193bps of ECB hikes by July versus 186bps on Wednesday (and as much as 210bps of Fed hikes by March). As of 7:15am ET, S&P 500 futures slipped 0.1% after a tumultuous few days of trading following the consumer price index reading; Nasdaq 100 futures fell 0.4%. Both underlying indexes had slumped on Tuesday after the report, nearly erasing a four-day rally, before slightly rebounding on Wednesday. European stocks were flat, while the MSCI Asia Pacific Index reversed earlier gains to trade down. The dollar resumed its rise while the yuan dropped below the critically important 7.00 level against the greenback. Ethereum completed the merge and traded around $1600 without any big moves in either direction.

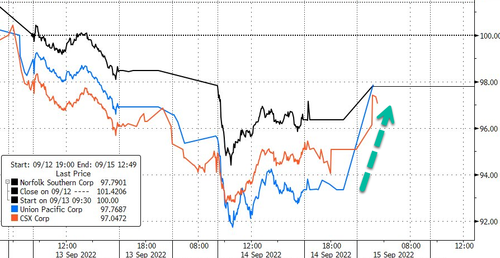

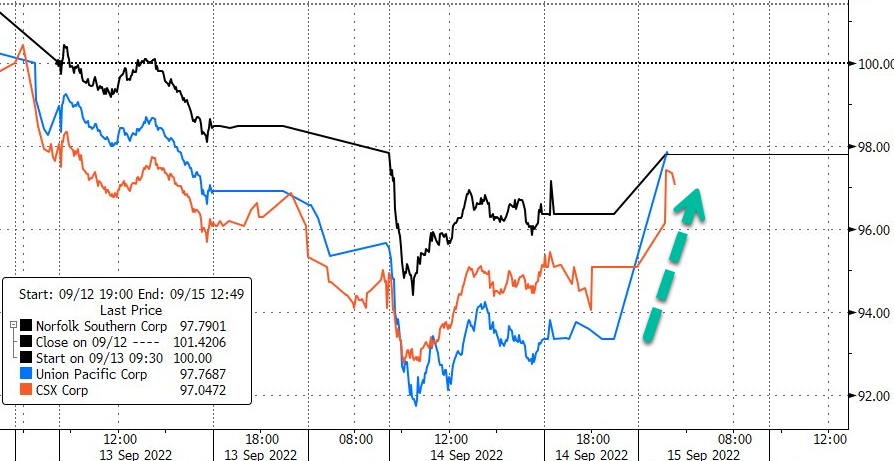

In US premarket trading, Netflix advanced 2.2% after Evercore ISI raised the stock to outperform from in-line, saying that Netflix’s launch of an ad-supported plan is one of the biggest catalysts in the internet sector over the next 12 months. Meanwhile, railway operators Union Pacific Corp and CSX Corp gained after the US government said railroad companies and unions representing more than 100,000 workers reached a tentative agreement in a breakthrough that looks to avert a labor disruption that risked adding supply-chain strains to the world’s largest economy. Here are some other notable premarket movers

- Danaher (DHR US) shares rise 4.2% in premarket trading after the company says it will spin off environmental and applied solutions unit. Analysts responded positively to the news, saying a more streamlined Danaher has potential to unlock value.

- Union Pacific (UNP US) shares rise 4.7% in premarket trading as US railroad companies and unions representing more than 100,000 workers reached a tentative agreement, the government said, a breakthrough that looks to avert a labor disruption.

- Yum China Holdings (YUMC US) shares advance 3.2% in US premarket trading after the Chinese megacity of Chengdu said it had controlled the spread of Covid-19 and would start easing the lockdown.

- Devon Energy (DVN US) declines 1% in premarket trading as the stock was cut to neutral at JPMorgan in note titled ‘E&P Fall Playbook,’ while EOG Resources (EOG US), Permian Resources (PR US) and Vermilion Energy (VET CN) shares were upgraded.

- Watch US cryptocurrency-exposed stocks as digital tokens traded in tight ranges Thursday while Ethereum completed the crypto world’s biggest and most ambitious software upgrade to date. Keep an eye on shares including Coinbase (COIN US), Marathon Digital (MARA US), Riot Blockchain (RIOT US), Ebang (EBON US).

- Watch department store shares as Jefferies says there are still selective opportunities within the sector, upgrading Nordstrom (JWN US) to buy and downgrading Kohl’s (KSS US) to hold.

- Keep an eye on hotel operators as Berenberg upgraded Marriott (MAR US), Hyatt (H US) and Hilton Worldwide (HLT US) shares to buy, saying the accelerating recovery in lodging performance hasn’t yet been reflected in share prices of these companies.

- Watch Phillips 66 (PSX US) stock as it was cut to peer perform at Wolfe, which said that competitors are better positioned to deliver catalysts for shareholder returns.

Traders have been extremely focused on US economic data, with a decline in producer prices providing some relief after Tuesday’s consumer inflation jolt saw wagers for rate increases ratchet higher and stocks slump the most in two years. Investors are now bracing for the Fed’s meeting next week, with some concerned that the central bank can hike rates by as much as 100 basis points. Meanwhile, all eyes will be on fresh jobs, manufacturing and retail numbers later Thursday for further clues on the path of monetary policy.

“It still seems unlikely the Fed will go by more than 75 basis points at this point despite the collective freakout of the past couple of days,” said Michael Hewson, chief market analyst at CMC Markets UK. Retail sales figures “could reinforce this hawkish narrative if we get another strong number.”

Swaps traders are pricing in a 75 basis point hike when the Fed meets next week, with odd for a full-point move dropping to 20% from almost 50% two days ago, after JPM said that it is unlikely that the Fed will rise a full percent. The continued rise in rate-sensitive Treasuries deepened the curve inversion to a level unseen this century.

Meanwhile, Bridgewater’s Ray Dalio came out with a gloomy prediction for stocks and the economy. A mere increase in rates to about 4.5% would lead to a nearly 20% plunge in equity prices, he wrote in a LinkedIn article dated Tuesday, which is odd since the market is already pricing in rates rising to well over 4%. But then again “cash is trash” or something…

“Markets seem torn between a bearish sentiment on one hand, supported by lingering macro threats in a tighter liquidity environment, and dip buyers on the other who continue to bet on the inflation peak,” said Pierre Veyret, an analyst at ActivTrades. “Most benchmarks aren’t registering strong and significant bullish corrections following Tuesday’s sell-off, but continue to trade sideways in a volatile manner, which highlights the ‘wait and see’ situation ahead of today’s new batch of US data, tomorrow’s EU CPI report and next week’s Fed decision on rates.”

In Europe, the Stoxx 50 index rose 0.2%. FTSE 100 outperforms peers, adding 0.5%, CAC 40 underperforms. Banks, miners and health care are the strongest-performing sectors. European banks rose to a three-month high on Thursday, with Spanish banks among the best performers after a local website said the government is open to modifying the tax it plans to impose on windfall profits. Also boosting sentiment on the sector, Morgan Stanley upgraded its view on European banks to attractive

Earlier in the session, Asian stocks extended their recent weakness as investors remained cautious over tighter Federal Reserve policy, with losses in China weighing on the regional benchmark. The MSCI Asia Pacific Index erased earlier gains to fall as much as 0.4%, on track to fall for a third day. Financials and energy shares advanced the most, while technology stocks were the biggest drag. Chinese stocks led declines in the region as a meeting between President Xi Jinping and Vladimir Putin nears, an event that traders say raises geopolitical risks. Meanwhile, the People’s Bank of China’s kept its key rate unchanged while draining liquidity from the banking system. An easing of lockdown in the Chinese megacity of Chengdu was insufficient to provide reassurance. Asian markets were jittery ahead of the Fed’s policy decision next week, though a month-on-month decline in US producer prices offered some relief. Traders are expecting an outsized interest rate increase by the Fed to curb persistent inflation.

“Overall risk sentiments will continue to carry a cautious tone,” Jun Rong Yeap, a market strategist at IG Asia Pte, wrote in a note. “The absence of any clear resolution in China’s Covid-19 policy and uncertainty on further moderation in economic conditions ahead remain a weighing block for risk sentiments.” Markets in Japan, Australia and Hong Kong were among those in the green.

Japanese equities edged higher as investors assess the Fed’s hawkish stance and await further data that would provide clearer signals on the direction of the global economy. The Topix Index rose 0.2% to close at 1,950.43, while the Nikkei advanced 0.2% to 27,875.91. Sony Group Corp. contributed the most to the Topix Index gain, increasing 0.9%. Out of 2,169 stocks in the index, 1,100 rose and 926 fell, while 143 were unchanged. “US stocks have calmed down and there is a sense of relief buying,” said Masayuki Otani, a chief market strategist at Securities Japan. “But there is still a wait-and-see mood ahead of next week’s FOMC meeting and US retail sales to be announced tonight, Japan time.”

Australia’s S&P/ASX 200 index rose 0.2% to close at 6,842.90, boosted by gains in energy shares and banks. Australian unemployment unexpectedly rose in August, the first increase in 10 months, a result that supports the Reserve Bank’s signal of a potential shift to smaller interest-rate increases. In New Zealand, the S&P/NZX 50 index was little changed at 11,658.94. Shares of Wellington-listed Pushpay fell 11%, after a report that a pending buyout of the digital payments firm may be nearing collapse.

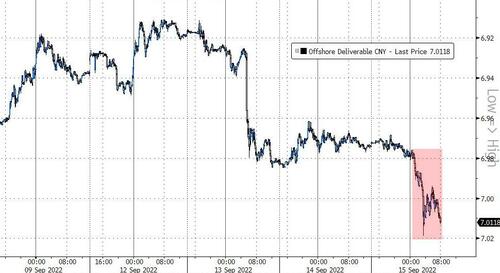

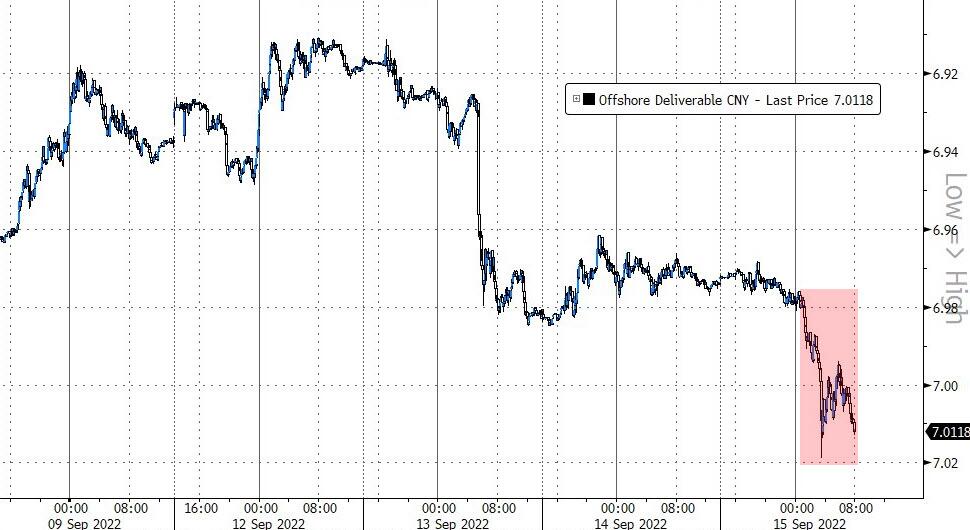

In Fx, the Bloomberg dollar spot index is flat. NOK and JPY are the weakest performers in G-10 FX, as CHF and EUR outperform. Asian currencies remained at risk from a strong greenback. The offshore yuan weakened above 7 per dollar for the first time since July 2020. The yen declined to trade around 143.6 per dollar after it rallied away from just under the closely-watched 145 level Wednesday on signs the Bank of Japan was preparing an intervention. Ominously, despite the plunge in the yen, Japan’s trade hit a record deficit in August.

- The euro traded little changed, slightly below parity against the dollar.

- The pound led G-10 losses, with focus turning to next week’s Bank of England decision. Demand for one- week sterling-dollar downside protection covering the BOE meeting is around the least since before the Feb. decision, perhaps reflecting the drop in spot. Cable one-week implied volatility touches 14.5%, a level unseen since Sept. 9, when the meeting was delayed

- The yen fell as wariness over potential FX intervention from Japan receded, undermined by Japan’s trade deficits and expectations the US Fed will retain its hawkish stance. The government bond yield curve steepened after a weak 20-year auction

- Japan’s unadjusted trade deficit expanded to 2.82 trillion yen ($19.7 billion) last month, the finance ministry reported Thursday. The gap was far larger than economists’ estimates and extends the sequence of red ink to 13 months, the longest stretch since 2015

- Australia’s sovereign bonds extended opening declines after a government report showed employers added workers last month, even as the jobless rate rose. The Aussie traded in a tight range

In rates, Treasury futures traded near session lows after grinding lower during Asia session and European morning, leaving yields cheaper by about 5bp across long-end of the curve. US 10-year yields trade around 3.45%, cheaper by nearly 5bp vs Wednesday’s close; front-end outperforms slightly; 2-year German yields cheaper by 8bp on the day following hawkish remarks by ECB policy makers Holzmann and Kazaks late Wednesday. US session features packed economic data slate headed by retail sales. Corporate bond sales may go forward after some issuers stood down over past two days.

European bonds slipped: Bunds, Italian bonds fell as money markets wagered on a faster ECB tightening pace following hawkish remarks from policy makers Holzmann and Kazaks late Wednesday. Bund yields rise between 4-2bps across the curve. Gilts outperform bunds and USTs. Treasury 10-year yield up 3.8bps to 3.44%.

In commodities, oil fluctuated as traders grappled with concerns about global demand and assessed comments from the US on refilling strategic reserves. WTI trades within Wednesday’s range, falling 0.2% to near $88.33. Natural gas increased as traders assessed Europe’s steps to contain the energy crisis, with governments making plans to shut down power in some places to avoid a total collapse of the system this winter. Spot gold falls roughly $10 to trade near $1,687/oz. Spot silver loses 1.1% to around $19.

Bitcoin meanders around USD 20k and Ethereum fell under USD 1.6k after completing the Ethereum Merge.

To the day ahead now, and data releases from the US include retail sales, industrial production and capacity utilisation for August, the Empire State manufacturing survey and the Philadelphia Fed business outlook for September, and the weekly initial jobless claims. From central banks, we’ll hear from ECB Vice President de Guindos and the ECB’s Centeno. Lastly, earnings releases include Adobe.

Market Snapshot

- S&P 500 futures little changed at 3,949.25

- STOXX Europe 600 up 0.2% to 418.54

- MXAP down 0.3% to 152.10

- MXAPJ down 0.2% to 499.22

- Nikkei up 0.2% to 27,875.91

- Topix up 0.2% to 1,950.43

- Hang Seng Index up 0.4% to 18,930.38

- Shanghai Composite down 1.2% to 3,199.92

- Sensex down 0.5% to 60,020.39

- Australia S&P/ASX 200 up 0.2% to 6,842.89

- Kospi down 0.4% to 2,401.83

- German 10Y yield little changed at 1.75%

- Euro little changed at $0.9980

- Gold spot down 0.5% to $1,688.07

- U.S. Dollar Index little changed at 109.73

Top Overnight News from Bloomberg

- Shortly before invading Ukraine in February, Vladimir Putin and Xi Jinping declared a “no limits” friendship. Yet even as Russian forces suffer humiliating losses on the battlefield, Putin shouldn’t expect much help from Xi at their first meeting since the invasion

- China is considering allowing its oil refiners to export more fuel in an attempt to revive its economy, in what would be a reversal from a focus on minimizing emissions

- Investors in high-risk emerging-market debt are finally seeing positive returns as fears of an economic meltdown ease. In a reversal of fortunes from the first half of the year, junk- rated emerging corporate and sovereign bonds in dollars have returned 7.2% in the past two months, according to Bloomberg indices. That follows a brutal 18% slide until June, marking the worst year since the 2008 credit crisis

- Germany will likely face “waves” of gas shortages this winter, Klaus Mueller, president of the country’s energy regulator, told Handelsblatt in an interview published on Thursday

- Swedish long-term inflation expectations staying put in July offered a rare piece of good news for the country’s central bank, which looks set to step up interest-rate hikes after a string of higher-than-expected inflation outcomes

- Swedish right-wing opposition parties are intensifying negotiations on forming a new government, after Prime Minister Magdalena Andersson announced her resignation on Wednesday

A more detailed look at global markets courtesy of Newsquawk

Asia stocks mostly traded with mild gains after the slight reprieve on Wall Street where inline PPI data provided some solace from inflationary woes, although mixed data and hawkish central bank expectations scuppered a broad recovery. ASX 200 was led higher by outperformance in energy and financials but with upside capped after the miss on jobs data. Nikkei 225 eked mild gains as expectations of looming stimulus and looser border controls offset the mixed trade data. Hang Seng and Shanghai Comp were mixed despite the latest policy support pledges by China including an extension of tax reliefs for small firms and a CNY 200bln relending facility by the PBoC, while the easing of lockdown restrictions in some cities also failed to spur risk appetite as participants digest the PBoC MLF announcement in which it partially rolled over maturing loans and maintained the rate at 2.75%, as expected.

Top Asian News

- PBoC injected CNY 400bln vs CNY 600bln maturing via 1-year MLF with the rate kept at 2.75%.

- PBoC set USD/CNY mid-point at 6.9101 vs exp. 6.9153 (prev. 6.9116).