GOLD; $1715.70 UP $13.70

SILVER: $18.34 UP 34 CENTS

ACCESS MARKET:

GOLD $1718.30

SILVER: $18.47

Bitcoin morning price: $18,756 DOWN 1229

Bitcoin: afternoon price: $19,129 DOWN 853

Platinum price closing UP $16.30 AT $868.20

Palladium price; closing UP $16.30 at $2046.75

END

DONATE

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,700.400000000 USD

INTENT DATE: 09/06/2022 DELIVERY DATE: 09/08/2022

FIRM ORG FIRM NAME ISSUED STOPPED

132 C SG AMERICAS 18

435 H SCOTIA CAPITAL 20

657 C MORGAN STANLEY 2

661 C JP MORGAN 101

690 C ABN AMRO 5

709 C BARCLAYS 141

737 C ADVANTAGE 16 8

800 C MAREX SPEC 2 2

905 C ADM 3

TOTAL: 159 159

MONTH TO DATE: 2,094

JPMorgan stopped: 101/159

_____________________________________________________________________________________

GOLD: NUMBER OF NOTICES FILED FOR SEPT CONTRACT:

159 NOTICES FOR 15900 OZ //0.4945 TONNES

total notices so far: 2094 contracts for 209,400 oz (6.5132 tonnes)

SILVER NOTICES: 66 NOTICES FILED FOR 330,000 OZ/

total number of notices filed so far this month 5948 : for 29,740,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $13.40

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//

INVENTORY RESTS AT 971.05 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $.34

AT THE SLV// ://BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 0.830 MILLION OZ FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 467.419 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL SIZED 198 CONTRACTS TO 138,300. AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE HUGE LOSS IN OI WAS ACCOMPLISHED WITH OUR $0.01 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.13) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC SILVER LONGS AS WE HAD A HUGE GAIN OF 1687 CONTRACTS ON OUR TWO EXCHANGES,; WE HAD MINOR SPECULATOR LIQUIDATION.

WE MUST HAVE HAD:

I) SOME// SPECULATOR SHORT LIQUIDATIONS ////CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 215,000 OZ QUEUE JUMP / // V) SMALL SIZED COMEX OI GAIN/(//SOME SPEC LIQUIDATION/)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: –86

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTACTS for 4 days, total 4751 contracts: 23.755 million oz OR 5.938 MILLION OZ PER DAY. (1187 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 23.755 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 23.755 MILLION OZ///

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 198 WITH OUR $0.01 GAIN IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 1020 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /SOME BANKER ADDITIONS A// MINOR SPEC SHORT LIQUIDATIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 215,000 OZ QUEUE JUMP // .. WE HAD A STRONG SIZED GAIN OF 1304 OI CONTRACTS ON THE TWO EXCHANGES FOR 6.520 MILLION OZ AS..THE SPECS STILL BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 66 NOTICE(S) FILED TODAY FOR 330,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 2466 CONTRACTS TO 465,908 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY:–685 CONTRACTS.

.

THE FAIR SIZED INCREASE IN COMEX OI CAME DESPITE OUR STRONG FALL IN PRICE OF $9.40//COMEX GOLD TRADING/TUESDAY / WE MUST HAVE HAD STRONG SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND /STRONG SPECULATOR SHORT COVERINGS//CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 8.401 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG JUMP OF 400 OZ //NEW STANDING 11.216 TONNES

YET ALL OF..THIS HAPPENED WITH OUR STRONG FALL IN PRICE OF $9.40 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 4990 OI CONTRACTS 15.52 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2524 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 465,908

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4990 CONTRACTS WITH 2466 CONTRACTS INCREASED AT THE COMEX AND 2524 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 4990 CONTRACTS OR 17.651 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2524) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (2466): TOTAL GAIN IN THE TWO EXCHANGES 5675 CONTRACTS. WE NO DOUBT HAD 1) STRONG SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 8.409 TONNES FOLLOWED BY TODAY’S QUEUE. JUMP OF 400 oz. 3) ZERO LONG LIQUIDATION//// //.,4) FAIR SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

11,022 CONTRACTS OR 1,102,200 OZ OR 34.28 TONNES 4 TRADING DAY(S) AND THUS AVERAGING: 2755 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 4 TRADING DAY(S) IN TONNES: 34.28 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 34.28/3550 x 100% TONNES 0.95% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 34.28 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT., FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A SMALL SIZED 198 CONTRACT OI TO 138,300 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1020 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 1020 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1020 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 198 CONTRACTS AND ADD TO THE 1020 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 1218 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 6.090 MILLION OZ

OCCURRED WITH OUR GAIN IN PRICE OF $0.01

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 2.85 PTS OR 0.09% //Hang Sang CLOSED DOWN 158.43 OR 0.82% /The Nikkei closed DOWN 196.21 OR .71%. //Australia’s all ordinaires CLOSED DOWN 1.37% /Chinese yuan (ONSHORE) closed DOWN AT 6.9782//OFFSHORE CHINESE YUAN DOWN 6.9943// /Oil DOWN TO 87.09 dollars per barrel for WTI and BRENT AT 92,81 / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 2466 CONTRACTS TO 465,908 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR FALL IN PRICE OF $9.40 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2524 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2524 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :2524 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2524 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED SIZED TOTAL OF 4990 CONTRACTS IN THAT 2524 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF24662 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $9.40. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING SEPT (11.216),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 11.216 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $9.40) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A GOOD SIZED TOTAL GAIN ON OUR TWO EXCHANGES // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS COVERED SOME OF THEIR POSITIONS////// WE HAVE REGISTERED A GOOD SIZED GAIN OF 17.651 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR SEPT. (11.216 TONNES)…

WE HAD -685 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 5675 CONTRACTS OR 567500 OZ OR 17,651 TONNES

Estimated gold volume 168,030/// poor/

final gold volumes/yesterday 219,015/ poor

INITIAL STANDINGS FOR SEPT ’22 COMEX GOLD //SEPT 7

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 126,309.158 oz Brinks Manfra (771 kilobars) |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 35,741.224 oz Loomis |

| No of oz served (contracts) today | 159 notice(s) 15900 OZ 0.4945 TONNES |

| No of oz to be served (notices) | 1512 contracts 151,200 oz 4.702 TONNES |

| Total monthly oz gold served (contracts) so far this month | 2094 notices 209,400 OZ 6.5132 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i) Into Loomis: 35,741.224 oz

total deposits 35,741.224 oz

2 customer withdrawals:

i) Out of Brinks 101,520.737

ii) Out of Manfra: 24,788.421 oz (771 kilobars)

total: 126,309.158 oz

total in tonnes: 3.928 tonnes

Adjustments: 1

jpmorgan: 16,686.342 oz dealer to customer

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPT.

For the front month of SEPT we have an oi of 1671 contracts having LOST121 contracts .

We had 125 notices filed on TUESDAY so we gained 4 contracts or an additional 400 oz

will stand for gold in this very non active delivery month of September.

October GAINED 495 contracts UP to 42,703

November GAINED 0 contracts to stand at 6

December GAINED 953 contracts UP to 379,273.

We had 159 notice(s) filed today for 15,900 oz FOR THE SEPT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 159 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 101 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2022. contract month,

we take the total number of notices filed so far for the month (2094) x 100 oz , to which we add the difference between the open interest for the front month of (SEPT 1671 CONTRACTS ) minus the number of notices served upon today 159 x 100 oz per contract equals 360,600 OZ OR 11.216 TONNES the number of TONNES standing in this NON active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month:

No of notices filed so far (2094) x 100 oz+ (1671) OI for the front month minus the number of notices served upon today (159} x 100 oz} which equals 360,600 oz standing OR 11.216 TONNES in this NON active delivery month of SEPTEMBER.

TOTAL COMEX GOLD STANDING: 11.216 TONNES (A GREAT STANDING FOR A SEPT ( NON ACTIVE) DELIVERY MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,363,363.815 oz 73.508 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 27,629,782.094 OZ

TOTAL REGISTERED GOLD: 13,644,286.297 OZ (424.39 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 13,985.494.797 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 11,280,923. OZ (REG GOLD- PLEDGED GOLD) 350.88 tonnes//rapidly declining

END

SILVER/COMEX/SEPT 7

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 104,090.460 oz CNT DELAWARE |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 467,315.300 oz Delaware |

| No of oz served today (contracts) | 66 CONTRACT(S) 330,000 OZ) |

| No of oz to be served (notices) | 284 contracts (1,420,000 oz) |

| Total monthly oz silver served (contracts) | 5948 contracts 29,740,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) Into Delaware: 467,315.300 oz

total deposit: 467,315.300 oz

JPMorgan has a total silver weight: 168.702 million oz/325.521million =51.89% of comex

Comex withdrawals:2

i) Out of CNT: 101,095.560 oz

ii) Out of Delaware: 2994.900 oz

total: 104,090.460 oz

adjustments: 1/dealer to customer

JPMorgan: 14,928.660 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 47.449 MILLION OZ

TOTAL REG + ELIG. 325.519 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF SEPT OI: 350 CONTRACTS HAVING LOST 137 CONTRACTS. WE HAD

180 CONTRACTS SERVED ON TUESDAY SO WE GAINED 43 CONTRACTS OR AN ADDITIONAL

215,000 OZ WILL STAND FOR METAL IN THIS VERY ACTIVE MONTH OF SEPT.

WE WILL GAIN IN TOTAL SILVER STANDING EACH TRADING DAY UNTIL THE END OF THE MONTH

(CONTINUAL QUEUE JUMPING BY OUR BANKERS SEARCHING FOR SILVER METAL)

OCTOBER GAINED 11 CONTRACTS TO STAND AT 679 CONTACTS.

NOVEMBER GAINED 9 CONTRACTS TO STAND AT 12

DECEMBER SAW A GAIN OF 97 CONTRACTS UP TO 125,668.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 66 for 330,000 oz

Comex volumes:46.682// est. volume today// fpoor

Comex volume: confirmed yesterday: 76,669 contracts ( good)

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 5948 x 5,000 oz = 29,740,000 oz

to which we add the difference between the open interest for the front month of SEPT(350) and the number of notices served upon today 66 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT./2022 contract month: 5,948 (notices served so far) x 5000 oz + OI for front month of SEPT (350) – number of notices served upon today (66) x 5000 oz of silver standing for the SEPT contract month equates 31,160,000 oz. .

We have an inventory of 47.464 million oz of registered silver at the comex so Sept delivery of 31.160 MILLION OZ represents 65.400% of that category of silver.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:71,745// est. volume today// fair

Comex volume: confirmed yesterday: 66,045 contracts ( fair)

END

GLD AND SLV INVENTORY LEVELS

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

AUGUST 31.WITH GOLD DOWN $10.20:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.24 TONNES FROM THE GLD////INVENTORY RESTS AT 973.37 TONNES

AUGUST 30.WITH GOLD DOWN $12.00:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 980.61 TONNES

AUGUST 29/WITH GOLD DOWN $.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD/////INVENTORY RESTS AT 982.64 TONNES

AUGUST 26/WITH GOLD DOWN $26.60; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 25/WITH GOLD UP $9.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 18/WITH GOLD DOWN $5.25: GIGANTIC CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.78 TONNES FROM THE GLD////INVENTORY RESTS AT 985.83 TONNES

AUGUST 17/WITH GOLD DOWN $12.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 992.20 TONNES

AUGUST 16/WITH GOLD DOWN $7.85: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 993.94 TONNES

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

AUGUST 10//WITH GOLD UP $2.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES

AUGUST 9/WITH GOLD UP $6.70: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES.

AUGUST 8/WITH GOLD UP $13.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FORM THE GLD//INVENTORY RESTS AT 999.16 TONNES

AUGUST 5/WITH GOLD DOWN $14.25: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .33 TONNES FROM THE GLD////INVENTORY RESTS AT 1000.32 TONNES

AUGUST 4 WITH GOLD UP $29.00 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES FROM THE GLD///INVENTORY REST AT 1000.65 TONNES

AUGUST 2/WITH GOLD UP $3.70; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD//INVENTORY RESTS AT 1002.97 TONNES//

AUGUST 1/WITH GOLD UP $5.75: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1005.87 TONNES

GLD INVENTORY: 971.05 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

AUGUST 31/WITH SILVER DOWN 36 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 3.087 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 465.573 MILLION OZ//

AUGUST 30/WITH SILVER DOWN 34 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 1.478 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 470.135 MILLION OZ//

AUGUST 29/WITH SILVER DOWN 7 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY A THE SLV: A WITHDRAWAL OF 2.765 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 470.135 MILLION OZ//

AUGUST 26/WITH SILVER DOWN 39 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 25/WITH SILVER UP 21 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

AUGUST 18/WITH SILVER DOWN 27 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 369,000 OZ INTO THE SLV////INVENTORY RESTS AT 485.482 MILLION OZ//

AUGUST 17/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.106 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.113 MILLION OZ//

AUGUST 16/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 486.219 MILLION OZ/

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 10/WITH SILVER UP 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 9/WITH SILVER DOWN 25 CENTS TODAY: TWO CHANGES IN SILVER INVENTORY AT THE SLV: FIRST: A DEPOSIT OF 461,000 OZ INTO THE SLV AND THEN A WITHDRAWAL OF 1.014 MILLION OZ..//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 8/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 5/WITH SILVER DOWN 28 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 922,000 OZ FROM THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 4 WITH SILVER UP 21 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 527,000 OZ FROM THE SLV////INVENTORY RESTS AT 486.634 MILLION OZ

AUGUST 2/WITH SILVER DOWN 21 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.504 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.161 MILLION OZ//

AUGUST 1/WITH SILVER UP 17 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE GLD: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 483.657 MILLION OZ//

CLOSING INVENTORY 467.419 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

GOLD/SILVER

END

3.Chris Powell of GATA provides to us very important physical commentaries

A little late but a well worthwhile paper

(Alasdair Macleod)

Alasdair Macleod: Supply chain breakdown will worsen the inflationary storm

Submitted by admin on Tue, 2022-09-06 13:07Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Tuesday, September 6, 2022

The disruption of global supply chains is seen to be a temporary problem yet to be resolved, but there are good reasons to believe it is now permanent.

Following the end of the cold war against China and the foundation of a new peaceful era, American and other manufacturers began to expand their production facilities into China and Southeast Asia. It was the beginning of what became a trade system based on global supply chains, increasingly sophisticated logistics, and just-in-time inventory management.

Global supply chains deliver enormous benefits between peaceful nations, but they cease to work when they are at war.

Souring trade relations between America and China, covid, and the disruption to international logistics pits them into an undeclared conflict. The trade environment is now against a background of an increasingly belligerent geopolitical struggle, involving both China and Russia on one side, and America and its allies on another. In the absence of détente, which now seems a distant prospect, the system of global supply chains can operate no longer. They must become re-established within national borders.

The consequences are long-term product supply disruption, higher consumer prices, and soaring energy prices already evidenced in Europe. Coming on top of a new trend of rising interest rates and contracting bank credit, it has the makings of an economic crisis for the West, to which governments are bound to respond by creating an inflationary storm.

This article analyses these new war-time trade conditions in the geopolitical context and examines the likely consequences. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/supply-chains-interest-rates-and-inflation?gmrefcode=gata

end

END

4. OTHER GOLD/SILVER COMMENTARIES

-END-

.

end

5.OTHER COMMODITIES:

COMMODITIES IN GENERAL/COAL

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.9782

OFFSHORE YUAN: 6.9943

HANG SENG CLOSED DOWN 158,43 PTS OR 0.82%

2. Nikkei closed DOWN 196.21 OR 0.71%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 110.68/Euro FALLS TO 0.98803

3b Japan 10 YR bond yield: RISES TO. +.244/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 144.97/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.587%/Italian 10 Yr bond yield FALLS to 3.88% /SPAIN 10 YR BOND YIELD RISES TO 2.75%…

3i Greek 10 year bond yield FALLS TO 4.12//

3j Gold at $1701.55 silver at: 18.13 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 15/100 roubles/dollar; ROUBLE AT 61.08//

3m oil into the 87 dollar handle for WTI and 92 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 144.97DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 9856– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9737well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.346 UP 1 BASIS PTS

USA 30 YR BOND YIELD: 3.491 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,23

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Flat, Dollars Steamrolls To New Record Highs Ahead Of Fed Speaker Barrage

WEDNESDAY, SEP 07, 2022 – 07:52 AM

S&P futures swung in illiquid overnight trading, first sliding below the key 3,900 level after the Japan open, only to recover all losses after Europe opened, with the dollar storming to new record highs and steamrolling all FX competitors as traders braced for a slew of hawkish Fed speakers to assess the path of monetary policy and its impact on the economy. S&P 500 futures edged 0.1% higher at 7:15 a.m. in New York after the underlying benchmark fell six out of the last seven sessions, while Nasdaq 100 futures rose 0.3%, as both European and Asian market slumped. The Bloomberg Dollar index hit a new record high as the Yen plunge below 144 for the first time since 1998 and the Chinese yuan flirted with the key 7.00 level. Bitcoin recovered modestly after tumbling to new 2022 lows and oil erased a decline after Russian President Vladimir Putin underlined that his country won’t supply oil and fuel if price caps on the country’s exports are introduced..

In premarket trading, UiPath tumbled 21% after the application software company gave weaker-than-expected third-quarter revenue forecast. Meanwhile, Gitlab gained 3% in US premarket trading after second-quarter earnings. While analysts were broadly positive on the software development platform’s increased revenue guidance, especially given a tough backdrop, Piper Sandler flagged “noise” around a deceleration in billings. Here are the other notable premarket movers:

- Coupa Software (COUP US) rises about 12% in premarket trading on Wednesday after boosting its full-year earnings guidance and posting better-than-expected second-quarter results, helped by strong billings in North America. While analysts were positive about the results, they remained cautious about softness in Europe.

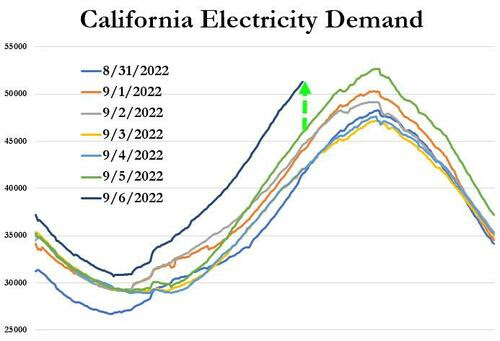

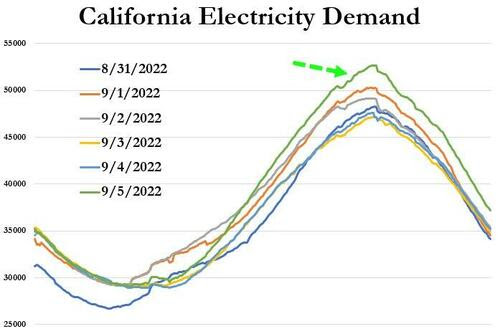

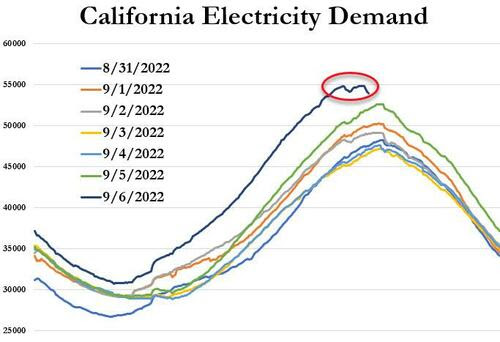

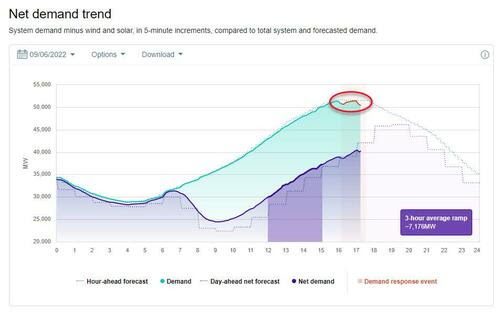

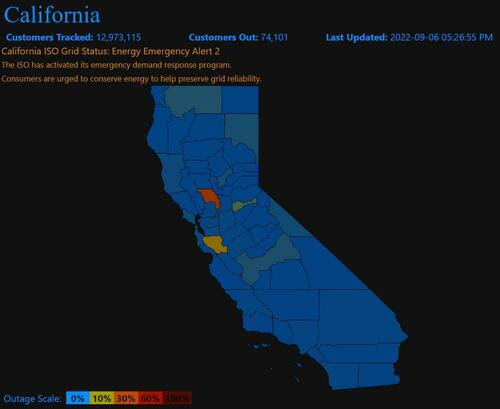

- Keep an eye on shares in US utilities and energy suppliers, incuding PG&E (PCG US), Edison International (EIX US) and Sempra Energy (SRE US) amid a deepening power crisis in California, where a heat wave is piling pressure on the US state’s power grid.

- Watch US digital health companies, as Truist initiates coverage on 16 firms, with a positive view on the industry overall. Progyny (PGNY US), Privia Health (PRVA US), Accolade (ACCD US), Agilon (AGL US) and R1 RCM (RCM US) all started with buy ratings.

- Watch Petco (WOOF US) stock as it was initiated with an outperform rating and $17 PT at RBC, with the broker saying near-term risks are reflected in the shares and the long-term picture is positive for the pet health company.

- Keep an eye on Guidewire (GWRE US) as RBC Capital Markets says that the software company has reported a “mixed” quarter amid macroeconomic headwinds with “muted” guidance.

- Alvotech (ALVO US) stock may be in focus as it was initiated with an equal-weight rating at Morgan Stanley, with broker flagging “many knowns” and a wide range of possible outcomes of the biotech’s US launch of its lead product, the biosimilar Humira.

- Newell Brands (NWL US) fell 4.6% in US postmarket trading on Tuesday after the consumer-products company cut its normalized earnings per share guidance for the full year. The firm has “limited” visibility and is buffeted by macroeconomic pressures, Morgan Stanley says.

On today’s calendar, no less than four Fed officials including Vice Chair Lael Brainard and Cleveland President Loretta Mester are set to speak before the release of the US Beige book later this afternoon. Richmond President Thomas Barkin already said rates must stay high until inflation eases. Investors will closely monitor their comments for clues about the pace of interest rate hikes in the face of slowing growth and still-elevated inflation. The consumer-price index reading due next week will also be paramount for the Fed’s September decision. Bets on another 75 basis points Fed interest-rate hike to tackle high inflation have spurred a selloff in Treasuries, while traders are bracing for a European Central Bank rates decision due on Thursday, with the potential for a similar-size move.

Aside from tightening monetary settings and an apparently unstoppable dollar, markets are also contending with a debilitating energy crisis in Europe and Covid lockdowns in China. Concerns are growing about the outlook for company earnings given the various global economic headwinds and a rebound seen in equity markets since mid-June is fading.

The S&P 500 rose too much in July and is overvalued by about 10% compared to macroeconomic fundamentals, according to Joachim Klement, head of strategy, accounting and sustainability at Liberum Capital. He expects the Federal Reserve to hike rates by 75 basis points even if inflation declined in August. “The current wait-and-see mode of the US market should be short-lived,” he said. “We expect another leg down in the S&P 500 into the fourth quarter before we find a bottom.”

“At this point, we see no positive triggers to keep the rally going, while there are rising risks moving into autumn amid a gloomier economic backdrop,” Amundi SA Chief Investment Officer Vincent Mortier and his deputy, Matteo Germano, wrote in a note. “To cope with this environment, we believe investors should adjust their asset allocation stances.”

Europe’s Stoxx 600 Index fell 0.4%, with tumbling miners leading the declines; IBEX outperforms, adding 0.4%, FTSE 100 lags, dropping 0.7%. Banks, miners and retailers are the worst-performing sectors.

Earlier in the session, Asiun stocks were pressured amid spillover selling from Wall St owing to the higher yield environment and as participants digested the latest Chinese trade data. ASX 200 weakened from the open with the index dragged lower by the energy and mining-related sectors and with somewhat mixed GDP data not doing much to spur risk appetite. Hang Seng and Shanghai Comp were subdued amid the ongoing COVID woes and following the softer than expected Chinese trade data in which all metrics missed forecasts.

Japanese stocks also fell as the yen slumped to a level that leaves it on track for its worst year on record, prompting government warnings and putting traders on edge as volatility rises. The Topix Index fell 0.6% to 1,915.65 as of market close Tokyo time, while the Nikkei declined 0.7% to 27,430.30. Sony Group Corp. contributed the most to the Topix Index decline, decreasing 2.3%. Out of 2,169 stocks in the index, 492 rose and 1,610 fell, while 67 were unchanged. While currency weakness is generally seen as favorable for exporters, rapid depreciation raises input costs and can complicate business decisions. “With the yen this weak, it’s difficult for the stock market to rally,” said Ayako Sera, a market strategist at Sumitomo Mitsui Trust Bank Limited.

In Australia, the S&P/ASX 200 index fell 1.4% to close at 6,729.30, dragged by declines in banks and mining shares. Energy-related shares fell after oil retreated to the lowest level since January on concern a global slowdown will cut demand in Europe and the US just as China’s Covid Zero strategy hurts consumption. In New Zealand, the S&P/NZX 50 index fell 0.4% to 11,548.30.

In India, key equity indexes dropped on Wednesday, tracking a selloff in Asia, with companies such as ICICI Bank and Reliance Industries putting pressure on the market. The S&P BSE Sensex closed 0.3% lower at 59,028.91 in Mumbai, while the NSE Nifty 50 Index fell 0.2%, extending its decline for a second day. Still, all but five of the 19 sector sub-gauges compiled by BSE Ltd. gained, led by an index of basic material companies. Automobile stocks were the worst performers. However, the broader market, including mid- and small-cap companies, gained as basic material stocks advanced on the back of recent decline in commodity prices. The S&P BSE MidCap Index fell as much as 0.5%, before closing higher by an equal measure and climbing to its highest level since Jan. 17.

In FX, the Bloomberg dollar index surged to a fresh record as strong US data and hawkish comments from a Federal Reserve official reinforced aggressive tightening bets. The Bloomberg Dollar Spot Index gained as much as 0.4% fuelling weakness among all of its Group-of-10 peers.

Fed’s Richmond President Thomas Barkin said in an interview with the Financial Times that the central bank must raise interest rates to a level that restrains economic activity and keep them there until policy makers are “convinced” that rampant inflation is subsiding.

- The yen fell to a fresh 24-year low, prompting Japan’s top spokesman Hirokazu Matsuno to say he’s concerned about recent rapid, one-sided moves in the yen and the country would need to take “necessary action” if these movements continue. But despite this verbal intervention, “markets appear quite happy with testing their tolerance” and 145.00 might be the line in the sand, Francesco Pesole, a strategist at ING Groep NV wrote in a note. USD/JPY rose as high as 144.99. The Bank of Japan said it would boost scheduled bond purchases as Japan’s benchmark 10- year yield hit 0.24% — approaching the 0.25% upper limit of the BOJ’s tolerated trading band

- GBP/USD fell 0.4% to 1.1471 erasing gains made after reports of Prime Minister Liz Truss’s energy support package. The pound has managed to “discount much of the bad news but that does not mean that it will bound higher anytime soon,” Steve Barrow, a strategist at Standard Bank wrote in a note.

- AUD/USD lost 0.2% to 0.6722; a drop below the July 14 low of 0.6682 would take it to the lowest since 2020

In rates,Treasuries hold gains, reversing some of Tuesday’s declines, amid a bull-steepening rally in gilts where 2-year yields are richer by around 25bp on the day as BOE speakers discuss inflation outlook amid proposed government action. US yields richer by 2bp to 4bp across the curve with gains led by front-end, steepening 2s10s spread by around 1bp; 10-year yields at 3.33%, richer by 2.5bp and underperforming bunds and gilts in the sector by 3.5bp and 6bp.Sharp bull-steepening in gilts follows dovish comments from BOE’s Tenreyro; UK 2s10s, 5s30s spreads widen 8bp and 7bp into the front-end led rally.Fed speaker slate includes Vice Chair Brainard on the economic outlook; Chair Powell has an appearance scheduled for Thursday; August CPI report to be released Sept. 13 falls during the blackout period.IG dollar issuance slate includes IFC $2b 3Y SOFR and IADB 7Y SOFR; more than $35b priced Tuesday with issuers paying just over 10bps in concessions on deals 2.8x covered, and at least three borrowers stood down.

WTI crude drifts 0.6% higher to trade near $87.38 after Putin said Russia won’t supply oil, fuel or gas if price caps are introduced; gold adds about ~$3 to $1,705. Bitcoin prices slipped overnight to under USD 19,000 whilst Ethereum tested 1,500 to the downside; and gold recovered to trade above $1,700 an ounce.

To the day ahead now, and there’s plenty on the central bank side, as the Bank of Canada announce their latest policy decision and the Fed release their Beige Book. We’ll also hear from Bank of England Governor Bailey, as well as the BoE’s Pill, Mann and Tenreyro as they testify before the Treasury Select Committee. In addition, there are scheduled remarks Fed officials, including Vice Chair Brainard, Vice Chair Barr, and Mester and Barkin. Otherwise, data releases include German industrial production and Italian retail sales for July.

Market Snapshot

- S&P 500 futures up 0.1% to 3,915.00

- STOXX Europe 600 down 0.5% to 412.19

- MXAP down 1.3% to 150.62

- MXAPJ down 1.2% to 496.50

- Nikkei down 0.7% to 27,430.30

- Topix down 0.6% to 1,915.65

- Hang Seng Index down 0.8% to 19,044.30

- Shanghai Composite little changed at 3,246.29

- Sensex down 0.2% to 59,092.96

- Australia S&P/ASX 200 down 1.4% to 6,729.34

- Kospi down 1.4% to 2,376.46

- Brent Futures down 0.3% to $92.56/bbl

- Gold spot up 0.1% to $1,703.64

- U.S. Dollar Index little changed at 110.31

- German 10Y yield little changed at 1.59%

- Euro up 0.1% to $0.9916

- Brent Futures down 0.3% to $92.57/bbl

Top Overnight News from Bloomberg

- The Federal Reserve must raise interest rates to a level that restrains economic activity and keep them there until policy makers are “convinced” that rampant inflation is subsiding, Fed Richmond President Thomas Barkin said in an interview with the Financial Times

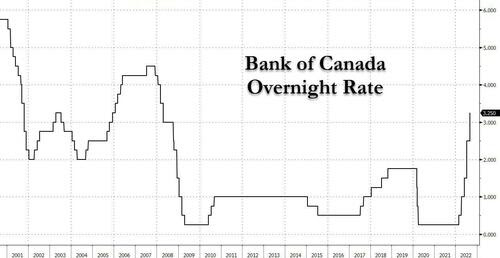

- All 31 economists surveyed by Bloomberg expect Bank of Canada policy makers led by Governor Tiff Macklem to raise the benchmark overnight rate by at least 50 basis points, and most say it will be 75 basis points

- The ECB’s interest-rate hikes may fail to fully filter through into markets without a shift in its policies. Interest-rate rises are already struggling to be reflected across money markets because there’s too much cash chasing scarce high-quality securities, depressing their yields

- The euro-area economy expanded by more than initially estimated in the second quarter, with the revision revealing greater support from consumer and government spending. Output rose 0.8% from the previous three months — stronger than an earlier reading of 0.6%

- “Give us turbines and we’ll turn on Nord Stream tomorrow, but they won’t give us anything,” President Vladimir Putin said at the Eastern Economic Forum in Vladivostok

- The European Commission recommends member states cap the price of electricity from producers like wind farms, nuclear and coal plants at EU200 per MWh, the Financial Times reported, citing a draft of proposals it has seen

- The yen has slumped to a level that leaves it on track for its worst year on record, prompting the strongest warnings to date from senior Japanese government officials aimed at stemming the slide

- The world’s original and longest-running experiment in negative interest rates will finally end this week as Denmark raises borrowing costs in tandem with the euro zone. The move is likely as the ECB delivers a large hike on Thursday, because Danish monetary policy often shadows such moves to protect the krone’s peg to the single currency

- Developed economies are taking a hit from the dollar’s appreciation to multi-decade highs in ways that were once more familiar to their emerging-market peers

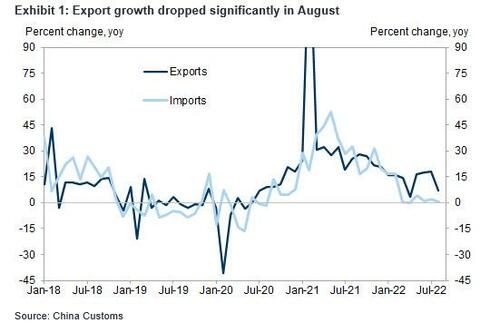

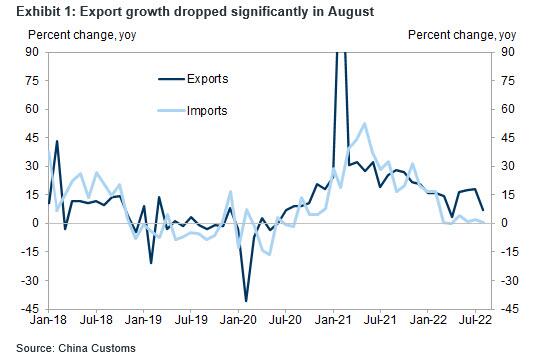

- China’s export growth slowed in August and imports stagnated, a sign of a darkening global economic picture and weak domestic growth hit by Covid lockdowns and a property slump. Exports in US dollar terms expanded 7.1% last month from a year earlier, far weaker than economists had predicted

- China sent its most powerful signal yet on its discomfort with the yuan’s weakness by setting its reference rate for the currency with the strongest bias on record

A more detailed look at global markets courtesy of Newsquawk

Asia stocks were pressured amid spillover selling from Wall St owing to the higher yield environment and as participants digested the latest Chinese trade data. ASX 200 weakened from the open with the index dragged lower by the energy and mining-related sectors and with somewhat mixed GDP data not doing much to spur risk appetite. Nikkei 225 declined despite a further weakening in the JPY as the recent rapid currency depreciation raised further questions surrounding the BoJ’s dovish resolve. Hang Seng and Shanghai Comp were subdued amid the ongoing COVID woes and following the softer than expected Chinese trade data in which all metrics missed forecasts.

Top Asian News

- Japanese Chief Cabinet Secretary Matsuno believes relaxation of border control measures could be an advantage with the weak JPY, while they are concerned by recent rapid, one-sided currency moves and are ready to take appropriate action on FX market moves if necessary, according to Reuters.

- Japanese Finance Minister Suzuki, when asked about the chance of currency intervention, says will take necessary steps, according to Reuters.

- Japan’s former MOF FX head Watanabe said there is no need for Japan to intervene in the currency market to stem the yen’s declines and that Japan intervening solo in the FX market would be meaningless as current FX moves are driven by broad dollar gains, while he noted that intervening solo would be a waste of money as markets would know Tokyo has limited to how much reserves it can tap to continue with such actions. Wakatabe also stated that USD/JPY is overshooting somewhat now and may briefly reach 145 later this month but such increases likely won’t last long, while he doesn’t think the BoJ will raise rates just to stem JPY’s declines.

- Xi, Putin to Meet for First Time Since Russia’s War in Ukraine

- China’s Xi Has Broad Support for Continued Rule, Envoy Says

- Korean Won Still Near 13-Year Low After Central Bank Warning

- Vietnam Wins Rating Upgrade From Moody’s on stronger Growth

- China State-Backed Expo Pulls Ukraine Trade Event at Last Minute

- Goldman Sachs, BNP Paribas at Odds Over Asia Earnings Outlook

European bourses have trimmed the losses seen at the open, but still trade mostly lower. European sectors are mostly lower after opening with a mild defensive bias – that bias has since eased somewhat, with some cyclicals making their way up the ranks. Stateside, US equity futures were softer in early trade, but to a lesser extent than peers across the pond, and have since mostly moved into the green as yields ease

Top European News

- UK PM Truss spoke with US President Biden with Truss said to be looking forward to working with Biden to tackle shared challenges, particularly extreme economic problems from Russian President Putin’s war, while they discussed domestic issues and agreed on the importance of protecting the Good Friday Agreement, according to Downing Street.

- UK PM Truss will not activate the emergency Article 16 override provision in the Northern Ireland protocol in the coming weeks and pulling away from an early confrontation with the EU over Brexit, according to FT citing the PM’s allies.

- BoE Governor Bailey noted that we have had volatile markets in the last six weeks, still seeing extreme volatility in energy markets. On the UK exchange rate, said there are dollar-specific factors in play; said the Fed is more focussed on bringing demand shock under control. Bailey added a review of the Bank’s mandate would not be a recognition that the BoE regime is failing.

- BoE Chief Economist Pill said he does not want to comment on fiscal stimulus without seeing the details. He expects headline inflation to decline in the short-term. Pill emphasised the importance of BoE inflation target as an anchor, not considering new regime.

- BoE’s Mann said trade, financial flows, and GBP may have heightened role in the next year. Mann added that more forceful bank rate moves open door for policy to be on hold or a reversal later. She added that short-term inflation spikes are getting increasingly embedded in domestic prices.

- BoE’s Tenreyro said demand is already weakening, and added when close to equilibrium rate, gradual hikes allow BoE to react before it tightens too far into contractionary territory. “Even without rate increases in August, rates were at a sufficient level to return inflation to target over the medium-term.”

FX

- DXY maintains bullish momentum but remained under 110.50 throughout most of the European session in a 110.17-69 range (at the time of writing).

- JPY underperforms with USD/JPY extending above 144.00 despite a slew of verbal intervention by Japanese officials, whilst the Yuan shrugged off another firm CNY fixing by the PBoC.

- EUR, and CHF are all trading mid-range vs the USD whilst the NZD, AUD, and CAD track risk sentiment.

Fixed Income

- Debt futures are hovering just below best levels having extended rebounds to fresh intraday highs in the run up to UK and German auctions that saw solid demand.

- Bunds sit under their 145.24 peak (+44 ticks vs -33 ticks at one stage), Gilts skirt 106.00 from 106.11 (+38 ticks vs -59 ticks at the Liffe low).

- 10yr T-note holds closer to 115-27 than 115-13+ following some hefty block purchases (two 10k clips in particular)

Commodities

- WTI and Brent futures have been bouncing off worst levels after printing multi-month lows.

- Spot gold fluctuates on either side of USD 1,700/oz, driven largely by bond yields.

- Base metals are mostly lower with upside hampered by disappointing Chinese trade data overnight.

- Indian PM Modi said keen to boost ties with Russia; said Russia and India can work closely on coking coal supply.

US Event Calendar

- 07:00: Sept. MBA Mortgage Applications, prior -3.7%

- 08:30: July Trade Balance, est. -$70.2b, prior -$79.6b

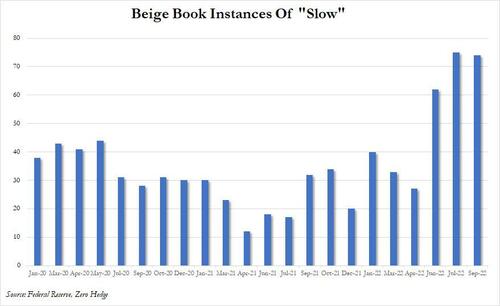

- 14:00: U.S. Federal Reserve Releases Beige Book

Fed Speakers

- 09:00: Fed’s Barkin Speaks at MIT

- 10:00: Fed’s Mester speaks at MNI virtual event

- 12:40: Fed’s Brainard Discusses the Economic Outlook

- 14:00: Fed’s Barr Speaks on Financial System Fairness and Safety

DB’s Jim Reid concludes the overnight wrap

The air of feral fog will lift from our house this morning as the kids go back to school. Only about 12-50 years, depending on the debts we collectively leave to our children, until they leave home. After the summer she’s had looking after them I’m slightly worried my wife will leave first. A big fingers crossed she doesn’t.

On this theme, today I’ve just launched a back-to-school survey as part of our regular monthly series. This month we ask whether you think Europe will make it through winter without gas rationing, whether you are thinking about using less energy, at recession probabilities, whether the next big move in bonds and equities will be up or down, your inflation expectations and which if any central banks are likely to make a policy error and in which direction. All help filling it in very much appreciated as usual. See here for the survey.

Yesterday I released my latest chartbook, which also has a back-to-school vibe as we review where we are on important issues facing global markets and the economy over the coming months. Among the charts, we look at how August was the worst month for European bonds in decades, why inflation isn’t going away over the medium-to-longer term, the latest on the European energy crisis, and also briefly examine the upcoming Italian election and the Chinese property sector’s troubles. As ever, it’s full of big easy-to-read figures and titles that explain our biases. Here’s the link. ***

With different asset classes swinging between gains and losses over the last 24 hours, it’s been difficult to point to a single factor behind the various moves. On the one hand, investors remain cautious about the growing array of risks on the horizon, ranging from the European energy situation to Chinese lockdowns to hawkish central banks. But on the other hand, the latest ISM services index for August added to the recent run of US data releases that’s pointed to an improving outlook, suggesting that the Fed can afford to be more aggressive in raising rates, which in turn led to a sharp selloff in Treasuries that leaves them on track for their 6th consecutive weekly decline.

In terms of the details of that ISM print, the headline measure unexpectedly rose in August to a 4-month high of 56.9 (vs. 55.3 expected), with improvements in the new orders and employment components as well. That follows in the footsteps of the ISM manufacturing reading last Thursday that was similarly better than expected, the weekly initial jobless claims that fell for a 3rd week running, and the Conference Board’s consumer confidence measure that hit a 3-month high in August. Now all this might be a last hurrah before our long expected 2023 recession, but there’s no doubt that recent data has been more positive than expected, and is coming alongside some other tailwinds of note like falling gasoline prices.

Given the stronger data, there were growing expectations (again) that the Fed might hike by 75bps in a couple of weeks’ time, with the hike priced in for September up by +2.9bps to 68.0bps. Treasury yields surged across the curve in response (with also a small catch-up after being closed on Monday), with some of the increase likely exacerbated by a banner day for corporate debt issuance ahead of the next Fed meeting (not to mention ahead of the next crucial CPI print), with the 10yr yield up +16.0bps on the day to 3.35%, and the 30yr yield (+15.6bps) even hitting a post-2014 high of 3.50%. That was driven by a rise in real yields, with the 10yr real yield (+15.0bps) rising to a post-2019 high of 0.87%. This morning in Asia, yields on the 10yr USTs are fairly stable. Bear in mind that it was less than -1% in early March after Russia invaded Ukraine, so we’ve seen an incredible shift in real borrowing costs over the last 6 months.

With US real yields reaching new heights, the dollar index advanced +0.62% to reach its strongest level in over two decades. However, it was bad news for equities and the S&P 500 (-0.41%) built on its run of 3 consecutive weekly declines to close at a 7-week low. The more interest-sensitive sectors were particularly affected, and the NASDAQ (-0.74%) and the FANG+ index (-1.50%) saw even larger declines, while there was a clear preference for defensive sectors with real estate (+1.02%) and utilities (+0.22%) outperforming the rest of the pack. Over in Europe there was a moderately better performance however, with the STOXX 600 up +0.24%, and the German Dax (+0.87%) recovering somewhat from the previous day’s heavy losses. Futures are weak this morning though with contracts on the S&P 500 (-0.52%), NASDAQ 100 (-0.53%) and DAX (-1.15%) lower.

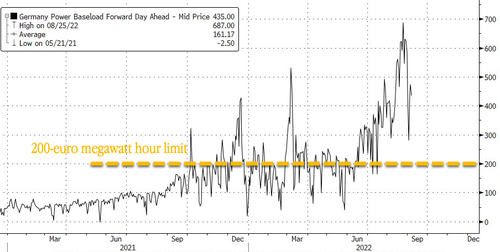

When it comes to the energy situation, there wasn’t much respite yesterday as we look forward to Friday’s meeting of EU energy ministers. Natural gas futures in Europe fell by -2.47% to €240 per megawatt-hour, and German power prices for next year were also down -6.02% to €536 per megawatt-hour. But relative to their levels from last year they are still incredibly elevated. One piece of news we did get was from German Chancellor Scholz, who said that when it came to a cap on power prices, “If we have our way, it will take weeks rather than months”. In the meantime, European sovereign bonds lost further ground, with yields on 10yr bunds (+7.4bps), OATs (+3.5bps) and BTPs (+3.3bps) all moving higher.

Here in the UK, Liz Truss was appointed as the new Prime Minister yesterday, succeeding Boris Johnson after three years in the job. In her initial speech in front of Downing Street, she said that action would be taken on the energy crisis this week, so that’s one to keep an eye out for, with reports across the press (as we previewed yesterday) indicating that bills will be frozen around current levels rather than going up in October. That came as gilts strongly underperformed their continental counterparts yesterday, with 10yr yields up by +15.7bps to 3.09%, which is their highest closing level since 2011. Interestingly however, there was a major steepening in the yield curve, with 2yr yields down -2.0bps as investors reacted to the prospect of lower short-term inflation in light of the potential freeze on bills.

Asian equity markets are weak this morning with the Hang Seng (-1.65%) leading losses followed by the Kospi (-1.50%) and the Nikkei (-0.95%). Over in Mainland China, the Shanghai Composite (-0.05%) and the CSI (-0.08%) are wavering between gains and losses in early trade.

The latest trade data coming out of China this morning showed exports growing at a slower pace in August (+7.1% y/y) against market forecast of a +13.0% increase and compared to July’s +18.0% rise as global demand continued to soften. At the same time, imports rose only +0.3%, falling short of expectations for a +1.1% gain. Elsewhere, Australia’s GDP expanded +0.9% in the second quarter, in-line with market expectations as consumers kept spending while energy exports boomed. The growth figure for the previous quarter (+0.7%) was downwardly revised though.

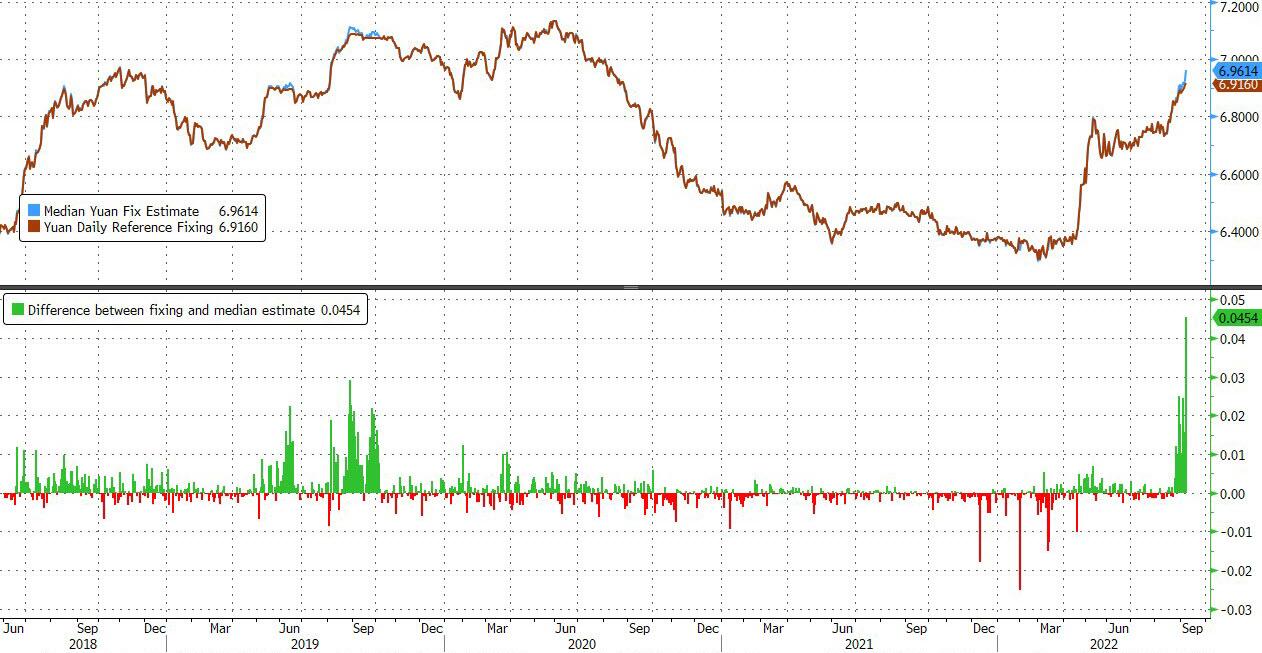

In FX news, the Japanese yen (-0.90%) this morning slid to a fresh 24-year low of 144.09 against the US dollar. Widening rate differential is the main reason for yen’s depreciation while yesterday’s better than expected US data probably also pushed the yen weaker. Separately, the People’s Bank of China (PBOC) fixed the yuan at 6.9160 to the dollar, its strongest bias on record and the 11th successive increase as the authorities continue to fight the global trend of a strong dollar against virtually every currency.

In energy markets, oil prices are trading lower in Asian trade with Brent futures down -1.45% at $91.48/bbl as the demand could remain under pressure amid China’s Covid-19 lockdowns.

There wasn’t a great deal of other data yesterday, though in Europe we did get the German and UK construction PMIs for August, which were both in contractionary territory at 42.6 and 49.2 respectively. German factory orders in July also contracted by a faster-than-expected -1.1% (vs. -0.7% expected). Otherwise in the US, the final composite and services PMI for August painted quite a different picture to the ISM numbers, with the final services PMI revised down to 43.7 (vs. flash 44.1) and the final composite PMI revised down to 44.6 (vs. flash 45).

To the day ahead now, and there’s plenty on the central bank side, as the Bank of Canada announce their latest policy decision and the Fed release their Beige Book. We’ll also hear from Bank of England Governor Bailey, as well as the BoE’s Pill, Mann and Tenreyro as they testify before the Treasury Select Committee. In addition, there are scheduled remarks Fed officials, including Vice Chair Brainard, Vice Chair Barr, and Mester and Barkin. Otherwise, data releases include German industrial production and Italian retail sales for July.

AND NOW NEWSQUAWK

US Market Open: European bourses have trimmed the losses seen at the open; JPY underperforms with USD/JPY extending above 144.00 – Newsquawk US Market Open

WEDNESDAY, SEP 07, 2022 – 06:37 AM

- European bourses have trimmed the losses seen at the open; US equity futures meander around the flat mark.

- DXY maintains bullish momentum but remained under 110.50 throughout most of the European session.

- Debt futures are hovering just below best levels having extended rebounds to fresh intraday highs.

- WTI and Brent futures have been bouncing off worst levels after printing multi-month lows; Base metals are mostly lower with upside hampered by disappointing Chinese trade data overnight.

- Looking ahead, highlights include BoC Rate Decision, Fed Beige Book, EIA STEO, and Speeches from Fed’s Barkin, Mester, Brainard & Barr.

For the full report and more content like this check out Newsquawk

Try a 14 day trial with Newsquawk and hear breaking trading news as it happens.

7th September 2022

LOOKING AHEAD

- BoC Rate Decision, Fed Beige Book, EIA STEO, Speeches from Fed’s Barkin, Mester, Brainard & Barr

- Click here for the Week Ahead preview.

GEOPOLITICS

RUSSIA-UKRAINE

- Russian President Putin said trust in the USD, EUR, and GBP has been undermined; Russia has cut usage of the currencies. Putin said Gazprom and China have moved to RUB and CNY settlements for gas in a 50/50 proportion. Putin said will have to think of changing routes for Ukrainian grain; says problems with food will intensify.

- Russian President Putin said demand for Russian energy in China is rising, according to Reuters.

EUROPEAN TRADE

EQUITIES

- European bourses have trimmed the losses seen at the open, but still trade mostly lower.

- European sectors are mostly lower after opening with a mild defensive bias – that bias has since eased somewhat, with some cyclicals making their way up the ranks.

- Stateside, US equity futures were softer in early trade, but to a lesser extent than peers across the pond, and have since mostly moved into the green as yields ease

- Click here for more detail.

FX

- DXY maintains bullish momentum but remained under 110.50 throughout most of the European session in a 110.17-69 range (at the time of writing).

- JPY underperforms with USD/JPY extending above 144.00 despite a slew of verbal intervention by Japanese officials, whilst the Yuan shrugged off another firm CNY fixing by the PBoC.

- EUR, and CHF are all trading mid-range vs the USD whilst the NZD, AUD, and CAD track risk sentiment.

- Click here for more detail.

Notable FX Expiries, NY Cut:

- EUR/GBP: 0.8575 (1.21BN)

- Click here for more detail

FIXED INCOME

- Debt futures are hovering just below best levels having extended rebounds to fresh intraday highs in the run up to UK and German auctions that saw solid demand.

- Bunds sit under their 145.24 peak (+44 ticks vs -33 ticks at one stage), Gilts skirt 106.00 from 106.11 (+38 ticks vs -59 ticks at the Liffe low).

- 10yr T-note holds closer to 115-27 than 115-13+ following some hefty block purchases (two 10k clips in particular)

- Click here for more detail.

COMMODITIES

- WTI and Brent futures have been bouncing off worst levels after printing multi-month lows.

- Spot gold fluctuates on either side of USD 1,700/oz, driven largely by bond yields.

- Base metals are mostly lower with upside hampered by disappointing Chinese trade data overnight.

- Indian PM Modi said keen to boost ties with Russia; said Russia and India can work closely on coking coal supply.

- Click here for more detail.

PRICE CAPS

- Czech Industrial Minister said Russian gas price cap should be taken off the table at the EU Energy Minister meeting, according to CTK cited by Reuters.

- EU is planning a EUR 200/MWh electricity price cap by non-gas power producers (wind, nuclear, coal), according to a draft proposal cited by FT; the document suggests a target of reducing consumption by 5% during peak pricing hours. Proposal is to be discussed today ahead of Friday’s energy meeting.

- Russian President Putin reiterated that Russia will not stick to oil and gas contracts if prices are capped.

CRYPTO

- Bitcoin prices slipped overnight to under USD 19,000 whilst Ethereum tested 1,500 to the downside.

NOTABLE EUROPEAN HEADLINES

- UK PM Truss spoke with US President Biden with Truss said to be looking forward to working with Biden to tackle shared challenges, particularly extreme economic problems from Russian President Putin’s war, while they discussed domestic issues and agreed on the importance of protecting the Good Friday Agreement, according to Downing Street.

- UK PM Truss will not activate the emergency Article 16 override provision in the Northern Ireland protocol in the coming weeks and pulling away from an early confrontation with the EU over Brexit, according to FT citing the PM’s allies.

- BoE Governor Bailey noted that we have had volatile markets in the last six weeks, still seeing extreme volatility in energy markets. On the UK exchange rate, said there are dollar-specific factors in play; said the Fed is more focussed on bringing demand shock under control. Bailey added a review of the Bank’s mandate would not be a recognition that the BoE regime is failing.

- BoE Chief Economist Pill said he does not want to comment on fiscal stimulus without seeing the details. He expects headline inflation to decline in the short-term. Pill emphasised the importance of BoE inflation target as an anchor, not considering new regime.

- BoE’s Mann said trade, financial flows, and GBP may have heightened role in the next year. Mann added that more forceful bank rate moves open door for policy to be on hold or a reversal later. She added that short-term inflation spikes are getting increasingly embedded in domestic prices.

- BoE’s Tenreyro said demand is already weakening, and added when close to equilibrium rate, gradual hikes allow BoE to react before it tightens too far into contractionary territory. “Even without rate increases in August, rates were at a sufficient level to return inflation to target over the medium-term.”

NOTABLE EUROPEAN DATA

- EU GDP Revised YY (Q2) 4.1% vs. Exp. 3.9% (Prev. 3.9%)

- EU GDP Revised QQ (Q2) 0.8% vs. Exp. 0.6% (Prev. 0.6%)

- EU Employment Final QQ (Q2) 0.4% vs. Exp. 0.3% (Prev. 0.3%, Rev. 0.7%)

- EU Employment Final YY (Q2) 2.7% vs. Exp. 2.4% (Prev. 2.4%, Rev. 3.1%)

NOTABLE US HEADLINES

- Fed’s Barkin (2024 voter) warned that rates must stay high until inflation eases and said the Fed would need to tighten policy further so that real interest rates sit above zero, according to FT.

- Fed Fund Futures imply a 75% chance of a 75bps Fed rate hike this month, according to FedWatch cited by Reuters.

APAC TRADE

- APAC stocks were pressured amid spillover selling from Wall St owing to the higher yield environment and as participants digested the latest Chinese trade data.

- ASX 200 weakened from the open with the index dragged lower by the energy and mining-related sectors and with somewhat mixed GDP data not doing much to spur risk appetite.

- Nikkei 225 declined despite a further weakening in the JPY as the recent rapid currency depreciation raised further questions surrounding the BoJ’s dovish resolve.

- Hang Seng and Shanghai Comp were subdued amid the ongoing COVID woes and following the softer than expected Chinese trade data in which all metrics missed forecasts.

NOTABLE APAC HEADLINES

- PBoC set USD/CNY mid-point at 6.9160 vs exp. 6.9686 (prev. 6.9096)

- Japanese Chief Cabinet Secretary Matsuno believes relaxation of border control measures could be an advantage with the weak JPY, while they are concerned by recent rapid, one-sided currency moves and are ready to take appropriate action on FX market moves if necessary, according to Reuters.

- Japanese Finance Minister Suzuki, when asked about the chance of currency intervention, says will take necessary steps, according to Reuters.

- Japan’s former MOF FX head Watanabe said there is no need for Japan to intervene in the currency market to stem the yen’s declines and that Japan intervening solo in the FX market would be meaningless as current FX moves are driven by broad dollar gains, while he noted that intervening solo would be a waste of money as markets would know Tokyo has limited to how much reserves it can tap to continue with such actions. Wakatabe also stated that USD/JPY is overshooting somewhat now and may briefly reach 145 later this month but such increases likely won’t last long, while he doesn’t think the BoJ will raise rates just to stem JPY’s declines.

DATA RECAP

- Chinese Trade Balance USD (Aug) 79.39B vs. Exp. 92.7B (Prev. 101.26B)

- Chinese Exports YY* (Aug) 7.1% vs. Exp. 12.8% (Prev. 18.0%)

- Chinese Imports YY* (Aug) 0.3% vs. Exp. 1.1% (Prev. 2.3%)

- Chinese Trade Balance (CNY)(Aug) 535.9B vs Exp. 661.9B (Prev. 682.7B)

- Chinese Exports YY (CNY)(Aug) 11.8% vs Exp. 18.5% (Prev. 23.9%)

- Chinese Imports YY (CNY)(Aug) 4.6% vs Exp. 6.3% (Prev. 7.4%)

- Australian Real GDP QQ SA (Q2) 0.9% vs. Exp. 1.0% (Prev. 0.8%)

- Australian Real GDP YY SA (Q2) 3.6% vs. Exp. 3.5% (Prev. 3.3%)

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 2.85 PTS OR 0.09% //Hang Sang CLOSED DOWN 158.43 OR 0.82% /The Nikkei closed DOWN 196.21 OR .71%. //Australia’s all ordinaires CLOSED DOWN 1.37% /Chinese yuan (ONSHORE) closed DOWN AT 6.9782//OFFSHORE CHINESE YUAN DOWN 6.9943// /Oil DOWN TO 87.09 dollars per barrel for WTI and BRENT AT 92,81 / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

3 a./NORTH KOREA/ SOUTH KOREA/

///NORTH KOREA/SOUTH KOREA/

3B JAPAN

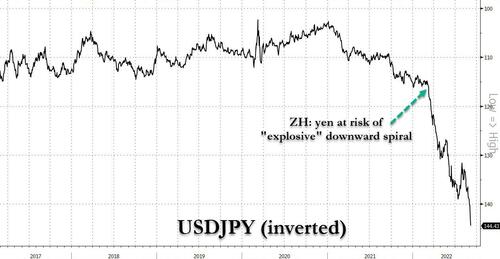

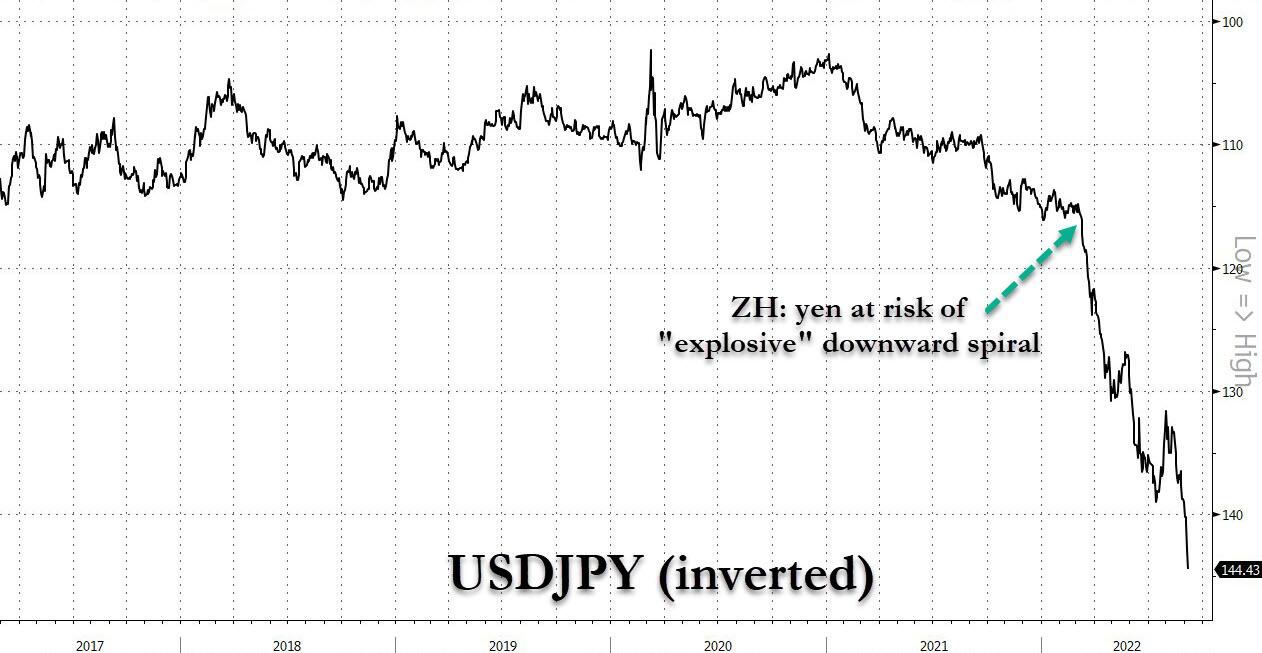

The Yen implodes to 144.99 to the dollar. The Yuan also is wacked, as the record USA dollar surge sparks their plunges.

(zerohedge)

Japan, China On Edge After Record Dollar Surge Sparks “Explosive” Yen Plunge; China’s Yuan Not Far Behind

WEDNESDAY, SEP 07, 2022 – 02:04 PM

Back in late March, when USDJPY was at 121, we warned that the “Yen Was At Risk Of “Explosive” Downward Spiral With Kuroda Trapped… And Why China May Soon Devalue“, and since then the yen has… well, see for yourselves:

In short, we were right.