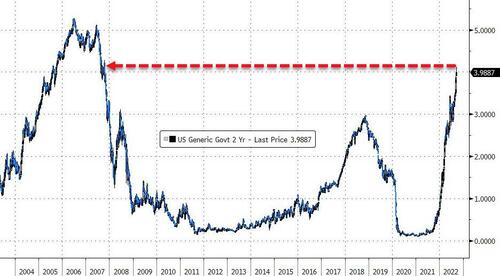

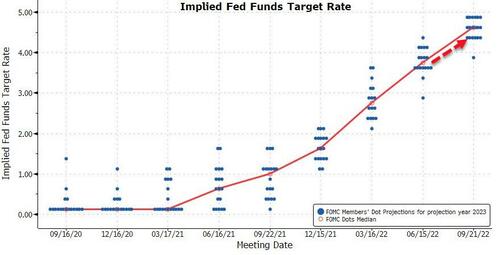

SEPT 21//FED HIKES RATES BY .75% BUT EXTENDS DOTS OUTWARD TO 4.6%//GOLD CLOSED UP $4.70 TO $1667.75//SILVER CLOSED UP 33 CENTS TO $19.50//PLATINUM CLOSED DOWN $2.75 TO $918.40//PALLADIUM CLOSED DOWN $23.55 TO $2123.75//MATHEW PIEPENBERG: A MUST READ//PUTIN CALLS UP 300,000 RESERVES IN HIS BATTLE WITH THE WEST (AND UKRAINE)//EUROPE’S BATTLE WITH HIGHER ENERGY COSTS//COVID UPDATES// DR PAUL ALEXANDER//VACCINE IMPACT//VACCINE INJURY//USA EXISTING HOUSING STARTS FALLS AGAIN SETTING THE STAGE FOR ANOTHER DOWNGRADE FROM ATLANTA FED//QUIETLY FACEBOOK AND GOOGLE SHED EMPLOYEES/THE USA 2 YR INTEREST RATE TOPS 4%//SWAMP STORIES FOR YOU TONIGHT//

323 C HSBC 52 435 H SCOTIA CAPITAL 1 624 H BOFA SECURITIES 437 657 C MORGAN STANLEY 20 661 C JP MORGAN 805 709 C BARCLAYS 1651 737 C ADVANTAGE 9 6 800 C MAREX SPEC 10 880 H CITIGROUP 349

total notices so far: 7775 contracts for 777,500 oz (24.105 tonnes)

SILVER NOTICES: 26 NOTICES FILED FOR 130,000 OZ/

total number of notices filed so far this month 6488 : for 32,440,000 oz

END

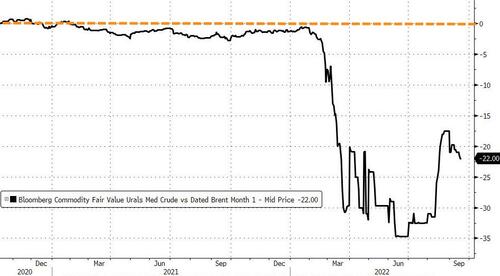

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $4.70

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: //// A WITHDRAWAL OF 5.79 TONNES FROM THE GLD/

INVENTORY RESTS AT 952.16 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $.33

AT THE SLV// ://GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV//: STRANGE ADEPOSIT OF 2.902 MILION OZ INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 482.115 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 578 CONTRACTS TO 132,107. AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.18 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.18) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC SILVER LONGS BUT WE DID HAVE A STRONG SILVER SHORT COVERING AS WE HAD A GOOD SIZED LOSS OF OF 524 CONTRACTS ON OUR TWO EXCHANGES. THE SPECS ARE FLEEING AS FAST AS THEIR LITTLE FEET WILL CARRY THEM.

WE MUST HAVE HAD: I) STRONG SPECULATOR SHORT COVERING ////CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A TINY ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 50,000 OZ QUEUE JUMP / // V) STRONG SIZED COMEX OI LOSS/(//CONSIDERABLE SPEC LIQUIDATION/)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -29

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTRACTS for 14 days, total 11,757 contracts: 58.785 million oz OR 4.190 MILLION OZ PER DAY. (839 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 58.785 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 58.785 MILLION OZ///

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 578 WITH OUR $0.18 LOSS IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A TINY SIZED EFP ISSUANCE CONTRACTS: 25 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /GOOD BANKER ADDITIONS A// CONSIDERABLE NET SPEC SHORT COVERINGS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 50,000 OZ QUEUE JUMP // .. WE HAD A STRONG SIZED LOSS OF 553 OI CONTRACTS ON THE TWO EXCHANGES FOR 2.765MILLION OZ AS..THE SPECS STILL ARE BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 26 NOTICE(S) FILED TODAY FOR 130,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 1844 CONTRACTS TO 469,393 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED+ 3440 CONTRACTS.

.

THE FAIR SIZED INCREASE IN COMEX OI CAME DESPITE OUR FALL IN PRICE OF $6.65//COMEX GOLD TRADING/TUESDAY / WE MUST HAVE HAD MAJOR SPECULATOR SHORT COVERINGS ACCOMPANYING OUR SMALL SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND //CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 8.401 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 176,500 OZ //NEW STANDING 24.951 TONNES

YET ALL OF..THIS HAPPENED DESPITE OUR FALL IN PRICE OF $6.65 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 2512 OI CONTRACTS 7.8133 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 668 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 469,393

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2512 CONTRACTS WITH 1844 CONTRACTS INCREASED AT THE COMEX AND 668 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2512 CONTRACTS OR 7.8133 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (668) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (1844): TOTAL GAIN IN THE TWO EXCHANGES 2512 CONTRACTS. WE NO DOUBT HAD 1) CONSIDERABLE SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS/// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 8.409 TONNES FOLLOWED BY TODAY’S MONSTROUS QUEUE. JUMP OF 176,500 oz. 3) ZERO LONG LIQUIDATION//// //.,4) FAIR SIZED COMEX OPEN INTEREST GAIN 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

35,359 CONTRACTS OR 3,535,900 OZ OR 109.98 TONNES 14 TRADING DAY(S) AND THUS AVERAGING: 2525 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 14 TRADING DAY(S) IN TONNES: 109.98 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 109.98/3550 x 100% TONNES 3.09% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 109.98 TONNES (SLIGHTLY FALLING THIS MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT., FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER,FELL BY A STRONG SIZED 578 CONTRACT OI TO 132,136 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 25 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 25 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 25 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 578 CONTRACTS AND ADD TO THE 25 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF 553 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 2.765 MILLION OZ

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED DOWN 5.23 PTS OR 0.17% //Hang Sang CLOSED UP 336.60 PTS OR 1.79% /The Nikkei closed DOWN 375.29 PTS OR 1.36% //Australia’s all ordinaires CLOSED DOWN 1.55% /Chinese yuan (ONSHORE) closed DOWN AT 7.0478//OFFSHORE CHINESE YUAN DOWN 7.0540// /Oil UP TO 85.91 dollars per barrel for WTI and BRENT AT 92,59 / Stocks in Europe OPENED MOSTLY GREEN. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 1844 CONTRACTS TO 469,393 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR FALL IN PRICE OF $6.65 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A SMALL SIZED EFP (668 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.. THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 668 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :668 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 668 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED SIZED TOTAL OF 2512 CONTRACTS IN THAT 668 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 1844 CONTRACTS..AND THIS SMALL LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR FALL IN PRICE OF GOLD $6.65. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING SEPT (24.951),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 24.951 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $6.65) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A SMALL SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 2512 CONTRACTS // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS TRIED TO COVER ON THEIR POSITIONS WITH MINIMAL SUCCESS////// WE HAVE REGISTERED A FAIR GAIN OF 2512 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR SEPT. (24.951 TONNES)…

WE HAD 3440 CONTRACTS ADDED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 930 CONTRACTS OR 93000 OZ OR 2.892 TONNES

Estimated gold volume 147,721/// poor//

final gold volumes/yesterday 156,593/ poor

INITIAL STANDINGS FOR SEPT ’22 COMEX GOLD //SEPT 21

Total monthly oz gold served (contracts) so far this month

7775 notices 777,500 OZ 24.105 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

1 customer withdrawals:

i) Out of JPMorgan: 120,565.141 oz

total: 120.565.141 oz

total in tonnes: 3.75 tonnes

Adjustments: 1

Malca/dealer to customer: 98,574.966 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPT.

For the front month of SEPT we have an oi of 1917 contracts having GAINED 1420 contracts .

We had 345 notices filed on TUESDAY so we gained a whopping 1765 contracts or an additional 176,500 oz

will stand for gold in this very non active delivery month of September.

October LOST 30 contracts REMAINING AT 42,943. Oct is generally a poor active delivery month. It WILL change!! (Look for a very unusually large Oct. delivery month.)

November LOST 16 contracts to stand at 303

December lost 100 contracts DOWN to 378,624

We had 1670 notice(s) filed today for 167,000 oz FOR THE SEPT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1670 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 805 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2022. contract month,

we take the total number of notices filed so far for the month (7775) x 100 oz , to which we add the difference between the open interest for the front month of (SEPT 1917 CONTRACTS) minus the number of notices served upon today 1675 x 100 oz per contract equals 802,200 OZ OR 24.951 TONNES the number of TONNES standing in this NON active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month:

No of notices filed so far (7775) x 100 oz+ (1917) OI for the front month minus the number of notices served upon today (1670} x 100 oz} which equals 802,200 oz standing OR 24.951 TONNES in this NON active delivery month of SEPTEMBER.

TOTAL COMEX GOLD STANDING: 24.951 TONNES (A HUMONGOUS STANDING FOR A SEPT ( NON ACTIVE) DELIVERY MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 6488 x 5,000 oz = 32,440,000 oz

to which we add the difference between the open interest for the front month of SEPT(150) and the number of notices served upon today 26 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT./2022 contract month: 6,488 (notices served so far) x 5000 oz + OI for front month of SEPT (150) – number of notices served upon today (26) x 5000 oz of silver standing for the SEPT contract month equates 33,060,000 oz. .

We have an inventory of 44.240 million oz of registered silver at the comex so Sept delivery of 33.060 MILLION OZ represents 74.79% of that category of silver.

If we add August’s final delivery (to Sept) for silver at 5.51 million oz, we have a total of 38.57 million oz delivered upon with a REGISTERED INVENTORY of 44.20 million oz or 87.26% of that category of silver.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

SEPT 21/WITH GOLD UP $4.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.79 TONNES FROM THE GLD///INVENTORY RESTS AT 952.16 TONNES

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

SEPT 13/WITH GOLD DOWN $22.85 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73ONNES FROM THE GLD////INVENTORY RESTS AT 964.91 TONNES

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

AUGUST 31.WITH GOLD DOWN $10.20:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.24 TONNES FROM THE GLD////INVENTORY RESTS AT 973.37 TONNES

AUGUST 30.WITH GOLD DOWN $12.00:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 980.61 TONNES

AUGUST 29/WITH GOLD DOWN $.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD/////INVENTORY RESTS AT 982.64 TONNES

AUGUST 26/WITH GOLD DOWN $26.60; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 25/WITH GOLD UP $9.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 18/WITH GOLD DOWN $5.25: GIGANTIC CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.78 TONNES FROM THE GLD////INVENTORY RESTS AT 985.83 TONNES

AUGUST 17/WITH GOLD DOWN $12.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 992.20 TONNES

AUGUST 16/WITH GOLD DOWN $7.85: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 993.94 TONNES

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

GLD INVENTORY: 952.16 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 21/WITH SILVER UP 33 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.902 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 482.115 MILLION OZ//

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

SEPT 13/WITH SILVER DOWN $.31 TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.899 MILLION OZ//

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

AUGUST 31/WITH SILVER DOWN 36 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 3.087 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 465.573 MILLION OZ//

AUGUST 30/WITH SILVER DOWN 34 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 1.478 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 470.135 MILLION OZ//

AUGUST 29/WITH SILVER DOWN 7 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY A THE SLV: A WITHDRAWAL OF 2.765 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 470.135 MILLION OZ//

AUGUST 26/WITH SILVER DOWN 39 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 25/WITH SILVER UP 21 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

AUGUST 18/WITH SILVER DOWN 27 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 369,000 OZ INTO THE SLV////INVENTORY RESTS AT 485.482 MILLION OZ//

AUGUST 17/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.106 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.113 MILLION OZ//

AUGUST 16/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 486.219 MILLION OZ/

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

CLOSING INVENTORY 482.115 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Fed Rate-Hikes Will Add Trillions To National Debt

Federal Reserve rate hikes will add trillions to the national debt, according to an analysis by the Committee for a Responsible Federal Budget.

The Fed delivered another 75-basis point rate-hike during its September FOMC meeting this afternoon and made it clear that rates will be ‘higher for longer’ to fight persistently high inflation. According to the Committee for a Responsible Budget (CFRB), rate hikes will add another $2.1 trillion to the national debt over the next decade.

Every increase in interest rate raises the federal government’s interest expense. So far in fiscal 2022, the US Treasury has forked out $471 billion just to fund the government’s interest payments.

To put that number into context, at this point in fiscal 2021 the Treasury’s interest expense stood at $356 billion. That represents a 30% year-on-year increase. Interest expense ranks as the sixth largest budget expense category, about $250 billion below Medicare. If interest rates remain elevated or continue rising, interest expenses could climb rapidly into the top three federal expenses. (You can read a more in-depth analysis of the national debt HERE.)

According to the Congressional Budget Office, this is exactly what will happen. It projects interest payments will triple from nearly $400 billion in fiscal 2022 to $1.2 trillion in 2032. And it’s worse than that. The CBO made this estimate in May. Interest rates are already higher than those used in its analysis.

In a statement to Fox Business, the CFRB concedes that rate hikes are necessary in this inflationary environment. It places the onus on the federal government to get its spending under control.

Policymakers can help the Fed by limiting the need for rate hikes with fiscal policy that pushes inflation in the right direction. That means not enacting legislation and executive orders like student loan forgiveness that have ballooned deficits and only made demand pressures worse.”

Even with pandemic-era spending programs expiring, the federal government continues to spend about half-a-trillion dollars every single month. In August alone, the Biden administration blew through another $523.3 billion. This brought total spending for fiscal 2022 to just over $5.35 trillion.

A paper published by the Kansas City Federal Reserve Bank acknowledged that the central bank can’t slay inflation unless the US government gets its spending under control. In a nutshell, the authors argue that the Fed can’t control inflation alone. US government fiscal policy contributes to inflationary pressure and makes it impossible for the Fed to do its job.

Trend inflation is fully controlled by the monetary authority only when public debt can be successfully stabilized by credible future fiscal plans. When the fiscal authority is not perceived as fully responsible for covering the existing fiscal imbalances, the private sector expects that inflation will rise to ensure sustainability of national debt. As a result, a large fiscal imbalance combined with a weakening fiscal credibility may lead trend inflation to drift away from the long-run target chosen by the monetary authority.”

This clearly isn’t in the cards.

“As interest rates rise and the nation’s debt grows, it will become even more expensive to borrow in the future. Congresses and presidents of both parties, over many years, have avoided making hard choices about our budget and failed to put it on a sustainable path. It is vital for lawmakers to take action on the growing debt to ensure a stable economic future,” the Peter Peterson Foundation said.

Interest expense isn’t the only problem the Fed’s inflation fight creates for the US government. Along with raising rates, the Fed is shrinking its balance sheet. That means it’s not buying Treasury bonds. The federal government needs the central bank to continue buying Treasuries in order to prop up the market and enable its borrowing. Without the Fed’s intervention in the bond market, prices will tank, driving interest rates on US debt even higher.

Something has to give.

The Fed can’t simultaneously fight inflation and prop up Uncle Sam’s spending spree. Either the government will have to cut spending or the Fed will have to keep creating money out of thin air in order to monetize the debt.

You can decide for yourself which scenario you find more likely.

END

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

Even a Weaponized Dollar Won’t Stop Gold’s Historical Turning Point

We have dedicated numerous articles and interviews addressing the dangerous strength of the USD on the heels of a deliberately hawkish Fed hiking rates into what is clearly a recession, official or otherwise.

Explaining the Inexplicable: Rising Rates into a Recession?

On the surface, such central bank tightening in the face of a tanking economy and increasingly volatile risk asset markets makes little sense, as a strong USD and higher interest expense (i.e., interest rate policy) crushes just about every asset class in its wake, from an empirically broken bond market and grotesquely over-valued stock market to the artificially repressed precious metals space.

So, why is the openly cornered Fed acting so openly at odds with the real world and the US economy after years of feeding it instant-liquidity at every “dip,” cough or market sniffle?

The Fake War on Inflation

The standard answer is to “fight” inflation (which the Fed’s own mouse-click money alone created).

But as we’ve also written and observed so many times, a Fed Funds Rate at 3%, 4% or even 5% is not only mathematically crippling to a nation which simply can’t afford such rates, it is equally impotent against a headline CPI print in the 8-9% range (and rising).

In short: Rate hikes won’t defeat money supply driven or supply-constraint driven inflation at all.

Thus, and again, what is the Fed really doing and thinking notwithstanding the official nonsense that makes the headlines or pours from their double-speaking lips?

A Weaponized Fed Running Out of Bullets

One answer: The Fed, like the SWIFT removals and FX reserve freezes, is just another weaponized tool against Russia and the seismic shifts (petrodollar, LBMA alternatives, mono-to-multi-currency trade agreements) resulting globally ever since the openly failed sanctions against Russia were commenced earlier this year.

To any who understand the origins, history and actual practices of the Federal Reserve, the notion that this cabal of private bankers is an “independent” entity is by now an open farce.

That is, the Fed is anything but “independent” and is not only a political fixture of the DC horizon, but rather a political hijacker of the American economy, markets and policy in ways the go far, way far, beyond its supposed “mandate” to simply manage U.S. inflation and employment.

It is my own strong belief that one of the primary motives behind the current rate policy to strengthen the USD has been to help the U.S. government break the financial back of Russia, which like all its prior policies/sanctions (based on the re-invigorated Russian currency, trade surpluses and multi-lateral trade agreements) is failing.

Toward this end, it is far more than likely that the Fed’s “weaponized” rate hiking will continue this week, much, frankly to the chagrin of a temporarily falling gold price.

What one has to ask however, is will this policy backfire as well (?), for it seems that this game of financial chicken with Putin is breaking the back of the US markets and economy (and its EU allies) with far greater effect.

Hubris Comes Before the Fall

I am once again reminded of the 2014 statement made by then U.S. Secretary of State, Condoleezza Rice, that Russia would run out of money long before the West ran out of energy.

Less than a decade after this classic example of American hubris was made, it seems Russia (as well as China, the BRICS and a string cite of emerging market economies) would beg to differ as the world shifts from a U.S.-led mono-currency system to an increasingly multi-national currency, trading and political new direction.

None of this, by the way, will be “orderly.”

Within the US markets and economy, conditions keep trending from bad to worse in every category– from risk assets, social division, and political impotence to the headline-making layoffs at Goldman Sachs, the tanking profits at FedEx and the destruction of the U.S. working class under the invisible tax of persistent rather than “transitory” inflation.

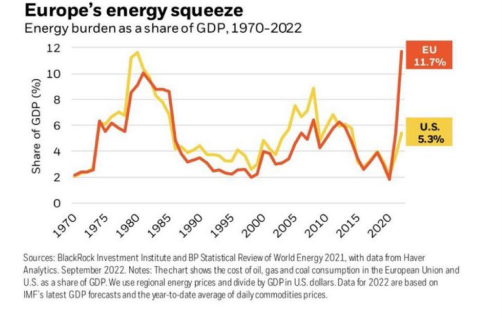

Meanwhile In Europe…

The price for blindly following the so-called “moral” lead of the US in its political and financial war against Putin (to save a less-than-moral thespian like Zelenskyy) is becoming increasingly high as the delusion that Putin has less leverage than the West becomes increasingly harder to sell, swallow or justify.

In addition to facing an extremely cold and expensive winter…

…the Europeans are seeing their currency at 20-year lows against an artificially inflated dollar.

But it’s not only Europe’s (or Japan or England’s) currency which is tanking, but their trade balances as well, which is otherwise atypical, as weakening currencies are supposed to improve rather than weaken export competitivity.

But not this time (see the EU’s trade balance, red line below).

At the End of the Day: Energy Matters

What the failed sanctions, policies and visions of the US-led West are now making abundantly clear is that energy matters, and folks, like it or not, Russia has more of it than the West as the US strangles rather than frees energy production in the US under a suicidal policy of a “green” new normal.

How the West Was Lost

In the immediate years after the Second World War, America’s greatest generation, as well as its dollar and Treasury bond, were undeniable leaders and influencers.

Those days, dollars, bonds and influencers, however, are no more.

But is it not comical to hear the IQ-challenged Governor of a failed state like California pushing electric cars as the new “solution” (?) — an example of open fantasy almost as comical as Christine Lagarde’s latest attempt to blame European inflation on climate change rather than her own bathroom mirror.

Having transitioned from a world of fair pricing, fair wages, gold-backed money, manageable bond obligations and strong exports, America has devolved into a modern feudalism of over-paid executives, a diminishing middle class, Wall Street socialism, a thin-air-backed dollar, a Fed-monetized (i.e., “zombie”) bond market, exported/outsourced labor and hence anemic productivity.

Once the world’s greatest producer and creditor, the US is now its greatest importer and debtor, and has not only exported US productivity to cheaper labor zip codes, but also exported its inflation, thereby destroying US credibility, trust and influence at the same rate America destroyed the inherent purchasing power of its so-called “strong dollar.”

The Real Cost of Only Bad Options Ahead

So, what can the Fed-directed/complicit U.S. do going forward in its pyric financial war against a changing, emerging East?

Well, it can send more debased money and scarce energy to its allies in the EU and Japan to avoid disaster there, which can only mean more not less inflation from sea to shining sea in the US.

Or, perhaps America’s allies in Brussels or Tokyo could cry “uncle” and reach a separate energy agreement with the Eastern nations who actually have the energy they need, an option which not only keeps the folks of the EU and Japan warmer, but improves their embarrassing trade imbalances (above) which resulted from the demands of Biden’s unofficial caretakers rather than the demands of realpolitik.

Of course, any such détente or separate arrangement would have to be paid for with printed euros and Yen, only adding to the global inflationary swamp our central bankers have created since the invention of the first mouse-click money printer.

As a final option, of course, Europe and Japan could simply stay the Western course and suffer an economic and currency crash (as the Yen hits 50-year lows) which would make 2020 or even 2008 seem like pleasant memories.

The West: Marching Toward a Breaking Point (and Pivot)

Without the benefit of a crystal ball or insider-influence within DC, Brussels or even Davos, one can only speculate rather than predict future events as dictated by current political charlatans.

Perhaps Japan and the EU will join the ever-increasing trend as well as crowd toward de-dollarization and reach a separate peace (i.e., trade arrangement) with the East on energy imports.

Equally likely, as well as mathematically essential, is that the Fed, after feigning concern for inflation (which they in fact needed to inflate away Uncle Sam’s bar tab), will pause and then pivot its failed QT policies by early 2023 and bring the USD and interest rates (via YCC) down to levels essential to combat a recession which they pretend doesn’t exist.

Despite all the fake, real, twisted, straight or bent words, facts and policies emerging today, the West in general and the US in particular cannot escape the natural laws of debt nor the hard realities (as well as consequences) of pretending that more debt, paid for with increasingly debased, mouse-clicked currencies, is a viable policy rather than an open comedy, as well as insult to the long-forgotten science of economics.

Once the reality of math supersedes the current DC policy of fluff, distraction and finger-pointing, the USD will come down, bond markets will be further “accommodated” and currencies will be increasingly debased.

At that looming turning point, of course, those holding gold will see its recent lows race toward record highs.

Why so certain?

Because, math, history and common sense have shown us (from the Ming Dynasty or 3rd century Rome, to 18th century France, 20th century Weimar and 21st century America) that all debt-soaked, decadent and fiscally wayward nations destroy their fiat currencies without exception, and the “modern” West will be no exception.

Not at all.

END

3.Chris Powell of GATA provides to us very important physical commentaries

Heading for a market crash. Read why

Craig Hemke: a must read…

(Craig Hemke)

Craig Hemke at Sprott Money: We’re still on ‘Crash Watch’

Submitted by admin on Tue, 2022-09-20 20:53Section: Daily Dispatches

By Craig Hemke TF Metals Report via Sprott Money, Toronto Tuesday, September 20, 2022

Through September we have been on “Crash Watch” over concerns that a global equity market drop could lead to a liquidity-driven margin call across all asset classes.

The watch continues through this week’s Federal Open Market Committee meeting and then into October. …

What are the conditions that prompted the watch? Here are just a few:

— The Fed draining liquidity via “quantitative tightening.

— Sharply higher interest rates in the United States and globally.

— Concerns that selling in the U.S. treasury market could accelerate uncontrollably.

— The soaring U.S. dollar index.

— Commodity collateral issues in China and elsewhere.

— Yen and yuan plunging versus the dollar.

— Positive real interest rates when measured versus inflation expectations. …

Countries are smart: they are taking their Russian gold and sending it to Switzerland for restamping.

(Spence/BloombergNews/GATA)

Swiss imports of Russian gold rise to most since April 2020

Submitted by admin on Tue, 2022-09-20 21:17Section: Daily Dispatches

By Eddie Spence Bloomberg News Tuesday, September 20, 2022

Switzerland’s imports of Russian gold surged to the highest in more than two years, a sign that more old bullion from the country may be being remelted to make it easier to sell.

About 5.7 tons — worth $324 million — of Russian metal was imported by the refining hub in August, according to data from the Swiss Federal Customs Administration. That’s the most since April 2020.

The shipment was Russian metal that arrived from the UK, the customs administration said in a statement today. Swiss customs data show the last place the precious metal was refined, rather than where it was last shipped from.

Russia’s gold has become taboo since the country invaded Ukraine earlier in the year. New Russian gold has been sanctioned by the United States, European Union, and Switzerland, but bars exported from the country before Aug 4 are not subject to the import ban, the customs authority said. …

In my latest YouTube video, I talk about my journey to get an official investigation by ASIC.

It took me a direct investment of $AUD 50,000 to complete my own 9-month investigation which resulted in me submitting a 608 page report of alleged misconduct to the Australian Securities and Investments Commission (ASIC) in April 2022.

With chances of less than 1% and with no legal expertise or law enforcement experience, I was able to get ASIC to confirm 7 weeks ago (in late July 2022) that an official investigation had commenced.

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.0478

OFFSHORE YUAN: 7.0546

SHANGHAI CLOSED: DOWN 5.23 PTS OR 0.17%

HANG SENG CLOSED DOWN 336.60 PTS OR 1.79%

2. Nikkei closed DOWN 375.79 PTS OR 1.36%

3. Europe stocks SO FAR: MOSTLY GREEN

USA dollar INDEX UP TO 110.47/Euro FALLS TO 0.99073

3b Japan 10 YR bond yield: RISES TO. +.249/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 144.03/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.886%***/Italian 10 Yr bond yield FALLS to 4.143%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.034%…** DANGEROUS

3i Greek 10 year bond yield FALLS TO 4.43//

3j Gold at $1675.00 silver at: 19.56 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 5/100 roubles/dollar; ROUBLE AT 60.65//

3m oil into the 85 dollar handle for WTI and 92 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 144.03DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this .9630–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9542well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

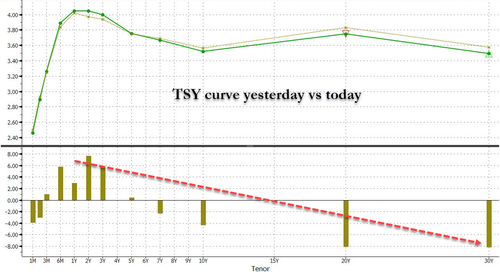

USA 10 YR BOND YIELD: 3.542 DOWN 3 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.546 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,32…GETTTING DANGEROUS

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Neurotic Markets Swing Ahead Of Fed Decision, Eyeing Ukraine War Escalation

WEDNESDAY, SEP 21, 2022 – 07:45 AM

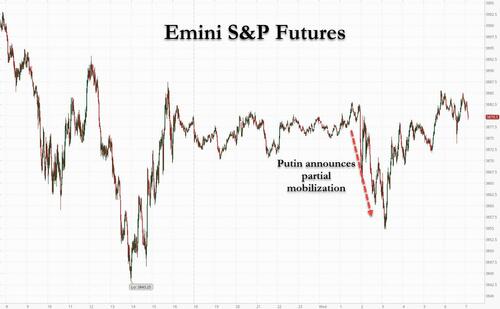

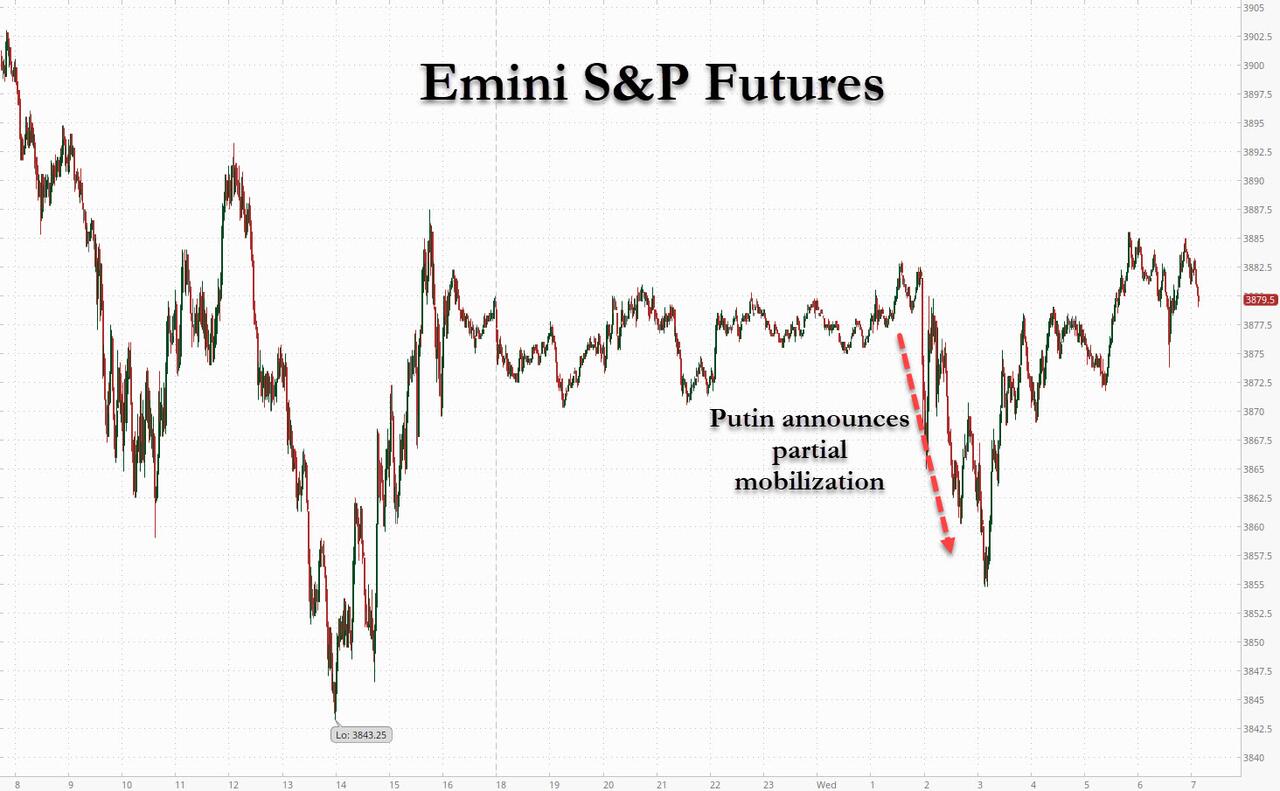

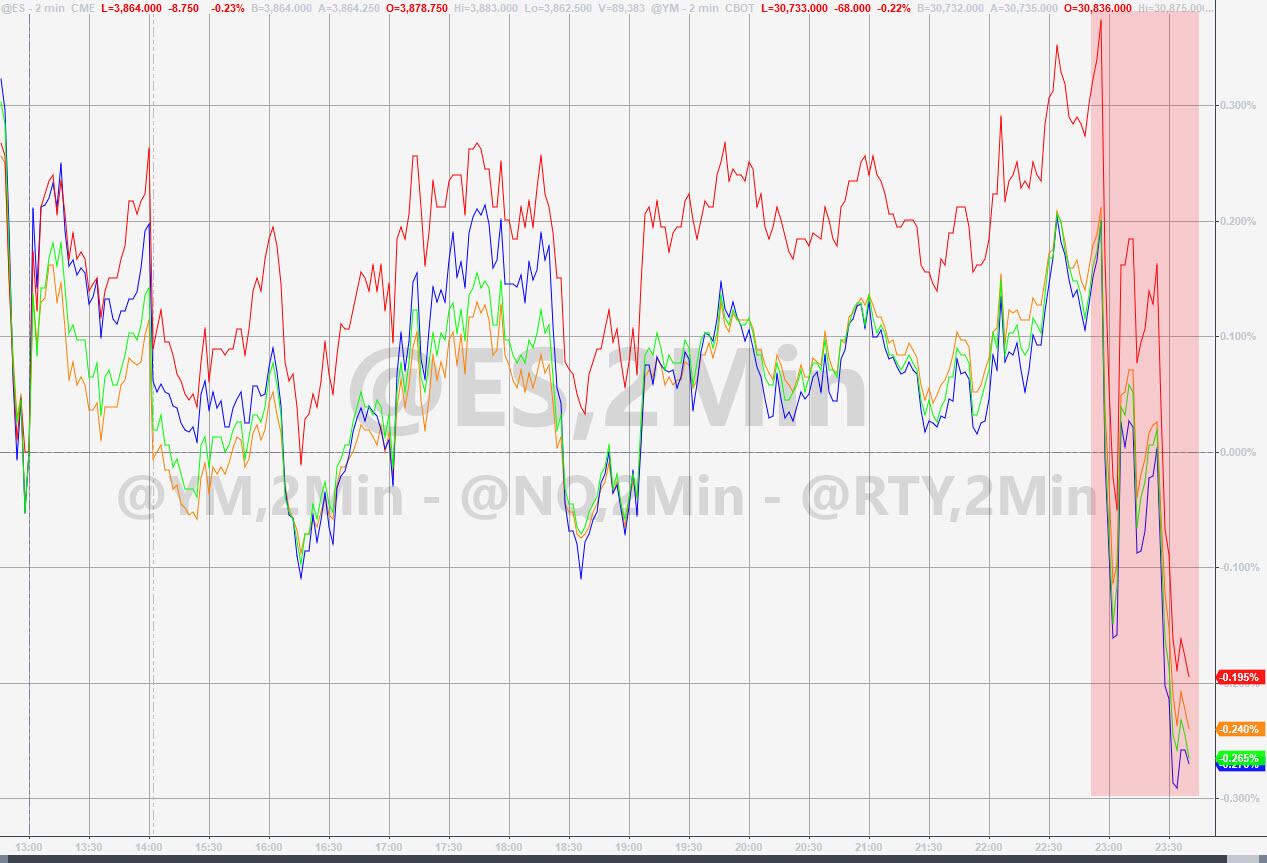

With traders nervously doing nothing ahead of today’s FOMC meeting, where Powell will announce a 75bps rate hike but all attention will be on whether the 2023 median dot (which as we previewed will unleash havoc if it comes above 4.5% which is where market expectations top out for this hiking cycle), today’s extremely illiquid market got an extra jolt of volatility just before the European open when shortly after 2am ET Vladimir Putin delivered his postponed message to announce a “partial mobilization” over the Ukraine war. The news slammed stocks, yields, and the euro while sending oil and commodities sharply higher. And while the initial spike lower has reversed and futures are modestly in the green now, there is zero liquidity right now and the smallest sell program could topples risk assets.

As of 7:15am ET, US futures pointed to a recovery from Tuesday’s tumble on anxiety policy makers are hoping to spark a recession in their zeal to subdue price pressures. S&P futures were up 0.2% after trading down 0.6% earlier, with Nasdaq futures 0.1% in the green. 10Y yields dipped 3bps to 3.54% even though the USD was higher and bitcoin fluctuated between losses and gains.

In premarket trading, the MIC won again with US defense stocks rising amid after Russian President Vladimir Putin declared a “partial mobilization” with the Kremlin also moving to annex occupied regions of Ukraine. Northrop Grumman +1.9%, Lockheed Martin +2.8% and Raytheon +2.5%. Oil and gas shares also rose in US premarket trading, benefiting from a surge in crude prices after Putin ordered a partial mobilization to hold on to disputed territories in Ukraine. Exxon +1.2%, Devon Energy +2%, Marathon Oil +1.8%, Occidental Petroleum +1.9%, Schlumberger +1.5%. Other notable premarket movers:

Stitch Fix (SFIX US) shares are down 10% in premarket trading after the personal styling company issued a weaker-than-expected 4Q update and disappointed analysts with its FY23 outlook. At least two analysts cut their PT on the stock

Keep an eye on Oxford Industries (OXM US) as Citi upgrades it to neutral in note, citing the apparel company’s continued momentum and “attractive” acquisition of the Johnny Was brand

Watch Coty (COTY US) as the company raised its outlook for the current quarter because of stronger-than-expected sales of more expensive fragrances and personal-care products, showing demand for higher-end items remains robust despite rising living costs

The escalation of the Russian war is likely to reverberate across markets, deepening the energy and food crisis, according to Ales Koutny, portfolio manager at Janus Henderson Investors. Putin’s land grab and military escalation comes after a Ukrainian counteroffensive in the last few weeks dealt his troops their worst defeats since the early months of the conflict, retaking more than 10% of the territory that Russia held.

“This will continue to put risk assets under pressure, with sentiment playing a significant part for both equities and credit,” Koutny said. “We believe the USD will continue to benefit as the US is isolated from a geographic perspective and more resilient due to the make-up of its economy.”

Turning to today’s main event, Powell is widely expected to boost rates by 75 basis points for the third time in a row, according to the vast majority of analysts surveyed by Bloomberg. Only two project a 100 basis points move.

“There’s been so much speculation about the Fed’s next step that finally having a decision should provide some much needed relief for investors,” said Danni Hewson, an analyst at AJ Bell Plc. “If it sticks to script and delivers another 75 basis point hike markets are likely to rally somewhat, partly because the specter of a full percentage point rise didn’t come to pass.”

European equities also swung higher after posting early losses in the run-up to the Fed meeting; the Stoxx 50 was little changed. FTSE MIB outperforms peers, adding 0.8%, DAX lags, dropping 0.1%. UK stocks climbed and the pound slid after the British government unveiled a £40 billion bailout to help companies with their energy bills this winter amid soaring prices that threaten to put many out of business. Travel, autos and tech are the worst-performing sectors. European defense stocks and energy stocks gain after President Vladimir Putin declared a “partial mobilization” and vowed to use all means necessary to defend Russian territory as the Kremlin moved to annex parts of Ukraine that it’s occupied, threatening to escalate the conflict further. Rheinmetall rises as much as +11%, Thales +6.1%. Energy stocks outperform as oil rallies, with Shell up as much as +3.3% TotalEnergies +3.0%. Here are some other notable premarket movers:

UK homebuilders gain, bucking a broader market decline, following a Times of London report saying Prime Minister Liz Truss will outline a plan to cut stamp duty during Friday’s mini budget

Fortum shares rise as much as 20%, the biggest jump ever, after Germany said it will buy all of the Finnish company’s stock in Uniper at a better-than-expected price of EU1.70 a share. Meanwhile, Uniper slides as much as 39% on the news, its biggest drop ever.

Vodafone shares gain as much as 2.4% after French billionaire Xavier Niel’s 2.5% stake in the telecom company adds to the pressure for the telecom giant to accelerate its M&A push, according to New Street Research

Renault shares drop as much as 4.0% after Bernstein says it remains cautious about the carmaker’s earnings prospects for 2023 following the stock’s recovery from the Russia crisis earlier this year

Autoliv drops as much as 4.7% in Stockholm, to the lowest since mid July, following SEB downgrade in Sept. 20 note citing a “more uncertain” outlook for 2023

Games Workshop shares fall as much as 16%, the most since Jan. 11, after the maker of the Warhammer series of games said pretax profit in the three-month period to Aug. 28 slid to ~£39m from £45m a year earlier

Earlier in the session, Asian stocks declined ahead of an expected interest-rate hike by the Federal Reserve and as Russia’s escalation of war sapped investors’ appetite for risk. The MSCI Asia Pacific Index fell as much as 1.5%, driven by losses in technology shares. The benchmark held the loss as Russia said it was mobilizing more troops for its war against Ukraine. Hong Kong’s Hang Seng Index led declines among regional measures, with notable drops also in Japan, South Korea, Australia and the Philippines. The main gauge of Hong Kong-listed Chinese firms sank into a technical bear market. With a third 75-basis-point rate hike by the Federal Open Market Committee widely expected, some investors have moved to price in an even larger increase. Fed Chair Jerome Powell’s comments on efforts to fight inflation will be closely parsed for clues on the future rate path.

“Asian markets are still uncertain about size of rate hikes in upcoming FOMC meetings including today’s meeting,” said Banny Lam, head of research at CEB International Investment Corp. “Also, recent depreciation of Asian currencies, especially RMB, enlarges the weakness of equity markets.” The dollar’s strength has pushed a gauge of Asian currencies to a 19-year low, prompting global investors to withdraw funds from the region’s emerging stock markets. Central bank decisions are also due this week from Japan, Taiwan, Indonesia and the Philippines. The Asian Development Bank cut its economic growth forecast for China and also lowered its outlook for developing Asia amid rising interest rates, a prolonged war in Ukraine and Beijing’s Covid-Zero policy.

Japanese equities fell as investors await decisions from central banks including the Federal Reserve and the BOJ. The Topix Index fell 1.4% to 1,920.80 as of market close Tokyo time, while the Nikkei declined 1.4% to 27,313.13. Toyota Motor Corp. contributed the most to the Topix Index decline, decreasing 2.4%. Out of 2,169 stocks in the index, 345 rose and 1,734 fell, while 90 were unchanged. “The focus is on the FRB terminal rate and how far the monetary tightening will go,” said Ayako Sera, a market strategist at Sumitomo Mitsui Trust Bank Limited. “They have a strong stance of controlling inflation no matter what happens to the economy and it’s questionable whether they can really do that.”

In Australia, the S&P/ASX 200 index fell 1.6% to close at 6,700.20, with miners and banks weighing the most on the benchmark, as investors positioned for a hefty interest rate hike from a hawkish Federal Reserve. All sectors except communication services declined. In New Zealand, the S&P/NZX 50 index fell 0.6% to 11,498.95

In FX, the dollar headed for a fresh record, rising for a second day as the greenback traded steady to higher against all of its Group-of-10 peers. CHF and JPY are the strongest performers in G-10 FX in haven play, SEK and EUR underperform. Sweden’s krona suffered the steepest loss among G-10 peers to trade at around 11 per dollar, and is set for its longest slump since June, one day after the . The euro plunged as much as 0.9% to $0.9885, a two-week low, after Vladimir Putin threatened to step up his war in Ukraine. Bunds and Italian bonds advanced, outperforming Treasuries on haven buying and snapping two-day declining streaks. The pound dropped to a fresh 37-year low against a broadly stronger US dollar. Data showing a rise in UK government borrowing also weighed on sterling.

The offshore yuan fell to the lowest against the greenback since mid 2020, even after the People’s Bank of China set the daily reference rate for the currency stronger-than-expected for a 20th day.

In rates, Treasuries advanced, with yields falling up to 4bps, led by the belly of the curve trailing bigger gains for most European bond markets after Russia’s Putin mobilized more troops for Ukraine invasion and referenced nuclear capabilities. US 10-year yields around 3.55%, richer by ~2bp on the day and trailing comparable bunds by ~1bp in the sector; gilts lag by ~3bp; 2s10s curve is flatter by ~2bp, 5s30s by ~1bp. Euro-area bonds advanced, with the German 10-year yield dropping three basis points to 1.89%. Gilts 10-year yield down 2bps to 3.27%.

In commodities, WTI drifts 2.7% higher to trade near $86.17. Spot gold rises roughly $9 to trade near $1,674/oz.

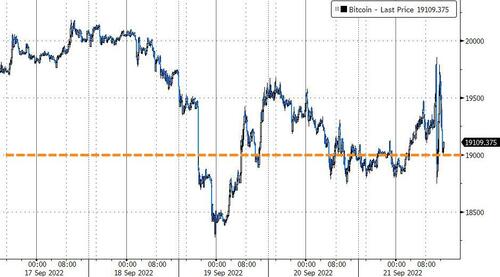

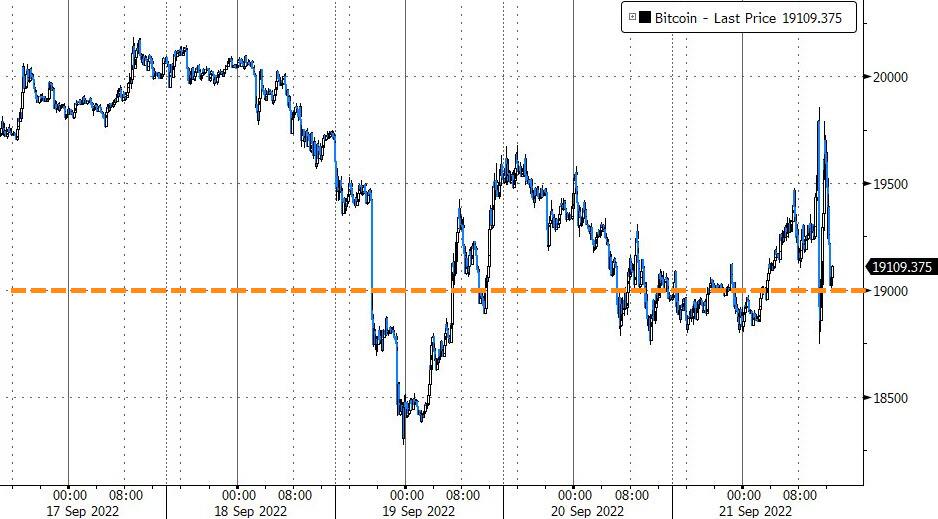

Crypto markets saw a leg lower following the Putin-induced risk aversion, with Bitcoin still under the $19,000 mark.

In terms of the day ahead, the highlight will be the Fed’s policy decision and Chair Powell’s press conference. We’ll also hear from ECB Vice President de Guindos, and on the data side we’ll get US existing home sales for August.

Market Snapshot

S&P 500 futures little changed at 3,874.75

STOXX Europe 600 up 0.3% to 404.48

MXAP down 1.4% to 148.38

MXAPJ down 1.4% to 485.75

Nikkei down 1.4% to 27,313.13

Topix down 1.4% to 1,920.80

Hang Seng Index down 1.8% to 18,444.62

Shanghai Composite down 0.2% to 3,117.18

Sensex down 0.2% to 59,574.87

Australia S&P/ASX 200 down 1.6% to 6,700.22

Kospi down 0.9% to 2,347.21

German 10Y yield little changed at 1.85%

Euro down 0.7% to $0.9901

Brent Futures up 2.6% to $93.00/bbl

Gold spot up 0.4% to $1,670.80

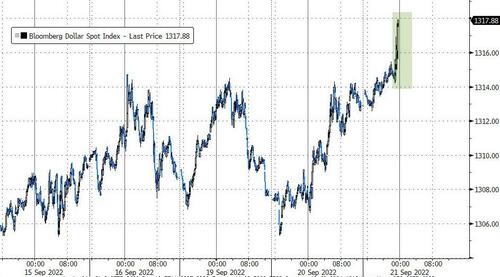

U.S. Dollar Index up 0.51% to 110.77

Top Overnight News from Bloomberg

The US dollar’s rally is at risk of a reversal if the Federal Reserve sets its interest-rate outlook at a lower level than traders are betting on after market-implied expectations for the so-called dot plot jumped this month

Currency traders are girding for the biggest price swings in months in the build up to this week’s crucial Federal Reserve and Bank of Japan policy decisions

Some investors have a message for anyone looking to bet big before one of the most pivotal Federal Reserve policy meetings of this year: don’t, or risk getting burned

The ECB faces a delicate balancing act as it seeks to address record euro-zone inflation while the economy weakens, according to European Central Bank Vice President Luis de Guindos

The British government unveiled a multibillion-pound bailout to help companies with their energy bills this winter amid soaring prices that threaten to put many out of business

Prime Minister Liz Truss will cut the rates of stamp duty for UK home purchases as the government attempts to stimulate growth, The Times of London reported. Shares of UK homebuilders climbed

China’s current interest rates are “reasonable” and provide room for future policy action, the People’s Bank of China said, adding to expectations it may resume lowering rates in coming months

A right-wing coalition is widely expected to win Italy’s election on Sunday. Such an outcome may raise doubts over the path of reforms that are a condition for the country to receive EU funds to hasten its post-pandemic recovery

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded lower as the region followed suit to the global risk aversion heading into today’s FOMC policy announcement and amid heightened geopolitical concerns surrounding Ukraine as several separatist regions plan to hold a referendum to join Russia, while Russian President Putin is to address the nation in which many expect him to call for a mobilisation. ASX 200 declined with the commodity-related sectors and tech leading the downturn seen across all industries. Nikkei 225 was subdued ahead of central bank announcements including the BoJ which began its 2-day meeting. Hang Seng and Shanghai Comp were also negative with underperformance in Hong Kong amid tech weakness and with sentiment not helped by the US FCC adding more companies to its national security threat list.

Top Asian News

Asian Development Bank cut its Developing Asia growth forecast for 2022 to 4.3% from 5.2% and for 2023 to 4.9% from 5.3%, while it cut its China growth forecast for 2022 to 3.35 from 5.0% and for 2023 to 4.5% from 4.8%.

FCC added China Unicom (762 HK) to its national security threats list.

North Korean leader Kim sent a message to Chinese President Xi and said that ties with China are to reach a new high stage, according to state media.

RBA Deputy Governor Bullock said policy is not restrictive as yet and is looking at opportunities to slow hikes at some point, while she noted concerns about the health of China’s economy, zero-COVID policy and property market.

RBA announced its review of the pandemic bond-buying program (BPP) in which it found that it should only be used in extreme circumstances and said it recorded large mark to market losses on BPP bonds in 2021/22, while it plans to hold BPP bonds to maturity and receive face value to offset accounting losses, according to Reuters.

Stocks in Europe have clambered off worst levels with the region now trading mixed on the eve of the FOMC following initial Russian-induced downside. Overall sectors are now more mixed, and the earlier defensive bias has somewhat dissipated. Stateside, after the dust settled and earlier moves have been trimmed, with US equity futures now trading on either side of the unchanged mark.

Top European News

UK PM Truss is to tell the UN General Assembly that she will lead a new Britain for a new era and will call on democracies to harness the power of cooperation seen since Russia’s invasion of Ukraine “to constrain authoritarianism”, according to Downing Street. Furthermore, PM Truss is to tell the UN that Britain will no longer be dependent on those who seek to weaponise the global economy and will argue that the free world must prioritise economic growth and security, according to Reuters and Sky News. Furthermore, PM Truss is to launch a new defence review and call on Russian reparations, according to FT.

UK PM Truss is to announce plans to cut stamp duty in the mini-budget this week in an effort to drive economic growth, according to The Times.

ECB SSM member McCaul said the ECB is particularly concerned about banks that are heavily exposed to highly vulnerable corporates with a weak debt servicing capacity.

ECB’s de Guindos said FX rate is one of the most important variables that need to be looked at carefully.

FX

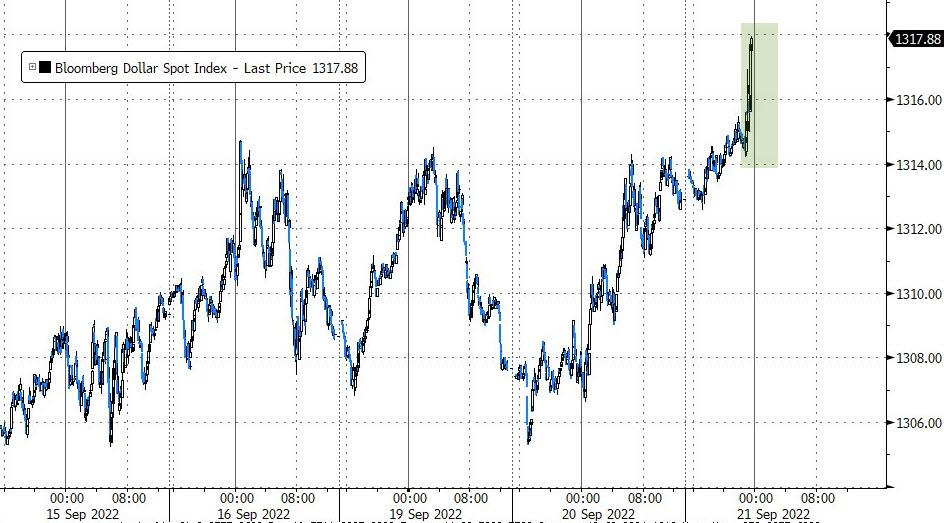

USD bid on risk-aversion pre-FOMC, though the DXY has since eased from the fresh YTD high at 110.87.

Amidst this, the EUR slipped below 0.99 and away from hefty OpEx with G10 peers broadly softer amid the above USD move.

However, petro-fx bucks the trend given the pronounced crude rally and has seen the CAD and NOK derive modest upside.

PBoC set USD/CNY mid-point at 6.9536 vs exp. 6.9539 (prev. 6.9468).

BoC’s Beaudry said the bank will continue to do whatever is necessary to restore price stability and maintain confidence it can meet the 2% target, while Beaudry thinks August inflation data is still too high but added that the data shows we are headed in the right direction. Beaudry also stated that to avoid de-anchoring and to bring inflation sustainably back to target, some suggested a substantial slowdown or even a recession be engineered.

Fixed Income

A concerted initial bid for core benchmarks driven by broad risk-aversion, lifting Bund to a unsuccessful test of 142.00 briefly.

Though, as action settles post-Putin and pre-Fed EGBs have backed away from best levels though retain a positive foothold.

Note, it is worth caveating that today’s upside is well within existing parameters for the week – given the pronounced hawkish action on Tuesday.

10 year T-note is hovering on the 114-00 handle within a 114-07+/113-27+ band and awaiting the Fed & Chair Powell.

Commodities

The crude complex has been propped up by the escalation in rhetoric from Russia.

US Private Inventory Data (bbls): Crude +1.0mln (exp. +2.2mln), Cushing +0.5mln, Gasoline +3.2mln (exp. -0.4mln), Distillates +1.5mln (exp. +0.4mln).

Spot gold caught a bid despite the firmer Dollar on the back of post-Putin haven demand.

LME copper has given up its earlier gains as the Dollar gained and sentiment soured.

US Event Calendar

07:00: Sept. MBA Mortgage Applications +3.8%, prior -1.2%

10:00: Aug. Existing Home Sales MoM, est. -2.3%, prior -5.9%

10:00: Aug. Home Resales with Condos, est. 4.7m, prior 4.81m

Markets are often in a holding pattern when we arrive at Fed decision days, with investors waiting for the policy announcement before the big moves take place. But the last 24 hours have been a very different story, with the selloff accelerating thanks to concerns that the Fed and other central banks still have plenty of hawkish medicine left to deliver. See my CoTD here yesterday for the 500bps of hikes from major central banks expected between yesterday and lunchtime tomorrow. As I also showed the ratio of global hikes to cuts now stand at 25:1, this hasn’t got above 5:1 in the 25 years I have comprehensive global data. Email jim-reid.thematicresearch@db.com if you want to be on the daily CoTD list.

Those rate hike jitters were present from early in the session yesterday after Sweden’s Riksbank unexpectedly announced a bumper 100bps hike, which came shortly after a stronger-than-expected print on German producer prices for August. In the meantime, the latest on the Ukraine situation didn’t help sentiment either, as it was announced that referendums would be held later this week in the Russian-occupied regions on whether they should be part of Russia.

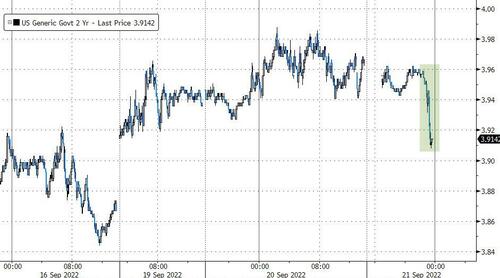

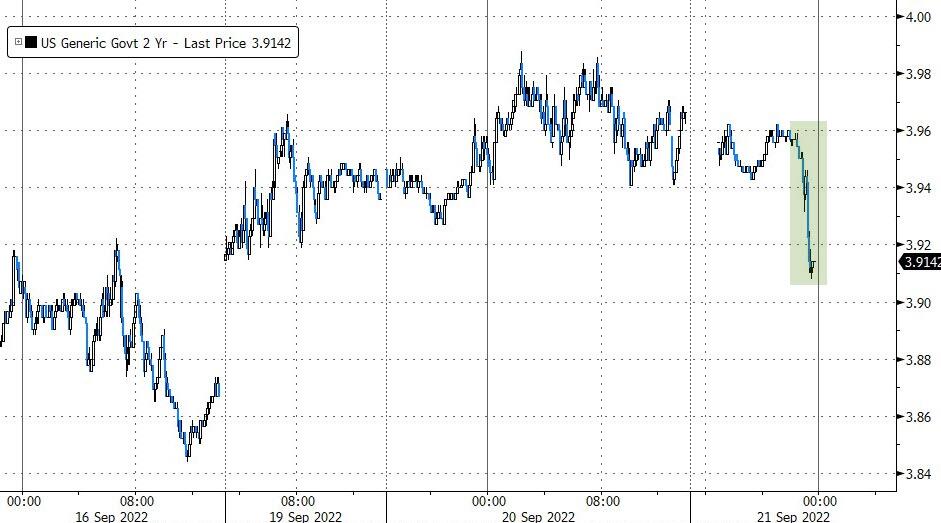

By the close of trade, this had led to a very challenging day across the major asset classes, with little respite for investors anywhere. In particular, there were some big moves on the rates side as Treasury yields hit their highest levels in years, with the 10yr Treasury yield up +7.3bps to a post-2011 high of 3.56% after trading as much as +10bps higher, intraday. The 2yr followed a similar pattern, increasing as much as +5.2bps intraday before ending the day +3.1bps higher at 3.97%, not quite breaching the 4% mark in trading, which would have been for the first time since 2007. This morning in Asia, yields on 10yr USTs (-0.59 bps) are fairly stable.

To counter higher bond yields, the Bank of Japan (BOJ) in an unscheduled government bond buying operation this morning, announced that it would purchase 150 billion yen ($1.04 billion) of debt with a remaining life of five to 10 years, and 100 billion yen of securities maturing in 10 to 25 years. The fresh buying would be in addition to the central bank’s already existing daily offer of buying unlimited quantities of 10yr JGBs at 0.25%. However, the response was muted as the Japanese yen was trading flat at about 143.8 against the US dollar, still in the vicinity of a 24-year historical low as we go to print. Debate around the BoJ’s defence off its YCC policy will only intensify as global yields are under pressure. One to watch again.

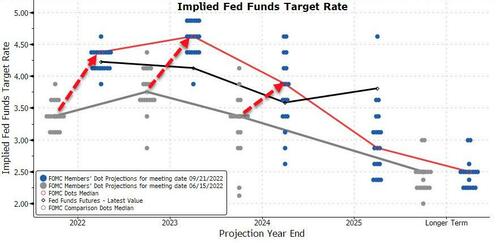

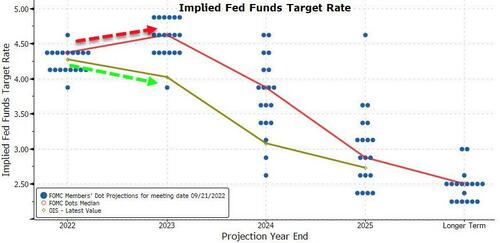

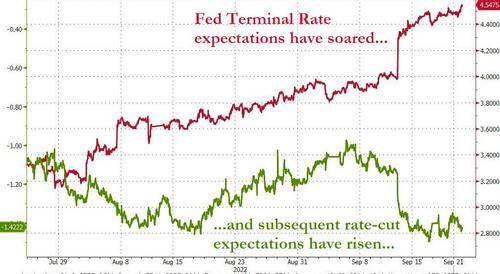

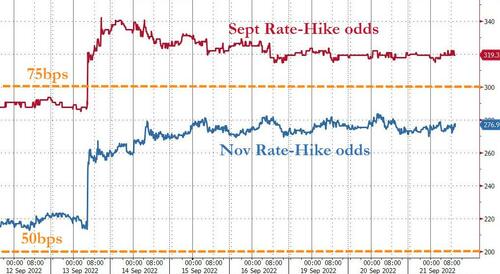

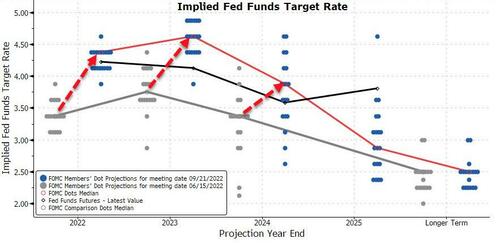

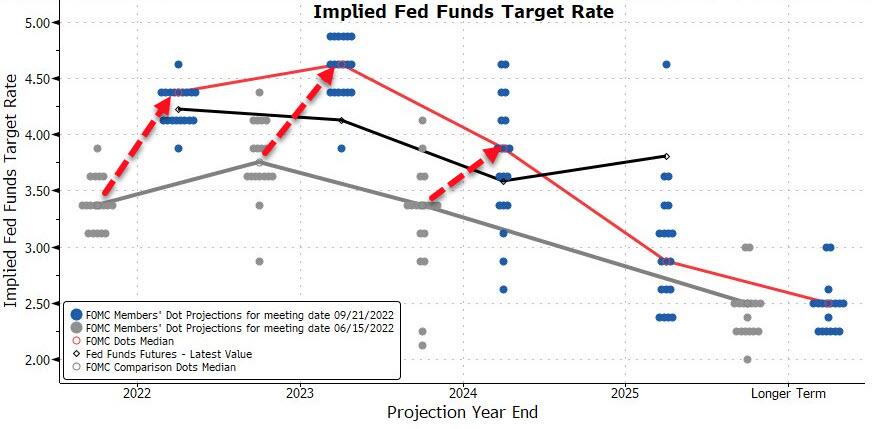

Yesterday’s bond losses come against the backdrop of the Fed’s decision today at 19:00 London time, where futures are fully pricing in a third consecutive 75bps hike. That’s quite the turnaround since the last meeting in July, when markets initially latched on to a dovish interpretation after Chair Powell said “it likely will become appropriate to slow the pace of increases”, which led to an easing of financial conditions following the meeting and well into August. However, no such slowdown is in sight following last week’s CPI print, which shut down any lingering questions about a slower pace of hikes for the time being. In fact, any doubts over today’s decision are all about whether the Fed might go even faster and hike by 100bps, with futures currently pricing in a 18% chance of such a move. So clearly not dismissing the possibility, although the absence of “well informed” journalist articles preparing the ground for 100bps speaks volumes

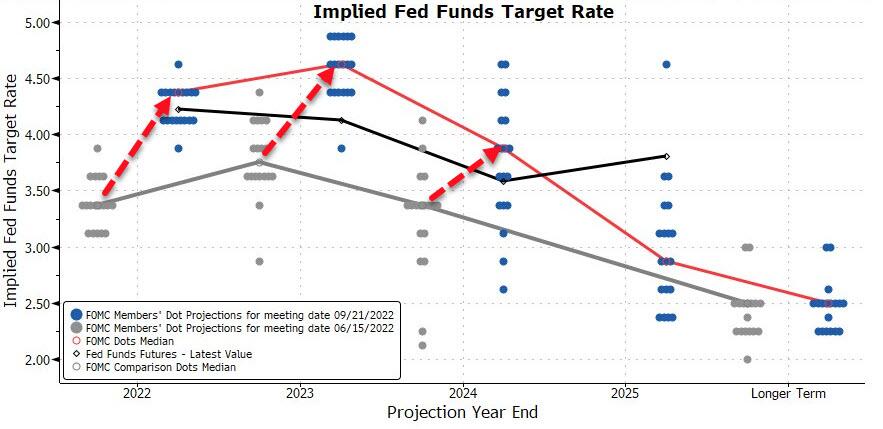

Our US economists’ expectations (link here) are in line with market pricing today, and they expect a 75bps move that’ll be followed up with another 75bps hike in November. One thing to keep an eye out for will be the latest Summary of Economic Projections, which they expect will signal more pain in the labour market in order to tame inflationary pressures, with an upgrade to their unemployment forecasts. We’ll also get a first look at the 2025 dot plot, which they think will show the Fed funds rate at 3.4%, so still above their long-run estimate for the nominal fed funds rate, and they think the tone in Chair Powell’s press conference will sound more like the hawkish messaging out of Jackson Hole rather than the dovish signals from July.

Those hawkish expectations meant that risk assets continued to struggle alongside sovereign bonds, with the S&P 500 (-1.13%) very nearly ending up back in bear market territory. It was much the same story in Europe, where the STOXX 600 (-1.09%) lost ground for a 6th consecutive session for the first time since the June slump, and is within 1% of the YTD lows. Germany’s DAX (-1.03%) is now down by more than -20% on a YTD basis again. Interestingly, European equities had initially opened higher on the day, with the STOXX 600 up +0.96% at its peak. However, sentiment turned around the time we heard of the Riksbank’s policy decision, as they unexpectedly hiked by 100bps, rather than the 75bps expected by the consensus, whilst also signalling further rate hikes ahead. In turn, that fuelled speculation that the Fed might also pull off a surprise move, even if that’s still far from the market’s base case.

Staying on Europe, it’s worth noting that the rise in sovereign bond yields there were more dramatic than those seen in the United States. For instance, yields on 10yr bunds (+12.1bps) rose to a post-2014 high of 1.92%, whilst those on BTPs (+10.1bps) hit a post-2013 high of 4.18%. Following the end of European bond trading, ECB President Lagarde noted that inflation was much higher and persistent than anticipated, which has driven the front-loading of ECB rate hikes we’ve seen to date. She reiterated the ECB plans to raise rates over the next few meetings, and will size those hikes on a meeting-by-meeting basis. Like some Fed speakers, she noted the ECB cannot take anchored inflation expectations for granted, but drew contrast to the situation in the United States by spending a lot of her speech outlining why European inflation was not as demand-driven, but a result of supply shocks. I personally would say that’s up for debate with unemployment at the lowest since the Euro came into being and wage growth high.

Gilts were the biggest underperformer ahead of tomorrow’s Bank of England decision, with 10yr yields up +15.4bps to a post-2011 high of 3.29%. In terms of market pricing for that decision tomorrow, overnight index swaps are pricing in 65.2bps worth of hikes, so nearly equidistant between 50bps and 75bps.

Whilst central banks are in focus this week, there was significant news from Ukraine as four Russian-controlled regions will be holding referendums this week on whether they should be a part of Russia. They’re set to happen from September 23-27, and will take place in the regions of Donetsk and Luhansk, as well as in Kherson and Zaporizhzhia. Further, as reported in Bloomberg, the concern is that Russia is moving toward a more full mobilisation, which would only lead to a further entrenchment of the war. All this news doesn’t suggest that the peaceful end of the war is imminent and that the counter offensive successes by Ukraine 10 days ago might have escalated tensions as was feared at the time. We expect to hear public remarks from President Putin later this morning, so more to come on what already promises to be a big macro day for markets.

Asian equity markets are continuing with their downward trend this morning. Among the major indices, the Hang Seng (-1.66%) is the biggest laggard in early trade, reversing the previous session’s recovery. Elsewhere, the Nikkei (-1.37%), Shanghai Composite (-0.58%), the CSI (-0.98%) and the Kospi (-0.95%) are all trading in the red.

US stock futures are fluctuating with contracts on the S&P 500 (+0.09%) and NASDAQ 100 (+0.07%) just above flat but with DAX futures (-0.29%) lower.

In terms of yesterday’s data releases, US housing starts rose by more than expected in August, reaching an annualised rate of 1.575m (vs. 1.45m expected), while the prior month was revised down to 1.404m from 1.446m. Meanwhile, building permits continued to fall, down to an annualised 1.517m (vs. 1.604m expected), which is their lowest level since June 2020. The net impact of the housing data had the Atlanta Fed’s GDPNow model revise down third quarter growth to 0.3% from 0.5% after downgrading residential investment growth to -24.5% from -20.8%. So, we’re a surprise or two away from a third straight quarter of negative headline GDP growth, and yet more equivocation about why the US currently is or is not in a recession.

Otherwise, German producer prices were up by +45.8% in August on a year-on-year basis (vs. +36.8% expected). That said, there was some weaker-than-expected inflation from Canada, where CPI fell to +7.0% year-on-year (vs. +7.3% expected).

In terms of the day ahead, the highlight will be the Fed’s policy decision and Chair Powell’s press conference. We’ll also hear from ECB Vice President de Guindos, and on the data side we’ll get US existing home sales for August.

AND NOW NEWSQUAWK

Initial Putin induced risk-off has dissipated ahead of the FOMC – Newsquawk US Market Open

WEDNESDAY, SEP 21, 2022 – 06:30 AM

Stocks in Europe have clambered off worst levels with the region now trading mixed on the eve of the FOMC following the initial Russian-induced downside

US equity futures are modestly firmer, but near the unchanged mark overall

USD bid on risk-aversion pre-FOMC, though the DXY has since eased from the fresh YTD high at 110.87

The concerted initial bid for core benchmarks has waned with yields subdued

Crude propped up by the Russian rhetoric and relatively resilient to the paring of initial moves elsewhere

Specifically, Russian President Putin declared a partial mobilisation and used “nuclear” language in a threat to the west

Looking ahead, highlights include the FOMC Policy Announcement & Press Conference

Or why not try Newsquawk’s squawk box free for 7 days?

LOOKING AHEAD

FOMC Policy Announcement/Press Conference.

GEOPOLITICS

RUSSIA-UKRAINE

Russian President Putin, in his televised speech to the nation this morning, announced that partial mobilisation will begin today (September 21st) whilst threatening the west with “All means of destruction, including nuclear ones”, and warned that this is not a bluff. The Russian Defence Minister Shoigu was interviewed in the minutes after Putin and suggested Russia is not fighting just against Ukraine, but NATO and the collective West.Full Newsquawk analysis, details and reaction available here

“Negotiations with Ukraine will become impossible after the entry of Donbass into Russia”, according to Tass citing the head of the State Duma Committee on International Affairs.