SEPT 20/GOLD CLOSED DOWN $6.65 TO $1663.05//SILVER CLOSED DOWN 18 CENTS TO $19.17//PLATINUM ROSE BY $2.45 TO 921.15//PALLADIUM CLOSED DWON $69.10 TO $2147.10//UPDATES ON EUROPE/GERMANY’S ECONOMIC WOES RE ENERGY//HUNGARY’S GAS STATIONS WILL RUN OUT OF GAS IN ONE WEEK//EU THREATENS HUNGARY AGAIN AS THEY REFUSE TO TOE THE LINE//SWEDEN SHOCKS MARKETS WITH A 100 BASIS POINT INTEREST RATE RISE//RUSSIA VS UKRAINE UPDATES//COVID UPDATES//VACCINE MANDATES//DR PAUL ALEXANDER///VACCINE IMPACT//VACCINE INJURY//ATLANTA FED LOWERS Q3 GDP TO ONLY .3% YEAR/YEAR: IT WILL BE BELOW PAR BY THE END OF THE QUARTER//HUGE CRASH IN HOUSING PERMITS AS THE HOUSING SECTOR IN THE USA IMPLODES//SWAMP STORIES FOR YOU TONIGHT//

total notices so far: 6105 contracts for 610,500 oz (18.989 tonnes)

SILVER NOTICES: 3 NOTICES FILED FOR 15,000 OZ/

total number of notices filed so far this month 6462 : for 32,310,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $6.65

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: //// A WITHDRAWAL OF 2.90 TONNES FROM THE GLD/

INVENTORY RESTS AT 957.95 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN $.18

AT THE SLV// ://GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV//: STRANGE@@!! A DEPOSIT OF 1.475 MILION OZ INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 479.213 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 1526 CONTRACTS TO 132,685. AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GIGANTIC LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR TINY $0.02 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.02) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC SILVER LONGS BUT WE DID HAVE A MASSIVE SILVER SHORT COVERING AS WE HAD A HUGE LOSS OF OF 1376 CONTRACTS ON OUR TWO EXCHANGES. THE SPECS ARE FLEEING AS FAST AS THEIR LITTLE FEET WILL CARRY THEM.

WE MUST HAVE HAD: I) STRONG SPECULATOR SHORT COVERING ////CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 10,000 OZ QUEUE JUMP / // V) HUGE SIZED COMEX OI LOSS/(//CONSIDERABLE SPEC LIQUIDATION/)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -29

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTRACTS for 13 days, total 11,732 contracts: 58.660 million oz OR 4.512 MILLION OZ PER DAY. (902 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 58.660 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 58.660 MILLION OZ///

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1526 DESPITE OUR TINY $0.02 LOSS IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 150 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /GOOD BANKER ADDITIONS A// CONSIDERABLE NET SPEC SHORT COVERINGS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 10,000 OZ QUEUE JUMP // .. WE HAD A VERY STRONG SIZED LOSS OF 1376 OI CONTRACTS ON THE TWO EXCHANGES FOR 6.735MILLION OZ AS..THE SPECS STILL ARE BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 3 NOTICE(S) FILED TODAY FOR 15,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 2082 CONTRACTS TO 467,551 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY:+ 75 CONTRACTS.

.

THE FAIR SIZED INCREASE IN COMEX OI CAME DESPITE OUR FALL IN PRICE OF $4.80//COMEX GOLD TRADING/MONDAY / WE MUST HAVE HAD MAJOR SPECULATOR SHORT COVERINGS ACCOMPANYING OUR SMALL SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND //CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 8.401 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 32,100 OZ //NEW STANDING 19.4618 TONNES

YET ALL OF..THIS HAPPENED DESPITE OUR FALL IN PRICE OF $4.80 WITH RESPECT TO MONDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 3199 OI CONTRACTS 9.701 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 1037 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 467,476

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3177 CONTRACTS WITH 2082 CONTRACTS INCREASED AT THE COMEX AND 1037 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3199 CONTRACTS OR 9.701 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1037) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (2082): TOTAL GAIN IN THE TWO EXCHANGES 3119 CONTRACTS. WE NO DOUBT HAD 1) CONSIDERABLE SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS/// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 8.409 TONNES FOLLOWED BY TODAY’S QUEUE. JUMP OF 32,100 oz. 3) ZERO LONG LIQUIDATION//// //.,4) FAIR SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

34,691 CONTRACTS OR 3,469,100 OZ OR 107.90 TONNES 13 TRADING DAY(S) AND THUS AVERAGING: 2669 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAY(S) IN TONNES: 107.90 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 104.67/3550 x 100% TONNES 2.95% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 107.90 TONNES (SLIGHTLY RISING THIS MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT., FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER,FELL BY A HUGE SIZED 1526 CONTRACT OI TO 132,685 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 150 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 150 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1200 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1497 CONTRACTS AND ADD TO THE 150 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF 1376 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 6.880 MILLION OZ

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED UP 6.80 PTS OR 0.22% //Hang Sang CLOSED UP 215.45 PTS OR 1.16% /The Nikkei closed UP 120.77 PTS OR .44% //Australia’s all ordinaires CLOSED UP 1.17% /Chinese yuan (ONSHORE) closed DOWN AT 7.0128//OFFSHORE CHINESE YUAN DOWN 7.0203// /Oil UP TO 85.80 dollars per barrel for WTI and BRENT AT 92,32 / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 2082 CONTRACTS TO 467,551 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR FALL IN PRICE OF $4.80 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A SMALL SIZED EFP (1037 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1037 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :1037 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1037 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED SIZED TOTAL OF 3119 CONTRACTS IN THAT 1037 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 2082 CONTRACTS..AND THIS FAIR GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $4.80. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING SEPT (19.4618),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 19.4618 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $4.80) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A FAIR SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 3119 CONTRACTS // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS TRIED TO COVER ON THEIR POSITIONS////// WE HAVE REGISTERED A FAIR GAIN OF 3119 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR SEPT. (19.4618 TONNES)…

WE HAD 75 CONTRACTS ADDED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3119 CONTRACTS OR 311,900 OZ OR 9.701 TONNES

Estimated gold volume 143,643/// poor//

final gold volumes/yesterday 149,894/ poor

INITIAL STANDINGS FOR SEPT ’22 COMEX GOLD //SEPT 20

Total monthly oz gold served (contracts) so far this month

6105 notices 610,500 OZ 18.989 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

2 customer withdrawals:

i) Out of Brinks: 14,228.678 oz

ii) Out of HSBC 8032.565 oz

total: 22,261.243 oz

total in tonnes: 0.6925 tonnes

Adjustments: 1

Brinks/dealer to customer: 22,859.361 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPT.

For the front month of SEPT we have an oi of 497 contracts having LOST 106 contracts .

We had 427 notices filed on MONDAY so we gained a whopping 321 contracts or an additional 32,100 oz

will stand for gold in this very non active delivery month of September.

October LOST ONLY 239 contracts DOWN to 42,973. Oct is generally a poor active delivery month. It may change!! (Look for a very unusually large delivery month.)

November gained 44 contracts to stand at 329

December lost 1953 contracts DOWN to 378,724

We had 345 notice(s) filed today for 34,500 oz FOR THE SEPT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 345 notices were issued from their client or customer account. The total of all issuance by all participants equate to 345 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 169 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2022. contract month,

we take the total number of notices filed so far for the month (6105) x 100 oz , to which we add the difference between the open interest for the front month of (SEPT 2007 CONTRACTS) minus the number of notices served upon today 345 x 100 oz per contract equals 625,700 OZ OR 19.4618 TONNES the number of TONNES standing in this NON active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month:

No of notices filed so far (6105) x 100 oz+ (497) OI for the front month minus the number of notices served upon today (345} x 100 oz} which equals 625,700 oz standing OR 19.4618 TONNES in this NON active delivery month of SEPTEMBER.

TOTAL COMEX GOLD STANDING: 19.4618 TONNES (A HUMONGOUS STANDING FOR A SEPT ( NON ACTIVE) DELIVERY MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 6462 x 5,000 oz = 32,310,000 oz

to which we add the difference between the open interest for the front month of SEPT(143) and the number of notices served upon today 3 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT./2022 contract month: 6,462 (notices served so far) x 5000 oz + OI for front month of SEPT (143) – number of notices served upon today (3) x 5000 oz of silver standing for the SEPT contract month equates 33,010,000 oz. .

We have an inventory of 43.855 million oz of registered silver at the comex so Sept delivery of 33.010 MILLION OZ represents 75.27% of that category of silver.

If we add August’s final delivery (to Sept) for silver at 5.51 million oz, we have a total of 38.52 million oz delivered upon with a REGISTERED INVENTORY of 43.855 million oz or 87.83% of that category of silver.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

SEPT 13/WITH GOLD DOWN $22.85 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73ONNES FROM THE GLD////INVENTORY RESTS AT 964.91 TONNES

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

AUGUST 31.WITH GOLD DOWN $10.20:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.24 TONNES FROM THE GLD////INVENTORY RESTS AT 973.37 TONNES

AUGUST 30.WITH GOLD DOWN $12.00:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 980.61 TONNES

AUGUST 29/WITH GOLD DOWN $.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD/////INVENTORY RESTS AT 982.64 TONNES

AUGUST 26/WITH GOLD DOWN $26.60; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 25/WITH GOLD UP $9.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 18/WITH GOLD DOWN $5.25: GIGANTIC CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.78 TONNES FROM THE GLD////INVENTORY RESTS AT 985.83 TONNES

AUGUST 17/WITH GOLD DOWN $12.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 992.20 TONNES

AUGUST 16/WITH GOLD DOWN $7.85: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 993.94 TONNES

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

GLD INVENTORY: 957.95 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

SEPT 13/WITH SILVER DOWN $.31 TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.899 MILLION OZ//

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

AUGUST 31/WITH SILVER DOWN 36 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 3.087 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 465.573 MILLION OZ//

AUGUST 30/WITH SILVER DOWN 34 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 1.478 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 470.135 MILLION OZ//

AUGUST 29/WITH SILVER DOWN 7 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY A THE SLV: A WITHDRAWAL OF 2.765 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 470.135 MILLION OZ//

AUGUST 26/WITH SILVER DOWN 39 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 25/WITH SILVER UP 21 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

AUGUST 18/WITH SILVER DOWN 27 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 369,000 OZ INTO THE SLV////INVENTORY RESTS AT 485.482 MILLION OZ//

AUGUST 17/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.106 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.113 MILLION OZ//

AUGUST 16/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 486.219 MILLION OZ/

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

CLOSING INVENTORY 479.213 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

END

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

Goldman Sachs and Morgan Stanley Have Mysteriously Disappeared from this Week’s Senate and House Banking Hearings

By Pam Martens and Russ Martens: September 20, 2022 ~

There are eight Global Systemically Important Banks (G- SIBS) in the U.S. They are: JPMorgan Chase, Citigroup, Bank of America, Goldman Sachs, Bank of New York Mellon, Morgan Stanley, State Street and Wells Fargo. These are the banks that pose the greatest risk to the stability of the U.S. financial system and are monitored under the Federal Reserve’s stress tests.

Five of those eight banks pose the greatest risk to financial stability because together they hold $200.18 trillion (yes trillion) in notional derivatives (face amount) or 86 percent of all derivatives held by all of the nation’s banks, according to the Office of the Comptroller of the Currency – the federal regulator of national banks. Those banks are: JPMorgan Chase, Citigroup, Goldman Sachs, Morgan Stanley, and Bank of America.

In any Senate Banking or House Financial Services Committee hearing that is going to probe if these mega banks could blow up the U.S. financial system again — as they did in 2008 – these five banks have to be at the table for the hearing to be credible.

But for some reason – which fails to pass the smell test from every angle – Goldman Sachs and Morgan Stanley have gone missing from the witness table at both the hearing on Wednesday at the House Financial Services Committee and at the hearing on Thursday at the Senate Banking Committee. The CEOs of the other banks will be present to be grilled on their most recent crimes.

Adding to the fishy smell, both banks were included at last year’s large bank hearings by the same Committees. This year, instead of Goldman Sachs and Morgan Stanley, new additions to the witness panel have popped up out of the blue. The CEOs of PNC, U.S. Bank and Truist have been added to the witness panel at both the Senate and House hearings, despite the fact that none of these banks have been designated Global Systemically Important Banks; rank anywhere near Goldman Sachs and Morgan Stanley when it comes to derivative exposure; or played any key role in blowing up the U.S. financial system in 2008.

Researchers at the government’s own Office of Financial Research (OFR), created under the Dodd-Frank financial reform legislation of 2010 to monitor systemic risk in the financial system, also share the view that the five Wall Street mega banks referenced above are what Congress and the federal bank regulators need to closely monitor.

In a comprehensive report in February 2015, OFR researchers sounded the alarm that those five mega banks posed enormous risks to U.S. financial stability. Systemic risk scores were based on size, interconnectedness, substitutability, complexity, and cross-jurisdictional activities.

According to the OFR researchers Meraj Allahrakha, Paul Glasserman, and H. Peyton Young:

“The larger the bank, the greater the potential spillover if it defaults; the higher its leverage, the more prone it is to default under stress; and the greater its connectivity index, the greater is the share of the default that cascades onto the banking system. The product of these three factors provides an overall measure of the contagion risk that the bank poses for the financial system. Five of the U.S. banks had particularly high contagion index values — Citigroup, JPMorgan, Morgan Stanley, Bank of America, and Goldman Sachs.”

It’s certainly not that Goldman Sachs or Morgan Stanley have cleaned up their act so much that they no longer need to be a focus of Congressional Committees. As recently as May 6 of this year, Wall Street On Parade reported as follows:

“We’ve been reading SEC filings for more than 35 years. We have to sadly say that the 10-Q that Goldman Sachs filed with the SEC on May 2, for the quarter ending March 31, 2022, shocks even our well-documented assessment of Wall Street as a crime syndicate. Goldman Sachs has listed pretty much everything the firm does as a target of an ongoing investigation, notwithstanding that the company and a subsidiary were criminally charged by the U.S. Department of Justice in the looting and bribery scandal known as 1MDB in October 2020, admitted to the charges, and had to pay over $2.9 billion. The good news is that Goldman Sachs’ Dark Pools are one of the areas it lists as being under a probe.”

On August 4, Goldman Sachs provided the following disclosure when it filed its quarterly report (10-Q) with the Securities and Exchange Commission:

“The firm is cooperating with the Consumer Financial Protection Bureau in connection with an investigation of GS Bank USA’s credit card account management practices, including with respect to the application of refunds, crediting of nonconforming payments, billing error resolution, advertisements, and reporting to credit bureaus.”

According to our review of the complaints filed in the database of the Consumer Financial Protection Bureau, hundreds of Apple credit card holders are alleging being put through a living hell by Goldman Sachs when fraudulent charges are made on their Apple credit card and a host of other problems.

Then there was the report just last Friday by Bloomberg News that the federally-insured online bank operated by Goldman Sachs Bank USA, Marcus, was under investigation by the Federal Reserve. The article provides this bleak assessment of a deposit-taking bank backed by the U.S. taxpayer:

“At mid-year, the bank’s own internal forecast estimated the business would post a record loss of more than $1.2 billion this year.

“The cash burn has gotten all the more painful in recent months as a pandemic-era surge in Wall Street deals subsides, making Marcus a fraught topic among Goldman managers. Investment bankers and traders bracing for job cuts or lower bonuses are competing with a division that was once supposed to break even in 2022, but has instead eaten up more than $4 billion since inception in 2016. That’s not including Goldman’s acquisition of installment-loans provider GreenSky Inc. in a deal initially valued at more than $2.2 billion last year at what turned out to be the peak of the market for fintech ventures.”

Morgan Stanley is currently under an investigation by the Justice Department for the manner in which it has handled block trades, according to Bloomberg News. It has put several of its traders on leave as that probe continues.

There is also the unanswered question as to how many more Archegos-type of family office hedge fund clients might be lurking under the radar at Morgan Stanley, which owns two federally-insured banks. Morgan Stanley admitted to losing $911 million last year when Archegos blew up with derivatives created by Morgan Stanley and other Wall Street mega banks. See our report: Justice Department and SEC Portray Serially-Charged Banks on Wall Street as Hapless Victims of Archegos Fraud. Nobody’s Buying It.

Last year, the Senate Banking and House Financial Services Committees held their Big Bank hearing in the early spring. We kept asking Committee aides when the hearing was coming this year. We continued to hear back that it will be coming. The mysterious disappearance of Morgan Stanley and Goldman Sachs from this week’s hearings may simply result from the refusal of their CEOs to appear before Congress. Since both firms are under probes, their legions of lawyers might have advised the CEOs to simply decline the invitation to appear.

But that doesn’t answer the question as to why the Committees wouldn’t have demanded their appearance by subpoena. According to the Congressional Research Service, the Senate Banking Committee has adopted a rule that requires a majority vote to issue a subpoena for documents or witnesses. The ranking member of the Senate Banking Committee, Republican Pat Toomey of Pennsylvania, does not seem like a person who would agree to subpoena the CEO of Goldman Sachs to appear. Since 2011, Goldman Sachs ranks as Toomey’s third largest campaign donor.

According to the Congressional Research Service, the Chair of the House Financial Services Committee, Democrat Maxine Waters, can issue a subpoena as long as she first “consults” with the ranking member. Currently that ranking member is the right-wing Republican Patrick McHenry of North Carolina whose top-10 largest campaign donors in the current election cycle include Wall Street mega banks, private equity firms and asset managers, among others.

A different campaign money trail might possibly explain why Goldman Sachs and Morgan Stanley got a pass without a subpoena forcing their presence. Jones Day, the law firm that dominated the Donald Trump administration and sent 12 of its law partners to executive branch positions on the very day that Trump was inaugurated, is also long-time counsel to both Goldman Sachs and Morgan Stanley. Curiously, while Jones Day’s employees and their family members gave 74.62 percent of their campaign donations to Republicans in the 2016 presidential election that put Trump in the White House, in the current campaign cycle 68 percent of their donations have gone to Democrats, for a whopping $338,654 in campaign donations thus far.

According to campaign finance records at the Federal Election Commission, individual partners at Jones Day have made some very generous donations to Democrats. Hilda Galvan, the Partner-in-Charge of Jones Day’s Dallas office, gave a check of $36,500 to the Democratic National Committee in December.

The Democratic Congressional Campaign Committee (DCCC) received a February donation of $10,000 from Edward Nalbantian, Of Counsel at Jones Day, who has a “particular focus on over-the-counter (OTC) derivatives….” Another $5,000 went to the DCCC in February from Cynthia Cwik, who listed her employer as Jones Day although she does not currently appear on its website as a lawyer there. In June of last year, law partner Robert Rawson gave $10,000 to the Ohio Democratic Party. And in September of last year, Jones Day partner in Financial Markets, Linda Hesse, contributed $5,000 to the Democratic Senatorial Campaign Committee (DSCC).

Could it be possible that someone from Jones Day negotiated a pass for Goldman Sachs and Morgan Stanley at this week’s hearings?

Jones Day was outside counsel for the Trump 2016 and Trump 2020 political campaigns and represented Trump in lawsuits seeking to stop votes from being counted in the 2020 election. A New York Times Magazine article last month by David Enrich, with a subtitle of “The untold story of Jones Day’s push to move the American government and courts to the right,” characterized Jones Day as follows:

“Jones Day’s influence seems poised to grow. This year, it has been collecting fees from a remarkable assortment of prominent Republican players: a Trump political-action committee; moderates like Senator Susan Collins; Trump allies like Dr. Mehmet Oz; hard-liners like Representative Kevin McCarthy of California, the House minority leader, and Senator Ron Johnson of Wisconsin — not to mention an assortment of super PACs supporting fringe candidates like Herschel Walker, the former N.F.L. star who is running for a Senate seat in Georgia. [Jones Day partner Noel] Francisco recently represented former Attorney General Bill Barr before the House committee investigating the Jan. 6 attack on the Capitol. McGahn recently began representing Senator Lindsey Graham as he fights a grand jury subpoena to testify about Trump’s efforts to overturn the election results in Georgia.”

The “McGahn” referenced in the above sentence is Don McGahn, a law partner from Jones Day who became Trump’s first White House Counsel. McGahn has returned to Jones Day. Its website says he is now available for “high stakes matters that require navigating and challenging assertions of government authority.”

Who else is it that has attempted to undermine government authority for the last 40 years: Libertarian billionaire Charles Koch and his fossil fuels conglomerate, Koch Industries. Jones Day has a long-term history of legally representing Koch Industries, its subsidiaries and at least one of its front groups, Freedom Partners.

The bottom line here is that as long as Congress fails to pass sweeping campaign finance reform, trust in Congress and the U.S. government will continue to erode and the threats to both democracy in America and its financial system will continue to grow.

GOLD/SILVER

END

3.Chris Powell of GATA provides to us very important physical commentaries

Submitted by admin on Mon, 2022-09-19 21:29Section: Daily Dispatches

By Noah Zivitz BNN Bloomberg Monday, September 19, 2022

Kinross Gold Corp. announced plans to ramp up its share repurchases subsequent to talks with a renowned activist investor and other shareholders.

The Toronto-based miner said in a news release today that it will aim to buy back US$300 million of its shares before the end of this year. It added that it will allocate 75% of excess cash to buybacks in 2023 and 2024.

Kinross said the updated strategy stems from talks with Elliott Investment Management and an unspecified number of other investors. It also cautioned that buybacks in 2023 and 2024 are contingent on the company’s net leverage ratio remaining below the current level, and stated the repurchases would be paused in the event of a ratings downgrade, a significant drop in the price of gold, or major operational setbacks.

An Elliott portfolio manager saluted the Kinross and said the hedge fund will remain in contact with the company.

“Kinross today possesses a high-quality, Americas-focused portfolio with strong potential for future growth through Great Bear, yet it trades at a significant discount to both its peers and to the value of its assets. We believe that with this new capital-allocation framework, Kinross is taking a major step toward closing that gap and realizing the upside potential in its stock,” said Mark Cicirelli, a portfolio manager at Elliott, in the release.

The announcement didn’t include any details about Elliott’s investment in Kinross and a spokesperson couldn’t immediately be reached to confirm the investment manager’s stake.

Elliott’s most recent 13F quarterly filing with the U.S. Securities and Exchange Commission didn’t list Kinross as one of its holdings as of June 30. …

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.0128

OFFSHORE YUAN: 7.0203

SHANGHAI CLOSED: UP 6.80 PTS OR 0.22%

HANG SENG CLOSED UP 215.45 PTS OR 1.16%

2. Nikkei closed UP 120.77 PTS OR .44%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 109.62/Euro FALLS TO 0.9994

3b Japan 10 YR bond yield: RISES TO. +.249/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 143.58/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.913%***/Italian 10 Yr bond yield RISES to 4.189%*** /SPAIN 10 YR BOND YIELD RISES TO 3.056%…** DANGEROUS

3i Greek 10 year bond yield FALLS TO 4.44//

3j Gold at $1667.30 silver at: 19.26 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 24/100 roubles/dollar; ROUBLE AT 59.94//

3m oil into the 85 dollar handle for WTI and 92 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 143.58DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this .9658–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9655well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.549 UP 6 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.568 UP 7 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,31…GETTTING DANGEROUS

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Slide As Hawkish Rikshock Sends Dollar, Yields Higher Again Ahead Of Fed

TUESDAY, SEP 20, 2022 – 07:44 AM

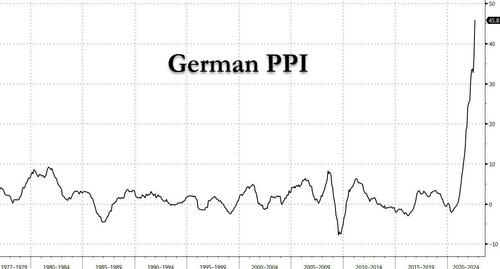

Market sentiment was quite cheerful heading into the overnight session, with futures hitting a third-day high of 3,936 thanks to yesterday’ late day delta squeeze (plunge in VIX as both calls and especially puts were sold) but then it quickly soured after first German PPI came in at a mindblowing 45.8% (vs expectations of 37.1%) the highest on record since World War II…

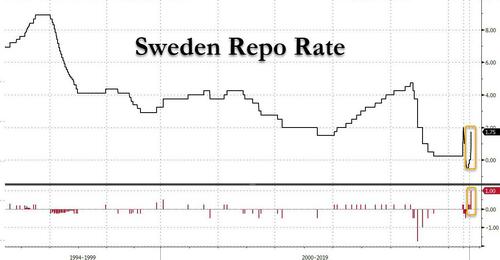

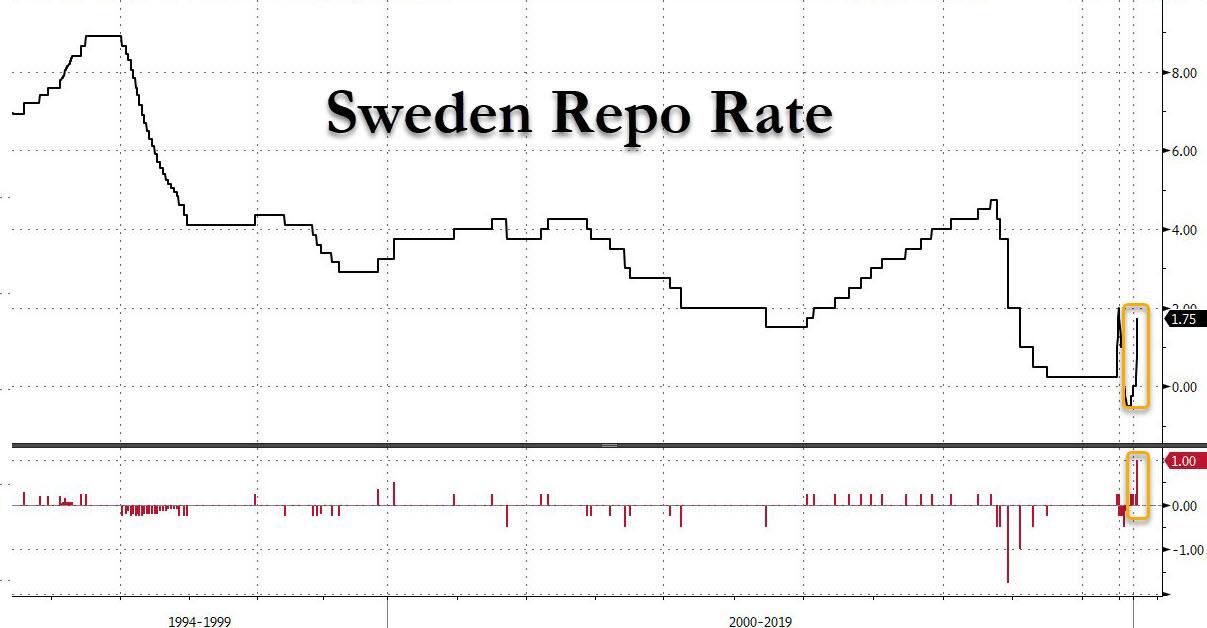

…but what really spooked futures was the record hike by the Swedish central bank, the Riksbank, which pushed the repo rate higher by a more than expected 100bps to 1.75%, and even though the central bank eased back on terminal rate expectations, the market still saw the Riksbank surprise as potentially indicative of what the BOE and Fed may do in the coming hours.

As such, European stocks fell with US equity futures, giving up early gains, as traders braced for another supersized US rate hike amid rising anxiety the Federal Reserve could overtighten and raise the odds of a hard landing. Europe’ Stoxx 600 Index dropped 0.8%, paced by losses on real estate and miners as US equity futures also stumbled those the tech-heavy and rate-sensitive Nasdaq 100 underperforming S&P 500 peers. As of 730am, S&P futures were down 0.4% and Nasdaq contracts were down 0.5%. 10Y yields hit a fresh 11 year high as the dollar surged and gold resumed its slide.

In premarket trading, Ford shares dropped 5.2% after the carmaker said 3Q supply costs were running $1b above expectations and warned that EBIT could be in the $1.4b -$1.7b range, below what was previously foreseen. General Motors stock also slid 2.3% in premarket trading. Here are some other notable premarket movers:

Change Healthcare shares rise 7.1% in premarket trading after winning court approval for the $7.8b acquisition by UnitedHealth, defeating a Justice Department lawsuit that had sought to block the deal

US- listed Macau casino stocks rise in premarket trading, on the possibility that Hong Kong would ease Covid restrictions such as mandatory hotel quarantine. Las Vegas Sands and Wynn Resorts gain about 3% in US premarket trading; Keep an eye on Melco (MLCO US) and MGM Resorts (MGM US) when trading volume picks up

Western Digital shares slid 1.7% in premarket trading as Deutsche Bank cut the recommendation on the stock to hold from buy, saying it’s difficult to see meaningful upside in the next six to nine months as oversupply in the flash memory market persists

Watch Cognex shares after the company boosted its revenue guidance for the third quarter; and the guidance beat the average analyst estimate

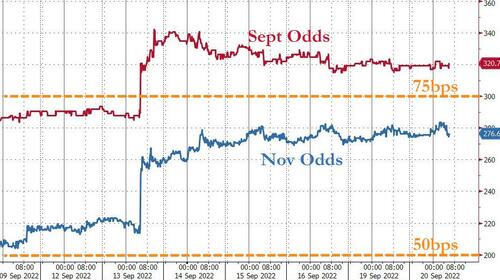

The Fed kicks off its meeting today and is expected to again hike rates by 75 basis points Wednesday – now that Timiraos has taken off 100bps off the table – signal rates are heading above 4% and will then pause. Market participants have dialed back expectations of an even larger increase and only two of 96 economists in a Bloomberg survey now predict a full-point move.

“The Federal Reserve is likely tightening policy straight into the teeth of a recession,” Danielle DiMartino Booth, CEO and chief strategist of Quill Intelligence, wrote in an email. “The stock market’s addiction to Fed easing when stocks decline may be what Jerome Powell is aiming to quash by aggressively hiking rates, in addition to inflation.”

Meanwhile in rates, Treasury 10-year yields topped 3.5% rising to a fresh 11.5 year high, while yields on the more policy-sensitive two-year rate hit the highest since 2007 and are poised to crack above 4%, reflecting hard-landing fears. In a worrying trend for stocks, real rates – Treasury yields adjusted for inflation – rose to the highest level since 2011. When they were pinned in negative territory during a decade of easy-money policies, real rates had been a key driver of risk-asset rallies.

Markets have fairly priced in yield on the two-year Treasury inching closer to 4% and “it might scratch a bit higher, but not an awful lot at this point,” Peter Kinsella, head of foreign exchange strategy at Union Bancaire Privee Ubp SA, said on Bloomberg Television. It would still be reasonable for the 10-year Treasury yield to go towards 3.5% or 3.7%, “but there’s probably not a lot more juice in that trade,” he said.

In Europe the Stoxx 50 fell 0.5%, reversing earlier gains with the UK’s FTSE 100 flat but outperforms peers, IBEX lags, dropping 0.8%. Real estate, retailers and miners are the worst-performing sectors.

Earlier in the session, Asian stocks advanced, on track to snap a five-day losing streak, amid signals that Hong Kong will move toward easing Covid restrictions. The MSCI Asia-Pacific Index gained as much as 1% as Tencent, Alibaba and TSMC provided the most support. Benchmarks across the region rose. Indexes in Hong Kong gained at least 1.2%, with one key gauge climbing from the edge of a bear market. Hong Kong’s chief executive said the city wants to relax Covid travel curbs after nearly three years of restrictions. The Hang Seng Tech Index added 2%. Australia’s main gauge rose more than 1%, led by the materials sector. Japan’s stock market advanced despite high inflation data, after being closed Monday.

“China’s reopening has helped revive sentiment in Asia this week,” said Charu Chanana, a senior strategist at Saxo Capital Markets. “There’s some level of positioning there ahead of a slew of central bank meetings this week, but volatility will likely remain elevated.” Despite Tuesday’s rally, Asia’s benchmark is still close to its lowest level since the middle of 2020 amid concerns over higher US interest rates and the dollar’s strength. Investors are betting that the Federal Reserve will hike interest rates by 75-basis-point at a policy meeting on Wednesday. Investors are also awaiting other central bank decisions this week from nations including the Philippines, Indonesia, Taiwan and Japan

Some more details: Japanese stocks advanced, tracking a rebound in US shares, as investors continued to weigh the market impact of further interest rate hikes from the Federal Reserve. Tokyo’s stock market was closed Monday for a holiday. The Topix Index rose 0.5% to 1,947.27 as of market close Tokyo time, while the Nikkei advanced 0.4% to 27,688.42. Keyence Corp. contributed the most to the Topix Index gain, increasing 2.2%. Out of 2,169 stocks in the index, 1,481 rose and 582 fell, while 106 were unchanged. “Assuming it is 75bps, the thing to consider is where it will go from there, as I think that the rate hike will remain hawkish as far as the Jackson Hole and economic indicators are concerned,” said Naoki Fujiwara, chief fund manager at Shinkin Asset Management. “A comment that accelerates the rate hike would be negative, while a comment that takes the economy into consideration would be positive for the stocks.” Traders are betting the Fed will hike by 75 basis points Wednesday.

India stock indexes rose for the second day, driven by a continuing rally in consumer goods makers and a surge in healthcare stocks. The S&P BSE Sensex gained 1% to 59,719.74 in Mumbai, while the NSE Nifty 50 Index rose 1.1%. The main indexes rose as much as 1.6% and 1.7%, respectively but failed to hold the advance. “Intraday volatility could be the ongoing theme for markets as investors world over are bracing for a stiff interest rate hike by the US Federal Reserve to weigh on rising inflation,” said Prashanth Tapse, an analyst with Mehta Securities. All of the 19 sector sub-indexes traded higher, led by a gauge of healthcare companies. Banking and consumer goods stocks continued their climb on expectations of a demand surge during the upcoming festive season. ICICI Bank contributed the most to the Sensex’s gain, increasing 2%. Out of 30 shares in the Sensex index, 26 rose and 4 fell.

In rates, the Treasury curve bear-flattened and yields rose by 4-5bps as Treasuries extend Monday’s session slide. Supply pressure in the form of 20-year bond auction awaits for Tuesday’s session, before Fed meeting Wednesday where OIS has eased slightly, pricing in 78bp of hikes for the meeting, following WSJ report that a three-quarter point move is expected. Core European rates underperform, led by gilts catching up from Monday UK’s holiday. Bunds fell, led by the belly of the curve, with yields rising up to 10bps as money markets continued to add to ECB tightening. UK bonds lead the wider market lower, headed by the short end and belly of the curve, and underperforming bunds and USTs as they catch up after Monday’s holiday. Curves bear-flatten as money markets up their ECB and BOE rate-hike bets. Swedish front-end bond yields rose more than their German peers, in response to the front-loaded rate increase. Australia’s dollar and bond yields declined after minutes from the RBA’s September meeting showed the central bank is getting closer to “normal settings.”

In FX, the Bloomberg Dollar Spot Index reversed a modest Asia session loss as the greenback advanced versus all of its Group-of-10 peers, with GBP and DKK the strongest performers in G-10 FX, NZD and NOK underperform. and yet as Bloomberg notes, options bets in the dollar are the least bullish they have been this year before the Federal Reserve was expected to announce an interest-rate increase. Some more details:

The euro gave up gains to touch parity against the dollar, despite a record German PPI print (the highest since WWII)

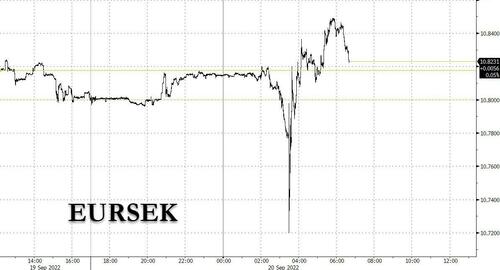

Sweden’s krona erased gains after initially rallying on the Riksbank’s surprise jumbo hike, as the market had priced in a more aggressive profile for the rate path, with a peak at around 3.5%.

The pound was supported by growing speculation that the Bank of England may raise interest rates by 75 basis points later this week. Markets were also anticipating a speech by the UK’s finance minister, who is expected to outline details for a big spending plan to help households through an energy crisis in coming months

Gilts dropped, catching up with Monday’s bond tumble when UK markets were closed for a holiday

In commodities, WTI drifts 0.5% higher to trade near $86.19. Spot gold falls roughly $8 to trade near $1,668/oz. Spot silver loses 1.3% near $19. European natural gas benchmark futures drop much as 6.8% for a fourth session of declines, the longest run since July.

Elsewhere, Bitcoin struggled to return to the $20,000 level. Oil slipped below $86 per barrel and gold fell.

To the day ahead now. In data we have US August housing starts, building permits, Germany August PPI, Italy July current account balance, July ECB current account, Canada August CPI, while the ECB’s Muller will give remarks.

Market Snapshot

S&P 500 futures fell 0.2% to 3,911.50

STOXX Europe 600 fell 0.5% to 405.78

MXAP up 0.7% to 150.68

MXAPJ up 1.0% to 493.17

Nikkei up 0.4% to 27,688.42

Topix up 0.4% to 1,947.27

Hang Seng Index up 1.2% to 18,781.42

Shanghai Composite up 0.2% to 3,122.41

Sensex up 1.5% to 60,021.83

Australia S&P/ASX 200 up 1.3% to 6,806.43

Kospi up 0.5% to 2,367.85

German 10Y yield little changed at 1.86%

Euro down 0.2% to $1.0007

Gold spot down 0.4% to $1,669.80

U.S. Dollar Index little changed at 109.80

Top Overnight News from Bloomberg

Treasury two-year yields are poised to crack above 4% for the first time since 2007 as the Federal Reserve’s steepest tightening cycle in a generation drives them higher

ECB Governing Council member Madis Muller said interest rates remain far from levels that would restrict economic expansion in the euro zone

The German government released another 2.5 billion euros ($2.5 billion) of credit lines to secure gas supplies, as it writes off Russia as a reliable energy supplier

Hungary said it was prepared to meet EU demands that it take action to curb fraud and corruption after the bloc threatened to freeze 7.5 billion euros ($7.5 billion) of funds that have been earmarked for the country

A more detailed look at global markets courtesy of Newsquawk

Asian stocks followed suit to the improved risk appetite stateside but with the advances capped ahead of this week’s risk events. ASX 200 was led higher by strength in the commodity-related sectors and with resilience in nearly all industries aside from healthcare, while the RBA minutes provided little in the way of new information but continued to point to a future slowdown in the hiking cycle. Nikkei 225 gained on return from the extended weekend but was off its highs after the mostly firmer-than-expected Japanese inflation data. Hang Seng and Shanghai Comp conformed to the upbeat mood with Hong Kong boosted by outperformance in tech stocks and as authorities consider adjusting COVID restrictions, while the advances in the mainland were contained after the PBoC maintained its 1-Year and 5-Year Loan Prime Rates as expected. “Investors should not be pessimistic about the (Chinese) stock market, as multiple signs emerge that bode well for equities”, according to the Securities Daily cited by SCMP.

Top Asian News

China’s Shanghai unvels RMB 1.8trln (around USD 257bln) worth of inftrastructure investments, has launched eight of them.

Hong Kong Chief Executive Lee said they are exploring further adjustments to COVID policy and aim to make an announcement soon with the details to be announced in one go. Lee added they would like to facilitate events for Hong Kong and bring back activities to the city, while they would want to stay connected with the world and allow an orderly opening up.

Japan’s Ministry of Finance said the government is to spend JPY 3.48tln in budget reserves to manage price hikes and COVID-19, while Finance Minister Suzuki said they will create an additional budget in addition to the reserve fund and for the time being, reserve money will be used for essential output. There were also comments from LDP Secretary-General Motegi that a stimulus package of at least JPY 15tln is needed to fill the output gap.

Bourses across Europe have been dipping from best levels, with sentiment somewhat sullied by a marked and unexpected acceleration in German PPI, coupled with a larger-than-forecast Riksbank rate hike to kick off the myriad of G10 central banks this week. The bias across sectors has titled more towards the defensive side, with Food & Beverages, Personal Goods, and Healthcare making their way up the ranks. US equity futures have slipped into negative territory, but the breadth of the market remains shallow as the clock ticks down to the FOMC tomorrow. German Gov’t draft law re. gas levy says Co’s receiving it may not see any notable profits, manager slaries must be limited. Restriction on profits to those with a market share above 1.0%, via Reuters sources.

Top European News

Traders Wager BOE Will Join Fed With Two Jumbo Hikes by Year- End

Germany to Spend Another $2.5 Billion on LNG to Ease Crisis

UBS’s Khan ‘Confident’ on Asset Target Despite Market Rout

Russia to Flood Asia With Fuel as Europe Ramps Up Sanctions

Riksbank Kicks Off Global Hiking With 100 Basis-Point Move

Central Banks

WSJ’s Timiraos writes “Fed’s Third Straight 0.75-Point Interest-Rate Rise Is Anticipated” and signaling intentions to raise and hold the benchmark above 4.0% in the months ahead, via WSJ.

Riksbank hikes its Rate by 100bps to 1.75% (exp. 75bps hike to 1.50%); Forecast indicates rate will be raised further in the coming six months. Full details, reaction & newsquawk analysis available here.

ECB’s Muller says rates are far from the level that would slow the economy; rates are still low in the historical context.

PBoC set USD/CNY mid-point at 6.9468 vs exp. 6.9483 (prev. 6.9396).

PBoC 1-Year Loan Prime Rate (Sep) 3.65% vs. Exp. 3.65% (Prev. 3.65%)

PBoC 5-Year Loan Prime Rate (Sep) 4.30% vs. Exp. 4.30% (Prev. 4.30%)

RBA September meeting minutes stated members saw the case for a slower pace of rate increase as becoming stronger as the level of the Cash Rate increases, while the board expects to increase rates further over months ahead but is not on a pre-set path. RBA Board is committed to doing what is necessary to ensure inflation returns to target over time and members noted that inflation in Australia was at its highest level in several decades which was expected to increase further over the months ahead with inflation expected to peak later this year and then decline back towards the 2-3% target range. Furthermore, the Board acknowledged that monetary policy operates with a lag and interest rates had been increased quite quickly and were getting closer to normal settings.

FX

DXY remains towards the top of today’s intraday parameter but under the 110.00 mark.

SEK was flagging near recent lows against the Euro and Dollar before the Riksbank delivered a hawkish surprise by raising rates a bigger than expected 100 bp (vs +75 bp consensus).

NZD remained under pressure and extended its decline against the Greenback to the low 0.5900 zone, while sliding through 1.1300 vs the Aussie.

JPY failed to glean much impetus from firmer than Japanese inflation metrics on the premise that the BoJ is unlikely to budge from its accommodative stance this week.

Fixed Income

Debt futures continue to plunge amidst fleeting bouts of consolidation and lame rebounds – the latest catalyst came via Sweden’s Riksbank.

Bunds have been down to 141.08 for a 154 tick loss on the day, Gilts to 104.33, 91 ticks below par.

US 10-year T-note fell to 114-01+, with corresponding yields soaring towards 3.55%.

Commodities

WTI and Brent front-month futures hold onto modest gains, but the upside remains capped by the cautious risk tone in early European trade. Overnight, the complex was relatively uneventful as it took a breather from the recent volatility.

Russia’s government wants to collect about RUB 1.4tln from raw material exporters next year to cover the budget deficit and proposed to raise the export duty on gas to 50% among other measures, according to Kommersant.

Gazprom says it will halt power of Siberia gas pipeline to China on Sept 22-29, citing maintenance, via Reuters.

Aramco CEO says the response to the global energy crisis thus far shows a deep misunderstanding of how we got there, increases in oil/gas investment are “too little too late” in the short term; when the global economy recovers, can expect demand to rebound further – eliminating the little spare oil production capacity available.

Spot gold is subdued by the Dollar but in recent ranges after hitting multi-year lows last week as the yellow metals look ahead to the Fed.

LME futures resumed trade following the long weekend, with 3M copper flat at the time of writing under the USD 7,800/t, mimicking the risk tone and awaiting the next catalyst.

US Event Calendar

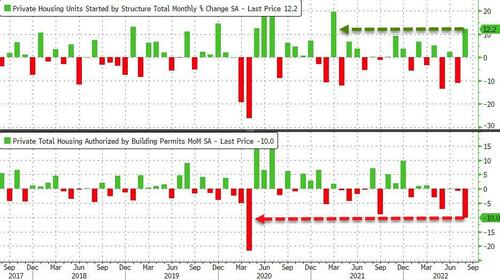

08:30: Aug. Building Permits MoM, est. -4.8%, prior -1.3%, revised -0.6%

08:30: Aug. Housing Starts MoM, est. 0.3%, prior -9.6%

08:30: Aug. Building Permits, est. 1.6m, prior 1.67m, revised 1.69m

08:30: Aug. Housing Starts, est. 1.45m, prior 1.45m

DB’s Jim Reid concludes the overnight wrap

It was an extraordinary day here in the UK yesterday for the Queen’s funeral. The vast majority of the world’s leaders and dignitaries were present, hundreds of thousands lined the streets of London, and it was broadcast to an estimated global TV audience of four billion. It was hard not to get swept up in the emotion, pageantry, and enormity of the event. It’s also hard to imagine that the world will see a similar type of event again in our lifetime.

With all this going on, markets started the week on a quiet note, with the UK closed, Japan on holiday, and the data docket light. Yields took another leg higher though and curves flattened on the prospect of another round of global central bank tightening this week. Meanwhile, global equity markets were looking for direction, with European equities slightly lower, and US equities tracking flat for most of the day until a strong late rally (S&P +0.69%) changed the complexion of the day a bit.

The central bank focus remains the main game in town. With Fed pricing for Wednesday (79.8bps of hikes implied by the close, our US economics full preview here) still incorporating some premium of a 100 basis point hike, markets were watching for any blackout period communications from the Fed. A prominent Fed watcher from the WSJ did have a piece that garnered attention, but it was focused more on the previously-recognised pivot from Chair Powell to focus more on fighting inflation rather than providing a strong signal about Wednesday’s potential policy action one way or another. In turn, implied policy pricing for Wednesday was perfectly flat on the day.

Farther out the curve, however, rates markets priced in tighter Fed policy for longer, with the entire Treasury curve selling off, driving a bear flattening. 2yr Treasury yields increased +6.9bps to 3.94%, their highest levels since 2007, while 10yrs were +4.1bps higher to 3.49%, the highest since 2011, leaving the yield curve at -45.0bps and just short of its most inverted levels reached this summer (-49.6bps). Yields have pulled back a touch in Asia though, with 10yr USTs (-1.95 bps) at 3.47% and 2yr yield trading -1bps lower at 3.93% as we go to press.

In line with the tighter expected policy path, real yields are bearing the brunt of the recent selloff, with 10yr real yields increasing +6.5bps to 1.14%, their highest since 2018. The selloff and curve move was replicated in bunds, where 2yrs increased +8.8bps to 1.59% and 10yrs climbed +4.7bps to 1.80%, its highest since early 2014. 10yr OATs were in line with bunds, increasing +4.6bps, while BTPs marginally underperformed, increasing +5.8bps.

The STOXX 600 was as much as -1.0% lower intraday, but climbed through the afternoon to finish just in the red at -.09%, while the CAC marginally underperformed, falling -0.26% whilst the DAX managed to eke out a +0.49% gain. Elsewhere out of Germany, regulators reported that German gas storage levels were at 89.67% as of yesterday, something to keep an eye on as we head into winter. The gas build has been very impressive but with the strong possibility of there being no more Russian gas flowing this winter, unless temperatures are mild, it’s likely that rationing, in some shape or form, is likely.

US equities, opened nearly -1.0% lower, but quickly rallied to flat where it oscillated around most of the day before the late rally send it up +0.69%. 9 out of 11 S&P sectors ended in the green, with sectoral dispersion pointing toward a cyclical over defensives day – materials (+1.63%), discretionary (+1.34%) and industrials (+1.33%) led while health care (-0.54%) and real estate lagged (-0.22%). The NASDAQ was slightly stronger, increasing +0.76%, but very much followed the same intraday price action as the S&P.

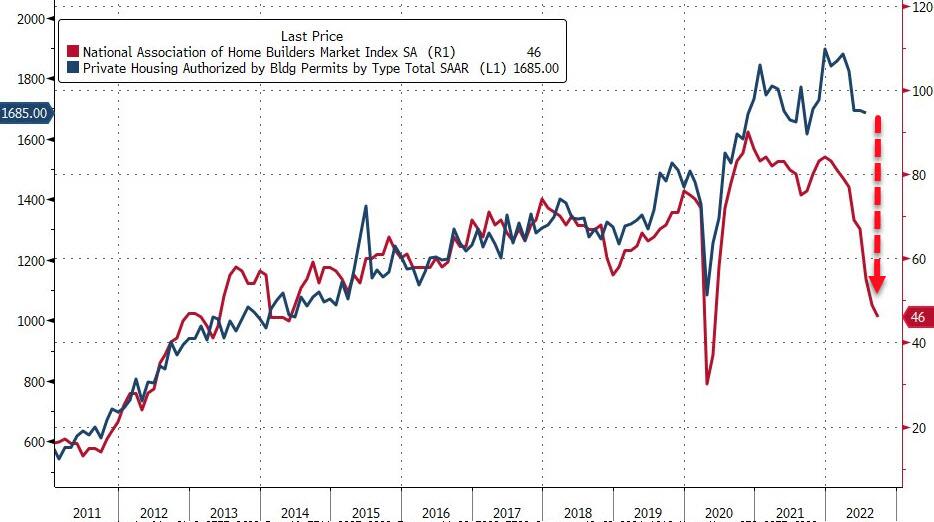

In terms of data, the NAHB Housing Market Index declined to 46 (vs. 47 expectations and 49 prior), but didn’t necessarily tell us anything we didn’t already know: housing market sentiment is bad. It remains one of the sectors where the impacts of Fed tightening has already been acutely felt.

Asian equity markets are broadly higher this morning following the late rally on Wall Street overnight. As I type, the Hang Seng (+1.44%) is leading gains across the region, rebounding from two consecutive sessions of losses while Chinese shares are also higher with the Shanghai Composite (+0.46%) and CSI (+0.33%) both up in early trade after the lifting of Covid-19 lockdowns in both Chengdu and Dalian yesterday. Elsewhere, the Nikkei (+0.42%) as well as the Kospi (+0.33%) have held on to their gains.

DMs stock futures are pointing to a positive start with contracts on the S&P 500 (+0.20%), NASDAQ 100 (+0.23%) and DAX (+0.53%) are edging higher.

Early morning data showed that Japan’s core consumer inflation quickened to +2.8% y/y in August (v/s +2.7% expected), notching its fastest annual pace in nearly eight years as pressures from higher raw material costs and a weak yen broadened. Markets were expecting a +2.7% gain compared to July’s +2.4% rise.

Meanwhile, headline inflation hit 3.0% y/y in August, the highest since 1991. The data will be slightly uncomfortable for the BoJ as they meet on Thursday but they are not expected to change direction yet from their increasingly outlier zero rates policy stance on the global stage.

Elsewhere, the People’s Bank of China (PBOC) kept its main lending rates unchanged leaving the 1-year loan prime rate (LPR) intact at 3.65% and the 5-year rate, a reference for mortgages, at 4.3% after a 15bps cut in August.

The latest minutes from the Reserve Bank of Australia (RBA) indicate that the board members “saw the case for a slower pace of increase in interest rates as becoming stronger” over the months ahead but reiterated that the policy is not on a pre-set path considering the uncertainties surrounding the outlook for inflation and growth. Actually our economists have upgraded their RBA call to a 50bps hike in October (from 25bps) in line with the global direction of travel. They don’t think the RBA will step down to 25bps hikes until November and December.

To the day ahead now. In data we have US August housing starts, building permits, Germany August PPI, Italy July current account balance, July ECB current account, Canada August CPI, while the ECB’s Muller will give remarks.

AND NOW NEWSQUAWK

Sentiment sullied after hotter-than-expected Japanese CPI, eye-watering German PPI, and a jumbo Riksbank hike – Newsquawk US Market Open

TUESDAY, SEP 20, 2022 – 06:44 AM

Bourses across Europe have been dipping with sentiment initially sullied by a marked and unexpected acceleration in German PPI

US equity futures have slipped into negative territory, but the breadth of the market remains shallow as the clock ticks down to the FOMC tomorrow

DXY remains towards the top of today’s intraday band but under the 110.00 mark, JPY failed to gain impetus from hotter-than-expected Japanese CPI

Debt futures continue to plunge amidst fleeting bouts of consolidation and lame rebounds; US 10yr yield topped 3.55%

Looking ahead, highlights include Canadian CPI, ECB’s Lagarde, and US 20yr Supply

Or why not try Newsquawk’s squawk box free for 7 days?

20th September 2022

LOOKING AHEAD

Canadian CPI, ECB’s Lagarde and US 20yr Supply.

GEOPOLITICS

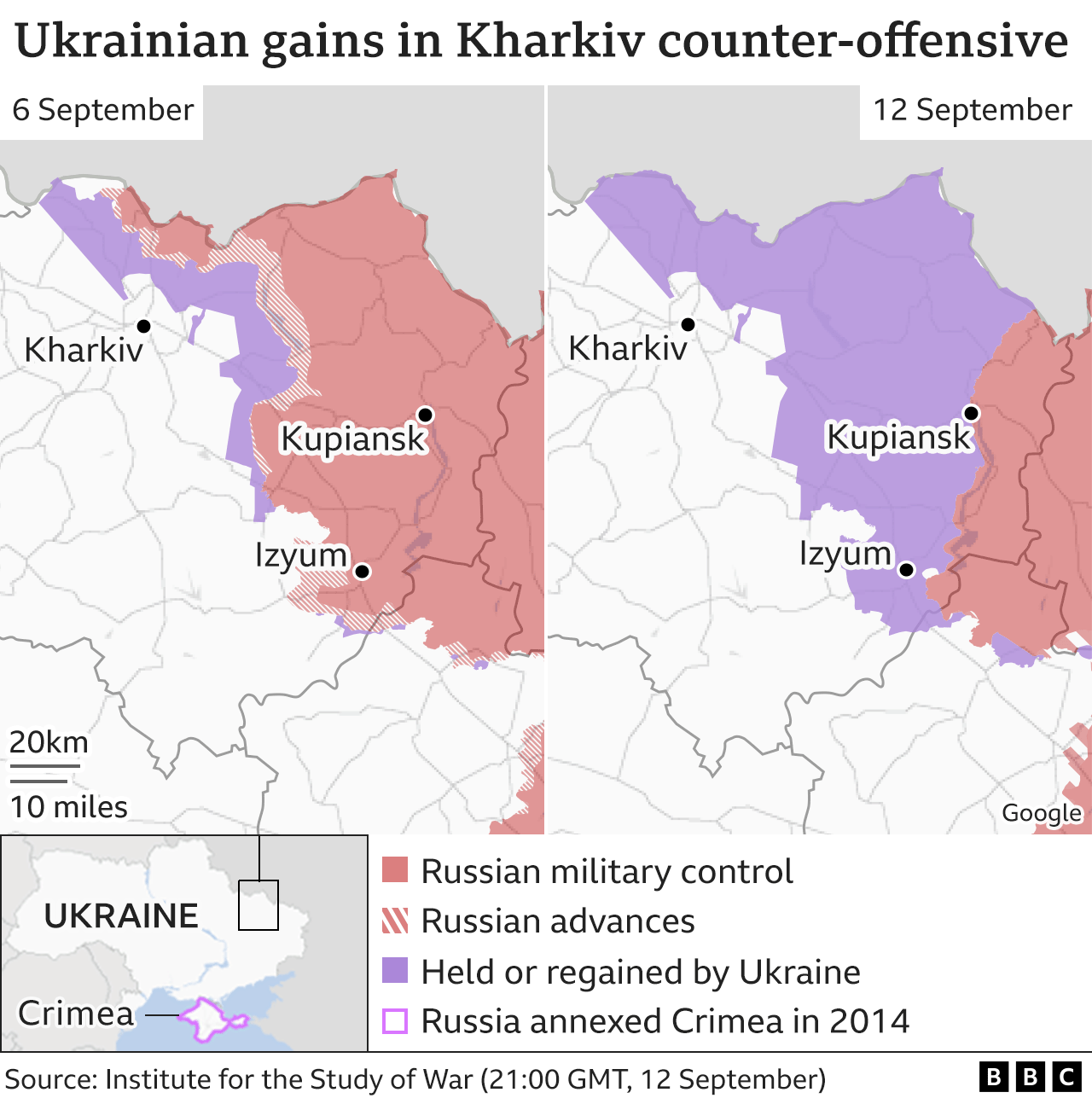

RUSSIA-UKRAINE

Russian forces carried out a missile strike which narrowly missed the Pivdennoukrainsk nuclear power plant in southern Ukraine, according to Kyiv officials cited by the FT.

UK is to spend at least GBP 2.3bln on the Ukraine war effort next year, according to FT.

Turkish President Erdogan says Russia must return the occupied territories to Ukraine as part of a peaceful settlement. Adding, “What prompted us to mediate is my belief that Putin is ready to end this as soon as possible”, via AJABreaking citing PBS.

OTHER

US Secretary of State Blinken hosted Armenian and Azerbaijan foreign ministers for the first direct talks since recent fighting and Blinken encouraged Armenia and Azerbaijan leaders to meet again before month-end, according to Reuters.

EUROPEAN TRADE

CENTRAL BANKS

WSJ’s Timiraos writes “Fed’s Third Straight 0.75-Point Interest-Rate Rise Is Anticipated” and signaling intentions to raise and hold the benchmark above 4.0% in the months ahead, via WSJ.

Riksbank hikes its Rate by 100bps to 1.75% (exp. 75bps hike to 1.50%); Forecast indicates rate will be raised further in the coming six months. Full details, reaction & newsquawk analysis available here.

ECB’s Muller says rates are far from the level that would slow the economy; rates are still low in the historical context.

PBoC set USD/CNY mid-point at 6.9468 vs exp. 6.9483 (prev. 6.9396).

PBoC 1-Year Loan Prime Rate (Sep) 3.65% vs. Exp. 3.65% (Prev. 3.65%)

PBoC 5-Year Loan Prime Rate (Sep) 4.30% vs. Exp. 4.30% (Prev. 4.30%)

RBA September meeting minutes stated members saw the case for a slower pace of rate increase as becoming stronger as the level of the Cash Rate increases, while the board expects to increase rates further over months ahead but is not on a pre-set path. RBA Board is committed to doing what is necessary to ensure inflation returns to target over time and members noted that inflation in Australia was at its highest level in several decades which was expected to increase further over the months ahead with inflation expected to peak later this year and then decline back towards the 2-3% target range. Furthermore, the Board acknowledged that monetary policy operates with a lag and interest rates had been increased quite quickly and were getting closer to normal settings.

EQUITIES

Bourses across Europe have been dipping from best levels, with sentiment somewhat sullied by a marked and unexpected acceleration in German PPI, coupled with a larger-than-forecast Riksbank rate hike to kick off the myriad of G10 central banks this week.

The bias across sectors has titled more towards the defensive side, with Food & Beverages, Personal Goods, and Healthcare making their way up the ranks.

US equity futures have slipped into negative territory, but the breadth of the market remains shallow as the clock ticks down to the FOMC tomorrow.

German Gov’t draft law re. gas levy says Co’s receiving it may not see any notable profits, manager slaries must be limited. Restriction on profits to those with a market share above 1.0%, via Reuters sources.

DXY remains towards the top of today’s intraday parameter but under the 110.00 mark.

SEK was flagging near recent lows against the Euro and Dollar before the Riksbank delivered a hawkish surprise by raising rates a bigger than expected 100 bp (vs +75 bp consensus).

NZD remained under pressure and extended its decline against the Greenback to the low 0.5900 zone, while sliding through 1.1300 vs the Aussie.

JPY failed to glean much impetus from firmer than Japanese inflation metrics on the premise that the BoJ is unlikely to budge from its accommodative stance this week.

WTI and Brent front-month futures hold onto modest gains, but the upside remains capped by the cautious risk tone in early European trade. Overnight, the complex was relatively uneventful as it took a breather from the recent volatility.

Russia’s government wants to collect about RUB 1.4tln from raw material exporters next year to cover the budget deficit and proposed to raise the export duty on gas to 50% among other measures, according to Kommersant.

Gazprom says it will halt power of Siberia gas pipeline to China on Sept 22-29, citing maintenance, via Reuters.

Aramco CEO says the response to the global energy crisis thus far shows a deep misunderstanding of how we got there, increases in oil/gas investment are “too little too late” in the short term; when the global economy recovers, can expect demand to rebound further – eliminating the little spare oil production capacity available.

Spot gold is subdued by the Dollar but in recent ranges after hitting multi-year lows last week as the yellow metals look ahead to the Fed.

LME futures resumed trade following the long weekend, with 3M copper flat at the time of writing under the USD 7,800/t, mimicking the risk tone and awaiting the next catalyst.

Bitcoin is subdued but just about holds onto a USD 19,000 handle whilst Ethereum meanders around 1,350.

Wintermute, cryptocurrency market maker, has been hacked for USD 160mln according to the CEO, remains solvent.

NOTABLE EUROPEAN HEADLINES

EU Affairs Ministers meeting today are to discuss proposals to remove/limit the unanimity rule on foreign affair matters, via Politico.

NOTABLE EU DATA

German Producer Prices YY (Aug) 45.8% vs. Exp. 37.1% (Prev. 37.2%), MM (Aug) 7.9% vs. Exp. 1.6% (Prev. 5.3%)

Swiss Government sees 2022 GDP (Sport Event Adj.) growth at +2.0% (prev. +2.6%), sees 2023 GDP (Sport Event Adj.) growth At +1.1% (prev. +1.9%). Sees 2022 CPI +3.0% (prev. +2.5%), 2023 CPI seen at +2.3% (prev. +1.4%)

NOTABLE US HEADLINES

World Bank’s Malpass said a strong dollar is part of the resilience underpinning US financial markets, according to Reuters.

APAC TRADE