by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSE: DOWN $24.60 to $1648.35

SILVER PRICE CLOSE: DOWN 68 cents to $18.92

Access prices: closes

Gold ACCESS CLOSE 1644.30

Silver ACCESS CLOSE: 18.89

Bitcoin morning price: $18,890 DOWN $594

Bitcoin: afternoon price: $18,772 DOWN 692

Platinum price closing DOWN $54.40 AT $864.00

Palladium price; closing DOWN $52.35 at $2071.40

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,670.800000000 USD

INTENT DATE: 09/22/2022 DELIVERY DATE: 09/26/2022

FIRM ORG FIRM NAME ISSUED STOPPED

323 C HSBC 3

435 H SCOTIA CAPITAL 124

624 H BOFA SECURITIES 22

657 C MORGAN STANLEY 15

661 C JP MORGAN 221 575

690 C ABN AMRO 56

709 C BARCLAYS 502

737 C ADVANTAGE 4

880 H CITIGROUP 332

905 C ADM 10

TOTAL: 932 932

JPMorgan stopped 575/932 contracts

MONTH TO DATE: 9,505_____________________________________________

GOLD: NUMBER OF NOTICES FILED FOR SEPT CONTRACT:

932 NOTICES FOR 93,200 OZ //2.8989 TONNES

total notices so far: 9505 contracts for 950,500 oz (29.564 tonnes)

SILVER NOTICES: 48 NOTICES FILED FOR 240,000 OZ/

total number of notices filed so far this month 6643 : for 33,215,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $24.60

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: //// A WITHDRAWAL OF 2.03 TONNES FROM THE GLD/

INVENTORY RESTS AT 950.13 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 68 CENTS

AT THE SLV// ://BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF OF 0.507 MILLION OZ INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 481.931 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A FAIR SIZED 402 CONTRACTS TO 132,106 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE FAIR GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.10 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.10) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC SILVER LONGS AS WE HAD A GOOD GAIN OF 900 CONTRACTS ON OUR TWO EXCHANGES. WE DID HAVE A STRONG SILVER SHORT COVERING. THE SPECS ARE FLEEING AS FAST AS THEIR LITTLE FEET WILL CARRY THEM.

WE MUST HAVE HAD:

I) STRONG SPECULATOR SHORT COVERING ////CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 355,000 OZ QUEUE JUMP / // V) FAIR SIZED COMEX OI GAIN/(//CONSIDERABLE SPEC LIQUIDATION/)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: +52

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTRACTS for 16 days, total 12,755 contracts: 63.775 million oz OR 3.986 MILLION OZ PER DAY. (797 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 63.775 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 63.775 MILLION OZ///

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 402 WITH OUR $0.10 GAIN IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE CONTRACTS: 550 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /GOOD BANKER ADDITIONS A// CONSIDERABLE NET SPEC SHORT COVERINGS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 355,000 OZ QUEUE JUMP // .. WE HAD A STRONG SIZED GAIN OF 952 OI CONTRACTS ON THE TWO EXCHANGES FOR 4.76MILLION OZ AS..THE SPECS STILL ARE BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 48 NOTICE(S) FILED TODAY FOR 240,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 283 CONTRACTS TO 465,884 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED – 125 CONTRACTS.

.

THE SMALL SIZED DECREASE IN COMEX OI CAME DESPITE OUR RISE IN PRICE OF $5.20//COMEX GOLD TRADING/THURSDAY / WE MUST HAVE HAD MAJOR SPECULATOR SHORT COVERINGS ACCOMPANYING OUR SMALL SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND //CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 8.401 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 61,100 OZ //NEW STANDING 30.799 TONNES

YET ALL OF..THIS HAPPENED WITH OUR RISE IN PRICE OF $5.20 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 5295 OI CONTRACTS 16.469 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5295 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 465,884

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5295 CONTRACTS WITH 283 CONTRACTS DECREASED AT THE COMEX AND 5578 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 5295 CONTRACTS OR 16.86 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5578) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (283): TOTAL GAIN IN THE TWO EXCHANGES 5295 CONTRACTS. WE NO DOUBT HAD 1) CONSIDERABLE SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS/// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 8.409 TONNES FOLLOWED BY TODAY’S MONSTROUS QUEUE JUMP OF 61,100 oz. 3) ZERO LONG LIQUIDATION//// //.,4) SMALL SIZED COMEX OPEN INTEREST LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

44,868 CONTRACTS OR 4,486,800 OZ OR 139.56 TONNES 16 TRADING DAY(S) AND THUS AVERAGING: 2804 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES: 139.56 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 139.56/3550 x 100% TONNES 3.94% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 139.56 TONNES (SLIGHTLY FALLING THIS MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT., FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER,ROSE BY A FAIR SIZED 402 CONTRACT OI TO 132,106 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 550 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 550 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 550 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 402 CONTRACTS AND ADD TO THE 550 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 952 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 4.76 MILLION OZ

OCCURRED WITH OUR GAIN IN PRICE OF $0.10

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED DOWN 20L54 PTS OR 0.66% //Hang Sang CLOSED DOWN 214.68 PTS OR 1.18% /The Nikkei closed HOLIDAY //Australia’s all ordinaries CLOSED DOWN 1.92% /Chinese yuan (ONSHORE) closed DOWN AT 7.1198//OFFSHORE CHINESE YUAN DOWN 7.1312// /Oil DOWN TO 80.07 dollars per barrel for WTI and BRENT AT 87.68 / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 283 CONTRACTS TO 466,009 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED DESPITE OUR RISE IN PRICE OF $5.20 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (5578 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 5578 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :5578 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5578 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED SIZED TOTAL OF 5295 CONTRACTS IN THAT 5578 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI LOSS OF 158 CONTRACTS..AND THIS STRONG GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR RISE IN PRICE OF GOLD $5.20. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING SEPT (30.799),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 30.799 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $5.20) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A STRONG SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 5295 CONTRACTS // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS TRIED TO COVER ON THEIR POSITIONS WITH MINIMAL SUCCESS////// WE HAVE REGISTERED A STRONG GAIN OF 5420 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR SEPT. (30.799 TONNES)…

WE HAD 125 CONTRACTS ADDED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 5420 CONTRACTS OR 542,000 OZ OR 16.86 TONNES

Estimated gold volume 242,315/// fair//

final gold volumes/yesterday 251,651/ fair

INITIAL STANDINGS FOR SEPT ’22 COMEX GOLD //SEPT 23

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 44,320.52 oz BRINKS Manfra 1685 kilobars Manfra |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 932 notice(s) 93,200 OZ 2.8989 TONNES |

| No of oz to be served (notices) | 397 contracts 39700 oz 1.2348 TONNES |

| Total monthly oz gold served (contracts) so far this month | 9505 notices 950,500 OZ 29.564 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

2 customer withdrawals:

i) Out of Brinks 54,174.440oz( 1685 kilobars)

ii) Out of Manfra: 206.08 oz

total: 54,320.520 oz

total in tonnes: 1.68 tonnes

Adjustments: 2

JPM/ customer to dealer: 191,845.017 oz

Brinks: dealer to customer; 35,398.251 0z

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPT.

For the front month of SEPT we have an oi of 1329 contracts having LOST 187 contracts .

We had 798 notices filed on THURSDAY so we gained a whopping 611 contracts or an additional 61,100 oz

will stand for gold in this very non active delivery month of September.

October LOST ONLY 356 contracts LOWERING TO 41,689. Oct is generally a poor active delivery month. It WILL change!! (Look for a very unusually large Oct. delivery month.)

November GAINED 14 contracts to stand at 354

December GAINED 410 contracts UP to 376,833

We had 932 notice(s) filed today for 93200 oz FOR THE SEPT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 220 notices were issued from their client or customer account. The total of all issuance by all participants equate to 932 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 575 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2022. contract month,

we take the total number of notices filed so far for the month (9505) x 100 oz , to which we add the difference between the open interest for the front month of (SEPT 1329 CONTRACTS) minus the number of notices served upon today 932 x 100 oz per contract equals 990200 OZ OR 30.799 TONNES the number of TONNES standing in this NON active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month:

No of notices filed so far (932) x 100 oz+ (1329) OI for the front month minus the number of notices served upon today (932} x 100 oz} which equals 990,200 oz standing OR 30.799 TONNES in this NON active delivery month of SEPTEMBER.

TOTAL COMEX GOLD STANDING: 30.799 TONNES (A HUMONGOUS STANDING FOR A SEPT ( NON ACTIVE) DELIVERY MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,250,165.318 oz 76.21 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 26,779,401.170 OZ

TOTAL REGISTERED GOLD: 13,143,659.393 OZ (408.82 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 13,635,741.747 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,893,494. OZ (REG GOLD- PLEDGED GOLD) 338.83 tonnes//rapidly declining

END

SILVER/COMEX/SEPT 23

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 899.277.167 oz Brinks CNT Delaware HSBC Int.Delaware |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,172,742.451 oz HSBC Loomis |

| No of oz served today (contracts) | 48 CONTRACT(S) 240,000 OZ) |

| No of oz to be served (notices) | 59 contracts (295,000 oz) |

| Total monthly oz silver served (contracts) | 6643 contracts 33,215,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 2 deposits into the customer account

i) Into HSBC: 572,711.481 oz

ii) Into Loomis: 600,030.970 oz

total deposit: 1,172,742.451l oz

JPMorgan has a total silver weight: 164.074 million oz/316.610million =51.80% of comex

Comex withdrawals: 5

i) out of HSBC 637,623.472 oz

ii) Out of Brinks: 14,471,870 oz

iii)Out of CNT 27,380.505 oz

iv)Out of Delaware: 22,929.340 oz

v) Out of Int Delaware: 206,871.980 oz

total: 899,277.980 oz

adjustments: 1// customer to dealer

i) Delaware 19,163.380 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 43.590 MILLION OZ (declining rapidly)

TOTAL REG + ELIG. 316.610 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF SEPT OI: 107 CONTRACTS HAVING LOST 36 CONTRACTS. WE HAD

107 CONTRACTS SERVED ON THURSDAY SO WE GAINED 71 CONTRACTS OR AN ADDITIONAL

355,000 OZ WILL STAND FOR METAL IN THIS VERY ACTIVE MONTH OF SEPT.

WE WILL GAIN IN TOTAL SILVER STANDING EACH TRADING DAY UNTIL THE END OF THE MONTH

(CONTINUAL QUEUE JUMPING BY OUR BANKERS SEARCHING FOR SILVER METAL)

OCTOBER LOST 53 CONTRACTS TO STAND AT 456 CONTACTS.

NOVEMBER GAINED 44 CONTRACTS TO STAND AT 150

DECEMBER SAW A GAIN OF 140 CONTRACTS DOWN TO 116,464

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 48 for 240,000 oz

Comex volumes:74,817// est. volume today// good

Comex volume: confirmed yesterday: 66,160 contracts ( good)

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 6643 x 5,000 oz = 33,215,000 oz

to which we add the difference between the open interest for the front month of SEPT(107) and the number of notices served upon today 48 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT./2022 contract month: 6,643 (notices served so far) x 5000 oz + OI for front month of SEPT (107) – number of notices served upon today (48) x 5000 oz of silver standing for the SEPT contract month equates 33,155,000 oz. .

We have an inventory of 43.590 million oz of registered silver at the comex so Sept delivery of 33.510 MILLION OZ represents 77.02% of that category of silver.

If we add August’s final delivery (to Sept) for silver at 5.51 million oz, we have a total of 39.02 million oz delivered upon with a REGISTERED INVENTORY of 43.51 million oz or 89.68% of that category of silver.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:50,941// est. volume today// poor

Comex volume: confirmed yesterday: 43,847contracts ( poor)

END

GLD AND SLV INVENTORY LEVELS

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

SEPT 21/WITH GOLD UP $4.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.79 TONNES FROM THE GLD///INVENTORY RESTS AT 952.16 TONNES

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

SEPT 13/WITH GOLD DOWN $22.85 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73ONNES FROM THE GLD////INVENTORY RESTS AT 964.91 TONNES

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

AUGUST 31.WITH GOLD DOWN $10.20:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.24 TONNES FROM THE GLD////INVENTORY RESTS AT 973.37 TONNES

AUGUST 30.WITH GOLD DOWN $12.00:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 980.61 TONNES

AUGUST 29/WITH GOLD DOWN $.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD/////INVENTORY RESTS AT 982.64 TONNES

AUGUST 26/WITH GOLD DOWN $26.60; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 25/WITH GOLD UP $9.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

GLD INVENTORY: 950.13 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION OZ/

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

SEPT 21/WITH SILVER UP 33 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.902 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 482.115 MILLION OZ//

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

SEPT 13/WITH SILVER DOWN $.31 TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.899 MILLION OZ//

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

AUGUST 31/WITH SILVER DOWN 36 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 3.087 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 465.573 MILLION OZ//

AUGUST 30/WITH SILVER DOWN 34 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 1.478 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 470.135 MILLION OZ//

AUGUST 29/WITH SILVER DOWN 7 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY A THE SLV: A WITHDRAWAL OF 2.765 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 470.135 MILLION OZ//

AUGUST 26/WITH SILVER DOWN 39 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 25/WITH SILVER UP 21 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

CLOSING INVENTORY 481.931 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

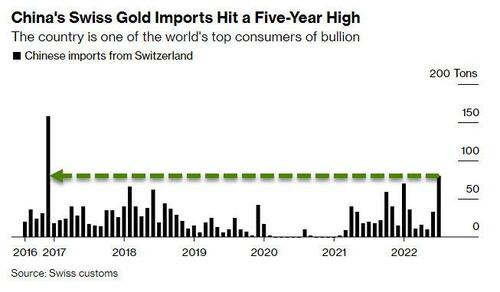

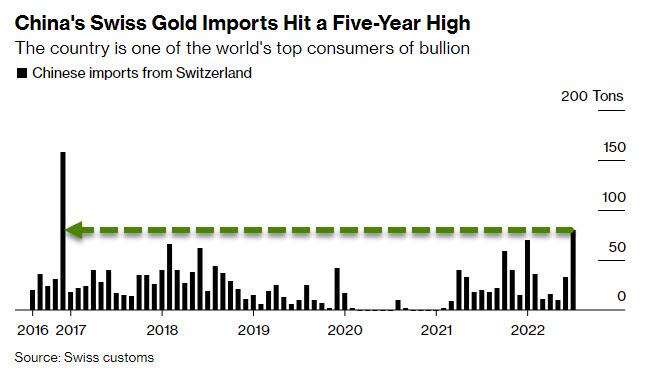

Chinese Gold Demand Appears To Be Picking Up Again

FRIDAY, SEP 23, 2022 – 11:45 AM

Gold demand in China showed renewed strength over the last two months despite scattered COVID-19 lockdowns. Both gold withdrawals from the Shanghai Gold Exchange (SGE) in August and gold imports in July were up.

China ranks as the world’s number one gold consumer.

Gold withdrawals from the SGE totaled 166 tons in August. That represents a 3% month-on-month rise and an 11% annual increase. According to the World Gold Council, “This was impressive given COVID-19 resurgences and subsequent restrictions imposed on mobility in cities such as Sanya.”

Analysts say manufacturers are stocking up on gold ahead of the peak gold consumption season. This is a good sign that manufacturers expect healthy demand in the coming months. October is traditionally a big month for gold jewelry sales during the seven-day National Day Holiday early in the month.

The most recent gold import numbers also offer a reason for optimism. Imports rocketed upward, increasing by 71 tons in July. Year on year, imports were up by 111 tons. Total gold imports came in at 178 tons on the month. That was the highest July total since 2017.

China shipped in more than 80 tons of Gold from Switzerland alone in July, according to the Swiss Federal Customs Administration. Imports from the major refining hub more than doubled the June total and were eight times higher than in May.

The WGC said, “This reflects the combination of recent strong gold demand and a rising local gold price premium, which often incentivizes importers.”

The recent increase in gold import activity reverses the decline we saw in the spring. Import numbers dropped significantly in April and May, but rebounded to over 100 tons in June before the big surge in July.

According to Bloomberg, “The data indicates that Chinese gold demand is picking up, after being hurt by lockdowns to control Covid outbreaks in several major cities. While the country’s purchases rarely have the power to drive prices higher, they can provide a floor when Western investors sell.”

Last year, China gave the green light to up gold imports. The report notes that China’s returning appetite for gold could potentially “support global prices.” Reuters called the size of the expected Chinese gold imports a “dramatic return to the global bullion market.”

Earlier this year, gold demand seemed to be maintaining the strength we saw in the market late last year, but it fell off dramatically in the spring with rising COVID cases and the government’s response. The big rebound in July indicates the Chinese gold market might be back on track.

END

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

In light of today, this article is worth repeating

(Mathew Piepenburg)

Even A Weaponized Dollar Won’t Stop Gold’s Historical Turning Point

FRIDAY, SEP 23, 2022 – 12:45 PM

Authored by Matthew Piepenburg via GoldSwitzerland.com,

We have dedicated numerous articles and interviews addressing the dangerous strength of the USD on the heels of a deliberately hawkish Fed hiking rates into what is clearly a recession, official or otherwise.

Explaining the Inexplicable: Rising Rates into a Recession?

On the surface, such central bank tightening in the face of a tanking economy and increasingly volatile risk asset markets makes little sense, as a strong USD and higher interest expense (i.e., interest rate policy) crushes just about every asset class in its wake, from an empirically broken bond market and grotesquely over-valued stock market to the artificially repressed precious metals space.

So, why is the openly cornered Fed acting so openly at odds with the real world and the US economy after years of feeding it instant-liquidity at every “dip,” cough or market sniffle?

The Fake War on Inflation

The standard answer is to “fight” inflation (which the Fed’s own mouse-click money alone created).

But as we’ve also written and observed so many times, a Fed Funds Rate at 3%, 4% or even 5% is not only mathematically crippling to a nation which simply can’t afford such rates, it is equally impotent against a headline CPI print in the 8-9% range (and rising).

In short: Rate hikes won’t defeat money supply driven or supply-constraint driven inflation at all.

Thus, and again, what is the Fed really doing and thinking notwithstanding the official nonsense that makes the headlines or pours from their double-speaking lips?

A Weaponized Fed Running Out of Bullets

One answer: The Fed, like the SWIFT removals and FX reserve freezes, is just another weaponized tool against Russia and the seismic shifts (petrodollar, LBMA alternatives, mono-to-multi-currency trade agreements) resulting globally ever since the openly failed sanctions against Russia were commenced earlier this year.

To any who understand the origins, history and actual practices of the Federal Reserve, the notion that this cabal of private bankers is an “independent” entity is by now an open farce.

That is, the Fed is anything but “independent” and is not only a political fixture of the DC horizon, but rather a political hijacker of the American economy, markets and policy in ways the go far, way far, beyond its supposed “mandate” to simply manage U.S. inflation and employment.

It is my own strong belief that one of the primary motives behind the current rate policy to strengthen the USD has been to help the U.S. government break the financial back of Russia, which like all its prior policies/sanctions (based on the re-invigorated Russian currency, trade surpluses and multi-lateral trade agreements) is failing.

Toward this end, it is far more than likely that the Fed’s “weaponized” rate hiking will continue this week, much, frankly to the chagrin of a temporarily falling gold price.

What one has to ask however, is will this policy backfire as well (?), for it seems that this game of financial chicken with Putin is breaking the back of the US markets and economy (and its EU allies) with far greater effect.

Hubris Comes Before the Fall

I am once again reminded of the 2014 statement made by then U.S. Secretary of State, Condoleezza Rice, that Russia would run out of money long before the West ran out of energy.

Less than a decade after this classic example of American hubris was made, it seems Russia (as well as China, the BRICS and a string cite of emerging market economies) would beg to differ as the world shifts from a U.S.-led mono-currency system to an increasingly multi-national currency, trading and political new direction.

None of this, by the way, will be “orderly.”

Within the US markets and economy, conditions keep trending from bad to worse in every category– from risk assets, social division, and political impotence to the headline-making layoffs at Goldman Sachs, the tanking profits at FedEx and the destruction of the U.S. working class under the invisible tax of persistent rather than “transitory” inflation.

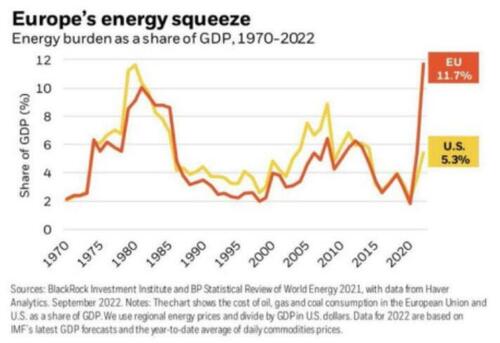

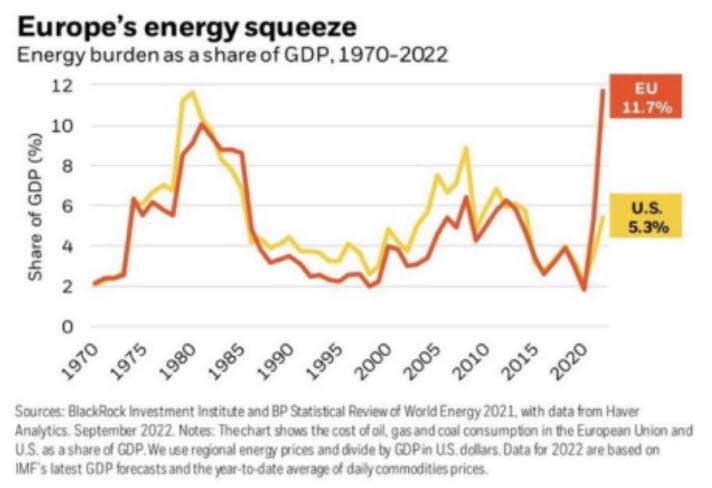

Meanwhile In Europe…

The price for blindly following the so-called “moral” lead of the US in its political and financial war against Putin (to save a less-than-moral thespian like Zelenskyy) is becoming increasingly high as the delusion that Putin has less leverage than the West becomes increasingly harder to sell, swallow or justify.

In addition to facing an extremely cold and expensive winter…

…the Europeans are seeing their currency at 20-year lows against an artificially inflated dollar.

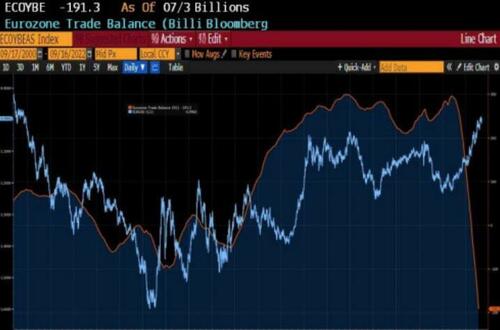

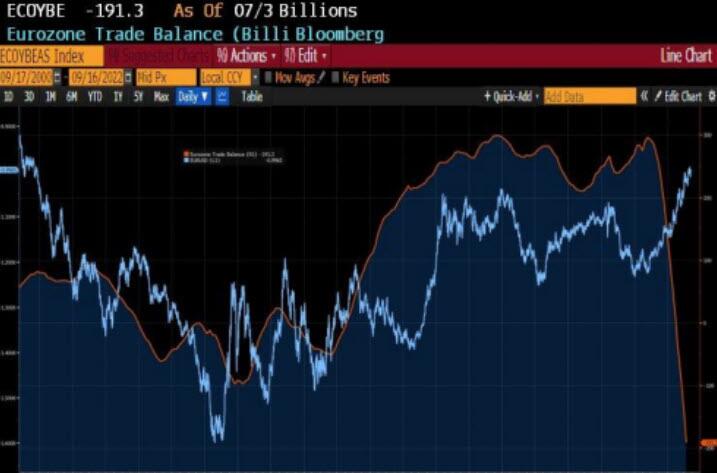

But it’s not only Europe’s (or Japan or England’s) currency which is tanking, but their trade balances as well, which is otherwise atypical, as weakening currencies are supposed to improve rather than weaken export competitivity.

But not this time (see the EU’s trade balance, red line below).

At the End of the Day: Energy Matters

What the failed sanctions, policies and visions of the US-led West are now making abundantly clear is that energy matters, and folks, like it or not, Russia has more of it than the West as the US strangles rather than frees energy production in the US under a suicidal policy of a “green” new normal.

How the West Was Lost

In the immediate years after the Second World War, America’s greatest generation, as well as its dollar and Treasury bond, were undeniable leaders and influencers.

Those days, dollars, bonds and influencers, however, are no more.

But is it not comical to hear the IQ-challenged Governor of a failed state like California pushing electric cars as the new “solution” (?) — an example of open fantasy almost as comical as Christine Lagarde’s latest attempt to blame European inflation on climate change rather than her own bathroom mirror.

Having transitioned from a world of fair pricing, fair wages, gold-backed money, manageable bond obligations and strong exports, America has devolved into a modern feudalism of over-paid executives, a diminishing middle class, Wall Street socialism, a thin-air-backed dollar, a Fed-monetized (i.e., “zombie”) bond market, exported/outsourced labor and hence anemic productivity.

Once the world’s greatest producer and creditor, the US is now its greatest importer and debtor, and has not only exported US productivity to cheaper labor zip codes, but also exported its inflation, thereby destroying US credibility, trust and influence at the same rate America destroyed the inherent purchasing power of its so-called “strong dollar.”

The Real Cost of Only Bad Options Ahead

So, what can the Fed-directed/complicit U.S. do going forward in its pyric financial war against a changing, emerging East?

Well, it can send more debased money and scarce energy to its allies in the EU and Japan to avoid disaster there, which can only mean more not less inflation from sea to shining sea in the US.

Or, perhaps America’s allies in Brussels or Tokyo could cry “uncle” and reach a separate energy agreement with the Eastern nations who actually have the energy they need, an option which not only keeps the folks of the EU and Japan warmer, but improves their embarrassing trade imbalances (above) which resulted from the demands of Biden’s unofficial caretakers rather than the demands of realpolitik.

Of course, any such détente or separate arrangement would have to be paid for with printed euros and Yen, only adding to the global inflationary swamp our central bankers have created since the invention of the first mouse-click money printer.

As a final option, of course, Europe and Japan could simply stay the Western course and suffer an economic and currency crash (as the Yen hits 50-year lows) which would make 2020 or even 2008 seem like pleasant memories.

The West: Marching Toward a Breaking Point (and Pivot)

Without the benefit of a crystal ball or insider-influence within DC, Brussels or even Davos, one can only speculate rather than predict future events as dictated by current political charlatans.

Perhaps Japan and the EU will join the ever-increasing trend as well as crowd toward de-dollarization and reach a separate peace (i.e., trade arrangement) with the East on energy imports.

Equally likely, as well as mathematically essential, is that the Fed, after feigning concern for inflation (which they in fact needed to inflate away Uncle Sam’s bar tab), will pause and then pivot its failed QT policies by early 2023 and bring the USD and interest rates (via YCC) down to levels essential to combat a recession which they pretend doesn’t exist.

Despite all the fake, real, twisted, straight or bent words, facts and policies emerging today, the West in general and the US in particular cannot escape the natural laws of debt nor the hard realities (as well as consequences) of pretending that more debt, paid for with increasingly debased, mouse-clicked currencies, is a viable policy rather than an open comedy, as well as insult to the long-forgotten science of economics.

Once the reality of math supersedes the current DC policy of fluff, distraction and finger-pointing, the USD will come down, bond markets will be further “accommodated” and currencies will be increasingly debased.

At that looming turning point, of course, those holding gold will see its recent lows race toward record highs.

Why so certain?

Because, math, history and common sense have shown us (from the Ming Dynasty or 3rd century Rome, to 18th century France, 20th century Weimar and 21st century America) that all debt-soaked, decadent and fiscally wayward nations destroy their fiat currencies without exception, and the “modern” West will be no exception.

Not at all.

END

3.Chris Powell of GATA provides to us very important physical commentaries

Your weekend reading material: the danger of high interest rates and problems with fiat currencies.

(Alasdair Macleod)

Alasdair Macleod: Gold has never been so attractive

Submitted by admin on Thu, 2022-09-22 11:28Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, September 22, 2022

In our lifetimes we have not seen anything like the developing economic and financial crisis. Rising interest rates are way, way behind reflecting where they should be.

Interest rates have yet to discount the continuing loss of purchasing power in all major currencies. The theory of time preference suggests that central bank interest rates should be multiples higher to compensate for the current loss of currency purchasing power, enhanced counterparty risk, and a rapidly deteriorating economic and monetary outlook.

There is no doubt that the majority of investors are not even aware of the true scale of danger that interest rates pose to their financial assets. Some wealthier, more prescient investors are only in the early stages of beginning to worry.

But if you liquidate your portfolio, you end up with depreciating cash paying insufficient interest. What can you do to escape the fiat currency trap?

This article argues that having everything in fiat currencies is the problem. The solution is a flight into real money — that is only physical gold, as the rest is rapidly depreciating fiat credit.

Owning real money is the only way to escape the calamity that is engulfing our current economic, financial, and fiat currency world. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/gold-has-never-been-so-attractive?gmrefcode=gata

end

For your interest…

(the Hill/GATA)

Trump was once paid in gold bars by leaseholder, book says

Submitted by admin on Thu, 2022-09-22 21:09Section: Daily Dispatches

By Zach Schonfeld

The Hill, Washington

Thursday, September 22, 2022

Former President Trump was once paid with dozens of gold bars to cover the lease of a Manhattan parking garage he owned, according to a new book.

New York Times journalist Maggie Haberman’s forthcoming book, titled “Confidence Man: The Making of Donald Trump and the Breaking of America,” includes an episode detailing the payment and other business practices, according to an excerpt shared with CNN.

The book, which comes out on Oct. 4, chronicles Trump’s life as a New York City businessman to his rise to the presidency. …

… For the remainder of the report:

end

4. OTHER GOLD/SILVER COMMENTARIES

andrew maguire

| Harvey Organ <harveyorgan@gmail.com> | 9:37 AM (19 minutes ago) | ||

| t |

5.OTHER COMMODITIES:

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.1198

OFFSHORE YUAN: 7.1312

SHANGHAI CLOSED: DOWN 20.54 PTS OR 0.66%

HANG SENG CLOSED DOWN 214.68 PTS OR 1.18%

2. Nikkei closed

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 112.00/Euro FALLS TO 0.97448

3b Japan 10 YR bond yield: FALLS TO. +.230/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 142.83/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.025%***/Italian 10 Yr bond yield FALLS to 4.28%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.16%…** DANGEROUS

3i Greek 10 year bond yield RISES TO 4.64//

3j Gold at $1648.20 silver at: 19.08 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 2 AND 02/100 roubles/dollar; ROUBLE AT 56.79//

3m oil into the 80 dollar handle for WTI and 87 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

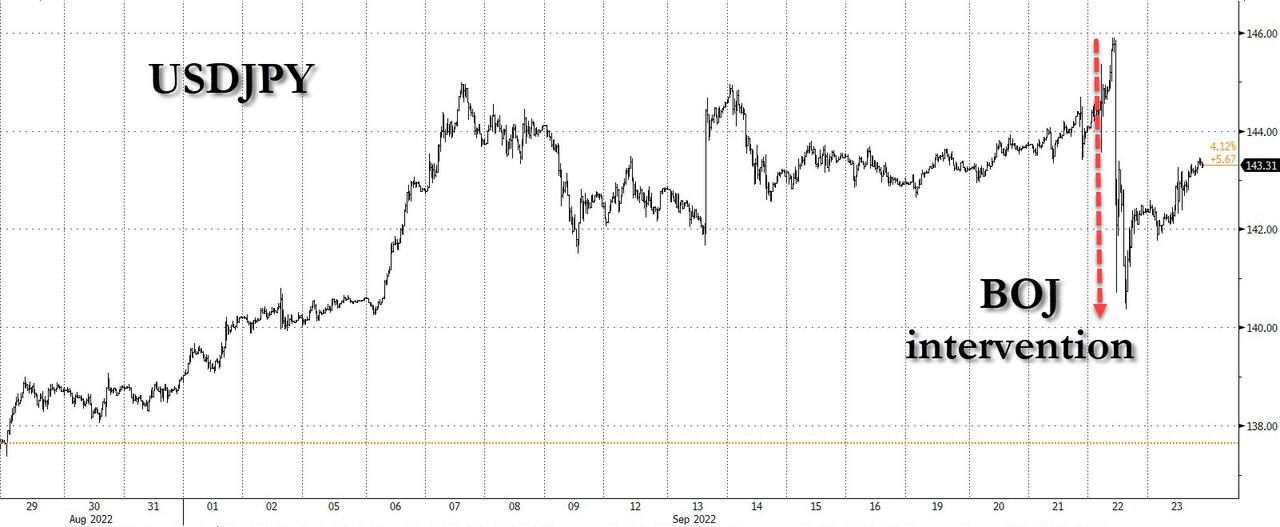

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 142.83DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this .9803– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9553well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

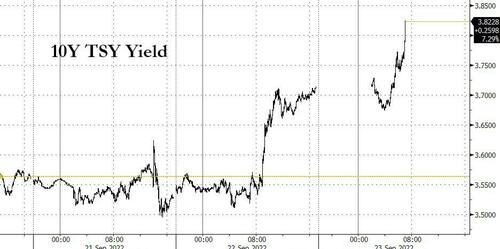

USA 10 YR BOND YIELD: 3.774 UP 7 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.675 UP 4 BASIS PTS//(USA 30 YR INVERTED TO THE USA 10)

USA DOLLAR VS TURKISH LIRA: 18,41…GETTTING DANGEROUS

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

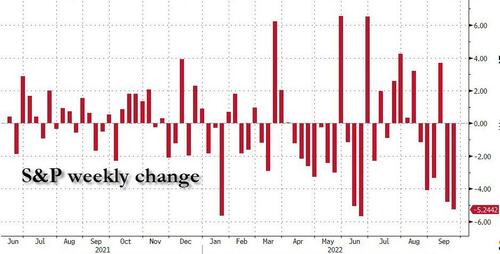

Futures Crash, Stocks At 2022 Lows; Yields, Dollar Explode As UK Stimulus Plan Sparks Global Market Panic

FRIDAY, SEP 23, 2022 – 08:03 AM

One week after stocks suffered their biggest drop since June, futures are in freefall on Friday with the dollar soaring to the now default daily record high…

… 10Y yields exploding higher, surging more than 10bps so far today…

… in what appears to be the latest bond market flash smash which has pushed 10Y yields to the highest level since 2010…

… and S&P futures plunging over 1.4%, and the S&P set to open at a fresh 2022 low…

… with futures set to drop nearly 5% (or more) for a 2nd consecutive week, and down 5 of the past 6 weeks!

Besides the soaring dollar, two other drivers contributed to today’s widespread market panic:

- first, the shocking UK mini budget saw the country’s new administration slash tax rates by the most since 1970s at a time when the country is about to enter recession and is battling with runaway inflation which crashed UK bonds and sent the pound tumbling to a 37 year low as markets priced in a more aggressive pace of tightening to offset the government’s growth plan,

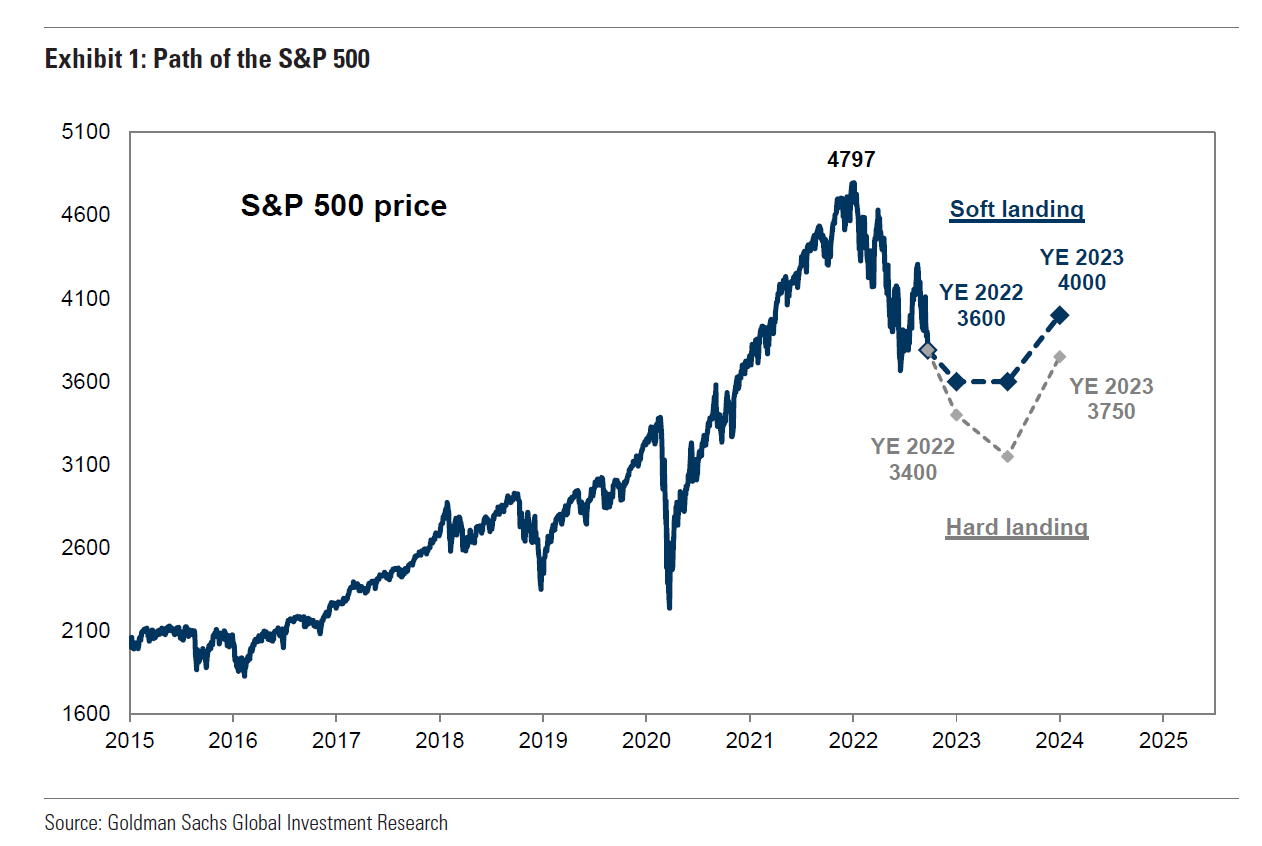

- second, traders also freaked out over a Goldman research report which slashed the bank’s S&P price-target to just 3,600 from 4,300, making the bank one of the biggest bears on Wall Street.

In premarket trading, Costco shares declined 3.3% as analysts flagged that volatility may remain high for the company’s shares. Analysts mostly welcomed its report of modest improvements in inflation and supply chains. here are the other notable premarket movers:

- AMD shares dropped 1.5% in premarket trading as Morgan Stanley trimmed price target to $95 from $102, citing a worsening PC end market and headwinds on the client business, including a collapse in gaming GPUs.

- Tritium DCFC shares jumped 4% in postmarket trading, following six straight losing sessions, after the maker of electric-vehicle chargers reported sales orders of $203 million for fiscal year ended June 30, and revenue of $86 million.

- CalAmp gained 3% postmarket after the maker of tracking devices posted fiscal 2Q revenue that beat estimates.

- DocuSign edged higher in postmarket trading after announcing that the board of directors has hired Allan Thygesen as Chief Executive Officer.

Europe’s Stoxx 600 dropped more than 1%, declining 20% from January record high, set to enter a new bear market. Energy, miners and real estate are the worst-performing sectors amid broad-based declines. Here are the most notable European movers:

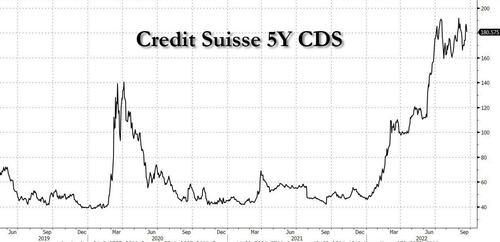

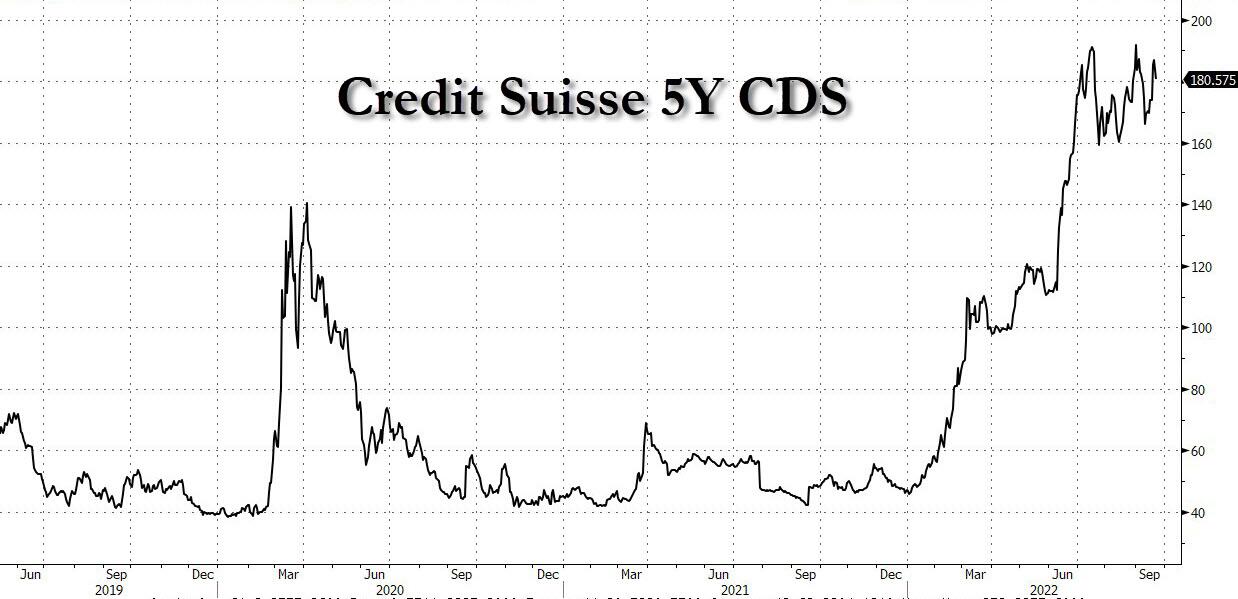

- Credit Suisse shares declined as much as 9.4% to a record low for a second day running, even as the bank denied a report that it was considering an exit from its US operations

- Ericsson falls as much as 6.1% to 2-year lows after a Radio Sweden report saying the communications equipment maker continued to send products to Russia after saying deliveries had been suspended

- Energy is among the worst-performing sectors on Europe’s Stoxx 600 index on Friday, with the subindex falling as much as 2.6% to the lowest since July 27 as oil heads for a fourth weekly loss

- European warehouse firms slide after Barclays issued a review on the sector, cutting target prices on average by 20%, downgrading Tritax Big Box REIT and Warehouses De Pauw to underweight

- Bureau Veritas falls as much as 5% after Oddo cuts to underperform, saying the valuation gap with peers and recent stock performance seems to leave more downside than upside in relative terms

- Nordic Semiconductor shares rise after DNB said it had found a component from the firm in the latest version of Apple’s AirPods Pro earphones which were released today. Varta, meanwhile drops as much as 13% after DNB found batteries from its rival Samsung in the new earphones

- UK homebuilders, retailers and banks get a boost as Chancellor of the Exchequer Kwasi Kwarteng announces several tax relief measures, with much of the sector trimming earlier losses

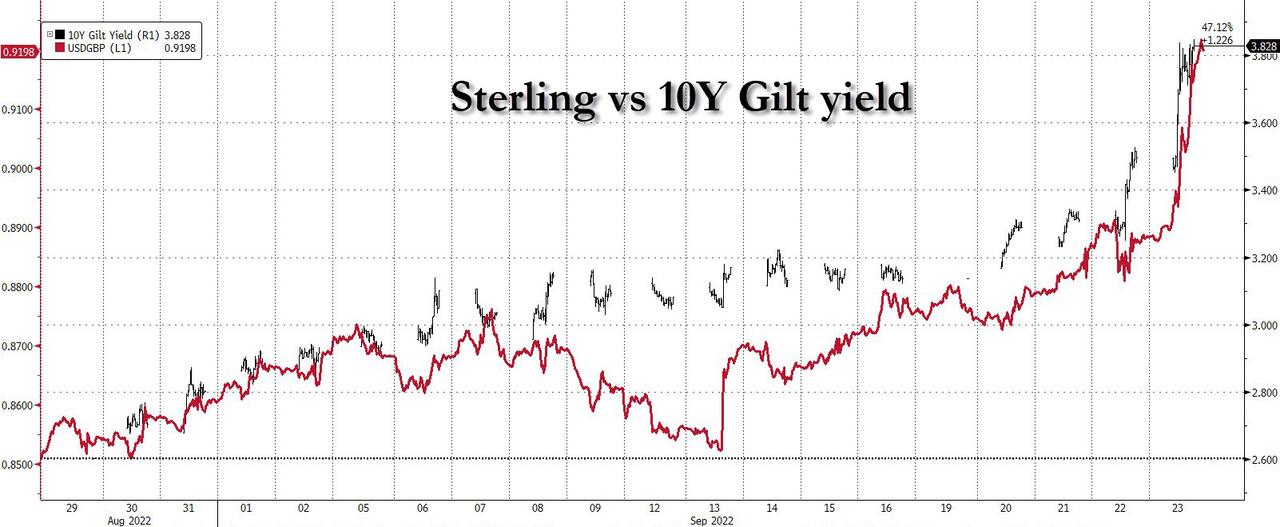

As reported earlier, UK stocks, bonds and the cable all plunged as traders ramped up their bets on Bank of England rate hikes, betting on a 50% chance of a 100-basis-point increase from the central bank at its next rate decision in November, as the government set out its most radical package of debt-financed tax cuts since 1972 and the Debt Management Office increased its gilt sales plan more than expected. “The markets will do what they will,” said Chancellor of the Exchequer Kwasi Kwarteng, when challenged in parliament on the mayhem in markets.

The European Central Bank will also forge ahead with increases in borrowing costs, according to Governing Council member Martins Kazaks, even as recession risks rise across the continent.

Earlier in the session, Asian stocks fell, with investors continuing to flee riskier assets as Treasury yields surged following the Fed’s rate hike that increased recession fears. The MSCI Asia Pacific Excluding Japan Index slipped as much as 1.6% while the broader MSCI Asia Pacific Index was on course for its sixth weekly retreat, the longest losing streak since May. TSMC and Tencent were the biggest drags on both gauges as the tech sector led declines. All markets in the region dropped, with several hitting grim milestones. Hong Kong’s Hang Seng Index fell to the lowest in more than a decade, while South Korea’s Kospi finished at its lowest since Oct. 2020. Australia’s benchmark fell nearly 2% as the country resumed trading after a holiday. Japan was closed.

“The intense tightening by the Federal Reserve to go all-out against inflation heightened fears that it could destroy demand and cause a recession,” said Han Jiyoung, an analyst at Kiwoom Securities in Seoul. The MSCI Asia Pacific Index has lost about a third of its value from a 2021 peak as the Fed’s rate-hike campaign and the strengthening US dollar prompted an exodus of funds from emerging markets. China’s regulatory crackdowns and its strict Covid lockdown policies have also weighed on sentiment. Hong Kong stocks ended in the red even as the city scrapped hotel quarantine for inbound travelers, the most substantial move yet in the city’s push to revive its status as a global financial center. “It’s optimistic to think a recession can be avoided and in our opinion any chance of a soft landing has evaporated,” said George Brown, an economist at Schroders. “We believe a recession will be needed to bring inflation under control.”

In rates, the yield on 10- year Treasuries exploded higher as bonds briefly flash crashed, sending the 10Y yields as low as 3.82% in a bear-flattening move that lifted front-end yields more than 10bp; 2-year and 3-year yields peak above 4.25% with all tenors reaching multiyear highs. Move follows soaring gilt yields where belly of the UK curve is cheaper by 50bp on the day into early US session, while the UK pound drops to a fresh 27-year low as mounting fiscal stimulus threatens to undermine Bank of England’s control on inflation. US yields are cheaper by 12bp to 5bp across the curve with front-end led losses flattening 2s10s by 3.5bp, 5s30s by 7.5bp on the day; 10-year yields around 3.80%, outperforming gilts by ~20bp in the sector.

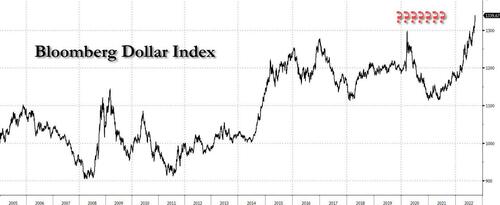

In FX, the dollar rallied broadly, hitting a new all-time high against a currency basket and pushing the euro to a 20-year low wjhile the pound plunged to a fresh 35 year low just above 1.10 after the new UK government unveiled a massive fiscal stimulus plan to boost economic growth, which is sure to send inflation soaring even higher and force the BOE to do even more QT and so on. Safe-haven demand also boosted the greenback amid more signs of a slowing Chinese economy, which raised concerns about the outlook for global economic growth.

- Broad dollar strength pushed the Bloomberg Dollar Spot Index as much as 0.6% higher, hitting its highest on record going back to 2005

- The euro fell as much as 0.9% to 0.9751, its weakest level since 2002. The single currency extended losses after sizable stop-loss orders were triggered below 0.9800 and 0.9780, a Europe-based trader says. Options-related bids at $0.9750 and $0.9700 were seen offering near-term support.

- The pound sank nearly 1% to 1.1151, a 35-year low, pushing the Bloomberg UK Pound Index to its a lifetime high. The UK currency trimmed losses as the UK government announced a massive fiscal stimulus plan to boost economic growth.

“For the USD to weaken meaningfully, the Fed has to get more concerned about growth than inflation-and we are not there yet.” Bank of America analysts write in a note. It adds that, for the euro to start appreciating, “the ECB needs not only to act, but also to communicate forcefully.”

In commodities, WTI drops more than 2% lower to trade just above $80, a level where OPEC+ production cuts are expected. Spot gold falls roughly $9 to trade near $1,662/oz. Spot silver loses 1.1% near $19.

Looking to the day ahead now, data releases include the September flash PMIs for Europe and the US. Otherwise, central bank speakers include Fed Chair Powell, as well as the ECB’s Kazaks and Nagel. Remember the Italian election on Sunday.

Market Snapshot

- S&P 500 futures down 0.5% to 3,752.25

- MXAP down 1.2% to 145.59

- MXAPJ down 1.6% to 470.98

- Nikkei down 0.6% to 27,153.83

- Topix down 0.2% to 1,916.12

- Hang Seng Index down 1.2% to 17,933.27

- Shanghai Composite down 0.7% to 3,088.37

- Sensex down 1.6% to 58,191.14

- Australia S&P/ASX 200 down 1.9% to 6,574.73

- Kospi down 1.8% to 2,290.00

- STOXX Europe 600 down 0.9% to 396.36

- German 10Y yield little changed at 1.93%

- Euro down 0.8% to $0.9756

- Brent Futures down 1.9% to $88.75/bbl

- Gold spot down 0.4% to $1,664.46

- U.S. Dollar Index up 0.60% to 112.03

Top Overnight News from Bloomberg

- BofA Says Cash is King as Investor Pessimism Hits 2008-Era High

- Goldman Slashes S&P 500 Target Citing Higher Fed Rates Path

- UK Sets Out Biggest Tax Cuts Since 1988 to Boost Economic Growth

- Era of Inflation Has Ended — for Asset Prices on Wall Street

- Oil Set for Fourth Weekly Loss With Rate Hikes Darkening Outlook

- Goldman to BofA Throw in the Towel on a Year-End Rally in Europe

- Treasury Selloff Drives SOFR Spread Toward Record One-Day Drop

- Wall Street’s Top Banks Are Backing Oil to Stage a Recovery

- Nasdaq Increases Scrutiny of Small-Cap IPOs After Big Swings

- Japan Has a Pile of Dollars It Can Tap Before Selling Treasuries

- Chinese Money Pours Into Offshore Debt After Rare Yield Reversal

- China Compares Taiwan Independence Push to Charging Rhino

- China’s Most Locked-Down City Shows Perils of Endless Covid Zero

- Crypto Outperforms Stocks for a Change as Correlation Breaks

- Raytheon Beats Lockheed, Boeing on $1 Billion Hypersonic Job

- Zelle Emerges as Lawmakers’ Surprise Foe at Bank Hearings

- Alex Jones Renews ‘Deep State’ Claim at Defamation Trial

- It’s Every Nation for Itself as Dollar Batters Global Currencies

- Nikola Investor Lost $160,000 on Milton’s Hype, He Tells Jury

- FedEx to Cut Costs, Hike Rates in Battle Against Flagging Demand

- With Shelters Overflowing, NYC to Put Up Tents for Migrants

- Senior-Care Provider Cano Health Said to Weigh Sale

- Banks Dust Off Lockdown Plans to Beat Possible Power Blackouts

A more detailed look at global markets courtesy of Newsquawk

Asian stocks were negative in the aftermath of the rush of global central bank rate hikes during ‘Super Thursday’ and with risk appetite not helped by the absence of participants in Japan for the Autumnal Equinox Day. ASX 200 was heavily pressured on return from yesterday’s national day of mourning closure and took its first opportunity to react to the hawkish FOMC with the tech and consumer-related sectors the worst hit. KOSPI declined with the recent flurry of central bank rate hikes adding to the arguments for the BoK to continue on its hiking cycle as South Korean officials look to avert one-sided currency moves. Hang Seng and Shanghai Comp slightly deteriorated throughout the session as the early support from reports regarding Hong Kong and Macau potentially easing restrictions for arrivals gradually waned, while US audit watchdog officials recently arrived in Hong Kong for audit inspections as firms seek to avoid delisting from US exchanges.

Top Asian News

- White House Indo-Pacific coordinator said China clearly has ambitions in the Pacific which have caused concerns among Pacific Island leaders, according to Reuters.

- Hong Kong will announce today the end of mandatory hotel quarantine for overseas arrivals, according to SCMP.

- Japan PM Kishida said excessive yen movement repeatedly caused by speculation cannot be overlooked and they will take action should there be any excessive volatility in the yen, according to Reuters.

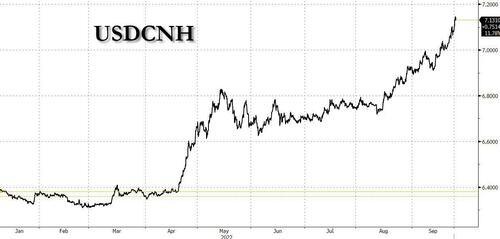

- Yuan Weakens to Near Trading Band Limit as Pressure Mounts

- China Junk Debt Ends Longest Rally of Year as Distress Mounts

- Times China Told Bondholders It Hasn’t Paid Interest Due Thurs

- Peak Pessimism Setting in for Chinese Stocks Ahead of Congress

- Iron Ore Fluctuates as China Steel Hub Tangshan Lifts Lockdowns

- JPM Analysts Liken UK Bank Deposit Speculation to Windfall Tax

European bourses are pressured across the board after the Flash PMI releases for the region indicate a contraction; Euro Stoxx 50 -1.5% Pressure that was exacerbated, particularly in the UK, on the mini-Budget and subsequent Gilt/BoE pricing, despite the measures being designed to stimulate the economy. Stateside, futures are lower in sympathy and continuing APAC performance awaiting their own PMI metrics and Fed commentary.

Top European News

- ECB’s Kazaks says they will continue to hike rates, via Bloomberg; adds, faster Fed hikes have weakened the EUR. His choice for the October ECB hike is either 50bps or 75bps.

- UK COVID-19 hospitalisations rose 17% in a week which is the first significant increase since July and is sparking fears of a new wave, according to The Telegraph.

- Credit Suisse Hits Fresh Low; Denies Report of Looming US Exit

- UK Probably in Recession as Pound’s Weakness Boosts Inflation

- UK Bonds Plunge as Debt Office Plans More Sales Than Expected

- VW Warns of Production Shift From Germany Over Gas Shortage

- Ericsson Governance Worries Mount After Russia Sales Debacle

- European Watchdog Backs New Trading Halts for Energy Market

FX

- DXY has surged to a fresh 112.3+ peak to the detriment of peers across the board with the Yuan taking the strain.

- GBP dented post-PMIs/budget despite initial support from BoE pricing as the USD’s surge continues.

- Amidst this, EUR has been hit on the flash-PMIs and accompanying commentary around recession fears and a resurgence in price pressures.

Fixed Income

- Gilts decimated to sub-99.00 from the 102.30 region in wake of the budget and accompanying fund consideration and potential inflationary implications

- Action that has sparked a surge in BoE pricing with markets now implying a 50/50 chance of a 100bp increase in November.

- More broadly, EGBs and USTs are dragged down in tandem though seem to have reached a ‘floor’ ahead of the afternoon’s events.

Commodities

- Crude benchmarks are pressured by pronounced USD strength and risk action amid recessionary fears.

- Additionally, participants are attentive to potential weekend developments with EU member states set to discuss Russian sanctions.

- Russian President Putin spoke to Saudi Crown Prince MBS and discussed the question of coordination to ensure stability in the oil market, while they praised efforts within the OPEC+ framework and confirmed the intention to continue sticking to existing agreements, according to Reuters.

- Metals dented across the board by the USD with base metals in particular hit amid broader sentiment with LME Copper slipping below USD 7.5k/T.

US event calendar

- 09:45: Sept. S&P Global US Composite PMI, est. 46.1, prior 44.6

- 09:45: Sept. S&P Global US Services PMI, est. 45.5, prior 43.7

- 09:45: Sept. S&P Global US Manufacturing PM, est. 51.0, prior 51.5

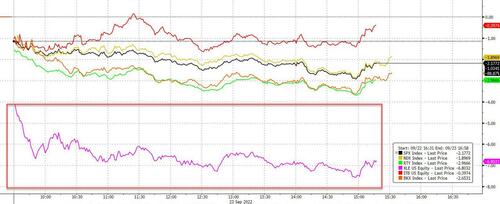

DB’s Jim Reid concludes the overnight wrap

It’s a bit of a broken record at the moment as markets have again been reeling over the last 24 hours, with another major selloff for bonds and equities taking place after central bankers showed no sign of letting up on their campaign of rate hikes to tackle inflation. The hawkish Fed decision on Wednesday set the backdrop for the slump, but that was compounded by further hikes yesterday in the UK, Switzerland, Norway, South Africa, Indonesia and the Philippines. Inturn, that led investors to expect an even more aggressive pace of rate hikes over the months ahead, with current market pricing for each of the Fed, ECB and the BoE indicating that a 75bps hike at the next meeting is now considered the most likely outcome for all three.

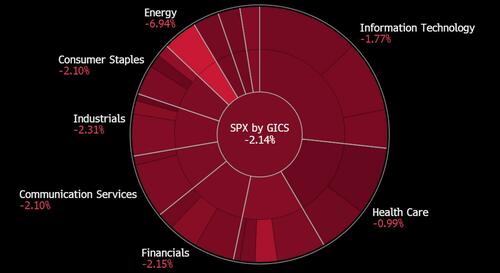

In terms of those market moves, equities lost ground across the board as the prospect that tighter monetary policy would trigger recessions moved increasingly into view. The S&P displayed a lot of volatility into the close, ultimately falling -0.84% and moving deeper into bear market territory and on track for its worst annual performance since 2008. Under the hood, sector performance had a consistent macro story, where there was an outperformance in defensives (health care led the way up +0.51%) and an underperformance in cyclicals (discretionary lagged at -2.16%).

In Europe the losses were even more severe as they finally got to react to the Fed’s announcement the previous evening, with the STOXX 600 (-2.09%) actually falling beneath its July lows to close at levels unseen in over 20 months. It’s fascinating that there’s hardly been any wider mention of the Italian election this Sunday even with the centre-right populists ahead in the polls. There are much bigger things to worry about to be fair and it seems that there is limited political appetite in Italy at the moment to deviate too far from EU fiscal rules. See here for our economists’ preview.

The declines mentioned above for equities were just as dramatic for sovereign bonds, with yields on 10yr Treasuries surging by +18.4bps to a post-2011 high of 3.71%. That was primarily driven by a rise in real yields, which similarly hit a high for the decade at 1.30%. We did get some positive data on the weekly initial jobless claims, which came in at 213k (vs. 217k expected) for the week ending September 17, and the previous week was revised down -5k. But that just compounded the selloff, since the fact that claims are on a firmly downward trend was seen as giving the Fed even more space to hike rates over the coming months without worrying about a sharp rise in unemployment. Those expectations of additional rate hikes were evident among Fed funds futures, which moved towards the more hawkish FOMC dot plot, with the rate implied by December 2023 up +10.0bps on the day to 4.33%.

Over in Europe it was much the same story, with yields on 10yr bunds (+7.2bps), OATs (+7.8bps) and BTPs (+3.9bps) seeing fresh rises. Gilts were the biggest underperformer however, with 10yr yields up +18.1bps after the Bank of England hiked by 50bps for a second consecutive meeting, taking Bank Rate up to 2.25%. The decision was a 3-way split among policymakers, with 5 of the 9 MPC members in favour of the 50bp hike, 3 members wanting a larger 75bps move, and 1 wanting a smaller 25bps hike. They also voted (unanimously) to reduce the stock of gilts by £80bn over the next 12 months. Our UK economist sees this decision as slightly hawkish (link here), and sees the BoE as having opened the door for a larger rate hike in November. As a result, he now expects that the MPC will deliver a 75bps hike at the next meeting, although this is a very close call, with the terminal rate still reaching 4% in this hiking cycle.

Staying on the UK, it’s also an important day on the fiscal side as new Chancellor Kwasi Kwarteng will be unveiling the government’s Growth Plan in the House of Commons this morning. Ahead of that, we got confirmation yesterday that the 1.25pp increase in National Insurance (a payrolls tax) is going to be reversed from 6 November. Otherwise, it’s been widely reported that they’ll confirm that corporation tax will remain frozen at 19%, rather than increasing to 25% as had been planned, and recent days have also seen press speculation about a potential cut to stamp duty (the home purchase tax). Our UK economist has a preview of the event here.

On oil, the EU is apparently working on a new effort to impose a price cap on Russian oil in response to President Putin’s escalation and partial mobilisation announcement yesterday. However, the plan will still face hurdles given the dire energy situation in Europe and the need to arrive at an unanimous decision. Elsewhere, the Nigerian oil minister echoed previous remarks from other cartel members by saying OPEC may need to cut output if prices fell more. Brent crude prices were +0.70% higher, after being as much as +3.31% higher intraday but are back roughly to where they were 24 hours ago this morning in Asia.

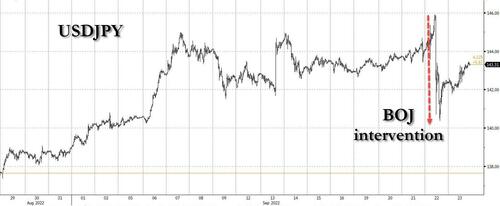

Looking elsewhere, there was plenty of other monetary action to digest after Japan intervened to support the Yen for the first time since 1998. That came shortly after the BoJ’s latest decision we mentioned in yesterday’s edition, which saw the yen weaken above 145 per US Dollar initially, before the intervention led to a sharp pullback that saw the yen close at 142.39. Confirmation came from Masato Kanda, Japan’s top currency official, who said that “The government is concerned about excessive moves in the foreign exchange markets, and we took decisive action just now”. In a statement from the US Treasury, a spokesperson said that “We understand Japan’s action, which it states aims to reduce recent heighted volatility of the yen.” George Saravelos writes here that the intervention is unlikely to work and could lead to an unnecessary loss of reserves and credibility.

Asian equity markets are limping towards a sixth weekly loss this morning. The Kospi (-1.59%) is the largest underperformer across the region mirroring Wall Street losses overnight followed by the Shanghai Composite (-1.08%), CSI (-0.96%) and the Hang Seng (-0.91%). Elsewhere, markets in Japan are closed for a holiday with no trading of cash Treasuries in the Asian trading hours. US stock futures are pointing to further declines today with those on the S&P 500 (-0.17%) and NASDAQ 100 (-0.28%) both down.

Early morning data from Australia showed that the flash manufacturing PMI rose slightly to 53.9 in September from 53.8 in August while the services PMI came in at 50.4 compared to 50.2 in August.

In other news, Japan is ending its Covid-19 restrictions and opening the door back up to mass tourism in a move to revive the nation’s tourism industry as the Covid pandemic recedes. The new policies will come into effect on October 11.

In terms of yesterday’s other data, sentiment wasn’t helped after the European Commission’s consumer confidence indicator for the Euro Area fell to a record low of -28.8 in September on the preliminary reading. Bear in mind that series covers both Covid and the GFC so that’s a seriously negative print. Over in the US, the Kansas City Fed’s manufacturing index fell to 1 in September (vs. 5 expected), marking its lowest level since July 2020.

To the day ahead now, and data releases include the September flash PMIs for Europe and the US. Otherwise, central bank speakers include Fed Chair Powell, as well as the ECB’s Kazaks and Nagel. Remember the Italian election on Sunday.

AND NOW NEWSQUAWK

Contraction/recession concerns post-PMIs hit sentiment, Gilts sink post-Kwarteng – Newsquawk US Market Open

FRIDAY, SEP 23, 2022 – 06:59 AM

- European bourses are pressured across the board after the Flash PMI releases for the region indicate a contraction & resurgence in price pressures; Euro Stoxx 50 -1.5%

- Stateside, futures are lower in sympathy and continuing APAC performance awaiting their own PMI metrics and Fed commentary

- Gilts decimated to sub-99.00 from the 102.30 region in wake of the mini-Budget and accompanying fund consideration and potential inflationary implications

- DXY surging to a fresh 112.3+ peak to the detriment of peers across the board, GBP pressure exacerbated post-Kwarteng

- Crude benchmarks are pressured by pronounced USD strength and risk action amid recessionary fears; awaiting potential weekend updates

- Looking ahead, highlights include US Flash PMIs and a speech from Fed Chair Powell.

As of 11:20BST/06:20ET

View the full premarket movers and news report.

Or why not try Newsquawk’s squawk box free for 7 days?

LOOKING AHEAD

- Looking ahead, highlights include US Flash PMIs and a speech from Fed Chair Powell.

- Click here for the Week Ahead preview.

UK MINI-BUDGET

- Click here for the newsquawk snap analysis and reaction to the mini-Budget.

- Chancellor Kwarteng says to support the energy market, is announcing a financing scheme with the BoE; energy cap will reduce cost of servicing index-linked debt.

- Estimated cost of energy plan is uncertain, total cost likely to be GBP 60bln over the next six-months; It is right to borrow to fund temporary support, like UK did in COVID pandemic.

- Announced numerous wide-ranging tax reductions/incentives, to be worth GBP 45bln in total.. Full details on the newsquawk headline feed

- UK DMO says net financing requirement for 2022-23 is GBP 234.1bln (April revision: GBP 161.7bln); gross 2022-23 Gilt issuance seen at GBP 193.9bln (vs April revision of GBP 131.5bln). Increased Gilt issuance concentrated on shorter-dated Gilts, DMO to hold one additional conventional Gilt syndication in week of 31st October, for Jan 2038, DMO to hold 13 extra Gilt auctions in the rest of the 2022-23 year.

- Cost of UK Chancellor Kwarteng’s fiscal package is GBP 161bln over a five-year period, via Bloomberg.

- UK Chief Secretary to the Treasury says OBR forecast most likely to be published in December; says Government is sticking to its spending review which was published in 2021

GEOPOLITICS

RUSSIA-UKRAINE

- Referendums on Russian annexation begin in occupied Ukrainian territory, according to AFP News Agency.

- Russia’s Kremlin says “The negotiation process with Ukraine is required to achieve our goals, but we see no signs of resuming it”, via Sky News Arabia.

CHINA-TAIWAN