SEPT 30/FIRST DAY NOTICE FOR GOLD/SILVER CONTRACTS AT THE COMEX: GOLD CLOSED UP $3.75 TO $1664.35//SILVER CLOSED UP $31 TO $19.07//PLATINUM CLOSED UP 40 CENTS TO $867.30//PALLADIUM CLOSED DOWN $33.55 TO $2182.85//MUST READ: TED BUTLER ON THE MANIPULATION INSIDE THE GOLD/SILVER COMEX//UPDATES ON THE EXPLOSION RE NORDSTEAM 1 AND TWO//RUSSIA ANNEXES THE OBLASTS AND THE WEST RESPONDS//COVID UPDATES: DR PAUL ALEXANDER//VACCINE IMPACT//VACCINE INJURY//PROBLEMS CONTINUE IN THE UK WITH PENSION FUNDS STILL LIQUIDATING//USA CORE PCE (FED’S INDICATOR FOR INFLATION) RED HOT//TWO USA STOCKS CRASH: CARNIVAL CRUISE LINES AND RENT- A -CENTER AND NIKE//UPDATES ON THE AFTER AFFECTS ON HURRICANE IAN AND THE UPCOMING ONSLAUGHT ATTACK ON SOUTH CAROLINA// SWAMP STORIES FOR YOU TONIGHT//

072 C GOLDMAN 2000 553 072 H GOLDMAN 3900 104 C MIZUHO 13 118 C MACQUARIE FUT 715 118 H MACQUARIE FUT 173 323 C HSBC 19 323 H HSBC 2929 365 H ED&F MAN CAPITA 2 435 H SCOTIA CAPITAL 48 624 C BOFA SECURITIES 865 624 H BOFA SECURITIES 862 657 C MORGAN STANLEY 2418 661 C JP MORGAN 3912 6372 685 C RJ OBRIEN 5 686 C STONEX FINANCIA 9 686 H STONEX FINANCIA 382 690 C ABN AMRO 352 709 C BARCLAYS 7412 709 H BARCLAYS 2383 732 C RBC CAP MARKETS 311 800 C MAREX SPEC 97 878 C PHILLIP CAPITAL 4 880 C CITIGROUP 3845 905 C ADM 75

TOTAL: 19,828 19,828 MONTH TO DATE: 19,828

JPMORGAN STOPPED

GOLD: NUMBER OF NOTICES FILED FOR OCT CONTRACT:

19,828 NOTICES FOR 19,828 OZ //61.67 TONNES

total notices so far: 19,828 contracts for 1,982800 oz (61.67 tonnes)

SILVER NOTICES: 55 NOTICES FILED FOR 275,000 OZ/

total number of notices filed so far this month 55 : for 275,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $3.75

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: //// A WITHDRAWAL OF 2.01

TONNES FROM THE GLD/

INVENTORY RESTS AT 941.15 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 31 CENTS

AT THE SLV// ://BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF OF 1.013 MILLION OZ INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 480.917 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL SIZED 74 CONTRACTS TO 129,783 AND CLOSER TO THE NEW RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE SMALL GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.15 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.15) BUT WERE UNSUCCESSFUL IN KNOCKING OFF SOME SPEC SILVER LONGS AS WE HAD A SMALL GAIN OF 276 CONTRACTS ON OUR TWO EXCHANGES. WE DID HAVE ATTEMPTED SPEC SHORT COVERINGS WITH THE BANKERS CONTINUALLY ON THE BUY SIDE.

WE MUST HAVE HAD: I) CONTINUAL SPECULATOR SHORT COVERINGS ////CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.580 MILLION OZ / // V) SMALL SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: –26

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTRACTS for 21 days, total 14,805 contracts: 74.025 million oz OR 3.523 MILLION OZ PER DAY. (705 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 74.025 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 74 WITH OUR $0.15 LOSS IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 175 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /GOOD BANKER ADDITIONS A// NET SPEC SHORT LIQUIDATIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR OCT. OF 1.580 MILLION OZ .. WE HAD A SMALL SIZED GAIN OF 249 OI CONTRACTS ON THE TWO EXCHANGES FOR 1.245MILLION OZ..

WE HAD 55 NOTICE(S) FILED TODAY FOR 275,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 3748 CONTRACTS TO 453,488 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED — -576 CONTRACTS.

.

THE FAIR SIZED DECREASE IN COMEX OI CAME DESPITE OUR TINY LOSS IN PRICE OF $0.85//COMEX GOLD TRADING/THURSDAY / WE HAD FINAL SPREADER LIQUIDATION// SOME SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR OCT. AT 66.102 TONNES ON FIRST DAY NOTICE //NEW STANDING 66.102 TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL COMMENCE ON MONDAY)

YET ALL OF..THIS HAPPENED WITH OUR TINY LOSS IN PRICE OF $0.85 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A SMALL SIZED LOSS OF 219 OI CONTRACTS 0.681 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3529 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 453,488

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 219 CONTRACTS WITH 3748 CONTRACTS DECREASED AT THE COMEX AND 3529 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 357 CONTRACTS OR 1.110 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3529) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (3748): TOTAL LOSS IN THE TWO EXCHANGES 219 CONTRACTS. WE NO DOUBT HAD 1) SMALL ATTEMPTED SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS/// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 66.102 TONNES. 3) ZERO LONG LIQUIDATION //// //.,4) FAIR SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/5/FINAL SPREADER LIQUIDATION.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

65,631 CONTRACTS OR 6,563,100 OZ OR 204.13 TONNES 21 TRADING DAY(S) AND THUS AVERAGING: 3125 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 21 TRADING DAY(S) IN TONNES: 204.13 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 204.13/3550 x 100% TONNES 5.75% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT., FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER,ROSE BY A SMALL SIZED 74 CONTRACT OI TO 129,783 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 175 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 175 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 175 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 101 CONTRACTS AND ADD TO THE 175 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED GAIN OF 249 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 1.245 MILLION OZ

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED DOWN 16.82 PTS OR 0.55% //Hang Seng CLOSED UP 56.96 PTS OR 0.33% /The Nikkei closed DOWN 484.84PTS OR 1.84% //Australia’s all ordinaires CLOSED DOWN 1.21% /Chinese yuan (ONSHORE) closed UP AT 7.1165//OFFSHORE CHINESE YUAN UP 7.1260// /Oil DOWN TO 81.51 dollars per barrel for WTI and BRENT AT 86.99 / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 3748 CONTRACTS TO 453,488 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS FAIR COMEX DECREASE OCCURRED WITH OUR FALL IN PRICE OF $0.85 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (3529 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF OCT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3529EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :3529 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3529 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED SIZED TOTAL OF 219 CONTRACTS IN THAT 3529LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 3748 CONTRACTS..AND THIS SMALL LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR SMALL DROP IN PRICE OF GOLD $0.85. WE HAD OUR CONCLUSION OF SPREADER LIQUIDATION//WE HAD SPEC SHORT DESPERATELY TRYING TO COVER WITH BANKERS TAKING THE BUY SIDE, IT IS BECOMING EXTREMELY DIFFICULT FOR OUR SHORTERS. THUS, WE ARE NOW WITNESSING THE SPECULATORS CONTINUING TO GO MASSIVELY SHORT WHILE THE BANKERS WHO ARE HUGELY LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS ONCE THE SIGNAL HAS BEEN GIVEN TO ANNIHILATE THE SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING OCT (66.099),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 66.099 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $0.85) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A SMALL SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 357 CONTRACTS // WE HAVE REGISTERED A SMALL LOSS OF 249 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR SOCT. (66.099 TONNES)…

WE HAD -576 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 219 CONTRACTS OR 21,900 OZ OR 0.681TONNES

Estimated gold volume 165,761/// poor//

final gold volumes/yesterday 217,443/ fair

INITIAL STANDINGS FOR OCT ’22 COMEX GOLD //SEPT 30

Total monthly oz gold served (contracts) so far this month

19,828 notices 1,982,800 61.67 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

customer withdrawals: 1

i) Out of JPMorgan: 160,755.000 oz

(5,000 kilobars)

total: 160,755.000 oz

total in tonnes: 5.000 tonnes

Adjustments: 1

Brinks: dealer to customer; 6462.351 0z

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCT we have an oi of 21,252 contracts having LOST 1345 contracts .

Thus by definition, the initial amount of gold standing in this active delivery month of October is as follows:

21,251 notices filed x 100 oz per notice = 2,125,100 oz or 66.099 tonnes

This is a huge delivery for a generally poor delivery month.

November GAINED 643 contracts to stand at 2091

December LOST 4427 contracts DOWN to 381,375

We had 19,828 notice(s) filed today for 1,982,800 oz FOR THE OCT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 3912 notices were issued from their client or customer account. The total of all issuance by all participants equate to 19,828 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 6372 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT /2022. contract month,

we take the total number of notices filed so far for the month (19,828) x 100 oz , to which we add the difference between the open interest for the front month of (OCT 21,251 CONTRACTS) minus the number of notices served upon today 19,828 x 100 oz per contract equals 2,125,100 OZ OR 66.099 TONNES the number of TONNES standing in this active month of OCT.

thus the INITIAL standings for gold for the OCT contract month:

No of notices filed so far (19,828) x 100 oz+ (21,252) OI for the front month minus the number of notices served upon today (19,828} x 100 oz} which equals 2,125,100 oz standing OR 66.099 TONNES in this NON active delivery month of OCTOBER.

TOTAL COMEX GOLD STANDING: 66.099 TONNES (A HUMONGOUS STANDING FOR OCT (GENERALLY THE POOREST DELIVERY MONTHS FOR AN ACTIVE MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 55 x 5,000 oz = 275,000 oz

to which we add the difference between the open interest for the front month of OCT(316) and the number of notices served upon today 55 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT./2022 contract month: 55 (notices served so far) x 5000 oz + OI for front month of OCT (316) – number of notices served upon today (55) x 5000 oz of silver standing for the OCT contract month equates 1,580,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

SEPT 21/WITH GOLD UP $4.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.79 TONNES FROM THE GLD///INVENTORY RESTS AT 952.16 TONNES

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

SEPT 13/WITH GOLD DOWN $22.85 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73ONNES FROM THE GLD////INVENTORY RESTS AT 964.91 TONNES

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

AUGUST 31.WITH GOLD DOWN $10.20:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.24 TONNES FROM THE GLD////INVENTORY RESTS AT 973.37 TONNES

AUGUST 30.WITH GOLD DOWN $12.00:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 980.61 TONNES

AUGUST 29/WITH GOLD DOWN $.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD/////INVENTORY RESTS AT 982.64 TONNES

AUGUST 26/WITH GOLD DOWN $26.60; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 25/WITH GOLD UP $9.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

GLD INVENTORY: 941.15 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

SEPT 21/WITH SILVER UP 33 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.902 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 482.115 MILLION OZ//

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

SEPT 13/WITH SILVER DOWN $.31 TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.899 MILLION OZ//

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

AUGUST 31/WITH SILVER DOWN 36 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 3.087 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 465.573 MILLION OZ//

AUGUST 30/WITH SILVER DOWN 34 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 1.478 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 470.135 MILLION OZ//

AUGUST 29/WITH SILVER DOWN 7 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY A THE SLV: A WITHDRAWAL OF 2.765 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 470.135 MILLION OZ//

AUGUST 26/WITH SILVER DOWN 39 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 25/WITH SILVER UP 21 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

CLOSING INVENTORY 480.917 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Hurricane Cleanup Will Stimulate The Economy? Not So Fast!

If the Keynesians are right, Hurricane Ian will create an economic boom here in Florida. After all, breaking windows creates demand and that stimulates the economy. And after this massive hurricane cut through Florida, there were a lot of broken windows — and much worse.

Now, you might be wondering what in the world I’m talking about. How does breaking windows create an economic boom?

I’m referring to the “broken window fallacy” first explained by French economist Frédéric Bastiat. And at some point in the next few weeks, more than one economist will try to put a positive spin on the destruction by claiming it will create economic activity. This is yet another common fallacy we run into whenever their is a disaster, right along with the hand-wringing over price gouging.

Imagine that somebody throws a rock through a shop window. Many economists will argue that’s good for the economy because the shop owner will have to pay the window fixer to repair the window. As Bastiat put it in his essay, “If you have been present at such a scene, you will most assuredly bear witness to the fact, that every one of the spectators, were there even thirty of them, by common consent apparently, offered the unfortunate owner this invariable consolation: ‘It is an ill wind that blows nobody good. Everybody must live, and what would become of the glaziers if panes of glass were never broken?’

You see, the shopowner’s misfortune is the glass fixer’s good luck.

With the money he makes fixing the window, the glazier can go buy a new suit. The tailor will then have money in his pocket to go to a baseball game. The owner of the baseball team benefits from another fan in the seats, and on and on it goes. The broken window led to a string of economic transactions. As Bastiat put it, the careless child “spurred trade to the amount of six francs.”

On the surface, it does seem as if the broken window led to a small economic boom. But when you dig below the surface, it becomes clear that the boom is a mirage.

But if, on the other hand, you come to the conclusion, as is too often the case, that it is a good thing to break windows, that it causes money to circulate, and that the encouragement of industry in general will be the result of it, you will oblige me to call out, ‘Stop there! Your theory is confined to that which is seen; it takes no account of that which is not seen.’”

What have we missed?

We don’t see the money that was never spent.

If the shopkeeper hadn’t had to spend 6 francs on a new window, he would have bought a pair of shoes. Now, that transaction won’t happen and the cobbler won’t receive that income. As a result, the cobbler will have to postpone buying a new book for his library.

Bastiat sums it up this way.

Let us take a view of industry in general, as affected by this circumstance. The window being broken, the glazier’s trade is encouraged to the amount of six francs: this is that which is seen.

“If the window had not been broken, the shoemaker’s trade (or some other) would have been encouraged to the amount of six francs: this is that which is not seen.”

A good economist always tried to account for the unseen. But sadly, most people aren’t good economists — and that includes a lot of economists.

It should be clear breaking a window does not make society better off. It becomes even more clear when you magnify the destruction to the level produced by Hurricane Ian. Yes, billions will be spent to repair and clean up. Roofers, builders and others will make a lot of money. But you have to stop and consider the cost to others. I doubt anybody in Ft. Meyers will claim they’re better off because their house lost a roof or filled up with water. And just stop and imagine whould would have been done with those billions had the hurricane never materialized.

Destruction isn’t progress. This is just silly, Keynesian claptrap.

Never forget the unseen.

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

end

END

3.Chris Powell of GATA provides to us very important physical commentaries

Your weekend reading material

Alasdair Macleod on the failure of the Bank of England….

Alasdair Macleod: Kwarteng and a job half done

Submitted by admin on Thu, 2022-09-29 10:53Section: Daily Dispatches

By Alasdair Macleod GoldMoney, Toronto Thursday, September 29, 2022

Following the new Kwarteng/Truss economic policies revealed in last week’s mini budget for the United Kingdom, the widespread condemnation is a reflex Keynesian response from a world that has become hostage to erroneous economic and monetary groupthink in its major institutions.

Kwarteng has jogged the global statist establishment out of its complacent drift into totalitarianism. His is a wake-up call to markets everywhere, a catalyst for the unwinding of accumulated market distortions. Mounting criticism from all quarters is shooting the messenger, but the message has been delivered.

In one important respect, the criticism is valid. Kwarteng must address the budget deficit urgently by taking steps to reduce the size of the state as a proportion of the total economy. Only then can inflation be conquered and the pound stabilise. In another respect, the new policy is sensible: By plotting its own free market/Hayekian course, Britain can emerge out of the crisis sooner than other nations stuck in the current democratic-socialist paradigm.

If we assume that Kwarteng does address the size of the state and eliminate budget deficits as early as practically possible, he will have a practical plan for a post-crisis Britain. Economic recovery can than happen sooner rather than later, a major consideration given that the next general election is in a little over two years.

It is too late to avoid the gathering global crisis, the financial consequences of which are bound to devolve in large measure on London’s financial centre. Indeed, Kwarteng’s wake-up call may be the trigger for a financial avalanche. But what he is unlikely to realise is that the gathering crisis is so severe that even the continued existence of fiat currencies will be threatened, with the euro and sterling being particularly vulnerable.

In this article I also comment on the Bank of England’s failure as an institution, whose future role in monetary affairs should be strictly curtailed. And I advocate the abandonment of all trade tariffs, with the possible exception of agriculture for political reasons. These are fundamental reforms which must accompany free market policies.

We must proceed with our commentary ignoring the existential threat to currencies if it is to be relevant to the government’s economic policies and their global impact. …

Submitted by admin on Thu, 2022-09-29 11:02 Section: Daily Dispatches

By Julie Zhu Reuters Thursday, September 29, 2022

HONG KONG — China’s central bank has asked major state-owned banks to be prepared to sell dollars for the local unit in offshore markets as it steps up efforts to stem the yuan’s descent, four sources with knowledge of the matter said.

State banks were told to ask their offshore branches, including those based in Hong Kong, New York and London, to review their holdings of the offshore yuan and ensure U.S. dollar reserves are ready to be deployed, three of the sources, who declined to be identified, told Reuters.

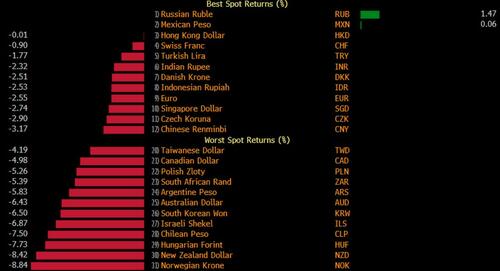

The simultaneous selling of dollars and buying of yuan could put a floor under the Chinese currency, which has lost more than 11% to the dollar so far this year and looks set for its biggest annual loss since 1994, when China unified its official and market rates.

The UK’s crisis of confidence was years in the making

Submitted by admin on Thu, 2022-09-29 11:24Section: Daily Dispatches

By Philip Aldrick, Libby Cherry, and David Goodman Bloomberg News via Yahoo News, Sunnyvale, California Thursday, September 29, 2022

Britain is in a self-inflicted financial crisis, years in the making, that threatens to accelerate the economy’s dive into recession — and the country’s new prime minister is coming under intense pressure to blink.

In the week since the government unveiled the biggest tax cuts since 1972 with scant detail of how they will be financed, the pound has crashed to its lowest-ever level against the dollar, the cost of insuring British government debt against the risk of default has soared to the highest since 2016, and the Bank of England has been forced to intervene amid concerns about the nation’s pension funds.

What happens next will determine just how deep the looming recession proves. Central to that question is whether Liz Truss’s three-week old administration can restore its credibility with investors.

Friday’s mini-budget has become a flashpoint for not just investors’ short-term concerns about unfunded tax cuts at a time when inflation is running close to a four-decade high, or the Bank of England’s failure to contain price growth. It has given sharp focus to their long-held fears about Britain, its current-account deficit, its fractious relationship with its closest trading partner and, above all, a mistrust of what successive politicians promise. …

I have been pointing out to you for the past 6 months, large hedge funds going short while the bankers are going long

Butler explains it beautifully

(Ted Butler)

Ted Butler: The monetary metals bear trap: Is it finally set?

Submitted by admin on Thu, 2022-09-29 20:05Section: Daily Dispatches

By Ted Butler SilverSeek.com Thursday, September 29, 2022

What has been occurring in the gold and silver markets is nothing short of extraordinary. In the face of all objective and measurable conditions in the physical markets pointing to higher prices, instead prices have collapsed over the past six months by amounts comparable to the sharpest selloffs in history. From the price top of March 8, gold has fallen as much as $450 (22%), while silver has fallen by as much as $10 (36%) in recent dealings

Yet all visible signs point to extreme physical tightness, the likes of which I have never seen, in everything from the most persistent retail premiums in silver in history, to surging wholesale physical demand in India and China — all with no notable increase in actual supply.

To an extent never witnessed before, the past six months have featured the sharpest divergence between surging physical demand and a steep and highly counterintuitive historical price collapse. To any believer in the free market law of supply and demand, it has been the strangest (and most trying) time ever — or at least the strangest time in my near 50-year experience. …

What has been occurring in the gold and silver markets is nothing short of extraordinary. In the face of all objective and measurable conditions in the physical markets pointing to higher prices, instead prices have collapsed over the past six months by amounts comparable to the sharpest selloffs in history. From the price top of March 8, gold has fallen as much as $450 (22%), while silver has fallen by as much as $10 (36%) in recent dealings.

Yet, all visible signs point to extreme physical tightness, the likes of which I have never seen, in everything from the most persistent retail premiums in silver in history, to surging wholesale physical demand in India and China – all with no notable increase in actual supply. To an extent never witnessed before, the past six months have featured the sharpest divergence between surging physical demand and a steep and highly-counterintuitive historical price collapse. To any believer in the free market law of supply and demand, it has been the strangest (and most trying) time ever – or at least the strangest time in my near 50-year experience.

Of course, surging physical silver and gold demand and collapsing prices can’t occur for no reason and finding the reason is the responsibility of anyone interested in gold and silver. In fact, there is only one possible reason to explain the conundrum of surging demand and physical tightness and sharply lower prices and it is the same reason I have advanced for more than 35 years – an ongoing price manipulation on the COMEX. While I am gratified that more observers than ever seem to have come to grasp the basics of the long-term COMEX price manipulation; somewhat ironically, we appear to have reached (or are extremely close) the termination point of the long-running price manipulation, regardless of public awareness.

The key feature of the four decades-old COMEX price manipulation has been the ability of a tight-knit group of large traders, classified as commercials (mostly banks), to sell future contracts short in unlimited quantities to cap and contain silver and gold prices. This resulted in COMEX silver having the largest concentrated short position of any commodity for 40 years when compared to actual world production. A key component of the manipulative unlimited short selling was the refusal of the commercial short sellers to ever buy back and cover short positions on rising prices – only when prices fell. This was the key to absolute price control.

Limited (by choice) to only buying back short positions on lower prices (otherwise prices would explode higher), the only way for the COMEX commercial shorts to buyback and cover the maximum number of short contracts was to create the price environment most suited to getting other large COMEX traders to sell short and replace the commercial shorts. Fortunately for the commercial traders, there existed such a group of traders, classified as the managed money traders, willing to sell a large (but not unlimited) number of short contracts under the right technical conditions. The “right” technical conditions were, essentially, steadily falling prices and this was right up the commercials’ alley, since they had sufficient means of dictating prices (think spoofing).

Therefore, maximum commercial short-covering could only be met with maximum managed money short selling under a price selloff that was epic in both time and scope. The selloff had to be both pronounced, but also consistent and of such duration so as to entice the managed money traders to fully-load up on the short side. A selloff that could be termed the “mother of all selloffs” (as I recently termed it). It appears to me that the six-month selloff in COMEX gold and silver from the top on March 8 (the day of the LME nickel default), when gold hit its all-time high of $2080 and silver hit $27.50, fully-qualifies as the epic selloff required to induce maximum managed money shorting and maximum commercial short covering. Maybe there’s a bit more to go, but not much, in my opinion.

Since March 8, the total commercial net short position in gold has declined by more than 230,000 contracts (23 million oz) and by as much as 70,000 net contracts (350 million oz) in COMEX silver, among the largest reductions in history. Even more compelling is that the commercial concentrated short positions have declined, proportionately, even more, to the lowest levels in history. If you are looking for the reason explaining how gold and silver prices could decline as much as they have over the past six months, in the face of perhaps the strongest physical demand ever seen, then look no further. The COMEX commercials set out to induce the maximum amount of managed money selling (so that the commercial could buy) and succeeded masterfully. Now what?

Now we are at or extremely close to the point of maximum bullishness, where prices are quite capable of exploding higher in a manner none of us have ever really witnessed. Because there has been so much managed money shorting in gold and silver and because prices are so far below the key moving averages (particularly in gold), these traders know full-well that they will need to buy back the bulk of their short positions long before all the key moving averages are penetrated to the upside – otherwise the money risk is just too great, considering the size of the managed money short positions, to wait until all the key moving averages (the 50, 100 and 200-day moving averages) are upwardly penetrated. We’ve seen this in silver recently, as $2 rallies resulted in significant short covering before prices were then rigged lower and the manged money shorts were enticed back in.

I suppose that it’s always possible for even more managed money shorting on even lower prices, or that the collusive commercials may toy a bit more with the managed money shorts (as they have in silver), letting a number out on a quick pop up in price, only to rig prices lower to bring those who bought back, right back onto the short side, but these short-term price wiggles are beyond prediction (at least for me). The important point is to not get hung up on the daily price gyrations at this point and consider the whole picture – which is bullish beyond words.

Thus, the stage has been set for a bear trap of epic proportions in gold and silver. For those unfamiliar with the term, here’s a quick description of the set up –

It goes without saying that the key to the next big move to the upside is entirely dependent on whether the former big commercial shorts in COMEX gold and silver add aggressively to new short positions as the rally unfolds. That goes hand-in-hand with the manipulation premise I have alleged for 35 years. While no one knows for sure what these big former commercial shorts will do, I’ve always held it generally doesn’t matter much in terms of prediction, as there is generally ample warning of what they are doing in the ongoing COT reports. But in addition to that, there is now the case that the physical market is so tight as to be a discouragement against renewed big commercial short selling. Plus, there’s another new factor arguing against aggressive short selling by the big commercial traders that I’m not sure if I’ve covered previously.

That additional factor is the cumulative weight on the big banks brought about by years of settlements and fines and convictions for manipulating gold and silver prices, largely as result of spoofing illegalities. Yesterday’s announcement of yet another major regulatory settlement involving unrecorded conversations between bank traders. Left out of the announcement was that the unrecorded conversations were designed to cheat other market participants and further proof of collusion – otherwise why weren’t they recorded?

It’s hard to come up with the name of single bank that hasn’t settled or been fined for such violations over the past several years, often accompanied by deferred criminal prosecution agreements – violation of which is even more serious. The fines and agreements start with the master precious metals criminal, JPMorgan, and extend from there. Of course, JPM is sitting pretty, having accumulated at least a billion oz of physical silver and upwards of 30 million oz of physical gold over a decade of stealth acquisition.

There’s no doubt (in my mind) that the US regulators (the CFTC and Justice Dept) stopped way short of charging JPMorgan and the other banks with the type of precious metals manipulation that would have put them out of business and instead stuck to spoofing and now improper communication charges, which allowed the banks to stay in business. Then again, it’s not possible that the too-lenient regulatory findings left the banks in a stronger position to continue the decades-old COMEX manipulation. Looking at the stock prices for some of the foreign banks which settled and paid fines for precious metals manipulation on the COMEX, they are basket cases.

My point is that the previous fines, settlements and agreements have made it even more unlikely for the crooked banks to operate as they have in the past and increase the likelihood that the big former commercial shorts will stand aside and not add to shorts on the next rally. Of course, time will tell, but I doubt more than ever that the former big commercial shorts will have the gall to re-short aggressively on the coming rise in prices and the commercial bear trap of the managed money shorts looks complete or nearly so.

Ted Butler

September 29, 2022

END

A good commentary from Frank Holmes showing that gold always is a great store of value

(Frank Holmes/GATA)

Frank Holmes: Gold has been a great store of value amid the ‘everything selloff’

Submitted by admin on Thu, 2022-09-29 21:55Section: Daily Dispatches

By Frank Holmes U.S. Global Investors, San Antonio, Texas Wednesday, September 28, 2022

“Gold is no longer a safe haven.”

“Gold isn’t an effective hedge against inflation.”

“Gold is dead.”

You may have heard and read these comments, and others like it, numerous times over the course of the recent “everything selloff.” This is staggeringly shortsighted to me. Gold is down only around 9.5% for the year despite surging bond yields and despite the U.S. dollar being at its strongest level ever relative to other major currencies.

Given these incredible headwinds, you would expect gold to have lost far more of its value than it has. But compared to other assets, from stocks to bonds to digital currencies, the yellow metal has been remarkably resilient.

And that’s gold priced in the U.S. dollar. When we price it in other currencies, gold has done even better, since many currencies have declined significantly in value relative to the greenback. This week the British pound fell to an all-time low against the dollar, as did the Chinese renminbi.

Of the various gold prices shown in the chart below, only two — those priced in the dollar and Brazilian real — were negative for the year as of September 27. The others, including gold priced in the Canadian dollar, were positive. …

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 7.1165

OFFSHORE YUAN: 7.1260

SHANGHAI CLOSED: DOWN 16.82 PTS OR 0.55%

HANG SENG CLOSED UP56.96 PTS OR 0.33%

2. Nikkei closed DOWN 484.84 PTS OR 1.84%

3. Europe stocks SO FAR: ALL GREEN

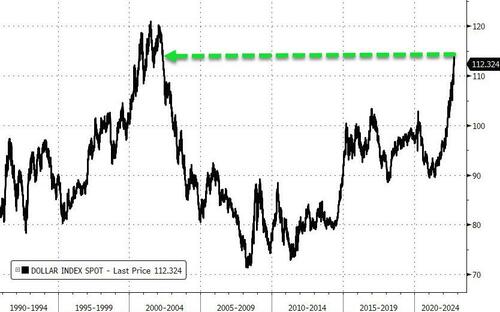

USA dollar INDEX UP TO 112.51/Euro RISES TO 0.9754

3b Japan 10 YR bond yield: FALLS TO. +.238/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 144.55/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP -// OFF- SHORE: UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.071%***/Italian 10 Yr bond yield FALLS to 4.51%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.25%…** DANGEROUS

3i Greek 10 year bond yield FALLS TO 4.81//

3j Gold at $1663.50//silver at: 18.96 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 2 AND 34/100 roubles/dollar; ROUBLE AT 54.86//

3m oil into the 81 dollar handle for WTI and 86 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 144.55DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this .9807–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9567well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.696 DOWN 5 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.635 DOWN 6 BASIS PTS//(USA 30 YR INVERTED TO THE USA 10)

USA DOLLAR VS TURKISH LIRA: 18,55…GETTTING DANGEROUS

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Bounce In Futures Fizzles As Dollar Surge Returns

FRIDAY, SEP 30, 2022 – 08:10 AM

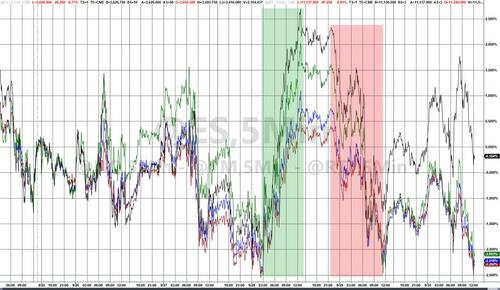

If yesterday markets made little sense, when the dollar and yields slumped yet stocks and other risk assets tumbled alongside them in a puzzling reversal of traditional risk relationships (a move which was likely precipitated by the plunge in AAPL and KMX), today things are a bit more logical with the dollar initially extending its slide helping futures rise to session highs just below 3,700, before the dollar surged just after 5am as sterling tumbled after Bloomberg reported that Prime Minister Liz Truss’s government signaled it was sticking with its plan for tax cuts after a meeting with the UK’s fiscal watchdog, dashing market expectations that a policy U-turn might be imminent which has pushed cable briefly above 1.12 overnight, wiping out a week’s worth of losses. As a result, after rising as much as 0.8%, S&P futures were flat, up just 0.1%, the same as Nasdaq futures. Government bonds rallied across Europe and the US, as the dollar strengthened after reversing its earlier loss.

In premarket trading, Nike shares fall 10% after the sportswear giant cut its margin outlook for the year while reporting surging inventory, fueling worries over consumers’ ability to spend as inflation takes a toll. Micron shares rose 3% in premarket trading, after analysts said the ongoing inventory correction was only a short-term hurdle and that the bottom is near, a potential relief for semiconductor stocks that have taken a beating this year. Amylyx Pharmaceuticals’s (AMLX US) shares soared as much as 13% in US premarket trading after winning FDA approval for its Relyvrio drug, for the treatment of amyotrophic lateral sclerosis (ALS) in adults. Analysts said they expected the drug to see a strong launch given demand from patients. Xos jumped 6.3% in extended trading after delivering 13 battery-electric vehicles to FedEx.

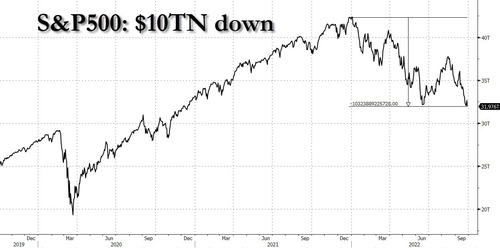

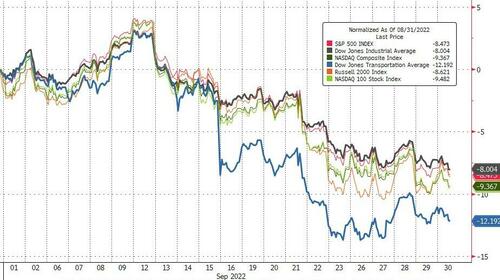

Thursday’s bruising session took the S&P 500 down 2% to the lowest in almost two years and the Nasdaq 100 tumbling almost 4%. The S&P 500 Index has dropped on seven of the past 8 days, and is headed for its third straight quarter of losses for the first time since 2008-2009 and the Nasdaq 100 Stock Index for the first time in 20 years. Fears of global recession are growing by the day as the threat of higher rates saps growth and as the Fed confirms with every speech that not even a recession will stop it. The case of the UK shows how faultlines between government and central bank policy on tackling inflation can erupt into a crisis. Hopes evaporated that the British government would succumb to pressure to back down from tax cuts that brought the pound to the edge of dollar parity.

“Today, everything is just oversold so you are seeing a rebound,” said Esty Dwek, chief investment officer at Flowbank SA. “We are closer to bottoms and sentiment is so negative the downside is becoming more limited.”

Elsewhere, Global equity funds garnered inflows of $7.6 billion in the week to Sept. 28, according to data compiled by EPFR Global. Bonds had $13.7 billion of outflows in the week, while $8.9 billion flowed into US stocks, the data showed.

In Europe, the Stoxx 50 rose 0.9%. Real estate, energy and retailers are the strongest-performing sectors. Here are some of the biggest European movers today:

Krones shares rose as much as 2.7% to their highest intra-day level since Feb. 2022, after HSBC increased the German machinery and equipment company’s price target to EU102

Clariant shares rally by the most intraday since mid-May after Credit Suisse raises to outperform, partly as it expects Clariant’s new management team to boost performance

ABN Amro jumped as much as 6.3% after Goldman Sachs raised the stock to buy from neutral, citing its gearing toward higher interest rates, increasing estimates on net interest income

Zealand Pharma rise as much as 35%, the most on record, after the company announced positive data from its phase 3 trial of glepaglutide to treat patients with short bowel syndrome

Sinch shares rise as much as 24% after SoftBank sold its entire stake in Sinch AB following a share price collapse of more than 90% in the Swedish cloud-based platform provider

Adidas and Puma drop as their US peer Nike slumped in late trading Thursday after it said inventory buildup forced it to push through margin-busting discounts

Hurricane Energy shares drop as much as 5.6% after 1H earnings; Canaccord Genuity notes the results did not surprise, and flags lack of regulatory reassurance on gas-management approvals

Fingerprint Cards shares drop as much as 17% after saying it is raising fresh capital in order to strengthen the balance sheet and to address a forecasted covenant breach

Earlier in the session, Asian stocks fell again, putting the regional benchmark on course for its worst monthly performance since 2008, as a selloff spurred by concerns over higher interest rates and a global recession deepened. The MSCI Asia Pacific Index slid 0.5% after earlier falling as much as 1% on Friday. Still down over 12% this month, the gauge has trailed global peers and is set to cap a seventh straight week of declines. That matches its losing streak from September 2015, which was the longest since 2011. Equities in Japan, which has the highest weight in the Asia index, were among the biggest losers on Friday, with the Topix falling 1.8%. Consumer discretionary and industrials were the worst sectors, while Chinese tech shares listed in Hong Kong also fell. READ: China Shares Plunge to Lowest Valuation on Record in Hong Kong Global funds have pulled almost $10 billion from Asian emerging-market stocks excluding China this month, as the dollar and Treasury yields climbed after Federal Reserve officials ramped up their rate-hike rhetoric. Taiwan’s tech-heavy market has suffered the bulk of the outflow from Asia. Its regulators tightened short selling rules as shares extended their slide.

“I think emerging markets as a whole are still going to have a pretty difficult six months until the Fed rate peaks,” Louis Lau, a fund manager at Brandes Investment Partners, said in an interview with Bloomberg TV. How much damage is a strong dollar causing? That’s the theme of this week’s MLIV Pulse survey. It’s brief and we don’t collect your name or any contact information. Please click here to share your views. The turmoil in the UK has been another source of market volatility for Asia investors, who continue to grapple with the fallout from strict lockdowns in China, the region’s biggest economy. “There’s been some correlation (between risk assets and sterling) recently,” said Takeo Kamai, head of execution services at CLSA. Overall, “the theme hasn’t changed. The scenario that the Fed will cut rates next year is breaking down. I think we could see further downside in stock prices towards November,” he said. Stocks in India gained after the central bank raised the benchmark rate by an expected 50 basis points. The MSCI Asia Pacific Index is down 4% this week and on course for its lowest close since April 2020

Japanese equities extended declines on Friday as a global market rout deepened, capping its worst month since the onset of the pandemic in 2020. The Topix Index fell 1.8% to 1,835.94 as of market close Tokyo time, taking declines in September to 6.5%. The Nikkei declined 1.8% to 25,937.21. Toyota Motor Corp. contributed the most to the Topix Index decline, decreasing 4.2%. Out of 2,169 stocks in the index, 299 rose and 1,823 fell, while 47 were unchanged. Federal Reserve officials reiterated Thursday that they will keep raising interest rates to rein in high inflation. “There are concerns that the economy will slow from further rate hikes while inflation doesn’t stop,” said Kenji Ueno, a portfolio manager at Sompo Asset Management.

In Australia, the S&P/ASX 200 index fell 1.2% to close at 6,474.20, dragged by banks and industrials, after another plunge on Wall Street as the prospect of higher interest rates and turmoil in Europe stoked fears of global recession. The benchmark notched its third-straight week of losses. In New Zealand, the S&P/NZX 50 index fell 1.2% to 11,065.71

Stocks in India outperformed Asian peers after the Reserve Bank of India raised borrowing costs and exuded confidence to tackle inflation without any major impact to its growth projections. The S&P BSE Sensex added 1.8% to 57,426.92, while the NSE Nifty 50 Index rose by 1.6% as the indexes posted their biggest single-day jump since Aug. 30. Despite the rally, the key gauges fell more than 1% each for the week and over 3% for the month, their biggest decline since June. India’s central bank raised its repurchase rate by 50 basis points to 5.90%, matching the expectations of most economists. The RBI trimmed the economic growth outlook for the financial year ending March to 7% while retaining it 6.7% forecast for inflation. The increase in the benchmark interest rate “mainly supports stocks of financial companies, which have been seeing strong credit growth,” said Prashanth Tapse, an analyst at Mehta Securities.

In FX, the Bloomberg Dollar Spot Index rebounded after sliding initially, as cable tumbled when it emerged that Liz Truss is not backtracking on its massive fiscal easing. Iniitlally, the pound advanced a fourth day, to briefly trade above $1.12, fully reversing the moves since last Friday, however it then tumbled, wiping out all gains after Prime Minister Liz Truss’s government signaled it’s sticking with its plan for tax cuts after a meeting with the UK’s fiscal watchdog, dashing market expectations that a policy U-turn might be imminent. Notable data: U.K. 2Q final GDP rises 0.2% q/q versus preliminary -0.1%. The Aussie and kiwi crept higher, but are still set for their biggest monthly declines since April as rising Fed interest rates and fears of a global economic slowdown sap demand for risk assets

In rates, Treasuries advanced, 10-year yield dropping 8bps while bunds 10-year yield drops 6bps to 2.11%. Treasury 10-year yields around 3.685%, richer by 10bp on the day — largest moves seen in UK front-end where 2-year yields are richer by 25bp on the day as BOE tightening premium fades out of interest-rate swaps. Short-end UK bonds surged amid political pressure on the government to water down some of its budget proposals, while the pound regained its budget-shock losses. US session focus is on PCE data and host of Federal Reserve speakers while month end may add some support into long end of the curve. Long end of the Treasuries curve may find additional month-end related buying support over the session; Bloomberg index projects 0.07yr Treasury extension for October. Gilts rallied, with short-end bonds leading gains as traders trimmed BOE tightening bets amid political pressure on the government to water down some of its budget proposals. Meanwhile in Japan, JGBs gained after the BOJ boosted purchases for maturities covering the benchmark 10-year zone. The Bank of Japan will buy more bonds with maturities of at least five years in the October-December period, according to a statement from the central bank

In commodities, WTI trades within Thursday’s range, adding 1.3% to near $82.26. Spot gold rises roughly $10 to trade near $1,671/oz.

Bitcoin is essentially unchanged and in very tight ranges of circa. USD 400 and as such well within the week’s existing parameters

Looking to the day ahead now, and data releases include the flash Euro Area CPI release for September, as well as the Euro Area unemployment rate for August and German unemployment for September. In the US, we’ll also get August data on personal income and personal spending, the MNI Chicago PMI for September, and the University of Michigan’s final consumer sentiment index for September. Finally, central bank speakers include Fed Vice Chair Brainard, the Fed’s Barkin, Bowman and Williams, as well as the ECB’s Schnabel, Elderson and Visco.

Market Snapshot

S&P 500 futures up 0.9% to 3,686.00

STOXX Europe 600 up 1.3% to 387.83

MXAP down 0.5% to 139.25

MXAPJ little changed at 453.72

Nikkei down 1.8% to 25,937.21

Topix down 1.8% to 1,835.94

Hang Seng Index up 0.3% to 17,222.83

Shanghai Composite down 0.6% to 3,024.39

Sensex up 2.0% to 57,539.66

Australia S&P/ASX 200 down 1.2% to 6,474.20

Kospi down 0.7% to 2,155.49

Brent Futures up 1.2% to $89.55/bbl

Gold spot up 0.7% to $1,671.56

U.S. Dollar Index down 0.52% to 111.67

German 10Y yield little changed at 2.10%

Euro up 0.3% to $0.9840

Top Overnight News from Bloomberg

Prime Minister Liz Truss is under pressure to cut spending on the same scale as George Osborne’s infamous austerity drive of 2010 in order to stabilize the UK public finances and win back the confidence of investors

Prime Minister Liz Truss and Chancellor of the Exchequer Kwasi Kwarteng are holding talks Friday with the UK government’s fiscal watchdog, amid intense criticism over their unfunded tax cuts that roiled markets

A dash for cash among sterling investors after market turmoil sparked by pension fund margin calls is coming at a bad time, according to an M&G Investments executive

The ECB shouldn’t let concerns about its profitability obstruct decision-making over monetary policy, according to Governing Council member Gediminas Simkus

The SNB trimmed its foreign-exchange portfolio in the second quarter as the franc gyrated against the euro before rising above parity for the first time since 2015. The central bank sold 5 million francs ($5.1 million) worth of foreign currencies in the three months through June

Norway’s central bank will increase its purchases of foreign currency to 4.3 billion kroner ($400 million) a day in October from 3.5 billion in September as it deposits energy revenues into the $1.1 trillion sovereign wealth fund.

Japan’s factory output expanded by 2.7% in August from July, according to the economy ministry Friday, beating analysts’ 0.2% forecast. The output of semiconductor and flat-panel making equipment hit its highest level in data going back to 2003, as the effect of lockdowns in China abated

Japanese Prime Minister Fumio Kishida instructed the government Friday to come up with an economic stimulus package by the end of October to help mitigate the impact of inflation, as economists warned against over-sized spending

China’s factory activity continued to struggle in September, while services slowed, as the country’s economic recovery was challenged by lockdowns in major cities and an ongoing property market downturn. The official manufacturing purchasing managers index rose to 50.1 from 49.4 in August

An organization formed by China’s biggest foreign- exchange traders asked banks to trade the currency at levels closer to the central bank’s fixing at the market open, according to people familiar with the matter

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mostly lower after the negative performance across global peers amid inflationary headwinds and with risk appetite subdued heading quarter-end, while the region also digested mixed Chinese PMI data. ASX 200 declined amid weakness across most sectors and with tech the notable underperformer after the recent upside in yields and with Meta the latest major industry player to announce a hiring freeze. Nikkei 225 was pressured and fell below the 26,000 level with better-than-expected Industrial Production and Retail Sales data releases overshadowed by the broad risk aversion. Hang Seng and Shanghai Comp were indecisive after the PBoC conducted its largest weekly cash injection in more than 32 months ahead of the week-long closure in the mainland, while participants also digested mixed PMI data in which Official Manufacturing PMI topped forecasts with a surprise return to expansion, but Non-Manufacturing and Composite PMIs slowed and Caixin Manufacturing PMI printed at a wider contraction. NIFTY eventually notched mild gains in the aftermath of the RBI rate decision in which it hiked the Repurchase Rate by 50bps to 5.90% as expected via 5-1 split and with the central bank refraining from any major hawkish surprises.

Top Asian News

Japan’s Chief Cabinet Secretary Matsuno said they want to compile an extra budget swiftly after the economic package in late October, while they will consider further support for hard-hit consumers and businesses in view of higher energy and food prices, as well as consider steps to promote wage hikes, according to Reuters.

Chinese Finance Ministry is to offer a tax refund for people who sell their homes and repurchases new ones by the end of 2023; additionally, China has told banks to provide USD 85bln in property funding by the end of the year, according to Bloomberg.

Chinese NBS Manufacturing PMI (Sep) 50.1 vs. Exp. 49.6 (Prev. 49.4); Non-Manufacturing PMI (Sep) 50.6 vs Exp. 52.4 (Prev. 52.6)

Chinese Composite PMI (Sep) 50.9 (Prev. 51.7)

Chinese Caixin Manufacturing PMI Final (Sep) 48.1 vs. Exp. 49.5 (Prev. 49.5)

Japanese Industrial Production MM SA (Aug P) 2.7% vs. Exp. 0.2% (Prev. 0.8%); Retail Sales YY (Aug) 4.1% vs. Exp. 2.8% (Prev. 2.4%)

European equities are attempting to claw back some of yesterday’s downside on quarter and month end. Sectors are firmer across the board with Real Estate outperforming peers in what has been a tough week for the UK property market. Stateside, futures are also attempting to recover from yesterday’s losses which saw a tough session for the tech sector after Apple shed the best part of 5%.

Top European News

UK OBR Chair Hughes says a statement will be released today after the meeting with UK PM Truss and Chancellor Kwarteng. On this, the UK Treasury has not sought to accelerate watchdog’s economic forecast, according to Bloomberg. Reminder, UK PM Truss to conduct emergency talks with the OBR on Friday after failing to calm markets, according to the Guardian.

UK cross-party MPs in the Treasury Select Committee called for Chancellor Kwarteng to release a full economic forecast from the OBR by end of October, according to Sky News.

UK PM Truss has confirmed she will attend next week’s European Political Community summit, via BBC.

Reports that technical level discussions between the UK and EU could resume as soon as next week, via BBC’s Parker; writing, that there has been a ‘warmer’ tone in recent weeks, some believe pressure from the US on the UK has had influence.

German VDMA, survey of members: majority expect nominal sales growth in 2022 and 2023.

FX

GBP’s revival has continued ahead of a meeting between PM Truss and the OBR, with a statement expected, a move that has taken Cable above 1.12 but shy of mini-Budget levels.

USD is firmer overall but continues to retreat from YTD peaks, though the DXY is seemingly drawn to the 112.00 area.

Yuan derived further, fleeting, support from reports the FX body has asked banks to trade closer to the onshore fixing.

Elsewhere, FX peers are under modest pressure but more contained vs USD; EUR unfased by a record EZ flash CPI print of 10.0%.

Fixed Income

Benchmarks bid but modestly off best levels with Bunds leading the charge, but well within recent ranges, amid potential month/quarter-end influence.

Gilts lifted, but the 10yr yield remains above 4.0% ahead of the OBR statement.

Stateside, USTs are equally buoyed ahead of a packed PM agenda include PCE Price Index and Fed speak.

Commodities

The broader commodity market is benefitting from a pullback in the USD coupled with a broader risk appetite.

Metals are buoyed by the recent pullback in the Dollar with spot gold edging above its 10 DMA (USD 1,656.72/oz) and towards the USD 1,680/oz mark which coincides with the yellow metal’s 21DMA (USD 1,680.56/oz) and 200WMA (USD 1,680.20/oz).

Base metals are also firmer across the board with 3M LME copper back above the USD 7,500/t mark, whilst nickel and aluminium outperform on the exchange.

Central Banks

China loosened FX restrictions in response to the Fed rate hike and the yuan’s fall over the past week, according to people familiar with the matter cited by FT.

China’s FX body is reportedly asking banks to trade the Yuan closer to the PBoC fixing, according to Bloomberg.

PBoC injected CNY 128bln via 7-day reverse repos with the rate kept at 2.00% and injected CNY 58bln via 14-day reverse repos with the rate kept at 2.15% for a CNY 184bln net daily injection and a net CNY 868bln weekly injection.

RBI hiked Repurchase Rate by 50bps to 5.90%, as expected, via 5-1 vote and the Standing Deposit Facility was adjusted to 5.65%. RBI Governor Das said MPC is to remain focused on the withdrawal of accommodation and that the persistence of high inflation necessitates further calibrated withdrawal of monetary accommodation. However, Das noted that the Indian economy continues to be resilient with economic activity stable and overall monetary and liquidity conditions still remain accommodative, while Real GDP growth forecast for 2022/23 was revised lower to 7.0% from 7.2% and 2022/23 CPI was seen at 6.7%.

RBI is reportedly encouraging state-run refiners to reduce USD buying in the spot market; asking to lean on USD 9bln credit line instead, according to Reuters sources.

BoE was reportedly warned about a looming catastrophe in the pensions sector within the next 5 years before it was forced to intervene to prevent a market collapse, according to The Telegraph.

Fed’s Daly (2024 voter) said a downshift in economic activity and labour is needed to bring down inflation and additional rate increases are necessary and appropriate. Daly also stated that a myriad of risks narrows the path to a smooth landing but does not close it, while she added they have gotten rates to neutral and expect to raise rates further in coming meetings and early next year.

Norges Bank will purchase FX equivalent to NOK 4.3bln/day in October (3.5bln in September); reflecting an increase in projected NOK revenues from petroleum activity.

Geopolitics

Russian President Putin signed decrees recognising occupied Ukrainian regions of Kherson and Zaporizhzhia as independent territories which is an intermediate step before the regions are formally incorporated into Russia, according to Reuters.

** Russia’s Kremlin says strikes against the new territories incorporated into Russia will be considered an act of aggression against Russia**; says Ukraine has shown no willingness to negotiate, via Reuters.

Russia’s Spy Chief says they have material which show a Western role in Nord Stream incidents, via Ifx.

Armenia’s Foreign Ministry says their Ministers and Azerbaijani counterparts will meet in Geneva on October 2nd, via AJA Breaking.

US Event Calendar

08:30: Aug. Personal Spending, est. 0.2%, prior 0.1%

Aug. Real Personal Spending, est. 0.1%, prior 0.2%

Aug. Personal Income, est. 0.3%, prior 0.2%

Aug. PCE Deflator MoM, est. 0.1%, prior -0.1%

Aug. PCE Core Deflator MoM, est. 0.5%, prior 0.1%

Aug. PCE Core Deflator YoY, est. 4.7%, prior 4.6%

Aug. PCE Deflator YoY, est. 6.0%, prior 6.3%

09:45: Sept. MNI Chicago PMI, est. 51.8, prior 52.2

10:00: Sept. U. of Mich. Current Conditions, est. 58.9, prior 58.9

U. of Mich. Sentiment, est. 59.5, prior 59.5

U. of Mich. Expectations, est. 59.9, prior 59.9

U. of Mich. 1 Yr Inflation, est. 4.6%, prior 4.6%; 5-10 Yr Inflation, est. 2.8%, prior 2.8%

Central Bank Speakers

08:30: Fed’s Barkin Speaks at Chamber of Commerce Event

09:00: Fed’s Brainard Speaks at Fed Conference on Financial Stability

11:00: Fed’s Bowman Discusses Large Bank Supervision

12:30: Fed’s Barkin Discusses the Drivers of Inflation

16:15: Williams Speaks at Fed Conference on Financial Stability

DB’s Jim Reid concludes the overnight wrap