by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSE: UP $29.30 to $1693.40

SILVER PRICE CLOSE: UP $1.46 to $20.53

Access prices: closes

Gold ACCESS CLOSE 1699.20

Silver ACCESS CLOSE: 20.70

New: early this morning//very ominous:

On Monday, October 3, 2022 at 12:15 p.m., a meeting of the Board of Governors of the Federal Reserve System was held under expedited procedures, as set forth in section 261b.7 of the Board’s Rules Regarding Public Observation of Meetings, at the Board’s offices at 20th and C Streets, N.W., Washington, D.C. and by audio/video conference call, to consider the following matters of official Board business.

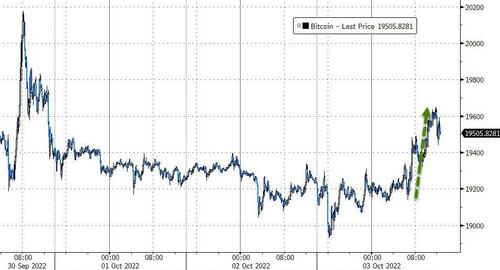

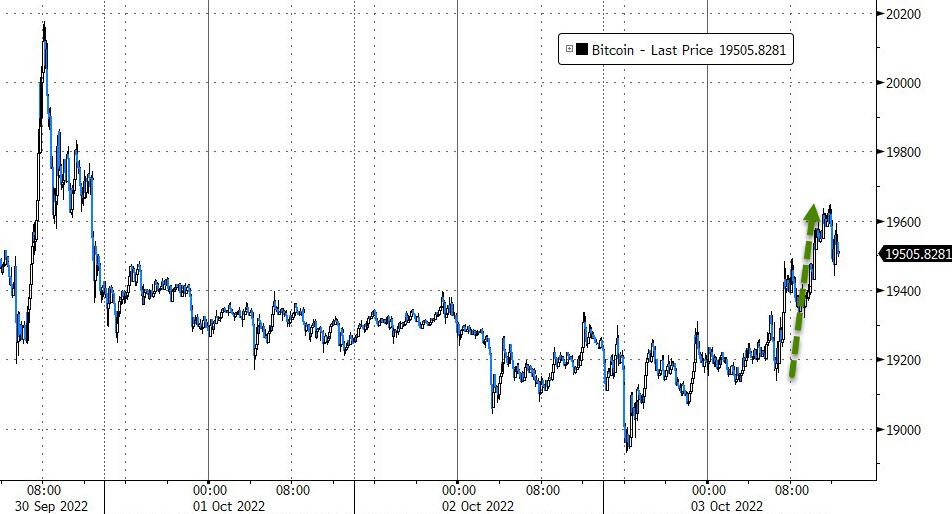

Bitcoin morning price: $19,235 DOWN 496

Bitcoin: afternoon price: $19,491 DOWN 200

Platinum price closing UP 35.30 AT $902.60

Palladium price; closing UP $58.05 at $2240.40

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: OCTOBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,662.400000000 USD

INTENT DATE: 09/30/2022 DELIVERY DATE: 10/04/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 21

104 C MIZUHO 13

118 C MACQUARIE FUT 27

323 H HSBC 115

365 H ED&F MAN CAPITA 2

624 C BOFA SECURITIES 34

624 H BOFA SECURITIES 34

657 C MORGAN STANLEY 96

661 C JP MORGAN 266

685 C RJ OBRIEN 5

686 C STONEX FINANCIA 6

686 H STONEX FINANCIA 14

690 C ABN AMRO 101

700 C UBS 572

732 C RBC CAP MARKETS 12

800 C MAREX SPEC 97 39

845 C GOLDMAN SACHS C 1

878 C PHILLIP CAPITAL 4

880 C CITIGROUP 151

905 C ADM 13 3

TOTAL: 813 813

MONTH TO DATE: 20,641

JPMORGAN STOPPED 266/813

GOLD: NUMBER OF NOTICES FILED FOR OCT CONTRACT: 813

20,641 NOTICES FOR 2,064,100 OZ //64.202 TONNES

total notices so far: 20,641 contracts for 2,064,100 oz (64.202 tonnes)

SILVER NOTICES: 3 NOTICES FILED FOR 15,000 OZ/

total number of notices filed so far this month 55 : for 275,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $29.30

VERY STRANGE!!

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: //// A WITHDRAWAL OF 1.45

TONNES FROM THE GLD/

INVENTORY RESTS AT 939.70 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $1.46

AT THE SLV// ://BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF OF 1.013 MILLION OZ INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 480.917 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 2401 CONTRACTS TO 127,382 (ALL TIME LOW) AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE HUGE LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.31 GAIN IN SILVER PRICING AT THE COMEX ON FRIDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.31) AND WERE UNSUCCESSFUL IN KNOCKING OFF SOME SPEC SILVER LONGS AS WE HAD A HUGE LOSS OF 2228 CONTRACTS ON OUR TWO EXCHANGES. WE DID HAVE HUGE SPEC SHORT COVERINGS WITH THE BANKERS CONTINUALLY ON THE BUY SIDE.

WE MUST HAVE HAD:

I) CONTINUAL HUGE SPECULATOR SHORT COVERINGS ////CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.580 MILLION OZ FOLLOWING A ZERO QUEUE JUMP / // V) GIGANTIC SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: –53

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTRACTS for 1 days, total 50 contracts: 0.250 million oz OR 0.250MILLION OZ PER DAY. (50 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 0.25 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2401 DESPITE OUR STRONG $0.31 GAIN IN SILVER PRICING AT THE COMEX// FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 50 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER ADDITIONS A// NET SPEC SHORT LIQUIDATIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR OCT. OF 1.580 MILLION OZ FOLLOWED BY TODAY’S ZERO QUEUE JUMP .. WE HAD A GIGANTIC SIZED LOSS OF 2351 OI CONTRACTS ON THE TWO EXCHANGES FOR 11.755MILLION OZ..

WE HAD 3 NOTICE(S) FILED TODAY FOR 15,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GIGANTIC SIZED 21,464 CONTRACTS TO 432,024 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED — -186 CONTRACTS.

.

THE GIGANTIC SIZED DECREASE IN COMEX OI CAME DESPITE OUR GAIN IN PRICE OF $3.75//COMEX GOLD TRADING/FRIDAY / WE HAD HUGE FINAL SPREADER LIQUIDATION WHICH HAD NO EFFECT ON PRICE// CONSIDERABLE SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR OCT. AT 66.099 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 1800 OZ//NEW STANDING 66.155 TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $3.75 WITH RESPECT TO FRIDAY’S TRADING

WE HAD A GIGANTIC SIZED LOSS OF 17,778 OI CONTRACTS 55.172 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3726 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 432,024

IN ESSENCE WE HAVE A GIGANTIC SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 17,738 CONTRACTS WITH 21,464 CONTRACTS DECREASED AT THE COMEX AND 3726 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 17,738 CONTRACTS OR 54,59 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3726) ACCOMPANYING THE GIGANTIC SIZED LOSS IN COMEX OI (21,464): TOTAL LOSS IN THE TWO EXCHANGES 17,738 CONTRACTS. WE NO DOUBT HAD 1) CONSIDERABLE SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS/// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 66.099 TONNES FOLLOWED BY TODAY’S 1800 OZ QUEUE JUMP///NEW STANDING 66.155 TONNES//. 3) ZERO LONG LIQUIDATION //// //.,4) GIGANTIC SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/5/FINAL SPREADER LIQUIDATION.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT. :

3726 CONTRACTS OR 372600 OZ OR 11.58 TONNES 1 TRADING DAY(S) AND THUS AVERAGING: 3726 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAY(S) IN TONNES: 11.58 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 11.58/3550 x 100% TONNES 0.309% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 11.58 TONNES INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER,FELL BY A GIGANTIC SIZED 2401 CONTRACT OI TO 127,382 AND FURTHER FROM TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 50 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 50 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 50 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2401 CONTRACTS AND ADD TO THE 50 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED LOSS OF 2351 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 11.755 MILLION OZ

OCCURRED WITH OUR GAIN IN PRICE OF $0.31

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)MONDAY MORNING// SUNDAY NIGHT

SHANGHAI CLOSED //Hang Seng CLOSED DOWN 143.32 PTS OR 0.83% /The Nikkei closed UP 278.58PTS OR 1.07% //Australia’s all ordinaires CLOSED DOWN 0.33% /Chinese yuan (ONSHORE) closed //OFFSHORE CHINESE YUAN DOWN 7.1471// /Oil UP TO 83.00 dollars per barrel for WTI and BRENT AT 88.48 / Stocks in Europe OPENED ALL MIXED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAK AGAINST US DOLLAR/OFFSHORE WEAK

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GIGANTIC SIZED 21,278 CONTRACTS TO 432,210 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS HUGE COMEX DECREASE OCCURRED DESPITE OUR RISE IN PRICE OF $3.75 IN GOLD PRICING FRIDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (3728 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF OCT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3726 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :3726 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3529 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GIGANTIC SIZED SIZED TOTAL OF 17,552 CONTRACTS IN THAT 3726 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GIGANTIC SIZED COMEX OI LOSS OF 21,278 CONTRACTS..AND THIS HUGE LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR SMALL RISE IN PRICE OF GOLD $3.75. WE HAD OUR FINAL CONCLUSION OF SPREADER LIQUIDATION WHICH SURPRISINGLY HAD NO EFFECT ON THE GOLD PRICE//WE HAD SPEC SHORT DESPERATELY TRYING TO COVER WITH BANKERS TAKING THE BUY SIDE. IT IS BECOMING EXTREMELY DIFFICULT FOR OUR SHORTERS. THUS, WE ARE NOW WITNESSING THE SPECULATORS CONTINUING TO GO MASSIVELY SHORT WHILE THE BANKERS WHO ARE HUGELY LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS ONCE THE SIGNAL HAS BEEN GIVEN TO ANNIHILATE THE SPECS. (SEE THE TED BUTLER ARTICLE ON THIS MATTER/FRIDAY//SEPT 30)

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING OCT (66.155),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 66.155 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $3.75) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A HUGE SIZED TOTAL LOSS ON OUR TWO EXCHANGES OF 17,552 CONTRACTS // WE HAVE REGISTERED A HUGE LOSS OF 55,172 PAPER TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR SOCT. (66.155 TONNES)…ALL OF THE LOSS IN OI WAS DUE TO THE CONCLUSION OF SPREADER LIQUIDATION

WE HAD -186 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 17,738 CONTRACTS OR 1,773,800 OZ OR 55.172 TONNES

Estimated gold volume 165,761/// poor//

final gold volumes/yesterday 217,443/ fair

INITIAL STANDINGS FOR OCT ’22 COMEX GOLD //OCT 3

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 40,638.860 oz Brinks |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 18,560.923 oz |

| No of oz served (contracts) today | 813 notice(s) 81300 OZ 2.528 TONNES |

| No of oz to be served (notices) | 1423 contracts 142,300oz 4.435 TONNES |

| Total monthly oz gold served (contracts) so far this month | 20,641 notices 2,064,100 64.202 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

customer withdrawals: 1

i) Out of Brinks: 40,638.860 oz

total: 40,638.600 oz

total in tonnes: 1.264 tonnes

Adjustments: 2

JPM: dealer to customer; 32,118.822 0z

JPM enhanced: customer to dealer: 41,736.838

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCT we have an oi of 1441 contracts having LOST 19,810 contracts . We had 19,828 contracts

filed on Friday, so we gained 18 contracts or an additional 1800 oz will stand in this active delivery month of Oct.

This is the second straight delivery month where we witness QUEUE jumping on day two of the delivery cycle.

We will gain gold oz standing on each and every trading day from this day forth until the conclusion of October.

(remember that queue jumping is really EFP’s exercised from London for gold underwritten by COMEX based bankers)

November GAINED 47 contracts to stand at 2138

December LOST 1978 contracts DOWN to 379,397

We had 813 notice(s) filed today for 81300 oz FOR THE OCT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 813 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 266 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT /2022. contract month,

we take the total number of notices filed so far for the month (20,641) x 100 oz , to which we add the difference between the open interest for the front month of (OCT 1441 CONTRACTS) minus the number of notices served upon today 813 x 100 oz per contract equals 2,126900 OZ OR 66.155 TONNES the number of TONNES standing in this active month of OCT.

thus the INITIAL standings for gold for the OCT contract month:

No of notices filed so far (20,641) x 100 oz+ (xx) OI for the front month minus the number of notices served upon today (813} x 100 oz} which equals 2,126,900 oz standing OR 66.155 TONNES in this NON active delivery month of OCTOBER.

TOTAL COMEX GOLD STANDING: 66.155 TONNES (A HUMONGOUS STANDING FOR OCT (GENERALLY THE POOREST DELIVERY MONTHS FOR AN ACTIVE MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,057,668.110 oz 64.00 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 26,318,372.766 OZ

TOTAL REGISTERED GOLD: 13,092,999.826 OZ (407.24 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 13,225,372.940 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 11,035.331 OZ (REG GOLD- PLEDGED GOLD) 343.234 tonnes//rapidly declining

END

SILVER/COMEX

OCT 3//INITIAL OCT SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2,428,982.600 oz Brinks CNT Delaware HSBC JPMorgan Manfra |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,476,137.010 oz HSBC CNT |

| No of oz served today (contracts) | 3 CONTRACT(S) 15,000 OZ) |

| No of oz to be served (notices) | 261 contracts (1,305,000 oz) |

| Total monthly oz silver served (contracts) | 58 contracts 290,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 2 deposits into the customer account

i) Into HSBC: 581,708.100 oz

ii) Into CNT: 581,708.100 oz

Total deposits: 1,476,137.010 oz

JPMorgan has a total silver weight: 161.817million oz/313.059million =51.69% of comex

Comex withdrawals: 6

i)Out of CNT 122,116.340 oz

ii)Out of Brinks: 595,746.250 oz

iii) Out of Delaware 15,288.988 oz

iv) Out of hSBC: 2051.440 oz

v) JPMorgan: 1,129,168.772 oz

vi) Out of Manfra: 564,010.810 oz

total withdrawals: 2,428,982.810 oz

adjustments: // 5

DEALER TO CUSTOMER:

i)Brinks: 1,102,972.800 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 41.112 MILLION OZ (declining rapidly)

TOTAL REG + ELIG. 313.059 MILLION OZ (also declining)

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF OCT OI: 261 CONTRACTS HAVING LOST 55 CONTRACTS.

WE HAD 55 NOTICES FILED ON FRIDAY SO WE NEITHER GAINED NOR LOST ANY

SILVER CONTRACTS STANDING FOR OCT.

NOVEMBER GAINED 18 CONTRACTS TO STAND AT 283

DECEMBER SAW A LOSS OF 2541 CONTRACTS DOWN TO 111,483

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 3 for 15,000 oz

Comex volumes:81,613// est. volume today// good

Comex volume: confirmed yesterday: 65,273 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 58 x 5,000 oz = 290,000 oz

to which we add the difference between the open interest for the front month of OCT(261) and the number of notices served upon today 3 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT./2022 contract month: 58 (notices served so far) x 5000 oz + OI for front month of OCT (261) – number of notices served upon today (3) x 5000 oz of silver standing for the OCT contract month equates 1,580,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:52,182// est. volume today// poor

Comex volume: confirmed yesterday: 61,393contracts ( poor)

END

GLD AND SLV INVENTORY LEVELS

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

SEPT 21/WITH GOLD UP $4.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.79 TONNES FROM THE GLD///INVENTORY RESTS AT 952.16 TONNES

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

SEPT 13/WITH GOLD DOWN $22.85 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73ONNES FROM THE GLD////INVENTORY RESTS AT 964.91 TONNES

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

GLD INVENTORY: 939.70 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

OCT 1/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

SEPT 21/WITH SILVER UP 33 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.902 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 482.115 MILLION OZ//

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

SEPT 13/WITH SILVER DOWN $.31 TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.899 MILLION OZ//

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

CLOSING INVENTORY 480.917 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

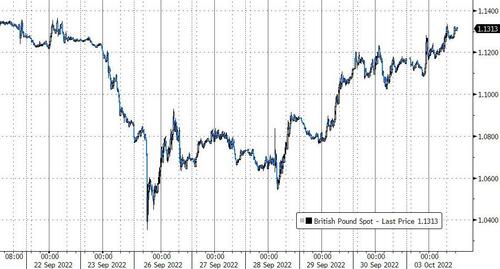

Peter Schiff: The Bank Of England Rings The Mother Of All Bells

MONDAY, OCT 03, 2022 – 12:25 PM

Last week, the Bank of England suddenly pivoted.

It gave up its inflation fight to rescue its pension funds and bond market. What exactly happened? And what does it tell us about the Federal Reserve’s inflation fight? Peter Schiff explained it all on his podcast.

There is an old expression — “No one rings a bell” — meaning there’s no warning when there is a major top or bottom in the markets. But Peter said there often is a bell but nobody hears it. Last week, Peter said we got the “mother of all bells.”

It was literally Big Ben that rang because the bell was in England… The Bank of England was the first major central bank to blink in this global game of chicken.”

Last week, the Bank of England pivoted and returned to quantitative easing.

Peter called this development “very significant.” Because up until the announcement, Bank of England Governor Andrew Bailey was just as hawkish as Jerome Powell. The Bank of England raised interest rates from 0.1% last December to roughly 2.25%, including a 50 basis point rate hike in August. It was the largest BoE rate hike in 27 years.

He was talking tough about how resolute the Bank of England was to fighting inflation. They’ve got the highest inflation in Europe. It’s way above their 2% target. It’s a double-digit number. It’s above 10%.”

Bailey even said he was committed to bringing down inflation no matter the cost and said he was willing to endure some pain, just like Jerome Powell.

Well, that was all a bluff because we got some pain overnight and Bailey folded like a cheap suit. And instead of quantitative tightening, they’re back to quantitative easing. The rate hikes are probably permanently on hold because the Bank of England refused to allow a potential crisis to unfold as a result of rising interest rates.”

The crisis manifested itself in the UK pension system with plunging bond prices. CNBC summed up the problem.

In order to top up the collateral on these bonds, some funds had to raise cash. But due to the speed of this crisis, many funds were caught out and were forced to liquidate their next most liquid assets, long-term bonds or gilts, causing prices of bonds to fall even more.”

In order to stabilize bond prices, the BoE stepped in to buy long-term bonds, creating artificial demand and propping up prices.

This pension problem isn’t exclusive to the United Kingdom. Pensions systems worldwide face the same issue, including in the United States.

When interest rates fall to zero, bond holdings in pension funds don’t generate as much interest income. Pensions need this income to pay benefits. So, in order to boost their incomes, pension funds borrow money at low interest rates to buy new long-term bonds using existing bonds as collateral. They make up for lower yields by holding more bonds.

But when interest rates rise, the value of their bond portfolio collapses even as the interest on their debt rises.

All of the pension funds that had borrowed short to buy long-term bonds were getting crushed because the value of the bonds they owned was collapsing and the cost of servicing the debt was soaring, and they were in a position where they were going to get margin calls. Those margin calls were going to force an already collapsing bond market to fall even more and that would have wreaked havoc throughout the United Kingdom.”

In simple terms, instead of raising pension contributions or cutting pension benefits to deal with their shortfalls, pension managers took the easy, but reckless way out and borrowed money.

On top of that, the newly elected British prime minister rewarded voters with a big tax cut that threw even more gasoline on the inflationary fire.

Great Britain was looking at a potential crash in the bond market and the Bank of England rode in to save the day.

The Bank of England folded. They pivoted. They decided to launch a new QE program. Remember, yesterday, they were committed to quantitative tightening. Now they said they will buy whatever it takes. They have committed to another QE infinity in order to prop up the bond market. They now have to print British pounds to buy these gilts. So, instead of fighting inflation, which yesterday was public enemy number one – it had to be brought down at any cost – now, all of a sudden, when you see the cost, well, forget about that. We’re now going to create inflation.”

The central bankers in England claim this is not a monetary policy decision. It was a move to avert a crisis. But as Peter said, it is most definitely a monetary policy decision.

That’s the only policy they make — monetary policy. Deciding to launch QE is monetary policy. I don’t care what you want to pretend. That’s what it is.”

The BoE also said it just wants to maintain an orderly market.

Well, you can’t fight inflation and maintain an orderly market because the markets have been propped up by inflation. So, if you’re going to fight inflation, you’d better be prepared for a disorderly market. And until yesterday, the Bank of England was bluffing that they were. But now that their bluff has been called, they had to show their cards, and they’re holding nothing. And so, inflation won.”

You might think this has nothing to do with you if you’re reading this in the US. The problem is, the Federal Reserve is also bluffing. It’s only a matter of time before their bluff gets called.

Is the Federal Reserve, when confronted with the same situation, will they make a different choice than the Bank of England? Does the Federal Reserve have more integrity? Are these guys willing to allow a financial crisis? Because the same thing is going to happen here. We’ve got all sorts of leverage in our markets. We’ve got a bigger debt bubble than the British. It’s just that the day of reckoning for us is not going to come as early as it did for them because the dollar is going up.”

When that day of reckoning does come, Peter said he expects Jerome Powell to make the same decision as Andrew Bailey.

I don’t care how much he wants to bark about being tough on inflation. At the end of the day, he will not bite. The Fed is a paper tiger and it will fold just as quickly as the Bank of England when they’re confronted with an actual crisis.”

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

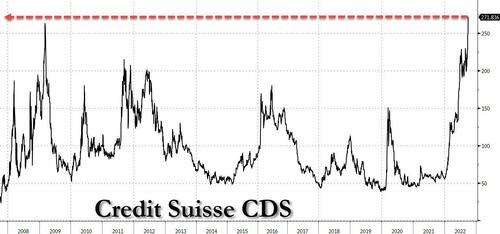

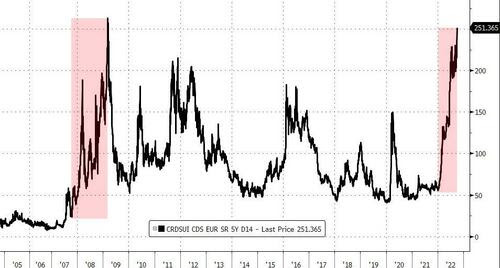

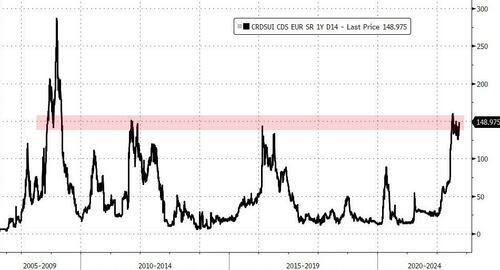

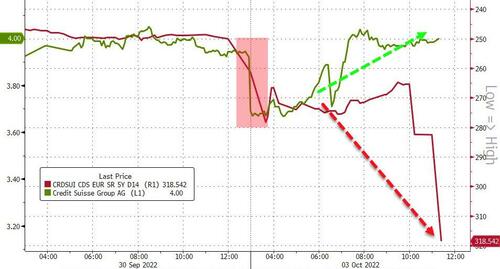

The Credit Default Swap mess of Credit Suisse:

Pam and Russ Martens

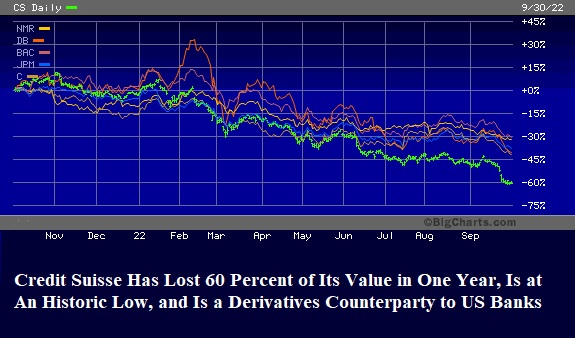

Here’s the Chart of the Global Bank Causing Panic in Markets This Morning

By Pam Martens and Russ Martens: October 3, 2022

The Swiss global bank, Credit Suisse, which is a derivatives counterparty to major Wall Street banks and U.S. insurers, raised alarm bells in markets on Friday and is raising more anxiety this morning. Its 5-year credit default swap (CDS), a measurement of its risk of defaulting on its debt, jumped to 250 basis points on Friday and traded as high as 350 basis points in early morning trade today.

The big move in the CDS on Credit Suisse is further impacting the price of its common stock. The shares closed on Friday in New York at $3.92, just pennies away from its all-time low, then dropped another 11 percent in early morning trading in Europe today.

When a major derivatives counterparty begins to see a blowout in its credit default swaps, that impacts the stock prices of all major Wall Street banks with significant exposure to derivatives. It also raises the risk of systemic contagion — as occurred in the financial crisis of 2008 when Citigroup and Lehman Brothers were teetering and were major derivative counterparties. The chart above shows the dramatic declines in not just Credit Suisse over the past year but in Nomura (NMR), Deutsche Bank (DB), Bank of America (BAC), JPMorgan Chase (JPM), and Citigroup (C).

The reputation of Credit Suisse has taken major hits in the past few years. On March 26, 2021, the family office hedge fund, Archegos Capital Management, defaulted on margin calls to its prime brokers and went belly up, leaving major investment banks with more than $10 billion in losses. Credit Suisse took the lion’s share of those losses, acknowledging a loss of more than $5 billion.

To understand the nature of the wildly risky structure of the derivatives that led to the blowup of Archegos, see our report: Archegos: Wall Street Was Effectively Giving 85 Percent Margin Loans on Concentrated Stock Positions – Thwarting the Fed’s Reg T and Its Own Margin Rules.

Credit Suisse was also deeply enmeshed in the Greensill Capital scandal and has suffered serious reputational damage as a result.

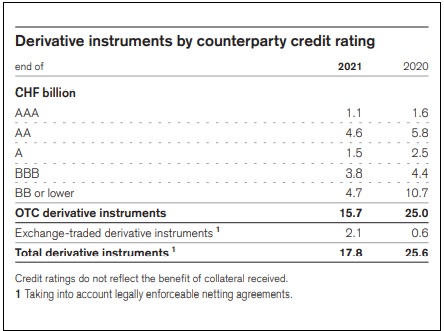

Making stock investors equally nervous is the fact that Credit Suisse admitted in its 2021 Annual Report that some of its billions in derivatives are difficult to accurately price. It writes:

“In addition, the Group holds financial instruments for which no prices are available and for which have few or no observable inputs (level 3). For these instruments, the determination of fair value requires subjective assessment and judgment depending on liquidity, pricing assumptions, the current economic and competitive environment and the risks affecting the specific instrument. In such circumstances, valuation is determined based on management’s own judgments about the assumptions that market participants would use in pricing the asset or liability (including assumptions about risk). These instruments include certain OTC derivatives, including interest rate, foreign exchange, equity and credit derivatives, certain corporate equity-linked securities, mortgage-related securities, private equity investments, certain loans and credit products, including leveraged finance, certain syndicated loans and certain high yield bonds.”

Under “Major Risks,” the 2021 Annual Report for Credit Suisse calls out the following risk for its Investment Bank:

“Loan underwriting and lending commitments to corporate clients, markets and trading activities including securities financing and derivatives products with global institutional clients, including banks, insurance companies, asset managers and hedge funds; through the use of derivatives clients may take positions that are exposed to movements in risk factors such as interest rates, credit spreads, foreign exchange rates or equity prices.”

All eyes on Wall Street are going to be watching the price action of Credit Suisse and other major banks on Wall Street this week in an effort to discern which banks are most heavily exposed to Credit Suisse as a derivatives counterparty.

Derivatives by Counterparty Credit Rating Reported by Credit Suisse in Its 2021 Annual Report

end

Lawrie Williams

very important read, especially the last paragraph

Lawrie Williams: Gold and silver make gains in nervous markets

The gold price picked up nicely, and silver even more so in percentage terms, when markets opened in Europe and the U.S. on Monday, although it remains to be seen whether the gains so made can be sustained throughout the day, let alone the week ahead. The principal stimulus appears to have been renewed safe haven demand following President Putin’s announcement on Friday that Russia was annexing Ukraine’s Luhansk, Donetsk, Zaporizhzhia and Kherson oblasts as integral parts of the Russian state. This followed on from the hastily-arranged dubious referenda which had appeared to confirm, according to the Russians, that that was the will of the people in those regions by huge majorities. The outcomes of these referenda were largely dismissed as false and unrepresentative by the world at large.

However, the official annexation of these territories into the Russian state, even though some of them are only partially under Russian control, could give President Putin the excuse to describe any Ukrainian attacks on them as an ‘invasion’ of Russia itself and a reason for a massive escalation of hostilities. His partial mobilisation of reservists to support his existing forces could just thus be the beginning, but how the Russian people would see this could be something of a gamble. There already seems to be evidence of a growing build-up of opposition to the existing partial call-up – or is this just Western propaganda?

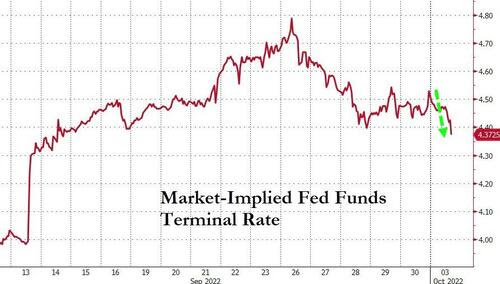

In any case, the prospects of an escalation of the Ukraine conflict, which currently, at least according to Western media, appears to be going badly for the Russians, has certainly given precious metals prices something of a boost. Equity and bitcoin prices were trending higher too with the U.S. dollar index falling. This had all come about given a sharp fall in market sentiment on the market’s view of the likelihood of yet another 75 basis point rate rise at the November 2nd FOMC meeting. This has now, according to the CME’s Fedwatch Tool come down to a near 50:50 chance of only being a 50 basis point rise and may well slip further during the month between now and the actual meeting date. This has been somewhat coloured by the Bank of England’s recent supportive move, seen by some as a return to Quantitative Easing, in support of the U.K. economy and the pound which had been on a sharp downturn following the recent budget announcement from the new UK Chancellor Kwasi Karteng. The BoE move seems to have stabilised the UK situation and one of the tax reducing measures in the original budget announcement – the withdrawing of the 45% higher tax rate for high earners – has been reversed and the pound has seen something of a recovery on the foreign exchange markets. Nonetheless, the fact that one of the world’s major central banks seemed to be returning to a more stimulative policy raised hopes that the U.S. Fed might consider doing so too.

In the U.S. though, the latest Personal Consumption Expenditure (PCE) index figures were released. This is the Fed’s preferred inflation measure, and it didn’t make for happy reading, particularly as far as the core inflation index measure was concerned. This rose by 0.4% month-on- month indicating that the Fed’s interest rate raising programme is having little or no effect so far. As it is the core index level which will be of most concern to the Fed this does not suggest that it will likely consider any reduction in its approach to an aggressive interest rate raising policy unless there are strong signs of an inflation turn around within the time period before the next meeting takes place. This is certainly not outside the bounds of possibility, but it would probably be wise to play safe and steer clear of general equities for now. Recession is almost certainly upon us – it is only the depth thereof which is in doubt.

Meanwhile keep a close eye on the Ukraine war and the Russian reaction to any Ukrainian advances in the Russian- claimed territories. If Russia is prepared to seriously escalate its reactions, precious metals – or at least gold and silver – could see further advances, with gold back into the $1,700s and silver maybe into the $21s. There is also a rumour that the OPEC nations may cut oil output which could boost energy prices too. Still difficult times ahead as we enter the northern winter season.

03 Oct 202

-END-

END

3.Chris Powell of GATA provides to us very important physical commentaries

An excellent video interviewing of Alasdair Macleod by Andrew Maguire

(GATA/Andrew Maguire)_

Eurasia will lead the world back to gold, Macleod tells Maguire

Submitted by admin on Fri, 2022-09-30 21:23Section: Daily Dispatches

9:25p ET Friday, September 30, 2022

Dear Friend of GATA and Gold:

Discussing world financial affairs with London monetary metals trader Andrew Maguire on Kinesis Money’s “Live from the Vault” program, GoldMoney research director Alasdair Macleod says a new world payment system is likely to arise from the Eurasian powers and that it will draw heavily on gold.

Additionally, Macleod notes the steady devaluation of many major currencies and says the entire fiat currency system well may collapse.

The interview is an hour long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

London gold dealer Blundell runs out of bullion as the Truss budget shocks Britons

(Spence/Bloomberg/GATA)

London gold dealer runs out of bullion as Truss budget shocks

Submitted by admin on Sat, 2022-10-01 09:01Section: Daily Dispatches

By Eddie Spence

Bloomberg News

Saturday, October 1, 2022

When the pound slumped as Kwasi Kwarteng presented his mini-budget, some Britons rushed to the safety of a haven that has recently lost its luster: gold.

As the UK currency slid to an all-time low early Monday, bullion priced in pounds climbed close to a record. That would typically encourage selling and deter buyers, but this time round the turmoil in British bond and currency markets increased the allure of the precious metal

“Buying has increased exponentially,” said Ash Kundra, who runs coin dealer J Blundell & Sons in London’s historic Hatton Garden jewelry quarter. “I keep running out of coins. I keep running out of bars.”

The rush for gold in the UK contrasts with the bearish sentiment that has seen dollar prices for the precious metal slump by more than 20% from a March peak, as the Federal Reserve’s aggressive monetary tightening makes the non-interest-bearing asset less attractive. Still, bullion’s status as a hedge against inflation and currency debasement is keeping demand from retail investors strong. …

… For the remainder of the report:

END

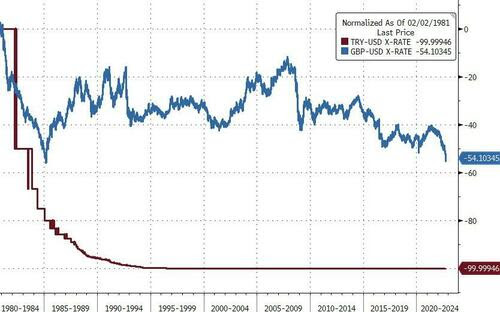

At least the Turkish central bank realizes the lira is in trouble so the country becomes the top gold buying this year.

(Daily Sabah/Istanbul/GATA)

Turkish central bank is top gold buyer among central banks this year

Submitted by admin on Sat, 2022-10-01 09:10Section: Daily Dispatches

From the Daily Sabah, Istanbul

Friday, September 30, 2022

The Turkish central bank has been the top gold buyer among its global peers so far this year, according to data from the World Gold Council.

The Central Bank of the Republic of Türkiye bought around 9 tons of gold in August, the council said Thursday, increasing its total purchases to 84 tons year-to-date

This brought its official gold reserves (central bank plus treasury holdings) to 478 tons, the highest level since the second quarter of 2020, the data showed.

Meanwhile, global central bank net purchases of gold slowed to 20 tons in August, halving month-over-month, Krishan Gopaul, a senior analyst at the gold council for Europe, the Middle East and Africa, said in a blog. It marked the fifth consecutive month of net purchases from the central banking sector. …

… For the remainder of the report:

END

Qatar boosts its gold reserves in one month by 14.8 tonnes, the largest per month its history. It’s reserves now stand at 72.3 tonnes.

(Ronan Manly/Bullion star)

Qatar boosts gold reserves as FIFA World Cup nears

Submitted by admin on Sat, 2022-10-01 23:38Section: Daily Dispatches

By Ronan Manly

Bullion Star, Singapore

Saturday, October 1, 2022

With many eyes across the world soon turning towards the Gulf State of Qatar as it hosts the 2022 FIFA World Cup later this year, now is a good time to look at another interesting development in the Qatari rmirate — the recent rapid growth of Qatar’s monetary gold reserves.

In August the Qatar central bank raised a few eyebrows when it announced that during July it had purchased about 14.8 tonnes of gold, thereby bringing the country’s official gold reserves to 72.3 tonnes.

This addition to Qatar’s gold holdings was significant because it was both the largest ever single monthly purchase of gold by Qatar’s central bank (or its predecessors), and it also raised Qatar’s monetary gold reserves to their highest level ever. In September the Qataris continued their gold buying, raising their gold reserve holdings to 77 tonnes. …

… For the remainder of the report:

END

4. OTHER GOLD/SILVER COMMENTARIES

PHYSICAL SILVER/GOLD

LOWEST PREMIUMS FROM MME: IN SILVER $9.50 OVER SPOT

| Money Metals News AlertOctober 3, 2022 – Gold and silver prices recovered last week. The Federal Reserve Note “dollar” lost a bit of ground in the currency markets late in the week, after rising to almost 115 on Wednesday. Stocks and bonds got pounded once again. |

| The metals are starting to show some strength in the face of the rising DXY. Silver, in particular, seems to have put in a bottom. Silver traded from its low of $17.82/oz to $19.26/oz at the end of September. The U.S. Dollar Index traded at 109.69 on September 1 and finished the month at 112.17. 10 Oz Silver BarsShop Now >> |

| The dollar just hit its highest level in 20 years, relative to other fiat currencies, but silver prices moved higher despite that pressure. Now investors want to see gold prices confirm silver’s relative strength. |

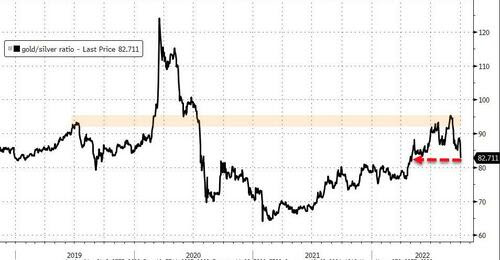

(Weekly Gain/Loss)Monday Morning (Gain/Loss from Friday’s Close)Gold$1,669 (+1.1%)$1,678 (+0.5%)Silver$19.26 (+1.0%)$20.42 (+6.0%)Platinum$882 (+0.7%)$901 (+2.2%)Palladium$2,243 (+4.6%)$2,273 (+1.3%)Gold : Silver Ratio (as of Friday’s closing prices) – 86.7 to 1 |

| Mint Shortages Further Pressure Supply Amid High DemandShare this Article: |

| In August, demand for bullion had slacked a bit from the frenetic pace set over the past two years. But buyers came back with a vengeance during September, and inventories of the most popular products are showing the strain. |

Premiums are back on the rise and delivery delays have returned for many items, with silver inventories being hardest hit. Money Metals’ weaker competitors are especially struggling. |

| As buyers turn away from higher-priced silver coins (particularly the problematic Silver Eagle, one-ounce silver rounds and bars of various sizes are now experiencing supply issues. The major constraint, once again, is in the capacity of mints and refiners to produce retail bullion products. While demand for 1,000 oz silver bars also appears strong, premiums for those large bars are holding steady. Money Metals’ Vault Silver storage offering is by far the lowest premium way to acquire silver ounces right now. If 1,000 oz bar premiums rise, it would be signaling a true shortage of silver. For now, though, the shortage is in the fabrication capacity of mints and refiners who convert large bars into smaller products. The pressure on premiums has been driven, at least in part, by the U.S. Mint. Despite its obligation to produce coins in quantities “sufficient to meet public demand,” the Mint has done nothing to increase supply. |

| Demand spiked for bullion products two and a half years ago. Private mints and refiners have been steadily growing capacity, but the U.S. Mint is manufacturing excuses instead. Congressman Alex Mooney (R-WV) sent a terse letter to Mint Director, Ventris Gibson, just over a month ago. Ms. Gibson replied last week. She blamed issues on COVID and on the vendors who supply blanks.  Rep. Mooney recently chastised the U.S. Mint for mismanagement. Rep. Mooney recently chastised the U.S. Mint for mismanagement. |

| The U.S. Mint’s response letter was predictably long on excuses and short on solutions. The top U.S. Mint bureaucrat says she hopes to add some new vendors who can produce blanks, rather than gearing up to produce blanks in-house. There was no mention of plans to dramatically increase inventories during periods when demand is slower. If the Mint has plans to add any people, equipment or in-house capacity, Gibson didn’t discuss that either. |

| Until and unless the U.S. Mint gets its act together, it remains wise to avoid the extraordinarily high premiums that come with American Eagles – and even consider selling the Silver Eagles you have to Money Metals for $9.50 over spot to redeploy the funds into more ounces in other forms. |

| Rounds and bars offer much better value – as do many other silver coins. As alluded to above, the lowest-cost way to own physical bullion is through Vault Silver and Vault Gold. Pricing there is based on large commercial bar premiums, which remain low and stable. Vault Metals should get a serious look from any investor planning to have their metal stored in a depository. They will also be a good choice for investors who ultimately want to take delivery of metal, but don’t mind buying and storing low-premium metal until the high premiums for deliverable products subside. |

5.OTHER COMMODITIES: ALUMINUM

COMMODITIES IN GENERAL/

END

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings MONDAY morning 7:30 AM

ONSHORE YUAN: CLOSED

OFFSHORE YUAN: 7.1471

SHANGHAI CLOSED:

HANG SENG CLOSED DOWN 143.32 PTS OR 0.83%

2. Nikkei closed UP 278.58 PTS OR 1.07%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UP TO 112.36/Euro RISES TO 0.9760

3b Japan 10 YR bond yield: FALLS TO. +.239/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 144.95/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: XX -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.002%***/Italian 10 Yr bond yield FALLS to 4.43%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.20%…** DANGEROUS

3i Greek 10 year bond yield RISES TO 4.85//

3j Gold at $1665.80//silver at: 19.42 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 57/100 roubles/dollar; ROUBLE AT 57.88//

3m oil into the 83 dollar handle for WTI and 88 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 144.95DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this .9888– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9649well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.714 DOWN 9 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.698 DOWN 7 BASIS PTS//(USA 30 YR INVERTED TO THE USA 10)

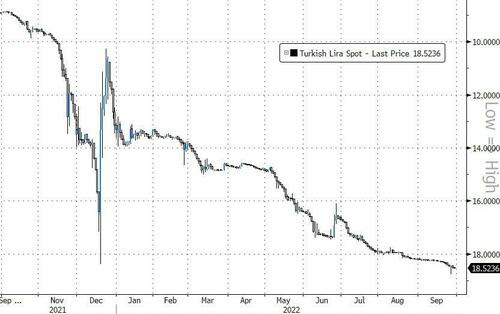

USA DOLLAR VS TURKISH LIRA: 18,57…GETTTING DANGEROUS

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Swing Wildly As Nervous Traders React To Every Rumor In Extremely Illiquid Markets

MONDAY, OCT 03, 2022 – 08:04 AM

After a disastrous September, stocks have started off the new month of October – which at least historically tends to do much better than its predecessor – in extremely jittery fashion, with global stocks falling to a two-year low and US equity futures first sliding as much as 0.6%, before rising as much as 0.7% in what can only be described as an extremely illiquid market where Emini top of book liquidity is now at or below 1 million. Nasdaq futures were flat, as was the dollar while 10Y yields slumped perhaps in response to Mark Cabana’s latest note predicting a Fed “Twist” operation is on the horizon as the TSY market faces “breakdown.”

Risk got a boost after the new UK Chancellor of the Exchequer Kwasi Kwarteng dropped a plan unviled just 10 days ago, to abolish a 45% rate of income tax for the country’s highest earners, claiming it is helping to preserve credibility when in reality it achieved just the opposite. On the other hand, the continue blow out in Credit Suisse CDS, indicative of a potential “New Lehman”, pushed the company’s credit risk to new record highs, surpassing even the Lehman crisis wides, and sending the company’s stock to new all time lows as bets that the Swiss lender will blow up next soar.

In premarket trading, Tesla (TSLA US) fell as much as 6.5% in premarket trading after the electric vehicle maker missed third-quarter deliveries as it struggled to get its cars to customers. Shares of fellow EV makers are also under pressure on Monday as the ongoing supply- chain snarls might affect peers as they ramp up production. On the other end, energy stocks rose as the OPEC+ alliance considered its biggest production cut since the pandemic, sending West Texas Intermediate crude oil prices to just over $83 a barrel. Chevron (CVX US) +2.9% and Exxon (XOM US) +2.9%

Other notable premarket movers:

- Wells Fargo (WFC US) shares advance as much as 1.2% in US premarket trading after Goldman Sachs upgraded the investment bank to buy from neutral, while Citigroup shares drop as much as 1.1% after the broker downgraded it to neutral from buy.

- Myovant Sciences (MYOV US) shares gain 26% after the company confirmed it has received a proposal from Sumitovant Biopharma and Sumitomo Pharma to acquire its outstanding shares for $22.75 per share in cash, according to a statement. .

- Shares in LiveWire (LVWR US) gain 65% in US premarket trading. The move came after the standalone electric motorcycle brand spun out of Harley- Davidson raised $295 million on Sept. 27 after closing its merger with AEA-Bridges Impact Corp.

- DocuSign (DOCU US) fell 3.5% in US premarket trading after Morgan Stanley cut its recommendation on the stock to underweight from equal-weight, saying that increasing competition, e-signature commoditization and pricing pressures create incremental downside

As Bloomberg notes, global markets remain jittery over the potential impact of monetary tightening on the economy after central banks, including the Federal Reserve, reiterated their resolve to contain runaway inflation. US stocks ended the previous quarter with a third straight quarter of losses for the first time since 2009 after the Federal Reserve delivered a third jumbo hike last month. Traders now await US jobs data later this week to gauge the path of the economy and Fed policy.

“The Fed is actively trying to tighten financial conditions and weaker equity markets is one way you get there,” said Colin Asher, a senior economist Mizuho Bank Ltd. in London. “Because inflation is so high central banks will be wary of declaring victory just yet.”

In Europe, stocks fell as the region’s energy crisis threatened to escalate further; the Euro Stoxx 50 dropped 1.3%. The CAC 40 lags, dropping 1.4%. Tech, banks and financial services are the worst-performing sectors. The pound and UK government bonds initially rallied after Chancellor of the Exchequer Kwasi Kwarteng withdrew a proposal to abolish the top 45% tax rate, before ceding some of those gains. The other big focus was Switzerland’s Credit Suisse Group AG, which slumped more than 11% as speculation mounted about the company’s future and its requirement for fresh capital. The cost of insuring against exposure to the company surged to a record high as investors shrugged off Chief Executive Officer Ulrich Koerner’s efforts to calm the market. Here are some of the biggest European movers today:

- European energy stocks are in focus after oil surges on indications the OPEC+ alliance is considering slashing production by more than 1 million barrels a day when it meets this week. Shell rises as much as 1.9%, BP +2.5%, TotalEnergies +2.5%

- UK homebuilders outperform as gilt yields ease, following news that Prime Minister Liz Truss has dropped a plan to cut taxes for the highest earners. Vistry gains as much as +3.2%, Crest Nicholson +3.6%, Bellway +3.4%.

- Tenaris rises as much as 6.9% after the company held an investor presentation in New York on Sept. 30. Mediobanca highlights a “constructive message” from the event and other analysts also note positive indications.

- Vodafone gains as much as 3.6%, leading European telecom stocks higher, after a Sky News report that the company has accelerated a talk with Three UK about a deal to combine their British operations.

- Credit Suisse fell as much as 12% to new lows, even after CEO sought to calm markets as credit default swaps climbed to a record.

- VGP drops as much as 33%, the most intraday on record, after the company and its joint venture partner Allianz Real Estate announced they postpone the seed portfolio closing of the Europa Joint Venture previously envisaged for November due to volatile market environment.

- Banca Generali falls as much as 6.9% after Bloomberg reported Assicurazioni Generali has considered selling the unit to Mediobanca among options to help finance a potential deal, in a move questioned by Deutsche Bank.

- Danske Bank slides as much as 8.4% as Barclays says the Danish bank is unlikely to meet its FY22 profit outlook.

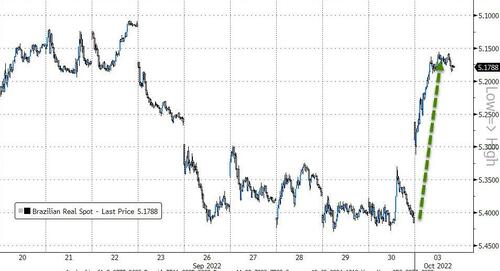

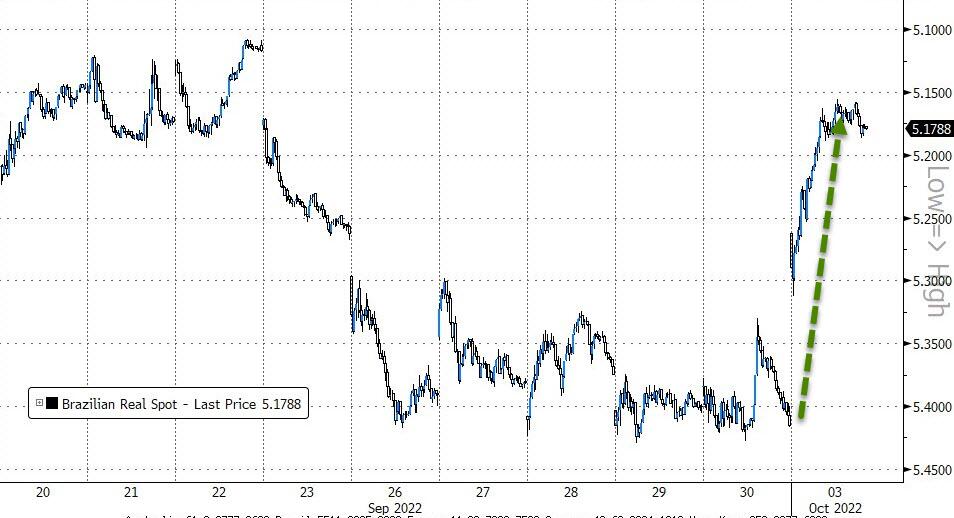

Investors also waited to see how Brazil-linked assets would fare after the country’s presidential election headed to a run-off vote on Oct. 30. An early indication came from the Lyxor MSCI Brazil ETF in Paris, which jumped the most since July 7.

Earlier in the session, Asian stocks slid after capping their worst month since 2008, as cautious sentiment prevailed amid worries about global recession and higher interest rates. The MSCI Asia Pacific Index fell 0.5%, with consumer staples and utilities leading losses. A jump in oil prices also kept traders on edge due to its impact on inflation. Thin trading volumes heightened price moves as China, South Korea and Sydney were closed for a holiday. The MSCI Asia gauge is trading at its most oversold level since March 2020 as concerns over China’s economic growth add to global headwinds. China remains closed this week for the Golden Week holiday, and any weakness in spending during the peak travel season may further disappoint traders already bruised from months of selloff.

Japan was one of the only markets in the green on Monday, with stocks rebounding as the yen’s weakness continued to support the nation’s exporters (more below). Taiwan’s stock benchmark Taiex Index fell slightly even as tighter rules on short selling took effect. Gauges in Hong Kong declined, while Vietnam’s fell the most in the region as leveraged traders liquidated positions. “Some respite was seen in the US yields and the US dollar last week, but data due this week could bring further risk-off,” Saxo Capital Markets strategists wrote in a note. READ: Relentless Dollar Rally Raises Bets on Interventions: MLIV Pulse US jobless claims, unemployment and factory orders are among the data that will be released later this week.

Japanese equities reversed earlier losses to advance as the yen’s weakness continues to support the nation’s exporters. The Topix Index rose 0.6% to 1,847.58 as of market close Tokyo time, while the Nikkei advanced 1.1% to 26,215.79. Toyota Motor Corp. contributed the most to the Topix Index gain, increasing 3.5%. Out of 2,168 stocks in the index, 1,018 rose and 1,069 fell, while 81 were unchanged. The yen hit the 145-per-dollar psychological level during afternoon trading hour. Japan’s stocks were the biggest boost to the MSCI’s Asia equity benchmark. “Automobiles are being bought on the back of the weak yen, and high-priced tech stocks are also in demand,” said Ryuta Otsuka, a strategist at Toyo Securities

In Australia, the S&P/ASX 200 index fell 0.3% to close at 6,456.90, as declines in technology and consumer stocks offset gains in energy and utilities. Sydney trading was impacted by a holiday in New South Wales. In New Zealand, the S&P/NZX 50 index fell 1% to 10,959.45.

Indian equities resumed their slide on Monday as banking and information technology firms slumped, while worries over inflation and slowing growth continued to dampen global investor sentiment. The S&P BSE Sensex dropped 1.1% to 56,788.81 in Mumbai, while the NSE Nifty 50 Index slipped 1.2%. Both rose more than 1.5% on Friday after the Reserve Bank of India raised its key lending rate by 50 basis points to 5.90% and largely retained its growth and inflation estimates. Despite the rally on Friday, the benchmarks posted their eighth drop in nine sessions mainly due to selling by foreign investors, who have offloaded $1.4 billion of local shares in the month through Sept. 29. For September, both gauges lost more than 3% each, the most since June. For the year, the Sensex is down 2.5% while the Nifty has lost 2.7%. All but two of the 19 sector sub-gauges compiled by BSE Ltd. declined on Monday, led by power and utilities companies. “We believe that the market may remain volatile with possibility of near term correction given the sharp recent out-performance,” Antique Stock Broking analyst Pankaj Chhaochharia wrote in a note. He cited reduction in banking liquidity, a flattening of the yield curve and the deteriorating global growth outlook as factors that could drag Indian stocks.

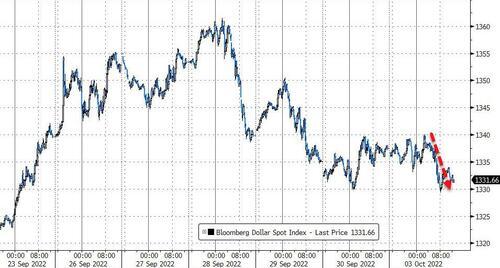

In FX, the Bloomberg Dollar Spot Index was little changed as the greenback traded mixed versus its Group-of-10 peers; JPY and SEK are the weakest performers in G-10 FX, NZD and AUD outperform.

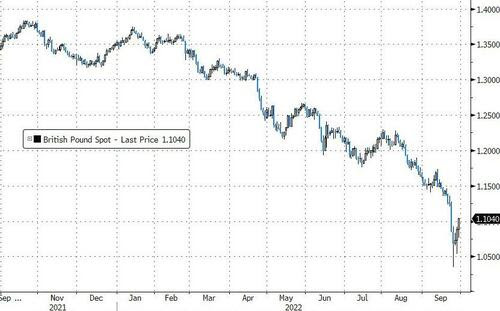

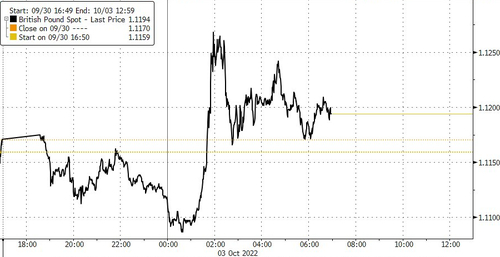

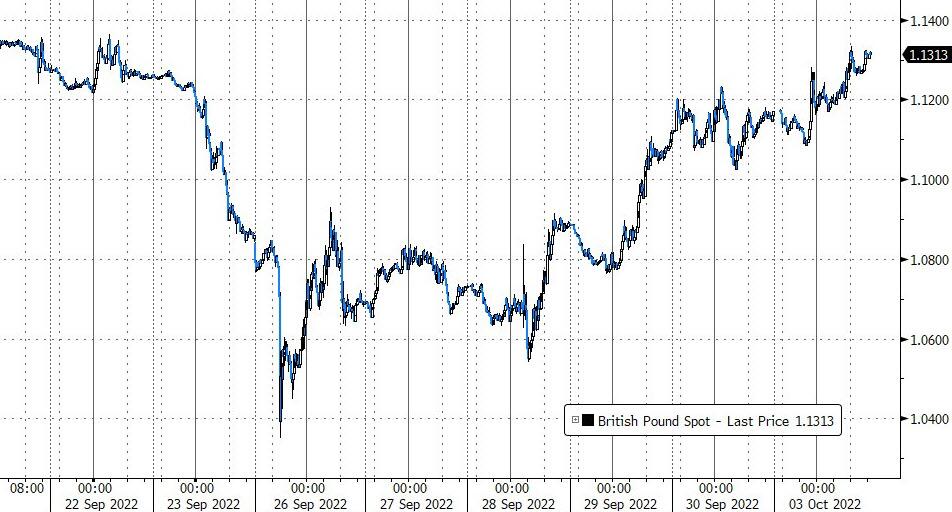

- Sterling pared gains after earlier rallying as much as 1% to $1.1281 as Chancellor of the Exchequer Kwasi Kwarteng dropped a plan to abolish a 45% rate of income tax for the country’s highest earners. Still, options traders add weaker-sterling bets the more it rallies. UK bonds rose across all maturities, sending the 10-year yield below 4% for the first time since Sept. 23, and money markets eased BOE tightening wagers.

- The euro steadied near $0.98 while bunds were little changed and Italian bonds fell.

- The yen weakened back beyond 145 per dollar as traders test the government’s resolve to arrest declines in the currency. Bonds gained after the central bank boosted its planned debt purchases for the fourth quarter. An index of sentiment among Japan’s biggest manufacturers edged down to 8 in September from 9, worsening for a third-straight quarter, according to the BOJ’s quarterly Tankan report released Monday.

- Commodity currencies were the best performers, led by Australian and New Zealand dollars amid rising oil prices. The Aussie-greenback’s one-week implied volatility jumped to the highest since April 2020 on Monday, with two key events in the coming days: an Australian policy review and US jobs data. Both RBNZ and RBA meet this week. Most economists surveyed by Bloomberg see a fifth straight half percentage-point hike by the Reserve Bank of Australia on Oct. 4 to take the cash rate to 2.85%, before opting for smaller hikes going ahead

Treasuries rallied, perhaps in response to Mark Cabana’s warning that the Fed will soon have to do a new Twist (which pushing long duration bond yield lower), and paring much of late Friday’s steep selloff into month-end. Gains were led by the front-end of the curve, paced by bull-steepening in gilts after UK Chancellor Kwarteng drops plan to abolish 45% top tax rate. Treasuries bull steepened, with yields falling between 3-9bps as traders pared Fed tightening bets; Treasury yields richer by up to 14bp across front-end of the curve with 2s10s, 5s30s spreads steeper by more than 3bp; 10- year yields around 3.72%, richer by 10bp on the day and outperforming bunds by 4bp, gilts by 2bp. Gilts 10-year yield drops as much as 10bps to 3.99% before paring the move to 4.07% as money markets ease BOE tightening wagers. Bunds little changed at 2.1% while USTs 10-year yield drops 4bps to 3.78%.

In commodities, WTI rises 4.7% to around $83.20 on signals the OPEC+ group may opt for a production cut of more than 1 million barrels a day. WTI futures jump on indications OPEC+ alliance is considering slashing production by

n-fitting with the last few sessions, Bitcoin is within narrow sub-500 ranges but is at the lower-end of these parameters and under modest pressure around USD 19.1k.

Looking at today’s US calendar we have US September ISM manufacturing index, total vehicle sales, August construction spending, Japan September vehicle sales; Friday brings the September jobs report.

Market Snapshot

- S&P 500 futures down 0.2% to 3,593.75

- MXAP down 0.3% to 138.45

- MXAPJ down 0.8% to 449.10

- Nikkei up 1.1% to 26,215.79

- Topix up 0.6% to 1,847.58

- Hang Seng Index down 0.8% to 17,079.51

- Shanghai Composite down 0.6% to 3,024.39

- Sensex down 1.0% to 56,877.88

- Australia S&P/ASX 200 down 0.3% to 6,456.87

- Kospi down 0.7% to 2,155.49

- STOXX Europe 600 down 1.5% to 382.21

- German 10Y yield little changed at 2.13%

- Euro up 0.2% to $0.9818

- Brent Futures up 4.0% to $88.55/bbl

- Gold spot up 0.2% to $1,664.59

- U.S. Dollar Index down 0.13% to 111.97

Top Overnight News from Bloomberg

- UK Prime Minister Liz Truss dropped a plan to cut taxes for the highest earners just 10 days after announcing it, in a bid to fend off a mounting rebellion from Members of Parliament in her own Conservative Party

- A corporate treasurer or finance minister looking to issue new notes now would likely have to pay interest that’s about 156 basis points higher on average than the coupons on existing securities, after that gap surged to a record in recent days. That all adds up to about $1.01 trillion in additional costs if all those securities were refinanced, according to calculations using a Bloomberg index tracking some $65 trillion of government and corporate debt across currencies

- When pandemic inflation took off last year, it was seen as more likely to stick around in the US — where stimulus was much bigger and consumer demand stronger — than in Europe. But the energy crisis has upended that picture

- The premium that holders of euros and yen need to pay to swap into dollars jumped as UK financial turmoil and Federal Reserve hawkishness gave a further tailwind to the greenback, with a Bloomberg gauge of the dollar rising to another record last week

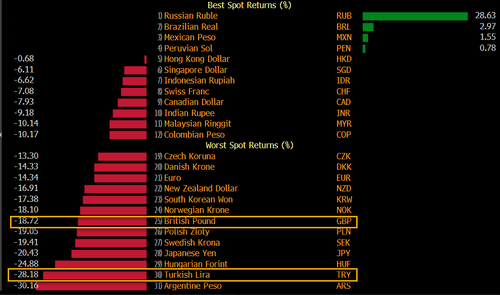

- Turkish inflation accelerated last month to a level last seen in mid-1998, fueled by an experimental central-bank policy that has chased away foreign investors and eroded the lira’s value. Consumer prices rose 83.5% on an annual basis in September, according to data released on Monday by Turkey’s statistics agency, in line with the median forecast in a Bloomberg survey. Monthly inflation accelerated 3.1%, slightly less than expected in a separate poll

- Japanese Prime Minister Fumio Kishida said he would strengthen the economy in a way that makes the most of the weak yen, including encouraging the building of chip and battery factories as well as pushing farm exports

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks were mostly lower as the region failed to shrug off the negative mood following last Friday’s losses on Wall St. and with risk sentiment in Asia also clouded by holiday closures ahead of this week’s key events. ASX 200 was lacklustre with price action contained amid the quasi-holiday conditions in Australia. Nikkei 225 recovered from early weakness and reclaimed the 26,000 level despite the mixed Tankan data in which headline Large Manufacturers’ sentiment worsened for a 3rd consecutive quarter and printed its lowest level since March 2021, although Large All Industry Capex topped forecasts. Hang Seng was choppy in which the index briefly recouped initial losses as the property sector strengthened after the recent announcement by the PBoC to allow some cities to cut mortgage rates for first-time buyers, although the recovery was short-lived amid the absence of mainland participants and Stock Connect flows for a week-long closure.

Top Asian news

- PBoC and other departments issued the overall plan for three pilot areas of inclusive financial reform, according to Reuters.

- BoJ Summary of Opinions stated that Japan’s core consumer inflation is likely to accelerate towards year-end and narrow the pace of increase thereafter, while it added the Bank should maintain monetary easing and that it is desirable to maintain current forward guidance with a dovish bias as the impact of the pandemic is uncertain and inflation is likely to slow next fiscal year and onwards.

- Morgan Stanley Says Likely Fed Pivot Won’t End Earnings Pain

- Hong Kong’s Yuan-Stock-Trading Plan Gets Industry Support

- Emerging-Market Eurobond Sales Drop to 11-Year Low in September