by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSE: UP $28.65 to $1722.05

SILVER PRICE CLOSE: UP $0.51 to $21.04

Access prices: closes

Gold ACCESS CLOSE 1726.20

Silver ACCESS CLOSE: 21.07

New: early yesterday morning//very ominous:

On Monday, October 3, 2022 at 12:15 p.m., a meeting of the Board of Governors of the Federal Reserve System was held under expedited procedures, as set forth in section 261b.7 of the Board’s Rules Regarding Public Observation of Meetings, at the Board’s offices at 20th and C Streets, N.W., Washington, D.C. and by audio/video conference call, to consider the following matters of official Board business.

Bitcoin morning price: $19,945 UP 454

Bitcoin: afternoon price: $20,078 up 587

Platinum price closing UP 29.10 AT $931.70

Palladium price; closing UP $68.85 at $2309/85

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: OCTOBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,692.900000000 USD

INTENT DATE: 10/03/2022 DELIVERY DATE: 10/05/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 4

118 C MACQUARIE FUT 6

323 H HSBC 25

624 C BOFA SECURITIES 7

624 H BOFA SECURITIES 7

657 C MORGAN STANLEY 5 20

657 H MORGAN STANLEY 3

661 C JP MORGAN 123

686 H STONEX FINANCIA 155

732 C RBC CAP MARKETS 5 3

800 C MAREX SPEC 39 27

845 C GOLDMAN SACHS C 1

880 C CITIGROUP 11 33

880 H CITIGROUP 36

TOTAL: 255 255

MONTH TO DATE: 20,896

JPMORGAN STOPPED 123/255

GOLD: NUMBER OF NOTICES FILED FOR OCT CONTRACT: 255

255 NOTICES FOR 25500 OZ //.7932 TONNES

total notices so far: 20,896 contracts for 2,089,600 oz (64.995 tonnes)

SILVER NOTICES: 24 NOTICES FILED FOR 120,000 OZ/

total number of notices filed so far this month 82 : for 410,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $28.85

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: //// A DEPOSIT OF 3,19

TONNES FROM THE GLD/

INVENTORY RESTS AT 942.89 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $0.51

AT THE SLV// ://NO CHANGES IN SILVER INVENTORY AT THE SLV//:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 480.917 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GIGANTIC SIZED 2,697 CONTRACTS TO 30,079 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE HUGE GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR HUGE $1.46 GAIN IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $1.46) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC SILVER LONGS AS WE HAD AN ATMOSPHERIC GAIN OF 5832 CONTRACTS ON OUR TWO EXCHANGES. WE DID HAVE ATTEMPTED SPEC SHORT COVERINGS WITH THE BANKERS CONTINUALLY ON THE BUY SIDE ALONG WITH NEWBIE SPEC LONGS.

WE MUST HAVE HAD:

I) CONTINUAL SPECULATOR SHORT COVERINGS ////CONTINUED BANKER OI COMEX ADDITIONS ///NEWBIE SPEC LONG ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GIGANTIC ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.580 MILLION OZ FOLLOWING A 200,000 OZ QUEUE JUMP / // V) GIGANTIC SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: –77

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTRACTS for 2 days, total 3108 contracts: 15.540 million oz OR 5.180MILLION OZ PER DAY. (1036 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 15.54 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 15.54 MILLION OZ INITIAL

RESULT: WE HAD A GIGANTIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2697 WITH OUR STRONG $1.46 GAIN IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A GIGANTIC SIZED EFP ISSUANCE CONTRACTS: 3058 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER ADDITIONS A// ATTEMPTED SHORT LIQUIDATIONS//INITIAL NEWBIE SPEC LONG ADDITIONS// /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR OCT. OF 1.580 MILLION OZ FOLLOWED BY TODAY’S 200,000 QUEUE JUMP .. WE HAD A GIGANTIC SIZED GAIN OF 5832 OI CONTRACTS ON THE TWO EXCHANGES FOR 29.160MILLION OZ..

WE HAD 24 NOTICE(S) FILED TODAY FOR 120,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 5951 CONTRACTS TO 437,975 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED — -248 CONTRACTS.

.

THE STRONG SIZED INCREASE IN COMEX OI CAME WITH OUR GAIN IN PRICE OF $20.70//COMEX GOLD TRADING/MONDAY // ATTEMPTED SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR OCT. AT 66.099 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 11,500 OZ//NEW STANDING 66.516 TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $20.70 WITH RESPECT TO MONDAY’S TRADING

WE HAD A VERY STRONG SIZED GAIN OF 9488 OI CONTRACTS 29.511 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3785 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 437,727

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 9488 CONTRACTS WITH 703 CONTRACTS INCREASED AT THE COMEX AND 3785 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 9736 CONTRACTS OR 30.283 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3786) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (5703): TOTAL GAIN IN THE TWO EXCHANGES 9,488 CONTRACTS. WE NO DOUBT HAD 1) ATTEMPTED SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS///NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 66.099 TONNES FOLLOWED BY TODAY’S 11,500 OZ QUEUE JUMP///NEW STANDING 66.516 TONNES//. 3) ZERO LONG LIQUIDATION //// //.,4) STRONG SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT. :

7511 CONTRACTS OR 751,100 OZ OR 23.36 TONNES 3TRADING DAY(S) AND THUS AVERAGING: 2503 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAY(S) IN TONNES: 23.36 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 23.36/3550 x 100% TONNES 0.64% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 23.36 TONNES INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER,ROSE BY A GIGANTIC SIZED 2697 CONTRACT OI TO 130,079 AND FURTHER FROM TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 3058 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 3058 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3058 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2697 CONTRACTS AND ADD TO THE 3058 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN ATMPSPHERIC SIZED GAIN OF 5755 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 28.775 MILLION OZ

OCCURRED WITH OUR GAIN IN PRICE OF $1.46

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED //Hang Seng CLOSED /The Nikkei closed UP 776.42PTS OR 2.96% //Australia’s all ordinaires CLOSED UP 3,74% /Chinese yuan (ONSHORE) closed //OFFSHORE CHINESE YUAN UP 7.0748// /Oil UP TO 84.72 dollars per barrel for WTI and BRENT AT 90.25 / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 5703 CONTRACTS TO 437,975 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS STRONG COMEX INCREASE OCCURRED WITH OUR RISE IN PRICE OF $20.70 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (3785 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF OCT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3785 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :3785 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3585 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG SIZED SIZED TOTAL OF 9,488 CONTRACTS IN THAT 3785 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI GAIN OF 5,703 CONTRACTS..AND THIS VERY STRONG GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR HUGE RISE IN PRICE OF GOLD $20.70//WE HAD SPEC SHORT DESPERATELY TRYING TO COVER WITH BANKERS TAKING THE BUY SIDE. IT IS BECOMING EXTREMELY DIFFICULT FOR OUR SHORTERS. TODAY WAS A HUGE DAY FOR GOLD AS SPECS COULD NOT FIND MANY CONTRACTS FROM WHICH TO COVER BUT THE BANKERS KNOWING THE STATE OF THE ECONOMY CONTINUES TO PILE ONTO THE BUY SIDE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING OCT (66.516),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 66.516 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $20.70) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A VERY STRONG SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 9,736 CONTRACTS // WE HAVE REGISTERED A HUGE GAIN OF 9,736 PAPER TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR OCT. (66.516 TONNES)…THIS WAS ACCOMPLISHED DESPITE ATTEMPTED SPECULATOR SHORT COVERING

WE HAD -248 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 9488 CONTRACTS OR 948,800 OZ OR 29.511 TONNES

Estimated gold volume 197,705// poor//

final gold volumes/yesterday 226,801/ fair

INITIAL STANDINGS FOR OCT ’22 COMEX GOLD //OCT 4

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 10,704.640 oz Brinks HSBC |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 18,560.923 oz |

| No of oz served (contracts) today | 255 notice(s) 25500 OZ 0.7932 TONNES |

| No of oz to be served (notices) | 489 contracts 48,900oz 1.5209 TONNES |

| Total monthly oz gold served (contracts) so far this month | 20,896 notices 2,089,600 64.995 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

customer withdrawals: 2

i) Out of Brinks: 2,668.840 oz

ii) Out of HSBC: 8036.100 oz

total: 10,704.64 oz

total in tonnes: 0.3329 tonnes

Adjustments: 1

JPM: dealer to customer; 65,978.537 0z

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCT we have an oi of 744 contracts having LOST 697 contracts . We had 813 contracts

filed on Monday, so we gained 115 contracts or an additional 11,500 oz will stand in this active delivery month of Oct.

We will gain gold oz standing on each and every trading day from this day forth until the conclusion of October.

(remember that queue jumping is really EFP’s exercised from London for gold underwritten by COMEX based bankers)

November GAINED 63 contracts to stand at 2201

December GAINED 3999 contracts UP to 383,396

We had 255 notice(s) filed today for 25,500 oz FOR THE OCT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 255 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 123 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT /2022. contract month,

we take the total number of notices filed so far for the month (20,896) x 100 oz , to which we add the difference between the open interest for the front month of (OCT 744 CONTRACTS) minus the number of notices served upon today 255 x 100 oz per contract equals 2,138,500 OZ OR 66.516 TONNES the number of TONNES standing in this active month of OCT.

thus the INITIAL standings for gold for the OCT contract month:

No of notices filed so far (20,896) x 100 oz+ (744) OI for the front month minus the number of notices served upon today (255} x 100 oz} which equals 2,138,500 oz standing OR 66.516 TONNES in this NON active delivery month of OCTOBER.

TOTAL COMEX GOLD STANDING: 66.516 TONNES (A HUMONGOUS STANDING FOR OCT (GENERALLY THE POOREST DELIVERY MONTHS FOR AN ACTIVE MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,057,668.110 oz 64.00 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 26,307,668.126 OZ

TOTAL REGISTERED GOLD: 13,027,021.189 OZ (405.199 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 13,280,646.87 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,969,353 OZ (REG GOLD- PLEDGED GOLD) 341.19 tonnes//rapidly declining

END

SILVER/COMEX

OCT 4//INITIAL OCT SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2,578,755.646 oz Brinks CNT Delaware HSBC JPMorgan Manfra Loomis |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,688,124.036 oz Delaware CNT JPMorgan |

| No of oz served today (contracts) | 24 CONTRACT(S) 15=20,000 OZ) |

| No of oz to be served (notices) | 274 contracts (1,370,000 oz) |

| Total monthly oz silver served (contracts) | 82 contracts 410,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 3 deposits into the customer account

i) Into Delaware: 523m850.363 oz

ii) Into CNT: 600,418.810 oz

iii) Into JPMorgan 563,854.853

Total deposits: 1,688,124.036 oz

JPMorgan has a total silver weight: 161.99million oz/312.168million =51.88% of comex

Comex withdrawals: 7 (vaults very busy/demand high)

i)Out of CNT 171,878,885 oz

ii)Out of Brinks: 1,316,038.490 oz

iii) Out of Delaware 4001.231 oz

iv) Out of HSBC: 30,468.980 oz

v) JPMorgan: 189,602.100 oz

vi) Out of Manfra: 585,968.400 oz

vii) Out of Loomis: 80,797.560 oz

total withdrawals: 2,578,755.646 oz

adjustments: // 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 41.112 MILLION OZ (declining rapidly)

TOTAL REG + ELIG. 312.168 MILLION OZ (also declining)

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF OCT OI: 298 CONTRACTS HAVING GAINED 37 CONTRACTS.

WE HAD 3 NOTICES FILED ON MONDAY SO WE GAINED 40

SILVER CONTRACTS OR AN ADDITIONAL 200,000 OZ WILL STAND FOR OCT.

NOVEMBER LOST 12 CONTRACTS TO STAND AT 271

DECEMBER SAW A GAIN OF 1973 CONTRACTS UP TO 113,456

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 24 for 120,000 oz

Comex volumes:81,613// est. volume today// good

Comex volume: confirmed yesterday: 65,273 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 82 x 5,000 oz = 410,000 oz

to which we add the difference between the open interest for the front month of OCT(298) and the number of notices served upon today 24 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT./2022 contract month: 82 (notices served so far) x 5000 oz + OI for front month of OCT (298) – number of notices served upon today (24) x 5000 oz of silver standing for the OCT contract month equates 1,780,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:69,131// est. volume today// fair

Comex volume: confirmed yesterday: 101,687contracts ( strong)

END

GLD AND SLV INVENTORY LEVELS

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

SEPT 21/WITH GOLD UP $4.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.79 TONNES FROM THE GLD///INVENTORY RESTS AT 952.16 TONNES

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

SEPT 13/WITH GOLD DOWN $22.85 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73ONNES FROM THE GLD////INVENTORY RESTS AT 964.91 TONNES

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

GLD INVENTORY: 942.89 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

SEPT 21/WITH SILVER UP 33 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.902 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 482.115 MILLION OZ//

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

SEPT 13/WITH SILVER DOWN $.31 TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.899 MILLION OZ//

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

CLOSING INVENTORY 480.917 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Central banks continue to add gold to their official reserves as they know that their number is up

(Peter Schiff)

Central Banks Add Gold For Fifth Straight Month

TUESDAY, OCT 04, 2022 – 06:30 AM

Central banks globally added to their net gold holdings for the fifth consecutive month in August, according to the latest data released by the World Gold Council.

On net, central banks added 20 more tons of gold to their reserves. Three banks drove buying in August and there were no notable sellers.

So far this year, central banks have added over 300 tons of gold to their goldings.

Turkey was the biggest buyer in August and has added more gold than any other country in 2022 to date. With its 8.9-ton purchase in August, Turkey has increased its gold reserves by 84 tons year-to-date. Turkey now holds 478 tons of gold between its central bank and treasury holdings, the highest level since Q2 2020.

Uzbekistan added 8.7 tons to its reserves in August, roughly the same amount as the previous five months. This brings its y-t-d net purchases to over 19 tons despite having begun the year by selling almost 25 tons in the first quarter. Gold reserves account for just over 60% of Uzbek’s total reserves.

After being the only notable seller in July, Kazakhstan bought 2 tons of gold in August. Total Kazakh gold reserves stand now just shy of 375 tons, down almost 28 tons since the start of the year. It is not uncommon for banks that buy from domestic production – such as Uzbekistan and Kazakhstan – to switch between buying and selling.

Mexico and Serbia both made small 0.1-ton purchases in August.

Qatar was the biggest gold buyer in July with an addition of 14.8 tons added to its reserves. Preliminary data published by the Qatar Central Bank suggests a further addition to its gold reserves during August, but the data has not been reported but the IMF IFS database. The WGC said it decided to exclude the Qatar purchase from their data until the IMF reports the official numbers.

India’s lack of gold purchases in August was notable. India had been buying gold consistently for months. India now owns 781 tons of gold, ranking it as the ninth largest gold-holding country in the world. Since resuming buying in late 2017, the Reserve Bank of India has purchased over 200 tons of gold. In August 2020, there were reports that the RBI was considering significantly raising its gold reserves.

Central banks purchase a net 270 tons of gold through the first half of the year. This fell in line with the five-year H1 average of 266 tons.

“This is a continuation of the strong buying that we saw last year and we now expect full-year central bank demand for 2022 to be on a par with 2021 levels,” a World Gold Council report said.

Central banks added 463 tons of gold to global reserves in 2021. That was 82% higher than in 2020.

A WGC survey found that “gold’s performance during a time of crisis and its role as a long-term store of value/inflation hedge are key determinants in the decisions of central banks to hold it.”

Last year was the 12th consecutive year of net purchases. Over that time, central banks have bought a net total of 5,692 tons of gold.

After record years in 2018 and 2019, central bank gold-buying slowed in 2020 with net purchases totaling about 273 tons. The lower rate of purchases in 2020 was expected given the strength of central bank buying both in 2018 and 2019. The economic chaos caused by the coronavirus pandemic has also impacted the market.

Central bank demand came in at 650.3 tons in 2019. That was the second-highest level of annual purchases for 50 years, just slightly below the 2018 net purchases of 656.2 tons. According to the WGC, 2018 marked the highest level of annual net central bank gold purchases since the suspension of dollar convertibility into gold in 1971, and the second-highest annual total on record.

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

MATHEW PIEPENBURG

The Fed’s Strong Dollar Policy: A Recipe For Systemic Implosion

TUESDAY, OCT 04, 2022 – 07:20 AM

Authored by Mathew Piepenburg via GoldSwitzerland.com,

From Main Street USA to the village corners and central banks of Europe, Japan and elsewhere, the Fed’s strong USD policy is backfiring—big time. Just ask the Brits…

Having spent years creating the inflation (QE1 to unlimited QE, Repo bailouts, massive money supply expansion, and an historical wealth transfer from an inflated, Fed-driven stock market), the Fed will be cleaning up its own inflation mess on the backs of the U.S. working class and its other global “allies” while blaming the CPI inflation on Putin, Covid and climate change.

How’s that for rigged to fail?

But that’s just the beginning, and it’s not just about the USA.

Engineering a Recession Powell Can’t Control

By raising rates into what we all know is a recession, Powell, who delusionaly pretends to be Volcker re-born, wants to solve the inflation he helped create by engineering a demand-crippling recession which he thinks he can control, but can’t and won’t.

And this will be the mother of all recessions, as there is an historical and concomitant debt (and hence currency) crisis in every corner of the globe ($300T+) as well as every corner of the nation ($90T+(USA )/harvey), from the toxic corporate bond market and over-strapped households to a grotesquely bloated ($30T+ USA/harvey) government debt market.

Keep It (Horribly) Simple

It’s all horribly simple, in fact.

If debt is the everywhere-driver of the economy and markets, then any significant increase in the cost of that debt will destroy every corner of that economy and those markets, from zombie enterprises to negative yielding US Treasuries.

Powell’s hawkish stance will lead to anything but a “contained recession,” which the Fed will be no less effective “containing” as they were in “containing” their so-called “transitory inflation.”

Rising rates will cripple nearly every asset but the artificially inflated USD until all savings are gone, most citizens are hand-out dependent, and most markets and currencies are on their knees.

At that point, Uncle Sam will either default on the IOU’s (Treasury bonds) which no one will want, or the Fed will pivot to more mouse-click money to buy/support his debt addiction, following the recent example in the UK.

And since the US is too arrogant to fail/default (TAF), the Fed’s only stupid choice left among a long history of stupid, will be a gold-boosting QE pivot.

When?

Yes, An Inevitable Pivot

So, again, when will Powell pivot?

After the pain, politics and panics have reached levels the US and global economy and markets haven’t seen since the FDR era, Powell will throw in the towel and pivot.

In the interim, the US (as well as global) middle class can thank Greenspan, Bernanke, Yellen and Powell for all the pain ahead, as it is the direct (and I mean direct) result of years of unprecedented drunken free money and bloated debt, the hangover for which is going to be a record-breaking B!c7%…

A Treasury Market on the Cliff’s Edge

Investors are forgetting that not only is Hawkish Powell raising rates into a debt bubble, he’s slowly tightening the Fed’s balance sheet, which just means dumping more Treasury supply into a demand-less sovereign bond market.

And this supply stream means bonds will fall even further and hence their yields (and interest rates) will keep rising, thereby by adding massive insult to an already fatally injured credit/debt market.

I feel that when UST’s start to tank en masse, Powell’s fantasy of being the next Volcker will end and the pivot toward money printing will be fast and furious—sending precious metals to record highs.

But until then, buckle up.

Powell’s Master Dollar Plan—Foreign Suckers

For now, Powell’s plan is to let rates, yields and hence the dollar rise, in the hopes that the Greenback will be the only place left for global investors (suckers) to hide, which is where they are indeed beginning to hide.

It’s only a matter of time, however, before foreign investors, nostalgic for the days of former US glory, realize that such glory is gone, and that the only way UST’s will ever be “risk-free-return” is if the Fed prints more debased money to buy them, which is not Powell’s current practice.

In essence then, foreigners aren’t hiding in “risk-free-return,” but drowning in “return-free-risk” as even 3-4% yields on the US 10Y Treasury yield a negative -5% return when adjusted for inflation, despite it being under-reported by 50%.

Remember when I said the Fed has no good options left? I meant it. It’s either tighten and risk systemic collapse, or ease and destroy the currency.

Pick your poison.

Furthermore, and ironically, the USD (i.e., world reserve currency) is highly illiquid, despite being mouse-clicked for years. For this USD scarcity, and the immense pressure it is putting on USD-denominated debt holders and sovereign financial partners, we can thank that other poison known as the quadrillion-dollar derivatives market, of which I’ve already written.

Losing Faith in Uncle Sam’s IOU’s

At some point, Americans, as well as the rest of the world, will realize that the US is not what she used to be, and neither are her IOU’s.

For the first time in almost a century, faith in Uncle Sam will reach a nadir and precious metals their apex. But faith, as I’ve also written, is a hard financial indicator to time.

This is not “gold-bug” posturing but hard math and political reality colliding with the lessons of current and past history.

Take the Pathetic Example of Japan

The Fed’s rate hikes have pushed Tokyo and its Yen to its knees.

The Bank of Japan, unlike the controllers of the world reserve currency (i.e., the Fed), flatly cannot afford to raise rates and pay its JGB’s (i.e., IOU’s) at the same time.

Net result?

The Bank of Japan is printing Yen like gangbusters and keeping inflation deliberately above interest rates.

Yet even in this openly negative-real-yield nightmare, the Japanese 10Y didn’t trade for 2 days.

Meanwhile, as the Yen dropped to 50-year lows, Japan was forced for the first time in nearly three decades to prop its currency by making a direct intervention in the FOREX, which entails selling a batch of the UST’s it had on reserve.

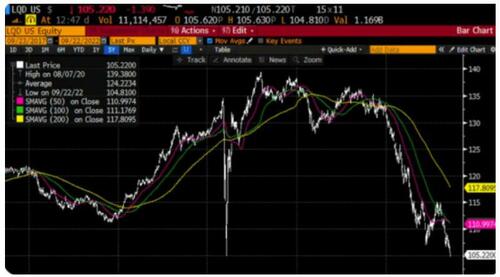

This explains why the TLT (US Treasury ETF) lost 3% on the same day. Meanwhile, US junk bonds (as measured by the LQD ETF), fell to lows not seen since the COVID lows.

Tanking junk bonds, by the way, are typically leading indicators for tanking equity markets.

Just saying…

And Then There’s the EU…

Japan, of course, won’t be the last nation to reach such desperate levels, and as more UST’s are dumped/sold, debt costs in the US will only get more, not less painful, regardless of what the Wizard of Powell does from DC/Oz.

Again, just ask the Bank of England and its recent, headline-making pivot to more QE. No shocker at all there…

Foreigners own over $18T is USD assets, including bonds, real estate and dollars. Once the distressed selling starts, it goes from slow to rapid very quickly, which means pain levels for Main Street American debtors will rise equally fast.

Other nations “friendly” to the US are feeling equal pain from Powell’s hawkish Fed and strong USD.

Germany, for example, is seeing yields on its two-year bonds above 2% for the first time since 2008, an otherwise once anemic rate which it literally can’t afford.

As yields in the EU rise as a result of its US “ally’s” policies, the EU starts to quiver and shake, as this means the EU’s interest rates rise too.

But with debt-soaked countries like Italy teetering towards Frankenstein levels, Powell is pushing the EU into a national security (currency and debt) trap as well as political crack-up.

Again, what will EU nations do?

They’ll likely turn Japanese and start dumping US Treasuries and dollars to keep the lights on from Paris to Portugal.

Even in China, big firms are already selling USD assets and commercial real estate (over $20B since 2019) at an increasingly alarming rate.

Powell’s Strong Dollar Policy is Backfiring

In short, Powell’s strong USD policy, like the West’s sanctions against Putin, are openly backfiring as America’s “allies” bend under the oppressive ripple effects and weight of an artificially strong USD—and all of this as the EU heads into a winter with less energy from the East.

Then again, the Fed is always at least two to three steps behind its own learning curve.

As a political rather than independent bank, they can only rely on words and distortions rather than math and honesty when speaking to a public which they have mis-served since the day of their official (and Wall-Street-leaning) birth in December of 1913.

These converging currency, debt and energy patterns look like the weather map of a perfect storm.

In short, foreign currencies, suffocating under the weight of Powell’s strong USD, will continue to tank as global bond markets continue to dry up and hence implode.

Unless the Fed reverses course on its strong USD policy (and pivots to more QE/Mouse-click “magic”), global markets face a legitimate risk of systemic collapse.

But then again, more mouse-click money just means a currency crisis. Again: Pick your poison.

For all of these reasons, I remain steadfast that global currency and sovereign debt markets cannot and will not last long under Powell’s current strong USD policy.

Unless the Fed pivots to more pathetic QE (and hence a weaker, debased USD), the systemic risk discussed above will become systemic implosion.

For now, the ball (or dollar) is in Powell’s court, and he’s got a weak serve.

end

Lawrie Williams

END

3.Chris Powell of GATA provides to us very important physical commentaries

Foolish Erdogan!! Turkish official inflation tops 83% (unofficial around 200%) while Erdogan promises more interest rate cuts.

A recipe for failure.

(London’sFinancial Times/GATA)

Turkish inflation tops 83% as Erdogan promises more interest rate cuts

Submitted by admin on Mon, 2022-10-03 12:07Section: Daily Dispatches

By Laura Pitel

Financial Times, London

Monday, October 3, 2022

Turkey’s official inflation rate climbed to a new 24-year high last month as the country reeled from President Recep Tayyip Erdoğan’s unorthodox economic policy.

The consumer price index rose 83.45 per cent in September, according to data from the Turkish Statistical Institute, the highest level since July 1998 and up from 80.21 per cent the previous month. …

Erdogan rejects the established economic consensus that raising interest rates helps to curb inflation.

He has ordered the central bank to cut borrowing costs twice in the past two months, bringing the benchmark interest rate down to 12%.

Last week he said he wanted the main rate to come down to single digits by the end of the year as he pushes for growth ahead of critical elections that are due to take place in June 2023.

“My biggest battle is against interest. My biggest enemy is interest,” Erdoğan said in televised remarks. “We have now lowered the interest rate to 12%. Is that enough? It is not enough. This needs to come down further.” …

… For the remainder of the report:

https://www.ft.com/content/d6b86397-5b1a-4f54-a21d-786da4b0abc9

END

Governments around the world will try to intervene to stem the dollar’s rise. The USA is weaponizing the dollar against emerging nations and of course Russia

(Bloomberg/GATA)

Relentless dollar rally raises chance of interventions, investors say

Submitted by admin on Mon, 2022-10-03 09:54Section: Daily Dispatches

Not much more would need to be done than to end the longstanding interventions against gold.

* * *

By Liz McCormick, Simon White, and Matt Turner

Bloomberg News

Sunday, October 2, 2022

The U.S. dollar is expected to extend its gains, increasing speculation that governments will stage unusual market interventions to drive up the value of the currencies on the losing end of the trade.

About 45% of 795 respondents to the latest MLIV Pulse survey expect an orchestrated attempt by major world powers to weaken the dollar, even though the U.S. has moved to tamp down talk of such a move. Nearly as many said they expect Japan to step up its pricey efforts to shore up the yen by itself, without the support of others. Two thirds of respondents see the Bloomberg dollar spot index climbing to new highs over the next month. …

The dollar has surged as international investors seize on higher U.S. interest rates or seek a haven from market turmoil, including in crisis-ridden UK and emerging markets. The rally is exaggerating the economic difficulties of nations around the world by pushing up prices of imported food and fuel.

That is putting further pressure on many central banks, which have been raising interest rates in an effort to tamp down the surge in consumer prices. …

… For the remainder of the report:

END

For your interest…

USAGold’s October letter finds some encouragement for the monetary metal

Submitted by admin on Mon, 2022-10-03 10:17Section: Daily Dispatches

10:17a ET Monday, October 3, 2022

Dear Friend of GATA and Gold:

USA Gold’s October edition of its “News & Views” letter begins by asserting that “finding an encouraging word on the gold and silver markets isn’t easy” — and with heroic diligence proceeds to find a bunch of encouraging words.

The October edition is posted in the clear at USAGold here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

4. OTHER GOLD/SILVER COMMENTARIES

PHYSICAL SILVER/GOLD

5.OTHER COMMODITIES: COAL

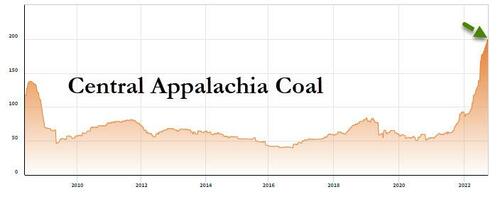

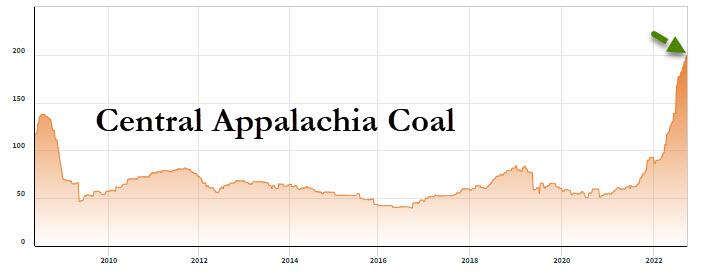

USA coal prices soar above 200$ per tonne amid the energy crunch

(zerohedge)

US Coal Prices Soar Above $200 Amid Energy Crunch

MONDAY, OCT 03, 2022 – 08:40 PM

US natural gas production will need to increase to maintain soaring liquefied natural gas (LNG) exports while ensuring adequate domestic supplies for households and businesses this winter. If not, then electricity generators at power plants will find NatGas uneconomical to run turbines and switch to coal-fired generators. That’s precisely what could be happening as US coal prices soar over the $200 per ton mark for the first time.

Bloomberg said spot coal prices for the week ending Sept. 30 increased to $204.95 per ton. Data was sourced from US Energy Information Administration, which said this was the highest price in records dating back to 2005.

The energy-market shockwaves from Russia’s invasion of Ukraine and rejiggering of Europe’s energy supply chain have dramatically increased US LNG exports to the EU this summer and fall. Domestic supplies have significantly tightened the availability for large users, which has pressured prices higher.

As a result, the once-mighty coal industry is returning as the global (in China and Europe) NatGas-to-coal switching could be set to intensify. The rise in coal prices may suggest stockpiling by utilities ahead of a cold winter.

Rising spot coal prices have been favorable for big coal companies: Peabody Energy Corp shares rose 6% to $26.25, and Arch Resources Inc. jumped 7.5% to $127.49. Both coal stocks have been in a lateral formation for much of this year and could break out to the upside if coal prices continue to rise.

The rally in spot coal and coal mining stocks comes under the most progressive White House ever that attempts to kill the fossil fuel industry to decarbonize the power grid with unreliable renewable power sources that have backfired. Worse, US-led sanctions against Russia have further sparked global energy market chaos.

Coal’s comeback is a remarkable turnaround for an industry that was on the brink of disaster as banks halted financing and investment firms divested from mines and coal-fired power plants, though some of this has been reversed ahead of what’s expected to be a cold and expensive winter.

Increasing coal generation could be a move to help offset some of the power bill pains millions of Americans are facing as NatGas prices send electricity prices higher.

There’s one shocking figure by the National Energy Assistance Directors Association that shows about 20 million households across the country have already fallen behind on their utility bills.

Perhaps it’s time to suspend Biden’s decarbonization efforts to protect American families that could be financially slaughtered by energy hyperinflation if NatGas prices were to soar even more.

We don’t believe coal will be a long-term solution for grid stability. Instead, we’ve reminded readers that nuclear could be a big winner in the years ahead.

end

COMMODITIES IN GENERAL/

END

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED

OFFSHORE YUAN: 7.0748

SHANGHAI CLOSED:

HANG SENG CLOSED

2. Nikkei closed UP 776.42 PTS OR 2.96%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 111/12/Euro RISES TO 0.98913

3b Japan 10 YR bond yield: FALLS TO. +.225/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 144.83/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: XX -// OFF- SHORE: UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.8255%***/Italian 10 Yr bond yield FALLS to 4.196%*** /SPAIN 10 YR BOND YIELD FALLS TO 2.98%…** DANGEROUS

3i Greek 10 year bond yield RISES TO 4.56//

3j Gold at $1706.70//silver at: 20.76 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 23/100 roubles/dollar; ROUBLE AT 58.62//

3m oil into the 84 dollar handle for WTI and 90 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 144.83DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this .9880– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9771well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.589 DOWN 6 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.658 DOWN 5 BASIS PTS//(USA 30 YR INVERTED TO THE USA 10)

USA DOLLAR VS TURKISH LIRA: 18,53…GETTTING DANGEROUS

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Storm Higher After Smaller Than Expected RBA Rate Hike Boosts Speculation Global Tightening Is Ending

TUESDAY, OCT 04, 2022 – 08:11 AM

Yesterday’s furious rally, which following a miserable September and Q3, was the best start to a quarter since 2009 and the best start of a Q4 since 2002 according to Bespoke …

… extended on Tuesday with S&P futures rising as much as 1.9% amid growing bets that we have seen the peak of the Fed’s hawkishness, sentiment which was boosted after the RBA unexpectedly hiked its Cash Rate Target by only 25bps to 2.60%, below the market’s 50bps expectation (having been the first central bank to warn that a pivot is coming a month ago), and sending the AUD and local bond yields tumbling while Australian stocks soared the most in two years! The sudden dovishness reverberated around the world, hammering the dollar for a second day, propelling European higher for the best day since June, sending the two-year Treasury yield plunging below the 4% mark and sending 10Y yields as low at 3.56%, almost half a percent below the 4% reached last Friday. Oil advanced on expectations the OPEC+ alliance will deliver a substantial supply cut.

In premarket trading, major US technology and internet stocks were higher in premarket trading, set to extend their gains for a second straight session. Tesla (TSLA US) joined in on the action, gaining 3% after Cathie Wood bought the carmaker’s dip on Monday. Bank stocks also rallied, putting them on track to gain for a second straight day. Meanwhile, Saudi Arabia appointed BNP Paribas, Citigroup, Goldman Sachs, JPMorgan and Standard Chartered as primary dealers in the government’s local debt instruments. In corporate news, most asset managers that promised to eliminate their financed emissions by 2050 have failed to submit plausible plans toward achieving that goal, according to environmental think tank Universal Owner. here are other notable premarket movers:

- Rivian (RIVN US) rose 9% in premarket trading after the automaker reported a boost in production and reaffirmed its annual goal to build 25,000 electric vehicles.

- Bed Bath and Beyond’s (BBBY US) shares rise as much as 3.3% in premarket trading. WSJ reported late Monday that some of the home furnishings retailer’s bondholders are working with Perella Weinberg Partners ahead of debt talks expected to be held with the company.

- Poshmark (POSH US) jumped as much as 14% in US premarket trading on Tuesday, after South Korea’s Naver agreed to buy the firm in a deal worth $1.2 billion.

- Adeia (ADEA US) jumped as much as 150% in US premarket trading, before paring gain to 24%. The shares are set to extend Monday’s jump on the first day of trading following the completion of the spinoff of TiVo Parent Xperi.

- Shares of cryptocurrency-exposed stocks including Marathon Digital (MARA US) and Coinbase (COIN US) rallied in premarket trading as Bitcoin climbs to breach the closely watched $20,000 level.

The surge started on Monday after investors saw the far weaker-than-estimated US ISM manufacturing data – and especially the biggest drop in the employment index since the covid crash – supporting a dovish tilt at the Fed after 3 percentage points of hikes began to tell on the economy. Money markets now see the Fed Funds Rate peaking below 4.5% by March. And as Bloomberg notes, echoing the above, “speculation is growing that the global wave of disruptive monetary tightening is nearing its end, especially after the Reserve Bank of Australia raised rates by half as much as expected.”

“While the more rational approach outlined by the RBA does not bring forward rate cuts, it offers the possibility of stepping back from the more extreme hawkishness of recent weeks,” Stephen Innes, managing partner at SPI Asset Management, wrote in a note. “That implies bull steepening in bond markets and should provide some support for equity markets if other central banks follow suit.”

As a result of the fresh burst of hope in peak hawkishness, money markets now signal the Fed will hike rates a further 125 basis points at most by March compared with as much as 165 basis points seen following the third three-quarter point increase last month. These pared expectations spurred a rally in Treasuries across the curve on Tuesday. The 10-year rate shed 6 basis points Tuesday, while the two-year yield slid 12 basis points to trade at 3.99%.

In Europe, the Stoxx 600 rallied as travel, technology and retail companies posted some of the biggest gains. Travel, tech and retailers are the strongest-performing sectors. UK domestic stocks outperformed as beaten-down sectors including retail and travel & leisure rebounded. The move, with the domestically-focused FTSE 250 up 2.4%, came as the pound extended gains against the dollar. Chancellor of the Exchequer Kwasi Kwarteng is due to bring forward the announcement of his medium-term fiscal plan. Here are the biggest European movers today:

- European airlines advance, with British Airways owner IAG rising as much as 5.5% after getting an upgrade to buy from hold at Goodbody, while Ryanair gains as much as 5.9% after reporting Sept. load factor data.

- The Stoxx 600 Tech Index rallied as much as 4.2%, the biggest intraday climb since mid-March. Chip stocks were among the biggest gainers, including ASML rising as much as +5.4%, ASM International +6.8%, STMicro +5.3% and Infineon +5.3%.

- Vodafone shares gain as much as 3.3% and extend gains as Oddo BHF upgrades the stock to outperform from neutral, saying the telecom operator’s share price is still at a low, with three transactions being launched and more “on the way.”

- Credit Suisse shares rise as much as 6.0%, recouping most of their losses amid a wider stock market rebound on Monday, after having fallen as much as 12% earlier in the day. The Swiss lender’s gauge of credit risk spiked to a record on Monday, crushing hopes of its CEO to calm markets on capital levels and liquidity.

- HSBC shares rise as much as 3.9%, extending early trading gains, after Sky News reported the bank has instructed JPMorgan to sound out prospective buyers.

- Greggs shares gain as much as 11%, among the top performers in the FTSE 250 Index, after the UK bakery chain said sales grew 14.6% in the third quarter. Jefferies said the update shows “impressive resilience.”

- Private equity firm EQT fall as much 8.2%, the most since June, after Nasdaq Nordic updated its index methodology to divide shareholders into two groups of “strategic investors and non-strategic investors.”

- Rheinmetall shares fall as much as 7.2% after a report that a contract announcement on a key defense program in Australia could be delayed until March.

- M6 shares decline as much as 12% after Bertelsmann’s RTL Group said it will keep its stake in the French TV broadcaster due to “legal risks and uncertainties” around antitrust approval.

- Drax shares suffered decline as much as 7.7%, their biggest intraday drop in nearly two months, after the BBC’s Panorama program said the UK power firm is cutting down “environmentally important” forests.

Earlier in the session, the MSCI Asia Pacific Index rallied 2.2%, poised for their biggest daily advance since March, after weak US manufacturing data trimmed bets on the Federal Reserve’s hawkishness and revived appetite for risk. The MSCI Asia Pacific Index gained as much as 2.4% with all sectors rising. A regional tech sub-gauge jumped more than 3% after Treasury yields slipped and the dollar weakened. Taiwanese chip firms serving Chinese customers got a further boost from a report that the US plans to announce fresh curbs on semiconductor exports to China. Australia’s benchmark led gains in the region after the country’s central bank delivered a smaller-than-expected interest rate hike.

Japanese stocks also surged, with the benchmark Topix rising more than 3%, boosted by technology shares. even after North Korea fired a missile over the country for the first time since 2017. Liquidity in the region was relatively thin as China and Hong Kong markets were closed for a holiday. Despite the latest gains, caution remains over how sustainable any recovery in Asian shares may be. MSCI’s regional gauge is still down 27% this year, partly weighed by China’s strict Covid controls. “Until we see more signs of inflation peaking out in the US, expect the Fed to stay aggressive, for the dollar to continue to climb and Asian stocks to remain under pressure,” said Manish Bhargava, fund manager at Straits Investment Holdings

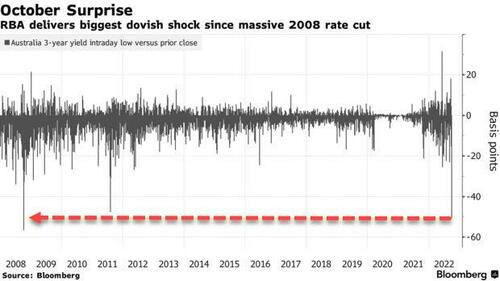

Australian stocks soared the most in two years on RBA’s smaller hike: the S&P/ASX 200 index rose 3.8% to close at 6,699.30 after the RBA surprised investors by raising interest rates by a quarter percentage point, ending a streak of outsized increases. The benchmark notched its biggest gain since June 2020. All sectors climbed, with banks contributing the most to the gauge’s advance. In New Zealand, the S&P/NZX 50 index rose 1.2% to 11,090.03, ahead of the RBNZ’s policy decision on Wednesday. The central bank is poised to raise interest rates by half a percentage point for a fifth straight time, and some economists are tipping it will need to keep tightening well into next year.

Indian stocks posted their biggest advance in more than a month, tracking an extended rally in global equities on hopes of potential easing of hawkish monetary policies by central banks. The S&P BSE Sensex rose 2.3% to 58,065.47 in Mumbai, while the NSE Nifty 50 Index advanced by an equal measure. Shares of financial companies, automobile makers and consumer goods firms were among top gainers in India as the festive season began this week. Local markets will be closed Wednesday for the Dussehra festival. All of the 19 sector sub-indexes compiled by BSE Ltd. gained, led by metal and finance stocks. On the macroeconomic front, India’s trade deficit narrowed for a second straight month in September, mainly due to easing global commodity prices. However, a weakness in the local currency continued to put pressure on the south Asian economy. HDFC Bank and ICICI Bank contributed the most to the Sensex’s gain, increasing 2.8% and 2.3%, respectively. All but three of the 30 shares in the Sensex index advanced.

In FX, the dollar headed for the lowest level since Sept. 22, as the greenback traded weaker against most of its Group-of-10 peers with a rebounding British pound acting as the biggest drag. The UK’s withdrawal of a tax-cut plan soothed nerves about the government’s fiscal health, though doubts remained about the outlook for the currency. Scandinavian currencies led gains while the Aussie was the worst performer. The euro neared a two-week high versus the greenback.

- The pound extended gains against the dollar amid broad-based greenback weakness, rising above $1.14 for the first time in two weeks. Gilts bull steepened with traders also trimming their pricing of BOE hikes.

- The Aussie trimmed losses on the back of a weaker dollar. It earlier fell as much as 1% and the Australian 3-year yield briefly tanked as much as 58bps as the Reserve Bank raised the cash rate to 2.6%, less than the median of 2.85% expected by economists surveyed. Governor Philip Lowe reinforced his commitment to tightening even as he acted on signals last month of a slower pace of increase

- An advance by the New Zealand dollar may be held back by the Aussie’s decline, with RBNZ set to raise interest rates by a half-point Wednesday, to 3.5%

- The yen underperformed the greenback as the second half of Japan’s fiscal year begun. JGBs gained after a solid 10-year auction. Options traders reduce long-gamma exposure in the yen in the front-end given the threat of Japanese intervention in the currency market means dollar bullish calls are no longer in vogue

In rates, treasuries advanced led by the front end and temporarily sending the US 2-year yield below 4% for the first time since Sept. 21, as money markets continued to pare Fed hike wagers. Bunds and Italian bonds bull steepened as money markets continued to pare ECB tightening wagers. Treasuries extended Monday’s bull-steepening move with front-end yields richer by nearly 10bp on the day in early US session. Treasury yield richer by 8bp to 3bp across the curve with 2s10s, 5s30s spreads steeper by ~2bp and ~4bp on the day; 10-year is around 3.58% with gilts trading ~8bp richer in the sector. Gilts lead as BOE rate-hike premium fades further, and Australian front-end surged overnight after RBA surprised with a smaller rate hike than expected. US session features a busy Fed speaker slate. Across front-end UK 2-year yields are richer by 25bp on the day while Aussie 2-year notes closed down more than 30bp after RBA hiked cash rates by 25bp vs 50bp expected. Fed-dated OIS contracts continue to shift to a more dovish policy path, with additional 112bp of hikes now expected over the next two policy meetings vs 115bp at Monday’s close.

In commodities, WTI broke above Monday’s range, adding 1.3% to near $84.94, Brent rose above $90. Spot gold rises roughly $9 to trade near $1,709/oz.

Bitcoin is bid and briefly reclaimed the USD 20k handle, though has since dipped marginally back beneath the figure.

To the day ahead now, and data releases include US factory orders and the JOLTS job openings for August, as well as the final August readings for durable goods orders and core capital goods orders. In the Euro Area, we’ll also get the August PPI reading. From central banks, we’ll hear from ECB President Lagarde, the ECB’s Centeno, as well as the Fed’s Williams, Mester, Jefferson and Daly.

Market Snapshot

- S&P 500 futures up 1.4% to 3,743.25

- STOXX Europe 600 up 2.1% to 399.04

- MXAP up 2.2% to 141.85

- MXAPJ up 1.8% to 458.20

- Nikkei up 3.0% to 26,992.21

- Topix up 3.2% to 1,906.89

- Hang Seng Index down 0.8% to 17,079.51

- Shanghai Composite down 0.6% to 3,024.39

- Sensex up 2.1% to 58,006.25

- Australia S&P/ASX 200 up 3.8% to 6,699.29

- Kospi up 2.5% to 2,209.38

- German 10Y yield little changed at 1.84%

- Euro up 0.5% to $0.9871

- Brent Futures up 0.7% to $89.51/bbl

- Gold spot up 0.4% to $1,707.42

- U.S. Dollar Index down 0.44% to 111.26

Top Overnight News from Bloomberg

- EU internal market chief Thierry Breton and Paolo Gentiloni, the bloc’s economy czar, said the current situation requires solidarity among member states, including the issuance of joint- guaranteed debt similar to what was done during the Covid pandemic

- UK Prime Minister Liz Truss said she’s yet to decide whether welfare payments in the UK should be increased in line with inflation, an issue that threatens to spark another bitter row with her disgruntled Conservative MPs

- Britain’s bond market should comfortably absorb the extra £62 billion of debt announced after the government’s September mini-budget despite undergoing “‘a major repricing,” Reuters reported, citing UK Debt Management Office head Robert Stheeman

- Global stock and bond bulls are hoping the market impact of Australia’s dovish rate surprise will stick as it offers their best chance at arguing the worldwide wave of disruptive hikes is closer to the end than the beginning

- North Korea fired a missile over Japan for the first time in five years, further ratcheting up tensions over Kim Jong Un’s nuclear program and prompting a rare public safety warning to be issued by Tokyo

A more detailed look at global markets courtesy of Newqsuawk

Asia-Pac stocks notched firm gains as the region took impetus from the strong performance on Wall St where stocks rallied amid a decline in the dollar and yields, while equities were unfazed by North Korea’s latest launch. ASX 200 gained at the open as the commodity-related sectors led the broad gains across the index after recent strength in oil and precious metals, while stocks were further boosted after the RBA opted for a smaller than expected rate increase of 25bps. Nikkei 225 advanced closer to the 27k level after the latest Tokyo CPI data printed in line with expectations. KOSPI strengthened despite North Korea’s missile launch which flew over Japan for the first time since 2017 and prompted Japan to issue a warning for residents to take shelter, before landing outside of Japan’s EEZ.

Top Asian News

- China is demanding that foreign diplomats provide floor plans of Hong Kong missions, according to FT.

- Taiwan is to open its border and lift quarantine rules in 10 days, according to the Ministry of Foreign Affairs.

- RBA hiked the Cash Rate Target by 25bps to 2.60% (exp. 50bps hike). RBA stated that the Board is committed to returning inflation to the 2–3% range over time and expects to increase interest rates further over the period ahead. RBA added that today’s increase in interest rates will help achieve this goal and that the Cash Rate had been increased substantially in a short period of time, while the size and timing of future interest rate increases will continue to be determined by the incoming data and the Board’s assessment of the outlook for inflation and the labour market.

- Japan Defends Appointing Premier’s Son as Senior Aide

- What Adding India to Global Bond Indexes Would Mean: QuickTake

- Naver Sinks 9% on Announcing $1.2 Billion Poshmark Deal

- Samsung Woos US Chip Buyers With Tech Advances, Texas Focus

European bourses have commenced the session on the front foot as broader sentiment remains constructive largely in a continuation of yesterday’s recovery. Sectors are all in the green with Travel names outperforming amid Heathrow ending the passenger cap while defensively-biased names lag a touch given broader sentiment. Stateside performance is very in-fitting, ES +1.5%, ahead of Fed speak and after a constructive update from Foxconn. Foxconn (2317 TW) September sales +40.4% YY; Q3 revenue better than expected. Maintain FY22 guidance, as stated in August; Q4 outlook is cautiously positive. Need to closely monitor inflation, demand, COVID and supply chains in the period. September: strong revenue performance in smart consumer electronics products was the main driver of overall revenue; smart consumer electronics, cloud and networking products delivered strong double-digit growth. Apple (AAPL) iPhone exports from India doubling, according to Bloomberg, in a boon to the plan of Indian PM Modi; additionally, exports of India-made iPhones surpass USD 1bln in a five-month period, via ET Now citing sources.

Top European News

- UK PM Truss said abolishing the 45p top rate of tax was a tiny part of the plan and had become an unnecessary distraction, according to The Telegraph.

- German Finance Minister Lindner says they are open to joint steps on the international gas market, prepared to discuss measures to contain gas prices, EU power market needs to be reformed and joint purchases need to be considered.

- EU Economy and Single Market Commissioners have called for joint EU borrowing to deal with the energy crisis.

- EU Chiefs Eye Joint Debt as German Fiscal Force Worries Allies

- Russia Sanctions Germany’s Operator of Katharina Gas Storage

- Rheinmetall Drops on Report of Australian Defense Contract Delay

- Vodafone-Three Merger Set to Be £14 Billion Test for Watchdogs

- Tendam Brands Offering of Senior Secured 2028 Notes for EU300m

- ECB’s de Cos Says Spanish Banks Must Be Cautious Amid Slowdown

Commodities

- Crude benchmarks are modestly bid this morning, taking the lead from broader sentiment and associated FX action.

- Benchmarks are firmer by just shy of USD 1/bbl and towards the top-end of the sessions parameters and more broadly are well within the ranges of the last few days/weeks.

- Precious and base metals have benefited from the pullback in the USD. Lifting spot gold back above USD 1700/oz to a session best USD 10/oz above the figure and bringing the 50-DMA into focus at USD 1723/oz

- Saudi Aramco CEO says they maintain their market within Asia, despite demand from Europe; oil spare capacity is extremely low, market is focused on short-term economics, rather than long-term, via Reuters.

- Trafigura Chief Economist says sees dated Brent oil benchmark price above USD 75bbl at the end of next year, via Reuters.

- US Treasury Official Harris says Russian oil price cap will be high enough to maintain Russian incentive to continue producing; not yet been a decision on the price, via Reuters. December 5th sanctions will target Russian crude, then diesel and lastly lower value products such as Naphtha.

US Event Calendar

- 10:00: Aug. Factory Orders, est. 0%, prior -1.0%

- Factory Orders Ex Trans, est. 0.2%, prior -1.1%

- 10:00: Aug. Durable Goods Orders, est. -0.2%, prior -0.2%

- -Less Transportation, est. 0.2%, prior 0.2%

- Cap Goods Orders Nondef Ex Air, prior 1.3%

- Cap Goods Ship Nondef Ex Air, prior 0.3%

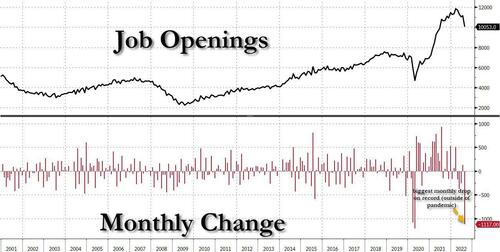

- 10:00: Aug. JOLTs Job Openings, est. 11.1m, prior 11.2m

Central bank Speakers

- 09:00: Fed’s Logan Gives Welcoming Remarks at Event on Technology

- 09:00: Williams Gives Opening/Closing Remarks at Work Culture Event

- 09:15: Fed’s Mester Speaks at Conference on Payment System

- 11:45: Fed’s Jefferson Speaks at Conference

- 13:00: Fed’s Daly Speaks to the Council on Foreign Relations

DB’s Jim Reid concludes the overnight wrap