by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSE: UP $0.70 to $1712.40

SILVER PRICE CLOSE: UP $0.11 to $20.61

Access prices: closes

Gold ACCESS CLOSE 1712.60

Silver ACCESS CLOSE: 20.67

New: early yesterday morning//very ominous:

On Monday, October 3, 2022 at 12:15 p.m., a meeting of the Board of Governors of the Federal Reserve System was held under expedited procedures, as set forth in section 261b.7 of the Board’s Rules Regarding Public Observation of Meetings, at the Board’s offices at 20th and C Streets, N.W., Washington, D.C. and by audio/video conference call, to consider the following matters of official Board business.

Bitcoin morning price: $20,242 UP 164 (from Tuesday)

Bitcoin: afternoon price: $20,035 DOWN 43

Platinum price closing DOWN 5.70 AT $925.50

Palladium price; closing DOWN $31.05 at $2278.80

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/closing ACCESS

CANADIAN GOLD $2355.00 CDN DOLLARS PER OZ UP $18.50 CDN DOLLARS

BRITISH GOLD INPOUNDS: 1534.05 POUNDS PER OZ UP 21.13 BRITISH POUNDS PER OZ/

EURO GOLD: 1748.37 EUROS PER OZ// UP 14.60 EUROS PER OZ///

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: OCTOBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,711.400000000 USD

INTENT DATE: 10/05/2022 DELIVERY DATE: 10/07/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 1

118 C MACQUARIE FUT 33

132 C SG AMERICAS 12

323 H HSBC 6

435 H SCOTIA CAPITAL 341

624 C BOFA SECURITIES 1

624 H BOFA SECURITIES 109

657 C MORGAN STANLEY 4

657 H MORGAN STANLEY 15

661 C JP MORGAN 166

732 C RBC CAP MARKETS 1

800 C MAREX SPEC 9 25

880 C CITIGROUP 7

TOTAL: 365 365

MONTH TO DATE: 21,334

JPMORGAN STOPPED 166/365

GOLD: NUMBER OF NOTICES FILED FOR OCT CONTRACT: 255

365 NOTICES FOR 36500 OZ //1.123 TONNES

total notices so far: 21,334 contracts for 2,133,400 oz (66.357 tonnes)

SILVER NOTICES: 31 NOTICES FILED FOR 155,000 OZ/

total number of notices filed so far this month 253 : for 1,265,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $0.70

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: //// A DEPOSIT OF 3,45

TONNES FROM THE GLD/

INVENTORY RESTS AT 946.34 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $0.11

AT THE SLV// ://BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A HUGE WITHDRAWAL OF 5.300 MILLION OZ FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 475.617 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 3357 CONTRACTS TO 126,167 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE HUGE LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR HUGE $0.54 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.54). HOWEVER OUR SPEC SHORTS ARE DESPARATELY TRYING TO COVER THEIR MASSIVE COMEX OI SHORTFALL. BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS.

WE MUST HAVE HAD:

I) CONTINUAL SPECULATOR SHORT COVERINGS ////CONTINUED BANKER OI COMEX ADDITIONS /// SOME NEWBIE SPEC LONG ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GIGANTIC ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.580 MILLION OZ FOLLOWING A 105,000 OZ QUEUE JUMP / // V) GIGANTIC SIZED COMEX OI LOSS/SPEC COVERING THEIR SHORTS.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: –157

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTRACTS for 6 days, total 49,425 contracts: 29.65 million oz OR 4.94MILLION OZ PER DAY. (823 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 29.65 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.65 MILLION OZ INITIAL

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3357 WITH OUR STRONG $0.54 LOSS IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A GIGANTIC SIZED EFP ISSUANCE CONTRACTS: 1650 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER ADDITIONS A// HUGE SHORT LIQUIDATIONS//SMALL NEWBIE SPEC LONG ADDITIONS// /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR OCT. OF 1.580 MILLION OZ FOLLOWED BY TODAY’S 105,000 QUEUE JUMP .. WE HAD A GIGANTIC SIZED LOSS OF 1747 OI CONTRACTS ON THE TWO EXCHANGES FOR 8.735MILLION OZ..

WE HAD 31 NOTICE(S) FILED TODAY FOR 155,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 3889 CONTRACTS TO 433,176 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED — -1211 CONTRACTS.

.

THE FAIR SIZED DECREASE IN COMEX OI CAME WITH OUR LOSS IN PRICE OF $10.35//COMEX GOLD TRADING/WEDNESDAY // SOME SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR OCT. AT 66.099 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 3,500 OZ//NEW STANDING 68.065 TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $10.35 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A VERY SMALL SIZED LOSS OF 1396 OI CONTRACTS 4.342 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2493 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 433,176

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1396 CONTRACTS WITH 3889 CONTRACTS DECREASED AT THE COMEX AND 2493 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 1396 CONTRACTS OR 04.342 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2678) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (3889): TOTAL LOSS IN THE TWO EXCHANGES 1396 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS///NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 66.099 TONNES FOLLOWED BY TODAY’S 3500 OZ QUEUE JUMP///NEW STANDING 68.065 TONNES//. 3) ZERO LONG LIQUIDATION //// //.,4) FAIR SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT. :

12,507 CONTRACTS OR 1,250,700 OZ OR 38.90 TONNES 6TRADING DAY(S) AND THUS AVERAGING: 2084 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 6 TRADING DAY(S) IN TONNES: 38.90 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 38.90/3550 x 100% TONNES 1.09% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 38.90 TONNES INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A GIGANTIC SIZED 3357 CONTRACT OI TO 126,167 AND FURTHER FROM TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1610 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 1610 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1610 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 3357 CONTRACTS AND ADD TO THE 1610 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED LOSS OF 1747 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 8.735 MILLION OZ

OCCURRED WITH OUR LOSS IN PRICE OF $0.54

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED //Hang Seng CLOSED /The Nikkei closed UP 190.77PTS OR 0.78% //Australia’s all ordinaires CLOSED UP 0.04% /Chinese yuan (ONSHORE) closed //OFFSHORE CHINESE YUAN UP 7.0720// /Oil UP TO 87.32 dollars per barrel for WTI and BRENT AT 93.01 / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 3357 CONTRACTS TO 434,387 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS FAIR COMEX DECREASE OCCURRED WITH OUR FALL IN PRICE OF $10.35 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2493 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF OCT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3785 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :3785 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3585 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY TINY SIZED SIZED TOTAL OF 185 CONTRACTS IN THAT 2493 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 3357 CONTRACTS..AND THIS VERY SMALL LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR FALL IN PRICE OF GOLD $10.35//WE HAD SPEC SHORTS ADDING TO THEIR POSITIONS WITH BANKERS TAKING THE OTHER SIDE AS BUYERS OF COMEX GOLD CONTRACTS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING OCT (68.065),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 68.065 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $10.35) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A VERY TINY SIZED TOTAL LOSS ON OUR TWO EXCHANGES OF 185 CONTRACTS // WE HAVE REGISTERED A SMALL LOSS OF 4.342 PAPER TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR OCT. (68.065 TONNES)…THIS WAS ACCOMPLISHED DESPITE ATTEMPTED SPECULATOR SHORT COVERING

WE HAD -1211 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 1396 CONTRACTS OR 139,600 OZ OR 4.342 TONNES

Estimated gold volume 133,881// poor//

final gold volumes/yesterday 185,989/ poor

INITIAL STANDINGS FOR OCT ’22 COMEX GOLD //OCT 6

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 14,477,295 oz Brinks Delaware HSBC |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | NIL oz |

| No of oz served (contracts) today | 365 notice(s) 36500 OZ 0.7932 TONNES |

| No of oz to be served (notices) | 549 contracts 54,900oz 1.707 TONNES |

| Total monthly oz gold served (contracts) so far this month | 21,334 notices 2,133,400 66.357 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

customer withdrawals: 3

i) Out of Brinks: 96.46 oz 3 kilobars

ii) Out of Delaware: 2604.23 oz 81 kilobars

iii) Out of JPMorgan: 11,776.604 oz

total: 14,477.295 oz

total in tonnes: 0.4502 tonnes

Adjustments: 2

JPM: dealer to customer; 17,361,540 0z

and

Brinks: 5883.633 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCT we have an oi of 914 contracts having GAINED 280 contracts . We had 255 contracts

filed on Wednesday, so we gained 35 contracts or an additional 3500 oz will stand in this active delivery month of Oct.

We will gain gold oz standing on each and every trading day from this day forth until the conclusion of October.

(remember that queue jumping is really EFP’s exercised from London for gold underwritten by COMEX based bankers)

November GAINED 298 contracts to stand at 2793

December lost 6264 contracts down to 374,909

We had 365 notice(s) filed today for 36500 oz FOR THE OCT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 365 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 166 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT /2022. contract month,

we take the total number of notices filed so far for the month (21,334) x 100 oz , to which we add the difference between the open interest for the front month of (OCT 914 CONTRACTS) minus the number of notices served upon today 365 x 100 oz per contract equals 2,188,300 OZ OR 68.065 TONNES the number of TONNES standing in this active month of OCT.

thus the INITIAL standings for gold for the OCT contract month:

No of notices filed so far (21.334) x 100 oz+ (914) OI for the front month minus the number of notices served upon today (365} x 100 oz} which equals 2,188,300 oz standing OR 68.065 TONNES in this NON active delivery month of OCTOBER.

TOTAL COMEX GOLD STANDING: 68.065 TONNES (A HUMONGOUS STANDING FOR OCT (GENERALLY THE POOREST DELIVERY MONTHS FOR AN ACTIVE MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,067,434.605 oz 64.30 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 26,255,834.279 OZ

TOTAL REGISTERED GOLD: 13,003,776.116 OZ (404,447 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 13,252,058.163 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,936,342 OZ (REG GOLD- PLEDGED GOLD) 340.166 tonnes//rapidly declining

END

SILVER/COMEX

OCT 6//INITIAL OCT SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,673,074,.106 oz Brinks CNT Delaware Int Delaware JPMorgan Manfra Loomis |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,211,371/828 oz Delaware HSBC CNT |

| No of oz served today (contracts) | 31 CONTRACT(S) 155,000 OZ) |

| No of oz to be served (notices) | 76 contracts (380,000 oz) |

| Total monthly oz silver served (contracts) | 253 contracts 1,265,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 3 deposits into the customer account

i) Into Delaware: 8124.004 oz

ii) Into CNT: 580,371.460 oz

iii) Into HSBC 623,876.350

Total deposits: 1,211,371.828 oz

JPMorgan has a total silver weight: 161.406million oz/312.735million =51.61% of comex

Comex withdrawals: 7 (vaults very busy/demand high)

i)Out of CNT 10,329.474 oz

ii)Out of Brinks: 7627.02 oz

iii) Out of Delaware 21,870.848 oz

iv) Out of Int Delaware: 101,794.390 oz

v) JPMorgan: 585,464.120 oz

vi) Out of Manfra: 245m225.973 oz

vii) Out of Loomis: 700,762.280 oz

total withdrawals: 1,673,074.106 oz

adjustments: // 1

jpmorgan: dealer to customer 4965.800 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 40.150 MILLION OZ (declining rapidly)

TOTAL REG + ELIG. 312.735 MILLION OZ (also declining)

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF OCT OI: 107 CONTRACTS HAVING LOST 119 CONTRACTS.

WE HAD 140 NOTICES FILED ON WEDNESDAY SO WE GAINED 21

SILVER CONTRACTS OR AN ADDITIONAL 105,000 OZ WILL STAND FOR OCT.

NOVEMBER GAINED 6 CONTRACTS TO STAND AT 405

DECEMBER SAW A LOSS OF 3890 CONTRACTS DOWN TO 108,630

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 31 for 155,000 oz

Comex volumes:81,613// est. volume today// good

Comex volume: confirmed yesterday: 65,273 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 253 x 5,000 oz = 1,265,000 oz

to which we add the difference between the open interest for the front month of OCT(107) and the number of notices served upon today 31 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT./2022 contract month: 253 (notices served so far) x 5000 oz + OI for front month of OCT (107) – number of notices served upon today (31) x 5000 oz of silver standing for the OCT contract month equates 1,645,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:50,721// est. volume today// poor

Comex volume: confirmed yesterday: 84,600contracts ( good)

END

GLD AND SLV INVENTORY LEVELS

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DWEPOSIT OF 3.45 TONNES INTOTHE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

SEPT 21/WITH GOLD UP $4.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.79 TONNES FROM THE GLD///INVENTORY RESTS AT 952.16 TONNES

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

SEPT 13/WITH GOLD DOWN $22.85 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73ONNES FROM THE GLD////INVENTORY RESTS AT 964.91 TONNES

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

GLD INVENTORY: 946.34 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

SEPT 21/WITH SILVER UP 33 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.902 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 482.115 MILLION OZ//

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

SEPT 13/WITH SILVER DOWN $.31 TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.899 MILLION OZ//

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

CLOSING INVENTORY 475.617 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

end

Lawrie Williams

END

3.Chris Powell of GATA provides to us very important physical commentaries

This will be good for the gold price: banks are diverting gold supply from India to China and Turkey

There is not enough gold to supply the gold hungry gang from India

(Reuters)

Banks divert gold supply from India to China and Turkey

Submitted by admin on Tue, 2022-10-04 16:37Section: Daily Dispatches

By Rajendra Jadhav

Reuters

Tuesday, October 4, 2022

MUMBAI — Gold-supplying banks have cut back shipments to India ahead of major festivals in favour of focusing on China, Turkey, and other markets where better premiums are offered, three bank officials and two vault operators told Reuters.

That could create scarcity in the world’s second-biggest market for gold, and force Indian buyers to start paying hefty premiums for supplies in the approaching peak-demand season.

Leading gold suppliers to India — which include ICBC Standard Bank, JPMorgan, and Standard Chartered — usually import more gold ahead of festivals and store it in vaults.

But vaults now hold less than 10% of the gold they did a year ago, the sources said on Tuesday.

“Ideally a few tonnes of gold should be there in vaults during this time of the year. But now we only have a few kilos,” said one Mumbai-based vault official. …

… For the remainder of the report:

END

GATA’s Ed Steer interviewed by Dave Russell of GoldCore

Submitted by admin on Tue, 2022-10-04 21:42Section: Daily Dispatches

9:42p Tuesday, October 4, 2022

Dear Friend of GATA and Gold:

GATA board member Ed Steer, publisher of Ed Steer’s Gold and Silver Digest, is interviewed today by GoldCore’s Dave Russell about the international financial markets, the depression he sees looming ahead, and the potential for the monetary metals and commodities to serve as havens against disaster.

The interview is 28 minutes long and can be heard at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

4. OTHER GOLD/SILVER COMMENTARIES

PHYSICAL SILVER/GOLD

5.OTHER COMMODITIES:

end

COMMODITIES IN GENERAL/

END

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED

OFFSHORE YUAN: 7.0720

SHANGHAI CLOSED:

HANG SENG CLOSED

2. Nikkei closed UP 190.77 PTS OR 0.70%

3. Europe stocks SO FAR: ALL RED

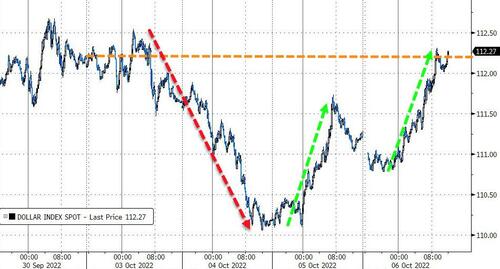

USA dollar INDEX UP TO 111.41/Euro FALLS TO 0.98580

3b Japan 10 YR bond yield: RISES TO. +.244/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 144.68/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: XX -// OFF- SHORE: UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.018%***/Italian 10 Yr bond yield RISES to 3.76%*** /SPAIN 10 YR BOND YIELD RISES TO 3.197%…** DANGEROUS//ECB IS MANIPULATING ITALIAN BOND YIELD DOWN/ALL THE REST UP

3i Greek 10 year bond yield RISES TO 4.705//

3j Gold at $1717.90//silver at: 20.70 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 6/100 roubles/dollar; ROUBLE AT 60.23//

3m oil into the 87 dollar handle for WTI and 93 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 144.68DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this .9842– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9710well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.769 UP 1 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.760 DOWN 1 BASIS PTS//(USA 30 YR INVERTED TO THE USA 10)

USA DOLLAR VS TURKISH LIRA: 18,58…GETTTING DANGEROUS

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

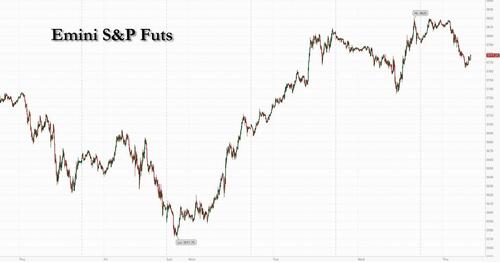

Futures Slide As OPEC+ Cut Sparks Gas Inflation Fears And “Tighter For Longer” Fed

THURSDAY, OCT 06, 2022 – 08:02 AM

Two days ago, when stocks were melting up even as oil was storming higher and threatened to rerate inflation expectations sharply higher, we mused that algos were clearly ignoring this potentially ominously convergence.

And while yesterday we saw the first cracks developing in the meltup narrative as oil extended gains following OPEC’s stark slap on the face of the dementia patient in the White House, it was only today that the “oil is about to push inflation sharply higher” discussion entered the broader financial sphere, with JPM writing this morning that “OPEC+ presents inflation risk”, Bloomberg echoing JPM that “OPEC+ alliance’s plan to cut oil supply stoked inflation fears and as traders awaited labor-market data to gauge the risk of recession” and Saxo Bank also jumping on the bandwagon, warning that OPEC+ supply cut will worsen global inflation which “raises the risk of inflation staying higher for longer” and “sends the wrong signal to the US Federal Reserve… It could send a signal that they have to keep on their foot on the brake for longer.”

And sure enough, with oil rising above its 50DMA for the first time since Aug 30, futures have slumped overnight as oil kept its gains, with S&P and Nasdaq 100 futures both sliding 0.5% as of 730am, while Europe’s Stoxx 600 erased an advance and traded near session lows. US crude futures held on to weekly gains of about 11% after the oil cartel said it would cut daily output by 2 million barrels. Treasuries were steady, the 10Y trading around 3.77%, with the 2Y rate hovering about the 4.15% level.

In pre-market trading, Credit Suisse jumped as much as 5.2% after JPMorgan upgraded to neutral from underweight, saying it sees $15bn as a minimum value for the lender, in-line with the estimated value of the Swiss legal entity. Shares were 2% higher by 13:20pm CET in Zurich, after Bloomberg News reported that the lender is trying to bring in an outside investor to inject money into a spinoff of its advisory and investment banking businesses, citing people with knowledge of the deliberations. Other banks did not do as well, and slumped in premarket trading Thursday, putting them on track to fall for a second straight day. Twitter shares fell as much as 1.1% to $50.75, trading nearly 7% below Elon Musk’s offer price of $54.20 as investors await progress in the revived deal. Here are the other notable premarket movers:

- Pinterest (PINS US) shares jump as much as 5.8% in US premarket trading after Goldman Sachs upgraded the social networking site to buy from neutral on improving user growth and better engagement trends, even as the backdrop for digital advertising remains uncertain.

- Biohaven Ltd. (BHVN US) shares rise 9.7% in US premarket trading, set to extend a 75% gain over the past two days as regular trading in the newly constituted drug developer began following an unusual deal with Pfizer Inc.

- SurgePays (SURG US) shares soar as much as 11% in premarket trading after the company gave an update on subscriber numbers for its subsidiary SurgePhone Wireless.

- Flutter (FLTR LN) gained 3.3% in premarket trading as it was initiated at outperform at Exane as the best-placed online gambling name, while Entain also at outperform and DraftKings started at underperform.

- Richardson Electronics (RELL US) rose 8.2% in extended trading after reporting year-over-year growth in net sales and earnings per share for the fiscal first quarter.

While higher energy prices could stoke inflation, some have speculated that this will also divert discretionary income from core items thus pushing core inflation lower and hit company earnings — potentially encouraging the Federal Reserve to slow monetary tightening.

While such expectations fueled equity gains this week, several money managers are cautioning that the economic path to a less aggressive Fed could be painful: “If you want to preempt the Fed, you are playing a very high-stakes game,” said Kenneth Broux, a strategist at Societe Generale SA. “The Fed do not want financial conditions to loosen; they don’t want equity markets to take off and get too comfortable.”

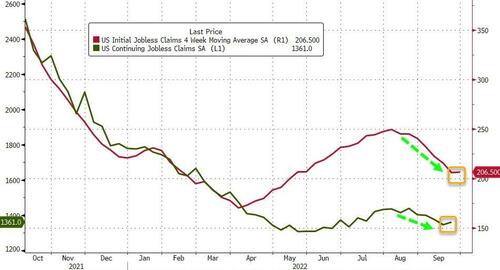

That said, investors are wary of placing large-scale equity bets as they await a report on US initial jobless claims later Thursday and the official nonfarm payrolls data Friday. A Bloomberg survey shows the US economy will have added 260,000 jobs last month; a higher-than-anticipated number may spook markets.

In Europe, the Stoxx 50 dropped -0.3% to session lows. Stoxx 600 outperforms peers, adding 0.2%, FTSE MIB lags, dropping 0.5%. Energy and insurance underperform while real estate and travel lead gains. Here are all the notable European movers:

- Imperial Brands shares rise as much as 4.7% after the tobacco company said it will buy back up to £1b worth of stock. The move was welcomed by analysts, with RBC calling it a “big deal” and Citigroup saying the announcement was earlier than expected.

- Home24 SE gains as much as 126% to EU7.53 after XXXLutz offered to buy all outstanding shares in the German online furniture retailer for EU7.50 apiece. The bid is generous and the deal is straightforward from a regulatory perspective, according to Tradition.

- Credit Suisse jumps as much as 5.2% after JPMorgan upgraded to neutral from underweight, saying it sees $15b as a minimum value for the lender, in-line with the estimated value of the Swiss legal entity.

- CMC Markets climbs as much as 6.5% after the online trading firm said it sees first- half net operating income up 21% y/y, with market volatility in August and September boosting the results. Numis upgraded the stock to add from hold following the report.

- Shell drops as much as 5% as analysts say the oil and gas major’s trading update looks “weak” and may mean that FY consensus proves too ambitious.

- Kloeckner falls as much as 12% as the company faces a “high likelihood” of an imminent profit warning, Bankhaus Metzler says, double-downgrading the stock to sell from buy.

- Swiss Re is among the weakest members of the Stoxx 600 insurance index on Thursday, declining as much as 4.0%, as Morgan Stanley lowers its price target ahead of third-quarter earnings.

- Accor drops as much as 2.5% after the hotel chain owner was downgraded to underweight from equal-weight at Barclays, which sees short-term risks as bigger for the company compared with peers and feels investors are looking more at potential negative factors heading into FY23 than 2022 upgrades.

Earlier in the session, Asian stocks rose for a third day as hardware technology stocks in South Korea and Japan advanced on views they may have reached a bottom. The MSCI Asia Pacific Index climbed as much as 0.9%, lifted by TSMC, SoftBank and Sony. The benchmark trimmed gains later in the day, but remains on track to advance for the week, following a seven-week losing streak that was the longest since 2015.Korea’s Kospi Index was the region’s best-performing major benchmark, jumping about 1%. The advance was helped by chipmakers extending their gains amid Morgan Stanley’s bullish view on the sector. Hong Kong stocks retreated after Wednesday’s catch-up rally.

Trading volume in the region was light as mainland China remains closed for the Golden Week holiday. The MSCI’s Asian benchmark has rebounded this week from its lowest in more than two years. The move tracked a nascent revival in global equities on bets that the Federal Reserve may turn less aggressive in its tightening. In a potential harbinger of shifting market views, Morgan Stanley strategists upgraded emerging-market and Asia ex-Japan stocks to overweight from equal-weight. Investors are also optimistic that monetary policies in China and Japan, which have bucked the global wave of tightening to remain loose, could provide further support to the nations’ equities. “While the rest of the world is tightening, Japan and China are still easing, especially China where we are going to see more easing policies going forward,” Chi Lo, senior investment strategist for Asia Pacific at BNP Paribas Asset Management, said in an interview with Bloomberg TV. “That makes us more positive on EM Asia.”

Japanese equities gained for a fourth day as investors awaited domestic corporate earnings coming out later this month. The Topix rose 0.5% to 1,922.47 as of the market close in Tokyo, while the Nikkei 225 advanced 0.7% to 27,311.30. Sony Group contributed the most to the Topix’s gain, increasing 1.7%. Out of 2,168 stocks in the index, 1,564 rose and 490 fell, while 114 were unchanged. “There is relatively little concern about corporate earnings for Japanese stocks with the economy restarting and the yen weakening,” said Shogo Maekawa, a strategist at JPMorgan Asset Management.

In FX, the Bloomberg Dollar Spot Index consolidated within the recent day’s ranges, while Britain’s pound slipped 0.4% and gilt yields rose after Fitch Ratings lowered its outlook on the nation to negative. The greenback advanced against most of its G-10 peers. The euro steadied just below $0.99. Euro hedging costs are on the rise again as traders position ahead of Friday’s payrolls print and next week’s US inflation report. Commodity currencies were the worst performers along with the pound. Australian and New Zealand dollars gave up an Asia-session advance. The yen traded in a narrow range.

In rates, Treasuries were slightly cheaper across the curve after paring declines led by gilts in London trading after a Bank of England survey found expectations for higher prices. Focal points of US session include several Fed speakers and potential for risk-reduction ahead of Friday’s September jobs report Friday. US yields cheaper by less than 2bp across the curve in bear- flattening move, 10-year by 2bp vs 17bp for UK 10-year, the downside leader in developed market sovereign bonds. German and Italian bond curves flattened modestly as yields on shorter-dated notes rose, while those further out fell.

In commodities, West Texas Intermediate futures traded near $88 a barrel, while Brent crude held near $93.30. The output-cut plan drew a warning from the White House about negative effects on the global economy. Goldman Sachs Group Inc. increased its fourth-quarter price target for Brent to $110 a barrel.

To the day ahead now, and data releases include German factory orders for August, the German and UK construction PMIs for September, Euro Area retail sales for August, and the weekly initial jobless claims from the US. Meanwhile from central banks, we’ll get the ECB’s account of their September meeting, as well as remarks from the Fed’s Evans, Cook, Kashkari, Waller and Mester, and the BoE’s Haskel.

Market Snapshot

- S&P 500 futures down 0.3% to 3,783.50

- STOXX Europe 600 up 0.3% to 400.25

- MXAP up 0.4% to 145.05

- MXAPJ up 0.3% to 471.37

- Nikkei up 0.7% to 27,311.30

- Topix up 0.5% to 1,922.47

- Hang Seng Index down 0.4% to 18,012.15

- Shanghai Composite down 0.6% to 3,024.39

- Sensex up 0.6% to 58,403.02

- Australia S&P/ASX 200 little changed at 6,817.52

- Kospi up 1.0% to 2,237.86

- German 10Y yield little changed at 2.05%

- Euro little changed at $0.9886

- Brent Futures up 0.3% to $93.62/bbl

- Gold spot up 0.0% to $1,716.69

- U.S. Dollar Index little changed at 111.24

Top Overnight News from Bloomberg

- UK bond markets face a potential “cliff edge” when the Bank of England exits the market at the end of next week, leaving traders to navigate a turbulent backdrop without the support of a buyer of last resort

- Millions more Britons will be dragged into higher rates of income tax over the next three years, costing twice as much as Prime Minister Liz Truss’s personal tax cuts, according to calculations by the Institute for Fiscal Studies

- Britain’s construction industry turned more pessimistic in September after rising interest rates and the risk of recession held back new orders

- The European Union plans to examine whether Germany’s massive plan to shelter companies and households from surging energy costs respects the bloc’s rules on public subsidies, EU Commissioner Thierry Breton said

- German factory orders dropped in August after the previous month was revised to show an increase, hinting at a lack of momentum as the economy stands on the brink of a recession

- Societe Generale SA cut its exposure to counterparties on trades in China by about $80 million in the past few weeks as global banks seek to guard against any potential fallout from rising geopolitical risks in the world’s second-largest economy

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded mixed as the region partially shrugged off the lacklustre lead from the US where the major indices snapped a firm two-day rally and finished the somewhat choppy session with mild losses amid higher yields and as Fed rhetoric essentially pushed back against a policy pivot. ASX 200 lacked direction amid underperformance in the Real Estate and the Consumer sectors, although the downside was also limited by strength in energy after oil prices were lifted by the OPEC+ output cut. Nikkei 225 was positive with notable gains in exporter names and with Rakuten leading the advances as Mizuho looks to acquire a 20% stake in Rakuten Securities for USD 555mln. Hang Seng was lacklustre and took a breather after the prior day’s more than 5% jump with the mood also not helped after Hong Kong PMI slipped into contraction territory for the first time in 6 months.

Top Asian News

- Haikou city in China’s Hainan imposed a COVID lockdown for Thursday, according to Bloomberg.

- Malaysia PM May Propose Parliament Dissolution, Bernama Reports

- Why Polio, Once Nearly Eradicated, Is Rebounding: QuickTake

- Legoland Korea’s Default Flags Risks for Nation’s Developers

- Paris Club Seeks China Collaboration in Sri Lanka Debt Talks

- Yen Rout Is Over on Peak US Rate Hike Bets, Says Top Forecaster

European bourses are under modest pressure as sentiment broadly takes a slight turn for the worst amid limited newsflow as participants look to Friday’s NFP. Currently, European benchmarks are lower by 0.1-0.3% while US futures are posting slightly larger losses of circa 0.7 ahead of Fed speak.

Top European News

- Fitch affirmed the UK at AA-; Outlook revised to Negative from Stable, while it stated that the fiscal package announced as part of the new UK government’s growth plan could lead to a significant increase in deficits over the medium-term, according to Reuters.

- The UK Treasury is set to impose GBP 21bln of additional income taxes despite the “tax-cutting mini-budget”, according to a study by the Institute for Fiscal Studies. (Times)

- BoE Monthly Decision Maker Panel data – September 2022; looking ahead, DMP members expected CPI inflation to be 9.5% one-year ahead, up from 8.4% in the August survey, and 4.8% in three years’ time.

- BoE’s Cunliffe says the FPC will publish its next financial policy statement and record on October 12th, liquidity conditions in the run up to the BoE gilt intervention were “very poor”, MPC will make a full assessment of recent developments at its November 3rd meeting.

- UK government has proposed easing the fee cap for illiquid assets in pensions, according to a rule consultation publication by the government.

- Swedish Economy Shrinks More Than Estimated on Weak Industry

- UK Tech M&A Spree Pauses as Buyers Pull Out Amid Chaotic Markets

FX

- USD benefits from the mentioned risk tone, with the DXY extending to a 111.35 peak to the modest detriment of peers.

- However, EUR is relatively resilient and holding around 0.99 vs the USD as we await the ECB Minutes account for near-term guidance.

- Cable faded sub-1.1400 and reversed through 1.1300 again amid the USD’s move and prior to a letter exchange from the BoE to Treasury re. the Gilt Intervention.

- Antipodeans under pressure given the USD move and associated action in metals, while the Yuan initially lent a helping hand but this has since dissipated.

- Given the broader tone, the traditional havens are holding near unchanged levels though yield dynamics are a hinderance.

Fixed Income

- Gilts are once again the standout laggard following rating agency action and the BoE DMP showing inflation pressures were already elevated MM before the fiscal update.

- As such, the UK yield has extended back above 4.10%; in the US, yields are also bid though to a much lesser extent before Fed speak and Friday’s jobs.

- Back to Europe, Bunds are pressured though only modestly so vs UK counterparts awaiting the ECB’s September account

Commodities

- Crude benchmarks are modestly firmer at present, extending marginally above yesterday’s best levels with fresh newsflow limited as participants digest yesterday’s OPEC+ action.

- WTI and Brent are towards the mid-point of circa. USD 1/bbl ranges, though Brent Dec’22 briefly surpassed the 200-DMA at USD 94.11/bbl before moving back below the figure.

- Acting Kuwaiti Oil Minister said the OPEC+ decision to cut output will have positive ramifications for oil markets, while they understand consumers’ concerns about prices increasing but added that the main motive in OPEC+ is balancing supply and demand, according to Reuters.

- US National Security official stated the US sanctions policy on Venezuela remains unchanged and there are no plans to change the sanctions policy without constructive steps from Maduro, according to Reuters.

- Norway’s Budget proposes changing the temporary tax rules for the petroleum sector, entails that the uplift is reduced to 12.40% (prev. 17.69%), via Reuters.

- Saudi sets the November Arab Light OSP to N.W Europe at Ice Brent +USD 0.90/bbl; to the US at ASCI +USD 6.35/bbl, via Reuters citing a document; to Asia at Oman/Dubai +USD 5.85 (Unch.), via Reuters sources.

Geopolitics

- North Korea launched two short-range ballistic missiles which were fired from Pyongyang and landed outside of Japan’s exclusive economic zone, according to the South Korean military cited by Yonhap. Furthermore, North Korea said that its missile launches are counteraction measures against the US and South Korean military drills.

- North Korean jets and bombers have been seen flying in an exercise, according to Yonhap; South Korean jets take off in response, via Reuters.

- US State Department condemned North Korea’s ballistic missile launch and said North Korea’s missile launches pose a threat to regional neighbours and the international community, while it added that the US remains committed to a diplomatic approach to North Korea and called on North Korea to engage in dialogue, according to Reuters.

- The EU has approved the 8th round of Russian sanctions; as expected.

US Event Calendar

- 08:30: Sept. Continuing Claims, est. 1.35m, prior 1.35m

- 08:30: Oct. Initial Jobless Claims, est. 204,000, prior 193,000

Central bank Speakers

- 08:50: Fed’s Mester Makes Opening Remarks

- 09:15: Fed’s Kashkari Takes Part in Moderated Q&A

- 13:00: Fed’s Evans Takes Part in Moderated Q&A

- 13:00: Fed’s Cook Speaks on the Economic Outlook

- 13:00: Fed’s Kashkari Discusses Cyber Risk and Financial Stability

- 17:00: Fed’s Waller Discusses the Economic Outlook

- 18:30: Fed’s Mester Discusses the Economic Outlook

DB’s Henry Allen concludes the overnight wrap

After an astonishing rally at the beginning of Q4, markets reversed course yesterday as investors became much more sceptical that we’ll actually get a dovish pivot from central banks after all. The idea of a pivot has been a prominent theme over recent days, particularly after the financial turmoil during the last couple of weeks, thus sparking the biggest 2-day rally in the S&P 500 since April 2020 as the week began. But over the last 24 hours, solid US data releases have created a pushback against that narrative, since they were seen as giving the Fed more space to keep hiking rates over the coming months. And if markets had any further doubt about the Fed’s intentions, San Francisco Fed President Daly explicitly said yesterday that she didn’t expect there to be rate cuts next year, in direct contrast to futures that are still pricing in rate cuts from Q2. Indeed for a sense of just how volatile the reaction has been, 10yr bund yields were up by +16.3bps yesterday, which is their largest daily rise since March 2020 during the initial wave of the pandemic.

Looking at the details of those releases, it was evident that markets are still treating good news as bad news at the minute, since they sold off even as data pointed to a more resilient performance from the US economy than had been thought. For example, the ISM services index came in above expectations at 56.7 (vs. 56.0 expected), and the employment component moved up to a 6-month high of 53.0. So that’s a noticeably different picture to the manufacturing print on Monday, when there was a surprise contraction in the employment component. Furthermore, there was another sign of labour market strength from the ADP’s report of private payrolls, which came in at +208k in September (vs. +200k expected), and the previous month’s reading was also revised upwards. We’ll see if that picture is echoed in the US jobs report tomorrow, but there was a clear reaction to the ISM print in markets, as investors moved to upgrade the amount of Fed hikes they were expecting whilst the equity selloff accelerated.

Those expectations of a more hawkish Fed were given significant support by comments from Fed officials themselves. The most obvious came from San Francisco Fed President Daly, who was asked about the fact that futures were pricing in rate cuts, and said “I don’t see that happening at all”. In fact when it came to rates, she not only said that they were raising them into restrictive territory, but that they would be “holding it there” until inflation fell. Atlanta Fed President Bostic struck a similar tone, emphasising rate cuts in 2023 were not likely and that “I am not advocating a quick turn toward accommodation. On the contrary.” He said he wanted fed funds rates between 4% and 4.5% by the end of this year, “and then hold at that level and see how the economy and prices react.”

That backdrop led to a sizeable cross-asset selloff yesterday on both sides of the Atlantic. The effects on the rates side were particularly prominent, with 10yr US Treasury yields bouncing back +12.0bps to 3.75%. And that move was entirely driven by real yields, which rose +15.1bps as investors moved to price in a more hawkish Fed over the months ahead. You could see that taking place in Fed funds futures too, with the rate priced in for December 2023 up by +8.9bps to 4.19%, thus partially reversing the -22.2bps move lower over the previous two sessions. This morning, 10yr yields are only down -1.0 bps, so far from unwinding those moves.

The hawkish tones also proved bad news for equities, with the S&P 500 taking a breather following its blistering start to the week, retreating -0.20% after being as low as -1.80% in the New York morning. European equities did not enjoy the benefits of a New York afternoon rally, leading to a transatlantic divergence, and the STOXX 600 was down -1.02% on a broad-based decline. The energy sector outperformed in both the S&P 500 and STOXX 600 following a rally in crude oil which saw both Brent crude (+2.81%) and WTI (+2.53%) oil prices hit a 3-week high. That followed a decision from the OPEC+ group, who cut output by 2 million barrels per day. Those gains have continued in overnight trading as well, with Brent Crude now at $93.48/bbl.

In Europe, the performance of sovereign bonds echoed that for US Treasuries, as yields on 10yr bunds (+16.3bps), OATs (+17.6bps) and BTPs (+29.0bps) all saw their largest daily increases since March 2020. As in the US, that reflected growing scepticism about a dovish pivot from the ECB, but another factor not helping matters was the rebound in energy prices, with natural gas futures up +7.25% on the day to close at €174 per megawatt-hour, alongside the oil rebound mentioned above. That’s been reflected in inflation expectations too, with the 10yr German breakeven up another +8.0bps yesterday to 2.15%, after having closed beneath 2% on Monday for the first time since Russia’s invasion of Ukraine began.

Here in the UK, we also saw several key assets lose ground once again following their rally over the last week. For instance, sterling ended a run of 6 consecutive daily gains against the US Dollar to close -1.31% lower, closing back at $1.13. And that wasn’t simply a story of dollar strength, as the pound weakened against every other G10 currency as well. Gilts were another asset to struggle, with real yields in particular seeing significant daily rises of at least +30bps across most of the yield curve, including a +33.0bps rise for the 10yr real yield, and a +36.7bps rise for the 30yr real yield. That came as the Bank of England said they didn’t buy any gilts under their emergency operation for a second day running. In the meantime, there were fresh signs that the turmoil after the fiscal announcement was impacting the mortgage market, with Moneyfacts saying that the average 2yr fixed-rate mortgage had risen to 6.07%, which is the highest since November 2008. Last night that was then followed up by the news that Fitch had downgraded the UK’s outlook from stable to negative.

Overnight in Asia there’s been a mixed performance from the major equity indices. Both the Nikkei (+0.94%) and the Kospi (+1.25%) have recorded solid advances, which continues their run of having risen every day this week. In addition, futures in the US and Europe are both pointing higher, with those on the S&P 500 up +0.49%. However, the Hang Seng is down -0.43% and Australia’s S&P/ASX 200 is down -0.05%, whilst markets in mainland China remain closed for a holiday. The dollar index has also lost ground overnight, falling -0.25%, which comes in spite of those hawkish comments from Fed officials pushing back against rate cuts next year.

Looking at yesterday’s other data, the final services and composite PMIs mostly echoed the data from the flash readings. The composite PMI for the Euro Area was revised down a tenth to 48.1, and the US composite PMI was revised up two-tenths to 49.5. There was a bigger rise in the UK however, where the composite PMI was revised up seven-tenths to 49.1.

To the day ahead now, and data releases include German factory orders for August, the German and UK construction PMIs for September, Euro Area retail sales for August, and the weekly initial jobless claims from the US. Meanwhile from central banks, we’ll get the ECB’s account of their September meeting, as well as remarks from the Fed’s Evans, Cook, Kashkari, Waller and Mester, and the BoE’s Haskel.

AND NOW NEWSQUAWK

Risk sentiment dips in limited newsflow ahead of Fed speak with focus turning to NFP – Newsquawk US Market Open

THURSDAY, OCT 06, 2022 – 06:33 AM

- European bourses are under modest pressure as sentiment broadly takes a slight turn for the worst amid limited newsflow as participants look to Friday’s NFP.

- USD benefits from the mentioned risk tone, with the DXY extending to a 111.35 peak to the modest detriment of peers; though EUR is relatively resilient.

- Gilts are once again the standout laggard following rating agency action and the BoE DMP showing inflation pressures were already elevated MM before the fiscal update.

- Crude benchmarks are modestly firmer at present, extending marginally above yesterday’s best levels with fresh newsflow limited as participants digest yesterday’s OPEC+ action.

- Softer sentiment has led strength to the USD, to the detriment of metals with spot gold once again capped by the 50-DMA at USD 1722/oz.

- The EU has approved the 8th round of Russian sanctions, as expected. While N. Korea fired missiles and bombers/jets have been seen.

- Looking ahead, highlights include ECB Minutes, Speeches from Fed’s Waller, Evans, Cook & Mester.

As of 11:10BST/06:10ET

View the full premarket movers and news report.

Or why not try Newsquawk’s squawk box free for 7 days?

LOOKING AHEAD

- ECB Minutes, Speeches from Fed’s Waller, Evans, Cook & Mester.

- Click here for the Week Ahead preview.

GEOPOLITICS

- North Korea launched two short-range ballistic missiles which were fired from Pyongyang and landed outside of Japan’s exclusive economic zone, according to the South Korean military cited by Yonhap. Furthermore, North Korea said that its missile launches are counteraction measures against the US and South Korean military drills.

- North Korean jets and bombers have been seen flying in an exercise, according to Yonhap; South Korean jets take off in response, via Reuters.

- US State Department condemned North Korea’s ballistic missile launch and said North Korea’s missile launches pose a threat to regional neighbours and the international community, while it added that the US remains committed to a diplomatic approach to North Korea and called on North Korea to engage in dialogue, according to Reuters.

- The EU has approved the 8th round of Russian sanctions; as expected.

EUROPEAN TRADE

EQUITIES

- European bourses are under modest pressure as sentiment broadly takes a slight turn for the worst amid limited newsflow as participants look to Friday’s NFP.

- Currently, European benchmarks are lower by 0.1-0.3% while US futures are posting slightly larger losses of circa 0.7 ahead of Fed speak.

- Click here for more detail.

FX

- USD benefits from the mentioned risk tone, with the DXY extending to a 111.35 peak to the modest detriment of peers.

- However, EUR is relatively resilient and holding around 0.99 vs the USD as we await the ECB Minutes account for near-term guidance.

- Cable faded sub-1.1400 and reversed through 1.1300 again amid the USD’s move and prior to a letter exchange from the BoE to Treasury re. the Gilt Intervention.

- Antipodeans under pressure given the USD move and associated action in metals, while the Yuan initially lent a helping hand but this has since dissipated.

- Given the broader tone, the traditional havens are holding near unchanged levels though yield dynamics are a hinderance.

- Click here for more detail.

- Click here for OpEx for the NY Cut.

FIXED INCOME

- Gilts are once again the standout laggard following rating agency action and the BoE DMP showing inflation pressures were already elevated MM before the fiscal update.

- As such, the UK yield has extended back above 4.10%; in the US, yields are also bid though to a much lesser extent before Fed speak and Friday’s jobs.

- Back to Europe, Bunds are pressured though only modestly so vs UK counterparts awaiting the ECB’s September account.

- Click here for more detail.

COMMODITIES

- Crude benchmarks are modestly firmer at present, extending marginally above yesterday’s best levels with fresh newsflow limited as participants digest yesterday’s OPEC+ action.

- WTI and Brent are towards the mid-point of circa. USD 1/bbl ranges, though Brent Dec’22 briefly surpassed the 200-DMA at USD 94.11/bbl before moving back below the figure.

- Acting Kuwaiti Oil Minister said the OPEC+ decision to cut output will have positive ramifications for oil markets, while they understand consumers’ concerns about prices increasing but added that the main motive in OPEC+ is balancing supply and demand, according to Reuters.

- US National Security official stated the US sanctions policy on Venezuela remains unchanged and there are no plans to change the sanctions policy without constructive steps from Maduro, according to Reuters.

- Norway’s Budget proposes changing the temporary tax rules for the petroleum sector, entails that the uplift is reduced to 12.40% (prev. 17.69%), via Reuters.

- Saudi sets the November Arab Light OSP to N.W Europe at Ice Brent +USD 0.90/bbl; to the US at ASCI +USD 6.35/bbl, via Reuters citing a document; to Asia at Oman/Dubai +USD 5.85 (Unch.), via Reuters sources.

- Softer sentiment has led strength to the USD, to the detriment of metals with *spot gold *once again capped by the 50-DMA at USD 1722/oz.

- Click here for more detail.

NOTABLE EUROPEAN HEADLINES

- Fitch affirmed the UK at AA-; Outlook revised to Negative from Stable, while it stated that the fiscal package announced as part of the new UK government’s growth plan could lead to a significant increase in deficits over the medium-term, according to Reuters.

- The UK Treasury is set to impose GBP 21bln of additional income taxes despite the “tax-cutting mini-budget”, according to a study by the Institute for Fiscal Studies. (Times)

- BoE Monthly Decision Maker Panel data – September 2022; looking ahead, DMP members expected CPI inflation to be 9.5% one-year ahead, up from 8.4% in the August survey, and 4.8% in three years’ time.

- BoE’s Cunliffe says the FPC will publish its next financial policy statement and record on October 12th, liquidity conditions in the run up to the BoE gilt intervention were “very poor”, MPC will make a full assessment of recent developments at its November 3rd meeting.

- UK government has proposed easing the fee cap for illiquid assets in pensions, according to a rule consultation publication by the government.

DATA:

- German Industrial Orders MM* (Aug) -2.4% vs. Exp. -0.7% (Prev. -1.1%, Rev. 1.9%)

- EU S&P Global Construction PMI (Sep) 45.3 (Prev. 44.2), German S&P Global Construction PMI (Sep) 41.8 (Prev. 42.6)

NOTABLE US HEADLINES

- Twitter (TWTR) and Elon Musk agreed to postpone Musk’s Thursday deposition with no new time set, according to a source familiar with the litigation cited by Reuters.

- Click here for the US Early Morning Note.

CRYPTO

- Bitcoin is modestly firmer a present but, once again, remains within fairly contained parameters and holding around the USD 20k mark.

APAC TRADE

- APAC stocks traded mixed as the region partially shrugged off the lacklustre lead from the US where the major indices snapped a firm two-day rally and finished the somewhat choppy session with mild losses amid higher yields and as Fed rhetoric essentially pushed back against a policy pivot.

- ASX 200 lacked direction amid underperformance in the Real Estate and the Consumer sectors, although the downside was also limited by strength in energy after oil prices were lifted by the OPEC+ output cut.

- Nikkei 225 was positive with notable gains in exporter names and with Rakuten leading the advances as Mizuho looks to acquire a 20% stake in Rakuten Securities for USD 555mln.

- Hang Seng was lacklustre and took a breather after the prior day’s more than 5% jump with the mood also not helped after Hong Kong PMI slipped into contraction territory for the first time in 6 months.

NOTABLE APAC HEADLINES

- Haikou city in China’s Hainan imposed a COVID lockdown for Thursday, according to Bloomberg.

NOTABLE APAC DATA

- Hong Kong PMI (Sep) 48.0 (Prelim. 51.2)

- Australian Trade Balance (AUD)(Aug) 8.3B vs. Exp. 10.1B (Prev. 8.7B)

- Australian Exports (Aug) 3% (Prev. -10%); Imports (Aug) 4% (Prev. 5%)

i)THURSDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED //Hang Seng CLOSED /The Nikkei closed UP 190.77PTS OR 0.78% //Australia’s all ordinaires CLOSED UP 0.04% /Chinese yuan (ONSHORE) closed //OFFSHORE CHINESE YUAN UP 7.0720// /Oil UP TO 87.32 dollars per barrel for WTI and BRENT AT 93.01 / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

2 a./NORTH KOREA/ SOUTH KOREA/

///NORTH KOREA/SOUTH KOREA/

2B JAPAN

end

3c CHINA

CHINA/

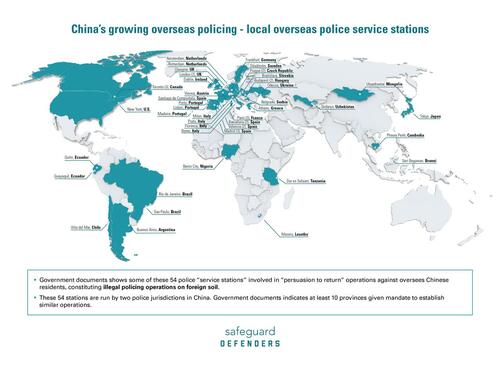

Three stations in Canada as well: China has set up dozens of unofficial police stations around the world.

Simply awful!

China Has Set Up Dozens Of Unofficial Police Stations Around The World: Report

TUESDAY, OCT 04, 2022 – 10:25 PM

The Chinese Communist Party (CCP) has opened dozens of unofficial police stations around the world, including at least three in Toronto, Canada, according to a September report from human rights NGO, Safeguard Defenders.

The report claims that China has been engaging in “long-arm policing” around the world in what has been dubbed the “110 overseas police stations,” named after the police emergency number in China; 110.

The report has identified 54 Chinese overseas police stations spanning 30 countries – which are under the jurisdiction of two local-level police services in China; the Fuzhou Public Security Bureau in Fuzhou City, Fujian Province, and the Qingtian County police in Zhejiang Province.

More via the Epoch Times;

Peter Dahlin, founder and director of Safeguard Defender and co-author of the report, says that following the release of his organization’s findings, security police or related government agencies from North America and Europe have approached his organization asking “to sit down and have a briefing discussion” on the Chinese operations overseas.

“So they are certainly aware of it, at least in some countries,” Dahlin told The Epoch Times.

More Locations

While the Chinese authorities say these police stations are created to better serve its overseas nationals, the report noted that those stations have been used to “persuade” up to 230,000 Chinese nationals to “voluntarily” return to China to face criminal proceedings between April 2021 and July 2022.

“Persuasion to return” is a key method of the Chinese regime’s “involuntary returns” operations, which include its “Operation Fox Hunt” and the broader “Sky Net” campaign, according to Safeguard Defenders. Many of the targets for persuasion to return were overseas Chinese allegedly involved in telecommunication fraud, though the report said a number of non-suspects and their family members in China have also been targeted for police harassment and intimation.

Dahlin said that in addition to the three stations in Toronto—two in Markham and one in Scarborough, whose locations were published in a Chinese state media outlet—there are likely other unofficial Chinese police stations either existing or being established in Canada, though they have yet to be discovered.

“We’ve also seen a [Chinese] government notice that said that 10 different provinces should launch these types of operations on a pilot basis,” he told The Epoch Times, pointing to the report’s citation of a July 5, 2018, news release issued by the Chinese regime.

“So, we have two of these operations uncovered [in Fujian Province and Zhejiang Province]. There might be eight more provinces doing this that could have their own stations, and we have not been able to track down that information yet. That’s why we keep saying that … we believe and we have good reason to think that there are more [overseas Chinese police stations].”