by harveyorgan · in Uncategorized · Leave a comment·Edit

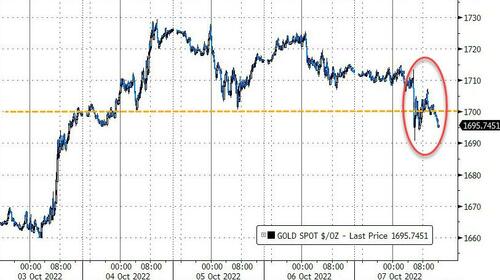

GOLD PRICE CLOSE: DOWN $10.70 to $1701.70

SILVER PRICE CLOSE: DOWN $0.37 to $20.24

Access prices: closes

Gold ACCESS CLOSE 1694.70

Silver ACCESS CLOSE: 20.13

New: early yesterday morning//very ominous:

On Monday, October 3, 2022 at 12:15 p.m., a meeting of the Board of Governors of the Federal Reserve System was held under expedited procedures, as set forth in section 261b.7 of the Board’s Rules Regarding Public Observation of Meetings, at the Board’s offices at 20th and C Streets, N.W., Washington, D.C. and by audio/video conference call, to consider the following matters of official Board business.

Harvey: Credit Suisse?

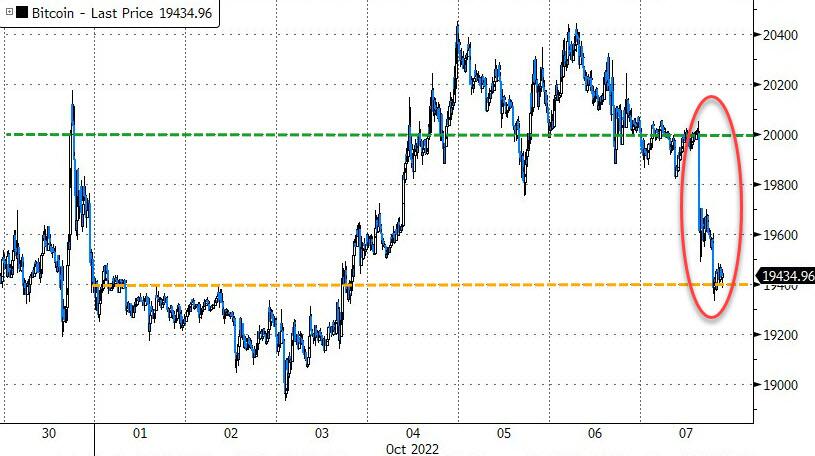

Bitcoin morning price: $20,004 DOWN 31

Bitcoin: afternoon price: $19,439 DOWN 596

Platinum price closing DOWN 6.40 AT $919.10

Palladium price; closing DOWN $82.35 at $2195.65

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/closing ACCESS

CANADIAN GOLD $2322.00 CDN DOLLARS PER OZ DOWN $30.0 CDN DOLLARS

BRITISH GOLD IN POUNDS: 1526.30 POUNDS PER OZ DOWN 7 BRITISH POUNDS PER OZ/

EURO GOLD: 1736/37 EUROS PER OZ// DOWN 12/39 EUROS PER OZ///

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: OCTOBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,711.700000000 USD

INTENT DATE: 10/06/2022 DELIVERY DATE: 10/10/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 4

132 C SG AMERICAS 2

624 H BOFA SECURITIES 12

657 H MORGAN STANLEY 16

661 C JP MORGAN 17

800 C MAREX SPEC 25 6

TOTAL: 41 41

MONTH TO DATE: 21,375

JPMORGAN STOPPED 17/41

GOLD: NUMBER OF NOTICES FILED FOR OCT CONTRACT:

41 NOTICES FOR 4100 OZ //.1275 TONNES

total notices so far: 21,375 contracts for 2,137,500 oz (66.485 tonnes)

SILVER NOTICES: 68 NOTICES FILED FOR 340,000 OZ/

total number of notices filed so far this month 321 : for 1,605,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $10.70

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD: ////

INVENTORY RESTS AT 946.34 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 37 CENTS

AT THE SLV// ://BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A HUGE WITHDRAWAL OF2.447 MILLION OZ FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 473.130 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL SIZED 125 CONTRACTS TO 126,292 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE HUGE LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.11 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.11). HOWEVER OUR SPEC SHORTS ARE DESPERATELY TRYING TO COVER THEIR MASSIVE COMEX OI SHORTFALL. BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS.

WE MUST HAVE HAD:

I) CONTINUAL SPECULATOR SHORT COVERINGS ////CONTINUED BANKER OI COMEX ADDITIONS /// SOME NEWBIE SPEC LONG ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GIGANTIC ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.580 MILLION OZ FOLLOWING A 160,000 OZ QUEUE JUMP / // V) SMALL SIZED COMEX OI GAIN/ SOME SPEC COVERING THEIR SHORTS.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: –45

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTRACTS for 7 days, total 49,425 contracts: 29.65 million oz OR 4.23MILLION OZ PER DAY. (706 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 29.65 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.65 MILLION OZ INITIAL

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 125 WITH OUR SMALL $0.11 GAIN IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A ZERO SIZED EFP ISSUANCE CONTRACTS: 0 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER ADDITIONS A// SMALL SHORT LIQUIDATIONS//SMALL NEWBIE SPEC LONG ADDITIONS// /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR OCT. OF 1.580 MILLION OZ FOLLOWED BY TODAY’S 160,000 QUEUE JUMP .. WE HAD A SMALL SIZED GAIN OF 125 OI CONTRACTS ON THE TWO EXCHANGES FOR .6250 MILLION OZ..

WE HAD 68 NOTICE(S) FILED TODAY FOR 340,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 71 CONTRACTS TO 433,247 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED — -369 CONTRACTS.

.

THE SMALL SIZED INCREASE IN COMEX OI CAME WITH OUR GAIN IN PRICE OF $0.70//COMEX GOLD TRADING/THURSDAY // SOME SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR OCT. AT 66.099 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 2,000 OZ//NEW STANDING 68.123 TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $0.70 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 3711 OI CONTRACTS 11.54 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3640 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 433,616

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3711 CONTRACTS WITH 71 CONTRACTS INCREASED AT THE COMEX AND 3640 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 4280 CONTRACTS OR 13.312 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3640) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (71): TOTAL GAIN IN THE TWO EXCHANGES 3711 CONTRACTS. WE NO DOUBT HAD 1) MINOR SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS///NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 66.099 TONNES FOLLOWED BY TODAY’S 2,000 OZ QUEUE JUMP///NEW STANDING 68.123 TONNES//. 3) ZERO LONG LIQUIDATION //// //.,4) SMALL SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT. :

15,147 CONTRACTS OR 1,544,700 OZ OR 47.113 TONNES 7TRADING DAY(S) AND THUS AVERAGING: 2163 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAY(S) IN TONNES: 47.113 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 47.113/3550 x 100% TONNES 1.32% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 47.113 TONNES INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A SMALL SIZED 125 CONTRACT OI TO 126,292 AND CLOSER TO TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 0 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 125 CONTRACTS AND ADD TO THE 0 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED GAIN OF 125 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 0.62 MILLION OZ

OCCURRED WITH OUR GAIN IN PRICE OF $0.11

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED //Hang Seng CLOSED DOWN 272.10 OR 1.51% /The Nikkei closed DOWN 195.19PTS OR 0.77% //Australia’s all ordinaires CLOSED DOWN 0.82% /Chinese yuan (ONSHORE) closed //OFFSHORE CHINESE YUAN UP 7.0896// /Oil UP TO 89.86 dollars per barrel for WTI and BRENT AT 95.92 / Stocks in Europe OPENED ALL MIXED. ONSHORE YUAN TRADING XXX LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 71 CONTRACTS TO 433,247 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS FAIR COMEX DECREASE OCCURRED WITH OUR RISE IN PRICE OF $0.70 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (3640 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF OCT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3640 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :3640 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3640 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 3711 CONTRACTS IN THAT 3640 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 71 CONTRACTS..AND THIS GOOD GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR SMALL RISE IN PRICE OF GOLD $0.70//WE HAD SPEC SHORTS ADDING TO THEIR POSITIONS WITH BANKERS TAKING THE OTHER SIDE AS BUYERS OF COMEX GOLD CONTRACTS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING OCT (68.127),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 68.127 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $0.70) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A GOOD SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 3711 CONTRACTS // WE HAVE REGISTERED A GOOD GAIN OF 11.54 PAPER TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR OCT. (68.127 TONNES)…THIS WAS ACCOMPLISHED WITH A SMALL RISE IN PRICE OF $.70

WE HAD -269 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3711 CONTRACTS OR 371100 OZ OR 11.54 TONNES

Estimated gold volume 154,330// poor//

final gold volumes/yesterday 149,323/ poor

INITIAL STANDINGS FOR OCT ’22 COMEX GOLD //OCT 7

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 95,199.111 oz HSBC |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 69,156.79 oz Brinks 2151 kilobars |

| No of oz served (contracts) today | 41 notice(s) 4100 OZ 0.1275 TONNES |

| No of oz to be served (notices) | 528 contracts 52,800oz 1.642 TONNES |

| Total monthly oz gold served (contracts) so far this month | 21,375 notices 2,137,500 66.485 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

Into HSBC: 95,199.111 o (2961 kilobars)

total deposits 95,199.111 oz

customer withdrawals: 1

i) Out of Brinks: 69,156.790 oz (2151 kilobars)

total: 69,156.790 oz

total in tonnes: 2.512 tonnes

Adjustments: 4// all dealer to customer

HSBC: 56,894.928 oz

JPMorgan: 122,893.131 oz

Malca 5883.633 oz

Manfra: 3443.840 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCT we have an oi of 569 contracts having LOST 345 contracts . We had 365 contracts

filed on THURSDAY, so we gained 20 contracts or an additional 2000 oz will stand in this active delivery month of Oct.

We will gain gold oz standing on each and every trading day from this day forth until the conclusion of October.

(remember that queue jumping is really EFP’s exercised from London for gold underwritten by COMEX based bankers)

November GAINED 53 contracts to stand at 2846

December lost 1780 contracts down to 373,129

We had 41 notice(s) filed today for 4100 oz FOR THE OCT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 41 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 17 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT /2022. contract month,

we take the total number of notices filed so far for the month (21,375) x 100 oz , to which we add the difference between the open interest for the front month of (OCT 569 CONTRACTS) minus the number of notices served upon today 41 x 100 oz per contract equals 2,190,300 OZ OR 68.127 TONNES the number of TONNES standing in this active month of OCT.

thus the INITIAL standings for gold for the OCT contract month:

No of notices filed so far (21,375) x 100 oz+ (569) OI for the front month minus the number of notices served upon today (41} x 100 oz} which equals 2,190,300, oz standing OR 68.127 TONNES in this NON active delivery month of OCTOBER.

TOTAL COMEX GOLD STANDING: 68.127 TONNES (A HUMONGOUS STANDING FOR OCT (GENERALLY THE POOREST DELIVERY MONTHS FOR AN ACTIVE MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,067,434 OZ (REG GOLD- PLEDGED GOLD) 340.166 tonnes//rapidly declining

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 26,281,876.600 OZ

TOTAL REGISTERED GOLD: 12,814,660.585 OZ (398.58 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 13,467,216.016 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,747,226 OZ (REG GOLD- PLEDGED GOLD) 334.283 tonnes//rapidly declining

END

SILVER/COMEX

OCT 7//INITIAL OCT SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,297,972.649 oz HSBC CNT |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,`86,312.000 oz Loomis CNT |

| No of oz served today (contracts) | 68 CONTRACT(S) 1,605,0000 OZ) |

| No of oz to be served (notices) | 40 contracts (200,000 oz) |

| Total monthly oz silver served (contracts) | 321 contracts 1,605,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 2 deposits into the customer account

i) Into CNT: 600,343.600 oz

ii) Into Loomis: 585,968.400

Total deposits: 1,186,312.000 oz

JPMorgan has a total silver weight: 161.406million oz/312.623million =51.61% of comex

Comex withdrawals: 2

i)Out of CNT 725,261.168 oz

ii) Out of HSBC: 572,711.481 oz

total withdrawals: 1,297,972.649 oz

adjustments: // 3

JPMorgan 14,601.150 oz

ii) Loomis: 9599.140 oz

iii) Manfra: 10,087.400 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 40.116 MILLION OZ (declining rapidly)

TOTAL REG + ELIG. 3126235 MILLION OZ (also declining)

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF OCT OI: 108 CONTRACTS HAVING GAINED 1 CONTRACT(S.)

WE HAD 31 NOTICES FILED ON THURSDAY SO WE GAINED 32

SILVER CONTRACTS OR AN ADDITIONAL 160,000 OZ WILL STAND FOR OCT.

NOVEMBER LOST 9 CONTRACTS TO STAND AT 356

DECEMBER SAW A LOSS OF 1293 CONTRACTS DOWN TO 107,337

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 68 for 340,000 oz

Comex volumes:81,613// est. volume today// good

Comex volume: confirmed yesterday: 65,273 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 321 x 5,000 oz = 1,605,000 oz

to which we add the difference between the open interest for the front month of OCT(108) and the number of notices served upon today 68 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT./2022 contract month: 321 (notices served so far) x 5000 oz + OI for front month of OCT (108) – number of notices served upon today (68) x 5000 oz of silver standing for the OCT contract month equates 1,805,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:61,618// est. volume today// poor

Comex volume: confirmed yesterday: 54,383contracts ( poor)

END

GLD AND SLV INVENTORY LEVELS

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTOTHE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

SEPT 21/WITH GOLD UP $4.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.79 TONNES FROM THE GLD///INVENTORY RESTS AT 952.16 TONNES

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

SEPT 13/WITH GOLD DOWN $22.85 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73ONNES FROM THE GLD////INVENTORY RESTS AT 964.91 TONNES

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

GLD INVENTORY: 946.34 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

SEPT 21/WITH SILVER UP 33 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.902 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 482.115 MILLION OZ//

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

SEPT 13/WITH SILVER DOWN $.31 TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.899 MILLION OZ//

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

CLOSING INVENTORY 475.617 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: A Massive Fiscal Time Bomb

FRIDAY, OCT 07, 2022 – 07:30 AM

Federal Reserve Chairman Jerome Powell knew fighting inflation would cause big problems in a bubble economy loaded up with debt. He put it off as long as he could, calling inflation “transitory.” But once inflation became a huge problem, the central bank had no choice but to get into the fight and start tightening monetary policy. The problem is, the Fed’s plan won’t work. And one reason it won’t work is the massive national debt.

Peter Schiff talked about it in this clip from his podcast.

The federal government already spends about $500 billion per year on interest payments on the $31 trillion debt. Peter noted a CNBC discussion where they speculated that in 10 years, the US government could be paying $1 trillion per year on interest alone.

Ten years? We could be paying $1 trillion in interest in one year! How are these guys getting 10 years?”

Four percent of the $31 trillion debt is $1.25 trillion. The average maturity on the debt is under five years. A third of the debt will mature in the next year. Meanwhile, the debt continues to skyrocket. The national debt grew by $1 trillion in just eight months even with pandemic spending programs winding down.

Five years from now, the national debt will be over $40 trillion, and we’re going to have to pay an interest rate probably more than 5% on that. So, a $1 trillion tab for interest on the national debt isn’t a decade away. It’s a year, maybe two away. That’s how close this crisis is.”

That raises an important question: where is the government going to get the money to pay for this? It will cost something like 30% of all tax revenue just to pay the interest on the debt. Huge interest payments will mean even more borrowing.

This is a massive fiscal time bomb.”

During a hearing in January 2021, Janet Yellen was asked if we should be worried about the national debt. She said, no. Instead, she said we should be focusing on how low interest rates are and how inexpensive it is to service the debt. In other words, the debt didn’t matter because financing was cheap.

At the time, Peter asked, “What happens when rates go up?” He compared it to adjustable-rate mortgages. When rates go up, homebuyers often can’t afford the higher payments.

The Treasury wasn’t taking advantage of low 30-year borrowing costs. The Fed was borrowing for six months, for one year, for two years. So, they were rolling the dice and gambling that interest rates stay low. Well, they’re not low. They’re much higher. I wonder if Janet Yellen is worrying about the national debt now that interest rates have moved up so much. Or, is she going to start worrying? Because we already know that they’re going to move much higher.”

For years, the government justified borrowing money because interest rates were low. Peter said that argument might have flown if the government was locking in the low rates for 30 years. But not when the Treasury was rolling over the debt every 30 days, 90 days, or even every year.

I often said, ‘Wait a minute. Just because something is cheap doesn’t mean you should do it. I would say, ‘Hey, if heroin was free, if they were giving out free heroin, would you say, hey, heroin is free! I might as well use it.’ If something is bad, just because the cost goes down, that doesn’t mean you do it. And taking on all this debt was bad. Just because it was temporarily cheap, it wasn’t a reason to do it.”

But the government did it. And now we have to deal with the consequences.

The Federal Reserve deliberately created inflation since 2008 to postpone the pain. Why did it do quantitative easing? Why did it keep interest rates at zero for so long?

Because the Fed did not want to allow a bad recession, or allow a bad recession to get worse. The Fed wanted to prop up stock prices. The Fed wanted to prop up real estate prices. So, in order to do that, we created inflation. We put interest rates at zero. We did quantitative easing. Well now, we’ve got a huge inflation problem. And now the Fed has to fight a monster that it created. But the Fed can’t fight and create inflation at the same time.”

And the US government can’t service its debt, much less maintain its borrowing and spending without the Fed creating inflation.

That’s why this inflation fight is doomed to fail

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

end

Lawrie Williams

END

3.Chris Powell of GATA provides to us very important physical commentaries

The crooked bankers on Wall Street double down on risk as they continue to be the seller of credit default swaps

(Pam and Russ Martens/GATA)

Pam and Russ Martens: Wall Street banks double down on risk, sell credit default swaps

Submitted by admin on Thu, 2022-10-06 11:07Section: Daily Dispatches

By Pam and Russ Martens

Wall Street on Parade

Thursday, October 6, 2022

Last Thursday, while news outlets focused on videos of the devastating impact of Hurricane Ian on the southwest coast of Florida, two researchers at the Office of Financial Research published a breathtaking and almost surreal analysis of how the mega banks on Wall Street are once again doubling down on unprecedented risk with derivatives and threatening the financial stability of the United States.

The report was ignored by mainstream business media. …

… For the remainder of the analysis:

END

Your weekend reading material

(Alasdair Macleod)

Alasdair Macleod: The consequences of imploding credit

Submitted by admin on Thu, 2022-10-06 11:21Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, October 6, 2022

There is a growing realisation that the world faces a combination of persistent inflation of prices and a recession at the same time. The factors driving both are visibly intensifying. Those of us versed in the cycle of bank credit are aware that it is the contraction of bank balance sheets which is driving the recession, while it is continuing currency debasement driving inflation.

Neo-Keynesians in the establishment think the current position is contradictory, that current rates of price inflation will decline back to their 2% target in a recession, and interest rates can then be reduced to stimulate economic activity.

The key to understanding why prices can continue to rise in a recession requires a fuller understanding of the role of credit in an economy and what it represents. Its role is far greater than commonly thought, with considerably more than several quadrillions of dollar equivalents outstanding. All economic activity and wealth are credit. This article sketches out the various types of credit, and how credit equates to our collective wealth.

It also requires us to differentiate between a currency which is anchored to gold specie and one without a specie anchor.

The former imposes a discipline on the state of non-intervention, while the latter encourages intervention. It is that intervention which leads to fiat currencies and all credit based upon it finally collapsing. …

For the remainder of the analysis:

https://www.goldmoney.com/research/imploding-credit-the-consequences?gmrefcode=gata

END

end

4. OTHER GOLD/SILVER COMMENTARIES

Ep. 94 Live from the Vault

Card counters create 5 days of COMEX hell

In this week’s Live from the Vault, Andy Maguire exposes the Chinese and Indian deep-pocket traders who aggressively capitalise on the $1000-per-contract silver futures price divergence.

As the COMEX-driven backwardation reaches unprecedented extremes, the London wholesaler analyses the increasing potential for the freshly-emerged competitors to ignite the massive silver short squeeze.

PHYSICAL SILVER/GOLD

5.OTHER COMMODITIES:

end

COMMODITIES IN GENERAL/

END

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED

OFFSHORE YUAN: 7.0895

SHANGHAI CLOSED:

HANG SENG CLOSED DOWN 272.10 OR 1.51%

2. Nikkei closed DOWN 195197 PTS OR 0.77%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UP TO 112.01/Euro FALLS TO 0.9796

3b Japan 10 YR bond yield: RISES TO. +.244/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 144.86/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: XX -// OFF- SHORE: 7.0896

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.144%***/Italian 10 Yr bond yield RISES to 4.58%*** /SPAIN 10 YR BOND YIELD RISES TO 3.33%…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.75//

3j Gold at $1706.05//silver at: 20.42 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND20/100 roubles/dollar; ROUBLE AT 61.10//

3m oil into the 88 dollar handle for WTI and 95 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 144.86DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this .9907– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9703well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.833 UP 1 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.785 DOWN 1 BASIS PTS//(USA 30 YR INVERTED TO THE USA 10)

USA DOLLAR VS TURKISH LIRA: 18,59…GETTTING DANGEROUS

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Jittery Futures Coiled Tightly Ahead Of Today’s Jobs Report Main Event

FRIDAY, OCT 07, 2022 – 07:49 AM

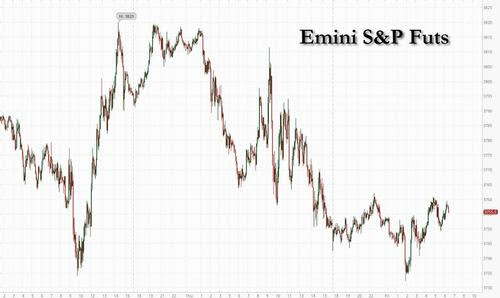

S&P futures rebounded from an overnight drop and swung between gains and losses as investors looked forward to the week’s main event, the September payrolls report, for clues on what the Fed will do next after a raft of hawkish Fed doused expectations on Thursday for a quick halt to rate hikes. Nasdaq 100 futs fell 0.3%, trimming deeper losses, amid a sharp premarket drop for semiconductor stocks prompted by a plunge in AMD which slumped after it preannounced much weaker-than-expected 3Q revenue and margins . Meanwhile, S&P500 futures on the S&P 500 Index traded little changed, although the benchmark was poised for the best weekly advance since June. Treasuries drifted lower, the dollar was flat, and cryptos were unchanged.

In premarket trading, Credit Suisse shares gained 7.9% after the lender offered to buy back debt securities for as much as CHF BN, in a show of financial strength after recent concerns about the bank’s solidity. Shares are up 14% this week, best weekly return since June 2020. They have recovered from a 12% intraday drop on Monday, when the stock slumped to a fresh low Shares are 49% down YTD. On the other end, chipmakers led the slide in early New York trading. Besides AMD’s 6% plunge, Nvidia Corp. and Intel Corp. fell more than 2% each amid concern that a slowing world economy will sharply dent semiconductor demand. Here are some other notable premarket movers

- Twitter shares fell as much as 1.9% to $48.45 in US premarket trading on Friday, trading almost 10% below Elon Musk’s offer price of $54.20 as the deal is said to be contingent on receiving $13 billion in debt financing, according to people familiar with the matter. They were flat by 6am in New York.

- Chip stocks were lower in US premarket trading after Samsung and AMD reported disappointing figures within hours of each other. The announcements signaled a deteriorating climate for global chip demand affecting the entire personal computers supply chain, including chipmakers, semiconductor equipment makers and PC manufacturers. AMD -6.4%, Nvidia -3.3%, Intel -2.8%.

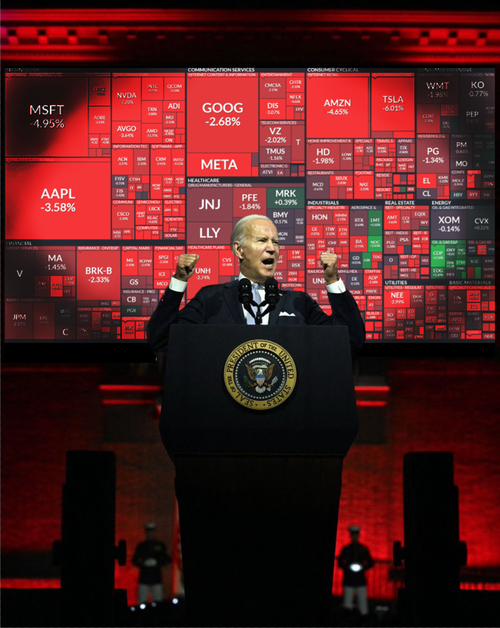

- Pot stocks rallied in US premarket trading on Friday, set to extend Thursday’s gains after President Joe Biden pardoned thousands of Americans for possession of marijuana and ordered a review of its legal status, sparking hopes that decriminalization of the drug was drawing nearer and a more favorable regulatory environment for cannabis-related firms. Tilray Brands +9%, Canopy Growth +9%, Cronos Group +2.4%.

- DraftKings shares jump as much as 9.2% in US premarket trading on Friday, boosted by a report that the sports-betting firm is said to be nearing a sizable new partnership with Disney’s ESPN, signaling that interest in legalized sports betting in increasing. DraftKings trades at a price-to-sales multiple of 4.2 times, according to Bloomberg data, down from a peak of around 37 times reached in March 2021.

- Levi Strauss shares fell as much as 4.6% in US premarket trading on Friday after the jeans maker cut its adjusted earnings per share and net revenue growth outlook for the full year, stoking worries that it could be tough for retailers in the near-term as the company grapples with the impact of a stronger dollar, weakness in its European markets and supply-chain disruption.

- Payoneer Global jumps as much as 8.4% in premarket trading following news that the company will join the S&P SmallCap 600 index before trading opens on Oct. 12.

- Lyft shares fall 3.7% in US premarket trading after RBC downgraded the ride- sharing firm and slashed its PT, saying its bull case for the stock looks increasingly less likely.

- Aehr Test Systems jumped 9% in extended trading after the semiconductor manufacturing company reported net sales growth and improved adjusted earnings in the fiscal first quarter.

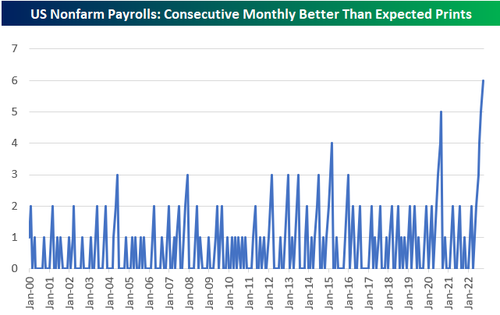

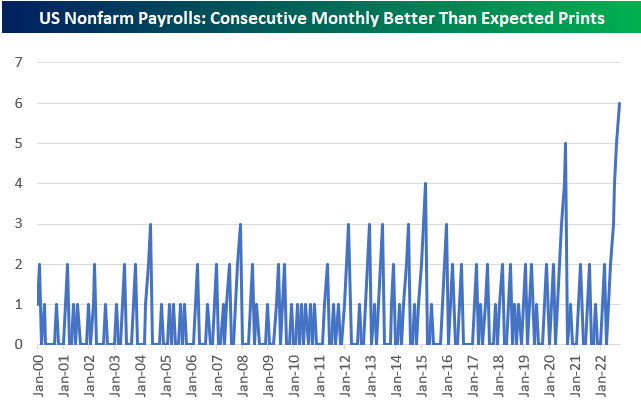

As previewed earlier, today’s main event is the jobs report and as JPM noted, prior to Friday’s NFP (and CPI next Wednesday), the market has been oscillating between the “hawkish Fed” and “Fed pivot” narrative. While the JOLTS Job Openings and the ISM Manufacturing employment index showed more evidence of a slowing labor market, the stronger than expected ADP/ISM Services once again proved the economy still remains strong and therefore weakens the hope of a near-term pivot from the Fed. In a nutshell, according to JPM’s trading deks, with consensus expected tomorrow’s NFP to print +255k, Equity bulls would need a print ~100k to see the market alter its Fed expectations (full preview here).

The data will follow hawkish comments from Fed officials. Chicago Fed President Charles Evans said the benchmark rate will probably be at 4.5% to 4.75% by next spring, and Minneapolis Fed’s Neel Kashkari said the central bank is “quite a ways away” from pausing its campaign of rate increases.

“Barring an unexpectedly shocking number, I do not think today’s release will prompt the Fed to change tack,” said Stuart Cole, the head macro economist at Equiti Capital. “This has certainly been the message that various Fed officials have been promulgating.”

Meanwhile, according to Bloomberg, US Treasury yields are heading for a 10th week of increases, the longest streak since 1984, as the Fed stays resolute in its fight against inflation despite recent data suggesting a cooling of the economy. Investors are being swayed between hopes for an end to monetary tightening by March next year and concern over the possibility of a deep recession that such a pivot would underscore.

At the same time, investor focus is increasingly trained on signs of a weaker earnings-reporting season. Besides Thursday’s dour trading update from European oil major Shell, underwhelming figures from AMD and South Korean Samsung Electronics Co. are reinforcing concerns for the global economy.

“The issue of the Fed pivot remains the main factor restricting risk appetite,” Sebastien Barbe, the head of emerging-market research and strategy at Credit Agricole CIB, wrote in a note. “Cautiousness should remain in place ahead of the US jobs report. Given the repeated hawkish comments by Fed speakers, this may not be enough to sustainably support risk appetite.”

In Europe, the Stoxx 50 fell 0.2%. FTSE MIB outperforms, adding 0.2%; IBEX lags, dropping 0.5%. Tech, consumer products and retailers are the worst-performing sectors. Here are the biggest European equity movers:

- Renault shares climb as much as 4.8%. The automaker is raised to outperform from neutral and PT hiked to EU55 from EU35 at Oddo on its successful operational recovery and accelerating “product offensive.”

- Credit Suisse shares gain 8.4% after the lender offered to buy back debt securities for as much as CHF3bn, in a show of financial strength after recent concerns about the bank’s solidity.

- Telenor shares jump as much as 5.1%, the most since July 2020, after the telecom operator agreed to sell a 30% stake in its Norwegian fiber network to a consortium led by KKR and Oslo Pensjonsforsikring.

- Storytel gains as much as 11%, the most since August, after the Swedish publishing house released preliminary streaming revenue for the third quarter that was slightly above guidance, according to DNB

- European chip stocks are under pressure on Friday after industry bellwethers AMD and Samsung posted results that widely missed analysts’ expectations. ASML drops as much as 2.9%

- Adidas shares decline as much as 3.2% with UBS saying the uncertainty about its partnership with Kanye West’s Yeezy brand is a “negative development” for the sportswear group.

- Ocado shares decline as much as 3.1% after PT cut to a Street-low 420p from 595p at Morgan Stanley, which maintains an underweight rating on the grocery delivery group and says the case for its automated model has “got harder.”

- Building materials group Marshalls slumps 28% after it warned on a slowdown in demand for its landscaping products, prompting Peel Hunt to cut earnings estimates.

Asian stocks fell, on track to snap a three-day winning streak, as Federal Reserve officials reiterated their hawkish views and tech shares weighed. The MSCI Asia Pacific Index declined as much as 1.3%, with tech and consumer discretionary shares falling after five Fed officials on Thursday separately signaled inflation remained too high in the US. Some chip shares slid after Advanced Micro Devices’ preliminary third-quarter sales missed projections and Samsung reported disappointing preliminary quarterly results. Meanwhile, China’s electric-vehicle firms led declines on the Hong Kong market as concerns grew over weaker-than-expected orders. Vietnam’s stocks tumbled to the lowest in almost two years as a wave of forced selling hit the market amid concerns about rising interest rates. Liquidity remained relatively low with the onshore China market closed for the Golden Week holiday. The Asian gauge remains on track for its best week since July after weak US economic data earlier fueled hopes that the Fed may be less aggressive in tightening. Traders will scrutinize the US payroll data out later Friday for signs of economic slowdown and the impact on monetary policy. “Clearly the equity market is still playing chicken with the Fed around,” Joshua Crabb, head of Asia Pacific equities at Robeco, told Bloomberg Television. The interest-rate environment “is here to stay and that will continue to put pressure on some of the more highly valued sort of companies.”

Japanese stocks dropped as investors remained cautious over the outlook for Fed policy and awaited an upcoming monthly US payrolls report. The Topix fell 0.8% to 1,906.80 as of the market close in Tokyo, while the Nikkei 225 declined 0.7% to 27,116.11. Mitsubishi UFJ Financial Group contributed the most to the Topix’s decline, decreasing 2.2%. Out of 2,168 stocks in the index, 569 rose and 1,495 fell, while 104 were unchanged. “There is uncertainty whether US interest rate hikes could be 75bps or 100bps during the FOMC meeting in November,” said Naoki Fujiwara, chief fund manager at Shinkin Asset Management. “We are watching the unemployment rate and wage growth.”

Stocks in India ended flat on Friday but posted their first weekly advance in four, helped by a recovery in metal companies. The S&P BSE Sensex was little changed at 58,191.29 in Mumbai, while the NSE Nifty 50 Index dropped 0.1%. For the week, the gauges rose 1.3% each. Tata Consultancy Services was the most prominent decliner among the Sensex 30 companies, dropping 1.3%. The country’s biggest software exporter will kickoff quarterly earnings season Monday. Titan was among the best performers after reporting strong sales growth for three-months through September. Eleven of the 19 sector sub-indexes compiled by BSE Ltd. retreated, led by oil & gas companies, while consumer durables makers were the top performers. A measure of metal companies was the top gainer for the week, posting its best advance since July.

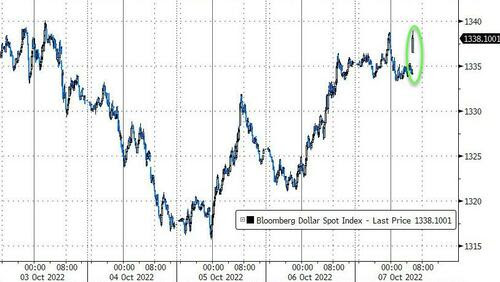

In FX, the Bloomberg Dollar Spot Index slipped 0.1% as the dollar fell against all Group of 10-peers apart from the kiwi. Demand for dollar topside exposure in the long-end remains strong ahead of the payrolls report.

- The euro rose above $0.98 and Bund yields climbed by up to 4bps as real yields continued to push higher alongside ECB tightening wagers.

- The cable led G-10 gains to trade above $1.12 after reversing early European session weakness. Yields on gilts rose by 3-6bps.

- The New Zealand dollar rose against the greenback as the nation’s bond yields closed up to 10bps higher.

- Australian dollar and Norwegian krone strengthened somewhat. Australian yields rose up to 7bps.

- The yen snapped a two-day decline as traders weigh the risk of an intervention by Japanese authorities to support the currency after it weakened past 145 per dollar. The currency is still set for an eighth straight week of declines

In rates, Treasuries were slightly cheaper across the curve after most yields reached weekly highs while maintaining narrow ranges ahead of September jobs report. Gilts and bunds weigh, underperforming Treasuries. US yields cheaper by up to 3bp across belly of the curve, cheapening 2s5s30s fly by 3.5bp on the day to around 12bp, up from as low as -13.7bp on Tuesday; 10-year yields around 3.85%, richer vs bunds and gilts by 6bp and 2bp. UK 10-year yield rises 2.5bps to 4.19%, while German 10-year climbs 4.5bps to 2.13%.

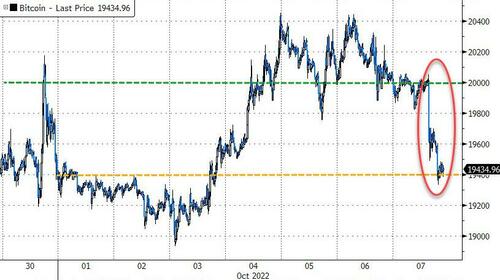

In commodities, US crude futures rose to approach $89 a barrel, on course for the biggest weekly surge since March. Spot gold is little changed at ~$1,713/oz. Bitcoin is contained within very narrow parameters, essentially pivoting the USD 20k mark as we head into the NFP release.

To the day ahead now, and the highlight will likely be the aforementioned US jobs report for September. Otherwise, data releases include German industrial production and Italian retail sales for August. From central banks, we’ll hear from the Fed’s Williams, Kashkari and Bostic, as well as BoE Deputy Governor Ramsden. Finally, EU leaders will be meeting in Prague.

Market Snapshot

- S&P 500 futures down 0.2% to 3,748.50

- STOXX Europe 600 down 0.2% to 395.56

- MXAP down 1.1% to 143.02

- MXAPJ down 1.3% to 463.87

- Nikkei down 0.7% to 27,116.11

- Topix down 0.8% to 1,906.80

- Hang Seng Index down 1.5% to 17,740.05

- Shanghai Composite down 0.6% to 3,024.39

- Sensex down 0.3% to 58,069.57

- Australia S&P/ASX 200 down 0.8% to 6,762.77

- Kospi down 0.2% to 2,232.84

- German 10Y yield little changed at 2.13%

- Euro up 0.2% to $0.9813

- Brent Futures up 0.1% to $94.53/bbl

- Gold spot up 0.0% to $1,712.81

- U.S. Dollar Index down 0.24% to 111.9

Top Overnight News from Bloomberg

- Investors poured the most money into cash since April 2020 on fears of a looming recession, but stocks could see further declines as they don’t fully reflect that risk, say Bank of America Corp. strategists

- Underlying inflation in the euro area is increasingly driven by higher demand, according to the European Central Bank, which has listed the trend among reasons to lift borrowing costs

- Inflation expectations among euro-zone consumers held steady in August, according to the European Central Bank, which has been raising interest rates in the face of record price gains

- The European Central Bank is ratcheting up pressure on some banks to keep 2022 bonuses in check amid fears about the darkening economic outlook, according to people with knowledge of the matter

- A report by the Recruitment & Employment Confederation showed UK companies are starting to impose hiring freezes because of pessimism about the outlook, and employees are deciding “stay put” rather than apply for other jobs

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were lower as the region followed suit to the weak performance seen in global counterparts with risk appetite sapped amid the slew of hawkish Fed rhetoric and with participants awaiting the key US jobs data. ASX 200 was subdued by underperformance in the real estate sector and after the RBA Financial Stability Review noted financial stability risks have increased globally and that some households are already feeling the strain from higher rates which is likely to persist for some time. Nikkei 225 was pressured and briefly dipped below the 27,000 level after disappointing data in which Household Spending showed a surprise M/M contraction and with wage growth softer than previous. Hang Seng declined amid weakness in property and tech stocks with sentiment also not helped by reports that the US is to announce new measures that will effectively halt some exports of US equipment to Chinese firms making advanced NAND and DRAM memory chips.

Top Asian News

- BoK said it will maintain its stance of raising interest rates going forward to combat inflation which is expected to remain in the 5-6% range for a considerable period of time, according to Yonhap.

- RBA Financial Stability Review stated that financial stability risks have increased globally and markets are stressed by synchronised policy tightening, geopolitical tension, higher USD and rising energy prices. RBA also stated that stability risks would be magnified by further substantial tightening in global markets and some households are already feeling the strain from higher rates which is likely to persist for some time.

- Japanese top currency diplomat Kanda says has never felt a limit to ammunition for currency intervention, making various steps so as not to face a limit to ammunition when it comes to FX intervention, via Reuters.

- Malaysia Cuts Personal Income Tax by 2 Percentage Points

- Tycoon Faces Key Vote for Plan to Tap Vedanta Cash Reserves

- Gold Set for Largest Weekly Gain Since March as Jobs Data Loom

- Taiwan Exports Shrink for First Time Since 2020 on Global Slump

European bourses are modestly on the backfoot, though have trimmed this slightly as the session progresses, in limited newsflow pre-NFP. Nonetheless, are still on track to conclude the week with upside of just over 2% WTD for the Stoxx 600. Stateside, futures are similarly contained and lie either side of the unchanged mark with NQ -0.1% modestly lagging amid yield upside as officials pushback on an imminent pivot. ECB recently told some banks to exercise restraint on pay and dividends amid concerns about a potential wave of defaults, according to Bloomberg.

Top European News

- UK PM Truss is watering down former UK PM Johnson’s plans to cut 91k civil service jobs, according to FT.

- Irish Foreign Minister Coveney says the new air of positivity has created a flicker of optimism, lots of issues yet to be resolved (re. Brexit/N. Ireland).

- Greece Should Take Turkey’s Warnings Seriously, Erdogan Says

- Credit Suisse Short Bets Soar Weeks Ahead of Strategy Review

- Brexit Grudges Recede as Truss Makes Inroads With EU Allies

- New Jupiter Boss to Shake Up Dozens of Funds and Cut CIO Role

- Swedish Housing Market Slump Deepens on Rate, Energy Worries

Geopolitics

- US President Biden said the nuclear ‘Armageddon’ threat is back for the first time since the Cuban Missile Crisis, according to AFP News Agency.

- Japanese government spokesperson Kihara said Japan is to impose additional sanctions against Russia and will freeze assets of more Russians after the annexation of parts of Ukraine, according to Reuters.

- US and South Korea are to conduct joint maritime drills involving the US aircraft carrier off the east coast on October 7th-8th, while the South Korean military said it will continue to strengthen its abilities to respond against North Korean provocation through joint drills, according to Yonhap.

- US forces conducted an airstrike in northern Syria on Thursday which killed Islamic State leader Abu-Hashum Al-Umawi and another IS official, according to Reuters.

- Turkish President Erdogan in a call with Russian President Putin discussed improving bilateral relations, according to the Turkish readout via Reuters.

FX

- Typically tense pre-NFP trade has seen the DXY briefly dip below 112.00, to a 111.94 low, before regathering itself and holding marginally above the figure.

- Action that comes to the benefit of peers across the board with GBP the primary beneficiary, Cable to a 1.1218 peak, but closely followed by other activity FX.

- EUR/USD is more contained given a hefty amount of OpEx around today’s NY Cut, with participants also cognisant of worrying German data.

- After yesterday’s relative outperformance, the CHF and NZD are the relative laggards and are currently unchanged on the session.

- CNB Minutes (Sep): Mora and Holub voted for a 75bp hike, other members regarded rates as commensurate with the current situation. Consensus that inflation was probably close to peaking.

- HKMA purchases HKD 1.57bln from the market as the HKD hits the weak end of its trading range.

Fixed Income

- Core benchmarks dipped to lows amid the morning’s German data release, with Import Prices lifting again, though have gained some poise since in quiet trade.

- Currently, Bunds are towards the mid-point of a ~70tick range with similarly settled action in USTs and Gilts before US data & Fed speak.

- As such, yields are elevated but off highs of 3.85%, 2.16% & 4.22% for US, German and UK 10yrs respectively.

Commodities

- WTI and Brent are off highs but still holding onto gains of around USD 0.50/bbl and are at the top-end of the week’s USD 86.35/bbl – 95.00/bbl parameter in Brent Dec’22.

- For today, the main potential catalyst is the EU’s informal meeting of heads of state. A gathering which is focused on “Russia’s war in Ukraine, energy and the economic situation.”

- US Secretary of State Blinken said the US will not do anything that infringes upon its interests and is reviewing a number of response options when asked about ties with Saudi Arabia and OPEC+ cuts, according to Reuters.

- US Republican Senator Grassley will seek to add the NOPEC bill to the defence policy bill, according to Reuters.

- OPEC Sec Gen says oil production capacity freed up by the latest production reductions could allow nations to intervene in the event of any crises in the oil market, according to Al Arabiya.

- Spot gold is little changed overall having derived some very brief upside from the DXY’s move below 112.00; however, the metal remains capped by the 50-DMA.

US Event Calendar

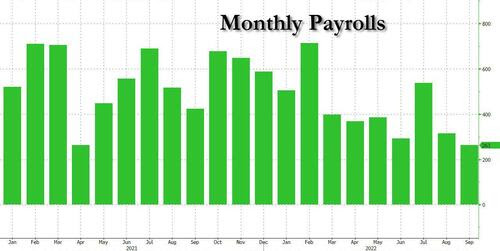

- 08:30: Sept. Change in Nonfarm Payrolls, est. 255,000, prior 315,000

- Change in Private Payrolls, est. 275,000, prior 308,000

- Change in Manufact. Payrolls, est. 20,000, prior 22,000

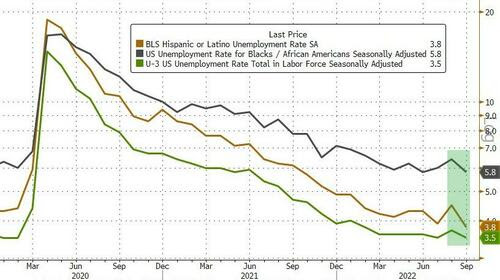

- Unemployment Rate, est. 3.7%, prior 3.7%

- Underemployment Rate, prior 7.0%

- Labor Force Participation Rate, est. 62.4%, prior 62.4%

- Average Hourly Earnings YoY, est. 5.0%, prior 5.2%; Average Hourly Earnings MoM, est. 0.3%, prior 0.3%

- Average Weekly Hours All Emplo, est. 34.5, prior 34.5

- 10:00: Aug. Wholesale Trade Sales MoM, est. 0.5%, prior -1.4%;

- Wholesale Inventories MoM, est. 1.3%, prior 1.3%

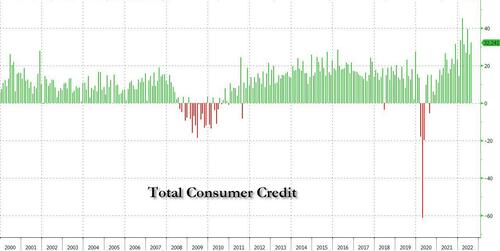

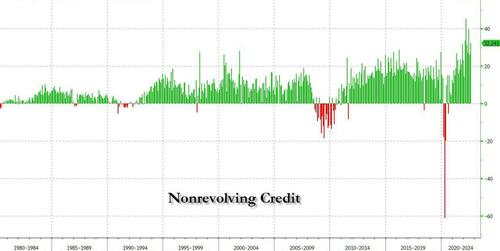

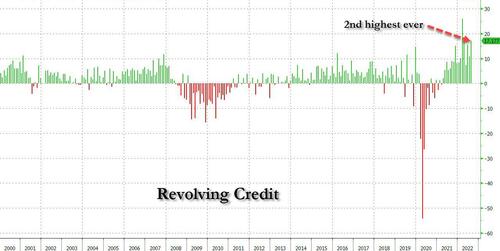

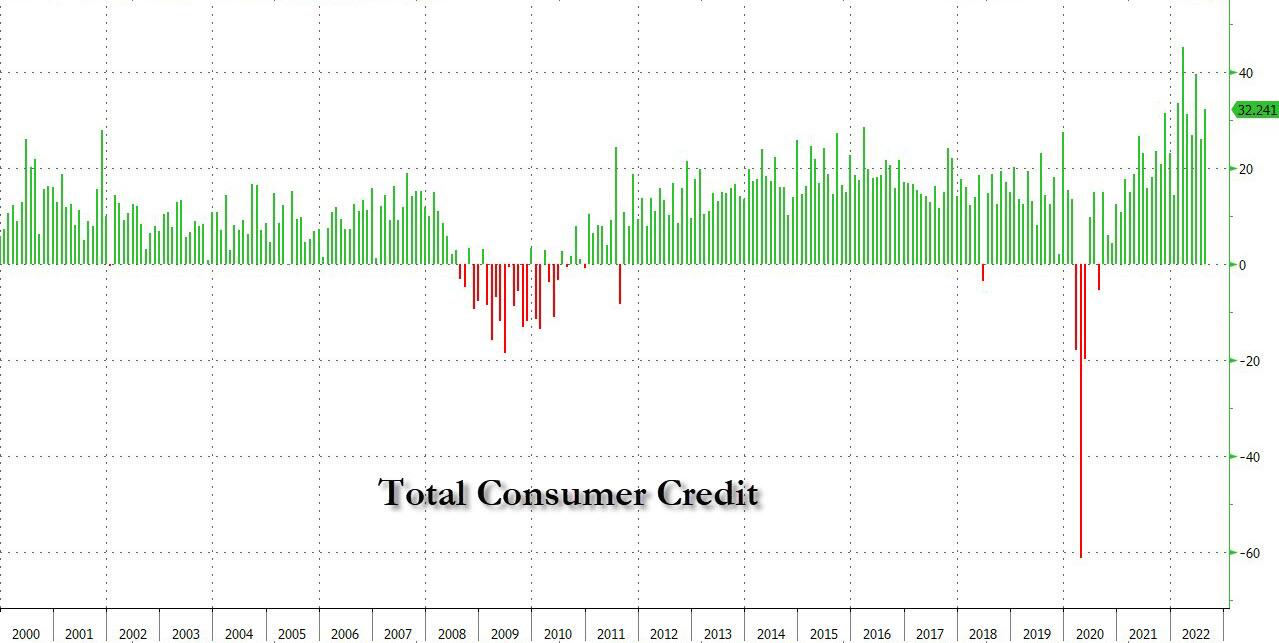

- 15:00: Aug. Consumer Credit, est. $25b, prior $23.8b

Fed speakers

- 10:00: Fed’s Williams Speaks in Moderated Q&A

- 11:00: Fed’s Kashkari Discusses Agriculture, Food and Inflation

- 12:00: Fed’s Bostic Discusses Inequality

DB’s Jim Reid concludes the overnight wrap

In these stressful markets I’ve kept my personal anecdotes to a minimum but I have a few butterflies this morning as I have a big 36 hole golf matchplay final on Sunday. After 2 major knee operations in the last 12 months, 4 back injections in the last 18, a long period with a trapped nerve in my shoulder, a numb hand and countless rounds of physio, I’ve eventually played the best golf of my life this year and have got down to a 2.6 handicap. I have to give my opponent 16 shots over 36 holes though so it’s going to be hard. A couple of weeks later I’m also in a scratch final with no shots given. However the problem is my opponent is off +1. My current mid-life crisis obsession (after piano, cycling, etc. previously) is to get down to scratch. I suspect I’ll fail as I don’t hit it far enough. However I’m doing weights and speed training which is why I keep getting injured. My wife despairs at my obsessiveness most of the time but it keeps me going!!

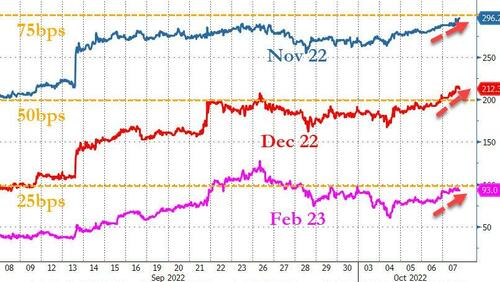

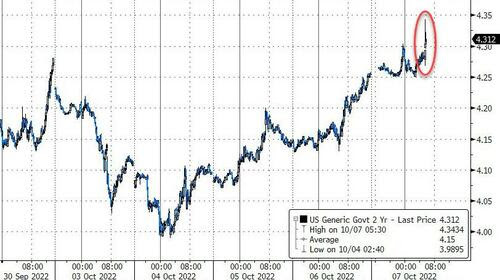

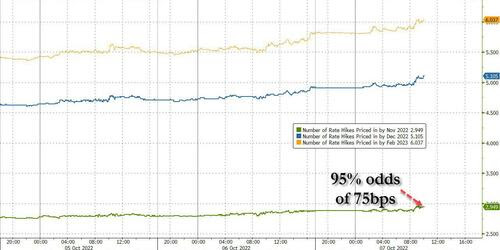

We’re all going to be obsessing about payrolls today and then US CPI next week. Clearly the latter has more potential to shape trading over the next few weeks but the former is always a big event. In terms of what to expect from today’s jobs report, our US economists are forecasting that nonfarm payrolls grew by +275k in September. That’s slightly above the +250k consensus print, but if realised that would still be the slowest pace of monthly job growth since April 2021. However versus long-term average that would still be a hefty print even if you adjust for population. Our economists think that’ll be enough to push the unemployment rate down a tenth to 3.6%, especially given the three-tenths rise in the participation rate in August. When it comes to the Fed, both futures and our US economists see a +75bps move as the likely outcome at the next meeting, and a strong report today would cement those expectations, not least given the recent chatter that the Fed might slow down their pace of hikes earlier than anticipated.

Today’s print comes as the mood has soured again over the last 48 hours even if the prior 48 hours were spectacular enough to leave us notably stronger for the week still for risk even if bonds have given up their gains.

Yesterday saw a fresh selloff in stocks and bonds alongside further dollar strength after multiple Fed speakers pushed back on speculation that they’re about to ease up on hiking rates. That wasn’t helped by the news on the inflation side either, with oil prices reaching a one-month high, whilst commodities more broadly advanced for a 4th day running.

Going through some of these themes we’ll start with the Fed, since yesterday saw an array of speakers who reiterated hawkish talking points from the get-go. In particular, Minneapolis Fed President Kashkari said that “Until I see some evidence that underlying inflation has solidly peaked and is hopefully headed back down, I’m not ready to declare a pause. I think we’re quite a ways away from a pause.” So that adds to the previous day’s FOMC members who similarly pushed back on an imminent reversal. Later in the session, we heard from Presidents Evans and Mester, Governors Cook and Waller. They all held the line, pushing back on any pivot pricing. Notably, President Evans, another reformed dove, said rates would be near 4.5-4.75% by the spring of next year, with the market pricing terminal rates at the lower end of that range at 4.55% as of March.

Against that backdrop, investors continued to price out the chances of a Fed pivot next year, with Fed funds futures for December 2023 up +13.4bps on the day to 4.33%, their biggest one-day increase since the September FOMC itself. Now that’s still beneath the 4.6% that the FOMC had in their dot plot for end-2023 a couple of weeks back, and the 4.50% the market priced in 8 days ago, but the moves over the last couple of days do suggest they’re having some success in pushing back on the rate cut speculation. The impact of that worked its way through to Treasury yields, with the 10yr yield up +7.1bps to 3.82%, having been led by a +6.8bps rise in the real yield to 1.61%. That’s still some room below the late September intraday peak of 4.02%, but quite a bounce from Tuesday’s intraday low of 3.56%. That range is all within seven days, such is the recent volatility in bond markets. This morning in Asia, yields on the 10yr are just a tad lower as we go to press.

It’s worth keeping an eye on long-end Gilts as they continue to unwind some of the once in a lifetime sized rally from 5% last week after the BoE stepped in. 30yr yields closed at 4.29% having been as low as 3.62% on Monday. Anecdotal evidence points to the LDI saga still impacting that end of the curve.

The hawkish Fed rhetoric impacted on equities as well, with the S&P 500 (-1.02%) and the STOXX 600 (-1.25%) each seeing a noticeable pullback. The NASDAQ proved more resilient falling only -0.68%. In addition, the VIX index of volatility picked up again following a run of 4 consecutive declines, moving up +1.97pts to finish above 30 again at 30.52.

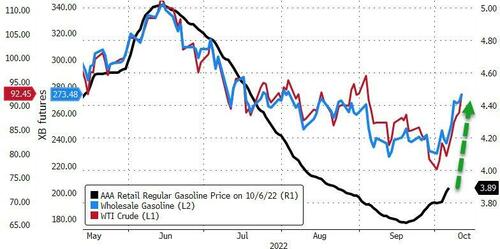

One factor that won’t be welcomed by policymakers is the latest rise in commodity prices, with Brent crude (+1.12%) and WTI (+0.79%) oil prices rising for a 4th day running, which follows the decision by the OPEC+ group to cut their production levels the previous day. In response, US President Biden said that his reaction was “Disappointment. And we’re looking at what alternatives we may have”. In the meantime, there was a modest downtick in European natural gas futures (-3.91%) to €167 per megawatt-hour. Speaking of which, our research colleagues in Frankfurt published their latest gas supply monitor yesterday (link here), in which they update their scenarios for this winter to reflect the latest developments. They also preview what to expect from the informal meeting of EU leaders taking place in Prague today.

Staying on Europe, sovereign bonds lost ground across the continent in line with the US moves, with yields on 10yr bunds (+5.4bps), OATs (+4.4bps) and BTPs (+4.7bps) all moving higher. That follows a similar dose of scepticism from investors about whether the ECB might pivot alongside the Fed, and the deposit rate priced in by overnight index swaps for June 2023 moved up more than 15bps for the second straight day, increasing +15.5bps yesterday to 2.89%. Those moves also came as we got the accounts from the ECB’s September meeting when they hiked by 75bps, which indicated that “some members” had preferred to only hike by 50bps, although “all members joined a consensus to raise the three key ECB interest rates by 75 basis points”. There was also a view that policy rates were still “significantly below the neutral rate”, even with the latest rate hike”, and it said that chief economist Lane had “stressed that price pressures were extraordinarily high and likely to persist for an extended period.”

Back in the UK, there were fresh signs that the recent market turmoil was impacting the mortgage market, after Moneyfacts reported that the average 5yr fixed mortgage rate was now above 6%. That puts it at its highest level since February 2010, and follows the previous day’s news that the 2yr fixed rate had also passed the 6% milestone. Furthermore, there were some warnings on the energy front, with National Grid saying that there was one scenario (although not its base case) that could see 3-hour power cuts if there wasn’t enough gas supply. The more negative newsflow occurred as sterling continued to lose ground against the US Dollar again, with a further -1.45% fall that brings its declines over the last two sessions to -2.76%. And gilts struggled as well, and not just at the long-end as discussed earlier, with 10yr yields up +13.3bps on the day to 4.15%.

Asian equity markets are also declining this morning with the Hang Seng (-1.13%) leading losses, pulling back from a strong rebound earlier this week with the Nikkei (-0.59%) also trading in negative territory. Meanwhile, the Kospi (+0.06%) is swinging between gains and losses with the index heavyweight Samsung Electronics downbeat 3Q preliminary earnings forecast weighing on sentiment. Elsewhere, markets in China are closed for the National Day holiday.

Looking forward, stock futures in the US are fluctuating with contracts tied to the S&P 500 (+0.03%) and NASDAQ 100 (+0.04%) just above flat ahead of the big day.

Early morning data showed that Japan’s real wages (-1.7% y/y) fell in August for the fifth consecutive month, following a revised -1.8% fall in July. At the same time, household spending (+5.1% y/y) increased in August (v/s +6.7% expected) following a +3.4% gain in July as the economy continued to recover from COVID-19 restrictions albeit with rising prices probably preventing further gains.

Ahead of today’s US jobs report, the weekly initial jobless claims for the week ending October 1 came in at 219k (vs. 204k expected), although there was a -3k downward revision to the previous week, without any apparent impact from the recent hurricane, which our US econ team believes will show up in next week’s data. Elsewhere, German factory orders contracted by more than expected in August, falling -2.4% (vs. -0.7% expected), but there was a sharp upward revision to the previous month, as the data now showed a +1.9% expansion (vs. -1.1% previously).

To the day ahead now, and the highlight will likely be the aforementioned US jobs report for September. Otherwise, data releases include German industrial production and Italian retail sales for August. From central banks, we’ll hear from the Fed’s Williams, Kashkari and Bostic, as well as BoE Deputy Governor Ramsden. Finally, EU leaders will be meeting in Prague.

AND NOW NEWSQUAWK

Tentative trade awaiting NFP and Fed speak for fresh ‘pivot’ guidance – Newsquawk US Market Open

FRIDAY, OCT 07, 2022 – 06:21 AM

- European bourses are modestly on the backfoot, though have trimmed this slightly as the session progresses, in limited newsflow pre-NFP.

- Stateside, futures are similarly contained and lie either side of the unchanged mark with NQ -0.1% modestly lagging amid yield upside

- Typically tense pre-NFP trade has seen the DXY briefly dip below 112.00, to a 111.94 low, before regathering itself and holding marginally above the figure.

- Core benchmarks dipped to lows amid the morning’s German data release, with Import Prices lifting again, though have gained some poise since in quiet trade.

- WTI and Brent are off highs but still holding onto gains of around USD 0.50/bbl and are at the top-end of the week’s USD 86.35/bbl – 95.00/bbl parameter in Brent Dec’22.

- Fed’s Mester (2022/2024) and Waller (voter) spoke overnight and added to the pivot-pushback

- Looking ahead, highlights include US & Canadian jobs reports, BoE’s Ramsden, Fed’s Williams, Kashkari, Bostic

As of 10:55BST/10:55ET

View the full premarket movers and news report.

Or why not try Newsquawk’s squawk box free for 7 days?

LOOKING AHEAD

- Looking ahead, highlights include US & Canadian jobs reports, BoE’s Ramsden, Fed’s Williams, Kashkari, Bostic

- Click here for the Week Ahead preview.

- Click here for the newsquawk NFP Preview.

GEOPOLITICS

- US President Biden said the nuclear ‘Armageddon’ threat is back for the first time since the Cuban Missile Crisis, according to AFP News Agency.

- Japanese government spokesperson Kihara said Japan is to impose additional sanctions against Russia and will freeze assets of more Russians after the annexation of parts of Ukraine, according to Reuters.