OCT 26/GOLD PRICE ROSE BY $11.65 TO $1665.20//SILVER PRICE ROSE 13 CENTS TO $19.50//PLATINUM PRICE ROSE $32.05 TO $953.20//PALLADIUM PRICE UP $25.75 TO $1953.25//MASSIVE AMOUNTS OF GOLD AND SILVER LEAVE THE COMEX VAULTS//HUGE GOLD QUEUE JUMP OF 3 TONNES AS NEW STANDING EXCEEDS 76 TONNES FOR OCTOBER///COVID UPDATES: DR PAUL ALEXANDER//VACCINE IMPACT//VACCINE INJURY/WEALTHY CHINESE TRYING TO FIGURE OUT HOW TO GET THEIR MONEY OUT OF THE COUNTRY//EU IS SET TO REFUSE HANDING OUT MONEY TO POLAND AND THAT SHOULD CAUSE A POLAND-EXIT//UPDATES ON THE FREEZING OF EUROPE//FEDDERMAN SIMPLY AWFUL IN DEBATE WITH DR OZ //LOOKS LIKE THE REPUBLICANS WILL WIN THE SENATE AND THE HOUSE//SWAMP STORIES FOR YOU TONIGHT..

132 C SG AMERICAS 2 323 C HSBC 29 661 C JP MORGAN 50 880 C CITIGROUP 34 880 H CITIGROUP 53

TOTAL: 84 84 MONTH TO DATE: 23,391

JPMORGAN STOPPED 0/84

GOLD: NUMBER OF NOTICES FILED FOR OCT CONTRACT: 84 NOTICES FOR 8400 OZ or 0.01264 TONNES

total notices so far: 23,391 contracts for 2,339,100 oz (72.756 tonnes)

SILVER NOTICES: 4 NOTICE(S) FILED FOR 20,000 OZ/

total number of notices filed so far this month 456 : for 2,280,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $11.65

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////NO CHANGE IN GLD INVENTORY /INVENTORY REMAINS AT 928.39 TONNES

INVENTORY RESTS AT 928.39 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 13 CENTS

AT THE SLV// :/BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A HUGE WITHDRAWAL OF 1.013 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 486.670 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 1114 CONTRACTS TO 139,085 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE STRONG GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.17 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS/HFT WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.17)., BUT UNSUCCESSFUL IN KNOCKING OFF ANY SPEC LONGS, AS WE HAD AN ATMOSPHERIC GAIN IN OUR TWO EXCHANGE OF 1397 CONTRACTS. HUGE SPECS CONTINUE TO ADD TO THEIR SHORTFALLS FROM WHICH OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. SOME SPEC LONGS ADDED TO THEIR POSITIONS

WE MUST HAVE HAD: I) ZERO SPECULATOR SHORT COVERINGS BUT HUGE SHORT ADDITIONS ////CONTINUED BANKER OI COMEX ADDITIONS /// CONSIDERABLE NEWBIE SPEC LONG ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.580 MILLION OZ FOLLOWING AN 35,000 OZ QUEUE. JUMP / // V) GIGANTIC SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: –33

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS OCT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT:

TOTAL CONTRACTS for 20 days, total 56,505 contracts: 28.252 million oz OR 1.413MILLION OZ PER DAY. (282 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 28.252 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 28.252 MILLION OZ INITIAL

RESULT: WE HAD A GIGANTIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1147 WITH OUR $0.17 GAIN IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 250 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR OCT. OF 1.580 MILLION OZ FOLLOWED BY TODAY’S 35,000 QUEUE JUMP .. WE HAD AN ATMOSPHERIC SIZED GAIN OF 1397 OI CONTRACTS ON THE TWO EXCHANGES FOR 6.985 MILLION OZ..

WE HAD 4 NOTICE(S) FILED TODAY FOR 20,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GIGANTIC SIZED 11,662 CONTRACTS TO 456,072AND CLOSER TO FROM TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -136 CONTRACTS.

.

THE HUGE SIZED INCREASE IN COMEX OI CAME DESPITE OUR SMALL GAIN IN PRICE OF $3.85//COMEX GOLD TRADING/TUESDAY // ZEERO SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION AND CONSIDERABLE SPEC SHORT ADDITIONS BUT ZERO SPEC SHORT COVERINGS. // CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR OCT. AT 66.099 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE QUEUE. JUMP OF 79800 OZ//NEW STANDING 76.217TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $3.85 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A GIGANTIC SIZED GAIN OF 14,337 OI CONTRACTS 44.17 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2539 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 456,072

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 14,337 CONTRACTS WITH 11,798 CONTRACTS INCREASED AT THE COMEX AND 2539 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 14,201 CONTRACTS OR 44.17 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2539) ACCOMPANYING THE GIGANTIC SIZED GAIN IN COMEX OI (11,662): TOTAL GAIN IN THE TWO EXCHANGES 14,201 CONTRACTS. WE NO DOUBT HAD 1) STRONG SPECULATOR SHORT ADDITIONS// CONTINUED GOOD BANKER ADDITIONS/// ZERO SPEC SHORT COVERINGS// STRONG NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 66.099 TONNES FOLLOWED BY TODAY’S 79,800 OZ QUEUE. JUMP ///NEW STANDING 76.217 TONNES//. 3) ZERO LONG LIQUIDATION //// //.,4) HUGE SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT. :

48,274 CONTRACTS OR 4,827,400 OZ OR 150.15 TONNES 20 TRADING DAY(S) AND THUS AVERAGING: 2413 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAY(S) IN TONNES: 150.15 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 150.15/3550 x 100% TONNES 4.22% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 150.15 TONNES INITIAL ( MUCH SMALLER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GIGANTIC SIZED 11414CONTRACT OI TO 139,085 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 250 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 250 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 250 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1114 CONTRACTS AND ADD TO THE 250 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN ATMOSPHERIC SIZED GAIN OF 1364 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 6.820 MILLION OZ//

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

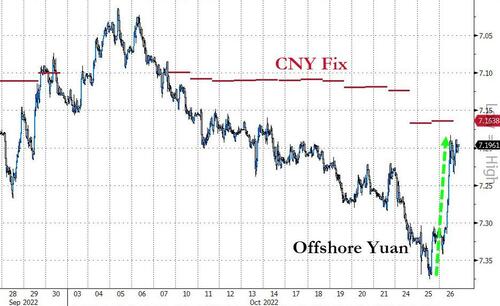

SHANGHAI CLOSED UP 23.22 PTS OR 0.78% //Hang Seng CLOSED DOWN 152,08 OR 1.00% /The Nikkei closed UP 181.56PTS OR 0.67% //Australia’s all ordinaires CLOSED UP 0.16% /Chinese yuan (ONSHORE) closed UP TO 7.1743 //OFFSHORE CHINESE YUAN DOWN 7.1972// /Oil DOWN TO 86.07 dollars per barrel for WTI and BRENT AT 94.09 / Stocks in Europe OPENED ALL MIXED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A HUGE SIZED 11,662 CONTRACTS TO 456,072 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS HUGE COMEX INCREASE OCCURRED DESPITE OUR SMALL RISE IN PRICE OF $3.85 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2539 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF OCT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2539EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC : 2539 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2539 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GIGANTIC SIZED TOTAL OF 14,201 CONTRACTS IN THAT 2539LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A HUGE SIZED COMEX OI GAIN OF 11,798 CONTRACTS..AND THIS GOOD SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR SMALL GAIN IN PRICE OF GOLD $3.85//WE HAD CONSIDERABLE SPEC SHORTS ADDITIONS, WITH BANKERS AS BUYERS OF COMEX GOLD CONTRACTS. WE ALSO HAD HUGE ADDITIONAL NEWBIE SPECS GOING LONG

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING OCT (76.217),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 76.217 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $3.85) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS// SPEC SHORTS ADDED TO THEIR POSITIONS AS WE HAD A GOOD SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 2379 CONTRACTS // WE HAVE REGISTERED A FAIR GAIN OF 14.214 PAPER TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR OCT. (76.217 TONNES)…THIS WAS ACCOMPLISHED WITH OUR RISE IN PRICE OF $3.85

WE HAD +136 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 14,337 CONTRACTS OR 1,433,700 OZ OR 44.59 TONNES

Total monthly oz gold served (contracts) so far this month

23,391 notices 2,339,100 72.756 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

customer withdrawals:3

ii) Out of Brinks 88,897.520 OZ (2765 kilobars)

iii) Out of JPM 267,542.625

iv) Out of HSBC: 4,227.356 oz

total: 360,697.501 oz

total in tonnes: 11.218 tonnes

Adjustments: 5// dealer to customer//huge activity

i)Delaware: 5505.065 oz

ii) Out of Brinks 7,499.956 oz

iii) Out of JPMorgan: 112,594.582 oz

iv) Out of HSBC: 13,173,939 oz

v) Out of Manfra 16,767.314 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCT we have an oi of 1197 contracts having GAINED 794 contracts . We had 4 contracts

filed on TUESDAY, so we GAINED A STRONG 798 contracts or an additional 79,800 oz will stand in this active delivery month of Oct. From this point

we should gain in total gold standing through to the end of Oct.( This is queue jumping and in reality it is the exercising of London based EFP;s for gold at the comex)

November SHOCKINGLY GAINED 210 contracts to stand at 3833 (WE ARE GOING TO HAVE AN EXTRAORDINARILY LARGE NOV.GOLD DELIVERY)

December GAINED 3704 contracts DOWN to 359,945

We had 84 notice(s) filed today for 8400 oz FOR THE OCT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 50 notices were issued from their client or customer account. The total of all issuance by all participants equate to 84 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT /2022. contract month,

we take the total number of notices filed so far for the month (23,391) x 100 oz , to which we add the difference between the open interest for the front month of (OCT 1197 CONTRACTS) minus the number of notices served upon today 84 x 100 oz per contract equals 2,450,400 OZ OR 76.217 TONNES the number of TONNES standing in this active month of OCT.

thus the INITIAL standings for gold for the OCT contract month:

No of notices filed so far (23,391) x 100 oz+ (1197) OI for the front month minus the number of notices served upon today (84} x 100 oz} which equals 2,450,400 oz standing OR 76.217 TONNES in this NON active delivery month of OCTOBER.

TOTAL COMEX GOLD STANDING: 76.217 TONNES (A HUMONGOUS STANDING FOR OCT (GENERALLY THE POOREST DELIVERY MONTHS FOR AN ACTIVE MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 456 x 5,000 oz = 2,280,000 oz

to which we add the difference between the open interest for the front month of OCT(240) and the number of notices served upon today 4 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT./2022 contract month: 456 (notices served so far) x 5000 oz + OI for front month of OCT (240) – number of notices served upon today (4) x 5000 oz of silver standing for the OCT contract month equates 3,460,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

OCT 26/WITH GOLD UP $11.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 25/WITH GOLD UP $3.85: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 928.39 TONNES

OCT 24/WITH GOLD DOWN $1.80 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES FROM THE GLD////INVENTORY RESTS AT 928.10 TONNES

OCT 21/WITH GOLD UP $19.10: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 930.99 TONNES

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

TONNES

GLD INVENTORY: 928.39 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

OCT 26/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.013 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 486.670 MILLION OZ./.

OCT 25/WITH SILVER UP 17 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.083 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.683 MILLION OZ/

OCT 24/WITH SILVER UP 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .553 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.610 MILLION OZ//

OCT 21/WITH SILVER UP 43 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .46 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 486.163MILLION OZ//

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: AWITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

CLOSING INVENTORY 486.670 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Roubini Warns Of Imminent Dollar Crash: The Fed Is Going To “Wimp Out” In The Inflation Fight

Economist Nouriel Roubini says Federal Reserve is going to “wimp out” on the inflation fight and that will lead to a dollar crash.

Roubini is the Professor Emeritus at the Stern School of Business, New York University. He recently appeared on Bloomberg Markets and Finance to talk about threats to the global economy.

Roubini predicted the housing bubble would pop in an IMF position paper in 2006. When asked if we were there again, he emphatically said, “Yes.”

Yes, we are here again. But in addition to the economic, monetary and financial risks — and there are new ones now, we’re going toward stagflation like we’ve never seen since the 70s — in the book, I point out that there are also geopolitical risks.”

These include possible confrontations with China and Russia, environmental risks, health risks, and technological risks. Roubini called it a confluence of “mega risks.”

You might not expect Roubini to talk like this. He served in the Clinton administration as a senior economist in the White House Council of Economic Advisers and then moved to the Treasury department as a senior adviser to Timothy Geithner who was undersecretary for international affairs at the time. Despite his work in a Democratic Party administration, he sounds a lot like Peter Schiff when it comes to his views on the trajectory of the economy.

Roubini pointed out the amount of debt in the global financial system. Debt to GDP has gone from 200% to 350% globally. In the US the debt to GDP ratio is higher than after the Great Depression and WWII. After the 2008 financial crisis and during the pandemic, Zombie households, corporations, banks and governments were bailed out by negative interest rates and quantitative easing.

This time around is different because we have so much debt and central banks like the Fed have to increase interest rates to fight inflation so that zombie institutions are going to go bankrupt. That’s why not only are we going to have inflation and stagflation, but we’ll have a stagflationary debt crisis.”

We had supply shocks in the 70s similar to those we’ve experienced in the post-pandemic era. But at that time in most of the developed world, debt ratios were low. There were no debt crises in developed nations. But we did see debt crises in Latin America because those countries like Brazil, Mexico and Argentina had borrowed too much. When Volker jacked up interest rates to 20%, they went bankrupt.

Today, we have the worst of the 70s. We have a massive amount of stagflationary negative supply shock … and at the same time, we have a debt ratio like we’ve never seen before. So, we get a stagflationary debt crisis.”

The IMF identifies around 40 emerging market countries on the verge of a sovereign debt crisis. And Roubini said we are starting to see these problems spilling to developed nations. He specifically mentioned the United Kingdom being forced to monetize reckless fiscal stimulus.

Right now, all central banks are playing tough, and talking tough, and acting tough – hawkish – because they have a problem of credibility. But in my view, there are two problems. One problem is if they try to get to 2% inflation, they cause a recession. And this recession is not going to be short and shallow. It is not going to be garden variety. It’s not going to be plain vanilla. It’s not going to be two quarters of negative growth and then inflation collapses and they can ease again. … It’s going to be a severe recession because of the debt ratio — because we’re going into fiscal and monetary tightening. And at the same time, not only do we have an economic crash, you’re going to have also a fiscal crash.”

Roubini called it a debt trap. There is so much private and public debt that any attempt to seriously fight inflation will ultimately cause a crash in financial markets.

And not just the stock market. That’s the least important. Credit markets and bond markets — And that crash and the financial crash feeds on the economic crash and vice versa. And therefore, they’re going to wimp out and they’re going to blink.”

The Bank of England already blinked. Roubini said the Federal Reserve is going to do the same.

Roubini also warns of an impending dollar crash. He said the greenback is at risk due to the twin deficits – budget and trade. He also mentions the weaponization of the dollar. But the real catalyst will be the Fed “wimping out.”

Once the Fed is going to essentially prevent an economic and financial crash – or try to prevent it by … stopping raising rates, even though inflation is too high, then the dollar is going to start to sharply weaken. That is going to be the trigger for it. Because what is raising the dollar is tight monetary policy.”

So, what can you do to protect yourself? Roubini recommends buying gold.

Gold has not done very well because you have tight monetary policy and a strong dollar. But if central banks are going to blink and wimp out, gold is going to rise in value.”

END

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

JPMorgan Chase Quietly Settles Whistleblower Case Involving Charges of Keeping Two Sets of Books and Improper Payments to Tony BlairBy Pam Martens and Russ Martens: October 26, 2022 ~It was a lawsuit that should have made front page headlines in every major newspaper in America and on the evening television news. Instead, as we predicted, it was quietly settled on Monday, just 10 business days before a trial was scheduled to begin. The dollar amount of the settlement was not disclosed. Yesterday, Wall Street’s paper of record, the Wall Street Journal, devoted a mere 299 words to the settlement and the details of the case.The lawsuit was filed in the federal district court for the Southern District of New York – a court system where mega Wall Street banks have a long history of evading justice.The plaintiff in the case is Shaquala Williams, an attorney and financial crimes compliance professional with more than a decade of experience at multiple global banks. The defendant is JPMorgan Chase – the largest bank in the U.S. which has been charged with five felony counts by the U.S. Department of Justice since 2014. Despite the bank’s unprecedented crime spree, federal regulators and the Board of Directors of JPMorgan Chase have allowed the same Chairman and CEO, Jamie Dimon, to continue to run the bank.Williams charged in her lawsuit that JPMorgan Chase was keeping two sets of books and effectively making a monkey out of the U.S. Department of Justice by brazenly flouting the non-prosecution agreement it had signed with the Justice Department in a previous case. It came out in her deposition testimony, which is part of the court record, that one of the people being paid under her allegation of the bank keeping two sets of books was Tony Blair, the former Prime Minister of the U.K. (See our report: JPMorgan Whistleblower Names Former U.K. Prime Minister Tony Blair in Court Documents as Receiving “Emergency” Payments from Bank.)In 2016 the Justice Department had charged that JPMorgan’s Asia subsidiary engaged in quid pro quo agreements with Chinese officials to obtain investment- banking business and had falsified internal documents to cover up the activities. The quid pro quo agreements involved the bank putting the children of high-ranking Chinese government officials on its payroll in order to enhance its business interests in China. In exchange for avoiding prosecution by receiving a non-prosecution agreement, the Justice Department required the bank to put in place compliance controls around third-party payments. Williams alleges, among other serious charges, that the so- called third-party payment controls were a sham and that when she blew the whistle to her superiors at the bank, JPMorgan Chase retaliated against her by firing her in October 2019.Williams alleges the following was happening inside the bank to subvert the required compliance controls:”If properly implemented, invoice controls would ensure that JPMorgan was not funding corruption by labeling corrupt third-party payments as legitimate business expenses.”Williams also raised concerns because the Bank had no requirements for the Compliance group to review invoices for red flags, high risk indicators, or other anomalies that indicate corrupt payments; because the Bank granted many third-party intermediaries exemptions from invoice requirements without documenting or explaining the basis for doing so; because the Bank had no controls to ensure that the entity requesting payment was the same third-party intermediary that had contracted with the Bank; because the Bank had no controls to ensure that the third party intermediary had a contract or other agreement with the Bank before performing the services; and because the Bank could not reconcile actual payments with the invoices…”Williams also raised concerns about JP Morgan’s inaccurate books and records. There were inconsistencies between the TPI [Third Party Intermediaries] payment records and the Bank’s centralized payment systems that feed into its general ledger. For example, a former government official (‘TPI1’) was a high risk JPMorgan third-party intermediary for Jamie Dimon (‘Dimon’), JPMorgan’s Chief Executive Officer. The Bank processed the invoices for TPI1 through the ‘emergency payment method.’ The Bank’s policies made clear that the ‘emergency payment method’ should be used for urgent payments critical to the day-to-day operations of Chase such as emergency utility bills ‘to prevent the lights from going out.’ The TPI1 invoices did not satisfy this standard, thus leaving the payment method open to unchecked corrupt payments and violations of the Bank’s accounting controls, the NPA, SEC Order, SEC rules and regulations, and provisions of Federal law relating to fraud against shareholders. Further, the payments as reflected in the general ledger did not correspond with management’s general or specific authorization for the invoice payments, thereby creating inaccurate records that also constituted violations of the NPA, the SEC Order, SEC rules and regulations and/or provisions of Federal law relating to fraud against shareholders.”Williams’ lawsuit contains this additional allegation related to these invoices:”Williams raised concerns that GACC [her department] was maintaining an alternate ledger of corrected transactions that did not match the uncorrected transactions on the official JPMorgan balance sheet.”Raising judicial transparency alarm bells in this case, on January 6 Senior U.S. District Court Judge Jed Rakoff signed a dangerous Protective Order covering the lawsuit. The Protective Order that Rakoff approved permits large parts of the documents obtained during discovery to be stamped “Confidential.” It also indicates that if anyone leaks those confidential documents, they can be held in contempt of court. It then says that “…the Court is unlikely to seal or otherwise afford confidential treatment to any Discovery Material introduced in evidence at trial, even if such material has previously been sealed or designated as Confidential.”Of course, if JPMorgan Chase knew it was never going to let this case go before a jury trial, then it had effectively gotten a Protective Order for eternity on key details of this case.The law firm representing Williams is Vladeck, Raskin, & Clark P.C., which describes itself as follows: “Because we are prepared to take cases to trial, we are frequently successful in negotiating resolutions for our clients short of litigation. In fact, some of our biggest successes are settlements you will not find on our website or in reported decisions.” That business model might be good for plaintiffs seeking a monetary settlement in order to get on with their lives and the bottom line of lawyers. But it subverts the public interest in seeing actual justice served against a powerful mega bank and serial lawbreaker on Wall Street.Despite the suggestion in the Protective Order that Rakoff “is unlikely to seal or otherwise afford confidential treatment to any Discovery Material introduced in evidence at trial,” there is this telling statement at Paragraph 16 of the Protective Order: “This protective order shall survive the termination of the litigation.”The law firm representing JPMorgan Chase in the matter is Morgan, Lewis & Bochius, whose former law partner, Kenneth Polite, now heads the Criminal Division of the Justice Department. When Polite was confirmed by the Senate for the position, Morgan Lewis immediately issued a press release bragging about Polite’s impressive new role. In that press release, the law firm also bragged about their roster of lawyers that had also traveled through the revolving door, writing:”For example, Matthew Miner, who prior to rejoining the firm in January 2020 served as the DOJ’s Deputy Assistant Attorney General; Sandra Moser previously served as former chief of the DOJ’s Fraud Section; Zane Memeger previously served as the United States Attorney for the Eastern District of Pennsylvania; and more than a dozen have served as AUSAs [Assistant U.S. Attorneys].”This lucrative revolving door between the Justice Department and outside counsel for the serial lawbreaking Wall Street mega banks needs to be closed by Congress. Until it is, justice will continue to erode in the United States.Related Article:There Are Three Separate Cases in Federal Court Accusing JPMorgan Chase of a Culture of Fraud

3.Chris Powell of GATA provides to us very important physical commentaries

Extremely important; the uSA dollar index will front run the Fed pivot

(Craig Hemke/GATA)

Craig Hemke at Sprott Money: All eyes on the dollar index

Submitted by admin on Tue, 2022-10-25 20:56Section: Daily Dispatches

8:56p ET Tuesday, October 25, 2022

Dear Friend of GATA and Gold:

Craig Hemke of the TF Metals Report, writing tonight at Sprott Money,argues that the U.S. dollar index will anticipate the ending of the Federal Reserve’s interest-rate-raising cycle, breaking below its moving averages. Hemke’s writes that such a point has not yet arrived but it will. His analysis is headlined “All Eyes on the Dollar Index” and it’s posted at Sprott Money here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

end

This new gold exchange will be very important for price discovery and is well needed due to the antics

of the LBMA and Comex

(zerohedge)

New gold exchange may transform India from price taker to price maker

Submitted by admin on Tue, 2022-10-25 09:12Section: Daily Dispatches

BSE Launches Electronic Gold Receipts

From the Press Trust of India via The Times of India, Mumbai Tuesday, October 25, 2022

NEW DELHI — Leading stock exchange BSE has launched its electronic gold receipts on its platform, a move that will help in efficient and transparent price discovery of the yellow metal.

The exchange has introduced two new products of .995 and .999 purity during the Muhurat trading on Diwali and trading will be in multiples of 1 gram and deliveries in multiples of 10 grams and 100 grams, the exchange said in a statement.

The announcement came after the exchange last month received final approval from the Securities and Exchange Board of India (SEBI) for introducing electronic gold receipts on its platform. …

The EGR platform will lead to greater assurance in the quality of gold supplied, efficient price discovery, and transparency in transacting. This can create a vibrant gold ecosystem in India by enabling actual fungibility of gold.

India is the second largest consumer of gold globally with annual gold demand of approximately 800-900 tonnes and holds an important position in the global markets.

The country has remained a price taker in the global markets and at present does not play any significant role in influencing the price-setting for the commodity.

A platform for EGR infuses transparency in gold spot transactions, enables India to emerge as the price setter, and would eliminate existing market inefficiencies.

Adams/North – The Criminals Have Less Than Fifteen Hours Left To Escape!

John Adams

6:55 AM (22 minutes ago)

to bcc: me

Senator Bragg will move a motion tomorrow in the Australian Senate between 11:15am and 12:15pm establishing an inquiry into ASIC via the Senate Economics References Committee.

Tomorrow is the ultimate policy test for every Australian Senator.

Martin North and I have published a quick video calling for the Australian people to let Senators know that we need an independent stand-alone ASIC inquiry!

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 7.1743

OFFSHORE YUAN: 7.1972

SHANGHAI CLOSED UP 23.22 PTS OR .78%

HANG SENG CLOSED UP 152.08 OR 1.00%

2. Nikkei closed UP 181.56 PTS OR 0.67%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 110.04/Euro RISES TO 1.0026

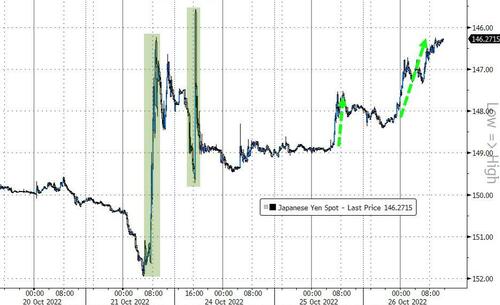

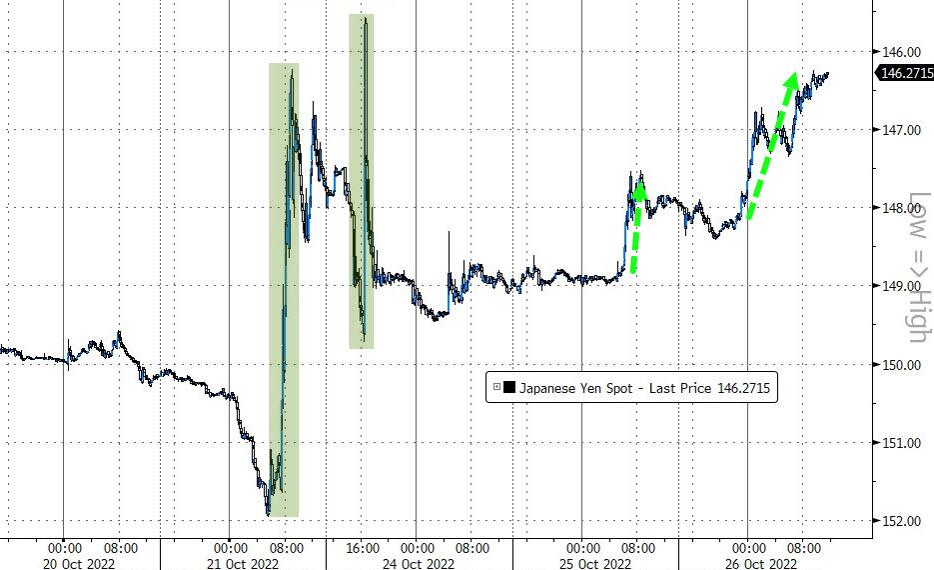

3b Japan 10 YR bond yield: FALLS TO. +.246/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 146.91/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP -// OFF- SHORE: UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.178%***/Italian 10 Yr bond yield FALLS to 4.410%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.28%…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.66//

3j Gold at $1670.15//silver at: 19.60 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 19/100 roubles/dollar; ROUBLE AT 61.29//

3m oil into the 86 dollar handle for WTI and 94 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 146.91DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9887–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.99139well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.055% DOWN 6 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 4.199% DOWN 7 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,61…GETTTING DANGEROUS

GREAT BRITAIN/10 YEAR YIELD: 3.6795%

end

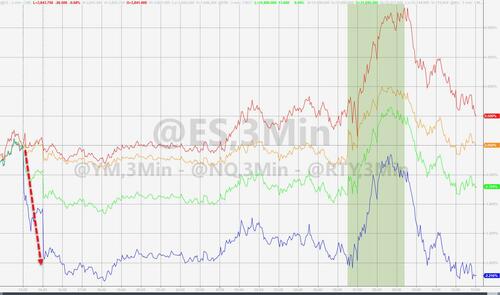

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Slide As Tech Giants Shed $300 Billion; Dollar Tumbles For 2nd Day

WEDNESDAY, OCT 26, 2022 – 08:05 AM

US index futures are lower this morning, set to give back some of Tuesday’s 1.6% sharp rally as technology giants’ earnings and outlook disappointed investors, stoking concerns about the industry’s profitability and raising new doubts over whether this year’s $5.5 trillion selloff is nearing a bottom.

S&P 500 futures dropped as much as 1.2%, and were down 0.7% at 7:30am while Treasuries extended gains, with the 10-year yield falling to around 4.05%. Nasdaq 100 fell more than 1.5% as megacap stocks tumbled in premarket trading after Alphabet’s 3Q miss and disappointing outlook from Microsoft and Texas Instruments weighed on the cohort, which is set to lose approximately $300 billion in market value if losses hold at open. The combined weight of the three companies amounts to more than 19% of the Nasdaq 100.

“Google and Microsoft reversed the joyful Tuesday sentiment,” said Ipek Ozkardeskaya, senior analyst at Swissquote Bank. She added that “there is nothing official pointing at a potential softening tone from the Fed just yet. Hence, the recent fall in the US dollar, and rebound in equities may not last.”

S&P 500 futures had rallied 1.6% on Tuesday, closing at the highest in over a month as yields pulled back amid growing speculation the Treasury will anounce buybacks soon. The dollar and the yield on 10-year Treasuries fell for a second day after a report that US home-price growth slowed by the most on record as a doubling of borrowing costs saps demand. The Bloomberg dollar index tumbled for a second day to its lowest level in three weeks…

… following apparent massive intervention by state banks in China seeking to stabilize the plunging yuan which surged by a record 1.8% against the dollar. Alas just like Japan, expect this intervention to fizzle soon as absent a Fed pibot, the yield differentials remain just too strong to swim against the strong USD current.

It wasn’t just the yuan that bounced: a near 5% rebound in a gauge of US-listed Chinese stocks on Tuesday helped claw back some of the record loss suffered in the wake of President Xi Jinping breaking with China’s collective leadership. Hong Kong’s tech gauge made strong gains for a second day but was still short of recouping Monday’s near 10% slide.

Meanwhile, the British pound held an advance against the greenback after the government said a much-anticipated fiscal statement will be delayed until November. Sterling rallied earlier after New Prime Minister Rishi Sunak named an experienced Cabinet to lead the UK through what he called a “profound economic crisis.”

In premarket trading, megacap stocks tumbled after disappointing quarterly updates from Alphabet (which missed across the board) and Microsoft (which had a lackluster forecast for sales growth in its Azure cloud-computing services business) wiped out about $295 billion in market value from the biggest US companies. Meanwhile, Twitter is set to open at the closest to Elon Musk’s offer since he launched his takeover bid in April. Among other tech stocks falling in sympathy: Apple -0.8%, Amazon.com -3.8%, Meta Platforms -3.9%, Adobe -1.3%, Oracle +0.8%, ServiceNow -6.7%, Workday -1.2%, Intuit -0.8%, Datadog -6.2%, Snowflake -5.7%. On the other end, bank stocks are mostly higher in premarket trading putting them on track to gain for a fourth straight session. In corporate news, Barclays traders beat estimates in the third quarter, offsetting steep declines for its investment bankers. Meanwhile, Goldman Sachs’s China-focused stock hedge fund clients had their second-worst trading day this year during Monday’s sell-off. Here are the most notable premarket movers:

Alphabet shares are down 6% in premarket trading after the tech juggernaut’s search-based ads business, which had largely dodged the digital-ad slowdown that hit rivals earlier this year, no longer seemed immune to macro headwinds. Among other megacaps Amazon -3.6%, Apple -0.6%, Tesla -1.2%, Meta -3%

Microsoft falls 6% after the software company reported its weakest quarterly sales growth in five years and gave a lackluster forecast for sales growth in its Azure cloud-computing services business.

Enphase Energy’s rises 5.6% as the solar firm’s quarterly results were strong and analysts retain confidence the company can continue to deliver robust growth and margins.

Texas Instruments falls 4.2% after the chipmaker’s fourth-quarter outlook signaled that the semiconductor industry’s slump is spreading beyond PCs and smartphones to the once-healthy industrial segment.

Chip stocks drop in US premarket trading after a disappointing quarterly forecast from Texas Instruments. Nvidia -2.4%, Qualcomm -0.8%, Advanced Micro Devices -1.9%, Intel -0.6%

Twitter is set to open at the closest to Elon Musk’s offer since he launched a bid in April, with shares trading as high as $53.18 against the offer price of $54.20, signaling investors’ confidence to see a deal get over the line on time is growing.

Skechers (SKX US) slumps 14% after the footwear brand reported weak 3Q EPS as well as 4Q profit and sales outlook. Morgan Stanley said “unique” pressures from freight and logistics offset the company’s top-line strength.

Invesco (IVZ US) falls 1.5% as Credit Suisse downgrades to underperform from neutral following the company’s third- quarter earnings, saying there are “too many adverse moving parts.”

Mattel (MAT US) slid 5.5% in US postmarket trading on Tuesday after the toymaker cut its adjusted EPS guidance for the year citing a “challenging macroeconomic environment.”

Juniper Networks (JNPR US) analysts were encouraged by the internet infrastructure company’s results and outlook for the fourth quarter. Juniper’s shares rose more than 4% in US afterhours

Stocks had been buoyed in recent days by mostly solid earnings and speculation the Federal Reserve may curb the pace of rate increases amid evidence its aggressive tightening is starting to weigh on the economy. About a quarter of S&P 500 companies have reported third-quarter results, with more than two-thirds beating (sharply lowered) analysts’ estimates despite the big-tech setback. But concern is mounting that slowing output will dent corporate profits in coming months.

“Yes we’re seeing earnings beats at the moment,” Mike Ingram, a senior market strategist at ActivTrades, said on Bloomberg TV. “But where I do start to have a bit of a problem at this juncture is that some earnings expectations going into next year are looking still a bit punchy.”

Goldman strategists said conditions for a trough in US equities are not visible yet as the asset class doesn’t fully reflect the latest rise in real yields and odds of a recession. None of the US assets tracked by Goldman are fully pricing in a recession, with equities factoring in the lowest odds of a “severe hawkish scenario,” the strategists wrote.

While the recent US data haven’t changed expectations that the Fed will hike interest rates by 75 basis points next month, they’re fueling speculation that an end to aggressive tightening may come next year. Analysts are also projecting challenges for now in Europe, with a jumbo hike of 75 basis points expected from the European Central Bank on Thursday. That’s even as many economists now reckon a recession has begun in the euro region.

“Sentiment’s still incredibly fragile. We do expect to see further market volatility,” Catherine Yeung, investment director at Fidelity International, said on Bloomberg Radio. “All eyes are still on the rate cycle globally speaking as well as where inflation does go. I think going into the end of the year, again, it’s going to be volatile.”

In Europe, the Stoxx Europe 600 index fluctuated and pared losses amid a raft of mostly positive earnings from heavyweights including Barclays Plc, Deutsche Bank and Mercedes-Benz. The technology sector dropped more than 1%, weighing on the benchmark, while brewer Heineken NV plunged after missing analysts’ estimates for volume growth; construction and miners leading while food and beverages, personal care and tech lag. Here are the biggest European movers:

UniCredit climbed as much as 4.2% after the Italian lender boosted its guidance for a second quarter, which Intesa analysts said could lead to an increase in consensus estimates.

Assa Abloy rises as much as 3.8% after 3Q Ebit and sales came in ahead of consensus owing to strong demand across all of the Swedish lockmaker’s geographies, further fueled by a sharp recovery for Global Technologies.

BASF rises as much as 2.2% as 3Q results contain few surprises following its pre-release and the share response is likely to be subdued, analysts say.

Skanska rises as much as 6.0% as co. saw a big beat on profitability in the third quarter, with stronger construction helping to offset weaker residential, Morgan Stanley writes.

ASM International’s shares slump as much as 10% after the semiconductor-equipment firm warned that the impact of sanctions on China could hurt more than 40% of its sales in that country. Peer ASML also declines.

Reckitt shares drop as much as 5.0%, underperforming the FTSE 100 Index, after a decline in 3Q sales volumes in the consumer goods company’s hygiene business — which had previously benefited from the increased focus on cleanliness during the pandemic — overshadowed a beat in total like-for-like sales.

Heineken falls as much as 11%, the most since March 2020, after reporting 3Q organic beer volume that missed estimates and as the brewer noted greater reasons to be cautious on the macroeconomic outlook

Santander shares declined as much as 5.0%, the most in a month as analysts flagged higher-than-expected costs and growing non-performing loans in Brazil and the US, which outweighed earnings that beat estimates.

Earlier in the session, Asian stocks climbed for a second day, as Chinese authorities sought to boost investor confidence and the dollar fell alongside Treasury yields. The MSCI Asia Pacific Index rose as much as 1.3%, with most markets advancing in the region as local currencies strengthened versus the dollar. Tech stocks were among the top sectoral gainers, bolstered by a slide in benchmark borrowing costs. Stocks in Hong Kong and China rebounded following a rout earlier in the week, as Chinese authorities said late Tuesday that they would ensure a healthy development of financial markets. The gauges pared gains as a lockdown in one of Wuhan city’s central districts reinforced investor concerns about China’s strict Covid Zero policy. The earnings season also gave a boost to tech stocks, including heavyweight chip shares. SK Hynix shares climbed even after an earnings miss, as traders reacted positively to the Korean firm’s announcement of a cut in capital expenditure. Samsung SDI’s quarterly profit beat estimates on robust electric-vehicle battery sales.

“We are likely going into a period when very bad earnings in Asia may be good news for some ‘optically cheap’ stocks as it might imply that earnings expectations also get washed out completely – on top of already low valuations,” said Chetan Seth, Asia Pacific equity strategist at Nomura Holdings Inc. “Low earnings expectations and low valuations is a good sign for eventual bottoming out in some of these stocks,” he added. More than 200 of the MSCI Asia index members tracked by Bloomberg have reported earnings so far, as analysts watch for the impact of China’s Covid lockdowns and the dollar’s strength on corporate profits. India markets are closed Wednesday. Overall, the Asian gauge remains down for the month and has lost almost 30% this year, hammered by risks including China’s slowdown and global monetary tightening.

Japanese stocks climbed for the third day, following a rise in the US cash market overnight as investors continued to monitor the flow of corporate earnings coming out this week. The Topix Index rose 0.6% to 1,918.21 as of market close Tokyo time, while the Nikkei advanced 0.7% to 27,431.84. Daiichi Sankyo Co. contributed the most to the Topix Index gain, increasing 2.9%. Out of 2,166 stocks in the index, 1,402 rose and 661 fell, while 103 were unchanged. The S&P 500 Index rallied for the third session through Tuesday. US futures slid during Asian trading hours on Wednesday, however, as post-market earnings from tech giants Microsoft and Alphabet disappointed. “Stock prices tend to settle down when actual earnings seasons begin, once a number of companies that gave out warnings show results that exceed their original forecasts,” said Hideyuki Suzuki, general manager at SBI Securities. “Japanese companies’ earnings will be the key focus this week and early next week as they will be in full swing.”

Australian stocks also gained for a third day as inflation accelerated. The S&P/ASX 200 index edged up 0.2% to close at 6,810.90, extending gains to a 3rd day and marking the highest close in almost three weeks. The property and utility sectors led the increase. The benchmark index pared some of its earlier gains after Australia’s annual headline inflation accelerated to a 32-year high in the third quarter, validating the Reserve Bank’s rapid policy tightening. Inflation is “public enemy number one” in Australia’s economy, Treasurer Jim Chalmers said.

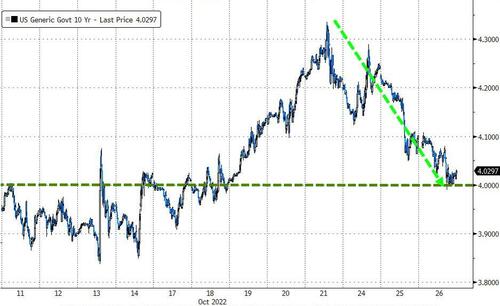

In rates, Treasury futures were off best levels of the day, although they remain richer by up to 6bp across long-end of the curve which bull flattens. US 10-year yields dropped as low as 4.02%, and were last around 4.055%, close to bottom of Tuesday session range and outperform bunds and gilts by 6.5bp and 7.5bp on the day; long-end led gains flattens 5s30s spread by almost 4bp on the day while 20s outperform further out with 10s20s30s fly richer by 2.4bp. Gains were seen overnight in Treasuries as stocks pared back portion of Tuesday rally following soft earnings from tech giants including Microsoft, Alphabet and Texas Instruments. Auction cycle resumes with $43b five-year at 1pm, follows Tuesday’s soft two-year sale which tailed by 1.2bp — auctions conclude with $35b seven-year Thursday. US session focused on five-year auction while Bank of Canada rate decision is at 10am New York. Bunds and gilts 10-year yields trim gains, back to unchanged on the day.

In FX, the dollar tumbled for a second day, providing relief across currencies. The pound surges to $1.16; the euro trades above parity against USD, while the yen rises to around 146.71/dollar. Offshore yuan gains 1.7% to 7.1831 per dollar. However, dollar weakness wasn’t able to lift US futures as S&P 500 falls 0.5% while Nasdaq 100 slips 1.4% on disappointing mega tech earnings.

The Pound rallied more than 1% to as high as $1.162 as it gained for a second day.

Euro advanced past parity with the US dollar for the first time since Sept. 20; overnight volatility in the euro shows traders are preparing for a relatively wide intraday range into the European Central Bank decision.

Australia’s dollar advanced, eventually finding traction as short-covering increased on expectation that local yields will recover after third-quarter CPI hit a 32-year high, putting the spotlight back on Reserve Bank pricing.

The yen jumped to 147 per dollar ahead of the Bank of Japan’s policy decision Friday, when monetary settings are expected to be kept unchanged. Meanwhile, the central bank boosted purchases of longer-dated government bonds as rising yields threatened to loosen its grip on the yield curve.

In commodities, oil was steady as an industry report showed a rise in US crude stockpiles and investors fretted about weaker demand amid slowing growth. Crude benchmarks were modestly firmer on the session despite initial downbeat performance in wake of readacross from US after-market earnings and on fresh COVID updates in China alongside the below Private Inventory release. WTI and Brent Dec’22 contracts reside at the top-end of 1.50/bbl parameters though remain capped by USD 86/bbl and USD 94/bbl respectively, buoyed by the USD’s pullback. Metals are similarly USD driven, spot gold has surpassed the 10- & 21-DMAs with base metals similarly buoyed. Spot gold rises roughly $20 to trade near $1,673/oz.

Looking to the day ahead, economic data releases will include wholesale and retail inventories, new home sales and advance goods trade balance in the US and consumer confidence in France. In earnings, results will be due from Meta, Thermo Fisher Scientific, Bristol-Myers Squibb, Boeing, Iberdrola, Boston Scientific, Mercedes-Benz, Heineken, Ford, Kraft Heinz, Santander, BASF, Barclays, Telenor and Puma.

Market Snapshot

S&P 500 futures down 0.6% to 3,847.75

STOXX Europe 600 up 0.2% to 408.51

MXAP up 1.2% to 137.05

MXAPJ up 1.2% to 436.97

Nikkei up 0.7% to 27,431.84

Topix up 0.6% to 1,918.21

Hang Seng Index up 1.0% to 15,317.67

Shanghai Composite up 0.8% to 2,999.50

Sensex down 0.5% to 59,543.96

Australia S&P/ASX 200 up 0.2% to 6,810.87

Kospi up 0.6% to 2,249.56

German 10Y yield down 0.4% at 2.16%

Euro up 0.7% to $1.0038

Brent Futures up 0.2% to $93.68/bbl

Gold spot up 1.1% to $1,670.70

U.S. Dollar Index down 0.67% to 110.20

Top Overnight News from Bloomberg

UK Prime Minister Rishi Sunak may delay an economic plan scheduled for Oct. 31 to give him time to square it with his agenda, Foreign Secretary James Cleverly said.

Hedge funds have cut portfolio leverage this year in a conservative turn that has sucked borrowed money from global markets, adding selling pressure to stocks and bonds.

Five trillion euros of liquidity is eroding the bridge between European interest-rate policy and borrowing costs in money markets, spurring debate over the kind of toolkit needed to stop the dislocation warping the cost of funding in the wider economy.

Australia faces mounting debt and deficits in the years ahead even as Treasurer Jim Chalmers scrimped and saved in his first budget to hold down spending and avoid further fueling inflation.

US Treasury Secretary Janet Yellen respects Tokyo’s decision not to disclose whether it has intervened in foreign exchange markets, according to Japan’s top currency official.

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks equities traded higher across the board following the positive lead from Wall Street. ASX 200 opened firmer following the Aussie budget, but gains were capped by hotter-than-expected Australian CPI data which resulted in a modest uptick in RBA pricing for a 50bps hike at the next meeting. Nikkei 225 topped 27,500 with gains led by the pharma and manufacturing sectors. KOSPI held onto mild gains whilst chipmaker SK Hynix missed earnings expectations and cut its 2023 capex by over 50% vs 2022. Hang Seng and Shanghai Comp opened firmer as the bourses conformed to the gains across global peers, while the PBoC also injected CNY 280bln via reverse repo, with the former eventually outperforming.

Top Asian News

China’s Hanyang district (900k population) in Wuhan city, entered a five-day temporary lockdown until October 30th, according to Chinese press.

Universal Studios in Beijing temporarily closed amid COVID measures, according to a notice cited by Reuters.

PBoC injected CNY 280bln via 7-day reverse repos at a maintained rate 2.00% for a daily injection of CNY 278bln.

BoJ raised the purchase amounts for 10-25yr and 25yr+ JGB maturities in a bid to curb the surge in yields, via Reuters.

Japan’s Top FX Diplomat Kanda reiterated that they will continue to take bold steps against excessive FX moves, and are in close contact with G7 everyday, including on FX and geopolitics.

Japan Chief Cabinet Secretary says it is important to keep enough FX reserves to support its own currency in case of sharp, excessive market volatility, via Reuters.

Japanese life insurers’ investment plans show a preference to cut holdings of foreign debt, mainly US Treasury bonds, in the second half of the fiscal year ending March amid elevated FX hedging costs, according to Nikkei citing investment plan release.

Hong Kong Futures Exchange has temporarily suspended the volatility control mechanism for futures products in derivatives market; halt due to external vendor software issues.

Japan is set to lower electricity bills by around 20% in early 2023 under a new package amid accelerating inflation, according to Kyodo News sources.

SK Hynix (000660 KS) Q3 2022 (KRW): Revenue 10.98tln (exp. 11.1tln). Operating Profit 1.66tln (exp. 1.87tln). Net Profit 1.1tln (exp. 1.37tln), Q3 average DRAM and NAND selling prices -20%; cuts 2023 investment spending by over 50% vs 2022.

Australian Treasurer Chalmers expects inflation to peak at the end of the year.

European bourses are mixed and yet to make much ground either side of the unchanged mark, Euro Stoxx 50 -0.2%; amid numerous European updates and the US tech headwind. Sectors, feature Tech as the main underperformer as such with the broader picture in-fitting with bourses and mixed overall. Stateside, the NQ -1.7% is weighed on by GOOGL and MSFT post-earnings and ahead of further large-cap updates including META after-hours.

Top European News

UK medium-term fiscal plan has been delayed until November 17th, via BBC; upgraded to a full Autumn Statement. Subsequently confirmed by Chancellor Hunt

Sunak is to meet Chancellor Hunt on Wednesday to discuss proposals to increase taxes and cut public spending, according to The Times.

Heineken Warns of Softer Demand as Inflation Hits Drinkers

UniCredit CEO Committed to Disengage, Reduce Russia Exposure

WPP Raises Sales Forecast After Ad Budgets Prove Resilient

European Stock Rally Moderates as Investors Weigh Earnings, ECB

Heathrow Ramps Up Hiring, Says It Will Take Years to Recover

Traders Price Less Than 150 Bps of BOE Rate Hikes By Year-End

Barclays Traders Beat Estimates as Uncertainty Freezes Deals

Storebrand Falls After 3Q Solvency II Misses Estimates

Major Banks Upbeat on UK House Price Growth Despite Rising Rates

Fixed Income

Initial modest upside has waned and been replaced by an incremental negative bias, Gilts are lagging slightly and back below 101.00 post a sub-par 7yr sale and as the UK’s fiscal update has been delayed.

Amidst this, both Bunds and USTs have slipped though latter remain bid overall in a slight role reversal from recent performance; stateside, the curve is slightly flatter.

Finally, within the periphery BTPs have slipped ahead of a Senate vote but the BTP-Bund spread remains relatively narrow and sub-220bp after yesterday’s House performance from Meloni.

Commodities

Crude benchmarks are modestly firmer on the session despite initial downbeat performance in wake of readacross from US after-market earnings and on fresh COVID updates in China alongside the below Private Inventory release.

WTI and Brent Dec’22 contracts reside at the top-end of USD 1.50/bbl parameters though remain capped by USD 86/bbl and USD 94/bbl respectively, buoyed by the USD’s pullback.

Metals are similarly USD driven, spot gold has surpassed the 10- & 21-DMAs with base metals similarly buoyed.

US Energy Inventory Data (bbls): Crude +4.5mln (exp. +1.0mln), Cushing +0.7mln, Gasoline -2.3mln (exp. -0.8mln), Distillate +0.6mln (exp. -1.1mln).

FX

Scramble to cover Sterling shorts inflicts more pain for the Buck as Cable tops 1.1600 and DXY sinks below 110.000.

Euro back above parity vs Greenback, but may be hampered by decent option expiry interest at the strike.

Kiwi and Aussie make more headway against their US rival through 0.5800 and towards 0.6500 respectively.

Yen probes 147.00 vs Dollar without thrust of obvious intervention and Loonie eyes 1.3500 ahead of BoC amidst split opinions on 50 or 75 bp rate hike.

Yuan relieved Buck retreat, stronger than spot PBoC CNY fix and reports of major Chinese bank buying late yesterday.

PBoC set USD/CNY mid-point at 7.1638 vs exp. 7.1983 (prev. 7.1668)

Major Chinese state-owned banks sold USD in both onshore and offshore markets in late trade on Tuesday to prop up the weakening yuan, according to Reuters sources

Geopolitics

Japan’s Vice Foreign Minister intends to further deepen trilateral cooperation between Japan, South Korea, and the US.

German foreign ministry, in internal paper, said Cosco stake in German ports disproportionately strengthens China’s influence on Germany and in Europe, via Reuters.

US Event Calendar

07:00: Oct. MBA Mortgage Applications -1.7%, prior -4.5%

08:30: Sept. Advance Goods Trade Balance, est. -$87.5b, prior -$87.3b

08:30: Sept. Retail Inventories MoM, est. 1.2%, prior 1.4%

Wholesale Inventories MoM, est. 1.0%, prior 1.3%

10:00: Sept. New Home Sales MoM, est. -15.3%, prior 28.8%

New Home Sales, est. 580,000, prior 685,000

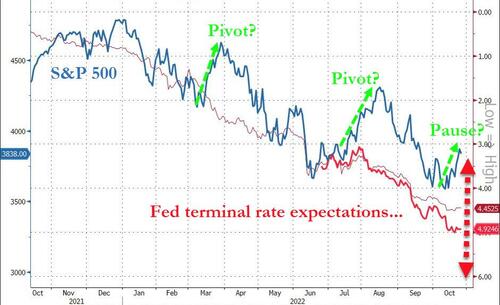

DB’s Jim Reid concludes the overnight wrap

Morning from NY. I say morning but I flagged after writing about the weak late US tech earnings below. Jet lag hit so I’m passing this onto Galina to finish off and send in the London morning. Indeed the weaker tech earnings have slightly ruined the joint bond and equity rally that’s been in place for several days now.

More specifically, I’m not sure if anyone else is playing this game but we continue to try to work out whether Friday’s WSJ article by Nick Timiraos marks the start of the 6th attempt at a sustained Fed pivot narrative over the last 12 months. If you want to examine the previous 5, see Henry’s note earlier this month here for more. After a bit of push / pull on rates after the immediate Timiraos-led move, yesterday saw a fresh rates (and equity) rally on the back of obviously weaker economic data. Before we delve into that remember that from last night, 20% of the S&P 500 report in 48 hours across just 5 mega cap tech stocks. Last night, Alphabet fell -6.7% in after hours after both revenue and earnings missed estimates and the company said it was focusing on costs and constraining hiring. For Microsoft, despite beats on both revenue and net income, disappointing growth forecasts for Azure, its cloud platform, as well as strong dollar, European energy costs and falling demand for PCs weighed on the share price. In after-hours trading the stock also traded -6.7%. Elsewhere, Texas Instruments, which “only” has a market cap of c.$150bn to Alphabets’ $1.36tn and Microsoft’s $1.87tn, also disappointed the market after-hours due to a soft outlook for the current quarter with the stock -5.2% in extended trading. With its chips used across a variety of goods, the CEO’s comments about weakness in both personal electronics and industrial sectors is telling about demand in the broader economy. This morning we have also heard demand concerns from SK Hynix, a South Korean chipmaker. All this has cast a shadow on futures this morning with S&P 500 and Nasdaq 100 contracts -0.90% and -1.90%, respectively. Watch out for Meta earnings after hours tonight and Apple and Amazon tomorrow.

Back now to that weaker data that created the rates rally and helped tech along the way in normal trading hours. Markets are getting increasingly sensitive to housing at the moment and thus the news that the FHFA house price index surprised on the downside, falling by -0.7% MoM vs -0.6% expected seemed to be the rates catalyst yesterday. This was the lowest reading and the first back-to-back monthly decline since 2011. The S&P CoreLogic Case-Schiller index also fell for a second month with the 20 largest cities falling -1.3% MoM. We also saw consumer confidence miss, coming in at 102.5, falling from 108.0 in September and by more than expected (105.9), with both present situation and expectations declining. Lastly, a miss on the Richmond Fed manufacturing index (-10 vs -5) added to a downbeat message from the data.

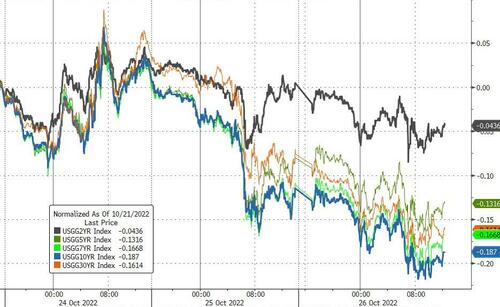

As discussed, this softness weighed on US yields, with the 10y dropping by -14.0bps but with 2yrs only -2.8bps lower. Moves in Europe were almost a mirror image with Bunds (-16.0bps) and OATs (-16.1bps) sharply lower and with peripheral yields continuing to outperform (BTPs -20.8bps). Like the US, the front end saw milder moves (Germany 2y -2.6bps, France 2y +1.0bps). These declines in turn translated into around 2-5bps being taken out of both the Fed and the ECB pricing for next year meetings. This morning longer-end US yields continue to trend lower, with 10y down by -1.2bps and the 2y unchanged.

Before the after-hours fall, US tech stocks rejoiced on the back of those rates moves, with the Nasdaq jumping +2.25%, ahead of the S&P 500 (+1.63%). Sector-wise, of the 10 top level ones only energy (-0.05%) fell despite slight upward moves in oil (WTI +0.87%). Outside of the big tech reports mentioned at the top, notable large-cap earnings beats included Coca Cola (which also had an upward guidance revision), General Motors and UPS. So aside from Fed pivot pricing there was also the fundamentals story feeding into the day time rally.

Over in Europe, it was a quieter day with not much economic data released yesterday. The Ifo survey surprised on the upside on key metrics like business climate (84.3 vs 83.5 expected), current assessment (94.1 vs 92.5) and expectations (75.6 vs 75.0). Combined with falling yields, this turbocharged the Stoxx 600 (+1.44%) for another day of a more than a 1% gain amid gains in real estate (+5.06%), IT (+3.80%) and consumer discretionary (+2.47%) stocks. Undoubtedly, sub-100 euro gas prices (for a second day +0.84%) in Europe on the back of stories about potential LNG glut in the region and falling futures prices have helped.

In the UK, moves were milder as much of the action post-Sunak’s victory already happened yesterday and today’s official ceremonies and cabinet reshuffle didn’t move the markets much. The 2y gilt yield declined by -1.2bps and the 10y yield was down by -10.9bps. GBP rallied +1.72% though most of the move coincided with a big fall in the dollar index at the same time. It ended -0.93%.

Overnight in Asia, major bourses are defying the sell-off in US futures, with the Nikkei (+1.08%) and the KOSPI (+0.79%) in the green. Chinese stocks are having an even bigger rally, with the Hang Seng (+2.17%) and the Shanghai Composite (+1.42%) marching higher after closing in the red yesterday despite gains earlier in the day. In data, we got services PPI from Japan this morning which was in line with expectations at 2.1% (1.9% in August).