OCT 27//GOLD CLOSED DOWN $3.80 TO $1661.40//SILVER CLOSED UP AGAIN BY 3 CENTS TO $19.53//PLATINUM IS UP $10.60 TO $964.10//PALLADIUM IS DOWN $13.35 TO $1944.50//COVID UPDATES//DR PAUL ALEXANDER//VACCINE IMPACT//ECB RELUCTANTLY RAISES ITS INTEREST RATE BY .75% AND YET THE EURO AND POUND FALL//CREDIT SUISSE IN BIG TROUBLE AS THEY CONTEMPLATE A RESTRUCTURING(BANKRUPTCY PROTECTION) AND PLAN ON LAYING OFF 9,000//ANNOUNCED THAT THEY WERE HAVING YOUR OLD FASHIONED BANK RUN!!//IN THE USA POLLSTER 538 (THESE GUYS AND TRAFALGAR ARE THE ONLY ONES YOU PAY ATTENTION TO) SHOWS THE DEMOCRATS IN A DEEP DECLINE//IMPORTANT LETTER TO POWER FROM SENATOR BROWN DEMANDING THAT POWELL PIVOTS CAUSES STOCK MARKETS TO RISE//RAIL: SIGNALMEN REJECT BIDEN’S PRELIMINARY SETTLEMENT AND THAT MAY CAUSE A WALKOUT SHORTLY//TWITTER: MUSK WILL NO DOUBT TAKE OVER THE COMPANY TOMORROW AND THEN THE COMPANY IS DELISTED//SWAMP STORIES FOR YOU TONIGHT/

323 C HSBC 1 435 H SCOTIA CAPITAL 1 657 C MORGAN STANLEY 2 880 H CITIGROUP 2

TOTAL: 3 3 MONTH TO DATE: 23,394

JPMORGAN STOPPED 0/3

GOLD: NUMBER OF NOTICES FILED FOR OCT CONTRACT: 3 NOTICES FOR 300 OZ or 0.00933 TONNES

total notices so far: 23,394 contracts for 2,339,400 oz (72.765 tonnes)

SILVER NOTICES: 233 NOTICE(S) FILED FOR 1,165000 OZ/

total number of notices filed so far this month 689 : for 3,445,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $3.80

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////NO CHANGE IN GLD INVENTORY /INVENTORY REMAINS AT 928.39 TONNES

INVENTORY RESTS AT 928.39 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 3 CENTS

AT THE SLV// :/BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A HUGE WITHDRAWAL OF 2.579 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 484.091 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 742 CONTRACTS TO 139,827 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE STRONG GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR SMALL $0.13 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS/HFT WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.13)., AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC LONGS, AS WE HAD A VERY STRONG GAIN IN OUR TWO EXCHANGE OF 897 CONTRACTS. HUGE SPECS CONTINUE TO ADD TO THEIR SHORTFALLS FROM WHICH OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. SOME SPEC LONGS ADDED TO THEIR POSITIONS

WE MUST HAVE HAD: I) ZERO SPECULATOR SHORT COVERINGS BUT STRONG SHORT ADDITIONS ////CONTINUED BANKER OI COMEX ADDITIONS /// CONSIDERABLE NEWBIE SPEC LONG ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.580 MILLION OZ FOLLOWING AN120,000 OZ QUEUE. JUMP / // V) STRONG SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: –286

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS OCT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT:

TOTAL CONTRACTS for 21 days, total 57,070 contracts: 28.535 million oz OR 1.358MILLION OZ PER DAY. (271 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 28.535 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 28.535 MILLION OZ INITIAL

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 742WITH OUR $0.13 GAIN IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 565 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR OCT. OF 1.580 MILLION OZ FOLLOWED BY TODAY’S 120,000 QUEUE JUMP .. WE HAD A VERY STRONG SIZED GAIN OF 1391 OI CONTRACTS ON THE TWO EXCHANGES FOR 6.955 MILLION OZ..

WE HAD 233 NOTICE(S) FILED TODAY FOR 1,165,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 1657 CONTRACTS TO 457,729 AND CLOSER TO FROM TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -642 CONTRACTS.

.

THE FAIR SIZED INCREASE IN COMEX OI CAME WITH OUR STRONG GAIN IN PRICE OF $9.25//COMEX GOLD TRADING/WEDNESDAY // ZERO SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION AND CONSIDERABLE SPEC SHORT ADDITIONS BUT MINOR SPEC SHORT COVERINGS. // CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR OCT. AT 66.099 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S SMALL EFP JUMP TO LONDON OF 3400 OZ//NEW STANDING 76.111TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $9.25 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 2913 OI CONTRACTS 9.06 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1256 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 457,729

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2913 CONTRACTS WITH 1657 CONTRACTS INCREASED AT THE COMEX AND 1256 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2913 CONTRACTS OR 9.06 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1256) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (1657): TOTAL GAIN IN THE TWO EXCHANGES 2913 CONTRACTS. WE NO DOUBT HAD 1) STRONG SPECULATOR SHORT ADDITIONS// CONTINUED GOOD BANKER ADDITIONS/// MINOR SPEC SHORT COVERINGS// SOME NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 66.099 TONNES FOLLOWED BY TODAY’S 3400 OZ E.F.P JUMP TO LONDON ///NEW STANDING 76.111 TONNES//. 3) ZERO LONG LIQUIDATION //// //.,4) FAIR SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT. :

49,530 CONTRACTS OR 4,953,000 OZ OR 154.05 TONNES 21 TRADING DAY(S) AND THUS AVERAGING: 2358 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 21 TRADING DAY(S) IN TONNES: 154.05 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 154.05/3550 x 100% TONNES 4.33% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 154.55 TONNES INITIAL ( MUCH SMALLER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 742 CONTRACT OI TO 139,827 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 565 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 565 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 565 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 742 CONTRACTS AND ADD TO THE 565 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 1307 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 6.9535MILLION OZ//

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

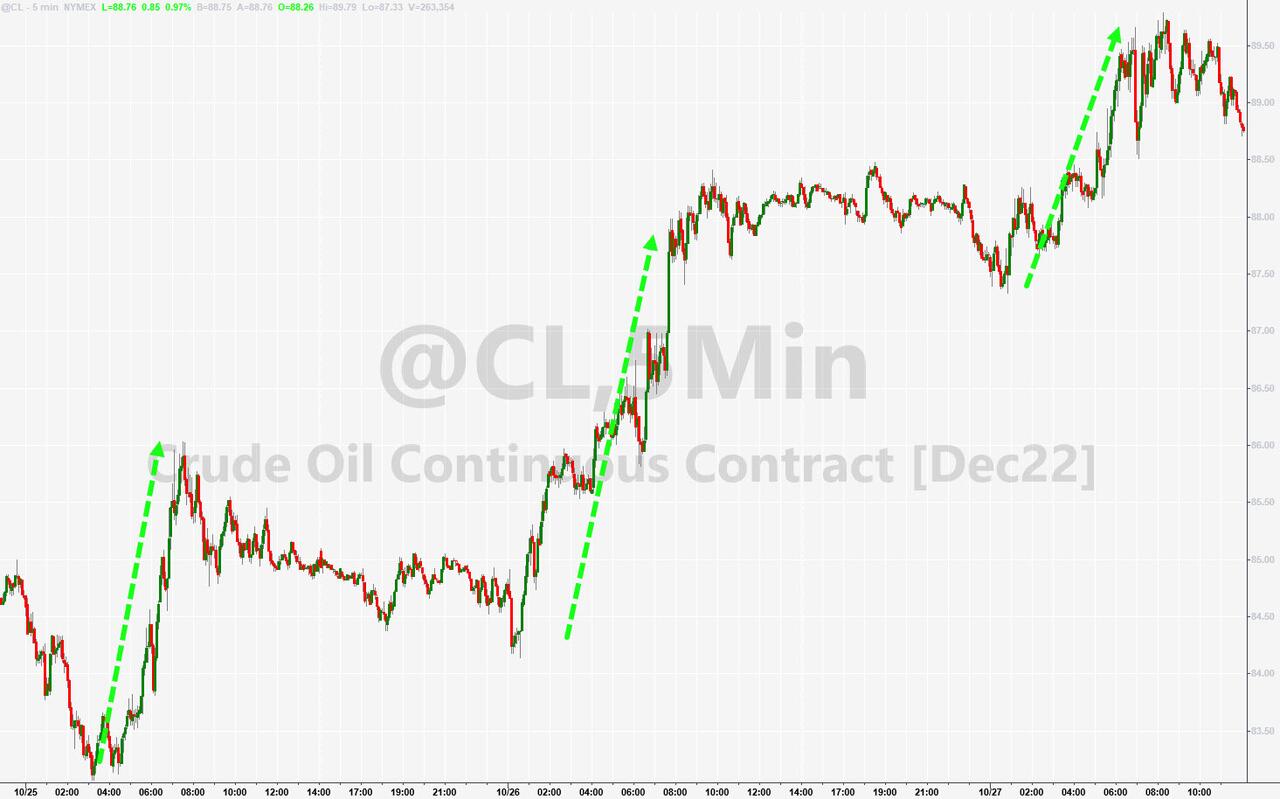

SHANGHAI CLOSED DOWN 16.60 PTS OR 0.55% //Hang Seng CLOSED UP 110.27 OR 0.72% /The Nikkei closed DOWN 36.60 PTS OR 0.32% //Australia’s all ordinaires CLOSED UP 0.53% /Chinese yuan (ONSHORE) closed DOWN TO 7.2286 //OFFSHORE CHINESE YUAN DOWN 7.2493// /Oil UP TO 88.17 dollars per barrel for WTI and BRENT AT 95.96 / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

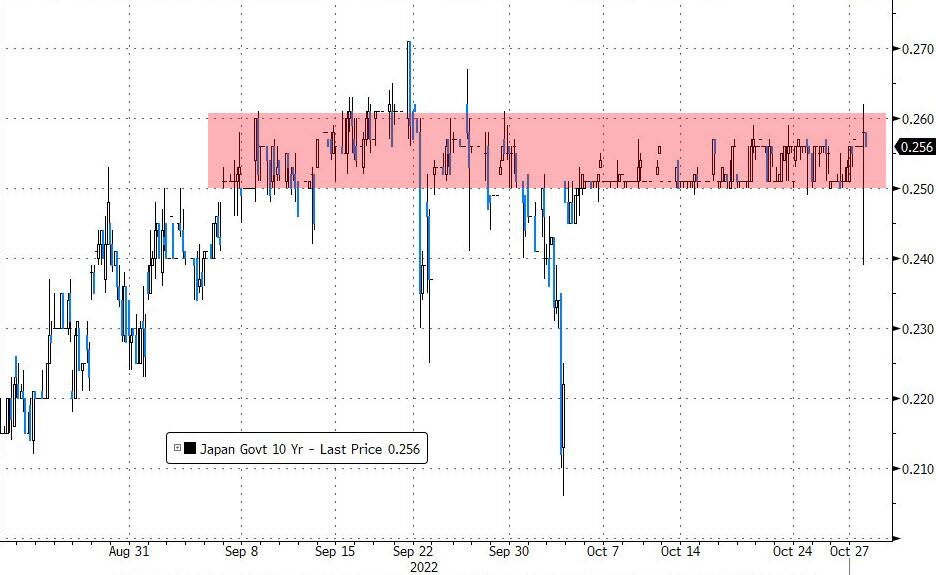

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 1657 CONTRACTS TO 457,729 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS FAIR COMEX INCREASE OCCURRED WITH OUR STRONG RISE IN PRICE OF $9.25 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (1256 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF OCT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1256EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC : 1256 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1256 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2,913 CONTRACTS IN THAT 1256LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 2299 CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF GOLD $9.25//WE HAD CONSIDERABLE SPEC SHORTS ADDITIONS, WITH BANKERS AS BUYERS OF COMEX GOLD CONTRACTS. WE ALSO HAD SOME ADDITIONAL NEWBIE SPECS GOING LONG

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING OCT (76.217),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 76.217 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $9.25) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS// SPEC SHORTS ADDED TO THEIR POSITIONS AS WE HAD A FAIR SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 2913 CONTRACTS // WE HAVE REGISTERED A FAIR GAIN OF 11.05 PAPER TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR OCT. (76.217 TONNES)…THIS WAS ACCOMPLISHED WITH OUR RISE IN PRICE OF $9.25

WE HAD -642 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 2913 CONTRACTS OR 291300 OZ OR 9.06 TONNES

Total monthly oz gold served (contracts) so far this month

23,394 notices 2,339,400 72.765 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i) Into brinks: 5132.067 oz

total deposits 5132.067 oz

customer withdrawals:2

ii) Out of Brinks 803.77 OZ (25 kilobars)

iii) Out of Manfra 5132.067 oz

total: 5935.837 oz

total in tonnes: 0.1846 tonnes

Adjustments: 1// customer to dealer

i)Out of Malca 7426.881

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCT we have an oi of 1079 contracts having LOST 118 contracts . We had 84 contracts

filed on WEDNESDAY, so we LOST A SMALL 34 contracts or an additional 3400 oz will NOT stand in this active delivery month of Oct as they were EFP’d to London.

November SHOCKINGLY lost only 50 contracts to stand at 3783(WE ARE GOING TO HAVE AN EXTRAORDINARILY LARGE NOV.GOLD DELIVERY OF AROUND 10 TONNES OF GOLD.)

December GAINED 607 contracts UP to 360,552

We had 3 notice(s) filed today for 300 oz FOR THE OCT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 3 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT /2022. contract month,

we take the total number of notices filed so far for the month (23,394) x 100 oz , to which we add the difference between the open interest for the front month of (OCT 1079 CONTRACTS) minus the number of notices served upon today 3 x 100 oz per contract equals 2,447,000 OZ OR 76.111 TONNES the number of TONNES standing in this active month of OCT.

thus the INITIAL standings for gold for the OCT contract month:

No of notices filed so far (23,394) x 100 oz+ (1079) OI for the front month minus the number of notices served upon today (3} x 100 oz} which equals 2,447,000 oz standing OR 76.111 TONNES in this NON active delivery month of OCTOBER.

TOTAL COMEX GOLD STANDING: 76.111 TONNES (A HUMONGOUS STANDING FOR OCT (GENERALLY THE POOREST DELIVERY MONTHS FOR AN ACTIVE MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM TOMORROW ONWARD UNTIL THE END OF THE MONTH.

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 689 x 5,000 oz = 3,445,000 oz

to which we add the difference between the open interest for the front month of OCT(260) and the number of notices served upon today 233 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT./2022 contract month: 689 (notices served so far) x 5000 oz + OI for front month of OCT (260) – number of notices served upon today (233) x 5000 oz of silver standing for the OCT contract month equates 3,580,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

OCT 27/WITH GOLD DOWN $3.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 26/WITH GOLD UP $11.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 25/WITH GOLD UP $3.85: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 928.39 TONNES

OCT 24/WITH GOLD DOWN $1.80 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES FROM THE GLD////INVENTORY RESTS AT 928.10 TONNES

OCT 21/WITH GOLD UP $19.10: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 930.99 TONNES

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

TONNES

GLD INVENTORY: 928.39 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

OCT 27/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE S: AWITHDRAWAL OF 2.579 MILLION OZ FROMTHE SLV/////INVENTORY RESTS AT 484.091 MILLION OZ//

OCT 26/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.013 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 486.670 MILLION OZ./.

OCT 25/WITH SILVER UP 17 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.083 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.683 MILLION OZ/

OCT 24/WITH SILVER UP 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .553 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.610 MILLION OZ//

OCT 21/WITH SILVER UP 43 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .46 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 486.163MILLION OZ//

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

And Peter Schiff thinks the central bank has folded with a soft pivot. He explained why on his podcast.

I’m going to go out on a limb here and predict that we’ve already seen the Fed pivot. Now, it wasn’t a pivot in the sense that the Fed has gone from hiking interest rates to cutting interest rates. It hasn’t gone from quantitative easing to quantitative tightening. But it is a pivot in rhetoric. And what it amounts to is an easing of monetary conditions. Because what the Fed is going to be doing going forward is starting to walk back just how aggressive its rate-hiking campaign is going to be.”

The shift may be subtle, but it will be significant. Instead of talking about the urgency of the inflation fight, Peter said he thinks the central bankers at the Fed will start talking about how much progress they have made.

Since they’ve made progress, maybe not completely declaring victory, but indicating they’re seeing the light at the end of the tunnel — that maybe they don’t have to raise interest rates as high as they thought, or maybe leave them as high for as long as they thought. And so the path back down to 2% inflation may not require as aggressive a rate-hiking campaign as they may have previously thought before they started to see the evidence of their success.”

What led Peter to this conclusion?

Last Thursday (Oct. 20), the bond market looked close to a complete collapse. That morning, the yield on the 30-year Treasury nearly rose to 4.4%. Meanwhile, the curve between the 10-year and the 30-year moved positive out of inversion. This was a sign investors were beginning to price in prolonged inflation. Meanwhile, the stock market was also under pressure due to the weakness in the bond market.

The Achilles heel of this bubble economy is interest rates because we’ve got so much debt. And if interest rates rise high enough, the whole thing is going to collapse.”

Consider this tweet Peter sent last Friday.

That would make the interest on the debt the biggest US government expense. (You can read a more in-depth analysis of the national debt HERE.)

Do you see the problem here? Debt is spiraling out of control and is going to crowd out all of the other government spending.

Basically, the US government would become a conduit from taxpayers to bondholders. Now obviously, this can’t happen. At some point, something has to give. And I think that something already gave. I think it gave on Friday morning, and that’s why I think the Fed folded with this ‘soft’ pivot. The reason I’m saying a soft pivot and not a hard pivot is because the Fed is still on the trajectory of hiking rates. I just think it shifted into a lower gear. So that, in and of itself, constitutes an easing. Even if the Fed is tightening, if it’s tightening less aggressively than the markets had thought, then it’s an easing. It’s a forward guidance that is easing conditions a little bit and telling the markets, ‘Hey, you’re too tight. You’re pricing in too many rate hikes. Because we’re probably not going to have to hike as many times as you think. The terminal rate is not going to be as high as you think because we’re already making good progress.’”

The soft pivot was telegraphed to the markets by a Wall Street Journal report saying some Fed members were expressing “unease” and were concerned about overtightening. The story reported that San Francisco Fed President Mary Daly said, “The time is now to start planning for stepping down.”

Peter went on to detail some of the bad economic data the Fed will also have to reckon with including contractionary October PMI, tanking consumer confidence, and rising shelter costs (even though housing prices are falling).

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

WEDNESDAY, OCT 26, 2022 – 10:00

JIM RICKARDS….

TALKING ABOUT GOLD MANIPULATION

Rickards: “Rigging (Gold) Futures is Child’s Play”

-with emphasis and special edits added for ZH readers

Many analysts say gold is volatile. But they should say that the gold market is volatile. That’s because most of it is paper gold, with only a small amount of physical gold to support it. Think of the gold market as an inverted pyramid, with a small amount of gold at the bottom, holding up a huge amount of paper gold. The paper market could be 100 times the size of the physical market.

That means there are 100 paper claims upon each ounce of physical gold. Imagine a coat check at a restaurant issuing 100 claims for one actual jacket. Well, there’s only one coat so 99 claimants are out of luck. It’s the same in the gold market.

It’s the paper market that creates the volatility. Gold itself is remarkably stable. It only appears unstable because its price is quoted in dollars, which fluctuates. When gold goes down, it’s really because the dollar is going up. When gold goes up, it’s really because the dollar is going down.

Right now we have a strong dollar, compared to other currencies at least. In reality, the dollar is simply the cleanest shirt in the laundry pile. And the paper market is highly vulnerable to price manipulation, and there’s been gold price manipulation over the years. There’s no question about it. That’s not just an opinion. The evidence has been very clear, in fact.

The Smoking Gun

I don’t believe in making strong claims without strong evidence. And the evidence is all there. A few years back, I spoke to a PhD statistician who worked for one of the biggest hedge funds in the world. I can’t mention the fund’s name but it’s a household name.

He looked at COMEX (the primary market for gold) opening prices and COMEX closing prices for a 10-year period. He was dumbfounded. He said it was the most blatant case of manipulation he’d ever seen. He said if you went into the aftermarket, bought after the close and sold before the opening every day, you would make risk-free profits.

He said statistically that’s impossible unless there’s manipulation occurring. I also spoke to Professor Rosa Abrantes-Metz at the New York University Stern School of Business. She’s the leading expert on globe price manipulation. She has actually testified in gold manipulation cases.

[EDIT- having worked with Rosa on background collaborating forensic processes in Gold and Silver manipulation, her assertions, in our opinion, are correct. – VBL]

She wrote a report reaching the same conclusions. The bottom line is, price manipulation isn’t just an opinion or some deep, dark conspiracy theory. It’s real. Here you have a PhD statistician and a prominent market expert lawyer, expert witness in litigation, qualified by the courts and as straight-laced as they come, who independently reached the same conclusion. Who carries it out?

Anatomy of a Swindle

Gold manipulation can be done by market players like hedge funds and other major players using ETFs and leasing and unallocated contracts. These manipulations do exist and can influence the price of gold in the short term.The price of gold is a struggle akin to a tug-of-war between physical and paper transactions.

The price of gold will move, in part, because of manipulators’ actions. There’s very strong mathematical evidence that the gold market is manipulated to suppress prices.How do they do it? The easiest way to perform paper manipulation is through rigging the futures market. It’s a bit complicated, but don’t worry about the details. Just realize that they’re meant to suppress gold prices.

Currently the price of gold is set in two places. One is the London spot market, controlled by six big banks including Goldman Sachs and JPMorgan. The other is the New York gold futures market controlled by COMEX, which is governed by its big clearing members, also including major western banks.

In effect, the big western banks have a monopoly on gold prices even if they do not have a monopoly on physical gold. That’s key.

The easiest way to perform paper manipulation is through COMEX futures. Rigging futures markets is child’s play. You just wait until a little bit before the close and put in a massive sell order. By doing this you scare the other side of the market into lowering their bid price; they back away.

[EDIT- Called “Banging the close”-VBL]

That lower price then gets trumpeted around the world as the “price” of gold, discouraging investors and hurting sentiment. The price decline spooks hedge funds into dumping more gold as they hit “stop-loss” limits on their positions.

[Edit- This is why pricing in USD and having that mechanism used worldwide for deals is key to advertising their price-message. It is a function of USD as reserve currency, and creates “pricing power”.

As that pricing power moves eastward with demand, the COMEX loses relevancy. At some point, either the USD loses its status, COMEX loses all its metal or both.

When that happens, spoofing becomes ineffective on COMEX. The sad part is, it probably moves to ASIA along with the demand and the bank traders.- VBL]

The Snowball Effect

A self-fulfilling momentum is established where selling begets more selling and the price spirals down for no particular reason except that someone wanted it that way. Eventually a bottom is established and buyers step in, but by then the damage is done.

Futures have a huge amount of leverage that can easily reach 20 to 1. For $10 million of cash margin, they can sell $200 million of paper gold. Rigging futures markets is child’s play. You just wait until a little bit before the close of trading and put in a massive sell order.

By doing this you scare the other side of the market into lowering their bid price; they back away. That lower price then gets trumpeted around the world as the “price” of gold, discouraging investors and hurting sentiment.

[Edit- because if they know it is coming, why pay a higher price?- VBL]

The price decline spooks hedge funds into dumping more gold as they hit “stop-loss” limits on their positions. A self-fulfilling momentum is established where selling begets more selling and the price spirals down for no particular reason except that someone wanted it that way.

Eventually a bottom is established and buyers step in, but by then the damage is done.If you want more details on this topic, please see my book The New Case for Gold. Specifically, read Chapter 4, “Gold Is Constant.”

Take the Long View

I’m not arguing that manipulation is a principle component of today’s depressed gold price. But it is something to keep in mind.

Ultimately, the shrewd gold investor takes the long view. That’s how patient investors preserve wealth in the gold market. For those who flit in and out and occasionally buy rallies and sell dips in panic mode, all I can say is good luck. You’re probably going to get crushed.

My advice to investors is that when you have gold, you should think about the quantity of gold by weight, not dollar price. Don’t get too hung up on the dollar price, because the dollar could collapse quickly and then the dollar price wouldn’t matter. What would matter is how much physical gold you have.The goal is to preserve wealth for the long run.

Last week’s tactical bullish call was met with doubt from Morgan’s clients, which means there is still upside as we transition from Fire to Ice—falling inflation expectations can lead to lower rates and higher stock prices in the absence of capitulation from companies on 2023 EPS guidance. Yesterday ZH did a prem. piece on it entitled: Wall Street’s Biggest Bear… Expects S&P To Rise As High As 4150.

Wilson summarizes that we are in this particular bear market which began well over a year ago for the average stock. More specifically, he noted, “Many active managers are having a difficult year which puts them on their back foot and unable to fight powerful trends both up and down. This suggests passive trend-following strategies can have even more influence on price than normal.”

So now a bear is tactically bullish. This should bode well for mining stocks too. Good Luck

Continue reading including Moor Gold technicals here

Free Posts To Your Mailbox

END

3.Chris Powell of GATA provides to us very important physical commentaries

Did not expect this: Russian banks are running low on large gold bars amid a surging demand

(Russia today/Moscow/GATA)

Russian banks run low on gold amid surging demand

Submitted by admin on Wed, 2022-10-26 19:46Section: Daily Dispatches

From Russia Today, Moscow Tuesday, October 25, 2022

Banks in Russia are facing a shortage of gold bars after demand for the precious metal increased sharply, the Vedomosti newspaper reported, citing experts.

The executive director of precious metals operations at Uralsib Bank, Andrey Vasiliev, told the media outlet that supply disruptions arose due to the limited production capacity of refineries and growing demand for gold bars from citizens.

Small ingots are more in demand among individuals, while refineries were focused on bulk purchases of large bars and couldn’t quickly adapt to new market requirements, he explained. The production of small gold bars is a more expensive process, according to experts. It is cheaper to produce one ingot weighing 12 kg than several smaller ones, Evgeny Safonov from Promsvyazbank has confirmed. …

This is the latest from Harris Kupperman, founder of Praetorian Capital, a hedge fund focused on using macro trends to guide stock selection. Mr. Kupperman is also the chief adventurer at Adventures in Capitalism, a website that details his investments and travels.

I published recent thoughts from Harris just days ago, in a post outlining his thoughts on why the Fed has backed themselves into a corner they can’t get out of.

Harris is one of my favorite Twitter follows and I find his opinions – especially on macro and commodities – to be extremely resourceful. I’m certain my readers will find the same. I was excited when he offered up his latest investor letter to Fringe Finance, which is published in part below.

Harris On Markets and Macro

I have genuinely been surprised at the vigor with which the Federal Reserve has raised rates in their campaign to quash inflation. For my entire investing career, the Fed has been dovish, standing by and ready to reassure speculators at every market gyration. For the first time in my career, they’re actively targeting the stock market in an effort to create a recession and reduce the “wealth effect” when it comes to consumer spending. This is a terrifying policy change that was unexpected by most market observers—including myself.

At the same time, I feel that they have no real heart for this campaign. As political animals, they’ll be forced to pivot after they succeed in breaking something. Unfortunately, breaking something may lead to scary outcomes in the shorter term and we’ve kept our exposures at reduced levels until it is clear that they’re ready to pivot. When they do pivot, I believe that energy will be the primary beneficiary as both oil and uranium currently exhibit structural deficits that will be difficult to overcome absent substantial increases in capital spending.

In fact, I think that the magnitude of the movements in energy pricing will stun people who are accustomed to gradual changes in commodity price regimes. If anything, the volatility in European energy prices ought to be a wake-up call for all market participants. It would seem that with structural deficits and rapidly growing demand, the rules have adjusted, and many investors are unprepared for the change. To me, this creates opportunity.

Unfortunately for the Fed, higher energy prices will feed into higher structural inflation levels and at some point, the Fed will have to decide if they want to continue fighting inflation (which is likely impossible to quash outside of a global depression that dramatically reduces energy demand) or if they want to adjust their mandate and accept an increased level of inflation. Despite them clinging to their inflation-fighting mandate all year, I believe they have no desire to inflict a depression on voters. They’ll eventually pivot and accept dramatically higher inflation levels, while continuing to subsidize interest rates to avert the depression that they seem fixated on creating. As a result, we have continued to increase our exposure to US housing on this pullback, as that will be a prime beneficiary of this set of macroeconomic outcomes.

Thoughts On Portfolio Valuations

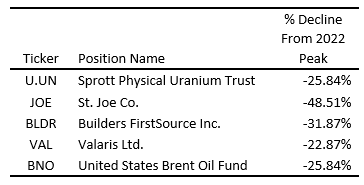

Despite only experiencing a -2.87% net decline (performance net of fees) in our fund since the start of the year, many of our largest positions have experienced far more dramatic declines and now represent unusual value. As a way of demonstrating the magnitude of the declines, as of the end of the third quarter, these are our top 5 positions and the declines experienced from their peak price points during 2022.

Now, you should be asking yourself how it is possible that so many positions have declined dramatically, yet the fund hasn’t performed demonstrably worse. The answer would be a combination of continued gains from the Event-Driven book, realized gains on a number of profitable investments and loss mitigation strategies when trading around core positions. Additionally, we did not own BLDR or BNO at the start of the year, so they are new additions, purchased at depressed prices. Absent these factors, our returns for the year would have been a good deal worse. While the percentage decline from the peak price in a year, is a somewhat arbitrary way to think about a portfolio’s return, I think it is important to point out that the portfolio itself is doing a whole lot better than its larger components. Additionally, the magnitude of the declines from the peak prices is likely indicative of the relative value inherent in our portfolio.

Get 50% off: If you would like to support my work and have the means, I would love to have you as a subscriber and can offer you 50% off for life: Get 50% off forever

As an absolute performance vehicle, I believe that a benchmark would be a foolish metric to use when referencing this fund’s performance. At the same time, it’s hard to ignore the fact that many global equity and bond markets are down dramatically, and our fund is down a good deal less despite being more than 100% net long for most of the year and rarely utilizing shorts or hedges. I believe this is due to my constant focus on sectors that are positively inflecting with strong macro tailwinds. History has shown that despite what happens in global economics or geopolitics, there is always a bull market somewhere. The key is to identify those bull markets and then find the components within those markets that offer exponential upside with a reduced opportunity for a permanent loss of capital. Discipline in this regard often trumps simple valuation, as cheap stocks can always get cheaper. Meanwhile, those with strong tailwinds rarely stay cheap for long.

As a result of focusing on inflecting trends, we’ve side-stepped a good deal of the carnage in global risk markets, while capturing returns from the Event-Driven book. As a result, I think that we’ve set ourselves up for the continuation of the various trends that we are most fixated on. While history only somewhat repeats when it comes to the markets, my experience has been that strong trends often struggle to produce price positive performance during periods of overall market weakness. Then, when there is a pause in the decline of the overall market, those positions that declined the least with the broader market, tend to lead the next charge higher. The overall strength of many of our positions is indicative to me that we may be setting up for a similar explosive move higher in our portfolio positions when the market eventually bottoms.

For now, my focus is on avoiding unforced errors, keeping exposure down and being prepared to dramatically increase our exposure to inflation assets when the Fed finally pauses in its rate cycle.

Russian Securities

During last quarter’s letter, I gave an update on our Russian securities positions and noted that we had moved them into a side-pocket and marked them all at zero. Nothing has changed regarding the side-pocket or the mark on the positions. However, we did succeed in removing the GDR wrapper from 3 of our Russian positions and now own Russian shares. Our fourth position is a Cypriot company and thus far, we have not been capable of removing the GDR wrapper. Fortunately, it does not appear to be at the same risk of disappearing if we do not remove the wrapper.

While it may require some time until we can liquidate these positions, we believe that we’ll ultimately realize sizable gains on them.

Position Review (top 5 position weightings at quarter end from largest to smallest)

Uranium Basket (Entities holding physical uranium along with production and exploration companies)

It may take some time still, but I believe that society will eventually settle on nuclear power as a compromise solution for baseload power generation. This will come at a time when there is a deficit of uranium production, compared with growing demand. As aboveground stocks are consumed, uranium prices should appreciate towards the marginal cost of production. Additionally, there is currently an entity named Sprott Physical Uranium Trust (U-U – Canada) that is aggressively issuing shares through an At-The-Market offering, or ATM, in order to purchase uranium (we are long this entity). I believe that these uranium purchases will accelerate the price realization function by sequestering much of the available above-ground stockpile at a time when utilities have run down their inventories and need substantial purchases to re-stock. The combination of these factors ought to lead to a dramatic increase in the price of uranium as it will take at least two years for incremental supply to come online—even if the re-start decision were made today.

While most of our exposure to physical uranium is within the Sprott trust, because it allows us to express this view with reduced risk, we also own shares of Kazatomprom (KAP – UK). I am well aware that mining is one of the riskiest businesses out there, but Kazatomprom is the lowest-cost diversified producer globally, with incredible scale in what is a highly-consolidated industry. At the same time, I recognize that we take on certain risks when owning a company engaged in mineral extraction, especially in a country like Kazakhstan that can be politically unstable at times. That said, I believe that the recent change in government will do little to impact the operating environment in Kazakhstan, though the tax rate may expand moderately.

Ironically, uranium will be a prime beneficiary of sanctions on Russia as Russia is one of the world’s largest enrichers of uranium. As the West is forced to enrich more of the uranium that ultimately goes into reactors, underfeeding of tails will flip to an overfeeding of tails. The net effect could be anywhere between 10% and 30% of the global supply of uranium disappearing—which may dramatically accelerate the timing of my thesis while increasing the ultimate magnitude of the upward swing in uranium prices.

Energy Services Basket (Positions Not Currently Disclosed)

In 2020 when oil traded below zero, drilling activity ground to a halt and many energy service providers declared bankruptcy. Many of these businesses had teetered on the verge of bankruptcy for years due to reduced demand and over-leveraged balance sheets. The bankruptcies led to consolidation and reduced future industry capacity, removing future competition in the recovery.

With oil prices now at multi-year highs, I believe that demand for drilling and other services will recover. While producers have been slow to increase spending on exploration, despite dramatic recoveries in energy prices, I believe that this only extends the timing on the thesis. In the end, the only way to reduce energy prices is to see a dramatic increase in global oilfield services spending. Any postponement of this spending only leads to higher prices and more wealth transfer from the global economy to the oil producers, which will likely end up resulting in an increase in spending on exploration and production.

We purchased many of these positions at fractions of the equipment’s replacement cost, despite restored balance sheets and positive operating cash flow. As spending in the sector recovers, I believe that the potential for cash flow will become more apparent and this equipment will trade up to valuations closer to replacement cost.

Oil Futures, Futures and ETF Options and Call Spreads

I believe that years of reduced capital expenditures, along with ESG restricting capital access, combined with Western governments that are openly hostile to fossil fuels, have created an environment for dramatically higher oil prices. While we could purchase oil producers, I feel it is far more conservative to simply own the physical commodity itself. We own December 2025 oil futures, along with various futures calls and call spreads, an ETF and ETF call options and call spreads. I believe that this leveraged play on oil gives us the most upside to oil and ultimately inflation, while exposing us to reduced risk when compared to producers.

St. Joe (JOE – USA)

JOE owns approximately 175,000 acres in the Florida Panhandle. It has been widely known that JOE traded for a tiny fraction of its liquidation value for years, but without a catalyst, it was always perceived to be “dead money.”

Over the past few years, the population of the Panhandle has hit a critical mass where the Panhandle now has a center of gravity that is attracting people who want to live in one of the prettiest places in the country, with zero state income taxes and few of the problems of large cities.

The oddity of the current disdain for so-called “value investments” is that many of them are growing quite fast. I believe that JOE will grow revenue at 30% to 50% each year for the foreseeable future, with earnings growing at a much faster clip. Meanwhile, I believe the shares trade at a single-digit multiple on Adjusted Funds from Operations (AFFO) looking out to 2024, while substantial asset value is tossed in for free.

Besides the valuation, growth, and high Return on Invested Capital (ROIC) of the business, why else do I like JOE? For starters, land tends to appreciate rapidly during periods of high inflation— particularly an inflationary period where interest rates are likely to remain suppressed by the Federal Reserve. More importantly, I believe we are about to witness a massive population migration as people with means choose to flee big cities for somewhere peaceful.

I suspect that every convulsion of urban chaos and/or tax-the-rich scheming will launch JOE shares higher, and it will ultimately be seen as the way to “play” the stream of very wealthy refugees fleeing for somewhere better.

Builders FirstSource (BLDR – USA)

Builders FirstSource produces and distributes building materials, primarily for the home building industry. It trades at a low-single digit cash flow multiple on recent earnings and is using that cash flow to rapidly repurchase shares. One could say that the low multiple is due to peak cyclical earnings. I take a different view and believe that we’re in the early stages of a long-term housing boom caused by migration to low tax states along with a catch-up phase as home construction rates were below trendline over the past decade.

I believe that the US needs in excess of 1 million new single-family homes each year, just to provide for population growth, ignoring the other factors. As a result, this business does not appear to be at peak earnings; instead, I believe we are seeing a new baseline for earnings—though the earnings will be quite volatile—particularly if interest rates remain elevated or increase further.

Summary

In summary, during the third quarter of 2022, the fund experienced a pullback in many of its core positions. I have used this pullback to moderately increase a number of our positions, which has increased our overall exposure. Our exposure is a bit more concentrated in inflation, particularly in energy, than I’d normally expect it to be, but those are also my favorite themes. We’ve expressed this view through instruments like physical uranium, long-dated oil futures and futures options, energy equipment services companies, and land plays, which I believe should have a reduced risk of permanent impairment.

I also believe we are in the early stages of this inflationary boom and while there will be sizable volatility going forward, we are positioned well.

Harris’ Disclaimer:

Nothing set forth herein shall constitute an offer to sell any securities or constitute a solicitation of an offer to purchase any securities. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents for Praetorian Capital Fund LLC (the “Fund”) which include, among others, a confidential offering memorandum, operating agreement and subscription agreement. Such formal offering documents contain additional information not set forth herein, including information regarding certain risks of investing in the Fund, which are material to any decision to invest in the Fund.

No information is warranted by PCM or its affiliates or subsidiaries as to completeness or accuracy, express or implied, and is subject to change without notice. This document contains forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forwardlooking statements reflect PCM’s views as of such date with respect to possible future events. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond PCM’s control. Investors are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document.

Opinions, estimates, and forward-looking statements in these materials constitute PCM’s judgment and should be considered current only as of the date of publication without regard to the date on which you may receive or access the information. PCM maintains the right to delete or modify information without prior notice. Statements made herein that are not attributed to a third-party source reflect the views and opinions of PCM.

Return targets or objectives, if any, are used for measurement or comparison purposes and only as a guideline for prospective investors to evaluate a particular investment program’s investment strategies and accompanying information. Targeted returns reflect subjective determinations by PCM based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Performance may fluctuate, especially over short periods. Targeted returns should be evaluated over the time period indicated and not over shorter periods. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

The past performance of the Fund, or PCM, its principals, members, or employees is not indicative of future returns. The performance reflected herein and the performance for any given investor may differ due to various factors including, without limitation, the timing of subscriptions and withdrawals, applicable management fees and incentive allocations, and the investor’s ability to participate in new issues.

All references to a “net return” or “performance, net of fees” within this letter are for a net return of an investor that is subject to all standard fees and accrued incentive allocation, if any, at Praetorian Capital Fund LLC (“PCF”), as provided for in the PCF’s offering documents, and has been an investor in the PCF since the beginning of the current year or period.

There is no guarantee that PCM will be successful in achieving the Fund’s investment objectives. An investment in the Fund contains risks, including the risk of complete loss.

The investments discussed herein are not meant to be indicative or reflective of the portfolio of the fund. Rather, such examples are meant to exemplify PCM’s analysis for the fund and the execution of the fund’s investment strategy. While these examples may reflect successful trading, obviously not all trades are successful and profitable. As such, the examples contained herein should not be viewed as representative of all trades made by PCM.

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.2286

OFFSHORE YUAN: 7.2493

SHANGHAI CLOSED DOWN 16.60 PTS OR .55%

HANG SENG CLOSED UP 110.27 OR 0.72%

2. Nikkei closed DOWN 181.56 PTS OR 0.67%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 109.95/Euro FALLS TO 1.0047

3b Japan 10 YR bond yield: FALLS TO. +.248/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 146.67/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.177%***/Italian 10 Yr bond yield FALLS to 4.404%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.27%…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.66//

3j Gold at $1660.85//silver at: 19.40 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 49/100 roubles/dollar; ROUBLE AT 61.26//

3m oil into the 88 dollar handle for WTI and 95 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 146.67DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9902–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9949well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.067% UP 5 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 4.184% UP 7 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,60…GETTTING DANGEROUS

GREAT BRITAIN/10 YEAR YIELD: 3.6325%

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Coiled Ahead Of Data, Earnings Juggernaut

THURSDAY, OCT 27, 2022 – 08:01 AM

US equity futures swung between gains and losses (a remarkable achievement considering the collapse in generals such as GOOGL and MSFT and last night’s 25% implosion in META, something which startled even JPMorgan’s top trader) as investors weighed disappointing tech earnings amid growing hopes of a Fed pivot and/or a Treasury buyback (Op Twist) announcement.

Contracts on the S&P 500 were little changed as of 7:30 a.m. in New York, while Nasdaq 100 futures fell 0.4% after both indexes snapped a three-day winning streak on Wednesday, dragged down by negative sentiment toward tech following a string of disappointing earnings.

In premarket trading, Nvidia led chipmakers with exposure to data centers higher after Meta Platforms said it’s planning for even bigger capital expenditures in 2023. As noted last night, Facebook Meta projected capex of $34 billion to $39 billion in 2023, up from $32 billion to $33 billion in 2022. Meanwhile, shares in social-media companies tumbled after Meta gave a lukewarm revenue forecast for the fourth-quarter amid ballooning costs, stoking worries about a slowdown in the advertising market amid a weaker economic backdrop. Meta crashed as much as 20% in US premarket trading – its second biggest drop on record; peer Snap drops as much as 1.7%, Pinterest falls as much as 3.6%. Meanwhile, Twitter traded closer to Elon Musk’s offer price of $54.20, with a court-ordered deadline to complete the $44 billion deal just one day away. Here are the other notable premarket movers:

Ford shares declined as much as 2.6% in US premarket trading after narrowing its profit outlook for the year, though the move was relatively muted given the automaker had already issued a profit warning last month.

Wolfspeed shares tumble 24% in premarket trading after the semiconductor device company provided second-quarter revenue guidance that was worse than anticipated. Analysts are confident in the company’s longer-term vision, but see near-term headwinds clouding visibility.

Teladoc Health’s shares jumped as much as 11% in US premarket trading on Thursday, with analysts reassured by the telehealth company’s smaller-than-expected tweak to its 2023 guidance, making its fourth-quarter goals easier to achieve.

Twitter shares rise 1.2% to $53.98 in US premarket trading hours, moving closer to Elon Musk’s offer price of $54.20, with a court-ordered deadline to complete the $44 billion deal just one day away.

Vertiv Holdings stock gains 2.1% in premarket trading on thin volume as Cowen upgraded it to outperform from market perform, saying its confidence in the company’s “compelling” guidance has now been restored.

Keep an eye on Sleep Number’s stock after the air mattress manufacturer reported third-quarter results that were ahead of expectations, while issues with chip inventory and weakening consumer demand led the company to scale back earnings per share guidance for the full year.

Watch Silicon Laboratories as the stock was cut to hold from buy at Needham following Wednesday’s results, based on concerns regarding slowing consumer demand.

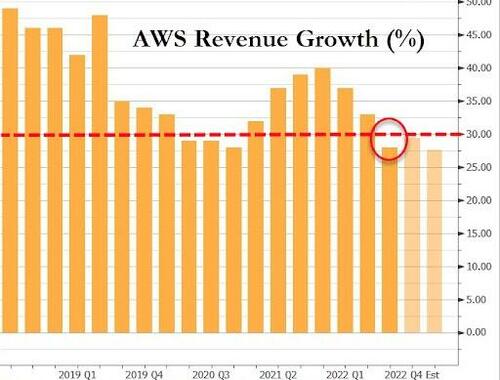

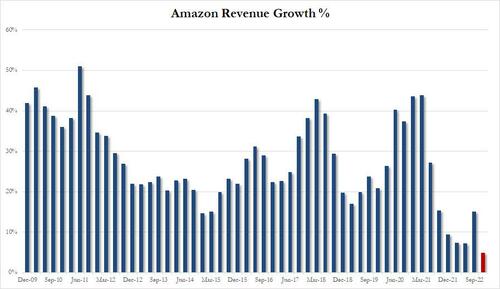

It’s another big day for US tech earnings with Amazon.com, Apple and Intel all reporting after market hours.

As Bloomberg notes, hopes for a Fed pivot rose again after a lower-than-expected rate hike from the Bank of Canada on Wednesday, while investors bet that the central bank will be less aggressive as earnings and economic data point to an economic slowdown. The 10-year US Treasury yield receded to the 4% level before bouncing slightly on Thursday, while the Bloomberg Dollar Index was at this month’s after a contraction in services and manufacturing and fewer new home sales showed the Fed’s efforts to cool the economy seem to be bearing some fruit. Still, economists expect the Fed to hike by 75 basis points for the fourth time in a row when it meets next week. Traders have cut expectations for rates to peak next year to 4.86% from 5% a week ago.

“We will hit peak inflation sometime this calendar year and then we’ll see interest rates peaking sometime early next year” ahead of a slowdown, said Jun Bei Liu, a portfolio manager at Tribeca Investment Partners Pty Ltd. “In that scenario, equity doesn’t look too bad. Actually, equity looks pretty well-positioned, even though we may be staring at a mild recession in the US.”

We also get the first read of US Q3 GDP shortly: while consensus still calls for a 2.4% expansion in US gross domestic product in the third quarter, a few forecasters cut their projections after Wednesday’s trade data were released, with one dropping by nearly a full percentage point. The GDP figures are due out later Thursday, along with data on durable-goods orders and weekly first-time unemployment claims.

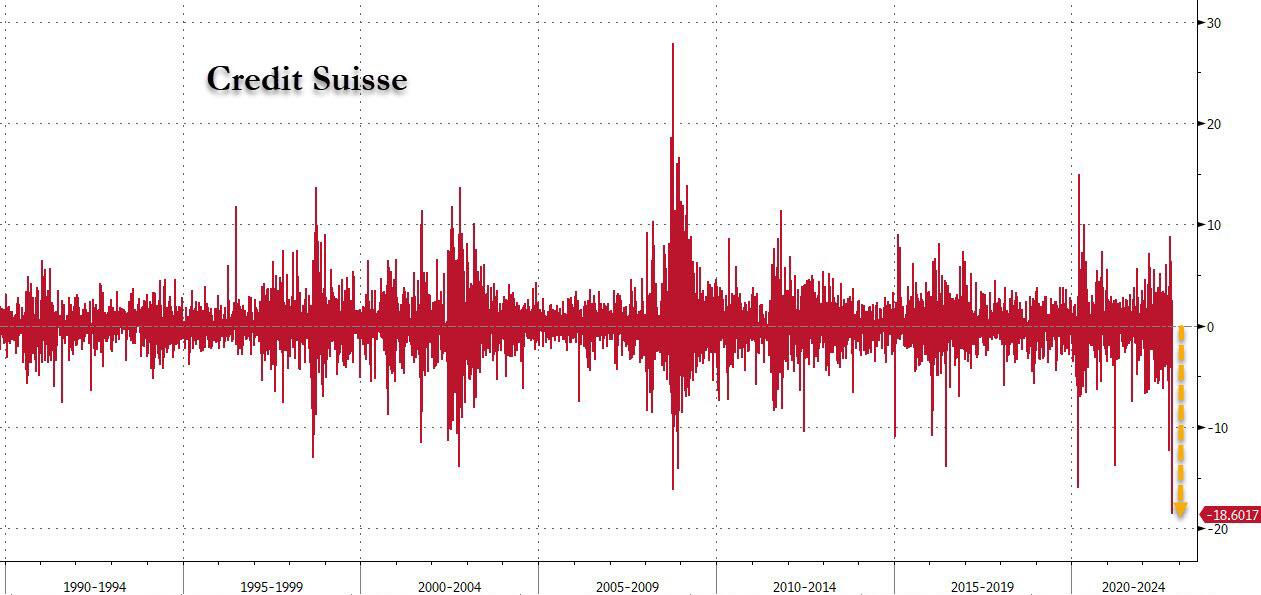

In Europe, equities slipped before a European Central Bank rate decision. The Stoxx Europe 600 Index was weighed down by technology and mining stocks. Credit Suisse Group AG plunged as much as 16% as the bank reported its fourth straight loss and announced a huge corporate overhaul, an equity offering and massive layoffs. Oil stocks rose after Shell Plc raised its dividend and TotalEnergies SE posted a record profit. Here are the biggest European movers:

Shell shares gain as much as much as 5.8% as it raises its dividend after posting its second-highest profit on record, even as some parts of its business showed signs of slowing.

AB InBev rises as much as 6.9% after beating 3Q results estimates and raising the lower end of its growth forecast.

Casino shares rise as much as 30% on signs that the company’s debt burden is manageable. Rebound in shares may also be driven in part by bearish speculators reversing their bets on sharp declines in the stock this year, rather than just fresh buying by bulls.

Aegon shares rise as much as 9.8% after announcing it will combine its Dutch activities with ASR for a total consideration of €4.9 billion, in a move that analysts think makes strategic sense, given scope for material synergies.

Credit Suisse shares slumped as much as 16% after the Swiss lender reported a $4b loss and announced a massive overhaul, including thousands of job cuts, the sale of its structured products group and a capital increase to the tune of 4 billion francs.

European chip stocks slide on Thursday, with STMicro the biggest decliner of the group after the chipmaker guided fourth-quarter revenue slightly below consensus estimates, triggering concerns that the slowdown in semiconductor demand is spreading beyond consumer end-markets. Peer ASML drops as much as 3.7%

Ipsen shares fall as much as 9.7%, the most since April, after the French pharmaceuticals firm published 3Q sales numbers that beat estimates, even as revenue fell for Somatuline, a long-time key drug that’s facing increased competition from generics.

Inspecs shares drop as much as 50% to a record low with Peel Hunt (buy) flagging a deteriorating outlook for the eyewear firm.

In just a few minutes, the ECB is set to look past Europe’s growing recession by lifting its main interest rate by another 75 basis points to the highest in more than a decade as it battles record euro-zone inflation. The pace of increases is likely to slow to 50 basis points in December, according to economists.

“We are oriented with consensus, expecting a big hike of 75 basis points” from the ECB, Monica Defend, head of the Amundi Institute, said on Bloomberg Television. “We think they will continue being hawkish until December and then with the beginning of the new year, they might review or slow down a little bit the pace. Yesterday the Central Bank of Canada surprised the market with their final hike — we think the ECB will remain bold.”

Earlier in the session, Asian stocks were mixed, with most advancing for a third straight day, as Hong Kong shares jumped and a weaker dollar supported regional equities, while Japanese equities led declines. The MSCI Asia Pacific Index rose as much as 1.2%, lifted by technology shares, before paring its gain. Gauges in Hong Kong also trimmed their advance to less than 1%, while investors focused on a slew of earnings and awaited further policy guidance following China’s party congress. Benchmarks in Taiwan and South Korea were also higher as some chip stocks rose, with the measures buoyed by encouraging earnings beats this week including by Samsung SDI and LG Energy. The drop in the US 10-year Treasury yield and dollar this week is giving currencies and equity measures in Asia a boost, with traders looking ahead to US employment data later this week for further clues on the Fed’s rate-hike path. And with China’s historic rout on Monday on the mend and the quarterly earnings season providing some positive surprises, the Asian benchmark is close to erasing losses for the month.

“Any admission of major Western central banks having to pause or give up the inflationary fight entirely would be rather big news, potentially leading to sharp asset price reversals,” Martin W. Hennecke, head of Asia investment advisory at wealth management firm St. James’s Place, wrote in a note. If inflation really is to be addressed more seriously, there should arguably be more focus on budget deficits to be brought under better control, he added.

Japanese equities fell for the first time in four sessions, as investors assessed the latest earnings from domestic and foreign companies. The Topix dropped 0.7% to close at 1,905.56, while the Nikkei declined 0.3% to 27,345.24. Mitsubishi UFJ Financial Group Inc. contributed the most to the Topix decline, decreasing 2.6%. Out of 2,166 stocks in the index, 576 rose and 1,484 fell, while 106 were unchanged. “There are no big surprises in Japanese earnings results,” said Takeru Ogihara, chief strategist at Asset Management One. “On the other hand, although all the results have not been released yet, US earnings are down quite a bit, so I think they may be having a greater impact.”

In India, key stocks gauges overcame volatility induced by the expiry of monthly derivative contracts and resumed their recent advance, with metals and real estate companies recovering. The gains in local shares were in line with Asian peers, which rose tracking decline in the dollar. The S&P BSE Sensex jumped 0.4% to 59,756.84 in Mumbai, recovering from a drop of 0.1% during the session. The NSE Nifty 50 Index advanced 0.5%. All but three of the 19 sector sub-gauges compiled by BSE Ltd. ended higher. Both key indexes have now gained in eight out of nine sessions, a period that includes the one-hour ceremonial Diwali trading on Monday. The benchmarks are now less than 3% short of their respective records set last year. Trading resumed after a holiday on Wednesday.

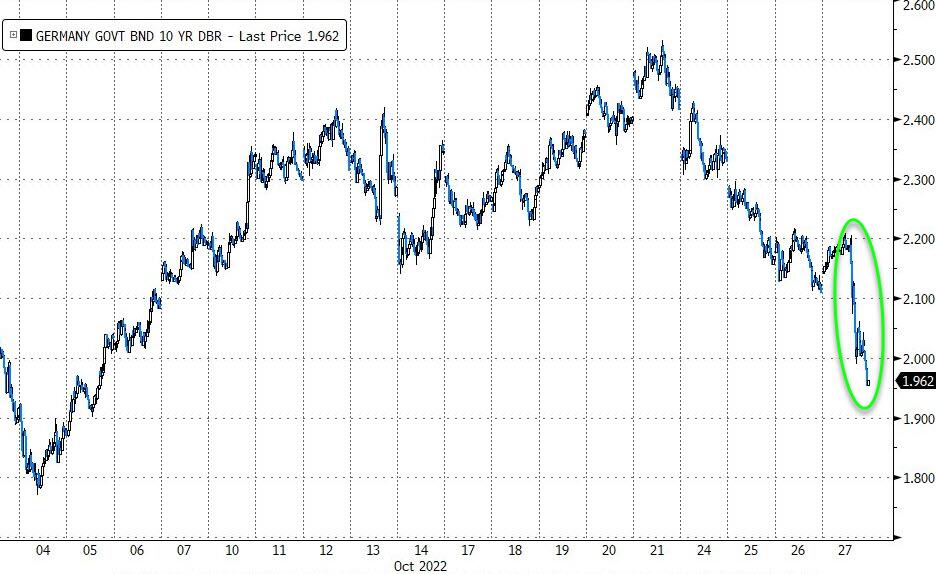

In rates, the yield on the 10-year Treasury bond rebounded after inching below 4% earlier, with investors positioning for less aggressive rate hikes as earnings and economic data indicate a slowdown. The benchmark US yield has dropped more than 20 basis points over the past two days. A gauge of the dollar gained after two days of steep declines. On Wednesday morning, US yields cheaper by 5bp to 8bp across the curve with losses led by belly, flattening 5s30s by nearly 2bp on the day while 2s5s30s fly cheapens 4bp; 10-year yields around 4.075%, with bunds trading 1bp cheaper in the sector. The US auction cycle concludes with 7-year note sale at 1pm, while first estimate of 3Q GDP leads economic calendar. Money markets pricing around 72bp of rate hikes for ECB policy meeting, and attention will also be centered on possible changes to TLTRO loans. German bonds fell across the curve; the 10-year bund yield climbing 7bps higher to 2.89%.

In Fx, the Bloomberg Dollar Spot Index rose 0.3%, halting two days of steep losses; data due later Thursday may show the US economy rebounded in the third quarter.

The yen jumped to a three-week high, before paring gains, as traders geared up for a Bank of Japan policy decision on Friday. The market is abuzz with talk that the BOJ may step in to prop up the yen should the currency weaken if the central bank maintains its super-easy monetary policy as expected.

The pound pulled back from early gains against the US dollar to trade 0.6% lower at $1.1560; further gains could be limited given uncertainties about how a revamped UK fiscal plan could impact the economy just as it enters a recession

In commodities, oil fluctuated after touching the highest level in about two weeks after US Secretary of State Anthony Blinken said a deal with Iran would be unlikely to advance in the short term. Traders placed bets on a soaring price for aluminum as the US considers adding the metal to sanctions against Russia, a major producer. Iron ore futures slumped to the lowest since May 2020 on concern overan economic slowdown in China.

Bitcoin is under modest pressure, downside which has increased amid the recent relative resurgence in the USD.

Looking at the day ahead, today’s big data release will be the advance reading of Q3 GDP in the US. After back-to-back negative readings earlier this year, economists see today’s print at +2.4%, a solid rebound, on the back of strong net exports that could compensate for slowing demand. We will also get the quarterly core PCE, which should provide a clue to tomorrow’s September reading. Other indicators released in the US will include durable goods orders and Kansas City Fed manufacturing activity index. In earnings, we will hear from Apple, Amazon, Mastercard, Samsung, Merck, Shell, McDonald’s, T-Mobile, Linde, TotalEnergies, Comcast, Honeywell, Intel, S&P Global, Caterpillar, AB InBev, American Tower, Gilead Sciences, EDF, Neste, STMicroelectronics, Shopify, PG&E, Repsol, EDP, Pinterest, First Solar, Credit Suisse, Deutsche Lufthansa, Hertz and Ubisoft. So a busy day with the ECB as well.

Market Snapshot

S&P 500 futures up 0.4% to 3,855.75

STOXX Europe 600 down 0.2% to 409.35

MXAP up 0.6% to 138.12

MXAPJ up 0.9% to 441.27

Nikkei down 0.3% to 27,345.24

Topix down 0.7% to 1,905.56

Hang Seng Index up 0.7% to 15,427.94

Shanghai Composite down 0.6% to 2,982.90

Sensex up 0.2% to 59,661.74

Australia S&P/ASX 200 up 0.5% to 6,845.13

Kospi up 1.7% to 2,288.78

German 10Y yield up 3.1% to 2.17%

Euro down 0.2% to $1.0058

Brent Futures up 0.3% to $95.93/bbl

Gold spot up 0.1% to $1,665.68

U.S. Dollar Index little changed at 109.74

Top Overnight News from Bloomberg