NOV 2/GOLD CLOSED UP 55 CENTS TO $1647.15//SILVER CLOSED DOWN 9 CENTS TO $19.59//PLATINUM CLOSED DOWN $3.05 TO $945.20//PALLADIUM CLOSED DOWN $28.70 TO $1858.80//FOMC DISAPPOINTS EQUITIES (REPORT BELOW)COVID UPDATES: CHINA REAFFIRMS ITS ZERO COVID POLICY AS YESTERDAY WAS A TOTAL LIE//DR PAUL ALEXANDER//VACCINE IMPACT//BIRD FLU HITS THE UK BIG TIME AS WELL AS AN IOWA FARM//UKRAINE: CITIZENS LINE UP FOR FRESH WATER THROUGHOUT THE COUNTRY AS THEIR INFRASTRUCTURE WAS DESTROYED//WHEAT FALLS AS RUSSIA RESUMES WHEAT SHIPPMENTS THROUGH THE BLACK SEA//PRIVATE ADP REPORT SHOWS THE USA ECONOMY SLOWLY RECOVERING//SWAMP STORIES FOR YOU TONIGHT//

118 C MACQUARIE FUT 400 132 C SG AMERICAS 24 190 H BMO CAPITAL 122 323 C HSBC 77 323 H HSBC 373 657 C MORGAN STANLEY 4 661 C JP MORGAN 362 690 C ABN AMRO 12 732 C RBC CAP MARKETS 8 737 C ADVANTAGE 9 26 800 C MAREX SPEC 5 9 880 H CITIGROUP 121 905 C ADM 22

TOTAL: 787 787

JPMORGAN STOPPED 781/1600

GOLD: NUMBER OF NOTICES FILED FOR NOV. CONTRACT: 787 NOTICES FOR 78,700 OZ or 2.4473 TONNES

total notices so far: 2817 contracts for 281,700 oz (8.7620 tonnes)

SILVER NOTICES: 7 NOTICE(S) FILED FOR 35000 OZ/

total number of notices filed so far this month 91 : for 455,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $0.55

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////A BIG CHANGE IN GLD INVENTORY: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD// /INVENTORY LOWERS TO 920.57 TONNES

INVENTORY RESTS AT 919.12 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 9 CENTS

AT THE SLV// :/SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF OF .092 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 483.216 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A SMALL SIZED 282 CONTRACTS TO 138,875 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE SMALL LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR STRONG $0.53 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS/HFT WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.53)., AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC LONGS, AS WE HAD A HUMONGOUS GAIN IN OUR TWO EXCHANGE OF 1905 CONTRACTS. HUGE SPECS TRIED TO COVER THEIR SHORTFALLS // OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. SOME NEWBIE SPEC LONGS ADDED TO THEIR POSITIONS/

WE MUST HAVE HAD: I) SOME SPECULATOR SHORT COVERINGS WITH NO SHORT ADDITIONS ////CONTINUED BANKER OI COMEX ADDITIONS /// SOME NEWBIE SPEC LONG ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A POWERFUL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.045 MILLION OZ FOLLOWED BY TODAY’S 60,000 QUEUE JUMP//NEW STANDING:1.125 MILLION OZ/ / // V) SMALL SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: — 47

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS NOV. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF NOV:

TOTAL CONTRACTS for 2 days, total 2140 contracts: 10.700 million oz OR 5.35MILLION OZ PER DAY. (1070 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 10.700 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 10.7 MILLION

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 285 DESPITE OUR $0.53 GAIN IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUMONGOUS SIZED EFP ISSUANCE CONTRACTS: 2140 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR NOV. OF 1.345 MILLION OZ FOLLOWED BY TODAY’S 60,000 QUEUE JUMP/ .. WE HAVE A VERY STRONG SIZED GAIN OF 1905 OI CONTRACTS ON THE TWO EXCHANGES FOR 9.525 MILLION OZ..

WE HAD 7 NOTICE(S) FILED TODAY FOR 35,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 2651 CONTRACTS TO 467,276 AND CLOSER TO TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -407 CONTRACTS.

.

THE FAIR SIZED INCREASE IN COMEX OI CAME WITH OUR RISE IN PRICE OF $9.20//COMEX GOLD TRADING/TUESDAY // ZERO SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION AND CONSIDERABLE SPEC SHORT COVERINGS . // CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR NOV. AT 12.386 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE 55,300 OZ QUEUE JUMP //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR RISE IN PRICE OF $9.20 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A VERY GOOD SIZED GAIN OF4981 OI CONTRACTS 15.49 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2330 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 467,276

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3058 CONTRACTS WITH 3058 CONTRACTS INCREASED AT THE COMEX AND 2330 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 4981 CONTRACTS OR 15,49 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2330) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (2651): TOTAL GAIN IN THE TWO EXCHANGES 4981 CONTRACTS. WE NO DOUBT HAD 1) STRONG SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS/// // CONSIDERABLE NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR NOV. AT 12.386 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 55,300 OZ //NEW STANDING 15.393 TONNES///3) ZERO LONG LIQUIDATION //// //.,4) FAIR SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

NOV

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV. :

5035 CONTRACTS OR 503,500 OZ OR 15.660 TONNES 2 TRADING DAY(S) AND THUS AVERAGING: 2517 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAY(S) IN TONNES: 15.660 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 15.660/3550 x 100% TONNES 0.439% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 15.660 TONNES//INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A SMALL SIZED 282 CONTRACT OI TO 138.875 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 2140 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 2140 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2140 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 235 CONTRACTS AND ADD TO THE 2140 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A VERY STRONG SIZED GAIN OF 1858 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 9.240MILLION OZ//

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 34.17 PTS OR 1.15% //Hang Seng CLOSED UP 371.90 OR 3.41% /The Nikkei closed DOWN 15.53 PTS OR 0.06% //Australia’s all ordinaires CLOSED UP 0.12% /Chinese yuan (ONSHORE) closed DOWN TO 7.2811 //OFFSHORE CHINESE YUAN DOWN 7.3010// /Oil UP TO 88.41, dollars per barrel for WTI and BRENT AT 94.65 / Stocks in Europe OPENED MOSTLY RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 2651 CONTRACTS TO 467,276 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED WITH OUR RISE IN PRICE OF $9.20 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2330 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF NOV.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2330EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC : 2330 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2330 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 4,981 CONTRACTS IN THAT 2330LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 3058 CONTRACTS..AND THIS GOOD SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR RISE IN PRICE OF GOLD $9.20//WE HAD SOME SPEC SHORTS COVERINGS WITH BANKERS AS BUYERS OF COMEX GOLD CONTRACTS. WE ALSO HAD STRONG ADDITIONAL NEWBIE SPECS GOING LONG

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING NOV (15.393),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 15.393 TONNES/INITIAL

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $9.20) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A GOOD SIZED GAIN ON OUR TWO EXCHANGES//// SPEC SHORTS COVERED A SMALL PORTION OF THEIR POSITIONS AS WE HAD A GOOD SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 4981 CONTRACTS // WE HAVE REGISTERED 16.758 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR NOV. (15.393 TONNES)…THIS WAS ACCOMPLISHED WITH OUR RISE IN PRICE OF $9.20

WE HAD -407 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 4981 CONTRACTS OR 498100 OZ OR 15.49 TONNES

Estimated gold volume 199,696// poor//

final gold volumes/yesterday 204,080/ poor

INITIAL STANDINGS FOR NOVEMBER 2022 COMEX GOLD //NOV 2

Total monthly oz gold served (contracts) so far this month

2817 notices 281,700 8.7620 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

customer withdrawals:4

i) Out of Delaware 7499.956 oz

ii) Out of Brinks 289.35 (9 kilobars)

iii) Out of HSBC: 40,207.433 oz

total: 233,455.097 oz

total in tonnes: 1.49 tonnes

Adjustments: 1// customer to dealer HSBC: 96.45 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR NOVEMBER.

For the front month of NOV. we have an oi of 2919 contracts having GAINED 203 contracts. We had 350 notices served upon Monday so we gained a whopping 553

or an additional 55,300 will stand in this non active month of November. We will have Nov gold tonnage standing increase daily from this day forth until the end of the month.

This queue jumping originates in London with the exercising of London based EFP’s for comex gold.

December LOST 7333 contracts DOWN to 350,775.

JANUARY gained 50 contracts to stand at 52.

February gained 9085 contacts up to 80,729.

We had 787 notice(s) filed today for 78,700 oz on the first day notice FOR THE NOV. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 787 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 362 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the NOV. /2022. contract month,

we take the total number of notices filed so far for the month (2817) x 100 oz , to which we add the difference between the open interest for the front month of (NOV 2919 CONTRACTS) minus the number of notices served upon today 787 x 100 oz per contract equals 494,900 OZ OR 15.393 TONNES the number of TONNES standing in this non active month of NOV.

thus the INITIAL standings for gold for the NOV. contract month:

No of notices filed so far (2817) x 100 oz+ (2919) OI for the front month minus the number of notices served upon today (787} x 100 oz} which equals 494,900 oz standing OR 15.393 TONNES in this NON active delivery month of NOV..

TOTAL COMEX GOLD STANDING: 15.393 TONNES (A HUMONGOUS STANDING FOR NOV (GENERALLY THE POOREST DELIVERY MONTHS FOR A NON ACTIVE MONTH)

To calculate the number of silver ounces that will stand for delivery in NOV. we take the total number of notices filed for the month so far at 91 x 5,000 oz = 455,000 oz

to which we add the difference between the open interest for the front month of NOV(141) and the number of notices served upon today 7 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the NOV../2022 contract month: 91 (notices served so far) x 5000 oz + OI for front month of NOV (141) – number of notices served upon today (7) x 5000 oz of silver standing for the NOV. contract month equates 1,125,000 oz. .(CME TOTALS CORRECTED AGAIN)

We will gain in silver oz standing from this day forth until the end of the month.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

NOV 2/WITH GOLD UP 55 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 919.12 TONNES.

NOV 1/WITH GOLD UP $9.20 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES FORM THE GLD../INVENTORY RESTS AT 920.57 TONNES

OCT 31/WITH GOLD DOWN $4.00; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD//INVENTORY RESTS AT 922.59. TONNES//

OCT28/WITH GOLD DOWN $19.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 TONNES FROM THE GLD..///INVENTORY RESTS AT 925.20 TONNES

OCT 27/WITH GOLD DOWN $3.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 26/WITH GOLD UP $11.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 25/WITH GOLD UP $3.85: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 928.39 TONNES

OCT 24/WITH GOLD DOWN $1.80 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES FROM THE GLD////INVENTORY RESTS AT 928.10 TONNES

OCT 21/WITH GOLD UP $19.10: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 930.99 TONNES

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

GLD INVENTORY: 919.12 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

NOV 2/WITH SILVER DOWN 9 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 92,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.216 MILLION OZ//

NOV 1/WITH SILVER UP 53 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 415,000 OZ FORM THE SLV////INVENTORY RESTS AT 483.308 MILLION OZ

OCT 31: WITH SILVER FLAT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .644 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 483.723 MILLION OZ//

OCT 28/WITH SILVER DOWN 35 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.367 MILLION OZ//

OCT 27/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE S: A WITHDRAWAL OF 2.579 MILLION OZ FROMTHE SLV/////INVENTORY RESTS AT 484.091 MILLION OZ//

OCT 26/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.013 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 486.670 MILLION OZ./.

OCT 25/WITH SILVER UP 17 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.083 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.683 MILLION OZ/

OCT 24/WITH SILVER UP 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .553 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.610 MILLION OZ//

OCT 21/WITH SILVER UP 43 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .46 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 486.163MILLION OZ//

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

CLOSING INVENTORY 483.216 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

-END-

3.Chris Powell of GATA provides to us very important physical commentaries

This is huge!! Central bank buying of gold: 399 tonnes!! And this is real gold not paper gold

(Reuters/GATA)

Record central bank buying lifts global gold demand, gold council says

Submitted by admin on Mon, 2022-10-31 23:14Section: Daily Dispatches

By Peter Hobson Reuters Tuesday, November 1, 2022

LONDON — Central banks bought a record 399 tonnes of gold worth around $20 billion in the third quarter of 2022, helping to lift global demand for the metal, the World Gold Council said today.

Demand for gold was also strong from jewellers and buyers of gold bars and coins, the gold council said in its latest quarterly report, but exchange traded funds storing bullion for investors shrank.

Gold is typically seen as a safe asset for times of uncertainty or turmoil.

But many financial investors sold shares in gold-backed ETFs as interest rates rose and pushed up returns on other assets. …

Who are the mystery buyers? For sure China and Turkey and maybe Russia

(Bloomberg News//GATA)

Who are the mystery buyers responsible for central bank gold boom?

Submitted by admin on Tue, 2022-11-01 07:50Section: Daily Dispatches

By Eddie Spence Bloomberg News Monday, October 31, 2022

Central banks bought a record amount of gold last quarter as they diversified foreign-currency reserves, with a large chunk of the purchases coming from as yet unknown buyers.

Almost 400 tons were scooped up by central banks in the third quarter, more than quadruple the amount a year earlier, according to the World Gold Council. That takes the total so far this year to the highest since 1967, when the dollar was still backed by the metal.

Bullion prices have been pressured this year by aggressive U.S. interest-rate hikes as the Federal Reserve tackles soaring inflation, which have prompted exchange-traded fund investors to sell the non-yielding asset. But support has come from other areas, such as retail buyers in Asia and central banks.

Central banks including Turkey and Qatar were among recent buyers, as well as unreported purchases from institutions — which, the WGC said, while not uncommon, amounted to a “substantial” estimate. Not all countries report their gold purchases regularly, including major ones like China and Russia. …

Submitted by admin on Tue, 2022-11-01 10:27Section: Daily Dispatches

10:27a ET Tuesday, November 1, 2022

Dear Friend of GATA and Gold:

USA Gold’s “News & Views” letter for November, published today, has excerpts from 15 analysts commenting on gold, currencies, and the economy. The letter is headlined “Steady Wins the Race” and it’s posted in the clear at USA Gold here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

end

(courtesy Chris Marcus/Andy Schectman)

Andy Schectman: Silver demand driving premiums higher

With the silver premiums continuing to rise, and many products now facing delays, Andy Schectman of Miles Franklin joins me on the show to provide an update of the conditions in the retail physical silver market.

In this call he talks about the delays that are being seen throughout the industry on most silver products, how the refineries continue to struggle to keep up with demand, and how the majority of his orders continue to favor silver over gold.

He mentions that the people who are calling in to purchase silver are concerned about the events they see going on in the world, the persistent inflation, and how they don’t see an easy way out for the Federal Reserve. So as a result, they continue to turn to silver as a means of protection.

Silver dealers throughout the industry have described intense buying unlike any previous time, and one can only wonder how much longer this can go on for before there’s movement in the underlying spot price. So to find out more, click to watch this video now! (below)

On October 7, 2022, US congressman Alex Mooney (a Republican from West Virginia) introduced a bill (the Gold Standard Restoration Act, H.R. 9157) that stipulates that the US dollar must be backed by physical gold owned by the US Treasury. The initiative clearly indicates that the increasingly inflationary US dollar is triggering efforts to get better money.

It should be noted that there have already been many legislative changes to make precious metals more attractive as a means of payment in recent years: in many US states, the value-added and capital gains taxes on gold and silver, but also on platinum and palladium, have been abolished. Mr. Mooney’s proposal is divided into three sections.

The first section of the bill establishes the need for a return to a gold-backed US dollar. For example, it is said that the US dollar—or more precisely, the bill refers to “Federal Reserve Notes”—that is, banknotes issued by the US Federal Reserve (Fed)—has lost its purchasing power on a massive scale in the past: Since 2000, it has dropped by 30 percent, and since 1913 by 97 percent. The bill also argues that with an inflation target of 2 percent, the Fed will not preserve the purchasing power of the US dollar but will have it halved after just thirty-five years. Moreover, the bill points out that it is in the interest of US citizens and firms to have a “stable US dollar.” The bill highlights that the inflationary US dollar has been eroding the industrial base of the US economy, enriching the owners of financial assets, while endangering workers’ jobs, wages, and savings.

The second section of the bill describes in more detail the technical process for reanchoring the US dollar to the US official gold stock. It states that (1) the US secretary of the Treasury must define the US dollar banknotes using a fixed fine gold weight thirty days after the law goes into effect, based on the closing price of the gold on that day. The Fed must (2) ensure that the US banknotes are redeemable for physical gold at the designated rate at the Fed. (3) If the banks of the Fed system fail to comply with peoples’ exchange requests, the exchange must be made by the US Treasury, and in return, the Treasury takes the Fed’s bank assets as collateral.

The third section specifies how a “fair” gold price in US dollar can develop in an orderly manner within thirty days after the bill has taken effect. To this end, (1) the US Treasury and the Fed must publish all of their gold holdings, disclosing all purchases, sales, swaps, leases, and all other gold transactions that have taken place since the “temporary” suspension of the redeemability of the US dollar into gold on August 15, 1971, under the Bretton Woods Agreement of 1944. In addition, (2) the US Treasury and the Fed must publicly disclose all gold redemptions and transfers in the 10 years preceding the “temporary” suspension of the US dollar’s gold redemption obligation on August 15, 1971.

What to Make of This?

The bill’s core is the idea of reanchoring the US dollar to physical gold based on a fair gold price freely determined in the market. (By the way, this is an idea put forward by the economist Ludwig von Mises (1881–1973) in the early 1950s.) In this context, the bill refers to US banknotes. However, banknotes only comprise a (fractional) part of the total US dollar money supply. But since US bank deposits can be redeemed (at least in principle) in US banknotes, not only US dollar cash (coins and notes) could be exchanged for gold, but also the money supply M1 or M2 as fixed and savings deposits could be exchanged for sight deposits, and sight deposits, in turn, could be withdrawn in cash by customers, and the banknotes could then be exchanged for gold at the Fed.

As of August 2022, the stock of US cash (“currency in circulation”) amounted to $2,276.3 billion. Assuming that the official physical gold holdings of the US Treasury amount to 261.5 million troy ounces, and the market expected US cash to be backed by the official US gold stock, a gold price of about $8,700 per troy ounce would result. This would correspond to a 418 percent increase compared to the current gold price of $1,680. If, however, the market were to expect the entire US money supply M2 to be covered by the official US gold stock, then the price of gold would move toward $83,000 per troy ounce—an increase of 4.840 percent compared to the current gold price. Needless to say, such an appreciation of gold has far-reaching consequences.

All goods prices in US dollars can be expected to rise (perhaps to the extent that the price of gold has risen). After all, the purchasing power of the owners of gold has increased significantly. Therefore, they can be expected to use their increased purchasing power to buy other goods (such as consumer goods, but also stocks, houses, etc.). If this happens, the prices of these goods in US dollar terms will be pushed up—and thus, the initial purchasing power gain that the gold dollar holders have enjoyed by being tied to the increased gold price will melt away again. Moreover, if US banks were willing to accept additional gold from the public in exchange for issuing new US dollar, reanchoring the US dollar in gold would increase the upward price effect.

A reanchoring of the US dollar in the US official gold stock will result in a far-reaching redistribution of income and wealth. In fact, it would be fatal for the outstanding US dollar debt: US dollar goods prices would rise, caused by a rise in the US dollar gold price at which the US dollar is redeemable for physical gold, thereby eroding the US dollar’s purchasing power. In the foreign exchange markets, the US dollar would probably appreciate drastically against those currencies that are not backed by gold and against currencies which are backed by gold not as fine compared to the fineness of the gold backing of the US dollar. The purchasing power of the US dollar abroad would increase sharply, while the US export economy would suffer. US goods would become correspondingly expensive abroad, while foreign companies gain high price competitiveness in the US market.

Once the US dollar is reanchored in gold, today’s chronic inflation will end; monetary policy–induced boom-and-bust cycles will come to an end; the world will become more peaceful because financing a war in a gold-backed monetary system will be very expensive, and the general public will most likely not want to bear its costs. However, there is still room for improvement. A “Gold Standard Restoration Act” will deserve unconditional support if and when it paves the way toward a truly “free market for money.” A free market in money means that you and I have the freedom to choose the kind of money we believe serves our purposes best; and that people are free to offer their fellow human beings a good that they voluntarily choose to use as money.

In a truly free market, people will choose the good they want to use as money. Most importantly, in a truly free market in money, the state (as we know it today) loses its influence on money and money production altogether. In fact, the state (and the special interest groups that exploit the state) no longer determine which kind of gold (coins and bars, cast or minted) can be used as money; the state is no longer active in the minting business and cannot monopolize it anymore; there is no longer a state-controlled central bank to intervene in the credit and money markets and influence market interest rates. That said, let us hope that the Gold Standard Restoration Act proposed by Mr. Mooney will pave the way to reforming the US dollar currency system—and that it will eventually move us toward a truly free market in money.

5.OTHER COMMODITIES: URANIUM/ENERGY

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.2811

OFFSHORE YUAN: 7.3010

SHANGHAI CLOSED UP 34.17 PTS OR 1.15%

HANG SENG CLOSED UP 371.90 OR 2.41%

2. Nikkei closed DOWN 15.53PTS OR 0.06%

3. Europe stocks SO FAR: ALL MOSTLY RED

USA dollar INDEX DOWN TO 111.14/Euro FALLS TO 0.9888

3b Japan 10 YR bond yield: FALLS TO. +.243!!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 147,06/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.128%***/Italian 10 Yr bond yield RISES to 4.285%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.218%…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.568//

3j Gold at $1655.85//silver at: 19.76 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 30/100 roubles/dollar; ROUBLE AT 61.54//

3m oil into the 88 dollar handle for WTI and 94 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 147,06DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9973–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9861well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

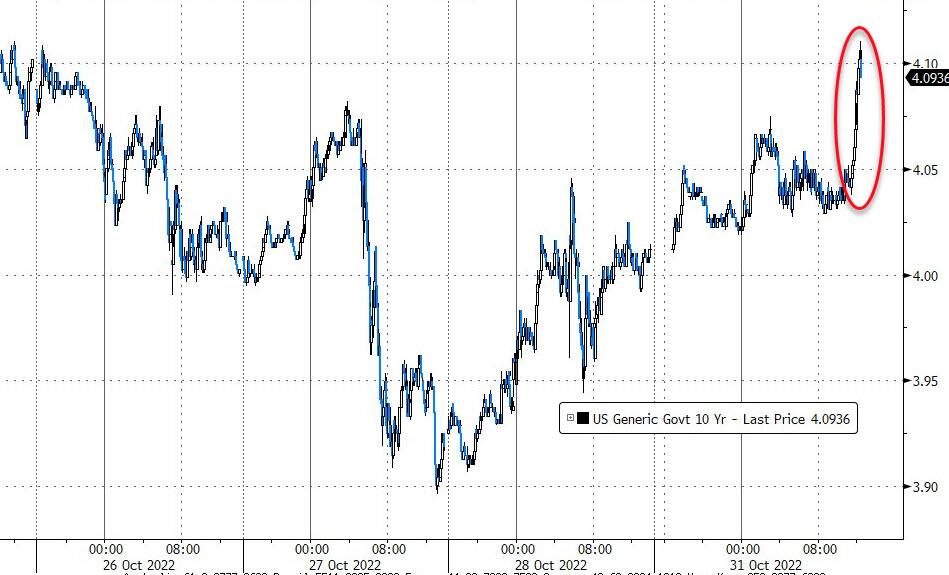

USA 10 YR BOND YIELD: 4.044% DOWN 1 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 4.102% DOWN 2 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,62…GETTTING DANGEROUS

GREAT BRITAIN/10 YEAR YIELD: 3.4870%

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Steady Ahead Of Fed Decision

WEDNESDAY, NOV 02, 2022 – 08:10 AM

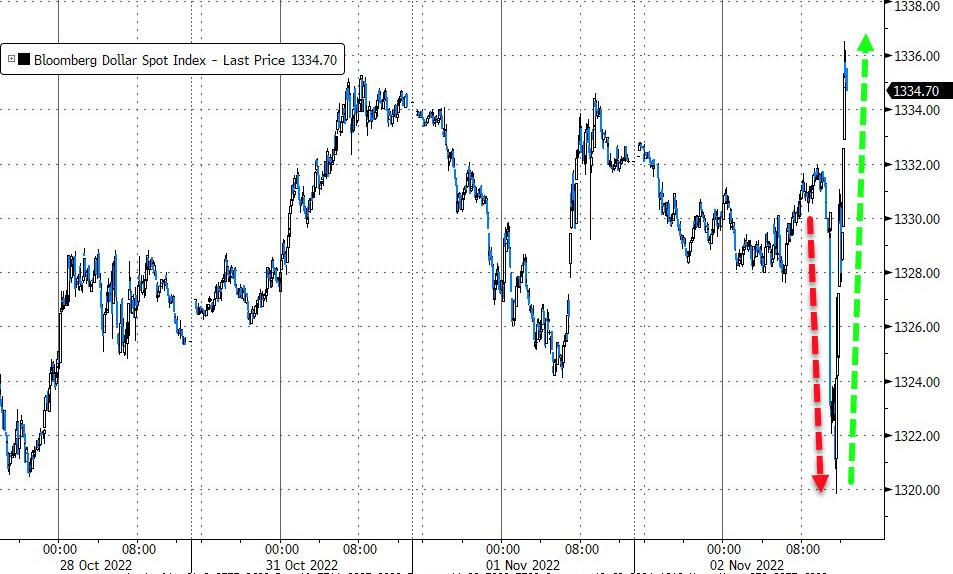

US equity futures were unchanged after two days of declines in underlying gauges as investors brace for today’s 2pm Fed interest-rate decision along with its monetary policy outlook (although a potentially more surprising treasury buyback announcement could come as soon as 830am when the Treasury publishes its quarterly refunding announcement). Contracts on the S&P 500 were little unchanged, while Nasdaq 100 futures advanced 0.2% as of 7:30 a.m. in New York. Stocks have stabilized after a drop in the S&P 500 on Tuesday that was triggered by a surprise surge in job openings. European stocks erased earlier gains while US-listed Chinese stocks rallied in premarket trading and the Hang Seng Index rose in a session cut short by a storm warning as growing speculation over China’s reopening spurred another rally in Asia. The US dollar dropped for the second day as the yen strengthened in a sign traders anticipate a muted impact of Fed tightening on the currency; 10Y yields traded unchanged around 4.04%.

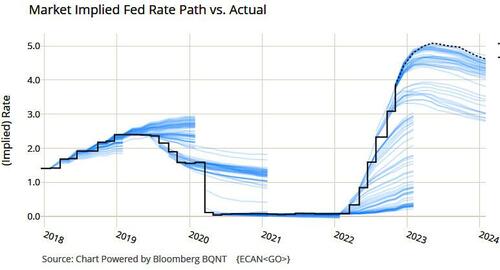

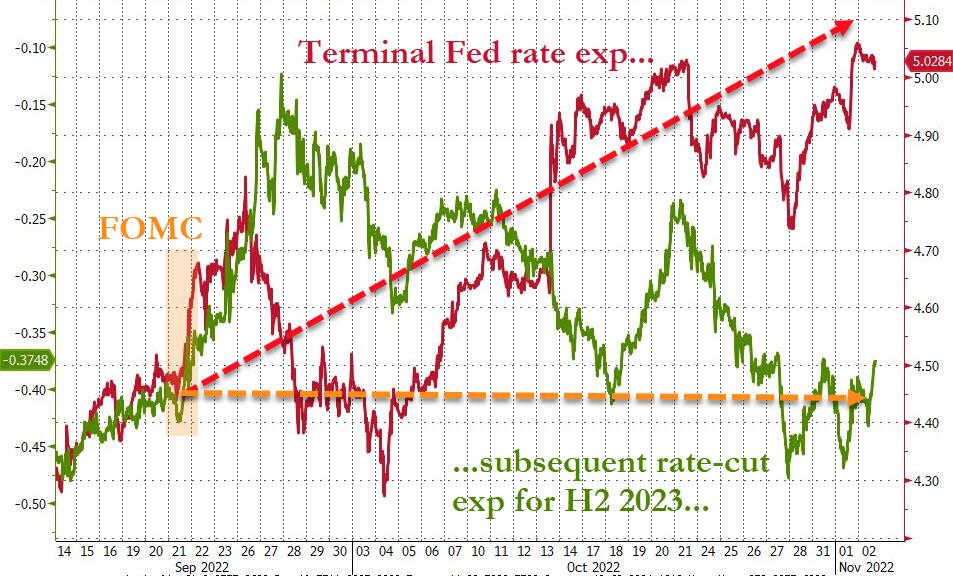

All eyes will be on the Fed later, when the central bank is widely expected to raise rates by 75 basis points for a fourth time in a row; the question is what the Fed does in December and onward. Here is a summary of Fed rate-hike expectations from major banks for Sept and Dec:

Bank of America: 75 bps, 50 bps

Barclays: 75 bps, 75 bps

Citigroup: 75 bps, 50 bps

Deutsche Bank: 75 bps, 75 bps

JPMorgan Chase: 75 bps, 50 bps

Goldman Sachs: 75 bps, 50 bps

Morgan Stanley: 75 bps, 50 bps

Wells Fargo: 75 bps, 50 bps

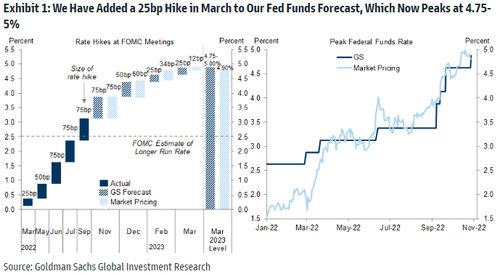

Goldman expects a more dovish 50bps Dec rate hike, but also a slower rise to peak as it has now added a 25bps rate hike in March which brings the Fed to 5.00%.

Chair Jerome Powell’s comments will be key, especially after a 7.8% rally in the S&P 500 since Oct. 12, triggered mostly by expectations of easing in the central bank’s hawkish narrative given risks to economic growth. Our full FOMC preview can be found here.

“It’s a matter of balance here — the Fed doesn’t want to signal too much hawkishness, but also doesn’t want to sound too dovish as that would result in a huge leg up in share prices and too much of an easing in financial conditions,” said Shane Oliver, head of investment strategy at AMP Services. Oliver feels caution is still needed. “We may have seen the bottom in the share market and certainly sentiment has been very negative, but by the same token given recession risks and the yield curve continuing to invert in the US, that suggests risks are still high,” he said on Bloomberg TV.

“It’s a challenge for messaging because they don’t want to ease financial conditions significantly,” said Julia Coronado, the founder of MacroPolicy Perspectives LLC. “They need tight financial conditions to keep cooling the economy off. So he doesn’t want to sound dovish, but he may want to go slower.”

“Continuation of the year-end rally is contingent on the Fed delivering on the pivot narrative,” said Barclays Plc strategists led by Emmanuel Cau, who see current market optimism as misplaced. “It feels premature for the Fed to loosen financial conditions via equity and bond markets — inflation is just too high.” Former Treasury Secretary Larry Summers also warned that expectations the central bank would pivot were “badly misguided,” saying the Fed should “stay on the current course.”

In premarket trading, US-listed Chinese stocks rallied for the second day and were set to extend Tuesday’s gains, after new unverified social media posts claimed the government is considering a slew of changes to its Covid Zero policy, including a shorter quarantine period for inbound travelers. Chipmaker Advanced Micro Devices rose after topping profit estimates, but Airbnb slumped after its bookings outlook for the fourth quarter fell short of expectations. Apple shares slipped after China ordered a seven-day lockdown of the area around Foxconn Technology Group’s main plant in Zhengzhou, a move that will severely curtail shipments in and out of the world’s largest iPhone factory. Here are all the notable premarket movers:

AMD rose 4.9% after topping profit estimates as the semiconductor company’s expansion into the server processor market helped offset falling demand for chips used in PCs.

Airbnb shares decline 6% after giving a downbeat outlook for 4Q bookings. While analysts applauded the firm’s robust 3Q results, they also highlighted the moderately weaker prospects for the alternative accommodation specialist amid FX headwinds.

Arcturus Therapeutics shares surge 33% in US premarket trading after the biotech entered a collaboration and license agreement with a unit of CSL. The pact reduces execution risk, Cantor Fitzgerald says, prompting the broker to raise its price target.

Bally’s cut to hold at Stifel, which says macro, regulatory and development risks in the near-term force the broker into “capitulation” and a move to the sidelines. Shares decline 1.8%

Bandwidth shares jump 15% in US premarket trading after the company forecast fourth-quarter revenue above the average analyst estimate and raised its full-year outlook.

Benefitfocus shares rise 48% to $10.35 in US premarket trading, after Voya Financial agreed to buy the company at $10.50 a share in cash.

Canada Goose cut its non-IFRS adjusted earnings per share guidance for the full year; the guidance missed the average analyst estimate. Shares declined as much as 3.6%.

Coty and L’Oreal declined after peer Estee Lauder’s second-quarter and full-year forecasts trailed consensus estimates, sinking the stock as much as 13% in premarket trading. Coty shares decline 2.8% and L’Oreal shares fell 1.7%.

Chegg jumps as much as 17.5% after the education-focused company reported better-than-expected third- quarter earnings and boosted its full-year outlook for revenue and adjusted Ebitda.

Match Group surges as much as 14.7% after the owner of dating apps including Tinder and OkCupid reported third-quarter revenue that beat the average analyst estimate and pledged to control costs. Analysts said that while 4Q and initial 2023 guidance were below expectations, they look achievable based on the current macro environment.

DuPont gain 3.6% in thin premarket trading after the company scrapped a planned $5.2 billion acquisition of Rogers Corp., a move which analysts say will bolster DuPont’s balance sheet and improve the scope for share buybacks.

Offerpad Solutions slump 3.8% in US premarket trading on Wednesday, ahead of the real estate firm’s third-quarter results due after the market close.

TFF Pharmaceuticals Inc. plunges 38% in premarket trading as studies of two inhaled powder therapies have been impacted by challenges tied to “staffing shortages, shipping, and global supply chain delays,” the company said in a release.

Tupperware shares plunged 33.4% after the company reported worse- than-expected third quarter results, including revenue and adjusted EPS that both missed analyst estimates.

Yum China shares jump 13.6% in US premarket trading after the restaurant operator reported flat same-store sales growth in the third quarter, enough to impress analysts who had expected a decline, given stringent Covid control measures in China.

ZoomInfo Technologies (ZI) shares plunge as much as 22% as analysts cut their price targets following 3Q results. Despite a beat-and- raise, comments from the software company that the operating environment is becoming more challenging show that it could be susceptible to a slowdown in the economy, according to analysts, who see growth moderating next year.

European equities are mixed after euro-area manufacturing activity sank to the lowest level since May 2020. Euto Stoxx 50 little changed, erasing earlier gains; the CAC 40 outperforms peers, while FTSE 100 and DAX lag. Healthcare stocks outperformed in Europe after Novo Nordisk A/S raised its operating profit and sales forecasts for the year; consumer products and personal care are among the best performing sectors. Here are some of the biggest European movers today:

Sinch shares rally as much as 36% after 3Q results, with improved free cash flow, reduced net debt and prolonged short- term financing giving another boost to the heavily shorted stock.

Shares in Danish wind turbine manufacturer Vestas rose as much as 8.6%, the most since August, after positive pricing concealed a 3Q results miss which led to a 5.5% fall in early trading.

Novo Nordisk rises as much as 5.9%, hitting the highest since August, with analysts noting the Danish drugmaker’s guidance raise and its confirmation on the timeline for its Wegovy obesity treatment.

Hiscox climbs as much as 6.2%, the most since August, after the insurer reported smaller-than- anticipated Hurricane Ian losses and solid trading across the rest of its business.

Next Plc rises as much as 3.7% after maintaining its profit guidance, which is a “small positive read to the online retail space,” RBC said.

Demant falls as much as 15%, the most since mid August, after the company cut its full- year guidance.

VGP slumps as much as 12% after Barclays downgraded the real estate developer to underweight from overweight.

Maersk drops as much as 7.3%, with Citi noting that the shipping firm’s lower expectations for contract rates are likely to weigh on investor sentiment.

Smurfit Kappa declines as much as 5.1% in Dublin after results, with Goodbody analysts highlighting the company’s “challenging market conditions” and labor inflation pressures. Packaging peer DS Smith also slides.

Euro-area manufacturing activity sank to the lowest level since 2020 and A.P. Moller-Maersk A/S, a bellwether for global trade, cut its forecast for the global container market, saying inflation will persist even as demand drops as much as 4% this year. The company’s shares fell.

Earlier in the session, Asian stocks headed for a three-day advance as growing speculation over China’s reopening spurred another strong rally, while traders awaited the Federal Reserve’s decision on interest rates. The MSCI Asia Pacific Index rose as much as 0.9%, led by the consumer discretionary sector. Chinese and Hong Kong stocks drove gains in the region as investors scooped up shares following wide circulation of unverified posts outlining a loosening of the nation’s Covid Zero policy. Still, enthusiasm that sparked the rally in Chinese stocks could fade if authorities there don’t follow up on the speculation, Jun Rong Yeap, a market strategist at IG Asia Pte, wrote in a note.

The Hang Seng Index had its best two-day run since March before the session was cut short by a storm warning; The Hang Seng China Enterprises Index rose 2.8%, also capping its best two-day rally since March. Trading in Hong Kong closed earlier than usual due to a tropical storm. Most other markets posted modest gains or declines as investors opted to wait and assess the Fed’s policy signals. Data on Tuesday showing a solid US labor market bolstered speculation that policy could remain aggressively tight even with the threat of a recession. The central bank is set to raise rates by 75 basis points for the fourth time in a row on Wednesday.

In rates, Treasuries were mixed ahead of FOMC rate decision at 2pm ET, with long-end yields slightly cheaper on the day and front-end yields richer by ~3bp, steepening the curve as the 2-year yield fell by around 3bps and 30-year yields added 2bps. 10-year TSY yields were little changed around 4.04% as the curve steepens around the sector; 2s10s, 5s30s spreads are wider by ~2bp and ~3bp on the day vs UK 2s10s, 5s30s spreads wider by ~9bp and ~13bp Broadly subdued price action compares with aggressive steepening in gilt curve, where 2- and 5-year UK yields are ~1bp richer on the day. Focus on Fed rate decision may limit price action over early US session; traders have been hedging prospect of Fed to hint at a slowdown in rate hikes for the December policy meeting over the past couple of weeks The quarterly refunding announcement at 8:30am is viewed as having limited potential for auction size changes and may signal progress toward a buyback program. Bunds bear-flattened, as yields rose up to 4bps. Italian bond yields rose by around 5bps across the curve.

In FX, the Bloomberg Dollar Spot Index fell by around 0.2% as the greenback was steady or weaker against all of its Group-of-10 peers amid positioning ahead of today’s Fed meeting. SEK and GBP are the weakest performers in G-10 FX, NZD and JPY outperform

The euro staged a slight rebound to trade around $0.99 after two days of losses against the dollar.

The pound was steady around $1.15 while front-end gilts rallied, sending 2- year yields down by around 11bps

The yen led G-10 gains along with New Zealand’s currency; the yen rose a second day versus the dollar. Bank of Japan Governor Kuroda told parliament the nation’s economy is no longer in deflation since the central bank started its current easing program, though added that inflation was seen slowing in fiscal year 2023; minutes of the BOJ’s September meeting noted it was desirable to keep an easing bias

The kiwi and sovereign yields advanced as unemployment stayed near a record low in the third quarter while wages surged.

In commodities, wheat futures fell after Turkey’s Erdogan said grain shipments via the Ukraine corridor would resume. oil traded near $88 a barrel ahead of the Fed rate decision. West Texas Intermediate futures pared an earlier gain to trade little changed with prices stuck in a $12 band over the last month. Glencore Plc officials delivered cash in private jets to officials in west Africa, UK prosecutors said as they laid out a web of bribery and corruption orchestrated by the London oil trading desk. President Joe Biden’s threat to slap a tax on oil-company profits is more bluster than threat as the clock runs out on the administration’s efforts to tame fuel prices ahead of midterm elections. Spot gold rises roughly $8 to trade near $1,656/oz as traders mull the possibility of a rate-hike slowdown.

Market Snapshot

S&P 500 futures up 0.3% to 3,877.75

STOXX Europe 600 up 0.4% to 416.07

MXAP up 0.8% to 139.99

MXAPJ up 0.8% to 448.01

Nikkei little changed at 27,663.39

Topix up 0.1% to 1,940.46

Hang Seng Index up 2.4% to 15,827.17

Shanghai Composite up 1.2% to 3,003.37

Sensex down 0.5% to 60,846.16

Australia S&P/ASX 200 up 0.1% to 6,986.66

Kospi little changed at 2,336.87

Brent Futures up 0.2% to $94.81/bbl

Gold spot up 0.3% to $1,652.92

U.S. Dollar Index down 0.27% to 111.18

German 10Y yield up 0.5% to 2.14%

Euro up 0.3% to $0.9902

Top Overnight News from Bloomberg

Overnight volatility rallies for the major currencies as traders position for the Federal Reserve monetary policy decision later Wednesday. Pound hedging costs lead the race as the Bank of England also meets Thursday

The Federal Reserve looks set to deliver a fourth straight super-sized rate increase with Chair Jerome Powell repeating his resolute message on inflation and opening the door to a downshift — without necessarily pivoting yet

Euro-area manufacturing activity sank to the lowest level since the first Covid-19 lockdowns in 2020 as record inflation and a weakening global economy erode demand for goods

German companies have never been so concerned about sales as they struggle with the energy crisis and a gloomy world economy, and they fear the worst is yet to come, a survey found

People’s Bank of China Governor Yi Gang gave an optimistic outlook for the economy on Wednesday, saying it remains “broadly on track” and he hoped the property market can achieve a “soft landing”

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed with the region cautious and price action mostly rangebound after the lacklustre handover from the US where strong JOLTS data spurred a more hawkish Fed terminal rate pricing and as markets await the FOMC. ASX 200 was kept afloat by strength in the commodity-related sectors but with upside capped after PM Albanese rejected providing cash handouts and with the property industry pressured after home loans and building approvals fell. Nikkei 225 was indecisive as earnings releases remained in focus and officials continued their currency jawboning. KOSPI wiped out nearly all its early gains amid geopolitical concerns after North Korea reportedly fired at least 10 missiles and which was the first time its missiles fell near South Korea’s territorial waters. Hang Seng and Shanghai Comp eventually extended their recent rumour-driven surge regarding China reopening despite the denial by a Foreign Ministry spokesperson and with officials pledging policy support measures, while Hong Kong markets were closed after half-day due to a storm signal 8.

Top Asian News

PBoC Governor Yi said China’s economy is broadly on track and potential growth is to remain in a reasonable range, and noted that inflation remains subdued and accommodative monetary policy is to support the economy. PBoC Governor Yi added that they will continue to improve the business environment, while they will deepen supply-side reforms and step up targeted support for key and weak sectors, according to Reuters.

China state planner official said China’s foreign investment increased steadily so far this year and will encourage more foreign investment in the manufacturing industry, according to Reuters.

China locked down the area around the world’s largest iPhone factory, according to Bloomberg.

BoJ September Meeting Minutes stated a few members said they need to be vigilant to the impact monetary tightening by some central banks could have on global markets, while several members said a weak yen could hurt households, small firms and non-manufacturers. Members agreed that Japan’s economy is picking up and several members said the BoJ must communicate to the public its monetary policy does not directly target FX moves.

RBNZ Financial Stability Report noted that the financial system remains resilient but added some households and businesses will be challenged by the rising interest rate environment, while it also stated that there are increasing downside risks to the global economic outlook and the extent to which the economic activity will slow due to monetary policy tightening remains uncertain. Furthermore, the RBNZ later stated it will consider tightening policy faster or slower at the Monetary Policy Statement.

Chinese Commerce Ministry says it will expand the imports of advanced technology, key equipment and components, and increase imports of energy and agricultural products in short supply, via a Party Congress supplementary reading cited by Reuters.

European bourses are mixed as the initial positive bias faded amid downward PMI revisions and increasing geopolitical tensions, Euro Stoxx 50 +0.2%. Health Care is the outperforming sector after Q3 earnings from GSK (+1.6%) and Novo Nordisk (+4.5%), more broadly sectors are mixed with no overarching bias. US futures are similarly contained but have been less reactive to the geopolitical and PMI developments as participants remain firmly affixed on the Fed, ES Unch. & NQ +0.2%. A.P. Moeller-Maersk (MAERSK DC) expect a slowdown of the global economy to lead to softer market in ocean. Cuts FY22 global container demand forecast to -2% to -4%. Freight rates have begun normalising during Q3; Maersk -5.0%. Moody’s downgrades the outlook for the banking sector in Germany, Italy, Hungary, Poland, Slovakia, to negative from stable; citing energy crisis, high inflation, and rising rates, via Reuters.

Top European News

Germany’s DIHK says German companies are bracing for another economic slump in the next 12 months; 52% of firms see business worsening in the next 12 months; says German GDP should be +1.2% in 2022 and -3% in 2023,

Germany’s VDMA engineering orders in Sep -5% Y/Y (Domestic -4%, Foreign Orders +8%); in first 9M orders +1% Y/Y (Domestic -3%, Foreign +2%)

Next Sales Better Than Expected Despite UK’s Costs Crisis

Vestas Cuts Outlook Again as Wind Turbine Industry Spirals

North Korea Fires 17 Missiles in Biggest-Ever Daily Barrage

Novo Boosts Sales Forecast on Demand for Obesity Drug Wegovy

Sampo 3Q Pretax Profit Misses Estimates; Decides on Dual Listing

Britishvolt Says Loan Gives EV Battery Startup Weeks of Runway

FX

USD is under modest pressure as we count down to the FOMC, action which is benefiting peers across the board with the antipodeans and JPY currently the main beneficiaries.

DXY has slipped to a 111.12 low from earlier highs above the 111.50 mark, with brief respite for the USD occurring alongside the NY Times article re. Russia.

EUR/USD relatively unreactive to the morning’s PMI revisions, downbeat commentary and numerous surveys out of Germany featuring a similar narrative, single currency holding around 0.9900.

NZD outpaces and has lifted to a test of the 0.59 mark, where the current WTD peak resides, following domestic data which seemingly keeps hawkish impulses in focus.

JPY is the next best performer given its haven status and after BoJ Minutes noted several members said a weak yen could hurt; USD/JPY probing but yet to lose 147.00.

BoC Governor Macklem said they expect the policy rate will need to rise further and how much further rates will go up depends on how monetary policy is working, how supply chains are resolving and how inflation is responding to tightening. Macklem added that there are no easy outs to restoring price stability and reiterated the tightening phase will draw to a close and they are getting close but are not there yet.

Fixed Income

EGBs are modestly pressured with yields a touch higher as such, though the complex is currently relatively contained ahead of a busy PM docket incl. the FOMC.

USTs are essentially flat with yields incrementally steeper but similarly contained as such; note, the pre-FOMC docket is busy and features ADP alongside Quarterly Refunding.

Back to Europe, Bunds and peers haven’t been too reactive to the downbeat PMI releases/commentary, with Bunds also conscious of upcoming Green supply; 10yr yield continues to lift from 2.10%.

Commodities

Crude benchmarks have given up their USD and China induced APAC upside amid downbeat commentary from Maersk and the EZ Final Manufacturing PMIs.

Currently, the benchmarks are incrementally softer on the session and in proximity to the USD 88/bbl and USD 94/bbl handles for WTI and Brent respectively.

Spot gold is deriving support from the USD’s pullback and renewed geopolitical focus on both N.Korea and Russia, with the yellow metal having surpassed its 10-DMA but currently capped by the 21-DMA at USD 1659/oz; base metals similarly firmer on the USD action and overnight trade.

Russia’s Kremlin exports of Russian fertiliser was an integral part of grain deal, but difficulties remain; says Russia’s participation in the deal remains suspended, via Reuters; prior to this, Turkish President Erdogan said the Russian Defence Minister told his Turkish counterpart the the grain deal will resume; grain deal will resume on mid-day Wednesday.

Most recently, Russia is to resume participation in the Black Sea grain deal, according to Reuters citing the Defence Ministry; it was possible to obtain written guarantees from Kyiv not to use grain corridor for military operations against Russia.

Geopolitics

Ukrainian President Zelensky said they need reliable, long-term defence for the grain corridor and that Russia must be told it will receive a firm world response if it takes steps to disrupt Ukrainian food exports, according to Reuters.

Senior Russian military leaders recently had conversations to discuss when and how Moscow might use a tactical nuclear weapon in Ukraine, according to NYT citing sources, President Putin was not part of the conversations; “The intelligence about the conversations was circulated inside the U.S. government in mid-October.”.

North Korea has reportedly fired at least 23 missiles in total from the east and west coasts on Wednesday the initial rounds of which prompted South Korea to place its Ulleung Island under an air raid warning and was the first time North Korean missiles fell near the South’s territorial waters, according to Yonhap and YTN.

South Korean President Yoon ordered a swift and firm response and South Korea launched air-to-ground missiles which were fired towards the north of the maritime border, while South Korea closed some air routes off the east coast of the Korean peninsula after North Korea’s missile launches, according to the Transport Ministry cited by Reuters.

US Event Calendar

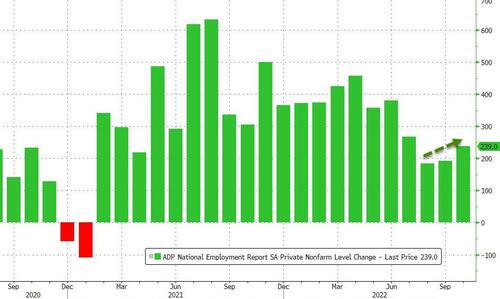

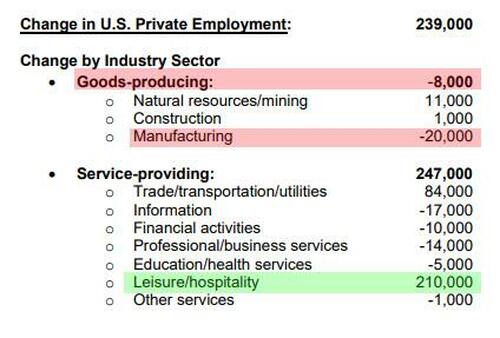

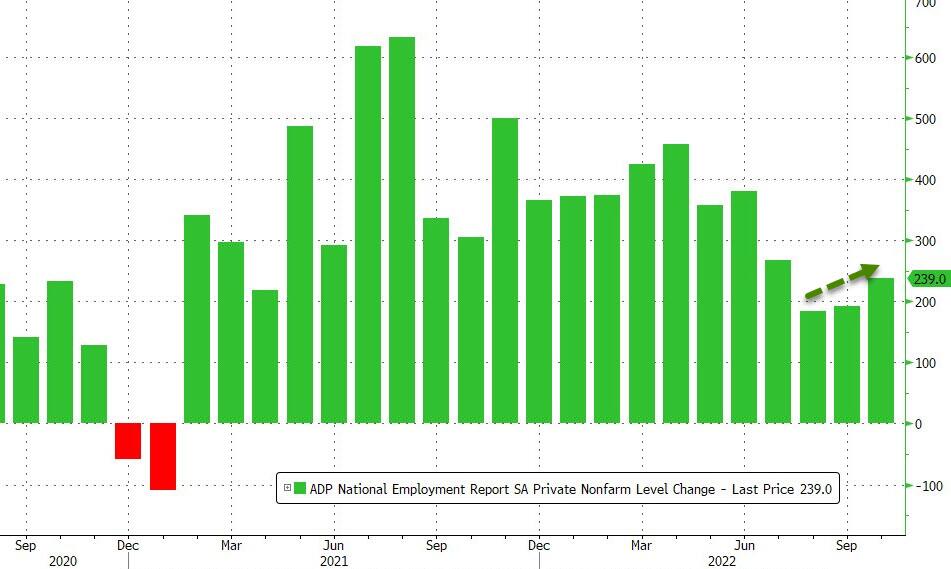

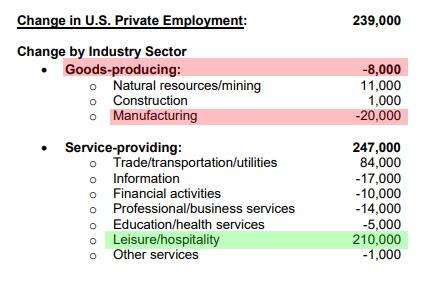

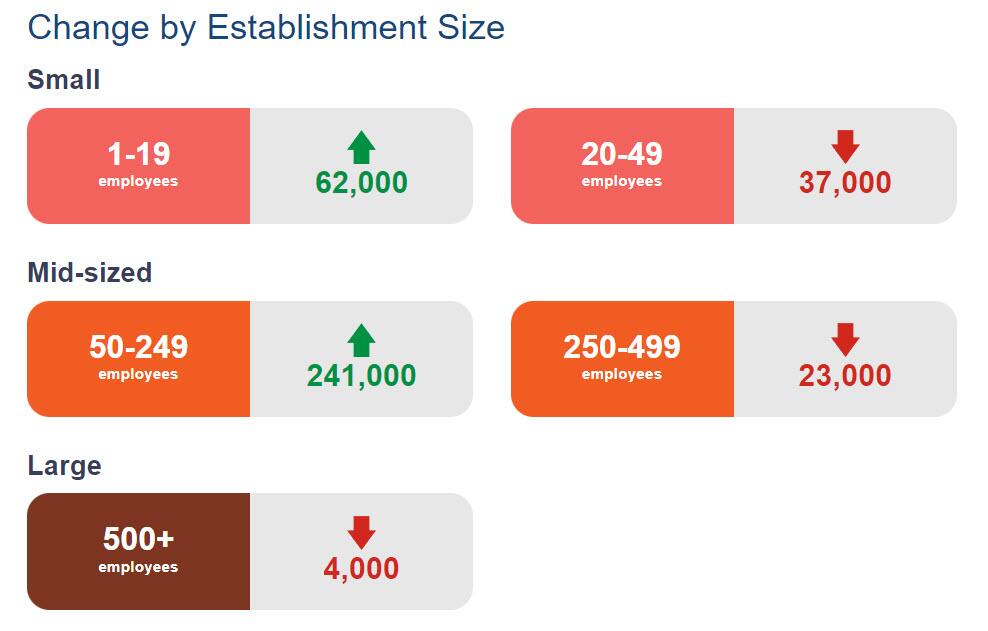

07:00: Oct. MBA Mortgage Applications, prior -1.7%

08:15: Oct. ADP Employment Change, est. 185,000, prior 208,000

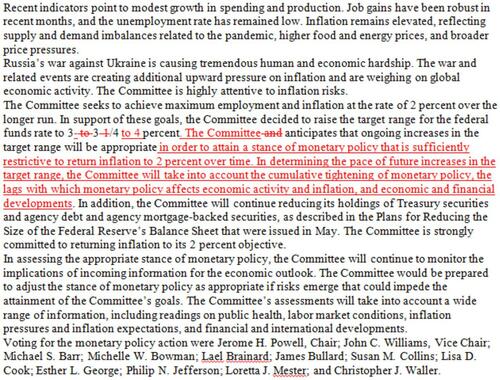

14:00: Nov. FOMC Rate Decision

DB’s Jim Reid concludes the overnight wrap

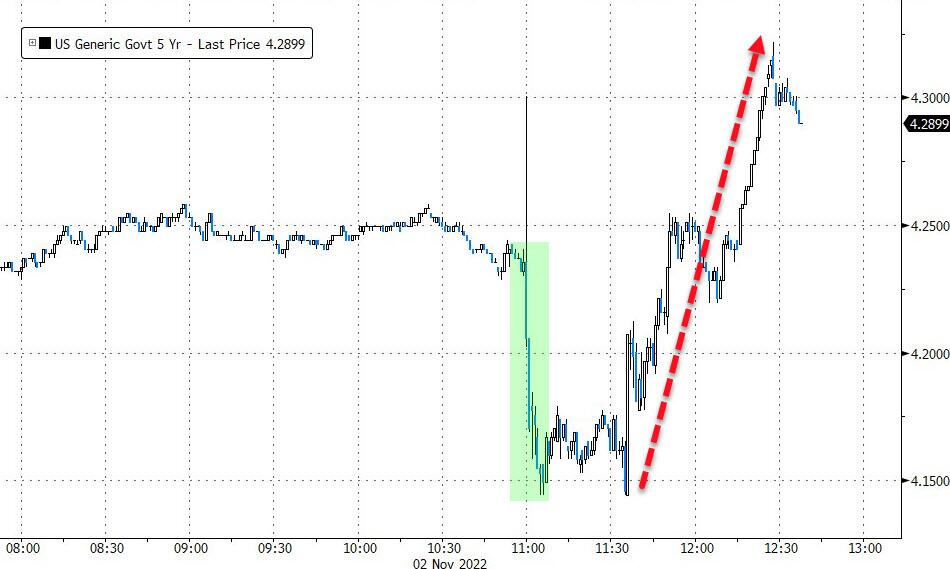

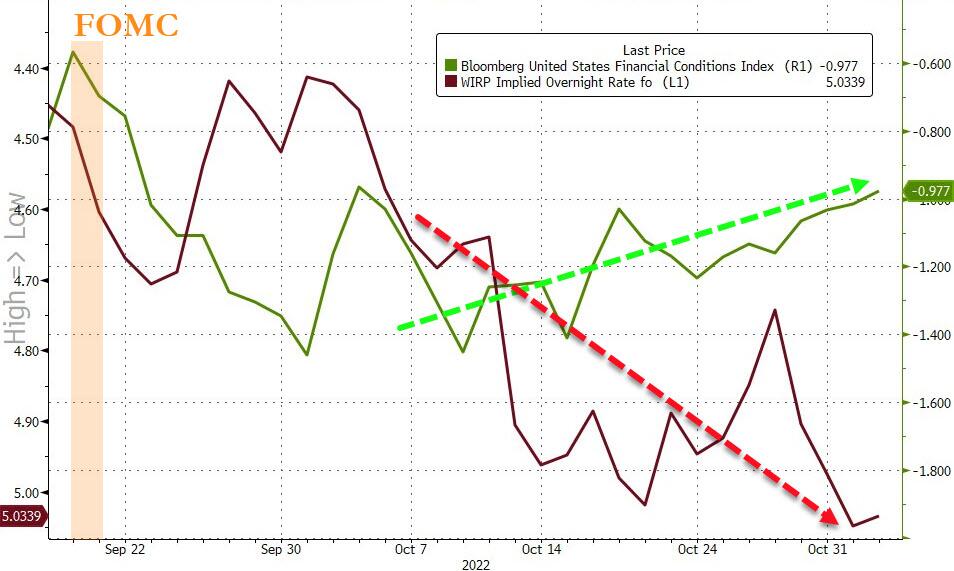

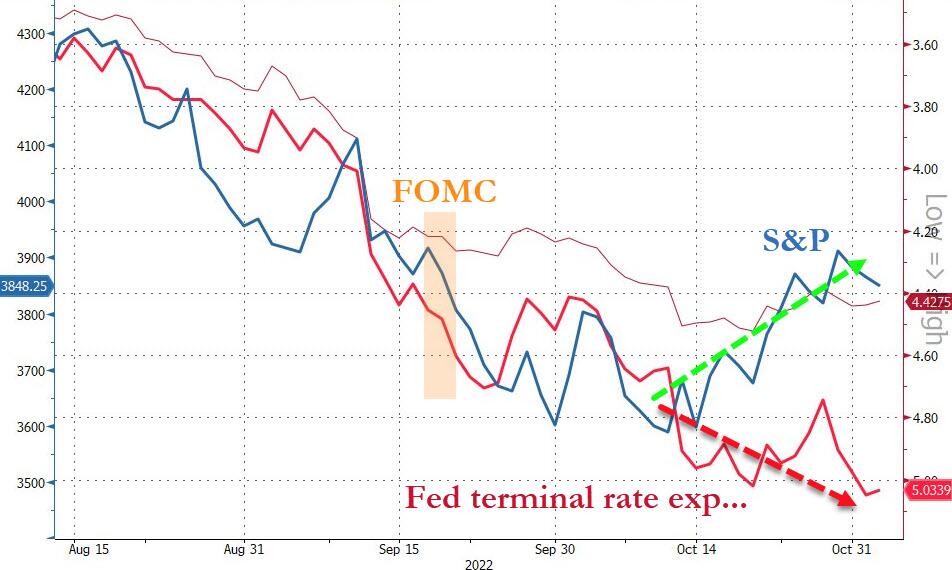

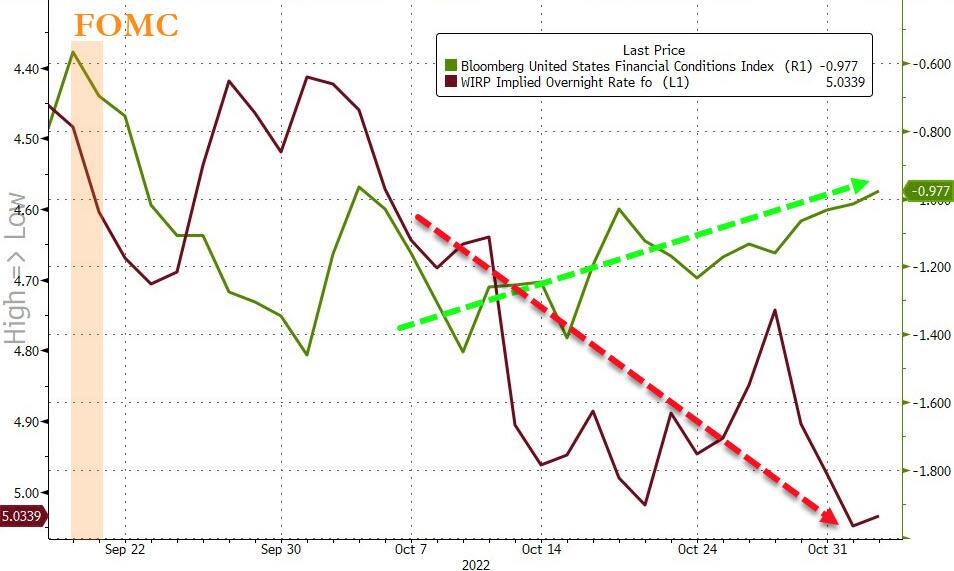

As we arrive at the latest decision day for the Fed, any remaining hopes of a dovish pivot continued to fizzle out over the last 24 hours, with futures once again pricing in a terminal fed funds rate above 5%. The main driver behind that was another round of US data yesterday, which showed that labour markets were tighter and the economy was in better shape than previously thought, which in theory should give the Fed more space to keep hiking rates. In turn, that prompted a big turnaround for risk assets, with the S&P 500 (-0.41%) losing ground for a second day running, whilst 10yr Treasury yields shot up by more than +15bps intraday after the releases came out.

Ahead of those releases, there had actually been a strong rally across multiple asset classes thanks to speculation that China might ease up on their Covid restrictions (more on which below). But the latest data caused a sharp reversal shortly after US markets opened, particularly given the news that US job openings had unexpectedly risen in September to 10.717m (vs. 9.750m expected), alongside an upward revision to the August number. That means there were still 1.86 job openings per unemployed worker in September, which is creating significant inflationary pressures, and suggests that the decline in job openings in August to a one-year low might have been a blip. On top of that, the quits rate of those voluntarily leaving their jobs (which is strongly correlated with wage growth) remained at 2.7% for a third month running.

Just as the labour market appeared to be in surprising strength, there was an additional dose of optimism about the economy from the ISM manufacturing reading for October, which came in at 50.2 (vs. 50.0 expected). Although it’s true that was the weakest reading since May 2020, it was still a touch better than expected and came amidst improvements in the employment (50.0) and new orders (49.2) components relative to last month, which gave further ground for optimism. In addition, the final manufacturing PMI for October was revised up half a point from the flash reading to 50.4, leaving it back above the 50-mark that separates expansion from contraction.

When it comes to today’s policy decision, the Fed are widely expected to hike rates by 75bps for a fourth consecutive meeting. But the more important question for markets today (and where there’s considerably more doubt) is whether the Fed might signal a downshift in the pace of hikes at subsequent meetings. This is a tricky balancing act for them, since any signal of a pivot risks leading to easier financial conditions that makes their job of bringing down inflation even harder. That was what happened after the July meeting, where investors interpreted matters in a dovish light, and the Fed had to reiterate their hawkish intent, culminating in Chair Powell’s August speech at Jackson Hole. Our US economists write in their preview (link here) that Chair Powell’s press conference will likely not pre-judge the outcome of the December meeting and will emphasise the data dependence of the decision, not least with another couple of CPI reports and jobs reports beforehand. They expect him to leave open the prospects of another 75bp hike in December, but present a strong base case for downshifting the pace of hikes by early 2023 at the latest.

Ahead of the Fed’s decision, markets moved to ratchet back up their expectations of how high they’re set to take rates over the coming months. Indeed, the rate priced in by end-2023 moved up another +9.9bps to 4.66%, which brings its gains over the last 3 sessions to +37.1bps and means that the bulk of the move lower after October 21 thanks to Nick Timiraos’ WSJ article has now reversed. In light of that, 2yr Treasuries yield gained +6.2bps on the day to reach 4.54%, with the moves higher occurring entirely after those strong US data releases mentioned above. The 10yr Treasury yield (-0.6bps) did close slightly lower at 4.04%, but that was still more than +10bps above its intraday levels prior to the releases and in overnight trading they’re back up +0.9bps to 4.05%. Over in Europe, sovereign bonds followed a similar pattern over the day, with a sharp intraday reversal following the US data, although yields on 10yr bunds (-1.0bps), OATs (-0.1bps) and BTPs (-3.5bps) still ended the session lower.

Those expectations of a more hawkish Fed led to a reversal for equities too, and the S&P 500 (-0.41%) swiftly gave up its gains after the open to fall back for a second consecutive session. Tech stocks led the declines once again, and there was a significant milestone for the FANG+ index (-0.95%) of megacap tech stocks, with the index closing at a 2-year low, having now shed -45.65% since its peak just under a year ago. European equities ended the day in positive territory, albeit only after giving up a decent chunk of their earlier gains, with the STOXX 600 moving from an intraday peak of +1.51% to only close up +0.53%.

That earlier momentum had been propelled in large part thanks to speculation about a potential end to Covid restrictions in China, with that backdrop seeing the CSI 300 post its strongest daily performance since March yesterday. The moves were triggered by unconfirmed posts on social media that China was forming a committee which would look at relaxing restrictions, with a suggestion for reopening in March 2023. However, a spokesman for the Chinese Foreign Ministry said that he was “not aware of what you mentioned” when asked about the issue at a press briefing on Tuesday.

Overnight in Asia, that continued speculation about a policy reversal has seen a fresh outperformance in a number of equity indices, with the Hang Seng (+2.50), the CSI 300 (+1.48%) and the Shanghai Comp (+1.29%) all recording solid gains. That’s in spite of the absence of any official confirmation about a change in China’s policy. Elsewhere, some of the other indices have been more mixed, with the Nikkei (-0.10%) slightly lower and the Kospi (+0.24%) recording a modest advance, although US futures are pointing in a more positive direction, with those on the S&P 500 up +0.32% ahead of the Fed’s decision.

On the data side, there were some fresh indications of global inflationary pressures overnight, with South Korea’s CPI inflation seeing its first rebound in three months as it rose to +5.7% as expected, whilst core CPI surpassed expectations to hit a 13-year high of +4.8% (vs. 4.5% expected). In the meantime, we also heard from Bank of Japan Governor Kuroda who reiterated their dovish policy, saying that they were not thinking of rate hikes or changing their yield curve control policies now.

Back in the US, we’re now less than a week away from the mid-term elections on Tuesday, and momentum has remained with the Republicans in recent days. According to FiveThirtyEight’s model, they now have a 51% chance of taking the Senate, which is up from 30% only six weeks ago, whilst the chances of them regaining the House now stand at 83%.

To the day ahead now, and the main highlight will be the Fed’s latest policy decision and Chair Powell’s press conference. In the meantime, ECB speakers today include Makhlouf, Villeroy and Nagel. On the data side, we’ll get October data on German unemployment, the final Euro Area manufacturing PMIs, and the ADP’s report of private payrolls for the US. Finally, earnings releases include Qualcomm, CVS Health and Booking Holdings.

end

AND NOW NEWSQUAWK (EUROPE/REPORT)

European bourses are mixed; North Korea has reportedly fired at least 23 missiles in total; Russian-Ukraine grain deal resumes – Newsquawk US Market Open

WEDNESDAY, NOV 02, 2022 – 06:42 AM

European bourses are mixed as the initial positive bias faded amid downward PMI revisions and increasing geopolitical tensions

US futures similarly contained and less reactive to the above factors pre-FOMC

DXY under modest pressure to the benefit of G10 peers with antipodeans and JPY outpacing, EGBs/USTs contained with a slight negative bias

Crude benchmarks have given up their USD and China induced APAC upside amid downbeat commentary from Maersk and the EZ Final Manufacturing PMIs.

North Korea has reportedly fired at least 23 missiles in total from the east and west coasts on Wednesday

Ags in focus amid two-way commentary from Russian and Turkish officials

Looking ahead, highlights include Australian Services & Composite PMI (Final), FOMC Policy Announcement & Press Conference.

Or why not try Newsquawk’s squawk box free for 7 days?

EUROPEAN TRADE

EQUITIES

European bourses are mixed as the initial positive bias faded amid downward PMI revisions and increasing geopolitical tensions, Euro Stoxx 50 +0.2%.

Health Care is the outperforming sector after Q3 earnings from GSK (+1.6%) and Novo Nordisk (+4.5%), more broadly sectors are mixed with no overarching bias.