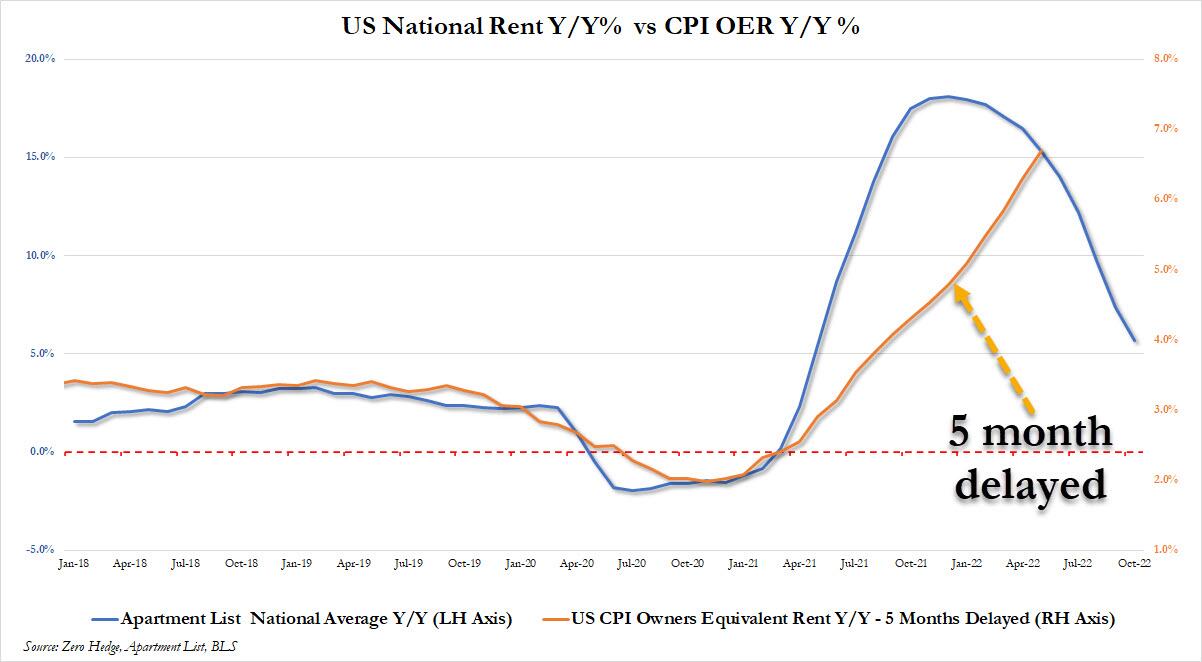

NOV 3/ POST POWELL NON PIVOT REACTION:GOLD CLOSED DOWN $18.30 TO $1628.05//SILVER DOWN 16 CENTS TO $19.43//PLATINUM DOWN $25.75 TO $922.50//PALLADIUM DOWN $72.00 TO $1815.60//COVID UPDATES: CHINA’S IPHONE CITY IN TOTAL CHAOS WITH THEIR ZERO COVID POLICY//DR PAUL ALEXANDER//VACCINE IMPACT, VACCINE INJURY/SLAY NEWS//UK RAISES RATES BY .75% BUT VERY UNCOMFORTABLE WITH THE RAISE//RUSSIA MOVING 70,000 CITIZENS FROM KHERSON BECAUSE OF FEAR OF A BOMBING OF THEIR DAM//USA RENTS TUMBLING BECAUSE OF THE DOWNTURN IN THE ECONOMY//ALSO DOWNDRAFT IN USA SERVICE INDUSTRY SERVICE ALSO PAINTS A PICTURE THAT THE USA IS IN A HUGE DOWNTURN//SWAMP STORIES FOR YOU TONIGHT//

118 C MACQUARIE FUT 298 132 C SG AMERICAS 41 190 H BMO CAPITAL 130 323 C HSBC 82 435 H SCOTIA CAPITAL 250 657 C MORGAN STANLEY 3 661 C JP MORGAN 391 486 690 C ABN AMRO 74 732 C RBC CAP MARKETS 9 737 C ADVANTAGE 28 45 800 C MAREX SPEC 9 11 880 H CITIGROUP 228 905 C ADM 15

TOTAL: 1,050 1,050 MONTH TO DATE: 3,86

JPMORGAN STOPPED 486/1050

GOLD: NUMBER OF NOTICES FILED FOR NOV. CONTRACT: 1050 NOTICES FOR 105,000 OZ or 3.2659 TONNES

total notices so far: 3867 contracts for 386700 oz (12.0279 tonnes)

SILVER NOTICES: 63 NOTICE(S) FILED FOR 315000 OZ/

total number of notices filed so far this month 154 : for 770,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $18.30

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////A BIG CHANGE IN GLD INVENTORY: A WITHDRAWAL OF 4.05 TONNES FROM THE GLD// /INVENTORY LOWERS TO 920.57 TONNES

INVENTORY RESTS AT 915.07 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 16 CENTS

AT THE SLV// :/SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF OF .566 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 482.650 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A SMALL SIZED 155 CONTRACTS TO 138,588 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE SMALL LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.09 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS/HFT WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.09)., AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC LONGS, AS WE HAD A GOOD GAIN IN OUR TWO EXCHANGE OF 495 CONTRACTS. SOME SPECS TRIED TO COVER THEIR SHORTFALLS // OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. SOME NEWBIE SPEC LONGS ADDED TO THEIR POSITIONS ESPECIALLY AT THE LOWER PRICES

WE MUST HAVE HAD: I) SOME SPECULATOR SHORT COVERINGS SOME NO SHORT ADDITIONS ////CONTINUED BANKER OI COMEX ADDITIONS /// SOME NEWBIE SPEC LONG ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.045 MILLION OZ FOLLOWED BY TODAY’S 95,000 QUEUE JUMP//NEW STANDING:1.220 MILLION OZ/ / // V) SMALL SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: +32

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS NOV. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF NOV:

TOTAL CONTRACTS for 3 days, total 2790 contracts: 13.950 million oz OR 4.65MILLION OZ PER DAY. (930 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 13.95 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 13.95 MILLION

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 155 WITH OUR $0.09 LOSS IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE CONTRACTS: 650 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR NOV. OF 1.345 MILLION OZ FOLLOWED BY TODAY’S 95,000 QUEUE JUMP/ .. WE HAVE A GOOD SIZED GAIN OF 495 OI CONTRACTS ON THE TWO EXCHANGES FOR 2.415 MILLION OZ..

WE HAD 63 NOTICE(S) FILED TODAY FOR 315,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A TINY SIZED 218 CONTRACTS TO 467,431 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -373 CONTRACTS.

.

THE TINY SIZED DECREASE IN COMEX OI CAME WITH OUR FALL IN PRICE OF $0.55//COMEX GOLD TRADING/WEDNESDAY // ZERO SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION AND SOME SPEC SHORT COVERINGS . // CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR NOV. AT 12.386 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE 52,200 OZ QUEUE JUMP //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR FALL IN PRICE OF $0.55 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 2900 OI CONTRACTS 9.02 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2900 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 467,058

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2900 CONTRACTS WITH 218 CONTRACTS DECREASED AT THE COMEX AND 3118 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2900 CONTRACTS OR 9.020 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3118) ACCOMPANYING THE TINY SIZED LOSS IN COMEX OI (218): TOTAL GAIN IN THE TWO EXCHANGES 3273 CONTRACTS. WE NO DOUBT HAD 1) MINOR SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS/// // CONSIDERABLE NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR NOV. AT 12.386 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 52,200 OZ //NEW STANDING 17.017 TONNES///3) ZERO LONG LIQUIDATION //// //.,4) TINY SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

NOV

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV. :

8153 CONTRACTS OR 815,300 OZ OR 25.35 TONNES 3 TRADING DAY(S) AND THUS AVERAGING: 2717 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAY(S) IN TONNES: 25.35 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 25.35/3550 x 100% TONNES 0.714% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 25.35 TONNES//INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A SMALL SIZED 155 CONTRACT OI TO 138,720 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 650 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 650 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 650 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 155 CONTRACTS AND ADD TO THE 650 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GOOD SIZED GAIN OF 495 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 2.475MILLION OZ//

Last year, Nigeria launched its much-ballyhooed eNaira, Africa’s first central bank digital currency (CBDC).

Central bankers, academics, politicians, and an assortment of elites from over 100 countries hoping to launch their own CBDCs have closely followed the eNaira.

They used Nigeria—Africa’s largest country by population and size of its economy—as a Petri dish to test their nefarious plans to use CBDCs to enslave the people of North America, Europe, and beyond.

The jury is now in.

The eNaira has been a massive failure.

According to Bloomberg, only 1 in 200 Nigerians use the eNaira. That’s even after the government implemented discounts and other incentives as desperate measures to increase adoption.

This came as a surprise to the elites.

Nigeria has one of the highest Bitcoin adoption rates in the world—ranking #11 among all countries.

Bitcoin’s ability to bypass the government’s capital controls—which restrict the use of foreign currencies and sending and receiving money from abroad—was a big draw for Nigerians, as it is in other countries with these repressive policies.

A long history of rampant currency debasement in Nigeria—including six devaluations in recent years—also helped spur the adoption of Bitcoin, which is totally resistant to inflation.

In short, the elites have miscalculated. They figured Nigerians wouldn’t be able to differentiate between Bitcoin and the eNaira—they are both digital currencies, after all.

The Bloomberg article admitted, “Nigerians’ passion for cryptocurrencies doesn’t extend to the central bank offering.”

It also said Nigerians view the eNaira as “a symbol of distrust in the ruling elite” and that the people view the government as “hostile to them and therefore have no interest in anything it introduces.”

To all the Nigerians rejecting the eNaira, I say bravo!

The failure of CBDCs in Nigeria could throw sand in the gears of the elites’ plan to implement them worldwide. That would be a big positive for human freedom.

The flop of CBDCs in Nigeria is an encouraging development.

It also reveals an outcome that was probably the opposite of what the elites desired—increased Bitcoin adoption.

CBDCs and Bitcoin

Despite all the hype, CBDCs are nothing but the same fiat currency scam on steroids.

It’s doubtful CBDCs can save otherwise fundamentally unsound currencies—as I believe all fiat currencies are.

If the current fiat system is not viable, then CBDCs are even less viable as they enable the government to engage in even more currency debasement.

Would a CBDC have saved the Zimbabwe dollar, the Venezuelan bolivar, the Argentine peso, or the Lebanese lira?

I don’t think so.

The eNaira did not save the Nigerian fiat currency. And a CBDC won’t save the US dollar or the euro from their fates either.

There are a lot of bad things that come with CBDCs.

But there’s a silver lining…

CBDCs are going to introduce and familiarize people with using digital currencies. It’s then only then a matter of time before they discover Bitcoin.

CBDCs and Bitcoin share some characteristics. For example, they are both digital and facilitate fast payments from a mobile phone. But that is where the similarities end.

The reality is that CBDCs and Bitcoin are entirely different in the most fundamental ways.

You need the government’s permission and blessing to use a CBDC, whereas Bitcoin is permissionless.

Governments can (and will) create as many CBDC currency units as they want. With Bitcoin, there can never be more than 21 million, and there is nothing anyone can do to inflate the supply more than the predetermined amount in the protocol.

CBDCs are centralized. Bitcoin is decentralized.

Governments can censor transactions and freeze, sanction, and confiscate CBDC units whenever they want. Bitcoin is censorship-resistant. No country’s sanctions or laws can affect the protocol.

There is no privacy with CBDCs. However, with Bitcoin, if you take specific steps, it is possible to maintain reasonable privacy.

CBDCs are government money that are easy to produce and give politicians a terrifying amount of control over people’s lives. On the other hand, Bitcoin is non-state hard money that helps liberate individuals from government control.

In short, CBDCs are a pathetic attempt to compete with Bitcoin.

CBDCs make an inferior form of money even worse, but at the same time, it’s an excellent Trojan Horse for Bitcoin.

It doesn’t take much imagination to see that once governments inevitably inflate their CBDC units, censor transactions, freeze people’s accounts, and confiscates funds, it will push people to look for better digital alternatives, first and foremost Bitcoin.

That’s how, contrary to conventional wisdom, CBDCs could be an enormous catalyst for Bitcoin adoption. The failure of the eNaira in Nigeria is proof of this dynamic.

* * *

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 5.56 PTS OR 0.19% //Hang Seng CLOSED DOWN 487.08 OR 3.08% /The Nikkei closed HOLIDAY //Australia’s all ordinaires CLOSED DOWN 1.77% /Chinese yuan (ONSHORE) closed DOWN TO 7.4166 //OFFSHORE CHINESE YUAN DOWN 7.3104// /Oil UP TO 88.48, dollars per barrel for WTI and BRENT AT 95.00 / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A TINY SIZED 218 CONTRACTS TO 467,058 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR FALL IN PRICE OF $0.55 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (3118 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF NOV.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3118EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC : 3118 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3118 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2900 CONTRACTS IN THAT 3118LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A TINY SIZED COMEX OI GAIN OF 155 CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $0.55//WE HAD MINOR SPEC SHORTS COVERINGS WITH BANKERS AS BUYERS OF COMEX GOLD CONTRACTS. WE ALSO HAD STRONG ADDITIONAL NEWBIE SPECS GOING LONG

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING NOV (17.017),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 17.017 TONNES/INITIAL

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $0.55) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES//// SPEC SHORTS COVERED A SMALL PORTION OF THEIR POSITIONS AS WE HAD A GOOD SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 3273 CONTRACTS // WE HAVE REGISTERED 9.020 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR NOV. (17.017 TONNES)…THIS WAS ACCOMPLISHED WITH OUR FALL IN PRICE OF $0.55

WE HAD -373 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3273 CONTRACTS OR 327,300 OZ OR 10.180 TONNES

Estimated gold volume 270,466// fair to good//

final gold volumes/yesterday 250,501/ fair

INITIAL STANDINGS FOR NOVEMBER 2022 COMEX GOLD //NOV 3

Total monthly oz gold served (contracts) so far this month

3867 notices 386700 12.0279TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

customer withdrawals:2

ii) Out of Brinks 2,154.120 (67 kilobars)

iii) Out of HSBC: 13,173.939 oz

total: 15,328.059 oz

total in tonnes: 0.476 tonnes

Adjustments: 1// customer to dealer Int Delaware: 96.45 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR NOVEMBER.

For the front month of NOV. we have an oi of 2654 contracts having LOST 265 contracts. We had 787 notices served upon TUESDAY so we gained a whopping 522

or an additional 52,200 will stand in this non active month of November. We will have Nov gold tonnage standing increase daily from this day forth until the end of the month.

This queue jumping originates in London with the exercising of London based EFP’s for comex gold.

December LOST 3688 contracts DOWN to 347,087.

JANUARY LOST 18 contracts to stand at 36.

February gained 1474 contacts up to 82,203.

We had 1050 notice(s) filed today for 105,000 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 391 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1050 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 486 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the NOV. /2022. contract month,

we take the total number of notices filed so far for the month (3867) x 100 oz , to which we add the difference between the open interest for the front month of (NOV 2654 CONTRACTS) minus the number of notices served upon today 1050 x 100 oz per contract equals 547,100 OZ OR 17.017 TONNES the number of TONNES standing in this non active month of NOV.

thus the INITIAL standings for gold for the NOV. contract month:

No of notices filed so far (3867) x 100 oz+ (2654) OI for the front month minus the number of notices served upon today (1050} x 100 oz} which equals 547,100 oz standing OR 17.017 TONNES in this NON active delivery month of NOV..

TOTAL COMEX GOLD STANDING: 17.017 TONNES (A HUMONGOUS STANDING FOR NOV (GENERALLY THE POOREST DELIVERY MONTHS FOR A NON ACTIVE MONTH)

To calculate the number of silver ounces that will stand for delivery in NOV. we take the total number of notices filed for the month so far at 154 x 5,000 oz = 770,000 oz

to which we add the difference between the open interest for the front month of NOV(153) and the number of notices served upon today 63 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the NOV../2022 contract month: 154 (notices served so far) x 5000 oz + OI for front month of NOV (153) – number of notices served upon today (63) x 5000 oz of silver standing for the NOV. contract month equates 1,220,000 oz.

We will gain in silver oz standing from this day forth until the end of the month.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

NOV 3/WITH GOLD DOWN $18.30 TO $1628.85: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.05 TONNES FROM THE GLD////INVENTORY RESTS AT 915.07 TONNES

NOV 2/WITH GOLD UP 55 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 919.12 TONNES.

NOV 1/WITH GOLD UP $9.20 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES FORM THE GLD../INVENTORY RESTS AT 920.57 TONNES

OCT 31/WITH GOLD DOWN $4.00; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD//INVENTORY RESTS AT 922.59. TONNES//

OCT28/WITH GOLD DOWN $19.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 TONNES FROM THE GLD..///INVENTORY RESTS AT 925.20 TONNES

OCT 27/WITH GOLD DOWN $3.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 26/WITH GOLD UP $11.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 25/WITH GOLD UP $3.85: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 928.39 TONNES

OCT 24/WITH GOLD DOWN $1.80 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES FROM THE GLD////INVENTORY RESTS AT 928.10 TONNES

OCT 21/WITH GOLD UP $19.10: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 930.99 TONNES

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

GLD INVENTORY: 915.07 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

NOV 3.WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 566,000 OZ FROM THE SLV////INVENTORY RESTS AT 482.650 MILLION OZ//

NOV 2/WITH SILVER DOWN 9 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 92,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.216 MILLION OZ//

NOV 1/WITH SILVER UP 53 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 415,000 OZ FORM THE SLV////INVENTORY RESTS AT 483.308 MILLION OZ

OCT 31: WITH SILVER FLAT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .644 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 483.723 MILLION OZ//

OCT 28/WITH SILVER DOWN 35 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.367 MILLION OZ//

OCT 27/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE S: A WITHDRAWAL OF 2.579 MILLION OZ FROMTHE SLV/////INVENTORY RESTS AT 484.091 MILLION OZ//

OCT 26/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.013 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 486.670 MILLION OZ./.

OCT 25/WITH SILVER UP 17 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.083 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.683 MILLION OZ/

OCT 24/WITH SILVER UP 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .553 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.610 MILLION OZ//

OCT 21/WITH SILVER UP 43 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .46 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 486.163MILLION OZ//

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

CLOSING INVENTORY 482.650 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Economically Ignorant Americans Want More Stimmy Checks To Fight Inflation

Proving that most people have no idea what causes inflation, the majority of Americans in a recent poll said they want the federal government to hand out stimulus checks to combat inflation.

In the poll commissioned by Newsweek, 63% of the respondents said they agreed that the feds should issue new stimulus checks to tackle inflation. Forty-two percent said they “strongly agree” while only 18% disagreed. Fifteen percent said they neither agreed nor disagreed.

The results of this poll reveal the effects of redefining “inflation.”

Properly defined, inflation is an increase in the money supply. Rising consumer prices are one symptom of inflation. But the government has effectively redefined inflation as “rising prices.” In effect, most people think a symptom of inflation is inflation. As a result, most people have no clue where inflation comes from.

This was on purpose.

Of course, when you accurately define inflation, it becomes crystal clear who is to blame — the Federal Reserve and the US government.

Economist Ludwig von Mises explained exactly why this redefinition of inflation is so pernicious.

People today use the term `inflation’ to refer to the phenomenon that is an inevitable consequence of inflation, that is the tendency of all prices and wage rates to rise. The result of this deplorable confusion is that there is no term left to signify the cause of this rise in prices and wages. There is no longer any word available to signify the phenomenon that has been, up to now, called inflation. . . . As you cannot talk about something that has no name, you cannot fight it. Those who pretend to fight inflation are in fact only fighting what is the inevitable consequence of inflation, rising prices. Their ventures are doomed to failure because they do not attack the root of the evil. They try to keep prices low while firmly committed to a policy of increasing the quantity of money that must necessarily make them soar. As long as this terminological confusion is not entirely wiped out, there cannot be any question of stopping inflation.”

Today, people aren’t even asking the government to fight inflation. They just want Uncle Sam to hand them money in order to mitigate the pain of rising prices.

Ironically, stimulus during the pandemic is one of the factors causing the high prices today.

The Federal Reserve pumped over $3 trillion into the economy after the 2008 financial crisis through quantitative easing.

It also stimulated credit creation with 0% interest rates that lasted more than a decade. During the pandemic, the Fed doubled down, pumping nearly $5 trillion more into the economy and dropping rates to zero again.

The federal government exacerbated the situation during the pandemic by handing out three rounds of stimulus money, along with trillions in other aid.

This enabled consumers to keep spending even though they were sitting at home playing Xbox and not producing anything. With more dollars chasing fewer goods and services, a massive spike in consumer prices was entirely predictable.

It’s no wonder people are clamoring for more stimulus. But it will only make the situation worse. In the first place, it will put more dollars in consumers’ hands without any corresponding increase in the supply of goods and services. That’s a recipe for even more price increases.

Furthermore, the US government doesn’t have any money to hand out. It just ran a $1.3 trillion budget deficit. In order to give everybody stimmy checks, the government would have to borrow more money. The Treasury market is already reeling due to rising interest rates. Ultimately, the Federal Reserve would almost certainly have to monetize that new debt with more quantitative easing. The only other alternative would be to let interest rates soar, making the interest payment on the debt even higher.

Stimulus checks might provide a little temporary relief, but they would ultimately make inflation worse and prices would rise even higher in the future. But most Americans don’t understand that. They don’t understand inflation. They just know they’re struggling and they want government to “make it better.”

The problem is the government never makes it better. It always makes things worse. And it’s important to remember you never get more government for free. You always pay.

You’re paying for your COVID stimmy checks today through the inflation tax. If you get another stimmy check tomorrow, that will mean an even bigger inflation tax increase down the road.

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

-END-

3.Chris Powell of GATA provides to us very important physical commentaries

They could easily solve central bank and government solvency by revaluing gold. The uSA will not engage in this due to the fact that they probably

lost of their gold

(Jan. Nieuwenjuijs/GATA)

Dutch central bank governor admits gold revaluation can restore bank’s solvency

Submitted by admin on Wed, 2022-11-02 12:01Section: Daily Dispatches

12:11p ET Wednesday, November 2, 2022

Dear Friend of GATA and Gold:

Gold researcher Jan Nieuwenhuijs reports today that the governor of the Netherlands central bank, Klaas Knot, is talking publicly about an upward revaluation of gold to restore the bank’s solvency.

The central banker’s comments might remind you of the gold revaluation speculations of the U.S. economists Paul Brodsky and Lee Quaintance and the Scottish economist Peter Millar, speculations GATA often has called to your attention:

Nieuwenhuijs’ report is headlined “Governor of Dutch Central Bank States Gold Revaluation Account Is Solvency Backstop” and it’s posted at the Gainesville Coins internet site here:

Submitted by admin on Wed, 2022-11-02 12:23 Section: Daily Dispatches

By Ambrose Evans-Pritchard The Telegraph, London Wednesday, November 2, 2022

The eurozone credit crunch has begun in earnest. Lending conditions across the currency bloc are the tightest since late 2012, when the region was still crippled by the sovereign debt crisis.

The European Central Bank’s lending survey is a leading indicator of what is to come. Both the supply and demand for credit definitively buckled in the third quarter, even if the eurozone economy eked out a last gasp of legacy growth. Lending is deteriorating most rapidly in Italy and Spain.

“The tightening in financing conditions corroborates our view that the euro area is headed towards a sharp recession,” said Ludovio Sapio from Barclays. Trouble is baked into the pie already, whatever happens to Vladimir Putin’s war and global gas prices.

Banks are doing what they always do at the rumble of thunder: they are imposing tougher terms on households and small firms; they are rejecting loan applications. This is a self-fulfilling process that can spin out of control at turning points in the business cycle. …

This past week has been monumental week in the history of Australia.

Last week, against all odds, the Parliament of Australia established not one, but TWO parliamentary inquiries into the Australian Securities and Investments Commission (ASIC) and their handling of reports of alleged misconduct.

For those who may be slight confused with the events of the past week:

· one inquiry will be held by the Senate Economics References Committee – this inquiry was established by a 43-20 vote of the Australian Senate.

These two inquiries come on the heels of my two independent reports into ASIC’s handling of reports of alleged misconduct which I published and submitted to Federal Parliament on 6 and 24 October 2022.

Even though ASIC’s senior executive leadership called my analysis ‘simplistic’, both the Sydney Morning Herald and News.com.au have both credited me in the past week as being the catalyst for the dramatic actions of the Australian Senate. See the following links:

In the past week, a lot of people have congratulated me on achieving this amazing outcome.

It is not every day that a private citizen can write their own report about a government agency, call on the Federal Parliament to hold an extensive inquiry and then pull it off through a dramatic majority vote in the Australian senate.

However, the real battle will be in the coming 3 months.

The bureaucratic cockroaches (especially their executive leadership) at ASIC have largely survived the past 11 years despite multiple reviews, inquiries and the 2018-19 Banking Royal Commission.

According to their own numbers, they have witnessed a material decline in their own enforcement performance despite having more staff and financial resources.

Thus, we cannot go through the current inquiry and just expect things will change. Rather, we have to make things change.

We need to ensure that as many people in Australia know about the current inquiries and that they are encouraged to make a submission so that the Federal Parliament can have all the evidence it requires to hold ASIC finally to account.

This time around heads must roll.

In the coming months, I will be working with multiple stakeholders from across Australia who have explosive case studies about either ASIC’s failure to act or ASIC acting both inappropriately and disproportionately.

Ensuring that these case studies are submitted and that key witnesses testify to the committee is very important.

Thus, the next 3 months is when the REAL BATTLE will be fought.

HOW TO MAKE A SUBMISSION?

Today, Martin North and I posted our latest “In the Interests of the People” video titled: “Rest In Peace ASIC – 3 February 2022”.

In this episode, we explain how to prepare high quality submissions for the Senate Economics References Committee inquiry which has set the deadline for submissions to be 3 February 2022.

I highly recommend that you watch this episode and spread it to your network.

There may be people who may be wondering what happened to the “PACKAGE” which I spoke about with Martin North on In the Interests of the People back on 21 September 2022. See the following link: (29052) The Package That Will Shock Australia – YouTube

The ASIC official investigation into the allegations that I submitted back in April 2022 remain ongoing.

In the past week, new devastating evidence has come to hand which my legal and accounting team has reviewed with me. I was able to spend time with ASIC investigators this past Tuesday sharing our latest evidence and explaining its significance.

The more real and tangible evidence that my team and I provide ASIC investigators, the more ammunition law enforcement has to expose the grand crime which I spent 9 months and $50,000 covertly investigating.

However, I am one of the lucky ones.

While ASIC is investigating my report of alleged misconduct, however there are hundreds of legitimate cases which ASIC has failed to act on – thus, the need for the parliamentary inquiry into ASIC’s performance.

IN SERVICE OF THE AUSTRALIAN PEOPLE

My campaign against tackling financial crime and Australia’s ineffective financial police force (ASIC) has been an intense operation over the past 4 months.

It has taken me countless hours, late nights and around the clock intense focus (including working on weekends) to engineer this outcome.

This campaign has been unpaid and high risk given that the degree of difficulty to engineer two parliamentary inquiries has been especially high.

Nevertheless, in my customary style, I rolled up my sleeves, did the work, took on the financial burden and pushed the envelope. I am grateful that my campaign on this occasion was successful.

For those who wish to contribute to my important public initiatives that allows me to deliver these amazing outcomes for the Australian public, you can make a financial contribution either via:

– my Public Crusader Fund Go Fund Me account – see the following link:

Last year, Nigeria launched its much-ballyhooed eNaira, Africa’s first central bank digital currency (CBDC).

Central bankers, academics, politicians, and an assortment of elites from over 100 countries hoping to launch their own CBDCs have closely followed the eNaira.

They used Nigeria—Africa’s largest country by population and size of its economy—as a Petri dish to test their nefarious plans to use CBDCs to enslave the people of North America, Europe, and beyond.

The jury is now in.

The eNaira has been a massive failure.

According to Bloomberg, only 1 in 200 Nigerians use the eNaira. That’s even after the government implemented discounts and other incentives as desperate measures to increase adoption.

This came as a surprise to the elites.

Nigeria has one of the highest Bitcoin adoption rates in the world—ranking #11 among all countries.

Bitcoin’s ability to bypass the government’s capital controls—which restrict the use of foreign currencies and sending and receiving money from abroad—was a big draw for Nigerians, as it is in other countries with these repressive policies.

A long history of rampant currency debasement in Nigeria—including six devaluations in recent years—also helped spur the adoption of Bitcoin, which is totally resistant to inflation.

In short, the elites have miscalculated. They figured Nigerians wouldn’t be able to differentiate between Bitcoin and the eNaira—they are both digital currencies, after all.

The Bloomberg article admitted, “Nigerians’ passion for cryptocurrencies doesn’t extend to the central bank offering.”

It also said Nigerians view the eNaira as “a symbol of distrust in the ruling elite” and that the people view the government as “hostile to them and therefore have no interest in anything it introduces.”

To all the Nigerians rejecting the eNaira, I say bravo!

The failure of CBDCs in Nigeria could throw sand in the gears of the elites’ plan to implement them worldwide. That would be a big positive for human freedom.

The flop of CBDCs in Nigeria is an encouraging development.

It also reveals an outcome that was probably the opposite of what the elites desired—increased Bitcoin adoption.

CBDCs and Bitcoin

Despite all the hype, CBDCs are nothing but the same fiat currency scam on steroids.

It’s doubtful CBDCs can save otherwise fundamentally unsound currencies—as I believe all fiat currencies are.

If the current fiat system is not viable, then CBDCs are even less viable as they enable the government to engage in even more currency debasement.

Would a CBDC have saved the Zimbabwe dollar, the Venezuelan bolivar, the Argentine peso, or the Lebanese lira?

I don’t think so.

The eNaira did not save the Nigerian fiat currency. And a CBDC won’t save the US dollar or the euro from their fates either.

There are a lot of bad things that come with CBDCs.

But there’s a silver lining…

CBDCs are going to introduce and familiarize people with using digital currencies. It’s then only then a matter of time before they discover Bitcoin.

CBDCs and Bitcoin share some characteristics. For example, they are both digital and facilitate fast payments from a mobile phone. But that is where the similarities end.

The reality is that CBDCs and Bitcoin are entirely different in the most fundamental ways.

You need the government’s permission and blessing to use a CBDC, whereas Bitcoin is permissionless.

Governments can (and will) create as many CBDC currency units as they want. With Bitcoin, there can never be more than 21 million, and there is nothing anyone can do to inflate the supply more than the predetermined amount in the protocol.

CBDCs are centralized. Bitcoin is decentralized.

Governments can censor transactions and freeze, sanction, and confiscate CBDC units whenever they want. Bitcoin is censorship-resistant. No country’s sanctions or laws can affect the protocol.

There is no privacy with CBDCs. However, with Bitcoin, if you take specific steps, it is possible to maintain reasonable privacy.

CBDCs are government money that are easy to produce and give politicians a terrifying amount of control over people’s lives. On the other hand, Bitcoin is non-state hard money that helps liberate individuals from government control.

In short, CBDCs are a pathetic attempt to compete with Bitcoin.

CBDCs make an inferior form of money even worse, but at the same time, it’s an excellent Trojan Horse for Bitcoin.

It doesn’t take much imagination to see that once governments inevitably inflate their CBDC units, censor transactions, freeze people’s accounts, and confiscates funds, it will push people to look for better digital alternatives, first and foremost Bitcoin.

That’s how, contrary to conventional wisdom, CBDCs could be an enormous catalyst for Bitcoin adoption. The failure of the eNaira in Nigeria is proof of this dynamic.

END

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.3166

OFFSHORE YUAN: 7.3484

SHANGHAI CLOSED DOWN 5.56 PTS OR 0.17%

HANG SENG CLOSED DOWN 487.08 OR 3.08%

2. Nikkei closed

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 112.89/Euro FALLS TO 0.9737

3b Japan 10 YR bond yield: RISES TO. +.246!!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 148.28/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.244%***/Italian 10 Yr bond yield RISES to 4.415%*** /SPAIN 10 YR BOND YIELD RISES TO 3.318%…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.657//

3j Gold at $1617.45//silver at: 18.88 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 22/100 roubles/dollar; ROUBLE AT 62.02//

3m oil into the 88 dollar handle for WTI and 95 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 148,28DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 1.0139–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9873well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.191% UP 13 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 4.215% UP 9 BASIS PTS//

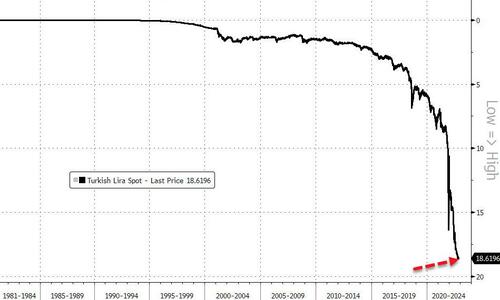

USA DOLLAR VS TURKISH LIRA: 18,62…GETTTING DANGEROUS

GREAT BRITAIN/10 YEAR YIELD: 3.5105%

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

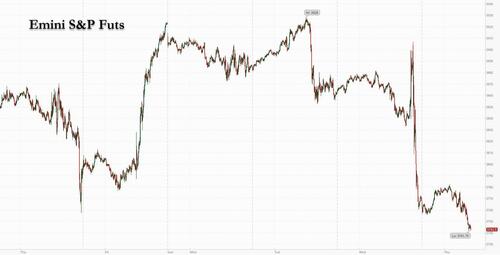

Futures Tumble After Powell Rugpull, BOE Hike On Deck

THURSDAY, NOV 03, 2022 – 07:55 AM

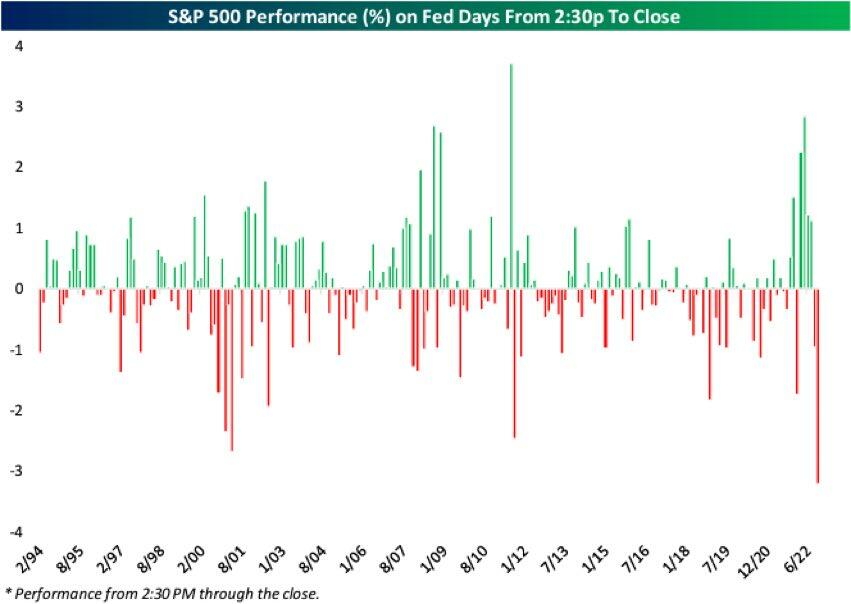

After Powell’s exquisite rugpull, where the most dovish Fed statement in almost one year was followed by the most brutally hawkish press conference where the Fed chair basically told markets to eat shit and die when he said that interest rates could go higher than previously projected, leading to the worst final 90 minutes of trading on a Fed day in history…

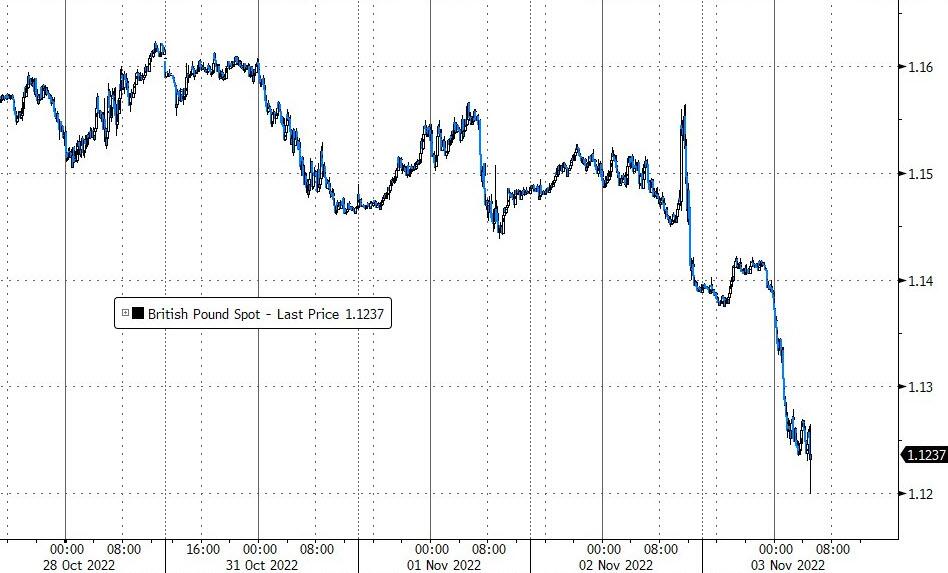

… US index futures extended their plunge on Thursday, signaling more losses for equities ahead of another 75bps rate hike (give or take) by the Bank of England. As of 730 a.m. ET, contracts on the S&P 500 dropped 0.7%, while Nasdaq 100 futures were down 0.9%, extending earlier losses.

Both underlying equity indexes have fallen for three straight days, with the S&P 500 losing 2.5% on Wednesday. The dollar gained as investors looked toward US jobs data, which may help to determine the pace of upcoming rate hikes. The pound fell more than 1% as concern mounted that a smaller-than-expected BOE hike could compound sterling’s drop, while Norway’s krone fell after its central bank delivered the smallest increase in its benchmark rate since June. 10Y Treasury yields soared to 4.20% while the 2s10s curve inverted the most in 2022, tumbling to -0.53%.

“Every time the market gets a little bit of dovish hope, it gets smacked on the nose with a rolled up newspaper,” said Scott Rundell, chief investment officer at Mutual Ltd. “There’s a lot of volatility still ahead.”

“There was perhaps a hint that the ‘jumbo’ rates increases are coming to an end, and this was sufficient for bond, credit and equity markets to initially at least perform well. The reality that the hiking cycle isn’t over yet is likely to limit the upside,” said Sandra Holdsworth, head of rates UK at Aegon Asset Management.

The Fed’s 75 basis-point increase is likely to be followed by a similar-sized hike from the Bank of England later on Thursday, though rates there are potentially limited by the risk of a severe recession. Powell disappointed traders betting on a pivot as the US economy remains resilient to stubbornly high inflation.

While Powell did his best to guide to lower future rate hikes while tightening financial conditions, investors haven’t found much respite in earnings either, with the season so far proving a mixed bag: both Moderna and Peloton imploded in premarket trading on poor earnings and a catastrophic outlook: Moderna plunged as much as 16% in premarket trading after cutting its vaccines purchase agreements guidance for 2022, while Peloton cratered 21% on a revenue miss and slashing Q2 revenue guidance. In other premarket moves, Qualcomm fell after maker of smartphone processors issued a weaker-than-expected forecast, citing the slowdown in phone markets. Rok also sank after offering cautious commentary about the advertising market. Etsy, EBay and Booking Holdings rallied after robust results. Here are some other premarket movers:

Cognizant shares fell around 10% in premarket trading following its third-quarter report as analysts say that the results and guidance reflect ongoing challenges the consultancy and outsourcing firm faces, which are now being complemented by a weakening macro picture.

Robinhood shares climbed as much as 4.8% in premarket trading. The online brokerage reached profitability earlier than expected, which analysts said was a positive sign that should increase investor confidence in the company’s strategy.

Lumen Technologies shares plunged as much as 16% in premarket trading, after the phone company reported earnings that fell short of expectations and eliminated its dividend, a move that which Wells Fargo analysts said was a “difficult” though a correct decision, that would allow the company to invest for growth.

Altice slumps 23% in premarket trading after the cable television provider reported worse-than-expected earnings per share in the third quarter and analysts drew attention to the company’s high levels of leverage and continued subscriber losses.

CF Industries earnings missed expectations on lower ammonia pricing, though analysts say the outlook for the fertilizer firm remains solid and a new share buyback is likely to be welcomed. CF shares fell 5.1% in premarket trading on thin volumes.

Fortinet shares fell about 13% in premarket trading as softer billings growth guidance and the cybersecurity firm’s decision to stop providing its closely-watched backlog number are both likely to be taken negatively, analysts say.

Booking (BKNG US) reported third-quarter revenue that beat the average analyst estimate, as the online travel agency continues to see resiliency in demand despite macro headwinds. Shares were up 5.1% in US postmarket trading.

“Prospects for riskier asset classes look weaker as interest rate hikes continue to curtail economic growth worldwide,” Pictet chief strategist Luca Paolini said. “We therefore remain underweight on equities, whose valuations are even more difficult to justify after the recent market rally.”

European stocks fell as Fed Chair Powell’s warning of a higher peak rate continues to roil assets. Euro Stoxx 600 down 1.1%. FTSE 100 outperforms peers, while IBEX lags, dropping 1.4%. All major sectors were in the red, with real estate, travel, technology, construction and autos the main underperformers.

Earlier in the session, Asian stocks snapped a three-day advance, with Hong Kong and mainland China shares losing ground after the government affirmed its Covid-Zero stance. China’s Caixin services PMI contracted more than expected. The MSCI Asia Pacific ex-Japan Index fell as much as 2.1%, led by consumer discretionary and tech shares. Nearly all markets in the region were down, with Australia slumping almost 2% and tech-heavy market Taiwan dropping nearly 1%. Japan was closed for a holiday. Fed Chair Jerome Powell’s comments that tightening still has “some ways to go” were perceived to be more aggressive and hawkish than before, triggering a reversal in US shares that spilled over into Asia. The Fed raised interest rates by 75 basis points for the fourth time in a row.

“Investors may be disappointed that they did not get the pivot from the FOMC that they are wishing for, given the hawkish tone overnight,” Tai Hui, chief market strategist for APAC at JPMorgan Asset Management, wrote in a note. “This could keep some pressure on risk appetite in the coming weeks.” Declines in Chinese and Hong Kong stocks dragged the region lower after the nation’s top health body said the zero-tolerance approach remains the overall strategy to fight Covid-19. Shares in the market rallied earlier in the week as speculation grew over the nation’s reopening. “We expect the dynamic Zero-Covid strategy will stay, but there will be increasing flexibility of its implementation as authorities have now got more experience and confidence in quickly deploying control measures,” said Redmond Wong, a market strategist at Saxo Capital Markets

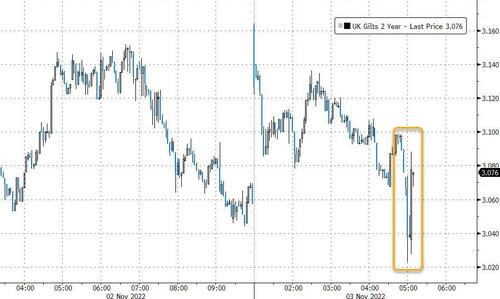

In fixed income, yields are higher across the board, led by Europe. US Treasuries hold losses as US trading day begins, extending the bear-flattening move unleashed by Wednesday’s Fed communications with Treasury yields adding 7bps to 11bps with the largest uptick seen in the short end of the curve. 2-year yield reached a new multiyear high, pushing 2s10s curve toward its YTD low. Yields across the curve higher by 7bp-10bp, 10-year around 4.18%; 2s10s little changed at -53bp after approaching -55bp, lowest since Oct. 14. US 2-year topped near 4.735%, fresh post-2007 high, 5-year at 4.423%, highest since Oct. 21, when YTD high 4.504% was reached. Dollar issuance slate empty so far after a quiet Wednesday; six issuers have sold $8 billion so far this week. Bunds and gilts trade broadly in line with Treasuries across the 10-year sector; money markets are pricing in around 72bp of rate hikes for the Bank of England meeting.

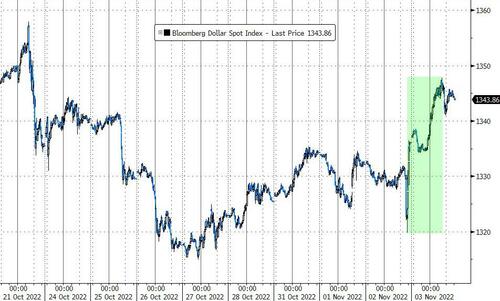

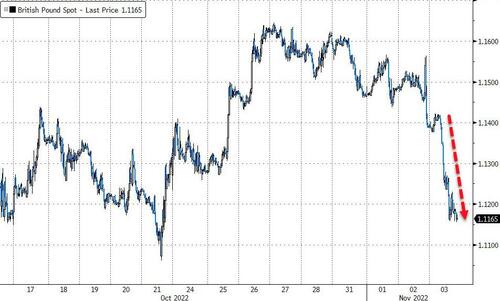

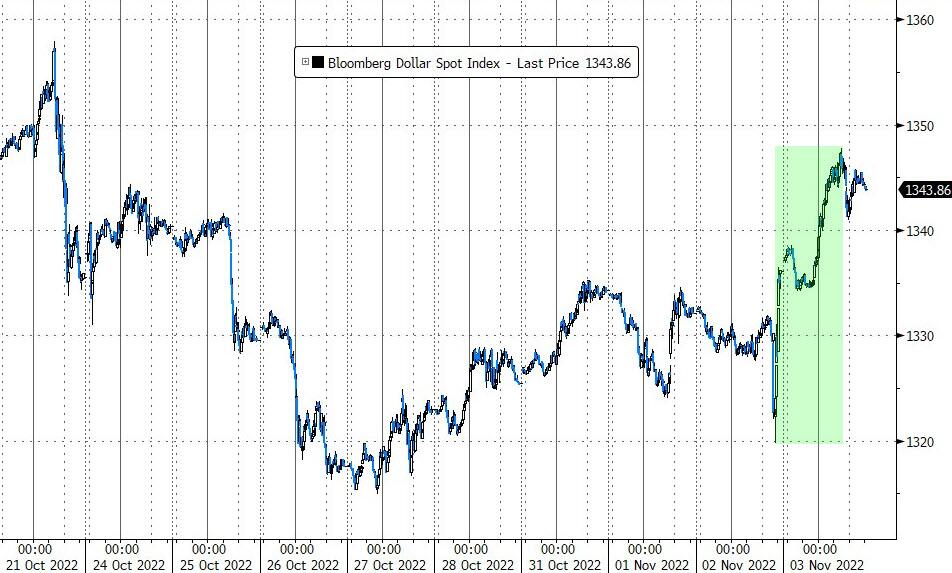

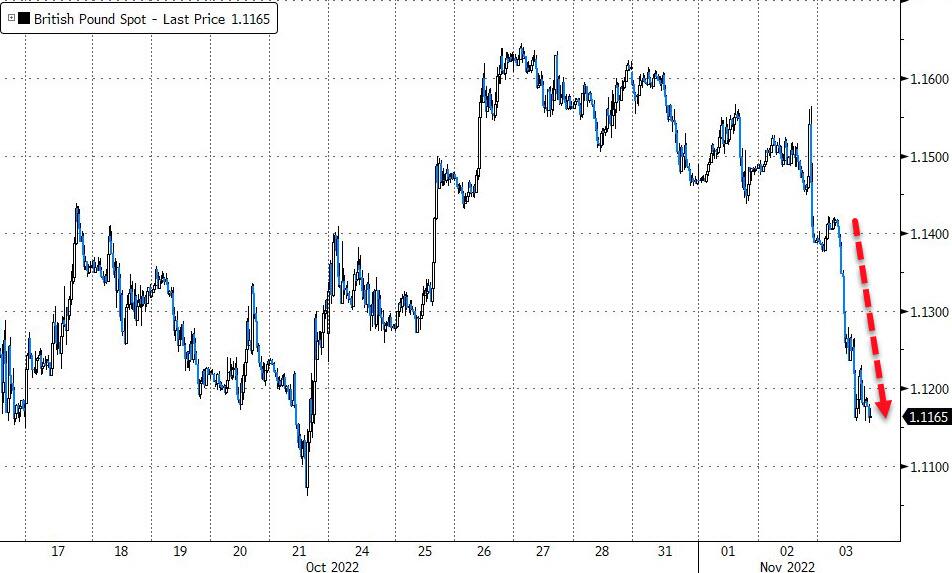

In FX, the Bloomberg Dollar Spot Index rose as much as 0.2% as the greenback advanced versus all of its Group-of-10 peers. JPY and CAD are the strongest performers in G-10 FX, while GBP tumbles ahead of the BOE. Crude futures decline.

The euro extended a decline to trade at an almost two-week low versus the greenback. Italian bonds lead euro-area peers lower as money markets raised ECB rate-hike bets in response to Wednesday’s hawkish Fed outcome.

The pound tumbled as much as 1.4% to 1.2337 per dollar before the Bank of England’s interest-rate meeting, as concern mounted that a smaller-than-expected hike could compound sterling’s drop. Gilt yields rose by around 8-10bps. The BOE is expected to raise interest rates 75bps to 3%. Options show that price action following the Bank of England decision has the potential to signal the pound’s direction into year-end

Norway’s krone pared losses after falling to a one-week low of 10.3710 per euro after Norges Bank raised its policy rate by 25bps to 2.50%, with estimates almost evenly distributed between a 25bps and a 50bps hike

Aussie yields climbed ~10bps across the curve. The Aussie fell more than 1% in European trading after earlier reversing an intraday loss as Australia’s trade surplus surged to A$12.4b in September from A$8.3b in August, exceeding economists’ forecast of A$8.8b

The yen held up best against the dollar among G-10 peers, with Japan on holiday

Commodities are under broad pressure given the continued post-FOMC advances in the USD, crude benchmarks lower by over USD 1.00/bbl. Metals are similar under USD-induced pressure, spot gold dropping further from the USD 1650/oz mark with LME copper below USD 7.5k/T once again. Spot gold falls roughly $14 to trade near $1,622/oz.

Bitcoin is modestly firmer on the session but continues to trade within fairly narrow parameters above the USD 20k mark post-FOMC as participants look to upcoming risk events.

Looking the day ahead now, and the main highlight will be the BoE’s policy decision and Governor Bailey’s press conference. We’ll also separately hear from the BoE’s Mann and a range of ECB speakers including President Lagarde, and the ECB’s Kazaks, Panetta, Nagel, De Cos, Elderson, Villeroy, Visco, Makhlouf and Centeno. Data releases include the ISM services index from the US, the weekly initial jobless claims, and September data on the trade balance. Lastly, earnings releases include Starbucks, PayPal and Moderna.

Market Snapshot

S&P 500 futures down 0.2% to 3,761.00

STOXX Europe 600 down 1.1% to 408.90

MXAP down 1.6% to 137.74

MXAPJ down 2.1% to 438.83

Nikkei little changed at 27,663.39

Topix up 0.1% to 1,940.46

Hang Seng Index down 3.1% to 15,339.49

Shanghai Composite down 0.2% to 2,997.81

Sensex down 0.3% to 60,705.30

Australia S&P/ASX 200 down 1.8% to 6,857.88

Kospi down 0.3% to 2,329.17

German 10Y yield up 4.5% to 2.24%

Euro down 0.5% to $0.9767

Brent Futures down 1.3% to $94.92/bbl

Gold spot down 0.5% to $1,627.50

U.S. Dollar Index up 1.17% to 112.65

Top Overnight News from Bloomberg

ECB President Christine Lagarde warned that a “mild recession” is possible but that it wouldn’t be sufficient in itself to stem soaring prices

Wall Street money managers looking to pile back into Treasuries after months of losses will have to contend with a Federal Reserve that stands ready to raise the stakes every step of the way

Central banks bought 399 tons of bullion in the third quarter, almost double the previous record, according to the World Gold Council. Just under a quarter went to publicly identified institutions, stoking speculation about mystery buyers

Turkish annual inflation accelerated for the 17th month in a row in October to 85.5% y/y, driven by a surge in food prices and energy costs, to its likely peak during President Recep Tayyip Erdogan’s two decades in power

A more detailed look at global market courtesy of Newsquawk

APAC stocks were mostly lower with the global risk appetite subdued in the aftermath of the FOMC, while the risk tone was also not helped by a deterioration in Chinese Caixin PMI data and the absence of Japanese participants for Culture Day holiday. ASX 200 was pressured as underperformance in the mining-related sectors led the broad declines in the index and after the New South Wales Chief Health Officer warned of a looming wave of COVID infections. KOSPI was contained amid geopolitical concerns after North Korea’s recent record number of missile launches, while it continued firing missiles again today. Hang Seng and Shanghai Comp were negative after Chinese Caixin Services and Composite PMI data worsened and with China’s National Health Commission reiterating adherence to zero-COVID policy, while the HKMA also raised rates by 75bps in lockstep with the Fed.

Top Asian News

Hong Kong Monetary Authority raised the base rate by 75bps to 4.25%, as expected, while the Macau Monetary Authority also raised its base rate for the discount window by 75bps to 4.25%.

RBNZ said there is high confidence that they can get inflation under control and that the labour shortage is the single most constraining factor for businesses in New Zealand, while Governor Orr also noted a laser-like focus on returning inflation to the 1%-3% target.

Earthquake shakes buildings within Tokyo, Japan, via Reuters citing witnesses; reports indicate an intensity of 4 and a magnitude of 5.2, epicentre in Chiba.

Malaysia Raises Key Rate by a Quarter Point Ahead of Vote

Kahoot Drops 17% After 3Q Revenue Misses Estimates

China’s Top PC Maker Boosts Profit After Lowering Costs

Latest Fed Hike Reverberates Through Asia as Policy Makers React

Sharp Yen Swing Has Traders on Watch for Post-Fed Japan Reaction

European bourses are subdued across the board, Euro Stoxx 50 -0.8%, as the post-Powell pressure reverberates across from APAC trade. Sectors are all in the red with the exception of banking names that are deriving some benefit from yields and conscious of numerous European earnings within the sector, including BNP and ING. Stateside, futures are lower across the board though only marginally so with a busy session ahead incl. BoE and ISM Services PMI; ES -0.3%, NQ -0.3%. Morgan Stanley (MS) reportedly plans to begin layoffs in the coming weeks as deal making slows, according to Reuters citing sources. Cigna Corp (CI) Q3 2022 (USD): EPS 6.04 (exp. 5.71), Revenue 45.3bln (exp. 44.76bln); raises FY22 outlook.

Top European News

Coal Gives Profit Boost to Offshore Wind Developer Orsted

BMW, Stellantis See Europe Demand Slowing as Inflation Bites

Rolls- Royce Falls as Engine Deliveries Hit Low End of Forecasts

Uniper Posts €40 Billion Loss as Russia Throttles Gas Supply

BNP Rides Rising Rates as Debt Trading Fuels Profit Beat

ING Plans €1.5 Billion Buyback as One-Off Charges Hit Profit

FX

USD continues to rise to the detriment of peers across the board following the FOMC/Powell-presser; DXY to a 112.91 peak from a 111.81 base.

JPY is the relative outperformer amid holiday outages for the region, the ever present possibility of intervention and perhaps some haven allure given broader risk aversion; though, USD/JPY is back above 148.00.

GBP is the standout underperformer given the USD action but also vs EUR, with EUR/GBP lifting past 0.8650 pre-BoE with the Pound unable to derive any real respite from upward PMI revisions.

NOK has been impaired by an as-guided but sub-market pricing 25bp hike from the Norges Bank; interestingly, Governor Bache hasn’t given much away on the likely December magnitude thus far.

Fixed Income

Core benchmarks under pressure across the board as yields continue to extend, particularly at the short-end of the UST curve.

Gilts are the relative outperformers, though still lower by over 50 ticks pre-BoE, as while 75bp is expected a ‘dovish’ surprise/dissent cannot be ruled out entirely.

Bunds are in-fitting with their US peer and significantly lower though they have held onto support at the 137.00 mark; for reference, numerous ECB speakers haven’t had much sway on EGB price action thus far.

Commodities

Commodities are under broad pressure given the continued post-FOMC advances in the USD, crude benchmarks lower by over USD 1.00/bbl.

Though, desks are cognisant of the substantial drawdowns in crude stockpiles this week as a potential cushioning factor.

Metals are similar under USD-induced pressure, spot gold dropping further from the USD 1650/oz mark with LME copper below USD 7.5k/T once again.

Urals and Siberian Light oil loadings from Novorossiisk set at 2.47mln/T for November (2.84mln/T in October), via Reuters citing sources

Central Banks

Norges Bank hikes by 25bps to 2.50% (exp. evenly split between 25bp & 50bp); the policy rate will most likely be raised further in December.. Click here for full details, reaction and newsquawk analysis.

ECB’s Kazaks says a EZ recession is already his baseline, but it should be shallow. Monetary policy must continue to tighten; rates need to go much higher, no need for a pause at turn of the year.

ECB’s Panetta says the medium term inflation outlook presents clear upside risks, further policy adj. is warranted. Need to bring inflation back to target as soon as possible, but not sooner.

ECB’s Lagarde says a recession is not sufficient to tame inflation.

ECB’s Centeno says a good part of rate hikes should already have occurred, EZ inflation should peak this quarter, via Publico.

Geopolitics

Ukrainian President Zelensky said a Russian plane fired cruise missiles on Wednesday which flew across the Black Sea corridor used to export grain, according to Reuters.

Russia’s Kremlin says Russia’s resumption of the grain agreement does not mean that it has been automatically extended and its results must be evaluated before a decision is made, via Al Jazeera.

South Korean military detected that North Korea fired one long-range and two short-range missiles, while it was reported that the North Korean missile went through a stage of separation but may have failed after the second stage separation, according to Yonhap.

US condemned North Korea’s ICBM launch and called on North Korea to refrain from further provocations and engage in sustained and substantive dialogue, according to Reuters.

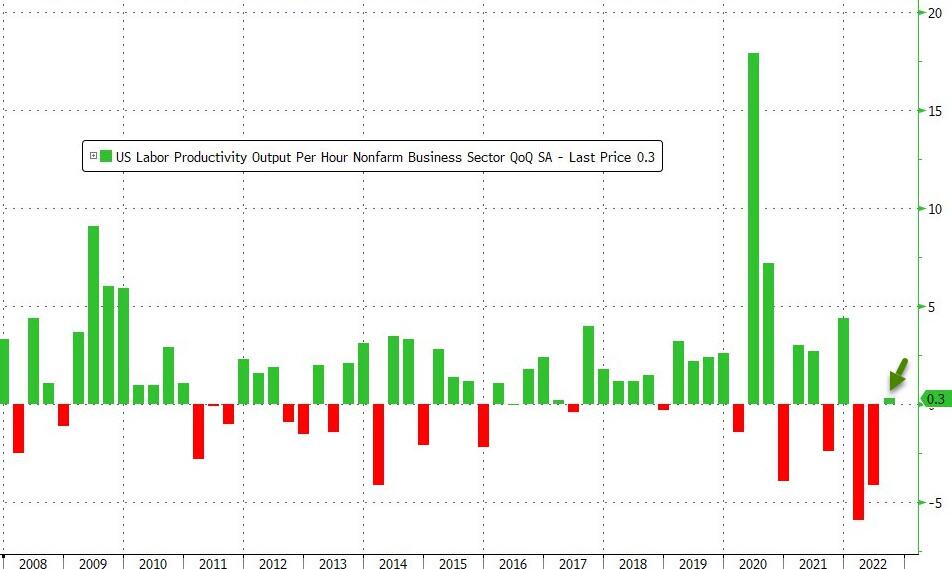

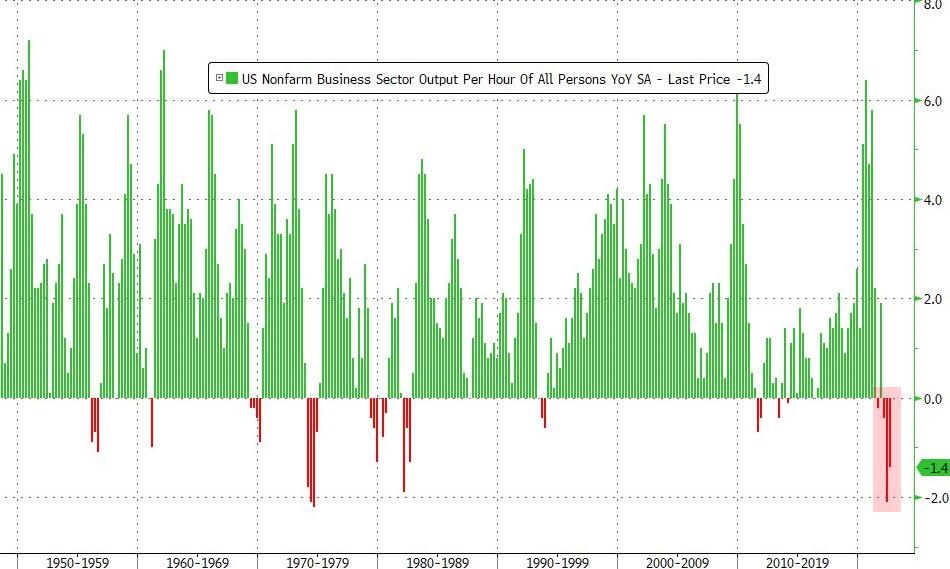

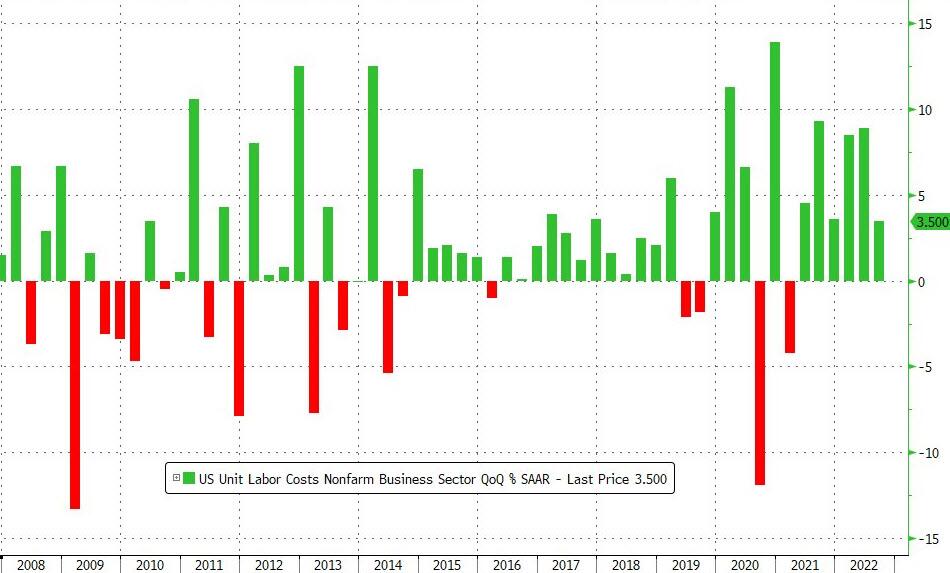

08:30: 3Q Unit Labor Costs, est. 4.0%, prior 10.2%

08:30: 3Q Nonfarm Productivity, est. 0.5%, prior -4.1%

08:30: Initial Jobless Claims, est. 220,000, prior 217,000

08:30: Continuing Claims, est. 1.45m, prior 1.44m

08:30: Sept. Trade Balance, est. -$72.2b, prior -$67.4b

09:45: Oct. S&P Global US Services PMI, est. 46.6, prior 46.6

10:00: Oct. ISM Services Index, est. 55.2, prior 56.7

10:00: Sept. Durable Goods Orders, est. 0.4%, prior 0.4%

10:00: Sept. -Less Transportation, est. -0.5%, prior -0.5%

10:00: Sept. Cap Goods Ship Nondef Ex Air, prior -0.5%

10:00: Sept. Cap Goods Orders Nondef Ex Air, est. -0.6%, prior -0.7%

10:00: Sept. Factory Orders Ex Trans, est. 0%, prior 0.2%

10:00: Sept. Factory Orders, est. 0.3%, prior 0%

DB’s Jim Reid concludes the overnight wrap

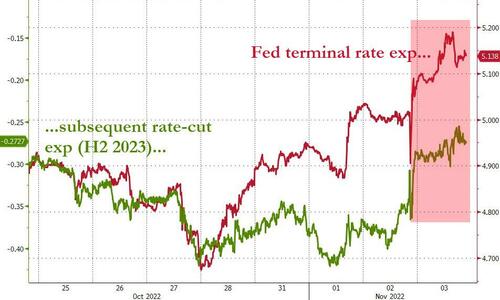

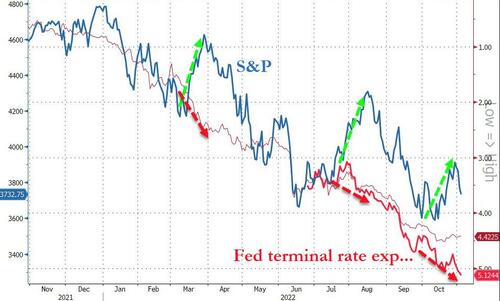

Markets could have saved themselves a lot of heartache and debate over the last 13 days as the WSJ article from Nick Timiraos was ultimately fairly accurate. However, the problem was that the market has been paying more attention the step-down debate Mr Timiraos hinted at rather than the rest of the article saying that the terminal rate may need to go higher. Even after the initial statement last night, the market focused on the former (with good reason). However, by the end of the press conference it was clear that this was a hawkish dovish pivot! If that makes any sense!

Let’s try to make sense of things. Firstly, the Fed of course hiked 75bps as virtually everyone expected. See our full US economics team’s wrap here.

Upon the release of the statement, markets quickly latched on to the inserted phrase that the “Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation” when assessing the path of future tightening. Market pricing assumed that this meant the Fed was teeing up a pivot, leading to a strong rally in yields and risk. The pivot/pause rally was short-lived, however, as Chair Powell stepped up to the mic and quickly disabused any interpretation that suggests a pause was forthcoming. He did so directly, saying that it was very premature to be thinking about a pause, and also by contextualising the new Statement language, highlighting that the hiking cycle had three important components: 1) the pace the Fed gets to terminal, 2) how high terminal needs to get, and 3) how long policy needs to stay restrictive. The new statement language only pertains to ‘1)’, and the Chair emphasized that the pace is not nearly as important anymore given how much tightening the Fed has done to date. Indeed, the Chair sounded more hawkish on the latter two points, noting that the data since September’s dots call for an even higher terminal rate, and that the Fed had a ways to go until achieving an appropriately restrictive stance. The tighter for longer restrictive policy stance also had the Chair bring his economic outlook closer to DB’s, as he downgraded the Fed’s prospects of achieving a soft landing, upgrading the probability he placed on a recession.

Powell was hawkish elsewhere in the presser, noting that it was still riskier to under- rather than over-tighten, given how precariously balanced inflation expectations are as core inflation continues to stay elevated. Over a longer time horizon, Powell noted that the historical record argued against prematurely loosening policy when inflation was this high. While some asked about greenshoots in the battle against inflation, Powell was much more focused on a labour market which remained historically tight and showing no signs of letting up.

The slower pace but higher terminal message (one that was reflected in that aforementioned WSJ article) was eventually well-understood by the market. Pricing for the December FOMC moved down -2.0bps to 56.5bps, while terminal pricing for May moved up +5.0bps to 5.10%, a new cycle high. Meanwhile, the rest of the Treasury yield curve and the S&P 500 fully retraced the post-statement pre-press conference rally, leaving 2yr yields +7.5bps higher and 10yr yields up +5.9bps, having climbed +18.7bps and +13.3bps, respectively, from the post statement lows. There is no cash trading of Treasuries in Asia this morning with Japan on holiday. (Meanwhile, the S&P 500 finished the day -2.50% having been +0.98% after the statement, making it the worst Fed day for the S&P 500 since January 2021. Likewise, the NASDAQ rallied into positive territory after the statement (+0.93%), only to take a sharp turn lower to end the day down -3.36%. In overnight trading, US futures are showing a small rebound with contracts tied to the S&P 500 (+0.25%) and NASDAQ 100 (+0.32%) both trading in positive territory. Qualcomm’s shares fell -7.10% after hours though following earnings where they lowered revenue guidance for the upcoming quarter on the back of slowing phone demand as well as continued Covid lockdowns in China.