GOLD PRICE CLOSE: UP $9.20 to $1646.60

SILVER PRICE CLOSE: UP $0.53 to $19.68

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1647.00

Silver ACCESS CLOSE: 19.62

New: early yesterday morning//

Bitcoin morning price: $20,544 UP 175

Bitcoin: afternoon price: $20,481 UP 112

Platinum price closing UP $17.25 AT $948.25

Palladium price; closing UP $32.35 at $1887.60

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: 2244/72 DOLLARS UP 22/73 CDN DOLLARS PER OZ

BRITISH GOLD: 1434.06 POUNDS PER OZ UP 22.87 POUNDS PER OZ

EURO GOLD: 1667.47 EUROS PER OZ UP 10.34 EUROS PER OZ.

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

EXCHANGE: COMEX//NOVEMBER

EXCHANGE: COMEX

CONTRACT: OCTOBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,648.700000000 USD

INTENT DATE: 10/24/2022 DELIVERY DATE: 10/26/2022

FIRM ORG FIRM NAME IS

EXCHANGE: COMEX

CONTRACT: NOVEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,635.900000000 USD

INTENT DATE: 10/31/2022 DELIVERY DATE: 11/02/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 81

132 C SG AMERICAS 30 14

190 H BMO CAPITAL 43

323 C HSBC 43

435 H SCOTIA CAPITAL 75

624 H BOFA SECURITIES 38

657 C MORGAN STANLEY 2

661 C JP MORGAN 98 169

690 C ABN AMRO 9 6

732 C RBC CAP MARKETS 4

737 C ADVANTAGE 41 11

800 C MAREX SPEC 16 5

880 H CITIGROUP 2

905 C ADM 13

TOTAL: 350 350

MONTH TO DATE: 2,030

JPMORGAN STOPPED 781/1600

GOLD: NUMBER OF NOTICES FILED FOR NOV. CONTRACT: 350 NOTICES FOR 35,000 OZ or 1.0886 TONNES

total notices so far: 2030 contracts for 203,000 oz (6.314 tonnes)

SILVER NOTICES: 73 NOTICE(S) FILED FOR 365000 OZ/

total number of notices filed so far this month 84 : for 420,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $9.20

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////A BIG CHANGE IN GLD INVENTORY: A WITHDRAWAL OF 2.02 TONNES FROM THE GLD// /INVENTORY LOWERS TO 920.57 TONNES

INVENTORY RESTS AT 920.57 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 53 CENTS

AT THE SLV// :/SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF OF .415 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 483.308 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 1030 CONTRACTS TO 139,157 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE STRONG GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR STRONG $0.00 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS/HFT WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.00)., AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC LONGS, AS WE HAD A VERY STRONG GAIN IN OUR TWO EXCHANGE OF 1032 CONTRACTS. HUGE SPECS CONTINUE TO ADD TO THEIR SHORTFALLS FROM WHICH OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. SOME SPEC LONGS COVERED THEIR SHORT POSITIONS /

WE MUST HAVE HAD:

I) SOME SPECULATOR SHORT COVERINGS BUT STRONG SHORT ADDITIONS ////CONTINUED BANKER OI COMEX ADDITIONS /// SOME NEWBIE SPEC LONG ADDITIONS ON THE LOWER PRICE. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.045 MILLION OZ FOLLOWED BY TODAY’S 20,000 QUEUE JUMP//NEW STANDING: / // V) HUGE SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: — 2

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS NOV. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF NOV:

TOTAL CONTRACTS for 1 days, total 0 contracts: 0.000 million oz OR 0.000MILLION OZ PER DAY. (0 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 0 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 0 MILLION

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1030 WITH OUR $0.00 LOSS IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A ZERO SIZED EFP ISSUANCE CONTRACTS: 0 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR NOV. OF 1.345 MILLION OZ FOLLOWED BY TODAY’S 20,000 QUEUE JUMP/ .. WE HAVE A VERY STRONG SIZED GAIN OF 1030 OI CONTRACTS ON THE TWO EXCHANGES FOR 5.15 MILLION OZ..

WE HAD 73 NOTICE(S) FILED TODAY FOR 365,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 3144 CONTRACTS TO 464,629 AND FURTHER FROM TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -8 CONTRACTS.

.

THE FAIR SIZED INCREASE IN COMEX OI CAME DESPITE OUR FALL IN PRICE OF $4.00//COMEX GOLD TRADING/MONDAY // ZERO SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION AND CONSIDERABLE SPEC SHORT ADDITIONS BUT MINOR SPEC SHORT COVERINGS. // CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR NOV. AT 12.386 TONNES ON FIRST DAY NOTICE //EXPECT HUGE QUEUE JUMPING BEGINNING ON 2ND DAY NOTICE: (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR FALL IN PRICE OF $4.00 WITH RESPECT TO MONDAY’S TRADING

WE HAD A VERY SMALL SIZED LOSS OF 459 OI CONTRACTS 1.427 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2705 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 464,633

IN ESSENCE WE HAVE A VERY SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 459 CONTRACTS WITH 3144 CONTRACTS DECREASED AT THE COMEX AND 2705 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 431 CONTRACTS OR 1.2305 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2705) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (3144): TOTAL LOSS IN THE TWO EXCHANGES 459 CONTRACTS. WE NO DOUBT HAD 1) STRONG SPECULATOR SHORT ADDITIONS// CONTINUED GOOD BANKER ADDITIONS/// ZERO SPEC SHORT COVERINGS// CONSIDERABLE NEWBIE SPEC ADDITIONS WITH THE LOWER PRICE ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR NOV. AT 12.386 TONNES ///NEW STANDING FOR NOV 12.386 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 33,400 OZ//NEW STANDING 13.673 TONNES//. 3) ZERO LONG LIQUIDATION //// //.,4) STRONG SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

NOV

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV. :

2705 CONTRACTS OR 270,500 OZ OR 8.413 TONNES 1 TRADING DAY(S) AND THUS AVERAGING: 2705 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAY(S) IN TONNES: 8.413 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 8.413/3550 x 100% TONNES 5.01% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 8.413 TONNES//INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A HUGE SIZED 1030 CONTRACT OI TO 139,159 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 0 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1030 CONTRACTS AND ADD TO THE 0 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A VERY STRONG SIZED GAIN OF 1030 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 5.16MILLION OZ//

OCCURRED DESPITE OUR HUGE LOSS IN PRICE OF $0.00

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

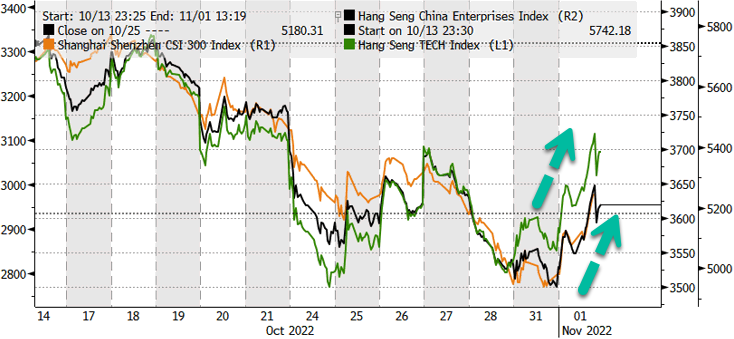

SHANGHAI CLOSED UP 75.72 PTS OR 2.62% //Hang Seng CLOSED UP 768.25OR 5.23% /The Nikkei closed UP 91.46 PTS OR 0.33% //Australia’s all ordinaires CLOSED UP 1.63% /Chinese yuan (ONSHORE) closed UP TO 7.2586 //OFFSHORE CHINESE YUAN UP 7.2627// /Oil UP TO 88.33, dollars per barrel for WTI and BRENT AT 94.69 / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 3144 CONTRACTS TO 464,629 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED DESPITE OUR FALL IN PRICE OF $4.00 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2705 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF NOV.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2705 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC : 2705 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2705 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY SMALL SIZED TOTAL OF 459 CONTRACTS IN THAT 2705 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 3136 CONTRACTS..AND THIS SMALL SIZED LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $4.00//WE HAD CONSIDERABLE SPEC SHORTS ADDITIONS, WITH BANKERS AS BUYERS OF COMEX GOLD CONTRACTS. WE ALSO HAD STRONG ADDITIONAL NEWBIE SPECS GOING LONG WITH THE LOWER PRICE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING NOV (13.673),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 13.673 TONNES/INITIAL

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $4.00) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A TINY LOSS ON OUR TWO EXCHANGES//// SPEC SHORTS ADDED TO THEIR POSITIONS AS WE HAD A VERY SMALL SIZED TOTAL LOSS ON OUR TWO EXCHANGES OF 459 CONTRACTS // WE HAVE REGISTERED A VERY SMALL LOSS OF 1.3406 PAPER TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR NOV. (13.673 TONNES)…THIS WAS ACCOMPLISHED WITH OUR FALL IN PRICE OF $4.00

WE HAD -8 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 459 CONTRACTS OR 45900 OZ OR 1.427 TONNES

Estimated gold volume 199,696// poor//

final gold volumes/yesterday 204,080/ poor

INITIAL STANDINGS FOR NOVEMBER 2022 COMEX GOLD //NOV 1

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 233,455.564oz Brinks Malca JPMorgan includes 372 kilobars and 759 kilobars |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | NIL oz |

| No of oz served (contracts) today | 350 notice(s) 350,000 OZ 6.314 TONNES |

| No of oz to be served (notices) | 2366 contracts 236,600 oz 7.359 TONNES |

| Total monthly oz gold served (contracts) so far this month | 2030 notices 203,000 6.314 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

customer withdrawals:3

i) Out of JPMorgan 197,092.775 oz

ii) Out of Brinks 11,960.180 372 kilobars)

iii) Out of Malca: 24,402.609oz ( 759 kilobars)

total: 233,455.097 oz

total in tonnes: 23.34 tonnes

Adjustments: 0//

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR NOVEMBER.

For the front month of NOV. we have an oi of 2716 contracts having LOST 1266 contracts. We had 1600 notices served upon Monday so we gained a whopping 334

or an additional 33400 will stand in this non active month of November. We will have Nov gold tonnage standing increase daily from this day forth until the end of the month.

This queue jumping originates in London with the exercising of London based EFP’s for comex gold.

December LOST 4403 contracts UP to 358,108.

JANUARY gained 2 contracts to stand at 2.

February gained 1960 contacts up to 71,645.

We had 350 notice(s) filed today for 350,000 oz on the first day notice FOR THE NOV. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 98 notices were issued from their client or customer account. The total of all issuance by all participants equate to 350 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 169 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the NOV. /2022. contract month,

we take the total number of notices filed so far for the month (2030) x 100 oz , to which we add the difference between the open interest for the front month of (NOV 2716 CONTRACTS) minus the number of notices served upon today 350 x 100 oz per contract equals 439,600 OZ OR 13.673 TONNES the number of TONNES standing in this non active month of NOV.

thus the INITIAL standings for gold for the NOV. contract month:

No of notices filed so far (2030) x 100 oz+ (2716) OI for the front month minus the number of notices served upon today (350} x 100 oz} which equals 439,600 oz standing OR 13.673 TONNES in this NON active delivery month of NOV..

TOTAL COMEX GOLD STANDING: 13.673 TONNES (A HUMONGOUS STANDING FOR NOV (GENERALLY THE POOREST DELIVERY MONTHS FOR A NON ACTIVE MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,996,891.215 OZ 62.11 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 24,726,208.097 OZ

TOTAL REGISTERED GOLD: 11,331,325,357 OZ (352.45 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 13,394,882.740 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,334,444 OZ (REG GOLD- PLEDGED GOLD) 290.034 tonnes//rapidly declining

END

SILVER/COMEX

NOV 1//INITIAL NOV. SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2,743,491.260 oz Brinks Loomis CNT Delaware JPMorgan Manfra |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,286,986.070 oz Loomis |

| No of oz served today (contracts) | 73 CONTRACT(S) (365,000 OZ) |

| No of oz to be served (notices) | 189 contracts (945,000 oz) |

| Total monthly oz silver served (contracts) | 84 contracts (420,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 6 withdrawals out of the customer account

i) Out of Brinks 771m048.030 oz

ii) out of Loomis: 80,452.100 oz

iii) Out of CNT: 857,314.520 oz

iv) Out of Delaware 16,667.317 o

v) Out of Manfra 435,439.280 oz

vi_ Out of JPMorgan 580,570.100 oz

Total withdrawals: 2,743,891.262 oz

JPMorgan has a total silver weight: 155.309million oz/299.703 million =51.78% of comex .//dropping fast

Comex deposits: 1

i) Into Loomis: 1,286,986.070 oz

total: 1,286,986.07- oz

adjustments: 3

dealer to customer

i./ JPMorgan 19,259.300oz

ii) Manfra 33,726.294 oz

customer to dealer

Delaware; 23,439.364 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 34.711 MILLION OZ (declining rapidly)

TOTAL REG + ELIG. 299.703 MILLION OZ (also declining)

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF NOV OI: 262 CONTRACTS HAVING LOST 7 CONTRACT(S.)

WE HAD 11 NOTICES FILED ON MONDAY, SO WE GAINED 4 CONTRACTS OR AN ADDITIONAL 20,000 OZ WILL STAND

FOR SILVER IN THIS VERY NON ACTIVE DELIVERY MONTH OF NOVEMBER.

DECEMBER SAW A GAIN OF 503 CONTRACTS DOWN TO 106,248

JANUARY SAW A GAIN OF 16 CONTRACTS UP TO 1144 CONTACTS.

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY:73 for 365,000 oz

Comex volumes:53,927// est. volume today// fair

Comex volume: confirmed yesterday: 59,548 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in NOV. we take the total number of notices filed for the month so far at 84 x 5,000 oz = 420,000 oz

to which we add the difference between the open interest for the front month of NOV(262) and the number of notices served upon today 73 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the NOV../2022 contract month: 84 (notices served so far) x 5000 oz + OI for front month of NOV (262) – number of notices served upon today (73) x 5000 oz of silver standing for the NOV. contract month equates 1,365,000 oz. . (CME CORRECTED OI FOR NOV)

We will gain in silver oz standing from this day forth until the end of the month.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:51,533// est. volume today// poor

Comex volume: confirmed yesterday: 60.788 contracts ( fair)

END

GLD AND SLV INVENTORY LEVELS

NOV 1/WITH GOLD UP $9.20 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES FORM THE GLD../INVENTORY RESTS AT 920/57 TONNES

OCT 31/WITH GOLD DOWN $4.00; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD//INVENTORY RESTS AT 922.59. TONNES//

OCT28/WITH GOLD DOWN $19.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 TONNES FROM THE GLD..///INVENTORY RESTS AT 925.20 TONNES

OCT 27/WITH GOLD DOWN $3.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 26/WITH GOLD UP $11.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 25/WITH GOLD UP $3.85: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 928.39 TONNES

OCT 24/WITH GOLD DOWN $1.80 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES FROM THE GLD////INVENTORY RESTS AT 928.10 TONNES

OCT 21/WITH GOLD UP $19.10: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 930.99 TONNES

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

TONNES

GLD INVENTORY: 920.57 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

NOV 1/WITH SILVER UP 53 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 415,000 OZ FORM THE SLV////INVENTORY RESTS AT 483.308 MILLION OZ

OCT 31: WITH SILVER FLAT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .644 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 483.723 MILLION OZ//

OCT 28/WITH SILVER DOWN 35 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.367 MILLION OZ//

OCT 27/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE S: A WITHDRAWAL OF 2.579 MILLION OZ FROMTHE SLV/////INVENTORY RESTS AT 484.091 MILLION OZ//

OCT 26/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.013 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 486.670 MILLION OZ./.

OCT 25/WITH SILVER UP 17 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.083 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.683 MILLION OZ/

OCT 24/WITH SILVER UP 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .553 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.610 MILLION OZ//

OCT 21/WITH SILVER UP 43 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .46 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 486.163MILLION OZ//

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

CLOSING INVENTORY 483.308 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: Stocks Are Priced For Perfection In An Imperfect World

TUESDAY, NOV 01, 2022 – 11:40 AM

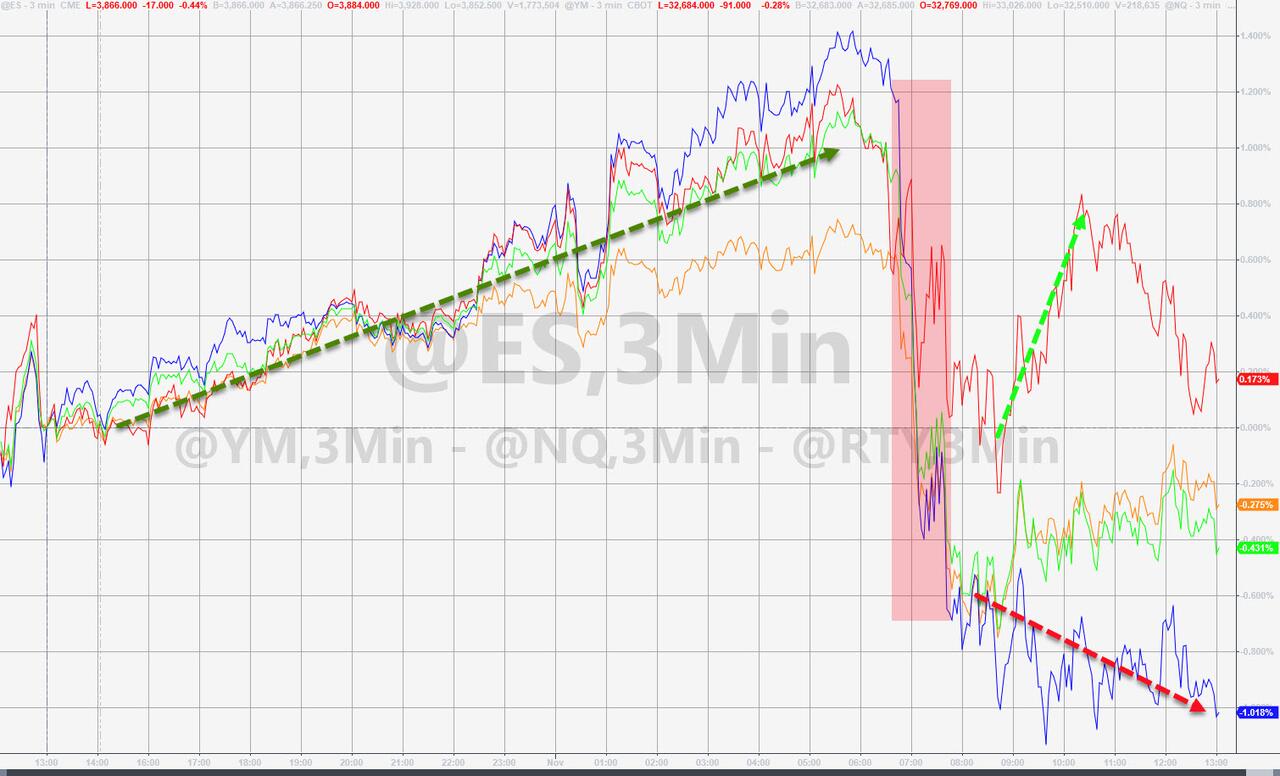

Despite all kinds of economic bad news, as of Friday, the Dow Jones was on pace for the best October in history. As Peter Schiff explained in his podcast, this demonstrates the fact that for now, bad news is good news, and stocks are priced for perfection in an imperfect world.

Over the past month, we saw more air come out of the housing bubble, PMI dip deeper into contraction, along with other signs of a deteriorating economy. Even the positive growth GDP print wasn’t really good news. But the markets shrugged it all off. As of Friday, Oct. 28, the Dow was up 14.4% on the month.

Peter called this a bear market correction.

He also noted that the rotation from growth to value stocks continued. This is evidenced by the losses in the NASDAQ.

Investors are moving out of hype and momentum into real value, into real dividends. And why is that happening? That is because interest rates have moved up, and so, we’re no longer pricing stocks based on a fantasy. Plus, we now have a cost of capital. There is an interest rate with which to discount future earnings.”

Peter said he thinks we’re just at the beginning of this rotation. In fact, it could last the rest of this decade. That means the indices heavy with momentum-oriented stocks have a long way to decline.

To show just how elevated markets are, Peter went back to 1995 and found the average price-to-earnings (before taxes) was 14.1. The current ratio is 19.6.

So, in order for the market to return to the normal ratio, we need another 28% decline from here. Not from the highs, but from where we are right now.”

The price-to-sales ratio also indicates an overvalued market.

Peter said the only way you can justify a market this expensive is if interest rates go back down.

The only reason we had such high multiples, whether it is price to earnings or price to sales — it was all a function of 0% interest rates. Well, we don’t have 0% interest rates anymore.”

If interest rates stay where they are, or continue to move higher, which the Fed is promising, the markets have a long way to fall to get back to normal.

But there is no reason why the markets should be priced at a normal valuation given the adverse circumstances that are now taking place. We have the highest inflation in 40 years, maybe the highest inflation ever. The Fed has a monumental task in front of it if it’s actually going to deliver on its promise to bring inflation down to 2%. So, if you believe the Fed – that they’re every bit as resolute in their commitment to bring inflation back down to 2%, and they’re going to do whatever it takes to achieve the goal, then you have to concede that the market is not going to fall to normal valuation, but a below normal valuation.”

Think about it. At times since 1995, these metrics have been lower than average. Why? Because during those times the markets were facing adverse circumstances.

Well, I can’t think of more adverse circumstances than the ones that the markets are operating under right now.”

So, we should see a market getting cheaper compared to those historical averages.

But not only is the market not cheap, not only is it not averagely or fairly valued, but it is still extremely expensive. So, we have a market priced for perfection and we have anything but perfection in the current circumstances.”

Peter said this tells him investors still don’t believe the Fed. Or they believe that the Fed will be able to quickly bring inflation back down to 2%, and then it will be able to return rates back to artificially low levels.

Because without 0% interest rates and QE, there is no way to justify the current valuation of today’s market. But if investors believe that, they are wrong.”

Peter said the Fed isn’t going to get inflation anywhere near 2%. And even if the Fed did manage to pull that off, it wouldn’t be able to return to abnormally low interest rates without inflation quickly spiking again.

Neither of those outcomes is possible. The only way the market could be correct in attributing these high valuations to today’s market is is if I’m right about what happens – that the Fed pivots and gives up the fight against inflation even though inflation never returns to 2%.”

Peter recently said it looks like the Fed has already made a “soft” pivot.

He said even under the environment he envisions, price-to-earnings ratios will still come down.

The only way to justify the current level is if the Fed is able to return to those artificially low interest rates and QE, and inflation goes back down to 2% and stays there. But as I said, that is impossible. So, there is no actual way that you could justify the current valuation of the US market. So, the actual valuation have to come down.”

In this podcast, Peter also talked about Amazon, Apple and Netflix’s disappointing earnings reports, Meta and Alphabet’s pain as advertising money dries up, the need for consumers to save no and buy later, and Elon Musk’s Twitter purchase.

end

Why Should You Be Bullish On Silver?

TUESDAY, NOV 01, 2022 – 02:40 PM

There are reasons to be bullish on silver, not just because of its role as a monetary metal and inflation hedge, but also due to its importance as an industrial metal. Doug Casey recently talked about silver’s many uses and what it means for the future with International Man.

The first question posted to Casey was what makes silver useful and valuable?

Casey said in the first place, silver has historically been money.

Throughout history, three metals have been used as money: gold, silver, and copper. All share the five qualities of good money—durability, divisibility, portability, consistency, and intrinsic value—but in different proportions. All three metals can be bought for the same reasons as well—each is a long-term store of value, a medium of exchange, and an interesting speculation, at least periodically. Gold has always been, and probably always will be used primarily as money. Copper will probably remain an industrial metal. Silver falls neatly in between them both in price, the way it’s used, and where it fits into your investment portfolio. It can be viewed both as a way to save—like gold—and a way to speculate—like copper.”

Silver possesses qualities that make it ideal for use in electronics, medicine, along with other technological applications. It is an extremely important element in the green energy revolution. As Casey pointed out, of the 92 naturally occurring elements, silver is the best conductor of both heat and energy. About 60% of silver is used in industrial applications.

Some argue that a slowing economy will drag silver down. But Casey says that’s not necessarily the case.

If the economy continues to slow down a lot, which I expect as we go into the Greater Depression, industrial metals are likely to get hurt. But silver has a few things that ameliorate that situation. As I said, more high-tech uses are being discovered all the time, helping the consumption side of the equation. The fact that it’s mostly a byproduct of industrial metals means that as their production drops in an economic downturn, the production of silver will drop as well. I’m much more bullish about silver than any other industrial metal—with the possible exception of uranium. At the same time, the fact that it’s a monetary metal is going to bring in a lot of buying from savers and speculators, further supporting its price.”

Casey alluded to the fact that there are very few standalone silver mines. Most silver production is a byproduct of the mining of other metals. This means that economic slowdowns will likely impact the supply side as much as demand.

Global silver production totals about 800 million ounces annually. That compares to about 80 million ounces of gold. But as Casey points out, there are no substantial silver inventories in the world. On the other hand, most of the 6 billion ounces of gold mined over the course of history, are still in existence and being stored somewhere.

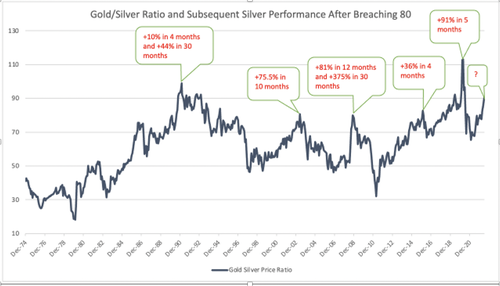

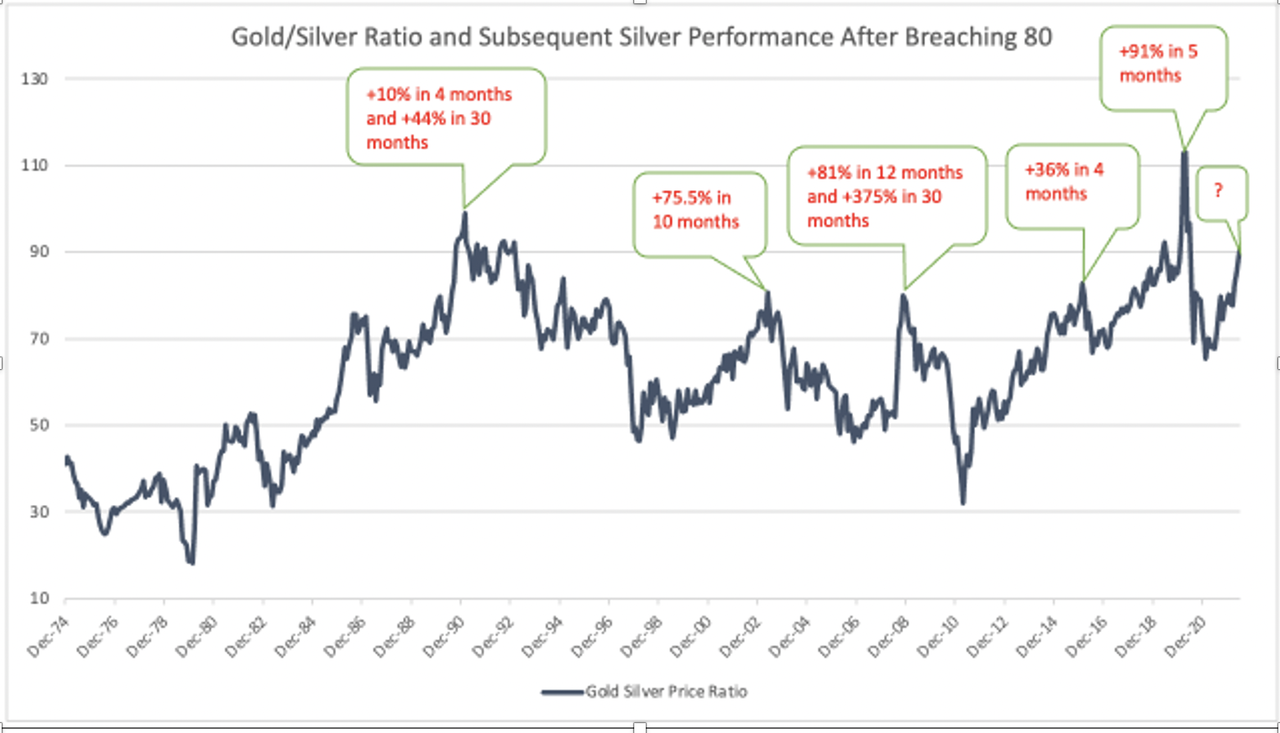

If you’re bullish on gold, you should be even more bullish on silver. Silver typically outperforms gold in a gold bull market. And the silver-gold ratio indicates that silver is significantly underpriced when compared to gold. Historically, when the spread gets this wide, silver doesn’t just outperform gold, it goes on a massive run in a short period of time. Since January 2000, this has happened four times. As this chart shows, the snapback is swift and strong.

Casey was asked why silver tends to outperform gold during gold bull runs.

Although about 80 million ounces of gold are produced every year, new production of gold is really unimportant to its price. That’s because all the gold that’s ever been mined, the 6 billion ounces that I mentioned before, is still above ground. What influences its price is the desire of people to hold it—not the roughly 1.3% added to its inventory every year. Gold is almost unique in this regard.

With silver, however, there’s not a huge relative amount of inventory to deal with. I don’t have that number, but it’s basically about new mine production. Silver inventories are in line with other industrial metals—very different from the days when the US government alone owned two billion ounces, not counting the billions more that used to be in US dimes, quarters, halves, and silver dollars. In relative terms, everything about silver is small, and small markets by their nature tend to be volatile.

There’s another thing: For many years, silver has developed a lot of fans who see it almost as a religious icon. Maybe they’re people that can’t afford gold, but silver has always, for some reason, been viewed as almost a magical element by some people, mostly Americans. They’re much more fanatical than gold bugs (among which I have to number myself).”

Casey said he is primarily bullish on silver, along with other commodities, because it is virtually the only sector in the financial markets that hasn’t been in a bubble.

If we get the kind of precious metals bull market that I’m anticipating, mining stocks, particularly silver stocks, could do phenomenally well. We’ll see them move 10-1 as a group, with some doing much better. It will have been worth the wait.”

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

LAWRIE WILLIAMS: Gold price picks up strongly in Europe amid strong CB demand report.

We had thought things probably couldn’t get any worse for the gold investor until, that is, late October trade in the U.S. took the price down to the mid $1,630s. But respite now looks as though it may be in store for aficionados of the yellow metal, at least in European trade at the beginning of November. The start of the new month saw a sharp rise in price back to the $1,650 level and above, amid reports from the World Gold Council (WGC) of record Q3 gold demand from central banks. It remains to be seen whether this represents the sea change in sentiment towards the precious metal that the gold bulls have long awaited, or is yet another false dawn. They will also have gained some encouragement from reports of some gold ETF inflows, albeit small ones, into non-U.S. exchange traded funds, after seemingly months of constant withdrawals.

It is early days yet, but the WGC analysis suggests that Q3 central bank gold inflows totalled almost 400 tonnes, reckoned to be over four times the amount the central banks added to their reserves in Q3 2021. The WGC thus puts the central bank purchases year-to-date at the highest level since 1967, when the dollar was still backed by gold. This puts a potential new high on full year central bank gold accumulations, although the WGC does not yet necessarily know the full list of central banks so involved, although there have been several which have pointed to an intention to add significantly to their gold reserves, but not necessarily confirmed that they have already done so.

Some recent known gold buyers have included India, Turkey and Qatar but many buyers are so far unreported, although some of these will eventually disclose increases in gold reserves in their reports on their gold holdings to the IMF, assuming they are forthcoming in this. There are some nations, though, which could be adding significant amounts of gold to their forex reserves which are known non- reporters – or rather only report increases to their holdings when they feel it is politically expedient for them to do so. These include China and Russia. The latter used to be a regular reporter of its reserve increases, but now that it is involved in its military incursions into Ukraine considers this sensitive strategic information and is an avowed non-reporter.

Today is also the first day of the two days of the U.S. Fed’s November Open Market Committee (FOMC) meeting at which the U.S. central bank will set its short term interest rate policy. This is widely expected to see a 75 basis point (3/4%) increase in the Federal Funds rate.

Markets will be looking for hints that there might be a slightly less aggressive approach to the Fed’s interest rate policy ahead despite there being apparently little let-up in inflation. What short term effect this may have on the gold price remains to be seen, but any signs of easing in the interest rate policy in forthcoming FOMC meetings will probably be positive for the yellow metal. Whether this would be sufficiently so to take the gold price back above the $1,700 mark or higher is perhaps dubious unless there are definite signs that inflation may at last be peaking, but that may yet be too soon to hope for.

-END-

3.Chris Powell of GATA provides to us very important physical commentaries

Another mining company goes down due to higher costs and not enough revenue

Toronto/Globe and Mail

Pure Gold shareholders face wipeout after junior fails at Red Lake mine

Submitted by admin on Mon, 2022-10-31 22:23Section: Daily Dispatches

By Niall McGee

Globe and Mail, Toronto

Monday, October 31, 2022

Pure Gold Mining Inc. PGM-X shareholders face losing their entire investment with the junior miner filing for creditor protection after it failed to turn around its gold project in the notoriously hard-to-mine Red Lake district of Northern Ontario.

Last year Vancouver-based Pure Gold ran into trouble when it encountered both grade and production shortfalls at its Madsen mine soon after putting it into production.

The Red Lake region, which has been mined for nearly 100 years, is known for its high-grade underground gold deposits. While tantalizingly rich in grade, Red Lake is also renowned for gold that is not evenly distributed but instead routinely occurs randomly and erratically, meaning miners need superb technical skills to get it right.

Over the past 18 months Pure Gold had tried to salvage its project by replacing its chief executive twice, redoing a technical study that aimed to find a path to profitable mining, and keeping itself going by raising cash through dilutive equity issues. But last week the junior put shareholders on notice by revealing it failed to raise nearly as much cash as it needed from its latest funding effort. The company also ceased production at Madsen, since it was running dangerously low on funds.

On Monday Pure Gold said it applied for creditor protection under the Companies’ Creditors Arrangement Act (CCAA) with the Supreme Court of British Columbia. When companies enter CCAA, typically it is only the debtholders who stand to salvage some of their holdings, while equity holders typically get wiped out.

Pure Gold, which at one point reached a market value of $685 million, closed today’s trading session on the TSX Venture Exchange worth almost nothing.

The company’s biggest shareholder is South African miner AngloGold Ashanti, with a 16.5% stake. Mark O’Dea, Pure Gold’s chief executive, has a 2.2% share. Mining financier Eric Sprott, who has myriad equity investments spread across many junior miners, is the second-biggest holder of Pure Gold with a 6.7% stake.

“I don’t think I lost $100 million, but it could very well be,” Mr. Sprott said in an interview. “At this point in time, the bigger the better, because it’s a tax write-off. Now that it’s worth nothing, please tell me I lost $100 million or $200 million. I’ll use the tax loss.”

Pure Gold holds only around $2 million in cash, compared with more than $200 million in liabilities. Sprott Resource Lending, which is owned by Sprott Inc. SII-T, a firm the billionaire investor founded, is its biggest creditor.

This isn’t the first time that the Red Lake district has claimed a junior miner. In 2016 shareholders at Rubicon Minerals Corp., which at one time had a market value of $1 billion, lost everything after the company’s mine ran into serious geological problems. A restructured version of the company, Battle North Gold Corp., was acquired by Australia’s Evolution Mining Ltd. last year.

In 2008 Goldcorp Inc., bought Red Lake exploration company Gold Eagle Mines Ltd. for $1.5 billion. The acquisition ended in disaster for Goldcorp, which was unable to put the project into production despite spending hundreds of millions in additional development costs.

Pure Gold’s Madsen project had previously operated for 40 years, producing 2.5 million ounces of gold, before it was shut down in the 1970s. Pure Gold’s founders, Mr. O’Dea and Darin Labrenz, acquired the defunct project in 2014 and their early development work indicated that a new iteration of the mine could produce an additional million ounces of gold. Eventually the pair attracted investment from the likes of Mr. Sprott and Robert McEwen, the founder of Goldcorp. While reviving dormant mine sites can be lucrative because upfront costs tend to be much lower than starting from scratch, they are far from risk-free.

“There probably was excessive optimism initially,” Mr. Sprott said. “Maybe things could have been done at a different level early on, when there was more market cap to work with, but c’est la vie.”

Despite the recurrent stumbles with Red Lake, it remains a gold district that generates excitement and lofty valuations. Last year Kinross Gold Corp. paid $1.8 billion to acquire Great Bear Resources Ltd., another Red Lake operator whose mining project hasn’t been built yet. The purchase price was one of the highest on record for the acquisition of a development company that has no proven reserves.

Evolution Mining had been mentioned by analysts as a possible buyer of Pure Gold before it filed for CCAA. Over the past few years the Sydney-based miner has invested heavily in the Red Lake region. In 2020 Evolution paid US$375 million to acquire Red Lake gold mines owned by U.S.-based Newmont Corp., assets that were previously owned and operated by Goldcorp.

end

European inflation hits a record 10.7%

(London’s Financial Times/GATA)

Eurozone inflation hits record 10.7%

Submitted by admin on Mon, 2022-10-31 12:54Section: Daily Dispatches

By Martin Arnold

Financial Times, London

Monday, October 21, 2022

Eurozone inflation surged to a record high of 10.7% in October, keeping the pressure on the European Central Bank to continue raising interest rates despite a sharp slowdown in growth in the third quarter.

The increase in eurozone consumer prices accelerated from 9.9% in September, which was already the highest in the 23-year history of the euro

The latest high, reported today by the European Commission’s statistics arm Eurostat, also outstripped the 10.2% expected by economists polled by Reuters. It was the 12th consecutive month that inflation has set a record high in the eurozone, taking it to more than five times the ECB’s 2% target.

Claus Vistesen, an economist at Pantheon Macroeconomics, said the latest inflation figures were “a proper Halloween nightmare for the ECB.” …

… For the remainder of the report:

https://www.ft.com/content/d783e38e-7a58-4285-b68a-55e357bb8c4b

END

BIS swaps remain at its lows at 57 tonnes

(Robert Lambourne/GATA)

Robert Lambourne: BIS gold swaps stay very low for second month

Submitted by admin on Mon, 2022-10-31 20:31Section: Daily Dispatches

By Robert Lambourne

Monday, October 31, 2022

The recently released September statement of account of the Bank for International Settlements —

— shows little change in the bank’s use of gold swaps for the second month running. The gold swaps outstanding at September 30 are estimated to be 57 tonnes versus 75 tonnes and 56 tonnes as of August 31 and July 29, respectively. This recent level is much reduced from the level of swaps at June 30, which was 202 tonnes.

As is clear from Table B below, the level of swaps had been significantly higher in the first half of the year. For example, at the end of January 2022 there were gold swaps of 501 tonnes.

Once again it is evident that the BIS remains an active trader of significant volumes of gold swaps on a regular basis, and the recent data indicates that a downward trend in the bank’s swaps is continuing. Certainly the current level of gold swaps is well below the levels reported in Table B below since August 2019.

The falling levels of gold swaps might indicate an exit from the swaps due potentially to “Basel III” regulations. As is usually the case with the BIS, it seems unlikely that any extra information on its use of gold swaps will be forthcoming.

… Historical context …

The BIS rarely comments publicly on its gold activities, but its first use of gold swaps was considered important enough to cause the bank to give some background information to the Financial Times for an article published July 29, 2010, coinciding with publication of the bank’s 2009-0 annual report.

The general manager of the BIS at the time, Jaime Caruana, said the gold swaps were “regular commercial activities” for the bank, and he confirmed that they were carried out with commercial banks and so did not involve central banks.

It also seems highly likely that the BIS’ remaining swaps are still all made with commercial banks, because the BIS annual report has never disclosed a gold swap between the BIS and a major central bank.

The swap transactions potentially create a mismatch at the BIS, which may end up being long unallocated gold (the gold held in BIS sight accounts at major central banks) and short allocated gold (the gold required to be returned to swap counterparties). This possible mismatch has not been reported by the BIS.

The gold banking activities of the BIS have been a regular part of the services it offers to central banks since the establishment of the bank 90 years ago. The first annual report of the BIS explains these activities in some detail:

http://www.bis.org/publ/arpdf/archive/ar1931_en.pdf

A June 2008 presentation made by the BIS to potential central bank members at its headquarters in Basel, Switzerland, noted that the bank’s services to its members include secret interventions in the gold and foreign exchange markets:

https://www.gata.org/node/11012

The use of gold swaps to take gold held by commercial banks and then deposit it in gold sight accounts held in the name of the BIS at major central banks doesn’t appear ever to have been as large a part of the BIS’ gold banking business as it has been in recent years, although the recent declines do seem to suggest this is changing.

As of March 31, 2010, excluding gold owned by the BIS, there were 1,706 tonnes held in gold sight accounts at major central banks in the name of the BIS, of which 346 tonnes or 20% were sourced from gold swaps from commercial banks.

If the BIS was adopting the level of disclosure made by publicly held companies, such as commercial banks, some explanation of these changes probably would have been required by the accounting regulators. This irony may not be lost on those dealing with regulatory activities at the BIS. Presumably the shrinkage of the BIS’ gold banking business shows that even central banks now prefer to hold their own gold or hold it in earmarked form — that is, as allocated gold.

A review of Table B below highlights recent BIS activity with gold swaps, and despite the recent declines, the recent positions estimated from the BIS monthly statements remain large, especially in early 2022, and the volume of trading has been significant.

No explanation for this continuing use of swaps has been published by the BIS. Indeed, no comment on the bank’s use of gold swaps has been offered since 2010.

This gold is supplied by bullion banks via the swaps to the BIS. The gold is then deposited in BIS gold sight accounts (unallocated gold accounts) at major central banks such as the Federal Reserve.

The reasons for this activity have never been fully explained by the BIS and various conjectures have been made as to why the BIS is facilitating it. One conjecture is that the swaps are a mechanism for gold secretly supplied by central banks to cover shortfalls in the gold markets to be returned to the central banks. The use of the BIS to facilitate this trade suggests a desire to conceal the rationale for the transactions.

As can be seen in Table A below, the BIS has used gold swaps extensively since its financial year 2009-10. No use of swaps is reported in the bank’s annual reports for at least 10 years prior to the year ended March 2010.

The February 2021 estimate of the bank’s gold swaps (552 tonnes) was higher than any level of swaps reported by the BIS at its March year-end since March 2010. The swaps reported at March 2021 were at the highest year-end level reported, as is clear from Table A.

—–

Table A — Swaps reported in BIS annual reports

March 2010: 346 tonnes.

March 2011: 409 tonnes.

March 2012: 355 tonnes.

March 2013: 404 tonnes.

March 2014: 236 tonnes.

March 2015: 47 tonnes.

March 2016: 0 tonnes.

March 2017: 438 tonnes.

March 2018: 361 tonnes.

March 2019: 175 tonnes

March 2020: 326 tonnes

March 2021: 490 tonnes

March 2022: 358 tonnes

—–

The table below reports the estimated swap levels since August 2018. It can be seen that the BIS is actively involved in trading gold swaps and other gold derivatives with changes from month to month reported in excess of 100 tonnes in this period.

—–

Table B — Swaps estimated by GATA from BIS monthly statements of account

Month ….. Swaps

& year … in tonnes

Sep-22………/57

Aug-22……./75

Jul-22………/56

Jun-22……./202

May-22……./270

Apr-22 ….. /315

Mar-22 …. /358

Feb-22 …. /472

Jan-22 ….. /501

Dec-21…. /414

Nov-21…. /451

Oct-21…. /414

Sep-21 …. /438

Aug-21 …. /464

Jul-21 …. /502

Jun-21 …./471

May-21 …./517

Apr-21 …. /472

Mar-21…. /490±

Feb-21 …../552

Jan-21 …. /523

Dec-20 …. /545

Nov-20 …. /520

Oct-20 …. /519

Sep-20…../ 520

Aug-20…../ 484

Jul-20 ….. / 474

Jun-20 …. / 391

May-20 …. / 412

Apr-20 …. / 328

Mar-20 …. / 326*

Feb-20 …. / 326

Jan-20 …. / 320

Dec-19 …. / 313

Nov-19 …. / 250

Oct-19 …. / 186

Sep-19 …. / 128

Aug-19 …. / 162

Jul-19 ….. / 95

Jun-19 …. / 126

May-19 …. / 78

Apr-19 ….. / 88

Mar-19 …. / 175

Feb-19 …. / 303

Jan-19 …. / 247

Dec-18 …. / 275

Nov-18 …. / 308

Oct-18 …. / 372

Sep-18 …. / 238

Aug-18 …. / 370

± The estimate originally reported by GATA was 487 tonnes, but the BIS annual report states 490 tonnes, It is believed that slightly different gold prices account for the difference.

* The estimate originally reported by GATA was 332 tonnes, but the BIS annual report states 326 tonnes. It is believed that slightly different gold prices account for the difference.

GATA uses gold prices quoted by USAGold.com to estimate the level of gold swaps held by the BIS at month-ends.

—–

As noted already, the BIS in recent times has refused to explain its activities in the gold market, nor for whom the bank is acting:

https://www.gata.org/node/17793

Despite this reticence the BIS is almost certainly acting on behalf of central banks in taking out these swaps, as they are the BIS’ owners and control its Board of Directors.

This refusal to explain prompts some observers to believe that the BIS acts as an agent for central banks intervening surreptitiously in the gold and currency markets, providing those central banks with access to gold as well as protection from exposure of their interventions.

A report published by Bullion Star’s Ronan Manly on the Bank of Portugal’s use of its gold reserves reinforces this point as the Bank of Portugal confirms that 20 tonnes of its gold is stored with the BIS:

https://www.gata.org/node/21950

This disclosure seems a little economical with the truth as the BIS has no gold storage facilities of its own. Gold held by the BIS on behalf of central banks is either deposited into a BIS gold sight (unallocated) account or a BIS earmarked (allocated) gold account and deposited normally with one of the central banks based at a major gold trading center, such as the Federal Reserve in New York.

Since Manly shows that the Bank of Portugal is focused on earning income from its gold, it seems likely that this gold is held in a BIS sight account, though its ultimate location is unclear.

It is possible that the swaps provide a mechanism for bullion banks to return gold originally lent to them by central banks to cover bullion bank shortfalls of gold. Some commentators have suggested that a portion of the gold held by exchange-traded funds and managed by bullion banks is sourced directly from central banks.

—–

Robert Lambourne is a retired business executive in the United Kingdom who consults with GATA about the involvement of the Bank for International Settlements in the gold market.

* * *

END

4. OTHER PHYSICAL SILVER/GOLD COMMENTARIES

5.OTHER COMMODITIES: URANIUM/ENERGY

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 7.2586

OFFSHORE YUAN: 7.2627

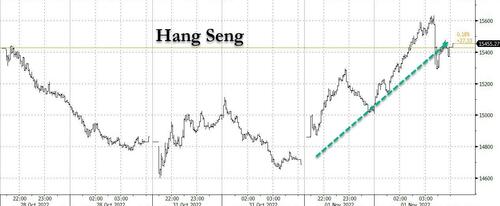

SHANGHAI CLOSED UP 75.72 PTS OR 2.62%

HANG SENG CLOSED UP 768.25 OR 5.23%

2. Nikkei closed UP 91.46PTS OR 0.33%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 110.65/Euro RISES TO 0.9945

3b Japan 10 YR bond yield: RISES TO. +.249!!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 147,05/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.035%***/Italian 10 Yr bond yield FALLS to 4.129%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.098%…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.518//

3j Gold at $1653.95//silver at: 19.97 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 5/100 roubles/dollar; ROUBLE AT 61.41//

3m oil into the 88 dollar handle for WTI and 94 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 147,03DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9918– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9863well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.941% DOWN 14 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 4.069% DOWN 14 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,62…GETTTING DANGEROUS

GREAT BRITAIN/10 YEAR YIELD: 3.4755%

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Surge Amid Speculation China Set To Ease Covid Zero; Dollar Tumbles

TUESDAY, NOV 01, 2022 – 08:12 AM

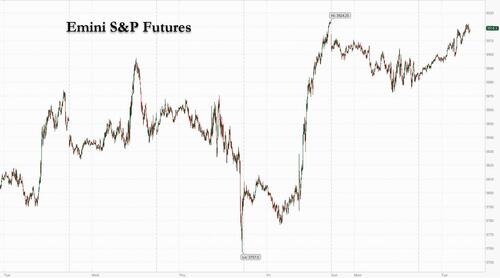

US equity futures started off the new month with a bang, set to surge after Monday’s less than spooky declines, as investors awaited Wednesday’s Fed decision (where JPM sees one outcome pushing stocks 10% higher… and another sending them crashing 8%), while sentiment got a big boost from speculation that Chinese policymakers are making preparations to gradually exit the stringent Covid Zero policy.

At 7:30am, contracts on the S&P 500 rose 1.0% while those on the Nasdaq 100 gained 1.1% on the first day of November, a month that has seen the underlying benchmarks end in the green on average for the past three decades. Dow Jones futures climbed 0.6% after the underlying gauge wrapped up its best month since 1976. Treasuries were poised for their biggest jump in a week as 10Y yields dropped to 3.94%, alongside real rates and the dollar as hawkish Fed hike wagers are trimmed ahead of this week’s policy outcome; the yen, euro and cable surged.

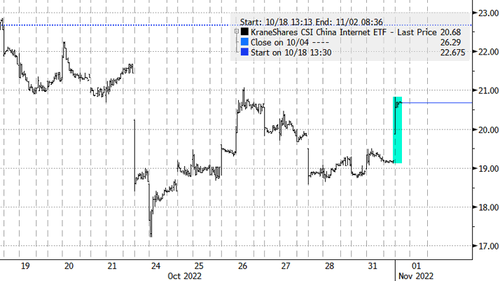

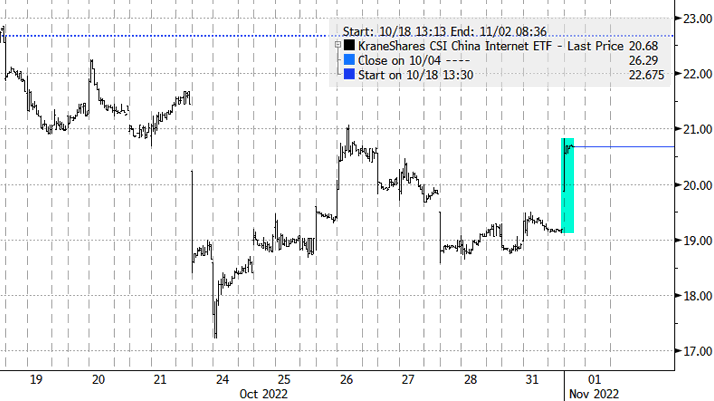

Chinese stocks listed in the US surged in New York premarket trading, their gains fueled by speculation that Beijing is preparing to phase out Covid Zero policies, even as the country’s Foreign Ministry said it was unaware of such a plan. The KraneShares CSI China Internet Fund, an exchange-traded fund holding more than 40 Chinese stocks, soared 7.7%. Also in the premarket, Tesla shares rose as much as 2.1% following a Reuters report that the EV maker plans to start mass production of its Cybertruck at the end of 2023. Here are other notable premarket movers:

- Abiomed shares soared 51% in US premarket trading to $379.55 after Johnson & Johnson agreed to buy all its outstanding shares for an upfront payment of $380 per share in cash plus a CVR consideration of up to $35 if certain clinical and commercial milestones are achieved

- GameStop shares rise as much as 5.6% in US premarket trading, with a meme-stock revival set to extend into a second day as other stocks popular with retail traders also rally. The video-game retailer also launched an NFT marketplace. Among other meme stocks AMC Entertainment (AMC US) +1.4%, Bed Bath & Beyond (BBBY US) +3.5%, Lucid (LCID US) +2.1%

- Carvana shares jump as much as 15% in US premarket trading after JPMorgan upgraded the online used-car platform to neutral from underweight, with analysts saying that risks appear to be “better understood” and liquidity is “manageable.”

- Macau casino stocks rise in US premarket trading amid speculation that China is planning to gradually exit its Covid Zero policies, even as the country’s Foreign Ministry said it was unaware of any government committee that’s assessing ways to carry out the plan. Melco Resorts (MLCO US) +7.5%, Las Vegas Sands (LVS US) +4.1%, Wynn Resorts (WYNN US) +3.3% and MGM Resorts (MGM US) +2.3%

- Stryker delivered a strong top-line that bodes well for the medtech group’s outlook, but questions remain on when that will translate into a stronger earnings performance, analysts say. Stryker shares fell 5% in postmarket trading after the update.

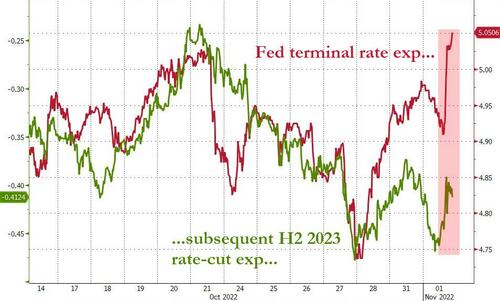

All eyes will be on the Fed on Wednesday, when it’s widely expected to raise rates by 75 basis points for a fourth time but the question is how Powell will guide for December and his views on the terminal rate. His comments will also be key in understanding the trajectory of tightening in the US, where the policy is already having an impact on company earnings.

“What is important is the path Chair Powell lays out for next year. The Fed probably doesn’t want the market to start pricing in rate cuts, and this is what the market tends to do,” said Stephen Innes, managing partner at SPI Asset Management. “It’s an open invitation to buy stocks in case we do get a Fed pivot or inflation starts abating and we get a huge asymmetrical move to the top side.”

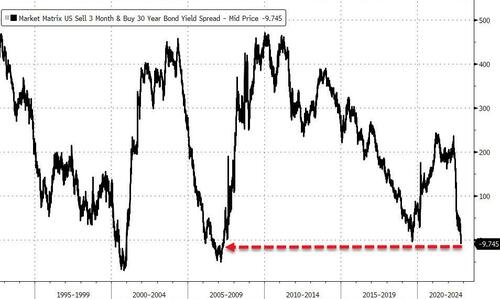

Strategists are expecting the US central bank to end tightening in the near term. Indicators including the inversion of the yield curve between 10-year and three-month Treasuries “all support a Fed pivot sooner rather than later,” according to Morgan Stanley’s Michael Wilson. Also, JPMorgan’s Marko Kolanovic is seeing signs boosting optimism that the global tightening cycle could end by early 2023, which of course is also market consensus.

“If the Fed does give us some indication that there is light at the end of the tunnel, we are very close if not already past peak dollar,” Mark Matthews, head of Asia research at Julius Baer said on Bloomberg TV. “Then all the currencies which have declined like the euro will rebound.”

Meanwhile, economists surveyed by Bloomberg said Fed officials will maintain their resolutely hawkish stance this week, laying the groundwork for interest rates reaching 5% by March 2023, moves that seem likely to lead to a US and global recession. Nomura Holdings Inc. quantitative strategist Yoshitaka Suda said derivatives cues imply the pace of the ongoing rebound in the S&P 500 benchmark is likely to dwindle after the Fed’s decision. The comparatively low volatility ahead of the meeting shows that the options market is “increasingly optimistic” about the event, he said. A shift in options hedging by traders could also weigh on the market, he added.

European equity benchmarks rose over 1% as bond yields retreated lower. CAC 40 outperfoms while the DAX lags peers a bit. Mining shares led gains as most base metals trade in the green. European luxury stocks jumped, tracking an earlier rally in Chinese markets on speculation that the country’s policymakers are looking at gradually unwinding its stringent Covid Zero policy. LVMH rose as much as 3.9%. Shares in tech investor Naspers and its unit Prosus also surged, following Tencent higher as Chinese tech stocks rose after unverified social media posts circulated online that a committee was being formed to assess scenarios on how to exit Covid Zero. A Chinese Foreign Ministry spokesman said he’s unaware of a committee. Here are the biggest European movers:

- Oil advanced and BP Plc climbed after announcing a further $2.5 billion buyback. Here are Europe’s biggest movers:

- Ocado Group surged as much as 40% in a brisk short covering rally sparked by news the UK online grocer has entered a partnership to develop Lotte’s online business in South Korea.

- Shares of European online retailers and food delivery firms rally on Tuesday after heavy selling this year, as yields on 10-year US Treasuries and German bunds slide. Delivery Hero rises as much as 15%.

- Scor shares gain as much as 6.3% as Mediobanca upgraded the reinsurer to outperform in a reshuffling of its sector preferences.

- ALKB- Abello fell as much as 7% after Danske Bank analyst Thomas Bowers cut the recommendation to hold from buy.

- Fresenius Medical Care falls as much as 5.5% after Warburg downgraded the stock to sell from hold, citing increased uncertainties regarding the supply chain and macro factors despite 3Q figures slightly above estimates.

- Rentokil shares drop as much as 4.5% after the company posted 3Q growth in line with expectations. Morgan Stanley noted that the firm’s maintained outlook implies more subdued progress on margins in 2H.

Asian stocks advanced ahead of a key US Federal Reserve rate decision, as Chinese shares staged a strong rebound on speculation of a potential reopening. The MSCI Asia Pacific Index jumped as much as 2.4%, the most in more than two weeks, as Chinese and Hong Kong gauges roared back from multi-year lows on speculation that policymakers are making preparations to gradually exit the stringent Covid Zero policy. The Hang Seng Index climbed more than 5%, with internet giants Meituan and Tencent Holdings the biggest contributors to the advance.

Unverified social media posts circulated online on Tuesday showed a committee was being formed to assess scenarios on how to exit Covid Zero. A Covid-induced economic slowdown in China has been one of the biggest overhangs for the region’s markets. “Obviously some people are betting big on China’s reopening,” said Willer Chen, an analyst at Forsyth Barr Asia. “At this level, it’s probably better to trade every rumor than ridiculing its authenticity.” Meanwhile, the Federal Reserve looks set to raise interest rates by 75 basis points on Wednesday amid its most-aggressive tightening campaign in four decades. Investors will be watching for any signs that hikes may slow in the future. Asian equities fell 2% in October, capping a third-straight monthly decline, amid headwinds including China’s slowdown and global monetary tightening. The MSCI Asian benchmark is hovering near the lowest level since April 2020.

Japanese stocks rose as the yen’s weakness was seen providing earnings benefits for the nation’s exporters. The Topix rose 0.5% to close at 1,938.50, while the Nikkei advanced 0.3% to 27,678.92. Keyence Corp. contributed the most to the Topix gain, increasing 3.4%. Out of 2,166 stocks in the index, 1,011 rose and 1,044 fell, while 111 were unchanged. “Japanese stocks are holding firm as the market sees a positive impact of the yen’s depreciation reflected in the recent earnings,” said Tetsuo Seshimo, portfolio manager at Saison Asset Management

Australian government bond yields reversed earlier gains and the nation’s stocks rallied to a seven-week high after the central bank raised interest rates by a quarter point as expected and signaled further tightening to come as it combats escalating inflation. Australia’s S&P/ASX 200 index rose 1.7% to close at 6,976.90, the highest since Sept. 13, Mining and bank shares boosted the benchmark most, with all 11 sectors advancing. In New Zealand, the S&P/NZX 50 index fell 0.2% to 11,316.64