NOV 9/USA ELECTIONS STILL UNDECIDED//GOLD CLOSED DOWN $2.00 TO $1710.15/SILVER CLOSED DOWN 10 CENTS TO $21.24/PLATINUM CLOSED DOWN $7.95 TO $989.50//PALLADIUM CLOSED DOWN $67.85 TO $1861.25//COVID UPDATES//VACCINE IMPACT/VACCINE INJURY REPORT//DR PAUL ALEXANDER//RUSSIA ORDERS ALL OF ITS TROOPS IN KHERSON TO LEAVE THE CITY//FED EX AND MAERSK ANNOUNCE HUGE DROP IN GLOBAL SHIPMENTS//USA ELECTION RESULTS//SWAMP STORIES FOR YOU TONIGHT//

132 C SG AMERICAS 12 190 H BMO CAPITAL 2 661 C JP MORGAN 5 737 C ADVANTAGE 4 2 880 H CITIGROUP 7

TOTAL: 16 16

JPMORGAN STOPPED 75/16

GOLD: NUMBER OF NOTICES FILED FOR NOV. CONTRACT: 16 NOTICES FOR 1600 OZ or 0.0497 TONNES

total notices so far: 4898 contracts for 489,800 oz (15.294 tonnes)

SILVER NOTICES: 126 NOTICE(S) FILED FOR 630,000 OZ/

total number of notices filed so far this month 287 : for 1,435,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $2.00

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////A BIG CHANGE IN GLD INVENTORY: A DEPOSIT OF 2.89 TONNES FROM THE GLD// /THIS MAKES NO SENSE@@!!!! THIS IS A CRIME SCENE

INVENTORY RESTS AT 908.38 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN $0.10

AT THE SLV// :/BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF OF 3.821 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 472.108 MILLION OZ (THIS IS ALSO A CRIME SCENE@!!!!

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GIGANTIC SIZED 3105 CONTRACTS TO 140,437 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE HUGE GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR STRONG $0.48 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR SHORTERS/HFT WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.48)., AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC LONGS, AS WE HAD AN ATMOSPHERIC SIZED GAIN IN OUR TWO EXCHANGES OF 5664 CONTRACTS. WE HAD A CONSIDERABLE SPEC SHORT COVERING THEIR SHORTFALLS .WE HAD NO SPEC SHORT ADDITIONS AS THE PRICE ESCALATED AWAY FROM THEM CAUSING LOTS OF LOSSES. // OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. HUGE NUMBER OF NEWBIE SPEC LONGS ADDED TO THEIR POSITIONS CAUSING MISERY TO OUR SHORTERS.

WE MUST HAVE HAD: I) CONSIDERABLE SPECULATOR SHORT COVERINGS WITH ZERO SHORT ADDITIONS ////CONTINUED BANKER OI COMEX ADDITIONS /// HUGE NEWBIE SPEC LONG ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GIGANTIC ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.045 MILLION OZ FOLLOWED BY TODAY’S 150,000 QUEUE JUMP//NEW STANDING:1.97 MILLION OZ/ / // V) HUGE SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -36

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS NOV. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF NOV:

TOTAL CONTRACTS for 7 days, total 16,800 contracts: 71.385 million oz OR 9.795MILLION OZ PER DAY. (2400 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 71.385 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 71.385 MILLION

RESULT: WE HAD A GIGANTIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3105 WITH OUR HUGE $0.48 GAIN IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A GIGANTIC SIZED EFP ISSUANCE CONTRACTS: 2523 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR NOV. OF 1.345 MILLION OZ FOLLOWED BY TODAY’S 150,000 QUEUE JUMP/ .. WE HAVE AN ATMOSPHERIC SIZED GAIN OF 5628 OI CONTRACTS ON THE TWO EXCHANGES FOR 28.140MILLION OZ.. THE SILVER SHORTS ARE NOW TRAPPED AS THEY ARE HAVING CONSIDERABLE DIFFICULTY IN COVERING THOSE SHORTS ESPECIALLY WITH THE GAIN IN PRICE ON TUESDAY.

WE HAD 126 NOTICE(S) FILED TODAY FOR 630,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A VERY STRONG SIZED 10,256 CONTRACTS TO 488,471 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -666 CONTRACTS.

.

THE VERY STRONG SIZED INCREASE IN COMEX OI CAME WITH OUR HUGE RISE IN PRICE OF $34.40//COMEX GOLD TRADING/TUESDAY // CONSIDERABLE ATTEMPTED SPECULATOR SHORT COVERINGS TO NO AVAIL//ZERO SPEC SHORT ADDITIONS, ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION WITH CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS. IT SEEMS THAT EVERYBODY WISHES TO BUY BUT NO SELLERS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR NOV. AT 12.386 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S GOOD 1600 OZ QUEUE JUMP //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR RISE IN PRICE OF $34.40 WITH RESPECT TO TUESDAY’S TRADING

WE HAD AN ATMOSPHERIC SIZED GAIN OF 15,027 OI CONTRACTS (46.74 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4771 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 488,471

IN ESSENCE WE HAVE AN ATMOSPHERIC SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 15,027 CONTRACTS WITH 10,256 CONTRACTS INCREASED AT THE COMEX (SHORT SPECULATORS FAILING TO GET OUT OF THEIR MESS) AND 4771 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 15,027 CONTRACTS OR 46.74 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4771) ACCOMPANYING THE VERY STRONG SIZED GAIN IN COMEX OI (10,256): TOTAL GAIN IN THE TWO EXCHANGES 15,027 CONTRACTS. WE NO DOUBT HAD 1) CONSIDERABLE ATTEMPTED BUT FAILED SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS. WE HAD ZERO SHORT SPEC ADDITIONS/// // CONSIDERABLE NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR NOV. AT 12.386 TONNES FOLLOWED BY TODAY’S GOOD QUEUE JUMP OF 1600 OZ //NEW STANDING 20.299 TONNES///3) ZERO LONG LIQUIDATION //// //.,4) VERY STRONG SIZED COMEX OPEN INTEREST GAIN 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

NOV

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV. :

31,398 CONTRACTS OR 3,139,800 OZ OR 97.66 TONNES 7 TRADING DAY(S) AND THUS AVERAGING: 4485 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAY(S) IN TONNES: 97.66 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 97.66/3550 x 100% TONNES 2.75% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 97.66 TONNES//INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GIGANTIC SIZED 3105 CONTRACT OI TO 140,437 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 2523 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 2523 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2523 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 3141 CONTRACTS AND ADD TO THE 2523 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN ATMOSPHERIC SIZED GAIN OF 5628 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 28.140MILLION OZ//

OCCURRED WITH OUR RISE IN PRICE OF $0.48….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED DOWN 16.33 PTS OR 0.53% //Hang Seng CLOSED DOWN 198.79 OR 1.20% /The Nikkei closed DOWN 155.68 OR 0.56% //Australia’s all ordinaires CLOSED UP 0.52% /Chinese yuan (ONSHORE) closed DOWN TO 7.2527 //OFFSHORE CHINESE YUAN DOWN 7.2646// /Oil DOWN TO 88.06 dollars per barrel for WTI and BRENT AT 93.68 / Stocks in Europe OPENED MOSTLY RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKERHANGHAI CLOSED DOWN 16.33 PTS OR 0.53% //Hang Seng CLOSED DOWN 198.79 OR 1.20% /The Nikkei closed DOWN 155.68 OR 0.56% //Australia’s all ordinaries CLOSED UP 0.52% /Chinese yuan (ONSHORE) closed DOWN TO 7.2527 //OFFSHORE CHINESE YUAN DOWN 7.2646// /Oil DOWN TO 88.06 dollars per barrel for WTI and BRENT AT 93.68 / Stocks in Europe OPENED MOSTLY RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A VERY STRONG SIZED 10,256 CONTRACTS TO 489,137 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED WITH OUR HUGE GAIN IN PRICE OF $34.40 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (4771 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT SEEMS THAT SPEC SHORTS ARE STILL HAVING TROUBLE COVERING THEIR HUGE SHORTFALL.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON -ACTIVE DELIVERY MONTH OF NOV.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4771EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC : 4771 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4771 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: AN ATMOSPHERIC SIZED TOTAL OF 15,027 CONTRACTS IN THAT 4771LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A VERY STRONG SIZED COMEX OI GAIN OF 10,256 CONTRACTS..AND THIS GIGANTIC SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR STRONG RISE IN PRICE OF GOLD $34.40//WE FINALLY HAD SOME SPEC SHORTS TRYING TO COVER THEIR SHORTFALL WITH LIMITED SUCCESS. BANKERS CONTINUE AS NET BUYERS OF COMEX GOLD CONTRACTS AS THEY HAVE BEEN NET LONG FOR THE PAST FEW MONTHS. WE ALSO HAD HUGE ADDITIONAL NEWBIE SPECS GOING LONG. IT LOOKS LIKE OUR SPEC SHORTS ARE IN DEEP TROUBLE

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING NOV (20.299),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 20.299 TONNES/INITIAL (TOTAL SO FAR THIS YEAR 564.435 TONNES)

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $34.40) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS. HOWEVER WE DID HAVE SOME SPECULATOR SHORTS COVERING THEIR SHORTFALL BUT ZERO SPEC SHORT ADDITIONS.. WE HAD AN ATMOSPHERIC SIZED GAIN ON OUR TWO EXCHANGES OF 15,027 CONTRACTS.// WE HAVE GAINED A TOTAL OI OF 48.811 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR NOV. (20.299 TONNES)…THIS WAS ACCOMPLISHED DESPITE OUR RISE IN PRICE OF $34.40

WE HAD -666 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 15,027 CONTRACTS OR 1,502,700 OZ OR 46.74 TONNES

Estimated gold volume 317,061// very good//

final gold volumes/yesterday 240,099/ fair

INITIAL STANDINGS FOR NOVEMBER 2022 COMEX GOLD //NOV 9

Total monthly oz gold served (contracts) so far this month

4898 notices 489,800 15.294TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

customer withdrawals:2

ii) Out of Brinks: 11,031.284 oz

ii) Out of Manfra: 37,275.848 oz

total: 48,307.132 oz

total in tonnes: 1.502 tonnes

Adjustments: 3// dealer to customer

i) Out of Brinks: 8,000.46oz

ii) Out of HSBC: 385.812 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR NOVEMBER.

For the front month of NOV. we have an oi of 1644 contracts having LOST ONLY 6 contracts. We had 24 notices served on TUESDAY so we gained a strong 16

or an additional 1600 OZ (0.0497 TONNES) will stand in this non active month of November. We will have Nov gold tonnage standing increase daily from this day forth until the end of the month.

This queue jumping originates in London with the exercising of London based EFP’s for comex gold.

December LOST ONLY 14,611 contracts DOWN to 308,189. DEC WILL BE A DILLY OF A DELIVERY MONTH.

JANUARY GAINED 31 contract to stand at 183.

February gained 23,928 contacts up to 137,837.

We had 16 notice(s) filed today for 1600 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 16 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 5 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the NOV. /2022. contract month,

we take the total number of notices filed so far for the month (4898) x 100 oz , to which we add the difference between the open interest for the front month of (NOV 1644 CONTRACTS) minus the number of notices served upon today 16 x 100 oz per contract equals 652,600 OZ OR 20.299 TONNES the number of TONNES standing in this non active month of NOV.

thus the INITIAL standings for gold for the NOV. contract month:

No of notices filed so far (4898) x 100 oz+ (1644) OI for the front month minus the number of notices served upon today (16} x 100 oz} which equals 652,600 oz standing OR 20.299 TONNES in this NON active delivery month of NOV..

TOTAL COMEX GOLD STANDING: 20.299 TONNES (A HUMONGOUS STANDING//NEW RECORD FOR NOV (GENERALLY THE POOREST DELIVERY MONTHS FOR A NON ACTIVE MONTH)

To calculate the number of silver ounces that will stand for delivery in NOV. we take the total number of notices filed for the month so far at 287 x 5,000 oz = 1,435,000 oz

to which we add the difference between the open interest for the front month of NOV(233) and the number of notices served upon today 126 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the NOV../2022 contract month: 287 (notices served so far) x 5000 oz + OI for front month of NOV (233) – number of notices served upon today (126) x 5000 oz of silver standing for the NOV. contract month equates 1,970,000 oz.

We will gain in silver oz standing from this day forth until the end of the month.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:104,869// est. volume today// huge/shorts covered

NOV 9/WITH GOLD DOWN $2.00: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES INTO THE GLD////INVENTORY RESTS AT 908.38 TONNES

NOV 8/WITH GOLD UP $34.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.47 TONNES FROM THE GLD//: INVENTORY RESTS AT 905.49 TONNES

NOV 7/WITH GOLD UP $2.95: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.63 TONNES FROM THE GLD//INVENTORY RESTS AT 906.96. TONNES

NOV 4/WITH GOLD UP $44.45 TO $1673.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.48 TONNES FROMTHE GLD////INVENTORY RESTS AT 911.59 TONNES.

NOV 3/WITH GOLD DOWN $18.30 TO $1628.85: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.05 TONNES FROM THE GLD////INVENTORY RESTS AT 915.07 TONNES

NOV 2/WITH GOLD UP 55 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 919.12 TONNES.

NOV 1/WITH GOLD UP $9.20 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES FORM THE GLD../INVENTORY RESTS AT 920.57 TONNES

OCT 31/WITH GOLD DOWN $4.00; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD//INVENTORY RESTS AT 922.59. TONNES//

OCT28/WITH GOLD DOWN $19.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 TONNES FROM THE GLD..///INVENTORY RESTS AT 925.20 TONNES

OCT 27/WITH GOLD DOWN $3.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 26/WITH GOLD UP $11.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 25/WITH GOLD UP $3.85: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 928.39 TONNES

OCT 24/WITH GOLD DOWN $1.80 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES FROM THE GLD////INVENTORY RESTS AT 928.10 TONNES

OCT 21/WITH GOLD UP $19.10: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 930.99 TONNES

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

GLD INVENTORY: 908/38 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

NOV 9/WITH SILVER DOWN 10 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV/; A WITHDRAWAL OF 3.821 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 472.108 MILLION OZ//

NOV 8/WITH SILVER UP 48 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.751 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 475.929 MILLION OZ//

NOV 7/WITH SILVER UP 12 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 4/WITH SILVER UP $1.31 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.972 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 3.WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 566,000 OZ FROM THE SLV////INVENTORY RESTS AT 482.650 MILLION OZ//

NOV 2/WITH SILVER DOWN 9 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 92,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.216 MILLION OZ//

NOV 1/WITH SILVER UP 53 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 415,000 OZ FORM THE SLV////INVENTORY RESTS AT 483.308 MILLION OZ

OCT 31: WITH SILVER FLAT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .644 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 483.723 MILLION OZ//

OCT 28/WITH SILVER DOWN 35 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.367 MILLION OZ//

OCT 27/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE S: A WITHDRAWAL OF 2.579 MILLION OZ FROMTHE SLV/////INVENTORY RESTS AT 484.091 MILLION OZ//

OCT 26/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.013 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 486.670 MILLION OZ./.

OCT 25/WITH SILVER UP 17 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.083 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.683 MILLION OZ/

OCT 24/WITH SILVER UP 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .553 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.610 MILLION OZ//

OCT 21/WITH SILVER UP 43 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .46 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 486.163MILLION OZ//

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

Gold rallied by over $50 an ounce last Friday and the rally has extended into this week with the yellow metal moving back above $1,700 an ounce. In his podcast, Peter Schiff explained why he thinks that gold has bottomed and this is a significant reversal.

Commodity prices in general have been rallying over the last several days. News that China might be close to ending its zero-COVID policies sparked the rally. Industrial metals and oil both saw big gains.

This is bad news for the Federal Reserve.

It’s going to see inflation being pushed higher even as the economy continues to soften.”

Increased Chinese demand as the country’s economy reopens could also be a problem for the Fed. The central bank focuses on fighting inflation by lowering demand. But as Peter pointed out, demand is global, not just domestic.

I always talk about how we can have higher inflation during a recession because I realize that prices are not just determined by the ability of Americans to pay, but it’s the ability of everybody all around the world to pay. Americans are competing with foreigners for the same goods. And, it’s also not simply a function of demand, but it’s a function of supply. Even if demand in America goes down, supply in America could go down even more because demand outside America goes up, and supply is diverted from the United States abroad. So, even if American consumers are buying less, there are even fewer goods available for them to buy. And so, what ends up happening is fewer goods get bought, but the ones that do get bought are bought at ever-increasing prices.”

I think as it becomes more obvious that the dollar has seen its highs and is headed lower, I think you are going to get a rush to liquidate long dollar positions. So many people have been piling into the dollar as the only safe haven, as the least-dirty shirt in the hamper, the dollar milkshake theory — whatever it is, a lot of people have been buying dollars, and they are long dollars. The assumption was that the dollar would keep on rising. But the minute that momentum is lost, there is tremendous downside as everybody looks to unwind those positions.”

Peter said another signal that the dollar has reached its high is gold has reached its low.

Of all the big moves in the market during the week, I think the most significant move was the one made by gold.”

Gold made a new 52-week low interday last Thursday (Nov. 3). But on Friday, gold rallied with the price rising by $52.

If you look at the trading pattern for gold, it was an outside reversal week, where during the week, gold took out the low from the prior week, it took out the high from the prior week, and then it closed above the prior week’s high.”

Peter called it “a very significant reversal.”

And it continued this week with gold rallying back above $1,700 an ounce on Tuesday (Nov. 8).

Silver charted a similar rally. The difference was that silver did not make a new 52-week low last week.

When you see gold making a new low, but that new low not being confirmed by silver, that is an indication of a bottom because silver is normally weaker than gold until you get to the end of the bear market, and then silver starts to have some relative strength in relation to gold.”

Peter said gold mining stocks also confirmed the bottom. As a group, miners also failed to make a 52-week low even as gold did.

What makes me more confident in this call is the fact that even though gold itself made a new 52-week low on Thursday, the gold stocks did not. And then we had the explosive move up on Friday where both the GDX and the GDXJ rose better than 10% on the day. It is very rare that you see gold stocks up 10% in a single day.”

While both $50 up-moves in the price of gold and 10% rallies in mining stocks are rare, Peter said he thinks it will become less so in the coming months.

I figure, before too long, we’re going to finally see the price of gold rally by $100 in one day.”

You can already see the demand in physical gold and silver, where demand is skyrocketing. Central bank demand is skyrocketing.”

In fact, central bank demand set a Q3 record with a huge increase in unreported buying. Many speculate that the mystery buyer was China.

That makes a lot of sense to me. I think China is really trying to stockpile its gold, especially if China is thinking of doing something, maybe making a move against Taiwan. They’re not going to do that until they’ve really shored up their gold holdings. They want to divest themselves of US dollars and US Treasuries and be loaded up with gold before they do anything that may invoke sanctions.”

Peter said it’s only a matter of time before investors realize that the price of gold is not only going to rise commensurate with the cost of producing it, but it’s going to rise more.

Because as investors lose confidence in the ability of the Fed and other central banks to rein in inflation, now they’re more motivated to hedge against inflation because they can no longer count on the central banks to protect them. They have to look for their own protection, and they can find it in gold.”

In this podcast, Peter also talks about the continued decline in tech stocks, and the decline labor force participation rate.

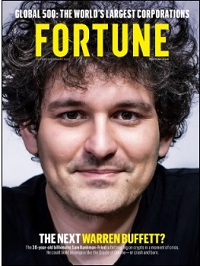

The August/September cover of Fortune Magazine raised the titillating question as to whether crypto billionaire Sam Bankman-Fried might be the next Warren Buffett – a man whose investment acumen has survived more than seven decades. Less than three months later, the public has its answer. Bankman-Fried’s crypto empire has turned to ruins in one week.

As it turns out, folks don’t have a lot of confidence in the crypto exchanges that hold their crypto. The equivalent of bank runs seen in the early 1930s, before federal deposit insurance was enacted by Congress in 1933, can wipe out a crypto exchange in a week’s time.

According to Reuters, Bankman-Fried’s crypto exchange, FTX, saw $6 billion of withdrawals in a 72-hour span through yesterday, leaving the exchange teetering amid questions about its solvency.

Changpeng (CZ) Zhao, the CEO of the competitor crypto exchange, Binance, who helped to spark the concerns about FTX, is now attempting to play the white knight and buy the troubled FTX. Or not.

According to Tweets from CZ, there are quite a few loopholes to the deal moving forward. CZ has given himself the escape routes of doing due diligence (“DD”), a “non-binding” Letter of Intent, and prominently noted in his Tweet that “Binance has the discretion to pull out from the deal at any time.”

We can see why CZ might want to buy himself some time before moving forward. According to CoinGecko, at 7:24 a.m. (ET) this morning, the FTX token, FTT, had lost 81.7 percent of its value over the span of the last seven days.

Despite all the hoopla stirred up by mainstream media about crypto being the hottest thing since sliced bread, on June 29 of this year Bank of America released its crypto survey findings, which included a stunning data point. Bank of America researchers noted that: “Ultimately, crypto assets comprise less than 1% of overall US household financial assets. The Bank of America survey suggests relatively few people view crypto assets as a reliable long-term investment.”

“Reliable” is the operative word in the above sentence. For the big picture on the reputational hits that crypto has taken this year, we offer the following 2022 articles from Wall Street On Parade:

3. Chris Powell of GATA provides to us very important physical commentaries”

end

4. OTHER PHYSICAL SILVER/GOLD COMMENTARIES

5.OTHER COMMODITIES:

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.2527

OFFSHORE YUAN: 7.2646

SHANGHAI CLOSED DOWN 16,33 PTS OR 0.53%

HANG SENG CLOSED DOWN 198.79 OR 1.20%

2. Nikkei closed DOWN 155.68 PTS OR 0.56%

3. Europe stocks SO FAR: MOSTLY RED

USA dollar INDEX UP TO 109.84/Euro FALLS TO 1.0043

3b Japan 10 YR bond yield: FALLS TO. +.242!!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 145,70/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.222%***/Italian 10 Yr bond yield FALLS to 4.328%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.266%…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.654//

3j Gold at $1707.75//silver at: 21.27 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 14/100 roubles/dollar; ROUBLE AT 61.12//

3m oil into the 88 dollar handle for WTI and 93 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 146.42DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9819–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9368well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.128% UP 0 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 4.263% UP 0 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,60…GETTTING DANGEROUS

GREAT BRITAIN/10 YEAR YIELD: 3.5515%

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Stock Rally Fizzles As Red Wave Downgraded To Red Ripple

WEDNESDAY, NOV 09, 2022 – 07:52 AM

Futures and yields are flat, both recovering from a dip earlier in the session, as investors kept an eye on midterm election results ahead of key inflation data later in the week. To the disappointment of bulls, a Red Wave failed to emerge in Congress as voters delivered a mixed verdict in elections shaped by inflation and split around social issues, with Republicans headed toward control of the US House, but by smaller margins than forecast, while the Senate majority remains a toss-up.

In the House, official results have Republicans on 196 and Democrats on 168. Projections from the New York Times (seats either already won by a party or projected to win) put the Republicans on 219 and Democrats on 207 with 9 seats viewed as “tossups”. In the Senate, official results have Republicans on 47 and Democrats on 48. Democrats won in PA (where a brain-damaged Fetterman managed to flip a critical seat which even liberal pollsters said was set to go to republican Challenger Dr. Oz ) and NH; GOP is leading in NV and WI; Democrats leading in AZ and GA. Three key battleground states which are yet to be called are Arizona, Nevada and Georgia. The Georgia seat could end up having to be decided via an election run-off which would be held on December 6th. As such, the outcome of the election might not be known for weeks.

“It is clear that any Republican majority is likely to be extremely narrow. From a market perspective, that would certainly be attractive,” said DWS Global Chief Investment Officer Bjoern Jesch. “On the one hand, this would remove corporate tax increases or other spending packages that would have threatened both houses if the Democrats marched through. On the other hand, the Republicans would probably be too divided to set their own strong accents in legislation.”

Back to markets, where Nasdaq 100 futures were down -0.5%, while S&P 500 futs slipped 0.4% at 7:30 am ET after fluctuating between gains and losses one day after stocks capped a three-day rally.

In premarket trading, News Corp. and Disney both tumbled at least 8% after posting disappointing results. A selloff in cryptocurrencies deepened, sending Bitcoin toward the biggest four-day slump since June. Oil slid on the now daily sluggish demand outlook from China. The dollar rose while yields were flat. Affirm Holdings shares tumbled 16% as analysts said the buy-now-pay-later firm’s guidance cut and ongoing credit deterioration overshadowed a solid quarter. Meta Platforms Inc. gained after confirming job cuts of about 13% and let more than 11,000 of employees go. Here are some of the biggest US movers today:

Amyris shares slump 22% in US premarket trading after the chemical products distributor reported third-quarter revenue that missed the average analyst estimate. Piper Sandler said more clarity was given on the outlook, but thought there was still some uncertainty.

Axon Enterprise reported strong quarterly results and the outlook for the taser and body cameras maker remains strong, analysts say. Axon shares rose 7.7% in extended trading following the results.

CarGurus shares drop 22% in premarket trading after the car retailer reported weak 3Q results and gave disappointing guidance, with analysts unsure how long it will take the firm to fix the challenges it faces.

Keep an eye on News Corp (NWSA US) after the company reported first-quarter revenue that came ahead of Guggenheim’s estimates, though the broker notes management’s comments on headwinds stemming from factors such as exchange rates persisting into the next quarter.

Kroger stock gains 1.3% in premarket trading as Evercore ISI upgraded it to outperform, saying that risk/reward appears favorable with food inflation likely to stay higher for longer.

Shares in cryptocurrency- exposed companies dropped in US premarket trading as digital currencies extended their losses, with Binance’s potential takeover of troubled rival exchange FTX stoking worries over the fragility of the industry.Riot Blockchain (RIOT US) -3.8%, Marathon Digital (MARA US) -5%, MicroStrategy (MSTR US) -7%, Coinbase (COIN US) -5%

Tesla shares rise as much as 1.9% in US premarket trading following three days of losses and lowest level since June 2021; CEO Elon Musk sold $3.95 billion of shares in the electric-vehicle maker.

Upstart slumps about 26% in US premarket trading and is set to hit the lowest level since its IPO in 2020. The AI lending platform’s 3Q results are well below expectations as it deals with significant pressure on its core business from a weakening macro backdrop, analysts say.

Investors had hoped for a Republican “Red Wave” in Congress, with the best outcome seen as GOP control of both the House of Representatives and Senate. Optimism for shares has been helped by a history of robust performance following midterm results. Stocks have tended to flourish during times when government is constrained and polls suggest Republicans could make gains, placing a check on Democratic policies. But voters – and the USPS – delivered a mixed verdict, with Republicans heading for control of the House by smaller margins than forecast and the race for Senate still wide open. The final outcome may not be known for days or even weeks if the results are as close as polls have suggested and if losers challenge results.

“The Republican aim of controlling both houses hangs by a thread,” Chris Beauchamp, the chief markets analyst at IG Group in London, wrote in a note. “A divided House might mean the partisan battles over spending and the debt ceiling are not quite as dramatic or vitriolic, but this is unlikely to brighten the policy outlook markedly. Instead, the focus will likely return to the Federal Reserve and the US economy.”

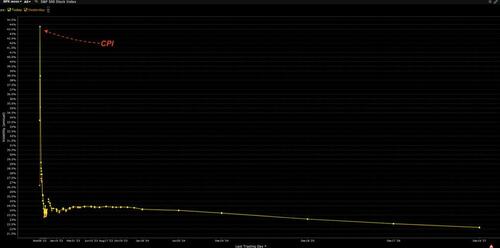

That left Thursday’s inflation report the next catalyst for markets. Economists are expecting the figures to show consumer prices cooled slightly compared with the previous month. The data could provide crucial clues on how the Federal Reserve is likely to proceed with tightening monetary policy.

“Tension is high and investors won’t want to be burnt by jumping the wrong way ahead of that inflation data, because in the past expectation has proved a little off the mark,” said Danni Hewson, a financial analyst at AJ Bell.

In Europe, the equity benchmark fell for the first time in four days, dragged by tech, real estate, travel- and automotive-industry shares. Euro Stoxx 50 falls 0.7%. IBEX is flat but outperforms peers, DAX lags, dropping 0.8%. Here are some of the biggest European movers today:

Vantage Towers shares jump as much as 11% after Vodafone said in a statement that it will deconsolidate its 81.7% interest in the tower business by creating a joint venture with KKR and Global Infrastructure Partners to hold the stake.

Smiths Group rises as much as 5.4%, hitting the highest since Feb. 2020, with analysts saying the industrial group delivered a strong start to its fiscal year.

Recordati shares rise as much as 4.8%, hitting the highest since Sept. 19 and extending gains after its results in the prior session, as Banca Akros upgrades its rating on the drugmaker.

Scor shares reversed earlier declines on the back of its third quarterly loss in a row and climbed as much as 4.5%, as analysts focused on their deep value and noted that a cost- cutting plan marked a pivotal moment for the French reinsurer.

Commerzbank shares decline despite the German lender delivering a beat on its quarterly earnings, with Deutsche Bank flagging what looks like conservative guidance for 2024. Shares fall as much as 7.6%.

Evotec falls as much as 12%, the most in three months, after analysts said the German biotech missed quarterly estimates, with investments in the Just-Evotec Biologics arm hurting profits.

ITV shares drop as much as 6.6% after the broadcaster said rising costs will be an issue in 2023. Barclays notes this is the first time ITV has mentioned that inflation may hit its costs and earnings. While 3Q results largely met expectations, analysts say the 4Q advertising outlook fell short amid growing economic uncertainty.

Marks & Spencer falls as much as 7%, the most since Sep. 29, after the UK retailer’s trading update is seen as offering little reassurance in the face of demand headwinds and cost inflation.

Earlier in the session, Asian shares were little changed after three straight gains of more than 1%, as a rally in tech stocks offset losses in Chinese shares and investor worries about US midterm election results. The MSCI Asia Pacific Index was up 0.01% as of 6:04 p.m. in Singapore, with chipmakers TSMC and Samsung Electronics among the biggest boosters, while Chinese internet names fell amid concerns over Singles Day sales. With Republicans headed toward control over the US House of Representatives — albeit by a smaller margin than forecast –some investors say it portends difficulty in passing legislation during a trying economic period, while others see political gridlock as preserving status quo. “This could be a dysfunctional political situation at a time of economic crisis,” said Gary Dugan, chief executive officer at the Global CIO Office. However, there may be some positive impact on Asia stocks if the dollar tops out, he added.

Meanwhile, tech shares extended a rebound on cheaper valuations, boosting benchmarks in Taiwan and South Korea. Key gauges in China and Hong Kong, however, dropped for a second straight day after a recent rebound. The decliners were influenced as Chinese producer prices fell into deflation for the first time in nearly two years amid lockdowns and new Covid cases in Beijing jumped. While Asia’s benchmark index has rebounded more than 7% from a recent trough, all eyes are on US consumer price inflation data due Thursday for a sense of the Federal Reserve’s next policy step. Growing lockdowns in China are also weighing on sentiment. “We don’t think the worst is over for Asian equities even though the markets have bounced back about 7% from the late October bottom and flows have picked up,” said Manishi Raychaudhuri, a strategist at BNP Paribas. “The Fed’s hawkish stance on inflation shall sustain till there are clear signs of core inflation peaking out.”

Japanese stocks fells: the Topix dropped 0.4% to 1,949.49 at the 3 p.m. close in Tokyo, while the Nikkei 225 declined 0.6% to 27,716.43. Nintendo contributed the most to the Topix’s loss, decreasing 7.1%. Out of 2,165 stocks in the index, 1,020 rose and 1,022 fell, while 123 were unchanged.

In India, stocks fell from their near-record levels as investors booked profits in recent outperformers such as ICICI Bank and Hindustan Unilever. Stocks across Asia were mixed as investors await midterm poll results in the US. The S&P BSE Sensex fell 0.3% to 61,033.55 in Mumbai, while the NSE Nifty 50 Index eased by an equal margin. Both indexes still trade about 1% short of their record levels seen in October last year. Fifteen of BSE Ltd.’s 19 sector sub-gauges dropped, led by consumer durable companies as trading resumed after a holiday on Tuesday. Tata Motors, the owner of Jaguar Land Rover, reported smaller-than-expected loss for September quarter, adding to Indian companies’ stronger show for the earnings season. Of the 44 Nifty firms that have announced results so far, 31 have met or beaten analysts’ estimates, while 10 missed. ICICI Bank contributed the most to the Sensex’s decline, decreasing 0.6%. Out of 30 shares in the index, 8 rose and 22 fell.

Australian stocks rallied for a 4th day: the S&P/ASX 200 index rose 0.6% to close at 6,999.30, boosted by gains in mining and real estate shares. A gauge of mining shares hit the highest since Aug. 26 after metal prices increased. Shares of gold miners, including St Barbara, were the benchmark’s best performers after the metal advanced on a slide in the US dollar. In New Zealand, the S&P/NZX 50 index was little changed at 11,143.48.

In FX, the Bloomberg Dollar Index rebounded and the greenback rose versus all of its Group-of-10 peers as risk assets turned lower. One-day hedging costs rallied across the major currencies, modestly higher than what the roll suggested, as focus shifts to Thursday’s US inflation report. Risk sensitive currencies, such as the kiwi and pound fell by around 1% against the greenback. The euro fell, but remained above parity.

The pound plunged by as much as 1.1% after three days of gains, while gilts twist flattened. Bank of England monetary policy committee members Jon Cunliffe and Jonathan Haskel are due to speak later, a day after Chief Economist Huw Pill suggested that the stimulus program through the pandemic was a mistake and contributed to inflation

Australian sovereign bonds extended opening gains after data showed that China’s producer prices fell into deflation for the first time in nearly two years. The producer price index declined 1.3% in October from a year earlier after gaining 0.9% the previous month

Japanese government bonds rose after a solid sale of 30-year bonds alleviated concerns about demand for super-long debt. The yen was steady

In rates, Treasuries were mixed with the curve flatter, pivoting around a little-changed 10-year sector. Bunds outperform, bull-flattening sharply, while stocks hover near top of Tuesday’s range. US yields richer by nearly 2bp across long-end of the curve and cheaper by ~1bp across front-end, leaving 2s10s, 5s30s spreads flatter by 1bp and 2bp on the day, while 10-year at around 4.125% is little changed from Tuesday’s close. Bunds outperform by 4.5bp in the 10-year sector, gilts by 1.2bp. Focal points of US session focus include 10-year note auction and a couple of Fed speakers ahead of Thursday’s inflation data: the US auction cycle resumes with $35b 10-year at 1pm, followed by $21b 30-year Thursday; Tuesday’s 3-year note sale was strong, drawing a yield 1.2bp below the WI at the bidding deadline. Two-year German and Italian government bond yields inched up while falling further out. One trader has placed a large bet using options on German 10-year futures, targeting the yield to fall to 1.55% for maximum profit, down from about 2.25% currently

In commodities, WTI drifts lower to trade near $88. WTI and Brent futures are softer intraday as the Dollar claws back some recently lost ground and sentiment remain tilted to the downside, while China’s COVID situation remains an overhang for the complex. Spot gold fell roughly $7 to trade near $1,705/oz, swayed from gains to losses after testing resistance at its 100 DMA (1,715/oz) in early European hours, before a turn in risk sentiment spurred the Dollar and hit the yellow metal. Base metals are pressured by the downbeat risk tone and the firmer Dollar, but 3M LME copper holds onto a USD 8,000/t handle after testing USD 8,100/t to the upside overnight.

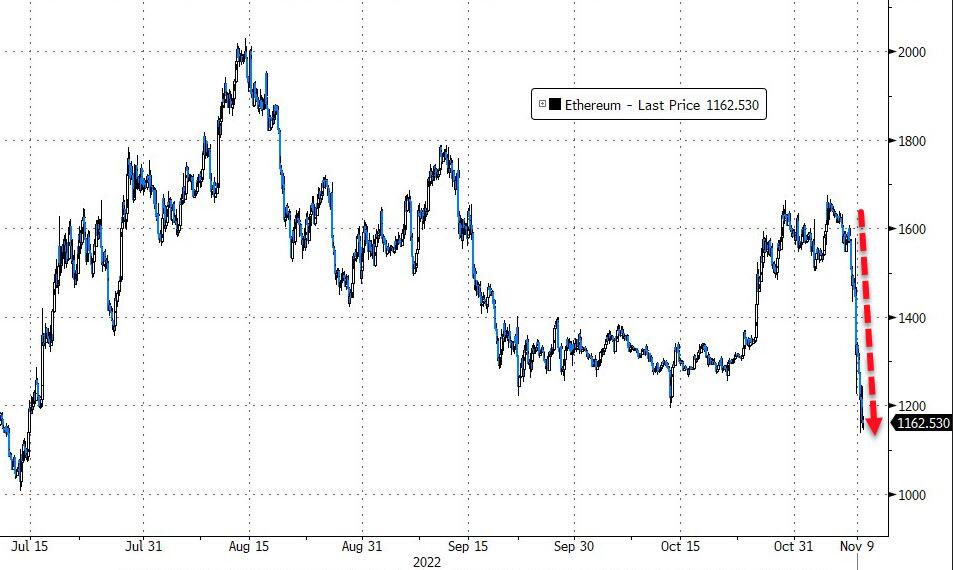

Cryptocurrencies slipped further as Binance’s potential takeover of embattled rival exchange FTX.com highlighted how strains in the digital-asset industry are buffeting some of its top players. Bitcoin traded as much as 7.7% lower.

To the day ahead now, and although investors will be digesting the midterm results, there are a few central bank speakers to look out for as well, including the Fed’s Williams and Barkin, the ECB’s Elderson, and the BoE’s Haskel and Cunliffe.

Market Snapshot

S&P 500 futures down 0.4% to 3,820.50

STOXX Europe 600 down 0.8% to 418.34

MXAP up 0.2% to 144.17

MXAPJ up 0.5% to 464.43

Nikkei down 0.6% to 27,716.43

Topix down 0.4% to 1,949.49

Hang Seng Index down 1.2% to 16,358.52

Shanghai Composite down 0.5% to 3,048.17

Sensex down 0.2% to 61,067.52

Australia S&P/ASX 200 up 0.6% to 6,999.30

Kospi up 1.1% to 2,424.41

German 10Y yield down 0.9% to 2.26%

Euro down 0.2% tp $1.0051

Brent Futures down 0.7% to $94.71/bbl

Gold spot down 0.3% to $1,707.98

U.S. Dollar Index up 0.1% to 109.79

Top Overnight News from Bloomberg

US voters delivered a mixed verdict in elections shaped by inflation and splits around social issues, with Republicans headed toward control of the US House, but by smaller margins than forecast

Consumers’ expectations for inflation over the next 12 months rose to 5.1% in September from 5% in August, European Central Bank says in statement summarizing the results of its monthly survey

Euro-area wage growth has jumped, with most occupations seeing raises of at least 3%, according to an analysis of job ads that also suggests the pace of increases may be flattening

Two key indicators of Chinese interbank borrowing costs have hit a three-month high, as the nation’s central bank faces a crucial decision on what to do with a massive amount of policy loans due next week

Hungary’s annual price growth increased by a full percentage point in October to 21.1%, data published Wednesday showed. The nation is closing in on the three Baltic states that have the fastest inflation in the EU

A more detailed summary of global markets courtesy of Newsquawk

Asia-Pac stocks traded cautiously and US equity futures were indecisive as attention focused on the trickling results from the US Midterm Elections where a red wave has so far not yet materialised although Republicans are in a strong position to take control of the House, while the Senate race is still widely viewed as a toss-up. ASX 200 was led higher by strength in the mining-related sectors although upside was capped as financials are subdued following results from National Australia Bank which posted an increase in FY profit but warned of a significant slowdown in lending growth for the current fiscal year. Nikkei 225 faded its initial gains with price action lacklustre amid a slew of earnings and despite Japan’s Cabinet approving a JPY 29.1tln extra budget to fund the stimulus package. Hang Seng and Shanghai Comp swung between gains and losses with early strength in property names after China’s state planner asked large banks to step up lending for manufacturing infrastructure and developers, with China to provide initial support of around CNY 250bln in bond financing to private firms, although COVID-related headwinds persisted following a further increase in China’s daily infections and participants also reflected on the mixed-to-soft inflation data. Chinese developers jumped the most in eight months as a regulator expanded financing support for the sector.

Top Asian News

China’s Guangzhou reportedly locked down a second district due to coronavirus. However, it was separately reported that China lifted the lockdown in the area around Foxconn’s Apple (AAPL) iPhone plant as planned, according to Bloomberg.

China’s Guangzhou locks down another district amid COVID, according to Bloomberg.

China reported 1,346 (prev. 890) new coronavirus cases in the mainland for November 8th, 1,294 (prev. 843) new local cases and 6,989 (prev. 6,801) new asymptomatic cases, according to Reuters.

US President Biden will highlight a commitment to rules-based international order in the South China Sea during the ASEAN summit and will talk about the need for peace and stability throughout the Indo-Pacific region and across the Taiwan Strait, according to a senior administration official cited by Reuters.

RBA’s Bullock reiterated that further rate hikes will be needed. Wage growth is a bit stronger than thought three months ago. Good reason to think approaching peak of the inflation cycle, via Reuters.

In Europe, major bourses hold a downside bias after seeing some choppiness at the cash open and following a somewhat mixed APAC handover. Sectors are all in the red with a clear defensive bias as Telecoms, Utilities, Healthcare, Food & Beverages post the shallowest losses, whilst Tech, Travel & Leisure, Real Estate and Retail reside at the other end of the spectrum. US equity futures traded sideways on either side of breakeven overnight and in early European hours but have since drifted under the overnight lows.

Top European News

UK PM Sunak could raise the top rate of income tax, according to The Telegraph. Options being discussed include raising the 45% top rate, or lowering the GBP 150k annual income threshold at which it kicks in.

UK Chancellor Hunt is set to scrap former PM Truss’ plan for investment zones, according to FT.

EU is mulling Eurobonds for Ukraine fund, Politico reported – will propose a new EU instrument to finance EUR 18bln.

ECB Says 12-Month Consumer Inflation Expectations Rose Slightly

Adidas Cuts Margin Forecast After Ending Yeezy Partnership

M&S Falls Amid Concerns Over Demand, Cost Inflation For Retail

Top Sunak Ally Williamson Resigns Amid Bullying Allegations

Commerzbank’s New Targets Disappoint Investors as Charges Mount

FX

DXY attempted to stop the rot and nurse some losses awaiting the remaining and potentially game-changing Midterm Election results, with the index now on either side of 110.00.

The NZD and GBP underperform and more ground than other majors as the Buck bounced, with nothing obvious in terms of negative NZ or UK factors.

Traditional havens JPY and CHF are off best levels, but retained a safety premium as the rout in crypto currencies raged on and the ripples reverberated across to stocks.

Fixed Income

US Treasuries are braced for the long bond sale that wraps up this week’s rather mixed Quarterly Refunding.

Gilts remain in the green having digested an average Green offering.

Bunds saw a lack of positive reaction despite a very well received 2032 German auction.

Commodities

WTI and Brent futures are softer intraday as the Dollar claws back some recently lost ground and sentiment remain tilted to the downside, whilst China’s COVID situation remains an overhang for the complex.

US Energy Inventory Data (bbls): Crude +5.6mln (exp. +1.4mln), Cushing -1.8mln, Gasoline +2.6mln (exp. -1.1mln), and Distillate -1.8mln (exp. -0.9mln).

IEA’s Birol said OPEC+ might need to rethink its output cut decision, according to Bloomberg

Spot gold swayed from gains to losses after testing resistance at its 100 DMA (1,715/oz) in early European hours, before a turn in risk sentiment spurred the Dollar and hit the yellow metal

Base metals are pressured by the downbeat risk tone and the firmer Dollar, but 3M LME copper holds onto a USD 8,000/t handle after testing USD 8,100/t to the upside overnight.

Geopolitics

North Korea fired a missile, according to South Korean military; could be a ballistic missile, according to Japanese Coast Guard; projectile has fallen outside of Japan’s EEZ.

German cabinet has agreed to block the prospective Chinese takeover of Elmos chip factory and ERS electronics, according to government sources cited by Reuters.

US Event Calendar

07:00: Nov. MBA Mortgage Applications, prior -0.5%

10:00: Sept. Wholesale Trade Sales MoM, est. 0.5%, prior 0.1%

10:00: Sept. Wholesale Inventories MoM, est. 0.8%, prior 0.8%

Central Banks

03:00: Fed’s Williams Discuss Risk and Uncertainty at Event in Zurich

11:00: Fed’s Barkin Discusses the Economic Outlook

20:00: Fed’s Kashkari Discusses Inflation and the Economy

DB’s Jim Reid concludes the overnight wrap

As has been anticipated, it will take a few days to unpack the full results of the US midterms. What is clear at this hour though is that neither major party is running away with the election in a ‘wave’ and it appears that Republicans are still on track to achieve a majority in the House of Representatives, a combo that should put a pin in any new fiscal stimulus for the next few years. The New York Times model is currently showing that the Senate will likely finish with 50 seats each. So overall maybe Democrats slightly outperforming but it’s not too far away from expectations. The mix also seems to not be surprising markets too much, as S&P 500 futures (-0.07%) are oscillating between gains and losses as we go to press. Our US team will be hosting a webinar later today to unpack the implications with the link to register here.

As we awaited the results of the midterm elections, risk assets continued to put in a decent performance yesterday, with the S&P 500 (+0.56%) advancing for a 3rd consecutive session. A reminder that if history’s any guide that could prove to be just the start however, since in all 19 post-war midterm elections, the S&P 500 has closed above its levels on the day of the election after a year. We highlighted this a couple of months ago and in yesterday’s CoTD we showed how the 3 quarters from midterms have been the top 3 quarters for the S&P 500 since 1949 across the 4 year presidential cycle. However as I’ve eluded for a while, although I’ve thought midterms would be a short-term positive catalyst I suspect we won’t see this record spell stretch into a 20th successive positive outcome 12 months on. I’m going to take a stab at why we should ignore history today in my CoTD.

Back to yesterday and gains were pretty broad-based for a relatively modest index-level increase, with over 70% of the index moving higher on the day, and only the consumer discretionary sector in the red (-0.30%) on the day thanks to Tesla’s (-2.93%) decline. The Nasdaq flitted around zero, trading as much as +1.70% higher and -0.87% lower before splitting the difference to finish up +0.49%. After the close, Mark Zuckerberg confirmed that layoffs would start at Meta tomorrow, which won’t help tech sentiment. The sentiment wasn’t any better following Disney’s after-hours earnings, which came in below consensus and had the company ready to find “meaningful efficiencies” in light of rising costs. Disney’s shares were -6.83% lower after the close.

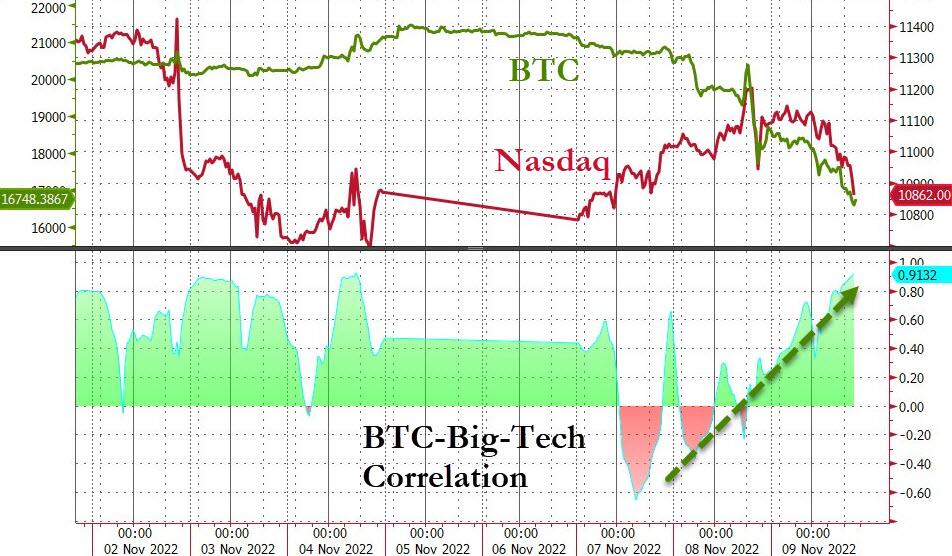

The S&P 500 had a bit of a wild swing after Europe went home moving from +1.35% to -0.55% in the space of an hour before closing higher (+0.56%) as Bitcoin (long time no mention) plunged to $17,187 having been as high as $20,655 as European equity markets closed. It bounced back into the close and is at similar levels as we type this morning at $18,430. Crypto exchange FTX.com had been suffering from a liquidity crunch before rival Binance agreed to buy it yesterday and the associated story created a fair amount of noise, some of it creeping into equities. This morning in Asia there are a few concerns the deal isn’t binding so one to keep an eye on. Before the late US vol, the STOXX 600 (+0.78%) hit its highest level in nearly two months, whilst the DAX (+1.15%) hit its highest level in nearly three months.

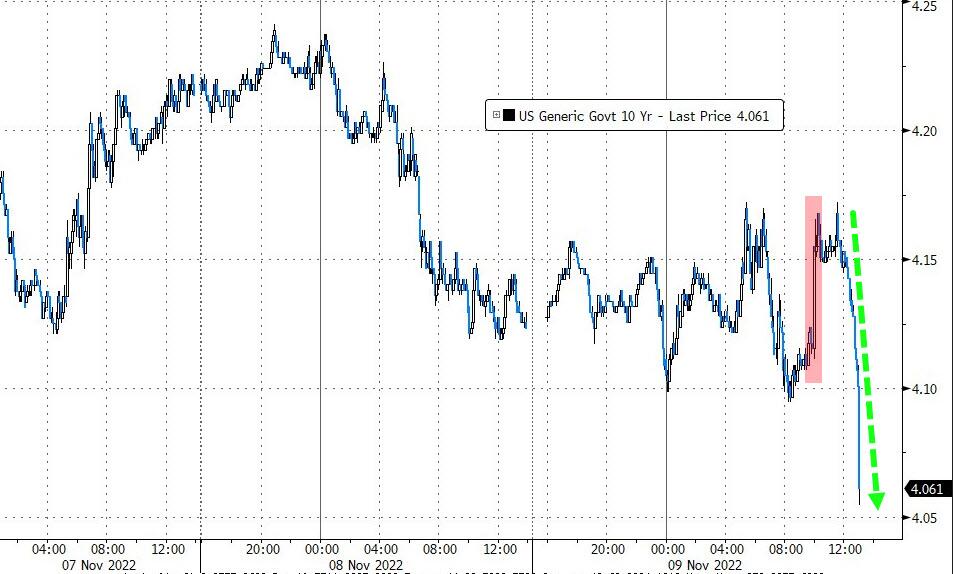

For sovereign bonds, the main focus is still on tomorrow’s US CPI report, but there was a decent rally ahead of that as investors modestly dialled back their expectations of future central bank rate hikes. For instance, the futures-implied rate for the Fed in December 2023 came down -6.1bps to 4.80%, having traded as high as 4.88% earlier in the European morning. In turn, that prompted a rally in Treasuries across the curve, with the 10yr yield down -9.0bps on the day to 4.12%, with roughly half of the decline in real yields, which fell -5.2bps. In the meantime, the 2s10s yield curve flattened -1.7bps to -53.1bps, remaining just above its post-1982 closing low of -57.3bps from last week. Meanwhile, in Asia, 2 and 10yr yields are back up a basis point.

Over in Europe, there was a similar sovereign bond rally, with yields on 10yr bunds (-6.3bps), OATs (-6.6bps) and gilts (-9.0bps) all lower on the day. At the front end however, UK gilts underperformed, with the 2yr yield up +5.3bps after BoE chief economist Pill said that “there is more to come” on rates following their 75bp hike last week. Overnight index swaps are currently pricing a nearly even split between a 50bps or 75bps hike at the next meeting in December.

This morning in Asia, equities are mostly trading lower led by the Hang Seng (-1.52%) with the CSI (-0.75%), the Shanghai Composite (-0.35%) and the Nikkei (-0.54%) all trading in negative territory. Elsewhere, the KOSPI (+1.00%) is bucking the trend.

We’ve had softer price data coming out of China as the nation’s producer price index (-1.3% y/y) in October fell for the first time in two years, down from +0.9% growth in September as strict Covid restrictions coupled with a sluggish property sector amid global recession risks dented the economy. Meanwhile, consumer inflation in October (+2.1% y/y) moderated from September’s 29-month high of +2.8% (v/s +2.4% expected) pointing towards underlying domestic price pressures remaining modest.

Staying on China, the Chinese yuan extended its decline for a third day, weakening past the 7.25 level against the dollar after the data. The subdued inflation figures suggests that the PBOC policy divergence against its global peers will continue.

There wasn’t much in the way of data releases yesterday, with Euro Area retail sales growing by +0.4% in September, in line with expectations. That said, there was a positive revision to August which showed that retail sales were unchanged, as opposed to the -0.3% contraction previously released. Otherwise in the US, the NFIB’s small business optimism index for October fell for the first time since June, coming in at 91.3 (vs. 91.4 expected).

To the day ahead now, and although investors will be digesting the midterm results, there are a few central bank speakers to look out for as well, including the Fed’s Williams and Barkin, the ECB’s Elderson, and the BoE’s Haskel and Cunliffe.

end

AND NOW NEWSQUAWK (EUROPE/REPORT)

Downside bias across stocks while crypto continues feeling the pain – Newsquawk US Market Open

WEDNESDAY, NOV 09, 2022 – 06:44 AM

Major bourses in Europe hold a downside bias after seeing some choppiness at the cash open and following a mixed APAC handover; US futures are also softer

US Midterm Elections are mostly as expected so far with GOP’s leading the House while the Senate is seen as a toss-up; there was very little market reaction in response to the mid-terms overnight

DXY attempts to nurse some recent losses and trades on either side of 110.00 whilst the GBP and NZD underperform

Crypto markets remain on the backfoot; Bitcoin briefly dipped under yesterday’s low and Ethereum fell under USD 1,200

Looking ahead, highlights include US Midterm Election Results, Speeches from Fed’s Barkin, ECB’s Elderson, BoE’s Haskel, Supply from US

In the House, official results have Republicans on 196 and Democrats on 168. Projections from the New York Times (seats either already won by a party or projected to win) put the Republicans on 219 and Democrats on 207 with 9 seats viewed as “tossups”.

In the Senate, official results have Republicans on 47 and Democrats on 48. Three key battleground states which are yet to be called are Arizona, Nevada and Georgia. The Georgia seat could end up having to be decided via an election run-off which would be held on December 6th. As such, the outcome of the election might not be known for weeks.

Major bourses hold a downside bias after seeing some choppiness at the cash open and following a somewhat mixed APAC handover.

Sectors are all in the red with a clear defensive bias as Telecoms, Utilities, Healthcare, Food & Beverages post the shallowest losses, whilst Tech, Travel & Leisure, Real Estate and Retail reside at the other end of the spectrum.

US equity futures traded sideways on either side of breakeven overnight and in early European hours but have since drifted under the overnight lows.

DXY attempted to stop the rot and nurse some losses awaiting the remaining and potentially game-changing Midterm Election results, with the index now on either side of 110.00.

The NZD and GBP underperform and more ground than other majors as the Buck bounced, with nothing obvious in terms of negative NZ or UK factors.

Traditional havens JPY and CHF are off best levels, but retained a safety premium as the rout in crypto currencies raged on and the ripples reverberated across to stocks.

WTI and Brent futures are softer intraday as the Dollar claws back some recently lost ground and sentiment remain tilted to the downside, whilst China’s COVID situation remains an overhang for the complex.

US Energy Inventory Data (bbls): Crude +5.6mln (exp. +1.4mln), Cushing -1.8mln, Gasoline +2.6mln (exp. -1.1mln), and Distillate -1.8mln (exp. -0.9mln).

IEA’s Birol said OPEC+ might need to rethink its output cut decision, according to Bloomberg

Spot gold swayed from gains to losses after testing resistance at its 100 DMA (1,715/oz) in early European hours, before a turn in risk sentiment spurred the Dollar and hit the yellow metal

Base metals are pressured by the downbeat risk tone and the firmer Dollar, but 3M LME copper holds onto a USD 8,000/t handle after testing USD 8,100/t to the upside overnight.

UK PM Sunak could raise the top rate of income tax, according to The Telegraph. Options being discussed include raising the 45% top rate, or lowering the GBP 150k annual income threshold at which it kicks in.

UK Chancellor Hunt is set to scrap former PM Truss’ plan for investment zones, according to FT.

EU is mulling Eurobonds for Ukraine fund, Politico reported – will propose a new EU instrument to finance EUR 18bln.

NOTABLE US HEADLINE

Fed’s Williams (voter) notes that stable long-term inflation expectations are good news, and is surprised by how much of the public expects deflation, according to Reuters.

Elon Musk reports the sale of Tesla (TSLA) shares in a filing; sold at least 19.5mln shares worth USD 3.5bln since Friday. TSLA +0.8% pre-market

CRYPTO

Bitcoin briefly dipped under yesterday’s low of USD 17,500 before finding support at USD 17,250 while Ethereum fell under USD 1,200.

GEOPOLITICS

North Korea fired a missile, according to South Korean military; could be a ballistic missile, according to Japanese Coast Guard; projectile has fallen outside of Japan’s EEZ.

German cabinet has agreed to block the prospective Chinese takeover of Elmos chip factory and ERS electronics, according to government sources cited by Reuters.

APAC TRADE

EQUITIES

APAC stocks traded cautiously and US equity futures were indecisive as attention centred on the trickling results from the US Midterm Elections where a red wave has so far not yet materialised although Republicans are in a strong position to take control of the House, while the Senate race is still widely viewed as a toss-up.

ASX 200 was led higher by strength in the mining-related sectors although upside was capped as financials are subdued following results from National Australia Bank which posted an increase in FY profit but warned of a significant slowdown in lending growth for the current fiscal year.

Nikkei 225 faded its initial gains with price action lacklustre amid a slew of earnings and despite Japan’s Cabinet approving a JPY 29.1tln extra budget to fund the stimulus package.

Hang Seng and Shanghai Comp swung between gains and losses with early strength in property names after China’s state planner asked large banks to step up lending for manufacturing infrastructure and developers, with China to provide initial support of around CNY 250bln in bond financing to private firms, although COVID-related headwinds persisted following a further increase in China’s daily infections and participants also reflected on the mixed-to-soft inflation data.

NOTABLE ASIA-PAC HEADLINES

China’s Guangzhou reportedly locked down a second district due to coronavirus. However, it was separately reported that China lifted the lockdown in the area around Foxconn’s Apple (AAPL) iPhone plant as planned, according to Bloomberg.

hina’s Guangzhou locks down another district amid COVID, according to Bloomberg.

China reported 1,346 (prev. 890) new coronavirus cases in the mainland for November 8th, 1,294 (prev. 843) new local cases and 6,989 (prev. 6,801) new asymptomatic cases, according to Reuters.

US President Biden will highlight a commitment to rules-based international order in the South China Sea during the ASEAN summit and will talk about the need for peace and stability throughout the Indo-Pacific region and across the Taiwan Strait, according to a senior administration official cited by Reuters.

RBA’s Bullock reiterated that further rate hikes will be needed. Wage growth is a bit stronger than thought three months ago. Good reason to think approaching peak of the inflation cycle, via Reuters.

DATA RECAP

Chinese CPI MM * (Oct) 0.1% vs. Exp. 0.3% (Prev. 0.3%)

Chinese PPI YY * (Oct) -1.3% vs. Exp. -1.5% (Prev. 0.9%)

Chinese CPI YY * (Oct) 2.1% vs. Exp. 2.4% (Prev. 2.8%)

Australian Building Approvals MM (Sep F) -5.8% (Prev. 23.1%)

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED DOWN 16.33 PTS OR 0.53% //Hang Seng CLOSED DOWN 198.79 OR 1.20% /The Nikkei closed DOWN 155.68 OR 0.56% //Australia’s all ordinaires CLOSED UP 0.52% /Chinese yuan (ONSHORE) closed DOWN TO 7.2527 //OFFSHORE CHINESE YUAN DOWN 7.2646// /Oil DOWN TO 88.06 dollars per barrel for WTI and BRENT AT 93.68 / Stocks in Europe OPENED MOSTLY RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

2 a./NORTH KOREA/ SOUTH KOREA/

///NORTH KOREA/SOUTH KOREA/

end

2B JAPAN

JAPAN

END

3c CHINA

CHINA

4.EUROPEAN AFFAIRS//UK AFFAIRS

UK

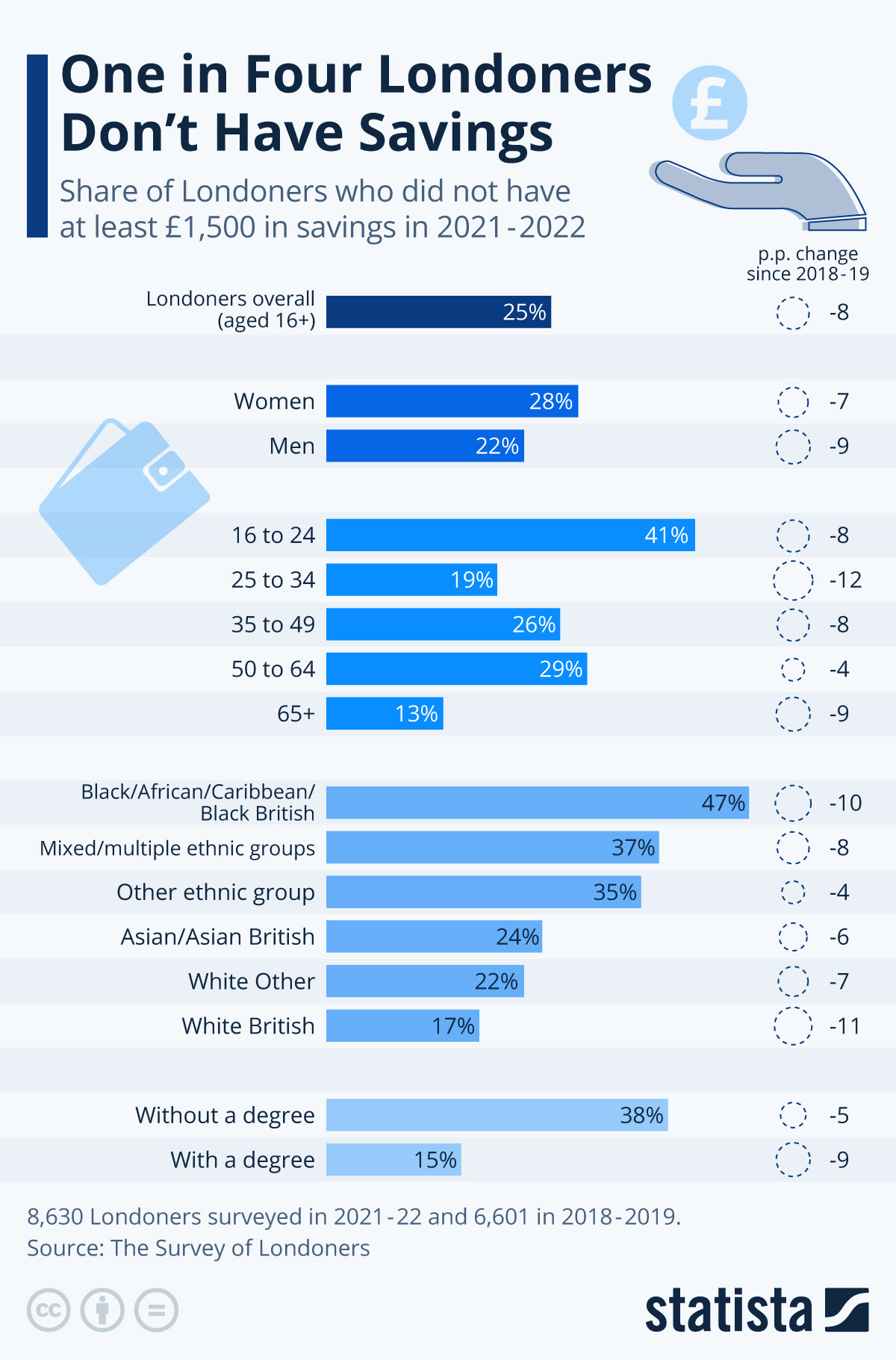

One in four Londoners do not have savings

(zerohedge)

One In Four Londoners Don’t Have Savings

WEDNESDAY, NOV 09, 2022 – 04:15 AM

As many as one in four Londoners did not own savings of at least £1,500 right before the full effects of the cost-of-living crisis began to set in, according to data from the 2022 Survey of Londoners.

The following chart, from Statista’s Anna Fleck, provides details on disparities that already existed and insight on which groups may be more vulnerable as a result now.