November 10, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSE: UP $15.25 to $1766.15

SILVER PRICE CLOSE: DOWN $0.02 to $21.61

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1766.75

Silver ACCESS CLOSE: 21.64

New: early yesterday morning//

Bitcoin morning price: $17,400 DOWN 9

Bitcoin: afternoon price: $16,726 UP 682

Platinum price closing DOWN $15.30 AT $1027.90

Palladium price; closing UP $66.10 at $2037.70

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: 2342.74 DOLLARS UP 6.79 CDN DOLLARS PER OZ

BRITISH GOLD: 1491.80 POUNDS PER OZ DOWN 6.46 POUNDS PER OZ

EURO GOLD: 1705,68 EUROS PER OZ DOWN 13.50 EUROS PER OZ.

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: NOVEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,750.300000000 USD

INTENT DATE: 11/10/2022 DELIVERY DATE: 11/14/2022

FIRM ORG FIRM NAME ISSUED STOPPED

132 C SG AMERICAS 12

190 H BMO CAPITAL 37

323 C HSBC 22

435 H SCOTIA CAPITAL 120

624 H BOFA SECURITIES 346

661 C JP MORGAN 71 225

732 C RBC CAP MARKETS 3

737 C ADVANTAGE 42 74

800 C MAREX SPEC 7 10

880 C CITIGROUP 24

880 H CITIGROUP 175

905 C ADM 4

TOTAL: 586 586

JPMORGAN STOPPED 225/586

GOLD: NUMBER OF NOTICES FILED FOR NOV. CONTRACT: 586 NOTICES FOR 58,600 OZ or 1.8227 TONNES

total notices so far: 5901 contracts for 590,100 oz (18.354 tonnes)

SILVER NOTICES: 10 NOTICE(S) FILED FOR 50,000 OZ/

total number of notices filed so far this month 355 : for 1,775,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $15.25

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////HUGE CHANGES IN GLD INVENTORY: A DEPOSIT OF 3.19 TONNES INTO THE GLD//

INVENTORY RESTS AT 911.57 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN $.02

AT THE SLV// :/SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF OF 0.553 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 471.923 MILLION OZ (THIS IS ALSO A CRIME SCENE@!!!!

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GIGANTIC SIZED 1836 CONTRACTS TO 140,199 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE HUGE GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR STRONG GAIN OF $0.39 IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR SHORTERS/HFT WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY ONLY $0.39)., AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC LONGS, AS WE HAD AN ATMOSPHERIC SIZED GAIN IN OUR TWO EXCHANGES OF 4361 CONTRACTS. WE HAD A SOME ATTEMPTED SPEC SHORT COVERINGS OF THEIR SHORTFALLS WITH MINOR SUCCESS .WE HAD ZERO SPEC SHORT ADDITIONS AS THE PRICE OF THE METAL SKYROCKETED . // OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. HUGE NUMBER OF NEWBIE SPEC LONGS ADDED TO THEIR POSITIONS CAUSING MISERY TO OUR SHORTERS.

WE MUST HAVE HAD:

I) SOME ATTEMPTED SPECULATOR SHORT COVERINGS WITH ZERO SHORT ADDITIONS ////CONTINUED BANKER OI COMEX ADDITIONS /// HUGE NEWBIE SPEC LONG ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GIGANTIC ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.045 MILLION OZ FOLLOWED BY TODAY’S 240,000 QUEUE JUMP//NEW STANDING:2,435,000 MILLION OZ/ / // V) HUGE SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: +–

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS NOV. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF NOV:

TOTAL CONTRACTS for 9 days, total 20,350 contracts: 101.75 million oz OR 11.350MILLION OZ PER DAY. (2261 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 101.75 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 101.75 MILLION

RESULT: WE HAD A GIGANTIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1836 WITH OUR STRONG $0.39 GAIN IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A GIGANTIC SIZED EFP ISSUANCE CONTRACTS: 2525 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR NOV. OF 1.345 MILLION OZ FOLLOWED BY TODAY’S 240,000 QUEUE JUMP/ .. WE HAVE A HUGE SIZED GAIN OF 4837 OI CONTRACTS ON THE TWO EXCHANGES FOR 24,185MILLION OZ.. THE SILVER SHORTS ARE NOW TRAPPED AS THEY ARE HAVING CONSIDERABLE DIFFICULTY IN COVERING THOSE SHORTS D WITH THE HUGE GAIN IN PRICE ON THURSDAY.

WE HAD 10 NOTICE(S) FILED TODAY FOR 50,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 3949 CONTRACTS TO 495,950 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -902 CONTRACTS.

.

THE GOOD SIZED INCREASE IN COMEX OI CAME WITH OUR HUGE GAIN IN PRICE OF $40.75//COMEX GOLD TRADING/THURSDAY // CONSIDERABLE ATTEMPTED SPECULATOR SHORT COVERINGS TO NO AVAIL//ZERO SPEC SHORT ADDITIONS, ACCOMPANYING OUR GOOD SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION WITH CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS. IT SEEMS THAT EVERYBODY WISHES TO BUY BUT NO SELLERS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR NOV. AT 12.386 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S GIGANTIC 18,300 OZ QUEUE JUMP //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR HUGE GAIN IN PRICE OF $40.75 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 8800 OI CONTRACTS (27.37 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4851 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 495,206

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8800 CONTRACTS WITH 3949 CONTRACTS INCREASED AT THE COMEX (SHORT SPECULATORS FAILING TO GET OUT OF THEIR MESS) AND 4851 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 8800 CONTRACTS OR 27.37 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4851) ACCOMPANYING THE GOOD SIZED GAIN IN COMEX OI (3949): TOTAL GAIN IN THE TWO EXCHANGES 8800 CONTRACTS. WE NO DOUBT HAD 1) CONSIDERABLE ATTEMPTED BUT FAILED SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS. WE HAD ZERO SHORT SPEC ADDITIONS/// // CONSIDERABLE NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR NOV. AT 12.386 TONNES FOLLOWED BY TODAY’S GOOD QUEUE JUMP OF 18,300 OZ //NEW STANDING 21.048 TONNES///3) ZERO LONG LIQUIDATION //// //.,4) GOOD SIZED COMEX OPEN INTEREST GAIN 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

NOV

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV. :

40,271 CONTRACTS OR 4,027,100 OZ OR 125.25 TONNES 9 TRADING DAY(S) AND THUS AVERAGING: 4474 EFP CONTRACTS PER TRADING DAY9TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES: 125.25 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 125.25/3550 x 100% TONNES 3.52% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 125.25 TONNES//INITIAL ( SO FAR MUCH LARGER THAN PREVIOUS MONTHS)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GIGANTIC SIZED 1836 CONTRACT OI TO 140,199 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 2312 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 2312 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2312 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1836 CONTRACTS AND ADD TO THE 2312 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED GAIN OF 4361 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 24.185MILLION OZ//

OCCURRED WITH OUR RISE IN PRICE OF $0.39….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED UP 51.16 PTS OR 1.68% //Hang Seng CLOSED UP 1,224.62 OR 7.74% /The Nikkei closed UP 547.14 OR 1.97% //Australia’s all ordinaires CLOSED UP 2.86% /Chinese yuan (ONSHORE) closed UP TO 7.1078 //OFFSHORE CHINESE YUAN UP 7.0943// /Oil DOWN TO 88.97 dollars per barrel for WTI and BRENT AT 96.09 / Stocks in Europe OPENED MOSTLY MIXED. ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GOOD SIZED 3949 CONTRACTS TO 495,950 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR RISE IN PRICE OF $40.75 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (4022 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT SEEMS THAT SPEC SHORTS ARE STILL HAVING TROUBLE COVERING THEIR HUGE SHORTFALL.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON -ACTIVE DELIVERY MONTH OF NOV.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4851 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC : 4851 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4851 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG SIZED TOTAL OF 8800 CONTRACTS IN THAT 4693 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED COMEX OI GAIN OF 3949 CONTRACTS..AND THIS STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR HUGE RISE IN PRICE OF GOLD $40.75//WE ARE FINALLY WITNESSING SOME SPEC SHORTS TRYING TO COVER THEIR SHORTFALL WITH LIMITED SUCCESS. BANKERS CONTINUE AS NET BUYERS OF COMEX GOLD CONTRACTS AS THEY HAVE BEEN NET LONG FOR THE PAST FEW MONTHS. WE ALSO HAD HUGE ADDITIONAL NEWBIE SPECS GOING LONG. IT LOOKS LIKE OUR SPEC SHORTS ARE IN DEEP TROUBLE

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING NOV (21.048 TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 21.048 TONNES/INITIAL (TOTAL SO FAR THIS YEAR 564.435 TONNES)

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $40.75) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A VERY STRONG GAIN OF 6808 CONTRACTS ON OUR TWO EXCHANGES. WE HAD ZERO SPEC SHORT ADDITIONS AND MINIMAL SPEC SHORT COVERINGS.. WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 8800 CONTRACTS.// WE HAVE GAINED A TOTAL OI OF 27.37 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR NOV. (21.048 TONNES)…THIS WAS ACCOMPLISHED DESPITE OUR STRONG FALL IN PRICE OF $2.00

WE HAD -902 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 9544 CONTRACTS OR 9544 OZ OR 29.685 TONNES

Estimated gold volume 261,315// fair//

final gold volumes/yesterday 380,402/ excellent

INITIAL STANDINGS FOR NOVEMBER 2022 COMEX GOLD //NOV 11

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 162,052.885oz Brinks 21 KILOBARS Loomis: 230 kilobars and JPM |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | NIL oz |

| No of oz served (contracts) today | 586 notice(s) 58600 OZ 1.8227 TONNES |

| No of oz to be served (notices) | 866 contracts 86.600 oz 2.693 TONNES |

| Total monthly oz gold served (contracts) so far this month | 5901 notices 590100 18.354TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

customer withdrawals:3

i) Out of Brinks: 675.17 (21 kilobars)

ii0 Out of JPMorgan: 153,955.837 oz

iii) Out of Loomis: 7426.881 oz (230 kilobars)

total: 162.057.885 oz

total in tonnes: 5.04 tonnes

Adjustments: 0//

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR NOVEMBER.

For the front month of NOV. we have an oi of 1452 contracts having LOST 234 contracts. We had 417 notices served on THURSDAY so we gained a strong 183

or an additional 18,300 OZ (0.569 TONNES) will stand in this non active month of November. We will have Nov gold tonnage standing increase daily from this day forth until the end of the month.

This queue jumping originates in London with the exercising of London based EFP’s for comex gold.

December LOST ONLY 16,667 contracts DOWN to 276,059. DEC WILL BE A DILLY OF A DELIVERY MONTH.

JANUARY GAINED 29 contract to stand at 29.

February gained 19,222 contacts up to 174,588.

We had 586 notice(s) filed today for 58600 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 71 notices were issued from their client or customer account. The total of all issuance by all participants equate to 586 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 225 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the NOV. /2022. contract month,

we take the total number of notices filed so far for the month (5901) x 100 oz , to which we add the difference between the open interest for the front month of (NOV 1452 CONTRACTS) minus the number of notices served upon today 585 x 100 oz per contract equals 676,700 OZ OR 21.048 TONNES the number of TONNES standing in this non active month of NOV.

thus the INITIAL standings for gold for the NOV. contract month:

No of notices filed so far (5901) x 100 oz+ (1452) OI for the front month minus the number of notices served upon today (586} x 100 oz} which equals 676,700 oz standing OR 21.048 TONNES in this NON active delivery month of NOV..

TOTAL COMEX GOLD STANDING: 21.048 TONNES (A HUMONGOUS STANDING//NEW RECORD FOR NOV (GENERALLY THE POOREST DELIVERY MONTHS FOR A NON ACTIVE MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,927,397.697 OZ 59.95 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 24,128,689.166 OZ

TOTAL REGISTERED GOLD: 11,188,196.268 OZ (347.99 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 13,102,526.606 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,260,799OZ (REG GOLD- PLEDGED GOLD) 288.04 tonnes//rapidly declining

END

SILVER/COMEX

NOV 11//INITIAL NOV. SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 982,748.421 oz Brinks CNT Int. Delaware Manfra |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 338,371.360 oz Delaware |

| No of oz served today (contracts) | 10 CONTRACT(S) (50,000 OZ) |

| No of oz to be served (notices) | 132 contracts (660,000 oz) |

| Total monthly oz silver served (contracts) | 355 contracts (1,775,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 4 withdrawals out of the customer account

i) Out of CNT: 5023.08 oz

ii) Out of Int. Delaware: 60,722.150 oz

iii) Out of Manfra: 612,625.571 oz

iv) Out of Brinks 304,377.620 oz

Total withdrawals: 982,748.427 oz

JPMorgan has a total silver weight: 153.534million oz/298.070 million =51.51% of comex .//dropping fast

Comex deposits:

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 35,322 MILLION OZ (declining rapidly)

TOTAL REG + ELIG. 298.070MILLION OZ (also declining)

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF NOV OI: 142 CONTRACTS HAVING LOST 10 CONTRACT(S.)

WE HAD 58 NOTICES FILED ON THURSDAY, SO WE GAINED 48 CONTRACTS OR AN ADDITIONAL 240,000 OZ WILL STAND

FOR SILVER IN THIS VERY NON ACTIVE DELIVERY MONTH OF NOVEMBER.

DECEMBER SAW A LOSS OF 5593 CONTRACTS DOWN TO 76,900

(WE WILL HAVE A DANDY DEC. DELIVERY MONTH AS THE CONTRACTION IS GOING VERY SLOWLY)

JANUARY SAW A GAIN OF 19 CONTRACTS UP TO 1418 CONTACTS.

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY:10 for 50,000 oz

Comex volumes:89,156// est. volume today// strong

Comex volume: confirmed yesterday: 116,331 contracts ( huge)

To calculate the number of silver ounces that will stand for delivery in NOV. we take the total number of notices filed for the month so far at 355 x 5,000 oz = 1,775,000 oz

to which we add the difference between the open interest for the front month of NOV(142) and the number of notices served upon today 10 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the NOV../2022 contract month: 355 (notices served so far) x 5000 oz + OI for front month of NOV (142) – number of notices served upon today (10) x 5000 oz of silver standing for the NOV. contract month equates 2,435,000 oz.

We will gain in silver oz standing from this day forth until the end of the month.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:49,371// est. volume today// poor

Comex volume: confirmed yesterday: 101,267 contracts ( huge)

END

GLD AND SLV INVENTORY LEVELS

NOV 11/WITH GOLD UP $15.25//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD////INVENTORY RESTS AT 911.57 TONNES

NOV 10/WITH GOLD UP $40.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.38 TONNES

NOV 9/WITH GOLD DOWN $2.00: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES INTO THE GLD////INVENTORY RESTS AT 908.38 TONNES

NOV 8/WITH GOLD UP $34.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.47 TONNES FROM THE GLD//: INVENTORY RESTS AT 905.49 TONNES

NOV 7/WITH GOLD UP $2.95: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.63 TONNES FROM THE GLD//INVENTORY RESTS AT 906.96. TONNES

NOV 4/WITH GOLD UP $44.45 TO $1673.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.48 TONNES FROMTHE GLD////INVENTORY RESTS AT 911.59 TONNES.

NOV 3/WITH GOLD DOWN $18.30 TO $1628.85: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.05 TONNES FROM THE GLD////INVENTORY RESTS AT 915.07 TONNES

NOV 2/WITH GOLD UP 55 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 919.12 TONNES.

NOV 1/WITH GOLD UP $9.20 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES FORM THE GLD../INVENTORY RESTS AT 920.57 TONNES

OCT 31/WITH GOLD DOWN $4.00; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD//INVENTORY RESTS AT 922.59. TONNES//

OCT28/WITH GOLD DOWN $19.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 TONNES FROM THE GLD..///INVENTORY RESTS AT 925.20 TONNES

OCT 27/WITH GOLD DOWN $3.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 26/WITH GOLD UP $11.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 25/WITH GOLD UP $3.85: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 928.39 TONNES

OCT 24/WITH GOLD DOWN $1.80 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES FROM THE GLD////INVENTORY RESTS AT 928.10 TONNES

OCT 21/WITH GOLD UP $19.10: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 930.99 TONNES

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

GLD INVENTORY: 911.57 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

NOV 11/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ FROM THE SLV///INVENTORY RESTS AT 471.923 MILLION OZ//

NOV 10/WITH SILVER UP 39 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 368,000 OZ INTO THE SLV///INVENTORY RESTS AT 472.476 MILLION OZ//

NOV 9/WITH SILVER DOWN 10 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV/; A WITHDRAWAL OF 3.821 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 472.108 MILLION OZ//

NOV 8/WITH SILVER UP 48 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.751 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 475.929 MILLION OZ//

NOV 7/WITH SILVER UP 12 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 4/WITH SILVER UP $1.31 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.972 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 3.WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 566,000 OZ FROM THE SLV////INVENTORY RESTS AT 482.650 MILLION OZ//

NOV 2/WITH SILVER DOWN 9 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 92,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.216 MILLION OZ//

NOV 1/WITH SILVER UP 53 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 415,000 OZ FORM THE SLV////INVENTORY RESTS AT 483.308 MILLION OZ

OCT 31: WITH SILVER FLAT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .644 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 483.723 MILLION OZ//

OCT 28/WITH SILVER DOWN 35 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.367 MILLION OZ//

OCT 27/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE S: A WITHDRAWAL OF 2.579 MILLION OZ FROMTHE SLV/////INVENTORY RESTS AT 484.091 MILLION OZ//

OCT 26/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.013 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 486.670 MILLION OZ./.

OCT 25/WITH SILVER UP 17 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.083 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.683 MILLION OZ/

OCT 24/WITH SILVER UP 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .553 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.610 MILLION OZ//

OCT 21/WITH SILVER UP 43 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .46 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 486.163MILLION OZ//

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

CLOSING INVENTORY 471.923 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff .

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

MATHEW PIEPENBURG:

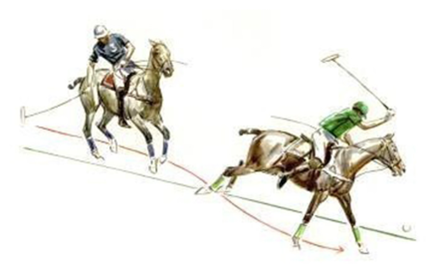

POLO METAPHORS, BOND FAILS AND GOLD’S PRICE DIRECTION

Matthew Piepenburg

November 9, 2022

Gold’s price direction is explained below.

From polo to hockey—it’s a known fact that the best players think three moves ahead.

Sadly, the same can’t be said of our financial elites…

But as playing conditions deteriorate across the bond, stock, property and currency markets, those with a “three-play- ahead” mindset will have the greatest advantage.

This is especially true for precious metal investors, regardless of their riding or skating skills.

More Horse-Droppings from the Treasury Dept.

One of the most important global players on today’s macro pitch is the credit market, and that horse is tired.

Last week, former Fed-Chair-turned-US-Treasury Secretary, Janet Yellen, told reporters that her office is “very focused” on Uncle Sam’s IOUs, and even confessed “concern” regarding “episodes of illiquidity” wherein it has been difficult to buy or sell US Treasuries, especially in large amounts.

Ultimately, however, the mule-riding Don Quixote, Janet Yellen, does not “see problems at this point in the U.S. Treasury Markets.”

Ahhhhh. That’s rich….

Apparently, Yellen has a very poor eye for the current playing field and is chasing windmills rather than the rules of a moving target.

Hiding Bond Liquidity with Verbal Liquidity

As we have been warning for months, these “episodes of illiquidity” are more than just a “concern.”

In fact, they serve as undeniable evidence that the world is running out faith in Uncle Sam’s bloated bar tab after years of monetary addiction to mouse-click money to pay for (monetize) the so-called “American way.”

In short, when GDP, tax receipts and good ol’ fashion productivity or trade surpluses no longer work, the US has become good at just borrowing and printing, a tactic (i.e., charade) that bought time, votes and even an appallingly ironic Noble Prize for Bernanke, but a ruse for which the rest of the world is now losing faith after years of importing American inflation.

In short, more and more of the world wants less and less of Uncle Sam’s sovereign debt, which means USTs are falling and hence yields and rates are rising.

And as previously reported, those rising yields are like rising shark fins approaching a debt-soaked global system already bleeding in the water.

Stated simply, when Yellen says she sees no problems, that’s precisely when you know there’s a problem.

Or as Otto von Bismarck (and Tree Rings) reminds: “Never believe anything in politics until it is officially denied.”

More Treasury Secretaries, More Mules Masquerading as Thoroughbreds …

Speaking of Treasury Secretaries (i.e., the worst players on the “cancha”), former Secretary Larry Summers is doing what he does best, namely: Causing problems behind the scenes (from repealing Glass Steagall to deregulating derivatives), denying/ignoring guilt, and then once those problems become obvious, making public warnings of the same to appear virtuous.

Like Minister Fouche under Napoleon, Summers blows in which ever direction the wind most suits his image.

Toward that end, he’s finally speaking of what most of us have known long ago: The US can’t afford rising rates in 2022 under Powell the way it could in 1980 under Volcker.

Thanks, again, Larry, for jumping on the band wagon long after it’s too late.

Given the foregoing realities, double-speak and just plain dumb out of DC’s lowest-goal but best-dressed players, the inevitable consequences of unloved Treasuries as a result of unimpressive Treasury Secretaries simply means an inevitable pivot toward more printed, debased and inflationary Dollars to keep Uncle Sam from defaulting on his bonds.

But politicians are clever foxes. They hide their addictions (and intentions) as cleverly as the BLS hides inflation facts.

Just More Backdoor QE Before the Real Thing

Just like politicos can deny a recession in a recession or deny inflation during inflation, they can pretend that QE is not QE, even when it is, well… QE.

Toward that end, we can expect the Treasury Department to start buying its own longer-dated bonds (USTs) by swapping them with shorter duration T-Bills.

Officially, this is not Quantitative Easing per se, but rather a “UST buyback.”

But why let fake semantics confuse honest math? The smart players are already three plays ahead of the Fed’s empty rhetoric and bad riding skills.

Like the daily repo support from the Fed, in the end, such “buyback” schemes are just QE under a different mask.

Powell’s Ruse Continues

Thus, as such shell games in DC continue to hide reality behind words, the Powell Fed will continue its ruse to fight inflation the “Volcker way” and likely announce and conduct additional (but 50 rather than 75 bps) rate hikes in the last chapters of 2022 and the early chapters of 2023 before the inevitable surrender to more QE.

Why the near-time rate hikes?

Powell knows that when the current recession becomes an official recession, he’ll need at least one tool in his ever-weakening toolbox.

In short: He’s only raising rates today so that he’ll at least have something to cut tomorrow.

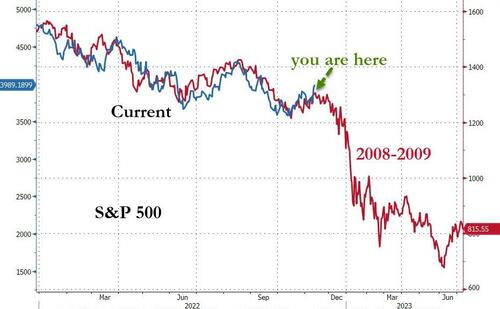

And speaking of recession, the following (and inverted) yield curve is a screaming sign that a recession is coming, if not already here.

I See Serious Stagflation Ahead

As for fighting inflation, any short-term hopes of beating inflation will end once the money printers are spinning again at full speed to buy Uncle Sam’s increasingly unloved IOUs.

This will likely occur in 2023, but frankly, who the hell knows precisely when it will rain QE money? I don’t.

The key is recognizing the shark fins and getting a safe boat. And as warned previously, we are all gonna need a bigger boat.

Stated bluntly and simply, there’s no way to ever unwind the Fed’s balance sheet nor the nation’s $31T deficit in the face of a recession that will take that deficit many, many, many trillions higher.

These obvious and fatal inflationary realities will ultimately collide with the disinflationary forces of a long and painful (as well as Fed-engineered) recession.

Given that I see inflation as a monetary issue rather than just a bogus CPI print, the further and inflationary debasement of the USD under further QE ahead (despite the USD’s growing and ironic relative strength) will be a stronger force than a deflationary recession.

In simple terms, this means we need to prepare for (rather than debate) some serious stagflation ahead.

Toward that end, and as already implied by a number of DC insiders, we can expect the Fed to slowly alter its “target inflation” narrative from the comical 2% range to an equally comical 4% or higher range in the coming months and quarters—all of course, to be blamed on Putin or COVID rather than years of mouse-click money.

Powell, like most mediocre politicians (or polo players), is ego driven rather than Main Street responsible. His main fear today is not about keeping his post, but assuring his legacy.

Secretly, Powell fears looking like another Arthur Burns, who let inflation get too hot. Thus, Powell’s public image today is about fighting inflation.

But I’m not buying it. The real goal today is to inflate away debt.

Karma’s a B!7@#

In reality, and to repeatedly shout from the rooftops, the only way to handle $31T in US public debt is to “inflate it away” by eventually loosening rather than tightening monetary policy once it becomes obvious that US IOUs won’t find enough buyers unless there’s a money printer to do so.

Needless to say, such grotesque reliance on a money printer (i.e., money killer) is the economic Karma of far too many years living on debt rather than productivity, and far too many years of the US exporting its inflation to the world and clipping the wings of their own allies by making the USD too strong to repay, settle or compete.

By 2024, I expect a disorderly “reset” and central bank digital currencies as the USD loses what little respect it has left.

The World Turning a Slow Back on a Fast Dollar

Toward this end, and as forewarned too many times to count, the rest of the world (I.e., the BRICS) is either turning away from the steroid-ruined USD (slowly but surely) or turning toward their currency-debasing money printers (think Japan and the UK yesterday and the ECB and the Fed tomorrow).

Meanwhile, Saudi Arabia is looking more toward China and less toward Biden to improve energy cooperation.

As warned, the Petrodollar system, so critical to the USD’s eminence (i.e., forced demand) in the world, is going to slowly unwind as Saudi starts accepting yuan rather than USD for its oil.

So yes, the world (and Dollar) is changing, and fast…

Poor Germany

Over the weekend, for example, I was in Munich, where inflation is already at 11.6% in a country which is considered Europe’s most reliable creditor.

But even Germany can’t seem to find any buyers for its bonds as Olaf Scholz scurries to raise $200B to pay for rising energy costs due to its blind (forced?) support for American sanctions against Putin in yet one more example of a long list of U.S. proxy wars on other peoples’ land.

But who wants to buy a German bond when the inflation rate is running some 900 basis points above the average interest rate, which means buyers lose almost 9% of their return to inflation the moment they bid?

In short, the reality of negative real yields (the hidden trick of all broke nations) is not only hitting the face of the average US citizen, but Germany’s as well.

Gold: Play the Direction of the Ball

As introduced above, all of these trends point not to where the golden polo ball or hockey puck sits currently, but toward where the ball or puck is headed…

Right now, and as explained at length elsewhere, an engineered and only relatively strong USD is taking the shine off gold. The current inverse correlation between gold and the USD is undeniable.

But that is where the ball sits now. Where it is headed is another matter, and great players, as well as investors, are always three plays ahead of the moment…

Stated more simply, as more and more currencies (including, yes, even the USD) weaken in a backdrop of inflationary realities and debasing consequences, gold is headed for an historical move, which means central bankers are about to get hit with a golden puck…

Toward this end, investors around the world are always asking Egon and I what the gold price will be in a month, a day, a year etc.

But gold price measured in what? In USD? Yen? Euros? Pound Sterling?

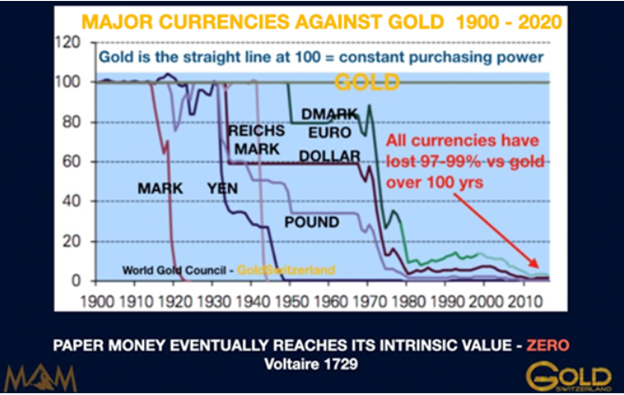

Folks, the simple point is why measure a fixed asset in an increasingly dying currency? Gold’s real measure is in ounces and grams, not fiat paper.

Or stated more simply: Gold doesn’t rise (see flat/constant top-line in graph below), it just holds its value as fiat currencies gyrate and then die like a fish flopping on the dock, which all fiat currencies have always done, throughout history, every time and without exception.

So, are you playing the ball where it lies now, or where it will be three plays ahead?

3. Chris Powell of GATA provides to us very important physical commentaries

A MUST READ OVER THE WEEKEND

KITCO FINALY ADMITS TO GOLD MANIPULATION!!

(zerohedge)

The End Times arrive! Kitco covers gold manipulation in some detail

Submitted by admin on Thu, 2022-11-10 13:51Section: Daily Dispatches

2:08p ET Thursday, November 10, 2022

Dear Friend of GATA and Gold:

More evidence that the End Times are here!

Yesterday Kitco News editor Michelle Makori moderated a discussion about gold market manipulation with mining entrepreneur Frank Giustra taking the position that the manipulation emanates from government and mining entrepreneur Rick Rule taking the position that it doesn’t.

Of course for gold market manipulation even to be mentioned at Kitco is highly unusual. But the End Times began when both Giustra and Makori began citing some of the documents of manipulation that GATA has been bringing to your (and their) attention for many year

Makori even displayed one such document, the transcript of the meeting between U.S. Secretary of State Henry Kissinger and Undersecretary of State for Economic and Business Affairs, Thomas O. Enders, at the State Department in April 1974. The transcript explains why U.S. government policy, to maintain the dollar as the world reserve currency, must push gold outside the world financial system and particularly must intimidate Western European countries, major gold holders, out of remonetizing gold:

https://www.gata.org/node/13310

Makori also mentioned Federal Reserve Chairman Alan Greenspan’s testimony to Congress in July 1998 that central banks lease gold precisely to suppress its price:

Giustra and Makori also cited the constant involvement in the gold market of the Bank for International Settlements, a subject that, until yesterday, was the exclusive provenance of GATA.

Indeed, the discussion almost seems to have been prompted by your secretary/treasurer’s presentation last month to the New Orleans Investment Conference, which covered some of the documents cited at Kitco yesterday.

https://www.gata.org/node/22229

Elaborating on the documents, Giustra demonstrated a comprehensive understanding of central banking’s view of the challenges and opportunities of monetized gold, including its potential for becoming the bedrock of an alternative to the weaponized dollar system.

By contrast Rule did not respond to any of the documentation cited. He never has responded to it even as he long has ridiculed the idea that governments might be engaged in suppressing the gold price.

Of course the discussion at Kitco did not credit GATA even once for compiling and publicizing the documentation being cited, despite the many years of blacklisting GATA has endured from mainstream financial news organizations and Kitco itself. But quite without giving any credit, just feeling compelled to produce the discussion must have been humiliating enough for Kitco. Maybe the coin and bullion dealer at last has managed to cover its shorts.

The discussion is almost two hours long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Another important reading material for you over the weekend

(Alasdair Macleod)

Alasdair Macleod: Legal definitions of money and credit

Submitted by admin on Thu, 2022-11-10 11:48Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, November 10, 2022

At these times of growing confusion over the future of currencies’ purchasing power, it is time to remove all doubt in the definitions of the differences between money, currency, and credit. This article traces the history and legal background to these relationships.

Despite the failure of the Bretton Woods agreement in 1971 and the state propaganda that followed, the position is clear. Both historically and legally money is and remains metallic coin — principally gold — and the rest is credit.

As a result of statist puffery of their fiat currencies, the public now wrongly believes it is fiat currencies that are money and that currencies have no price, except against each other. I show that this is factually incorrect. However, in financial markets legal money is always priced in legal tender, usually U.S. dollar currency, when it should be the other way round. This inversion of the truth will turn out to be a costly error for those making this mistake.

In this article I also show that the adverse consequences for prices from changes in the level of total commercial bank credit are significantly less than they are for changes in the level of central bank credit. Now that we are on the verge of a severe contraction of commercial bank credit, governments and their central banks are sure to respond by ramping up inflation of their currencies in a vain attempt to avoid deflation.

The consequences for fiat currencies are likely to be calamitous for them.

That will be the penalty we all face for ignoring the wisdom and findings of the Roman jurors, thinking that we know better with our economic models, macroeconomic policies, and statist control of markets.

Over two millennia of their careful deliberations, it was the Roman jurors who thoroughly examined and properly defined the difference between money and credit, upon which all economics and modern banking depend. Current monetary and economic fashions are mere ephemera in that context. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/legal-definitions-of-money-and-credit?gmrefcode=gata

END

Uzbekistan is reversing its policy of backing away from gold by acquiring considerable amounts during this year

(Bloomberg)

A top gold-buying central bank plans to acquire a lot more

Submitted by admin on Thu, 2022-11-10 18:21Section: Daily Dispatches

By Nariman Gizitdinov and Maria Kolesnikova

Bloomberg News

Thursday, November 10, 2022

The world’s second-biggest buyer of gold among central banks last quarter believes there’s hardly such a thing as too much bullion.

Uzbekistan has brought the share of the precious metal in its $32 billion reserves to almost two-thirds, in a reversal of a plan to cut it below 50% by buying U.S. and Chinese sovereign debt.

The proportion is now among the highest in developing economies tracked by the World Gold Council, even as total Uzbek reserves have grown by about a quarter since the central bank broached the idea of diversifying away from bullion more than three years ago.

“We thought about investing in Treasuries, but then the market itself didn’t let us do it,” the Uzbek central bank’s deputy chairman, Behzod Hamraev, said in an interview. …

… For the remainder of the report:

END

4. OTHER PHYSICAL SILVER/GOLD COMMENTARIES

Ep. 98 Live from the Vault

The COMEX Illusion Hides Massive Silver Load Out

In this week’s Live from the Vault, Andrew Maguire investigates the ‘officially sanctioned’ PsyOps paper-sell operation disrupting the COMEX’s gold and silver price-setting mechanism.

The London whistleblower takes a detailed look at the staggering scale of EFP outflows draining paper market liquidity, as global buyers demand the physical delivery of their bullion.

5.OTHER COMMODITIES:

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

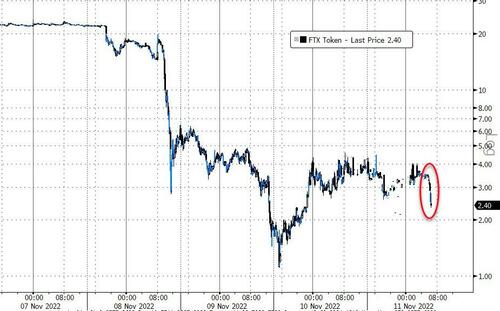

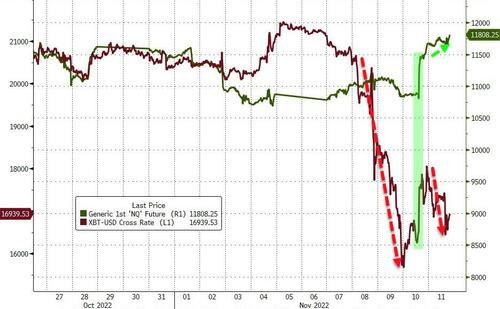

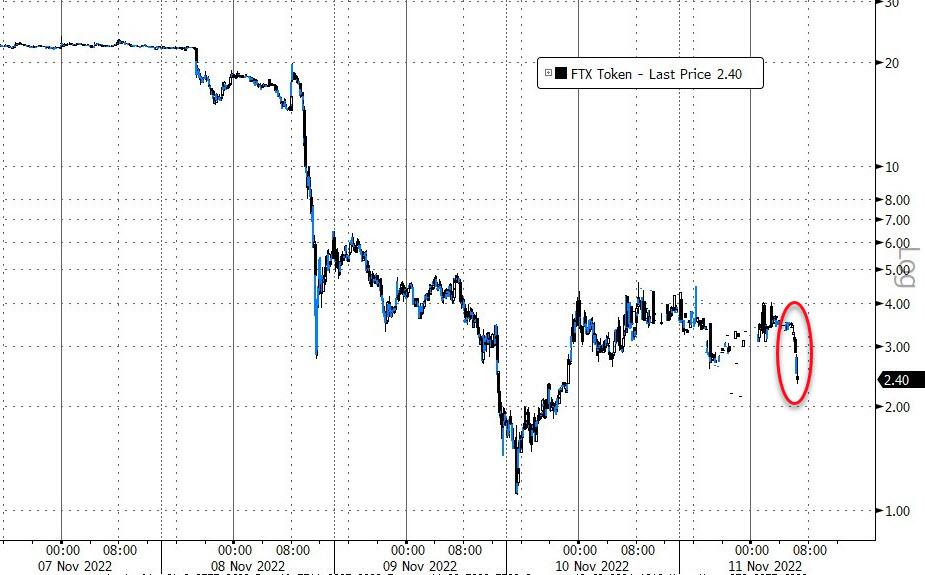

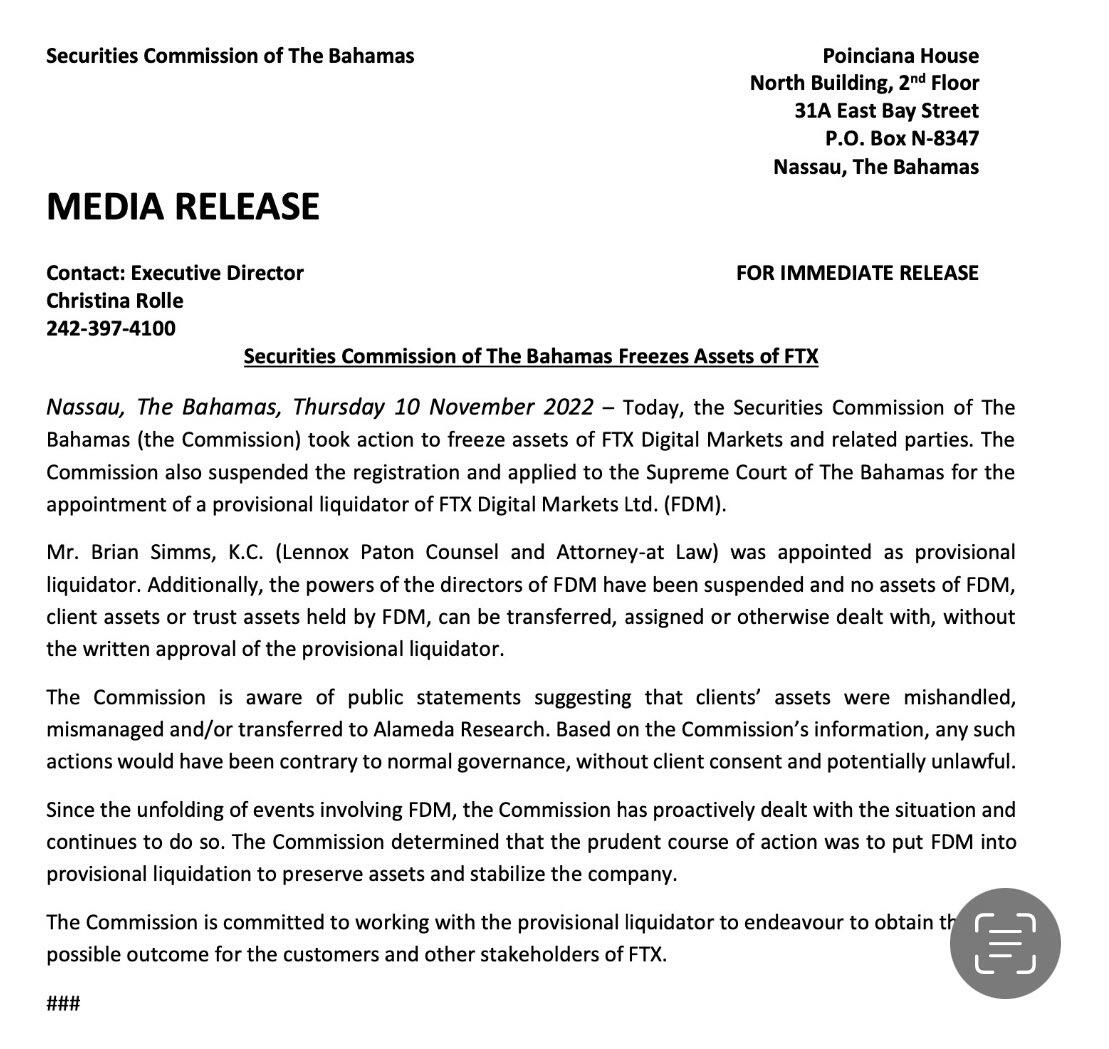

FTX files for bankruptcy.

This operation was nothing but a leverage scheme. Just like gold which is leveraged 100 to one, then FTX used the same principle.

(zerohedge)

FTX Files For Bankruptcy, Sam Bankman-Fried Resigns As CEO

FRIDAY, NOV 11, 2022 – 09:22 AM

As widely expected, FTX – which was clearly insolvent after the biggest fraud in crypto history – has filed for bankruptcy, and its soon-to-be incarcerated boss Sam Bankman-Fried, f/k/a “the JPMorgan of his generation”, has resigned as CEO. SBF is being replaced with John J. Ray, III – the lawyer who helped clean up Enron – as incoming CEO.

Press release below:

FIX Group Companies Commence Voluntary Chapter 11 Proceedings in the United States Begin Orderly Process to Review and Monetize Assets for Benefit of Global Stakeholders John J. Ray III Appointed Chief Executive Officer; Sam Bankman-Fried Resigns

FTX Trading Ltd. (d.b.a. FTX.com), announced today that it, West Realm Shires Services Inc. (d.b.a. FTX US), Alameda Research Ltd. and approximately 130 additional affiliated companies (together, the “FTX Group”), have commenced voluntary proceedings under Chapter 11 of the United States Bankruptcy Code in the District of Delaware in order to begin an orderly process to review and monetize assets for the benefit of all global stakeholders.

John J. Ray III has been appointed Chief Executive Officer of the FTX Group. Sam Bankman-Fried has resigned his role as Chief Executive Officer and will remain to assist in an orderly transition. Many employees of the FTX Group in various countries are expected to continue with the FTX Group and assist Mr. Ray and independent professionals in its operations during the Chapter 11 proceedings.

“The immediate relief of Chapter 11 is appropriate to provide the FTX Group the opportunity to assess its situation and develop a process to maximize recoveries for stakeholders,” said Mr. Ray. “The FTX Group has valuable assets that can only be effectively administered in an organized, joint process. I want to ensure every employee, customer, creditor, contract party, stockholder, investor, governmental authority and other stakeholder that we are going to conduct this effort with diligence, thoroughness and transparency. Stakeholders should understand that events have been fast-moving and the new team is engaged only recently. Stakeholders should review the materials filed on the docket of the proceedings over the coming days for more information.”

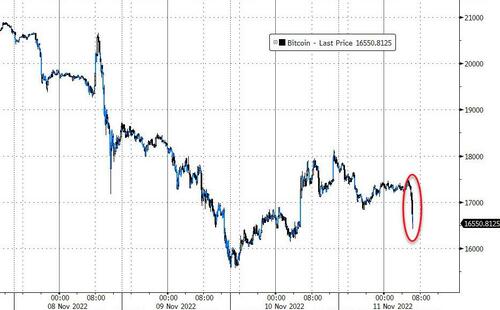

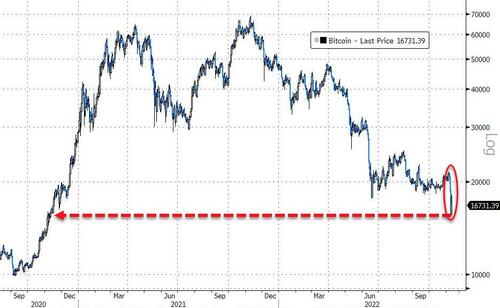

The news sparked the latest bout of selling in crypto which is back under $17,000 unable to stage even a modest bounce amid the relentless negative newsflow…

And the price FTX Token (FTT) is tumbling…

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 7.1078

OFFSHORE YUAN: 7.0983

SHANGHAI CLOSED UP 51.16 PTS OR 1.68%

HANG SENG CLOSED UP 1,224.62 OR 7.74%

2. Nikkei closed UP 547.14 PTS OR 1.97%

3. Europe stocks SO FAR: MOSTLY MIXED

USA dollar INDEX DOWN TO 106.69/Euro FALLS TO 0.99442

3b Japan 10 YR bond yield: FALLS TO. +.236!!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 139.37/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.115%***/Italian 10 Yr bond yield FALLS to 4.165%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.155%…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.505//

3j Gold at $1763.00//silver at: 21.63 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 13/100 roubles/dollar; ROUBLE AT 60.39//

3m oil into the 88 dollar handle for WTI and 96 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 139.37DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9544– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9844well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

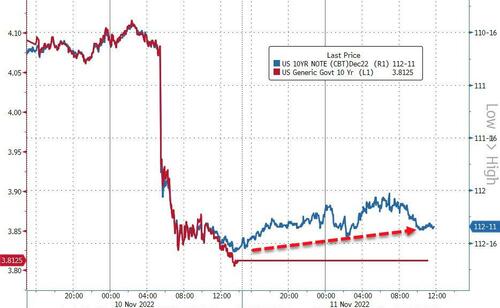

USA 10 YR BOND YIELD: 3.8112% DOWN 2 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 4.059% DOWN 2 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,53…

GREAT BRITAIN/10 YEAR YIELD: 3.383%

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Extend Gains As FOMO Spreads After China Eases Covid Measures

FRIDAY, NOV 11, 2022 – 08:05 AM

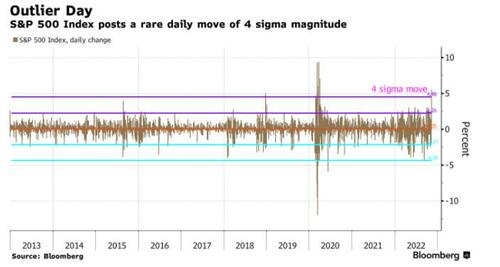

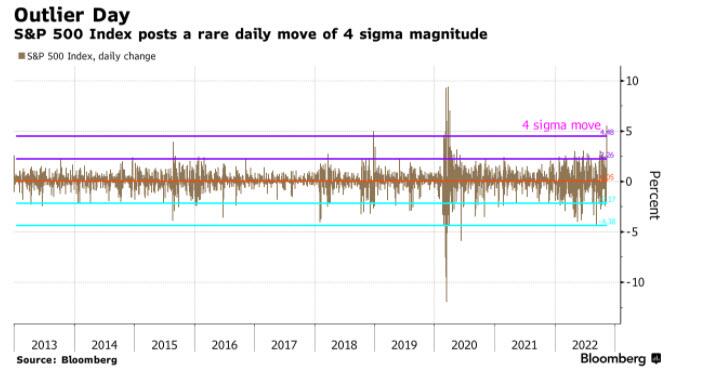

One day after its best day since April 2020, when the S&P500 added 5.5%, or a near-record $1.8 trillion in market cap in one day, a rare 4-sigma move that has only occurred 10 times over the past decade, which essentially showed how wrong-footed the market was ahead of the inflation surprise.…

… the index was set to extend its gains as a FOMO panic started to spread among traders fueled by a softer-than-expected US inflation print and as China reduced the amount of time travelers and close contacts of virus cases must spend in quarantine, and pulled back on testing, in a significant calibration of the Covid Zero policy that has upended the world’s second-largest economy and raised public ire.

Contracts on the US stock benchmark advanced 0.3% to 3,974 at 730 a.m. in New York, having earlier risen as high as 3,997. Nasdaq 100 futures also gained 0.7%, while Treasury futures weakened, with the cash market closed for the Veteran’s Day holiday. Commodities also rallied while the dollar retreated for a second day.

Overnight Beijing announced that travelers into China will be required to spend only five days in a hotel or government quarantine facility, down from ten, followed by three days confined to home, according to a National Health Commission statement Friday. The latest news on China’s Covid policy tweaks “plays with the grain of the post-US CPI moves down in the dollar,” said Ray Attrill, head of FX strategy at National Australia Bank Ltd. in Sydney. “The dollar is highly attuned to swings in risk sentiment, and for now that means dollar down.”

In US premarket trading, Chinese stocks listed in the US soared after Beijing made significant changes to the stringent Covid Zero policy that has bogged down the economy and dented appetite for the country’s equities. Alibaba and JD.com both advanced at least 3.6%. Amazon.com Inc. and Nvidia also extended their Thursday gains with major US technology and internet firms. Health insurance provider GoHealth Inc slumped as much as 22%, on track for the worst day in three months if the move holds, after the firm’s net revenue for the third quarter missed analyst estimates. Here are some other premarket news:

- Doximity shares jumped as much as 19% in US premarket trading after its earnings beat expectations, putting the online healthcare platform on track for its best day in nine months if the move holds. Analysts were encouraged to see the company reiterating its guidance for the full-year amid robust demand from hospital clients.

- GoHealth shares slumped as much as 22% in US premarket trading, on track for the worst day in three months if the move holds, after the health insurance provider’s net revenue for the third quarter missed analyst estimates. The company held off providing full-year 2022 guidance after suspending it back in August, contributing to an uncertain outlook. GoHealth’s shares had bounced 16% this week ahead of its release, though remain down 87% for the year.

- Matterport shares surged as much as 32% in US premarket trading, with the stock set for its biggest gain since its July 2021 IPO, after the 3D camera maker’s results beat demonstrated the company is holding up well amid a difficult real estate market. Demand for its latest products set it up well for next year, analysts noted, while Matterport also narrowed its revenue guidance for the year. Its shares are down 85% year-to- date.

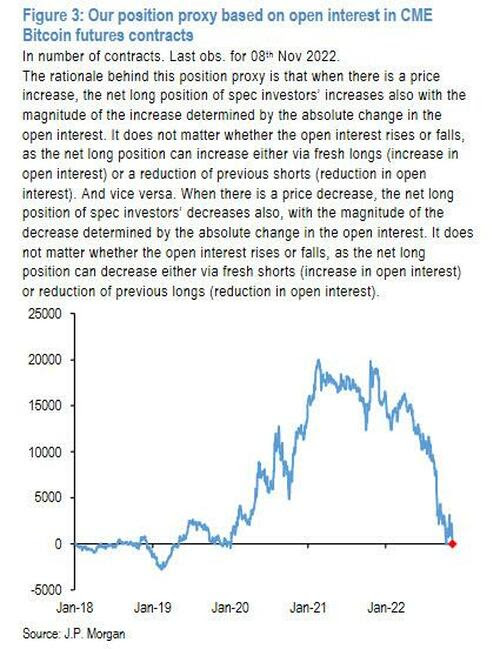

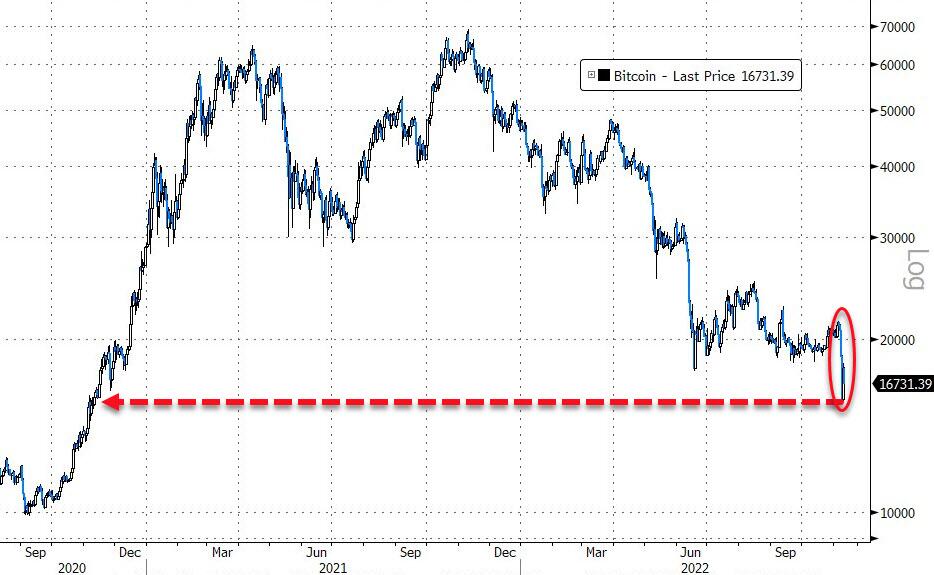

- Shares in cryptocurrency-exposed companies edged lower on Friday, with the price of Bitcoin under pressure amid the unfolding crisis at FTX. Coinbase -0.2%, Riot Blockchain -0.7%.

- Snail shares climb 83% premarket after the company announced a $5m-stock buyback plan. The repurchase plan represents 5.8% of the company’s current market value, data compiled by Bloomberg show.

- AirSculpt Technologies (AIRS US) shares plunged as much as 26% in US premarket trading, putting the stock on track to hit its lowest level since its initial public offering, after the provider of a type of liposuction to remove unwanted fat cut its year outlook.

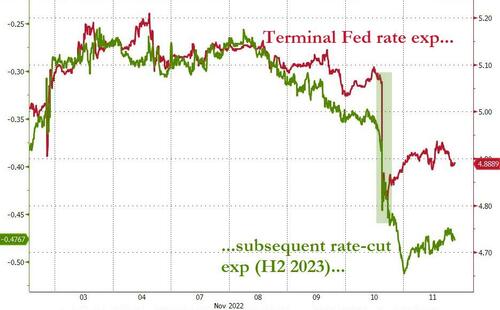

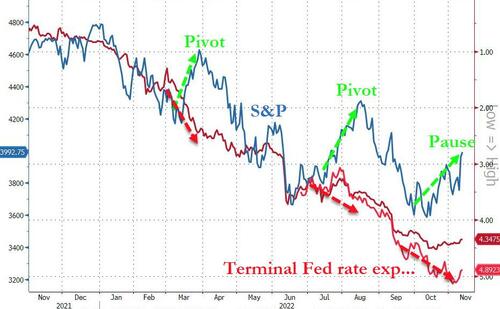

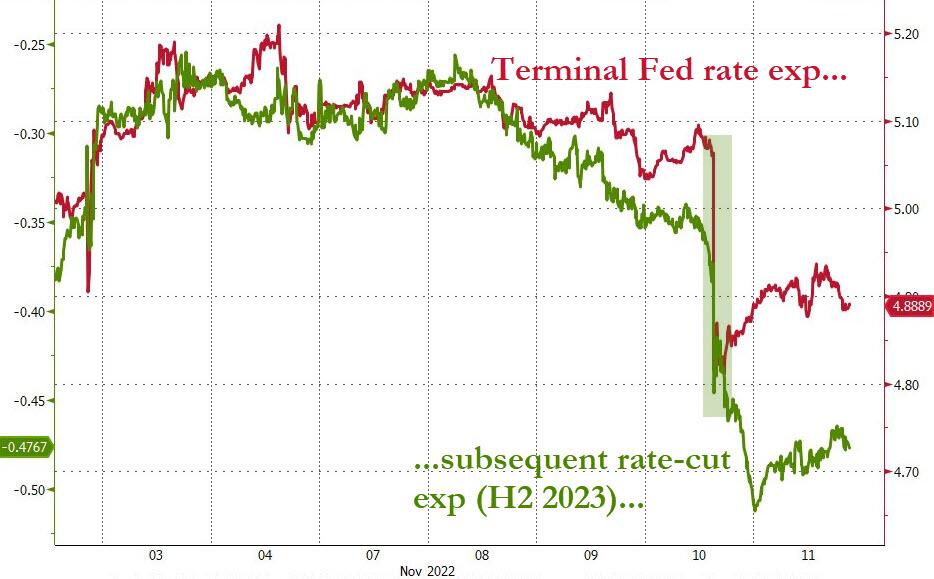

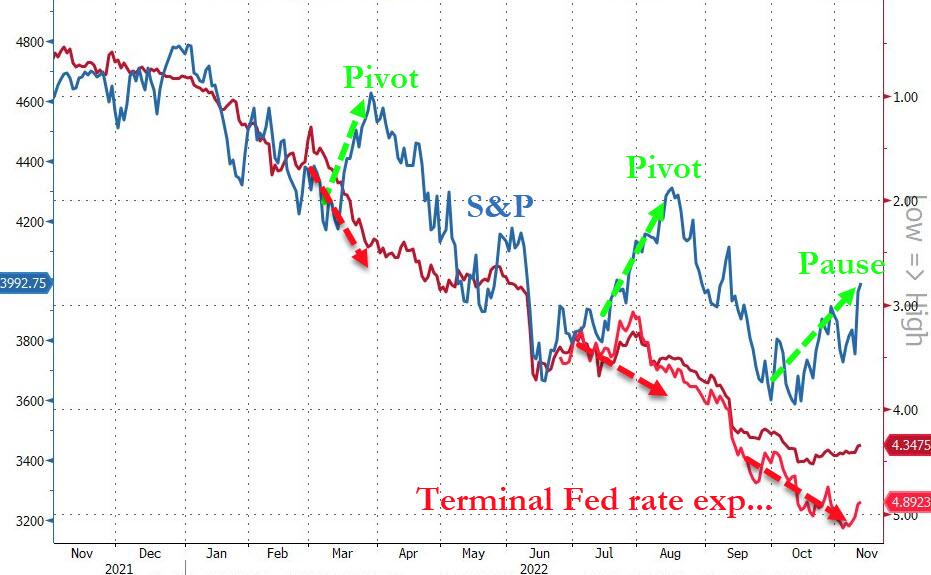

The S&P 500 and Nasdaq 100 are poised for their best week since June, after official US data showed the consumer price index rose 7.7% in October from a year before, its smallest annual advance since the start of 2022 That fueled bets that the Federal Reserve would rethink how fast it needs to move with interest rate hikes, and also lowered the terminal Fed Funds rate to 4.90% suggesting less than 4 rate hikes are left until the Fed halts tightening.

The positive mood was reinforced after China reduced the amount of time travelers and close contacts must spend in quarantine, scrapped flight bans and pulled back on testing, in a significant calibration of the Covid Zero policy that has isolated the world’s second-largest economy. Chinese stocks listed in the US soared in premarket trading.

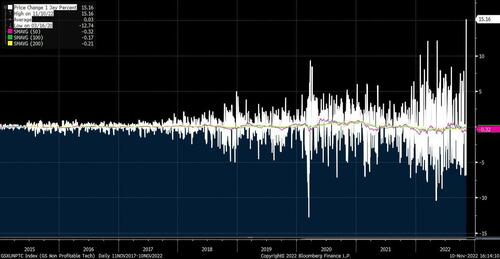

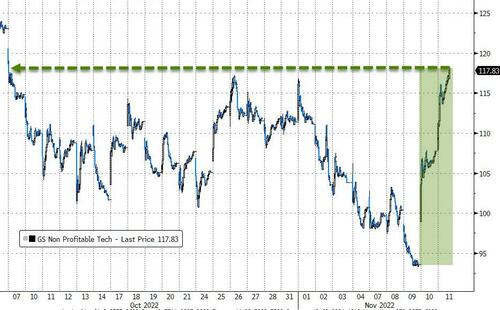

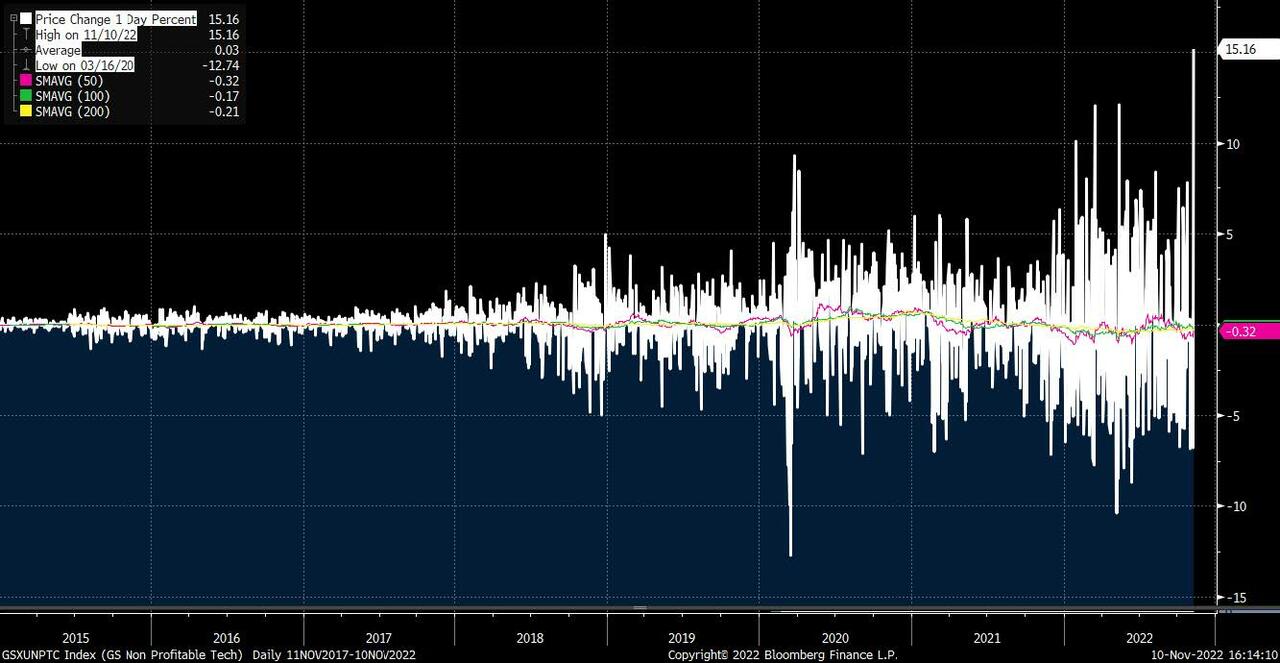

Thursday’s data not only spurred short covering as bearishly positioned investors bought back into the market, but it prompted the biggest one-day gain in such hated indexes as Goldman’s Non-Profitable Tech which exploded over 15% higher in one single day!

“Markets were not ready for good news, which is the key takeaway from yesterday’s market reaction. But having said that, inflation is still 7.7%. It doesn’t make a huge difference compared to 7.9% for the US consumer, and so the pressure is still very much there,” said Maurice Gravier, chief investment officer for the wealth management division of Emirates NBD Bank PJSC in Dubai.

Gravier expects volatility to continue until there is clarity about a Fed pause, which he says is slated for the middle of next year, he told Bloomberg TV.

In Europe, consumer products, miners and real estate are the strongest performing sectors. Euro Stoxx 50 rises 0.7%. CAC 40 outperforms peers, adding 0.8%, FTSE 100 lags, dropping 0.3%. Sterling reclaims $1.17. Here are the biggest European movers:

- Richemont reported 1H operating profit that beat estimates, as growth for the maker of Cartier jewelry and watches was led by retail. Shares rise as much as 21%, the most since October 2008, boosted along with peers as China eased some Covid measures.

- Prudential jumps as much as 9.5% to hit its highest level since Aug. 16, gaining alongside China-exposed sectors like luxury and mining

- European real estate stocks extend gains, following a surge in the previous session after US inflation data fueled optimism that the Fed might slow the pace of interest rate hikes. German landlord Aroundtown is among the biggest contributors to the gain at 10%

- Casino gains as much as 21% after the French grocer bought back €67m of Quatrim 2024 senior secured notes in the market, while as a highly indebted stock it also benefits from some relief following US inflation data.

- Defensive sectors retreat in Europe after Thursday’s softer-than-expected US inflation data and the easing of Covid restrictions in China triggered a market rotation into cyclical and growth stocks such as technology and retail. Thales is among the stocks leading the decline at 7.3% and Saab at 6.8%

- DKSH is initiated with a neutral rating and CHF70 PT at Credit Suisse, with the broker saying the risk-reward looks balanced for the distribution group. DKSH shares fall as much as 7.3%, the most since July.

- ACS declined as much as 3.7% on Friday after the Spanish infrastructure company reported earnings Thursday evening, which Renta 4 said showed pressure in the construction business margin.

- GSK is among the biggest laggards on the Stoxx 600 Health care subindex, falling as much as 5.5%, after UBS downgraded the shares to sell from hold, citing “uncertain times ahead still,” and seeing an “unattractive earnings scenario” after 2026.

Asian stocks also traded higher with gains as the region followed suit to the post-CPI global stock surge, while the adjustment of COVID protocols in China including a shorter quarantine for close contacts provided a late tailwind. Hang Seng and Shanghai Comp conformed to the heightened risk appetite with the Hong Kong benchmark frontrunning the advances as it gained by more than 1,000 points, while the mainland was also boosted in late trade on China relaxing its COVID protocols. Nikkei 225 jumped above the 28,000 level amid the risk-on mood and as participants digested a deluge of corporate earnings which have largely influenced the list of best and worst performers for the index.

Australian stocks soared to post the third weekly gain: the S&P/ASX 200 index rose 2.8% to close at 7,158.00, the highest since June 6, with technology and real estate shares rallying most. The benchmark gained for a third straight week. The move followed a broad-based rally in Asian stocks after slower-than-projected US inflation spurred bets the Federal Reserve will moderate its aggressive rate-hike path. In New Zealand, the S&P/NZX 50 index rose 2% to 11,311.76.

In FX, the dollar extended Thursday’s steep drop, falling against most Group-of-10 peers and hitting its lowest against the yen since late August after China eased some of its quarantine restrictions for inbound travelers, helping to boost demand for higher-risk currencies. The Bloomberg Dollar Spot Index dropped 0.9% after closing down 2% Thursday for its biggest fall since March 2009, when a softer CPI reading saw traders pull back bets on US rate hikes.

- USD/JPY fell as much as 1.6%, pushing below the psychologically key 140 level

- The euro rose to a three-month high of 1.0279 and headed for its best week since March 2020. Short-term bets turn bullish for the first time since Feb. 11 as shorts trim exposure

- The pound was among the worst-performing G-10 currencies. The gilt curve twist-steepened very modestly

- Australian dollar recovered from selling driven by leveraged funds trimming longs before the weekend. Bonds give back some of their opening gains in the wake of a softer core CPI reading that saw markets reprice the Federal Reserve’s terminal rate lower

In rates, cash treasury trading is closed for Veteran’s day; Treasury futures are open and are slightly lower on the day but remain near the top of the session range from Thursday, when the curve aggressively bull steepened following a lower-than-estimated CPI report. US futures losses are led by long-end of the curve, where long- bond contracts are around 21 ticks lower vs. Thursday close — 10-year futures around 112-08+, remain close to Thursday session highs. Gilts also lower on the day; BOE announced Thursday that the unwinding of emergency bond purchases will begin Nov. 29. Bunds are lower on the day, feeding through to weakness in Treasury futures, with German yields cheaper by 5.5bp to 9.5bp across the curve with losses led by belly. The German curve bear-flattened, while Italian bonds underperformed their German peers, with the 2-year yield rising by around 16bps. Money markets add to ECB tightening wagers ahead of a large slate of ECB speakers

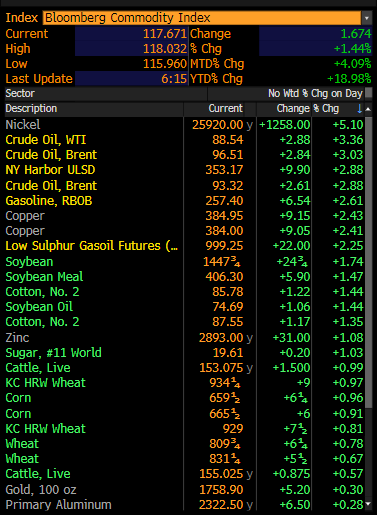

Commodities from oil to iron ore and copper jumped after China eased some Covid restrictions, raising hopes over a demand recovery in the world’s second-biggest economy. Saudi Arabia’s energy minister said OPEC+ will remain cautious on oil production, weeks after the group angered the US by lowering output. WTI drifts 2.4% higher to trade around $88.53; commodities widely surge after China eased some Covid restrictions. Spot gold rises roughly $6 to above $1,762/oz

In crypto, Bitcoin is modestly softer intraday but holds onto USD 17,000+ status. FTX CEO Bankman-Fried is facing an SEC probe related to his crypto empire, according to Bloomberg. Crypto exchange BlockFi tweeted that it is unable to operate business as usual and is pausing client withdrawals, citing a lack of clarity from FTX.com.

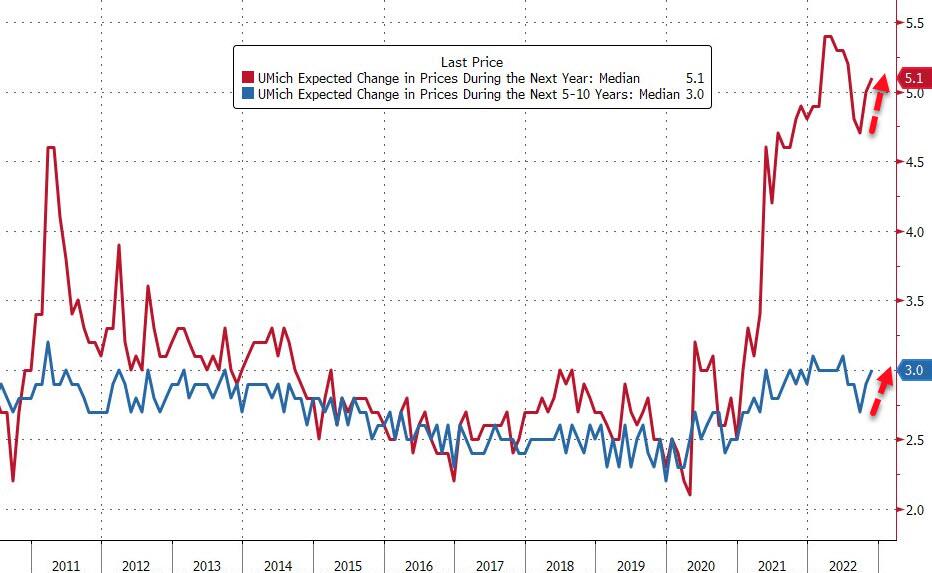

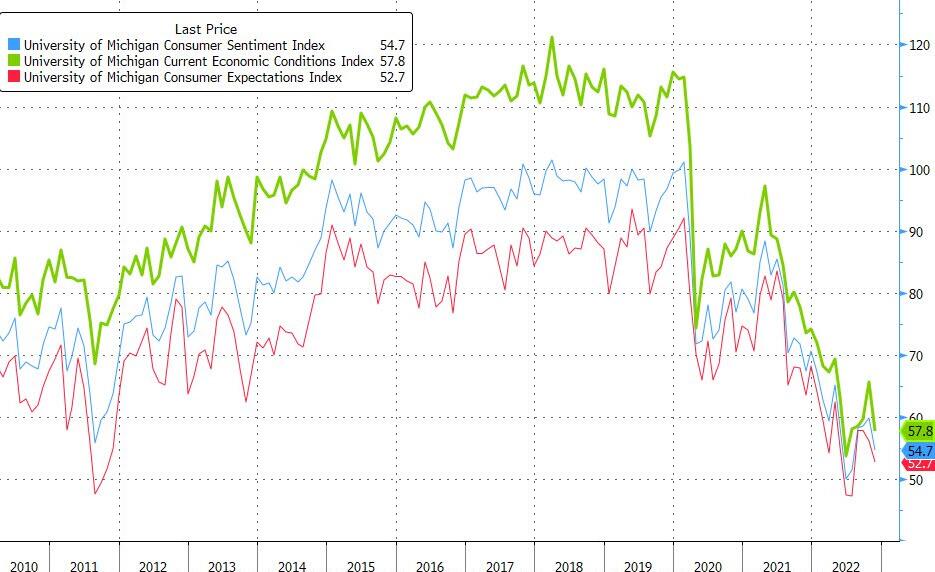

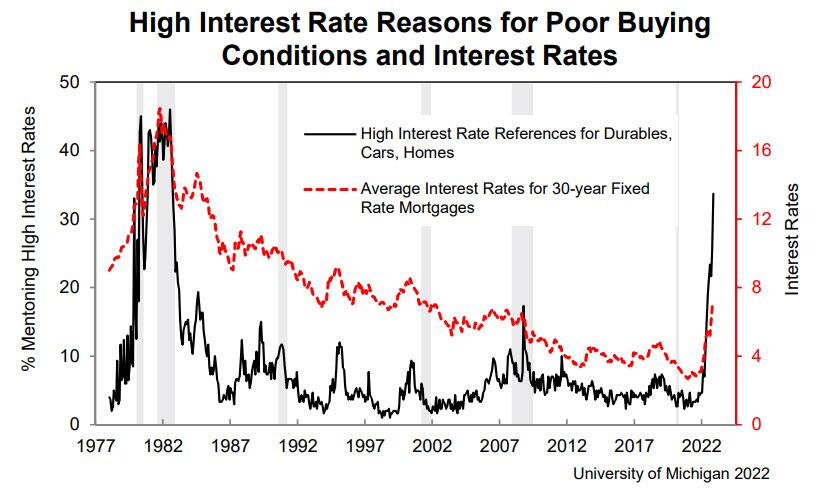

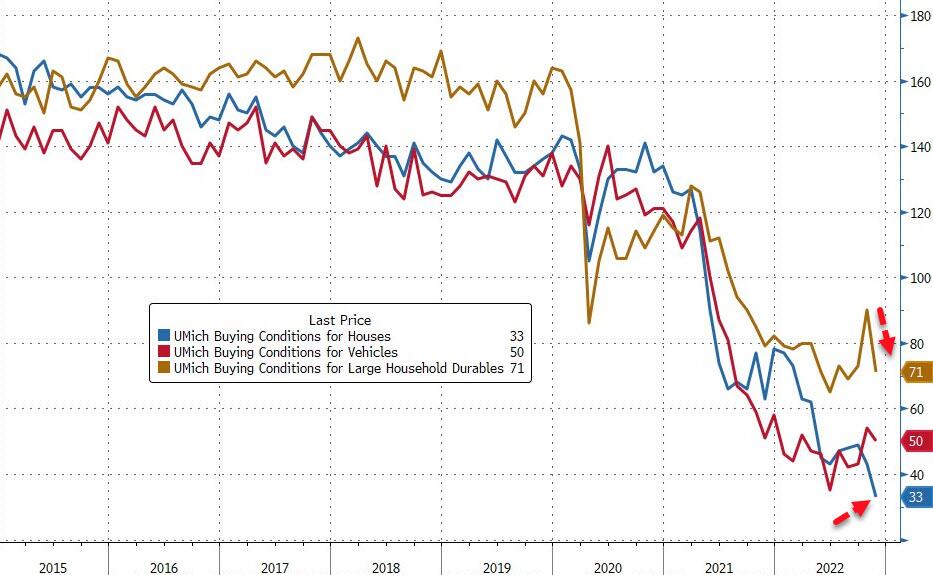

Looking to the day ahead now, and data releases include the University of Michigan’s preliminary consumer sentiment index for November in the US, along with the UK’s GDP reading for Q3. From central banks, speakers will include the ECB’s Vice President de Guindos, Holzmann, Panetta, Lane, de Cos, Centeno and Nagel, along with the BoE’s Haskel and Tenreyro. Finally, the EU Commission will be releasing their latest economic forecasts.

Market Snapshot

- S&P 500 futures up 0.5% to 3,979.75

- STOXX Europe 600 up 0.3% to 433.01

- MXAP up 4.8% to 150.99

- MXAPJ up 5.5% to 485.10

- Nikkei up 3.0% to 28,263.57

- Topix up 2.1% to 1,977.76

- Hang Seng Index up 7.7% to 17,325.66

- Shanghai Composite up 1.7% to 3,087.29

- Sensex up 2.0% to 61,803.85

- Australia S&P/ASX 200 up 2.8% to 7,157.95

- Kospi up 3.4% to 2,483.16

- Brent Futures up 2.3% to $95.80/bbl

- Gold spot up 0.4% to $1,761.68

- U.S. Dollar Index down 0.63% to 107.53

- German 10Y yield up 2.9% to 2.068

- Euro up 0.4% to $1.0249

Top Overnight News from Bloomberg

- The yuan has swung violently from one end of its tightly-managed trading band to the other like never before, as optimism toward a pivot from Covid-Zero evaporated concern about President Xi Jinping’s consolidation of power

- SNB Governing Board member Andrea Maechler expects inflation in Switzerland to stay elevated for at least two more years, she told newspaper L’Agefi

- UK Prime Minister Rishi Sunak faces an extraordinary balancing act in his autumn budget next week. He needs to appease financial markets with a package of spending cuts and tax increases, while also winning over disgruntled voters

- Chancellor of the Exchequer Jeremy Hunt is preparing to cut planned public spending growth to 2% or lower after 2024-25, compared to a previous provisional plan of 3.7% growth, according to a person familiar with his thinking

- The BOE signaled it will move cautiously in selling off the £19 billion ($22 billion) of UK government bonds it snapped up in emergency action in recent weeks, outlining a “demand-led” approach to the sales

- A decade ago this week, former UK chancellor George Osborne declared that income from bonds the Bank of England acquired under its quantitative-easing program could be used to reduce government debt. Now, the government expects to send £11 billion ($12.8 billion) to the central bank to cover an anticipated shortfall on the portfolio in the months to April

- German lawmakers approved next year’s federal finance plan including net new borrowing of €45.6 billion ($46.6 billion), according to documents seen by Bloomberg

- EU officials in Brussels on Friday slashed their forecast for growth next year, predicting barely any expansion, and raised all their projections for consumer prices. They reckon the economy is now shrinking and will keep contracting during the first quarter

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded with firm gains as the region followed suit to the post-CPI global stock surge, while the adjustment of COVID protocols in China including a shorter quarantine for close contacts provided a late tailwind. ASX 200 was led by tech and the real estate sector amid the lower yield environment. Nikkei 225 jumped above the 28,000 level amid the risk-on mood and as participants digested a deluge of corporate earnings which have largely influenced the list of best and worst performers for the index. Hang Seng and Shanghai Comp conformed to the heightened risk appetite with the Hong Kong benchmark frontrunning the advances as it gained by more than 1,000 points, while the mainland was also boosted in late trade on China relaxing its COVID protocols.

Top Asian News

- China’s National Health Commission released adjusted protocols for COVID prevention and control with quarantine for close contacts cut to 5 days centralised isolation and 3 days home quarantine from 7 days centralised isolation and 3 days home quarantine. China is also to cut COVID quarantine for inbound travellers from 10 days to 8 days and it cancelled the circuit breaker for inbound flights, according to Reuters.

- China disease control researcher earlier said that China is to continually improve its COVID-19 policies and will not relax them while the virus mutates and the epidemic situation changes, according to Reuters.

- Haizhu district of Guangzhou extended its COVID lockdown until November 13th, according to Reuters.

- China is expected to take additional measures to support the economy by conducting the largest cash injection this year through MLF loans or by reducing RRR, according to Bloomberg.

- US customs said it had seized 1,053 shipments of solar equipment since June under the China forced labour ban, while the shipments are primarily from Longi (601012 CH), Trina (688599 CH) and Jinkosolar, according to Reuters.

- Arm IPO unlikely to take place by March 2023, according to Softbank (9984 JT) sources cited by Reuters.

Major bourses in Europe are mostly firmer following CPI-induced optimism which saw further gains on Wall Street after the European cash close, with the sentiment then reverberating in APAC before seeing another boost on reports that China is easing its COVID measures. Sectors in Europe are mostly in the green with the laggards comprising of defensives, whilst the top performers include Tech, Real Estate, Retail, and Basic Resources. US equity futures are trading sideways with modest gains across the board, with futures holding onto yesterday’s upside.

Top European News

- UK Real Estate Slumped to Worst Quarter Since 2009 as Rates Bite

- Richemont Surges on Record Profit and China’s Covid Easing

- European Gas Prices Soften as Storage Fill Limits Rationing Risk

- European Mining Stocks Jump as Metals Gain on China Covid Easing

- United Internet Said to Pick IPO Banks for Web Hosting Unit

- European Stocks Set for Best Week Since March on Fed Bets, China

FX

- DXY remained downtrodden amidst further fallout, or capitulation on the back of October’s comparatively soft CPI data that ramped up Fed pivot expectations.

- G10s are firmer across the board against the Dollar, with the Japanese Yen the outperformer as USD/JPY fell under 140.00.

- The Yuan stands as the EM outperformer after China said it will ease some COVID measures.

Fixed Income

- US Treasuries are hovering midway between its 112-18/03+ overnight range ahead of prelim UoM sentiment and inflation expectations.

- Gilts pared more losses to get within 2 ticks of 105.00 having been down to 104.06.