NOV 17.//COMEX DATA COMPLETE//CURRENCY CLOSES FOR TODAY//EUROPE CLOSES FOR TODAY//BIG NEW DEVELOPMENTS IN THE FTX SCANDAL//OTHER IMPT NEWS EVENTS// SWAMP STORIES//

118 C MACQUARIE FUT 17 190 H BMO CAPITAL 2 435 H SCOTIA CAPITAL 2 661 C JP MORGAN 9 737 C ADVANTAGE 37 6 880 H CITIGROUP 1

TOTAL: 37 37 MONTH TO DATE: 6,318

TOTAL: 220 220 MONTH TO DATE: 6,12

JPMORGAN STOPPED 85/220

GOLD: NUMBER OF NOTICES FILED FOR NOV. CONTRACT: 37 NOTICES FOR 3700 OZ or 0.1150 TONNES

total notices so far: 6318 contracts for 631800 oz (19.632 tonnes)

SILVER NOTICES: 11 NOTICE(S) FILED FOR 55,000 OZ/

total number of notices filed so far this month 402 : for 2,010,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $12,75

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////HUGE CHANGES IN GLD INVENTORY: A WITHDRAWAL OF 3,77 TONNES INTO THE GLD//

INVENTORY RESTS AT 906,35TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN $.52

AT THE SLV// :/SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF OF 1.842 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 473.965 MILLION OZ (THIS IS ALSO A CRIME SCENE@!!!!

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 2716CONTRACTS TO 138,907 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE HUGE LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR LOSS OF $0.18 IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR SHORTERS/HFT WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.18)., AND WERE SUCCESSFUL IN KNOCKING OFF SOME SPEC LONGS, AS WE HAD AN STRONG SIZED LOSS IN OUR TWO EXCHANGES OF 2001 CONTRACTS. WE HAD CONSIDERABLE SPEC SHORT COVERINGS OF THEIR SHORTFALLS . WE HAD SPEC SHORT ADDITIONS AS THE PRICE OF THE METAL FELL . // OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. A FEW NEWBIE SPEC LONGS ADDED TO THEIR POSITIONS CAUSING ADDITIONAL MISERY TO OUR SHORTERS.

WE MUST HAVE HAD: I) CONSIDERABLE SPECULATOR SHORT COVERINGS WITH SOME SHORT ADDITIONS ////CONTINUED BANKER OI COMEX ADDITIONS /// SOME NEWBIE SPEC LONG ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.045 MILLION OZ FOLLOWED BY TODAY’S 65,000 QUEUE JUMP//NEW STANDING:2,760,000 MILLION OZ/ / // V) GIGANTIC SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: xxx

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS NOV. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF NOV:

TOTAL CONTRACTS for 13days, total 23,270contracts: 116,350million oz OR 8.95MILLION OZ PER DAY. (1790CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 112.775 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 116,35MILLION

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2716 WITH OUR $0.18 LOSSIN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 715CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR NOV. OF 10.005MILLION OZ FOLLOWED BY TODAY’S 65,000 QUEUE JUMP/ .. WE HAVE A GIGANTIC SIZED LOSS OF 2001 OI CONTRACTS ON THE TWO EXCHANGES FOR 17.470MILLION OZ.. THE SILVER SHORTS ARE NOW TRAPPED AS THEY ARE HAVING CONSIDERABLE DIFFICULTY IN COVERING THOSE SHORTS D WITH THE HUGE GAIN IN PRICE ON THURSDAY.

WE HAD 11 NOTICE(S) FILED TODAY FOR 55000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GIGANTIC SIZED 17,387 CONTRACTS TO 477,724 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -xx CONTRACTS.

.

THE HUGE SIZED DECREASE IN COMEX OI CAME DESPITE OUR TINY LOSS IN PRICE OF $0.30//COMEX GOLD TRADING/WEDNESDAY // CONSIDERABLE SPECULATOR SHORT COVERINGS TO NO AVAIL//(MAYBE SOME SPEC SHORT ADDITIONS , ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD SOME LONG LIQUIDATION WITH CONTINUED ADDITIONS FROM OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS. IT SEEMS THAT EVERYBODY WISHES TO BUY BUT NO SELLERS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR NOV. AT 12.386 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S GIGANTIC 10,400OZ QUEUE JUMP //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $0.30 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A STRONG SIZED LOSS OF 9529 OI CONTRACTS (29.635PAPER TONNES) ON OUR TWO EXCHANGES..

(SOME OF THE COMEX LOSS WAS ALL TAKEN UP THROUGH EFP’S. THESE WILL CIRCLE BACK TO COMEX ON EXERCISING OF DELIVERY CONTRACTS). THE OTHER HALF OF THE LOSS WAS DUE TO SPECULATOR SHORT COVERING

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7858 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 477,724

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 9529CONTRACTS WITH 7858 CONTRACTS DECREASED AT THE COMEX (SHORT SPECULATORS GETTING OUT OF THEIR MESS) AND 7858EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON(AND THESE EFP’S WILL CIRCLE BACK AND EXERCISE FOR DELIVERABLE GOLD. THUS TOTAL OI loss ON THE TWO EXCHANGES OF 9529 CONTRACTS OR 29.631TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (7858) ACCOMPANYING THE HUGE SIZED LOSS IN COMEX OI (17,387): TOTAL LOSS IN THE TWO EXCHANGES 9529CONTRACTS. WE NO DOUBT HAD 1) CONSIDERABLE SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS. WE HAD SOME SHORT SPEC ADDITIONS/// // SOME NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR NOV. AT 12.386 TONNES FOLLOWED BY TODAY’S GOOD QUEUE JUMP OF 10,400OZ //NEW STANDING 23.33TONNES///3) ZERO LONG LIQUIDATION //// //.,4) HUGE SIZED COMEX OPEN INTEREST LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

NOV

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV. :

57,419CONTRACTS OR 5,741,900 OZ OR 178.59TONNES 13TRADING DAY(S) AND THUS AVERAGING: 4416EFP CONTRACTS PER TRADING DAY TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES: 154.16TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 178.59 //3550 x 100% TONNES 5.04% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 178.59TONNES//INITIAL ( SO FAR MUCH LARGER THAN PREVIOUS MONTHS)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A GIGANTIC SIZED 2716 CONTRACT OI TO 138,907 AND further from OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 715 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 1380 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 715 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2716 CONTRACTS AND ADD TO THE 715 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED LOSS OF 2001 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 10.005MILLION OZ//

OCCURRED WITH OUR FALL IN PRICE OF $0.18….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 4.54 PTS OR 0.13% //Hang Seng CLOSED DOWN 74.80 OR 0.47% /The Nikkei closed DOWN 99.73 OR 0.35% //Australia’s all ordinaires CLOSED DOWN % /Chinese yuan (ONSHORE) closed down TO 7.1574//OFFSHORE CHINESE YUAN DOWN 7.1544// /Oil DOWN TO 81.67 dollars per barrel for WTI and BRENT AT 89.76 / Stocks in Europe OPENED ALL red. ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING weaker AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GIGANTIC SIZED 17,387 CONTRACTS TO 477,724 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED DESPITE OUR TINY FALL IN PRICE OF $0.30 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (7858 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT SEEMS THAT SPEC SHORTS ARE STILL HAVING TROUBLE COVERING THEIR HUGE SHORTFALL.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON -ACTIVE DELIVERY MONTH OF NOV.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 7858EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC : 7858 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 7858 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 9529 CONTRACTS IN THAT 7858LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A HUGE SIZED COMEX OI LOSS OF 17,387 CONTRACTS..AND THIS STRONG SIZED LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR FALL IN PRICE OF GOLD $0.30//WE ARE FINALLY WITNESSING SOME SPEC SHORTS TRYING TO COVER THEIR SHORTFALL WITH LIMITED SUCCESS. BANKERS CONTINUE AS NET BUYERS OF COMEX GOLD CONTRACTS AS THEY HAVE BEEN NET LONG FOR THE PAST FEW MONTHS. WE ALSO HAD HUGE ADDITIONAL NEWBIE SPECS GOING LONG. IT LOOKS LIKE OUR SPEC SHORTS ARE IN DEEP TROUBLE

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING NOV (23.33 TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 23.33TONNES/INITIAL (TOTAL SO FAR THIS YEAR 564.435 TONNES)

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL$0.30) AND WERE SUCCESSFUL IN KNOCKING OFF SOME SPECULATOR LONGS AS WE HAD A STRONG LOSS OF 9529CONTRACTS ON OUR TWO EXCHANGES. WE HAD ZERO SPEC SHORT ADDITIONS AND CONSIDERABLE SPEC SHORT COVERINGS.. WE HAD A STRONG SIZED LOSSON OUR TWO EXCHANGES OF 9529 CONTRACTS.// WE HAVE LOST A TOTAL OI OF 29.639PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR NOV. (23.33 TONNES)…THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE OF $0.30

WE HAD -xx CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 9529CONTRACTS OR 9529,00 OZ OR 29.639TONNES

Estimated gold volume 346,777// very good//

final gold volumes/yesterday 227,682/ fair

INITIAL STANDINGS FOR NOVEMBER 2022 COMEX GOLD //NOV 15

Total monthly oz gold served (contracts) so far this month

6318notices 631800 19.652TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

customer withdrawals:2

i) Out of Brinks: 289.36 oz 9 kilobars

ii) Out of JPMorgan: 289.239 9 kilobars

total: 578.719 oz

total in tonnes: 0.014 tonnes

Adjustments: 2// dealer to customer 20,267.414 oz JPM

and 9645,314 oz Manfra

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR NOVEMBER.

For the front month of NOV. we have an oi of 1222 contracts having GAINED 87 contracts. We had 17 notices served on WEDNESDAY so we gained a WHOPPING 104

or an additional 10,400OZ (0.3233TONNES) will stand in this non active month of November. We will have Nov gold tonnage standing increase daily from this day forth until the end of the month.

This queue jumping originates in London with the exercising of London based EFP’s for comex gold.

December LOST A STRONG 27,307contracts DOWN to 198,613

It sure looks like Dec will be a dilly of a delivery month.

JANUARY gained 257 contract to stand at 477

February gained 8,343 contacts up to 230,419

We had 37 notice(s) filed today for 3700 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 37 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 11 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the NOV. /2022. contract month,

we take the total number of notices filed so far for the month (6318) x 100 oz , to which we add the difference between the open interest for the front month of (NOV 1222 CONTRACTS) minus the number of notices served upon today 37 x 100 oz per contract equals 750,300OZ OR 23.33 TONNES the number of TONNES standing in this non active month of NOV.

thus the INITIAL standings for gold for the NOV. contract month:

No of notices filed so far (6318 x 100 oz+ (1222) OI for the front month minus the number of notices served upon today (37} x 100 oz} which equals 750,300oz standing OR 23.33 TONNES in this NON active delivery month of NOV..

TOTAL COMEX GOLD STANDING: 22.834 TONNES (A HUMONGOUS STANDING//NEW RECORD FOR NOV (GENERALLY THE POOREST DELIVERY MONTHS FOR A NON ACTIVE MONTH)

To calculate the number of silver ounces that will stand for delivery in NOV. we take the total number of notices filed for the month so far at 402x 5,000 oz = 2,010,000 oz

to which we add the difference between the open interest for the front month of NOV(161 and the number of notices served upon today 11 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the NOV../2022 contract month: 402 (notices served so far) x 5000 oz + OI for front month of NOV (x161 – number of notices served upon today (11) x 5000 oz of silver standing for the NOV. contract month equates 2,760,000 oz.

We will gain in silver oz standing from this day forth until the end of the month.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

NOV !7. WITH GOLD DOWN $12,65 TODAY: A HUGE WITHDRAWAL OF 3.77 TONNES FROM THE GLD//INVENTORY RESTS AT 906.35 TONNES

NOV 15/WITH GOLD UP $.05: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 910.12 TONNES

NOV 14/WITH GOLD UP $7.30: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 910.12 TONNES

NOV 11/WITH GOLD UP $15.25//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD////INVENTORY RESTS AT 911.57 TONNES

NOV 10/WITH GOLD UP $40.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.38 TONNES

NOV 9/WITH GOLD DOWN $2.00: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES INTO THE GLD////INVENTORY RESTS AT 908.38 TONNES

NOV 8/WITH GOLD UP $34.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.47 TONNES FROM THE GLD//: INVENTORY RESTS AT 905.49 TONNES

NOV 7/WITH GOLD UP $2.95: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.63 TONNES FROM THE GLD//INVENTORY RESTS AT 906.96. TONNES

NOV 4/WITH GOLD UP $44.45 TO $1673.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.48 TONNES FROMTHE GLD////INVENTORY RESTS AT 911.59 TONNES.

NOV 3/WITH GOLD DOWN $18.30 TO $1628.85: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.05 TONNES FROM THE GLD////INVENTORY RESTS AT 915.07 TONNES

NOV 2/WITH GOLD UP 55 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 919.12 TONNES.

NOV 1/WITH GOLD UP $9.20 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES FORM THE GLD../INVENTORY RESTS AT 920.57 TONNES

OCT 31/WITH GOLD DOWN $4.00; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD//INVENTORY RESTS AT 922.59. TONNES//

OCT28/WITH GOLD DOWN $19.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 TONNES FROM THE GLD..///INVENTORY RESTS AT 925.20 TONNES

OCT 27/WITH GOLD DOWN $3.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 26/WITH GOLD UP $11.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 25/WITH GOLD UP $3.85: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 928.39 TONNES

OCT 24/WITH GOLD DOWN $1.80 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES FROM THE GLD////INVENTORY RESTS AT 928.10 TONNES

OCT 21/WITH GOLD UP $19.10: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 930.99 TONNES

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

GLD INVENTORY: 906.35 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

NOV !7/A DEPOSIT OF 1.842 MILLION OZ INTO THE SLV..INVENTORY RESTS AT 473.965 MILLION OZ

NOV 15/WITH SILVER DOWN $.56 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.923 MILLION OZ..

NOV 14/WITH SILVER UP 41 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.923 MILLION OZ//

NOV 11/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ FROM THE SLV///INVENTORY RESTS AT 471.923 MILLION OZ//

NOV 10/WITH SILVER UP 39 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 368,000 OZ INTO THE SLV///INVENTORY RESTS AT 472.476 MILLION OZ//

NOV 9/WITH SILVER DOWN 10 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV/; A WITHDRAWAL OF 3.821 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 472.108 MILLION OZ//

NOV 8/WITH SILVER UP 48 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.751 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 475.929 MILLION OZ//

NOV 7/WITH SILVER UP 12 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 4/WITH SILVER UP $1.31 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.972 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 3.WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 566,000 OZ FROM THE SLV////INVENTORY RESTS AT 482.650 MILLION OZ//

NOV 2/WITH SILVER DOWN 9 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 92,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.216 MILLION OZ//

NOV 1/WITH SILVER UP 53 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 415,000 OZ FORM THE SLV////INVENTORY RESTS AT 483.308 MILLION OZ

OCT 31: WITH SILVER FLAT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .644 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 483.723 MILLION OZ//

OCT 28/WITH SILVER DOWN 35 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.367 MILLION OZ//

OCT 27/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE S: A WITHDRAWAL OF 2.579 MILLION OZ FROM THE SLV/////INVENTORY RESTS AT 484.091 MILLION OZ//

OCT 26/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.013 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 486.670 MILLION OZ./.

OCT 25/WITH SILVER UP 17 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.083 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.683 MILLION OZ/

OCT 24/WITH SILVER UP 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .553 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.610 MILLION OZ//

OCT 21/WITH SILVER UP 43 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .46 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 486.163MILLION OZ//

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

CLOSING INVENTORY 473.965 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff .

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

14 Nov 2022

3. Chris Powell of GATA provides to us very important physical commentaries

Cryptocurrencies have been on the doldrums since the ‘Crypto Carnage’ of Spring 2021. Over the weekend, a Bahama-based crypto exchange FTX Exchange collapsed. It will probably not be the last one.

Due to the massive financial speculation, induced by the credit (QE) programs of central banks, the crypto market grew into a hub of speculation. During their first global crash in spring 2021, it was rumored that some players had been engaged in speculation with leverage of 100x. That is, by borrowing 100 times the value of the underlying asset (cryptocurrency) and investing it back into the market. I have to admit that I had never heard of anything similar. In standard economic thinking, leverage of 12x was considered extreme. That “rule of thumb” was shattered in the crypto markets.

Now, the situation is a bit similar but different. Leverage used in the crypto market has most likely fallen from the previous extremes, but now the ‘Ponzi schemes’ are starting to reveal themselves in the crypto markets. Some crypto exchanges seem to have used the money invested there to speculate on assets or to other suspicious activities.

FTX Exchange

To top of it all, the now defunct FTX Exchange released a note on Saturday stating that it had been hacked and hundreds of millions of dollars removed from its accounts. So, the situation with FTX Exchange looks like fraud. It has also been rumored to have dubious connections to the Democratic Party, but that may just be a political gimmick.

The FTX logo is seen on a computer in Atlanta, Ga. on Nov.10, 2022. (Michael M. Santiago/Getty Images)

I and the company I am running, GnS Economics, have warned about the instability of cryptocurrencies for some years. In a special report published in June 2021, we concluded that:

“While the technology itself is promising and even “revolutionary”, its application alone does not add a tremendous amount of value. Nobody owns blockchain technology and anyone can make a new cryptocurrency, and many have done just that. While artificial scarcity is induced by design for particular cryptocurrencies, there is no limit to the potential number of different cryptocurrencies. As a result, new competing cryptocurrencies are popping up with no end in sight. Which—if any—will survive in the medium or long run?”

Controlling Money

When the current carnage in the crypto markets is over, and the dust settles, they are likely to face another existential threat from central banks and governments who want to control money. They may try to regulate the cryptocurrencies that survive the crash to death. Cryptocurrencies have thus, most likely, entered a battle from which only few will survive.

However, I don’t consider the all-but-necessary reshuffling of the cryptocurrency scene as the main foretelling of the current crypto carnage. This is because the collapse of the crypto scene implies that speculation and leverage are being pulled from the financial system, starting from the most-speculative end, i.e., the crypto market.

There are three reasons for this: monetary tightening by the central banks, approaching recession, and the coming winter in Europe.

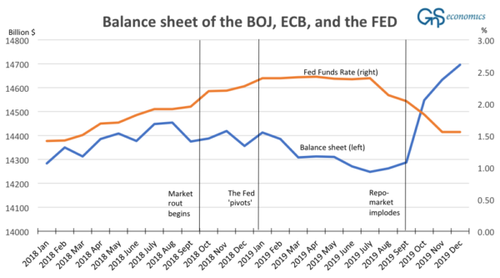

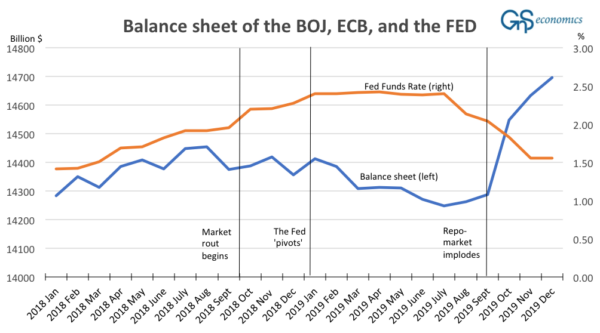

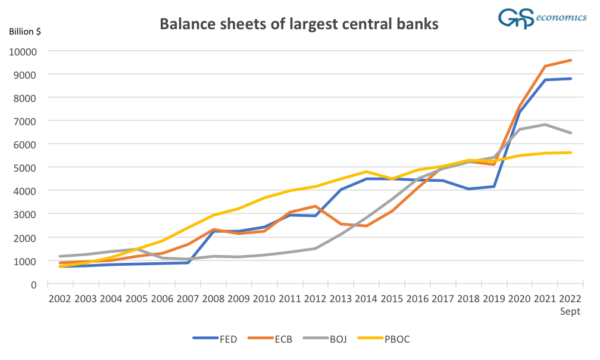

The last time central banks tried to diminish their global balance sheet, first asset and credit markets nearly crashed (in the turn of 2018/2019), and then the repurchase or repo markets imploded (September 2019). This event ended the global quantitative tightening. Now the central banks are trying to diminish their balance sheets from a much higher level. I wish them the best of luck, but I fear the worst.

A figure presenting the combined balance sheet of the Bank of Japan, European Central Bank, the Federal Reserve, the Fed Funds rate, and the major market events from Jan. 2018 to Dec. 2019. (GnS Economics, BoJ, ECB, Fed)

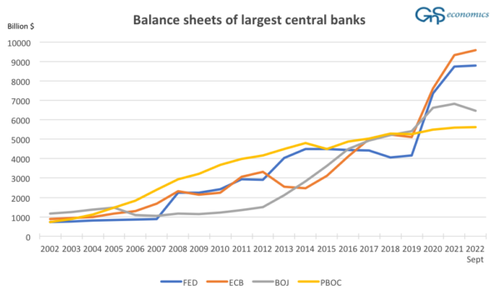

A figure of the balance sheets of the Bank of Japan, European Central Bank, the Federal Reserve, and the Peoples Bank of China in U.S. dollars. (GnS Economics, BoJ, ECB, Fed, PBoC)

I have been warning about the approaching recession for months. The European Commission now expects the Eurozone to fall into recession by the year-end, and it appears recession is also finally reaching the United States. Recently, FedEx, the global logistic giant, announced it would start furloughing the workforce due to “current business conditions impacting volumes.” There probably cannot be a clearer sign of impending recession that a logistics company announcing workforce diminution during the main holiday season of the year.

According to the forecasts, winter will arrive in Europe (it has been long overdue) this week. It will most likely lead to another spike in energy prices and, in the worst case, to rolling blackouts or even energy lockdowns down the line. An energy crisis is likely (it has already) hit the industrial mainland of Europe, Germany, hard and it will continue to reverberate across our continent.

It is questionable will the financial sector be able to handle yet another series of shocks just three months apart. My fear is that the hit may start the next stage of the economic collapse that began already in 2020.

The fact is that the global financial sector is in dire straits, which is visible when one analyzes the sources of global liquidity (credit). I will return to these issues in more detail in my following posts.

In the meantime, I am urging everyone to continue preparing for the winter, which may be the darkest we have seen for a very long time.

END

“This Is Unprecedented”: Enron Liquidator Overseeing FTX Bankruptcy Speechless: “I Have Never Seen Anything Like This”

THURSDAY, NOV 17, 2022 – 05:10 PM

A few days ago we asked how much longer do we have to wait for the “first-day affidavit” in the FTX bankruptcy, traditionally the most detailed and comprehensive summary of how any given company collapsed into Chapter 11 (and in FTX’s case, Chapter 7 soon, as this will soon become a full-blown liquidation)…

Because how else would one describe it when FTX’s new CEO and liquidator, John Ray III, who also oversaw the unwinding and liquidation of Enron, admits that “Never in my career have I seen such a complete failure of corporate controls and such a complete absence of trustworthy financial information as occurred here.”

And just in case his shock at FTX’s fraud of epic proportions was not quite clear enough, he adds that “from compromised systems integrity and faulty regulatory oversight abroad, to the concentration of control in the hands of a very small group of inexperienced, unsophisticated and potentially compromised individuals, this situation is unprecedented.”

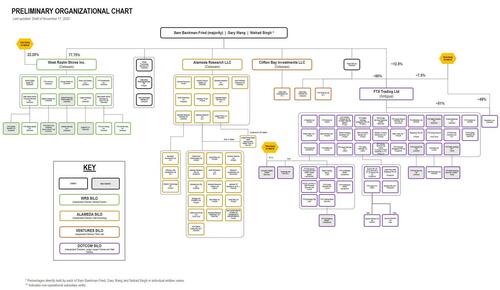

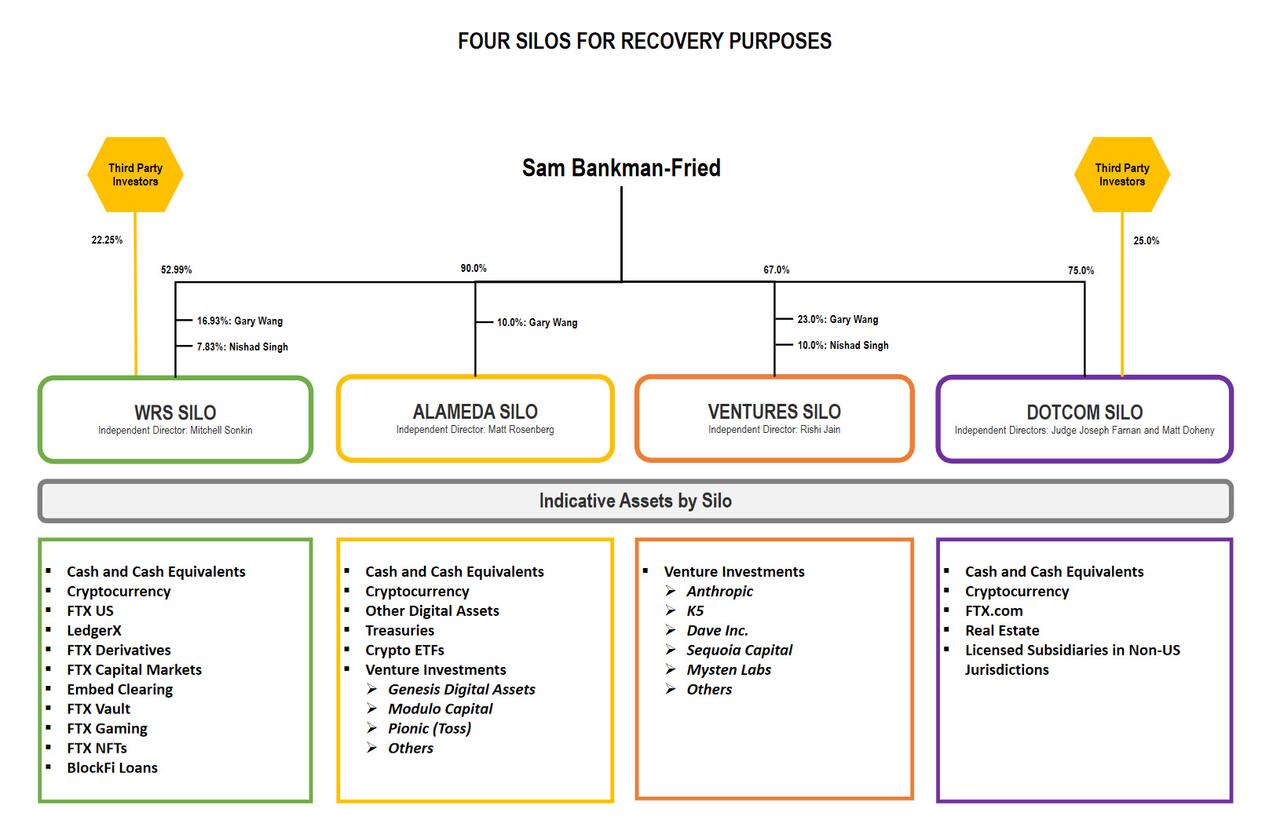

Courtesy of the affidavit, here is what the company’s org chart looks like as of Nov 17:

According to Ray, he has located “only a fraction” of the digital assets of the FTX Group that they hope recover during the Chapter 11 bankruptcy. They’ve so far secured about $740 million of cryptocurrency in offline cold wallets, a storage method designed to prevent hacks. This is just a fraction of the $10-$50 billion in liabilities the company disclosed in its bankruptcy filing.

How do we know it’s a fraud: as Ray writes on page 24, although the investigation has only begun and must run its course, it is my view based on the information obtained to date, “that many of the employees of the FTX Group, including some of its senior executives, were not aware of the shortfalls or potential commingling of digital assets.” Many maybe not, but some – and certainly SBF himself – did.

It gets better: Ray said that company’s audited financial statements should not be trusted, Ray said, adding that liquidators are working to rebuild balance sheets for FTX entities from the bottom up.

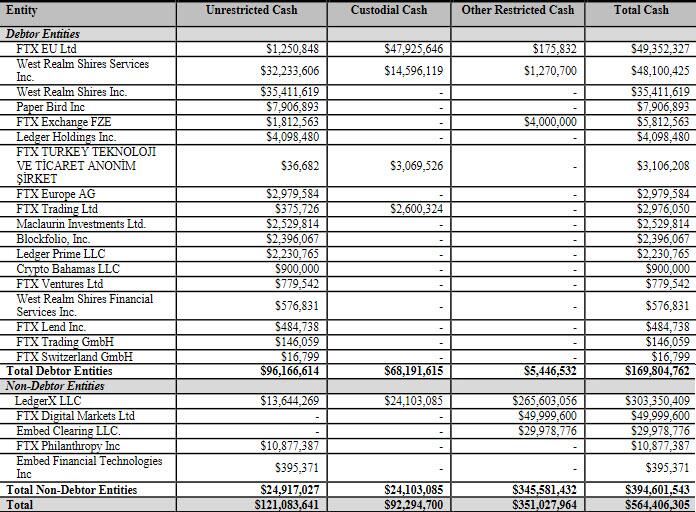

FTX “did not maintain centralized control of its cash” and failed to keep an accurate list of bank accounts and account signatories, or pay sufficient attention to the creditworthiness of banking partners, according to Ray. Advisers don’t yet know how much cash FTX Group had when it filed for bankruptcy, but has found about $560 million attributable to various FTX entities so far.

Although restructuring advisers have been in control of FTX for less than a week, they’ve seen enough to depict the crypto company as a deeply flawed enterprise. Lasting records of decision making are hard to come by: Bankman-Fried often communicated through applications that auto-deleted in short order and asked employees to do the same, according to Ray. Corporate funds of FTX Group were used to buy homes and other personal items for employees, Ray said.

Corporate funds were also used to buy homes and other personal items for employees and advisers, sometimes in their personal names.

“In the Bahamas, I understand that corporate funds of the FTX Group were used to purchase homes and other personal items for employees and advisors. I understand that there does not appear to be documentation for certain of these transactions as loans, and that certain real estate was recorded in the personal name of these employees and advisors on the records of the Bahamas,” Ray said, who also noted that the company didn’t have appropriate corporate governance and never held board meetings. There was no accurate list of bank accounts and account signatories, as well as insufficient attention paid to the creditworthiness of banking partners.

Ray said the company did not have “an accurate list” of its own bank accounts, or even a complete record of the people who worked for FTX (see below). He added that FTX used “an unsecured group email account” to manage the security keys for its digital assets.

The filing sheds light on the sloppy business practices, such as FTX employees asking to be paid through an online “chat” platform “where a disparate group of supervisors approved disbursements by responding with personalized emojis.”

Below we excerpt some of the most notable highlights from the affidavit, which we embed at the bottom of the post and which everyone should read to get a sense of just how massive Sam Bankman-Fried’s fraud was.

I have over 40 years of legal and restructuring experience. I have been the Chief Restructuring Officer or Chief Executive Officer in several of the largest corporate failures in history. I have supervised situations involving allegations of criminal activity and malfeasance (Enron). I have supervised situations involving novel financial structures (Enron and Residential Capital) and cross-border asset recovery and maximization (Nortel and Overseas Shipholding). Nearly every situation in which I have been involved has been characterized by defects of some sort in internal controls, regulatory compliance, human resources and systems integrity.

Never in my career have I seen such a complete failure of corporate controls and such a complete absence of trustworthy financial information as occurred here. From compromised systems integrity and faulty regulatory oversight abroad, to the concentration of control in the hands of a very small group of inexperienced, unsophisticated and potentially compromised individuals, this situation is unprecedented.

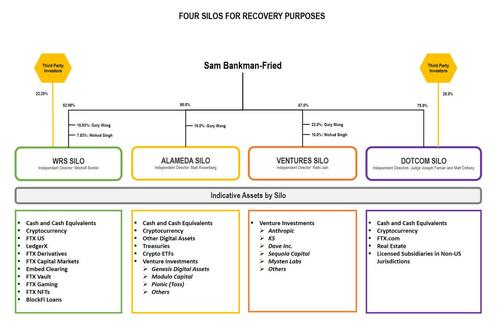

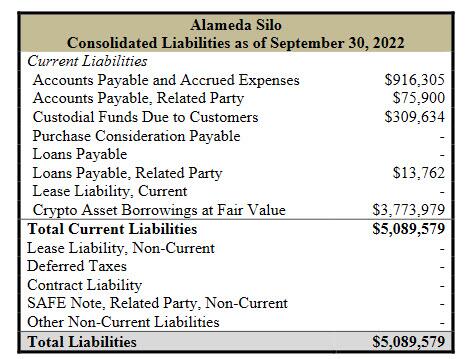

For purposes of managing the Debtors’ affairs, I have identified four groups of businesses, which I refer to as “Silos.” These Silos include:

(a) a group composed of Debtor West Realm Shires Inc. and its Debtor and non-Debtor subsidiaries (the “WRS Silo”), which includes the businesses known as “FTX US,” “LedgerX,” “FTX US Derivatives,” “FTX US Capital Markets,” and “Embed Clearing,” among other businesses;

(b) a group composed of Debtor Alameda Research LLC and its Debtor subsidiaries (the “Alameda Silo”);

(c) a group composed of Debtor Clifton Bay Investments LLC, Debtor Clifton Bay Investments Ltd., Debtor Island Bay Ventures Inc. and Debtor FTX Ventures Ltd. (the “Ventures Silo”);

(d) a group composed of Debtor FTX Trading Ltd. and its Debtor and non-Debtor subsidiaries (the “Dotcom Silo”), including the exchanges doing business as “FTX.com” and similar exchanges in non-U.S. jurisdictions. These Silos together are referred to by me as the “FTX Group.

Each of the Silos was controlled by Mr. Bankman-Fried.2 Minority equity interests in the Silos were held by Zixiao “Gary” Wang and Nishad Singh, the co-founders of the business along with Mr. Bankman-Fried. The WRS Silo and Dotcom Silo also have third party equity investors, including investment funds, endowments, sovereign wealth funds and families. To my knowledge, no single investor other than the co-founders owns more than 2% of the equity of any Silo.

The diagram attached as Exhibit A provides a visual summary of the Silos and the indicative assets in each Silo. Exhibit B contains a preliminary corporate structure chart. These materials were prepared at my direction based on information available at this time and are subject to revision as our investigation into the affairs of the FTX Group continues.

There is much more information on each of these silos in the affidavit at the bottom of this post, but what we are curious about at this stage is what the Alameda balance sheet looks like: after all, that’s what started this whole avalanche in the first place. Here are the details:

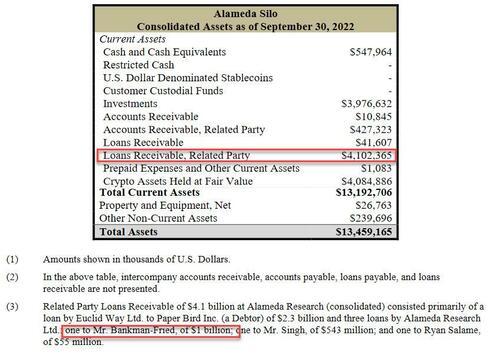

The parent company and primary operating company in the Alameda Silo is Alameda Research LLC, which is organized in the State of Delaware. Before the Petition Date (as defined below), the Alameda Silo operated quantitative trading funds specializing in crypto assets. Strategies included arbitrage, market making, yield farming and trading volatility. The Alameda Silo also offered over-the-counter trading services, and made and managed other debt and equity investments. In short, the Alameda Silo was a “crypto hedge fund” with a diversified business trading and speculating in digital assets and related loans and securities for the account of its owners, Messrs. Bankman-Fried (90%) and Wang (10%).

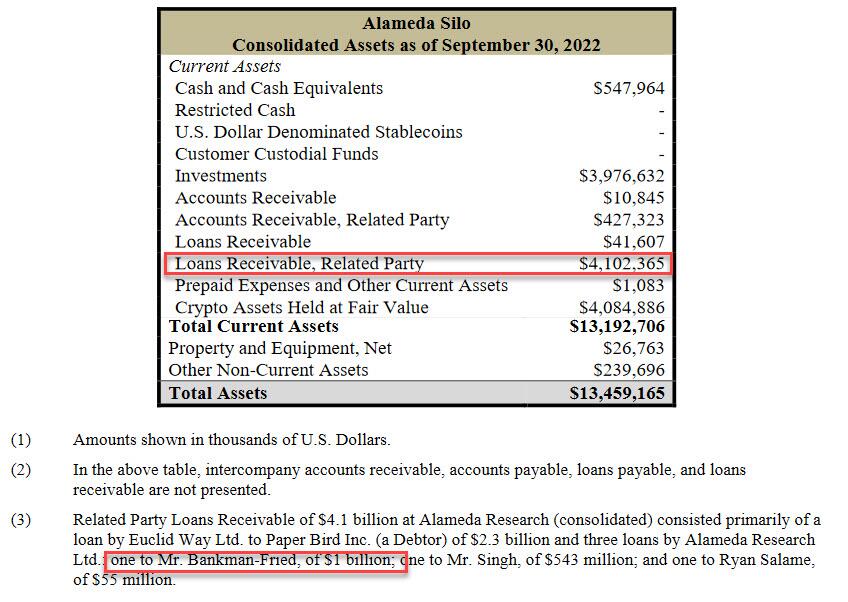

Alameda Research LLC prepared consolidated financial statements on a quarterly basis. To my knowledge, none of these financial statements have been audited. The September 30, 2022 balance sheet for the Alameda Silo shows $13.46 billion in total assets as of its date. However, because this balance sheet was unaudited and produced while the Debtors were controlled by Mr. Bankman-Fried, I do not have confidence in it and the information therein may not be correct as of the date stated.

Remarkably, among the assets listed in the document was $4.1bn of related party loans extended by Alameda, $3.3bn of which was to Bankman-Fried both personally and to an entity he controlled. Bankman-Fried previously said that FTX had “accidentally” given $8bn of FTX customer funds to Alameda.

The highlighted “related party receivable” is notable because as footnote 3 to the table reveals, it consisted of a loan by “Euclid Way Ltd. to Paper Bird Inc. (a Debtor) of $2.3 billion” and three loans by Alameda Research Ltd.: one to Mr. Bankman-Fried, of $1 billion; one to Mr. Singh, of $543 million; and one to Ryan Salame, of $55 million.

The liabilities as of September 30, 2022 were manageable. Unfortunately, the reality is that the asset and liability numbers at the consolidated level were flipped resulting in an $8 billion hole.

The problem, as we now know, is that the value of the assets was woefully overrepresented. But we’ll get to that.

First, let’s look at the immediate history that led to the bankruptcy filing:

EVENTS LEADING TO CHAPTER 11 FILING

The Debtors faced a severe liquidity crisis that necessitated the filing of these Chapter 11 Cases on an emergency basis on November 11, 2022, and in the case of Debtor West Realm Shires Inc., on November 14, 2022 (collectively, the “Petition Date”). In the days leading up to the Petition Date, certain of the circumstances described in Part III below became known to a broader set of executives of the FTX Group beyond Mr. Bankman-Fried and members of his inner circle. Questions arose about Mr. Bankman-Fried’s leadership and the handling of the Debtors’ complex array of assets and businesses.

As the situation became increasingly dire, Sullivan & Cromwell and Alvarez & Marsal were engaged to provide restructuring advice and services to the Debtors.

On November 10, 2022, the Securities Commission of the Bahamas (the “SCB”) took action to freeze assets of non-Debtor FTX Digital Markets Ltd., a service provider to FTX Trading Ltd. and the employer of certain current and former executives and staff in the Bahamas. Mr. Brian Simms, K.C. was appointed as provisional liquidator of FTX Digital Markets Ltd. on a sealed record. The provisional liquidator for this Bahamas subsidiary has filed a chapter 15 petition seeking recognition of the provisional liquidation proceeding in the Bankruptcy Court for the Southern District of New York.

In addition, in the first hours of November 11, 2022 EST, the directors of non-Debtors FTX Express Pty Ltd and FTX Australia Pty Ltd., both Australian entities, appointed Messrs. Scott Langdon, John Mouawad and Rahul Goyal of Korda Mentha Restructuring as voluntary administrators.

At the same time, negotiations were being held between certain senior individuals of the FTX Group and Mr. Bankman-Fried concerning the resignation of Mr. Bankman-Fried and the commencement of these Chapter 11 Cases. Mr. Bankman-Fried consulted with numerous lawyers, including lawyers at Paul, Weiss, Rifkind, Wharton & Garrison LLP, other legal counsel and his father, Professor Joseph Bankman of Stanford Law School. A document effecting a relinquishment of control was prepared and comments from Mr. Bankman-Fried’s team incorporated. At approximately 4:30 a.m. EST on Friday, November 11, 2022, after further consultation with his legal counsel, Mr. Bankman-Fried ultimately agreed to resign, resulting in my appointment as the Debtors’ CEO. I was delegated all corporate powers and authority under applicable law, including the power to appoint independent directors and commence these Chapter 11 Cases on an emergency basis.

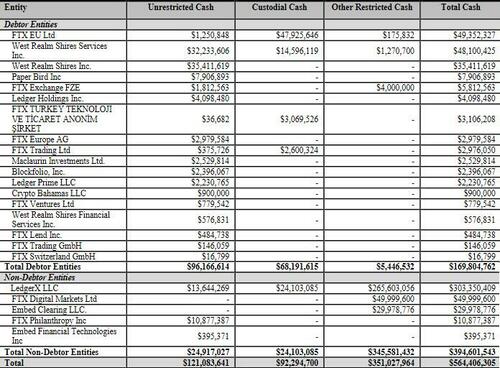

Cash management… or lack thereof:

The FTX Group did not maintain centralized control of its cash. Cash management procedural failures included the absence of an accurate list of bank accounts and account signatories, as well as insufficient attention to the creditworthiness of banking partner around the world. Under my direction, the Debtors are establishing a centralized cash management system with proper controls and reporting mechanisms.

During these Chapter 11 Cases, cash that the Debtors are able to locate and transfer to the United States without adverse consequences, including substantially all proceeds of the global reorganization effort, will be deposited into financial institutions in the United States that are approved depository institutions in accordance with the U.S. Trustee Guidelines. Each Silo will have a centralized cash pool, and the Debtors will implement appropriate arrangements for allocating costs across the various Silos and Debtors. The Debtors expect to file promptly a Cash Management Motion that will describe the new cash management system in more detail.

Because of historical cash management failures, the Debtors do not yet know the exact amount of cash that the FTX Group held as of the Petition Date. The Debtors are working with Alvarez & Marsal to verify all cash positions. To date, it has been possible to approximate the following balances as of the Petition Date based on available books and records:

The Debtors have been in contact with banking institutions that they believe hold or may hold Debtor cash. These banking institutions have been instructed to freeze withdrawals and alerted not to accept instructions from Mr. Bankman-Fried or other signatories. Proper signature authority and reporting systems are expected to be arranged shortly.

Effective cash management also requires liquidity forecasting, which I understand was also generally absent from the FTX Group historically. The Debtors are putting in place the systems and processes necessary for Alvarez & Marsal to produce a reliable cash forecast as well as the cash reporting required for Monthly Operating Reports under the Bankruptcy Code.

And now it gets really good: read this section on the company’s “Financial Reporting”

The FTX Group received audit opinions on consolidated financial statements for two of the Silos – the WRS Silo and the Dotcom Silo – for the period ended December 31, 2021. The audit firm for the WRS Silo, Armanino LLP, was a firm with which I am professionally familiar. The audit firm for the Dotcom Silo was Prager Metis, a firm with which I am not familiar and whose website indicates that they are the “first-ever CPA firm to officially open its Metaverse headquarters in the metaverse platform Decentraland.

have substantial concerns as to the information presented in these audited financial statements, especially with respect to the Dotcom Silo. As a practical matter, I do not believe it appropriate for stakeholders or the Court to rely on the audited financial statements as a reliable indication of the financial circumstances of these Silos.

The Debtors have not yet been able to locate any audited financial statements with respect to the Alameda Silo or the Ventures Silo.

Next, human resources: even more insanity here.

he FTX Group’s approach to human resources combined employees of various entities and outside contractors, with unclear records and lines of responsibility. At this time, the Debtors have been unable to prepare a complete list of who worked for the FTX Group as of the Petition Date, or the terms of their employment. Repeated attempts to locate certain presumed employees to confirm their status have been unsuccessful to date.

Nevertheless, there is a core team of dedicated employees at the FTX Group who have stayed focused on their jobs during this crisis and with whom I have established appropriate lines of authority and working relationships. The Debtors continue to review personnel issues but I expect, based on my experience and the nature of the Debtors’ business, that a large number of employees of the Debtors will need to continue to work for the Debtors for the foreseeable future in order to establish accountability, preserve value and maximize stakeholder recoveries after the departure of Mr. Bankman-Fried. As Chief Executive Officer, I am thankful for the extraordinary efforts of this group of employees, who despite difficult personal circumstances, have risen to the occasion and demonstrated their critical importance to the Debtors.

… and better: here are FTX’s “Disbursement Controls”

The Debtors did not have the type of disbursement controls that I believe are appropriate for a business enterprise. For example, employees of the FTX Group submitted payment requests through an on-line ‘chat’ platform where a disparate group of supervisors approved disbursements by responding with personalized emojis.

Digital Asset Custody… and the “use of software to conceal the misuse of customer funds.”

The FTX Group did not keep appropriate books and records, or security controls, with respect to its digital assets. Mr. Bankman-Fried and Mr. Wang controlled access to digital assets of the main businesses in the FTX Group (with the exception of LedgerX, regulated by the CFTC, and certain other regulated and/or licensed subsidiaries). Unacceptable management practices included the use of an unsecured group email account as the root user to access confidential private keys and critically sensitive data for the FTX Group companies around the world, the absence of daily reconciliation of positions on the blockchain, the use of software to conceal the misuse of customer funds, the secret exemption of Alameda from certain aspects of FTX.com’s auto-liquidation protocol, and the absence of independent governance as between Alameda (owned 90% by Mr. Bankman-Fried and 10% by Mr. Wang) and the Dotcom Silo (in which third parties had invested.

The Debtors have located and secured only a fraction of the digital assets of the FTX Group that they hope to recover in these Chapter 11 Cases. The Debtors have secured in new cold wallets approximately $740 million of cryptocurrency that the Debtors believe is attributable to either the WRS, Alameda and/or Dotcom Silos. The Debtors have not yet been able to determine how much of this cryptocurrency is allocable to each Silo, or even if such an allocation can be determined. These balances exclude cryptocurrency not currently under the Debtors’ control as a result of (a) at least $372 million of unauthorized transfers initiated on the Petition Date, during which time the Debtors immediately began moving cryptocurrency into cold storage to mitigate the risk to the remaining cryptocurrency that was accessible at the time, (b) the dilutive ‘minting’ of approximately $300 million in FTT tokens by an unauthorized source after the Petition Date and (c) the failure of the co-founders and potentially others to identify additional wallets believed to contain Debtor assets.

In response, the Debtors have engaged forensic analysts to identify potential Debtor assets on the blockchain, cybersecurity professionals to identify the parties responsible for the unauthorized transactions on and after the Petition Date and investigators to begin the process of identifying what may be very substantial transfers of Debtor property in the days, weeks and months prior to the Petition Date. The Debtors’ team includes business, accounting, forensic, technical and legal resources that I believe are among the best in the world at these activities. It is my expectation that the Debtors will require assistance from the Court with respect to these matters as the investigation and these Chapter 11 Cases continue.

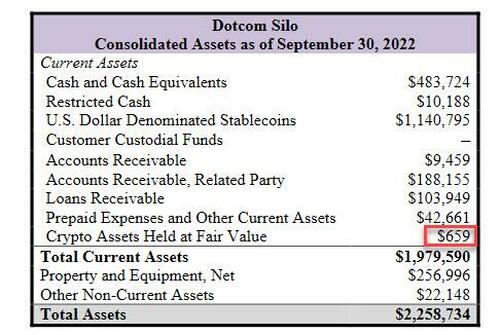

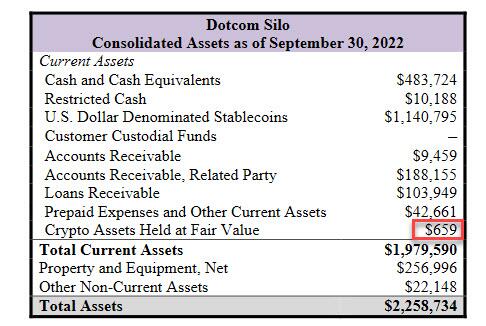

Additionally, Ray notes that the fair value of the crypto assets held by the FTX International exchange was just $659,000 as of September 30. As a reminder, SBF made this sound to be as large as $5.5bn just a few days ago. While the filing does not include an estimate of crypto assets owed to customers, but says they are expected to be “significant”.

As the FT notes, amid Ray’s first statements on the collapse of FTX, a jurisdictional fight over the company’s legal proceedings has emerged. Earlier in the week, Bahamian officials filed a Chapter 15 bankruptcy in a New York federal court asking a judge there to respect a liquidation effort that had commenced in the island nation.

At issue is an FTX subsidiary known as “FTX Digital” not involved in the US Chapter 11 case in which the Bahamas says significant customer assets reside. Ray on Thursday wrote in a court filing that the Chapter 15 case should be consolidated in the Delaware bankruptcy court.

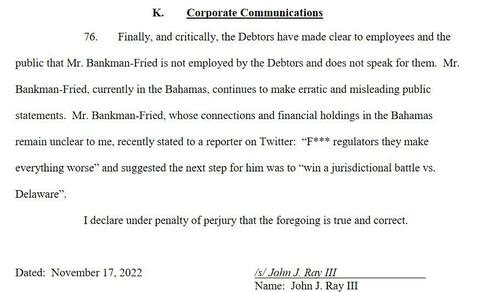

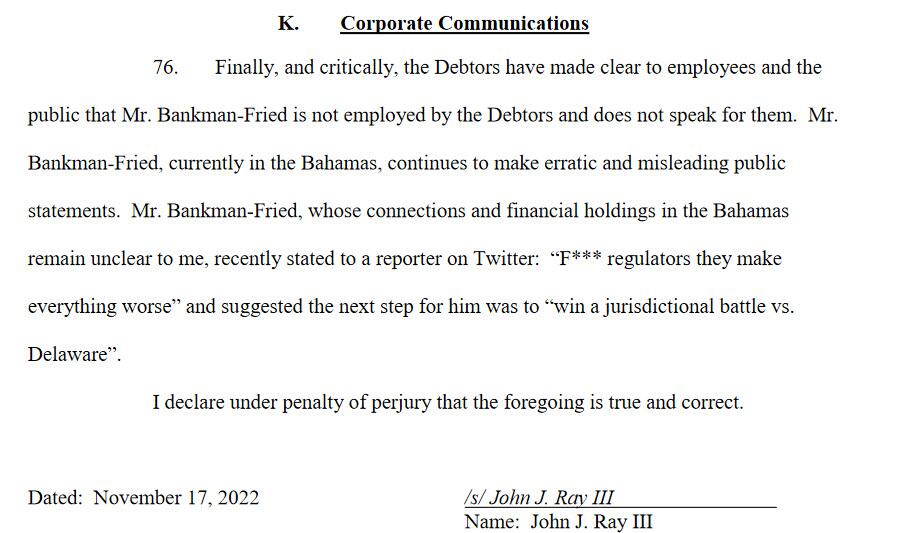

The punchline, however, was Ray’s final paragraph, a tangent on corporate communications which hardly needs discussion:

Finally, and critically, the Debtors have made clear to employees and the public that Mr. Bankman-Fried is not employed by the Debtors and does not speak for them. Mr. Bankman-Fried, currently in the Bahamas, continues to make erratic and misleading public statements. Mr. Bankman-Fried, whose connections and financial holdings in the Bahamas remain unclear to me, recently stated to a reporter on Twitter: “F*** regulators they make everything worse” and suggested the next step for him was to “win a jurisdictional battle vs. Delaware”.

To summarize:

No record of any bank accounts

No record of any cash accounts

No record of any signatories

No record of any employees

No record of any payables or receivables

No record of any investments

No record of any decision-making

No record of any board meetings

No record of anything

And, as Bryce Weiner adds, there was also no record of any chats which were set to auto-delete, so there is no record of any internal communications.

Translation: if SBF avoids prison it is only because his tens of millions in (stolen) “donations” to Democrats have bought him a get out of jail for life card.

The full affidavit is below.7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 7.0460

OFFSHORE YUAN: 7.0457

SHANGHAI CLOSED UP 50.68 PTS OR 1.64%

HANG SENG CLOSED UP 723.41 OR 4.11%

2. Nikkei closedUPN 26.70 PTS OR 0.10%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 105.98/Euro RISES TO 1.0405

3b Japan 10 YR bond yield: FALLS TO. +.239!!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 139,24/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.083%***/Italian 10 Yr bond yield FALLS to 4.058%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.109%…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.252//

3j Gold at $1785.65//silver at: 21.90 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 35/100 roubles/dollar; ROUBLE AT 60.21//

3m oil into the 85 dollar handle for WTI and 92 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 139.24DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9408–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9789well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.801% DOWN 7 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.998% DOWN 6 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,61…

GREAT BRITAIN/10 YEAR YIELD: 3.405%

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Sink To Session Lows As Sentiment Sours

BY TYLER DURDEN

THURSDAY, NOV 17, 2022 – 03:02 PM

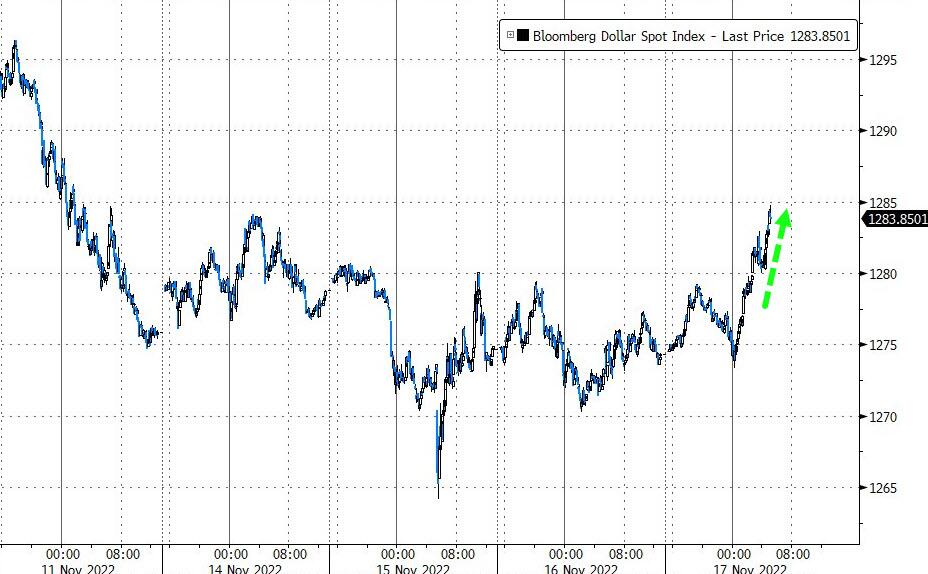

US equity futures dropped to session lows, and surrendered earlier gains of as much as 0.2%, setting up Wall Street stocks to extend Wednesday’s weakness, with traders assessing comments from Fed officials about the path of rate hikes amid earnings reports (such as those from Target) confirming that the US consumer is hunkering down for a recession. S&P 500 futures were 0.8% lower and those on the Nasdaq 100 dropped 0.6% at 7:30 a.m. in New York, with treasury yields bouncing after yesterday’s decline. 10-year Treasury yields rose, following indications from Fed officials on Wednesday that policy would tighten further. The dollar rallied half a percent against a basket of currencies.

Traders got mixed signals from policy makers, with Fed hawk Christopher Waller saying recent data have made him more comfortable with a moderate interest-rate increase of 50 basis points next month, but left the door open to a sequence of such increases if needed to curb inflation. Meanwhile, San Francisco Fed President Mary Daly said a pause in rate hikes was “off the table,” and New York Fed President John Williams said the central bank should avoid incorporating financial stability risks into its considerations.

“All this Fed talk in recent weeks starting with Powell’s press conference after the last meeting, they are indicating they are going to slow the pace of hikes,” Patrick Armstrong, CEO at Plurimi Wealth told Bloomberg TV, adding that he expected a 50 basis-point increase at the next meeting.

In premarket trading, Cisco Systems rose after the communications equipment company reported first-quarter results that beat expectations and raised its full-year forecast. Nvidia was also on the rise after topping estimates, lifting semiconductor peers AMD and Marvell. NetEase shares fell as the video game maker plans to end a 14-year partnership with Blizzard Entertainment. Bath & Body Works shares jumped the company boosted its full-year profit forecast. Here are the other notable premarket movers:

Ardelyx soars ~77% in premarket trading after its kidney disease therapy won the backing of a majority of a panel of FDA advisers. The response from analysts was mostly positive, with Piper Sandler upgrading the stock to overweight, saying it will be hard for the Food and Drug Administration to justify a rejection of the drug based on the advisory committee’s positive feedback.

Bath & Body Works shares jump ~21% in premarket trading after boosting its full-year profit forecast due to a focus on innovation and cost control. Analysts found the results to be impressive overall, noting the print was “strong” with the company reporting beats across the top line.

Elevate shares rise ~67% in premarket trading to ~$1.77 after it entered into a definitive agreement to be acquired by an affiliate of Park Cities Asset Management LLC for $1.87/share in cash, implying value of $67m.

NetEase shares fall in US premarket trading as the video game maker plans to end a 14-year partnership with Blizzard Entertainment after January, suspending services to licensed games that represented low-single-digit percentage of its revenue and net income in 2021.

Norwegian Cruise Line is double- downgraded to underperform from outperform at Credit Suisse, with the broker seeing downside risk to estimates and preferring the firm’s peers. Norwegian Cruise shares fall ~4% in US premarket trading.

Principal Financial drops ~2.4% in premarket trading after both Evercore and Morgan Stanley downgrade the stock, citing its high valuation.

Robinhood Markets shares gain ~1.4% in US premarket trading after the broker gave an operating update for October, with analysts positive on the company’s better performance during the month and early indications of stronger trading volumes for November.

Sonos jumped in postmarket trading after the speaker company reported fourth-quarter revenue that beat expectations and gave a full-year revenue forecast that is ahead of the analyst consensus.

US equities have marked a pause this week after the S&P 500 rallied 10.5% over the past month, while the Nasdaq 100 rose about 9.4% during the same period, with slowing inflation weighed against stronger-than-expected US economic data. “The market is likely to experience quite a few false bottoms” as seen in the IT sector at the moment, Jefferies strategists led by Sean Darby wrote in a note.

“We are cognizant that each time global markets attempt to rally on the back of speculation that the end of the Fed’s tightening intentions may be in sight, FOMC officials come out with a new paragraph of hawkish narrative, to tamp down any prospect of irrational exuberance,” Simon Ballard, chief economist at First Abu Dhabi Bank, wrote in a note to investors.

In Europe, the Stoxx 600 also erased gains to trade lower 0.4%. Basic resources and utilities underperformed, while food and consumer product stocks rose. The Dax outperformed while the FTSE 100 underperformed regional peers, while gilts 2-year yields rise above 3% and 10-year yields trade around 3.15%, both within Wednesday’s range. Investors braced for the release of the UK budget later in the day, while European Central Bank policy makers were said to consider a slowdown in interest-rate hikes, with only a 50 basis-point increase next month. Here are the biggest European movers”

Siemens jumps as much as 8.9% on the European engineering giant’s robust order books and outlook, which Jefferies says were well ahead of expectations and mainly driven by its division that makes factory automation software.

Chipmakers may be in focus after Nvidia posted quarterly sales that topped analysts’ estimates and Micron Technology said it was reducing production of chips due to weakening market conditions. ASML shares rose as much as 1.2%.

Subsea 7 gains as much as 7.7%, the most since March 7, after the Norwegian offshore energy firm published better-than-expected 3Q results, driven by higher margins and solid performance, Citi says.

Ocado drops as much as 9.4% after Kintbury Capital chief investment officer Chris Dale said even its bull case is for 50% downside in the stock, on expectations the UK company will struggle to finance itself.

Alstom declines as much as 6.1% — paring some of its post-earnings gains — after Morgan Stanley slashed its price target on worries about the French rail equipment maker’s balance sheet and record-low cash-flow guidance.

NN Group drops as much as 8.6%, the most since mid-August, after the insurer set new 2025 targets which Citi says may disappoint because of their “conservatism.”

Bouygues falls as much as 5.2% in Paris trading as a warning on margins at the Colas constructions unit overshadowed nine-month results from the French conglomerate that beat consensus estimates for operating income.

Embracer slides as much as 21%, the biggest intraday decline on record, after the Swedish video-game maker reduced its fiscal 2023 adjusted Ebit target, citing a delay in its Dead Island 2 game, a more challenging macro environment and a mixed reception to some of its key releases.

Earlier in the session, Asian stocks declined amid fears that Federal Reserve’s tightening still has further go to curb inflation after strong US retail sales print. The MSCI Asia Pacific Index declined as much as 1.3%, its biggest drop in a week before paring losses. Tech drove losses with Meituan, Samsung and Netease leading the gauge lower. Benchmarks in Hong Kong were notable losers in the region, with the Hang Seng Tech Index sliding as much as 5.6% before reducing the loss. They were down for a second day following rapid gains that put the gauges there into bull market territory. Equities in mainland China and South Korea also dropped while those in Japan, Australia and Singapore were slightly higher. Tencent Holdings Ltd.’s plan to pay out $20b of stock in Meituan sparked a broad selloff of Chinese internet stocks on Thursday as investors fear more divestments by the online gaming company are on the cards.

The People’s Bank of China warned inflation may accelerate as overall demand in the economy picks up, suggesting it may refrain from adding more long-term stimulus. It did still doubled short-term cash injection Thursday to ease a selloff in sovereign debt. In the US, San Francisco Fed President Mary Daly said the central bank should keep hiking, while New York Fed President John Williams said it should focus on the economy rather than financial risks as it raises rates. “The hotter-than-expected US retail sales data and hawkish leaning comments from Fed officials weighed on equities,” Saxo Capital Markets strategists including Redmond Wong wrote in a note. US retail sales posted the biggest increase in eight months in October

Japanese stocks traded range-bound as investors worried about further US interest rate hikes after San Francisco Federal Reserve President Mary Daly said that “pausing is off the table.” The Topix Index rose 0.2% to 1,966.28 as of market close Tokyo time, while the Nikkei declined 0.4% to 27,930.57. Sumitomo Mitsui Financial Group Inc. contributed the most to the Topix Index gain, increasing 2.1%. Out of 2,165 stocks in the index, 1,512 rose and 551 fell, while 102 were unchanged. “The US retail sales numbers came out higher than expected, also signaling that inflationary factors remain strong,” said Takeru Ogihara, chief strategist at Asset Management One.

Australian stocks snapped a 3-day losing streak as the S&P/ASX 200 index rose 0.2% to close at 7,135.70, boosted by strength in healthcare shares and banks. Australia’s jobless rate unexpectedly fell in October as a surge in full-time employment underpinned strong hiring, reinforcing the Reserve Bank’s arguments for further interest-rate increases. In New Zealand, the S&P/NZX 50 index rose 0.6% to 11,294.52.

Stocks in India declined, in line with global peers, as investors sought clarity over the Federal Reserve’s future policy moves and their impact on growth. Expiry of weekly derivative contracts also weighed on local shares as investors continued taking profits from recent gainers such as banks after conclusion of quarterly results season. The S&P BSE Sensex fell to close at 0.4%, its biggest drop since Nov. 10, to 61,750.60 in Mumbai, while the NSE Nifty 50 Index declined by an equal measure. For the week, the Sensex and Nifty are little changed. “With the result season now over, we expect the market to track global developments in the near term,” Motilal Oswal Financial Services analyst Siddhartha Khemka said. Mortgage lender HDFC and its banking unit provided the biggest drag to the Sensex. Out of 30 shares in the Sensex index, only eight rose and the rest fell. All but three of BSE Ltd.’s 19 sector sub-gauges closed lower, led by consumer durables stocks.

In rates, 10-year yields TSY yield add 3bps to 3.7%, while bunds 10-year yields drop 2bps to below 2%. Treasuries were cheaper by as much as 2.4bp across 10-year sector, with 3.714% yield vs session high 3.74%, following a more aggressive bear-flattening move in gilts after the UK government released its latest fiscal statement. Bunds outperform by 5bp in the sector while gilts lag by 2bp. UK curve sharply bear- flattens on the day with 2-year yield cheaper by 10bp, back above 3% level.

In commodities, crude benchmarks are under modest pressure given the USD recovery throughout the morning, generally softer APAC tone and a continuing deterioration to the China COVID case count weighing. Ags. in focus and pressured following a as-expected extension to the Black Sea grain deal. Currently, the yellow metal is holding around the lower-end of USD 1761-1774/oz parameters, and is thus a similar distance from the WTD peak of USD 1786/oz and the 10-DMA at USD 1738/oz.

WTI falls below $85. Spot gold falls roughly $8 to trade near $1,766/oz

To the day ahead now, and a key highlight will be the UK government’s autumn statement. Otherwise, data releases include US housing starts and building permits for October, the Philadelphia Fed’s business outlook index and the Kansas City Fed manufacturing index for November, and the weekly initial jobless claims. Finally, central bank speakers include the Fed’s Bullard, Bowman, Mester, Jefferson and Kashkari, the ECB’s Villeroy, and the BoE’s Pill and Tenreyro.

Market Snapshot

S&P 500 futures down 0.2% to 3,960.25

STOXX Europe 600 down 0.2% to 429.39

MXAP down 0.7% to 152.94

MXAPJ down 1.0% to 494.58

Nikkei down 0.3% to 27,930.57

Topix up 0.2% to 1,966.28

Hang Seng Index down 1.2% to 18,045.66

Shanghai Composite down 0.1% to 3,115.44

Sensex down 0.1% to 61,897.84

Australia S&P/ASX 200 up 0.2% to 7,135.65

Kospi down 1.4% to 2,442.90

German 10Y yield down 0.5% to 1.99%

Euro down 0.2% to $1.0378

Brent Futures down 0.5% to $92.39/bbl

Gold spot down 0.5% to $1,765.56

U.S. Dollar Index up 0.27% to 106.57

Top Overnight News from Bloomberg

Bank customers are the most enthusiastic about using the British pound for global payments since mid-2016, around the same time the UK voted to quit the European Union

President Joe Biden rejected Ukrainian President Volodymyr Zelenskiy‘s assertion that Russia fired a missile that landed in Poland — continuing efforts by the US and allies to de-escalate the deadly episode

Chinese regulators asked banks to report on their ability to meet short-term obligations after a rapid selloff in bonds triggered a flood of investor withdrawals from fixed-income products, according to people familiar with the matter

China will well implement agreements made by Chinese President Xi Jinping and US President Joe Biden at G-20 summit over economic policy and trade negotiations, Ministry of Commerce says

Turns out Chinese President Xi Jinping’s partnership with Vladimir Putin has limits after all: He doesn’t want to follow the Russian leader into diplomatic isolation

Brazil President-elect Luiz Inacio Lula da Silva will ask congress to circumvent a key fiscal safeguard by excluding the country’s most important social program from a public spending cap to pay for his campaign pledges

A more detailed look at global market courtesy of Newsquawk

APAC stocks traded mostly lower throughout the session following the downbeat lead from Wall Street. ASX 200 was the relative outperformer with gains lead but the Consumer Staples and IT sector, with no reaction seen in wake of the Aussie jobs data. Nikkei 225 traded on either side of the 28k mark before stabilising under the round figure, with losses modest during the session. KOSPI gave up earlier gains and drifted lower throughout the session with losses led by the chip and IT sectors, whilst sentiment in the region was soured by North Korea firing a short-range ballistic missile. Hang Seng and Shanghai Comp opened with and then extended on losses with the former seeing downside in Meituan, which fell around 6% after Tencent announced a special dividend in the form of Meituan shares, whilst People’s Daily also suggested China is able to achieve COVID Zero as mainland cases roses at the fastest pace since April.

Top Asian News

China reported 2,388 (prev. 1,623) new confirmed coronavirus cases in the mainland on Nov 16th, via Reuters

China is able to achieve COVID Zero, according to People’s Daily.

China has asked banks to report on liquidity following the sudden bond rout, according to Bloomberg.

PBoC injected CNY 132bln via 7-day reverse repos with the rate at 2.00% for a CNY 123bln net injection.

Tokyo to raise COVID alert level by one notch amid the recent rise in COVID cases, according to NTV.

BoJ Governor Kuroda said it is important to continue monetary easing to support the economy. Kuroda said recent price hikes are due to cost-push factors, according to Reuters. Kuroda said BoJ will closely coordinate with the government to conduct appropriate policy.

Senior BoJ official Uchida said it is too early to discuss the exit from monetary stimulus, via Reuters.

Saudi Arabia signed USD 30bln worth of investment agreements with South Korean firms, covering clean energy and medical tech, according to the Saudi Investment Minister

China’s Commerce Ministry, on China-US economic & trade dialogue, says will implement the key consensus reached by leaders, domestic exports/imports will see greater pressure.