Jan 11 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSED: UP $1.20 at $1875,20

SILVER PRICE CLOSED: DOWN $0.17 to $23.37

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1876.55

Silver ACCESS CLOSE: 23.40

Bitcoin morning price:, 17,418 DOWN 36 DOLLARS

Bitcoin: afternoon price: $17,533 UP 73 dollars

Platinum price closing $1074.05 DOWN $7.10

Palladium price; closing 1781.05 UP $4.70

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2519.30 DOWN $2.50 CDN dollars per oz

BRITISH GOLD: 1544.86 UP 0.30 pounds per oz

EURO GOLD: 1744,83 DOWN 3.26 euros per oz

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JANUARY 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,871.600000000 USD

INTENT DATE: 01/10/2023 DELIVERY DATE: 01/12/2023

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 7

435 H SCOTIA CAPITAL 19

657 C MORGAN STANLEY 69

661 C JP MORGAN 27

737 C ADVANTAGE 4 14

880 H CITIGROUP 73

905 C ADM 30 1

TOTAL: 122 122

MONTH TO DATE: 880

TOTAL: 15 15

JPM received 27/122 contracts (stopped)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR JAN/2023. CONTRACT: 122 NOTICES FOR 12,200 OZ or 0.3794 TONNES

total notices so far: 880 contracts for 88000 oz (2.7370 tonnes)

SILVER NOTICES: 0 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month 816 for 4,080,000 oz

END

GLD

WITH GOLD UP $1.20

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FORM THE GLD//

INVENTORY RESTS AT 914.17 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 17 CENTS

AT THE SLV// :/HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 950,000 OZ FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 508.700 MILLION OZ (THIS IS ALSO A CRIME SCENE@!!!!

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 2932 CONTRACTS TO 129,961 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.21 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. FOR THE PAST WEEK, OUR BANKERS HAVE RETURNED TO BEING NET SHORT AND THUS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.21 AND WERE SUCCESSFUL IN KNOCKING SOME SPEC LONGS, AS WE HAD A VERY STRONG LOSS ON OUR TWO EXCHANGES OF 2706 CONTRACTS. AS WELL WE HAD A ZERO OZ OF AN EXCHANGE FOR RISK TRANSFER ( 0 CONTRACTS). WE HAVE FINISHED WITH OUR SPEC SHORTS AS THEY COVERED WITH THE RISE IN PRICE . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY: BANKERS SHORT AND SPECS LONG SCENARIO.AND AS USUAL OUR SPECS GOT BEATEN UP AGAIN.

WE MUST HAVE HAD:

A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4,055. MILLION OZ FOLLOWED BY TODAY’S E.F.P’D. JUMP TO LONDON OF 5,000 OZ//NEW STANDING 4.170 MILLION OZ // V) HUGE SIZED COMEX OI LOSS/ SMALL EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –76

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN:

TOTAL CONTRACTS for 7 days, total 3283 contracts: OR 16.415 MILLION OZ PER DAY. (469 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 16.415 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 16.415 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2932 WITH OUR $0.21 LOSS IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 150 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JAN OF 4.055 MILLION OZ FOLLOWED BY TODAY’S E.F.P. JUMP OF 5,000 / //NEW STANDING DECREASES TO 4.170 MILLION OZ + EFR 2.5 MILLION = 6.670 MILLION OZ. .. WE HAVE A HUGE SIZED LOSS OF 2782 OI CONTRACTS ON THE TWO EXCHANGES FOR 13.91 MILLION OZ.. THE SILVER SHORTS HAVE BEEN HURT BADLY WITH SILVER’S RISE LATELY.

WE HAD 0 NOTICE(S) FILED TODAY FOR nil OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 5167 CONTRACTS TO 481,519 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 512 CONTRACTS.

.

THE GOOD SIZED INCREASE IN COMEX OI (5167 CONTRACTS) CAME WITH OUR $1.00 GAIN IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR JAN. AT 2.1710 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 91 CONTRACTS OR 9100 OZ //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S ) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London). NEW STANDING 2.7402 TONNES

YET ALL OF..THIS HAPPENED WITH OUR HUGE $1.00 GAIN IN PRICE WITH RESPECT TO TUESDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 7377 OI CONTRACTS (22.94 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2210 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 481,519

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7377 CONTRACTS WITH 5167 CONTRACTS INCREASED AT THE COMEX AND 2210 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 377 CONTRACTS OR 22.94 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2210 CONTRACTS) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (5167) TOTAL GAIN IN THE TWO EXCHANGES 7377 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) SMALL INITIAL STANDING AT THE GOLD COMEX FOR JAN. AT 2.1710 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 9100 OZ /NEW STANDING 2.7402 TONNES///3) ZERO LONG LIQUIDATION //4) STRONG SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JAN

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN :

18,547 CONTRACTS OR 1,854,700 OZ OR 57.689 TONNES 7 TRADING DAY(S) AND THUS AVERAGING: 2649 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAY(S) IN TONNES:57.689 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 57.689/3550 x 100% TONNES 1,63% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 57.689 TONNES INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH GOLD (

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A HUGE SIZED 2932 CONTRACTS OI TO 129,961 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 150 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 150 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 150 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2932 CONTRACTS AND ADD TO THE 150 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE LOSS OF 2782 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 13.910 MILLION OZ//

OCCURRED DESPITE OUR 21 CENT LOSS IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//CORN

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED DOWN 7.67 PTS OR0.24% //Hang Seng CLOSED UP 104/59 PTS OR 0.49% /The Nikkei closed UP 270.44 PTS OR 1.02% //Australia’s all ordinaries CLOSED UP 0.95% /Chinese yuan (ONSHORE) closed UP TO 6.7738//OFFSHORE CHINESE YUAN UP TO 6.7868// /Oil UP TO 75.47 dollars per barrel for WTI and BRENT AT 80.57 / Stocks in Europe OPENED ALL RED ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GOOD SIZED 5167 CONTRACTS UP TO 481,519 WITH OUR GAIN IN PRICE OF $1.00

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON-ACTIVE DELIVERY MONTH OF JAN… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2210 EFP CONTRACTS WERE ISSUED: ;: , . 0 FEB: 2210 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2210 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 7377 CONTRACTS IN THAT 2210 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED COMEX OI GAIN OF 5167 CONTRACTS..AND THIS STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $1.00. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG AS THEIR FOLLY INTO SHORTING HAS ENDED.

// WE HAVE A SMALL AMOUNT OF GOLD TONNAGE STANDING Jan (2.7402)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL (TOTAL SO FAR THIS YEAR 591.535 TONNES)

Dec. 64.541 tonnes

JAN/2023: 2.7402 tonnes

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $1.00) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG GAIN OF 7377 CONTRACTS ON OUR TWO EXCHANGES // WE HAVE GAINED A TOTAL OI OF 24.558 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JAN. (2.1710 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 9100 oz OR .2830 TONNES…THIS WAS ACCOMPLISHED WITH OUR RISE IN PRICE TO THE TUNE OF $1.00.

WE HAD – 512 CONTRACTS COMEX TRADES REMOVED FROM OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 14,876 CONTRACTS OR 1,487,600 OZ OR 46.277 TONNES

Estimated gold comex today 273,023// fair//

final gold volumes/yesterday 224,716/ fair

INITIAL STANDINGS FOR JAN 2023 COMEX GOLD //JAN 11//

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | nil oz . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 122 notice(s) 12200 OZ 0.3794 TONNES |

| No of oz to be served (notices) | 17 contracts 1700 oz 0.0528 TONNES |

| Total monthly oz gold served (contracts) so far this month | 880 notices 88000 2.7370 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 0

Total withdrawals: nil oz

total in tonnes: 0.0 tonnes

Adjustments:0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JANUARY.

For the front month of JANUARY we have an oi of 139 contracts having GAINED 76 contracts

We had 15 notices served on Tuesday, so we gained 91 contracts or an additional 9100 oz will stand for delivery in this

very non active delivery month of January. (queue jump)

February lost 18,118 contacts to 322,765

March gained 142 contracts to stand at 690.

April gained 21,360 contracts up to 117,566.

We had 122 notice(s) filed today for 12200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 122 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 27 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JAN. /2022. contract month,

we take the total number of notices filed so far for the month (880 x 100 oz , to which we add the difference between the open interest for the front month of (JAN. 139 CONTRACTS) minus the number of notices served upon today 122 x 100 oz per contract equals 88,100 OZ OR 2.7402 TONNES the number of TONNES standing in this non active month of January.

thus the INITIAL standings for gold for the JAN contract month:

No of notices filed so far (880 x 100 oz+ (139 OI for the front month minus the number of notices served upon today (122} x 100 oz} which equals 88,100 oz standing OR 2.7402 TONNES in this NON active delivery month of JAN..

TOTAL COMEX GOLD STANDING: 2.7402 TONNES (A POOR STANDING//COMEX RUNNING OUT OF PHYSICAL TO SERVE UPON OUR LONGS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

we had one adjustment of 110,631.591 oz Brinks

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,970,762.034 OZ 61.298 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,996,504.987 OZ

TOTAL REGISTERED GOLD:11,171,497.6431 OZ (347,46 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 11,825,007.741 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,200,735 OZ (REG GOLD- PLEDGED GOLD) 286,18 tonnes//rapidly declining

END

SILVER/COMEX

JAN 11/2023//INITIAL JAN. SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,287,830.197 oz CNT Brinks Int. Delaware |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 602,076.738 oz HSBC |

| No of oz served today (contracts) | 0 CONTRACT(S) (nil OZ) |

| No of oz to be served (notices) | 18 contracts (90,000 oz) |

| Total monthly oz silver served (contracts) | 816 contracts (4,080,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) HSBC: 602,076.738

Total deposits: 602,076.738 oz

JPMorgan has a total silver weight: 152.578 million oz/298.154 million =51.170% of comex .//dropping fast

Comex withdrawals: 3

i) Out of CNT: 602,067.271 oz

ii) Out of Brinks 592,356.810 oz

iii) Out of Int. Delaware 93,415.110 oz

Total withdrawals; 1,287,830.191 oz

adjustments: 0

total adjustment dealer to customer: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 33.195 MILLION OZ (declining rapidly).TOTAL REG + ELIG. 298.154 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR DEC

silver open interest data:

FRONT MONTH OF JAN/2023 OI: 18 CONTRACTS HAVING LOST 2 CONTRACT(S.). WE HAD 1 NOTICE

FILED ON TUESDAY SO WE LOST 1 CONTRACT(S) OR 5,000 OZ WERE E.F.P.’d TO LONDON BY THE BANKERS TO OBTAIN SOME SILVER OVER THERE.

FEB> GAINED 13 CONTRACTS TO 231 CONTRACTS

March LOST 3319 CONTRACTS UP TO 110,737 contracts

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 1 for 5,000 oz

Comex volumes// est. volume today 43,672//fair

Comex volume: confirmed yesterday: 51,600 contracts ( good)

To calculate the number of silver ounces that will stand for delivery in JANUARY. we take the total number of notices filed for the month so far at 816 x 5,000 oz = 4,080,000 oz

to which we add the difference between the open interest for the front month of JAN(18) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JAN./2023 contract month: 816 (notices served so far) x 5000 oz + OI for the front month of JAN (18 – number of notices served upon today (0) x 500 oz of silver standing for the JAN. contract month equates 4.170 million oz + 2.5 MILLION OZ OF EXCHANGE FOR RISK

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:57,337// est. volume today// good

Comex volume: confirmed yesterday: 45,745 contracts ( fair)

END

GLD AND SLV INVENTORY LEVELS

JAN 11/WITH GOLD UP $1.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FORM THE GLD////INVENTORY RESTS AT 914.17 TONNES

JAN 10/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 915.33 TONNES

JAN 9/WITH GOLD UP $ 8.60 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD//.//INVENTORY RESTS AT 915.33 TONNES

JAN 6/WITH GOLD UP $28.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 916.77 TONNES

JAN 5/WITH GOLD DOWN $17.05 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 916.77 TONNES

JANUARY 4/WITH GOLD UP $32.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.64 TONNES

JAN 3/WITH GOLD UP $20.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:STRANGE: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 917.64 TONNES

DEC 30/WITH GOLD UP $.80 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 918.51 TONNES

DEC 29//WITH GOLD UP $8.35 TODAY:; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 918.51 TONNES

DEC 28/WITH GOLD DOWN $6.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE DEPOSIT OF 5.50 TONNES INTO THE GLD..//INVENTORY REST S AT 918.51 TONNES

DEC 27/WITH GOLD UP $18.15 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 913.01 TONNES

DEC 23/WITH GOLD UP $19,15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 913.88 TONNES/

DEC 22/WITH GOLD DOWN $29.35 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 913.88 TONNES

DEC 21/WITH GOLD FLAT TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 913.88 TONNES

DEC 20/WITH GOLD UP $27.05: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES INTO THE GLD////INVENTORY RESTS AT 912.14 TONNES

DEC 19/WITH GOLD DOWN $2.10: HUGE CHANGES IN GOLD INVENTORY AT THE GLD> A BIG WITHDRAWAL OF 3.47 TONNES FROM THE GLD//INVENTORY RESTS AT 910.41 TONNES

DEC 16/WITH GOLD UP $12.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD//INVENTORY RESTS AT 913.88 TONNES

DEC 15//WITH GOLD DOWN $31.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 911.56 TONNES

DEC 14/WITH GOLD DOWN $6.20: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 912.72 TONNES

DEC 13/WITH GOLD UP $32.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD///INVENTORY RESTS AT 910.41

DEC 12/WITH GOLD DOWN $17.60: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

DEC 9/WITH GOLD UP $8.90//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

Dec 8/WITH GOLD UP $4.05, OVER THE PAST 3 WEEKS WE LOST 2.04 TONNES//INVENTORY RESTS AT 908.09 TONNES

NOV 14/WITH GOLD UP $7.30: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 910.12 TONNES

NOV 11/WITH GOLD UP $15.25//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD////INVENTORY RESTS AT 911.57 TONNES

NOV 10/WITH GOLD UP $40.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.38 TONNES

NOV 9/WITH GOLD DOWN $2.00: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES INTO THE GLD////INVENTORY RESTS AT 908.38 TONNES

GLD INVENTORY: 914,17 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JAN 11/WITH SILVER DOWN 17 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 950,000 OZ FROM THE SLV////INVENTORY RESTS AT 508.700 MILLION OZ

JAN 10/WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.65 MILLION OZ

JAN 9/WITH SILVER DOWN 9 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.65 MILLION OZ//

JAN 6/WITH SILVER UP 54 CENTS TODAY;BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.20 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 509.65 MILLION OZ//

JAN 5/WITH SILVER DOWN 50 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.10 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 505.45 MILLION OZ//

JAN 4/WITH SILVER DOWN 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 506.55 MILLION OZ/

JAN 3/WITH SILVER UP 24 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: STRANGE: A WITHDRAWAL OF 1.2 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 507.85 MILLION OZ/

DEC 30/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.050 MILLION OZ

DEC 29/ WITH SILVER UP $0.63 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.050 MILLION OZ

DEC 28//WITH SILVER DOWN 46 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.715 MILLION OZ INTO THE SLV///..INVENTORY RESTS AT 509.050 MILLION OZ

DEC 27/WITH SILVER UP 34 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 507.350 MILLION OZ//

DEC 23/WITH SILVER UP 29 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT507.900 MILLION O//

DEC 22/WITH SILVER DOWN 53 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 507.90 MILLION OZ//

DEC 21/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.0 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 507.90 MILLION OZ//

DEC 20/WITH SILVER UP 105 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV:: A DEPOSIT OF 700,000 OZ INTO THE SLV///INVENTORY RESTS AT 509.90 MILLION OZ//

DEC 19/WITH SILVER DOWN 13 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.05 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 509.20 MILLION OZ//

DEC 16/WITH SILVER UP 2 CENTS; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.85 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 508.15 MILLION OZ//

DEC 15/WITH SILVER DOWN 78 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF EXACTLY 2.00 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 510.000 MILLION OZ

DEC 14/WITH SILVER UP 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 512.000 MILLION OZ//

DEC 13/WITH SILVER UP 59 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 600,000 OZ FROM THE SLV////INVENTORY RESTS AT 513.900 MILLION OZ//

DEC 12/WITH SILVER DOWN 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 514.500 MILLION OZ//

DEC 9/WITH SILVER RISING 77 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.2 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 514.500 MILLION OZ.

DEC 8/WITH SILVER RISING 34 CENTS TODAY: OVER THE PAST 3 WEEKS, WE HAVE GAINED A STRONG: 44.777 MILLION OZ/INVENTORY RESTS AT 516.700 MILION OZ.

NOV 14/WITH SILVER UP 41 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.923 MILLION OZ//

NOV 11/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ FROM THE SLV///INVENTORY RESTS AT 471.923 MILLION OZ//

NOV 10/WITH SILVER UP 39 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 368,000 OZ INTO THE SLV///INVENTORY RESTS AT 472.476 MILLION OZ//

NOV 9/WITH SILVER DOWN 10 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV/; A WITHDRAWAL OF 3.821 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 472.108 MILLION OZ//

CLOSING INVENTORY 508.700 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

end

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

END

3. Chris Powell of GATA provides to us very important physical commentaries//

First Quantum threatens to shut vast Panama copper mine over tax dispute

Submitted by admin on Tue, 2023-01-10 10:32Section: Daily Dispatches

By Harry Dempsey and Michael Stott

Financial Times, London

Tuesday, January 10, 2023

First Quantum Minerals has threatened to close its vast copper mine in Panama if it fails to resolve a tax dispute that it says risks damaging the country’s business-friendly reputation.

Panama has demanded that the Canadian group pay corporate tax of at least $375 million a year along with a profit-based mineral royalty of 12-16%, a steep rise on the $61 million FQM paid to Panama on a project that raked in $1.4 billion of gross profit in 2021.

The Canadian group’s chief executive Tristan Pascall said it would put its flagship project, responsible for 1.4% of global copper supply, into “care and maintenance” if the country did not offer certain legal protections.

“Regrettably we would be compelled to follow that directive if the terms cannot be resolved on a reasonable basis,” he told the Financial Times. …

… For the remainder of the report:

https://12ft.io/proxy?q=https%3A%2F%2Fwww.ft.com%2Fcontent%2F824f7c46-8c16-48de-955e-3bd916c097a7

END

(GATA) Ronan Manly: China’s gold purchase announcements have strategic purpose

2p ET Wednesday, January 11, 2023

Dear Friend of GATA and Gold:

Bullion Star researcher Ronan Manly writes today that China’s announcements of gold purchases are made strategically, to remind the world that China is a big power in the currency markets, and that while many months may pass without such announcements, China is probably acquiring gold steadily anyway in pursuit of a plan to hold the world’s largest gold reserve.

Indeed, Manly adds, China already may be nearing that point.

His analysis is headlined “Chinese Central Bank Kicks off New Round of Gold Accumulation” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/ronan-manly/chinese- central-bank-kicks-off-new-round-of-gold-accumulation/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

With Musk’s support and ETFs doubtful, silver is explosive, GATA chairman says

Submitted by admin on Tue, 2023-01-10 22:02Section: Daily Dispatches

10p ET Tuesday, January 10, 2023

Dear Friend of GATA and Gold:

GATA Chairman Bill Murphy, interviewed by GoldSeek Radio’s Chris Waltzek, remarks that silver as an investment is even more explosive now that multi-billionaire Elon Musk is promoting the monetary metal, especially as the major silver exchange-traded funds are falling under suspicion. The interview is 13 minutes long and can be heard at GoldSeek’s companion site, SilverSeek, here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

4. Other gold/silver commentaries

Saudi Arabia Looks To Invest In Mining Assets To Secure Critical Minerals

WEDNESDAY, JAN 11, 2023 – 02:05 PM

Authored by Tsvetana Paraskova via OilPrice.com,

Saudi Arabian Mining Company (Ma’aden) has signed an agreement with the Saudi sovereign wealth fund, the Public Investment Fund, to set up a joint company that will invest in mining assets abroad to secure strategic minerals.

Under the joint venture agreement, Ma’aden will own 51% of the new company, while the Public Investment Fund (PIF) will own the remaining 49%, Ma’aden said in a statement on Wednesday.

The joint company plans to initially invest in the iron ore, copper, nickel, and lithium sectors as a non-operating partner taking minority equity positions, Ma’aden said.

“This will provide physical offtake of critical minerals to ensure supply security for domestic minerals downstream sectors and positioning Saudi Arabia as a key partner in global supply-chain resilience,” the company noted.

Separately, Ma’aden announced an agreement to buy 9.9% in U.S.-based technology firm Ivanhoe Electric Inc for $126.4 million and form with Ivanhoe Electric, a Saudi-based joint venture company, to explore and develop mining projects in Saudi Arabia.

According to Ma’aden’s statement, Ivanhoe Electric “applies a suite of technological solutions to dramatically increase the quality and efficiency of metals-focused exploration campaigns, which aligns with Ma’aden’s strategy to gain leverage of commodities with long-term growth potential.”

In October 2021, the top executive of the state miner of the world’s top oil exporter said that the company plans “huge” investments in exploring for lithium and nickel in Saudi Arabia over the next two decades.

“In the next 10 to 20 years we are going to spend huge amount of money looking for those metals in Saudi Arabia,” Maaden’s chief executive officer Abdulaziz Al Harbi told Bloomberg at the time, asked about the key battery metals lithium and nickel.

The world’s largest oil exporter is thus betting on critical battery metals, whose demand is set to grow exponentially in the energy transition.

END

6/CRYPTOCURRENCIES/BITCOIN ETC

FTX Boss SBF Aided Biden’s CIA Agenda For Weapons To Ukraine – Part 4

| Robert Hryniak | 10:15 AM (21 minutes ago) | ||

| to | |||

If you want to understand FTX and the scandal or criminal plot associated, have a read. Because this is on the same scale as the Iran-Contra scandal if not more. Fast and Furious was another scandal gun running.

And what we see in human deaths in the Ukrainian today is the fallout. And we have yet to see the truth about the bio labs so far covered up that lead to top of corrupt leadership.

https://rense.com/general97/ftx-crypto-pt4.php

END

.

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: UP TO 6.7838

OFFSHORE YUAN: 6.7868

SHANGHAI CLOSED DOWN 7.67 PTS OR 0.24%

HANG SANG CLOSED UP 104.59 PTS 0.49%

2. Nikkei closed UP 270.44 PTS OR 1.02%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 103,18 Euro FALLS TO 1.0732 DOWN 7 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.500!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 132.67/JAPANESE YEN RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.2214%***/Italian 10 Yr bond yield FALLS to 4.077%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.232…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.216//

3j Gold at $1877.40//silver at: 23.79 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 1 AND 17/100 roubles/dollar; ROUBLE AT 68.62//

3m oil into the 75 dollar handle for WTI and 80 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 132.21

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9268– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9940 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

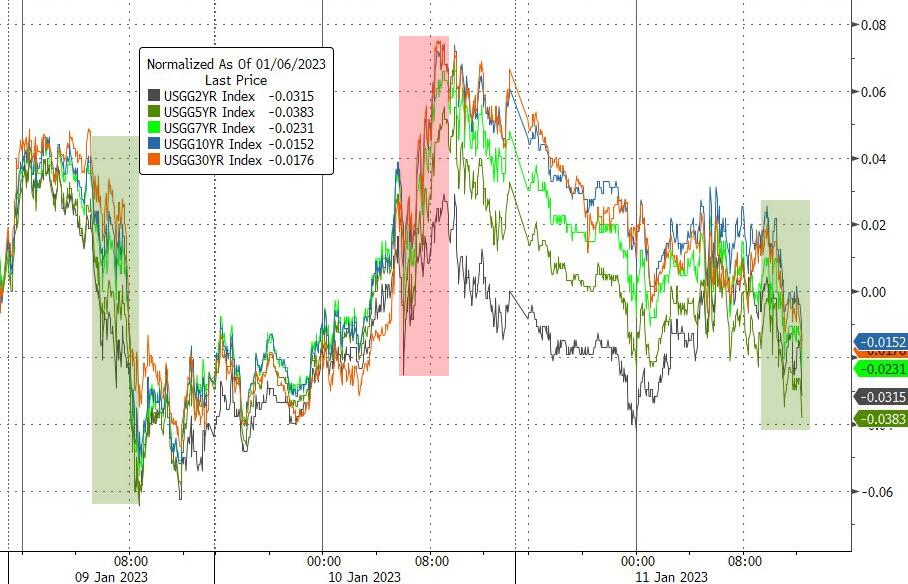

USA 10 YR BOND YIELD: 3.578% DOWN 4 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.706% DOWN 5 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,78…

GREAT BRITAIN/10 YEAR YIELD: 3.4715 % DOWN 9 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Rise Ahead Of Inflation Data As China Reopening Lifts Sentiment Again

WEDNESDAY, JAN 11, 2023 – 08:04 AM

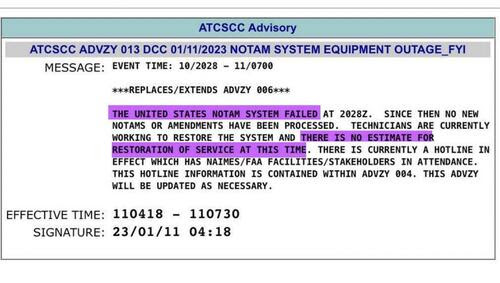

US equity futures were set to rise for a second day as upbeat sentiment ahead of tomorrow’s key CPI print – which JPM gives 85% odds of pushing stocks at least 1.5% higher – lifted global markets despite a freak outage of key FAA advisory system this morning led to a nationwide ground halt for all domestic flights (until at least 9am) pre. Contracts on the S&P 500 and Nasdaq 100 ticked up 0.1% as of 7:15am ET while Europe’s Stoxx 600 Index rose 0.8%. The FTSE 100 climbed within striking distance of a record high; Asian equities were supported by China lifting Covid restrictions. Among the top corporate news, Credit Suisse weighs cutting by half the bonus pool for 2022 after a turbulent year and Apple plans to start using its own custom displays in mobile devices as early as next year. Treasury yields dropped and the dollar gained for the second day in a row.

Among US premarket movers, airline stocks slipped in New York premarket as the failure of a key pilot notification system operated by the Federal Aviation Administration disrupted air travel. American Airlines Group Inc. fell 1.1% and United Airlines Holdings Inc. was down 0.6%. Delta Air Lines Inc. fell 0.8% as the FAA ordered a ground halt of all flights until at least 9am. Bed Bath & Beyond surged again and were on course for a third day of gains. World Wrestling Entertainment rose as much as 5.3%, extending a rally sparked by speculation that the company may sell itself. Chairwoman and co-CEO Stephanie McMahon announced she’s resigning from the company. Here are some other notable premarket movers:

- US biotech Prokidney surges 34% after early data from a mid-stage trial of its cell therapy for chronic kidney disease. Jefferies said the treatment has multi-billion dollar potential.

- CarMax falls 4.8% after JPMorgan cut its recommendation on the used-car retailer to underweight from neutral, citing unfavorable risk-reward following recent outperformance.

- JinkoSolar Holding ADRs rise 1.9% after Roth Capital upgrades the solar panel maker to buy, saying US policy improvements point to a stronger outlook.

- Levi Strauss drops 1.5% as Citi downgrades to neutral from buy to reflect what it describes as a challenging US backdrop in the near to medium term.

- Keep an eye on PTC and Autodesk as Berenberg begins coverage of both US design software companies with buy ratings, and initiates AspenTech at hold, saying all three have the potential to continue outperforming the industry in terms of growth.

- Data and analytics providers could be in focus as Redburn says they will have a significant opportunity to capitalize on growing and increasingly complex risk factors in financial markets. The broker has buy ratings on MSCI (MSCI US), S&P (SPGI US) and London Stock Exchange (LSEG LN), though initiates Verisk (VRSK US) at sell and cuts Morningstar (MORN US) to neutral.

The gains of US stocks since the start of 2023 has surprised many (very bearish) strategists who believe that much of the advance is conditional on inflation easing, which would allow the Federal Reserve to slow the pace of rate hikes. And while hawkish comments on Monday by San Francisco and Atlanta Fed presidents put a chill on the rally, a lack of subsequent reinforcement by Chair Powell led to a sharp rally on Tuesday. The next test for the market comes on Thursday with the US inflation report which will determine if the Fed hikes by 25bps or 50bps on Feb 1, and it’s widely believed that a lower-than-expected reading would trigger further gains. Investors are also closely watching technical levels as the S&P 500 Index nears its 200-day moving average.

“Tomorrow’s CPI event risk could be a decider where the S&P 500 can either break above its 200-day moving average, the 4,000 level and the downtrend line, or we head back to 3800,” says Gurmit Kapoor, a cross-asset sales trader at Aurel BGC.

While Powell didn’t directly comment on the Fed’s next steps at a forum in Stockholm, he did say that “restoring price stability when inflation is high can require measures that are not popular in the short term as we raise rates to slow the economy.”

Fed Governor Michelle Bowman said the central bank has more work to do to curb inflation, noting that further tightening is needed.

“We do expect an inflection in central bank policy later on this year,” said Mark Haefele, chief investment officer at UBS Global Wealth Management. “More risk-tolerant investors can look to anticipate this turn by phasing into markets, seeking early winners from a global improvement in sentiment, and identifying beneficiaries from China’s reopening. “However, we don’t believe we have yet reached the inflection point in policy or economic growth, and as we enter 2023 we continue to favor a defensive tilt when adding exposure in both equity and fixed-income markets,” he said.

“The prospect of a less cloudy economic outlook in both Europe and the US after recession risks in both regions eased back, combined with the reopening of the Chinese economy, is providing strong support toward risk appetite from investors,” said Pierre Veyret, a technical analyst at ActivTrades. “The lack of clear hints from Fed Chairman Jerome Powell yesterday also contributed to keeping the bullish trading stance alive, and most traders will now look toward tomorrow’s US inflation print for further clues.”

In Europe, real-estate and mining stocks led a 0.4% gain in the Stoxx Europe 600 Index amid subsiding inflation worries. Miners were boosted by optimism China’s economic reopening will spur demand for metals. Among the top corporate news, Credit Suisse weighs cutting by half the bonus pool for 2022 after a turbulent year. Here are some of the biggest European movers on Wednesday:

- Vestas shares jump as much as 5.6%, the most in a month, after being raised to buy at Jefferies, which says an inflection point has been reached for wind-turbine manufacturers

- JD Sports shares jump as much as 6.5%, reaching April highs, after the sports retailer said it sees headline pre-tax profit toward the top end of current market expectations

- TeamViewer shares gain as much as 7.3% after the software company reported preliminary 4Q billings. RBC says the firm posted “a surprisingly stronger- than-expected finish to the year”

- Corbion rises as much as 11%, reaching an almost 11-month high, after Barclays upgrades to overweight in note on “renewed conviction” following the Dutch ingredients maker’s CMD

- Bang & Olufsen rises as much as 4.5% on better-than-expected 2Q results. Nordnet says “B&O does what it can and maybe even a little more” despite a challenging environment

- Grafton shares rise as much as 4.7% after it predicted its profit will be at the top end of analysts’ forecasts. Investec expects 2022 underlying consensus profit to edge up

- Direct Line shares slump 30%, pulling peers down with it, after saying it no longer expects to pay a final dividend; news that is likely to be a “major shock” to the market, Jefferies says

- Adyen declines as much as 3.4% after BofA cuts the stock to neutral, saying risks of further slowdown in e-commerce sales and margin compressions are not properly accounted for

- Maersk shares fall as much as 4.1%, the most since November, after Goldman Sachs cut its recommendation to sell, anticipating a “great unwind” in air and sea freight markets

- Eurofins Scientific declines as much as 4.9% and is among the worst performers on France’s SBF 120 index after two brokers cut their recommendations for the French laboratory group

Earlier in the session, Asia’s equity benchmark resumed its advance, led by gains in key regional markets including Japan, South Korea and Hong Kong. The MSCI Asia Pacific Index climbed as much as 0.9% to the highest level in almost five months before paring about half of its gain. Tencent and Alibaba were the top contributors, with tech and communication services among the major sectoral boosters.

“A lot of traders and investors see the US being closer to peak inflation — if we have not already passed that point. Then that as a corollary also indicates an end to global central bank rate hike cycles,” said Justin Tang, head of Asian research at United First Partners. Though Chinese shares dropped on Wednesday, with liquor giant Kweichow Moutai among the decliners, investor sentiment remains bullish amid further signs of fading regulatory risks in the tech sector as well as more support coming for property developers. The dramatic recovery in Chinese equities, with a gauge of mainland companies listed in Hong Kong up more than 40% in about two months, helped the broad Asian benchmark enter a bull market this week. The key gauge is outperforming US peers so far in 2023 boosted by optimism over China’s reopening and a weakening dollar.

“In general the Chinese markets have been a pretty tough place to invest for almost five years now. So that recovery we’ve seen from below, there’s still a lot of value, support in the marketplace,” David Perrett, co-head of Asian equities at M&G Investment Management, said in an interview with Bloomberg TV

In FX, the Bloomberg dollar gauge rose, after hovering near a seven-month low and the greenback was mixed against its Group-of-10 peers, though most currencies traded in relatively narrow ranges. The euro traded in a narrow $1.0726-1.0757 range

- The Australian dollar led G-10 gains after solid inflation and retail sales prints for November reinforced expectations for a quarter-percentage-point interest rate hike at the Reserve Bank’s first meeting of the year next month. CPI advanced 7.4% seasonally adjusted from a year earlier, up from 6.9% in October and exceeding economists’ median estimate. Core prices, or the trimmed-mean gauge, climbed to 5.6% in November compared with a forecast 5.5%. Retail sales beat most estimates.

- The yen was sandwiched between large options expiring on Wednesday. Japan’s 30-year bonds gained after an auction of this tenor met resilient demand and the central bank announced unscheduled debt purchases.

- The Egyptian pound plunged 5% against the US dollar on Wednesday, after the International Monetary Fund said authorities were showing commitment to a flexible exchange rate.

In rates, treasury yields trimmed their advance from the previous session as yields shed up to 6bps as the curve bull-flattened and with the rate on 10-year debt slipping to below 3.58% as investors remained focused on the price outlook for the US. UK spreads flatter, leading core European rates higher with 2s10s, 5s30s tighter by 5.5bp and 2.5bp on the day; Bunds also bull-flattened and outperformed Treasuries as money markets eased ECB tightening bets before a German 10-year bond sale. Focus is also on scheduled ECB speeches. Japan’s 30-year bonds gained after an auction of this tenor met resilient demand and the central bank announced unscheduled debt purchases.

In commodities, oil reversed an earlier decline as traders weighed the outlook for stronger Chinese demand against a reported build in US crude stockpiles. Optimism over demand from China was evident in the iron ore market, with the steel-making ingredient rallying above $120 a ton in Singapore. Copper rose above $9,000 a ton for the first time since June, fueled by hopes of increased consumption by the world’s top user of the metal.

Looking to the day ahead now, it’s a quiet day and data releases include US Mortgage applications. Otherwise, central bank speakers include the ECB’s Holzmann, Villeroy and De Cos.

Market Snapshot

- S&P 500 futures up 0.2% to 3,948.50

- MXAP up 0.5% to 162.36

- MXAPJ up 0.3% to 535.96

- Nikkei up 1.0% to 26,446.00

- Topix up 1.1% to 1,901.25

- Hang Seng Index up 0.5% to 21,436.05

- Shanghai Composite down 0.2% to 3,161.84

- Sensex little changed at 60,124.03

- Australia S&P/ASX 200 up 0.9% to 7,195.34

- Kospi up 0.3% to 2,359.53

- STOXX Europe 600 up 0.5% to 448.06

- German 10Y yield little changed at 2.25%

- Euro up 0.1% to $1.0746

- Brent Futures up 0.8% to $80.75/bbl

- Brent Futures up 0.8% to $80.76/bbl

- Gold spot up 0.5% to $1,885.60

- U.S. Dollar Index little changed at 103.25

Top Overnight News from Bloomberg

- The collective hive mind of Wall Street is backing a view that the euro rally is just getting started. With energy prices tumbling and calls for a region-wide recession falling to the wayside, a clear narrative is emerging that the worst of the economic damage is over and European assets are cheap

- In Germany, Italy and Spain — three of the currency bloc’s top four economies — anxiety at inflation over the next year is close to or below the average since the euro was introduced in 1999, European Commission data show

- Only a slowdown in core inflation can alter the ECB’s resolve to raise interest rates, according to Governing Council member Robert Holzmann

- The ECB needs to be pragmatic as it raises interest rates in the coming months to get to a level by the summer that is sufficiently high to bring inflation back toward 2%, Governing Council member Francois Villeroy de Galhau said

- The French economy continued to grow at the end of 2022 and should avoid a contraction in the first weeks of the year despite headwinds from surging energy prices, a Bank of France survey showed

- China shouldn’t bail out the debt that local governments take off their balance sheets so as to discourage them from allowing hidden liabilities to snowball out of control, according to former Finance Minister Lou Jiwei

- Japan’s Finance Ministry will likely issue sovereign bonds to fund decarbonization efforts from the latter half of fiscal year 2023 after assessing investor needs, Michio Saito, a senior official at the ministry, says in a TV Tokyo interview

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks initially tracked the advances on Wall Street after Fed Chair Powell refrained from any major policy rhetoric and as participants looked ahead to upcoming US CPI data with hopes of softening price growth. ASX 200 tested the 7,200 level to the upside with the index led by outperformance in the mining and materials sectors, while participants also digested better-than-expected Retail Sales and a pickup in monthly inflation metrics. Nikkei 225 gained as earnings trickled in with outperformance in Yaskawa Electric after growth in its top and bottom lines, while there was encouragement from news that Fast Retailing will boost wages by as much as 40%. Hang Seng and Shanghai Comp were firmer for a bulk of the session after the PBoC pledged support measures including for the property sector and boosted its short-term liquidity efforts ahead of next week’s Lunar New Year celebrations, although gains were capped in the mainland after the recent mixed loans and aggregate financing data.

Top Asian News

- PBoC injected CNY 65bln via 7-day reverse repos with the rate kept at 2.00% and it injected CNY 22bln via 14-day reverse repos with the rate kept at 2.15% for a CNY 71bln net daily injection.

- Analysts noted there is room for China to cut RRR and interest rates this year, while analysts also see room for a rate cut in the property sector, according to China Securities Journal.

- BoJ offered to buy JPY 100bln in 1-3yr JGBs, JPY 100bln in 3-5yr JGBs, JPY 300bln in 5yr-10yr JGBs, JPY 200bln in 10yr-25yr JGBs and JPY 50bln in 25yr+ JGBs, while it also offered to buy an unlimited amount of JGBs at a fixed rate with maturities of 1yr-3yr and 3yr-5yr in an unscheduled announcement.

- Stocks Climb Amid Optimism Over Inflation, China: Markets Wrap

- Egypt Pound Plunges 5% in Test of Shift to Currency Flexibility

- Russia to Restart FX Operations in Yuan Under Fiscal Rule

- Philippine Finance Chief Sees Rate Hike Cycle Nearing End

European bourses are firmer across the board, Euro Stoxx 50 +0.8%, with an easing in yields seemingly spurring a modest extension of opening gains. Sectors are primarily in the green, though Insurance names are pressured in sympathy with Direct Line while Retail-related stocks are supported after updates from the likes of JD Sports. US futures posting marginal gains, ES +0.2%, with the US docket particularly thin ex-supply ahead of Thursday’s CPI. US FAA has reported a system equipment outage, all flights nationwide have been grounded, according to a source familiar with the situation, cited by NBC Washington reporter.

Top European News

- ECB’s Villeroy says they will need to be pragmatic on speed of hikes, will have to raise rates more in the coming months. Should aim to reach the terminal rate by the summer. Domestic inflation is likely to peak in H1, will avoid hard landing scenario.

- ECB’s Holzmann says rates will need to rise significantly further to reach levels that are sufficiently restrictive to ensure a timely return of inflation to target. Inflation is expected to subside but risks remain to the upside. There are no signs of de-anchored market expectations.

- Activist Coast Capital Sells Vodafone Stake Within a Year

- Russia to Sell Yuan From Wealth Fund as Oil Price Hits Budget

- Ukraine Latest: Zelenskiy Says Russian War Won’t Turn to WWIII

- Direct Line Shares Tumble as Insurer Cuts Dividend on Claims

FX

- DXY forms a foothold on 103.000 handle within a tight band post-Powell and pre-US CPI.

- Aussie outperforms on perky inflation metrics, strong retail sales data and gains in iron ore prices, AUD/USD holds near 0.6900 and AUD/NZD rebounds from around 1.0800 to top 1.0850.

- Euro retains grasp of 1.0700 handle, but Sterling sags around 1.2150 axis and Yen weakens after closing below a Fib to circa 132.75 and away from decent option expiries at 132.50.

- PBoC set USD/CNY mid-point at 6.7756 vs exp. 6.7776 (prev. 6.7611)

Fixed Income

- Core benchmarks continued to gain momentum throughout the morning with little clear sign of concession pre-supply and perhaps deriving some support from ECB remarks.

- However, the rally has run out of steam with a sub-par German outing aiding the pullback, with Bunds and Gilts now sub 137.00 and 103.00 respectively.

- Stateside, USTs have been following suit and it remains to be seen if the looming 10yr supply will influence broader action, an auction which follows Tuesday’s strong 3yr.

- UK DMO is to launch a new conventional Gilt maturing October 2053 in the week commencing January 23rd.

Commodities

- WTI and Brent have experienced a firmer start to the mid-week session, with the benchmarks posting upside of around USD 0.30/bbl within relatively narrow ranges that keeps the complex within WTD and recent parameters

- US and allies are reportedly preparing the next round of sanctions on Russian oil, via WSJ; intending to cap the sales price of Russian exports of refined petroleum products.

- Russian Kremlin, on possible losses from oil price caps, says there have been hardly any cases of the caps yet.

- Chinese Commerce Ministry will continue to impose anti-subsidy tariffs on dried distillers grains with solubles (DDGS) imported from the US.

- Standout mover has been LME Copper which eclipsed the USD 9k mark in an extension of yesterday’s price action after fairly contained/rangebound APAC trade for base metals.

- Spot gold is modestly firmer and resides towards the top-end of a USD 1872-1886/oz range, which is a fresh multi-month high leaving the figure itself as resistance before the May 2022 USD 1909/oz peak.

Geopolitics

- Russia’s ambassador to the US commented that the US training of Ukrainian troops on Patriot systems confirms Washington’s de facto participation in the conflict and that the US administration’s goal is to inflict the most damage on Russia on the battlefield by the hands of Ukrainians, according to Reuters.

- Russian Kremlin says there is a positive dynamic in the military situation around Ukrainian town of Soledar Putin is open to discussions on Ukraine.

- Russian Rights Commissioner says important ceasefire proposals have been made during her meeting with Turkish and Ukrainian colleagues in Turkey, via Reuters.

- Russia and Iran are working on a new shipping corridor to bypass sanctions and are looking to work with India, according to Nikkei. ]

US Event Calendar

- 07:00: Jan. MBA Mortgage Applications 1.2%, prior -10.3%

DB’s Jim Reid concludes the overnight wrap

Morning from Helsinki where snow is on the ground. This is the start of a whistle stop 4 countries in 2 days 2023 outlook tour. I’ve been coming here around this week every year for about the last 25, apart from the last 2 due to Covid. So it’s nice to have the old routine back. In the past I’ve landed in wild snow storms, seen the temperature hit -20c, seen piles and piles of snow, and yet everything always runs. Impressive! This year it’s all fairly calm with the temperature just above zero.

Markets have also been relatively quiet over the last 24 hours as we await tomorrow’s all important US CPI print. There was some speculation that remarks from Fed Chair Powell could inject some volatility into proceedings but overall markets turned steadily higher after his lack of commentary on the policy outlook at his panel in Stockholm.

Looking through the various moves yesterday, some of the biggest came from longer-dated core sovereign bond yields. For instance, yields on 10yr Treasuries were up +8.7bps to 3.619%, marking their biggest daily increase so far this year, and taking yields up to their highest level since the weak ISM services release last Friday. We have given back -3bps of that climb in Asia as I type. The rise yesterday though came as investors took out some of the dovish expectations for the Fed they’d been pricing over recent days, with the futures-implied rate for end-2023 up by +2.0bps on the day to 4.459%. Separately, we also heard from the Treasury Department that they were increasing the size of their T-bill auctions. It comes with many expecting that they’ll soon announce extraordinary measures in order to avoid exceeding the statutory cap imposed by the debt ceiling.

Sticking with the US Treasury Department, it was reported yesterday that Treasury Secretary Yellen has agreed to remain in her post after having been asked to by President Biden last month. This is a confirmation of Secretary Yellen’s own professed wished from back in November when she said she intended to stay through the entirety of Biden’s first term. This means at least one part of the upcoming debt ceiling negotiations will have some stability. Bloomberg reported that the Biden administration was preparing to turnover some cabinet-level positions now that the midterms are over.

Over in Europe it was a similar story, with yields on 10yr bunds (+8.0bps) seeing the largest increase on the day, along with smaller increases for OATs (+7.0bps) and BTPs (+3.6bps). And as in the US, the moves occurred with investors taking out some of the dovishness priced for the ECB, which got further support after the ECB’s Schnabel said that “interest rates will still have to rise significantly” and that “inflation will not subside by itself”.

When it comes to the Fed, we did hear from Chair Powell yesterday, but despite the anticipation he didn’t comment on the policy outlook. He was speaking on a panel on central bank independence, and stuck to that topic by defending the merits of an independent monetary policy. Interestingly, he acknowledged that “restoring price stability when inflation is high can require measures that are not popular in the short term as we raise interest rates to slow the economy.” Otherwise, he explicitly said that the Fed should “stick to our statutory goals and authorities”, and said that they would not be a “climate policymaker”. With little to go off from Powell, the focus will now turn to tomorrow’s US CPI release for December.

With Powell not taking a hawkish tone, equities drifted higher after Europe logged off. The S&P 500 ticked +0.70% higher, with both the NASDAQ (+1.01%) and the Dow Jones (+0.56%) also rising. The rally had a distinct risk-on tone with communications (+1.29%) and consumer discretionary (+1.26%) names outperforming while defensives like staples (-0.16%) and utilities (+0.04%) lagged. Having closed beforehand and catching up to the US reversal late Monday, European equities pulled back with the STOXX 600 down -0.59% on the day.

Asian markets are stronger this morning. As I type, the Nikkei (+1.02%) is leading gains followed by the Hang Seng (+1.01%), the KOSPI (+0.40%), the CSI (+0.22%) and the Shanghai Composite (+0.20%). Outside of Asia, stock futures in the US are fluctuating with contracts on the S&P 500 (+0.04%) just above flat while those on the NASDAQ 100 (-0.05%) are trading fractionally lower. Meanwhile, European futures tied to the DAX (+0.55%) are catching back up.

Early morning data showed that inflationary pressures are yet to ease in Australia as CPI advanced +7.3% y/y in November (v/s +7.2% expected), up from a surprise pullback to +6.9% in October. The latest inflation reading is at its highest level in 30 years with housing costs being the main contributor to the annual increase. Separately, retail sales rebounded +1.4% m/m in November, buoyed by consumer appetite for Black Friday sales despite rising interest rates and high inflation. Market expectations were for a +0.6% gain as against October’s upwardly revised +0.4% rise. The Australian dollar (+0.39%) nudged higher against the dollar, trading at $0.69 on the prospect of more interest rate hikes by the Reserve Bank of Australia (RBA).

In commodity news, copper prices are trading at the highest level since June inching towards $9,000 a ton as China’s exit from the Zero Covid policy enhanced the demand outlook of the commodity.

Elsewhere yesterday, the French government outlined a plan that would see the country’s retirement age rise to 64 by 2030, up from 62 at present. Moves to reform the pension system have long been an ambition of President Macron’s, but a previous attempt in his first term was postponed during the Covid-19 pandemic, and there remains opposition from trade unions and some other political parties. Macron’s party no longer has an absolute majority in parliament either, but they have made some concessions to the conservative Les Républicains to try and secure their votes.

In other news, the World Bank released their latest round of economic projections yesterday, with their global growth projection for 2023 now at +1.7%, marking a downgrade from their +3.0% forecast back in June. Those downgrades were mainly driven by the advanced economies, where growth is now seen at just +0.5% (vs. +2.2% in June), but the forecasts for emerging market and developing economies were also lowered, with this year’s growth now seen at +3.4% (vs. +4.2% in June).

Finally, there wasn’t a great deal of other data yesterday. One release in the US was the NFIB’s small business optimism index, which fell more than expected to 89.8 in December (vs. 91.5 expected). That’s the second-lowest reading in over a decade. Elsewhere, French industrial production grew by a faster-than-expected +2.0% in November (vs. +0.8% expected).

To the day ahead now, and data releases include Italian retail sales for November. Otherwise, central bank speakers include the ECB’s Holzmann, Villeroy and De Cos.

AND NOW NEWSQUAWK (EUROPE/REPORT)

Sentiment supported amid a pullback in yields, with just US 10yr supply due – Newsquawk US Market Open

WEDNESDAY, JAN 11, 2023 – 06:32 AM

- European bourses are firmer across the board, Euro Stoxx 50 +0.8%, with an easing in yields seemingly spurring a modest extension of opening gains.

- US FAA has reported a system equipment outage, all flights nationwide have been grounded, according to a source familiar via NBC

- DXY has consolidated above 103.00 to the modest detriment of peers, ex-antipodeans and Euro.

- The initial rally in fixed income has run out of steam and pulled back from best amid sub-par German supply ahead of a USD 10yr

- Crude benchmarks are posting modest gains while LME Copper has eclipsed USD 9k and spot-gold prints a fresh multi-month high

- Looking ahead, highlights include EIA Inventories & supply from the US.

View the full premarket movers and news report.

Or why not try Newsquawk’s squawk box free for 7 days?

EUROPEAN TRADE

EQUITIES

- European bourses are firmer across the board, Euro Stoxx 50 +0.8%, with an easing in yields seemingly spurring a modest extension of opening gains.

- Sectors are primarily in the green, though Insurance names are pressured in sympathy with Direct Line while Retail-related stocks are supported after updates from the likes of JD Sports.

- US futures posting marginal gains, ES +0.2%, with the US docket particularly thin ex-supply ahead of Thursday’s CPI.

- US FAA has reported a system equipment outage, all flights nationwide have been grounded, according to a source familiar with the situation, cited by NBC Washington reporter.

- Click here for more detail.

FX

- DXY forms a foothold on 103.000 handle within a tight band post-Powell and pre-US CPI.

- Aussie outperforms on perky inflation metrics, strong retail sales data and gains in iron ore prices, AUD/USD holds near 0.6900 and AUD/NZD rebounds from around 1.0800 to top 1.0850.

- Euro retains grasp of 1.0700 handle, but Sterling sags around 1.2150 axis and Yen weakens after closing below a Fib to circa 132.75 and away from decent option expiries at 132.50.

- PBoC set USD/CNY mid-point at 6.7756 vs exp. 6.7776 (prev. 6.7611)

- Click here for more detail.

FIXED INCOME

- Core benchmarks continued to gain momentum throughout the morning with little clear sign of concession pre-supply and perhaps deriving some support from ECB remarks.

- However, the rally has run out of steam with a sub-par German outing aiding the pullback, with Bunds and Gilts now sub 137.00 and 103.00 respectively.

- Stateside, USTs have been following suit and it remains to be seen if the looming 10yr supply will influence broader action, an auction which follows Tuesday’s strong 3yr.

- UK DMO is to launch a new conventional Gilt maturing October 2053 in the week commencing January 23rd.

- Click here for more detail.

COMMODITIES

- WTI and Brent have experienced a firmer start to the mid-week session, with the benchmarks posting upside of around USD 0.30/bbl within relatively narrow ranges that keeps the complex within WTD and recent parameters

- US and allies are reportedly preparing the next round of sanctions on Russian oil, via WSJ; intending to cap the sales price of Russian exports of refined petroleum products.

- Russian Kremlin, on possible losses from oil price caps, says there have been hardly any cases of the caps yet.

- Chinese Commerce Ministry will continue to impose anti-subsidy tariffs on dried distillers grains with solubles (DDGS) imported from the US.

- Standout mover has been LME Copper which eclipsed the USD 9k mark in an extension of yesterday’s price action after fairly contained/rangebound APAC trade for base metals.

- Spot gold is modestly firmer and resides towards the top-end of a USD 1872-1886/oz range, which is a fresh multi-month high leaving the figure itself as resistance before the May 2022 USD 1909/oz peak.

- Click here for more detail.

NOTABLE HEADLINES

- ECB’s Villeroy says they will need to be pragmatic on speed of hikes, will have to raise rates more in the coming months. Should aim to reach the terminal rate by the summer. Domestic inflation is likely to peak in H1, will avoid hard landing scenario.

- ECB’s Holzmann says rates will need to rise significantly further to reach levels that are sufficiently restrictive to ensure a timely return of inflation to target. Inflation is expected to subside but risks remain to the upside. There are no signs of de-anchored market expectations.

NOTABLE DATA

- German VDMA engineering orders (Nov) -14% Y/Y; domestic -7%, foreign -17%.

- German autos association VDA sees 2% growth in German passenger car market in 2023, to 2.7mln (Still a quarter below 2019 levels).

NOTABLE US HEADLINES

- US Treasury Secretary Yellen told President Biden that she planned to stay on as Treasury Secretary and Biden welcomed the decision, according to WSJ citing White House officials.

- US, Canada and Mexico are to explore standards to develop hydrogen as a regional clean energy source, while they will forge regional supply chains and promote targeted investment in key industries of the future including semiconductors and EV batteries.

- Click here for the US Early Morning note.

GEOPOLITICS

- Russia’s ambassador to the US commented that the US training of Ukrainian troops on Patriot systems confirms Washington’s de facto participation in the conflict and that the US administration’s goal is to inflict the most damage on Russia on the battlefield by the hands of Ukrainians, according to Reuters.

- Russian Kremlin says there is a positive dynamic in the military situation around Ukrainian town of Soledar Putin is open to discussions on Ukraine.

- Russian Rights Commissioner says important ceasefire proposals have been made during her meeting with Turkish and Ukrainian colleagues in Turkey, via Reuters.

- Russia and Iran are working on a new shipping corridor to bypass sanctions and are looking to work with India, according to Nikkei. ]

CRYPTO

- Bitcoin is under modest pressure and has slipped below the USD 17.5k mark, though the magnitude of the move is limited within tight parameters for the session.

APAC TRADE

- APAC stocks initially tracked the advances on Wall Street after Fed Chair Powell refrained from any major policy rhetoric and as participants looked ahead to upcoming US CPI data with hopes of softening price growth.

- ASX 200 tested the 7,200 level to the upside with the index led by outperformance in the mining and materials sectors, while participants also digested better-than-expected Retail Sales and a pickup in monthly inflation metrics.

- Nikkei 225 gained as earnings trickled in with outperformance in Yaskawa Electric after growth in its top and bottom lines, while there was encouragement from news that Fast Retailing will boost wages by as much as 40%.

- Hang Seng and Shanghai Comp were firmer for a bulk of the session after the PBoC pledged support measures including for the property sector and boosted its short-term liquidity efforts ahead of next week’s Lunar New Year celebrations, although gains were capped in the mainland after the recent mixed loans and aggregate financing data.

NOTABLE ASIA-PAC HEADLINES

- PBoC injected CNY 65bln via 7-day reverse repos with the rate kept at 2.00% and it injected CNY 22bln via 14-day reverse repos with the rate kept at 2.15% for a CNY 71bln net daily injection.

- Analysts noted there is room for China to cut RRR and interest rates this year, while analysts also see room for a rate cut in the property sector, according to China Securities Journal.

- BoJ offered to buy JPY 100bln in 1-3yr JGBs, JPY 100bln in 3-5yr JGBs, JPY 300bln in 5yr-10yr JGBs, JPY 200bln in 10yr-25yr JGBs and JPY 50bln in 25yr+ JGBs, while it also offered to buy an unlimited amount of JGBs at a fixed rate with maturities of 1yr-3yr and 3yr-5yr in an unscheduled announcement.

DATA RECAP

- Australian CPI YY (Nov) 7.3% vs Exp. 7.3% (Prev. 6.9%); Trimmed Mean CPI YY (Nov) 5.6% vs Exp. 5.5% (Prev. 5.3%)

- Australian Retail Sales MM Final (Nov) 1.4% vs. Exp. 0.6% (Prev. -0.2%, Rev. 0.4%)

1.c WEDNESDAY/ TUESDAY NIGHT

SHANGHAI CLOSED DOWN 7.67 PTS OR0.24% //Hang Seng CLOSED UP 104/59 PTS OR 0.49% /The Nikkei closed UP 270.44 PTS OR 1.02% //Australia’s all ordinaries CLOSED UP 0.95% /Chinese yuan (ONSHORE) closed UP TO 6.7738//OFFSHORE CHINESE YUAN UP TO 6.7868// /Oil UP TO 75.47 dollars per barrel for WTI and BRENT AT 80.57 / Stocks in Europe OPENED ALL RED ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

2 a./NORTH KOREA/ SOUTH KOREA/

///NORTH KOREA/SOUTH KOREA

end

2B JAPAN

Japan

end

3c CHINA /

CHINA/

China’s Credit Flood Is Coming, But December Was A Disappointment

TUESDAY, JAN 10, 2023 – 10:25 PM

Last week, when discussing the end of China’s “three red lines” policy to coincide with the premature end of China’s zero-covid policies, a policy U-turn which will have staggering consequences on the world’s biggest asset bubble and China’s economy, we said that “what China’s reversal means for the rest of the world is that a tidal wave of new credit is about to be unleashed, and as a recent report in Economic Information Daily said, the amount of new credit China issues is likely to reach another record high this year, while interest rates for longer-term loans could decline further. In other words, prepare for a surge in Chinese Total Social Financing as Beijing finally ends its latest experiment with austerity and is finally set to unleash the biggest credit expansion in history.”

And it will… but not just yet because while we expect a deluge of new Chinese credit (forced or otherwise) to flood the country – and then the world – in 2023, the last month of 2022 was a damp squab, with the PBOC reporting December credit data that was mixed at best.