jan 18 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSED: DOWN $1.95 at $1905.20

SILVER PRICE CLOSED: DOWN $0.41 to $23.51

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1908.10

Silver ACCESS CLOSE: 23.91

Bitcoin morning price:, 21,323 UP 121 DOLLARS

Bitcoin: afternoon price: $20,859 DOWN 343 dollars

Platinum price closing $1042.95 DOWN $0.50

Palladium price; closing 1719.40 DOWN $26.30

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2569.76 UP $13.83 CDN dollars per oz

BRITISH GOLD: 1542.50 DOWN 11.37 pounds per oz

EURO GOLD: 1764.21 DOWN 4.84 euros per oz

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JANUARY 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,907.200000000 USD

INTENT DATE: 01/17/2023 DELIVERY DATE: 01/19/2023

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 50

657 C MORGAN STANLEY 3

661 C JP MORGAN 656 2

737 C ADVANTAGE 2

880 H CITIGROUP 707

905 C ADM 2

TOTAL: 711 711

MONTH TO DATE: 2,951

JPMorgan stopped 2/711

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR JAN/2023. CONTRACT: 711 NOTICES FOR 71100 OZ or 2.2115 TONNES

total notices so far: 2,951 contracts for 295,100 oz (9.1788 tonnes)

SILVER NOTICES: 86 NOTICE(S) FILED FOR 430,000 OZ/

total number of notices filed so far this month 951 for 4,755,000 oz

END

GLD

WITH GOLD DOWN $1.95

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.9 TONNES FROM THE GLD //

INVENTORY RESTS AT 909.24 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 41 CENTS

AT THE SLV// :/HUGE CHANGES IN SILVER INVENTORY AT THE SLV// WHAT A MASSIVE FRAUD!!!

A HUGE WITHDRAWAL OF 8.15 MILLION OZ FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 498.05 MILLION OZ (THIS IS ALSO A CRIME SCENE@!!!!

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A FAIR SIZED 129 CONTRACTS TO 131,862 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.35 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. FOR THE PAST WEEK, OUR BANKERS HAVE RETURNED TO BEING NET SHORT AND THUS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.35 ABUT WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS, AS WE HAD A STRONG GAIN ON OUR TWO EXCHANGES OF 984 CONTRACTS. AS WELL, WE HAD ZERO EXCHANGE FOR RISK TRANSFER ( 0 CONTRACTS) AS THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 3.75 MILLION OZ. WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4,055. MILLION OZ FOLLOWED BY TODAY’S QUEUE. JUMP OF 150,000 OZ//NEW STANDING 4.790 MILLION OZ + 3.75 MILLION OF EXCHANGE FOR RISK//TOTAL STANDING 8.54 MILLION OZ//// V) FAIR SIZED COMEX OI GAIN/ STRONG EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –262

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN:

TOTAL CONTRACTS for 11 days, total 5373 contracts: OR 26.865 MILLION OZ PER DAY. (488 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 26.865 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 26.865 MILLION OZ

RESULT: WE HAD A FAIR SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 129 DESPITE OUR $0.35 LOSS IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 593 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JAN OF 4.055 MILLION OZ FOLLOWED BY TODAY’S 150,000 OZ. JUMP / //NEW STANDING INCREASES TO 4.790 MILLION OZ + EFR 3.75 MILLION = 8.540 MILLION OZ. .. WE HAVE A VERY STRONG SIZED GAIN OF 722 OI CONTRACTS ON THE TWO EXCHANGES FOR 3.612 MILLION OZ.. THE SILVER SHORTS HAVE BEEN HURT BADLY WITH SILVER’S HUGE RISE LATELY.

WE HAD 86 NOTICE(S) FILED TODAY FOR 430,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GOOD SIZED 5875 CONTRACTS TO 491,818 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 2416 CONTRACTS.

.

WE HAD A GOOD SIZED DECREASE IN COMEX OI (5875 CONTRACTS) WITH OUR $11.45 LOSS IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR JAN. AT 2.1710 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 700 CONTRACTS OR 70,000 OZ //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S ) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London). NEW STANDING 10.6189 TONNES

YET ALL OF..THIS HAPPENED DESPITE OUR $11.45 LOSS IN PRICE WITH RESPECT TO TUESDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 6192 OI CONTRACTS (19.259 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUMONGOUS SIZED 12,067 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 491,818

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 6192 CONTRACTS WITH 5875 CONTRACTS DECREASED AT THE COMEX AND 12,067 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 6192 CONTRACTS OR 19.259 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A HUGE SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (12,067 CONTRACTS) ACCOMPANYING THE GOOD SIZED LOSS IN COMEX OI (5875) TOTAL GAIN IN THE TWO EXCHANGES 8608 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) SMALL INITIAL STANDING AT THE GOLD COMEX FOR JAN. AT 2.1710 TONNES FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 70,000 OZ /NEW STANDING 8.2861 TONNES///3) ZERO LONG LIQUIDATION //4) GOOD SIZED COMEX OPEN INTEREST LOSS 5) HUMONGOUS ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JAN

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN :

40,213 CONTRACTS OR 4,021,300 OZ OR 125.079 TONNES 11 TRADING DAY(S) AND THUS AVERAGING: 3655 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAY(S) IN TONNES:125.079 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 125.079/3550 x 100% TONNES 3.52% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 125.079 TONNES INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH GOLD (

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A SMALL SIZED 129 CONTRACTS OI TO 131,862 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 593 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 593 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 593 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 391 CONTRACTS AND ADD TO THE 593 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG GAIN OF 722 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 3.612 MILLION OZ//

OCCURRED DESPITE OUR 35 CENT LOSS IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//CORN

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED UP 0.16 PTS OR 0.00% //Hang Seng CLOSED UP 100368 PTS OR 0.47% /The Nikkei closed UP 652.44 PTS OR 2.50% //Australia’s all ordinaries CLOSED UP 0.16% /Chinese yuan (ONSHORE) closed UP TO 6.7538//OFFSHORE CHINESE YUAN UP TO 6.7594// /Oil UP TO 81.63 dollars per barrel for WTI and BRENT AT 87.17 / Stocks in Europe OPENED ALL GREEN ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 5875 CONTRACTS DOWN TO 491,818 WITH OUR LOSS IN PRICE OF $11.45

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON-ACTIVE DELIVERY MONTH OF JAN… THE CME REPORTS THAT THE BANKERS ISSUED A HUMONGOUS SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 12,067 EFP CONTRACTS WERE ISSUED: ;: , . 0 FEB: 12,067 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 12067 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG SIZED TOTAL OF 6192 CONTRACTS IN THAT 12,067 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED COMEX OI LOSS OF 5875 CONTRACTS..AND THIS STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $11.45. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG .

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING Jan (10,6189)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL (TOTAL SO FAR THIS YEAR 591.535 TONNES)

Dec. 64.541 tonnes

JAN/2023: 10.6189 tonnes

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $11.45) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A VERY STRONG GAIN OF 6192 CONTRACTS ON OUR TWO EXCHANGES // WE HAVE GAINED A TOTAL OI OF 19.259PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JAN. (2.1710 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 70,000 oz OR 2.177 TONNES… ALL OF THIS WAS ACCOMPLISHED WITH OUR FALL IN PRICE TO THE TUNE OF $11.45.

WE HAD – 2416 CONTRACTS COMEX TRADES REMOVED FROM OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 8608 CONTRACTS OR 860,800 OZ OR 26.774 TONNES

Estimated gold comex today 233,065//fair//

final gold volumes/yesterday 315,452///good

INITIAL STANDINGS FOR JAN 2023 COMEX GOLD //JAN 18//

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | nil oz . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 711 notice(s) 71100 OZ 2.2115 TONNES |

| No of oz to be served (notices) | 463 contracts 46300 oz 1.440 TONNES |

| Total monthly oz gold served (contracts) so far this month | 2951 notices 295,100 9.1788 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 0

Total withdrawals: nil oz

total 0 oz

total in tonnes: 0 tonnes

Adjustments:0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JANUARY.

For the front month of JANUARY we have an oi of 1124 contracts having gained 603 contracts

We had 97 notices served on Tuesday, so we gained 700 contracts or an additional 70000 oz(2.1772 tonnes) will stand for delivery in this

very non active delivery month of January. (queue jump)

February lost 20,692 contacts to 235,016

March gained 75 contracts to stand at 796.

April gained 13,243 contracts up to 201,823.

We had 711 notice(s) filed today for 71100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 656 notices were issued from their client or customer account. The total of all issuance by all participants equate to 711 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 2 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JAN. /2023. contract month,

we take the total number of notices filed so far for the month (2951 x 100 oz , to which we add the difference between the open interest for the front month of (JAN.1174 CONTRACTS) minus the number of notices served upon today 711 x 100 oz per contract equals 341,400 OZ OR 10.6189 TONNES the number of TONNES standing in this non active month of January.

thus the INITIAL standings for gold for the JAN contract month:

No of notices filed so far (2951 x 100 oz+ (1174 OI for the front month minus the number of notices served upon today (711} x 100 oz} which equals 341,400 oz standing OR 10.6189 TONNES in this NON active delivery month of JAN..

TOTAL COMEX GOLD STANDING: 10.6189 TONNES (A VERY STRONG STANDING FOR METAL//COMEX RUNNING OUT OF PHYSICAL TO SERVE UPON OUR LONGS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

we had one adjustment of 110,631.591 oz Brinks

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,920,041.721 OZ 59.72 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,781,209.077 OZ

TOTAL REGISTERED GOLD: 11,077,098.948 OZ (344,54 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 11,704,110.129 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,157,051 OZ (REG GOLD- PLEDGED GOLD) 284,82 tonnes//rapidly declining

END

SILVER/COMEX

JAN 18/2023//INITIAL JAN. SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 50,846.470 oz CNT JPM |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 86 CONTRACT(S) (430,000 OZ) |

| No of oz to be served (notices) | 7 contracts (35,000 oz) |

| Total monthly oz silver served (contracts) | 951 contracts (4,755,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 0 deposits into the customer account

Total deposits: NIL oz

JPMorgan has a total silver weight: 151.981 million oz/295.292 million =51.52% of comex .//dropping fast

Comex withdrawals: 2

i) Out of CNT: 35,523.729 oz

ii) Out of JPMorgan: 15,322.750 oz

Total withdrawals; 50,846.470 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 33.195 MILLION OZ (declining rapidly).TOTAL REG + ELIG. 295.292 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JAN

silver open interest data:

FRONT MONTH OF JAN/2023 OI: 93 CONTRACTS HAVING GAINED 59 CONTRACT(S.). WE HAD 29 NOTICES

FILED ON TUESDAY SO WE GAINED 30 CONTRACT(S) OR 150,000 OZ QUEUE JUMP BY THE BANKERS TO OBTAIN SOME SILVER OVER HERE.

FEB> LOST 31 CONTRACTS TO 165 CONTRACTS

March LOST 442 CONTRACTS DOWN TO 109,972 contracts

TOTAL NUMBER OF NOTICES FILED FOR TODAY:86 for 430,000 oz

Comex volumes// est. volume today 80,378//strong

Comex volume: confirmed yesterday: 89,872 contracts ( strong)

To calculate the number of silver ounces that will stand for delivery in JANUARY. we take the total number of notices filed for the month so far at 951 x 5,000 oz = 4,755,000 oz

to which we add the difference between the open interest for the front month of JAN(93) and the number of notices served upon today 86 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JAN./2023 contract month: 951 (notices served so far) x 5000 oz + OI for the front month of JAN (93 – number of notices served upon today (86) x 500 oz of silver standing for the JAN. contract month equates 4.790 million oz + 3.75 MILLION OZ ( EXCHANGE FOR RISK) = 8.54MILLION OZ//(TOTAL OZ OF SILVER STANDING).

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:59,231// est. volume today// good

Comex volume: confirmed yesterday: 76,646 contracts ( very good)

END

GLD AND SLV INVENTORY LEVELS

JAN 18/WITH GOLD DOWN $1.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.9 TONNES FROM THE GLD////INVENTORY RESTS AT 909.24 TONNES

JAN 17/WITH GOLD DOWN $11.45 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.14 TONNES

JAN 13/WITH GOLD UP $22.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD///INVENTORY RESTS AT 912.14 TONNES

JAN 12/WITH GOLD UP $20.55 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 912.43 TONNES

JAN 11/WITH GOLD UP $1.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.17 TONNES

JAN 10/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 915.33 TONNES

JAN 9/WITH GOLD UP $ 8.60 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD//.//INVENTORY RESTS AT 915.33 TONNES

JAN 6/WITH GOLD UP $28.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 916.77 TONNES

JAN 5/WITH GOLD DOWN $17.05 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 916.77 TONNES

JANUARY 4/WITH GOLD UP $32.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.64 TONNES

JAN 3/WITH GOLD UP $20.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:STRANGE: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 917.64 TONNES

DEC 30/WITH GOLD UP $.80 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 918.51 TONNES

DEC 29//WITH GOLD UP $8.35 TODAY:; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 918.51 TONNES

DEC 28/WITH GOLD DOWN $6.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE DEPOSIT OF 5.50 TONNES INTO THE GLD..//INVENTORY REST S AT 918.51 TONNES

DEC 27/WITH GOLD UP $18.15 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 913.01 TONNES

DEC 23/WITH GOLD UP $19,15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 913.88 TONNES/

DEC 22/WITH GOLD DOWN $29.35 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 913.88 TONNES

DEC 21/WITH GOLD FLAT TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 913.88 TONNES

DEC 20/WITH GOLD UP $27.05: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES INTO THE GLD////INVENTORY RESTS AT 912.14 TONNES

DEC 19/WITH GOLD DOWN $2.10: HUGE CHANGES IN GOLD INVENTORY AT THE GLD> A BIG WITHDRAWAL OF 3.47 TONNES FROM THE GLD//INVENTORY RESTS AT 910.41 TONNES

DEC 16/WITH GOLD UP $12.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD//INVENTORY RESTS AT 913.88 TONNES

DEC 15//WITH GOLD DOWN $31.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 911.56 TONNES

DEC 14/WITH GOLD DOWN $6.20: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 912.72 TONNES

DEC 13/WITH GOLD UP $32.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD///INVENTORY RESTS AT 910.41

DEC 12/WITH GOLD DOWN $17.60: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

DEC 9/WITH GOLD UP $8.90//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

Dec 8/WITH GOLD UP $4.05, OVER THE PAST 3 WEEKS WE LOST 2.04 TONNES//INVENTORY RESTS AT 908.09 TONNES

GLD INVENTORY: 909.24 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JAN 18/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 8.15 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 498.05 MILLION OZ///

JAN 17/WITH SILVER DOWN 35 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 506.200 MILLION OZ//

JAN 13/WITH SILVER UP 46 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.5 MILLION OZ FROM THE SLV..//INVENTORY RESTS AT 506.200 MILLION OZ//

JAN 12/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 508.700 MILLION OZ/

JAN 11/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 508.700MILLION OZ

JAN 10/WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.65 MILLION OZ

JAN 9/WITH SILVER DOWN 9 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.65 MILLION OZ//

JAN 6/WITH SILVER UP 54 CENTS TODAY;BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.20 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 509.65 MILLION OZ//

JAN 5/WITH SILVER DOWN 50 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.10 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 505.45 MILLION OZ//

JAN 4/WITH SILVER DOWN 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 506.55 MILLION OZ/

JAN 3/WITH SILVER UP 24 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: STRANGE: A WITHDRAWAL OF 1.2 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 507.85 MILLION OZ/

DEC 30/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.050 MILLION OZ

DEC 29/ WITH SILVER UP $0.63 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.050 MILLION OZ

DEC 28//WITH SILVER DOWN 46 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.715 MILLION OZ INTO THE SLV///..INVENTORY RESTS AT 509.050 MILLION OZ

DEC 27/WITH SILVER UP 34 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 507.350 MILLION OZ//

DEC 23/WITH SILVER UP 29 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT507.900 MILLION O//

DEC 22/WITH SILVER DOWN 53 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 507.90 MILLION OZ//

DEC 21/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.0 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 507.90 MILLION OZ//

DEC 20/WITH SILVER UP 105 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV:: A DEPOSIT OF 700,000 OZ INTO THE SLV///INVENTORY RESTS AT 509.90 MILLION OZ//

DEC 19/WITH SILVER DOWN 13 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.05 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 509.20 MILLION OZ//

DEC 16/WITH SILVER UP 2 CENTS; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.85 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 508.15 MILLION OZ//

DEC 15/WITH SILVER DOWN 78 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF EXACTLY 2.00 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 510.000 MILLION OZ

DEC 14/WITH SILVER UP 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 512.000 MILLION OZ//

DEC 13/WITH SILVER UP 59 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 600,000 OZ FROM THE SLV////INVENTORY RESTS AT 513.900 MILLION OZ//

DEC 12/WITH SILVER DOWN 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 514.500 MILLION OZ//

DEC 9/WITH SILVER RISING 77 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.2 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 514.500 MILLION OZ.

DEC 8/WITH SILVER RISING 34 CENTS TODAY: OVER THE PAST 3 WEEKS, WE HAVE GAINED A STRONG: 44.777 MILLION OZ/INVENTORY RESTS AT 516.700 MILION OZ.

CLOSING INVENTORY 498.05 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

end

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

Open Madness in Global Bond Markets: Got Gold?

Matthew Piepenburg

January 18, 2023

The slow but steady implosion of global bond markets is no longer a debate but fact. Knowing this, investors can better brace themselves for the policy and market reactions to come.

Below, we once again follow the patterns of math and cycles (as well as the open failure of policy makers) to foresee the direction of risk assets, currencies and gold.

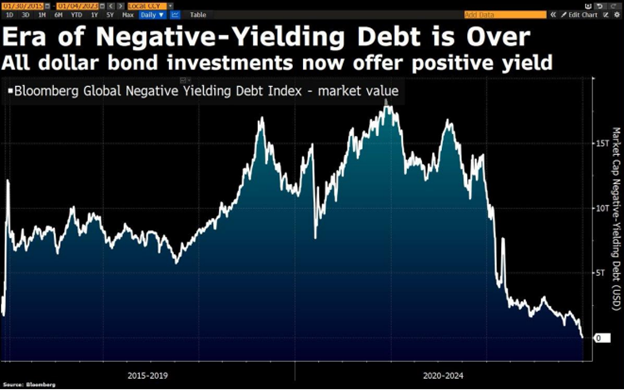

The End of Negative Yields: Anything but a Good Sign

Recently, Bloomberg happily announced that the era of “negative yielding” (which technically means “defaulting”) USD bonds is over as yields are now “nominally positive.”

“Great news!” they tell the huddling masses.

Nothing, however, could be further from the truth.

Let me repeat that: Nothing could be further from the truth.

Yields are only outpacing already embarrassing inflation metrics because bond prices, which move inversely to yields, are tanking in a world which no longer wants or trust USD-based IOUs.

In other words: All this means is that bonds are tanking and inflation is roaring at the same time.

Great news?

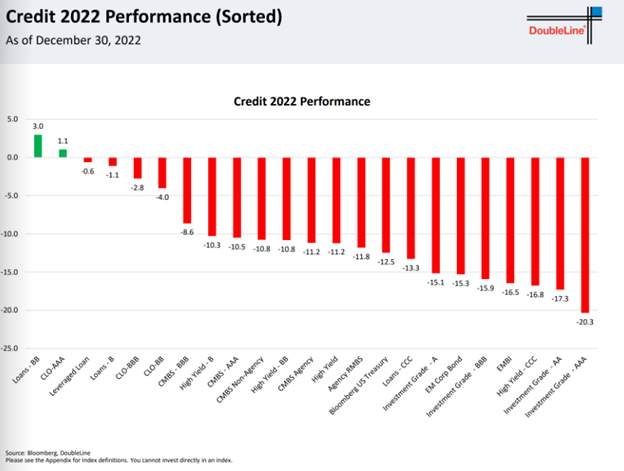

Furthermore, this so-called “return to normalcy” in positive nominal yields is in fact a neon-flashing sign (or needle) pointing toward the end (and bursting) of a global debt bubble in government bonds.

What’s worse, and as the following graph makes objectively clear, is that it’s not just sovereign bonds that are tanking, but the entire credit asset class, from CMBS to Investment Grade.

Just see for yourself:

These are appalling figures which cannot be ignored.

Facts, after all, are stubborn things.

Facts vs. Headlines

Despite such empirical data, many financial “journalists” are paid to sell a simplistic message rather than objective clarity. Ignoring the obvious fall in bond prices (above), they somehow have the gal to celebrate “positive nominal yields” in a twist of messaging that almost defies belief.

And few, if any, of these “experts” have the historical and non-linear market knowledge to place singular/linear headlines (fantasies) like positive nominal yields within the more nuanced context of 3-dimensional reality—namely dying bonds.

History, for example, would remind these misleading headlines that for well over a century, every time sovereign debt in advanced economies (now just banana republics) reaches unpayable levels (higher than even EM levels), the net result is unequivocal: It’s either inflation or default.

Always. Every time. Period.

The current disaster in global bond markets, playing out now, will be no different: Inflation, default or “reset.”

Policy Makers Heading in the Wrong Direction

After years of buying time, votes, book deals and even a Nobel Prize, global financial leaders have smiled in public while privately failing with staggering panache among the more informed.

Rather than openly face and solve $300+T debt disasters the hard way, namely via economic growth, fiscal austerity, debt restructuring, inflation recognition (vs. “transitory” denial) and an accountable and transparent need for financial repression (nod to Reinhart and Rogoff), our leaders and central bankers have gone in the complete opposite and wrong direction.

Instead, they have recklessly and addictively relied upon mouse-click fiat money rather than money tied to actual goods, services and production to provisionally support years and years of un-earned reputations and unloved bonds.

As opposed to politically unpopular fiscal austerity, the math-ignorant and job-preserving (i.e., pathologically selfish) US politicos just added another $1.7 trillion spending bill to bribe/pay for their tenure but which they can’t otherwise pay back.

Instead, they just hand the bill to my kids.

You really can’t make this stuff up. It’s embarrassing open madness and blatant self-interest over national interest.

But then again, that’s the effective definition of a politician: Self first, nation later. Facts be damned.

Just consider fact-allergic clowns like George Santos…

Nothing Left but Bad Choices

Economic growth, as we see it (and as housing, manufacturing, trade and services data confirm) will not save us or our bonds.

The debt is factually too high and the growth, even if China re-opens its COVID-locked doors, will never catch up.

Further debt and slower growth points to the only options left in the global bond markets: 1) Print more fake and grotesquely inflationary money to buy unloved bonds, 2) default on those bonds (political suicide) or 3) enter into a Western debt restructure—aka the big re-set for which I’ve previously warned will be “greased” via the introduction of a CBDC-driven control state masquerading as an “efficient payment system.”

Wonderful.

Watch the Bond Market: It’s the Thing

As I’ve said for years, and will openly say for years more: The bond market is the thing.

Everything follows the bond market’s lead, because debt rather than growth, manufacturing and sound fiscal leadership has been the singular and toxic wind beneath the broken wings of every national flag since Greenspan killed capitalism years ago.

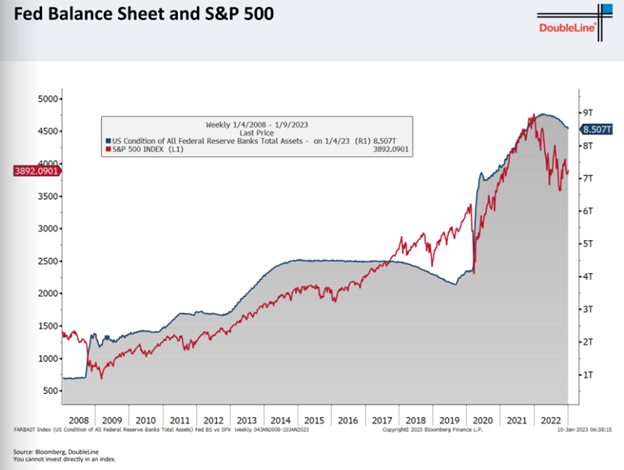

Debt, of course, buys time. And mouse-click money buys the debt. This madness creates false fun, intoxication and drunken euphoria. Our S&P, for example, simply tracks (up or down) Fed QE or QT. In short: A Fed Market.

But there’s a cost for such madness.

As Rates Rise, Markets Fall

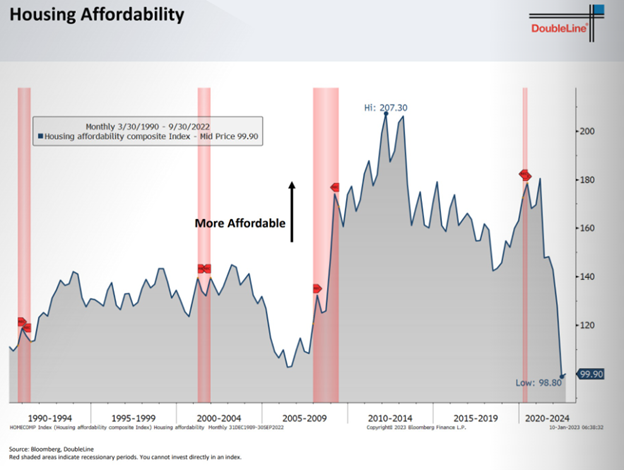

Mouse-click money also creates inflation and distorts every other asset class, from housing to stocks.

Property markets, for example, love low rates but crater once rates rise and affordability metrics tank, and I do mean TANK:

As we are seeing in real time, eventually the fantasy and artificial tailwind of drunken QE becomes a sickening hangover as central bankers like Powell try to “tighten” what was once “loose.”

Astounding Arrogance

These central bankers share the astounding arrogance of believing (or at least pretending) that markets can be carefully controlled like a home thermostat to usher in “soft QT landings” after years of fatally addictive QE highs.

But as the data now confirms, there’s nothing soft now or ahead.

During the QE intoxication period, when bonds are bought by central banks to keep yields and rates artificially repressed, the cost of debt is nearly free and the stock, bond and property markets balloon on free money, stock buy-backs and seemingly perpetual debt roll-overs.

Tech Stocks & Property Markets

This was especially true of tech stocks like the FANGS—their entire rise and fall was and is clearly correlated to a fake money printer and low rates, as I patiently warned years ago and had recently been shorting to my advantage once the sign was clear.

It was easy to see. The Fed (and rate markets) signaled it.

Too Little, Too Late: The Open Failure of Modern Monetary “Policy”

In 2022, when central bankers privately realized they had made an historical QE mistake and tried (far too late with far too little) to introduce QT, Titanic stock, property and currency bubbles began their slow then rapid fall toward the ocean’s floor.

In 2022, for example, the tightening Fed reduced its sickening balance sheet by a mere 2.4%. Hardly a dent.

But even that pathetically tiny bit of “tightening” in the US backdrop of a pathetically massive debt-to-GDP ratio of 125% was enough to usher in the worst year for stocks and bonds since 1871.

Please: Re-read those last lines and re-examine those last two graphs. Let it sink in.

By now, it should be bluntly obvious how central banks rather than natural market forces OWN our so-called “free markets”?

Where the money printing goes (up or down), so goes the debt-driven markets and debt-soaked economies they manipulate.

Far, far more alarming, however, is this little added fact: If QT continues at its current pace of -$95 billion per month, just imagine what such a 13% annualized Fed balance sheet reduction (as opposed to 2.4% in 2022) in 2023 will do to these already historically broken markets?

Will a QE Pivot Even Work?

In the past, of course, the Fed’s “easy solution” to tanking markets was just another drunken run (or pivot) toward a QE money printer to finance US debts and hence keep yields and rates “accommodated” and “controlled.”

But in the past, US deficits were below 20% of global GDP growth. That was a ticking time bomb.

But heading into 2023, US deficits are already greater than 30% of global GDP growth, which means that time bomb is already exploding.

Sensational?

Nope.

This is just the simple philosophy of debt and the open failure of years of easy money and easy credit, none of which our central bankers will transparently confess, as Putin and COVID serve as far better scapegoats for the real goats at the trigger of our mouse-clicked money.

In short, it took us 150 years to see markets this pathetic, and the worst is still to come.

Thus, as Congress spends like a drunken sailor, who will pay its embarrassing bar tab?

The private sector?

Nope. The balance sheets just aren’t there.

A pivot to more QE?

Well, short of an intervening “re-set,” that’s an inevitable albeit desperate possibility—and it will send gold soaring, and likely BTC as well, whatever one’s views on the current (and FTX infected) crypto narrative.

The US Dollar’s Slow Fall from Prominence

Of course, more money printing at the Fed will weaken even the relatively strong but unsustainable USD of 2022, as we’ve consistently warnedthroughout the USD’s 2022 rise.

The temporary, relative and artificially strong USD of 2022 was an absolute kick in the groin to currencies and nations like the EU, UK and Japan whose currency and bond markets didn’t and don’t have the global world reserve status to similarly raise rates hundreds of basis points in a year to “fight inflation” (or Putin’s Ruble…).

Japan & the EU: Fighting Back?

But even these hard realities haven’t prevented a zombie nation like Japan from attempting to now fight the USD, as Tokyo’s recent move to raise 10-year rates on the JGB confirms.

This rate hike provided a little wind behind the dying yen, as expected, in the now unofficial currency war taking place globally.

More importantly, there is increasing talk out of Tokyo to repatriate capital back to Japan, which would involve dumping more USTs to purchase more Japanese IOUs at a time when the US needs more not less buyers of its unloved and distrusted bonds.

By the way, less demand for USTs just means more rising yields and rates…

In sum, the slow but steady process of de-Dollarization continues its predictable trend as the US runs out of options, trust and friends in a bond and currency market in the middle of a major “Uh-Oh” moment.

The 2023 ECB, moreover, is already signaling similar rate hikes and flows away from USTs in favor of its own dying local bonds and currency. This won’t help Uncle Sam’s bar tab…

Again: The bond market is the thing, and these things (most notably US bonds) are objectively rotten to the core.

Shark Fins Approaching

More rising bond yields are the rising shark fins swimming at full speed toward global economies bloodying their waters with unsustainable debts and recessionary chum.

The Planned Recession

The only force to slow down these rising yields/shark fins is the mother of all Fed-induced recessions (deflationary), which means Powell’s promise of a “softish landing” is about as bankable as his promise of “transitory” inflation.

As I’ve said many times, no recession can be cured with rising rates and a strong currency. Never. Not once.

Thus, once the re-defined and unofficial recession we are already in becomes “official”—the US will weaken its Dollar, which gold, of course, will love. If not already in 2023, certainly by 2024.

All we can do for now is track those shark fins and doubt those bankers.

END

3. Chris Powell of GATA provides to us very important physical commentaries//

Barrick gold misses again, producing only 4.14 million oz last year

(Bloomberg)

Barrick misses gold guidance as output sinks to 22-year low

Submitted by admin on Tue, 2023-01-17 21:35Section: Daily Dispatches

By Jacob Lorine

Bloomberg News

Tuesday, January 17, 2023

Barrick Gold Corp.’s bullion output slid last year to its lowest level since 2000, missing analysts’ expectations and its own target as operational woes curbed production.

Barrick produced 4.14 million ounces of gold last year, marking its third straight decline in annual output, according to preliminary figures released today by the company. Chief Executive Officer Mark Bristow had said as recently as Nov. 3 that Barrick was on track to achieve its annual guidance of 4.2 million to 4.6 million ounces, albeit at the lower end of the range. …

… For the remainder of the report:

end

Trafigura plans to take a huge amount of LME copper. That should be interesting

(Reuters)

Trafigura plans to take large amounts of LME copper, sources tell Reuters

Submitted by admin on Tue, 2023-01-17 21:56Section: Daily Dispatches

How rude not to trust the London Metals Exchange!

* * *

By Pratima Desai

Reuters

Tuesday, January 17, 2023

LONDON — Commodity trader Trafigura is planning to take large amounts of copper from London Metal Exchange registered warehouses, two people familiar with the matter said, adding that the metal was likely to remain in Europe.

Copper stocks in LME registered warehouses stand at 83,325 tonnes and are already low. Canceled warrants — metal earmarked for delivery — stand at 31.2% or 26,000 tonnes. This compares with 12% on Jan. 3.

Most of the cancelled warrants — 20,600 according to the latest data from the LME — are in Rotterdam, Netherlands.

Trafigura declined to comment on whether it was behind the cancellations, but said: “In an environment of constrained supply, reflected by high copper benchmarks in Europe, we are ensuring we can continue to supply our customers with the metals they need.”

The cancellations and large holdings of copper warrants and cash contracts are fuelling some concern about supplies on the LME market. …

… For the remainder of the report:

END

The kiss of death to the Petrodollar scheme!!

(Bloomberg/GATA)

Saudi Arabia open to settling trade without U.S. dollars

Submitted by admin on Tue, 2023-01-17 22:29Section: Daily Dispatches

By Abeer Abu Omar and Manus Cranny

Bloomberg News

Tuesday, January 17, 2023

Saudi Arabia is open to discussions about trade in currencies other than the US dollar, according to the kingdom’s finance minister.

“There are no issues with discussing how we settle our trade arrangements, whether it is in the U.S. dollar, whether it is the euro, whether it is the Saudi riyal,” Mohammed Al-Jadaan told Bloomberg TV today in an interview in Davos, Switzerland.

“I don’t think we are waving away or ruling out any discussion that will help improve the trade around the world,” Al-Jadaan said. …

… For the remainder of the report:

end

Silver futures market is ‘ready to bust,’ GATA’s Steer says

Submitted by admin on Tue, 2023-01-17 22:42Section: Daily Dispatches

10:35p ET Tuesday, January 17, 2023

Dear Friend of GATA and Gold:

GATA board member Ed Steer, publisher of Ed Steer’s Gold and Silver Digest letter, tells Jim Goddard of HoweStreet.com that trader positioning in the U.S. silver futures market shows that it is “ready to bust.”

The interview is 18 minutes long and can be heard at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

end

4. Other gold/silver commentaries

end

Commodity commentaries//GLOBAL FREIGHT

END

IMPORTANT COMMENTARIES ON COMMODITIES:

-END-

6/CRYPTOCURRENCIES/BITCOIN ETC

FTX Says $413 Million Worth Of Cryptocurrency Was Stolen From Failed Exchange

WEDNESDAY, JAN 18, 2023 – 02:40 PM

Authored by Katabella Roberts via The Epoch Times,

Debtors for the bankrupt cryptocurrency exchange FTX have said that around $413 million worth of cryptocurrency was stolen from the company through “unauthorized transfers.”

In a report to creditors on Jan. 17, the company said that FTX debtors have identified approximately $1.6 billion of digital assets associated with FTX.com, of which $323 million of which was “subject to unauthorized third-party transfers” and $426 million of which was “transferred to cold storage under the control of the Securities Commission of The Bahamas.”

Another $742 million is in “cold storage” under the control of the FTX debtors, and $121 million of which is pending transfer to “cold storage” under the control of the FTX debtors.

The term “cold storage” refers to keeping cryptocurrency keys offline and unconnected to a network or the internet in order to improve security.

With regards to the FTX US exchange, the debtors identified roughly $181 million of digital assets, $90 million of which was “subject to unauthorized third-party transfers post-petition, $88 million of which is in cold storage under the control of the FTX debtors, and $3 million of which is pending transfer to cold storage under the control of the FTX debtors.”

FTX founder Sam Bankman-Fried leaves Manhattan Federal Court after his arraignment and bail hearings in New York, on Dec. 22, 2022. (David Dee Delgado/Getty Images)

‘Substantial Shortfall of Digital Assets’

Overall, the debtors have identified approximately $5.5 billion in liquid assets, including $1.7 billion in cash, $3.5 billion of crypto assets, and $300 million in securities since the firm filed for Chapter 11 bankruptcy in November 2022.

The company stopped short of providing an estimate of total liabilities, but added that based on current estimates of the amount of digital assets associated with the FTX.com and FTX US, there is a “substantial shortfall of digital assets at both exchanges.”

FTX, which was founded in 2019 and once valued at $32 billion, filed for bankruptcy protection on Nov. 11 following a spectacular collapse amid a liquidity crisis after it was revealed that the hedge fund Alameda had been using FTX customer assets to keep itself propped up.

A potential rescue deal by larger rival Binance was also pulled, adding further woes to the company as traders quickly raced to pull billions of cryptocurrency from the exchange.

According to a court filing, FTX owed its 50 largest creditors almost $3.1 billion while an estimated $8 billion in customer funds disappeared.

The firm’s founder, Sam Bankman-Fried, was subsequently arrested on Dec. 17 in the Bahamas, where the company was headquartered, and he was extradited to the United States, where he was released on a $250,000 bail and placed under house arrest at the California home of his parents, who were both law professors at Stanford University.

In January, Bankman-Fried pleaded not guilty to charges of fraud, conspiracy, campaign finance law violations, and money laundering.

Bankman-Fried Says He Didn’t Steal User Funds

Bankman-Fried is scheduled to go on trial in October 2023.

“We are making important progress in our efforts to maximize recoveries, and it has taken a Herculean investigative effort from our team to uncover this preliminary information,” said John J. Ray III, the chief executive officer and chief restructuring officer of the FTX debtors.

However, Ray stressed that the information is still preliminary and could change.

In his first statement since his arrest in the Bahamas, Bankman-Fried vowed to get customers their money back while doubling down on his previous claims that he did not steal users’ funds.

“I didn’t steal funds, and I certainly didn’t stash billions away,” the former founder wrote on his Substack blog on Jan. 12. He also claimed that FTX US was “fully solvent” and should be able to return all customers’ funds.

“It’s ridiculous that FTX US users haven’t been made whole and gotten their funds back yet,” Bankman-Fried wrote.

FTX debtors are also reviewing the roughly $2.1 billion equivalent in cash that cryptocurrency exchange Binance received as part of its exit from FTX in 2021, CNBC reports.

Binance chief executive Changpeng Zhao brushed off concerns that the exchange may have to hand the money back during an interview with the the media company in December, stating that the firm is “financially OK” and has a “very solid revenue.”

END

.

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: UP TO 6.7538

OFFSHORE YUAN: 6.7594

SHANGHAI CLOSED UP 0.16 PTS OR 0.00%

HANG SANG CLOSED UP 100.36 PTS 0.47%

2. Nikkei closed UP 652.44 PTS OR 2.50%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 101.90 Euro RISES TO 1.0822 UP 33 BASIS PTS

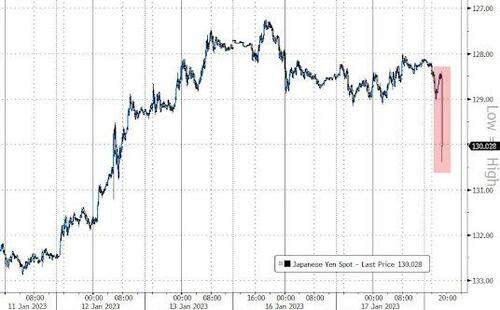

3b Japan 10 YR bond yield: FALLS TO. +.419!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 129.24/JAPANESE YEN RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.055%***/Italian 10 Yr bond yield FALLS to 3.837%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.016…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.024//

3j Gold at $1918.30//silver at: 24.21 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 20/100 roubles/dollar; ROUBLE AT 68.94//

3m oil into the 81 dollar handle for WTI and 87 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 129.24/10 YEAR YIELD AFTER BREAKING .54% FALLS TO .414% ON CENTRAL BANK (jAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9141– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9903 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

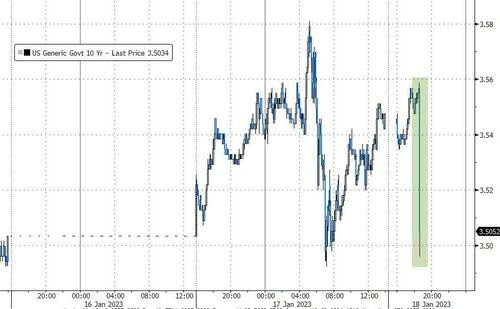

USA 10 YR BOND YIELD: 3.479% DOWN 6 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.601 DOWN 6 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,80…

GREAT BRITAIN/10 YEAR YIELD: 3.347 % DOWN 6 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Treasuries Drift Higher After BOJ Reversal, Await PPI And Retail Sales

WEDNESDAY, JAN 18, 2023 – 08:03 AM

US stock-index futures were muted on Wednesday, swinging between gains and losses, as investors initially welcomes a dovish announcement by the BOJ which refrained from further expanding its yield curve control band, then turned to corporate earnings for more clues on the health of corporate America amid growing prospects for a recession. Nasdaq 100 and the S&P 500 futures were up 0.2% as of 7:15 a.m. in New York. Treasury and JGB yields tumbled after the BOJ kept monetary settings unchanged, while the yen first slid against the dollar but then recovered all losses amid expectations the BOJ has only bought a few weeks of time. WTI crude added 1.7% this morning and has been holding above $80 amid optimism around China reopening demand. Dollar is weaker; DXY at 102 helping gold trade back over $1900.

Among notable movers in premarket trading, Moderna Inc. climbed 6.7% after saying its vaccine against respiratory syncytial virus infections met targets. IBM dropped 1.9% after Morgan Stanley cut the stock to equal-weight from overweight, saying that it is transitioning out of more defensive IT hardware name. Bank stocks are mixed as investors await the release of key economic data, including the Beige Book and retail sales. Coinbase said it’s halting operations in Japan. Meanwhile, Bank of Montreal has received approval from the Federal Reserve to acquire San Francisco-based Bank of the West. Here are the other notable premarket movers:

- United Airlines (UAL US) rises 2.6%, boosting carrier peers, after the airline operator’s guidance for the first quarter and 2023 beat analyst estimates. Brokers pointing to strong growth in sales, assuaging any worries over demand taking a hit from an economic slowdown. American Airlines +1.4%, Delta Air +1%

- GoDaddy (GDDY US) gains 3% after the website domain company was upgraded to outperform from inline at Evercore ISI, with the broker highlighting the firm’s relatively recession- resistant business model and new-product cycle.

- International Business Machines (IBM US) drops 1.9% after Morgan Stanley cut the stock to equal-weight from overweight, saying that it is transitioning out of more defensive IT hardware names.

- Skechers (SKX US) slides 2.1% after Morgan Stanley downgraded it to equal-weight on valuation, risk of FY23 guidance missing expectations and as the market shifts to early-cycle names. The broker raised Gap (GPS US) to equal-weight and anticipates a 2023 of two halves for US specialty retail and department stores.

- SmileDirectClub (SDC US) jumps 13% after the maker of dental aligners projected a narrower Ebitda loss for 2023 and said that it planned to rejig its global workforce and introduce additional cost savings. Jefferies, however, remains cautious on the stock, saying that the company saw a “weak” finish to a tough year.

- Oatly (OTLY US) gains 6.3% after Mizuho Securities upgrades its rating on the oat drink company to buy from hold, with long-term growth seen still intact.

While US stocks have gained in the new year as cooling inflation spurred bets of a softening in the Federal Reserve’s policy, they’ve dramatically underperformed international peers as investors worry that the combination of rising interest rates and slowing consumer demand could trigger an economic contraction. A weaker dollar and optimism around a China reopening have lured investors to non-US stocks. Goldman Sachs strategists said US equity funds have seen outflows in the first two weeks of the year, while Europe has seen inflows — both major trend reversals from 2022. UK inflation as well as a more muted start to the US earnings-reporting season boosted those who believe monetary easing would have to begin this year.

The yen dropped as much as 2.6% against the dollar after Japan’s policymakers doubled down on defending their stimulus, defying intense market speculation. The currency later trimmed the losses to 0.7%. Even as investors remain on guard for the central bank to continue large scale bond buying to protect its yield goal, there are doubts about how long it can continue. The yen’s drop proved to be an idiosyncratic trend in the foreign-exchange markets as the dollar fell against all but five of its 31 major peers including the Japanese currency.

Meanwhile, Analysts expect fourth-quarter earnings to show a drop of 2.7%, the first year-over-year decline since 2020, according to data from Bloomberg Intelligence. “Given the difficult backdrop, there’s fear among some parts of the market that US earnings forecasts might still be too high for 2023 and that stocks might not be able to sustain their current strength,” said Russ Mould, investment director at AJ Bell. He added that reports from the likes of Procter & Gamble Co., Schlumberger Ltd., Microsoft Corp. and Tesla Inc. “will certainly be ones to watch as their fortunes could have a major influence on market sentiment.”

European equity markets are mixed after the BOJ sent the yen spiraling lower by leaving its policy settings unchanged. The Stoxx 600 is up 0.1% with gains in the CAC and FTSE 100 while the DAX trades lower; today’s move brought the total Stoxx 600 gains since a Sept. 29 low to more than 19%. If the index closes at 20% or higher, it will join other regional peers in confirming a technical bull market. Tech, travel and miners are the best performing sectors while chemicals and real estate fall. Here are the notable European movers:

- Richemont shares gain as much as 2.8% in Europe despite the Cartier owner posting worse-than-expected 3Q sales as investors take the view that disruptions in China caused by a surge in Covid infections may prove temporary.

- Just Eat Takeaway.com jumps as much as 16% after 4Q Ebitda beat estimates as the food delivery firm said it remains focused on improving profitability. Peers Deliveroo and Delivery Hero rose as much as +5.5% and 6.3% respectively

- ASM International shares rise as much as 8.7% after 4Q update shows a strong beat on sales that is likely to boost sentiment on the semiconductor-equipment maker, analysts say. ASML shares rise as much as 2.1% in sympathy.

- Capgemini shares rise as much as 3.5%, hitting highest in just over a month, after Barclays upgrades the IT services firm to overweight on greater resilience in its business mix and on utilization.

- EQT shares drop as much as 8.4%, the most in more than three months, after the investment firm delivered results which analysts say missed on adjusted Ebitda.

- Continental shares fall as much as 5% after the German car-parts and tiremaker said late Tuesday that it expects FY22 adjusted free cash flow of €200m, below its outlook range of €600m to €800m.

- Encavis shares fall as much as 5.3% after Barclays analyst cut the recommendation to underweight from equalweight, Orsted also downgraded. Barclays notes that growth pipeline valuations for the two energy companies have moved significantly above vertically integrated peers.

- Wise shares drop as much as 5%, extending yesterday’s double-digit losses, after the UK money- transfer firm’s growth slowed and missed analyst expectations.

Earlier in the session Asian stocks edged higher as Japanese shares advanced after the Bank of Japan announced no change to its yield curve control policy, countering broader caution ahead of the Lunar New Year holidays. The MSCI Asia Pacific Index erased an earlier loss of as much as 0.7% to rise 0.5%, lifted by communication services and health care shares. Japanese equities jumped as the yen fell after the BOJ kept policy on hold, pushing back against intense market speculation of policy change by ramping up the defense of its stimulus framework.

“What has been happening so far is a fairly easy pattern to understand,” said Makoto Furukawa, chief portfolio strategist at Mitsubishi UFJ Morgan Stanley Securities. “I think the pattern of bank stocks rising and exchange-rate-sensitive stocks being hit will continue. Expectations for further revisions to the BOJ’s policy will emerge.” South Korea was among the biggest losers on Thursday, dragged by a loss in Samsung Electronics. Chinese benchmarks were mixed in thin volumes before market closures next week. The MSCI Asian stock benchmark has gained more than 20% from an October low to enter a bull market, outperforming US and European peers. Japanese stocks have underperformed, with the Nikkei down almost 1% in the same span, hurt in part by the BOJ’s December move to widen a band on bond yields.

Australian stocks edged higher: the S&P/ASX 200 index rose to close at 7,393.40, as healthcare and technology shares buoyed the benchmark. In New Zealand, the S&P/NZX 50 index rose 0.3% to 11,920.41. The nation’s home sales fell 39% y/y in December, according to the Real Estate Institute of New Zealand.

The Bloomberg Dollar Index is down 0.3%, swinging to a loss in European trading as the greenback weakened against all of its Group-of-10 peers apart from the yen; the JPY traded well off its worst levels. EUR gained after ECB’s Villeroy said he was surprised by the sources story suggesting they are considering smaller hikes beyond February. GBP rose after data showed UK core CPI was slightly stronger than expected in December. Some more details:

- The yen slumped as much as as 2.6% against the dollar, hitting 131.58, and Japan’s bond yields fell by up to 11bps after the BOJ pushed back against intense market speculation of policy change by ramping up the defense of its stimulus framework. Risk reversals in the front-end rallied in the run-up to the BOJ decision in favor of greenback calls, suggesting that the market was positioning for a no-change decision by the central bank. The move for risk reversals suggests that investors are still looking for bullish yen expressions over the medium-term, and especially after Kuroda’s term ends in April

- The Swiss franc extended its advance against to 0.9131 per dollar, the strongest level in a year

- The euro extended an advance against the dollar and bunds reversed opening gains after ECB official Francois Villeroy de Galhau said that guidance from ECB President Christine Lagarde that borrowing costs will continue to be lifted in half-point steps for some time still holds. One trader has placed a large bet using options on German 5-year futures, targeting the yield to rise above 2.40% for maximum profit, up from about 2.13% currently

- The pound rose against the dollar and traders added to wagers on the BOE’s hiking cycle after UK inflation figures showed month-on-month and core readings came in higher than anticipated in December

In rates, Treasuries and JGBs spiked higher overnight after the Bank of Japan kept monetary settings unchanged with no nod to any concession on current policy; 10-year TSY yields fell as much as 8.3bp to 3.465% and were trading at 3.47% last. Gains have been broadly maintained into early US session, with 10-year note futures trading near day’s high. Heavy US economic data slate includes PPI and retail sales, and Treasury auctions 20-year bonds. UK and German government bonds pared earlier advances to trade in the red as Treasury yields were richer by 3bp to 7bp across the curve with gains led by intermediates, flattening 2s10s spread by 4bp on the day; 10-year yields trade around 3.48% with bunds and gilts underperforming by 4bp and 7bp in the sector. Most gains in Treasuries were made during aggressive rally in JGBs after Bank of Japan policy announcement, which left benchmark JGB 10-year richer by around 8bp on the day. US Treasury auctions resume with $12b 20-year bond reopening at 1pm.

In commodities, crude futures rose with WTI adding 1.7% to trade near $81.50. Spot gold rises roughly $4 to trade near $1,913/oz

To the day ahead now, and data releases from the US include December’s PPI, retail sales and industrial production, whilst from the UK we’ll also get the December CPI release. From central banks, we’ll hear from the ECB’s Villeroy, and the Fed’s Bostic, Harker and Logan. Lastly, the Fed will also be releasing their Beige Book.

Market Snapshot

- S&P 500 futures little changed at 4,012.00

- MXAP up 0.5% to 166.79

- MXAPJ up 0.3% to 546.45

- Nikkei up 2.5% to 26,791.12

- Topix up 1.7% to 1,934.93

- Hang Seng Index up 0.5% to 21,678.00

- Shanghai Composite little changed at 3,224.41

- Sensex up 0.6% to 61,049.16

- Australia S&P/ASX 200 little changed at 7,393.36

- Kospi down 0.5% to 2,368.32

- STOXX Europe 600 up 0.1% to 457.14

- German 10Y yield little changed at 2.10%

- Euro up 0.6% to $1.0855

- Brent Futures up 1.1% to $86.89/bbl

- Gold spot up 0.3% to $1,913.84

- U.S. Dollar Index down 0.39% to 101.99

Top Overnight News from Bloomberg

- ECB policymakers are starting to consider a slower pace of interest-rate hikes than President Christine Lagarde indicated in December, according to officials with knowledge of their discussions

- The BOJ standing pat caught some traders by surprise, but is unlikely to douse speculation that it will normalize policy as inflation in Japan accelerates and Governor Haruhiko Kuroda nears the end of his term

- China’s top economic official told an audience of international billionaires and bankers that his country’s economy will likely rebound to its pre-pandemic growth trend this year after coronavirus infections passed their peak

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were positive albeit with price action mostly kept rangebound after the weak lead from Wall Street, while focus overnight centred on the BoJ policy announcement in which the central bank defied the increased speculation for a policy tweak. ASX 200 was flat with strength in the tech and consumer sectors offset by losses in commodity-related stocks. Nikkei 225 was boosted after the BoJ stuck with its ultra-easy policy settings and reaffirmed its dovish guidance. Hang Seng and Shanghai Comp were choppy but with strength in key tech names after China approved licences for 88 new games including titles from Tencent and NetEase in a further sign of an end to its tech crackdown.

Top Asian News

- PBoC injected CNY 133bln via 7-day reverse repos with the rate kept at 2.00% and injects CNY 447bln via 14-day reverse repos with the rate kept at 2.15% for a CNY 515bln net injection.

- China’s NDRC’s said the economic development situation this year is still complicated, external environment is turbulent and pressure is still large, but it is confident and capable of promoting the continuous recovery and overall improvement of China’s economy, according to Reuters.

- Hong Kong is expected to end its COVID mask mandate by March or April, according to sources cited by Ming Pao News.

European bourses are contained overall, Euro Stoxx 50 +0.1%, as the dovish BoJ fails to provide impetus. US futures are similarly steady ahead of earnings, data and Fed speak, ES +0.1%. Within Europe, sectors are mixed with marked outperformance in Tech after updates from Just Eat and ASM International.

Top European News

- ECB’s Villeroy reaffirms that a European recession should be avoided in 2023, will bring inflation back to target around 2024/2025. Lagarde’s 50bp guidance remains valid. Will remain at the terminal rate for as long as is necessary; will go to the terminal by summer, not there yet.

- UK Chancellor Hunt is reportedly planning a “slimmed down” spring budget which will not feature tax cuts within the statement, via The Guardian citing sources which add that there will be tax cuts before the next election, with the autumn statement the most likely point to announce such a change.

- Germany is reportedly to narrowly avoid a 2023 recession, with price-adj. growth of 0.2%, via Reuters citing source/draft of the economic report; Inflation: 2023 6.0%, 2024 2.8%.

- Magnitude 7.0 earthquake strikes off Sulawesi, Indonesia; Tsunami waves are possible for coasts located within 300km of Indonesia’s quake epicentre, Pacific Tsunami Centre says.

- Ukraine Latest: Helicopter Crash Kills 18 People Near Kyiv

- Sweden Boosts Capacity to Send Power South to Ease Supply Crunch

- French Power Crunch This Winter Now Less Likely, Grid Says

- Women Are Macron’s Biggest Critics on Pension Reform

- BASF Drops After €7.3 Billion Russia Writedown Sparks Loss

BOJ

- BoJ kept its policy settings unchanged with rates at -0.10% and YCC maintained to target 10yr JGBs at 0% via unanimous vote, while it kept the yield band and yield target unchanged. BoJ stuck with its forward guidance on interest rates and guidance that it will continue large-scale JGB buying and make nimble responses for each maturity, while it reiterated that it will not hesitate to take additional easing measures as necessary. Furthermore, the BoJ extended the fund operation to support financial lending by one year and the Outlook Report contained cuts to Real GDP growth forecasts and mostly upward revisions to Core CPI estimates, although fiscal 2023 and fiscal 2024 Core CPI forecasts remained below the 2% price goal.

- BoJ Governor Kuroda (post-meeting press conference) says he is not expecting 10yr JGB yields to continue trading with yields above 0.5%, and there is no need to further expand its bond target band; today’s decision is not a change in BoJ’s monetary policy. It is still early days since the adjustment to yield bands made in December, BoJ needs more time to assess impact on market functions. YCC is fully sustainable, widening band has made YCC more sustainable. Important for FX rates to move stably, reflecting fundamentals; he has no specific comments on FX levels, noting that currency policy is the jurisdiction of the government.

FX

- Yen yields gains made on the premise of further BoJ YCT adjustment as the Bank holds fire.

- USD/JPY jumps to 131.57 from the low 128.00 area at one stage, DXY rebounds accordingly to 102.900 before sharp reversal on the back of strength elsewhere in the index.

- Sterling extends on UK pay gains as services and core inflation top consensus, Cable breaches 1.2300 on the way to 1.2360+ peak.

- Euro eyes resistance in the high 1.0800 zone as the Dollar recoils and Kiwi approaches 0.6500 and Aussie takes firmer hold of 0.7000 handle

- PBoC set USD/CNY mid-point at 6.7602 vs exp. 6.7644 (prev. 6.7222)

Fixed Income

- Core benchmarks have picked off the European morning’s lows to near unchanged levels, but remain shy of overnight BoJ-inspired peaks.

- The overnight BoJ derived upside seemingly fizzled out amid ECB’s Villeroy dismissing the dovish source reports and hot UK core CPI.

- Stateside, USTs are holding firmer than their EGB peers ahead of a packed afternoon docket.

Commodities

- Crude benchmarks are bid and have broken out of contained overnight ranges following the latest geopolitical rhetoric, lifting the complex to fresh YTD peaks.

- WTI Feb’23 and Brent Mar’23 are at the top-end of USD 80.55-81.86/bbl and USD 86.13-87.43/bbl parameters, ranges that mark fresh YTD peaks for the complex, though, the benchmarks remain well within late-2022 extremes.

- China’s NDRC warned iron ore trading companies and iron ore futures companies against price gouging and speculation, while it will step up supervision on iron ore’s spot and futures markets, according to Reuters.

- IEA Oil Market Report: Demand set to increase by 1.9mln BPD to a record of 101.7mln BPD.

- Spot gold is essentially unchanged and unable to derive much support from the Dollar’s weakness as the overall tone remains a tentative one post-BoJ.

- Copper prices are bid this morning in the wake of disruption to Glencore’s Antapaccay copper mine in Peru, which is operating at restricted capacity amid anti-government protests, according to Reuters sources.

Geopolitics

- US reportedly sends Ukraine US arms which were stored in Israel, according to NYT.

- Russian Foreign Minister Lavrov says discussions with Ukraine President Zelenskiy are not possible; ready to respond to Western proposals on Ukraine but have not seen any serious proposals; adds, that they will have to take corresponding military measures if Finland/Sweden were to join NATO.

- Ukrainian Minister of Internal Affairs has died in a helicopter crash near Kyiv, according to local journalists.

- Serbian President Vucic says Crimea is Ukraine, and the EU path is the only one for Serbia.

US Event Calendar

- 07:00: Jan. MBA Mortgage Applications 27.9%, prior 1.2%

- 08:30: Dec. Retail Sales Ex Auto and Gas, est. 0%, prior -0.2%

- 08:30: Dec. PPI Final Demand MoM, est. -0.1%, prior 0.3%; YoY, est. 6.8%, prior 7.4%

- PPI Ex Food and Energy MoM, est. 0.1%, prior 0.4%; YoY, est. 5.6%, prior 6.2%

- 08:30: Dec. Retail Sales Advance MoM, est. -0.9%, prior -0.6%

- Retail Sales Ex Auto MoM, est. -0.5%, prior -0.2%

- Retail Sales Control Group, est. -0.3%, prior -0.2%

- 09:15: Dec. Industrial Production MoM, est. -0.1%, prior -0.2%

- 09:15: Dec. Capacity Utilization, est. 79.5%, prior 79.7%

- 09:15: Dec. Manufacturing (SIC) Production, est. -0.2%, prior -0.6%

- 10:00: Nov. Business Inventories, est. 0.4%, prior 0.3%

- 10:00: Jan. NAHB Housing Market Index, est. 31, prior 31

- 14:00: Federal Reserve Releases Beige Book

- 16:00: Nov. Total Net TIC Flows, prior $179.9b

Central Bank speakers

- 09:00: Fed’s Bostic Makes Welcoming Remarks at Academic Conference

- 14:00: Fed’s Harker Discusses the Economic Outlook

- 14:00: Federal Reserve Releases Beige Book

- 17:00: Fed’s Logan Gives Speech in Austin

DB’s Jim Reid concludes the overnight wrap

The big news overnight is that there is no big news overnight as the BoJ met economists expectation that they wouldn’t change anything on YCC today despite increasing market expectation that they would. The policy does seems unsustainable if current conditions persist though as since the last meeting on December 20th, they’ve spent $265bn (a whopping 6% of annual GDP!) buying bonds. Indeed, as George Saravelos pointed out yesterday there are some reports suggesting the BoJ may own more than 100% of some benchmark 10yr bonds. So not only has it bought the entire stock, but it has lent it out to short-sellers who have sold it back to the BoJ. Before the meeting our Japanese economists suggested that he does expect the BoJ to abandon YCC by the end of Q2 this year, but more around forces such as the “shunto” spring wage negotiations, a positive output gap and leadership changes at the bank.