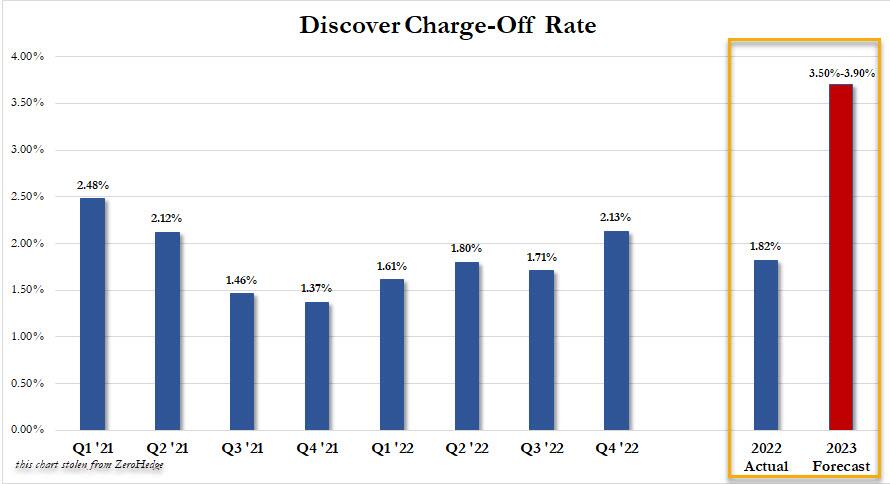

JAN 19/GOLD CLOSED UP $16.95 TO $1922.15/SILVER CLOSED HIGHER BY 24 CENTS TO $23.75//PLATINUM CLOSED DOWN $8.75 TO $1034.20//PALLADIUM CLOSED UP $36.50 TO $1755.90//COVID UPDATES//VACCINE IMPACT//VACCINE INJURY//DR PAUL ALEXANDER; A MUST VIEW TODAY//SLAY NEWS/UKRAINE VS RUSSIA UPDATES//FRANCE GRINDS TO A HALT DUE TO GOVERNMENT’S ATTEMPT TO CHANGE PENSION STATUS FROM 62 YRS OLD CITIZENS TO AGE 64//USA HOUSING STARTS PLUMMET//HUGE BUYER CANCELLATIONS IN NEW HOME CONTRACTS HITTING 68%//HUGE CHARGE OFFS IN DISCOVER CARDS DUE TO MASSIVE DELINQUENCY//SWAMP STORIES FOR YOU TONIGHT//

118 C MACQUARIE FUT 400 132 C SG AMERICAS 21 365 H MAREX CAPITAL M 1 624 H BOFA SECURITIES 969 657 C MORGAN STANLEY 1 2 661 C JP MORGAN 27 737 C ADVANTAGE 2 1 880 H CITIGROUP 1419 905 C ADM 4 1

TOTAL: 1,424 1,424 MONTH TO DATE: 4,375

JPMorgan stopped 0/1424

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR JAN/2023. CONTRACT: 1424 NOTICES FOR 142400 OZ or 4,429 TONNES

total notices so far: 4375 contracts for 437,500 oz (13.608 tonnes)

SILVER NOTICES: 16 NOTICE(S) FILED FOR 4,335,000 OZ/

total number of notices filed so far this month 951 for 4,755,000 oz

END

GLD

WITH GOLD UP $16.95

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 1.74 TONNES INTO THE GLD //

INVENTORY RESTS AT 910.98 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 24 CENTS

AT THE SLV// :/NO CHANGES IN SILVER INVENTORY AT THE SLV// WHAT A MASSIVE FRAUD!!!

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 498.05 MILLION OZ (THIS IS ALSO A CRIME SCENE@!!!!

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GIGANTIC SIZED 1058 CONTRACTS TO 132,920 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE HUGE GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.41 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. FOR THE PAST MONTH, OUR BANKERS HAVE RETURNED TO BEING NET SHORT AND THUS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.41 BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS, AS WE HAD A MONSTROUS GAIN ON OUR TWO EXCHANGES OF 2174 CONTRACTS. AS WELL, WE HAD ZERO EXCHANGE FOR RISK TRANSFER ( 0 CONTRACTS) AS THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 3.75 MILLION OZ. WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD: A GIGANTIC ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4,055. MILLION OZ FOLLOWED BY TODAY’S QUEUE. JUMP OF 80,000 OZ//NEW STANDING 4.870 MILLION OZ + 3.75 MILLION OF EXCHANGE FOR RISK//TOTAL STANDING 8.62 MILLION OZ//// V) GIGANTIC SIZED COMEX OI GAIN/ HUGE EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –146

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN:

TOTAL CONTRACTS for 12 days, total 6343 contracts: OR 31.715 MILLION OZ PER DAY. (519 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 31.715 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 31.715 MILLION OZ

RESULT: WE HAD A GIGANTIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1058 DESPITE OUR $0.41 LOSS IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A GIGANTIC SIZED EFP ISSUANCE CONTRACTS: 970 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JAN OF 4.055 MILLION OZ FOLLOWED BY TODAY’S 80,000 OZ. JUMP / //NEW STANDING INCREASES TO 4.870 MILLION OZ + EFR 3.75 MILLION = 8.620 MILLION OZ. .. WE HAVE AN ATMOSPHERIC SIZED GAIN OF 2028OI CONTRACTS ON THE TWO EXCHANGES FOR 10.14 MILLION OZ.. THE SILVER SHORTS HAVE BEEN HURT BADLY WITH SILVER’S HUGE RISE LATELY.

WE HAD 16 NOTICE(S) FILED TODAY FOR 80,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 3010 CONTRACTS TO 487,132 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 1676 CONTRACTS.

.

WE HAD A FAIR SIZED DECREASE IN COMEX OI (4686 CONTRACTS) WITH OUR $1.95 LOSS IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR JAN. AT 2.1710 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 1024 CONTRACTS OR 102400 OZ //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S ) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London). NEW STANDING 13.608 TONNES

YET ALL OF..THIS HAPPENED DESPITE OUR $1.95 LOSS IN PRICEWITH RESPECT TO TUESDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 2758 OI CONTRACTS (8.578 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A VERY STRONG SIZED 7444 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 487,132

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2758 CONTRACTS WITH 4686 CONTRACTS DECREASED AT THE COMEX AND 7444 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2758 CONTRACTS OR 8.578 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A VERY STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (7444 CONTRACTS) ACCOMPANYING THE GOOD SIZED LOSS IN COMEX OI (4686) TOTAL GAIN IN THE TWO EXCHANGES 2758 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) SMALL INITIAL STANDING AT THE GOLD COMEX FOR JAN. AT 2.1710 TONNES FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 102,400 OZ /NEW STANDING 13.648 TONNES///3) ZERO LONG LIQUIDATION //4) FAIR SIZED COMEX OPEN INTEREST LOSS 5) VERY STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JAN

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN :

47,657 CONTRACTS OR 4,765,700 OZ OR 148.23 TONNES 12 TRADING DAY(S) AND THUS AVERAGING: 3971 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES:148.23 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 148.23/3550 x 100% TONNES 4,16% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 148.23 TONNES INITIAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH GOLD (

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A GIGANTIC SIZED 1058 CONTRACTS OI TO 132,920 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 970 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 970 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 970 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1058 CONTRACTS AND ADD TO THE 970 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A MONSTROUS GAIN OF 2028 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 10.140 MILLION OZ//

OCCURRED DESPITE OUR 41 CENT LOSS IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//CORN

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED UP 15.87 PTS OR 0.49% //Hang Seng CLOSED DOWN 27.02 PTS OR 0.12% /The Nikkei closed DOWN 385.89 PTS OR 1,44% //Australia’s all ordinaries CLOSED UP 0.51% /Chinese yuan (ONSHORE) closed DOWN TO 6.7858//OFFSHORE CHINESE YUAN DOWN TO 6.7881// /Oil DOWN TO 78.94 dollars per barrel for WTI and BRENT AT 84.42 / Stocks in Europe OPENED ALL RED ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 4686 CONTRACTS DOWN TO 487,132 WITH OUR LOSS IN PRICE OF $11.45

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON-ACTIVE DELIVERY MONTH OF JAN… THE CME REPORTS THAT THE BANKERS ISSUED A VERY STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 7444 EFP CONTRACTS WERE ISSUED: ;: , . 0 FEB: 7444 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 7444 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2758 CONTRACTS IN THAT 7444 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED COMEX OI LOSS OF 4686 CONTRACTS..AND THIS GOOD SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $1.95. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG .

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING Jan (13.648)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL (TOTAL SO FAR THIS YEAR 591.535 TONNES)

Dec. 64.541 tonnes

JAN/2023: 13.648 tonnes

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $1.95) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A GOOD SIZED GAIN OF 4434 CONTRACTS ON OUR TWO EXCHANGES // WE HAVE GAINED A TOTAL OI OF 13.791PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JAN. (2.1710 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 102,400 oz OR 3.185 TONNES… ALL OF THIS WAS ACCOMPLISHED WITH OUR FALL IN PRICE TO THE TUNE OF $1.95.

WE HAD – XX CONTRACTS COMEX TRADES REMOVED FROM OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 4434 CONTRACTS OR 443,400 OZ OR 13.791 TONNES

Estimated gold comex today 228,536//fair//

final gold volumes/yesterday 253,813///fair

INITIAL STANDINGS FOR JAN 2023 COMEX GOLD //JAN 19//

Total monthly oz gold served (contracts) so far this month

4375 notices 437500 13.608 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i) Into HSBC: 92,209.068 oz

2868 kilobars

total deposits: 92,209.068 oz

customer withdrawals: 0

Total withdrawals: nil oz

total 0 oz

total in tonnes: 0 tonnes

Adjustments:1 Brinks: 37,502.217 oz dealer to customer

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JANUARY.

For the front month of JANUARY we have an oi of 1437 contracts having gained 313 contracts

We had 711 notices served on Wednesday, so we gained 700 contracts or an additional 102,400 oz(3.185 tonnes) will stand for delivery in this

very non active delivery month of January. (queue jump)

February lost 15,260 contacts to 219,756

March gained 143 contracts to stand at 939.

April gained 9,133 contracts up to 210,956.

We had 1424 notice(s) filed today for 142400 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 27 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1424 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JAN. /2023. contract month,

we take the total number of notices filed so far for the month (4375 x 100 oz , to which we add the difference between the open interest for the front month of (JAN.1427 CONTRACTS) minus the number of notices served upon today 1424 x 100 oz per contract equals 438,800 OZ OR 13.648 TONNES the number of TONNES standing in this non active month of January.

thus the INITIAL standings for gold for the JAN contract month:

No of notices filed so far (4375 x 100 oz+ (1427 OI for the front month minus the number of notices served upon today (1424} x 100 oz} which equals 438,800 oz standing OR 12.648 TONNES in this NON active delivery month of JAN..

TOTAL COMEX GOLD STANDING: 13.648 TONNES (A VERY STRONG STANDING FOR METAL//COMEX RUNNING OUT OF PHYSICAL TO SERVE UPON OUR LONGS.

To calculate the number of silver ounces that will stand for delivery in JANUARY. we take the total number of notices filed for the month so far at 964 x 5,000 oz = 4,820,000 oz

to which we add the difference between the open interest for the front month of JAN(23) and the number of notices served upon today 16 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JAN./2023 contract month: 964 (notices served so far) x 5000 oz + OI for the front month of JAN (23 – number of notices served upon today (16) x 500 oz of silver standing for the JAN. contract month equates 4.870 million oz + 3.75 MILLION OZ ( EXCHANGE FOR RISK) = 8.62MILLION OZ//(TOTAL OZ OF SILVER STANDING).

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:59,231// est. volume today// good

Comex volume: confirmed yesterday: 76,646 contracts ( very good)

END

GLD AND SLV INVENTORY LEVELS

JAN 19/WITH GOLD UP $16.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES INTO THE GLD///INVENTORY RESTS AT 910.98TONNES

JAN 18/WITH GOLD DOWN $1.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.9 TONNES FROM THE GLD////INVENTORY RESTS AT 909.24 TONNES

JAN 17/WITH GOLD DOWN $11.45 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.14 TONNES

JAN 13/WITH GOLD UP $22.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD///INVENTORY RESTS AT 912.14 TONNES

JAN 12/WITH GOLD UP $20.55 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 912.43 TONNES

JAN 11/WITH GOLD UP $1.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.17 TONNES

JAN 10/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 915.33 TONNES

JAN 9/WITH GOLD UP $ 8.60 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD//.//INVENTORY RESTS AT 915.33 TONNES

JAN 6/WITH GOLD UP $28.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 916.77 TONNES

JAN 5/WITH GOLD DOWN $17.05 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 916.77 TONNES

JANUARY 4/WITH GOLD UP $32.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.64 TONNES

JAN 3/WITH GOLD UP $20.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:STRANGE: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 917.64 TONNES

DEC 30/WITH GOLD UP $.80 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 918.51 TONNES

DEC 29//WITH GOLD UP $8.35 TODAY:; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 918.51 TONNES

DEC 28/WITH GOLD DOWN $6.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE DEPOSIT OF 5.50 TONNES INTO THE GLD..//INVENTORY REST S AT 918.51 TONNES

DEC 27/WITH GOLD UP $18.15 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 913.01 TONNES

DEC 23/WITH GOLD UP $19,15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 913.88 TONNES/

DEC 22/WITH GOLD DOWN $29.35 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 913.88 TONNES

DEC 21/WITH GOLD FLAT TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 913.88 TONNES

DEC 20/WITH GOLD UP $27.05: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES INTO THE GLD////INVENTORY RESTS AT 912.14 TONNES

DEC 19/WITH GOLD DOWN $2.10: HUGE CHANGES IN GOLD INVENTORY AT THE GLD> A BIG WITHDRAWAL OF 3.47 TONNES FROM THE GLD//INVENTORY RESTS AT 910.41 TONNES

DEC 16/WITH GOLD UP $12.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD//INVENTORY RESTS AT 913.88 TONNES

DEC 15//WITH GOLD DOWN $31.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 911.56 TONNES

DEC 14/WITH GOLD DOWN $6.20: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 912.72 TONNES

DEC 13/WITH GOLD UP $32.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD///INVENTORY RESTS AT 910.41

DEC 12/WITH GOLD DOWN $17.60: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

DEC 9/WITH GOLD UP $8.90//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

Dec 8/WITH GOLD UP $4.05, OVER THE PAST 3 WEEKS WE LOST 2.04 TONNES//INVENTORY RESTS AT 908.09 TONNES

GLD INVENTORY: 910.98 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JAN 19/WITH SILVER UP 24 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 498.05 MILLION OZ

JAN 18/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 8.15 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 498.05 MILLION OZ///

JAN 17/WITH SILVER DOWN 35 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 506.200 MILLION OZ//

JAN 13/WITH SILVER UP 46 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.5 MILLION OZ FROM THE SLV..//INVENTORY RESTS AT 506.200 MILLION OZ//

JAN 12/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 508.700 MILLION OZ/

JAN 11/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 508.700MILLION OZ

JAN 10/WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.65 MILLION OZ

JAN 9/WITH SILVER DOWN 9 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.65 MILLION OZ//

JAN 6/WITH SILVER UP 54 CENTS TODAY;BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.20 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 509.65 MILLION OZ//

JAN 5/WITH SILVER DOWN 50 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.10 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 505.45 MILLION OZ//

JAN 4/WITH SILVER DOWN 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 506.55 MILLION OZ/

JAN 3/WITH SILVER UP 24 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: STRANGE: A WITHDRAWAL OF 1.2 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 507.85 MILLION OZ/

DEC 30/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.050 MILLION OZ

DEC 29/ WITH SILVER UP $0.63 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.050 MILLION OZ

DEC 28//WITH SILVER DOWN 46 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.715 MILLION OZ INTO THE SLV///..INVENTORY RESTS AT 509.050 MILLION OZ

DEC 27/WITH SILVER UP 34 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 507.350 MILLION OZ//

DEC 23/WITH SILVER UP 29 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT507.900 MILLION O//

DEC 22/WITH SILVER DOWN 53 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 507.90 MILLION OZ//

DEC 21/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.0 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 507.90 MILLION OZ//

DEC 20/WITH SILVER UP 105 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV:: A DEPOSIT OF 700,000 OZ INTO THE SLV///INVENTORY RESTS AT 509.90 MILLION OZ//

DEC 19/WITH SILVER DOWN 13 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.05 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 509.20 MILLION OZ//

DEC 16/WITH SILVER UP 2 CENTS; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.85 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 508.15 MILLION OZ//

DEC 15/WITH SILVER DOWN 78 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF EXACTLY 2.00 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 510.000 MILLION OZ

DEC 14/WITH SILVER UP 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 512.000 MILLION OZ//

DEC 13/WITH SILVER UP 59 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 600,000 OZ FROM THE SLV////INVENTORY RESTS AT 513.900 MILLION OZ//

DEC 12/WITH SILVER DOWN 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 514.500 MILLION OZ//

DEC 9/WITH SILVER RISING 77 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.2 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 514.500 MILLION OZ.

DEC 8/WITH SILVER RISING 34 CENTS TODAY: OVER THE PAST 3 WEEKS, WE HAVE GAINED A STRONG: 44.777 MILLION OZ/INVENTORY RESTS AT 516.700 MILION OZ.

CLOSING INVENTORY 498.05 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

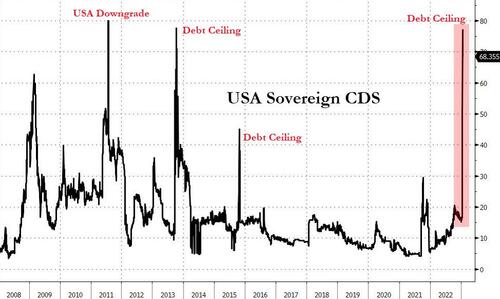

Here We Go Again! It’s Time For Another Debt Ceiling Fight

The clock is ticking down to another US debt ceiling fight.

According to Treasury Secretary Janet Yellen, the US government will officially bump up against the debt ceiling Thursday (Jan. 19).

The debt ceiling is “the total amount of money that the United States government is authorized to borrow to meet existing legal obligations, including Social Security and Medicare Benefits, military salaries, interest on the national debt, tax refunds and other payments.”

On Dec. 16, 2021, a law went into effect setting the new debt limit at $31.381 trillion. Once the government hits that debt level, it can no longer sell Treasuries or other debt instruments to fund spending.

But this doesn’t mean the government will simply shut down. The Treasury Department can implement “extraordinary measures” in order to continue funding government operations.

According to a letter Yellen sent to Congress, the Treasury will redeem existing investments and suspend future investments in the Civil Service Retirement Disability Fund and the Postal Service Retiree Health Benefits Fund. It will also suspend investment in a federal employee retirement system savings plan. According to Yellen, these moves will “reduce the amount of outstanding debt subject to the limit and temporarily provide extra capacity for Treasury to continue financing operations of the federal government.”

It’s not clear how long the government can continue operating using these extraordinary measures. Most analysts estimate it will give Congress until sometime in June. It will depend somewhat on how much revenue the IRS collects this spring.

HISTORY

Congress imposed the first debt ceiling in 1917. The Second Liberty Bond Act capped debt at $11.5 billion. This was supposed to put some kind of restraint on government borrowing. Of course, it didn’t. Every time the debt approaches the ceiling, Congress simply raises it. Between 1962 and 2011, lawmakers jacked up the debt “limit” 74 times, according to the Congressional Research Service.

In 2013, Congress came up with a new trick. Instead of raising the debt ceiling, it just suspended it. In 2014, Congress set the debt limit with a built-in “auto-adjust.” The auto-adjust ended in March 2015 with the debt ceiling set at $18.1 trillion. After that, Congress simply suspended the debt ceiling three times.

After Congress set the current debt ceiling in December 2021, it took just 46 days for Uncle Sam to dig itself another $1 trillion in the hole, pushing the national debt above the $30 trillion mark. Less than a year later, in October 2022, the national debt pushed above $31 trillion, setting the stage for yet another debt ceiling battle.

And this one might be a doozy with Republicans controlling the House, Democrats running the Senate, and Joe Biden in the White House.

LOOKING AHEAD

Make no mistake, Congress will raise the debt limit. It will posture. It will bluster. It will play a dramatic game of chicken. We might even have to endure another fake government shutdown. But when it’s all said and done, Republicans and Democrats will reach some kind of compromise. They will not leave the current debt ceiling in place. That would mean default – something nobody is seriously willing to contemplate.

In an honest world, the US would just go ahead and default. There is no way the federal government will ever pay off a $31 trillion-plus dollar debt. The government can’t even get its budget deficits under control. The Biden administration is spending money at a half-a-trillion-dollar per month clip, and any talk of spending cuts by the Republicans is nothing but window-dressing. The GOP had ample opportunity to slash spending during the first two years of Trump’s administration when it controlled both the White House and Congress. Instead, it ramped up spending and ran massive deficits.

As Peter Schiff noted in a recent tweet, the feds are running a Ponzi scheme to keep the government solvent.

Given that the debt ceiling has never meaningfully restrained borrowing and spending, why doesn’t Congress just scrap it altogether?

I think there are two reasons.

First, doing away with the debt ceiling would expose America’s fiscal irresponsibility to the world. We all know the federal government has a spending problem. But the debt ceiling creates the illusion of responsibility. It’s like a magic trick. We all know it’s not really magic. It’s an illusion created by the magician. But we like to believe it’s magic. It makes us feel good. The debt ceiling is an illusion that allows Americans to feel like their “representatives” are acting responsibly.

Second, the debt ceiling is ready-made for political theater. And there’s nothing politicians love more than political theater.

Republicans and Democrats are already jockeying for position in the debt ceiling fight. Republican leadership is demanding spending cuts before it will consider lifting the ceiling. A week ago, White House press secretary Karine Jean-Pierre said, “We will not be doing any negotiation.”

“I think it’s arrogance to say: ‘Oh, we’re not going to negotiate about anything,’ especially when it comes to funding. If anyone had a child and their credit card kept hitting the limit, you’d want to change the behavior,” Speaker of the House Kevin McCarthy (R) said.

Yellen warned that a failure to raise the debt ceiling would have dire consequences.

Failure to meet the government’s obligations would cause irreparable harm to the US economy, the livelihoods of all Americans, and global financial stability.”

Yellen’s not wrong. And this is exactly why Congress will raise the debt ceiling – or simply kick the can down the road by suspending it again.

In the meantime, brace yourself for hot political rhetoric and a lot of finger-pointing across the political aisle. We may even get another mythical government shutdown. But trust me, they won’t shut down any of the important things. The NSA will keep spying on you. The IRS will continue to collect taxes from you. The wars will rage on. And members of Congress will continue to collect their paychecks. There’s always money available for the things the government really wants to do.

The whole debt ceiling debate is nothing but political gamesmanship. So, grab a chair. Pop some popcorn. And enjoy the show.

end

“Reports Of Gold’s Death Are Greatly Exaggerated”: BofA

Gold posted a small gain in 2022, and it was one of the best-performing assets of the year. Nevertheless, there has still a perception in the mainstream that gold is dead. But that perception may be changing. In a recent note, Bank of America commodity strategist Michael Widmer said gold will be a “mainstay” in portfolios over the next several years.

The yellow metal faced significant headwinds in 2022. The Federal Reserve’s “war on inflation” meant higher interest rates and a strengthening dollar. Widmer said these dynamics have “prompted some soul-searching among market participants” when it comes to gold.

However, we think calling the death of gold is premature.”

Widmer said he is bullish on gold in 2023 and he thinks the bullish environment will persist for several years.

The macro backdrop is turning bullish gold; taking a longer-term perspective, our analysis also confirms that the yellow metal can be a potent portfolio diversifier.”

What exactly is that macro backdrop? Bank of America head of US economics Michael Gapen said he anticipates a mild recession in 2023 and that easing inflation will allow the Federal Reserve to pivot away from its tight monetary policy.

We anticipate the recession will be mild by historical standards, lasting two to three quarters before resolving by the end of the year. With inflation falling and unemployment rising, we think the Fed could begin to cut its policy rate beginning in December 2023.”

No. They’re going to surrender. Inflation is going to win that war. The Fed is going to run to fight another battle — at least it’s going to try to fight because it’s going to lose that battle too. That battle is going to be recession, maybe financial crisis, maybe a battle to try to prop up the US government whose insolvency is becoming a bigger problem with rising interest rates.”

But no matter the reason, any Fed pivot is bullish for gold, and that’s why Wilmer thinks investors will have renewed interest in the yellow metal.

Gold is a non-yielding asset, so tighter monetary policy raises opportunity costs, which in turn does not provide an incentive to increase exposure to the yellow metal. This has been a reason why price movements have been so muted in 2022. That said, we outlined in the past week that the macro-economic backdrop is now increasingly bullish gold, which meant that outflows from ETFs have subsided.”

With the big run-up of bitcoin over the last couple of years, many people proclaimed gold was dead. But Wilmer noted that gold and crypto are now following very different trajectories and have become essentially uncorrelated.

…gold and cryptocurrencies have sometimes been seen as competing for investor attention, with concerns that assets like Bitcoin (BTC) could cannibalise liquidity from the gold market.

Of course, both crypto and gold can be a means of payment, a store of value and are “no-man’s liability”.

We agree that BTC and gold share some similarities, but with various caveat, for instance around performance differentials. Meanwhile, with emissions becoming a focus, we highlight that the environmental damage from mining BTC relative to its value has been much larger than for gold.

Bottom line: the blockchain technology is evolving fast and there is more to crypto than BTC. Yet, for now, we think Bitcoin is not a direct challenger to gold.

The BoA note also referenced the recent surge in central bank gold buying and pointed out that some countries are diversifying away from the dollar. Gold can serve several functions, including serving as a means of payment and a store of value. It also mitigates counterparty risk.

With the world becoming multi-polar, the latter point is important for central banks, especially in emerging markets. To that point, in the run-up to the war in Ukraine, Central Bank of Russia had reduced USD holdings while at the same time boosting exposure to gold.”

While I find Bank of America’s macroeconomic analysis lacking, we end up drawing the same conclusion – the Federal Reserve will take its foot off the accelerator and return to loose monetary policy. After all, the global economy is built on easy money, debt, and money creation. It simply can’t operate without it. As Jim Grant said, “Certainly, the slowing rate of the rise in inflation is to be celebrated. It’s nice, but we are still left with a system that is inherently inflationary.”

At the end of the day, inflation and loose monetary policy are bullish for gold.

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

END

3. Chris Powell of GATA provides to us very important physical commentaries//

end

4. Other gold/silver commentaries

Global South: Gold-backed currencies to replace the US dollar

Robert Hryniak

4:45 PM (10 minutes ago)

to

The reality is energy intensive businesses are leaving Europe forever and going to China to survive in the long term. Thereby bypassing the US which is seen as on brink of decline. It is why the US should run from the Ukraine instead of rushing in as only hurt will come by diminished hegemony. Whether we in the West appreciate or like it the world moved and shook the day the US decided to take Russia off Swift which was colossal error. And now that genie released will never be put back. This will be changed reality that comes to each of us going forward.

The public’s pocketbooks have been hit hard by the skyrocketing cost of eggs in the last few months. Prices have doubled and, in some places, tripled over what they cost a year ago—if you can even find them in your local grocery store.

The average cost of a dozen eggs in the United States is over $4.25, more than twice what it was just a year ago. Options such as cage-free eggs or organic go for over $7. Inflation is a part of the reason, but the agriculture industry says the bigger cause is the outbreak of the avian flu here in the United States a year ago; nationwide, it has affected nearly 60 million birds—nearly 5 million of them here in Pennsylvania.

American consumers love their eggs. The food staple is highly regarded by every walk of life for its simplicity and accessibility; for some families, it is their major source of protein. For others, it is the most important ingredient in baking and the central element in preparing casseroles, pasta, and numerous other dishes.

For many of us, it is hard to make a meal without an egg, so of course consumers are deeply affected by this. However, there is another side of that story that we are not examining. That is the equally devastating economic impact this is having on American poultry farmers and all of those who work with them. Their lives, livelihoods, and family legacies have been upended and even destroyed by the avian flu, a worldwide outbreak that shows no signs of subsiding.

Stopping the spread of avian flu is like chasing a ghost.

The virus spreads easily through wild birds—in particular migratory birds that fly across the country, spreading it along the way with droppings that infect farm animals.

Farmers have to take drastic measures. Any interaction with the public is risky. And if even one bird is infected within a 6-mile radius of where an outbreak has occurred, the consequences can be devastating.

Chris Pierce, a member of a multiple-generation poultry farm family and president of the poultry management group Heritage Poultry in Annville, said he works with 120 poultry farms in Pennsylvania with management services that provide veterinarian nutritionists to assist the health and productivity of the farmer’s flocks that they service.

“The biosecurity measures all of the farmers infected or not, like not having visitors on your properties—covering your workers from head to toe in bio suits and constantly and meticulously disinfecting equipment, clothing, buildings, walls, tires—is expensive and mind-numbing,” he said. “Even the simplest thing such as a fertilizer truck or a delivery from UPS or Amazon or your children’s school bus can track the disease onto a farm and destroy their flocks, their income and their family’s legacy.”

“We’ve lost two of our family farms out of the 120 with the avian influenza in April of 2022,” he said. “If you are an area poultry farmer, your focus is on keeping birds healthy and caring for them because the birds cannot care for themselves. So that involves making sure all of the equipment in the barns, the feeders, the water system, the ventilation, the lighting systems is all safe because as an egg farmer, your No. 1 priority is the health and safety of your birds. It’s your income.”

Pierce says those are the things a poultry farmer can control. “When a disease you cannot control hits your farm, like the avian influenza, that can happen when there are 30,000 snow geese flying over your farm that have feces coming out. That’s when the uncertainty starts to unravel their lives and livelihoods,” he said.

Pierce also points to neighbors’ bird feeders and bird baths or homesteaders or families who purchase chickens to save money who don’t take the same stringent precautions as farmers do. These can inadvertently become a spreading source of the avian flu.

Pierce said having to isolate from everyone has devastated many of these farmers who rely on community and social gatherings such as church services, school functions, and festivals as part of their emotional well-being. The measures these farmers take are so drastic that many of them refuse to leave their farms for fear of picking up a particle on the tread of their tires or their shoes and then bringing it back to their farms and infecting their flocks.

“Then there is this constant fear and really a sense of hopelessness that despite all of the precautions, all of the economic and emotional toll, all of the hardships that this epidemic has had on poultry farmers, even more birds are going to die this upcoming season,” Pierce said.

Pierce is correct to be worried about the isolation, uncertainty, and fear that farmers are experiencing. These emotional impacts are rarely discussed in the farming community and in our culture, even though farmers and ranchers are nearly twice as likely to die by suicide as any other occupation, according to the Centers for Disease Control and Prevention.

Pierce said farmers are always affected by things that are out of their hands. “The weather, politics, global markets, commodities, trade, and the whims of newest food fad that influences the American consumer,” he explained. “The avian flu just adds to that uncertainty.”

For the first time in recent memory, poultry farmers in Pennsylvania, of which there are thousands, were not featured at the Pennsylvania Farm Show because of the deep precaution that local poultry farmers took to keep their flocks free of infection.

Chris Herr is the executive director of PennAg Industries, the trade group that represents over 500 agribusinesses and farms across Pennsylvania. He said he spent several days as a volunteer late last year euthanizing poultry whose farm had been infected. “It takes a toll on you, having to senselessly kill these birds,” he said, adding that he has spoken to several farm families who don’t know if they can take another year of this.

“The emotional impact of this isn’t just the killing of the poultry; it is also not being able to leave your farm. You know that fear is gripping to someone who understands that one trip to the store in town and a dropping from a migrant bird or something airborne might infect your entire livelihood.”

Gov.-elect Josh Shapiro (D-Pa.) was recently touring the massive Pennsylvania Farm Show with his newly named agriculture secretary, Russell Redding, a holdover from the Wolf administration. Both men said the issue remained a top priority heading into the new governor’s administration.

“There is the cost to the consumer, which is a big concern, but there is also the concerns of our poultry farmers that we our making our priority,” said Shapiro.

Pierce said that Redding, along with the state legislature, did a phenomenal job last Spring. “What they did and the challenges they had were handled very well. I am concerned as we head into what looks to be yet another year of this avian influenza this spring—can they do it again?” said Pierce.

This spring, the flu is expected to maintain its intensity across Pennsylvania. Indeed, Pierce mentioned that 20 percent of the testing done on the eggs in this country were conducted in the state’s labs.

“Our state is the No. 1 state in the country in USDA organic poultry,” Herr said. “This is an important industry, and it’s a point of pride for a lot of these farmers whose family has been doing this for two, three, four generations.”

Pierce says there are thousands of poultry farms in Pennsylvania alone. Some are small 30-acre farms; some are much larger. “There are a lot of niche markets in Pennsylvania,” he said. “We need to be able to have all of them communicate with each other. One outlier can take down an entire industry.”

-END-

6/CRYPTOCURRENCIES/BITCOIN ETC

END

.

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//THURSDAY MORNING.7:30 AM

ONSHORE YUAN: DOWN TO 6.7858

OFFSHORE YUAN: 6.7881

SHANGHAI CLOSED UP 15.87 PTS OR 0.49%

HANG SANG CLOSED DOWN 27.02 PTS 0.12%

2. Nikkei closed DOWN 385.89 PTS OR 1.44%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 102.06 Euro RISES TO 1.0816 UP 19 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.401!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 128.55/JAPANESE YEN RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.076%***/Italian 10 Yr bond yield RISES to 3.846%*** /SPAIN 10 YR BOND YIELD RISES TO 3.054…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.014//

3j Gold at $1907.60//silver at: 23.35 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 12/100 roubles/dollar; ROUBLE AT 68.87//

3m oil into the 78 dollar handle for WTI and 84 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 128.55/10 YEAR YIELD AFTER BREAKING .54% FALLS TO .401% ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9166–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9913 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.397% UP 2 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.563 UP 2 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,80…

GREAT BRITAIN/10 YEAR YIELD: 3.3715 % UP 6 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Slide With Treasuries As Recession Fears Mount

THURSDAY, JAN 19, 2023 – 08:05 AM

One day after the S&P had its worst day since Dec 15, failing to hold the 200dma, US equity futures entered Thursday extending recent losses with a third straight session in the red as renewed recession fears and the start of the earnings season weighed on risk appetite, sparking a risk-off tone that spread across global markets, from Japanese shares to oil contracts, sent bond yields lower and hit commodities. Pre-market Mega Caps and Metals/Miners were the biggest laggards. The dollar was flat, the VIX jumped above 21, and 10Y yields reversed earlier losses. The macro focus for today includes housing data, Philly Fed, and 3x Fedspeakers. Plus, there is a 10Y TIPS auction and NFLX kicks off MegaCap Tech earnings.

Contracts on the S&P 500 edged down 0.8% as of 7:30 a.m. ET and contracts for the Nasdaq 100 lost 0.7%.Stoxx 600 gauge halted a six-day rally. Most Treasuries erased gains, and the euro advanced, as hawkish remarks by ECB Governing Council member Klaas Knot reaffirmed the central bank’s aggressive stance.

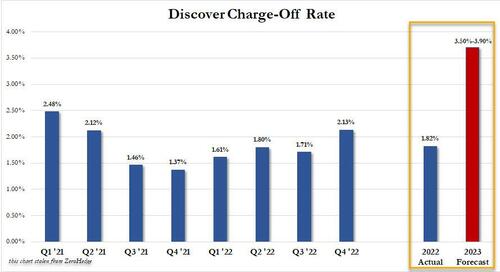

In pre-market trading, Discover Financial Services tumbled 6.4% as the company reported higher-than-forecast charges for the fourth quarter. Roblox Corp. slumped after the global gaming platform’s stock was downgraded to underweight from equalweight at Morgan Stanley, which expects slower bookings growth in the second half of the year. Freeport McMoRan also fell as copper resumed its losses. Philip Morris rose 1.2% after Jefferies upgraded the stock to buy, citing the outlook for reduced-risk products in the tobacco industry. Here are other notable premarket movers:

Alcoa shares slide 6.5% in US premarket trading after the aluminum and bauxite producer’s adjusted Ebitda for the fourth quarter fell short of analyst expectations, stoking worries that lower prices for aluminum and higher material and production costs were taking their toll.

CureVac gains 10% as UBS upgrades the stock to buy and more than doubles its price target, calling the Jan. 6 announcement on messenger RNA vaccines for flu and Covid-19 a “major de-risking” event.

Keep an eye on Chegg Inc. as KeyBanc Capital Markets analyst Jason Celino raised the recommendation to overweight from sector weight, citing Ebitda margin upside over the next 12 months.

Watch Alpine Immune Sciences after it was initiated with an overweight rating at Morgan Stanley, which said the biotech’s ALPN-303 treatment for autoimmune diseases is “underappreciated” and has broad potential.

Oppenheimer says it expects the US housing market to get worse before it gets better but that the backdrop is not as bad for homebuilder stocks as investors may expect. It initiates PulteGroup (PHM US) and Toll Brothers (TOL US) at outperform, Tri Pointe (TPH US) and DR Horton (DHI US) at perform.

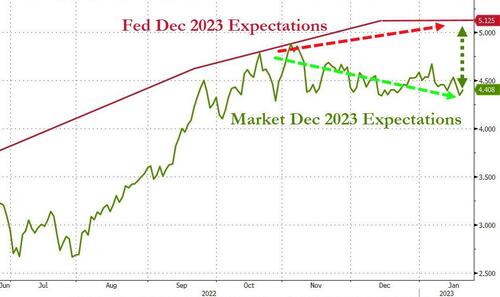

The S&P 500 had gained more than 4% in the first two weeks of the year on bets of easing inflation and as China reopens from Covid restrictions, a near-record short squeeze – which is now reversing – also helped. But this rally is now beginning to fizzle as data releases signal a decisive slowdown in the rest of the world. Reports from the US showed declines in consumer demand and business investment, boosting the probability of a recession in the world’s largest economy. That, however, didn’t deter Federal Reserve officials from reaffirming the need for tighter monetary policy.

St. Louis Fed President James Bullard said policy was not yet in restrictive territory and projected a forecast rate of up to 5.5% by the end of the year in the Fed’s dot plot projections. is “almost” in restrictive territory but not quite. Cleveland Fed President Loretta Mester said the Fed needs “keep going” and Philadelphia Fed chief Patrick Harker repeated his view of lifting interest rates in quarter-point increments “going forward.”

“This weakness in equity markets will continue a bit longer in this first quarter of the year as the market reprices what the Fed will do,” Sailesh Jha, the chief economist and head of market research for RHB Banking Group, said in an interview with Bloomberg Television.

“We think it remains possible that the rally is a ‘head fake,’ and that economic data will ultimately disappoint,”said UBS Global Wealth Management strategists, including Mark Haefele. “It remains too early to assume that the inflation threat has fully passed.”

European stocks are lower and on course to snap a six-day winning streak – the longest streak of gains since November 2021 – as evidence mounts of a slowdown in global growth. The Stoxx 600 is down 1.1% with miners, energy and consumer products leading declines. European Central Bank President Christine Lagarde said on Thursday that inflation remains far too elevated, vowing that policymakers won’t let up in their efforts to return price growth to the target. Here are the biggest European movers:

Belimo shares rise as much as 6.3% after FY22 sales beat consensus and the company’s own expectations, according to Baader, which expects another good year for the Swiss firm

Auto Trader shares rise as much as 3.4% after Goldman Sachs raised its recommendation to buy from neutral, citing appealing valuations and recovering auto sales revenue

Meltwater shares rise as much as 33%, to NOK17.65, after Altor and Marlin said they intend to offer NOK18 per share for the application software company

Deliveroo shares jump as much as 8.6% after the food delivery firm says its adj. Ebitda was almost breakeven in 1H, previously guided to be between 2H 2023 and 1H 2024

Hypoport rises as much as 9.7% on Thursday after Hauck & Aufhaeuser double upgrades to buy from sell and lifts price target by almost 180% on “game changing” messages in its 4Q report

Virbac shares jumped as much as 6.7% after the French health-care services provider reported positive fourth-quarter sales and outlook after the market close on Wednesday

Allfunds shares fall as much as 7.5% as HSBC cuts its rating on the wealth platform to hold from buy, saying 2023 is likely to remain challenging

Orsted shares drop as much as 4.1% after Oddo downgraded the Danish utility to neutral from outperform, citing a fairly uninspiring outlook and no margin for error in the last quarter

Boohoo shares drop as much as 8%, the most since Dec. 14, after the online clothing retailer said in a trading update that it would see a year-on-year decline in revenue

Metso Outotec shares slip as much as 3.1%, the most since Dec. 7, as Pareto cuts the mining and industrial equipment group to hold from buy after a strong recent performance

Earlier in the session, Asian stocks fell as Japanese shares gave back the gains made after the central bank left policy settings unchanged Wednesday, while Chinese tech giants retreated on worries about insider selling. The MSCI Asia Pacific Index dropped as much as 0.9% on Thursday, poised to snap a two-day rally. Japanese equities were the biggest drags to the regional benchmark as weak economic data from the US raised concerns over a slowdown and as the yen strengthened. The Topix Index fell 1% to 1,915.62 as of the 3 p.m. market close in Tokyo, while the Nikkei 225 declined 1.4% to 26,405.23. Toyota Motor contributed most to the Topix’s loss, decreasing 2.4%. Out of 2,161 stocks in the index, 596 rose and 1,436 fell, while 129 were unchanged. “In the end, it all comes down to the big question of how the US economy is doing,” said Ryuta Otsuka, a strategist at Tokyo Securities. “The US earnings season has just started and we will watch the overall movement of US stocks.” A gauge of Chinese technology stocks fell more than 1% after Kuaishou Technology’s co-founder sold some of his stake, fueling concerns that corporate insiders may be cashing out after the sector’s recent rally.

“In general, the market is concerned about the perception of an insider opportunistically selling after a recent rally. This concern is compounded when someone significant like a co-founder is selling,” said Justin Tang, head of Asian research at United First Partners. The soft US retail sales in December also added to concerns about economic growth, countering optimism that the Federal Reserve may start to ease its monetary tightening. That might create headwinds for Asian equities after their outperformance over US and European peers in the past few months. “Tempering optimism with cautionis not just prudent, but arguably necessary,” said Vishnu Varathan, Asia head of economics and strategy at Mizuho Bank Ltd. “Further tightening into 2023 will necessarily build on tail risks of a hard landing that accompanies a tightening cycle as pronounced as this one.”

Australian stocks gained: the S&P/ASX 200 index rose 0.6% to close at 7,435.30, swinging from an earlier loss, after employment unexpectedly fell last month while the jobless rate remained unchanged, sending the currency and bond yields lower as traders pared bets on a February interest-rate increase. The benchmark closed the highest since April 22, boosted by strength in mining shares and banks. In New Zealand, the S&P/NZX 50 index fell 0.3% to 11,885.64. Earlier, the nation’s Prime Minister Jacinda Ardern announced she is stepping down in a shock resignation ahead of a general election later this year

India stocks declined as earnings of makers of consumer staples and durables continue to signal slowing consumption, while elevated costs weaken sentiment. The S&P BSE Sensex fell 0.3% to 60,858.43 in Mumbai, while the NSE Nifty 50 Index eased by a similar measure. For the week, the gauges have ease risen nearly 1%, mainly helped by software exporters, as most of reported strong profit growth for the latest quarter. Asian Paints fell 2.7% as India’s biggest paint producer reported December-quarter earnings that trailed analysts’ estimates, with the company saying that extended monsoon impacted its volumes, sapping sales. Reliance Industries will release numbers on Friday. Fourteen of the 20 sector sub-gauges compiled by BSE Ltd. declined, led by utilities, while oil & gas index was the top gainer, helped by advances in state-run oil marketers that benefit from easing crude prices

In FX, the BBG Dollar Index was little changed and the greenback traded mixed against its Group-of-10 peers, while the yen is the best performer among the G-10s, rising 0.4% versus the greenback; the euro adds 0.3% after ECB’s Knot said he expects multiple 50bps hikes. His comments also pushed German 10-year bonds into negative territory while the US and UK equivalents hold on to small gains.

The euro rose to a day-high and the region’s front-end yields extended a rise after ECB Governor Christine Lagarde reaffirmed ambitions to get inflation back to target. ECB Governing Council member Klaas Knot earlier said there’ll be more than one half-point increase in interest rates, with the inflation situation still “not satisfactory”. Money markets rapidly added further tightening bets

The pound pared Wednesday’s rally. House prices in the UK slid for a third consecutive month in December according to a survey by the Royal Institution of Chartered Surveyors, which adds to concerns that the nation’s housing market is likely to tumble this year. The gilt curve twist-flattened

Norway’s krone pared losses after the central bank kept its policy unchanged, as forecast by the majority of economists in a Bloomberg survey. It signaled a likely quarter- point increase in borrowing costs in March is still needed to bring inflation under control

The Aussie and Kiwi were the worst G-10 performers. The Aussie dropped nearly 1% to a one-week low of 0.6875, after data showed employers cut jobs in December, when economists expected a job gain of 25,000. Australia’s bonds extended opening gains and traders dialed back expectations of a February rate hike

The yen strengthened as US yields dropped. Japan’s bonds were mixed. An auction of new 20-year debt received strong demand

Foreign selling of Japan’s bonds accelerated in the past week as the yield on the benchmark 10- year government bond rose and the Japanese yen strengthened

In rates, Treasuries initially advanced across the curve, but later gave up the gains. As of 8:00am ET, Treasuries from belly to long-end are slightly cheaper on the day after erasing gains. Slide was led by bunds following hawkish remarks by European Central Bank Governing Council member Klaas Knot. Asia-session gains tracked a rally in Australian bonds sparked by weak employment data. US front-end yields are little changed with longer maturities cheaper by 1bp-2bp, steepening 2s10s spread by ~2bp; 10-year around 3.39% lags German counterpart by ~3bp. Treasury auctions Thursday include $17b 10-year TIPS sale at 1pm New York time. The dollar issuance slate includes two deals so far; Wednesday volumes were light given many corporate issuers are in self- imposed quiet periods before reporting earnings.

In commodities, oil fell for a second day as traders had to contend with US recession worries as well as another build in inventories. West Texas Intermediate dropped below $79 a barrel after declining almost 1% on Wednesday. IEA’s head Birol says he does not see tightness in (the oil) market currently but have to be aware of uncertainties, via Reuters; may see tighter markets in 2023, more than some others may think. If China’s economy rebounds this year as expected, will see stronger demand that will pressure the market. Russian oil exports seem more resilient than initially thought but will fall further in Q1 and beyond. Spot gold rises roughly $6 to trade near $1,910/oz. Copper fell 1.4% in London trading

Bitcoin is little changed overall with numerous speakers ahead including ECB’s Knot explicitly on crypto, currently holding within USD 20.6k-20.8k parameters.

Looking to the day ahead now, and central bank speakers include ECB President Lagarde, the ECB’s Knot, Fed Vice Chair Brainard, and the Fed’s Collins and Williams. In addition, the ECB will be publishing the account of their December meeting. Otherwise, US data releases include the weekly initial jobless claims, December’s housing starts and building permits, along with the Philadelphia Fed’s business outlook survey for January. Finally, earnings releases include Procter & Gamble and Netflix.

Market Snapshot

S&P 500 futures down 0.4% to 3,930.00

STOXX Europe 600 down 0.7% to 454.23

MXAP down 0.5% to 166.17

MXAPJ down 0.3% to 544.50

Nikkei down 1.4% to 26,405.23

Topix down 1.0% to 1,915.62

Hang Seng Index down 0.1% to 21,650.98

Shanghai Composite up 0.5% to 3,240.28

Sensex down 0.3% to 60,889.40

Australia S&P/ASX 200 up 0.6% to 7,435.31

Kospi up 0.5% to 2,380.34

German 10Y yield little changed at 2.03%

Euro up 0.3% to $1.0821

Brent Futures down 0.8% to $84.30/bbl

Brent Futures down 0.8% to $84.30/bbl

Gold spot up 0.4% to $1,911.05

U.S. Dollar Index down 0.18% to 102.17

Top Overnight News from Bloomberg

UBS Asset Management and Schroders Plc are sticking with bets Japanese government bond yields will rise on the expectation the BOJ will eventually stop capping the 10-year benchmark at 0.5%, even after it kept the so-called curve control policy unchanged Wednesday. Torica Capital Pty also expects the central bank to fall in line and shift toward the global trend of raising rates

The best start to a year for bond returns is helping fuel an unprecedented debt-sale bonanza by governments and companies around the world of more than half a trillion dollars

Strikes coordinated by French unions aim to bring much of the country to a standstill on Thursday in a protest against government plans to revamp the pension system and a test of president Emmanuel Macron’s ability to resist street pressure

Foreign funds sold a record amount of Chinese bonds in 2022 mainly due to the nation’s wide yield gap with the US. Analysts are now weighing the outlook for the nation’s debt amid a potential Federal Reserve pivot and a reopening-led jump in yuan bond yields

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed with most major indices rangebound following the negative lead from Wall St, where risk sentiment deteriorated after a slew of disappointing US data and hawkish Fed rhetoric. ASX 200 climbed above 7,400 with the index led by miners after an increase in BHP’s quarterly iron ore output although gains were capped by disappointing jobs data and losses in the energy sector amid a pullback in oil prices and with Santos pressured due to a reduction in its FY output guidance. Nikkei 225 underperformed after markets mostly faded the BoJ-rally with many viewing the central bank’s decision to refrain from policy adjustments as a fleeting effort to delay the inevitable. Hang Seng and Shanghai Comp swung between gains and losses with price action cautious as the upside in the property sector counterbalanced the notable weakness in the large tech names.

Top Asian News

Chinese President Xi expressed concern about the spread of COVID-19 to rural areas as China heads towards the Lunar New Year, according to FT.

Hong Kong Chief Executive Lee said the government will scrap the quarantine order for people infected with COVID-19 from January 30th, according to Reuters.

New Zealand PM Ardern announced to step down on February 7th and the Labour party is to vote on a new leader on January 22nd which Deputy PM Robertson will not stand in. Furthermore, PM Arden said she no longer has enough in the tank to do the job justice and that the general election will be held on October 14th.

China is preparing for a new trading link with Hong Kong for foreigners to hedge bonds; PBoC shared draft riles for the Swap Connect to Chinese financial institutions last month, according to Bloomberg citing sources.

European bourses are pressured across the board, Euro Stoxx 50 -1.2%, as ECB officials continue to pushback on dovish reports. Sectors are all in the red with Basic Resources and Energy names lagging given underlying commodity pricing. US futures are lower across the board, as the ES continues to move below 4k ahead of more earnings and key Fed speak, ES -0.5%.

Top European News

ECB’S Knot says market developments of late are not entirely welcome, via CNBC; ECB won’t stop after a single 50bp hike, planning to hike by 50bp multiple times. No signs of underlying inflation pressures abating; core inflation shows no signs of abating. Currently only focused on the risk of doing too-little. Will be in “tightening mode” until at least mid-year.

ECB President Lagarde says economic news has become much more positive; may only see a small contraction in GDP in the Eurozone; 2023 will be better than feared. Will stay the course with rate hikes.

Irish PM Varadkar has said the 25th Anniversary of the Good Friday Agreement was not an absolute deadline in law for the EU and UK to secure agreement on the Northern Ireland Protocol, according to RTE’s Connelly.

FX

DXY was seemingly capped on approach to 102.50 amid a general downturn in risk with the USD facing pressure from the Euro and Yen.

With the JPY continuing its post-BoJ reversal and EUR/USD comfortably reclaiming 1.08+ in wake of ECB’s Knot pushing back on earlier dovish reports.

Antipodeans are the stand-out laggards with Australian labour data and the unexpected resignations of New Zealand’s PM contributing; AUD/USD sub-0.69 and NZD/USD sub-0.64.

NOK experienced modest gyrations around 10.75 against the EUR post-Norges Bank, with this perhaps just an unwinding of the minority hawkish positioning going into the announcement.

Norges Bank holds its Key Policy Rate at 2.75% (vs. split expectation for 25bps/Unch. but bias towards unchanged), decision was unanimous; “The policy rate will most likely be raised in March”. Subsequently, Governor Bache says they have not yet made new forecasts for rate developments beyond March.

CBRT holds its Weekly Repo Rate steady at 9.00% as expected.

PBoC set USD/CNY mid-point at 6.7674 vs exp. 6.7680 (prev. 6.7602).

Fixed Income

EGBs and particularly Bunds have retreated from initial peaks and have dragged Gilts and USTs lower in tandem.

Downside that was initially sparked by ECB’s Knot sticking to his hawkish lines and thereafter irrespective of well covered French and Spanish issuance.

USTs themselves have been dragged down to unchanged levels, with attention turning to a busy docket of Fed speak, with Brainard perhaps the highlight.

Commodities

WTI and Brent March’23 futures are softer intraday with prices meandering around USD 0.50/bbl above APAC lows of USD 78.10/bbl and USD 83.76/bbl respectively.

US Energy Inventory Data (bbls): Crude 7.6mln (exp. -0.6mln), Gasoline 2.8mln (exp. 2.5mln), Distillate -1.8mln (exp. 0.1mln), Cushing 3.7mln.

Qatar Energy set March-loading Al-Shaheen crude term price at a premium of USD 1.37/bbl above Dubai quotes which is the lowest in 21 months, according to Reuters citing traders.

IEA’s head Birol says he does not see tightness in (the oil) market currently but have to be aware of uncertainties, via Reuters; may see tighter markets in 2023, more than some others may think. If China’s economy rebounds this year as expected, will see stronger demand that will pressure the market. Russian oil exports seem more resilient than initially thought but will fall further in Q1 and beyond.

LME CEO says there is untapped demand for trading in Asian hours, via CNBC.

Spot gold mirrors Dollar action but the yellow metal found some overnight support around the USD 1,900/oz mark but remains off yesterday’s 1,925.79/oz peak.

Citi released some metal forecasts this morning and upgraded its 0-3month copper and aluminium forecasts to USD 10k/T (prev. 7.8k/T) and USD 2.7k/T (prev. 2.35k/T) respectively.

Geopolitics

US Secretary of State Blinken tweeted that the US announced an additional USD 125mln in funding to support Ukraine’s energy and electric grid against Russian attacks designed to leave millions without power during the winter months.

US is finalising a large package of military aid to Ukraine which officials said will likely total as much as USD 2.6bln, according to AP.

US Event Calendar

08:30: Jan. Continuing Claims, est. 1.66m, prior 1.63m

08:30: Dec. Building Permits MoM, est. 1.0%, prior -11.2%, revised -10.6%

08:30: Dec. Housing Starts MoM, est. -4.8%, prior -0.5%

08:30: Dec. Building Permits, est. 1.37m, prior 1.34m, revised 1.35m

08:30: Jan. Initial Jobless Claims, est. 214,000, prior 205,000

08:30: Jan. Philadelphia Fed Business Outl, est. -11.0, prior -13.8, revised -13.7

08:30: Dec. Housing Starts, est. 1.36m, prior 1.43m

Central Bank Speakers

09:00: Fed’s Collins Speaks at Housing Conference

13:15: Fed’s Brainard Discusses the Economic Outlook

18:35: Fed’s Williams Speaks at Event in New York

DB’s Jim Reid concludes the overnight wrap

Yesterday saw the biggest risk-off move so far in 2023, with equities slumping and sovereign bonds rallying after the latest US data magnified recession concerns and raised the prospect the Fed wouldn’t be as aggressive with their rate hikes as expected. In particular, the US PPI for December surprised substantially on the downside, adding to hopes that inflation was durably on the way down. That theme was then cemented by weak reports on retail sales and industrial production, which only added to the arguments in favour of the Fed easing up over the coming weeks. In turn, that spurred a big surge for Treasuries, with the 10yr yield down -17.8bps to 3.37%, and a further -4.9bps move overnight down to 3.32%. That means it’s now more than -100bps beneath its intraday high for this cycle of 4.34% back on October 21, whilst the S&P 500 (-1.56%) saw its biggest decline in a month.

When it comes to the specifics, the PPI release for December came in at -0.5% on a monthly basis (vs. -0.1% expected), and the previous month’s growth was also revised down a tenth to +0.2%. This came as a big surprise to markets, since it was beneath every economist’s estimate on Bloomberg, and it was also the fastest decline in monthly prices since April 2020 at the height of the pandemic. Furthermore, it took the year-on-year change down to +6.2% (vs. +6.8% expected), which is its weakest level since March 2021.

Alongside the PPI reading, we also had the latest retail sales data for December, which also surprised on the downside at -1.1% (vs. -0.9% expected), along with a four-tenths downward revision to November’s reading, which now shows a -1.0% contraction as well. For industrial production it was much the same story again, with a worse-than-expected contraction at -0.7% (vs. -0.1% expected), and a downward revision to the previous month.

With that downside surprise on the PPI data and the weaker-than-expected numbers elsewhere, investors moved to price in a less aggressive pace of rate hikes over the months ahead. In particular, the terminal rate priced in for June came down by -5.4bps to 4.86%, its lowest level so far this year, with a further decline of -1.7bps overnight to 4.84%. And looking further out, the rate priced in by end-2023 came down by -9.5bps to 4.35%, which again is the lowest of the year so far, with a further -3.7bps decline overnight to 4.31%.

When it came to Fed speakers, we heard from St. Louis Fed President James Bullard yesterday, who continued with his normally hawkish tone. He said that the policy rate was not yet in what he would call restrictive territory and that “policy has to stay on the tighter side during 2023.” He also noted that he expected fed funds to finish the year between 5.25% and 5.50%, and was in open to getting there quicker by increasing rates by 50bps at the next meeting. Cleveland Fed President Loretta Mester acknowledged that pricing pressures were moving the right way across different metrics but also that rates need to get higher. Finally, the latest Fed Beige Book pointed to expectations of easing inflation, saying that “contacts across districts said they expected future price growth to moderate further in the year ahead.” The report also held key information with regards to employment saying “firms hesitated to lay off employees even as demand for their goods and services slowed and planned to reduce headcount through attrition if needed.” This tracks with the recent economic data showing declining retail sales and robust payrolls.

The prospect of a less aggressive Fed led to a further rally in Treasuries, and as mentioned at the top 10yr yields came down -17.8bps to 3.37%. The moves were driven by lower real yields, with the 10yr real yield down by -13.6bps on the day to 1.24%. And the effects were evident elsewhere, with the dollar index (-0.03%) spending much of yesterday at its lowest level since May before recovering to finish with only a modest decline. Likewise, the Bloomberg index of US financial conditions eased to its most accommodative level since last February during European trading yesterday, before falling back as the risk-off sentiment took hold.

Although Treasuries were rallying, the risk-off tone meant that US equities were much less resilient, with the S&P falling back -1.56% as recession concerns mounted. That was echoed across the other major indices, with the NASDAQ (-1.24%) and the Dow Jones (-1.81%) falling back as well. However in Europe, the recent equity outperformance relative to the US continued, with the STOXX 600 (+0.23%) advancing for a 6th consecutive session. Looking forward, US futures are pointing to further losses ahead, with contracts on the S&P 500 (-0.13%) and NASDAQ 100 (-0.06%) edging lower.