FEB 22/GOLD CLOSED DOWN 60 CENTS TO $1832.65/SILVER CLOSED DOWN 22 CENTS TO $21.63//PLATINUM CONTINUES TO CLIMB AGAINST PALLADIUM: PLATINUM ROSE BY $11.65 TO $953.25 WHILE PALLADIUM CLOSED DOWN $36.70 TO $1491.95//UPDATES ON COVID//VACCINES//DR PAUL ALEXANDER/DR PANDA/VACCINE IMPACT//SLAY NEWS//UPDATES ON RUSSIA VS UKRAINE//UPDATES ON EAST PALESTINE DISASTER//TRUMP VISITS EAST PALESTINE//USA DATA: WORLD’S LARGEST CHIP MAKER INTEL SUFFERS LOSS AND CUTS ITS DIVIDEND//SWAMP STORIES FOR YOU TONIGHT./

072 C GOLDMAN 1 104 C MIZUHO 1 118 C MACQUARIE FUT 201 435 H SCOTIA CAPITAL 1 624 H BOFA SECURITIES 98 657 C MORGAN STANLEY 2 1 661 C JP MORGAN 10 686 C STONEX FINANCIA 5 709 C BARCLAYS 1 737 C ADVANTAGE 1 800 C MAREX SPEC 4 8 905 C ADM 13 991 H CME 67

TOTAL: 207 207

JPMORGAN STOPPED 10/207

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR FEB/2023. CONTRACT: 207 NOTICES FOR 20700 OZ or 0.6438 TONNES

total notices so far: 14,846 contracts for 1,484,700 oz (46.180 tonnes)

SILVER NOTICES: 8 NOTICE(S) FILED FOR 40,000 OZ/

total number of notices filed so far this month :860 for 4,300,000 oz

END

GLD

WITH GOLD DOWN $0.60

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/NO CHANGES IN GOLD INVENTORY AT THE GLD////

INVENTORY RESTS AT 919.92TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 22 CENTS

AT THE SLV// SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ INTO THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 485.693. MILLION OZ (CORRECTED)

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 2732 CONTRACTS TO 123,906 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE FAIR LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.14 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. WE HAVE NOW SURPASSED OUR ALL TIME LOW OF 124,000 OI CONTRACTS. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.14). AND WERE SUCCESSFUL IN KNOCKING SOME SPEC LONGS, AS WE HAD A HUGE SIZED LOSS ON OUR TWO EXCHANGES 1989 CONTRACTS. AS WELL, WE HAD 890 NOTICES FOR EXCHANGE FOR RISK TRANSFER (4.45 MILLION OZ. ) AS THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 6.225 MILLION OZ. WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD: A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS( 569 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 0.540. MILLION OZ FOLLOWED BY TODAY’S 115,000 OZ QUEUE JUMP OF 40,000 OZ// NEW TOTALS STANDING = 4.40 MILLION OZ + 6.225 MILLION OF EXCHANGE FOR RISK//TOTAL STANDING 10.625 MILLION OZ//// V) HUGE SIZED COMEX OI LOSS/ GOOD SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -174

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB:

TOTAL CONTRACTS for 15 days, total 14,067 contracts: OR 70.335 MILLION OZ . (937 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 70.335 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 70.335/ MILLION OZ/INITIAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2732 DESPITE OUR $0.14 GAIN IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE CONTRACTS: 569 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB OF 0.54 MILLION OZ FOLLOWED BY TODAY’S 40,000 OZ QUEUE JUMP = NEW STANDING: 4.40 MILLION OZ + 6.225 MILLION OZ EXCHANGE FOR RISK://NEW STANDING INCREASES TO 10.625 MILLION OZ .. WE HAVE A HUGE SIZED LOSS OF 1989OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 8 NOTICE(S) FILED TODAY FOR 40,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A TINY SIZED 132 CONTRACTS TO 422,648 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 1722 CONTRACTS.

.

WE HAD A TINY SIZED INCREASE IN COMEX OI ( 132 CONTRACTS) DESPITE OUR $7.45 LOSS IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR FEB. AT 41.601 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 6000 OZ //NEW STANDING: 47.079 TONNES//(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S ) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London). TONNES

YET ALL OF..THIS HAPPENED WITH OUR $7.45 LOSS IN PRICEWITH RESPECT TO TUESDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 1610 OI CONTRACTS (5.007 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1478 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 422,248

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1610 CONTRACTS WITH 132CONTRACTS INCREASED AT THE COMEX AND 1478 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1610 CONTRACTS OR 10.364 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1478 CONTRACTS) ACCOMPANYING THE TINY SIZED GAIN IN COMEX OI (132) TOTAL GAIN IN THE TWO EXCHANGES 1610 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 41.601 TONNES FOLLOWED BY TODAY’S 6,000 OZ QUEUE JUMP // ///3) ZERO LONG LIQUIDATION //4) TINY SIZED COMEX OPEN INTEREST GAIN// 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

FEB

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB :

38,887 CONTRACTS OR 3,740,900 OZ OR 120.95 TONNES 15 TRADING DAY(S) AND THUS AVERAGING: 2592 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15 TRADING DAY(S) IN TONNES 120.95 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 120.95/3550 x 100% TONNES 3.40% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 120.95 TONNES/INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH GOLD (

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUGE SIZED 2732 CONTRACTS OI TO 123,906 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A RECORD LOW OF 124,080 CONTRACTS TODAY.

EFP ISSUANCE 569 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 569 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 569 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2732 CONTRACTS AND ADD TO THE 569 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE LOSS OF 2163 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 10.815 MILLION OZ//

OCCURRED DESPITE OUR TINY $0.14 GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED DOWN 15.38 PTS OR 0.47% //Hang Seng CLOSED DOWN 105.65 PTS OR 0.85% /The Nikkei closed DOWN 368.78 PTS OR 1.34% //Australia’s all ordinaries CLOSED DOWN 0.36% /Chinese yuan (ONSHORE) closed DOWN 6.8947 //OFFSHORE CHINESE YUAN DOWN TO 6.9014// /Oil DOWN TO 75.93 dollars per barrel for WTI and BRENT AT 82.51 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A TINY SIZED 132 CONTRACTS UP TO 422,648 DESPITE OUR LOSS IN PRICE OF $7.45. I THINK WE HAVE HIT OUR LOW IN OPEN INTEREST YESTERDAY AT 422,516.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF FEB… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1478 EFP CONTRACTS WERE ISSUED: : APRIL 1478 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1478 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 1610 CONTRACTS IN THAT 1478LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 1854 CONTRACTS..AND THIS TINY SIZED GAIN ON OUR TWO EXCHANGES HAPPENED (DESPITE OUR FALL IN PRICE OF $7.45). WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: FEB (47.079)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 46.893 tonnes

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $7.45) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR SIZED GAIN OF 3332 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 5.007 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR FEB. (41.219 TONNES) FOLLOWED BY TODAY’S QUEUE. JUMP OF 6000 OZ OR 0.1866 TONNES//NEW STANDING INCREASES TO 47.079 tonnes … ALL OF THIS WAS ACCOMPLISHED DESPITE OUR FALL IN PRICE TO THE TUNE OF $7.45.

WE HAD- 1722 CONTRACTS COMEX TRADES (REMOVED) TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 1610 CONTRACTS OR 161,000 OZ OR 5.007 TONNES

Estimated gold comex today 123,827// //poor

final gold volumes/yesterday 220,181/// fair

INITIAL STANDINGS FOR FEB 2023 COMEX GOLD //FEB 22//

Total monthly oz gold served (contracts) so far this month

14,847 notices 1,484,700 46.180TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: NIL oz

customer withdrawals: 0

total withdrawals: NIL oz

in tonnes: 0.0 tonnes

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEBRUARY.

For the front month of FEBRUARY we have an oi of 496 contracts having gained 37 contracts. We had 23 notices

filed on Friday so we gained 60 contracts or an additional 6000 oz will stand searching for metal at the comex

March gained 60 contracts to stand at 2040.

April lost 3384 contracts down to 332,225

We had 207 notice(s) filed today for 20700 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 207 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer notice(s) was (were) stopped 10/ Received) by J.P.Morgan//customer account 3 and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the FEB. /2023. contract month,

we take the total number of notices filed so far for the month (14,847 x 100 oz ), to which we add the difference between the open interest for the front month of (FEBRUARY 496 CONTRACTS) minus the number of notices served upon today 207 x 100 oz per contract equals 1,513,600 OZ OR 47.079 TONNES the number of TONNES standing in this active month of February.

thus the INITIAL standings for gold for the FEB contract month:

No of notices filed so far (14,847 x 100 oz+ 496 OI for the front month minus the number of notices served upon today (207)x 100 oz} which equals 1,513,600 oz standing OR 47.079 TONNES in this active delivery month of FEBRUARY..

TOTAL COMEX GOLD STANDING: 47.079TONNES. SO JUST LIKE LAST MONTH WE START WITH A LOW INITIAL AMOUNT OF GOLD STANDING BUT THIS WILL GROW AS THE MONTH PROCEEDS TO ITS CONCLUSION.

To calculate the number of silver ounces that will stand for delivery in FEBRUARY. we take the total number of notices filed for the month so far at 860 x 5,000 oz = 4,300,000 oz

to which we add the difference between the open interest for the front month of FEB(28) and the number of notices served upon today 8 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB./2023 contract month:860 (notices served so far) x 5000 oz + OI for the front month of FEB 28 – number of notices served upon today (8) x 500 oz of silver standing for the FEB. contract month equates 4.40 million oz + PREVIOUS 1.775 MILLION OZ ( EXCHANGE FOR RISK)+ 4.450 NEW EXCHANGE FOR RISK = 10.625 MILLION OZ//(TOTAL OZ OF SILVER STANDING).

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

FEB 22/WITH GOLD DOWN 22 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 919.92 TONNES

FEB 21/WITH GOLD DOWN $7.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 919.92 TONNES

FEB 17/WITH GOLD DOWN $1.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 921.08 TONNES

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

FEB 8/WITH GOLD UP $6.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 920.82 TONNES

FEB 7/WITH GOLD UP $5.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 917.92 TONNES

FEB 6/WITH GOLD UP $3.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.24 TONNES

FEB 3/WITH GOLD DOWN $52.55 TODAY: STRANGE: BIG CHANGES AGAIN IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 920.24 TONNES

FEB 2/WITH GOLD $10.95 TODAY: BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 918.50 TONNES

FEB 1/WITH GOLD DOWN $2.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 31/WITH GOLD UP $6.55 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 30/WITH GOLD DOWN $6.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 918.50 TONNES

JAN 27/WITH GOLD DOWN $0.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 919.37 TONNES

JAN 26/WITH GOLD DOWN $11.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 919.37 TONNES

JAN 25/WITH GOLD UP $7.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 917.34 TONNES

JAN 24/WITH GOLD UP $7.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 23/WITH GOLD UP $0.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.63 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 20/WITH GOLD UP $4.75 TODAY;BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 912.43 TONNES

JAN 19/WITH GOLD UP $16.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES INTO THE GLD///INVENTORY RESTS AT 910.98TONNES

JAN 18/WITH GOLD DOWN $1.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.9 TONNES FROM THE GLD////INVENTORY RESTS AT 909.24 TONNES

JAN 17/WITH GOLD DOWN $11.45 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.14 TONNES

JAN 13/WITH GOLD UP $22.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD///INVENTORY RESTS AT 912.14 TONNES

JAN 12/WITH GOLD UP $20.55 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 912.43 TONNES

JAN 11/WITH GOLD UP $1.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.17 TONNES

JAN 10/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 915.33 TONNES

JAN 9/WITH GOLD UP $ 8.60 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD//.//INVENTORY RESTS AT 915.33 TONNES

JAN 6/WITH GOLD UP $28.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 916.77 TONNES

JAN 5/WITH GOLD DOWN $17.05 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 916.77 TONNES

JANUARY 4/WITH GOLD UP $32.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.64 TONNES

JAN 3/WITH GOLD UP $20.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:STRANGE: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 917.64 TONNES

GLD INVENTORY: 919.92 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

FEB 22/WITH SILVER DOWN 22 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ FROM THE SLV////INVENTORY RESTS AT 485.693 MILLION OZ

FEB 21/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.5363 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 486.382 MILLION OZ//

FEB 17/WITH SILVER UP 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 827,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.819 MILLION OZ/

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 485.693 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

Thomas Jefferson’s Blueprint For Handling The National Debt

The way Thomas Jefferson handled the national debt should serve as a blueprint for today. But instead, modern presidents look more like college students on a spending spree with their first credit cards.

We all know how the debt ceiling fight will end. Congress will raise the borrowing limit and the government will keep right on spending money.

That reveals the nature of the problem. It’s not the debt ceiling. It’s the spending.

When Donald Trump took office in January 2017, he inherited a $19.95 trillion federal debt. He handed over a $27.75 trillion debt to Joe Biden. In just four years, the Trump administration added $7.8 trillion to the national debt.

But there was a time when some presidents took paying off Uncle Sam’s debts seriously. For instance, Thomas Jefferson faced a huge national debt when he took office in 1800. But unlike his modern counterparts, he didn’t grow it further. In fact, he significantly whittled down the debt.

“I am for a government rigorously frugal and simple, applying all the possible savings of the public revenue to the discharge of the national debt and not for a multiplication of officers & salaries merely to make partizans, & for increasing, by every device, the public debt, on the principle of it’s being a public blessing.”

Despite facing a number of contingencies, Jefferson limited federal spending, keeping total outlays flat at between $8 and $10 million throughout his presidency.

The Democrat-Republicans held costs down by cutting the federal bureaucracy. And they even managed to do this with a federal workforce totaling just 130 employees.

There wasn’t a whole lot of fat to slice, so Jefferson went to part of the budget where the money was being spent – the military. He argued that funding a standing army in peacetime was a colossal waste of money. In his first message to Congress, Jefferson wrote:

“Sound principles will not justify our taxing the industry of our fellow citizens to accumulate treasure for wars to happen we know not when, and which might not perhaps happen but from the temptations offered by that treasure.”

Congress responded to Jefferson’s message, reducing the army to 3,000 soldiers and 172 officers. It also cut the navy to six frigates and reduced the number of foreign embassies to only three — in Britain, France, and Spain.

All of these spending cuts freed up about $7 million in revenue annually. Secretary of Treasury Albert Gallatin used the surplus to pay down the debt.

At the same time, Congress even reduced taxes, eliminating the hated whiskey tax, along with other internal taxes.

During Jefferson’s tenure, the federal debt fell from $83 million in 1801 to $57 million in 1809. As Chris Edwards at the Cato Institute noted, the drop in debt was impressive, especially considering that the government swallowed that $13 million of added debt from the Louisiana Purchase.

Jefferson was also the beneficiary of a growing economy. After falling in the first two years of his first term, primarily due to the tax cuts, federal revenues soared to nearly $17 million by the end of his presidency. This was largely a function of a huge increase in import duties. Instead of using growing revenue to increase the size and scope of the federal government, Jefferson and Gallatin applied the surplus to pay down the debt.

“A rigid economy of the public contributions and absolute interdiction of all useless expenses will go far towards keeping the government honest and unoppressive.”

end

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

Powell’s Gettysburg Moment, the USD’s Waterloo and Today’s Open Madness

Matthew Piepenburg February 22, 2023

Below we examine the historical interplay of losing wars, cornered egos, tanking currencies, greater controls and gold’s loyalty in times of open madness.

History Matters

Despite the fact that universities even in the Land of Lincoln have had a say in cancelling Abraham Lincoln (good grief…) for apparently not being “woke” enough circa 1861 to be as wise as the neo-liberal faculties of 2023, I’d still make a case that history matters, and by this, I mean all its wonderful and ugly nuances (and lessons), whether they offend modern sensibilities or not.

History, of course, is full of desperate figures and times, many of which involve desperate economies followed by equally desperate (proxy) wars and desperate turning points.

In this light, the more things change, the more they stay the same. Just look around you…

And in the largely forgotten history of war, there is no shortage of desperate generals at desperate turning points.

Wars Doomed from the Start

Napoleon, who having previously won countless battles from Rivoli to Austerlitz, found himself shivering through an 1812 Russia after losing the vast bulk of his army to General Russian Winter and remarking to one of his generals that it’s “only a fine line between the sublime and the ridiculous.”

Three years later, at Waterloo, Napoleon’s “sublime” days (and countless casualty numbers) ended for good.

At Gettysburg, on the 3rd day of July, 1863, an equally talented and grossly outnumbered Confederate States Army under Robert E. Lee, having humbled Union forces at Manassas 1 & 2, Fredericksburg, Gaines Mill and Chancellorsville, looked across an open field from Seminary Ridge to the Emmitsburg Road strewn with the dying and dead of his once bravest divisions as the U.S. Civil War reached a mathematical turning point.

Despite this carnage, the war (post Pickett’s doomed July 3rd charge) dragged on for 2 more horrendous years (and countless casualty numbers), ignoring the hard math of waning troop numbers, supplies, cannons and horses which now rendered Southern “victory” impossible.

Less than a century later, this time near Stalingrad in the winter of 1943, the seemingly invincible German Wehrmacht, having conquered Poland, France, North Africa and large swaths of the East, found itself (and General von Paulus) facing the equally mathematical reality of what once seemed like impossible defeat.

By all metrics the Germans, having engaged in a two-front war, were done, but the war (and countless casualty numbers) would continue for two more senseless years.

But what do any of these examples of doomed and costly wars have to do with current global markets and our financial “generals”?

In fact, quite a bit.

Financial Policies Doomed from the Start

The overlapping interplay of human ego, hard math, and failed strategies doomed from the start have their place in both military and financial history.

For example, once upon a time (circa 2008), our central bankers in general, and the U.S. Fed in particular, had the insanely bad idea that central banks could use fiat money created out of thin air to save bad banks, defeat recessions, manage inflation, monetize debt, win a Nobel Prize and ensure total employment with a “Pickett’s charge” of mouse-click money.

Such grand plans, like the promises of failed generals and insane wars of Lebensraum, la gloire de l’empire or the “Southern Cause,” were initially followed by a string of early “Austerlitz-like successes” (i.e., market bubbles) which brought near-term euphoria.

Unfortunately, those early and mouse-clicked victories ignored the longer-term realities/casualties, namely: historically unprecedented wealth inequality, grotesque currency debasement, the death of free-market price discovery and the birth of what amounts to little more than Wall Street socialism and market feudalism masquerading today as MMT “capitalism.”

Such short-term “glory” at the expense of longer-term ruin is a pattern all too familiar for those paying attention…

Emperor Powell, for example, thinks he can “win the war against inflation,” but like Napoleon, Lee and von Paulus, he is still unable to admit to himself (or us lieutenants) that his grand vision is doomed either way.

And so, he continues to desperately fight a losing cause at the expense of countless currencies and investors (casualties) around the world.

How can we know this?

It All Boils Down to Hard Math and Bad Options

As detailed in prior reports, the math speaks for itself.

Global debt levels are past their “Gettysburg moment”—there are no easy victories left once we start dealing in the quadrillions…

Whether Powell continues with QT or pivots to more QE, retail foot-soldiers here and abroad face either economic recession/depression or extreme inflation.

Pick your “victory” or your poison. I see both, namely: Stagflation

Regardless of whether the USD (DXY) rises or falls in the near-term, the end result is as inevitable and mathematical as Germany’s two-front war, Pickett’s charge or Napoleon’s Waterloo: Disaster.

Once stock and bond bubbles reach their tipping points, the last bubble to die is always the currency, which is precisely where our prize-winning (?) central bankers have placed us.

In short, and as shown below, the global economy and USD, led by Field Marshall Powell, is about to cross that infamously fine line from the sublime to the ridiculous…

The USD’s Sublime Last Moments

As in any losing war, however, there are always those clinging for hope, including those who think the USD will never, well…surrender. (In 2022, the British pound, the yen and the euro already caved…)

Recently, for example, the headlines, politicos, markets and perma-bulls were positively giddy over the stronger than expected US jobs report and non-farm payroll data. The DXY climbed in lock-step.

However, what was equally higher (60% higher…) than expected was the 2023 US Treasury borrowing estimate –aka: Uncle Sam’s increasing bar tab–$930B! –for Q1 alone.

Each of these data points has sent the USD temporarily higher, along with inflation expectations, which now seem to be embedded.

So, the big question today is this: Will the USD get stronger or weaker in 2023 and beyond?

There are two camps in this strategic debate, and two consequences depending on which camp is right. Neither are “victorious.”

Bad Scenario 1: A Rising Dollar’s Consequences

If the USD gets stronger, it kills just about every asset class but the USD…

Already, we are seeing this open carnage in credit markets as rising rates and General Powell’s strong-Dollar policies cripple lending and borrowing norms of the past.

Loan officers are confirming a tightening of credit availability (and a widening of bank lending spreads, above) at levels only seen in prior recessions, adding more weight to my ongoing contention that the US is already in a recession, despite every Göbbels-like attempt in DC to redefine, cancel, ignore or downplay the same.

The equally dismal rise of defaulting High Yield bonds adds further proof of the slow (then steady) death of bleeding bonds in a rising rate and strong USD backdrop/policy.

A strengthening USD will send bonds down and hence yields and rates higher, which will be deflationary as debt-soaked America gets poorer and foreigners are forced to sell more USTs alongside a tightening Fed which is doing exactly the same thing—namely: Bond dumping and yield-spiking.

Bad Scenario 2: A Falling Dollar’s Consequences

However, if the USD gets weaker, the inflation we are already feeling will only get worse as $2T+ deficits make their steady climb North toward $3T, $4T or even $5T+ for 2023.

So, once again: Will the USD get stronger or weaker?

The answer lies in what signals (or desperate generals) you track or trust: Powell’s Fed or the UST market?

Trust What Powell SAYS?—Strong Dollar Ahead

If, for example, you follow the Fed and its bogus yet deadly-serious inflation narrative, then you will be lured into Powell’s “we must beat inflation” war cry, which boils down to a zero-sum battle-plan of “high inflation bad, low inflation good. Must beat inflation.”

Equally part of this bogus battle plan (Powell needs inflation and negative rates…) is the courageous meme that “rising rates kills inflation.”

Well… yes, but at what cost?

If Powell wins the headline battle against inflation, he loses the war for global credit markets, economies and political credibility, which loss will be immediately blamed on a virus and Russian bad guy but never on the mad generals who pushed us over the debt cliff.

However, if we get beyond linear headlines and two-dimensional thinking of central bankers like Powell, we quickly realize that the 3-dimensional UST market is perhaps the real (and superior) indicator of future probabilities.

Or, Trust What Bond Markets DO?—Weaker Dollar Ahead

Thus, rather than watch the Fed, I’m looking at bond markets to get my directional compass-North in a world of policy cannon smoke.

As said more times than I can count: The bond market is the thing.

And as for the sovereign bond market, it has seen 3 periods of complete dysfunction in recent years, namely: 1) the repo rate spike of September 2019; 2) the March 2020 “Covid” crash, and 3) last October’s gilt implosion spawned by the rising USD.

Those who follow the Fed (and this is entirely understandable given that the Fed IS the market in our post-2008 centralized nightmare) can’t be blamed for therefore expecting the USD to rise on more tightening and Powell “inflation-fighting.”

But those who follow the Fed are also ignoring those 3 bond market cracks in the ice above.

It’s my view that this ice is about to break if we have a 4th “uh-oh” moment/crack in sovereign bonds.

Thus, rather than follow the Fed, we might be wiser to look at the UST market, which is heading precisely in that “uh-oh” direction unless someone (i.e., Yellen?) pushes another meme—namely more toxic liquidity and thus a weaker USD.

Failed Battle Plan 1: Tightening into a Debt Crisis (Stronger Dollar)

Let’s play out the Fed’s current scenario first.

If we look only at what the Fed says, and it tightens, which, for now seems like the plan for Q1 and Q2, the USD will strengthen, yields and rates (5% to 5.25%) will rise further and the UST market will see such a wave a selling (foreign and QT Fed-driven), that a fourth “uh-oh” moment in the sovereign bond market will be inevitable, and likely enough to not only “crack the ice” of global bond markets, but drown everyone skating above it.

Given these realities and risks in the UST market, risks which even a fork-tongued and totally cornered Jerome Powell understands, I see no realistic way forward other than a weaker USD and thus a move from QT to QE.

Why?

Again: Because I’m taking my signals from the bond market not Powell.

To track (and trust) Powell means a tanking US Treasury and fatally rising rates, which is like kryptonite to America’s debt-based “accommodation” model.

Instead, I believe Powell will be forced to strategically consider the fact that this inflation war has killed his army of USTs and hence force him (at Yellen’s direction) to change tactics.

Or stated more simply, just as Napoleon, Robert E. Lee, and even the Wehrmacht learned that no outnumbered army can win an extended war, Powell will discover that no sustained policy of rising rates can end well for the toxic bonds/IOUs which float a bankrupt nation.

In short: Unless Powell weakens the USD and injects more QE liquidity sometime in 2023, his victory over inflation will be at the expense of America’s life-blood—namely the UST market.

Failed Battle Plan 2: Resort to More Mouse-Click “Miracles” (Weaker Dollar)

At the end of the day, and despite all this “beat inflation” rhetoric from Powell, it is my admittedly contrarian and unpopular (don’t say “gold-bug”) view that saving Uncle Sam’s IOU lifeline (i.e., the UST market) will take strategic priority over “beating inflation.”

By the way, this appears to be a view shared by none of other than that Corps Commander of toxic liquidity herself: General Janet Yellen…

In other words, expect an eventual (not immediate) capitulation to more fake money—aka, QE, i.e., “liquidity.”

This means that despite gyrating USD moves and hence DXY flip-flops today, the only direction and choice in the longer term to beat a recession and save Uncle Sam’s IOUs is a weaker not stronger Dollar.

Ultimate End-Game? Blame, Reset and Centralized Control

A weaker USD will buy time (and USTs) until ultimately the developed economies of the world, which in fact have the balance sheets of banana republics, finally realize that there’s still nothing left to save them but a great big “reset”—i.e., a global Chapter 11 or Economic “Versailles Treaty.”

The need for this “re-set” will, of course, be conveniently blamed on Putin and Covid rather than the central bankers (failed generals) who caused this horrific war on real money, sustainable debt and sound fiscal spending years ago.

Switching from military to equestrian metaphors, I argued in 2022 that investors, like polo players, need to think where the ball is headed, not where it lies currently.

Regardless of what Powell says today, the real play is 3 to 4 moves ahead, which all point toward an inevitably weaker USD and thus an inevitably rising gold price.

Powell, of course, is more politician than economist, and central banks like the Fed are anything but independent.

As such, Powell, DC and the creative math and fiction writers at the BLS will continue to do what all politicians (or losing armies) do when things are going against them: Lie.

Thus, the DC creative writers will continue to fudge, distort and “tweak” the CPI data to mis-report true inflation as nearly “beating expectations,” thereby allowing Powell to save face in a losing “war against inflation” while Lieutenant Yellen quietly pushes a weaker USD narrative to save the UST market (i.e., prevent more foreign UST dumping).

This face-saving policy will then allow the US to do what it does best: Borrow, spend and go deeper into inflationary debt spirals.

The Pesky Human Factor

Based on bond market Realpolitik, the probabilities point toward a liquidity pivot and weaker USD, longer term.

But history also reminds us that power-drunk figures don’t like to admit defeat. Their egos get in the way of rational decisions.

Powell, who desperately wishes to be remembered as a Napoleonic Paul Volcker rather than a comical Arthur Burns, is no exception to such human-all-too-human small-mindedness.

Unwilling to accept a Gettysburg moment that originated with Colonel Greenspan, General J. Powell could indeed push too far and too long with rising rates, a stronger USD and tanking bonds until inflation and everything else is destroyed.

We can only wait and see.

The Gold Factor

Whether on battlefields or economic cycles, man’s history of the absurd and his disloyalty to the many for the benefit of a few is nothing new under the sun.

In short, chaos eventually rears its head.

Powell or Yellen, QT or QE, inflation to deflation, left or right, Davos or DC, the chaotic results are always the same: Currencies and markets die, opportunists, lies and controls increase and the little guy (and common sense) gets trampled, drafted or “cancelled.”

Physical gold, of course, loves chaos and offers far greater loyalty to those who put their trust in this natural metal rather than flimsy paper money and the even flimsier promises from on high.

So which form of money will you trust to preserve your wealth?

A fiat currency that is losing its purchasing power by the second?

Or a naturally finite monetary metal with infinite duration born from the earth rather than an anonymous code writer or over-heating printer?

The choice, of course, is yours.

END

3. Chris Powell of GATA provides to us very important physical commentaries//

this is good: Mississippi legislatures votes overwhelmingly to send sales taxes on gold and silver

(MMN/GATA)

Mississippi legislature votes overwhelmingly to end sales taxes on gold and silver

Submitted by admin on Tue, 2023-02-21 19:42Section: Daily Dispatches

By JP Cortez Money Metals News Service, Eagle, Idaho Tuesday, February 21, 2023

JACKSON, Mississippi — Both houses of the Mississippi Legislature have just voted overwhelmingly to exempt physical gold, silver, platinum, and palladium coins and bullion from the state sales tax, sending the bill to Governor Tate Reeves for his signature.

Senate Bill 2019, sponsored by Sen. Chad McMahan, R-6, passed yesterday out of the full Senate by a vote of 47-2. This afternoon, Rep. Jody Steverson’s identical House Bill 1661 passed out of the full house chamber on an overwhelming voice vote.

Backed by the Sound Money Defense League, Money Metals Exchange, and in-state Mississippi dealers and investors, the legislative effort built on last year’s momentum. In 2022 a similar sales tax exemption bill had passed out of the Mississippi House of Representatives overwhelmingly but it missed the deadline in the Senate needed to receive a hearing.

If Gov. Reeves signs the bill next week (or if he simply chooses not to veto it), Mississippi will become the 43rd state to exempt sales of sound money from state sales tax. The effective date is July 1, 2023. …

Turkey bought $3.6 billion worth of gold in January (58.3 tonnes). how did Turkey have that much foreign reserves in its account to purchase gold

(Reuters)

Switzerland shipped $3.6 billion of gold to Turkey in January, most since at least 2012

Submitted by admin on Tue, 2023-02-21 20:45Section: Daily Dispatches

By Peter Hobson Reuters Tuesday, January 22, 2023

LONDON — Switzerland sent 58.3 tonnes of gold worth 3.3 billion Swiss francs ($3.6 billion) to Turkey in January, by far the most for any month in records stretching back to 2012, Swiss customs data showed today.

Gold is traditionally seen as a safe means of storing wealth and Turkish demand for the metal has rocketed as sky-high inflation erodes the value of the local lira currency.

Switzerland is the world’s biggest bullion refining and transit hub. It shipped 188 tonnes of gold worth 10.1 billion Swiss francs last year to Turkey, up from only 11 tonnes in 2021.

But January’s shipments are an acceleration. Switzerland’s gold exports to Turkey have never previously exceeded 34 tonnes in a single month, Swiss data shows. …

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 6.8947

OFFSHORE YUAN: 6.9014

SHANGHAI CLOSED DOWN 15.38 PTS OR 0.47%

HANG SENG CLOSED DOWN 105.65 PTS OR 0.85%

2. Nikkei closed DOWN 368.78 PTS OR 1.34%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 104.14 Euro FALLS TO 1.0643 DOWN 8 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.5000!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 134.37/JAPANESE YEN RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.527%***/Italian 10 Yr bond yield RISES to 4.467%*** /SPAIN 10 YR BOND YIELD RISES TO 3.594…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.527//

3j Gold at $1837.95//silver at: 21.84 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 25/100 roubles/dollar; ROUBLE AT 74.80//

3m oil into the 75 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 134.60/10 YEAR YIELD AFTER BREAKING .54%, REMAINS AT .5000% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9275–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.98569well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.941% DOWN 1 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.965 DOWN 1 BASIS PTS//

UK 2 YR BOND YIELD: 4.689 DOWN 1 BASIS PT

USA DOLLAR VS TURKISH LIRA: 18,88…

GREAT BRITAIN/10 YEAR YIELD: 3.689% DOWN1 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Rebound As Yields, Dollar Drop, Fed Minutes Loom

WEDNESDAY, FEB 22, 2023 – 08:07 AM

After suffering their biggest one-day drop of 2023, US futures rebounded in muted trading on Wednesday, boosted by a drop in rates (the 10Y just hit a session low of 3.92% after rising as high as 3.97%) and weakness in the dollar, even as investors awaited further clues on the direction of monetary policy from the Federal Reserve’s minutes due out at 2pm today. S&P 500 and Nasdaq futures rose 0.3% and 0.4%, respectively, at 7:45am ET; sentiment was boosted by a CNBC appearance of the Fed’s “trial balloon” speaker, St Louis Fed president James Bullard, who was hawkish – saying he favors hiking rates to 5.375% as fast as possible, but not as hawkish as some had feared, leading to a sharp bounce in futures just after 7am. Yields dropped, as did the dollar, while oil, gold and crypto erased earlier losses.

In premarket trading, CoStar Group led declines in US premarket trading after its annual guidance disappointed analysts and News Corp. said it’s no longer involved in discussions to sell its Move subsidiary to the real estate information and services company. Coinbase Global Inc. declined after the cryptocurrency exchange posted a $557 million loss. Here are some other notable premarket movers:

Palo Alto shares rose nearly 10% after the cybersecurity company’s results beat across the board. Several analysts raised their price targets for the stock, saying the firm is managing macro pressures effectively and executing well on its strategy

Keep an eye on Constellation Energy as it was cut to neutral from outperform at Credit Suisse as the broker says the green energy group’s shares now look expensive and lack near-term catalysts

Watch Nordson after it was raised to overweight from sector weight at KeyBanc, with the broker saying a good entry point for the adhesives and sealants company has materialized following a post-earnings decline in its shares

Morgan Stanley is constructive on US software stocks, given that the moderation in forward IT spending growth is likely to prove less severe than feared. Valuations are still near multi-year trough levels and longer-term demand trends are intact

Keysight shares fell 7.1% in after-hours trading on Tuesday as the company’s results showed order weakness, and guidance will create cause for concern in the near term, analysts said, though they remain positive on the longer-term outlook for the electronic measurement services firm

Meanwhile disappointing earnings projections are seen everywhere. Walmart Inc. reported a weak profit outlook that fell short of analyst estimates, signaling another rocky year for the world’s largest retailer. Home Depot Inc. also released a profit-decline forecast. Only 68% of S&P 500 companies reporting results this season have beaten estimates, compared with about 80% seen during recent quarters.

Following strong business activity data on Tuesday, a classic example of “good news is bad news for markets”, stocks tumbled as evidence mounted that the Fed may have to hike even more (ignoring for a second the fact that the data is manipulated “strong” for purely political reasons and will soon slump) and prompted fears the powerful stock rally since the start of the year may be coming to an end, as hot economic indicators pressure central banks to keep monetary policy tight. And while until recently investors looked as though they may be pricing in a soft landing for the economy, that may be ending said Stephanie Niven, portfolio manager at Ninety One UK Limited, and hoping strong economic conditions may cushion higher rates.

“We will continue to see investors adjust their expectations,” said Niven. “We see a harsher economic cycle into the second half of this year, and we really think a harder landing is the likely outcome here.”

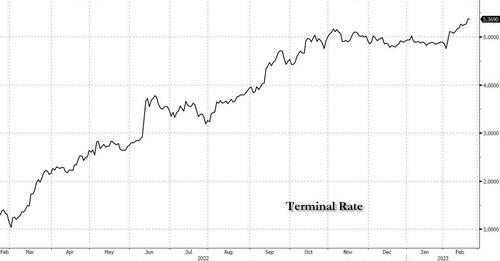

In a relatively quiet calendar, today’s main event will be the Minutes from the Fed’s Jan. 31-Feb. 1 meeting, which while naturally backward looking, may shed light on the path forward. For context, officials at the meeting voted unanimously to raise rates by just 25 basis points, moderating from a half-point hike in December after four 75-bp increases. The policy statement said the “extent of future increases” will depend on a number of factors including cumulative tightening of monetary policy, wording Fed watchers viewed as a signal the central bank may stick with smaller moves. Watch the minutes for insight into whether a larger hike is still on the table, which in turn may mean the Fed’s terminal rate is higher than some expect.

“Investors are waking up to a stark realization that the Fed’s work is not done, and that interest rates may have to be hiked even higher to cool hot inflation,” Susannah Streeter, the head of money and markets at Hargreaves Lansdown Plc, wrote in a note. “Waves of exuberance, which have propelled equities higher since the start of the year, have turned into tides of disappointment and apprehension about the difficulties that still may lie ahead for the mighty US economy.”

A rocky geopolitical outlook has not helped. President Vladimir Putin said Russia will suspend its observation of the New START nuclear weapons treaty with the US, a decision Secretary of State Antony Blinken called “irresponsible.” President Joe Biden hit back at Putin, saying he would never win his war in Ukraine.

In delayed response to yesterday’s US slump, European stocks fall for a second day after disappointing corporate earnings gave investors another reason to be cautious besides the prospect of tighter monetary policy. The Stoxx 600 is down 0.9%, headed for a second-day loss, though it came off the day’s lows. Lloyds Banking Group Plc dropped, weighing on the FTSE 100 Index, after results and guidance for 2023 came in below analyst estimates, despite announcing a £2 billion ($2.4 billion) share buyback. Miner Rio Tinto Plc fell after reporting lower than expected profit and slashing its dividend due to weak demand for metals in China. Here are some of the biggest movers on Wednesday:

Lloyds Banking Group shares fall as much as 3% after the lender reported fourth-quarter results and guidance that were mixed with the bank affected by competition in the mortgage market

Rio Tinto shares slip as much as 3.2% after the mining conglomerate slashes dividends and reports lower-than-expected profits, hurt by weaker demand and higher costs

Grifols shares fell as much as 8.2%, the most intraday in four months, after the Spanish blood plasma company said executive chairman Steven F. Mayer resigned after four months in the job

Covivio shares fall as much as 5.4%, the most since December, with analysts saying the French real estate firm’s guidance is soft and that its dividend is lower than expected

Korian shares fell as much as 20%, set to close at their lowest level since 2006, after the French care home operator reported 2022 full year results that came short of analysts’ expectations

Siegfried shares fall as much as 11%, the most since 2015, after the Swiss pharma company delivered an outlook analysts considered cautious given its strong performance in 2022

Danone shares rise as much as 2.8% in early Paris trading, before paring gains, after reporting full-year recurring operating income that beat estimates

Wolters Kluwer shares rise as much as 3.9%, the biggest intraday climb since October, after the information services company forecast organic sales growth this year will be in-line

UCB gains as much as 4.9% after the Belgian pharmaceuticals firm reported better-than- expected earnings

BE Semiconductor gains as much as 9.9% after reporting fourth-quarter orders that blew past analyst estimates

Stellantis shares rise as much as 3.4% to the highest since March 2022 after the carmaker’s full-year results beat expectations and it announced a buyback of as much as €1.5 billion

Earlier in the session, Asian stocks declined for a second day after the aforementioned jump in US Treasury yields undermined confidence in the equity market’s advance this year, with shares in Hong Kong falling to the brink of a correction. The MSCI Asia Pacific Index fell as much as 1.4% to its lowest level since Jan. 9, with TSMC and Tencent among the heaviest drags on the gauge. Shares in Australia, Japan and mainland China slipped, while losses in Hong Kong’s Hang Seng Index reached almost 10% since a Jan. 27 peak. Technology stocks dropped after Treasury yields touched new highs for the year amid growing concern the Federal Reserve will continue to raise interest rates. Investors are pricing in the federal funds rate climbing to around 5.3% in June. That compares with a perceived peak of 4.9% just three weeks ago.

“We see more signs of a growth slowdown” into year end, Alexander Wolf, Asia head of investment strategy at JPMorgan Private Bank, told Bloomberg Television. Fixed income “still remains our highest conviction call, given what we’ve seen with the move up in yields, you can achieve equity-like returns.” Read: Investors Stung by Treasuries Rout Brace for Next Fed Blow A key MSCI gauge of Indian stocks was also on course to enter a technical correction as the selloff in Adani Group shares deepened. Indexes in Vietnam and South Korea were among the biggest decliners in the region as investors awaited the release of Fed minutes from its latest policy meeting.

Japanese equities fell, following US peers lower on concerns of further Fed hikes and after weak corporate forecasts from US retailers Walmart and Home Depot. The Topix Index fell 1.1% to 1,975.25 as of market close Tokyo time, while the Nikkei declined 1.3% to 27,104.32. Sony Group Corp. contributed the most to the Topix Index decline, decreasing 2%. Out of 2,162 stocks in the index, 431 rose and 1,636 fell, while 95 were unchanged. “Expectations for an early halt to US interest rate hikes and cuts have faded, with the landing point for a rate hike higher than what the market expected,” said Kiyoshi Ishigane chief fund manager at Mitsubishi UFJ Kokusai Asset Management.

India’s benchmark stocks gauge posted its biggest single-day slump this year as a selloff across global equity markets extended amid worries over interest rates staying higher-for-longer. Sentiment in India continued to be weighed down by the ongoing decline in Adani shares. The rout triggered by US short-seller Hindenburg Research’s report has now stretched to $144 billion, with the group’s flagship firm Adani Enterprises plunging 11% today. All 10 group stocks declined during the session. The S&P BSE Sensex fell 1.5% to 59,744.98 in Mumbai, the most since Dec. 23 and is close to erasing its gains for February. The NSE Nifty 50 Index declined by a similar measure. “There is an increasing fear that the Fed may remain hawkish for a longer duration than expected, which may even force RBI to keep interest rates high,” Siddhartha Khemka, head of retail research at Motilal Oswal Financial, said in a note. All 20 sector sub-gauges compiled by BSE Ltd. declined, led by utilities, while 29 out of Sensex’s 30 companies closed lower

In FX, the dollar slid against its Group-of-10 currencies, where Sweden’s krona was the best performer followed by the yen while the Australian dollar and British pound are the weakest among. The euro fell a third day, to touch a low of $1.0630. Bund yields were a tad higher, led by longer maturities A German expectations gauge by the Ifo institute rose to 88.5 in February from 86.4 the previous month. That was better than the 88.3 median estimate in a Bloomberg poll of economists

The Swedish krona outperformed other G-10 peers against the dollar and neared 11 per euro in the wake of comments from the new Riksbank Governor Erik Thedeen, who described underlying inflation figures in January as worrying. He also said that Sweden is currently not experiencing a housing market crash

The pound fell, erasing some of its Tuesday gains, as investors mulled the UK economic outlook following data that showed the nation is weathering the sharpest cost-of-living crisis in generations better than feared. The gilt yield curve bear-flattened, with yields rising 3-6bps

The yen advanced as much as 0.3% to 135.06 per dollar as the nation’s benchmark bond yield climbed back above the BOJ ceiling for a second day amid a global bond selloff. BOJ Governor nominee Kazuo Ueda is due to face confirmation hearings in the parliament this week. BOJ Board Member Naoki Tamura says that any decision on conducting a policy assessment will be made by looking at wage growth, prices and the economy. A divergence in the spot and options markets for the dollar-yen pair suggests traders are looking once again to position for possible hawkish signals from BOJ officials

The New Zealand dollar was little changed after earlier rising as much as 0.4% to 0.6246 even as the RBNZ hiked rates by 50 basis points as expected and forecasting that it would take longer than previously expected to reach its 5.5% peak rate

The Australian dollar was the worst G-10 performer following a smaller-than-expected wages increase in the fourth quarter. Wage price index rose 0.8% q/q (estimate +1.0%) in 4Q

In rates, Treasuries held on to modest gains as US trading day begins, after erasing declines that pushed yields to new YTD highs, with the exception of the new 2-year note. Shorter-term Treasuries rose more than longer-dated ones in a choppy session. The two-year rate slid 5 basis points from the highest level since early November. Its 10-year counterpart was 3 basis points lower. The 10-year reached 3.966% before dropping as low as 3.92%. Gilts have led European bonds lower as markets continue to price in higher terminal rates for the Bank of England and European Central Bank. UK two-year yields are up 8bps while the German equivalent adds 2bps.

In the US, the Treasury auction cycle continues with 5-year note sale at 1pm New York time, and FOMC releases minutes of Jan. 31-Feb. 1 meeting at 2pm. WI 5-year yield 4.13%; current issue traded as high as 4.185%, still more than 30bp below last year’s multiyear high, as traders are assigning higher odds to more Fed rate increases to follow the 25bp move on Feb. 1. Since then, St. Louis Fed President Bullard — appearing on CNBC — has said he advocated for a 50bp hike and might support one in March, heightening interest in whether the minutes will reveal broader appetite for reacceleration.

Oil extended its longest run of losses this year, with West Texas Intermediate contracts falling for a sixth day. The prospect of more aggressive interest-rate hikes from the Fed to quell inflation have kept a lid on prices, despite increasing evidence of a robust recovery in China following the end of Covid Zero. Crude futures decline with WTI down 0.6% to trade around $75.89, off session lows. Spot gold rose to $1,840.

Looking to the day ahead. In terms of data releases, we have the German February ifo survey which came in stronger than expected, and the France February business and manufacturing confidence indicators; in the US. the latest MBA mortgage applications dropped -13.3%, following last week’s -7.7% slide. For central banks, first and foremost we have the release of the Fed’s FOMC minutes, and we will also hear from the Fed’s Williams. Finally, we will have earnings releases from NVIDIA, TJX, Pioneer and eBay.

Market Snapshot

S&P 500 futures little changed at 4,004.75

STOXX Europe 600 down 0.9% to 459.50

MXAP down 1.3% to 160.19

MXAPJ down 1.3% to 521.69

Nikkei down 1.3% to 27,104.32

Topix down 1.1% to 1,975.25

Hang Seng Index down 0.5% to 20,423.84

Shanghai Composite down 0.5% to 3,291.15

Sensex down 1.5% to 59,790.65

Australia S&P/ASX 200 down 0.3% to 7,314.50

Kospi down 1.7% to 2,417.68

German 10Y yield little changed at 2.56%

Euro little changed at $1.0643

Brent Futures down 1.1% to $82.13/bbl

Gold spot down 0.1% to $1,834.10

U.S. Dollar Index little changed at 104.26

Top Overnight News

Japan’s 10-year government bond yield on Wednesday breached the top end of the Bank of Japan’s policy band for a second straight session, prompting the central bank to step into the market with emergency bond buying and offering of loans. RTRS

Two of Japan’s biggest automakers (Toyota & Honda) agreed to the biggest wage hikes in decades in an early sign of momentum in annual pay negotiations as the central bank looks for evidence of a wage-price cycle that could lead to policy change. BBG

Chinese authorities have urged state-owned firms to phase out using the four biggest international accounting firms, signaling continued concerns about data security even after Beijing reached a landmark deal to allow US audit inspections on hundreds of Chinese firms listed in New York. BBG

Missing Chinese investment banker Bao Fan was preparing to move some of his fortune from China and Hong Kong to Singapore in the months leading up to his disappearance, according to four people with knowledge of his plans. FT

Investors increase bets on ECB lifting rates to all-time high. Buoyant service sector and wages fuel expectations of further rises in eurozone borrowing costs. FT

The Fed minutes may show how many officials pushed for a larger hike and whether they saw the need to take rates higher than anticipated. Markets expect tightening to be extended after stronger economic data and some hawkish messaging, with rates peaking at 5.36% this year. The RBNZ slowed its pace with a 50-bp increase to 4.75% after mulling another move of 75 bps. The projection for peak rates was left unchanged at 5.5%, over a slightly longer timeframe. BBG

Authorities accused crypto trader Avi Eisenberg of manipulating token prices on an exchange. Mr. Eisenberg countered, saying he did only what was permitted by the exchange’s software code. At the core of this case is the idea held by some crypto enthusiasts that “code is king.” WSJ

In the hunt for Lael Brainard’s successor, the White House is “focusing in” on Harvard University professor Karen Dynan, Northwestern University finance professor Janice Eberly and Morgan Stanley Chief Global Economist Seth Carpenter. BBG

JPMorgan cut staff access to ChatGPT, a person familiar said, confirming an earlier Telegraph report. The move wasn’t triggered by any specific incident. BBG

Consistent with the increase in leverage, demonstrated hedge fund equity market exposures have begun to rise from the extremely low levels registered late last year. Hedge funds exhibited exceptionally low betas to the equity market in 2022, reaching levels only matched during the last 20 years in 2009. Betas have rebounded in the last few weeks, driven in part by increased net length, but remain well below historical averages. GIR

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks were subdued after the declines on Wall St where the major indices were pressured on return from holiday as strong PMI data from Europe and the US spurred hawkish central bank repricing. ASX 200 briefly dipped below 7,300 amid a slew of earnings releases although clawed back most of its losses after weak data releases including a surprise contraction in Construction Work and softer-than-expected Wage Price Index, which removes some of the hawkish impulses for the RBA. Nikkei 225 underperformed and approached closer to testing the 27,000 level to the downside. Hang Seng and Shanghai Comp. conformed to the subdued mood in which weakness in tech briefly pulled the Hong Kong benchmark into correction territory although losses were then pared after the budget announcement which included a giveaway of HKD 5,000 in consumption vouchers and a cut to salary taxes, while there was also strength in HSBC and Hang Seng Bank post-earnings.

Top Asian News

Hong Kong Finance Secretary Chan delivered the Budget and confirmed the government will provide HKD 5k in consumption vouchers to residents aged 18 years old and above, while they will reduce salaries tax with a ceiling of HKD 6,000 which will benefit 1.9mln taxpayers and lower government revenue by HKD 8.5bln. Chan also noted that the city is at the beginning of a recovery and that GDP contracted by 3.5% in 2022, although the government expects Hong Kong GDP growth of 3.5%-5.5% in 2023.

China’s top diplomat Wang Yi met with Russia’s security chief and said the two sides discussed their willingness to oppose all forms of unilateral bullying and discussed ways to improve global governance. Furthermore, the two sides believe peace and stability in the Asia-Pac region should be resolutely upheld and they oppose the introduction of a cold war mentality, according to Reuters.

RBNZ hiked the OCR by 50bps to 4.75%, as expected, while it maintained its view for rates to peak at 5.50% and considered hikes of 50bps and 75bps at the meeting. RBNZ stated that although there are early signs of price pressure easing, core consumer inflation remains too high and the Committee agreed it must continue to raise the OCR to return inflation to the target and to fulfil its remit.

European bourses are softer across the board, Euro Stoxx 50 -0.8%, as hawkish price action remains in full swing. Sectors are lower across the board ex-Media following individual earning updates, while Basic Resources lag as underlying commodities are dented. Stateside, futures are flat/negative with the ES holding around the 4k mark having briefly and incrementally dipped below the figure in European trade.

Top European News

ECB’s Villeroy reiterates that there is excessive volatility of the market view on the terminal rate. Already in restrictive territory with a 2.5% rate, ECB is not obliged to hike at every meeting to September, via Les Echos. Remarks which echo his commentary from last Friday.

UK PM Sunak reportedly secured the backing of two key Brexiteers for the Northern Ireland trade deal with Heaton-Harris and Braverman getting behind the outline agreement, according to FT.

DUP’s Donaldson reportedly told an ERG meeting on Tuesday that UK PM Sunak was just halfway to meeting the DUP’s seven tests re. N. Ireland Protocol, having made progress towards three or four of them, via Politico citing sources; added that progress towards the remaining DUP tests is critical, telling PM Sunak to abandon the “arbitrary deadline” of April 10th.

FX

The DXY remains underpinned on haven dynamics and as yields continue to climb across the board, index continues to climb above a 104.00 base with the current high at 104.33

As such, peers are generally softer across the board with the AUD lagging post-data and as the NZD clings onto gains following the hawkish RBNZ announcement; AUD around 0.6810 and NZD near 0.6210 vs USD.

EUR was generally unreactive to the morning’s Ifo data while dovish commentary from Villeroy prompted some pressure, but this was brief and limited given his remarks are a repeat of Friday’s, EUR/USD at the lower-end of 1.0630-1.0663 parameters.

JPY and CHF are rangy and narrowly mixed against the USD, after the JPY regrouped on some convergence in JGB-UST yields irrespective of BoJ buying while CHF shrugged off an upbeat domestic investor survey.

GBP is giving back some of Tuesday’s marked upside, with caution around N. Ireland Protocol progress perhaps weighing though the focus is firmly on BoE-related dynamics; Cable around 20 pips shy of 1.21 though off worst.

EUR/SEK continues to test 11.00 with Riksbank’s Thedeen assisting while the ZAR is a touch softer heading into the budget announcement from 12:00BST/07:00ET onwards.

PBoC set USD/CNY mid-point at 6.8759 vs exp. 6.8776 (prev. 6.8557)

Yonhap reports that as USD/KRW soared “the foreign exchange authorities called an emergency market situation inspection meeting this afternoon.”.

Riksbank’s Thedeen says inflation is far too high; January’s inflation data was a negative surprise, it is worrying.

Fixed Income

EGBs have experienced a modest bounce in the wake of well-received EZ & UK supply, with Bunds now back to 104.00 from the new 133.63 YTD low and Gilts firmly above 101.00 in a similar fashion.

Prior to this, the complex had been under marked pressure in a continuation of recent hawkish price action with the German 10yr yield as high as 2.57%; though, pre-supply this eased following a rerun of recent dovish remarks from Villeroy.

Stateside, USTs have been moving in-tandem with EGBs with specific catalysts thin ahead of FOMC minutes and a 5yr sale, as such USTs are flat within 110.30+ to 111.08 parameters.

Commodities

Crude benchmarks remain underpressure with specific developments limited and focus on the broader risk tone; WTI & Brent Apr at the lower end of USD 74.96-76.55/bbl and USD 81.70-83.25/bbl intraday parameters respectively.

Nat Gas futures are mixed, though remain pressured vs recent levels as desks continue to cite relatively mild weather in the US and Europe.

Kazakhstan may send the first batch of oil to Germany in the coming days which could possibly occur today, according to RIA citing the Energy Minister.

Morgan Stanley sees Brent trading in a USD 90-100bbl range in H2 vs. its prev. view of USD 100-110bbl; raises estimate for oil demand growth to 1.9mln BPD from 1.4mln BPD.

Nigeria raises March Bonny Crude OSP to +0.95/bbl vs dated Brent; Qua Iboe raise to +1.27/bbl vs dated Brent.

Spot gold is little changed as any haven allure is offset by the USD’s strength, while base metals are lower given the tone and with focus on commentary from Rio Tinto overnight.

Ukraine could export a total of 8mln tonnes of agricultural good a month for Odesa and Mykolaiv ports; will talk to UN to extend the grain deal for another year, according to Ukrainian Deputy Minister.

Geopolitics

Russia reportedly conducted an ICBM test when US President Biden was recently in Ukraine although the test was said to have failed, while an official stated that Russia notified the US in advance of the launch through deconfliction lines, according to CNN.

Russian PM Medvedev says Russia is ready to defend itself with any weapon, including nuclear.

Russian Foreign Minister Lavrov says relations between Moscow and Beijing are developing despite the tense international situation; China’s Top Diplomat says we continue to maintain close communication with Russia, via Sky News Arabia. Subsequently, Russian Kremlin says President Putin is to meet with China’s Top Diplomat Wang Yi on Wednesday (as touted).

US President Biden’s administration is expected to impose fresh sanctions on about 200 Russian individuals and entities this week, according to WSJ citing sources.

North Korea could fire ICBMs at a normal angle and conduct its seventh nuclear test this year, according to South Korean lawmakers citing intelligence officials.

US Event Calendar

07:00: Feb. MBA Mortgage Applications, prior -7.7%

14:00: Feb. FOMC Meeting Minutes

17:30: Fed’s Williams Discusses Inflation

DB’s Jim Reid concludes the overnight wrap

I’m still in a bit of a state of shock this morning after the Liverpool / Real Madrid game last night. From wild jubilation to the end of the world within an hour. A Bit like financial markets in the last three weeks.