Mar 1, 2023 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSED: UP $18.90 at $1838.40

SILVER PRICE CLOSED: UP $0.04 to $20.99

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1837.50

Silver ACCESS CLOSE: 20.99

Bitcoin morning price:, 23,828 UP 603 Dollars

Bitcoin: afternoon price: $23,426 UP 207 dollars

Platinum price closing $961.4 UP $4.45

Palladium price; closing $1446.10 UP $26.40

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,498.53 UP $7.55 CDN dollars per oz

BRITISH GOLD: 1529.02 UP 11.53 pounds per oz

EURO GOLD: 1722.91 DOWN 3.05 euros per oz

COMEX DATA

EXCHANGE: COMEX

CONTRACT: MARCH 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,828.900000000 USD

INTENT DATE: 02/28/2023 DELIVERY DATE: 03/02/2023

FIRM ORG FIRM NAME ISSUED STOPPED323 C HSBC 5

363 H WELLS FARGO SEC 22

624 C BOFA SECURITIES 5

657 C MORGAN STANLEY 1

661 C JP MORGAN 32

726 C CUNNINGHAM COM 2

737 C ADVANTAGE 57 2

800 C MAREX SPEC 22 3

880 C CITIGROUP 6

905 C ADM 1TOTAL: 79 79

MONTH TO DATE: 1,462

JPMORGAN STOPPED 32/79

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR MAR/2023. CONTRACT: 79 NOTICES FOR 7900 OZ or 0.2457 TONNES

total notices so far: 1462 contracts for 146,200 oz (4.547 tonnes)

SILVER NOTICES: 943 NOTICE(S) FILED FOR 4,715,000 OZ/

total number of notices filed so far this month : 2176 for 10,880,000 oz

END

GLD

WITH GOLD UP $18.90

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD//// A WITHDRAWAL OF 2.31 TONNES OF GOLD OUT OF THE GLD/

INVENTORY RESTS AT 915.30TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 4 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2,574 MILLION OZ OUT OF THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 478.614. MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GOOD SIZED 667 CONTRACTS TO 123,900 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE GOOD SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.26 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. WE HAVE NOW SURPASSED OUR PREVIOUS ALL TIME LOW OF 124,080 OI CONTRACTS RECORDED FEB 22/2023. THUS NEW LOW COMEX OI SILVER WAS SET 123,900 MARCH 1/2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.26). BUT WERE SUCCESSFUL IN KNOCKING SOME SPEC LONGS, AS WE HAD A SMALL LOSS ON OUR TWO EXCHANGES 209 CONTRACTS. WE HAD 0 NOTICES FOR EXCHANGE FOR RISK TRANSFER ( AS THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 0 MILLION OZ. WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS( 458 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.58 MILLION OZ FOLLOWED BY TODAY’S EFP OF 660,000//NEW STANDING: 14.920 MILLION OZ/ //// V) GOOD SIZED COMEX OI LOSS/ GOOD SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL 29 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTRACTS for 1 days, total 458 contracts: OR 2.290 MILLION OZ . (458 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 2.290 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 2.290 MILLION OZ//INITIAL

RESULT: WE HAD A GOOD SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 667 DESPITE OUR $0.26 GAIN IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE CONTRACTS: 458 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAR OF 15.58 MILLION OZ FOLLOWED BY TODAY’S 660,000 E.F.P. JUMP TO LONDON .. WE HAVE A SMALL SIZED LOSS OF 209 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 943 NOTICE(S) FILED TODAY FOR 4,715,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 3673 CONTRACTS TO 426,890 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 888 CONTRACTS.

.

WE HAD A GOOD SIZED INCREASE IN COMEX OI ( 3673 CONTRACTS) WITH OUR $12.10 GAIN IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR FEB. AT 4.9953 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 33,700 OZ (1.048 TONNES) //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S ) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London). TONNES

YET ALL OF..THIS HAPPENED WITH OUR $12.10 GAIN IN PRICE WITH RESPECT TO TUESDAY’S TRADING

WE HAD A VERY STRONG SIZED GAIN OF 8884 OI CONTRACTS (27.63 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5211 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 426,890

IN ESSENCE WE HAVE A VERY STRONG INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8884 CONTRACTS WITH 3673 CONTRACTS INCREASED AT THE COMEX AND 5211 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 8884 CONTRACTS OR 27.63 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5211 CONTRACTS) ACCOMPANYING THE GOOD SIZED GAIN IN COMEX OI (3673) TOTAL GAIN IN THE TWO EXCHANGES 8884 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR MAR. AT 4.9953 TONNES FOLLOWED BY TODAY’S 33700 OZ QUEUE JUMP//NEW STANDING 6.0435 TONNES // ///3) ZERO LONG LIQUIDATION //4) GOOD SIZED COMEX OPEN INTEREST GAIN// 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

5211 CONTRACTS OR 521,100 OZ OR 16.208 TONNES 1 TRADING DAY(S) AND THUS AVERAGING: 5211 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAY(S) IN TONNES 16.208 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 16.208/3550 x 100% TONNES 0.4507% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 16.208 TONNES/INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH GOLD (

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A GOOD SIZED 667 CONTRACTS OI TO 123,900 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A RECORD LOW OF 123,929 CONTRACTS MARCH 1/2023.

EFP ISSUANCE 458 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 458 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 458 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 638 CONTRACTS AND ADD TO THE 458 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL LOSS OF 209 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 1.045 MILLION OZ//

OCCURRED DESPITE OUR $0.26 GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED UP 32,74 PTS OR 1.00% //Hang Seng CLOSED UP 833.77 PTS OR 4.21% /The Nikkei closed UP 70.93% PTS OR .26% //Australia’s all ordinaries CLOSED DOWN 0.03% /Chinese yuan (ONSHORE) closed UP 6.8636 //OFFSHORE CHINESE YUAN UP TO 6.8684// /Oil UP TO 76.53 dollars per barrel for WTI and BRENT AT 82.92 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GOOD SIZED 3673 CONTRACTS UP TO 427,778 WITH OUR GAIN IN PRICE OF $12.10.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAR… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 5211 EFP CONTRACTS WERE ISSUED: : APRIL 5211 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5211 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG SIZED TOTAL OF 8884 CONTRACTS IN THAT 5211 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED COMEX OI GAIN OF 3673 CONTRACTS..AND THIS VERY STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $12.10. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAR (6.0435) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 6.0435 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $12.10) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A VERY STRONG SIZED GAIN OF 8884 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 27.63 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAR. (4.9953 TONNES) FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 33,700 OZ (1.048 TONNES)… ALL OF THIS WAS ACCOMPLISHED WITH OUR RISE IN PRICE TO THE TUNE OF $12.10.

WE HAD -888 CONTRACTS REMOVED FROM COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 8884 CONTRACTS OR 888,400 OZ OR 27.63 TONNES

Estimated gold comex today 185,289// //poor

final gold volumes/yesterday 201,997/// fair

//MARCH 1//

MARCH 2023 CONTRACT

//

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | nil oz . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 79 notice(s) 7900 OZ 04.547 TONNES |

| No of oz to be served (notices) | 441 contracts 44100 oz 1.496 TONNES |

| Total monthly oz gold served (contracts) so far this month | 1462 notices 146200 4.547 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 0

total withdrawals: nil oz

in tonnes: 0.000 tonnes

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of MARCH we have an oi of 560 contracts having LOST 1046 contracts. We had 1383 notices filed yesterday so surprisingly we

gained 337 notices or an additional 33700 oz will stand for metal on day 2 of the delivery cycle. Usually we see an EFP jump on day 2.

April gained 977 contracts up to 325,452 contracts

May gained its initial 14 contracts to stand at 14

We had 79 notice(s) filed today for 7900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 79 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer notice(s) was (were) stopped 32/ Received) by J.P.Morgan//customer account 3 and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAR. /2023. contract month,

we take the total number of notices filed so far for the month (1,462 x 100 oz ), to which we add the difference between the open interest for the front month of (MAR. 560 CONTRACTS) minus the number of notices served upon today 79 x 100 oz per contract equals 160,600 OZ OR 4.9953 TONNES the number of TONNES standing in this active month of MARCH.

thus the INITIAL standings for gold for the MAR contract month:

No of notices filed so far (1,462 x 100 oz+ 560 OI for the front month minus the number of notices served upon today (79)x 100 oz} which equals 194,300 oz standing OR 6.0435 TONNES in this active delivery month of MARCH..

TOTAL COMEX GOLD STANDING: 6.0435 TONNES.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,789,729.416 OZ 55.67 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,651,865.517 OZ

TOTAL REGISTERED GOLD: 10,889,770.731 (338,71 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 10,762,094.786 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,100,041 OZ (REG GOLD- PLEDGED GOLD) 283.04 tonnes//dropping like a stone

END

SILVER/COMEX

MAR/2023// THE MARCH 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 13,776.000 oz Delaware |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 943 CONTRACT(S) (4,715,000 OZ) |

| No of oz to be served (notices) | 808 contracts (4,040,000 oz) |

| Total monthly oz silver served (contracts) | 2176 contracts (10,880,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 2 deposits into the customer account

i)Into CNT 599,614.690 oz

ii) into Delaware 8649.04 oz

Total deposits: 608,218.730 oz

JPMorgan has a total silver weight: 147.648 million oz/287.233 million =51.18% of comex .//dropping fast

Comex withdrawals: 1

i) Out of Delaware: 13,776.000 oz

Total withdrawals; 13,776.000 oz

adjustments: 2

customer to dealer

JPMorgan: 3,586,897.900 oz

dealer to customer:

Delaware 14,614.185 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 38.785MILLION OZ (declining rapidly).TOTAL REG + ELIG. 287.233 million oz

CALCULATION OF SILVER OZ STANDING FOR FEB

silver open interest data:

FRONT MONTH OF MAR/2023 OI: 1751 CONTRACTS HAVING LOST 1365 CONTRACT(S.) WE HAD 1233 NOTICES FILED

YESTERDAY, SO WE LOST 132 CONTRACTS OR AN ADDITIONAL 660,000 OZ WILL NOT STAND AND THESE GUYS DECIDED UP AN E.F.P. JUMP

TO LONDON.

April GAINED 102 CONTRACTS TO STAND at 512.

May GAINED 65 CONTRACTS UP TO 106,904.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 943 for 10,880,000 oz

Comex volumes// est. volume today 59,155// fair//

Comex volume: confirmed yesterday: 65.924 contracts ( good)

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 2176 x 5,000 oz = 10,880,000 oz

to which we add the difference between the open interest for the front month of MAR(1751) and the number of notices served upon today 943 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAR./2023 contract month: 2176 (notices served so far) x 5000 oz + OI for the front month of MAR (1751) – number of notices served upon today (943) x 500 oz of silver standing for the MAR. contract month equates 14.920 million oz +

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

FEB 28/WITH GOLD UP $12.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 917.61 TONNES

FEB 27/WITH GOLD UP $6.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.32 TONNES

FEB 24/WITH GOLD DOWN $9.10 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 917.32 TONNES

FEB 23/WITH GOLD DOWN $13.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 919.92 TONNES

FEB 22/WITH GOLD DOWN 22 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 919.92 TONNES

FEB 21/WITH GOLD DOWN $7.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 919.92 TONNES

FEB 17/WITH GOLD DOWN $1.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 921.08 TONNES

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

FEB 8/WITH GOLD UP $6.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 920.82 TONNES

FEB 7/WITH GOLD UP $5.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 917.92 TONNES

FEB 6/WITH GOLD UP $3.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.24 TONNES

FEB 3/WITH GOLD DOWN $52.55 TODAY: STRANGE: BIG CHANGES AGAIN IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 920.24 TONNES

FEB 2/WITH GOLD $10.95 TODAY: BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 918.50 TONNES

FEB 1/WITH GOLD DOWN $2.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 31/WITH GOLD UP $6.55 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 30/WITH GOLD DOWN $6.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 918.50 TONNES

JAN 27/WITH GOLD DOWN $0.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 919.37 TONNES

JAN 26/WITH GOLD DOWN $11.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 919.37 TONNES

JAN 25/WITH GOLD UP $7.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 917.34 TONNES

JAN 24/WITH GOLD UP $7.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 23/WITH GOLD UP $0.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.63 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 20/WITH GOLD UP $4.75 TODAY;BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 912.43 TONNES

JAN 19/WITH GOLD UP $16.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES INTO THE GLD///INVENTORY RESTS AT 910.98TONNES

JAN 18/WITH GOLD DOWN $1.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.9 TONNES FROM THE GLD////INVENTORY RESTS AT 909.24 TONNES

JAN 17/WITH GOLD DOWN $11.45 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.14 TONNES

JAN 13/WITH GOLD UP $22.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD///INVENTORY RESTS AT 912.14 TONNES

JAN 12/WITH GOLD UP $20.55 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 912.43 TONNES

JAN 11/WITH GOLD UP $1.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.17 TONNES

JAN 10/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 915.33 TONNES

JAN 9/WITH GOLD UP $ 8.60 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD//.//INVENTORY RESTS AT 915.33 TONNES

JAN 6/WITH GOLD UP $28.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 916.77 TONNES

JAN 5/WITH GOLD DOWN $17.05 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 916.77 TONNES

JANUARY 4/WITH GOLD UP $32.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.64 TONNES

JAN 3/WITH GOLD UP $20.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:STRANGE: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 917.64 TONNES

GLD INVENTORY: 915.30 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478/614 MILLION OZ.

FEB 28/WITH SILVER UP 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.241 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.188

FEB 27/WITH SILVER DOWN 15 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.471 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 482.429 MILLION OZ

FEB 24/WITH SILVER DOWN 46 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.172 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.900 MILLION OZ//

FEB 23/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.379 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.072 MILLION OZ//

FEB 22/WITH SILVER DOWN 22 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ FROM THE SLV////INVENTORY RESTS AT 485.693 MILLION OZ

FEB 21/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.5363 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 486.382 MILLION OZ//

FEB 17/WITH SILVER UP 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 827,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.819 MILLION OZ/

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 478.614 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

PREPARE FOR 10 YEARS OF GLOBAL DESTRUCTION

Egon von Greyerz

March 1, 2023

The final stages of major economic cycles are always accompanied by the maximum amount of bad news as well as heinous events. This time is no different as the West is in the process of committing Harakiri (Seppuku).

As Elon Musk said:

“My mentality is that of a Samurai. I would rather commit Seppuku than fail.”

Sadly, the problem for the West is that it is both committing Harakiri and failing.

For at least half a century, the world has been in a process of self-destruction.

As the decline accelerates, the next phase of 5-10 years will include major political, social, economic as well as wealth – destruction.

What can be more heinous than a total economic and financial collapse accompanied by a potential World War III that at worst could destroy the world totally.

A recent article of mine discussed global fragility due to War, Debt and Energy Depletion.

In this article I outline the major risks today, financial and geopolitical and also discuss the best way to protect against these risks. Physical Gold is of course the ultimate wealth preservation investment. The next major move up in gold is not far away. See further on.

Biden’s recent visit to Ukraine and whistle stop tour of Europe confirmed that there is no desire to make peace but only war. More support of weapons and money from the US is forthcoming. And whatever the US dictates, Europe follows without considering the consequences.

At the end of his Warsaw address Biden stated about Putin:

“For God’s sake, this man cannot remain in power”.

Hmmm…. Hardly the talk of a peace maker

China on the other hand is trying to act as peacemaker but their proposal last Friday was cold shouldered by the West.

More importantly, the Chinese Ministry of Foreign Affairs issued an important policy document this week which is a very strong attack on the US hegemony called:

“US Hegemony and Its Perils”.

The attack starts in the introduction:

“Since becoming the world’s most powerful country after the two world wars and the Cold War, the United States has acted more boldly to interfere in the internal affairs of other countries, pursue, maintain and abuse hegemony, advance subversion and infiltration, and wilfully wage wars, bringing harm to the international community.

It then goes on in detail to attack all the areas of US Hegemony like: Political – Throwing its Weight Around, Military – Wanton Use of Force, Economic – Looting and Exploitation, Technological – Monopoly and Suppression, Cultural – Spreading False Narratives.

The document exemplifies in detail the hegemonic policies and attacks of the US. Although US politicians will totally reject its contents, it is difficult to argue with the facts put forward by China.

As I mention regularly, I very much like America and its people but have difficulties accepting the policies of the Neocons who dominate US politics.

Here is an extract from the Conclusion in this Chinese document:

“The United States has been overriding truth with its power and trampling justice to serve self-interest. These unilateral, egoistic and regressive hegemonic practices have drawn growing, intense criticism and opposition from the international community.

Countries need to respect each other and treat each other as equals. Big countries should behave in a manner befitting their status and take the lead in pursuing a new model of state-to-state relations featuring dialogue and partnership, not confrontation or alliance. China opposes all forms of hegemonism and power politics, and rejects interference in other countries’ internal affairs.” (Here is a link to the full document.)

It is difficult to argue with this conclusion. But we need to wear the moccasins of the US and rest of the world and look at China from that perspective. This is to follow my adage to walk three moon laps in somebody’s moccasins before you judge him.

China is not attacking various countries in the world by force, but primarily using investments and trade routes to dominate the world like the Modern Silk Road called the Belt and Road Initiative. It sets out to connect 65% of the world’s population to China by creating a network of sea routes and land links. China is estimated to have spent $1 trillion so far but total estimates are as high as $8 trillion. It will most likely take decades to achieve and might become too costly as the world economy declines.

However, what is clear is that China is investing heavily in infrastructure around the world both in Europe, Africa and South America. For example China is buying up ports in a substantial number of countries. They are also investing heavily in the resource sector globally.

Another problem that the West has with China is their human rights record.

Regardless, the trend is clear. The West is in a long term structural decline and the shift to China and the rest of the East and the South is inevitable as I discussed in the article“AS WEST, DEBT & STOCKS IMPLODE, EAST, GOLD & OIL WILL EXPLODE”

THE STRUCTURAL DECLINE OF THE WEST

All empires are ephemeral and this is what the US and Europe are currently experiencing.

The final stages of empires, like the Han, Roman, Mongol, Ottoman, Spanish and British always include the same ingredients some of which are:

- Excessive Debts and Deficits

- Currency Collapse

- Collapse of asset prices including property, bonds and stocks

- Hyperinflation in the final stages, especially in food, commodities & services

- Migration

- High Crime Rates & Breakdown of Law & Order

- Moral Decadence

- Social Unrest, Civil War

- Wars

As the West is now falling (& failing), we can tick all the above events also in the current collapse.

Global debt has exploded since 1971 to $2-3 quadrillion as I have explained in many articles like here.

If it wasn’t for the Petrodollar, the US would have collapsed years ago. But as more countries are considering trading oil in other currencies like Yuan, the dollar will first Gradually lose its value and then Suddenly to paraphrase Hemingway.

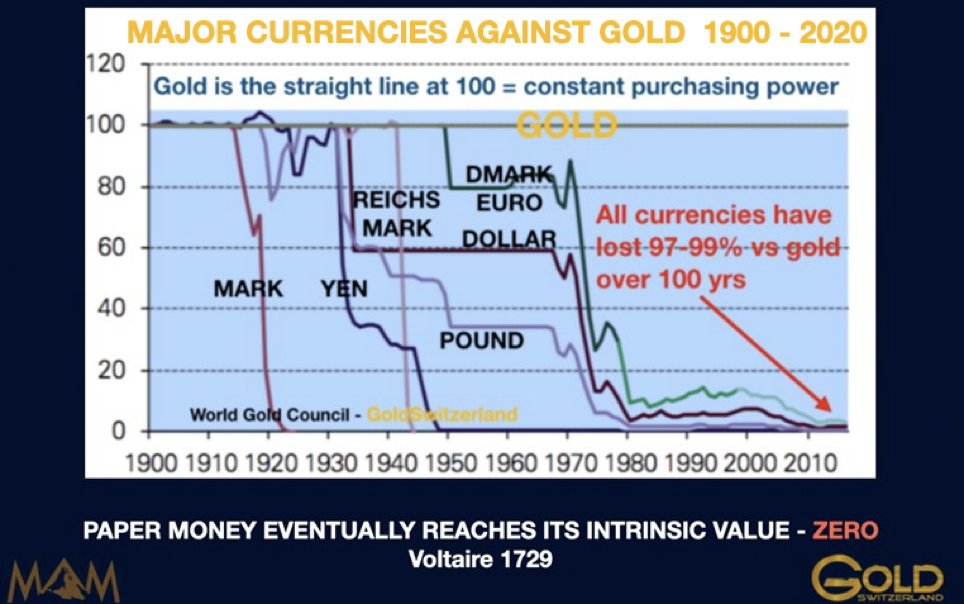

But remember that since Nixon closed the Gold Window in 1971, all currencies have lost at least 97-99% of their value in real terms which is against gold.

Empires seldom die overnight so this process which started in 1971 could take another 5-10 years. But since we are now in the final stages, it could also happen Suddenly.

So let’s paint a potential scenario for the next 5-10 years.

In simple terms it will be more of the same if we look at the 9 points above.

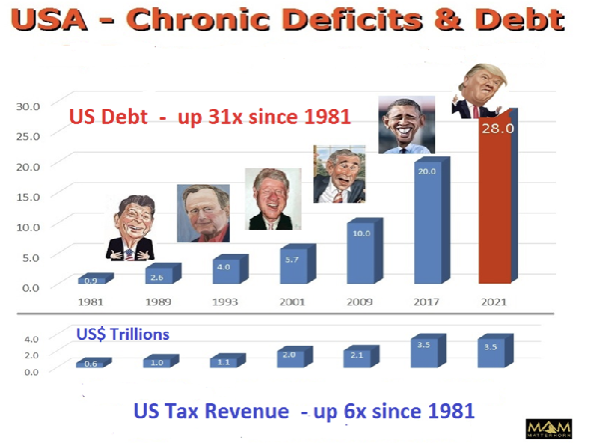

Debts and deficits will increase exponentially. I have for many years shown the growth in US debt which on average has doubled every 8 years since Reagan became president in 1981.

On December 6, 2016, the chart below was included in a Family Office presentation I gave in London:

I projected then in 2016 that when Trump would reach the end of his first term in January 2021, US debt would be $28 trillion on the way to $40 trillion four years later in 2025.

Interestingly, the debt was $28T in Jan. 2021. It doesn’t require a genius to project this figure as it is a straight extrapolation of the trend dating back 40 years. Still, I didn’t see anyone forecasting anywhere near the $28T debt in 2016.

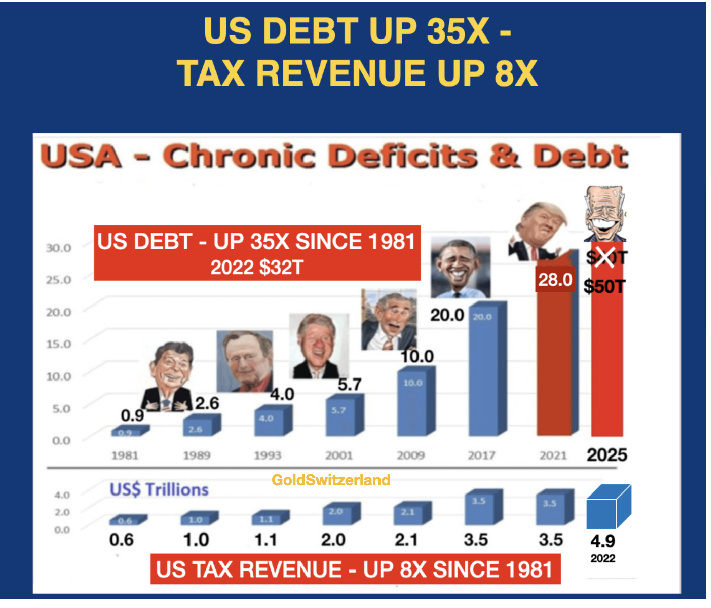

A couple of years ago, I raised my $40T debt in 2025 to $50T as the chart below shows:

So how is the US going to go from $32T to $50T in 3 years. Well, in the same way as bankrupt countries collapse with tax revenue falling precipitously and expenditure exploding.

THE ROAD TO PERDITION FOR THE US & THE WEST

As the value of the dollar collapses, think:

- Much higher war costs, social security, and pensions. As pension fund assets implode, there probably won’t be any pensions.

- Debt collapse both private and public with $2-3 quadrillion of derivatives turning into debt.

- All bubble assets of stocks, bonds and property, only held up by fake money, collapsing by 75-95% in real terms.

- Banks and financial institutions failing after initially having received $100s of trillions in printed, thus worthless, government support.

- With high inflation or hyperinflation, interest rates going to at least 20% or probably much higher. Financing a debt in the quadrillions at 20%+ will of course lead to even more money printing. The Fed and other central banks will clearly lose control of interest rates which will be determined by a market in panic..

WILL THERE BE A GLOBAL NUCLEAR WAR?

The US has at this point stressed that there will be no uniformed US military in Ukraine. Both Russia and Ukraine has lost around 150,000 soldiers each. The problem for Ukraine is that this is around 50% of their regular soldiers whilst for Russia it is 13%. Also, a major part of the weapons and ammunition from the West is not forthcoming or substantially delayed. There just isn’t the spare capacity available to fulfil those promises.

At this point, it looks like this war at best will be a very long drawn local conflict although Ukraine will find it difficult to sustain the war. In January 2022 the Ukraine population was 41 million and now 14 million are estimated to have left the country.

In a war of this nature between two super powers, it is impossible to forecast the outcome. An “accident” or false flag can easily trigger the start of a nuclear war.

Remember that this is a war between the US and Russia. So if there was a nuclear war, most missiles would be directed towards those two countries and potentially Ukraine.

But if the world will see a nuclear war, all bets are off since some parts of the world would then be destroyed for decades. Therefore, it is not worth speculation about.

WEALTH PRESERVATION & CBDCs

So assuming that this war remains a local conflict in Eastern Europe, how should people outside the war zone prepare financially?

Many countries are planing to introduce Central Bank Digital Money or CBDC.

As the current monetary system in the West collapses, CBDC will only be another form of fiat money. The worst part about it is the ability to spy on and control people that it gives governments. As Western governments’ finances implode, CBDC is the perfect system for the likely socialist or Marxist economies that many Western countries are likely to have.

For individuals who have the freedom to move, it would be preferable to leave the heavily indebted USA and Europe (especially the EU countries).

One country in Europe still stands out as probably the best in the world both politically, economically and socially. This is of course Switzerland.

Yes, I have skin in the game here! I am Swiss from birth and pleased that I am. I was born and educated in Sweden and also like Sweden.

But whilst Switzerland has remained a very sound country, Sweden has deteriorated dramatically. It now has one of the highest crime rates in Europe. As in the last 10-15 years Europe opened its borders for refugees from many poor and war struck countries, this has totally changed Swedish society.

There is nothing wrong with immigration. The world has always had migration. But until recent years, migrants had to look after themselves with no government subsidies. But in many countries in Europe and especially in Sweden, migrants arrive and get free housing and money to live. For many, there is no incentive to work and or to learn Swedish. Sadly an important percentage of men turn to crime and especially drug dealing. Fatal shootings between the immigrants are now happening daily in Sweden whilst 20 years ago, private weapons didn’t exist.

The best proof of a sound country and economy is the currency.

When I, as a younger man, came to Switzerland in the late 1960s, 1 Swiss Franc cost 1.10 Swedish Kroner. Today it costs 11.20 Swedish Kroner to buy one Franc. So the Krona has lost 90% in the last 50+ years.

The Swiss Franc has of course been strong against all currencies. The dollar for example has lost 80% against the Franc over 50 years.

THE SUPERIOR SWISS ECONOMY AND POLITICAL SYSTEM

But Switzerland has so much more than a strong currency and economy like:

- Low debt, normally no deficits

- Lowest crime rate in Europe and in the world (excluding some Middle East countries. It is one of the few countries where you can walk safely in any town at night.

- Rule of Law

- Direct Democracy allowing the population to have a referendum on virtually any topic. If the referendum is approved by a majority, it becomes part of the constitution and cannot be changed by government or parliament but only by another referendum. This is totally unique in the world.

- For example there will be a referendum on stopping Switzerland from becoming cashless

- Whilst all EU countries have decided to confiscate Russian assets, Switzerland has declared: “The expropriation of private assets of lawful origin without compensation is not permissible under Swiss law,” the government said on Thursday. “The confiscation of frozen private assets is inconsistent with the constitution,” it added, and “violates Switzerland’s international commitments”.

- The standard and quality of everything is very high, services, construction, communications etc

- Switzerland also has beautiful nature, and excellent food.

RISK OF WAR IN EUROPE

Some countries are worrying about a war in Europe. Except for a nuclear war which would be global, the risk of a war on the ground in Europe is in my view minimal.

Russia has been invaded many times with the most famous examples being Karl XII of Sweden in the early 1700s, Napoleon in the early 1800s and Hitler in the 1940s. But Russia has never made any serious invasion into Europe. Their interest lies primarily within their former empire. There was a brief entry into Finland at the beginning of WWII which lasted 3 months. Also at the end of WWII the Russians drove the invading Germans back to Berlin.

So in my view, there is absolutely no reason to fear a Russian invasion of Europe.

WEALTH PRESERVATION & GOLD

To protect your wealth against all the risks that I have outlined above is absolutely vital. Anyone invested in conventional assets like stocks, bonds and property, which have been artificially inflated by printing fake fiat money will in the coming 5+ years experience a major collapse of their wealth.

As I already said, for anyone who has the ability to move to a country outside the US and the EU, that would be the safest option. It is likely that these areas will have the biggest problems both in the economy and the financial system as well as socially. In that region, Switzerland will be an important exception.

Parts of South America like Uruguay should also avoid many of the problems in the West but sadly crime is high in many of these countries. Many Americans live in Central America but with the coming economic downturn, many countries will become less safe and also poor. In Asia, countries like Singapore and Thailand are very good but if there is a conflict between the US and China after a possible Chinese invasion of Taiwan, these areas could become more precarious.

The problem with Australia and New Zealand is that they are highly indebted with big asset bubbles, especially in property. The socialist policies are not a plus either. But the biggest risk is that a conflict in Taiwan could make these countries very risky with Chinese aspirations.

Many people are moving to Dubai today for tax reasons. Russians are moving there since Dubai doesn’t sanction them. The problem with the UAE is that conflicts in the Middle East occur with regular intervals.

For the ones who can’t move for job or family reasons, a second passport is advisable.

But the most important asset protection is having wealth preservation assets outside your country of residence.

There is no totally safe country today in an unsafe world.

For investors who want to preserve their wealth, the best asset is physical gold followed by the more volatile silver. Gold and silver shares have had a terrible 35 years but the good companies should perform spectacularly. Since most stocks are held by custodians within the financial system, they are not the same degree of wealth preservation as physical metals that you have direct control of.

So my own preference would be to own physical gold and silver that I have direct control of and can withdraw or sell with very short notice.

It is also important to deal with a company that can move your metals at very short notice if the security or geopolitical situation would necessitate it.

Our gold vault in the Swiss Alps is the biggest private gold vault in the world and is also nuclear bomb proof which is totally unique. This is for bigger investors. We also store gold in Zurich. Our second preference is Singapore with the reservations I have mentioned. We also have vaults in many parts of the world and as I have stated, this can be important if the situation in the world changes and the gold/silver needs to be moved.

The world is now moving towards troubled times.

Remember that family and friends are your most important asset and treasure them profoundly.

Also, except for family and friends, many of the best things in life are free like books, nature, music, and sports.

END

3. Chris Powell of GATA provides to us very important physical commentaries//

END

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

5.IMPORTANT COMMENTARIES ON COMMODITIES: +

END

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

end

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 6.8636

OFFSHORE YUAN: 6.8684

SHANGHAI CLOSED UP 32.74 PTS OR 1.00%

HANG SENG CLOSED UP 833.77 PTS OR 4.21%

2. Nikkei closed UP 70.97 PTS OR 0.26%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 104.10 Euro RISES TO 1.0684 UP 108 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.500!!(Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 135.39/JAPANESE YEN RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.6915%***/Italian 10 Yr bond yield RISES to 4.511%*** /SPAIN 10 YR BOND YIELD RISES TO 3.716…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.431//(ITALY WORSE THAN GREECE?)

3j Gold at $1839.05//silver at: 21.02 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 12/100 roubles/dollar; ROUBLE AT 75.09//

3m oil into the 76 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 135.39/10 YEAR YIELD AFTER BREAKING .54%, REMAINS AT .5000% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9354– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9993well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.9362% UP 2 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.920 DOWN 1 BASIS PTS//INVERTED TO THE 10 YEAR!!

USA 2 YR BOND YIELD: 4.8305 UP 3 BASIS PT

USA DOLLAR VS TURKISH LIRA: 18,89…

GREAT BRITAIN/10 YEAR YIELD: 3.84415% DOWN 1 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Rebound As China Economy Roars Back, Dollar Tumbles

WEDNESDAY, MAR 01, 2023 – 08:05 AM

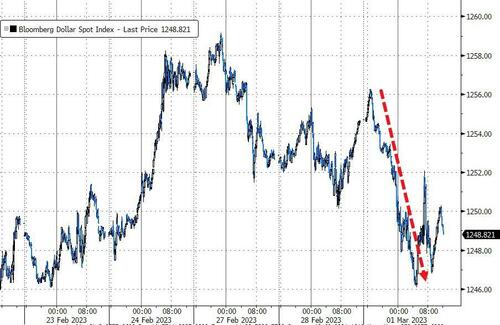

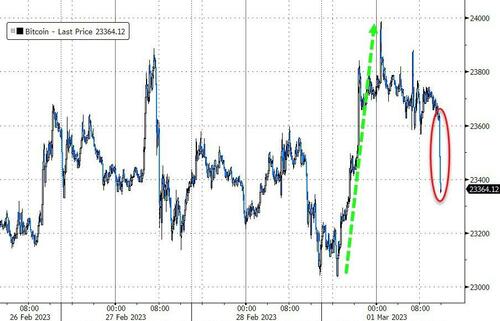

US equity rebounded from Tuesday’s month-end pension and CTA selling boosted by overnight news that China’s economy was roaring back sparked growth optimism and outweighed concerns about sticky inflation that could keep the Fed on its hawkish path. S&P 500 futures rose 0.3% at 7:40 a.m. ET, still hovering below the key technical support level of 4,000, while Nasdaq futures edged higher, up 0.4%. Sentiment was boosted by a sharp drop in the dollar which saw the Bloomberg Dollar Spot Index traded down 0.5% near session lows, the biggest drop since Feb. 14, as the yuan stormed higher. Treasuries edged lower, mirroring moves in Europe after German states saw annual inflation accelerate in February. Oil fell, while gold gained with Bitcoin.

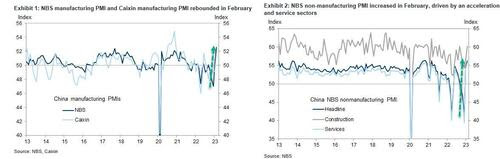

Boosting sentiment today was news that China’s economy is showing signs of a stronger rebound after Covid restrictions were abandoned, with manufacturing posting its biggest improvement in more than a decade. The big economic news overnight came from China’s random number generator, and specifically the manufacturing PMI which rose to 52.6 last month, the highest reading since April 2012. The Caixin manufacturing PMI also rose into expansion, to 51.6 in February from 49.2 in January. The NBS non-manufacturing PMI increased markedly to 56.3 in February from 54.4 in January, driven by an acceleration in both construction and service sectors. Both the NBS and Caixin manufacturing PMIs pointed to improvement in the manufacturing sector in February, as firm operations and customer demand recovered in February after the LNY impact dissipated and the post-Covid recovery gathered steam.

Some observations from Goldman on the Chinese data:

- The China NBS purchasing managers’ indexes (PMIs) survey suggested manufacturing activity improved significantly in February. The NBS manufacturing PMI headline index jumped to 52.6 in February from 50.1 in January, the highest reading since April 2012. The improvement was broad-based. Among major sub-indexes of NBS manufacturing PMI, the output sub-index rebounded to 56.7 from 49.8, the new orders sub-index increased sharply to 54.1 from 50.9, and the employment sub-index rose to 50.2 from 47.7. The suppliers’ delivery times sub-index rose notably to 52.0 in February from 47.6 in January, implying faster supplier deliveries and artificially depressed the headline PMI. NBS commented that business operations and customer demand accelerated on the dissipation of LNY impact and the removal of zero-Covid policy.

- The Caixin manufacturing PMI was released later in the morning. The headline index rose to 51.6 in February from 49.2 in January, on the relaxation of Covid restrictions. Surveyed companies mentioned that the increase in production was linked to easing Covid restrictions and recovery of business operations and client demand. Sub-indexes in the Caixin manufacturing PMI suggest expansion in output in February (53.3 vs. 49.0 in January), rising new orders (52.9 vs. 49.3 in January), stronger employment (50.6 vs. 48.4 in January), rising inventories in raw inputs (49.3 vs. 48.4 in January), faster suppliers’ delivery (51.2 vs. 49.3 in January), slightly stronger inflationary pressures in input and output prices (51.7 and 50.3 vs. 52.0 and 49.7 in January, respectively), and stronger new export orders (52.2 vs. 48.7 in January).

- Both the NBS and Caixin manufacturing PMIs reported expansion in new orders and output, stronger new export orders and faster suppliers’ delivery. Both manufacturing supply and demand expanded in February, as production quickly normalized, and domestic and external demand improved after the Covid policy change.

- The official non-manufacturing PMI (comprised of the services and construction sectors) rose to 56.3 in February (vs. 54.4 in January), driven by an acceleration in both sectors. The services PMI increased to 55.6 (vs. 54.0 in January). According to the survey, the PMIs of transport service industries such as postal, airline and road transport services were above 60 in February. The construction PMI rose in February to 60.2 (vs. 56.4 in January). NBS noted that the growth of the construction sector (presumably infrastructure-related) accelerated in February.

“US index futures are trying to rebound this morning following stronger than expected China figures suggesting the economy is responding positively to the reopening,” Peter Garnry, head of equity strategy at Saxo Bank, said in a note.

In premarket trading, Novavax shares plummeted more than 25% putting the Covid-19 vaccine maker on track for its worst day in more than two months, after fourth-quarter revenue missed analyst estimates and the firm said there is substantial doubt over its future. Reata Pharmaceuticals surged in premarket trading after winning FDA approval for a new drug. Meanwhile, Tesla is set to hold an investor day on Wednesday, where Chief Executive Officer Elon Musk is poised to unveil his latest and much-hyped “master plan” for the electric-vehicle maker. Several Wall Street analysts turned more bullish on the stock in anticipation of the event, but after a nearly 70% surge in just two months of this year, further gains may require more fireworks than are expected. Here are some other notable premarket movers:

- US-listed Chinese stocks stage a strong rally in premarket trading, rebounding from a recent slump, after a slew of data showed that China’s economy is on track for a stronger recovery. Alibaba (BABA US) +6.1%, Baidu (BIDU US) +6.8%, JD.com (JD US) +4.9%, Bilibili (BILI US) +9%, Nio (NIO US) +6%, XPeng (XPEV US) +7.4%

- Rivian (RIVN US) shares fell 8.1% after the electric-truck maker’s 2023 production forecast fell short of expectations amid supply-chain snags. Analysts at Truist cut their price targets on the stock, but noted that the lower outlook was mainly down to cost cuts, which should benefit the company in the long run.

- Sarepta Therapeutics (SRPT US) gains 20% after saying that the FDA doesn’t plan to hold an advisory committee for the approval of its experimental gene therapy to treat Duchenne muscular dystrophy.

- Monster Beverage (MNST US) shares drop 3.8% after the energy drink maker reported fourth- quarter results, with analysts highlighting the miss on revenue and earnings per share.

- BrightSpire Capital (BRSP US) shares fall 14% after holder DigitalBridge offered 30.4 million Class A shares in the mortgage finance company at $6 apiece, representing a 19% discount to Tuesday’s close.

The strong rally seen at the start of 2023 in US equities is showing signs of petering out, as inflation is proving stickier than expected, prompting investors to grow wary of the potential for hawkish central bank dynamics. The S&P 500 declined 2.6% in February, paring much of the strong year-to-date gains, but JPMorgan strategists believe this doesn’t capture the sharp increase in rates since the Federal Reserve’s last meeting and that the index at risk of further losses as a divergence with bonds is yet to close. Other strategists – in fact most of Wall Street – are similarly bearish

“The market is increasingly coming around to a more bearish view and previously expected rate cuts are being taken out of the curve and terminal rates are moving up,” Marija Veitmane, strategist at State Street Bank told Bloomberg. “Investors perceive any strong economic data as evidence that the Fed’s job is not yet done” while any poor data is sign of an imminent recession.

“Since the start of February, bond markets have been pricing in higher rate hikes from the Fed, but mixed economic data and lower decline in fourth-quarter earnings kept stocks afloat,” said Ipek Ozkardeskaya, senior analyst at Swiss Group. “Yet, US yields are poised to trend higher, and that will at some point pull equity valuations lower. A setting where yields and stocks rise together is not sustainable.”

Meanwhile, economic indicators are still running hot in the US, with official data on Monday showing that orders placed with US factories for business equipment increased in January by the most in five months. Wednesday’s data on construction spending, ISM manufacturing, and light vehicle sales will be watched closely by investors for further signs that the Federal Reserve might take as reason to tighten monetary policy more aggressively, or extend high interest rates for longer.

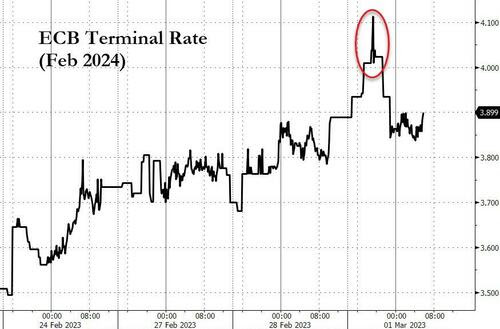

As a result, bond traders no longer view the odds of a Fed rate cut this year as better than-even, a shift from what they were expecting just a month ago. Market expectations also see the European Central Bank raising rates through February 2024, with a 4% ECB terminal rate fully priced. “February has poured cold water on hopes that policy makers may quickly tame inflation towards target,” Generali Investments strategists wrote in their monthly outlook. “We now have even higher peak rates in our books.” Watch this sentiment reverse with a bang the moment February jobs comes far below expectations next Friday..

On the other hand, contrary to expectations by Morgan Stanley’s Michael Wilson who has effectively staked his carrer on a forecast for a collapse in corporate profits, company earnings have proved more resilient than expected, even as traders question how long this can be sustained, given rising costs and the recessionary backdrop. In a sign that margins may yet be squeezed, asset manager Janus Henderson believes that dividend returns may be set to slow. Portfolio manager Jane Shoemake said she expects global dividend payouts to rise 2.3% to $1.6 trillion in 2023, a slower pace of growth compared with 8.4% last year, amid elevated inflation and geopolitical risks.

European stocks are ahead, tracking gains in Asia after Chinese manufacturing PMI rose to its highest in almost 11 years. The Stoxx 600 is up 0.1% with miners, autos and consumer products the strongest-performing sectors. Here are the biggest European movers:

- Aston Martin surges 22%, climbing to the highest since June, after the carmaker released results that analysts say showed a strong finish to the year with guidance for 2023 positive

- Moncler shares jumped as much as 8.5%, their biggest rise since November, after the luxury group’s full-year results beat expectations and Citigroup noted upbeat comments about its outlook

- Weir Group shares rise as much as 8.6%, hitting the highest since February 2021, with analysts saying the results from the mining-equipment firm are strong across the board

- Adidas shares jump as much as 3% after the sportswear brand was upgraded at HSBC, which says the company is likely to “embark on an ambitious path to reconquer market share”

- Ferrovial gains as much as 2.4% after the operator of London’s Heathrow Airport reported full-year results and a plan to shift domicile to the Netherlands and eventually apply for a US listing

- Euronext shares gain as much as 7.8% after the exchange operator withdrew its offer for investment platform Allfunds, a deal that analysts had questioned

- BNP Paribas shares dropped as much as 4.6%, their biggest decline since June, after Belgium’s Societe Federale de Participations & d’Investissement announced the sale of a 2.7% stake

- Just Eat Takeaway falls as much as 9.3% after failing to offer a gross transaction value forecast for 2023, a move analysts say looks disappointing after peer Delivery Hero did the same

Earlier in the session, Asian stocks were off to a strong start for March after China’s factory activity topped a decade high, spurring investor optimism ahead of an upcoming meeting of the nation’s political leaders. The MSCI Asia Pacific Index rose as much as 1.6%, the most since Jan. 9, lifted by communication and consumer discretionary shares. The Hang Seng China Enterprises Index jumped more than 5%, bouncing back from a recent selloff as strong manufacturing data underscores an acceleration in economic recovery.

“The latest economic data suggest China’s reopening has been working well,” said Nicolas Wang, senior equity advisor at Union Bancaire Privée. Hopes that a stimulus plan will be announced at the National People’s Congress have been somewhat priced into stocks, according to Union Bancaire’s Wang. Economists expect Premier Li Keqiang — who will deliver his last government work report on Sunday when the annual event kicks off — to outline a target for gross domestic product growth for this year of higher than 5%. Elsewhere in Asia, Taiwan advanced after traders returned from a two-day break, while Japan also edged higher. South Korean market was shut for a holiday. Asian stocks on Tuesday capped their worst month since September amid concerns over higher US interest rates and ongoing geopolitical risks. Traders no longer view the odds of a Federal Reserve rate cut this year as better-than-even, a shift from what they were expecting just a month ago.

Japanese equities rose, erasing early losses, after gauges of Chinese manufacturing beat economists’ expectations. The Topix rose 0.2% to close at 1,997.81, while the Nikkei advanced 0.3% to 27,516.53. The yen dipped about 0.1% against the dollar. Mitsui & Co. contributed the most to the Topix gain, increasing 3.4%. Out of 2,160 stocks in the index, 1,254 rose and 792 fell, while 114 were unchanged. “In addition to the cheaper yen, Japanese stocks are also benefiting from the rise in China and Hong Kong markets after the release of China’s PMI data,” said Yasuhiko Hirakawa, head of an investment department at Rakuten Investment Management. “Both manufacturing and non-manufacturing PMIs were higher previously expected, and there is positive sentiment toward the strong recovery of China’s economy.”

Australian stocks edged lower with the S&P/ASX 200 index ending 0.1% lower after a volatile session as investors assessed a slowdown in Australia’s inflation and economic growth, and how the data will impact monetary policy. The benchmark closed at 7.251.60 after swinging between gains and losses, weighed down by banks and property names. Australia’s monthly inflation eased in January to 7.4%, sending the currency and government bond yields lower. Meanwhile, the economy expanded at a slower-than-expected pace in the final three months of 2022, in a sign that the Reserve Bank’s rapid interest-rate increases are beginning to weigh on activity. In New Zealand, the S&P/NZX 50 index fell 0.2% to 11,876.35.

Stocks in India snapped an eight-day drop, the longest streak in more than three years, as investors looked for value after major benchmarks fell for a third straight month in February. The S&P BSE Sensex rose 0.8% to 59,411.08 in Mumbai, while the NSE Nifty 50 Index advanced by a similar measure. All of BSE Ltd.’s 20 sector sub-guages closed higher, led by metal and commodity related companies. All 10 companies that are part of the ports-to-power Adani conglomerate ended higher for the first time since the scathing report by US short seller Hindenburg Research was published on Jan. 24. The group is conducting a three-day roadshow this week to restore investor confidence. Reliance Industries contributed the most to the Sensex’s gain, increasing 0.9%. All but two of 30 shares in the Sensex index rose.

In FX, the Bloomberg Dollar Spot Index fell as much as 0.5%, the most since Feb. 14, as the greenback weakened against all its Group- of-10 peers, while the New Zealand dollar was the best performer.

- The New Zealand dollar led G-10 gains, rising as much as 1.3% to $0.6263, the highest since Feb. 17, and the Australian dollar swung to a gain after China’s manufacturing purchasing managers’ index rose to the highest in more than a decade and exceeded economists’ forecasts. The Aussie had dropped earlier and bonds advanced following slower-than-expected local inflation numbers.

- China’s manufacturing PMI rose to 52.6 last month, the highest reading since April 2012. A non-manufacturing gauge measuring activity in both the services and construction sectors improved to 56.3. Both indexes beat economists’ expectations. A non-manufacturing gauge measuring activity in both the services and construction sectors improved to 56.3. Both indexes beat economists’ expectations

- The euro gained as much as 0.8% to $1.0662 and European bonds dropped, led by the front end, after stronger inflation figures from Germany. Options traders scaled back their bearish bets on the euro amid money-market wagers that the ECB’s terminal rate will be higher than previously expected

- The pound pared an advance and gilts erased an earlier drop as traders trimmed bets on the peak in the BOE’s key rate. BOE Governor Andrew Bailey cautioned markets against assuming a rates move in either direction, while acknowledging the impact that monetary tightening is having on the economy

In rates, treasury futures narrowly mixed after paring losses during European morning, following wider gains across gilts where front-end outperforms. Treasuries curve pivots around a little-changed 7-year sector with long-end yields richer by more than 1bp vs Tuesday’s close and 2s10s, 5s30s spreads flatter. 10-year TSY yields are little changed around 3.92% day with gilts outperforming by 3.5bp in the sector. US curve extends Tuesday’s flattening move post month-end. Block flattener in futures adds to long-end outperformance over European session.

In Europe, Bund futures extended losses after the German state of North Rhine-Westphalia saw annual inflation accelerate in February, suggesting an upside surprise in the national reading later today. German 10-year yields are up 6bps while the UK equivalent falls 1bps. Gilts outperform following comments from BOE Governor Andrew Bailey, who said Wednesday that “nothing is decided” on the future path of rates.

In commodities, Crude futures decline with WTI falling roughly 1.0% to trade near $76.25. Spot gold adds around 0.3% to trade near $1,832.

Looking to the day ahead now, data releases include the global manufacturing PMIs for February and the ISM manufacturing reading from the US. From central banks, we’ll hear from BoE Governor Bailey, the Fed’s Kashkari, and the ECB’s Villeroy, Nagel and Visco. Finally, earnings releases include Salesforce and Lowe’s.

Market Snapshot

- S&P 500 futures up 0.2% to 3,983.00

- MXAP up 1.5% to 160.37

- MXAPJ up 2.0% to 521.54

- Nikkei up 0.3% to 27,516.53

- Topix up 0.2% to 1,997.81

- Hang Seng Index up 4.2% to 20,619.71

- Shanghai Composite up 1.0% to 3,312.35

- Sensex up 0.8% to 59,414.51

- Australia S&P/ASX 200 little changed at 7,251.60

- Kospi up 0.4% to 2,412.85

- STOXX Europe 600 little changed at 461.44

- German 10Y yield little changed at 2.71%

- Euro up 0.6% to $1.0642

- Brent Futures down 0.3% to $83.21/bbl

- Gold spot up 0.3% to $1,832.20

- U.S. Dollar Index down 0.40% to 104.45

Top Overnight News from Bloomberg

- China’s NBS PMIs for Feb were very strong, with manufacturing coming in at 52.6 (up from 50.1 in Jan and ahead of the St’s 50.6 forecast) and non-manufacturing climbing to 56.3 (up from 54.4 in January and above the St’s 54.9 forecast). BBG

- After three years of turbulence under the Covid pandemic, China’s leaders are expected to lay out economic goals to get growth back on track, restore confidence and avoid a build-up of financial risks. Economists expect Premier Li Keqiang — who will deliver his last government work report on Sunday when the annual National People’s Congress kicks off — to outline a target for gross domestic product growth for this year of higher than 5%. That’s after the economy expanded just 3% last year, missing the official goal by a wide margin. BBG

- US M2 money supply fell 1.7% Y/Y in January, the largest decline on record and the first time it has contracted in two consecutive months (but, money supply is still 39% higher than it was before COVID, which means the Fed still has plenty of work ahead of it). Barron’s

- Demand for U.S. workers shows signs of slowing, a long-anticipated development that is showing up in private-sector job postings even while official government reports indicate the labor market keeps running hot. ZipRecruiter Inc. and Recruit Holdings Co., two large online recruiting companies, say their data show the number of job postings is declining more than Labor Department reports of job openings. Investors recently hammered shares of those companies after disappointing earnings reports. WSJ

- The European Central Bank should reach its peak interest rate by September, Governing Council member Francois Villeroy de Galhau said. It would be unwise to expect the ECB to quickly reduce borrowing costs after their eventual peak, according to Governing Council member Madis Muller: BBG

- Bundesbank President Joachim Nagel said he supports a more rapid reversal of the ECB’s bond-buying to help tackle inflation, with more large interest-rate increases also a possibility beyond a planned hike this month: BBG

- The White House is coming under increased pressure to give F16 fighter jets to Ukraine (the process to deliver the jets and provide training for them is a long one, and many feel it should be started now). Wa Po

- The prices of new homes in 100 Chinese cities held steady in February versus January having fallen for seven consecutive months, data showed on Wednesday, as a flurry of property market easing measures improved buyer confidence. The flat reading followed a 0.02% decline in January from December, showed data from the China Index Academy. RTRS

- EU negotiators reached a deal to establish a green bond standard, giving investors long-awaited clarity that their money is aligned with the region’s climate ambitions: BBG

- UK house prices fell at their sharpest annual pace since 2012 last month, steepening a downturn sparked by a jump in mortgage rates. The average cost of a home fell 1.1% from a year ago last month after a gain of the same size in January, Nationwide Building Society said Wednesday. It marked the sixth consecutive monthly drop in prices and the first annual decline since June 2020: BBG

- Turkey’s parliamentary and presidential elections will take place as planned on May 14, President Recep Tayyip Erdogan has said, quashing speculation over whether the vote would be postponed following the two deadly earthquakes last month: BBG

- Economists expect China Premier Li Keqiang — who will deliver his last government work report on Sunday when the annual National People’s Congress kicks off — to outline a target for GDP growth for this year of higher than 5%. That’s after the economy expanded just 3% last year, missing the official goal by a wide margin

- Chinese President Xi Jinping welcomed Belarusian leader Alexander Lukashenko, a close Russian ally, in talks watched closely for signs that Beijing is expanding coordination with Moscow and its supporters in their standoff with the West

- BOJ Board Member Junko Nakagawa says that she wants to watch financial markets for a while longer to discern the impact of December’s adjustments to the BOJ’s yield curve control program

- The US crude buildup continues. Inventories increased by 6.2 million barrels last week, API data indicated, in what would be a 10th straight gain if confirmed by the EIA later. In fuel markets, gasoline and distillate stockpiles both eased. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly positive as the region digested a slew of data releases including the fastest pace of expansion for Chinese Manufacturing PMI in more than a decade. ASX 200 was initially pressured by weakness in telecoms and financials, but later pared the losses as the miss on quarterly GDP and softer monthly CPI data effectively eased some of the hawkish pressure on the RBA. Nikkei 225 lacked firm direction with price action confined to a narrow range around the 27,500 level. Hang Seng and Shanghai Comp. were supported by the blockbuster official Chinese PMI data which printed its highest since April 2012 and Caixin Manufacturing PMI also returned to expansion territory. Furthermore, a surge in tech spearheaded the outperformance in Hong Kong, while advances in the mainland were somewhat moderated by US-China frictions as the Biden administration considers revoking export licenses issued to US suppliers for sales to Huawei and with the US also barring chipmakers from expanding capacity in China for 10 years if they are to receive some of the federal funding from the CHIPS Act. US equity futures (ES Unch.) were uneventful but moved off lows as sentiment in Asia gradually improved

Top Asian News

- Chinese Finance Minister Liu Kun said proactive fiscal policy will be more forceful, while he added that China’s economy will continue its rebound and local governments will see better fiscal conditions.

- BoJ JGB market survey shows the index measuring market functioning deteriorating to -64 for February (prev. -51, Nov.), the lowest on record.

- China’s economy is recovering faster than expected by top officials, suggesting that the government might be restrained in rolling out new stimulus measures this year, according to Bloomberg sources.