Mar 7 2023 · by harveyorgan · in Uncategorized · Leave a comment·Edit

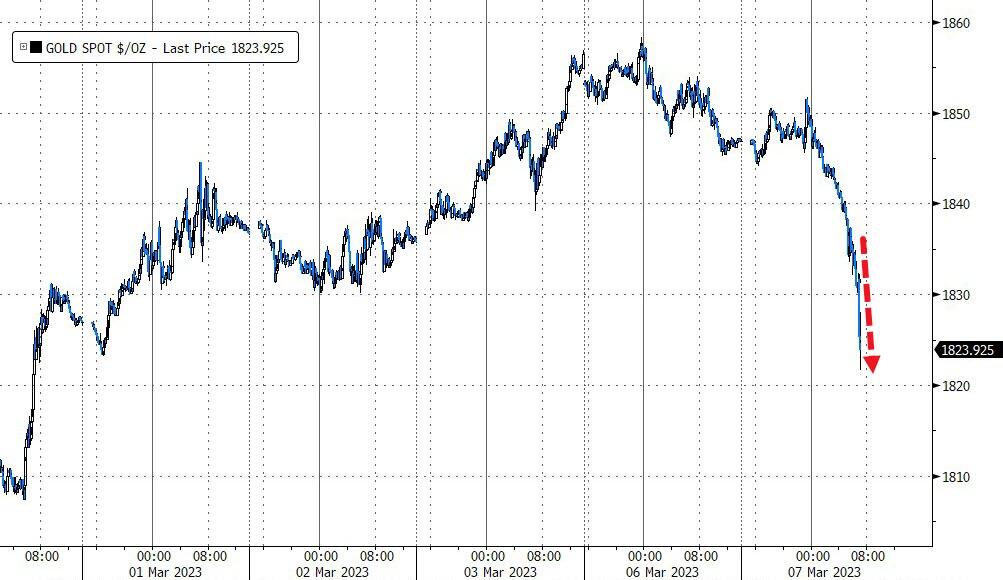

GOLD PRICE CLOSED: DOWN $33.20 at $1815.85

SILVER PRICE CLOSED: DOWN $0.88 to $20.15

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1814.25

Silver ACCESS CLOSE: 20.09

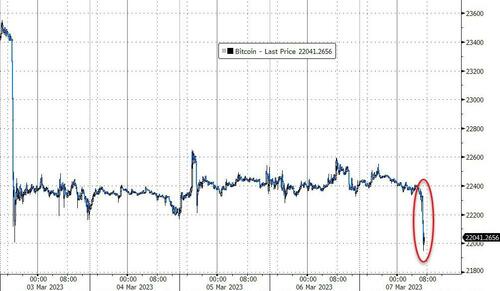

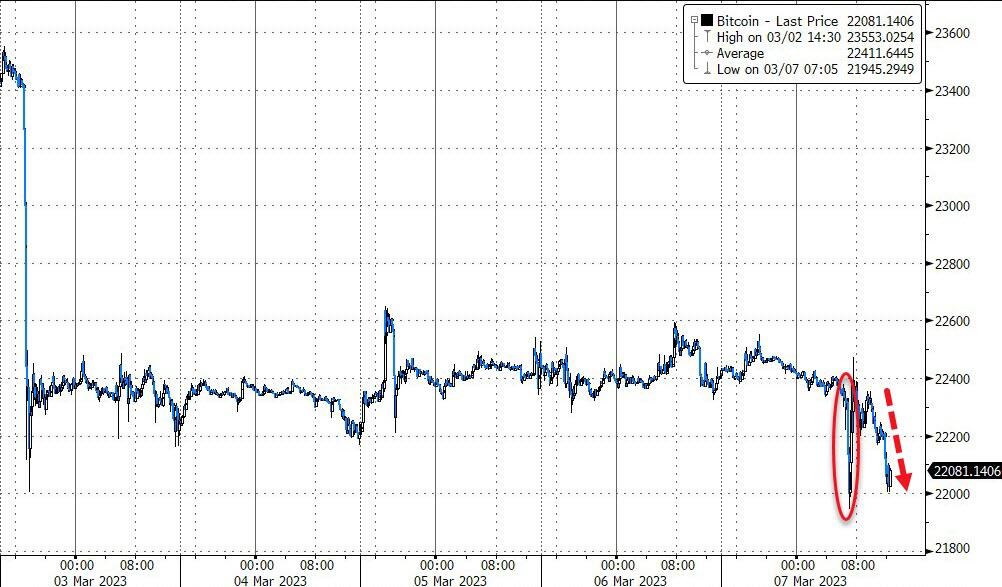

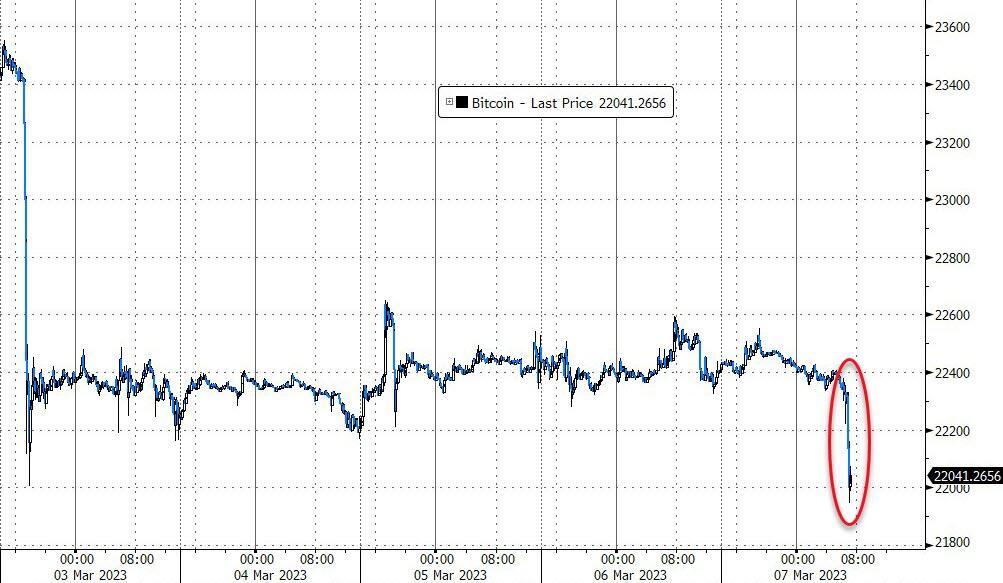

Bitcoin morning price:, 22368 DOWN 57 Dollars

Bitcoin: afternoon price: $22,097 DOWN 331 dollars

Platinum price closing $936.10 DOWN $42.15

Palladium price; closing $1394.40 DOWN $53.10

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,495.50 DOWN $18.85 CDN dollars per oz

BRITISH GOLD: 1534.50 DOWN 0.95 pounds per oz

EURO GOLD: 1720.02 DOWN 7.81 euros per oz

COMEX DATA

EXCHANGE: COMEX

COMEX//NOTICES FILED 0 oz of gold

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR MAR/2023. CONTRACT: 0 NOTICES FOR 0 OZ or 0.00 TONNES

total notices so far: 2169 contracts for 216,900 oz (6.7465 tonnes)

SILVER NOTICES: 59 NOTICE(S) FILED FOR 295,000 OZ/

total number of notices filed so far this month : 2857 for 14,289,000 oz

END

GLD

WITH GOLD DOWN $33.20

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/NO CHANGES IN GOLD INVENTORY AT THE GLD////

INVENTORY RESTS AT 912.12TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 88 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 478.143. MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A FAIR SIZED 360 CONTRACTS TO 122,402 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE FAIR SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.13 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. OUR NEW LOW COMEX OI SILVER WAS SET AT 121,299 MARCH 3/2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.13). BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS, AS WE HAD A GOOD GAIN ON OUR TWO EXCHANGES 610 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 1 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS( 250 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.58 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE JUMP OF 340,000 OZ//NEW STANDING: 14.745 MILLION OZ + THE 1.0 MILLION OZ OF EXCHANGE FOR RISK//THUS TOTAL NEW STANDING 15.745 MILLION OZ/ //// V) FAIR SIZED COMEX OI GAIN/ SMALL SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –29 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTRACTS for 5 days, total 1701 contracts: OR 8.505 MILLION OZ . (340 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 8.505 MILLION OZ

.

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 8.505 MILLION OZ//INITIAL

RESULT: WE HAD A FAIR SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 360 DESPITE OUR $0.13 LOSS IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 250 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAR OF 15.58 MILLION OZ FOLLOWED BY TODAY’S 340,000 QUEUE JUMP (WHICH INCREASES THE AMOUNT OF SILVER STANDING) + 1.0 MILLION OF EXCHANGE FOR RISK ISSUED EARLY IN MARCH (INCREASES THE AMOUNT OF SILVER STANDING) //NEW STANDING 15.745 MILLION OZ .. WE HAVE A GOOD SIZED GAIN OF 639 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 59 NOTICE(S) FILED TODAY FOR 295,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 3464 CONTRACTS TO 441,454 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 1559 CONTRACTS.

.

WE HAD A FAIR SIZED INCREASE IN COMEX OI ( 3464 CONTRACTS) DESPITE OUR TINY $0.55 GAIN IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR MAR. AT 4.9953 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 100 OZ (0.00311 TONNES) //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S ) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London).

YET ALL OF..THIS HAPPENED WITH OUR $0.55 GAIN IN PRICE WITH RESPECT TO MONDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 6099 OI CONTRACTS (18.970 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2635 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 441,454

IN ESSENCE WE HAVE A STRONG INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 6099 CONTRACTS WITH 3464 CONTRACTS INCREASED AT THE COMEX AND 2635 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 6099 CONTRACTS OR 18.97 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2635 CONTRACTS) ACCOMPANYING THE GOOD SIZED GAIN IN COMEX OI (3464) TOTAL GAIN IN THE TWO EXCHANGES 6099 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR MAR. AT 4.9953 TONNES FOLLOWED BY TODAY’S 100 OZ QUEUE JUMP//NEW STANDING 6.9642 TONNES // ///3) ZERO LONG LIQUIDATION //4) GOOD SIZED COMEX OPEN INTEREST GAIN// 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

TOTAL EFP CONTRACTS ISSUED: 14,569 CONTRACTS OR 1,456,900 OZ OR 45.32 TONNES 5 TRADING DAY(S) AND THUS AVERAGING: 2913 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAY(S) IN TONNES 45.32 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 45.32/3550 x 100% TONNES 1.26% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 45.32 TONNES/INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A FAIR SIZED 389 CONTRACTS OI TO 122,431 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A RECORD LOW OF 121,299 CONTRACTS MARCH 3/2023.

EFP ISSUANCE 250 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 250 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 250 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 360 CONTRACTS AND ADD TO THE 250 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG GAIN OF 610 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES //3.05 MILLION OZ

OCCURRED DESPITE OUR $0.13 LOSS IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED DOWN 36.93 PTS OR 1.11% //Hang Seng CLOSED DOWN 68.61 PTS OR 0.33% /The Nikkei closed UP 71.381% PTS OR 0.25% //Australia’s all ordinaries CLOSED UP 0.49% /Chinese yuan (ONSHORE) closed UP 6.9356 //OFFSHORE CHINESE YUAN UP TO 6.9457// /Oil UP TO 79,89 dollars per barrel for WTI and BRENT AT 85.71 / Stocks in Europe OPENED MOSTLY GREEN EXCEPT SPAIN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 3464 CONTRACTS UP TO 441,454 DESPITE OUR TINY GAIN IN PRICE OF $0.55.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAR… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2635 EFP CONTRACTS WERE ISSUED: : APRIL 2363 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2635 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 6099 CONTRACTS IN THAT 2635 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 3464 CONTRACTS..AND THIS GOOD SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR TINY GAIN IN PRICE OF $0.55. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAR (6.9642) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 6.9642 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $0.55) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG SIZED GAIN OF 6099 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 18.97 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAR. (4.9953 TONNES) FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 100 OZ (0.003211 TONNES)… ALL OF THIS WAS ACCOMPLISHED WITH OUR SMALL RISE IN PRICE TO THE TUNE OF $0.55.

WE HAD -1559 CONTRACTS REMOVED FROM COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 6099 CONTRACTS OR 609,900 OZ OR 18.97 TONNES

Estimated gold comex today 272,727// //fair

final gold volumes/yesterday 155,212/// poor

//MARCH 7/MARCH 2023 CONTRACT

//

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 96,453.000 oz JPMorgan 2 tonnes 2,000 kilobars) . |

| Deposit to the Dealer Inventory in oz | nil OZ Brinks |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 0 notice(s) 0 OZ 0.00 TONNES |

| No of oz to be served (notices) | 70 contracts 7000 oz 0.2177 TONNES |

| Total monthly oz gold served (contracts) so far this month | 2169 notices 216,900 6.7465 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 1

i) Out of JPMorgan; 96,453.000 o

(2,000 kilobars)

total withdrawals: 96453.000 oz

in tonnes: 2 tonnes

Adjustments; 1

i) Brinks: 23,417.201 oz dealer to customer

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of MARCH we have an oi of 70 contracts having LOST 58 contracts. We had 59 notices filed on Monday so we

gained another 1 contract or an additional 100 oz will stand for metal at the comex

April lost 833 contracts down to 318,347 contracts

May gained 3 contracts to stand at 97

We had 0 notice(s) filed today for nil oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer notice(s) was (were) stopped 0 Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAR. /2023. contract month,

we take the total number of notices filed so far for the month (2169 x 100 oz ), to which we add the difference between the open interest for the front month of (MAR. 70 CONTRACTS) minus the number of notices served upon today 0 x 100 oz per contract equals 223,900 OZ OR 6.9642 TONNES the number of TONNES standing in this active month of MARCH.

thus the INITIAL standings for gold for the MAR contract month:

No of notices filed so far (2169 x 100 oz+ 70 OI for the front month minus the number of notices served upon today (0)x 100 oz} which equals 223,900 oz standing OR 6.9642 TONNES in this active delivery month of MARCH..

TOTAL COMEX GOLD STANDING: 6.9642 TONNES.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,789,729.416 OZ 55.67 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,534,523.647 OZ

TOTAL REGISTERED GOLD: 10,894,494.910 (338.86 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 10,640,0238.737 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,104,765 OZ (REG GOLD- PLEDGED GOLD) 283.19 tonnes//dropping like a stone

END

SILVER/COMEX

MAR 6/2023// THE MARCH 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2.373,318.910 oz CNT Brinks Delaware HSBC JPMorgan |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 1200,261.756 oz CNT Loomis |

| No of oz served today (contracts) | 59 CONTRACT(S) (295,000 OZ) |

| No of oz to be served (notices) | 92 contracts (460,000 oz) |

| Total monthly oz silver served (contracts) | 2857 contracts (14,285,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 2 deposits into the customer account

i) Into CNT: 600,611.410 oz

ii) Into Loomis: 599,650.340 oz

Total deposits: 1200,261.756 oz

JPMorgan has a total silver weight: 146.605 million oz/285.730 million =51.22% of comex .//dropping fast

Comex withdrawals: 5

i) Out of CNT: 799,710.017 oz

ii) Out of Delaware: 12,410.272 oz

iii) Out of Brinks 16,175.350 oz

iv) Out of HSBC 600,183.290 oz

v) Out of JPMorgan: 1,042,838.940 oz

Total withdrawals; 2,372,318.919 oz

adjustments: 1//JPMorgan: dealer to customer: 1,796,229.496 oz

oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 39.239MILLION OZ (declining rapidly).TOTAL REG + ELIG. 286.902 million oz

CALCULATION OF SILVER OZ STANDING FOR MAR

silver open interest data:

FRONT MONTH OF MAR/2023 OI: 151 CONTRACTS HAVING LOST 46 CONTRACT(S.) WE HAD 114 NOTICES FILED

YESTERDAY, SO WE GAINED A HUGE 68 CONTRACTS OR AN ADDITIONAL 340,000 OZ WILL STAND FOR METAL ON THIS SIDE OF THE POND.

April LOST 10 CONTRACTS TO STAND at 400.

May LOST 689 CONTRACTS DOWN TO 104,962.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 59 for 295,000 oz

Comex volumes// est. volume today 70,202// strong//

Comex volume: confirmed yesterday: 60,940 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 2857 x 5,000 oz = 14,285,000 oz

to which we add the difference between the open interest for the front month of MAR(151) and the number of notices served upon today 59 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAR./2023 contract month: 2857 (notices served so far) x 5000 oz + OI for the front month of MAR (151) – number of notices served upon today (59) x 500 oz of silver standing for the MAR. contract month equates 14.745 million oz +the 1.0 million oz of exchange for risk//new total standing 15.745 million oz

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

FEB 28/WITH GOLD UP $12.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 917.61 TONNES

FEB 27/WITH GOLD UP $6.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.32 TONNES

FEB 24/WITH GOLD DOWN $9.10 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 917.32 TONNES

FEB 23/WITH GOLD DOWN $13.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 919.92 TONNES

FEB 22/WITH GOLD DOWN 22 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 919.92 TONNES

FEB 21/WITH GOLD DOWN $7.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 919.92 TONNES

FEB 17/WITH GOLD DOWN $1.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 921.08 TONNES

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

GLD INVENTORY: 912.12 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FORM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

FEB 28/WITH SILVER UP 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.241 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.188

FEB 27/WITH SILVER DOWN 15 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.471 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 482.429 MILLION OZ

FEB 24/WITH SILVER DOWN 46 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.172 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.900 MILLION OZ//

FEB 23/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.379 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.072 MILLION OZ//

FEB 22/WITH SILVER DOWN 22 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ FROM THE SLV////INVENTORY RESTS AT 485.693 MILLION OZ

FEB 21/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.5363 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 486.382 MILLION OZ//

FEB 17/WITH SILVER UP 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 827,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.819 MILLION OZ/

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 478.143 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

Peter Schiff: All Roads Lead To Hard Landing And Higher Inflation

MONDAY, MAR 06, 2023 – 03:45 PM

The markets still seem to believe the Federal Reserve can ratchet price inflation back down to 2% while bringing the economy to a relatively soft landing. In his podcast, Peter Schiff throws cold water on this hopeful narrative. He goes through the economic data that came out last week shows that all roads appear to lead to a hard landing and higher inflation.

The stock markets finished up last week thanks to optimism that the Fed will pause rate hikes this summer. Atlanta Fed president Raphael Bostic stoked that optimism when he said he’s in favor of lower — and slower — rate hikes. “Right now I’m still in very firmly in the quarter-point move pacing.” Even though Bostic tempered his comments, saying he will go where that data takes him, Peter said that’s all the markets needed.

The bulls were grasping for straws and this is the one they grabbed.”

We saw big swings from Thursday’s lows to Friday’s highs in all the major stock indices.

Basically, all of the weekly gains were attributable to the Thursday-Friday rally, which was 100 percent the result of Fed-speak about the potential for a pause.”

There was quite a bit of weak economic data last week as well, including a 4.5% drop in durable goods orders. The Dallas Fed Manufacturing Survey came in at -13, below the low end of expectations. The Chicago and Richmond Fed manufacturing surveys were also weaker than expected. Meanwhile, the goods trade deficit was $91.5 billion.

We keep getting number after number that disappoints to the weak side on manufacturing. This flies in the face of a soft landing narrative, because it suggests that if we land at all, it’s not going to be soft. But maybe this is one of the reasons that investors are believing that we’re nearing the end of the rate hike cycle, and we’re going to get a pause followed by a pivot where we get our first cut.”

But Peter emphasized that just because we have a recession doesn’t mean inflation is coming down. In fact, it could be the exact opposite. Regardless, inflation certainly doesn’t appear to be cooling right now based on the productivity and cost numbers for the fourth quarter.

Anybody who is hoping that the Fed is winning the inflation battle, these numbers throw cold water all over that narrative.”

Productivity was down to 1.7% in Q4 from the 3.0% pace in Q3. Meanwhile, unit labor costs surged more than expected by 3.2%.

So, we have lower productivity and higher labor costs. This is not good if you think inflation is under control. The best way to control prices is with increasing productivity. But we’re not getting that. What we’re getting is increasing costs.”

Keep in mind that just because unit labor costs are rising doesn’t mean workers are getting paid more. Unit labor costs also include things like health insurance premiums, payroll taxes and regulations.

In fact, a lot of things the government does to increase labor costs results in fewer people getting hired. Because the government makes it so expensive to hire people that businesses try to avoid hiring where they can. So, they hire fewer people as a result of these rising labor costs.”

Peter reiterated that all of this flies in the face of the notion that inflation is coming under control.

And while there were a couple of better-than-expected economic data points, the rule was weak economic data.

But not only weak economic data, but inflationary data, not just with the weakness in productivity and spiking labor costs, but the fact that all of the manufacturing output is low. We need more supply. Well, we’re not getting it. We’re not producing more. We’re certainly consuming. So, where are we going to get the goods if we’re not producing them? We’re going to import them. That’s what you saw with the merchandise trade deficit. We’re importing the merchandise that we don’t have the industrial capacity to produce, and this is driving up our trade deficit, which will ultimately drive down the value of the dollar and push up domestic consumer prices.”

Peter said most of the optimism about the Fed slowing down its monetary tightening isn’t as much about the economy weakening as it is inflation weakening. But as Peter explained in a previous podcast, once the inflation genie is out of the bottle, it’s impossible to get it back in.

Peter reiterates this point by talking about inflation in the Eurozone.

What the markets still don’t get is even if we end up in a recession — in fact, even if we end up in a financial crisis — the inflation rate is not coming down. In fact, I believe the next recession will be a catalyst to send inflation to new highs. … They still don’t get the reality of stagflation. And they still don’t understand that you can have stronger inflation in a weaker economy. And in fact, this economy is going to be so weak that it’s going to supercharge inflation because the Fed is going to be forced to respond not only to the weakness in the economy, but in particular, the weakness in financial markets and the precarious fiscal position of the US government by unleashing massive inflation — maybe even more than unleashed during the lockdown periods of COVID, and that is going to send the inflation rate to new highs and bond prices to new lows.”

In this podcast, Peter also talks about:https://www.zerohedge.com/markets/peter-schiff-all-roads-lead-hard-landing-and-higher-inflatio

- The fact that the ECB’s inflation goals were asinine.

- The Fed will soon break its money-losing record.

- Debt is going to spiral out of control.

- Big money is leaving crypto.

- Markets don’t get that inflation isn’t coming down.

- end

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

John Rubino:

This commentary is really good as Rubino explains how Japan will go bust and that will be followed by most other countries

(John Rubino)

How A Country Goes Bankrupt… In 10 Steps

TUESDAY, MAR 07, 2023 – 06:30 AM

Authored by John Rubino via Substack,

The past few decades of unnaturally easy money have created a world of “moral hazard” in which a ridiculous number of people borrowed far more than they should have.

Now, with money getting tighter, not just businesses and individuals but some governments are staring at the “suddenly” part of that old saying about bankruptcy.

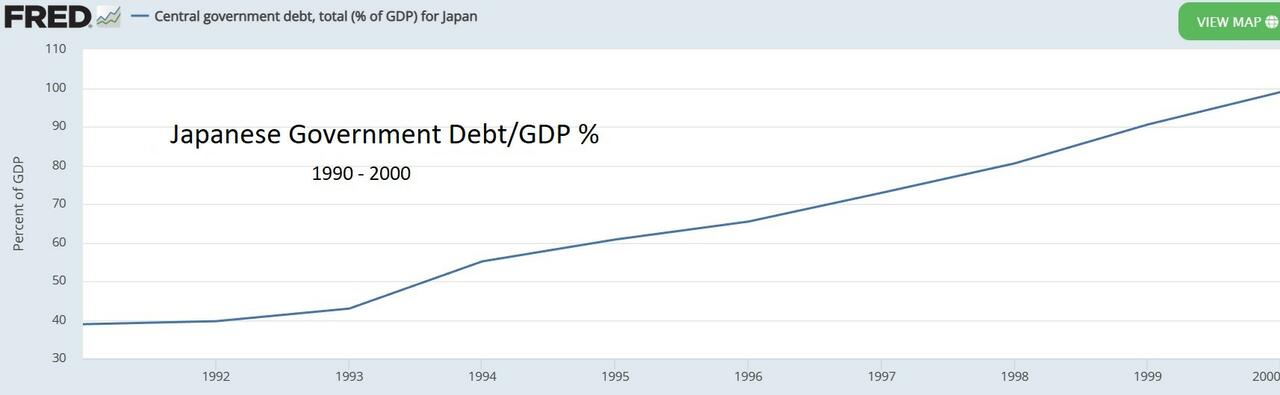

Japan is the poster child for this slow walk towards – then quick rush over – a financial cliff.

Here’s how it works for a government, in 10 steps.

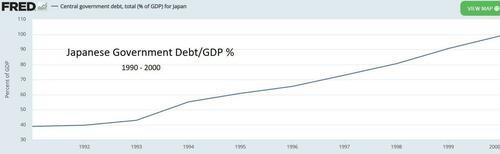

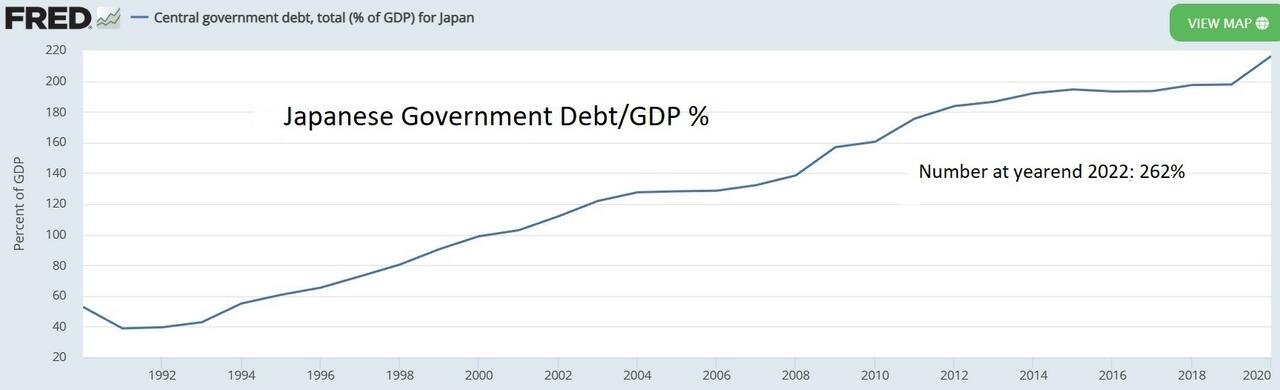

Step 1: Build up massive debt. A bursting real estate bubble in the 1990s confronted the Japanese government with a choice between accepting a brutal recession in which most of that debt was eliminated through default, or simply bailing out all the zombie banks and construction companies and hoping for the best. They chose bailouts, and federal debt rose from 40% of GDP in 1991 to 100% of GDP by 2000.

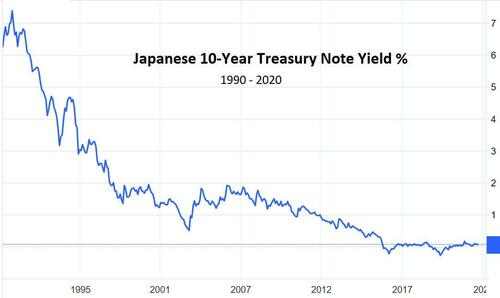

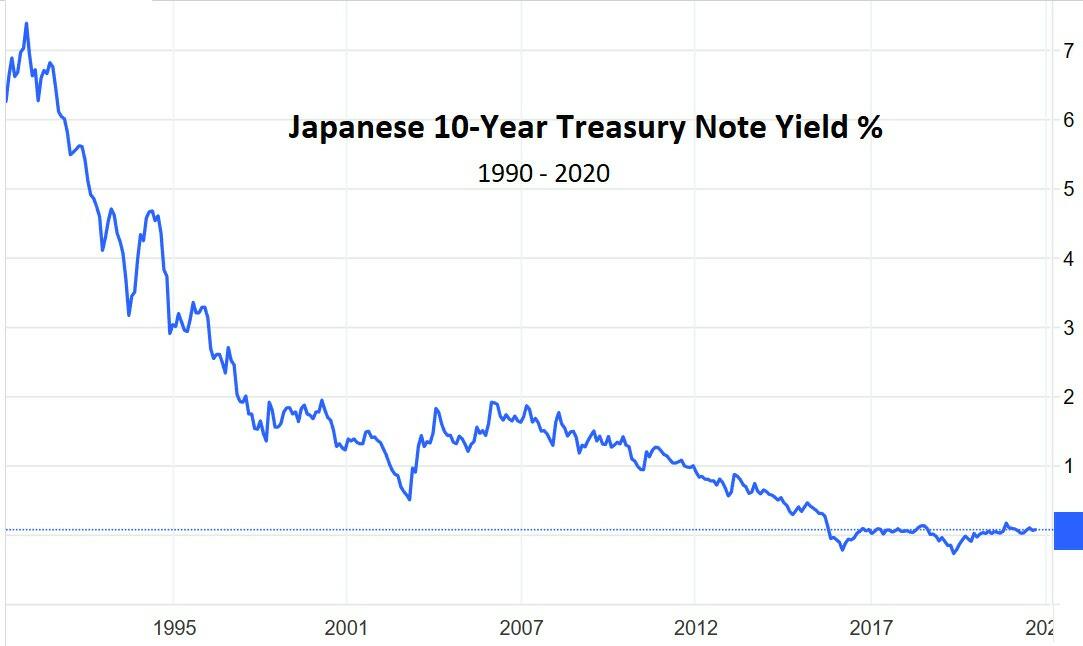

Step 2: Lower interest rates to minimize interest expense. Paying 6% on debt equaling 100% of GDP would be ruinously expensive, so the Bank of Japan pushed interest rates down as debt rose, thus keeping the government’s interest cost at tolerable levels.

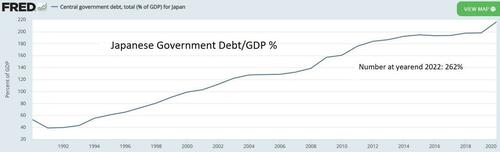

Step 3: Continue to borrow at virtually no cost. While interest rates fell, the zombie companies soaking up public funds were joined by a growing number of retirees who began drawing on japan’s versions of Social Security and Medicare. Government spending, as a result, continued to rise and deficits kept growing, further intensifying the pressure to lower interest rates. The BoJ began buying bonds with newly-created yen to force interest rates down to zero and even below (meaning that the remaining private sector buyers of Japanese government paper actually paid for the privilege). Since the government now earned money by borrowing, there seemed to be no reason to stop, and debt soared to the current 262% of GDP, which might be the highest figure ever recorded by a major government.

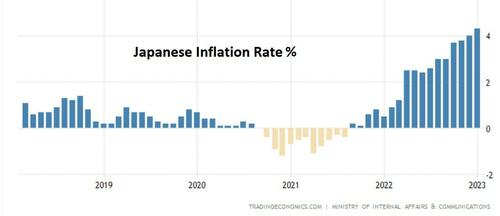

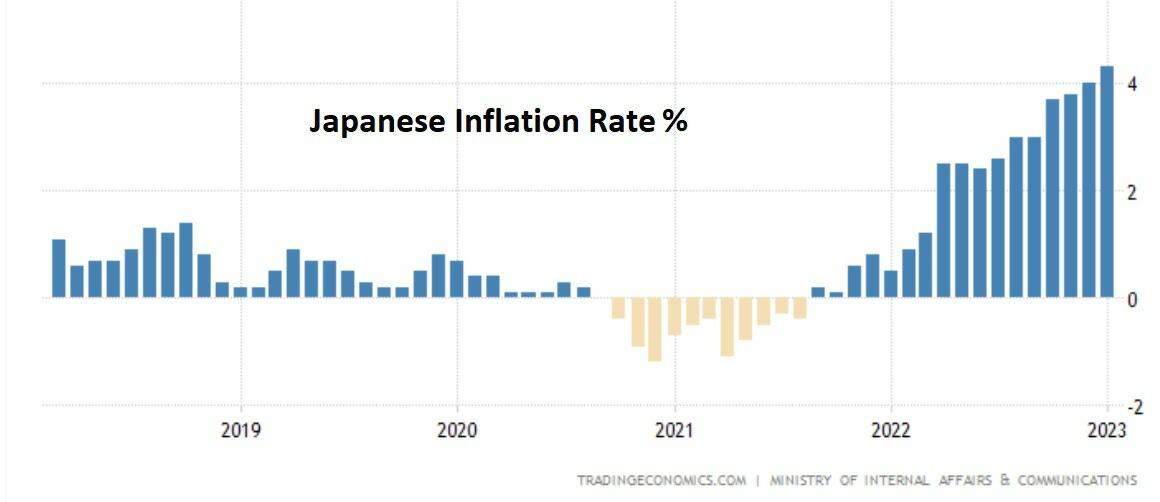

Step 4: Experience sudden, sharp inflation. In 2022, all that new currency finally caused the inflation that critics of easy money had been predicting. Japan’s official cost of living is now rising at a 4% annual rate, making the real yield on a zero-percent government bond -4%.

Step 5: Experience a plunging currency. With most other central banks tightening to combat inflation, the BoJ kept buying bonds to keep its interest rates low. Investors noticed this yield differential and stopped buying yen-denominated paper, sending the yen’s exchange rate down sharply versus the US dollar.

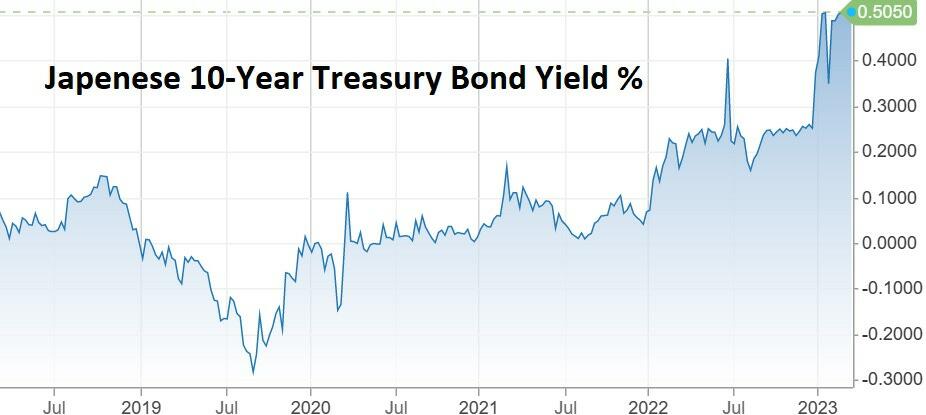

Step 6: Reluctantly allow interest rates to rise. Also in 2022, the BoJ realized that unless it wanted to buy all the paper the government was issuing, it would have to let interest rates rise a bit. Which they very quickly did, from 0% to .25% and then .5%.

Step 7: Get swamped by interest expense. Now all the debt issued or rolled over by Japan’s government carries a cost. Let’s say the average yield rises to the current 0.5%. On debt equaling 260% of GDP, interest expense equals 1.3% of GDP, a crushing burden that adds to already massive deficits, raising overall debt and therefore interest expense going forward.

Now For The “Suddenly” Part

All of the above has either happened or is happening. The next steps are scheduled for the near future:

Step 8: Desperately try to lower rates. Recognizing that soaring interest expense spells national bankruptcy, the BoJ tries to stop and reverse the trend by buying even more government debt with ever larger amounts of newly created yen. But the world’s other central banks are much slower to ease, so the gap between yields on Japanese paper and that of, for instance, the US and Germany, continues to widen.

Step 9: Watch impotently as the yen craters. With government debt rising parabolically and no one other than the BoJ willing to buy the resulting tsunami of paper, Japan enters the realm of full-on Modern Monetary Theory, where the government just finances itself with newly created currency. The rest of the world, recognizing the inflationary implications, dumps the yen and the currency’s exchange rate goes into free fall. A falling currency raises the cost of imports, which increases inflation, which weakens the yen further, putting upward pressure on interest rates, and so on, in what headline writers call a “death spiral”.

Step 10: Game over. Japan is forced into an official devaluation/currency reset which limits its ability to spend and inflate going forward. Everyone who trusted the government and held the old currency is impoverished while those who recognized the scam and converted cash and government bonds into real assets are enriched. It’s a familiar story. But this time it’s happening to a serious country.

Questions

The possibility of a major country going off a financial cliff raises questions about how widespread the effects might be and how US investors might prepare. And of course: “How do we short Japan”? That discussion is coming in a separate post next week.

END

PAM AND RUSS MARTENS:

Over the Past Year, Inflation Eroded Your Purchasing Power while the Stock Market Ate Away Your Investment Gains

By Pam Martens and Russ Martens: March 7, 2023

On Friday, March 4, 2022, the Dow Jones Industrial Average closed at 33,614.7971. Yesterday, one year later, the Dow closed at 33,431.44, a negligible loss of a fraction of one percent – but still a loss. The Dow is composed of just 30 stocks.

The S&P 500, a broader stock market index, includes the common stocks of 500 of the largest companies in the U.S. Over the past year, the S&P 500 fared even worse than the Dow. It went from 4,328.8729 on Friday, March 4, 2022 to yesterday’s closing price of 4,048.42 – a decline of 6 percent.

The tech heavy Nas daq Composite, which consisted of 3,607 component companies as of yesterday according to Nasdaq, delivered the worst performance of the three major indices over the past year. It traveled from 13,313.438 on Friday, March 4, 2022 to a closing price of 11,675.737 yesterday – a decline of 12.3 percent.

While the average American’s investment money was shrinking over the past 12 months, inflation was eating away at the purchasing power of their disposable income.

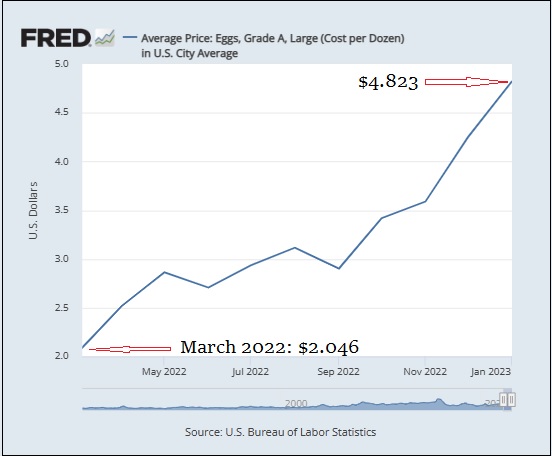

Among the most extreme examples of the toll of inflation on food costs was the price of eggs. As the chart below from the St. Louis Fed indicates, the average price of a box of Grade A, large eggs went from $2.046 in March of 2022 to $4.823 in January of this year.

The cold, hard facts on what the U.S. consumer’s money has been doing over the past 12 months raises puzzling questions about why consumer sentiment is holding up so well./p>

IIn June of last year, consumer sentiment, as measured by the University of Michigan Survey, slumped to the lowest recorded level since the University began collecting the data in November 1952. But as the chart below indicates, since that time consumer sentiment has made a puzzling climb back.

Another survey that takes the pulse of the U.S. consumer comes from the Conference Board. Its monthly Consumer Confidence Survey fell again in February for the second consecutive month./p>

The Conference Board’s Expectations Index, which is based on consumers’ short-term outlook for income, business, and labor market conditions, fell to 69.7 in February from a downwardly revised 76.0 in January. The Conference Board notes that “the Expectations Index has now fallen well below 80 — the level which often signals a recession within the next year. It has been below this level for 11 of the last 12 months.”

Against this backdrop comes Federal Reserve Chairman Jerome Powell testifying before the Senate Banking Committee this morning on the Fed’s monetary policy. The Fed has raised its benchmark interest rate – the Fed Funds Rate – eight times since March 17 of last year, moving from a zero-bound interest rate policy to a current target range of 4.5 to 4.75 percent. Democrats on the Senate Banking Committee are expected to express concerns this morning that the Fed is going to crash the economy with continued rate hikes while Republicans are likely to press the Fed to reassure markets that it remains focused on bringing down long-term inflation trends.

END

3. Chris Powell of GATA provides to us very important physical commentaries//

For your interest…

Agnico Eagle CEO mulls move to go big or get small in Australia

Submitted by admin on Mon, 2023-03-06 11:34Section: Daily Dispatches

By Jacob Lorinc

Bloomberg News

via Yahoo News, Sunnyvale, California

Monday, March 6, 2023

Agnico Eagle Mines Ltd. is weighing what to do with its only Australian gold mine after landing two big takeovers within two years that turned the Canadian company into the world’s third-largest gold producer.

Agnico gained an Australian mine as part of its combination with Kirkland Lake Gold Ltd., giving it a foothold into a region beyond its North American focus.

Agnico’s latest deal, set to close this month, reinforces the Toronto-based firm’s homegrown roots by taking full control of the Canadian Malartic mine in Quebec.

Chief Executive Officer Ammar Al-Joundi said he’ll spend this year reviewing Agnico’s operations, which also includes a gold mine in Finland, to determine next steps. That, he said, will involve making a decision on a key question: “Do we get bigger in Australia or do we get smaller?”

“We like Australia, we have no intention to sell Australia, but it would be disingenuous for me to say that we’ve got this big competitive advantage in Australia when we’ve got one mine,” Al-Joundi said Friday in an interview at Bloomberg’s Toronto office. …

… For the remainder of the report:

https://finance.yahoo.com/news/agnico-eagle-ceo-mulls-move-144000213.html

end

This is very interesting: the Perth Mint diluted its gold that it sold to China and others by a tiny bit

using silver or copper. The gold still was 99.99% but not .9999 that China wanted

(Australian Broadcasting Corp)

Perth Mint sold diluted gold to China, tried to cover it up

Submitted by admin on Mon, 2023-03-06 19:03Section: Daily Dispatches

By Angus Grigg, Ali Russell, Stephanie Zillman, and Meghna Bali

Australian Broadcasting Corp., Sydney

Sunday, March 5, 1013

The historic Perth Mint is facing a potential $9 billion recall of gold bars after selling diluted or “doped” bullion to China and then covering it up, according to a leaked internal report.

ABC’s “Four Corners” program has uncovered documents charting the Western Australian government-owned mint’s decision to begin “doping” its gold in 2018, and then how it withheld evidence from its largest client in an effort to protect its reputation.

While the gold remained above broader industry standards, the report estimated up to 100 tonnes of gold sent to Shanghai Gold Exchange (SGE) potentially did not comply with the exchange’s strict purity standards for silver content.

One Perth Mint insider, who asked not to be named and risk five years in jail if the insider’s identity is revealed, says it is a “scandal of the highest level.”

“I don’t know if I’ve ever seen one this big,” the insider says.

The mint is the largest processor of newly mined gold in the world, one of Perth’s top tourist attractions, and is well known for producing commemorative coins to mark everything from royal weddings to a new James Bond film.

Last year alone it sold A$20.3 billion in gold. It is the only mint in the world that has a government guarantee.

But in recent years the 124-year-old institution, officially known as Gold Corporation, has been plagued by a series of scandals. …

… For the remainder of the report:

https://www.abc.net.au/news/2023-03-06/perth-mint-gold-doping-china-cover-up-four-corners/102048622

* * *

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

Special thanks to G. for sending this to us:

(Kitco/Neumeyer)

Silver mines will likely be bought by automakers like Tesla, silver to $125 per ounce – Keith Neumeyer

Cornelius Christian Monday March 06, 2023 10:21

Kitco News

Share this article:

(Kitco News) – Automotive companies like Tesla could soon purchase silver mines, as they seek to control supply over critical metals required for electric vehicles. That’s according to Keith Neumeyer, President and CEO of First Majestic Silver who forecasts that this, combined with other demand-driven factors, will send the price of silver up to $125 per ounce.

“They [automobile companies] aren’t really aware of the supply-demand fundamentals of the metal,” he claimed. “I think as they educate themselves and actually learn the challenges for the silver industry to supply the automotive sector, they will start looking at this industry a lot more aggressively… If I were Elon Musk, I’d be very active in this area.”

Neumeyer, who founded First Majestic in 2002 and has four decades of experience in the financial industry, claimed that there would be more vertical integration and consolidated supply chains as automotive manufacturers and the solar industry seek to decrease margins they pay for raw materials.

Speaking at the BMO Global Metals, Mining, & Critical Minerals Conference with Michelle Makori, Lead Anchor and Editor-in-Chief at Kitco News, Neumeyer observed that 2023 is the first year that car manufacturers have been present at the conference. Some automotive companies have already bought stakes in minerals companies.

Neumeyer pointed to the fact that silver is needed for car batteries and solar panels to operate efficiently. Neumeyer observed that based on estimates, the average Tesla vehicle contains 1 kilogram of silver. As demand for electrification grows, the silver price is expected to rise.

“The estimated consumption in the solar panel industry is 160 million ounces of silver this coming year, 2023,” he claimed. “The electrical automotive sector is estimated to be slightly shy of 100 million ounces of silver… The Silver Institute is projecting an over 200-million-ounce deficit this year.”

Neumeyer forecast that silver could rise to $30 per ounce this year, while his medium to long term prediction is triple-digit silver. He suggested that a slowing economy would dampen the price of silver in the short-term

“I think silver is going to be somewhat delayed because of the economy, because it is an industrial metal,” he said. “I think we’re going to go to triple-digits [in the medium to long-term], and that has been my prediction for a couple of years now. Getting silver to $125 to $150, I think, is reasonable… we’re closer to that than we were a couple of years ago. The stars are aligning.”

To find out Neumeyer’s forecast for the gold price in 2023, watch the video above.

Silver Consortium

Neumeyer is a long-time advocate of silver miners forming a consortium so that they can sell silver directly to consumers, instead of going through derivatives markets like the COMEX and LBMA.

“[The mining sector] is at the mercy of banks, so if [banks] want to move these metals to whatever price they want to move them to, they can do it relatively easily” he claimed. “I wouldn’t necessarily call it manipulation. I think it’s just managing the book.”

The theory that the precious metals prices are manipulated to benefit the short position of commercial banks and governments has been advocated by a number of prominent voices, including mining mogul Frank Giustra.

Neumeyer suggested that this is not necessarily conspiratorial manipulation, as much as economic pressures from banks having to fulfill short positions.

To find out more about First Majestic Silver including its bullion products and mining operations, watch the video above.

Follow Michelle Makori on Twitter: @MichelleMakori

end

From Steve St Angelo: this is huge//all in costs are around $1576. per oz

Barrick and Newmont:

| SRSrocco Report | 2:56 PM (5 minutes ago) | ||

| to John, Tom, maneco64, Bix, Andy, TF, Arcadia, Chris, Dave, Dunagun, David, Bob, Ed, daniel, James, Rafi, robert, James, Midasnh@aol.com, me, Bill, J.C., Ted, Lionel, Ronan, Torgny, Don, Alasdair, badcharts, kenziecriley, Rebecca, Robert, steve, Gina | |||

To the Group,

While we discuss this information, the Two Largest Gold Producers in the world, BARRICK & NEWMONT, saw their total production cost hit the HIGHEST EVER at $1,576 per oz in 2022. Maybe this doesn’t mean anything to anyone here, but I can assure you, these gold companies can’t produce gold at a loss for long, or they will go out of business.

Isn’t that quite interesting in the past 22 years, the Gold market price hasn’t gone below the Top two Gold Miners’ Total Cost of Production? A mere coincidence? 🙂

steve

END

5.IMPORTANT COMMENTARIES ON COMMODITIES: +

END

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

end

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 6.9356

OFFSHORE YUAN: 6.9457

SHANGHAI CLOSED DOWN 36.93 PTS OR 1.11%

HANG SENG CLOSED DOWN 68.71 PTS OR 0.33%

2. Nikkei closed UP 71.38 PTS OR 0.25%

3. Europe stocks SO FAR: MOSTYL GREEN EXCEPT SPAIN

USA dollar INDEX UP TO 104.77 Euro FALLS TO 1.0661 DOWN 24 BASIS PTS

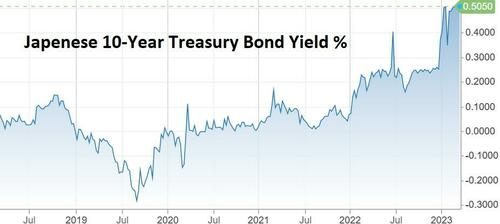

3b Japan 10 YR bond yield: RISES TO. +.500!!(Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 136.15/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.6745%***/Italian 10 Yr bond yield FALLS to 4.4790%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.683…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.438//(ITALY WORSE THAN GREECE?)

3j Gold at $1839.75//silver at: 20.86 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 18/100 roubles/dollar; ROUBLE AT 75.63//

3m oil into the 79 dollar handle for WTI and 85 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 136.15/10 YEAR YIELD AFTER BREAKING .54%, REMAINS AT .5000% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9339– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9958well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

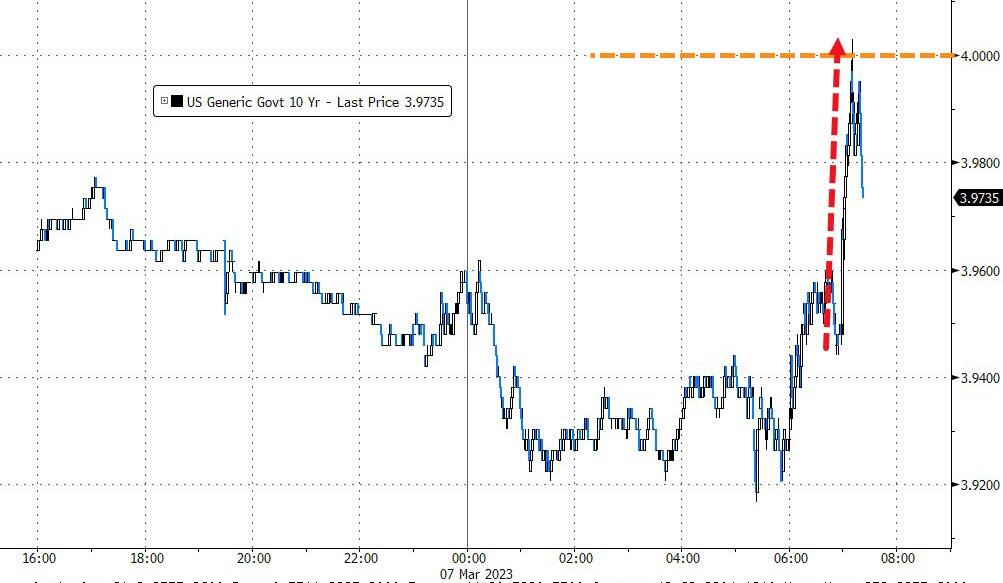

USA 10 YR BOND YIELD: 3.936% DOWN 5 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.872 DOWN 4 BASIS PTS//INVERTED TO THE 10 YEAR!!

USA 2 YR BOND YIELD: 4.8695 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,92…

GREAT BRITAIN/10 YEAR YIELD: 3.840% DOWN 1 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Rise Ahead Of Powell Senate Testimony

TUESDAY, MAR 07, 2023 – 08:09 AM

US stock-index futures were fractionally higher on Tuesday erasing a modest gain earlier in the session, set for the fourth day of gains as investors waited more visibility on monetary policy from Fed Chair Jerome Powell, who begins two days of testimony before the US Congress. Futures on the S&P 500 were 0.1% higher by 7:30 am ET after closing flat on Monday erasing a sizable earlier gain, while the Nasdaq 100 contracts climbed 0.3%. Another positive session today would place the S&P 500 on its longest winning streak since mid-January. Helping the mood today were Treasury bond yields holding below the key 4% mark even as the dollar rose to session highs. Oil, bitcoin and gold all dropped.

In premarket trading Meta Platforms was the most notable mover, rallying 2% on news the Facebook-owner is preparing to cull thousands more employees. Cara Therapeutics dropped 30% after the biotech company’s fourth-quarter revenue missed estimates and it reported a wider-than-expected loss per share, stoking worries over demand for the company’s Korsuva kidney disease drug and prompting analysts to cut their targets on the stock. Here are other notable premarket movers:

- Nutanix shares slumped as much as 9.1%, with analysts saying the delay of its 10-Q filling amid an investigation into its use of third-party evaluation software had eclipsed the cloud-platform provider’s strong preliminary results and raising of full-year guidance. Analysts said, however, that they don’t see the probe as having a big impact on the company.

- Rivian Automotive shares fell 5.8% after the electric-vehicle maker announced plans to raise $1.3 billion through the sale of green convertible bonds.

- Enlight Renewable Energy rose 1.2% after being initiated at Barclays and JPMorgan at overweight, and at Roth at buy, with analysts convinced of the US wind and solar project specialist’s long-term growth appeal, adding that the stock multiple is likely to rise closer to peers.

Today all eyes will be on Powell’s Senate testimony where he is expected to signal the Fed is ready to push rates higher than December’s dot plot indicated if inflation prints continue to exceed expectations, underscoring the FOMC’s resolve to get inflation under control. At the same time, he’ll acknowledge that the Fed’s dual mandate includes full employment, and that he retains hopes of achieving a soft landing for the economy (full preview here).

Many investors remain sidelined after being burnt repeatedly betting on an inflation peak, cooling US economy and Fed policy pivot. While the S&P 500 index is up 2% this month, recouping some of February’s losses – when stronger-than-expected economic and inflation data fueled concerns about a hawkish response from the Federal Reserve trying to keep price growth in check – traders are reluctant to push the gauge much higher, until they get more clarity on how high interest rates might go and whether the world’s largest economy will dodge recession.

Meanwhile, investors have upped their interest rates expectations and become more comfortable with the direction of monetary policy signaled by Powell, said John Plassard, investment specialist at Mirabaud. “I don’t expect today’s testimony to change that,” he said, adding that the positive momentum for stocks is likely to endure. “Some will call it a bear market rally but in the meantime, that’s the direction of travel,” Plassard added.

“There have been some positive developments — growth has been better than expected and interest rates have adjusted higher without too much volatility on equities,” said Francois Savary, chief investment officer at Swiss wealth manager Prime Partners. “We are at a point where the market is more or less correctly valued, so there is no need to be too negative on equities.” Savary expects the S&P 500 to stay in a range for the time being, noting that aside from the inflation question, “there are more challenges down the road on growth and it will be up to companies to show they can maintain earnings

Meanwhile, as Bloomberg notes, there is some relief that bond yields have not extended their run higher. Ten-year US Treasury borowing costs stayed around 3.92%, unable to sustain last week’s run above 4%, with investors noting the attraction of that yield level for buyers. Retail investors are also piling into Treasuries, snapping up the most six-month T-bills in nearly 30 years at an auction.

Citigroup strategists said that the bullish positioning in S&P 500 futures last week rose, but weekly notional changes were relatively small, with positioning net long and marginally above longterm averages. They added that bearish sentiment in Nasdaq futures continued to develop despite the underlying index climbing. “Short positioning grew last week, alongside ETF outflows. With nearly all shorts offside, and losses extending, there’s an increasing risk of a near-term squeeze,” said strategists led by Chris Montagu in a note.

European stocks edge higher as surprise increase in German factory orders reinforced the picture of a resilient euro zone economy. The Stoxx 600 is up 0.2% with utilities, healthcare and media the strongest-performing sectors. European bonds rallied, as a European Central Bank survey showed inflation expectations declining to 2.5% for three years ahead. Here are some of Europea’s biggest movers.

- Ashtead rises as much as 4.6% after the US-focused parent of the Sunbelt equipment rental firm predicts full-year results ahead of previous expectations

- Premier Foods shares jump as much as 10%, reaching the highest since April, after the maker of Mr. Kipling cakes boosted its sales and profit expectations for 2023

- Lufthansa shares gain as much as 1.9% in Frankfurt, wiping nearly all of the declines stemming from the Covid-19 pandemic, after Barclays gave a Street high price target to the German airline

- Wood Group shares jump as much as 17% after the consulting and engineering company said Apollo’s fourth proposal, at 237 pence per share, still undervalues the group

- Dufry shares gain as much as 2.7% after the Swiss airport retailer’s full-year sales beat forecasts, thanks to the recovery in travel demand as well as its confirmation of mid- term targets

- Zalando shares jump as much as 6% after the German online retailer delivered a profit outlook seen as slightly ahead of consensus, following 2022 earnings that beat estimates

- HelloFresh shares slump as much as 13% after the meal- kit provider set profit outlook that missed expectations, with the firm pledging to shift focus away from cost mitigation to its customer base

- Puma shares fall as much as 2.1% after UBS downgraded the sportswear brand to neutral from buy, saying the company’s strong market-share gains may be coming to an end

- Carlsberg shares drop as much as 4% after Chief Executive Officer Cees ‘t Hart announced his decision to retire by the end of the third-quarter “at the latest”

- Wincanton falls as much as 35%, the most ever, after the logistics firm says HM Revenue and Customs decided to move to another supplier for logistics services at inland border facilities

- Vodafone shares fall as much as 2.3% after the CEO of top shareholder Emirates Telecommunications Group says it does not plan to bid for all of the telecom operator

Asian equities were set to snap a two-day gain as Hong Kong-listed stocks reversed an earlier advance following weak China trade data and a bout of profit-taking. The MSCI Asia Pacific Index was down as much as 0.2%, erasing an earlier advance of as much as 0.6%. The Hang Seng China Enterprises Index closed lower, with market players citing weak export data for the first two months and policy uncertainty during the National People’s Congress as possible reasons. “Net exports are likely to be hit this year,” Wendy Chen, senior investment analyst at GAM Investments said in a note. “There are fears that the strengthening Chinese RMB, geopolitical conflict, as well as a potential recession in the US and developed markets, could result in less demand from overseas.”

Chinese state-owned firms pared gains after a call for better access to funding by the general manager of Shanghai Stock Exchange boosted stocks earlier. Most other markets were in positive territory, with India’s closed for a holiday. Australian stocks climbed after the nation’s central bank lifted interest rates in line with estimates and said it expects goods inflation to moderate in coming months. Energy stocks were the biggest sectoral gainers in Asia as oil broke above its 100-day moving average.

Japanese shares climbed ahead of commentary by Fed Chair Jerome Powell later Tuesday and the Bank of Japan policy meeting later this week. The Topix Index rose 0.4% to 2,044.98 as of market close Tokyo time, while the Nikkei advanced 0.3% to 28,309.16. Sony Group Corp. contributed the most to the Topix Index gain, increasing 1.3%. Out of 2,160 stocks in the index, 1,438 rose and 599 fell, while 123 were unchanged.

Australian stocks gained, the S&P/ASX 200 index rising 0.5% to close at 7,364.70, after Australia’s central bank signaled a pause in its tightening cycle after delivering a 25bps rate hike on Tuesday. “The monthly CPI indicator suggests that inflation has peaked,” RBA Governor Philip Lowe said in a statement. “Recent data suggest a lower risk of a cycle in which prices and wages chase one another.” The focus on services inflation in the central bank’s statement gives “a sop to the hawks, as does the tight labor market, but a reluctance to over-tighten into a real sector slowdown looks a key factor for the RBA in what is a slightly dovish communication,” Dwyfor Evans, head of APAC macro strategy at State Street Global Markets, wrote in a note. In New Zealand, the S&P/NZX 50 index was little changed at 11,919.56

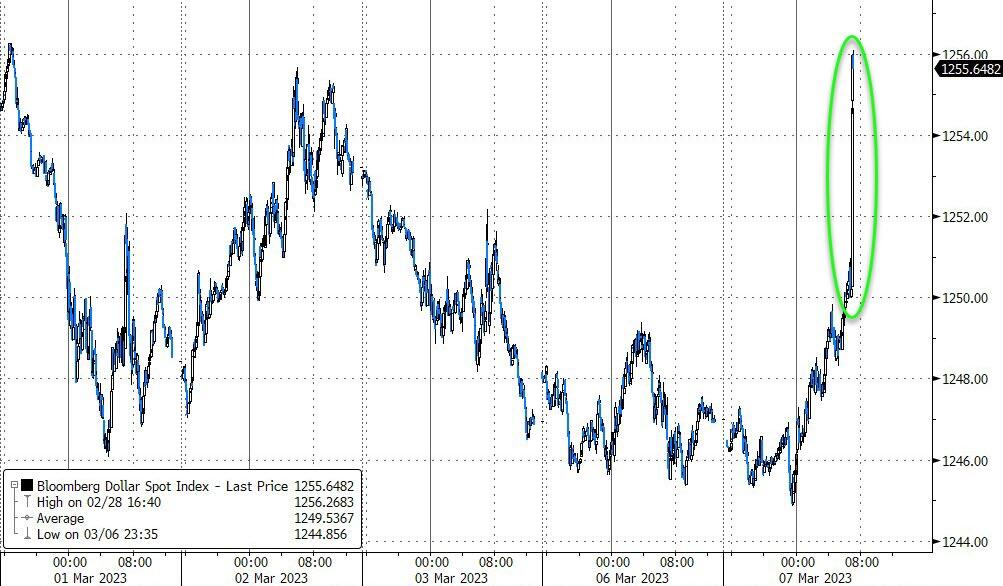

In FX, the Bloomberg Dollar Spot Index swung from a loss to a 0.1% gain as the greenback advanced against all of its Group-of-10 peers apart from the New Zealand dollar. The Australian dollar is the weakest among the G-10s, falling 0.9% versus the greenback after a dovish hike from the RBA.

- The euro fell 0.2% to $1.0664. Bunds advanced, led by the belly of the curve, and outperforming Treauries as traders eased tightening wagers after an ECB consumer survey shows inflation expectations decreased “significantly” to 2.5% for three years ahead

- The pound swung to a loss after BOE policy maker Catherine Mann said the pound could weaken further in the coming months as investors absorb the implication of the US Federal Reserve and European Central Bank’s plans to raise interest rates. Demand for low-delta exposure in cable remains in free-fall mode despite key risk events ahead. UK like-for-like retail sales climbed 4.9% from a year ago in February. It was well above the 12-month average of 1.6%

- The yen was steady while dollar-yen 1-week implied volatility jumped as much as 1.49 vol to 17.11, the highest in a month, before BOJ Governor Haruhiko Kuroda’s final policy meeting this week. Super-long government bonds fell after an auction drew subdued demand

- Australian dollar reversed a gain, to drop against all of its G-10 peers, after the RBA hiked rates 25 basis points as expected but said that it now believes inflationhas peaked. Sovereign bond yields flipped lower

Treasuries were richer across the curve, unwinding Monday’s losses and following wider gains across bunds and gilts during European morning. TSY yields are richer by 2bp-3bp with spreads little changed on the day; 10-year around 3.94%, with bunds and gilts outperforming by 3bp-5bp in the sector, supported by a significant drop in euro-area consumer inflation expectations. German 10-year yields are down 7bps while UK 10-year borrowing costs fall 76bps. Bunds rally extended after an ECB consumer survey found inflation expectations declined “significantly” to 2.5% for three years ahead. German yields richer by ~8bp across belly of the curve with gilts long-end richer by ~7bp. Treasury auction cycle begins with $40b 3-year new issue, followed by $32b 10- and $18b 30-year reopenings Wednesday and Thursday. WI 3-year yield at 4.565% is above auction stops since 2007 and ~50bp cheaper than February’s, which tailed by 4bp. Focal points of US session include Fed Chair Powell’s appearance before the Senate banking panel at 10am New York time and 3-year note auction at 1pm.

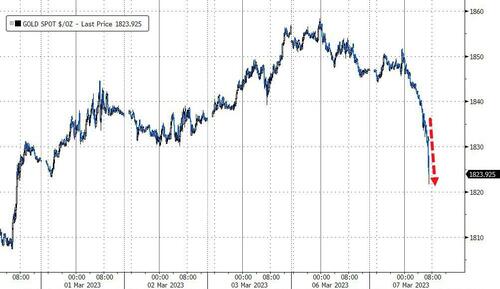

In commodities, crude futures decline with WTI down 0.2% to trade near $80.30. Spot gold falls roughly 0.2% to trade near $1,843.

To the day ahead now, and the main highlight will be Fed Chair Powell’s testimony before the Senate Banking Committee. Otherwise, data releases include German factory orders for January, and we’ll also get the ECB’s Consumer Expectations Survey.

Market Snapshot

- S&P 500 futures up 0.1% to 4,055.25

- STOXX Europe 600 up 0.2% to 465.32

- MXAP little changed at 162.31

- MXAPJ down 0.3% to 524.63

- Nikkei up 0.3% to 28,309.16

- Topix up 0.4% to 2,044.98

- Hang Seng Index down 0.3% to 20,534.48

- Shanghai Composite down 1.1% to 3,285.10

- Sensex up 0.7% to 60,224.46

- Australia S&P/ASX 200 up 0.5% to 7,364.65

- Kospi little changed at 2,463.35

- German 10Y yield little changed at 2.65%

- Euro down 0.2% to $1.0662

- Brent Futures down 0.2% to $85.97/bbl

- Gold spot down 0.1% to $1,845.90

- U.S. Dollar Index little changed at 104.39

Top Overnight News from Bloomberg

- Dovish Hike. Australia’s central bank signaled a pause in its 10-month tightening cycle is in prospect, prompting a selloff in the currency after policymakers delivered an expected interest-rate increase on Tuesday. The Reserve Bank lifted its cash rate by a quarter-percentage point to 3.6%, the highest level since May 2012. Governor Philip Lowe said in his statement that in assessing “when and how much further” rates need to go up, the RBA will pay close attention to incoming economic data. Meanwhile Jerome Powell’s testimony will be scoured for views on the economic outlook, specifically inflation, wage pressures and employment, as well as clues on the Fed’s rate path. Any dovishness may spark aggressive short-covering in short-dated Treasuries. BBG

- China’s trade numbers for Jan & Feb are mixed, with exports falling 6.8% YTD (vs. the St -9%) while imports drop 10.2% YTD (vs. the St -5.5%). WSJ

- Conventional wisdom says the US will avoid a devastating federal payments default later this year. But conventional wisdom has proved spectacularly wrong months ahead of shocks that upended the world in recent years: the failure of Lehman Brothers, the 2016 US election, the global spread of Covid-19. BBG

- President Xi Jinping sought to rally China’s private sector to help overcome “containment” by the US and other countries, in rare direct criticism of the nation’s biggest trading partner. BBG

- Japan wage numbers fall short of the St forecast, rising only 0.8% Y/Y in Jan (vs. the St forecast of +1.8% and down from +4.1% in Dec). RTRS

- Philippines witnessed modest disinflation in Feb, with the CPI coming in at +8.6% (down from +8.7% in Jan and below the St’s +8.9% forecast). RTRS

- Taiwan witnessed disinflation in Feb, with the CPI coming in at +2.43% (down from +3.04% in Jan and below the St’s +2.65% forecast) while the PPI fell to +4.1% (down from +5.61% in Jan). BBG

- Thailand’s CPI witnessed disinflation in Feb, with the headline number coming in at +3.79% (down from +5.02% in Jan and below the St’s +4.1% forecast). BBG Inflation expectations drop in latest ECB survey, a development likely to bring some comfort to Lagarde and her colleagues ahead of next week’s meeting. ECB

- White House will propose a plan to raise taxes on Americans earning more than $400K annually while cutting what Medicare pays for drugs in a bid to put the health program on a more sustainable fiscal footing. NYT

- Meta will lay off thousands of employees this week, people familiar said. The move is driven by financial targets and is on top of the 11,000 jobs slashed in November. The plan is being finalized before Mark Zuckerberg goes on parental leave for his third child, which may be imminent. BBG

- German factory orders rose 1% in January from the previous month, compared with a 0.7% decline predicted in a Bloomberg survey. The jump was due to capital goods, particularly aircraft and spacecraft construction and motor vehicle engines. BBG

- Greece’s central bank governor Yannis Stournaras expects the country to regain its investment-grade credit rating within months, he told the Financial Times in an interview. BBG

A more detailed look at global markets courtesy of newsquawk

Asia-Pac stocks traded mostly higher although gains were capped as participants digested the latest Chinese trade data and with cautiousness ahead of Fed Chair Powell’s testimony in Congress. ASX 200 pared losses after the RBA rate decision where it hiked rates as expected but provided a slightly less hawkish tone in which it noted the Board expects further tightening of monetary policy will be needed which was a subtle tweak from its prior guidance that the Board expects further increases in interest rates will be needed, while it also noted that monthly CPI suggests inflation seems to have peaked. Nikkei 225 shrugged off the early weakness to trade marginally higher in the aftermath of the softer-than-expected labour earnings data including the largest decline in real wages since May 2014 which reduces the likelihood of a sooner exit from the BoJ’s ultra-easy policy. Hang Seng and Shanghai Comp. were choppy amid mixed Chinese trade data which showed a continued contraction in both dollar-denominated exports and imports, while it was also reported that the White House is considering pushing Congress on dealing with TikTok and that US Senators will announce a bill to comprehensively address the ongoing threat posed by technology from foreign adversaries.

Top Asian News

- China’s State Councillor says they are to establish a national financial regulatory administration, to advance the reform of PBoC branches; to downsize staff of central-level state institutions by 5%. Deepen reform of local financial regulatory system. To abolish the China Banking and Insurance Regulatory Commission, regulator to become an agency directly under state council.

- China’s Housing Minister says full of confidence in the stabilisation and rebound in China’s property market; says confidence among market players is recovering. The resumption rate of many housing project has been greatly improved.

- Chinese President Xi condemned US-led suppression of China, according to state media cited by AFP.

- Chinese Foreign Minister Qin Gang said US perception of China has seriously deviated and that the US thinks China is its main rival. Qin also stated that US so-called competition means containing and suppressing China, while he warned there will be conflict and confrontation if the US does not change its path but also stated that China is committed to promoting healthy and stable development of China-US relations, according to Reuters.

- Taiwan’s Defence Minister Chiu said he is not aware of President Tsai meeting with US House Speaker McCarthy but added that if China makes a move, the military’s role is to fight. Chiu added that they don’t expect it to happen, but will not allow repeated provocations from China.

- US Senators Warner and Thune are to announce a bill on Tuesday that will comprehensively address the ongoing threat posed by technology from foreign adversaries such as TikTok. In relevant news, the German government plans to ban telecom operators from using certain components of Huawei and ZTE in 5G networks.

- RBA hiked rates by 25bps to 3.60%, as expected, while the Board remains resolute in its determination to return inflation to the target and expects further tightening of monetary policy will be needed which was a slight tweak from its previous guidance that the Board expects that further increases in interest rates will be needed, while it also noted that monthly CPI suggests inflation seems to have peaked. Furthermore, the RBA said growth in the Australian economy has slowed and the labour market remains very tight, although conditions have eased a little and that uncertainties mean that there is a range of potential scenarios for the Australian economy.

European bourses are contained, Euro Stoxx 50 +0.1%, and reside in contained ranges ahead of Fed Chair Powell. Sectors are mostly in the green, though the breadth of performance is narrow given the above. Stateside, futures are also in close proximity to the unchanged mark though they do have a slight upward-bias pre-Powell as yields ease; NQ +0.3%.

Top European News

- Barclays said UK February consumer spending rose 5.9% Y/Y which was hit by a reduction in non-essential spending and higher food prices, while the sales growth was also affected by comparison to the base as there was a spike in spending in February 2022 after COVID restrictions were lifted.

- ECB Consumer Expectations Survey: Inflation Expectations: 4.9% 12-months ahead (Dec 5.0%); Nominal Income: 1.3% over the next 12-months (Dec +1.0%); Nominal Spending: 3.8% over the next 12-months (Dec +4.2%)

- ECB’s Stournaras says he is confident that credit rating agencies will upgrade Greece’s bonds within months. Elsewhere, Stournaras would not pre-commit to specific further rate increases amid a backdrop of headline inflation declining; saying, it could increase rather than limit market confusion. (FT)

- ECB’s de Cos says core inflation is to remain elevated in the short term, and thereafter ease gradually.

- BoE’s Mann says more needs to be done with rates. Weak GBP is significant for inflation; could be more to go in terms of how much is priced into GBP.

- Riksbank’s Thedeen says wants to see a stronger SEK; there is not a strong argument that the SEK should be weak or weaker because of the housing market. Underlying inflation has not turned, and is still too high.

- TotalEnergies’ (TTE FP) Gonfreville refinery (240k BPD) is completely blocked; Exxon’s (XOM) Port Jerome (270k BPD) and Fos Sur Mer (140k BPD) refineries are on strike, via the union. Subsequently, TotalEnergies says there is no shortage of fuel within its gas stations, reserves at a high level.

FX

- The DXY continues to inch higher, but has seemingly hit a ceiling at 104.50 before Monday’s 104.69 best, with peers mostly contained/slightly softer vs USD pre-Powell.

- Though, AUD bucks-the-trend and is markedly softer after the RBA hiked by 25bp and tweaked its accompanying statement, which has been taken as a dovish-adjustment by markets; AUD/USD at the lower-end of 0.6669-0.6747 parameters.

- GBP and JPY are little changed despite familiar hawkish remarks from BoE’s Mann and a further easing of UST yields respectively; Cable holding at 1.20, where the 100-DMA resides, while USD/JPY has pulled back from a brief breach of 136.00.