MARCH 8/GOLD CLOSED DOWN $1.15 TO $1814.70//SILVER CLOSED DOWN 6 CENTS TO $20.09//PLATINUM CLOSED UP $5.45 WHEREAS PALLADIUM CONTINUES ON ITS DOWNWARD SPIRAL CLOSING DOWN $12.50 TO $1381.50//COVID UPDATES: DR PAUL ALEXANDER//DR PANDA//VACCINE IMPACT//SLAY NEWS//IMPORTANT COMMENTARIES TODAY: 1.MATHEW PIEPENBERG (PLIGHT OF CALIFORNIA AND THE USA AND 2.ZERO HEDGE DISCUSSING THE PLIGHT OF CHINA’S FINANCES// 3.DR SCOTT ATLAS//TWO OF TAIWANS UNDERSEA CABLES CUT BY MAINLAND CHINA AND THIS DOES NOT BODE WELL FOR TAIWAN//UKRAINE VS RUSSIA: EASTERN SECTION OF BUKHMAT NOW IN RUSSIAN HANDS//FRANCE UNDERGOES ANOTHER HUGE PROTEST WHICH BASICALLY SHUTS DOWN THE COUNTRY//REPUBLICAN SENATORS DEMAND DOCUMENTS ON INTELLIGENCE COMMITTEE’S COVID ORIGIN//SWAMP STORIES FOR YOU TONIGHT//VC FUNDS SEE MASS EXTINCTION IN 2023//

118 C MACQUARIE FUT 101 363 H WELLS FARGO SEC 91 435 H SCOTIA CAPITAL 321 624 C BOFA SECURITIES 1 624 H BOFA SECURITIES 307 657 C MORGAN STANLEY 5 661 C JP MORGAN 41 726 C CUNNINGHAM COM 2 737 C ADVANTAGE 20 4 880 C CITIGROUP 1 905 C ADM 2 2

TOTAL: 449 449 MONTH TO DATE: 2,618

JPMORGAN stopped 41/449 contracts

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR MAR/2023. CONTRACT: 449 NOTICES FOR 0 OZ or 1.3965 TONNES

total notices so far: 2618 contracts for 261,800 oz (8.1368 tonnes)

SILVER NOTICES: 35 NOTICE(S) FILED FOR 175,000 OZ/

total number of notices filed so far this month : 2892 for 14,440,000 oz

END

GLD

WITH GOLD DOWN $1.15

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD////A HUGE WITHDRAWAL OF 5.5 TONNES FORM THE GLD

INVENTORY RESTS AT 906.62TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 6 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 459,000 OZ FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 477.684. MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY AN ATMOSPHERIC SIZED 5101 CONTRACTS TO 127,503 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE MONSTROUS SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR HUGE $0.88 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR NEW LOW COMEX OI SILVER WAS SET AT 121,299 MARCH 3/2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.88). BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS, AS WE HAD A PLANETARY GAIN ON OUR TWO EXCHANGES 5826 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 1 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD: A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS( 725 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.58 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE JUMP OF 115,000 OZ//NEW STANDING: 14.860 MILLION OZ + THE 1.0 MILLION OZ OF EXCHANGE FOR RISK//THUS TOTAL NEW STANDING 15.860 MILLION OZ/ //// V) COLOSSAL SIZED COMEX OI GAIN/ STRONG SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –225 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTRACTS for 6 days, total 2426 contracts: OR 12.130 MILLION OZ . (485 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 12.130 MILLION OZ

.

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 8.505 MILLION OZ//INITIAL

RESULT: WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 5101 DESPITE OUR $0.88 LOSS IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 725 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAR OF 15.58 MILLION OZ FOLLOWED BY TODAY’S 110,000 QUEUE JUMP (WHICH INCREASES THE AMOUNT OF SILVER STANDING) + 1.0 MILLION OF EXCHANGE FOR RISK ISSUED EARLY IN MARCH (INCREASES THE AMOUNT OF SILVER STANDING) //NEW STANDING 15.855 MILLION OZ .. WE HAVE A MONSTROUS SIZED GAIN OF 5826 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 35 NOTICE(S) FILED TODAY FOR 175,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A COLOSSAL SIZED 17,020 CONTRACTS TO 458,474 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 345 CONTRACTS.

.

WE HAD A GIGANTIC SIZED INCREASE IN COMEX OI ( 17,020 CONTRACTS) DESPITE OUR HUGE $33.20 LOSS IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR MAR. AT 4.9953 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 44,500 OZ (1.384 TONNES) //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S ) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London).

YET ALL OF..THIS HAPPENED WITH OUR $33.20 LOSS IN PRICEWITH RESPECT TO TUESDAY’S TRADING

WE HAD AN ATMOSPHERIC SIZED GAIN OF 21,473 OI CONTRACTS (66.79 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4453 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 458,474

IN ESSENCE WE HAVE A MONSTROUS INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 21,473 CONTRACTS WITH 17,020CONTRACTS INCREASED AT THE COMEX AND 4453 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 21,473 CONTRACTS OR 67.863 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4453 CONTRACTS) ACCOMPANYING THE MONSTROUS SIZED GAIN IN COMEX OI (17,020) TOTAL GAIN IN THE TWO EXCHANGES 21,473 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR MAR. AT 4.9953 TONNES FOLLOWED BY TODAY’S 44,500 OZ QUEUE JUMP//NEW STANDING 8.345 TONNES // ///3) ZERO LONG LIQUIDATION //4) COLOSSAL SIZED COMEX OPEN INTEREST GAIN// 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

TOTAL EFP CONTRACTS ISSUED: 19,022 CONTRACTS OR 1,902,200 OZ OR 59.166 TONNES 6 TRADING DAY(S) AND THUS AVERAGING: 3170 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 6 TRADING DAY(S) IN TONNES 59.166 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 59.166/3550 x 100% TONNES 1.66% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 59.166 TONNES/INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A GIGANTIC SIZED 5101 CONTRACTS OI TO 127,503 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A RECORD LOW OF 121,299 CONTRACTS MARCH 3/2023.

EFP ISSUANCE 725 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 725 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 725 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 5101 CONTRACTS AND ADD TO THE 725 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A MONSTER GAIN OF 5826 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES //29.130 MILLION OZ

OCCURRED DESPITE OUR $0.88 LOSS IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED DOWN 1.85 PTS OR 0.06% //Hang Seng CLOSED DOWN 483.23 PTS OR 2.35% /The Nikkei closed UP 135.43% PTS OR 0.48% //Australia’s all ordinaries CLOSED DOWN 0.78% /Chinese yuan (ONSHORE) closed DOWN 6.9591//OFFSHORE CHINESE YUAN DOWN TO 6.9638// /Oil DOWN TO 77.19 dollars per barrel for WTI and BRENT AT 83.08 / Stocks in Europe OPENED MOSTLY MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY AN OUTER SPACED SIZED 17,020 CONTRACTS UP TO 458,474 DESPITE OUR GIGANTIC LOSS IN PRICE OF $33.20. THIS ABSOLUTELY DOES NOT MAKE SENSE

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAR… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4453 EFP CONTRACTS WERE ISSUED: : APRIL 4453 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4453 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: AN ATMOSPHERIC SIZED TOTAL OF 21,473 CONTRACTS IN THAT 4453LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD AN UNBELIEVABLY SIZED COMEX OI GAIN OF 17,020 CONTRACTS..AND THIS MONSTROUS SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR HUGE LOSS IN PRICE OF $33.20. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAR (8.345) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 8.345 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $33.20) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR MONSTROUS SIZED GAIN OF 21,818 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 66.79 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAR. (4.9953 TONNES) FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 44,500 OZ (1.384 TONNES)… ALL OF THIS WAS ACCOMPLISHED DESPITE OUR HUGE FALL IN PRICE TO THE TUNE OF $33.20

WE HAD -345 CONTRACTS REMOVED FROM COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 21,473 CONTRACTS OR 2,147,300 OZ OR 66.79 TONNES

Estimated gold comex today 257,855// //fair

final gold volumes/yesterday 298,127/// fair to good

Total monthly oz gold served (contracts) so far this month

2618 notices 261,800 8.1368 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i) Into Brinks: 32.15 oz

(one kilobar)

total deposits: 32.15 oz

customer withdrawals: 0

total withdrawals: nil oz

in tonnes: 2 tonnes

Adjustments; 3

2 customer to dealer

i) Brinks: 1060.983 oz

ii) HSBC: 11,477.907 oz

and one dealer to customer JPMorgan:

i) 64,334.151 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of MARCH we have an oi of 514 contracts having GAINED 444 contracts. We had 0 notices filed on Tuesday so we

gained another 445 contracts or an additional 44,500 oz will stand for metal at the comex

April lost 6182 contracts down to 312,165 contracts

May gained 20 contracts to stand at 117

We had 449 notice(s) filed today for 44900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 449 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 41 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAR. /2023. contract month,

we take the total number of notices filed so far for the month (2618 x 100 oz ), to which we add the difference between the open interest for the front month of (MAR. 514 CONTRACTS) minus the number of notices served upon today 449 x 100 oz per contract equals 268300 OZ OR 8.345 TONNES the number of TONNES standing in this active month of MARCH.

thus the INITIAL standings for gold for the MAR contract month:

No of notices filed so far (2618 x 100 oz+ 514 OI for the front month minus the number of notices served upon today (449)x 100 oz} which equals 268,300 oz standing OR 8.345 TONNES in this active delivery month of MARCH..

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 2892 x 5,000 oz = 14,440,000 oz

to which we add the difference between the open interest for the front month of MAR(115) and the number of notices served upon today 35 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAR./2023 contract month: 2892 (notices served so far) x 5000 oz + OI for the front month of MAR (115) – number of notices served upon today (35) x 500 oz of silver standing for the MAR. contract month equates 14.860 million oz +the 1.0 million oz of exchange for risk//new total standing 15.860 million oz

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

FEB 28/WITH GOLD UP $12.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 917.61 TONNES

FEB 27/WITH GOLD UP $6.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.32 TONNES

FEB 24/WITH GOLD DOWN $9.10 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 917.32 TONNES

FEB 23/WITH GOLD DOWN $13.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 919.92 TONNES

FEB 22/WITH GOLD DOWN 22 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 919.92 TONNES

FEB 21/WITH GOLD DOWN $7.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 919.92 TONNES

FEB 17/WITH GOLD DOWN $1.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 921.08 TONNES

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

GLD INVENTORY: 906.62 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWALOF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

FEB 28/WITH SILVER UP 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.241 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.188

FEB 27/WITH SILVER DOWN 15 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.471 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 482.429 MILLION OZ

FEB 24/WITH SILVER DOWN 46 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.172 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.900 MILLION OZ//

FEB 23/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.379 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.072 MILLION OZ//

FEB 22/WITH SILVER DOWN 22 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ FROM THE SLV////INVENTORY RESTS AT 485.693 MILLION OZ

FEB 21/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.5363 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 486.382 MILLION OZ//

FEB 17/WITH SILVER UP 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 827,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.819 MILLION OZ/

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 477.684 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

Central bank gold buying is relentless. Even city state powerhouse Singapore bought 45 tonnes in January

(Schiffgold)

Central Bank Gold Buying Takes Up Where It Left Off To Start 2023

Central banks globally added another net 77 tons to their gold reserves in January, according to the latest data compiled by the World Gold Council.

It was a 192% month-on-month increase from December and above the 20-60 ton range of reported purchases we’ve seen over the last 10 consecutive months of net buying.

A late report of a 45-ton gold purchase by Singapore in January bumped the numbers up from the initially reported 31 tons.

The Central Bank of Turkey was the biggest buyer in 2022 and continued to add gold to its reserves with another 23-ton purchase in January. Turkey now holds 565 tons of gold.

The country has been battling rampant inflation. Price inflation accelerated to as high as 85% last year and was at 64% in December. The Turkish lira depreciated by almost 30% last year. Meanwhile, the price of gold in lira terms increased by 40% on an annual basis, according to Bloomberg.

China reported another 14.9-ton increase in its gold reserves on top of the 62 tons reported between November and December 2022.

The Chinese central bank accumulated 1,448 tons of gold between 2002 and 2019, and then suddenly went silent until it resumed reporting in November 2022. Many speculate that the Chinese continued to add gold to its holdings off the books during those silent years.

There has always been speculation that China holds far more gold than it officially reveals. As Jim Rickards pointed out on Mises Daily back in 2015, many people speculate that China keeps several thousand tons of gold “off the books” in a separate entity called the State Administration for Foreign Exchange (SAFE).

The European Central Bank reported a nearly 2-ton increase in its gold holdings in January. According to the WGC, this was related to Croatia joining the eurozone.

The National Bank of Kazakhstan increased its gold reserves by a modest 3.9 tons in January after selling over 30 tons in November and December.

The only prominent seller in January was Uzbekistan with a 12-ton decrease in gold reserves.

It is not uncommon for banks that buy from domestic production – such as Uzbekistan and Kazakhstan – to switch between buying and selling.

The World Gold Council projects that central banks will continue to buy gold through 2023, but it’s not unreasonable to expect that the rate of buying won’t match the record level of 2022.

Looking ahead, we see little reason to doubt that central banks will remain positive towards gold and continue to be net purchasers in 2023. However, by how much is difficult to call, as evidenced by our expectations at the start of 2022. But it is also reasonable to believe that central bank demand in 2023 may struggle to reach the level it did last year.”

Total central bank gold buying in 2022 came in at 1,136 tons. It was the highest level of net purchases on record dating back to 1950, including since the suspension of dollar convertibility into gold in 1971. It was the 13th straight year of net central bank gold purchases.

According to the World Gold Council, there are two main drivers behind central bank gold buying — its performance during times of crisis and its role as a long-term store of value.

It’s hardly surprising then that in a year scarred by geopolitical uncertainty and rampant inflation, central banks opted to continue adding gold to their coffers and at an accelerated pace.”

World Gold Council global head of research Juan Carlos Artigas told Kitco News that the big purchases underscore the fact that gold remains an important asset in the global monetary system.

“Even though gold is not backing currencies anymore, it is still being utilized. Why? Because it is a real asset,” he said.

END

Solar energy production could require most of the global silver reserves by 2050

(Michael Maharrey/SchiffGold)

Solar Energy Production Could Require Most Of The Global Silver Reserves By 2050

Silver demand was at record levels in 2022 and there is reason to believe it will continue to run hot over the next several decades. One reason is the rapidly increasing demand for silver in the green energy sector. In fact, an Australian study projects solar cells may use most of the world’s silver reserves by 2050.

Due to its outstanding electrical conductivity, silver is an important element in the production of solar panels. It is used to conduct electrical charges out of the solar cell and into the system. Each solar panel only uses a small amount of silver, but with the demand for solar panels growing exponentially every year, those small amounts of silver add up.

According to a research paper by scientists at the University of New South Wales, solar manufacturers will likely require over 20% of the current annual silver supply by 2027. And by 2050, solar panel production will use approximately 85–98% of the current global silver reserves.

According to data from the Silver Institute, silver offtake for photovoltaics reached a record 113.7 million ounces in 2021. That compares to only 50.5 million ounces in 2013. Final figures aren’t in for 2022, but analysts estimate solar panel production used about 127 million ounces of silver last year.

The paper also noted that more efficient ‘N-type’ technologies now being developed require even more silver than current ‘PERC’ cells that make up more than 80%of the current market.

Some argue demand for silver in solar energy production will eventually flatten as the industry develops cheaper alternatives to the white metal. But according to the paper, even if the industry reduces the use of silver, demand will still increase.

The results show that the current rate of reduction in silver consumption is not sufficient to avoid increasing silver demand from the PV industry and that the transition to high-efficiency technologies including TOPCon (a more advanced N-type silicon cell technology, first scaled in 2019) and SHJ (Silicon heterojunction solar cells, which are very efficient) could greatly increase silver demand, posing price and supply risks.”

Silver possesses the lowest electrical resistance among all metals at standard temperatures. According to a Saxo Bank report in 2020, “Potential substitute metals cannot match silver in terms of energy output per solar panel.”

Further, due to technical hurdles, non-silver PVs tend to be less reliable and have shorter lifespans, presenting serious issues for their widespread commercial development.”

The study said recycling silver also won’t significantly dent supply issues.

Over the longer term, the recycling of older solar modules could provide a significant source of silver. However, further investment and research is needed here, and it may still be several decades before the volume of PV waste processed each year is enough for more than a marginal contribution of new silver.”

In the fall of 2021, Australia, France, India, the US, and the UK announced the launch of the “One Sun, One World, On-Grid” initiative. The plan is to connect solar energy grids across borders. This could provide a big boost to silver demand.

With billions of government money pouring into renewable energy, the solar industry is somewhat shielded from economic downturns. Even if the economy goes south, governments will continue to fund solar projects and other green energy initiatives. This means the green energy sector will likely drive demand for silver into the foreseeable future.

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

Mathew Piepenburg

This is a good piece: California’s spending is now out of control compared to its tax revenue. The tech layoffs are killing the state

(Mathew Piepenburg)

California Dreaming – State Metaphor for a Failing Nation

Matthew Piepenburg March 8, 2023

Below we consider the State of California as the metaphor of a failed state as well as the failing state of the American Union, which is anything but a dream.

Metaphors

For those already familiar with my articles, interviews or even daily banter, I have an admitted affinity for metaphors and analogies, as they help draw the simple from the complex.

As for politicians and political issues, there is always the risk of partisan bias and offending those who cling to only one perspective.

Fortunately, my take on the left or the right of current politics is fairly agnostic, as I view nearly all politicos as crooked as a dog’s hind leg.

Thus, as I turn my lens toward the state of California and its failed governor, I hope readers of the left or right can dispense with politics and just stick to math so that we can all get past the swamp of red vs. blue opinions and respect the objective facts of red vs. black balance sheets.

And when it comes to the State of California, she’s deeply in the red, and serves, ironically, as yet another broader yet applicable metaphor of the world economy in general and the United States in particular.

So, let’s dig in.

California Dreaming?

Oh, how I have loved California. It is home to some wonderful personal memories as well as personal wipeouts—and not just the surfing kind.

Its sunny appeal, however, is universally seductive, and like that famous Eagles song, one indeed feels like you can check in any time you’d like, but you can never really leave California’s tempting horizons and mythical spell where dreams come true.

Nevertheless, folks are leaving California, and have been doing so to the tune of over 500,000 exits in the last 2 years alone.

Why?

For those on the political right, California’s big-headed Gavin Newsom is an easy target.

His over-the-top COVID hysteria (similar to other failed experiments in Seattle, Chicago or Portland…) and unsustainable tax policies coupled with San Francisco’s soft-on-crime nightmare (car-jacking capital) and L.A.’s recent fall from City of Dreams to Tent City are all classic symbols of a failed state.

I once lived on this beach…

But let’s leave that issue, debate and fall to the woke, the left, the right, the angry and the smug.

For me, the math of California (whose nominal GDP ranked as the 5th largest in the world) makes the discussion far easier to sift through.

The Hard Reality of Simple Math

Like nearly all cornered politicians, Newsom is driven by obfuscating the obvious and trivializing the momentous (Chicago’s recently failed mayor of the nation’s “murder capital” comes to mind…).

For example, his January projected budget deficit of $22.5B (an already embarrassing figure which he nevertheless tried to downplay) was in fact off.

Way off.

It turns out that even Newsom’s “sunny” forecast and optimistic math had overlooked a few pesky facts.

First, the state’s monthly tax revenue for January was almost $14B less than the revenue for the month prior.

Secondly, California’s fiscal year, which started last July, is moving at a pace of $23B in less income than the previous year.

In short: California’s income stream is running toward an emptiness equivalent to Newsom’s IQ, despite sunsets as consistent as his immaculate wardrobe and “Hollywood” smile (smear?).

But as many Californian’s know—it’s not how things feel, but how they look which counts.

For the top income bracket, however, California’s tax bills (and revenues) aren’t looking good.

Even those wealthy and beautiful (from Topanga to Belvedere Island) are starting to squirm under a state tax structure that feels and looks anything but “dreamy.”

State tax for Californians earning over $1M is 13.3%, and the top 0.5% of California’s tax payers are responsible for over 40% of the state’s total tax income.

Many, of course, are getting sick of paying taxes for increasingly expensive sunsets, even from Orange County’s row of waterfront mic-mansions.

Furthermore, for those wealthy left-coasters who’ve lost their jobs or capital gains at Google, Amazon, Facebook and countless other Silicon Valley enterprises of late, that tax income is openly drying up, which means so are the state’s revenues.

“screw your freedom,” suggesting that the unvaccinated were all anti-science “schmuks… “

What a guy. What a dream.

But had some of Cali’s former leaders indeed studied any form of economics, they’d likely understand that rising deficits and falling revenues is the opposite of a dream—it’s the historically-confirmed prelude to a nightmare.

Even the once-reliable WSJ has confessed that California’s budget has imploded and that January revenues are poised to be down by 40% y/y.

Uh-oh?

One wonders how long the top 0.5% of California will want (or be able) to pay that ever-increasing bill as profits in their tech-heavy portfolios creep ever closer toward a cliff steeper than Malibu’s Point Dume.

California as Metaphor

Unfortunately, California’s embarrassing combination of tanking revenues, increased spending and expanding deficits is not happening in a vacuum.

In fact, California serves as a mirror to a broader problem within the United States as whole (or debt hole) …

Like the failed state of California, the equally failed state of the US government has a problem with incoming tax revenues, an issue I’ve been tracing throughout 2022.

Like the Californian wealthy 0.5%, the wealthy 1% of the United States taken collectively are the ones paying 40% of the national taxes.

And like California’s wealthy in general, the nation’s wealthy in particular get a lot of that wealth from a bubbling risk asset market whose best days are largely behind us and whose worst days (and hence weaker capital gain receipts) are still ahead.

In short, and like California, the United States is facing less tax revenues combined with greater deficits and increased spending, making the Cali crisis a leading indicator of a national crisis.

Uncle Sam’s bar tab (i.e., True Interest Expense) returns to Covid crisis/pain levels reminiscent of a seemingly forgotten yesterday:

In other words, the United States (along with California…) are mathematically heading toward a bar-tab (i.e., interest expense bill) as painful as the one we saw in March of 2020, when markets tanked and the Fed was required to print trillions in less than 8 months just to keep Uncle Sam’s nose (and Treasury market) above water.

For now, however, the Fed is not printing trillions via QE, but tightening ala QT.

Or stated more simply, US debt obligations are sailing toward yet another debt iceberg, only now the issue is not about too few lifeboats, but no life boats at all.

As I see it, and have said many times prior, the US is trapped with no easy solutions as debt levels are rising and revenues falling.

The end result is obvious, even if the precise timing of the iceberg is not.

Whether Powell’s Fed continues to tighten into a debt iceberg, or eventually seeks to temporary melt (monetize) that iceberg with more QE, the nation is doomed either way in a Hobbesian choice between tanking markets (QT-driven) or skyrocketing inflation (QE-driven).

debt elephant in the room–and all that this toxic debt inevitably implies.

Once debt levels become fatal, the direction of credit, stock, property and finally currency markets are easy to diagnosis, though the time of death is not.

Gold, of course, loves dying currencies.

The price of gold today, or the strength or weakness of the USD tomorrow, are frankly silly questions in the short term for any who understand the broader context of the long-term.

Currencies are always the last bubble to pop, and given that gold is a store of value rather than an instrument of speculation, gold investors (i.e., those whose aim is wealth preservation not asset speculation) recognize that gold never rises, currencies just fall.

Investors in physical gold therefore measure their wealth in ounces, grams and kilos, not highly toxic, increasing debased and (forever debated) fiat currencies whose race to the bottom is literally happening right before our eyes in real time.

To dismiss such simple deductions from admittedly complex market forces as just “gold bug” thinking ignores math, history and gold cycles.

But again, no one likes to see bears, even when they’re staring at them from the Californian state Capital.

END

3. Chris Powell of GATA provides to us very important physical commentaries//

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 6.9591

OFFSHORE YUAN: 6.9638

SHANGHAI CLOSED DOWN 1.85 PTS OR 0.06%

HANG SENG CLOSED DOWN 483.23 PTS OR 2.35%

2. Nikkei closed UP 135.43 PTS OR 0.48%

3. Europe stocks SO FAR: MOSTLY MIXED

USA dollar INDEX UP TO 105.62 Euro FALLS TO 1.0545 DOWN 4 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.496!!(Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 137.26/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.6760%***/Italian 10 Yr bond yield RISES to 4.4870%*** /SPAIN 10 YR BOND YIELD RISES TO 3.700…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.4780//(ITALY WORSE THAN GREECE?)

3j Gold at $1813.00//silver at: 20.08 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 0/100 roubles/dollar; ROUBLE AT 76.02//

3m oil into the 77 dollar handle for WTI and 83 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 136.15/10 YEAR YIELD AFTER BREAKING .54%, LOWERS TO .4960% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9425–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9939well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

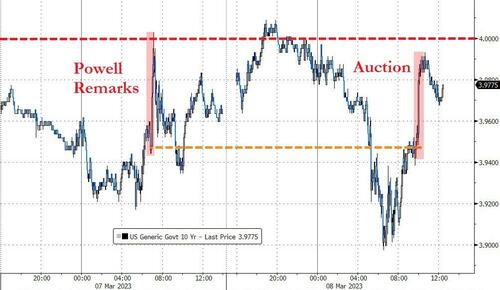

USA 10 YR BOND YIELD: 3.972% DOWN 0 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.875 DOWN 1 BASIS PTS//INVERTED TO THE 10 YEAR!!

USA 2 YR BOND YIELD: 5.0405 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,94…

GREAT BRITAIN/10 YEAR YIELD: 3.8305% UP 1 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Rebound After Powell-Inspired Rout

WEDNESDAY, MAR 08, 2023 – 08:06 AM

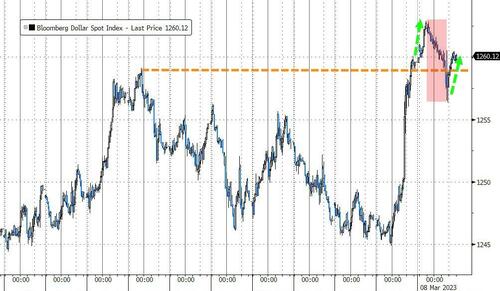

US stock futures were muted on Wednesday, swinging between modest gains and losses, one day after a market rout was sparked by yesterday’s warning from Fed Chair Jerome Powell that the pace of interest-rate increases may need to re-accelerate. S&P 500 futures down up 0.1% by 7:45 a.m. ET while Nasdaq futures were modestly in the green, showing marginal improvements in investor sentiment after Tuesday’s selloff, when the S&P 500 suffered the biggest decline in two weeks. The Bloomberg Dollar Spot Index was little changed near the highest in more than two months, as treasury yields climbed across the curve, pulling global bond markets along with them. Oil was flat while gold and Bitcoin fell extended their fall.

In US premarket movers, Crowdstrike rose after the cybersecurity software company reported results and a forecast that beat expectations. WeWork shares also gained after Bloomberg News reported that the workspace rental company is in talks to raise hundreds of millions in capital to support the business. Meanwhile, Tesla dropped after Berenberg downgraded the electric vehicle maker to hold from buy, saying the shares now have less upside potential and more limited room for disappointment; also impacting Tesla was an AP report that the NHTSA had opened a probe for steering wheels that can fall off. Here are other notable premarket movers:

Edwards Lifesciences slides 2% after Wells Fargo cut the recommendation on the medical technology stock to equal-weight from overweight.

Maxeon Solar jumps 14.7% after the renewable energy equipment provider delivered 4Q results and a bullish first quarter forecast that beat estimates. Morgan Stanley analysts say margin and order improvements are happening quicker than expected.

Rigel Pharmaceuticals surges 32% after the biotech’s earnings per share and total revenue for the fourth quarter beat analyst estimates. While analysts said that Rigel’s update was in line with January’s pre-announcement, they were positive on the prospects for the company’s two lead commercial treatments, a leukemia drug and a treatment of thrombocytopenia.

Shoals Technologies Group falls 8% after an offering of 24.5m class A shares by holders priced at $24.70 via Morgan Stanley.

SoundHound AI shares fell 11% after the artificial intelligence company reported wider net losses for the fourth quarter.

WeWork shares gain 7% after the workspace rental company was said to be in talks to raise hundreds of millions in capital to support the business.

Zymeworks jumps 9% after the biotech company’s revenue for the fourth quarter beat estimates, with Stifel highlighting that net income was better than expected and that the development of the company’s esophagus cancer drug is on track.

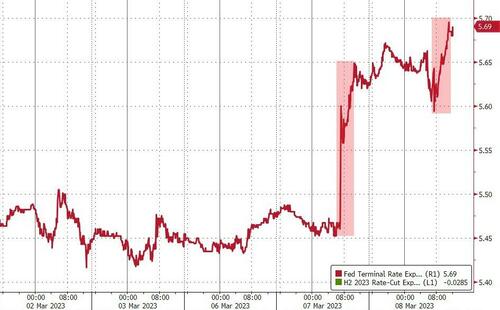

US stocks dropped on Tuesday after Powell said the ultimate level of interest rates is likely to be higher than previously anticipated after economic data came in stronger than expected. Powell speaks to Congress again later in the day, and for the March 21-22 Fed meeting futures trading suggests a 50 basis-point rate increase is more likely than 25 — the magnitude of the Fed’s last move, although JPMorgan’s Bob Michele says a Fed reversion to 50 bp hikes would be “pretty confusing.” Meanwhile, money markets are now pricing US interest rates to rise above 5.6% later this year.

“We would be foolhardy to expect we can’t reach 6% on Fed rates, and clearly that has an impact on asset markets across the globe,” Rabobank strategist Jane Foley told Bloomberg Television. If the Fed has to work harder to get inflation down, “that certainly does imply recession,” she added.

“The market now seems fairly convinced that there will be some sort of recession, but the employment data is still very strong,” said Roger Lee, head of UK equities at Investec Bank PLC. “There is this dilemma in the market; clearly recession risk is going up, because interest rate expectations are going up, but cyclicals have performed well this year, and that’s inconsistent with the yield inversion. There’s a tension there in the market causing a lot of uncertainty.”

Following the Tuesday selloff, the S&P 500 fell below 4,000, and a break below the 3,900 level can lead to an increase in selling pressure as this level has been a significant turning point for the US benchmark since May 2022, according to JPMorgan traders. It will all depend on the data, however: with US housing and employment data coming later today, and jobs data on Friday, investors will likely look to these as the next gage of probability for the path of interest rates. Meanwhile, rising US treasury yields are also putting further pressure on equities markets, with yield on the 2-year treasury note reaching 5% on Tuesday for the first time since 2007.

“In the US, bond yields versus S&P 500 yield are virtually the same, so equities look unattractive,” said Joachim Klement, strategist at Liberum Capital Ltd. “In the US, the risk premium for holding stocks has declined to levels seen around 2008, very low. Whereas in Europe, it is at levels pretty similar to 2015-16. That’s simply a reflection of the fact that Europe and UK haven’t hiked as aggressively as the US.”

European stocks were on course for a third consecutive decline following Fed Chair Jerome Powell’s hawkish message. The Stoxx 600 is down 0.3% with real estate, chemicals and utilities the worst-performing sectors. Here are the most notable European movers:

Adidas shares drop as much as 2.4% after the sportswear maker slashed its dividend, missing analyst estimates, with analysts also disappointed by the lack of firm medium-term targets

Darktrace shares fall 7.1% at London open after the UK cybersecurity firm, under attack by short seller Quintessential Capital Management, reduced forecast for free cash flow

Thales shares drop as much as 3.7% after the French defense company’s fourth-quarter earnings, with strong free cash flow offset by weaker guidance for cash in 2023

London Stock Exchange Group falls as much as 2.6% after Blackstone, Thomson Reuters and other investors sold about $2 billion of shares at a discount

Geberit shares fall as much as 4.5% after it reported a 4Q Ebitda that Morgan Stanley called “a touch light,” saying that destocking challenges at wholesalers are reduced but ongoing

Admiral drops as much as 9.4%, reaching its lowest in four months, after delivering results which analysts say show headwinds in motor insurance similar to its peers

Restaurant Group slumps as much as 14% after results from the Wagamama parent that analysts said were largely in line with expectations

Legal & General shares fall as much 2.2% as Morgan Stanley highlighted frailty in the UK financial services firm’s underlying full-year earnings, even as solvency looks robust

Fincantieri plunges as much as 9.3%, the most intraday since July 27, after the Italian shipbuilder released full-year results and an outlook for 2023 that came in below expectations

Continental shares gain as much as 7.4% after the German auto-parts maker projected an adjusted Ebit margin of about 5.5% to 6.5% for this year, an improvement from the 5% it reported in 2022

TeamViewer rises 3.4% after Kepler Cheuvreux upgrades, citing improving free cash flow outlook as the software company is set to end sponsorship for Manchester United football club

Quilter shares jump as much as 6.7%, the most in more than three months, after the wealth management firm reported full-year results that analysts said were stronger than anticipated

Sanford C. Bernstein strategists led by Sarah McCarthy said that while the equity risk premium has fallen in recent years, European stocks are still more attractive relative to bonds but that’s no longer the case in the US. BlackRock Inc. and Schroders Plc are among those who are weighing in on the debate of what will happen if US rates peak at 6%.

Earlier in the session, Asian equities also fell as hawkish comments from the Federal Reserve hurt appetite for risk assets, with China’s technology shares bearing the brunt of the selloff. The MSCI Asia Pacific Index declined as much as 1.5%, the most in three weeks, dragged by Tencent, Alibaba and Meituan. Fed Chair Jerome Powell told the Senate Banking Committee that the ultimate level of interest rates is likely to be higher than previously anticipated. Traders have since hiked their estimates on the terminal rate, with expectations for it to peak at about 5.6% in September. Stock gauges in Hong Kong and South Korea led losses in the region, while Japanese benchmarks were in positive territory. Still, regional emerging markets should get some buffer from lower inflation and close-to-peak interest rates.

Developed market “tightening will lead to slower growth and, ultimately, to cyclical recessions in the US, Europe and the UK later this year or next year,” said Matthew Quaife, head of multi asset investment management for Asia at Fidelity International. Emerging Asia, on the other hand, has the advantages of “falling inflation, peak monetary tightening, and attractive valuations,” he wrote in a note. The MSCI Asia gauge has been falling for two days, with sentiment shaky after a selloff in February stalled its rebound. The measure is struggling to cross its 50-day moving average amid concerns over the Fed’s policy path and a lack of major catalysts from the National People’s Congress in China.

Japanese stocks climbed after Federal Reserve Chair Jerome Powell’s hawkish remarks on interest rates weakened the yen to its lowest in more than two months. The Topix Index rose 0.3% to 2,051.21 as of the market close in Tokyo, while the Nikkei advanced 0.5% to 28,444.19. Sony Group Corp. contributed the most to the Topix Index gain, increasing 0.6%. Out of 2,160 stocks in the index, 1,436 rose and 615 fell, while 109 were unchanged.

In Australia, the S&P/ASX 200 index fell 0.8% to close at 7,307.80, weighed by declines in mining and energy shares. The broad-based selloff comes after hawkish rhetoric from Federal Reserve Chair Jerome Powell hurt appetite for risk taking. Meanwhile, the RBA has a “completely open mind” about its April policy meeting and will be guided by key economic data on whether to raise interest rates further or pause tightening, Governor Philip Lowe said at a conference in Sydney. Read: RBA’s Lowe Has ‘Open Mind’ on April Rate Pause, Says Data Is Key In New Zealand, the S&P/NZX 50 index fell 0.5% to 11,855.54.

Stocks in India were among few gainers in Asia as the benchmark Sensex advanced for a third consecutive session, helped by gains in index-heavy ITC and Larsen & Toubro. All of 10 companies controlled by the Adani Group advanced after prepayment of $902 million worth of borrowings by the founding family. The S&P BSE Sensex erased a loss of as much as 0.6% to close 0.2% higher at 60,348.09 in Mumbai. The NSE Nifty 50 Index advanced by a similar measure. Thirteen of the 20 sector sub-gauges rose, led by utilities and power companies. Realty stocks were the worst performers. Tobacco and consume goods makers ITC contributed the most to the Sensex’s gain, increasing 1.1%. Out of 30 shares in the Sensex index, 17 rose, while 13 fell.

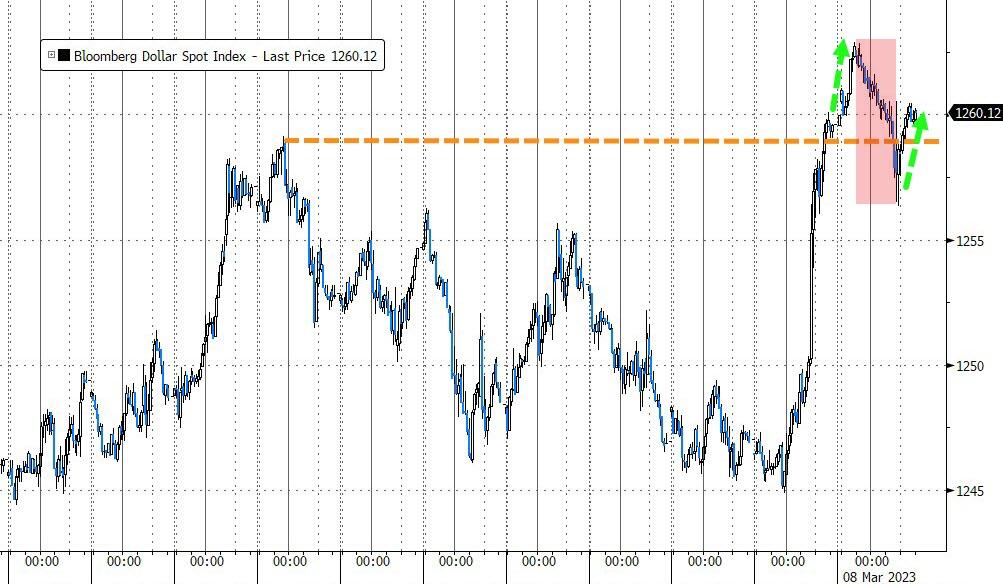

In FX, the Bloomberg Dollar Spot Index was little changed as the greenback traded mixed against its Group-of-10 peers. Rabobank’s Jane Foley predicted that dollar strength would filter through to emerging economies, which could find themselves having to tighten policy further. “That leads to the impression global growth will also be slowing,” she said.

The euro was little changed at $1.0542 after earlier falling to $1.0525, the weakest level in two months and close to year-to-date lows. Still, options traders don’t expect another big move over the next five trading days.

Scandinavian and Antipodean currencies were the best G-10 performers, reversing earlier losses

The yen was the worst G-10 performer and fell for a third day ahead of the BOJ’s monetary policy meeting later this week. Options traders trimmed hedges against gains in the yen, with 1-week risk reversals rebounding from near the lowest levels in almost nine months; 1- week implied volatility reached its highest level since mid- January. Super-long government bonds declined following weaker- than-expected auction results of 30-year debt yesterday

A decline in China’s yuan saw the central bank signal its intention to support the currency.

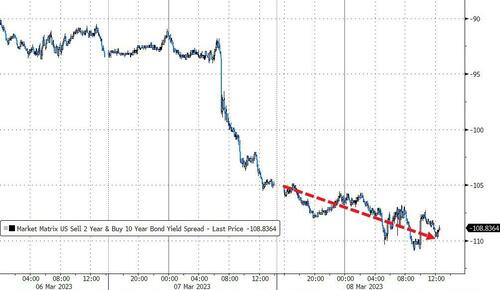

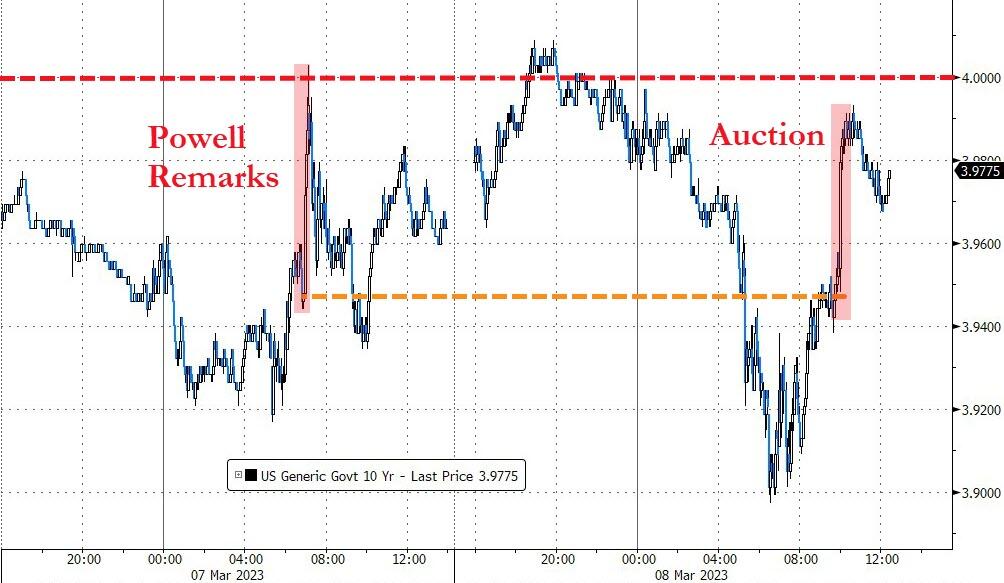

In rates, treasury yields were slightly higher, erasing a bigger spike earlier in the session which briefly pushed the 10Y back over 4.0%, with losses led by front-end as two-year yields rise another 3bps at 5.04% after Tuesday’s aggressive flattening move was extended during Asia session and European morning. 2-year yields cheaper by 3.4bp, deepening inversion of 2s10s by 3bp to -107bps with 5s30s flatter by 1.6bp; 10-year yields around 3.97% slightly cheaper vs Tuesday’s close with bunds and gilts outperforming by 2bp and 3bp in the sector. 2s10s spread reached -107.9bp, a new four-decade lows, while 5s30s breached last year’s low reaching -47.4bp, deepest inversion since 2000.

UK and German two-year yields are both higher by 3bps; in UK, money markets price in a 5% BOE peak rate for the first time since October, while core European front-end trades cheaper tied to Treasuries repricing. Bunds and Italian bonds saw minor yield upticks in the front end of the curves while they were little changed further out. In the US, the Treasury auction cycle continues with $32b 10-year note reopening at 1pm, concludes with $18b 30-year reopening Thursday. WI 10-year at 3.975% is above auction stops since November and ~36bp cheaper than February’s result.

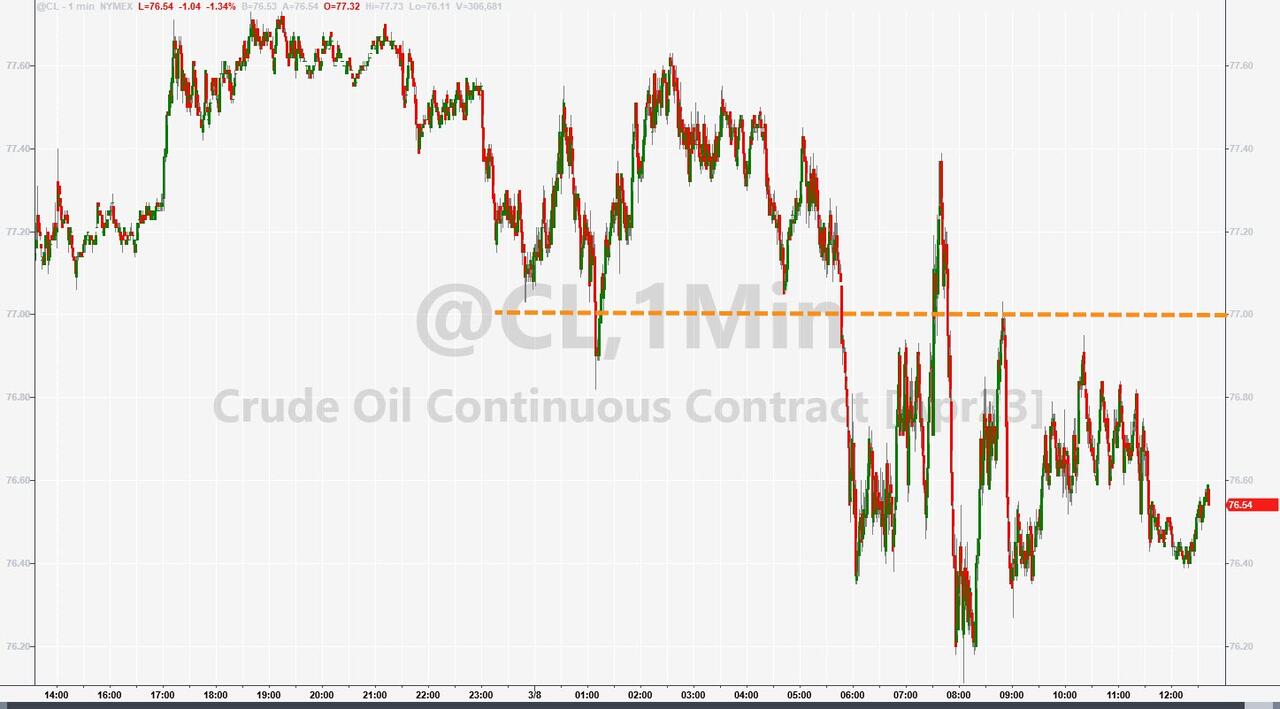

In commodities, oil held onto its losses following Powell’s hawkish coments; WTI hovered around $77.50. Diversey Holdings and Permian Resources are among the most active resources stocks in early premarket trading, gaining 39% and falling 4.1% respectively. Gas markets are mixed with TTF firmer while Henry Hub is softer but remains above the USD 2.50/MMBtu mark. Spot gold is flat near $1,1814

Looking to the day ahead now, we’ll hear from Fed Chair Powell again, who’s appearing before the House Financial Services Committee. Otherwise, we’ll hear from the Fed’s Barkin, ECB President Lagarde, the ECB’s Panetta and the BoE’s Dhingra. There’s also a policy decision from the Bank of Canada. On the data side, at 7 a.m., we got mortgage applications data which showed a 7.4% bounce after last week’s 5.7% drop, followed by the ADP employment report at 8:15 a.m. and JOLTs job openings figures are 10 a.m. The US will sell $32 billion of 10-year notes at 1 p.m. In Canada, the central bank is due to deliver a rate decision at 10 a.m. New York time. Over in Europe, we got German industrial production (which beat) and retail sales (which missed) for January.

Market Snapshot

S&P 500 futures little changed at 3,990.50

MXAP down 1.1% to 159.95

MXAPJ down 1.4% to 516.16

Nikkei up 0.5% to 28,444.19

Topix up 0.3% to 2,051.21

Hang Seng Index down 2.4% to 20,051.25

Shanghai Composite little changed at 3,283.25

Sensex up 0.1% to 60,295.62

Australia S&P/ASX 200 down 0.8% to 7,307.77

Kospi down 1.3% to 2,431.91

STOXX Europe 600 down 0.2% to 459.59

German 10Y yield little changed at 2.71%

Euro little changed at $1.0540

Brent Futures down 0.2% to $83.09/bbl

Gold spot up 0.0% to $1,814.19

U.S. Dollar Index up 0.11% to 105.73

Top Overnight News from Bloomberg

BOE policy maker Swati Dhingra cautioned against raising interest rates further, saying that doing so could damage an already weak UK economy

Ignazio Visco openly criticized ECB colleagues for making statements about future increases in borrowing costs when officials had agreed not to give such guidance

Riksbank’s First Deputy Governor Anna Breman said there’s a risk that it will take longer to get Swedish inflation back to target than earlier expected and there needs to be a broader fall in inflation pressures for the central bank to stop tightening

UK Prime Minister Rishi Sunak’s deal to solve the bitter dispute with the EU over Northern Ireland’s trading arrangements has sparked hope in the City of London that the two sides could finally formalize a pledge to work together on setting rules for banks and financial markets

Hungary’s headline inflation, the EU’s fastest, slowed for the first time in 19 months, to 25.4% in February from 25.7% the month before. The data matched the estimate in a Bloomberg survey

Japan’s bond market dysfunction has only worsened since the central bank doubled its cap on benchmark yields in December, keeping speculation alive that Governor Haruhiko Kuroda may surprise investors one last time on Friday

Japanese investors became net buyers of US sovereign bonds for the first time in five months in January, according to the Asian nation’s latest balance-of- payments data released Wednesday

The surge in government bond yields over the past year is boosting the potential allure of debt for investors, even as it heightens the risk that governments will get overwhelmed by the soaring cost of servicing what they owe

Australia’s central bank has a “completely open mind” about its April policy meeting and will be guided by key economic data on whether to raise interest rates further or pause tightening, Governor Philip Lowe said

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mostly lower amid headwinds from Wall St where risk assets suffered after Powell’s hawkish testimony in which he put a 50bps hike for March in play and flagged higher terminal rate projections. ASX 200 was negative with the declines led by underperformance in the commodity-related sectors, in particular, energy after a slump in underlying oil prices, while comments from RBA Governor Lowe failed to appease investors despite opening the door for a pause at the next meeting as he also noted that it will depend on the data and that further tightening is likely to be required to return inflation to the target. Nikkei 225 bucked the trend with the index kept afloat on currency effects and as record current account and trade deficits in Japan add to the case for a slow exit from the BoJ’s ultra-easy policy. Hang Seng and Shanghai Comp. conformed to the downbeat mood with Hong Kong heavily pressured by weakness in property stocks and tech amid the higher global yield environment and considering that the HKMA would have to move in lockstep should the Fed turn more aggressive. Foxconn (2317 TT) is reportedly in discussions with the Indian gov’t about setting up a plant on its own, without any gov’t assistance, via Economic Times.

Top Asian News

US House Speaker McCarthy confirmed plans to meet with Taiwanese President Tsai in the US this year but stressed the meeting doesn’t preclude a trip to Taiwan later, according to Bloomberg. Taiwan’s Presidential Office also said authorities are making plans and preparations for President Tsai’s foreign visit this year and will announce when decisions are made, according to Reuters.

US CDC is to lift COVID-19 testing travel restrictions from China on Friday, according to a Reuters source. South Korea is also to lift the pre-departure COVID-19 test requirements for travellers from China starting on March 11th, according to health authorities.

Chinese Embassy in Germany commented on the report that Germany could ban Huawei and ZTE from parts of 5G networks in which it stated that China is very puzzled and strongly dissatisfied with the rash decision by Germany with no factual basis if the report is true, according to Reuters.

Japanese Ministry of Finance said the January trade deficit was the largest on record and that the trade deficit tends to swing during the export-slowing month of January due in part to the Lunar Year Holidays in China, according to Reuters.

RBA Governor Lowe said they are closer to the point where it will be appropriate to pause and the timing of the pause will be determined by data and assessment of the outlook, while he added further tightening is likely to be required to return inflation to the target. Lowe also stated there will be several data releases before the next board meeting and if the data suggests a pause, they will do that but if the data suggests to keep going, then that is what they will do and will have a completely open mind at board meetings.

European bourses are mixed within very narrow parameters with sentiment generally tentative post-Powell and ahead of US ADP and numerous Central Bank speakers. Stateside, futures are in-fitting with their European peers, ES +0.1%, with Powell due to testify to the House in which he is likely to repeat Tuesday’s hawkish Senate testimony. China PCA Retail Passenger Vehicle Sales (Feb): 10.4% Y/Y (vs prelim 9.0% Y/Y; vs -37.9% Y/Y in January); CPCA says Tesla (TSLA) exported 40.5k China-made vehicles in February (prev. 39.2k MM)

Top European News

BoE’s Dhingra says overtightening poses a more material risk at this point, through potential negative impacts from increased borrowing costs and reduced supply capacity going forwards. A prudent strategy would hold policy steady amidst growing signs external price pressures are easing, and be prepared to respond to developments in price evolution. “My conclusion is that, given little evidence of further cost-push inflation, further tightening is a bigger risk to output and the medium-term inflation target.” Adds, the FX rate is less concerning than other factors.

UK Chancellor Hunt is considering providing British firms with additional tax relief on investment spending in an attempt to boost economic growth, according to Bloomberg sources.

Ireland Central Bank said significant uncertainty remains for inflation and it cut its 2023 HICP forecast to 5.0% from 6.3% but raised its 2024 forecast to 3.2% from 2.8%.

ECB’s Visco says monetary policy will need to remain prudent and should be guided by data as it comes available; adds, he does not appreciate colleagues statements on future and prolonged increases in interest rates.

ECB insider says slowing hikes to 25bps, but hiking for longer could be a compromise, Econostream reports.

Traffic on the French part of the Rhine River is at a standstill due to strikes, and international traffic has been disrupted, according to a union.

FX

The DXY continues to pick up and has made a fresh YTD peak of 105.88 (prev. 105.63, from Jan. 6th) post-Powell; amidst this, and as the index pauses off highs, G10 peers are mixed overall.

JPY is the standout laggard given yield action and pre-BoJ where Kuroda is expected to maintain the ultra-accommodative stance at his last meeting, USD/JPY at the mid-point of 137.09-137.91 parameters and above the 137.44 200-DMA.

Outperforming is the AUD, though the upside comes in the context of the magnitude of downside experienced earlier in the week post-RBA and exacerbated by Powell; AUD/USD inching above 0.66, NZD around 0.61.

CAD is essentially unchanged pre-BoC (newsquawk preview available) with an unconditional pause expected though options imply 60pips of break-even for the event.

GBP was unfazed by BoE’s Dhingra, who largely reiterated her stance from the February meeting by saying a prudent strategy would be to hold policy steady, remarks which are less-dovish than peer Tenreyro who has said a reduction is a possibility, though hasn’t specified when.

PBoC set USD/CNY mid-point at 6.9525 vs exp. 6.9551 (prev. 6.9156)

Fixed Income

Benchmarks are attempting to tick higher, though are within a handful of ticks of the unchanged mark, in what is more an attempted consolidation than any concerted upside given the magnitude of Tuesday’s action.

Currently, Bunds are at the top-end of 130.77-131.39 parameters with Gilts attempting to mount 100.00 as Dhingra makes the case, once again, for no further tightening.

Stateside, Treasuries are similarly attempting to grind higher ahead of Powell part 2, data and 10yr supply; yields mixed and inverting further with the short-end firmer and long-end slightly softer.

Commodities

WTI and Brent front-month futures remain subdued around yesterday’s worst levels after both contracts settled lower by almost USD 3.00/bbl following the Powell-induced selloff.

Gas markets are mixed with TTF firmer while Henry Hub is softer but remains above the USD 2.50/MMBtu mark.

US Energy Inventory Data (bbls): Crude -3.8mln (exp. +0.4mln), Cushing unchanged, Gasoline +1.8mln (exp. -1.9mln), Distillate +1.9mln (exp. -1mln).

Strikes are continuing at Exxon’s (XOM) Port Jerome (270k BPD) and Fos Sur Mer (140k BPD) French refineries, via Union; action which is blocking fuel deliveries.

Spot gold is essentially unchanged after Tuesday’s marked selloff with the yellow metal above late-February lows and the 100-DMA of USD 1806/oz; base metals mixed, overall.

Geopolitics

Russian embassy to the US said US media leaks on sabotage of the Nord Stream pipelines are intended to confuse. Furthermore, Kremlin spokesperson Peskov said the Kremlin is wondering how US officials can suggest anything regarding the ‘terrorist’ attack on Nord Stream without an investigation, while he suggested it is strange and smells of a ‘monstrous crime’, according to RIA.

US Event Calendar

07:00: March MBA Mortgage Applications, prior -5.7%

08:15: Feb. ADP Employment Change, est. 200,000, prior 106,000

08:30: Jan. Trade Balance, est. -$68.7b, prior -$67.4b

10:00: Jan. JOLTs Job Openings, est. 10.5m, prior 11m

14:00: Fed Releases Beige Book

Central Banks

08:00: Fed’s Barkin Speaks in Columbia, South Carolina

10:00: Powell Appears Before House Financial Service Committee

14:00: Fed Releases Beige Book

DB’s Jim Reid concludes the overnight wrap

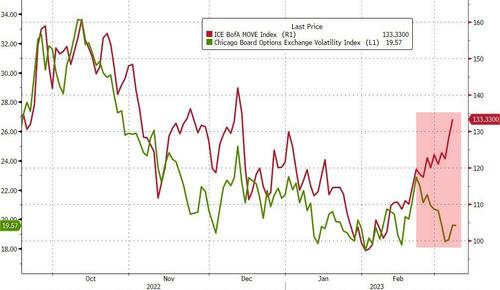

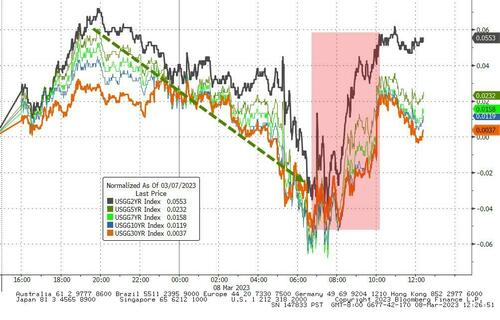

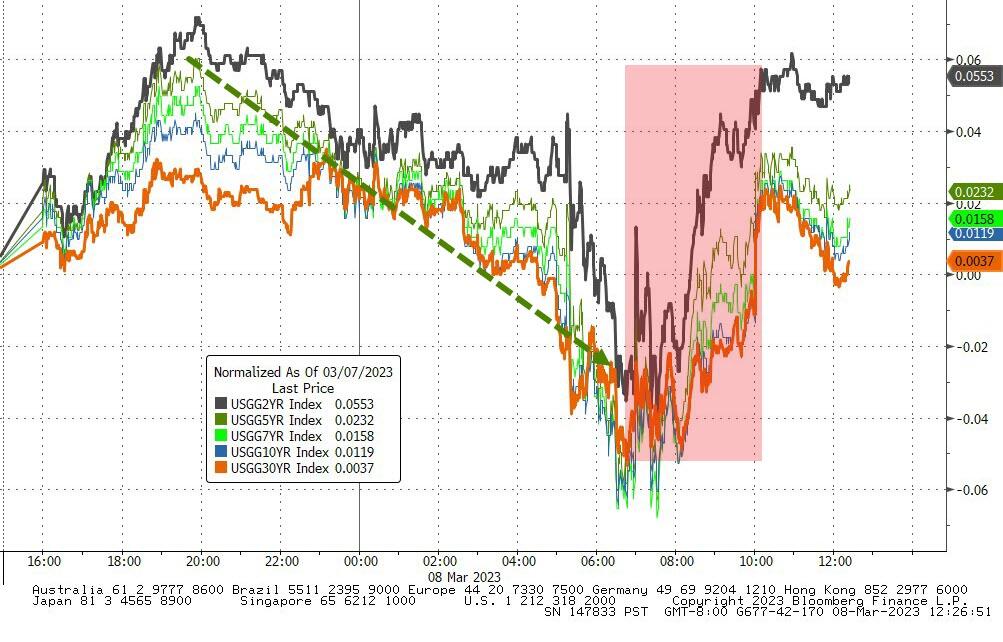

Morning from a surprisingly snowy Surrey this morning. My commute into London is going to be interesting as soon as I send this. Even rarer than snow in Southern England in March, it was another landmark day in markets yesterday, especially for the yield curve, as the US front end hawkishness revved up yet another gear after Powell’s first testimony of the week. US terminal has now gone past our street leading 5.6% forecast and closed at 5.624% (+14.8bps) last night (5.66% this morning). With US 2yr yields up +12.2bps and 10yr yields +0.06bp we saw a significant further inversion and the curve closed below -100bps (-104.9bps) for the first time since 1981. 2 and 10yr yields are up another +5.5bps and +3bps overnight with the curve breaking through -107bps.

Bear in mind that on all the previous occasions that the 2s10s has been more than -100bps inverted since data is available from the early 1940s (1969, 1979, 1980 and 1981) a recession has either been underway, or has occurred within a maximum of 8 months. To highlight the rarity of such an occurrence, there have only been 7-month end closes lower than -100bps in 80 years of available data. So we are in rarefied air.

In terms of the specifics of Powell’s comments, the biggest takeaway was his openness to larger hikes again, saying that “we would be prepared to increase the pace of rate hikes” if the data indicated. And he also pointed to a higher terminal rate as well, saying that “the ultimate level of interest rates is likely to be higher than previously anticipated.”

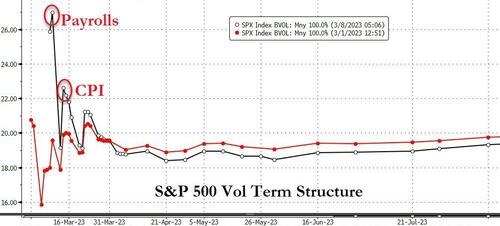

Those remarks from Powell mark a significant pivot for the Fed. Last year they signalled and then delivered a slowdown in rate hikes, moving away from four consecutive 75bp moves to 50bps in December, and then 25bps at the last meeting. Up to that point, all the indications had been that they wanted to move cautiously and assess the cumulative impact of what they’d delivered so far. In essence, the signal was that any further hikes would be at a 25bps pace until they stopped. But yesterday’s testimony explicitly opened the door to a more hawkish reaction function, which throws open several tail outcomes that had previously been closed off. See our economists’ review of his comments yesterday, and what it might mean for Fed policy here. Powell speaks again today at the House Finance Committee but it’s hard to see much new news coming after yesterday’s remarks. The JOLTS data today might be the most important event for monetary policy.

With a larger hike now in play for the next meeting, futures adjusted accordingly and a +40.7bps move is now priced in for March. That’s closer to 50 than 25, so it implies that investors view a 50bps move as the more likely outcome now. However, remember that before the next meeting in two weeks time, we’ve still got another jobs report on Friday as well as the CPI print next week, so there’s still plenty of evidence that could easily tip the 25 vs 50 debate one way or the other.

With more Fed hikes being priced in, as already briefly mentioned, Treasuries experienced a significant selloff, with the 2yr yield (+12.2bps) hitting 5.0% for the first time since June 2007 and closing at 5.01%. That said, for 10yr Treasuries, yields were basically flat on the day (+0.06bps) with the dramatic flattening likely pricing in the higher risk of a policy error and hard landing. The increase in fed futures pricing also saw inflation expectations reprice lower with the US 2y breakevens falling -10.4bps to 3.28%. That was the first meaningful drop since the first week of February when it was at 2.3%.

The prospect of more rate hikes took the steam out of the recent equity rally, with the S&P 500 (-1.53%) ending its run of three consecutive advances with its largest daily loss in two weeks. The declines were incredibly broad-based, with just 30 companies in the entire index moving higher on the day. Similarly to the day before, non-cyclical industries outperformed with consumer staples (-1.0%) the “best” performing sector while cyclicals such as banks (-3.6%), autos (-2.8%), and materials (-2.0%) declined. There were similar losses for both the NASDAQ (-1.25%) and the Dow Jones (-1.72%) as well. In Europe the STOXX 600 fell -0.77% and missed the last 0.5pp of the US equity sell-off.

Unlike in the US however, European sovereign bonds actually put in a fairly strong performance. For instance, yields on 10yr bunds (-5.7bps), OATs (-4.7bps) and BTPs (-4.8bps) all saw a substantial decline on the day. That was driven in part by very good news on inflation expectations, with the ECB’s latest Survey of Consumer Expectations showing a decline in January. In particular, median expectations at the 3yr horizon came down to 2.5%, having been at 3.0% in December. That’s their lowest level since May 2022, although there are still big questions as to whether this will prove to be sustained, since the 1yr expectation only fell a tenth to 4.9% (vs. 5.0% in December).

Overnight in Asia, Japanese equity markets are the only bright spot with most of the region otherwise selling off amid the overnight advances in US rates. The Nikkei 225 (+0.44%) is posting solid gains just as the Hang Seng (-2.53%), the Shanghai Composite (-0.48%) and the Kospi (-1.26%) are sliding. US equity futures are steady, with S&P 500 contracts (+0.03%) almost unchanged.

There wasn’t much in the way of data yesterday, but German factory orders unexpectedly grew by +1.0% in January (vs. -0.7% expected). That was driven by a rise in foreign orders of +5.5%, whereas domestic orders fell by -5.3%.

To the day ahead now, and we’ll hear from Fed Chair Powell again, who’s appearing before the House Financial Services Committee. Otherwise, we’ll hear from the Fed’s Barkin, ECB President Lagarde, the ECB’s Panetta and the BoE’s Dhingra. There’s also a policy decision from the Bank of Canada. On the data side, releases from the US include the ADP’s report of private payrolls for February, the JOLTS job openings for January, and the trade balance for January. Over in Europe, there’s also German industrial production and retail sales for January.

end

AND NOW NEWSQUAWK (EUROPE/REPORT)

DXY climbs & debt attempts to tick higher in tentative trade – Newsquawk US Market Open

WEDNESDAY, MAR 08, 2023 – 06:35 AM

Equities are mixed within fairly narrow parameters given the tentative post-Powell sentiment ahead of ADP & numerous speakers.

DXY has lifted to a fresh YTD peak, with peers mixed as AUD outperforms and JPY lags.

GBP was unfazed by Dhingra reiterating a preference to pause tightening, in remarks that were not as explicit as dovish-peer Tenreyro.

Fixed income is attempting to tick higher, in what is more an attempted consolidation than any real upside move.

Crude benchmarks are relatively contained around Tuesday’s lows with Nat Gas mixed and spot gold essentially unchanged.

Looking ahead, highlights include US ADP, International Trade & JOLTS, Canadian Trade Balance, BoC Policy Announcement, Speeches from Fed’s Powell, Barkin, Supply from the US, Earnings from Oracle.

Or why not try Newsquawk’s squawk box free for 7 days?

EUROPEAN TRADE

EQUITIES