MARCH 10: THE 18TH LARGEST BANK IN THE USA SILICON VALLEY BANK FAILED AND NOW IN RECEIVORSHIP: SLB WAS A BANK TO ALL THE MAJOR VENTURE CAPITALISTS WHO ARE NOW SCRAMBLING TONIGHT; SLB WAS AN INHOUSE PROVIDER OF MAJOR FINANCIAL SERVICES, MORTGAGES ETC. TO OUR VENTURE CAPITALISTS// AND THIS CAUSED GOLD TO SKYROCKET UP $31.60 TO $1862.30//SILVER WAS MUCH MORE SUBDUED UP ONLY 36 CENTS TO $20.47//PLATINUM WAS UP $19.55 TO $960.50 BUT PALLADIUM SUFFERED AGAIN DOWN $30.90 TO $1373.05//USA JOBS REPORT WAS STELLAR BUT NOBODY PAID ATTENTION//COVID UPDATES: DR PAUL ALEXANDER/DR PANDA/VACCINE IMPACT/SLAY NEWS//UKRAINE VS RUSSA UPDATES//ESSENTIAL READING TONIGHT: ALASDAIR MACLEOD , JAMES RICKARDS & PAM AND RUSS MARTENS//SWAMP STORIES FOR YOU TONIGHT//

132 C SG AMERICAS 219 323 C HSBC 66 363 H WELLS FARGO SEC 6 435 H SCOTIA CAPITAL 100 624 H BOFA SECURITIES 222 657 C MORGAN STANLEY 2 661 C JP MORGAN 2 690 C ABN AMRO 21 737 C ADVANTAGE 6 6

TOTAL: 325 325

JPMORGAN stopped 2/325 contracts

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR MAR/2023. CONTRACT: 325 NOTICES FOR 32500 OZ or 1.0108 TONNES

total notices so far: 3012 contracts for 301200 oz (9.3685 tonnes)

SILVER NOTICES: 4 NOTICE(S) FILED FOR 20,000 OZ/

total number of notices filed so far this month : 2947 for 14,735,000 oz

END

GLD

WITH GOLD UP $21.60

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.47 TONNES FROM THE GLD//////(VERY STRANGE)

INVENTORY RESTS AT 903.15TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 36 CENTS

AT THE SLV// NO CHANGES IN SILVER INVENTORY AT THE SLV: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 478.879. MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A SMALL SIZED 56 CONTRACTS TO 128,467 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE TINY SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR TINY $0.02 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR NEW LOW COMEX OI SILVER WAS SET AT 121,299 MARCH 3/2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.02). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS, AS WE HAD A STRONG GAIN ON OUR TWO EXCHANGES 646 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 1 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD: A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS( 702 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.58 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE JUMP OF 15,000 OZ//NEW STANDING: 15.120 MILLION OZ + THE 1.0 MILLION OZ OF EXCHANGE FOR RISK//THUS TOTAL NEW STANDING 16.120 MILLION OZ/ //// V) TINY SIZED COMEX OI LOSS/ STRONG SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –54 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTRACTS for 8 days, total 4137 contracts: OR 20.685 MILLION OZ . (517 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 20.685 MILLION OZ

.

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 20.685 MILLION OZ//INITIAL

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 56 WITH OUR $0.02 GAIN IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 702 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAR OF 15.58 MILLION OZ//FIRST DAY NOTICE// FOLLOWED BY TODAY’S 15,000 OZ QUEUE JUMP (WHICH INCREASES THE AMOUNT OF SILVER STANDING) + 1.0 MILLION OF EXCHANGE FOR RISK ISSUED EARLY IN MARCH (INCREASES THE AMOUNT OF SILVER STANDING) //NEW STANDING 16.120 MILLION OZ .. WE HAVE A STRONG SIZED GAIN OF 646 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 4 NOTICE(S) FILED TODAY FOR 20,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GOOD SIZED 5164 CONTRACTS TO 454,259 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 1302 CONTRACTS.

.

WE HAD A GOOD SIZED DECREASE IN COMEX OI ( 5,164 CONTRACTS) DESPITE OUR $16.50 GAIN IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR MAR. AT 4.9953 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 32,500 OZ (1.010 TONNES) //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S ) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London).

YET ALL OF..THIS HAPPENED WITH OUR $16.50 GAIN IN PRICEWITH RESPECT TO THURSDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 2183 OI CONTRACTS (6.790 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2981 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 454,259

IN ESSENCE WE HAVE A FAIR DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2183 CONTRACTS WITH 5164CONTRACTS DECREASED AT THE COMEX AND 2981 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 2183 CONTRACTS OR 6.790 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2981 CONTRACTS) ACCOMPANYING THE GOOD SIZED LOSS IN COMEX OI (5164) TOTAL LOSS IN THE TWO EXCHANGES 2183 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR MAR. AT 4.9953 TONNES FOLLOWED BY TODAY’S 32,150 OZ QUEUE JUMP//NEW STANDING 9.5707 TONNES // ///3) ZERO LONG LIQUIDATION //4) GOOD SIZED COMEX OPEN INTEREST LOSS// 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

TOTAL EFP CONTRACTS ISSUED: 26,082 CONTRACTS OR 2,608,200 OZ OR 81.125 TONNES IN 8 TRADING DAY(S) AND THUS AVERAGING: 3260 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8TRADING DAY(S) IN TONNES 81.125 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 81.125/3550 x 100% TONNES 2.02% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 81.125 TONNES/INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A SMALL SIZED 56 CONTRACTS OI TO 128,413 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A RECORD LOW OF 121,299 CONTRACTS MARCH 3/2023.

EFP ISSUANCE 702 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 702 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 702 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 56CONTRACTS AND ADD TO THE 702 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG GAIN OF 646 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES //2.009 MILLION OZ

OCCURRED WITH OUR $0.02 GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED DOWN 46.02 PTS OR 1.40% //Hang Seng CLOSED DOWN 605.82 PTS OR 3.04% /The Nikkei closed DOWN 479.18% PTS OR 1.67% //Australia’s all ordinaries CLOSED DOWN 2.21% /Chinese yuan (ONSHORE) closed UP 6.9518//OFFSHORE CHINESE YUAN UP TO 6.9573// /Oil DOWN TO 75.17 dollars per barrel for WTI and BRENT AT 81.86 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 5164 CONTRACTS DOWN TO 454,259 DESPITE OUR STRONG GAIN IN PRICE OF $16.50.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAR… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2981 EFP CONTRACTS WERE ISSUED: : APRIL 2981 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2981 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2183 CONTRACTS IN THAT 2981LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED COMEX OI LOSS OF 5164 CONTRACTS..AND THIS FAIR SIZED LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR STRONG GAIN IN PRICE OF $16.50. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAR (9.5707) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 9.5707 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $16.50) //// BUT WERE SUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD OUR FAIR SIZED LOSS OF 2183 CONTRACTS ON OUR TWO EXCHANGES (MAKES NO SENSE WITH A STRONG GAIN IN PRICE???)

WE HAVE LOST A TOTAL OI OF 6.790 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAR. (4.9953 TONNES) FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 32,500 OZ (1.0108 TONNES)… ALL OF THIS WAS ACCOMPLISHED DESPITE OUR STRONG GAIN IN PRICE TO THE TUNE OF $16.50

WE HAD -1302 CONTRACTS REMOVED FROM COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 2183 CONTRACTS OR 218300 OZ OR 6.790 TONNES

Total monthly oz gold served (contracts) so far this month

3012 notices 301,200 9.3685 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 1

i) Into HSBC: 35,588.875 oz

total withdrawals: 35,588.875 oz

in tonnes: 1.10 tonnes

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of MARCH we have an oi of 390 contracts having GAINED 256 contracts. We had 69 notices filed on THURSDAY so we

gained another 325 contracts or an additional 32,500 oz will stand for metal at the comex

April lost 27,576 contracts down to 265,545 contracts

May LOST 15 contracts to stand at 156

We had 325 notice(s) filed today for 32,500 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 325 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 2 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAR. /2023. contract month,

we take the total number of notices filed so far for the month (3012 x 100 oz ), to which we add the difference between the open interest for the front month of (MAR. 390 CONTRACTS) minus the number of notices served upon today 325 x 100 oz per contract equals 307700 OZ OR 9.5707 TONNES the number of TONNES standing in this active month of MARCH.

thus the INITIAL standings for gold for the MAR contract month:

No of notices filed so far (3012 x 100 oz+ 390 OI for the front month minus the number of notices served upon today (325)x 100 oz} which equals 307,700 oz standing OR 9.5707 TONNES in this active delivery month of MARCH..

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 2947 x 5,000 oz = 14,735,000 oz

to which we add the difference between the open interest for the front month of MAR(81) and the number of notices served upon today 4 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAR./2023 contract month: 2947 (notices served so far) x 5000 oz + OI for the front month of MAR (x81) – number of notices served upon today (4) x 500 oz of silver standing for the MAR. contract month equates 15.120 million oz +the 1.0 million oz of exchange for risk//new total standing 16.120 million oz

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MARCH 10//WITH GOLD UP $31.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 903.15 TONNES

MARCH 9/WITH GOLD UP $16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 906.62 TONNES

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

FEB 28/WITH GOLD UP $12.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 917.61 TONNES

FEB 27/WITH GOLD UP $6.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.32 TONNES

FEB 24/WITH GOLD DOWN $9.10 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 917.32 TONNES

FEB 23/WITH GOLD DOWN $13.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 919.92 TONNES

FEB 22/WITH GOLD DOWN 22 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 919.92 TONNES

FEB 21/WITH GOLD DOWN $7.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 919.92 TONNES

FEB 17/WITH GOLD DOWN $1.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 921.08 TONNES

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

GLD INVENTORY: 903.15 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 10.WITH SILVER UP 36 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ…

MARCH 9/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.979 MILLION OZ

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWALOF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

FEB 28/WITH SILVER UP 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.241 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.188

FEB 27/WITH SILVER DOWN 15 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.471 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 482.429 MILLION OZ

FEB 24/WITH SILVER DOWN 46 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.172 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.900 MILLION OZ//

FEB 23/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.379 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.072 MILLION OZ//

FEB 22/WITH SILVER DOWN 22 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ FROM THE SLV////INVENTORY RESTS AT 485.693 MILLION OZ

FEB 21/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.5363 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 486.382 MILLION OZ//

FEB 17/WITH SILVER UP 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 827,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.819 MILLION OZ/

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 478.879 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

END

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

JAMES RICKARDS>>>

Rickards explains perfectly in simplistic terms the Debt Ceiling debate as well as the budget debate and how both can cause the shutting down of Congress.

Remember Modern Monetary Theory or “MMT”? I first sounded the alarm back in 2018 and then again in 2021.

At the time, MMT was all the rage among monetary and fiscal policy wonks. It seemed to offer the best of all possible worlds. You can spend as much as you want without any downside.

The main tenets of MMT are that debt and deficits don’t matter because the Fed can monetize the debt by printing money. The Fed can just wire money directly to government contractors to pay bills.

But MMT gradually faded from the headlines.

The pandemic of 2020 changed everything. MMT was still not a topic of discussion. It didn’t matter, because MMT was being practiced, even if by stealth.

COVID relief and economic “stimulus” was Job One. Congress provided $2.7 trillion in new spending including $1,400 checks sent to every American. Then, on Dec. 21, 2020, Trump signed another $900 billion relief package that provided an additional $600 check to every American.

Wait, There’s More!

Not to be outdone, the new Biden administration passed the American Rescue Plan Act of 2021 (ARPA), which provided another $1.9 trillion of deficit spending, and sent another $1,400 check to every American.

The runaway spending didn’t end there. On Nov. 15, 2021, Joe Biden signed the $1 trillion Infrastructure Investment and Jobs Act. This was followed by $737 billion in new deficit spending for the Green New Deal in the misnamed Inflation Reduction Act of 2022 (IRA) signed by Biden on Aug. 16, 2022.

The U.S. debt-to-GDP ratio has risen from a dangerously high 106% at the start of the Trump administration to an astronomical 124% or so today, the highest in U.S. history.

For perspective, the other countries with a debt-to-GDP ratio in that range include Lebanon, Greece and Italy. The U.S. is now a full-fledged member of the deadbeat club.

Does this debt and deficit debacle mean that MMT has achieved its goals and is now the guiding light for fiscal and monetary policy?

The answer is: yes and no.

It’s Complicated

The “yes” answer is easy to explain. MMT says that spending doesn’t matter and deficits don’t matter. The U.S. can issue as much debt as it wants and spend as much money as it wants.

As long as the debt is denominated in dollars and the Fed has a U.S. dollar printing press, we can always monetize the debt with new money. Problem solved.

With $10 trillion of new debt in three years and a 124% debt-to-GDP ratio, the U.S. is certainly acting as if debt and deficits don’t matter. This is the essence of MMT.

The “no” answer is more nuanced and political. It’s true that we are acting in accordance with MMT, but the MMT advocates are keeping their heads down. Why shouldn’t they? They are getting exactly what they want and the Republicans have gone along with it.

Trump increased the deficit by $4.6 trillion in his last year in office, almost half the $10 trillion total increase under Trump and Biden together since 2020. There’s no need to push MMT or even discuss it if Republicans and Democrats are acting in accordance with it.

So the U.S. is implementing MMT without acknowledging or even understanding it. It now exists in practice, but it has not passed a political litmus test. The future of MMT hangs in the balance starting now.

The Debt Ceiling “Crisis”

We’re facing a debt ceiling “crisis.”

What is the debt ceiling exactly? It’s a numeric limit on the total debt that the U.S. Treasury is allowed to issue. There’s no debt ceiling in the U.S. Constitution. Instead, it’s imposed by statute. There’s no legal requirement for that statute.

The debt ceiling itself could be repealed by Congress at which point there would be no limit on the size of the national debt. Still, Congress likes the idea of a debt ceiling. It forces the White House and Treasury to come back to Congress from time to time to request increases as needed.

This gives Congress some leverage to ask for political concessions in return for raising the debt ceiling. So the debt ceiling is really a political football rather than a serious macroeconomic policy tool.

In the end, Congress always approves the ceiling increases. In a way, the debt ceiling debate is all for show. To be clear, the debt ceiling does not mean the Treasury cannot issue any new debt. It means that the Treasury cannot issue debt that increases the total outstanding above the ceiling.

The Looming “X-Date”

The “X-Date” is the day the Treasury is projected to run out of cash and can’t pay bills or pay off Treasury note holders. Right now, the X-Date is estimated to be around June 5, 2023, but even that is a guess. The real X-Date will depend on how much positive cash flow the Treasury generates during tax season around mid-April.

Congress and the White House are also battling over the budget for fiscal 2024, which begins on Oct. 1, 2023. If a new budget is not passed by Sept. 30, 2023, the government will shut down at midnight.

It is possible that Congress could extend that deadline with a continuing resolution (CR) that permits government agencies to keep spending at existing levels for existing programs until Congress gets around to passing a budget.

Although the debt ceiling increase and the budget are separate issues with separate procedures, they are converging at about the same time. Mid-April is the date when markets will focus on this more intently because of the X-Date.

We’ll have better estimates of the X-Date by April, and a kind of “countdown to default” will begin.

Where does the MMT crowd stand in all of this?

Putting MMT to the Test

As noted, supporters of MMT have had the luxury of getting everything they want politically without having to stand up and defend MMT publicly. COVID and climate change (really, bogus climate alarmism) acted as the perfect cover for the Trump and Biden spending seemingly without having to worry about debt or deficits at all.

The mantra in Washington was “spend, spend, spend.” And they did.

Now that the pandemic is over and the Green New Scam is law (for better or worse), a day of reckoning has arrived. If the debt ceiling is raised and deficit spending is increased without serious reforms, it will be left to MMT’ers to explain why none of this matters.

They will rise to the occasion. Again, the main tenets of MMT are that debt and deficits don’t matter because the Fed can monetize the debt by printing money. If inflation emerges, the government can simply raise taxes to cool off the inflation.

Of course, MMT is nonsense. One can be reasonably sure that if members of Congress don’t understand MMT, they definitely do not understand the flaws in MMT. But that won’t stop the banner from being raised. Expect to hear a lot of commentaries that “deficits don’t matter,” and “debt doesn’t matter” as the debt ceiling and budget battles are being waged in the months ahead.

We can be sure of a few things…

There Will Be No Default

The Treasury will not default on its debt. You’ll be reading a lot of stories about a debt default in the coming months. Those stories will be used to scare voters into a “clean” debt ceiling increase.

Whatever your views on the debt ceiling, you can ignore these default stories. It won’t happen because it serves no one’s interest. A better way is to think of the debt ceiling debate as a game of chicken between conservative Republicans and the White House.

In the end, Republicans will get some (not all) of what they want and the debt ceiling will be raised. That will lay the issue to rest … until the next time.

Passing the budget is more complicated. The budget is huge and there’s a lot more at stake than just debt issuance. Spending increases, defense spending, support for Ukraine, social programs, tax increases and more are all on the table.

Although the budget deadline is Sept. 30, Congress will try to get something done over the course of July and August. This will happen at exactly the same time that the debt ceiling and X-Date crisis is playing out.

In the end, the debt ceiling will be raised, most likely in July. A government shutdown in late September is a real possibility. That will be another point of high volatility in stocks. All in all, it will be an interesting year.

At a minimum, investors should expect increased market volatility as default talk grows louder. It may be a good time to reduce equity exposure and increase your cash allocation.

END

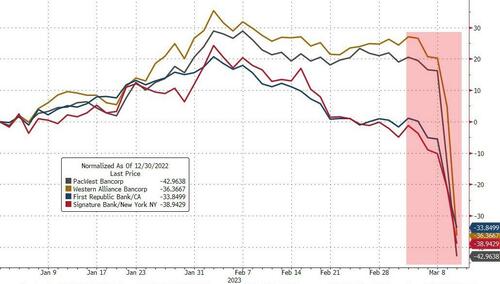

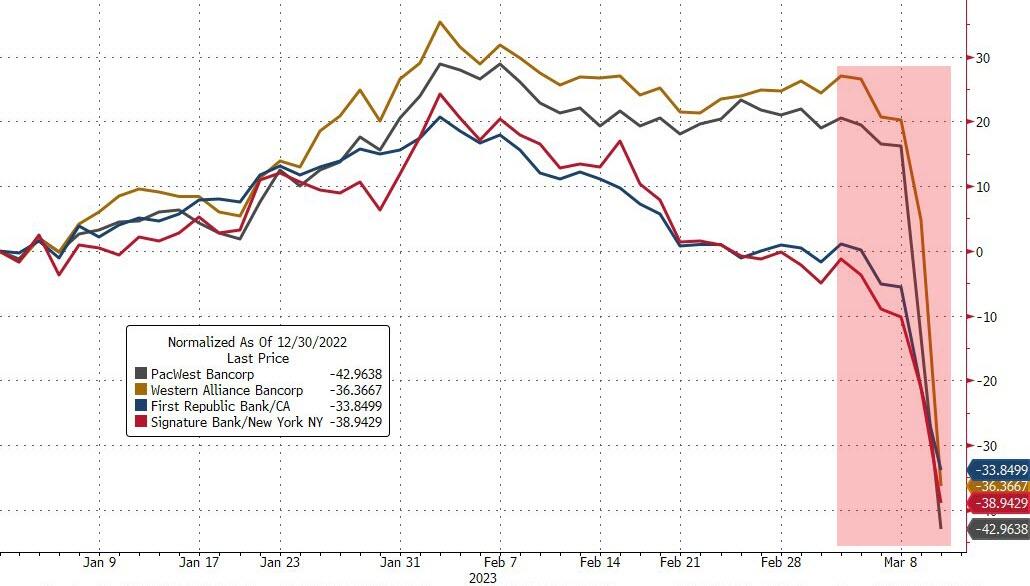

Pam and Russ Martens: Bank stocks plummet as runs gain momentum at non-traditional banks

Submitted by admin on Fri, 2023-03-10 10:34Section: Daily Dispatches

By Pam and Russ Martens Wall Street on Parade Friday, March 10, 2023

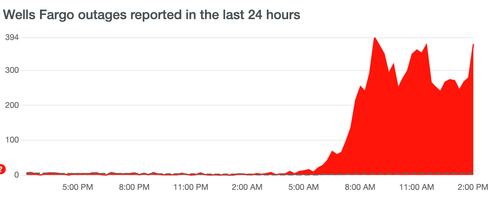

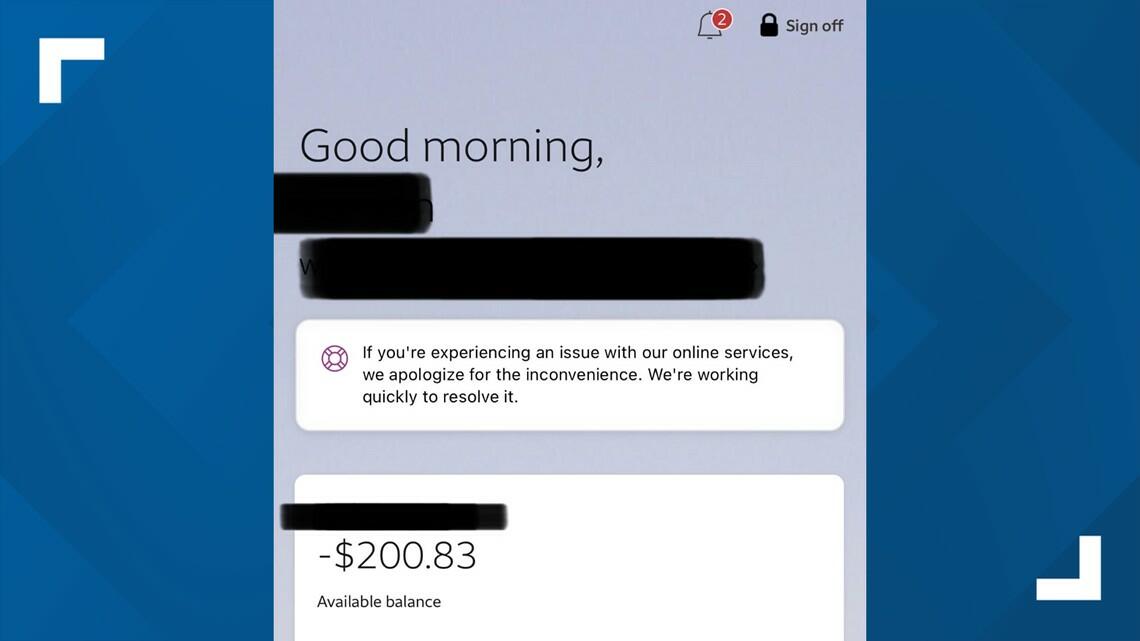

If you keep a diary or news journal, be sure to write down March 9, 2023, as the day that a full-blown bank run began at non-traditional banks in the United States.

Bank depositors were already nervous after federally-insured Silvergate Bank (ticker SI) announced Wednesday evening that it was closing and liquidating. Its publicly traded stock had already lost over 90% of its market value over the prior 12 months.

Silvergate had made the fatal decision several years ago to become the go-to bank for crypto companies, including scandalized Sam Bankman-Fried’s collapsed house of frauds, FTX and Alameda Research. As details of its questionable activities related to Bankman-Fried’s enterprises emerged, 68% of its deposits related to crypto companies took flight in just the last quarter of 2022. After Silvergate confirmed in an filing with the Securities and Exchange Commission on March 1 that an investigation of its conduct was underway at the U.S. Department of Justice, and that it had doubts about its ability to continue as a going concern, its fate was sealed.

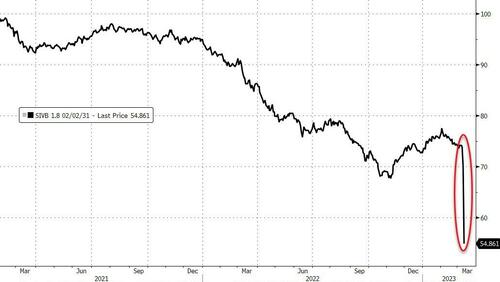

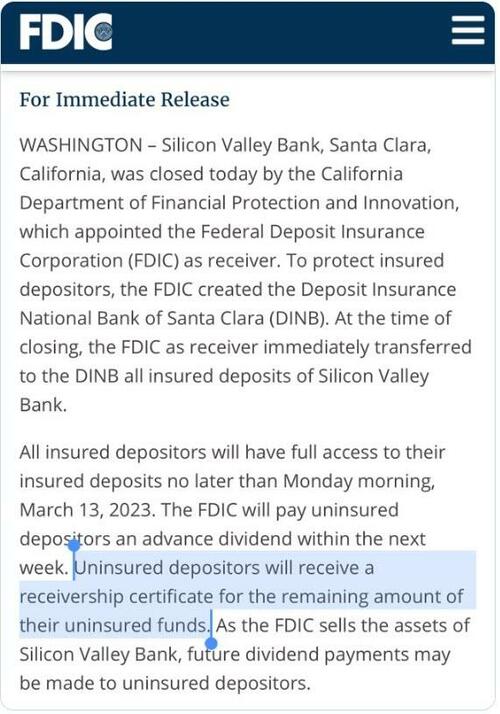

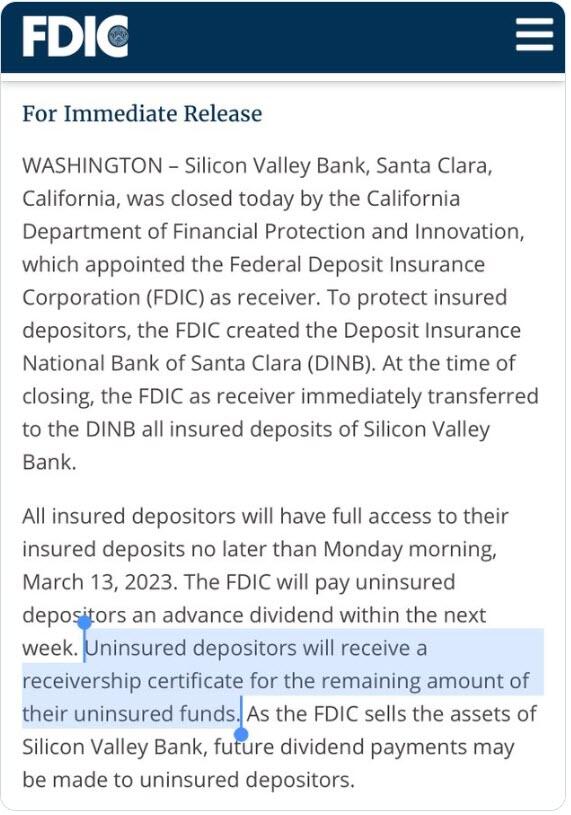

Now for the second time in less than two weeks depositors are panicking over the fate of another federally-insured bank. This time it’s Silicon Valley Bank (ticker for holding company is SIVB) which, like Silvergate Bank, had become a go-to bank for a special niche customer. Instead of crypto, its niche was venture capital outfits and private equity firms.

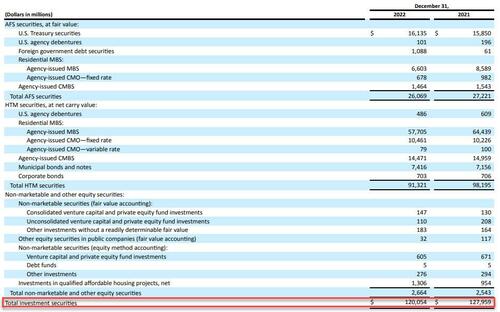

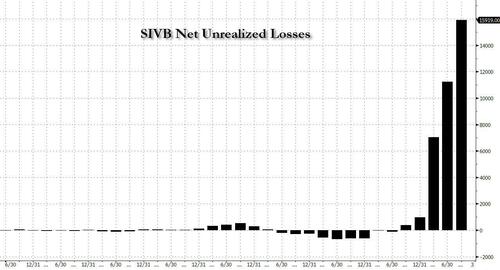

Silicon Valley Bank is not a small bank. According to its regulatory filings, as of December 31 it held $161.4 billion in domestic deposits and $13.9 billion in foreign deposits. …

3. Chris Powell of GATA provides to us very important physical commentaries//

Your weekend reading material:

Alasdair Macleod: Why credit needs a golden anchor

Submitted by admin on Thu, 2023-03-09 12:00Section: Daily Dispatches

By Alasdair Macleod GoldMoney, Toronto Thursday, March 9, 2023

This article examines the relationship between credit and its anchor in value. Today that anchor is fiat currency, which is both parochial and unstable. Historically and in law the anchor has always been gold.

It is a common error to think of credit in a narrow sense, without realising that officially recorded credit in the form of banknotes and deposit accounts with the commercial banks is only a minor part of the total credit in an economy. This article takes a holistic view of credit.

The relationship between credit and whatever provides an anchor to its value is a far larger topic from that commonly discussed in economic journals. It involves an understanding of the relationships between currency credit and commercial bank credit, the consequences of which rarely occur to economic commentators.

There is evidence that changes in central bank credit have a greater impact on prices than an equivalent change in commercial bank credit – a new and important topic for our consideration.

This article draws on the history of law as it applies to banking, money, and credit. For both contemporary economists and the layman, it involves some concepts that may be novel to them. But given that they concern the very survival of contemporary currencies, they are worth making the effort to understand. …

Perth Mint faces LBMA review over gold ‘doping’ charge

Submitted by admin on Thu, 2023-03-09 20:08Section: Daily Dispatches

By Deep Vakil Reuters Thursday, March 9, 2023

The London Bullion Market Association, the top accreditor of gold refiners, said today it was reviewing allegations that Perth Mint had sold “doped” gold to China.

An Australian media report Monday said Perth Mint, the largest processor of newly mined gold, may have to recall a potential $9 billion worth of diluted or “doped” 1-kilogram gold bars sold to top consumer China.

The Australian gold refiner, a member of the LBMA, rejected those allegations Tuesday, saying there was no question about the value and purity of gold bars it had sold to customers in China, after it implemented new procedures following a 2021 review of its refining practices.

“Doping” or “alloying” is an industry-wide accepted practice to minimise the amount of pure gold above the 99.99% purity level in each bar. …

Stefan Gleason writs that many states are moving bills toward sound money legislation

(Stefan Gleeson/MMN)

‘Sound money’ bills moving forward rapidly in many states

Submitted by admin on Thu, 2023-03-09 20:41Section: Daily Dispatches

8:40p ET Thursday, March 9, 2023

Dear Friend of GATA and Gold:

Writing for Money Metals News Service, Stefan Gleason tonight gives a summary of progress across the United States being made by “sound money” legislation, particularly in regard to eliminating sales and income taxes on the monetary metals and creating state gold reserves.

The summary is headlined “Sound Money Bills Moving Forward Rapidly in Many States” and it’s posted at Money Metals here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

Two Former Merrill Traders Sentenced To One Year In Prison For Precious Metal Manipulation

FRIDAY, MAR 10, 2023 – 12:25 PM

Two former Merrill Lynch traders were each sentenced to a year and a day in prison Thursday for manipulating the precious-metals markets, the US Department of Justice said Thursday.

Edward Bases, 61, and John Pacilio, 59, used large “spoof” orders to push precious metal prices up and down for their own gain, the Justice Department said in a statement.

They were convicted in Chicago in 2021 for fraudulently pushing market prices up or down by placing large “spoof” orders in the precious metals futures markets that they did not intend to fill. As a result they manipulated the price of gold, silver and platinum prices in the direction they wanted from 2008 to 2014.

The government has been targeting alleged market manipulation since the 2008 financial crisis, leading to convictions of traders and settlements with big banks. JPMorgan Chase & Co., the largest US bank, agreed to pay $920 million in 2020 to settle Justice Department spoofing allegations, by far the biggest fine for any financial institution.

In August, the head of the JPMorgan’s precious-metals business and his top gold trader were convicted of fraud and market manipulation. Another trader was convicted in December. A trial in 2020 led to convictions of two former Deutsche Bank AG traders, who also got a year in prison.

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 6.9518

OFFSHORE YUAN: 6.9573

SHANGHAI CLOSED DOWN 46.02 PTS OR 1.40%

HANG SENG CLOSED DOWN 605.82 PTS OR 3.04%

2. Nikkei closed UP 479.18 PTS OR 1.67%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 105.14 Euro RISES TO 1.0594 UP 9 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.402!!(Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 136.63/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.501%***/Italian 10 Yr bond yield FALLS to 4.301%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.534…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.302//(ITALY WORSE THAN GREECE?)

3j Gold at $1834.05//silver at: 20.09 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 14/100 roubles/dollar; ROUBLE AT 75.98//

3m oil into the 75 dollar handle for WTI and 81 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 136.63/10 YEAR YIELD AFTER BREAKING .54%, LOWERS TO .402% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9262–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9813well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

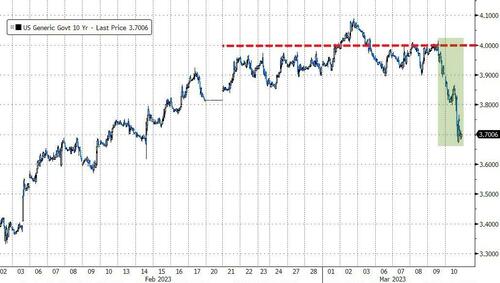

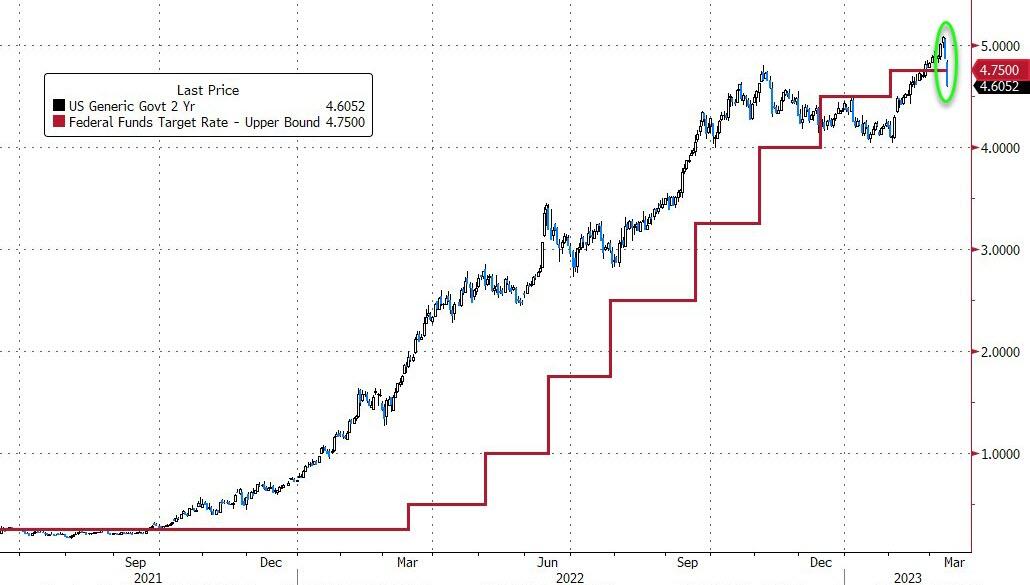

USA 10 YR BOND YIELD: 3.826% DOWN 10 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.807 DOWN 6 BASIS PTS//INVERTED TO THE 10 YEAR!!

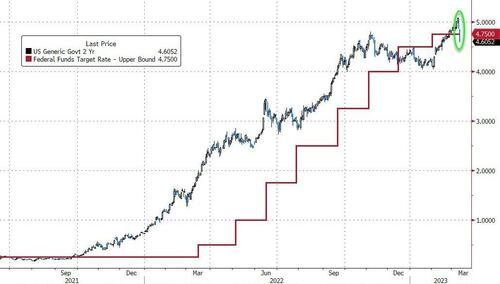

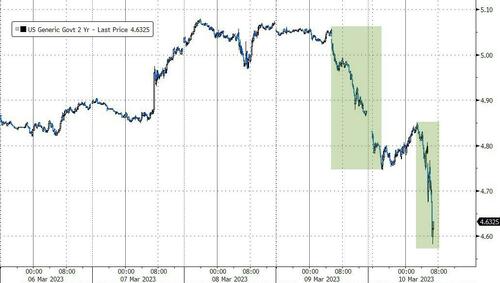

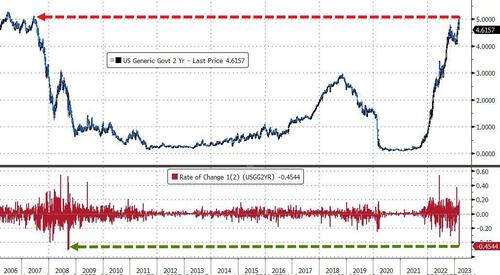

USA 2 YR BOND YIELD: 4.767 DOWN 13 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,96…

GREAT BRITAIN/10 YEAR YIELD: 3.716% DOWN 12 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Tumble As SVB Implosion Spark Global Banking Turmoil; Payrolls Loom

FRIDAY, MAR 10, 2023 – 08:01 AM

US futures and European stocks pared broader declines earlier sparked by a rush to havens amid concerns about the health of the US banking system following the collapse of Silvergate and the rout that has crushed Silicon Valley Bank, sending it shares down 40% premarket after plunging 60% on Thursday amid a spreading liquidity crisis. The collapse of the lender was sufficiently traumatic to push today’s payrolls report – until yesterday the highlight of the week – off the front page.

S&P 500 futures fell slightly, erasing a bigger drop that pushed eminis briefly below 3,900 setting up the underlying index to extend a rout fueled by liquidity concerns in the banking sector and as investors prepare for the monthly payrolls report. The benchmark dropped the most in over two weeks on Thursday, with banks slumping as SVB Financial Group took steps to shore up its capital position following losses in its securities portfolio. Nasdaq 100 futures were little changed.

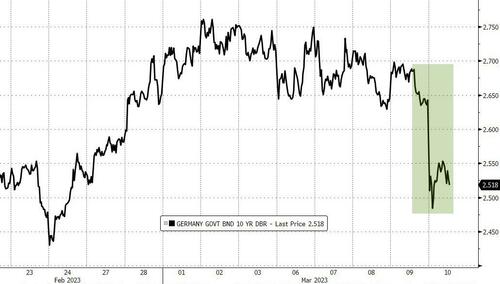

Europe’s Stoxx 600 equity gauge dropped more than 1%, with an index of bank stocks sliding the most since June. Bond markets were also roiled by the SIVB news, sending yields plunging and reversing sharp gains earlier this week following Powell’s hawkish speech. Treasuries extended gains for a second day, driving 10-year yields down by as much as 11 basis points to a three-week low, while German 10-year government borrowing costs were at one point poised for their biggest slump since early February.

In premarket trading, Shares of SVB – a major lender to startup companies – dropped 46% after a record 60% plunge on Thursday after a surprise announcement from SVB that it was holding a $2.25 billion share sale after a significant loss on its portfolio, which included US Treasuries and mortgage-backed securities. Other banks including JPMorgan and Bank of America also inched lower.

However, the big impact of SVB’s woes is that it has investors asking whether this be the start of a much bigger problem as attention turns to risks that may lurk in other financial institutions after the Fed’s steep rate hikes. Some market strategists said that the declines are likely to remain smaller Friday as the risk of contagion from SVB is relatively contained. Their thesis was not helped after several VC titans such as Peter Thiel’s Founders Fund and others advised portfolio businesses to withdraw their money.

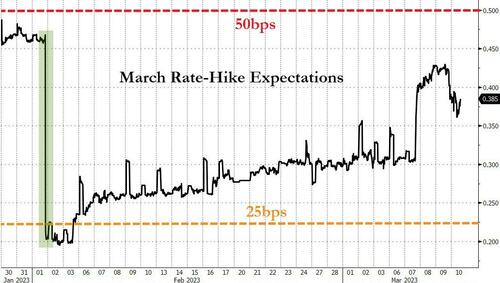

“The events around SVB highlight some of the additional risks of financial stress,” said Sarah Hewin, senior economist at Standard Chartered Bank in London. “There is a sense now of the bigger risks to the economy the more the Fed raises interest rates. At the margins it is raising the question of whether the Fed will indeed be able to do a 50 basis-point rate hike this month.”

“I suspect there’s some comfort that SVB’s troubles are not systemic as for the majority of banks — improving interest margins due to rising rates are offsetting losses on their long-duration investment portfolios,” said Marija Veitmane, senior multi-asset strategist at State Street Global Markets.

Here Are some of the other notable premarket movers:

Roblox (RBLX US) shares rise 2.2% as Jefferies raises the online games designer to buy from hold, saying it expects continued growth through near-term macro and competitive pressures.

Caterpillar (CAT US) shares fall 2.1% as UBS cuts the construction-machinery maker to sell from neutral, saying its growth momentum is not good enough to justify its valuation.

Oracle (ORCL US) fell 4.5% after the software company reported cloud license and on-premise license revenue that was weaker than expected. Overall revenue was essentially in line with the analyst consensus, while adjusted earnings were slightly stronger.

DocuSign (DOCU US) fell 13% after the e-signature company gave a first-quarter billings forecast that is weaker than expected. Analysts noted that the fourth-quarter results were strong but the company was re- investing much of its cost savings.

Allbirds (BIRD US) shares slump 22% after the sneaker brand reported fourth-quarter net revenue that missed estimates. Analysts noted a lower-than- expected first-quarter outlook.

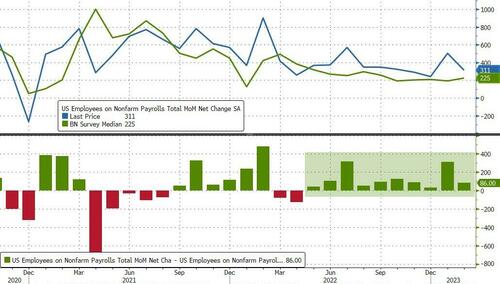

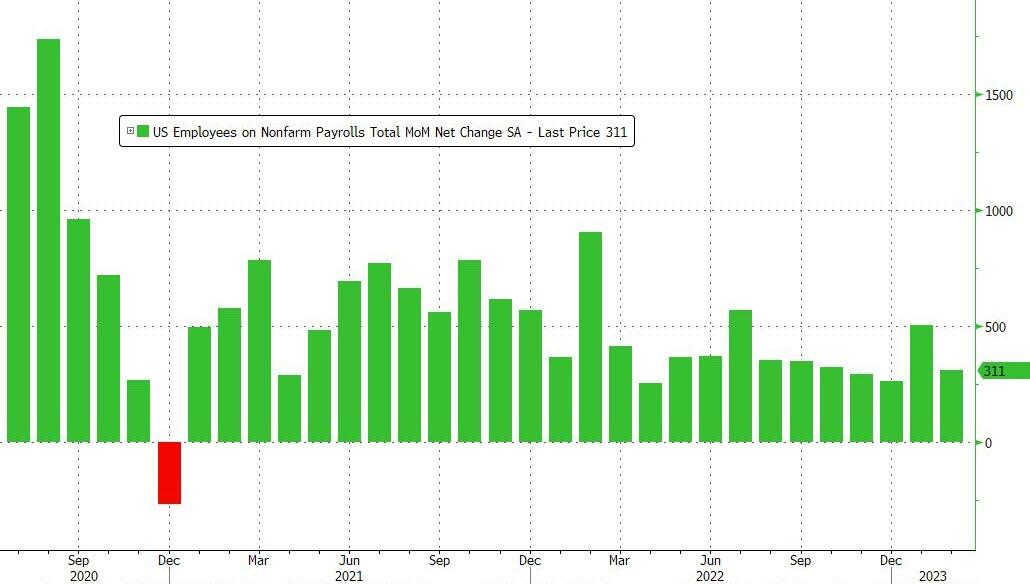

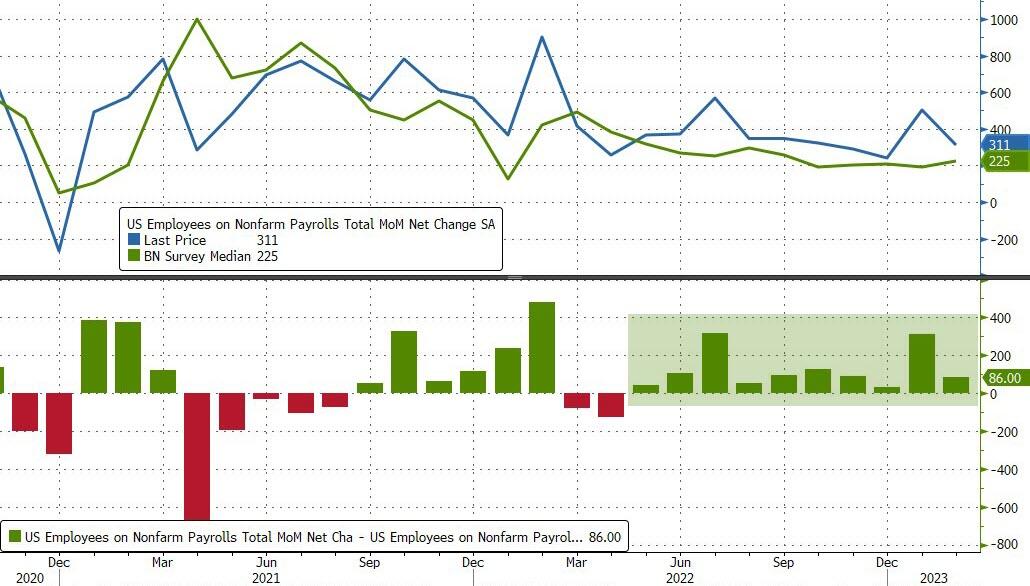

Meanwhile, all eyes today are on the jobs report for February, due at 8:30 a.m. in New York. Payroll growth has topped estimates for 10 straight months in the longest streak in decades, a trend that, if extended, will boost pressure on the Fed to keep hiking rates. Median estimate for February change in nonfarm payrolls is 225k after 517k gain in January, while crowd-sourced whisper number is 250k (our full preview is here).For today’s implied post-payrolls move, JPM’s Bram Kaplan estimates the options market is pricing a ~1.4% S&P 500 move for NFP. The bank’s chief economist, Mike Feroli, sees NFP to print around 200k vs 225k survey vs 517k prior and February Unemp rate to be same as Jan’s 3.4%, in line with consensus.

“For the Fed these ripples across the financial system will be something to monitor but they are much more focused on their inflation mandate,” said Georgina Taylor, head of multi-asset at Invesco. “A strong set of data “will keep pressure on the Fed,” she added.

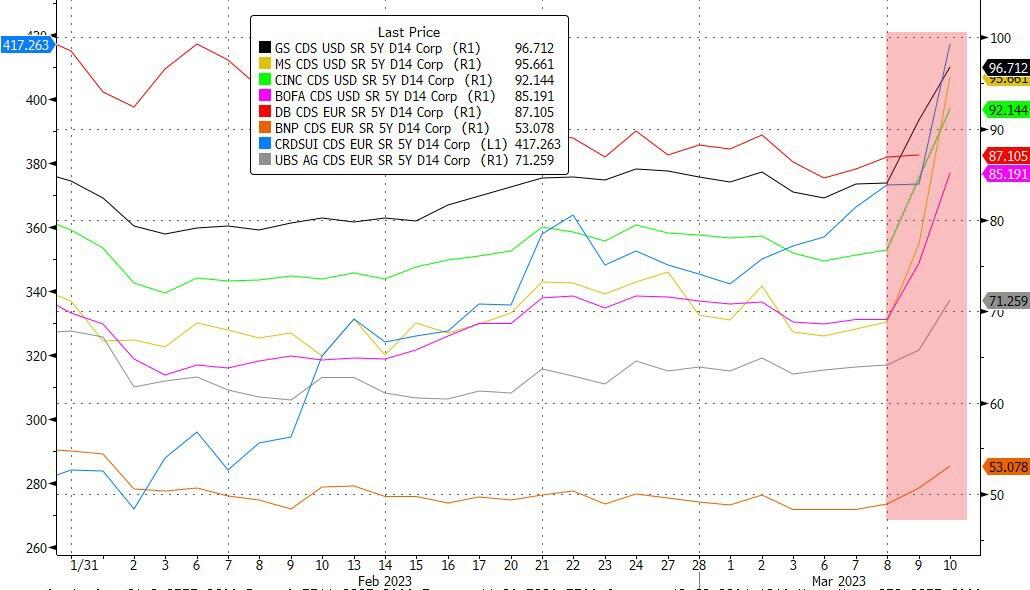

In Europe, banks and financial services are the worst-performing stock sectors, leading the Stoxx 600 down by as much as 1.9%, while bond-proxy utilities was the only sector up. European banks stocks slid on Friday and underperformed the broader market after after US peers plunged following the collapse of Silvergate Capital and concerns around SVB Financial. The Stoxx 600 Banks index dropped as much as 4.9%, the most since June; subindex is down 3.6% at 1:03pm CET, compared to a 1.2% decline for the Stoxx 600 benchmark. Deutsche Bank was the biggest faller in the subindex, down as much as 9.8%; HSBC, Santander, BNP Paribas and ING the other major drags on the index. UBS fell as much as 5.4% to drag on the Stoxx 600 Financial Services index; private equity investors Partners Group and EQT also sink, while Credit Suisse shares plunged as much as 6.1% to hit a new record low. Credit Suisse analyst Jon Peace says the drop for European banks, driven by worries about unrealized losses in bank bond portfolios, offers a buying opportunity (of course he would say that). Here are some of the most notable European movers:

Daimler Truck drops as much as 4.8% in Frankfurt after its fourth- quarter earnings miss and a broader selloff in cyclical shares overshadowed its 2023 outlook

Schroders shares fall as much as 4.3% after being cut to neutral from outperform at Credit Suisse as the broker sees the UK fund manager contending with headwinds

Bachem Holding falls as much as 8.5% after an offering of 1.25m shares priced at CHF86.50 apiece, representing a 5.9% discount to Thursday’s close

Kion falls as much as 6.7% after being cut to equal-weight from overweight at Morgan Stanley with the broker seeing an uncertain picture for price-volume dynamics at the forklift maker in 2023

Casino shares fall as much as 5.8% after the French grocer reported trading profit for the full year that missed the average analyst estimate

Mobilezone shares decline as much as 9.3% after it announced disappointing weaker gross and Ebit margins

OTP Bank shares decline as much as 1.9% after Hungary’s largest lender said 2022 profit fell after it booked a slew of charges linked to the war in Ukraine

Vodafone shares rise as much as 1.7% after Bloomberg reported that the UK telecom operator is at the final stages of talks to merge its British operations with Three UK

Breedon rises as much as 5% after Abicad Holding said it is acquiring about 5.3m ordinary shares at price of 75p apiece, representing a premium to the last close

U-blox shares climb as much as 11% after the Swiss position-systems provider reported strong profitability and free cash flow for 2022

Leonardo gains as much as 2.9% after the Italian defense group projected profit for 2023 that was slightly ahead of estimates

Earlier in the session, stocks in Asia tumbled, following US financial shares lower, after warnings from Silicon Valley bank led to concern about the broader sector, and the yen slides as the BOJ leaves policy unchanged. The Nikkei slumps 1.6% and Topix is 1.7% lower. China’s Shanghai Composite Index falls 1.2% and the CSI 300 slips 1.1%. Hong Kong shares also decline with the benchmark down 2.5% and Hang Seng Tech Index down 3.6%.

Japanese stocks had their biggest drop in more than five months as shares of the nation’s major lenders tumbled after the Bank of Japan’s decision to leave policy unchanged set off a plunge in bond yields. The Topix fell 1.9% to 2,031.58 as of the 3 p.m. close in Tokyo, having its steepest drop since Sept. 26. Mitsubishi UFJ Financial contributed the most to the decline, falling 6.1%. Out of 2,160 stocks in the index, 159 rose and 1,953 fell, while 48 were unchanged. The Nikkei 225 fell 1.7% to 28,143.97. The Topix’s gauge for banks slid the most in three years, with Sumitomo Mitsui Financial and Mizuho Financial each falling at least 4.9%. Banks also dropped after their US peers slumped on concerns that signs of trouble at a Silicon Valley-based lender may point to broader risks for the sector. “Perhaps some investors were hoping for a review of yield curve control after the BOJ’s monetary policy meeting,” said Tomoaki Kawasaki, a senior analyst at Iwaicosmo Securities Co. “There was probably some talk about Silicon Valley in the morning, and the stock market was falling a little.”

Australia’s stocks slumped the most in six months: the S&P/ASX 200 index fell 2.3% to close at 7,144.70, posting its biggest decline since mid-September after concerns over a Silicon Valley-based lender sapped investor appetite. Banks were among the biggest drags on the Australian gauge, following their Wall Street peers lower as troubles at SVB Financial Group spurred concerns about the wider lending sector. Read: Asian Bank Stocks Drop to Two-Month Low on SVB Worries In New Zealand, the S&P/NZX 50 index fell 0.8% to 11,727.04.

India’s banking stocks posted their biggest slump in more than a month to lead declines as the nation’s benchmark gauges joined a global selloff triggered by worries over the health of the US banking system. The S&P BSE Sensex fell 1.1% to 59,135.13 in Mumbai, while the NSE Nifty 50 Index declined 1%. Friday’s selloff saw both benchmarks end the week atleast a percent lower. For the year, the measures have lost 2.8% and 3.8%, respectively. HDFC Bank contributed the most to the Sensex’s decline, with a 2.6% fall on Friday. Of the 30 shares in the Sensex index, 21 dropped and nine advanced. Fifteen of 20 sector gauges compiled by BSE Ltd. closed lower, led by the banking index which fell 1.9%, its biggest drop since Jan. 27. Banking and financial stocks, with nearly 40% weight in the benchmarks, have been among the prominent decliners recently with higher interest rates expected to impact margins as well as hurt demand for fresh loans.

The Bloomberg Dollar Spot Index inched lower for a second day and the greenback traded mixed against its Group-of-10 peers. Treasuries extended a rally across the curve as money markets eased Fed tightening bets. Euro-area and UK bonds also rallied in early trade, with short-dated debt outperforming amid demand for haven assets and amid paring of central bank hikes. The euro rose to trade around $1.06. The cost of converting euro payments into dollars using cross-currency basis swaps rises at the European open as demand for the greenback surges

The pound rose, buoyed by stronger-than-forecast data on UK economic growth in January, which added to evidence of resilience in the face of a cost-of-living squeeze and widespread industrial unrest. Gilts followed moves in European bonds and Treasuries

Norway’s krone slumped after data showed the headline inflation rate declined to 6.3% in February, versus the median projection of 6.8% in a Bloomberg poll of analysts that was the same as the central bank’s estimate. Underlying inflation, the measure followed by Norges Bank, also declined from an all-time high to 5.9%, matching the central bank’s view, while analysts had expected a smaller slowdown

The yen reversed gains and government bonds advanced after the BOJ kept its policy settings for its negative interest rate and yield curve control program unchanged at Governor Haruhiko Kuroda’s last meeting

Australian sovereign bonds extended opening gains after the BOJ left its key policy rates unchanged. Aussie dollar dips were bought into by exporters and leveraged funds squaring up before US jobs data later today

Global bonds broadly rally: Treasuries are richer across the curve, extending Thursday’s sharp rally, while off session highs reached during European morning as stock futures pare losses. Yields are richer by 3bp-6bp across the curve led by intermediates, steepening 5s30s spread by 3bp on the day and adding to Thursday’s aggressive bull-steepening move; 10-year yields around 3.85%, richer by 5bp vs Thursday’s after touching 3.797%, lowest since Feb. 16. Flight-to-quality backdrop remains a theme, supporting Treasuries, amid mounting worries about contagion in US banking system from SVB Financial’s slump. Treasury yields underperform gilts and bunds across the curve as they catch up to Thursday’s action. Peripheral spreads widen to Germany. Bloomberg dollar spot index is flat.

In commodities, WTI Crude continues its decline trading ~$75. Spot gold rises roughly $3 to trade near $1,834/oz.

Looking to the day ahead now, the main highlight will be the aforementioned US jobs report for February. Other releases include the UK’s GDP for January. And from central banks, we’ll hear from the ECB’s Panetta.

Market Snapshot

S&P 500 futures down 0.2% to 3,910.75

MXAP down 1.9% to 156.95

MXAPJ down 1.8% to 502.93

Nikkei down 1.7% to 28,143.97

Topix down 1.9% to 2,031.58

Hang Seng Index down 3.0% to 19,319.92

Shanghai Composite down 1.4% to 3,230.08

Sensex down 1.1% to 59,130.19

Australia S&P/ASX 200 down 2.3% to 7,144.69

Kospi down 1.0% to 2,394.59

STOXX Europe 600 down 1.3% to 453.84

German 10Y yield little changed at 2.53%

Euro up 0.2% to $1.0597

Brent Futures down 0.3% to $81.35/bbl

Gold spot up 0.3% to $1,836.92

U.S. Dollar Index down 0.14% to 105.16

Top Overnight News from Bloomberg

President Joe Biden and European Commission leader Ursula von der Leyen will likely make their meeting at the White House on Friday convivial, despite trade tensions and the pressure of the war in Ukraine

UK GDP grew 0.3% in January, recovering part of a 0.5% decline in December when strikes halted activity, Office for National Statistics figures show. Economists forecast growth of 0.1% in January

Janus Henderson’s emerging-market hard currency debt fund has a “cautious overweight” on Argentina as the bonds are cheap and there’s expectation of a change in government at the October election, Thomas Haugaard says

The ECB will step up its fight against stubborn inflation by raising interest rates four more times and unwinding its €5 trillion ($5.3 trillion) bond portfolio at a quicker pace, according to a Bloomberg survey of economists

Japan’s broken bond market gave Governor Haruhiko Kuroda one last salute at his final policy meeting, when one of the 10-year tenors saw its yield turn negative

For the first time in years, the euro is poised to offer better returns than its Nordic counterparts. Should money-market wagers materialize, the ECB deposit rate will climb above the Norges Bank key rate for the first time ever and will surpass the Riksbank’s benchmark after five years lagging

Japan’s parliament gave a green light for veteran economics professor Kazuo Ueda to take the helm of the BOJ next month in the first change of governor in a decade

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks declined amid headwinds from the banking sell-off in the US owing to contagion fears related to Silicon Valley Bank in which shares of the group dropped more than 60% during Wall St trade and resulted in the four biggest US banks shedding a total of more than USD 50bln in market cap, while SVB suffered another 20% drop after-hours as funds advised companies to pull out of the lender. ASX 200 was pressured by losses in its largest-weighted financial industry on spillover selling from stateside peers and with the index also hit by weakness in the commodity-related sectors. Nikkei 225 declined with risk sentiment dampened following mixed household spending data and with banking shares further hit after the BoJ maintained its ultra-loose policy settings. Hang Seng and Shanghai Comp. conformed to the downbeat mood with Hong Kong underperforming amid a tech rout as JD.com shares suffer a double-digit drop despite beating on the bottom line, while property stocks are also in focus as shares in developer Kaisa initially dropped around 40% post-earnings and on return from a 12-month trading halt.

Top Asian News

China’s parliament elected Chinese President Xi for a third term as President and as Central Military Commission Chairperson, while the NPC also elected Zhao Leji as NPC Standing Committee Chairperson and Han Zheng as China’s Vice President.

US is working to close a loophole in the export ban related to China’s Inspur (000977 CH), while it was also reported that Senator Rubio introduced legislation seeking to block tax credits for batteries produced by the planned Ford (F) plant using Chinese technology.

BoJ kept policy settings unchanged, as expected, with rates held at -0.10% and QQE with yield curve control maintained to target 10yr JGB yields at around 0%, while it kept the band around the yield target at +/-50bps with the decision on YCC made by unanimous vote. BoJ also maintained its forward guidance on interest rates and said Japan’s economy is picking up with the economy expected to recover as the impact of the pandemic and supply constraints fade, while it stated that core consumer inflation is moving around 4% and inflation expectations are heightening.

BoJ’s Kuroda: premature to debate the specifics on the exit from monetary easing, policy rate and balance sheet the main things to consider when the debate begins; exit must be conducted only when 2% inflation is sustainably and stably achieved.

Japan’s upper house approved the appointment of Kazuo Ueda as the next BoJ Governor, while it approved the appointment of Shinichi Uchida and Ryozo Himino as Deputy Governors, as expected.

European bourses are lower across the board, Euro Stoxx 50 -1.5%, as contagion fears from SVB dents risk sentiment and weighs heavily on banks, SX7P -4.0%. As such, the Banking sector is underperforming with the exception of Utilities; aside from the above, pertinent movers on the upside are limited to Leonardo and Vodafone. Stateside, futures remain under pressure with the ES around 3900 while the NQ is the relative outperformer, and little changed overall, with yields lower amid haven action and as participants prepare for NFP.

Top European News

US President Biden and European Commission President von der Leyen have agreed to launch talks on critical mineral and subsidies, according to a senior US official; expects to discuss strengthening cooperation on Russian sanctions.

UK PM Sunak is to unveil up to GBP 5bln additional cash for defence, according to The Times.

Reuters poll showed all 60 economists surveyed unanimously forecast the ECB to hike the Deposit Rate by 50bps to 3.00% at its meeting next week, while expectations are for the Deposit Rate to peak at 3.75% in Q3 vs prev. forecast of a peak at 3.25% in Q2.

5.6 magnitude earthquake occurs in northern Colombia, via EMSC.

FX

The USD has failed to benefit from the broader risk tone, with the DXY underpressure though yet to test the 105.00 mark to the downside within 105.07-36 parameters.

JPY is the standout laggard, with USD/JPY testing 137.00 from a 135.82 base as hawkish positioning unwound following Kuroda’s last BoJ, where policy parameters were maintained.

At the other end of the spectrum is GBP, with firmer-than-expected headline GDP data and technicals via EUR/GBP assisting to lift Cable above 1.20; specifically, EUR/GBP moved below the 21- & 50-DMA’s of 0.8849 and 0.8838 in relatively quick succession.

Elsewhere, the CHF benefits on haven-flows while peers ex-JPY are generally firmer against the USD pre-NFP; CAD, ahead of its own jobs report, is litle changed in narrow 1.3823-3861 parameters.

Fixed Income

Core and periphery EGBs are benefiting from the glum risk tone; though, the benchmarks have eased from initial extremes as newsflow slows pre-NFP.

Specifically, Bunds are now below 133.00 within 132.37-133.82 ranges; Gilts back towards 101.16 vs 102.00+ best and USTs at 112.00 despite being 13 ticks above the mark earlier.

Amidst this, yields are lower across the curve with action in US yields most pronounced in the belly.

Commodities

Crude and base metals are dented by the deterioration in risk sentiment, with spot gold gleaning some modest upside from this.

Currently, WTI and Brent are just off initial lows within ranges of circa. USD 1/bbl while base metals are, broadly speaking, softer across the board with LME nickel particularly afflicted.

For gold specifically, the yellow metal briefly surmounted its 21-DMA and yesterday’s best at USD 1834/oz and USD 1835/oz respectively, but remains only modestly firmer overall.

Saudi Aramco is to supply full contract volumes of oil to at least four north Asian refiners in April.

North Korean leader Kim oversaw the fire assault drill on Thursday and the drill proved the capability to counter an actual war, while shells were aimed at simulated targets of enemy airport. Furthermore, North Korean leader Kim said the army should be ready to fight at any time citing ‘frantic war preparation moves’ by the enemy, according to KCNA.

US is to hold an informal meeting of UN Security Council members next week regarding human rights abuses in North Korea, according to Reuters.

Russian Deputy Foreign Minister Ryabkov says that Russia and the US remain in contact over the New START Treaty but progress is not expected from these contacts.

US Event Calendar

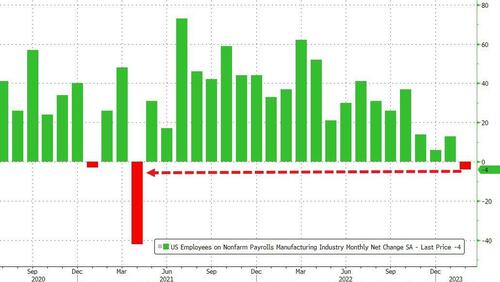

08:30: Feb. Change in Nonfarm Payrolls, est. 225,000, prior 517,000

Change in Private Payrolls, est. 215,000, prior 443,000

Change in Manufact. Payrolls, est. 10,000, prior 19,000

Unemployment Rate, est. 3.4%, prior 3.4%

Underemployment Rate, prior 6.6%

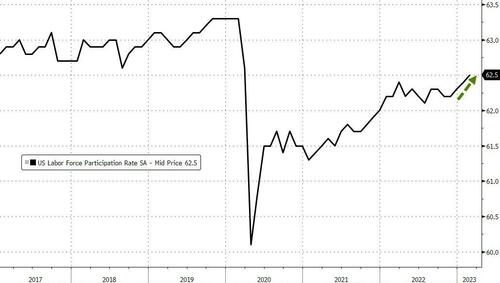

Labor Force Participation Rate, est. 62.4%, prior 62.4%

Average Weekly Hours All Emplo, est. 34.6, prior 34.7

Average Hourly Earnings YoY, est. 4.7%, prior 4.4%

Average Hourly Earnings MoM, est. 0.3%, prior 0.3%

14:00: Feb. Monthly Budget Statement, est. -$263b, prior -$216.6b

DB’s Jim Reid concludes the overnight wrap

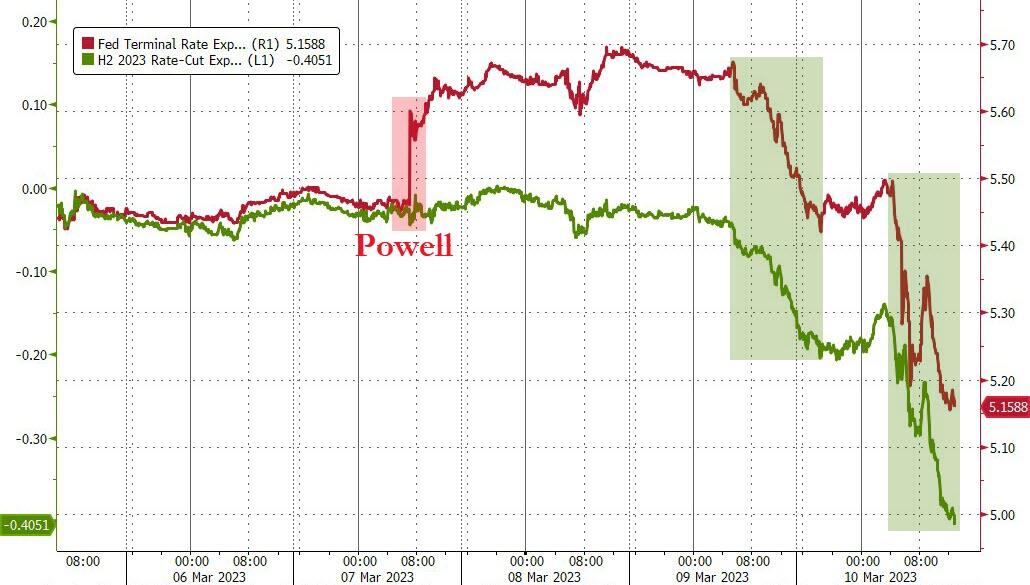

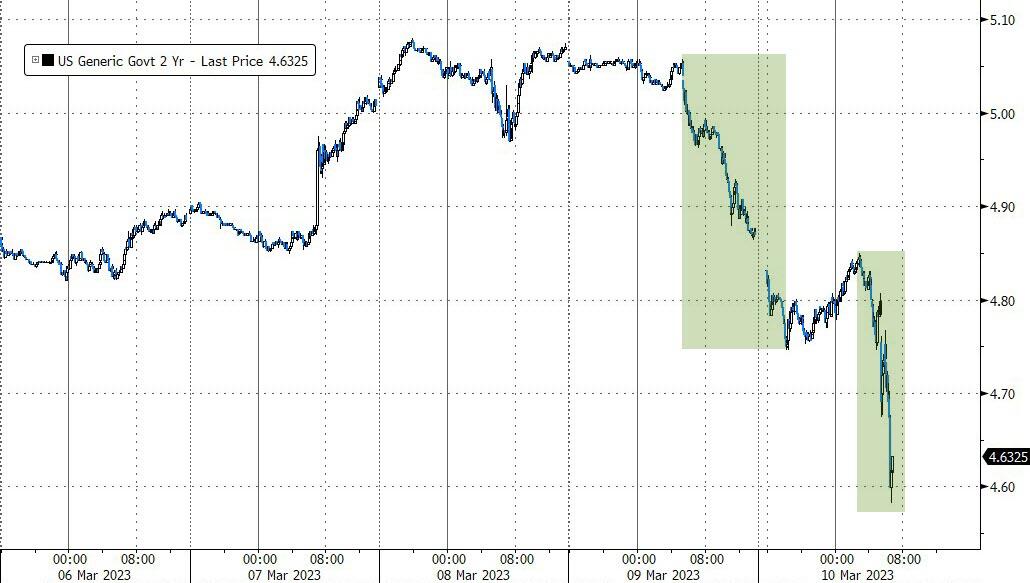

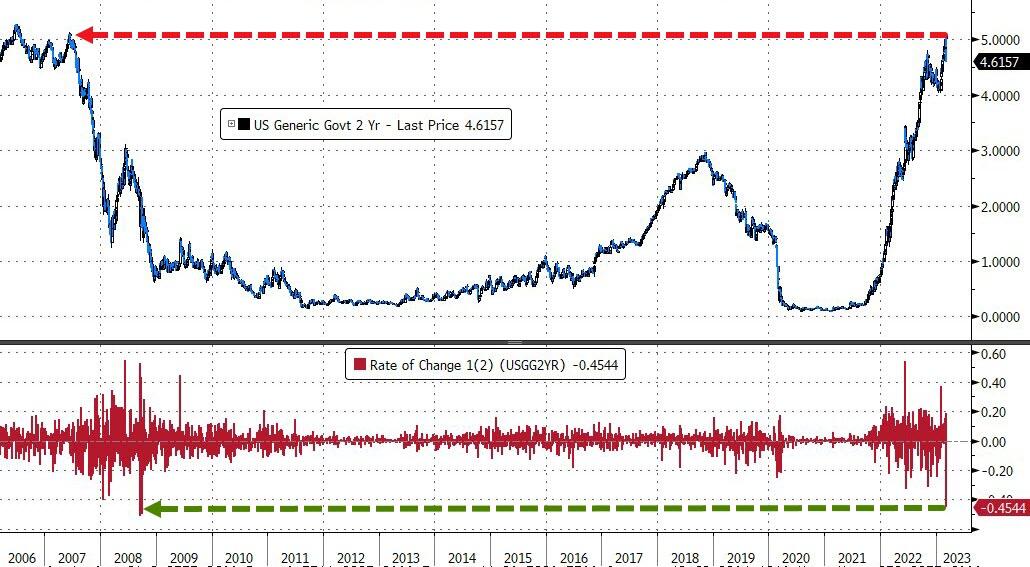

What do you get when you see one of the biggest hiking cycles on record, alongside one of the most inverted yield curves in history, at the same time as seeing one of the biggest tech bubbles bursting in history, coupled with runaway growth in private markets. The answer is that you get nights like yesterday where SVB (Silicon Valley Bank) Financial Group, closed -60.41% lower on the day, wiping out $9.6bn of market value. Although this story was brewing in the background for much of the day, it wasn’t until Europe went home that it exploded on the global macro stage as the S&P 500 went from around flat at that point to close -1.85%, with the KBW US bank index (-7.7%) seeing its worst day since June 2020. Rates saw a huge rally, especially at the front end as we’ll see below.

For background, SVB focuses on servicing emerging to middle-market growth technology companies that are usually backed by venture-capital firms. They announced that they had large losses on security sales and would be undergoing a stock offering to shore up its balance sheet. Silicon Valley Bank’s CEO pointed to the expectation of higher rates and persistent client outflows as to why the lender incurred a one-time $1.8bn loss on a security portfolio sale. Considering the client outflows are also likely driven by higher interest rates, it is not a stretch to say that this episode is emblematic of the higher-for-longer rate regime we appear to be at the start of, as well as inverted curves, and a tech venture capital industry that’s been seeing much tougher times of late. The perfect storm of all the things we’ve been worrying about in this cycle.

Sentiment across markets soured following the spreading of the SVB news. The KBW Bank index saw all of its 24 index member lower on the day with some high-profile names like JPM (-5.41%), BofA (-6.20%) and Citi (-4.10%) also much lower. The index has been down every day this week, with the 4-day performance (-12.31%) also the worst 4-day performance for US banks since June 2020.

We’ll have to see how this story develops but something always breaks hard during or after a Fed hiking cycle. Is this another mini wobble on this front or the start of something bigger? Tough to tell but I would be stunned if there weren’t many more casualties of this boom-and-bust cycle. Don’t forget, we haven’t been in recession yet. Imagine superimposing that on the leveraged world we live in.

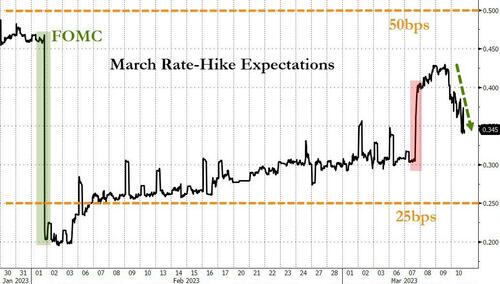

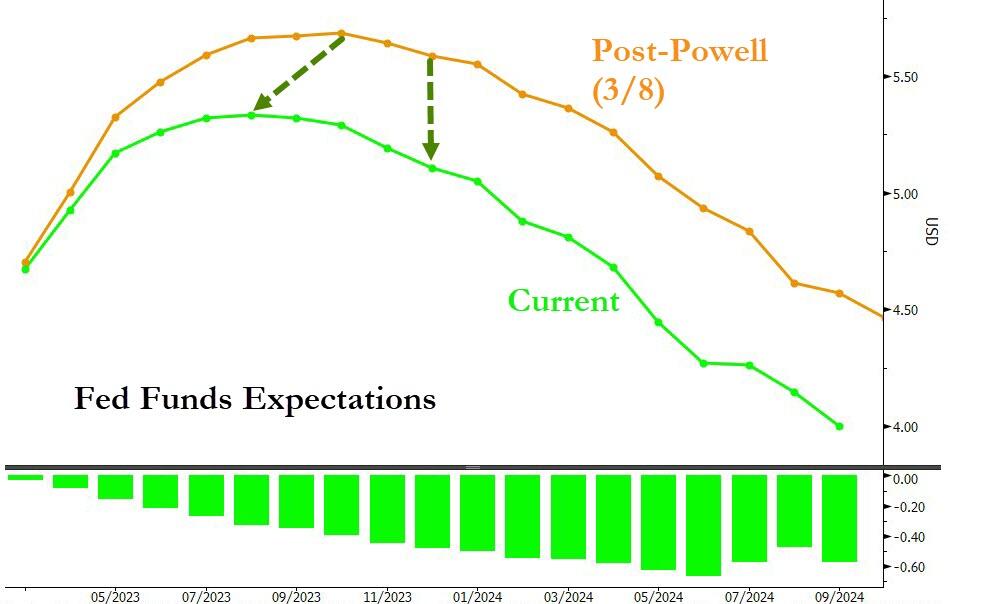

It’s fair to say a new payrolls Friday comes at a fraught moment with today’s probably up there with the most closely anticipated in recent times. This is before we see US CPI next Tuesday and what both imply for the March FOMC the following week. With such an outsized beat last month (+517k vs. 189k expected) it’s fair to say no-one has any real idea of what random number will be churned out today. Having said that, both 25bps and 50bps are in play for the FOMC and today and Tuesday will probably be swing factors with Fed Chair Powell stressing that “no decision has been made on this” earlier this week. SVB has to be thrown into the mix too.

As we look forward to the jobs report, the recent momentum behind a 50bp hike actually stalled slightly yesterday even before the SVB story spread. This was driven by the latest round of weekly jobless claims data coming in beneath expectations. In terms of the specifics of the release, initial jobless claims came in at 211k over the week ending March 4 (vs. 195k expected). That’s their highest level so far in 2023, and marks an unusually large surprise on the upside as well, having come in above every economist’s estimate on Bloomberg. In absolute terms, the surprise of +16k above consensus is also the biggest weekly surprise on the upside in 9 months, so this isn’t the sort of report we see often. There was some weather distortions, with California (+10k) seeing a spike following massive snow storms and making up nearly a third of the increase in NSA claims (+35k). We will see how this evolves over the next couple of prints. And at the same time, there was a negative story from the continuing claims release as well, which came in at 1.718m over the week ending February 25 (vs. 1.660m expected).

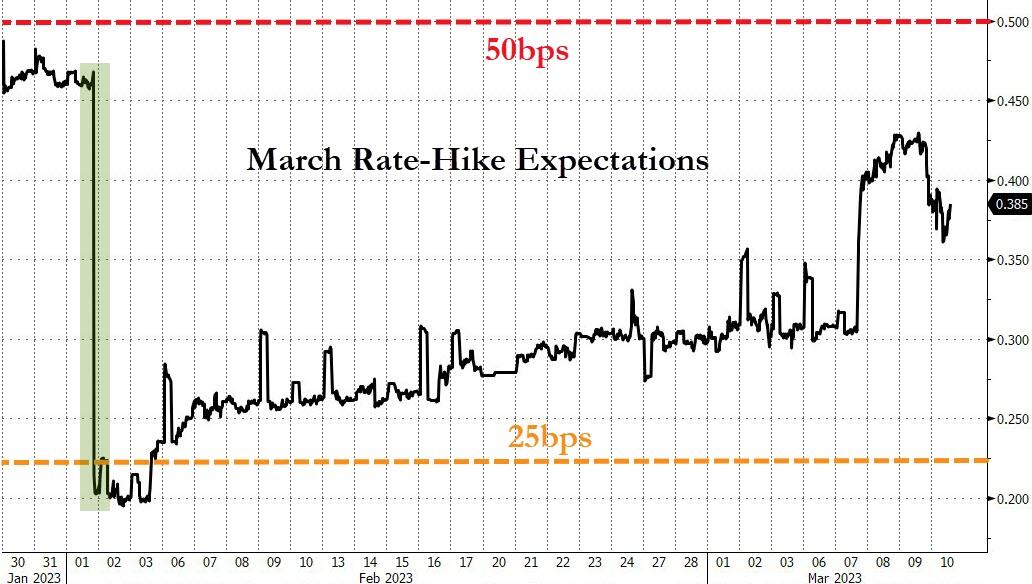

With the labour market appearing softer than otherwise expected, investors moved to dial back the amount of rate hikes priced for the months ahead. Looking on an intraday basis, expectations of the terminal rate had been at 5.67% immediately prior to the claims report, but fell to 5.61% shortly after, before ending the day -15.9bps lower at 5.515% for the July meeting after the SVB story. At the highs of the day, there was a 74% chance of a 50bp rate hike later this March, before the risk-off sentiment took the probability of a 50bp hike back down to 56% by the close.

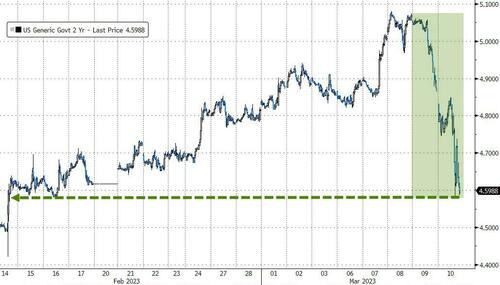

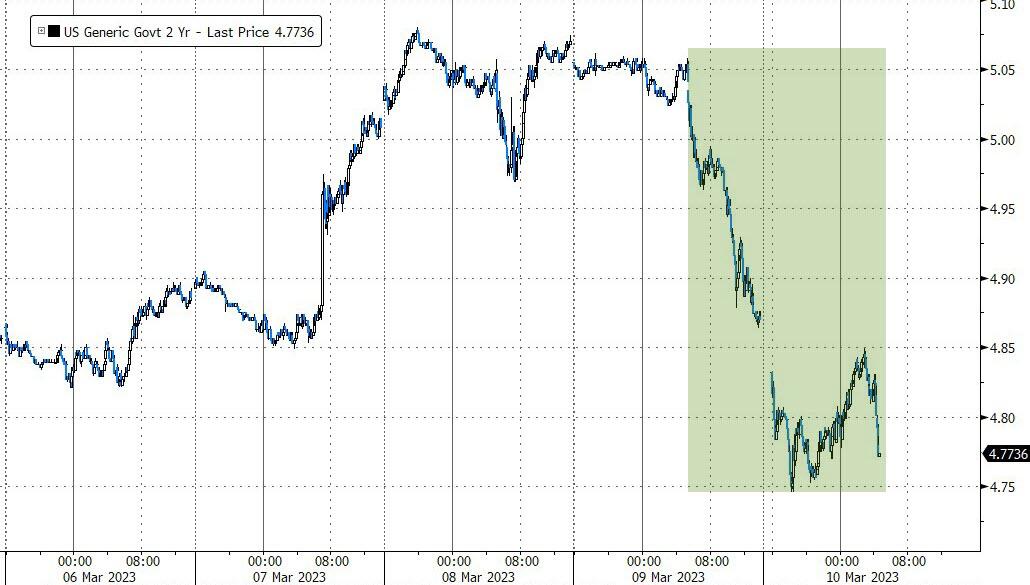

The broader sell-off across risk markets meant that the 2yr yield saw its biggest daily decline since January 6, thanks to a -20.0bps move to 4.87%. Longer-dated Treasuries also advanced, with the 10yr yield down -8.8bps to 3.90% and it even meant that the 2s10s curve steepened for the first time in a week as well, closing +11.4bps at -97.3bps. Both 2 and 10yr yields are down around another -8.5bps overnight.

Back to the S&P 500, every industry group was lower and only 26 index constituents were higher. Sector performance has tilted toward defensive non-cyclicals recently with utilities (-0.84%) and consumer staples (-0.95%) selling off less yesterday than cyclical peers such as materials (-2.54%) and autos (-4.76%). Over in Europe, the STOXX 600 (-0.22%) posted a small decline as well, though trading had closed before the deeper US sell-off.

The focus on the US labour market will of course be the main one today with the February jobs report. In terms of what to expect, our US economists think that nonfarm payrolls will have grown by +300k in February, in part thanks to mild weather during the survey week. That would be some way above the +225k consensus view, and would keep the unemployment rate at a 53-year low of 3.4%, with a risk it could round down to 3.3% if participation contracts slightly. This report will be very important when it comes to the Fed’s meeting on March 22, as what we’ve heard so far suggests that both 25 and 50bp hikes are still in play. Indeed, Chair Powell went out of his way while in Washington DC on Wednesday to say “I stress that no decision has been made on this”.

On the topic of Washington, President Biden unveiled the administration’s initial 2023 budget proposal yesterday afternoon. The $6.9tr budget proposal is viewed as an opening bid to House GOP members, who are expected to negotiate it down in the upcoming debt ceiling negotiations. The proposal increases funding on an array of government programs, including making Medicare more solvent, lowering prescription drug prices, and trimming the deficit by $3 trillion over the next decade. The deficit cutting is mostly coming in the form of higher taxes on capital gains (25% on those making over $1mn), a new tax bracket of 39.6% on every dollar made over $400k, a minimum 25% on billionaires, and hiking the corporate tax rate from 21% to 28%. Republicans have already called the proposal a non-starter, with Speaker McCarthy saying that he does “not believe raising taxes is the answer.” There was no House budget plan yet, as Speaker McCarthy said that Republicans wanted to analyse the White House’s budget first. The opening salvo does nothing to lower expectations of a protracted debt ceiling fight.

Returning to the theme of central banks, overnight the Bank of Japan (BOJ) left its key interest rate unchanged at -0.1%, while maintaining its YCC policy. In his last meeting as the BOJ’s Governor, Haruhiko Kuroda made no surprise move and lent support to the central bank’s long-standing ultra-dovish monetary policy. Following the decision, the Japanese yen lost ground, weakening as much as -0.6% against the dollar before cutting losses to trade at 136.53 per dollar as we go to press. Meanwhile, the Japan’s upper house in parliament has formally approved the appointment of Kazuo Ueda to be the next central bank chief in April. Additionally, the parliament also approved Shinichi Uchida and Ryozo Himino as the next BOJ Deputy Governors.

Following a weak handover from Wall Street overnight, Asian stocks are also trading lower. Across the region, the Hang Seng (-2.46%) is sharply lower, wiping out all the YTD gains with the CSI (-1.12%), the Shanghai Composite (-1.15%), the Nikkei (-1.59%) and the KOSPI (-1.05%) also tumbling this morning amid contagion worries related to SVB. Outside of Asia, US stock futures are indicating further losses with contracts tied to the S&P 500 (-0.78%) and NASDAQ 100 (-0.54%) quite weak for an overnight session. Bitcoin dropped below the key $20,000 mark in Asia trading hours for the first time since mid-January, reversing its strong 2023 uptrend.

Back in Europe yesterday, it was a fairly quiet day on the whole, with the focus now turning to next Thursday’s ECB meeting. Ahead of that, sovereign bonds rallied for the most part with very modest reductions for yields on 10yr bunds (-0.3bps) and OATs (-0.1pbs), alongside larger reductions at the front end. We will be set for a big rally this morning though given the late news last night. The only ECB official we did hear from yesterday was France’s Villeroy, who said “We will bring inflation toward 2% by the end of 2024 or beginning of 2025 – that’s a commitment, not just a forecast.” Investors have almost fully priced in a 50bps increase at the next meeting (97%), but there’s a bit more doubt over what they’ll do in May still, with 50bps considered the most likely as per our own House View, but with only a 74.7% chance of such a move.

To the day ahead now, and the main highlight will be the aforementioned US jobs report for February. Other releases include the UK’s GDP for January. And from central banks, we’ll hear from the ECB’s Panetta.

end

AND NOW NEWSQUAWK (EUROPE/REPORT)

SVB contagion fears weigh on sentiment in pre-NFP trade – Newsquawk US Market Open

FRIDAY, MAR 10, 2023 – 06:27 AM

European bourses are lower across the board, Euro Stoxx 50 -1.5%, as contagion fears from SVB dents risk sentiment and weighs heavily on banks, SX7P -4.0%.

Stateside, futures remain under pressure with the ES around 3900 while the NQ is the relative outperformer, and little changed overall, with yields lower.

USD has failed to benefit from the risk tone while JPY lags as hawkish bets unwind post-BoJ and GBP outperforms after data and aided by EUR/GBP technicals.

Core and periphery EGBs are benefiting from the glum risk tone; though, the benchmarks have eased from initial extremes as newsflow slows pre-NFP.

Crude and base metals are dented by the deterioration in risk sentiment, with spot gold gleaning some modest upside from this.

Looking ahead, highlights include US & Canadian Labor Market Reports and ECB’s Lagarde (Note, the ECB is in its quiet period).

Or why not try Newsquawk’s squawk box free for 7 days?

EUROPEAN TRADE

EQUITIES