MARCH 13/2023//THE FED/TREASURY AND FDIC MOVES TO SAVE DEPOSITORS AND THUS FORGOING A BANKING CRISIS: GOLD CLOSED UP $48.84 TO $1911.15//SILVER CLOSED UP $1.15 TO $21.82//PLATINUM CLOSED UP $43.40 TO $1003.70//PALLADIUM CLOSED UP $116.10 TO $1489.15//CHRONOLOGICAL EVENTS RE SILICON VALLEY BANK LEADING TO A 3 BANK BAILOUT//IMPORTANT COMMENTARIES FOR TODAY: MATHEW PIEPENBURG AND TOM LUONGO//CREDIT DEFAULT SWAPS RISE IN VALUE INDICATING HUGE RISK TO THE SOLVENCY OF THE BANK//HSBC TAKES OVER UK ASSETS FOR SILICON VALLEY BANK//RUSSIA VS UKRAINE UPDATES//COVID UPDATES//DR PANDA/DR PAUL ALEXANDER//VACCINE IMPACT//SLAY NEWS//SWAMP STORIES FOR YOU TONIGHT//

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR MAR/2023. CONTRACT: 9 NOTICES FOR 900 OZ or 0.02799 TONNES

total notices so far: 3021 contracts for 302100 oz (9.3965 tonnes)

SILVER NOTICES: 21 NOTICE(S) FILED FOR 105,000 OZ/

total number of notices filed so far this month : 2968 for 14,840,000 oz

END

GLD

WITH GOLD UP $48.85

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES FROM THE GLD//////(VERY STRANGE)

INVENTORY RESTS AT 901.42TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $1.35

AT THE SLV// NO CHANGES IN SILVER INVENTORY AT THE SLV: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 478.879. MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 558 CONTRACTS TO 128.972 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE STRONG SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR STRONG $0.36 GAIN IN SILVER PRICING AT THE COMEX ON FRIDAY. OUR NEW LOW COMEX OI SILVER WAS SET AT 121,299 MARCH 3/2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.36). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS, AS WE HAD A HUMONGOUS GAIN ON OUR TWO EXCHANGES 1571 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 1 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD: A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS( 850 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.58 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE JUMP OF NIL OZ//NEW STANDING: 15.120 MILLION OZ + THE 1.0 MILLION OZ OF EXCHANGE FOR RISK//THUS TOTAL NEW STANDING 16.120 MILLION OZ/ //// V) STRONG SIZED COMEX OI GAIN/ STRONG SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –162 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTRACTS for 9 days, total 4987 contracts: OR 24.935 MILLION OZ . (554 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 24.935 MILLION OZ

.

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 24.935 MILLION OZ//INITIAL

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 559 WITH OUR $0.36 GAIN IN SILVER PRICING AT THE COMEX//FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 850 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAR OF 15.58 MILLION OZ//FIRST DAY NOTICE// FOLLOWED BY TODAY’S NIL OZ QUEUE JUMP (WHICH INCREASES THE AMOUNT OF SILVER STANDING) + 1.0 MILLION OF EXCHANGE FOR RISK ISSUED EARLY IN MARCH (INCREASES THE AMOUNT OF SILVER STANDING) //NEW STANDING 16.120 MILLION OZ .. WE HAVE A HUMONGOUS SIZED GAIN OF 1409 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 21 NOTICE(S) FILED TODAY FOR 105,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A HUGE SIZED 15,542 CONTRACTS TO 469,801 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 441 CONTRACTS.

.

WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI ( 15,002 CONTRACTS) WITH OUR $31.60 GAIN IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR MAR. AT 4.9953 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 22,100 OZ (0.6874 TONNES) //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S ) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London).

YET ALL OF..THIS HAPPENED WITH OUR $31.60 GAIN IN PRICEWITH RESPECT TO FRIDAY’S TRADING

WE HAD A HUMONGOUS SIZED GAIN OF 22,367 OI CONTRACTS (69.570 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7366 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 469,801

IN ESSENCE WE HAVE A HUMONGOUS INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 22,367 CONTRACTS WITH 15,001CONTRACTS INCREASED AT THE COMEX AND 7366 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 22,367 CONTRACTS OR 6.790 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (7366 CONTRACTS) ACCOMPANYING THE HUGE SIZED GAIN IN COMEX OI (15,001) TOTAL GAIN IN THE TWO EXCHANGES 22,367 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR MAR. AT 4.9953 TONNES FOLLOWED BY TODAY’S 22,100 OZ QUEUE JUMP//NEW STANDING 10.258 TONNES // ///3) ZERO LONG LIQUIDATION //4) HUGE SIZED COMEX OPEN INTEREST GAIN// 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

TOTAL EFP CONTRACTS ISSUED: 33,448 CONTRACTS OR 3,344,800 OZ OR 104.037 TONNES IN 9 TRADING DAY(S) AND THUS AVERAGING: 3716 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES 104.037 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 104.037/3550 x 100% TONNES 2.92% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 104.037 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A STRONG SIZED 559 CONTRACTS OI TO 128,972 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A RECORD LOW OF 121,299 CONTRACTS MARCH 3/2023.

EFP ISSUANCE 850 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 850 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 850 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 559CONTRACTS AND ADD TO THE 850 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE GAIN OF 1409 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES //7.045 MILLION OZ

OCCURRED WITH OUR $0.36 GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)MONDAY MORNING//SUNDAY NIGHT

SHANGHAI CLOSED UP 38.62 PTS OR 1.20% //Hang Seng CLOSED UP 376.05 PTS OR % 1.95 /The Nikkei closed DOWN 311.01% PTS OR 1.11% //Australia’s all ordinaries CLOSED DOWN 0.51% /Chinese yuan (ONSHORE) closed UP 6.8724//OFFSHORE CHINESE YUAN UP TO 6.8928// /Oil DOWN TO 75.31 dollars per barrel for WTI and BRENT AT 80.98 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A HUGE SIZED 15,001 CONTRACTS UP TO 469,268 WITH OUR STRONG GAIN IN PRICE OF $31.60 ON FRIDAY

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAR… THE CME REPORTS THAT THE BANKERS ISSUED A VERY STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 7366 EFP CONTRACTS WERE ISSUED: : APRIL 7366 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 7366 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A HUMONGOUS SIZED TOTAL OF 22,367 CONTRACTS IN THAT 7366LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GIGANTIC SIZED COMEX OI GAIN OF 15,001 CONTRACTS..AND THIS HUMONGOUS SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR VERY STRONG GAIN IN PRICE OF $31.60. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAR (10.258) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 10.258 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $31.60) //// AND WERE SUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR HUMONGOUS SIZED GAIN OF 22,367 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 69.570 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAR. (4.9953 TONNES) FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 22.100 OZ (0.6874 TONNES)… ALL OF THIS WAS ACCOMPLISHED DESPITE OUR STRONG GAIN IN PRICE TO THE TUNE OF $31.60

WE HAD -441 CONTRACTS REMOVED FROM COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 22,367 CONTRACTS OR 2,236,700 OZ OR 69.570

TONNES

Estimated gold comex today 526,678// //huge

final gold volumes/yesterday 413,538///extremely good +

Total monthly oz gold served (contracts) so far this month

3021 notices 302,100 9.3965 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 0

total withdrawals: NIL oz

in tonnes: 0 tonnes

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of MARCH we have an oi of 286 contracts having LOST 104 contracts. We had 325 notices filed on FRIDAY so we

gained another 221 contracts or an additional 22,100 oz will stand for metal at the comex

April lost 11,808 contracts down to 253,737 contracts

May GAINED 9 contracts to stand at 166

We had 9 notice(s) filed today for 900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 9 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAR. /2023. contract month,

we take the total number of notices filed so far for the month (3021 x 100 oz ), to which we add the difference between the open interest for the front month of (MAR. 286 CONTRACTS) minus the number of notices served upon today 9 x 100 oz per contract equals 329,800 OZ OR 10.258 TONNES the number of TONNES standing in this active month of MARCH.

thus the INITIAL standings for gold for the MAR contract month:

No of notices filed so far (3021 x 100 oz+ 286 OI for the front month minus the number of notices served upon today (9)x 100 oz} which equals 329,800 oz standing OR 10.258 TONNES in this active delivery month of MARCH..

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 2968 x 5,000 oz = 14,840,000 oz

to which we add the difference between the open interest for the front month of MAR(77) and the number of notices served upon today 21 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAR./2023 contract month: 2968 (notices served so far) x 5000 oz + OI for the front month of MAR (77) – number of notices served upon today (21) x 500 oz of silver standing for the MAR. contract month equates 15.120 million oz +the 1.0 million oz of exchange for risk//new total standing 16.120 million oz

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MARCH 13/WITH GOLD UP $48.85 TODAY: VERY STRANGE HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY REST AT 901.42 TONNES

MARCH 10//WITH GOLD UP $31.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 903.15 TONNES

MARCH 9/WITH GOLD UP $16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 906.62 TONNES

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

FEB 28/WITH GOLD UP $12.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 917.61 TONNES

FEB 27/WITH GOLD UP $6.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.32 TONNES

FEB 24/WITH GOLD DOWN $9.10 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 917.32 TONNES

FEB 23/WITH GOLD DOWN $13.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 919.92 TONNES

FEB 22/WITH GOLD DOWN 22 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 919.92 TONNES

FEB 21/WITH GOLD DOWN $7.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 919.92 TONNES

FEB 17/WITH GOLD DOWN $1.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 921.08 TONNES

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

GLD INVENTORY: 901,42 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 13/WITH SILVER UP $1.35 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ//

MARCH 10.WITH SILVER UP 36 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ…

MARCH 9/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.979 MILLION OZ

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWALOF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

FEB 28/WITH SILVER UP 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.241 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.188

FEB 27/WITH SILVER DOWN 15 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.471 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 482.429 MILLION OZ

FEB 24/WITH SILVER DOWN 46 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.172 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.900 MILLION OZ//

FEB 23/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.379 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.072 MILLION OZ//

FEB 22/WITH SILVER DOWN 22 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ FROM THE SLV////INVENTORY RESTS AT 485.693 MILLION OZ

FEB 21/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.5363 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 486.382 MILLION OZ//

FEB 17/WITH SILVER UP 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 827,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.819 MILLION OZ/

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 478.879 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

END

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

Making Common, Golden Sense of the Next Senseless Bank Crisis

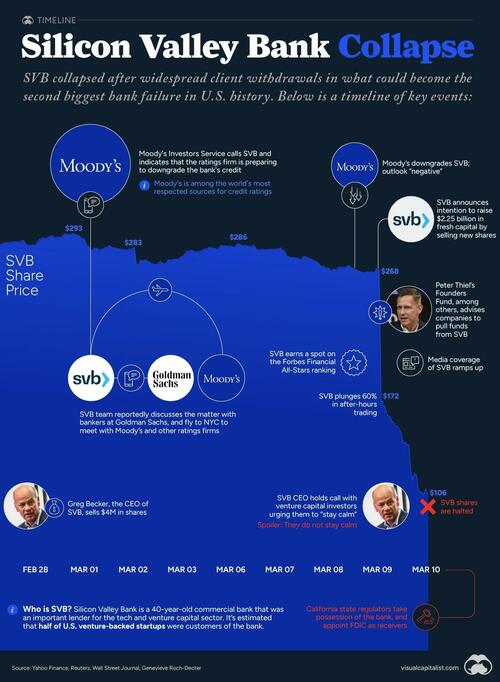

Matthew Piepenburg March 13, 2023

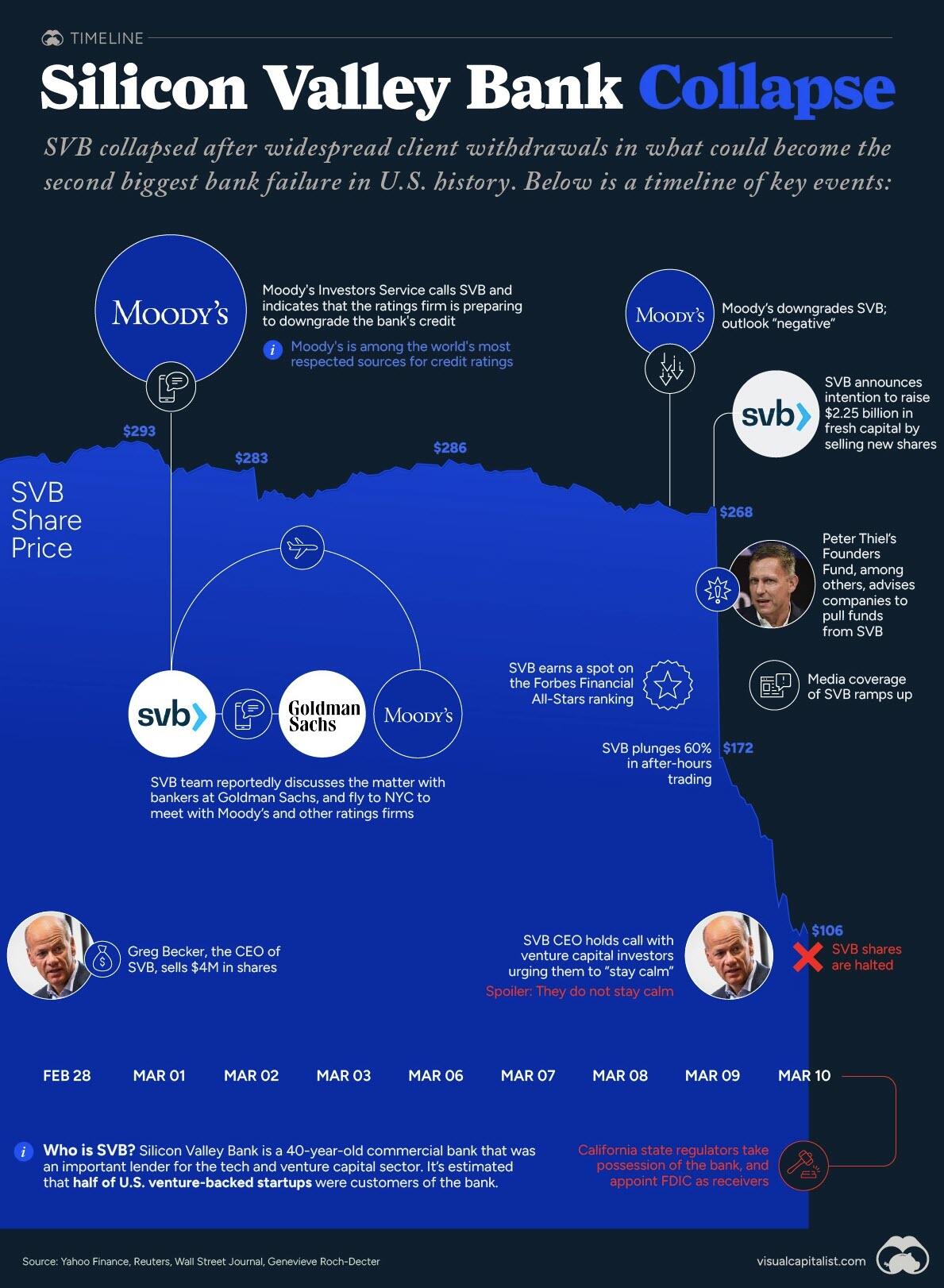

The latest headlines, of course, are all pointing toward the ripple effect of Silicon Valley Bank (SVB), and they should be.

This banking metaphor for the tech sector in particular and the previously described disaster in California as a whole or the matter of banking risk as a theme, require understanding and attention, provided below.

Once we get past a forensic look at the data and forces which explain SVB’s demise, we quickly discover that SVB is itself just a symbol of a much larger financial (and banking) crisis which ties together nearly all of the major macro forces we’ve been tracking since Powell began his QE to QT quest to be Volcker-reborn.

That is, we confirm that everything comes back to the Fed and bond market in general and the UST market in particular. But as I’ve argued for years, and will say again now: The bond market is the thing.

By the end of this brief report, we also discover that SVB is just the beginning; contagion inside and outside of the banking sector is about to get worse. Or stated more bluntly: “We aint seen nothing yet.”

But first, let’s look at the banks in Silicon Valley…

Two Failed Banks

The tech-friendly SVB story (i.e. FDIC shutdown) is actually preceded by another failed bank, namely the crypto-friendly Silvergate Capital. Corp, now heading into voluntary liquidation.

Because SVB was a much larger bank (>$170B in deposits) than Silvergate (>$6B in deposits), it got and deserved more headlines as the largest bank failure since well, the 2008 bank failures…

Unlike Lehman or Bear Stearns, the recent disasters at SVB and Silvergate were not the result of concentrated and levered bets/loans negligently packaged as investment-grade credits, but rather the result of a good ol’ fashioned bank run. Bank runs happen when depositors all want to get their money out of the banks at the same time—a scenario of which I’ve warned for years and compared to a burning theater with an exit door the size of a mouse-hole.

Banks, of course, use and lever depositor funds to lend and invest at risk (which is why Henry Ford warned of revolution if folks actually understood what banks actually do). Thus, if a mass of depositors suddenly wants their money at the same time, it’s just not gonna be there.

So, why were depositors in a panic to exit?

It boils down to crypto fears, tech stress and bad banking practices.

No Silver Lining at Silvergate

At Silvergate, they provided loans to crypto enterprises, which were the belle of the speculation ball until Sam Bankman-Fried’s FTX implosion made investors weary of crypto exchanges. Nervous depositors withdrew billions of their crypto-linked deposits at the same time.

Silvergate, of course, didn’t have the billions needed to meet depositor requests, because, well… banks by their operational (fractional reserve) nature never have the money when needed at the same time.

Thus, the bank had to quickly and desperately sell assets, which meant selling billions worth of non-mature Treasuries whose prices had tanked in the interim thanks to the Powell rate hikes.

(See how the Fed lurks, head down and silent, as the source behind nearly every crisis?)

This was selling bank assets at the worst time imaginable and immediately sent Silvergate into the red and toward the cold dark ocean floor.

Once DOJ investigations end and the FDIC insurance runs out, we’ll discover just how “whole” the bigger depositors at Silvergate will be—but this will take time and end in some degree of pain for many of them.

Death Valley for Silicon Valley Bank

As for the bigger disaster at SVB, they mostly serviced start-ups and technology firms with a major focus on life sciences start-ups—i.e., yesterday’s unicorns and tomorrow’s donkeys.

These unicorns, of course, were not only under the cloud of the FTX fears in particular and falling faith in tech miracles in general, but equally under the pressure of Powell’s rate hikes, which made funding (or debt-rollovers) harder and more expensive to obtain for tech names.

In short, the keg party of easy money for questionable tech enterprises was beginning to unwind.

SVB’s slow and then rapid demise came as depositors (at the advice of their VC advisors) withdrew billions at the same time, which SVB (like Silvergate) could not match after selling UST assets at a massive loss to save the first withdrawals while burning the later movers.

In short, and like all Ponzi schemes, banks suffering a bank run can’t and won’t make everyone whole—just the first money out—i.e., the fastest runners in the burning theater.

Burn Victims, Recovery?

Banks, ironically, can’t technically go bank-rupt. Silvergate plans to eventually make all depositors whole as they sift through their assets in liquidation. Hmmm. Good luck with that.

SVB, however, waited too long for voluntary liquidation procedures and was instead taken over by the FDIC as a receiver to manage the sale of assets to return investor deposits as a dividend over time.

Furthermore, the FDIC “insures” investor deposits up to $250K, but that won’t help the vast majority of SVB deposits (95.5%) not covered by this so-called insurance.

The Contagion Effect?

Notwithstanding the pain felt by depositors at Silvergate and SVB, the fear there has spread to the broader banking sector (big bank to regional), which saw expected sell-offs at the end of last week and has prompted the inevitable question, namely: Is this another Lehman moment?

For now, we are talking about bank runs rather than banks failing ala 2008 due to massive derivative exposures and bad loans. In short, this is not (yet at least) a 2008-like banking crisis.

That said, and as we’ve reported countless times, post-2008 banks are still massively over-levered and over-exposed to that toxic waste dump otherwise known as the COMEX and derivatives market.

Each day, the headlines change.

Signature Bank, this time in New York, was just shuttered by New York regulators.

The Fed then announced over the weekend that they will make depositors whole, which is tantamount to confessing yet another Fed bailout of bad banks under the new name of the $25B “Bank Term Funding Program”—or BTFP, an acronym which spurs reminders of the 2009 TARP days…

Such a bailout policy makes the odds of further Fed rate hikes in 2023 a bit less likely, and already the traders on Wall Street are renaming BTFP as “Buy The F***ing Pivot.”

As I’ve written for months (and show below), Powell’s QT plan would last until something inevitably broke, and it would seem that day has come, as expected.

Many are suggesting that the BTFB will need to be funded to at least $2T, not $25B, to backstop further banking risk.

Easy Prognosis

Based on context and current data, however, we can begin to make certain objective and early conclusions.

Cash flow from VC into tech is about to get a lot tighter, as we’ve been warning for the last 2 years.

SVB depositors may eventually get some or much of their money back over time once the bank’s assets (Treasuries, loans etc.) are sold off by the FDIC. Despite my very, very low opinion of bank regulators, at least SVB, unlike FTX, was regulated.

As to a full-on crisis across all banks, it’s a bit early to say that the foregoing regional cancers will spread across all banks of all flavors, though our blunt reports on banking risk in the past suggest that banks as a whole are anything but safe.

Cryptos, already under the cloud of FTX and now SVB, saw more pain, as the sell-offs in this space last week confirm. However, as banking fears prompt a more dovish Fed in Q2, many cryptos could rise.

The Bigger, Scarry Picture

In the still evolving nature of the current banking crisis, we see reasons to be concerned, very concerned, about systemic risk in the banking sector.

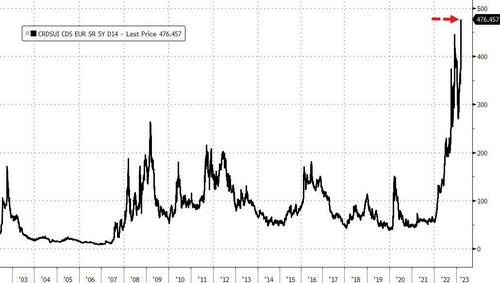

Banks, and banking practices, are complex little beasts. Just across town at that gasping entity known as Credit Suisse, for example, they have been too afraid to publicly report their cash-flow statements as the bank’s stock fell yet another 60%. So, yeah, things are complex…

But returning to the US in particular and banks in general, one can still derive the simple from the complex, which is simply scarry.

Keep It Simple

At the most basic level, banks fail when the cost of funding their operations rises dramatically above the returns or yields on their performing/earning assets.

It is our view that such a set-up for further pain across the banking sector is real, a set-up made all the worse by—you guessed it—that entirely un-natural destroyer of natural markets forces, free price-discovery and honest capitalism otherwise known as the U.S. Federal Reserve.

Central Bankers and Broken Bonds

As I’ve written and spoken, everything is connected, and everything eventually takes it signals from the bond market, which was long ago hijacked by the Fed.

Powell’s rate hikes, for example, don’t just occur in a vacuum to fight his bogus war on an inflation nightmare which he once promised was only “transitory.”

Fed QT and QE, for example, are more than just words, experiments or theories, they are un-natural, artificial and powerful toxins which can’t be contained to just making central bank balance sheets thinner or fatter and bogus CPI data higher or lower.

Instead, the Fed’s little tweaks, tricks and madness impact just about everything, and always end up screwing everything up.

Why? Because markets were designed to be managed by natural forces of supply and demand not artificial forces of fake money from central bankers.

By raising the Fed Funds Rates toward 5% and above at rapid pace, for example, Powell has done more than just make a tiny $300B dent in the Fed’s nearly $9T balance sheet. He has engineered a dis-inflationary recession and sent combined nominal returns in stocks AND bonds to levels not seen since 1871.

But when it comes to banking risk, Powell has also gut-punched that sector with criminal negligence.

How so?

Even the Banks Can’t Fight the Fed?

When the Fed began raising rates, it sent bonds to the floor and hence yields to the moon (yields and bond price are inversely related).

This impacts bank balance sheets because banks make a living by paying depositors at rate X while earning X+; but now those banks are in a deadly corner of the Fed’s own mis-design.

That is, the Fed has sent bond yields higher than the rates/yields which commercial banks offer depositors, which is why many depositors are questioning the advantage of being, well…depositors.

This mis-match, of course, will likely require banks to raise depositor rates to compete with rising UST yields, a costly tactic which cuts their profits and reddens their balance sheets.

Alternatively, banks could offer/issue more bank shares to increase their capital, but this dilutes existing share counts and value, which is how bankers are paid.

To add insult to injury, banks (and bankers) are also facing the real risk of rising or at least persistent inflation, which means that the real return on even “enhanced” depositor rates is ultimately a negative return when adjusted for the invisible tax of inflation.

All Conversations Return to Gold

So, no, we hardly think the commercial banking system, the massive and compounding risks of which we have reported for years, is anything remotely healthy, safe or credible.

All frowns and inevitable (yet increasingly empty) gold-bug critiques notwithstanding, we think holding a physical bar of segregated, allocated and non-levered gold in one’s own name in the world’s safest private vaults and jurisdictions makes a lot more sense than trusting your increasingly worthless paper or digital money to the world’s increasingly fractured banks, be they SVB, Credit Suisse or JP Morgan.

Just saying…

end

CHRIS POWELL//GATA AND OTHER IMPORTANT GOLD COMMENTARIES

BIS gold swaps reflect U.S. move to knock the price and protect dollar, Maguire says

Submitted by admin on Fri, 2023-03-10 21:31Section: Daily Dispatches

9:24p ET Friday, March 10, 2023

Dear Friend of GATA and Gold:

London metals trader Andrew Maguire tells this week’s “Live from the Vault” program from Kinesis Money that the recent 100-tonne increase in gold swaps undertaken by the Bank for International Settlements was a dumping of gold by the United States to protect the dollar.

But Maguire adds that such dumps are being aggressively used by central banks to add to their gold reserves. Metal is leaving the preserve of the London Bullion Market Association for safekeeping away from the clutches of the price suppressors, Maguire says.

He expects a big change in the gold and currency markets in April.

The program is 42 minutes long and can be seen at YouTube here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

END

Jay Newman: Why the U.S. dollar has become an at-risk currency

Submitted by admin on Sat, 2023-03-11 23:10Section: Daily Dispatches

By Jay Newman New York Post Saturday, March 11, 2023

Everywhere you turn there’s chatter about the ongoing US economic sanctions against Russia. The Russian Central Bank, Russian banks, Russian companies, Russian oligarchs — and anyone caught helping them — have seen their fortunes entangled since Moscow invaded Ukraine just over a year ago.

From Davos to Aspen, American Treasury officials tout the unprecedented scale and scope of this powerful economic weapon.

And why not? The effort has been impressive. The US government task forces have beached scores of yachts, grounded planes, blocked hundreds of millions of dollars of central bank assets and cut Russian financial institutions off from the global SWIFT financial system.

Sanctions are an ancient game: in 432 B.C. Athens crushed its rival — Megara — by banning their traders from Athenian marketplaces.

For the U.S. government in the 21st century, economic sanctions aren’t merely second nature, they’ve become a central tool of foreign policy. More than 10,000 people and dozens of countries are subject to sanctions worldwide.

But more than 100 countries haven’t signed on to those efforts. Which is why oil from the Urals still flows to Asia,Turkey and most of Africa, while grain stolen from Ukraine is winding up across the Black Sea in Russia.

Meanwhile, the profits of this illicit trade is finding its way to places like Dubai, now chockablock with “sanctioned” Russians looking for real estate.

This isn’t to say that we shouldn’t support Ukraine: we should — and we must. But while it makes sense to financially cripple our avowed enemies — Russia, China, Iran, North Korea — coalitions are forming around ways to avoid existing sanctions and to protect against the risk of future sanctions.

Much of the action involves creating alternatives to the dollar as the world’s default currency. If you can keep your reserves in another currency or park them in physical assets like gold or commodities, the thinking goes, you’re halfway to safety.

Take China, for whom supplanting and discrediting the dollar is a key component of its “winning without fighting” campaign known a detailed in the book Unrestricted Warfare. The sanctions push, however necessary, has accelerated China’s quest to defeat the dollar, and many other nations are taking note.

While a chorus of experts still insists that there’s no alternative to the dollar, this is untrue. The dollar will dominate as long as it serves the interest of those who use it. Once the dollar begins placing assets at risk, alternative tools of commerce are certain to emerge. And they already are.

Make no mistake: a shift away from the dollar would be a huge blow to America’s international standing. The days of being able to print limitless amounts of currency could end, along with our ability to buy foreign goods cheaply.

Stark proof that a new game is afoot filtered out of Davos last month. Saudi Arabia’s Finance Minister, Mohammed Al-Jadaan, made the stunning announcement that–for the first time in 48 years — the world’s biggest oil producer was open to trading in currencies other than the U.S. dollar.

That’s a far cry from the deal Richard Nixon cut with King Faisal decades ago to solely accept dollars as payment for oil. (In exchange, Nixon agreed to protect the Kingdom from Soviet, Iranian and Iraqi aggression.) That pact laid the groundwork for a strong dollar as oil money began to flow through the Federal Reserve.

Today, China imports 1.4 million barrels of oil a day from Saudi Arabia (up 39% over the past year), making it the Kingdom’s largest customer. Which is why both sides are seeking cheaper alternatives to using dollars for every transaction. With Aramco investing in a massive new refinery in China, the relationship will only deepen.

The Saudi shift is only the latest data point. At the 2022 BRICS summit in Beijing, Vladimir Putin announced plans to expand the Shanghai Cooperation Organization (SCO) and develop an alternative for international payments using a currency basket of Chinese RMB yuan, Russian rubles, Indian rupees, Brazilian reals, and South African rand. For reference, the SCO is the world’s largest regional organization, representing 40% of the world’s population and 30% of global GDP.

A new currency is only part of the picture. China is pioneering new exchanges to shift commodity trading from Western institutions like the troubled London Metal Exchange and the New York Mercantile Exchange.

Even the Europeans have gotten into the act, by creating a special-purpose vehicle — INSTEX — to facilitate non-dollar, non-SWIFT humanitarian transactions with Iran to sidestep U.S. sanctions. Russia, predictably, expressed interest in participating and the first transaction was completed in March 2020 to facilitate a medical equipment sale to Iran to combat COVID.

Russia and Iran are also developing a gold-backed stablecoin, oil traders are already using the UAE’s dirham to settle oil trades and the Indian rupee is finally being positioned as an international currency.

The beat goes on: China’s Cross-Border Interbank Payment System (CIPS) processes only 15,000 transactions a day — Western-favored CHIPS moves 250,000 daily — but it’s growing. Russia offers its own System for Transfer of Financial Messages to allow users to bypass SWIFT.

Even the Swiss-based Bank for International Settlements — Hitler’s banker — is getting into the act, creating a renminbi liquidity line to support contributing central banks in times of crisis. So far, the central banks of Chile, Hong Kong, Indonesia, Malaysia, and Singapore have subscribed.

In the 21st century, a currency’s value — including the dollar — will become increasingly competitive. If there is less demand for dollars, the value of the dollar will decline. Everything will become more expensive. Not all at once, but over time — making deficit spending more costly or, unthinkably, impossible.

It’s not farfetched to imagine the U.S. experiencing a debt crisis because no one shows up to buy its bonds. The U.S. dollar will become just one more currency, among many. And ultimately, if the dollar loses its shine, so will the ability of the U.S. to project power.

To stem this tide, hard choices must be made: like strategically reducing our enemy count even as we continue to support allies like Ukraine. Perhaps most difficult, the U.S. must get its economic house in order by — once and for all — finally figuring out how to live within its means.

—–

Jay Newman was a senior portfolio manager at Elliott Management and is the author of “Undermoney,” a thriller about the illicit money that courses through the global economy.

END

U.S. bails out Silicon Valley and Signature Bank and their uninsured depositors

Submitted by admin on Sun, 2023-03-12 19:17Section: Daily Dispatches

Who was worried about bail-ins?

* * *

SVB, Signature Bank Depositors to Get All Their Money as Fed Moves to Stem Crisis

By Nick Timiraos The Wall Street Journal Sunday, March 11, 2023

U.S. regulators took control of a second bank on Sunday and raced to roll out emergency measures to stem potential spillovers from Friday’s swift collapse of Silicon Valley Bank, backstopping uninsured depositors and making more funding available to the banking system.

Regulators announced that Signature Bank, one of the main banks for cryptocurrency companies, was closed Sunday. The New York bank’s depositors will be made whole, officials said.

Officials took the extraordinary step of designating SVB and Signature Bank as a systemic risk to the financial system, which gives regulators flexibility to backstop uninsured deposits.

The Federal Reserve and the Treasury Department also used emergency lending authorities to establish a new facility to backstop bank deposits.

Regulators announced the moves in a joint statement from Treasury Secretary Janet Yellen, Fed Chair Jerome Powell, and Federal Deposit Insurance Corp. Chair Martin Gruenberg. The group said that depositors at SVB and Signature would have access to all of their money on Monday. …

Pam and Russ Martens: Silicon Valley Bank was a Wall Street IPO pipeline in drag as a U.S.-insured bank

Submitted by admin on Mon, 2023-03-13 11:12Section: Daily Dispatches

By Pam and Russ Martens Wall Street on Parade Monday, March 13, 2023

If you want to genuinely understand why Silicon Valley Bank (SVB) failed and why Jerome Powell’s Fed led the effort yesterday to make sure $150 billion of the bank’s uninsured depositors’ money would be treated as FDIC insured and available today, you need to take a look at how the bank defined itself right up until it blew up on Friday.

This was a financial institution deployed to facilitate the goals of powerful venture capital and private equity operators, by financing tech and pharmaceutical startups until they could raise millions or billions of dollars in a Wall Street Initial Public Offering (IPO). The bank was also involved in managing the wealth of those startup millionaires or billionaires once they struck it big in an IPO.

Many of the former startup companies also continued to keep their operating money at the bank – in many cases in the millions of dollars, ignoring the fact that just $250,000 of that was insured by the Federal Deposit Insurance Corporation (FDIC). Last Friday, dozens of publicly-traded companies made filings with the Securities and Exchange Commission indicating that they had large sums of uninsured deposits now frozen at Silicon Valley Bank. Several indicated that the amounts represented 23 to 26 percent of the company’s cash and/or cash equivalents.

Roku, Inc., the publicly-traded manufacturer of digital media players for video streaming, reported the following to the SEC: “The Company has total cash and cash equivalents of approximately $1.9 billion as of March 10, 2023. Approximately $487 million is held at SVB, which represents approximately 26% of the Company’s cash and cash equivalents balance as of March 10, 2023.”

Publicly-traded Oncorus, Inc., a biopharmaceutical company focused on developing RNA-based medicine for cancer patients, reported the following to the SEC: “The Company informs its investors that it has deposit accounts with SVB with an aggregate balance of approximately $10 million, which is approximately 23% of the Company’s total current cash, cash equivalents and short-term investments. In addition, the Company has a standby letter of credit in place with SVB of approximately $3.4 million securing obligations under its lease agreement with IQHQ-4 Corporate Drive, LLC.”

In big, bold type on its website, Silicon Valley Bank bragged that “44% of U.S. venture-backed technology and healthcare IPOs YTD [year-to-date] bank with SVB.”

To put it bluntly, this was a Wall Street IPO machine that enriched the investment banks on Wall Street by keeping the IPO pipeline moving; padded the bank accounts of the venture capital and private equity middlemen; and minted startup millionaires for ideas that often flamed out after the companies went public. These are the functions and risks taken by investment banks. Silicon Valley Bank – with this business model — should never have been allowed to hold a federally-insured banking charter and be backstopped by the U.S. taxpayer, who was on the hook for its incompetent bank management.

We say incompetent based on this fact alone (although there were clearly lots of other problem areas): $150 billion of its $175 billion in deposits were uninsured. The bank was clearly playing a dangerous gambit with its depositors’ money. …

Richard Beale, the owner and managing director of Roma Numismatics, a London-based auction house that dealt in ancient coins, was arrested in New York in January on multiple charges relating to the sale of a multimillion-dollar coin, according to arrest warrants and a report by U.S. Homeland Security Investigations obtained by ARTnews.

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//MONDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 6.8724

OFFSHORE YUAN: 6.8928

SHANGHAI CLOSED UP 38.62 PTS OR 1.20%

HANG SENG CLOSED UP 376.05 PTS OR 1.95 %

2. Nikkei closed DOWN 311.01 PTS OR 1.11%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 103.84 Euro RISES TO 1.0662 UP 32 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.202!!(Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 133.24/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.224%***/Italian 10 Yr bond yield FALLS to 4.135%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.312…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.205//(ITALY WORSE THAN GREECE?)

3j Gold at $1887.80//silver at: 21.07 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 91/100 roubles/dollar; ROUBLE AT 75.18//

3m oil into the 75 dollar handle for WTI and 80 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 133.24/10 YEAR YIELD AFTER BREAKING .54%, LOWERS TO .202% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9147–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9785well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

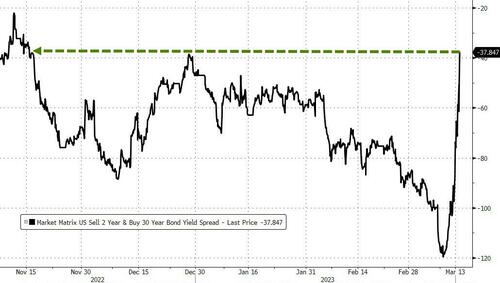

USA 10 YR BOND YIELD: 3.507% DOWN 19 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.674 DOWN 5 BASIS PTS//INVERTED TO THE 10 YEAR!!

USA 2 YR BOND YIELD: 4.1738 DOWN 41 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,97…

GREAT BRITAIN/10 YEAR YIELD: 3.458% DOWN 18 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

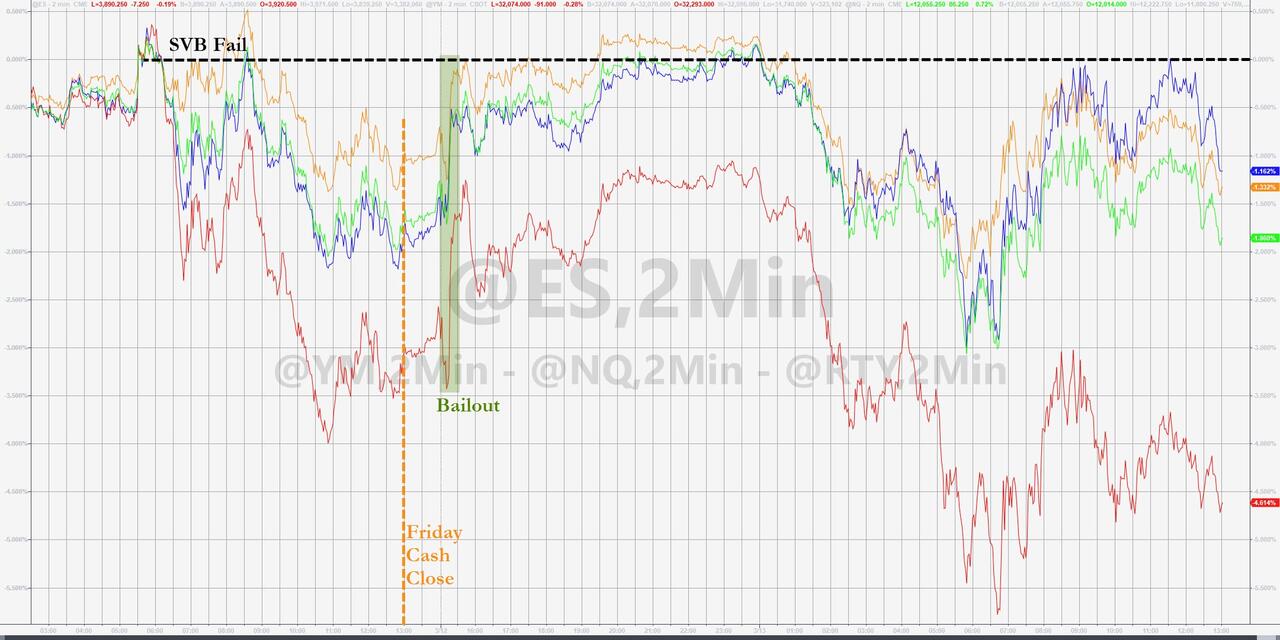

The following is your most important commentary today: the bailout of 3 USA banks and its consequences courtesy of zerohedge. He explains the credit event on Friday and how the Treasury is freaking out. In a nutshell, the FDIC is gone and the Fed is guaranteeing all USA deposits. The three banks, Silvergate, Silicon Valley and Signature bank witnesses their shareholders and debt holders wiped out. The derivatives orchestrated by these banks are not bailed out. No doubt that the Fed will not raise rates an inch anymore. QE will also no doubt commence shortly. The dollar will collapse and gold will be its beneficiary. All of the losses on the books of these banks and future banks will be absorbed by the Fed at over 620 billion dollars so far!!

Please read…

(zerohedge)

THE BAILOUT OF THREE USA BANKS AND ITS CONSEQUENCES:

What Bank Bailout Does, And Why US Treasury Is Freaking Out

Here’s What The Latest Bank Bailout Does, And Why The Treasury Is Quietly Freaking Out

by Tyler Durden

Sunday, Mar 12, 2023 – 09:13 PM

And so, we got our “credit event” and the Fed panicked, as did the Treasury, and the FDIC…

While we reported the big picture of the latest bank bailouts by the Big Three regulators, what is most notable is today’s latest entry to the Fed’s alphabet soup of bailout facilities, the BTFP lending program which, in theory, “will make loans on high quality collateral” (by which the Treasury simply means collateral that has already incurred mark-to-market losses of over $600 billion; more below).

The BTFP – or as we call it, the Buy The F-ing Pivot – is basically another bank bailout facility because no matter what you may read elsewhere (as the propaganda media now scrambles to avoid using words such as “bailout” in favor of the far less Democrat snowflake-triggering “backstop”), one which gives banks full credit for unrealized losses on their Held to Maturity Books, losses which as we showed last week amount to nearly a quarter trillion dollars at just the big 4 banks.

As the WSJ’s Ben Eisen recaps, “the facility will allow banks to take advances from the Fed for up to a year by pledging Treasury’s, mortgage-backed bonds and other debt as collateral.” And by allowing banks to pledge their bonds – not just at current market price but at cost (or at par) – banks can meet customer withdrawals without having to sell their bonds at a loss, which is what Silicon Valley Bank did last week, sparking a run on the bank.

Indeed, as Eisen underscores, the biggest draw of this facility is that “banks can borrow funds equal to the par value of the collateral they pledge, according to the Fed’s announcement. This means that the Fed won’t look to the market value of the collateral, which in many cases reflect big unrealized losses due to the jump in interest rates.”

That is a huge gift for the banks which are sitting on some $620 billion in unrealized losses on all securities (both Available for Sale and Held to Maturity) at the end of last year, according to the Federal Deposit Insurance Corp. It also means that just the Big 4 banks – as shown in the chart above – are getting a $210 billion bailout.

But wait, there’s more: the Fed also won’t demand that banks pledge collateral in excess of the advances they are taking, which is typically the case when banks borrow from, say, the Federal Home Loan Bank system.

And if banks can’t repay all the advances in a year’s time? The Treasury Department is providing $25 billion of credit protection to the Fed just in case. “The Federal Reserve does not anticipate that it will be necessary to draw on these backstop funds,” the Fed said in its announcement Sunday night.

That, in a nutshell, is how the TSY/Fed/FDIC hope to mitigate stress on the bank asset side.

At the same time, on the liability side (where the deposits are), the regulatory trio hopes that by making whole all depositors – including uninsured corporate depositors (those with more than $250,000 in deposits – at banks like the now defunct Silicon Valley Bank and Signature Bank, they will stem and contain the real epicenter of the current bank crisis: the bank run that is spreading from just SIVB as of Friday, to other banks (and the sudden and unexpected collapse of Signature Bank).

An artist’s impression of what the new FDIC sticker that graces the window of every bank teller is shown below.

And while we applaud the Fed’s desperate attempt to undo decades of errors by the Fed (because the reason why small banks are collapse left and right now is precisely because of the Fed’s aggressive hiking campaign which is a consequence of the Fed’s aggressive easing campaign preceding it, and so on), some – such as the ultra-liberal and socialist mouthpiece of the deep state, WaPo – can’t help but wonder if what just happened is even legal or in the Fed’s charter (since the Fed is taking on outright losses by valuing BTFP collateral at par and not at a “market” set by the Fed itself).

In fact, here is WaPo reporter Jeff Stein asking if “all uninsured deposits *nationally* are now implicitly backstopped by the FDIC?” Spoiler: yes, they are, but if the Treasury were to admit that, Monday would see historic howls of outrage from the left which will not be happy to learn that taxpayers are now backstopping major corporations.

I asked Treasury this question on a call with reporters this evening. This was their response pic.twitter.com/LeM9clLzmT — Jeff Stein (@JStein_WaPo) March 12, 2023

Legality of the latest Biden admin’s actions aside, will what was unveiled tonight be enough to restore public trust in small banks – the same ones we profiled in “Here Are The Banks Facing The Highest Deposit-Run Risk”? We’ll find out very soon when all the wire transfer requests from the weekend hit and banks suddenly find themselves scrambling to reallocate capital.

One thing we do know is that as of Q3, the FDIC’s Deposit Insurance Fund had some $125BN in it. Which means it has the firepower to plug $125BN in bank runs. Is that enough?

Well, the US has $18 trillion in deposits, and recall that $42BN in SVB deposits were pulled in hours, not days, not weeks… hours. So, you’d have to forgive us if we are just a little skeptical that the Treasury’s $25BN mini backstop bazooka and the FDIC’s $125BN in bank run buffer will do anything to prevent a far bigger bank crisis now that the horses have fled the barn.

But it’s not just us who are skeptical: according to Bloomberg is at least one senior US Treasury official who said that “there are some institutions with issues similar to Silicon Valley Bank”, while highlighting that moves by regulators Sunday are aimed at assuring deposits are safe. Well of course they are, the question is are the moves enough!

“There are some institutions that look like they have some similarities to SVB and perhaps to Signature”, the Treasury Department official told reporters on a call on Sunday, speaking on condition of anonymity, adding that “it could be that there are concerns about depositors at those institutions.”

It’s almost as if the official is hoping to accelerate the bank run on Monday.

There was more: the official highlighted the Federal Reserve’s new Bank Term Funding Program, which will make loans on “high quality collateral”, so high quality that they are carrying $600MM in unrealized losses at this moment. The official says that this “should” provide some assurance that depositors do not need to move to other institutions.

So… the Treasury’s entire plan is that the BTFP bailout facility – which is really backstopped by just $25BN in TSY funding – will be enough to reverse a small bank sector bank run, one which we saw on Friday drained $42 billion, or almost double the existing backstop facility, in hours!

Well, good luck with that.

The official concluded by saying – or rather hoping – that “this situation is not 2008, as there are a lot of reforms that have been put in place.” Yes, so many reforms that two bank with $300 Billion in assets – half of what Lehman had – just collapsed in the span of 2 trading days.

One can’t possibly imagine why depositors would feel nervous after this, and seek to pull any money they have at the first possible opportunity. And for those who believe depositors may in fact – get a little nervous, we urge you to reread our post “Here Are The Banks Facing The Highest Deposit-Run Risk.”

end

Futures Tumble, Yields Crater, Banks Plunge As Market Realizes Latest Bailout Is Insufficient

MONDAY, MAR 13, 2023 – 08:18 AM

Yesterday, when describing the nuances of the latest bank bailout (and big bank subsidy) we explained why the “Treasury is quietly freaking out” and asked rhetorically “ETA until market realizes $25BN is nowhere near enough and futs react appropriately?”

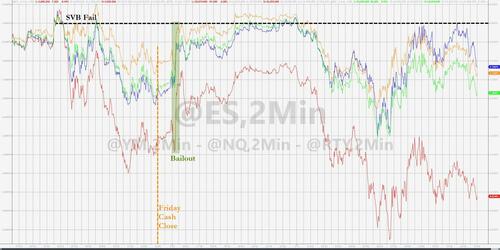

Turns out the answer was about 12 hours, because after initially spiking, and rising just shy of 4,000 amid widespread acceptance that the Fed’s tightening cycle is finally over, fears have shifted back to the growing bank crisis and depositor run, and futures were back down to 3,900, up just 0.2%, and wiping out most of their overnight gains…

… as bank stocks have resumed their plunge led by small US banks such as First Republic, which is down 60% this morning as the market realizes the bank run is only starting…

… but it’s not just the regional US banks which we warned were about to be wiped out: big international banks are also getting crushed with Italian bank giant UniCredit shares halted, while Credit Suisse shares are not only 10% lower to new all time lows, but its Credit Default Swaps just hit a record wide.

Here are some notable premarket movers:

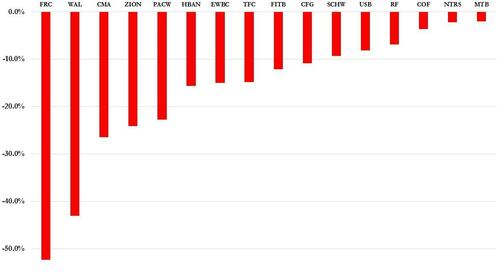

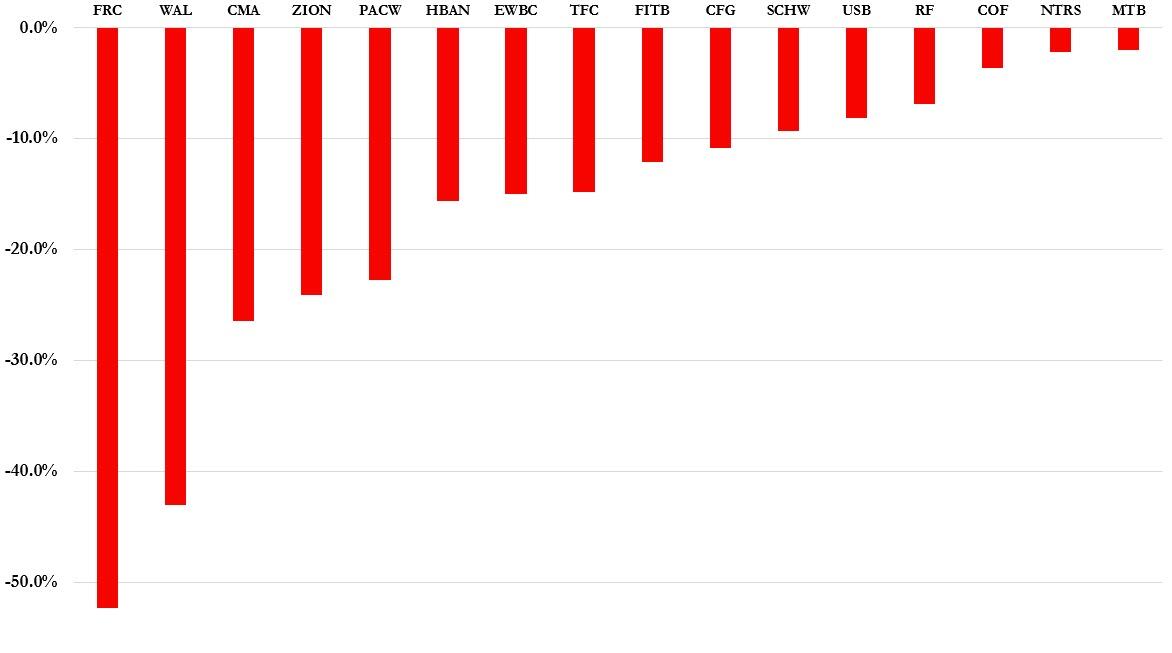

Most US banking stocks cede early gains to trade around flat or in the red, as initial optimism fueled by US authorities’ decisive action on SVB fades and fears mount for the health of the broader financial system. JPMorgan (JPM US) -2%; Bank of America (BAC US) -6.3%, Wells Fargo (WFC US) -3.5%, Citigroup (C US) -2.7%, Charles Schwab (SCHW US) -18%, Western Alliance Bancorp (WAL US) -25%, PacWest Bancorp (PACW US) -36%

First Republic Bank (FRC US) shares fell 63% after the US lender moved to try and quell concern about its liquidity following the failure of Silicon Valley Bank. The declines came after the bank said late Sunday it had more than $70 billion in unused liquidity from agreements that included the Federal Reserve and JPMorgan.

US-listed Chinese stocks rise in premarket trading, on track to halt five days of declines, as China’s new premier Li Qiang called for better cooperation between the two countries and signaled support to the private sector. Alibaba (BABA US) +0.8%, Baidu (BIDU US) +1.4%, PDD Holdings (PDD US) +1.2%, NetEase (NTES US) +1.9%, Trip.com (TCOM US) +1.2%, Li Auto (LI US) +2.8%

Cryptocurrency-exposed stocks rose after Bitcoin jumped on US agencies’ pledge to fully protect all Silicon Valley Bank depositors following the lender’s collapse. Marathon Digital (MARA US) +7.3%, Riot Platforms (RIOT US) +2.8%, Hut 8 Mining (HUT US) +5.6%, Coinbase (COIN US) +4%

Provention Bio (PRVB US) shares rise as much as 264% to $24.40 in US premarket trading after Sanofi agreed to buy the biotech for $25/share in cash, in a $2.9 billion deal intended to bolster the French drugmaker’s portfolio of diabetes medicines with a new therapy recently approved in the US.

Gold miners could be active on Monday as gold kept rising, with investors flocking to havens following the collapse of SVB. Watch shares including Barrick (GOLD US), Agnico Eagle (AEM US), Kinross (KGC US).

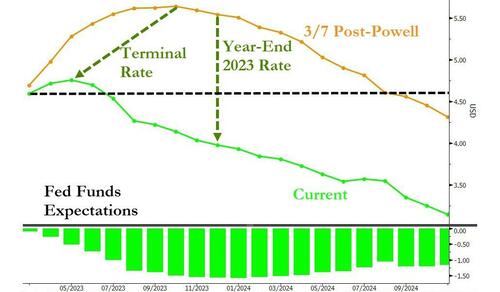

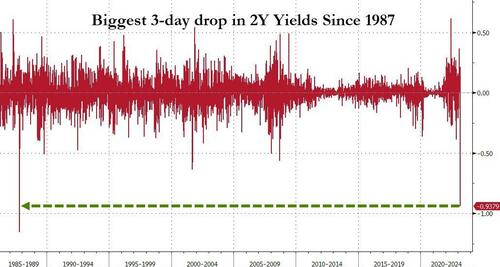

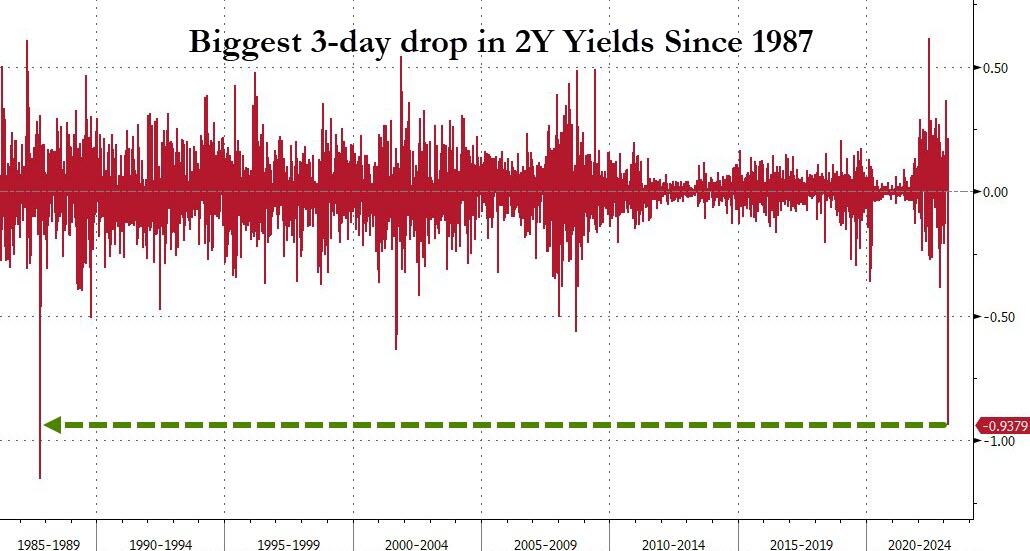

Meanwhile, with Goldman joining ZH in calling a Pause in the Fed’s hiking cycle, 2Y yields have plummeted an insane 50bps…

… suffering the biggest 2-day drop since Black Monday in October 1987! So much for all those macrotourists preaching “higherer for longerer”(but please buy their newsletter, they need the money to fund their own bailout).

And here is how the Fed’s rate hike narrative died a gruesome death in just 3 trading days.

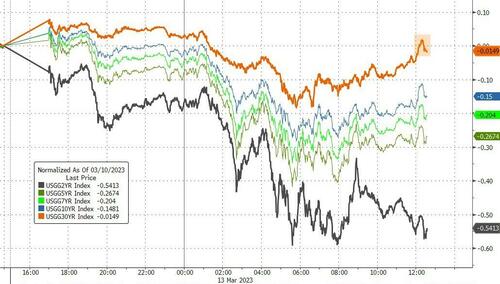

While not nearly as pronounced as the collapse in the short end, the 10-year yield fell to a one-month low and the dollar extended a decline against major peers. The yield on two-year German debt plunged 38 basis points to 2.72%, putting them on course for the steepest two-day fall on record.

The turmoil following SBV’s demise has caused a rapid repricing in markets for where the Federal Reserve will take policy. Swaps traders now only roughly even odds the central bank will raise rates at its meeting next week, especially after Goldman economists said they expect no change in the policy rate following the collapse of SVB. Expectations had built for a hike of as much as 50 basis points after Chair Jerome Powell addressed lawmakers Tuesday.

“The failure of SVB puts the Fed’s focus on financial stability,” said Marija Veitmane, senior multi-asset strategist at State Street Global Markets. “This is a difficult position Fed is in, on the one hand it needs to keep hiking to arrest inflation, but also it needs to protect the financial system. Feels like a lose-lose situation for the Fed and the market” which of course is a paraphrase of what we said last Thursday.

While US futures faded fast, Europe was a mess from the start as shares of European banks and insurers slumped on Monday, while yields on European bonds fell on anticipation that the Silicon Valley Bank collapse could force central banks to slow the pace of interest rate hikes. The pan-European bank stocks index was down by the most in a year, while real estate stocks also slipped but outperformed the broader index as the sector typically benefits from dovish monetary policy shifts. Banking stocks index is down 5.7%, worst performing European sector, while the broader market loses about 2.8% Commerzbank -12%, Banco de Sabadell -9.4% and ING -9% are top losers; and of course, as noted above Credit Suisse shares down 13% to new record low.

Earlier in the session, Asian stocks erased earlier declines as bond yields slid after Goldman Sachs Group Inc. said the Federal Reserve will stand pat next week. Equities in China and Hong Kong rallied the most. The MSCI Asia Pacific Index advanced as much as 0.6%, reversing a loss of up to 0.9%. Chinese shares led the charge higher as traders bet on policy continuity after the nation retained several familiar faces in its economic leadership team, including the central bank governor. Tech shares in the region also got a boost from falling US Treasury yields as Goldman Sachs economists said the recent stress in America’s banking system may prompt the Fed to pause its monetary tightening cycle next week. It also flagged uncertainty about the rate path in the months ahead. READ: Rate Bets Unwind Is Savage Enough to Evoke Black Monday Meanwhile, Japanese benchmarks were weighed down by financial shares as investors assessed the fallout of Silicon Valley Bank’s collapse. Asia’s benchmark stock gauge is trying to recover from last week’s 2% drop as SVB’s downfall highlighted the impact of higher interest rates on the US economy and financial system. “Although we do not think there is any material fundamental impact on Asian stocks, equity investor sentiment will likely remain fragile for now,” Nomura strategists including Chetan Seth wrote in a note. Market focus will likely remain on factors such as whether there are deposit outflows from other relatively smaller regional banks, they added.

Japanese stocks fell for a second day as investors continued to assess whether Silicon Valley Bank’s failure poses risks for the broader financial markets. The Topix Index fell 1.5% to 2,000.99 as of market close Tokyo time, while the Nikkei declined 1.1% to 27,832.96. The Topix’s gauge for banks and insurers was among the biggest sector losers. Mitsubishi UFJ Financial Group Inc. contributed the most to the Topix Index decline, decreasing 3.5%. Out of 2,160 stocks in the index, 202 rose and 1,906 fell, while 52 were unchanged. “SVB’s bankruptcy news and yen’s appreciation both dragged Japanese equities lower,” said Hirokazu Kabeya, chief global strategist at Daiwa Securities. “On the other hand, as the pace of US monetary tightening is expected to slow down given the situation, there might be some positive impacts as well.”

In FX, a gauge of the dollar fell for a third session as US government measures to ease concern over the collapse of Silicon Valley Bank curbed demand for havens. There’s expectation that the US emergency measures will limit the shock from SVB’s failure, including contagion risks, according to Teppei Ino, head of global markets research at MUFG Bank Ltd. “Dollar-yen was bought back to a certain extent as traders and investors welcomed measures including protection of depositors and securing of liquidity”.

In rates, treasury futures just off highs of the day after gapping up, as investors remained in risk-off mode as the collapse of Silicon Valley Bank reverberates through financial markets. Yields richer by more than 25bp across front-end of the curve with 2s10s, 5s30s spreads steeper by 15bp-16bp on the day; 10- year yields lower by around 12bp at 3.58% with bunds outperforming by 8bp in the sector. Curve is aggressively steepening as Fed-dated OIS swaps gap lower and rate-hike premium erodes from front-end of the curve; the 2s10s has moved from -110bps last week to 67% today after Goldman Sachs economists said they no longer expect the Fed to deliver a rate increase next week. Fed-dated OIS pricing in around 15bp of rate hikes for the March policy meeting with Fed peak gapping lower to around 4.90% for the June decision, implying around 35bp of additional hikes for this cycle.

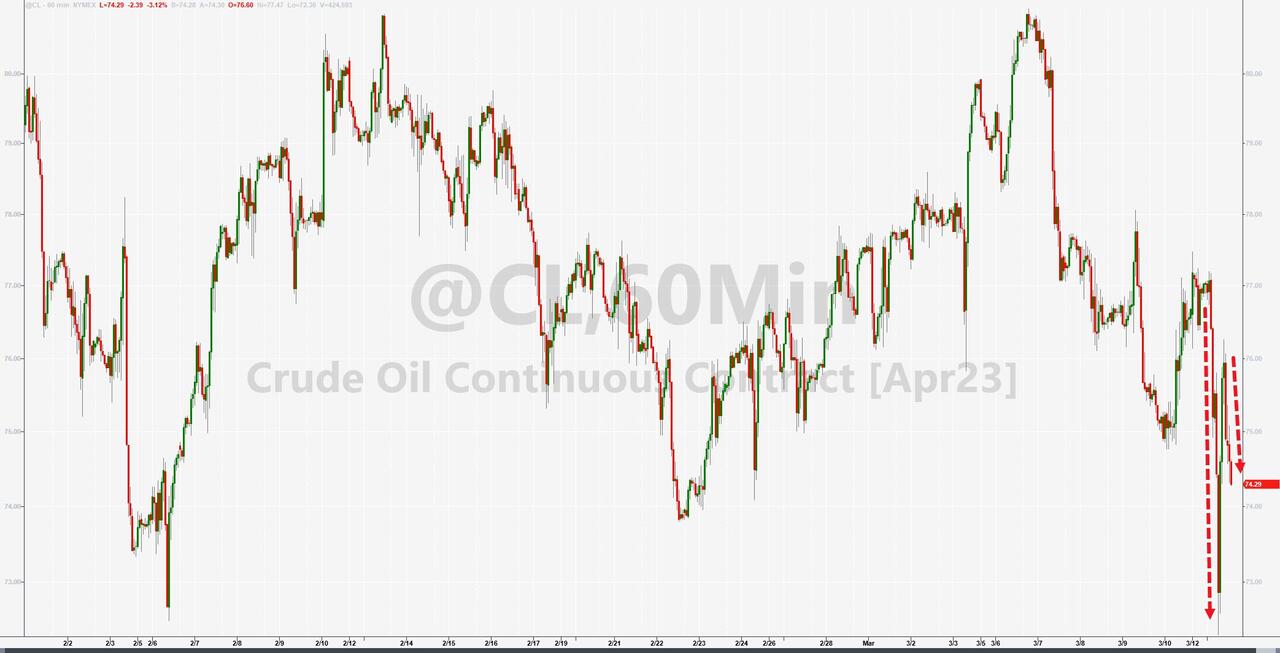

Commodities have, ex-spot gold, come under marked pressure as risk sentiment deteriorates throughout the European morning. Specifically, WTI and Brent front months have suddenly tumbled, accelerating an earlier loss, as the market prices in a recession.

Base metals are well off best levels, given the risk tone, but are somewhat cushioned by the USD continuing to slip. Action which is assisting spot gold, alongside traditional haven allure, with the yellow metal up to USD 1893/oz at best.

Lluckily, there is nothing scheduled on todays’ econ calendar; instead we will be focusing mostly on the worsening bank crisis.

Market Snapshot

S&P 500 futures down 0.6% to 3,876.5

STOXX Europe 600 down 1.1% to 448.71

MXAP up 0.2% to 158.26

MXAPJ up 1.0% to 508.50

Nikkei down 1.1% to 27,832.96

Topix down 1.5% to 2,000.99

Hang Seng Index up 1.9% to 19,695.97

Shanghai Composite up 1.2% to 3,268.70

Sensex down 1.2% to 58,442.44

Australia S&P/ASX 200 down 0.5% to 7,108

Brent Futures down 0.2% to $82.65/bbl

Gold spot up 0.5% to $1,878.19

U.S. Dollar Index down 0.56% to 103.99

German 10Y yield little changed at 2.38%

Euro up 0.6% to $1.0710

Top Overnight News

US authorities took extraordinary measures to shore up confidence in the financial system after the collapse of Silicon Valley Bank, introducing a new backstop for banks that Federal Reserve officials said was big enough to protect the entire nation’s deposits.

The turmoil following the collapse of Silicon Valley Bank continued to spread Monday, with First Republic Bank shares falling about 60% in pre-market trading despite efforts by the US regional lender to reassure investors on its liquidity.

HSBC Holdings Plc is buying the UK arm of Silicon Valley Bank, the culmination of a frantic weekend where ministers and bankers explored various ways to avert the SVB unit’s collapse.

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded mixed with financials hit amid the fallout from the SVB collapse and subsequent failure of Signature Bank, although US equity futures were supported and there was also a gradual improvement in Asia following efforts to stabilise the financial system with bank deposits guaranteed and the Fed announced to make additional funding available to eligible depository institutions to assure that banks have the ability to meet the needs of their depositors. ASX 200 was lower with weakness seen across most industries including the top-weighted financials sector although closed off its lows owing to the resilience in commodity-related stocks and with money market rates pricing in over 75% probability of a pause at next month’s RBA meeting. Nikkei 225 retreated to beneath the 28,000 level with financial stocks dominating the list of worst performers. Hang Seng and Shanghai Comp. were positive with Hong Kong boosted by gains in tech after President Xi advocated strengthening science and technology at the closing remarks of the NPC and with Bilibili boosted following the inclusion of its Z shares to the Stock Connect, while the mainland was also kept afloat after China reported stronger-than-expected loans/financing data and surprisingly retained PBoC Governor Yi Gang as the head of the central bank.

Top Asian News

China’s parliament officially approved senior government positions with Li Qiang as Premier, while Yi Gang will remain PBoC Governor and Liu Kun will remain Finance Minister, according to Xinhua.

Chinese President Xi said China should implement a strategy of rejuvenating the country through science and education, while he added that they should work to achieve greater self-reliance, strength in science and technology, as well as promote industrial transformation and upgrading, according to Reuters.

Chinese Premier Li said China needs to further enhance scientific and technological innovation capabilities, speed up construction of a modern market system and focus on high-quality development. Li said that China will unswervingly deepen reform and opening up, while he noted there are many favourable factors supporting China’s economy but also said that China faces many difficulties this year and that it is not easy to achieve the 2023 growth target of around 5%.

China’s NBS head Kang Yi said China’s economy still contains deep structural contradictions and problems.

China reportedly privately suggested that the US consider a simultaneous visit by US VP Harris to China if House Speaker McCarthy decides to go to Taiwan, according to US sources cited by SCMP.

China’s city of Xi’an in the Shaanxi province revealed an emergency response plan last week that would enable it to shut schools, businesses and “other crowded places” in the event of a severe flu epidemic, according to CNN.

European bourses are under substantial pressure, Euro Stoxx 50 -2.8%, with banking names leading the downside as contagion concern continues, SX7P -5.5%. Action which comes despite US and UK regulators stepping in over the weekend/Monday morning (details above) as concern remains over regional banks such as First Republic and Western Alliance Bank., -62% and -22% in the pre-market respectively. Stateside, futures have been faring comparably better given the backstop measures and strength in large-cap banking names; however, this has since eroded as broader sentiment deteriorated further, ES +0.1%, RTY -0.4%. Specifically, large-cap banking names in the US are now negative; JPM -2.5%, WFC -3.3% & BAC -5.0% in the pre-market.

Top European News

Germany’s Verdi trade union called for a strike of security personnel at Berlin airport on Monday due to disputes regarding remuneration for working nights, weekends and bank holidays, according to Reuters.

Riksbank is to begin selling gov’t bonds on 4th April, to take place every calendar month except for July and August.

FX

Buck loses safe-haven mantle to the Yen, Franc and Gold.

Dollar also down vs other majors irrespective of marked risk aversion, albeit off lows

EUR/USD back below 1.0700, Cable sub-1.2100, AUD/USD under 0.6650 and NZD/USD beneath 0.6200.

PBoC set USD/CNY mid-point at 6.9375 vs exp. 6.9380 (prev. 6.9655)

Fixed Income

Benchmarks are firmer across the board amid a significant dovish adjustment to expected Central Bank activity.

Specifically, USTs are firmer by in excess of a full point, though off an earlier 114.29+ peak, with Reuters pricing now having a roughly equal chance of an unchanged announcement in March or a 25bp hike from the Fed.