MARCH 17//BANK RESCUE OF CREDIT SUISSE AND USA REGIONAL BANKS FAIL AS THEIR STOCKS FALL BADLY AND THAT PROPELS PRECIOUS METALS HIGHER: GOLD CLOSED UP $50.50 TO $1968.70//SILVER FINISHED THE DAY UP 79 CENTS TO $22.38//PLATINUM WAS UP $14.25 WHILE PALLADIUM WAS UP $42.50//UPDATES ON THE CREDIT SUISSE PROBLEMS AS WELL AS PROBLEMS WITH USA BANKS//PAM AND RUSS MARTENS DISCUSS THE DERIVATIVE MESS AT USA AND FOREIGN BANKS: A MUST READ!!//COVID UPDATES//DR PAUL ALEXANDER/DR PANDA/VACCINE IMPACT//SLAY NEWS//UKRAINE VS RUSSIA UPDATE//GREG HUNTER INTERVIEWS BILL HOLTER AND DR PAUL CRAIG ROBERTS A MUST SEE//CHINA REDUCES ITS RR TRYING TO STIMULATE DEMAND/CHINA’S USA DOLLAR RESERVES FALLS TO $859 BILLION//USA DATA RELEASES//SWAMP STORIES FOR YOU TONIGHT//

435 H SCOTIA CAPITAL 97 624 H BOFA SECURITIES 7 657 C MORGAN STANLEY 1 661 C JP MORGAN 175 77 690 C ABN AMRO 21 732 C RBC CAP MARKETS 6 737 C ADVANTAGE 7 3 905 C ADM 24

TOTAL: 209 209 MONTH TO DATE: 4,460

JPMORGAN stopped 77/209 contracts

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR MAR/2023. CONTRACT: 209 NOTICES FOR 20900 OZ or 0.6500 TONNES

total notices so far: 4450 contracts for 44,600 oz (13.8724 tonnes)

SILVER NOTICES: 31 NOTICE(S) FILED FOR 155,000 OZ/

total number of notices filed so far this month : 3041 for 15,205,000 oz

END

GLD

WITH GOLD UP $50.50

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/NO CHANGES IN GOLD INVENTORY AT THE GLD://////

INVENTORY RESTS AT 914.72TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 79 CENTS

WHAT????????

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF OF 10.478 MILLION OZ FROM THE SLV: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 462.748. MILLION OZ

SOMEBODY WAS BADLY IN NEED OF SILVER FROM THE SLV TODAY.

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY AN GIGANTIC SIZED 1901 CONTRACTS TO 119,412 A NEW RECORD LOW AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS GIGANTIC SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.25 LOSSIN SILVER PRICING AT THE COMEX ON THURSDAY. THUS WE ARE NOW RECORDING FOR PROSPERITY OUR NEW LOW COMEX OI SILVER SET AT 119,412 CONTRACTS , MARCH 17/2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.25). AND WERE SUCCESSFUL IN KNOCKING SOME SPEC LONGS AS WE HAD A VERY STRONG LOSS ON OUR TWO EXCHANGES 1356 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 1 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD: A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS( 400 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.58 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE JUMP TO LONDON OF 110,000 OZ//NEW STANDING: 15.390 MILLION OZ + THE 1.0 MILLION OZ OF EXCHANGE FOR RISK//THUS TOTAL NEW STANDING 16.390 MILLION OZ/ //// V) HUGE SIZED COMEX OI LOSS/ GOOD SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –145 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTRACTS for 13 days, total 10,494 contracts: OR 52.470 MILLION OZ . (807 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 52.47 MILLION OZ

.

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 52.47MILLION OZ//INITIAL//ON PAR WITH LAST MONTH

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1901 CONTRACTS WITH OUR $0.25 LOSS IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE CONTRACTS: 400 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAR OF 15.58 MILLION OZ//FIRST DAY NOTICE// FOLLOWED BY TODAY’S 110,000 OZ QUEUE JUMP TO LONDON (WHICH INCREASES THE AMOUNT OF SILVER STANDING) + 1.0 MILLION OF EXCHANGE FOR RISK ISSUED EARLY IN MARCH (INCREASES THE AMOUNT OF SILVER STANDING) //NEW STANDING 16.390 MILLION OZ .. WE HAVE A GIGANTIC SIZED LOSS OF 1501OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 31 NOTICE(S) FILED TODAY FOR 155,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 1532 CONTRACTS TO 457,252 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 1363 CONTRACTS.

.

WE HAD A FAIR SIZED INCREASE IN COMEX OI ( 1532CONTRACTS) DESPITE OUR $6.95 LOSS IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR MAR. AT 4.9953 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 34,300 OZ (1.067 TONNES) //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London).

YET ALL OF..THIS HAPPENED WITH OUR $6.95 LOSS IN PRICEWITH RESPECT TO THURSDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 3762 OI CONTRACTS (11.70 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2230 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 457,252

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3762 CONTRACTS WITH 1532CONTRACTS INCREASED AT THE COMEX AND 2230 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3762 CONTRACTS OR 11.70 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2230 CONTRACTS) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (1532) TOTAL GAIN IN THE TWO EXCHANGES 3,762 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR MAR. AT 4.9953 TONNES FOLLOWED BY TODAY’S 34,300 OZ QUEUE JUMP//NEW STANDING 14.765 TONNES // ///3) ZERO LONG LIQUIDATION //4) FAIR SIZED COMEX OPEN INTEREST GAIN// 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

TOTAL EFP CONTRACTS ISSUED: 52,743 CONTRACTS OR 5,274,300 OZ OR 164.05 TONNES IN 13 TRADING DAY(S) AND THUS AVERAGING: 4057 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13TRADING DAY(S) IN TONNES 164.05 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 164.05/3550 x 100% TONNES 4.61% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 164.05 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A GIGANTIC SIZED 1901 CONTRACTS OI TO 119,412 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A RECORD LOW OF 119,412 CONTRACTS MARCH 17/2022

EFP ISSUANCE 400 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 400 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 400 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1901CONTRACTS AND ADD TO THE 400 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE LOSS OF 1501 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES //7.505 MILLION OZ

OCCURRED DESPITE OUR $0.25 LOSS IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED UP 23.66 PTS OR 0.73% //Hang Seng CLOSED UP 314,68 PTS OR 1.64% /The Nikkei closed DOWN 323.18 PTS OR 1.20% //Australia’s all ordinaries CLOSED UP 0.50% /Chinese yuan (ONSHORE) closed UP 6.8892//OFFSHORE CHINESE YUAN UP TO 6.8904// /Oil UP TO 68.91 dollars per barrel for WTI and BRENT AT 74,58 / Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 1532 CONTRACTS UP TO 457,252 DESPITE OUR LOSS IN PRICE OF $6.95 ON THURSDAY

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAR… THE CME REPORTS THAT THE BANKERS ISSUED A VERY FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2230 EFP CONTRACTS WERE ISSUED: : APRIL 2230 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2230 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 3762 CONTRACTS IN THAT 2230LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED GAIN OF 1532 COMEX CONTRACTS..AND THIS GOOD SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $6.95. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAR (14.765) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 14.765 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $6.95) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR GOOD SIZED GAIN OF 3762 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 11.70 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAR. (4.9953 TONNES) FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 34,300OZ (1.576 TONNES)… ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $18.75

WE HAD -1363 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3762 CONTRACTS OR 376200 OZ OR 11.70 TONNES

Total monthly oz gold served (contracts) so far this month

4460 notices 446,000 13.8724 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 1

i) out of BRINKS: 23,417.201 oz

total withdrawals: 23,417.201 oz

in tonnes: 0.728 tonnes

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of MARCH we have an oi of 496 contracts having LOST 101 contracts. We had 444 notices filed on THURSDAY so we

gained A HUGE 343 contracts or an additional 34,300 oz will stand for metal at the comex

April lost 6260 contracts down to 182,473 contracts

May LOST 3 contracts to stand at 270

We had 209 notice(s) filed today for 20,900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 209 notices were issued from their client or customer account. The total of all issuance by all participants equate to 209 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 77 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAR. /2023. contract month,

we take the total number of notices filed so far for the month (4,460 x 100 oz ), to which we add the difference between the open interest for the front month of (MAR. 496 CONTRACTS) minus the number of notices served upon today 209 x 100 oz per contract equals 440,400 OZ OR 13.698 TONNES the number of TONNES standing in this active month of MARCH.

thus the INITIAL standings for gold for the MAR contract month:

No of notices filed so far (4,460 x 100 oz+ 496 OI for the front month minus the number of notices served upon today (209)x 100 oz} which equals 474,700 oz standing OR 14.765 TONNES in this active delivery month of MARCH..

TOTAL COMEX GOLD STANDING: 14.765 TONNES WHICH IS HUGE FOR AN INACTIVE DELIVERY MONTH.

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 3041 x 5,000 oz = 15,205,000 oz

to which we add the difference between the open interest for the front month of MAR(68) and the number of notices served upon today 31 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAR./2023 contract month: 3041 (notices served so far) x 5000 oz + OI for the front month of MAR (68) – number of notices served upon today (31) x 500 oz of silver standing for the MAR. contract month equates 15.390 million oz +the 1.0 million oz of exchange for risk//new total standing 16.390 million oz

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

MARCH 15/THE IDES OF MARCH: WITH GOLD UP $18.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 913.27 TONNES

MARCH 14/WITH GOLD DOWN $4.75 TODAY: HUGE CHANGES: A MONSTER DEPOSIT OF 11.85 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 913.27 TONNES

MARCH 13/WITH GOLD UP $48.85 TODAY: VERY STRANGE HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY REST AT 901.42 TONNES

MARCH 10//WITH GOLD UP $31.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 903.15 TONNES

MARCH 9/WITH GOLD UP $16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 906.62 TONNES

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

FEB 28/WITH GOLD UP $12.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 917.61 TONNES

FEB 27/WITH GOLD UP $6.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.32 TONNES

FEB 24/WITH GOLD DOWN $9.10 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 917.32 TONNES

FEB 23/WITH GOLD DOWN $13.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 919.92 TONNES

FEB 22/WITH GOLD DOWN 22 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 919.92 TONNES

FEB 21/WITH GOLD DOWN $7.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 919.92 TONNES

FEB 17/WITH GOLD DOWN $1.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 921.08 TONNES

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

GLD INVENTORY: 914.72 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 17/WITH SILVER UP 79 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE WITHDRAWAL OF 10.478 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 462.748 MILLION OZ//

MARCH 16/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 5.009 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 473.226 MILLION OZ//

MARCH 15/WITH SILVER DOWN 7 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 643,000 OZ INTO THE SLV//INVENTORY RESTS AT 478.235 MILLION OZ/

MARCH 14/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.287 MILLION OZ FROM THE SLV////INVENTORY REST AT 477.592 MILLION OZ//

MARCH 13/WITH SILVER UP $1.35 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ//

MARCH 10.WITH SILVER UP 36 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ…

MARCH 9/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.979 MILLION OZ

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWALOF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

FEB 28/WITH SILVER UP 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.241 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.188

FEB 27/WITH SILVER DOWN 15 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.471 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 482.429 MILLION OZ

FEB 24/WITH SILVER DOWN 46 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.172 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.900 MILLION OZ//

FEB 23/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.379 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.072 MILLION OZ//

FEB 22/WITH SILVER DOWN 22 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ FROM THE SLV////INVENTORY RESTS AT 485.693 MILLION OZ

FEB 21/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.5363 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 486.382 MILLION OZ//

FEB 17/WITH SILVER UP 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 827,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.819 MILLION OZ/

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 462.748MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

Chinese Gold Demand Continued To Surge In February

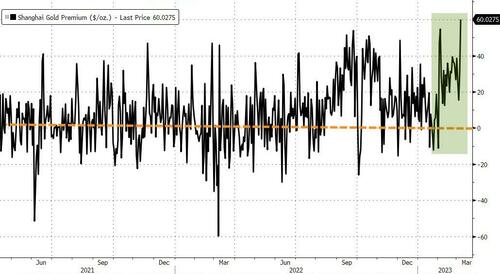

After ending 2022 on an upward trend that continued into January, Chinese gold demand surged again in February as the economy continues to rebound from government-imposed COVID policies.

Gold withdrawals from the Shanghai Gold Exchange (SGE) totaled 169 tons in February. This is a reflection of strong wholesale demand and signals an ongoing rebound in the world’s biggest gold market.

SGE withdrawals in February were up by 30 tons month-on-month and by a healthy 76 tons year-over-year. It was the strongest February for wholesale gold demand since 2014.

The World Gold Council pinpointed two primary drivers of strong demand for gold in February.

Healthy consumption amid the economic recovery and the release of pent-up demand

Retailers’ restocking activities after the Chinese New Year (CNY) holiday

The Shanghai-London gold price premium also continued to pick up in February, reflecting strong Chinese gold demand during the month.

After a weak first half of 2022, gold demand in China surged during the last half of the year as the government relaxed COVID restrictions. With demand rebounding last two quarters, China imported 1,343 tons of gold in 2022, the highest import level since 2018. Total gold imports for the year were up 64% over 2021.

A recovery in the Chinese economy after government COVID restrictions strangled it helped drive the rebound in the gold market last year and into 2023. China experienced a COVID peak in December. According to the World Gold Council, Chinese economic activities revived in January.

The recovery in the Chinese economy was evidenced by the official Comprehensive Purchasing Managers Index (PMI) surging to 56.4 in February. It was the highest PMI on record since 2017. Manufacturing activities expanded the most since April 2012, and the service PMI grew at the fastest pace in 22 months.

Also, as we’ve reported, the People’s Bank of China resumed official gold purchases in November. That continued into February, with the Chinese central bank adding another 25 tons to its reserves. Gold now accounts for 3.7% of China’s total reserves.

Over the last four months, Chinese gold reserves have increased by 102 tons, based on official reported numbers.

There has always been speculation that China holds far more gold than it officially reveals. As Jim Rickards pointed out on Mises Daily back in 2015, many people speculate that China keeps several thousand tons of gold “off the books” in a separate entity called the State Administration for Foreign Exchange (SAFE).

If this apparent rebound in the Chinese gold market continues deeper into 2023, it will drive overall global gold demand higher. Gold demand grew by 18% to 4,741 tons in 2022, the highest demand in 11 years.

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

U.S. Treasury Secretary Janet Yellen finds herself in a very dubious position. Under the Dodd-Frank financial reform legislation of 2010, the U.S. Treasury Secretary was given increased powers to oversee financial stability in the U.S. banking system. This increase in power came in response to the 2008 financial crisis – the worst financial collapse since the Great Depression. The legislation made the Treasury Secretary the Chair of the newly created Financial Stability Oversight Council (F-SOC), whose meetings include the heads of all of the federal agencies that supervise banks and trading on Wall Street. The legislation also required the Treasury Secretary’s authorization before the Federal Reserve could create any more of those $29 trillion emergency bailout programs for the mega banks – which had tethered themselves to casino trading on Wall Street since the repeal of the Glass-Steagall Act in 1999.

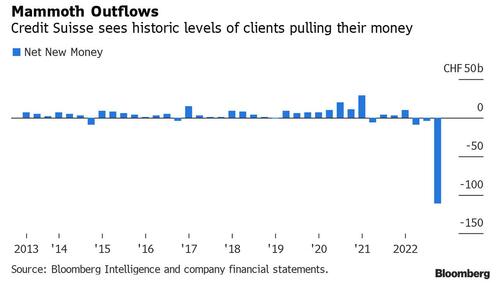

Yesterday, after the Swiss banking behemoth Credit Suisse had traded at an all-time low of less than two bucks; blown out its credit default swaps to unprecedented levels; and tanked the Dow Jones Industrial Average by more than 700 points intraday, Bloomberg News ran this headline at 12:54 p.m. – “US Treasury Reviewing US Banks’ Exposure to Credit Suisse.” By “exposure,” the Treasury really means how many billions of dollars of underwater derivatives are U.S. banks on the hook for as a counterparty to Credit Suisse. The Treasury also has to worry about U.S. banks’ exposure to Credit Suisse’s other major counterparties that U.S. banks do business with, even if the banks are not direct counterparties to Credit Suisse itself.

If the U.S. Treasury Secretary and her staff at F-SOC were just yesterday getting around to finding out which U.S. banks had counterparty exposure to Credit Suisse’s derivatives, we are all in very big trouble. The serious problems at Credit Suisse have been making headlines for two years, including here at Wall Street On Parade.

In July of 2021, the law firm Paul, Weiss, Rifkind, Wharton & Garrison released a 165-page report on the internal investigation it had conducted for the Board of Credit Suisse into how the bank came to lose $5.5 billion conducting highly-leveraged and dodgy derivative trades for the family office hedge fund, Archegos Capital Management, which went belly-up in March of 2021. The Paul, Weiss lawyers wrote:

“The Archegos-related losses sustained by CS are the result of a fundamental failure of management and controls in CS’s Investment Bank and, specifically, in its Prime Services business. The business was focused on maximizing short-term profits and failed to rein in and, indeed, enabled Archegos’s voracious risk-taking. There were numerous warning signals — including large, persistent limit breaches — indicating that Archegos’s concentrated, volatile, and severely under-margined swap positions posed potentially catastrophic risk to CS. Yet the business, from the in-business risk managers to the Global Head of Equities, as well as the risk function, failed to heed these signs, despite evidence that some individuals did raise concerns appropriately.”

Six months ago, Dennis Kelleher, President and CEO of the nonprofit watchdog, Better Markets, released a statement about the deteriorating condition of Credit Suisse, highlighting the following:

“As the financial condition of Credit Suisse continues to deteriorate, raising questions of whether it will collapse, the world and U.S. taxpayers should be deeply worried as multiple, simultaneous shocks shake the foundations of economies worldwide. Credit Suisse is a global, systemically significant, too-big-to-fail bank that operates in the U.S. and is deeply interconnected throughout the global financial system. Its failure would have widespread and largely unknown repercussions from the inconvenient to the possibly catastrophic.

“That is due, in part, to the failure of the Federal Reserve to properly regulate the activities of foreign banks that have U.S.-based operations. The U.S. has a largely ineffective regulatory framework with gaping loopholes that fail to include some of even the most basic safety and soundness requirements, which incentivizes regulatory arbitrage. As a result, the U.S. financial system and economy are needlessly threatened.

“An effective and appropriate regulatory framework for large foreign banks that covers all of their U.S.-based affiliates should have been established when the Fed set up so-called U.S.-based intermediate holding companies (‘IHCs’) that they regulate. Instead, U.S.-based branches of foreign banks (which are not consolidated within the IHC) face significantly weaker standards than the IHC, remarkably including no specific capital requirements in the U.S. Furthermore, the branches have significantly weaker liquidity requirements. This has resulted in many foreign banks – including in particular Credit Suisse – engaging in regulatory arbitrage by shifting large amounts of assets from their IHCs to their branches, entities that are entirely reliant on the resources of their foreign-based parent companies. The 2008 financial collapse proved that these resources are not available in periods of stress, which is why the U.S. bailed out so many foreign banks operating in the U.S. The Fed should have stopped that long ago.

“As is well-known, risks in the global financial system that materialize elsewhere easily end up becoming risks here in the U.S. and threaten our financial system and economy. Those risks are amplified by the unprecedented fiscal and monetary policies attempting to address the many unexpected shocks from the pandemic and war. The Fed must see Credit Suisse as a warning sign and improve the regulatory framework for large foreign banks and all banks to ensure that the American financial system and economy are properly protected.”

Credit Suisse’s reputation has taken more hits from its involvement in the Greensill Capital scandal and the infamous spy-gate scandal in 2019 where the bank spied on and followed various employees.

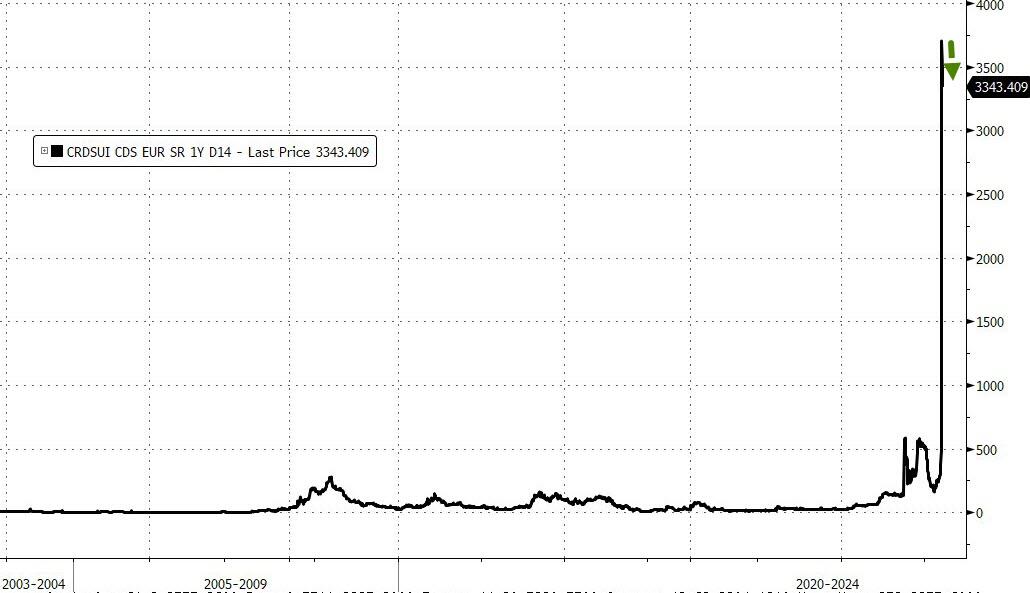

Nervousness about Credit Suisse reached a pivotal moment in the fall of last year. On November 30, its 5-year Credit Default Swaps (CDS) blew out to 446 basis points. That was up from 55 basis points in January of 2022 and more than five times where CDS on its peer Swiss bank, UBS, were trading. The price of a Credit Default Swap reflects the cost to traders, or investors with exposure, to insuring themselves against a debt default by the bank.

If all of this didn’t awaken Secretary Yellen from her slumber about the contagion risks posed by a deteriorating Credit Suisse, she should have been jolted upright on December 5 of last year when researchers for the Bank for International Settlement (Claudio Borio, Robert McCauley and Patrick McGuire) released an astonishing report that found that foreign banks had secret derivative debt that is “10 times their capital.”

The report focused on the amount of derivative debt that was not being captured through regular statistical reporting because it is held off the banks’ balance sheets. The researchers refer to this exposure as “staggering” and note the potential for upsets to dollar swap lines to settle it as it comes due.

The report raises further alarm bells with this: “For banks headquartered outside the United States, dollar debt from these instruments is estimated at $39 trillion, more than double their on-balance sheet dollar debt and more than 10 times their capital.” Their on-balance sheet dollar debt is $15 trillion.

The most recent quarterly derivatives report from the U.S. regulator of national banks, the Office of the Comptroller of the Currency (OCC), found that as of September 30, 2022 four U.S. mega banks held 88.6 percent of all notional amounts of derivatives in the U.S. banking system. The total notional amount for all banks was $195 trillion. JPMorgan Chase held $54.3 trillion of that; Goldman Sachs held $50.97 trillion; Citigroup’s Citibank held $46 trillion; and Bank of America held $21.6 trillion. Even though the Dodd-Frank legislation required that most of these derivative trades move to central clearing, as of September 30, 2022 the OCC report found that 58.3 percent of these derivatives were not being centrally-cleared, meaning they were over-the-counter (OTC) private contracts between counterparties, thus adding another layer of opacity to an unaccountable system.

For the role that Citigroup played in keeping these dangerous derivatives inside federally-insured banks, see our December 2014 report: Meet Your Newest Legislator: Citigroup.

end

3. CHRIS POWELL//GATA AND OTHER IMPORTANT GOLD COMMENTARIES

A must read….

Pam and Russ Martens: The next bomb to go off in the banking crisis will be derivatives

Submitted by admin on Thu, 2023-03-16 11:19Section: Daily Dispatches

By Pam and Russ Martens Wall Street on Parade Thursday, March 16, 2023

U.S. Treasury Secretary Janet Yellen finds herself in a very dubious position.

Under the Dodd-Frank financial reform legislation of 2010, the U.S. treasury secretary was given increased powers to oversee financial stability in the U.S. banking system. This increase in power came in response to the 2008 financial crisis — the worst financial collapse since the Great Depression. The legislation made the treasury secretary the chair of the newly created Financial Stability Oversight Council (F-SOC), whose meetings include the heads of all of the federal agencies that supervise banks and trading on Wall Street.

The legislation also required the Treasury secretary’s authorization before the Federal Reserve could create any more of those $29 trillion emergency bailout programs for the mega banks, which had tethered themselves to casino trading on Wall Street since the repeal of the Glass-Steagall Act in 1999.

Yesterday, after the Swiss banking behemoth Credit Suisse had traded at an all-time low of less than two bucks; blown out its credit default swaps to unprecedented levels; and tanked the Dow Jones Industrial Average by more than 700 points intraday, Bloomberg News ran this headline at 12:54 p.m.: “U.S. Treasury Reviewing U.S. Banks’ Exposure to Credit Suisse.”

By “exposure” the Treasury really means how many billions of dollars of underwater derivatives U.S. banks are on the hook for as a counterparty to Credit Suisse.

The Treasury also has to worry about U.S. banks’ exposure to Credit Suisse’s other major counterparties that U.S. banks do business with, even if the banks are not direct counterparties to Credit Suisse itself.

If the U.S. Treasury Secretary and her staff at F-SOC were just yesterday getting around to finding out which U.S. banks have counterparty exposure to Credit Suisse’s derivatives, we are all in very big trouble. The serious problems at Credit Suisse have been making headlines for two years. …

Alasdair Macleod: To rescue markets, pivoting Fed will wreck dollar

Submitted by admin on Thu, 2023-03-16 12:24Section: Daily Dispatches

By Alasdair Macleod GoldMoney, Toronto Thursday, March 16, 2023

Following the day-to-day twists and turns of a banking crisis can make us lose sight of the bigger picture. It is tempting to think that the banking authorities are in control and will secure the integrity of their commercial banking networks. Unfolding events may or may not prove this to be true.

The bigger picture is that the 40-year decline in interest rates is over, as well as the financial bubble that has built up with it. We should also be aware that there is a cycle of bank credit, the downturn of which is long overdue. The two have come together to create chaos in credit markets.

The reality is that central banks have already lost control over monetary policy and interest rates. Interest rates are now being driven by contracting bank credit, not by monetary policy.

The point commonly missed is that contracting credit at a time when credit demand is still increasing inevitably leads to higher interest rates and bad debts.

Having lost control over interest rates, the Federal Reserve has been forced into its much-heralded pivot, not by reducing interest rates, but by offering to buy Treasury and agency debt at face value whatever the coupon and maturity. This rescues banks from the immediate fate that collapsed Silicon Valley Bank. And it makes it easier for the U.S. Treasury to fund its deficit while containing borrowing costs.

But it is highly inflationary.

The pivot has now been made. The Fed has decided to rescue financial markets at the expense of the currency. Other central banks can be expected to follow suit to help rescue their banking systems. But they are writing the death warrants for their fiat currencies. …

The International Atomic Energy Agency (IAEA) has sounded the alarm bells over some 2.5 tons of Ghadafi-era natural uranium that has disappeared from a site in Libya that is not under control of the Tripoli-based Government of National Unity (GNU).

IAEA inspectors“found that ten drums containing approximately 2.5 tons of natural uranium in the form of UOC (uranium ore concentrate) previously declared by (Libya) … as being stored at that location were not present at the location,” the global nuclear watchdog said in a Wednesday statement delivered by IAEA head Rafael Grossi.

“The loss of knowledge about the present location of nuclear material may present a radiological risk, as well as nuclear security concerns,” Grossi added.

Libya’s long-running civil war had prevented the IAEA from inspecting the site earlier.

While the Agency has not indicated the exact location of the site, there is high probability that the site is Sabha, some 400 miles south-east of the western capital, Tripoli. This area is not controlled by the government. Raw uranium, or yellow cake, is also believed to be stored at the Tajura nuclear research facility near Tripoli; however, this area is under control of the GNU.

Sabha was a Ghadafi-era facility that had hoped to eventually enrich uranium for a nuclear weapons program until it was mothballed in 2003.

The IAEA vowed to investigate the circumstances surrounding the disappearance of the uranium.

The concern is that while natural uranium cannot be used either for energy or weapons without a complicated enrichment process, if it ended up in the wrong hands it could be sold to regimes with this capability.

Speaking to the BBC, Scott Roecker from the Nuclear Threat Initiative, said that in its current form, the natural uranium “cannot be made into a nuclear weapon”, but could be used as a “feedstock” for a nuclear weapons program. He also noted that the material “doesn’t really have any radiation in its current form”.

END

Nickel:

More problems for the LME:: bags of stones instead of nickel .

*LME Finds Some Nickel Underlying Its Contracts Is Missing

Problem found at Access World Rotterdam warehouse: sources

Access World spokesperson declined to comment on nickel

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 6.8892

OFFSHORE YUAN: 6.8904

SHANGHAI CLOSED UP 23.66 PTS OR 0.73%

HANG SENG CLOSED UP 314.68 PTS OR 1.64 %

2. Nikkei closed UP 323.18 PTS OR 1.20%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 103.95 Euro RISES TO 1.0619 UP 5 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.222!!(Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 132.56/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

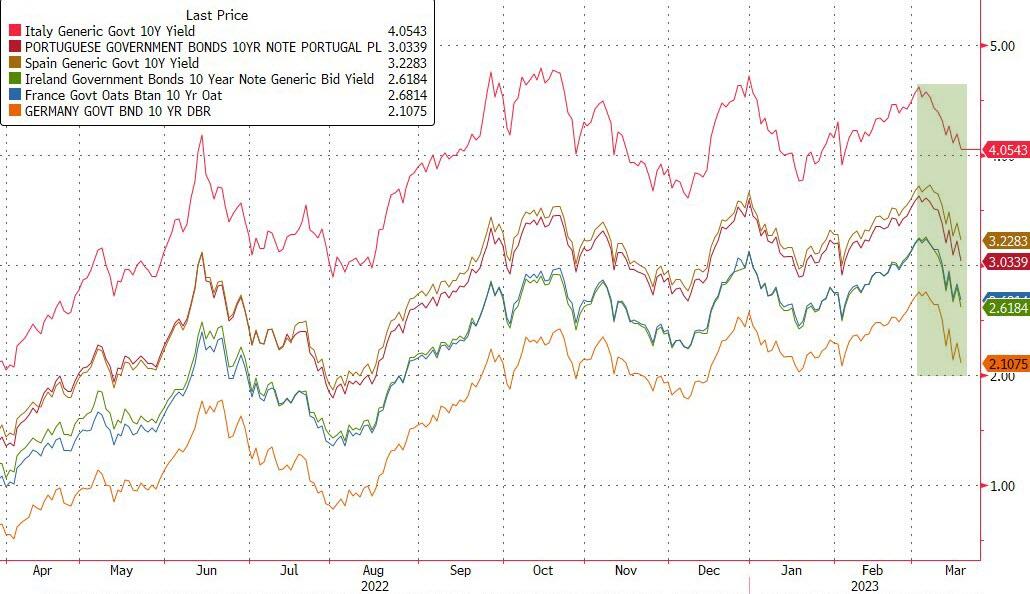

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.1865%***/Italian 10 Yr bond yield FALLS to 4.104%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.289…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.146//

3j Gold at $1935,20//silver at: 21.89 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 32/100 roubles/dollar; ROUBLE AT 76.72//

3m oil into the 68 dollar handle for WTI and 74 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 132.56/10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .222% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9270–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9842well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc. CREDIT SUISSE IN TROUBLE

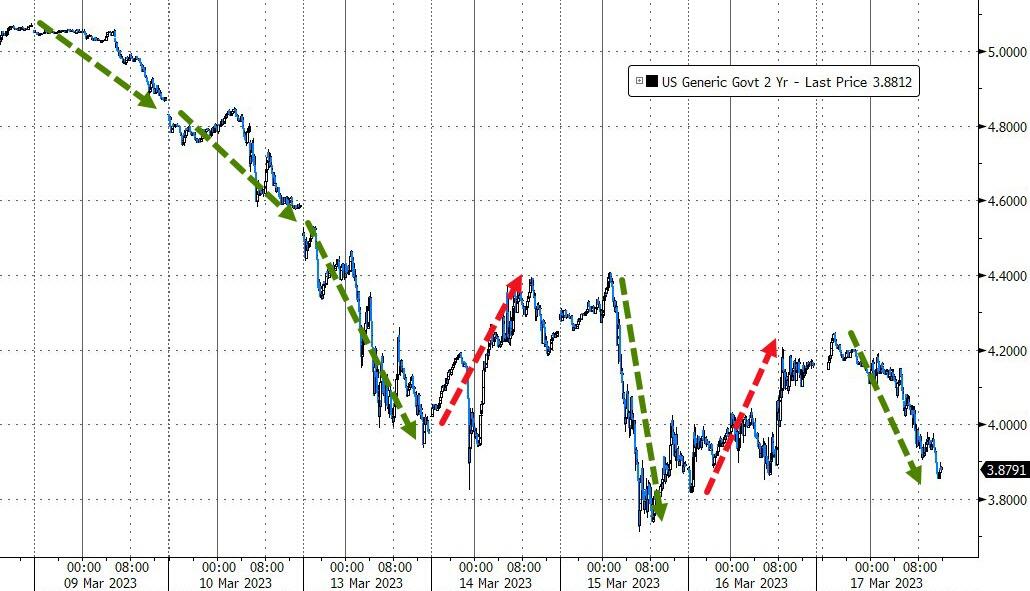

USA 10 YR BOND YIELD: 3.4850% DOWN 9 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.639 DOWN 8 BASIS PTS//INVERTED TO THE 10 YEAR!!

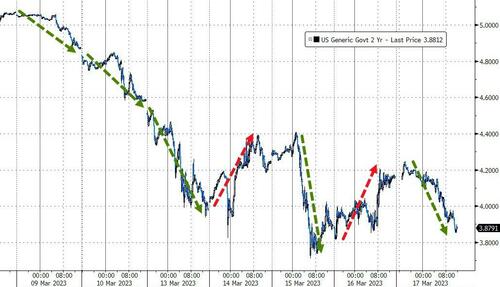

USA 2 YR BOND YIELD: 4.0839 DOWN 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.01…

GREAT BRITAIN/10 YEAR YIELD: 3.3475% DOWN 2 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Slide As $2.9 Trillion OpEx Chaos Clashes With Broke Bank Bailout Bash

FRIDAY, MAR 17, 2023 – 08:25 AM

Similar to Thursday, futures faded an earlier gain which pushed emini futures briefly above 4000 after the index rallied 1.8% yesterday, as investors were assessing whether a $30BN “deposit injection” rescue package for First Republic Bank is enough to ease the risk of financial contagion, with gains reversing after news that China was cutting its bank reserve ratio and injecting over $70BN in liquidity, which was viewed by the jittery, suspicious market that there may be more unpleasant surprises in the banking sector this time in China which was moving to “ringfence its banking sector.” US equity-index futures dropped 0.3%, reversing a similar gain, while the Stoxx Europe 600 index pared an advance and turned negative. A gauge of European banking stocks is heading for a drop of almost 9% this week. Nasdaq 100 futures were flat as the rates-sensitive gauge heads for its best week since November amid expectations the Federal Reserve will temper its tightening path. The 10-year Treasury yield fell eight basis points and a gauge of the dollar declined.

As detailed yesterday, as if the bank bailout bonanza, a larger than expected TLTRO repayment in Europe and China’s RRR cuts weren’t enough, traders are facing fresh turmoil by today’s $2.9 trillion options expiration after a week of bank drama. Such quad-witching days typically involve portfolio adjustments, spikes in volume and price swings, especially on day so near-record low liquidity such as these.

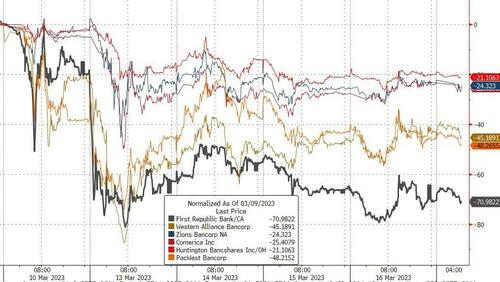

Financial stocks were lower in premarket trading Friday, in line with the broader market, as doubt persists around First Republic Bank despite a $30 billion rescue effort from large lenders and federal regulators. First Republic’s slide continues since market close Thursday, as the California bank discloses its borrowing from the Fed ranged from $20 billion to $109 billion in the last week while billionaire investor Bill Ackman warned the effort to rescue FRC was creating a “false sense of confidence” a remarkable U-turn from him begging for a bailout of SVB. First Republic Bank and PacWest Bancorp are among the most active financial stocks in early premarket trading, falling 11.9% and 4.7%, respectively. FedEx Corp. shares jumped in premarket trading after the parcel company boosted its profit guidance, beating the average analyst estimate. Nvidia Corp. gained slightly as Morgan Stanley upgraded the biggest US chipmaker to overweight from equal-weight. Here are some other notable premarket movers:

US Steel shares rise 5.6%, with analysts saying the company’s new first-quarter earnings guidance was much better than anticipated.

Baidu shares rise 5% in US premarket trading after the Chinese search-engine operator’s newly debuted AI chatbot gained positive reviews from analysts. Other AI-exposed stocks are also higher in premarket trading, with C3.ai (AI US) +3%, BigBear.ai (BBAI US) +8.5%, SoundHound AI (SOUN US) +7.1%.

Cryptocurrency-exposed stocks rose after Bitcoin extended its gains for a second consecutive session, rising back above the $26,000 threshold. Hive Blockchain (HIVE US) climbed 8.7%, Hut 8 Mining (HUT US) +5.8%, Marathon Digital (MARA US) +5.4%, Riot Platforms (RIOT US) +5.7%, Stronghold Digital (SDIG US) +5.1%.

Keep an eye at FMC Corp. stock as it was upgraded to buy from neutral at Redburn, which cites “strong” pipeline-driven growth and an expected further increase in the crop chemical producer’s “industry- leading” margins.

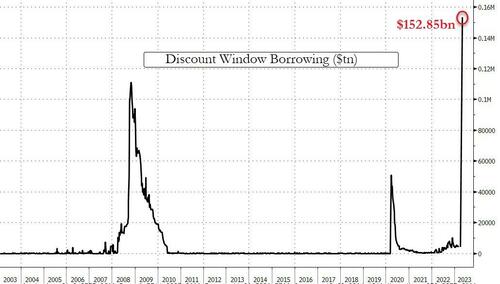

Investors are recovering from a turbulent week that began with banking-sector concerns driving the VIX index of stock volatility to the highest since October and pushing the S&P 500 to the lowest in more than two months. Friday’s quarterly so-called triple witching — where contracts for index futures, equity index options and stock options all expire — could amp up swings in trading. The failure of Silicon Valley Bank prompted the US government to step in, and banks borrowed a combined $164.8 billion from two Federal Reserve backstop facilities in the most recent week.

While that demand for emergency liquidity shows continued caution, the overall rescue efforts have eased the risk of a broader banking-sector contagion, according to Richard Hunter, head of markets at Interactive Investor. “The generally swift and decisive actions which have been taken have removed some of the sting from market volatility,” he said.

“We do not expect a full-blown financial crisis, but one must not dismiss the underlying dynamics,” said Karsten Junius, the chief economist at Bank J Safra Sarasin AG. “Financial conditions will most likely tighten further and increase recession risks. We therefore advocate a defensive positioning with regard to risk assets and a tactically cautious stance on the banking sector, even though the constructive case for banks remains intact over the medium to longer term.”

Bank of America strategist Michael Hartnett said investors should sell any rally in stocks as fund flows don’t yet reflect deep enough concern about a looming recession. The strategist, who correctly warned of a stock exodus in 2022, recommended selling the S&P 500 above 4,100 points, about 3.5% above its last close.

The Stoxx Europe 600 index erased an advance with energy, miners and tech the best-performing sectors. A gauge of European banking stocks is heading for a drop of more than 9% this week as yet another early rally lost steam Friday. Shares in Credit Suisse resumed a decline, falling as much as 10% as the idea of a forced combination with a larger rival UBS Group AG was shot down. The stock had rallied almost 20% Thursday after the Swiss central bank stepped in with support. Bonds across Europe gained, with Germany’s 10-year yield down 10 basis points. Here are the most notable European movers:

European mining stocks rebound from two sessions in the red, with copper, aluminum and steel-exposed names leading the bounce, and Glencore gaining 4.2% as of 10:32 a.m. CET

European logistics and freight stocks gain, after US peer FedEx’s results beat expectations and it upgraded its forecast, sending its shares surging in postmarket trading

Telenor shares rise as much as 3.2%, after a Financial Times report that CK Hutchison is in talks with the Nordic telecom operator about merging their operations in Denmark and Sweden

Webuild shares rise as much as 8.1% to add to a 12% post-earnings jump in the prior session, with Akros raising the Italian construction firm to accumulate from neutral

Nel shares gain as much as 6%, the most since Feb. 7, as Goldman Sachs raises the Norwegian electrolyzer firm to buy, from neutral, on an increasingly strong growth outlook

Enel shares gain as much as 2.4% in early trading. The Italian utility’s FY net income is ahead of expectations, while guidance on its debt and dividend looks robust, analysts say

LSE Group shares rise as much as 3% as UBS upgrades the exchange operator to buy from neutral, saying the risk-reward on the stock is “very favorable”

Credit Suisse fell as investors examine its prospects after a central bank backstop. The firm and UBS are opposed to a forced combination, Bloomberg News reported

Earlier in the session, Asia stocks rebounded, led by Hong Kong-listed shares as risk appetite was helped by a rescue package for First Republic Bank. The MSCI Asia Pacific Index advanced as much as 1.6%, reversing Thursday’s drop. Hong Kong’s Hang Seng China Enterprises Index jumped more than 2%, leading indexes in the region, as Baidu drove China’s artificial intelligence stocks higher after brokers tested its ChatGPT-like service. China’s central bank announced an unexpected cut to its reserve requirement ratio after domestic markets closed. Gains in Asia were broad-based with most markets in the green, after the biggest US lenders agreed to contribute $30 billion in deposits to First Republic. Bank stocks rose as jitters about the health of the US financial system and economy eased. The MSCI Asia gauge was still on track for a second straight week of losses, albeit with smaller declines, as rolling headlines on troubled lenders from Silicon Valley Bank and Signature Bank to Credit Suisse Group AG led to choppy trading. The stock measure came close to entering correction territory prior to Friday’s rebound, with markets also digesting a 50-basis-point rate hike by the European Central Bank ahead of the Federal Reserve’s meeting next week. Shares in Taiwan, South Korea and the tech hardware sector “have over-delivered” this year and are looking particularly vulnerable to shockwaves from the US banking stress, according to Goldman Sachs Group

Japanese stocks rose, following US peers higher, as sentiment improved after Wall Street banks stepped in to rescue First Republic Bank. The Topix Index rose 1.2% to 1,959.42 as of market close Tokyo time, while the Nikkei advanced 1.2% to 27,333.79. Sony Group Corp. contributed the most to the Topix Index gain, increasing 3.5%. Out of 2,159 stocks in the index, 1,567 rose and 509 fell, while 83 were unchanged. Japan equities were also buoyed by growth stocks, which “are outperforming value stocks today, especially tech stocks,” said Rina Oshimo, a senior strategist at Okasan Securities. Meanwhile, the European Central Bank went ahead with a planned half-point rate hike. “The reality of overseas banking problems is still unclear,” said Hajime Sakai, chief fund manager at Mito Securities. “While U.S. seems to be calming down, outlook in Europe remains uncertain.”

Key stock gauges in India advanced on Friday but registered their third weekly drop in four amid risk-off sentiment triggered by worries over global growth and future course of interest rates. The S&P BSE Sensex rose 0.6% to 57,989.90 in Mumbai, while the NSE Nifty 50 Index advanced 0.7% to 17,100.05. For the week, the Nifty 50 fell 1.8%, while the BSE Sensex declined 1.9%. Indian stocks have sharply underperformed Asian and emerging markets, both today and for the week, as investor concerns persist over the South Asian country’s relatively high valuations and slowing growth momentum. HDFC Bank contributed the most to Sensex’s gain, increasing 1.4%. Tata Consultancy Services was among the worst performing NIFTY IT stocks, and underperformed most of its listed Indian peers, as its CEO’s sudden resignation surprised investors. Out of 30 shares in the Sensex index, 21 rose and 9 fell.

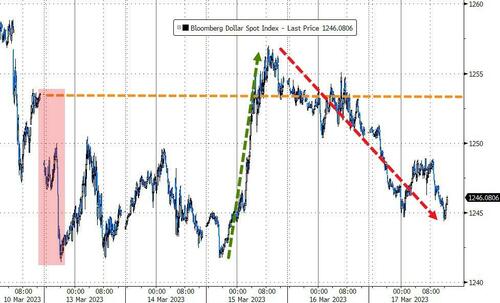

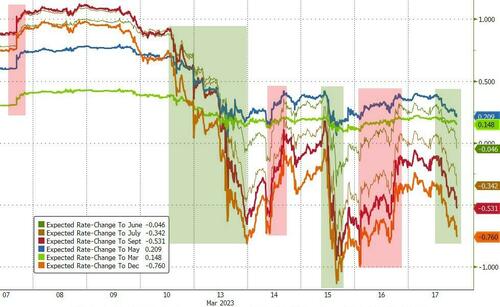

In FX, the Dollar Index is down 0.2% as the greenback falls versus all its G-10 rivals to head for a weekly. The New Zealand dollar and Australian dollar are the best performers. US overnight indexed swaps are now pricing for an 80% probability of a quarter-percentage point Fed rate hike next week, up from a coin toss earlier this week.

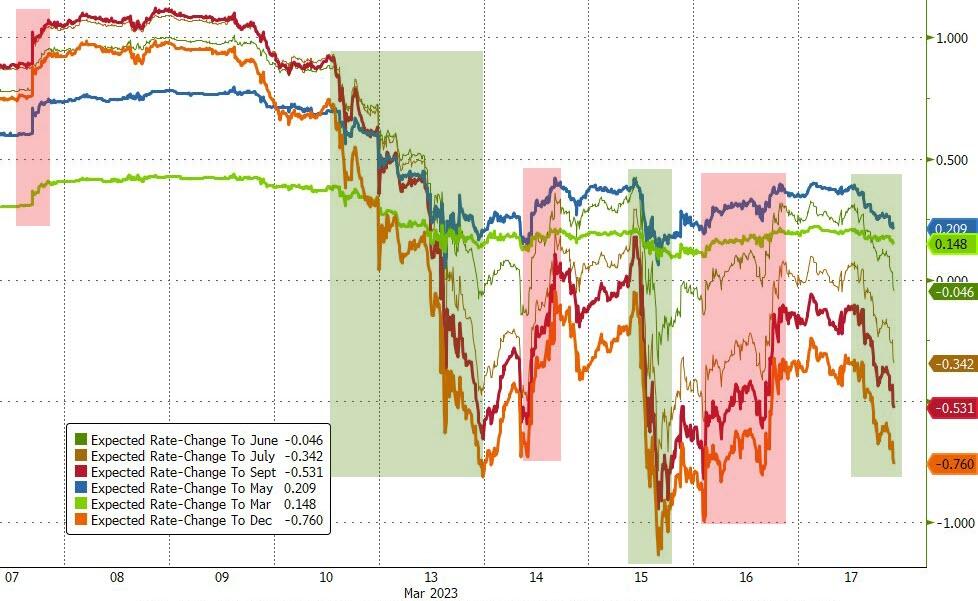

In rates, treasuries have recouped some of Thursday’s losses, led by bunds and gilts as euro-zone money markets trim rate-hike premium for May after Thursday’s post-ECB selloff. Intermediate sectors lead a limited advance for Treasuries as US stock futures hold most of Thursday’s steep gains. Two-year US yields fell 3bps to 4.11% while the 10-year rate slipped seven basis points to 3.49% vs Thursday’s close and paced by bunds and gilts. Fed-dated OIS contracts price around 20bp of rate-hike premium for next week’s policy decision, in line with Thursday’s close, while around 75bp of rate cuts are priced from May peak into year-end.

Oil headed for the biggest weekly decline this year after investor confidence plunged following the worst banking sector turmoil since the financial crisis. WTI futures in New York were down about 10% this week, even though they edged higher by 1.6% to trade near $69.40 to pare some of the decline. The failure of Silicon Valley Bank and troubles at Credit Suisse Group AG, compounded by oil options covering, triggered a three- day rout earlier this week that sent prices to the lowest in 15 months. Gold is headed for its biggest weekly gain since November after attracting haven demand due to banking turmoil in the US and Europe. U.S. Steel is among the most active resources stocks in premarket trading, gaining about 4%.

Looking to the day ahead now, and data releases from the US include the University of Michigan’s consumer sentiment index for March, industrial production for February, and the Conference Board’s leading index for February. Over in Europe, we’ll get the final Euro Area CPI reading for February. Lastly, central bank speakers include the ECB’s Simkus.

Market Snapshot

S&P 500 futures down 0.3% to 3,981

STOXX Europe 600 up 1.0% to 446.26

MXAP up 1.4% to 157.20

MXAPJ up 1.5% to 506.60

Nikkei up 1.2% to 27,333.79

Topix up 1.2% to 1,959.42

Hang Seng Index up 1.6% to 19,518.59

Shanghai Composite up 0.7% to 3,250.55

Sensex up 0.4% to 57,866.02

Australia S&P/ASX 200 up 0.4% to 6,994.80

Kospi up 0.7% to 2,395.69

Brent Futures up 0.7% to $75.22/bbl

Gold spot up 0.5% to $1,929.89

U.S. Dollar Index down 0.33% to 104.07

German 10Y yield little changed at 2.25%

Euro up 0.4% to $1.0653

Brent Futures up 0.7% to $75.22/bbl

Top Overnight News from Bloomberg

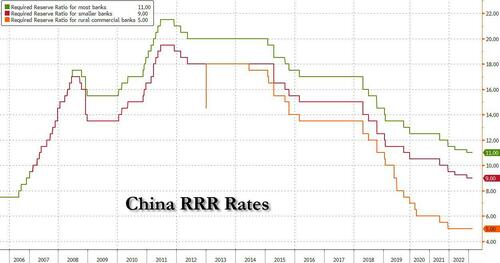

China cut the amount of cash banks must keep in reserve at the central bank in an effort to support lending and strengthen the economy’s recovery from pandemic restrictions and a property market slump: BBG

Central bank interest-rate hikes really started hitting home this week: BBG

Banks borrowed a combined $164.8 billion from two Federal Reserve backstop facilities in the most recent week, a sign of escalated funding strains in the aftermath of Silicon Valley Bank’s failure: BBG

If there’s one lesson from the European Central Bank’s latest monetary policy meeting, it’s that bond market volatility is here to stay: BBG

China’s Xi Jinping will visit Moscow next week for talks with Russian President Vladimir Putin, showcasing the deepening ties between the countries. WSJ

TikTok said that the Biden administration was pushing the company’s Chinese owners to sell the app or face a possible ban. But there are probably few companies, in the tech industry or elsewhere, willing or able to buy it, analysts and experts say. NYT

ECB officials (including Muller, Simkus, and Kazimir) deliver hawkish comments, warning that rates still have further to go on the upside. BBG

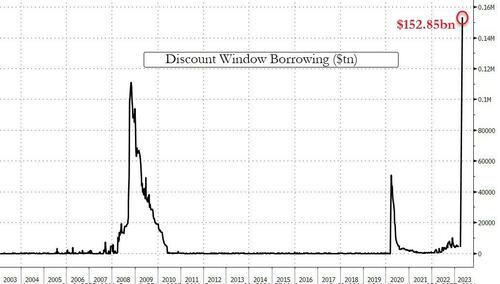

Banks borrowed a combined $164.8 billion from two Fed facilities in the week ended March 15, a sign of escalated funding strains. Discount window borrowing shot up to $152.85 billion, eclipsing the prior all-time high of $111 billion in 2008. Another $11.9 billion was borrowed from the new emergency backstop launched Sunday known as the Bank Term Funding Program. BBG

The US is committed to replenishing the Strategic Petroleum Reserve but won’t rush to do so immediately despite the recent decline in oil prices, a top Biden administration official said. BBG

Poland will send four of its MiG fighter jets to Ukraine in the coming days in what amounts to the first shipment of combat aircraft to the Zelensky gov’t. FT

Fresh turmoil for traders may be sparked by today’s options expiration after a week of bank drama. An estimated $2.7 trillion of derivatives contracts tied to stocks and indexes will mature, typically involving portfolio adjustments, spikes in volume and price swings. Demand for bearish options has been on the rise and market makers will be “short gamma,” requiring them to ride the prevailing trend. BBG

PacWest Corp is in talks about a liquidity boost with Atlas SP Partners and other investment firms. RTRS

Charles Schwab saw $8.8 billion in net outflows from its prime money market funds this week as investors rattled by turmoil at US banks plowed even more money into the brokerage’s other portfolios that favor assets with government backing. BBG

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were positive amid the improved global risk appetite after recent bank lifelines including the SNB liquidity backstop for Credit Suisse and with large US banks teaming up to deposit USD 30bln in First Republic Bank. ASX 200 was marginally higher with the index kept afloat amid outperformance in energy and as the top-weighted financial industry benefitted from the recent banking sector relief, although gains were limited by losses in real estate and the defensive sectors. Nikkei 225 made headway above the psychological 27,000 level with railway stocks among the top gainers, while automakers lagged at the opposite end of the spectrum. Hang Seng and Shanghai Comp. were in an upbeat mood as energy and tech spearhead the advances in Hong Kong and with Baidu eyeing double-digit percentage gains, while the mainland also benefitted from the PBoC’s continued liquidity efforts.

Top Asian News

China Securities Journal noted that the Chinese economy requires more fiscal and monetary support, as well as reiterated that the economic rebound is not yet solid.

Japan’s government and BoJ will hold a meeting on Friday evening after the SVB collapse, with the MoF, FSA and BoJ poised to exchange information on financial markets, according to Nikkei.

Japanese Finance Minister Suzuki said Japanese financial institutions have ample capital base and liquidity, while the financial system is stable as a whole. Suzuki added they are closely coordinating with the BoJ and other central banks regarding responding to financial situations.

Japanese Union Rengo says overall wages to rise 3.8% in Spring wage talks.

European bourses are firmer across the board, Euro Stoxx 50 +0.4%, as recent liquidity action settles sentiment on Quad Witching Friday. Sectors, are all in the green with the defensively-inclined names lagging and upside in Basic Resources and Banking names, SX7P +0.4%; note, Credit Suisse has dropped into negative territory despite opening in the green. Stateside, futures are essentially unchanged having eased from initial best levels around the European open ahead of Michigan data and as attention turns to the upcoming FOMC.

Top European News

UK Chancellor Hunt abandoned plans for sovereign wealth funds to pay corporation tax on property and commercial enterprises, according to FT.

Negotiations for the UK’s re-entry into the EU’s Horizon research scheme may begin within weeks following a resolution, in principle, of the post-Brexit Northern Ireland dispute, according to BBC’s Parker.

German Chancellor Scholz said he does not see the threat of a new financial crisis and the monetary system is no longer as fragile as it was before the financial crisis, according to Handelsblatt. It was also reported that Germany’s Economy Ministry said a technical recession can now no longer be ruled out.

FX

The USD is subdued, though has convincingly reclaimed the 104.00 mark after dropping to a 103.89 low earlier; action which comes to the benefit of G10 peers.

Antipodeans are the stand-out outperformers given their high-beta status amid the improvement in risk appetite, though NZD/USD peaked above 0.6250 and AUD/USD failed to surpass the 0.6720 21-DMA convincingly.

Other G10s are deriving upside, though magnitudes slightly less pronounced, with USD/JPY holding above 133.00, Cable above 1.21 and EUR around 1.0650.

Yuan saw some modest, but ultimately shortlived, pressure on the PBoC’s 25bp cut while the Scandis are benefitting from risk, though the SEK less so given unfavourable unemployment data.

PBoC set USD/CNY mid-point at 6.9052 vs exp. 6.9017 (prev. 6.9149).

Fixed Income

EGBs are markedly more contained thus far, though Bunds have still posted a +100tick range and are currently holding near 136.40 with the 10yr yield around 2.25%.

EGBs have largely disregarded numerous ECB speakers, who overall have added little, and the final EZ HICP reading for February while Gilts are following suit given a lack of specific drivers ahead of next week’s BoE.

Stateside, the direction and magnitude of price action is in-fitting with the above though the US yield curve is slightly mixed with the short-end a touch firmer and the long-end end dipping slightly.

Commodities

Commodities are, generally, deriving support from the firmer risk tone and as the USD remains under pressure; with the crude benchmarks choppy but most recently extending to incremental session highs.

Albeit, this upside places WTI Apr’23 just USD 0.30/bbl above USD 69.00/bbl and as such well within the week’s USD 65.65-77.47/bbl parameters.

Spot gold is similarly bid and at the top-end of USD 1918-1934/oz ranges, with base metals benefitting from the improved tone though the complex is still in the red for the week.

OPEC+ delegates are reportedly still encouraged by Asian demand; Delegates largely blame the recent sell-off on speculative money leaving the derivatives oil market rather than weakness in the physical market, according to Bloomberg.

US energy envoy Hochstein said US President Biden is committed to replenishing the petroleum reserve.

China to lower retail fuel prices from Saturday, according to NDRC.

Increasing oil demand from China has lifted shipping costs markedly, via WSJ; highlighting that the daily chartering cost for VLCC has roughly doubled MM.

Russia’s Kremlin said Russia is extending the Black Sea grain deal for 60 days.

China is reportedly mulling efforts to maintain iron ore supply and prices, according to NDRC; warn iron ore trading firms to avoid hoarding and price gouging.

Geopolitics

North Korea said its missile launch on Thursday was a Hwasong-17 ICBM which sent a warning to enemies and proved the capability to respond overwhelmingly if needed. North Korea added its launch was a response to US-South Korea military drills and its leader Kim called for boosting deterrence of nuclear war, while it noted the launch did not have any negative impact on the safety of neighbouring countries, according to NK News and KCNA.

Chinese President Xi is to visit Moscow on March 20-22, according to state media; Both presidents are set to sign “important documents”, and discuss strategic partnership, according to Tass.

Russia’s Kremlin said President Putin and President Xi will meet on March 20th, hold negotiations on March 21st, and there will be a press statement.

German Federal Education/Research minister is to visit Taipei, Taiwan on Tuesday, via FT citing sources; Foreign Minister Baerbock intends to visit Beijing, China in April/May.

US Event Calendar

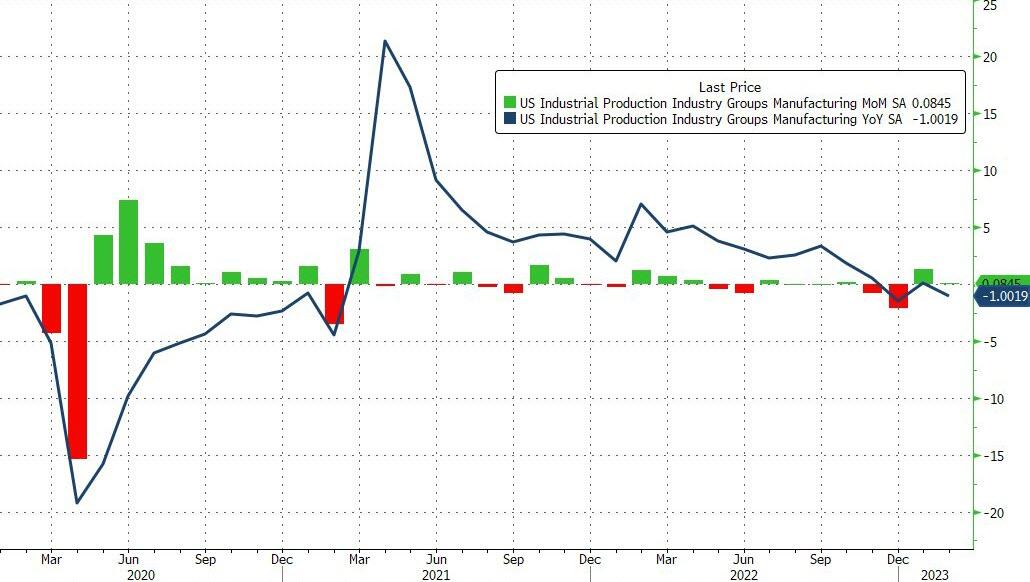

09:15: Feb. Industrial Production MoM, est. 0.2%, prior 0%

Feb. Manufacturing (SIC) Production, est. -0.3%, prior 1.0%

Feb. Capacity Utilization, est. 78.4%, prior 78.3%

10:00: March U. of Mich. Expectations, est. 64.8, prior 64.7; Current Conditions, est. 70.5, Sentiment, est. 67.0,

U. of Mich. 1 Yr Inflation, est. 4.1%, prior 4.1%

U. of Mich. 5-10 Yr Inflation, est. 2.9%, prior 2.9%

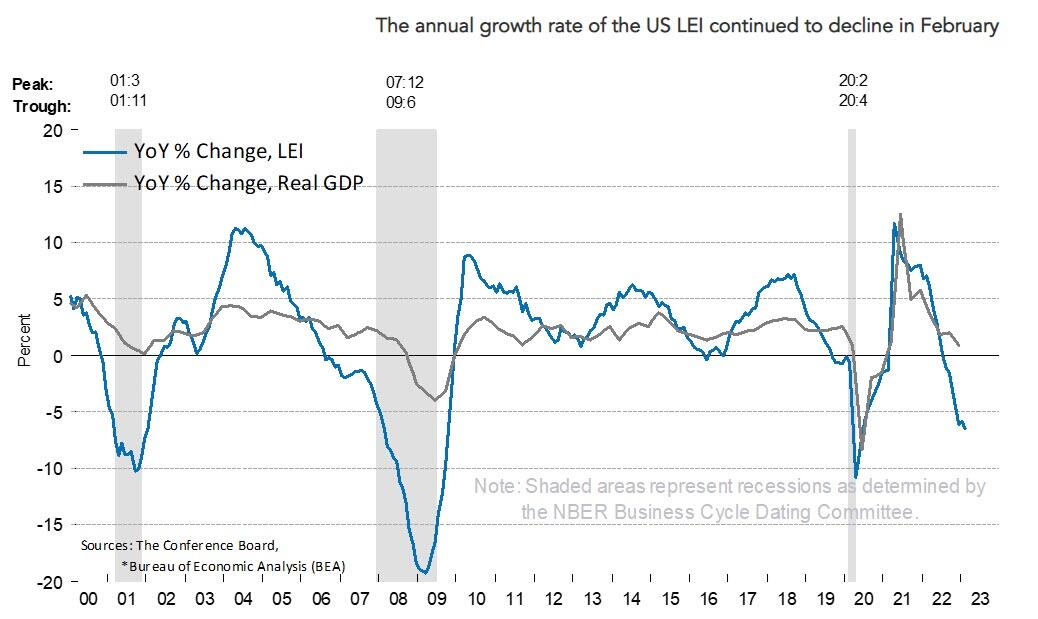

10:00: Feb. Leading Index, est. -0.3%, prior -0.3%

DB’s Jim Reid concludes the overnight wrap

Some optimism has returned to markets over the last 24 hours, with bank stocks stabilising on both sides of the Atlantic and 2yr yields surging back. Even the ECB’s decision to pursue a 50bp hike went without incident, and investors grew in confidence that the Fed would follow up with their own 25bps hike next week, so we’re starting to see a modest change in the mood music. It’s also telling this morning that in Asia, US yields and equity futures are fairly stable. Well, they were at the time of typing.

As we’ll see below, the concerns haven’t gone away though, as while Credit Suisse saw its equity price increase, its bonds/CDS were generally flat to weaker. Let’s start with the US banks as there was a lot of news surrounding First Republic Bank. The equity opened down a further -12% taking it to its lowest levels since going public, before recovering slowly as reports started filtering out about additional capital injections. Following numerous reports early yesterday that the US government was trying to agree to a rescue package with some of the major US banks, a deal was announced just before the US equity market closed. In a joint statement the consortium of banks including JPMorgan, Citigroup, Bank of America and Wells Fargo tried to reassure the public that their actions, “reflects their confidence in First Republic and in banks of all sizes.” Overall 11 banks are contributing $30bn of uninsured deposits to First Republic, with $5bn coming from JPMorgan, Citigroup, Bank of America and Wells Fargo. The banks’ commitment will extend for 120 days initially and could be extended at that point as necessary. In after-hours trading, First Republic’s shares fell c.-17% as the bank announced that it was suspending its dividend and plans to trim its debt burden. That leaves the stock nearer to where it was trading prior to the news of the deposit injection but still higher.

In terms of bank funding, last night the Fed released the weekly data of how its various lending facilities were used in the week ending March 15. The most anticipated release of the data since Covid did not disappoint in scale. In total, there was $164.8bn of borrowing between the Fed’s discount window ($152.85bn) and the Bank Term Funding Program ($11.9bn) that the Fed announced last week. The discount window figure blows away the previous high of $111bn during the 2008 financial crisis. However, as a function of overall deposits level yesterday’s data was about 1% of deposits, while at the height of the GFC the discount window usage in a week was as much as 1.8% of deposits. This data will be parsed more in coming weeks if stress persists but the 11 bank consortium into First Republic will be hoped to be enough to prevent that.

Nevertheless, we shouldn’t get ahead of ourselves, and it’s worth remembering that we’ve already had a temporary period of stability on Tuesday that was then dented by the Credit Suisse worries on Wednesday. Indeed, their bonds stayed fairly stressed yesterday even with the market bounceback. The 5yr credit default swaps stayed around the +1000 level, whilst there were further declines in the value of their debt – notably their ’29 EUR bonds are trading under €70. That was in spite of the announcement we highlighted yesterday that they’d be using a SNB liquidity facility, which initially saw the share price surge +40% at the open, before paring back around half those gains to “only” close up +19.15%.

With regard to Credit Suisse, if you’re looking for the positives in European banking see my CoTD here yesterday that shows the rest of the sector is more tightly packed together in 5yr CDS terms and that CS has been an outlier for months. So if the authorities manage to contain it, the immediate contagion risk is limited. However, the CoTD also highlights how we think the financial risk will eventually spread to corporates. If relatively lowly levered financials can get hit then highly levered corporates won’t be immune further down the line with the appropriate lag. Our YE targets for US and EU HY for YE 2023 have been around 860bp for 12 months now, but with most of the pain expected to occur in H2 2023. Our US Lev Loan target is +1000bp for the same time period. If you’re not on my CoTD (chart of the day), send an email to jim-reid.thematicresearch@db.com to get added.

Banks in aggregate recovered a bit yesterday, though the CS fallout continued to weigh as Europe’s STOXX Banks was up just +1.16% vs the -8.40% the day before. Meanwhile, the news of the further First Republic support saw the KBW Banks index up +2.57% – roughly 1.4% of that came after news hit that First Republic would get $30bn of deposits. We shouldn’t forget that both are still down more than -10% over the week as a whole, but the more positive tone supported a broader equity rally that left the S&P 500 (+1.76%) and Europe’s STOXX 600 (+1.19%) with solid performances on the day. That’s the best day for the S&P 500 in over 2 months and is entering today up +2.56% through the last four days, while the STOXX 600 is down -2.67% on the week so far.

Whilst all that was going on, the ECB followed through on their previous commitment to hike by 50bps at yesterday’s meeting, which takes the deposit rate up to a post-2008 high of 3%. President Lagarde said this was supported by a “large majority”, but in other respects the decision was a dovish one, and their statement dropped the previous guidance that they expected to raise rates further. Instead, the message was that they’d take a “data-dependent” approach at subsequent meetings, and there wasn’t much indication about what they were planning to do next. Their inflation forecasts (which were finalised before the current turmoil) were also revised down on the back of lower energy prices, and now see inflation falling from +5.3% in 2023 to +2.9% in 2024 and +2.1% in 2025. On the other hand, the core inflation forecast for 2023 was revised up to +4.6%, which shows that they still see underlying price pressures staying resilient.

When it came to the current turmoil, the ECB’s statement said that they were “monitoring current market tensions closely”, and it also affirmed that the “euro area banking sector is resilient, with strong capital and liquidity positions.” President Lagarde went on to deflect comparisons to 2008, saying that “the banking sector is in a much, much stronger position”. Looking forward, our European economists maintain their 3.75% baseline terminal rate call based around a 50bp hike in May and then 25bps in June. That view is predicated on the relatively rapid normalisation of the current global financial shock. Please see their report here for more.