Mar 20 2023 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSED: UP $9.60 at $1978.30

SILVER PRICE CLOSED: UP $0.15 to $22.53

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1978.80

Silver ACCESS CLOSE: 22.52

Trading today filled the gaps left with gold accelerating beyond its Friday closed of 1968.00 Now comes the exercise of the crooks defending $2000 gold. Should be exciting to watch:

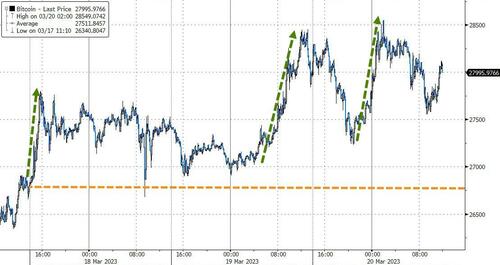

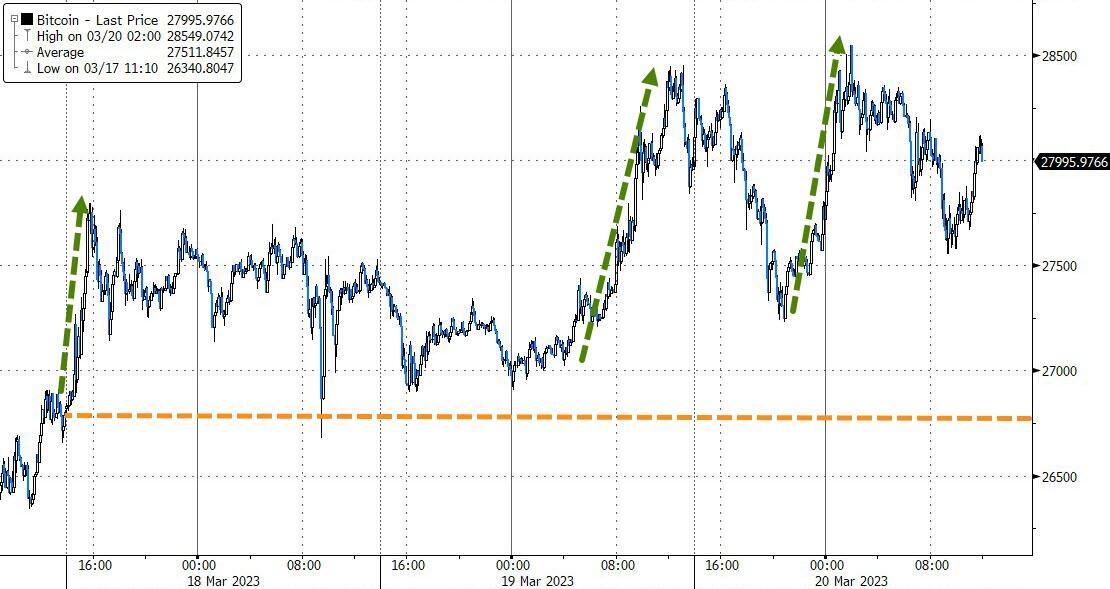

Bitcoin morning price:, $28,319 UP 1514 Dollars

Bitcoin: afternoon price: $27,932 UP 1127 dollars

Platinum price closing $989.50 UP $12.50

Palladium price; closing $1423.40 UP $17.85

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,703.70 DOWN 21.45 CDN dollars per oz (ALL TIME HIGH 2725.60)

BRITISH GOLD: 1611.33 DOWN 20.87 pounds per oz//(ALL TIME HIGH//1629.84)

EURO GOLD: 1844/91 DOWN 16.46 euros per oz //(ALL TIME HIGH//1860.82)

COMEX DATA

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: MARCH 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,969.800000000 USD

INTENT DATE: 03/17/2023 DELIVERY DATE: 03/21/2023

FIRM ORG FIRM NAME ISSUED STOPPED

435 H SCOTIA CAPITAL 138

624 H BOFA SECURITIES 8

657 C MORGAN STANLEY 3

661 C JP MORGAN 279 83

737 C ADVANTAGE 1 9

905 C ADM 39

TOTAL: 280 280

JPMORGAN stopped 83/280 contracts

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR MAR/2023. CONTRACT: 280 NOTICES FOR 28000 OZ or 0.8709 TONNES

total notices so far: 4740 contracts for 47,400 oz (14.7439 tonnes)

SILVER NOTICES: 46 NOTICE(S) FILED FOR 230,000 OZ/

total number of notices filed so far this month : 3087 for 15,435,000 oz

END

GLD

WITH GOLD UP $9.60

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD:////// A MASSIVE DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD//

INVENTORY RESTS AT 921.08TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 15 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF OF 3.401 MILLION OZ FROM THE SLV: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 459.347. MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY AN GIGANTIC SIZED 1305 CONTRACTS TO 120,717 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS GIGANTIC SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.79 GAIN IN SILVER PRICING AT THE COMEX ON FRIDAY. WE ARE NOW RECORDING FOR PROSPERITY OUR NEW LOW COMEX OI SILVER SET AT 119,412 CONTRACTS , MARCH 17/2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.79). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A MONSTROUS GAIN ON OUR TWO EXCHANGES 2040 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 1 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS( 735 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.58 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE JUMP TO LONDON OF 180,000 OZ//NEW STANDING: 15.570 MILLION OZ + THE 1.0 MILLION OZ OF EXCHANGE FOR RISK//THUS TOTAL NEW STANDING 16.570 MILLION OZ/ //// V) HUGE SIZED COMEX OI GAIN/ STRONG SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –116 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTRACTS for 14 days, total 11,229 contracts: OR 56.145 MILLION OZ . (802 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 56.145 MILLION OZ

.

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 56.145 MILLION OZ//INITIAL//ON PAR WITH LAST MONTH

RESULT: WE HAD A GIGANTIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1305 CONTRACTS WITH OUR $0.79 GAIN IN SILVER PRICING AT THE COMEX//FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 735 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAR OF 15.58 MILLION OZ//FIRST DAY NOTICE// FOLLOWED BY TODAY’S 180,000 OZ QUEUE JUMP TO LONDON (WHICH INCREASES THE AMOUNT OF SILVER STANDING) + 1.0 MILLION OF EXCHANGE FOR RISK ISSUED EARLY IN MARCH (INCREASES THE AMOUNT OF SILVER STANDING) //NEW STANDING 16.570 MILLION OZ .. WE HAVE A GIGANTIC SIZED GAIN OF 2156 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 46 NOTICE(S) FILED TODAY FOR 230,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GIGANTIC SIZED 18,476 CONTRACTS TO 475,728 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -464 CONTRACTS.

.

WE HAD A GIGANTIC SIZED INCREASE IN COMEX OI ( 18,476 CONTRACTS) WITH OUR $50.50 GAIN IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR MAR. AT 4.9953 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 6600 OZ (0.2052 TONNES) //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London).

YET ALL OF..THIS HAPPENED WITH OUR GIGANTIC $50.50 GAIN IN PRICE WITH RESPECT TO FRIDAY’S TRADING

WE HAD AN ATMOSPHERIC SIZED GAIN OF 26,057 OI CONTRACTS (81.048 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7581 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 475,728

IN ESSENCE WE HAVE A MONSTER SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 26,057 CONTRACTS WITH 18,476 CONTRACTS INCREASED AT THE COMEX AND 7581 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 26,057 CONTRACTS OR 81.048 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (7581 CONTRACTS) ACCOMPANYING THE HUGE SIZED GAIN IN COMEX OI (18,476) TOTAL GAIN IN THE TWO EXCHANGES 26,057 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR MAR. AT 4.9953 TONNES FOLLOWED BY TODAY’S 6600 OZ QUEUE JUMP//NEW STANDING 15.063 TONNES // ///3) ZERO LONG LIQUIDATION //4) GIGANTIC SIZED COMEX OPEN INTEREST GAIN// 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

TOTAL EFP CONTRACTS ISSUED: 60,324 CONTRACTS OR 6, 032,400 OZ OR 187.63 TONNES IN 14 TRADING DAY(S) AND THUS AVERAGING: 4309 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 14 TRADING DAY(S) IN TONNES 187.63 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 187.63/3550 x 100% TONNES 5.26% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 187.63 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A GIGANTIC SIZED 1305 CONTRACTS OI TO 120,717 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A RECORD LOW OF 119,412 CONTRACTS THIS PAST WEEK, MARCH 17/2022

EFP ISSUANCE 735 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 735 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 735 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1305

CONTRACTS AND ADD TO THE 735 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE GAIN OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2046 CONTRACTS.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES //10.200 MILLION OZ

OCCURRED DESPITE OUR $0.79 GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)MONDAY MORNING//SUNDAY NIGHT

SHANGHAI CLOSED DOWN 15.64 PTS OR 0.48% //Hang Seng CLOSED DOWN 517.88 PTS OR 2.65% /The Nikkei closed DOWN 388.12 PTS OR 1.42% //Australia’s all ordinaries CLOSED DOWN 1.43% /Chinese yuan (ONSHORE) closed UP 6.8795//OFFSHORE CHINESE YUAN UP TO 6.8802// /Oil DOWN TO 65.68 dollars per barrel for WTI and BRENT AT 72.13 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GIGANTIC SIZED 18,476 CONTRACTS UP TO 475,728 WITH OUR HUGE GAIN IN PRICE OF $50.50 ON FRIDAY

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAR… THE CME REPORTS THAT THE BANKERS ISSUED A VERY STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 7581 EFP CONTRACTS WERE ISSUED: : APRIL 7581 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 7581 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: AN ATMOSPHERIC SIZED TOTAL OF 26,057 CONTRACTS IN THAT 7581 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A HUGE SIZED GAIN OF 18,476 COMEX CONTRACTS..AND THIS MONSTER SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $50.50. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAR (15.063) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 15.063 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $50.50) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR HUGE SIZED GAIN OF 26,057 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 81.048 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAR. (4.9953 TONNES) FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 6,600 OZ (0.2052 TONNES)… ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $50.50

WE HAD -464 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 26,057 CONTRACTS OR 2,605,700 OZ OR 81.048 TONNES

TONNES

Estimated gold comex today 385,521// //very strong

final gold volumes/yesterday 425,632///extremely strong

//MARCH 20/ MARCH 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 2304.17 oz Brinks . |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 280 notice(s) 28,000 OZ 0.8709 TONNES |

| No of oz to be served (notices) | 73 contracts 7300 oz .2270 TONNES |

| Total monthly oz gold served (contracts) so far this month | 4740 notices 474,000 14.7439 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 1

i) out of BRINKS: 2,304.17 oz

total withdrawals: 2,304.17 oz

in tonnes: 0.07166 tonnes

Adjustments; 1

out of Brinks: 19,347.200 oz adjusted out of dealer into customer account

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of MARCH we have an oi of 353 contracts having LOST 143 contracts. We had 209 notices filed on FRIDAY so we

gained A STRONG 66 contracts or an additional 6600 oz will stand for metal at the comex

April LOST A SMALL 964 contracts DOWN to 181,509 contracts. It is here that our banker friends have to worry as many will try and take delivery in this upcoming delivery month.

May GAINED 16 contracts to stand at 286

We had 280 notice(s) filed today for 28,000 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 279 notices were issued from their client or customer account. The total of all issuance by all participants equate to 280 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 83 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAR. /2023. contract month,

we take the total number of notices filed so far for the month (4,740 x 100 oz ), to which we add the difference between the open interest for the front month of (MAR. 353 CONTRACTS) minus the number of notices served upon today 280 x 100 oz per contract equals 484,300 OZ OR 15.063 TONNES the number of TONNES standing in this active month of MARCH.

thus the INITIAL standings for gold for the MAR contract month:

No of notices filed so far (4,740 x 100 oz+ 353 OI for the front month minus the number of notices served upon today (280)x 100 oz} which equals 484,300 oz standing OR 15.063 TONNES in this active delivery month of MARCH..

TOTAL COMEX GOLD STANDING: 15.063 TONNES WHICH IS HUGE FOR AN INACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,765,662.466 OZ 54.919 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,364,092.907 OZ

TOTAL REGISTERED GOLD: 10,919,280.949 (339.63 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,444,841.958 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,154,588 OZ (REG GOLD- PLEDGED GOLD) 284.71 tonnes//

END

SILVER/COMEX

MAR 20/2023// THE MARCH 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 438,464.610 oz Brinks CNT Delaware Loomis . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 263,613.750 oz CNT |

| No of oz served today (contracts) | 46 CONTRACT(S) (230,000 OZ) |

| No of oz to be served (notices) | 27 contracts (135,000 oz) |

| Total monthly oz silver served (contracts) | 3087 contracts (15,435,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

Into CNT: 263,613.750 oz

Total deposits: 263,613.750 oz

JPMorgan has a total silver weight: 146.872 million oz/283.529 million =51.81% of comex .//dropping fast

Comex withdrawals: 4

i) Out of CNT 30,490.500 oz

ii) Out of Brinks 1,957.700 oz

iii) Out of Loomis: 402,266.910 oz

iv) Out of Delaware: 3749.500 oz

Total withdrawals; 438,464.610 oz

adjustments: 4 all dealer to customer

i) Brinks 14,795.200 oz

ii) CNT 25,520.430 oz

iii) HSBC 25,119.510 o

iv) JPMorgan 25,388.300oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 37.833MILLION OZ (declining rapidly).TOTAL REG + ELIG. 283.529 million oz

CALCULATION OF SILVER OZ STANDING FOR MAR

silver open interest data:

FRONT MONTH OF MAR/2023 OI: 73 CONTRACTS HAVING GAINED 5 CONTRACT(S.) WE HAD 31 NOTICES FILED

YESTERDAY, SO WE GAINED 36 CONTRACTS OR AN ADDITIONAL 180,000 OZ WILL STAND FOR METAL ON THIS SIDE OF THE POND

April GAINED 11 CONTRACTS TO STAND at 388.

May GAINED 994 CONTRACTS DOWN TO 97,982.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 46 for 230,000 oz

Comex volumes// est. volume today 62,797// good//

Comex volume: confirmed yesterday: 790,985 contracts ( very good)

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 3087 x 5,000 oz = 15,435,000 oz

to which we add the difference between the open interest for the front month of MAR(73) and the number of notices served upon today 46 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAR./2023 contract month: 3087 (notices served so far) x 5000 oz + OI for the front month of MAR (73) – number of notices served upon today (46) x 500 oz of silver standing for the MAR. contract month equates 15.570 million oz +the 1.0 million oz of exchange for risk//new total standing 16.570 million oz

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

MARCH 15/THE IDES OF MARCH: WITH GOLD UP $18.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 913.27 TONNES

MARCH 14/WITH GOLD DOWN $4.75 TODAY: HUGE CHANGES: A MONSTER DEPOSIT OF 11.85 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 913.27 TONNES

MARCH 13/WITH GOLD UP $48.85 TODAY: VERY STRANGE HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY REST AT 901.42 TONNES

MARCH 10//WITH GOLD UP $31.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 903.15 TONNES

MARCH 9/WITH GOLD UP $16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 906.62 TONNES

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

FEB 28/WITH GOLD UP $12.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 917.61 TONNES

FEB 27/WITH GOLD UP $6.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.32 TONNES

FEB 24/WITH GOLD DOWN $9.10 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 917.32 TONNES

FEB 23/WITH GOLD DOWN $13.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 919.92 TONNES

FEB 22/WITH GOLD DOWN 22 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 919.92 TONNES

FEB 21/WITH GOLD DOWN $7.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 919.92 TONNES

FEB 17/WITH GOLD DOWN $1.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 921.08 TONNES

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

GLD INVENTORY: 921.08 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

MARCH 17/WITH SILVER UP 79 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE WITHDRAWAL OF 10.478 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 462.748 MILLION OZ//

MARCH 16/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 5.009 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 473.226 MILLION OZ//

MARCH 15/WITH SILVER DOWN 7 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 643,000 OZ INTO THE SLV//INVENTORY RESTS AT 478.235 MILLION OZ/

MARCH 14/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.287 MILLION OZ FROM THE SLV////INVENTORY REST AT 477.592 MILLION OZ//

MARCH 13/WITH SILVER UP $1.35 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ//

MARCH 10.WITH SILVER UP 36 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ…

MARCH 9/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.979 MILLION OZ

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWALOF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

FEB 28/WITH SILVER UP 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.241 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.188

FEB 27/WITH SILVER DOWN 15 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.471 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 482.429 MILLION OZ

FEB 24/WITH SILVER DOWN 46 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.172 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.900 MILLION OZ//

FEB 23/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.379 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.072 MILLION OZ//

FEB 22/WITH SILVER DOWN 22 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ FROM THE SLV////INVENTORY RESTS AT 485.693 MILLION OZ

FEB 21/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.5363 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 486.382 MILLION OZ//

FEB 17/WITH SILVER UP 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 827,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.819 MILLION OZ/

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 459.347MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

The Comex Is In Far Worse Shape Than SVB If The Run On Physical Accelerates

SUNDAY, MAR 19, 2023 – 02:30 PM

Given the potential impacts of the ongoing banking crisis, I will start this article with the conclusion.

The current banking crisis could not have come at a worse time for the Comex system. Inventories have seen massive depletion over the last 2+ years as investors have slowly been pulling physical out of the vaults. I have previously called this a run on the vault but labeled it as a stealthy one. As though certain investors did not want to raise the alarm, but slowly take possession while inventory was still available.

Now that confidence in the banking system has been put to the test, people will look to alternative means to store their wealth and get their money out of the financial system. The easiest and safest way to do this would be to own physical precious metals, as people have done for thousands of years.

It is likely that demand for physical metal could increase significantly in the months ahead. The futures market is already showing a massive move in the price of gold, which is knocking on the door of $2,000. It’s only a matter of time before this moves into the physical market. When it does, the Comex vault run will pick up steam.

Investors looked at SVB and saw that it was undercapitalized and people could only get 80-90 cents on the dollar. If investors were to do the same due diligence on the Comex they would find an even worse fractional reserve system in the metals market. The recent discovery by the LME that some of their inventory was stones rather than nickel should only serve as another wake-up call that the supply of physical metal is extremely tight. If everyone rushes for physical at the same time, there won’t be nearly enough to satisfy demand at current prices (silver has 15 paper ounces per 1 physical ounce!).

We could be only months away from seeing a break in the Comex system. SchiffGold will be working all weekend to take orders. Best to get physical locked in at current prices while you still can.

Current Trends

This analysis focuses on gold and silver within the Comex/CME futures exchange. See the article What is the Comex? for more detail. The charts and tables below specifically analyze the physical stock/inventory data at the Comex to show the physical movement of metal into and out of Comex vaults.

Registered = Warrant assigned and can be used for Comex delivery, Eligible = No warrant attached – owner has not made it available for delivery.

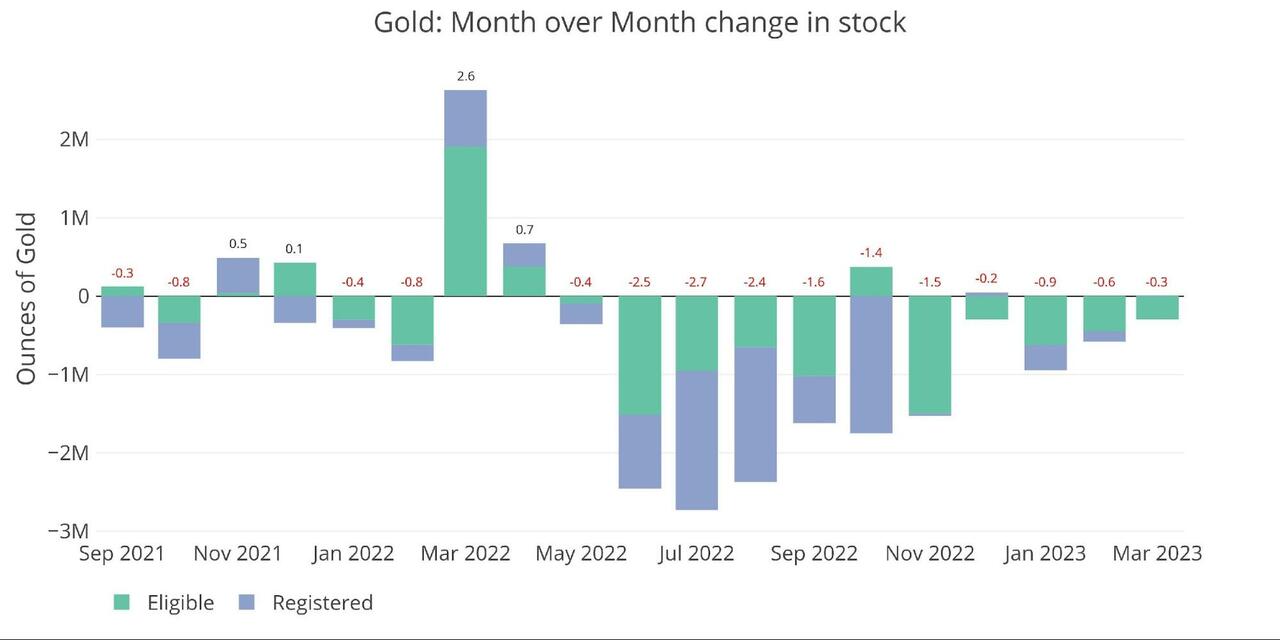

Gold

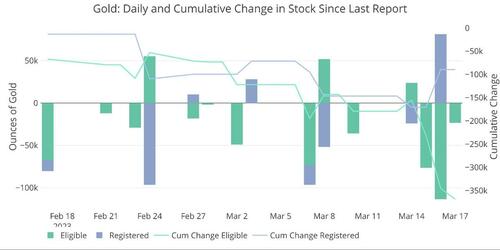

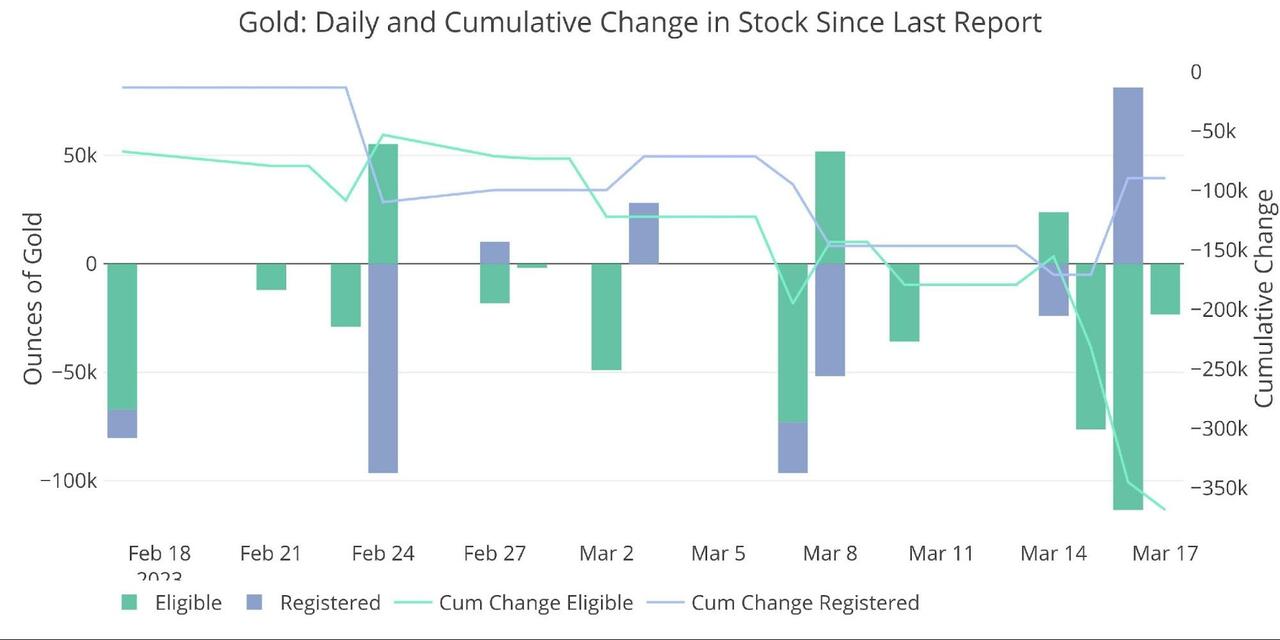

Gold is now in its 11th straight month of net outflows, seeing 285k ounces leave the vault so far in March. The exodus of metal has slowed since last year when some months saw almost 3M ounces leave Comex vaults.

Figure: 1 Recent Monthly Stock Change

As mentioned above, this could change quickly and may already be changing! As the chart below shows, this latest week was the busiest week of outflows in the last month. Given the price of gold finished the week at $1993, the ongoing banking crisis, and general fear in the market… it seems likely that demand for physical could be ready to soar. That could drive larger outflows from Comex vaults in the near future.

Figure: 2 Recent Monthly Stock Change

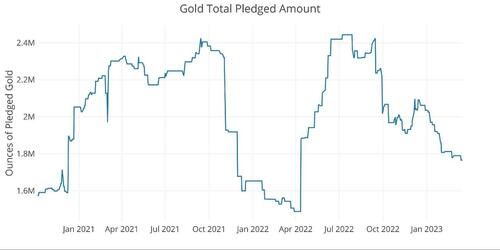

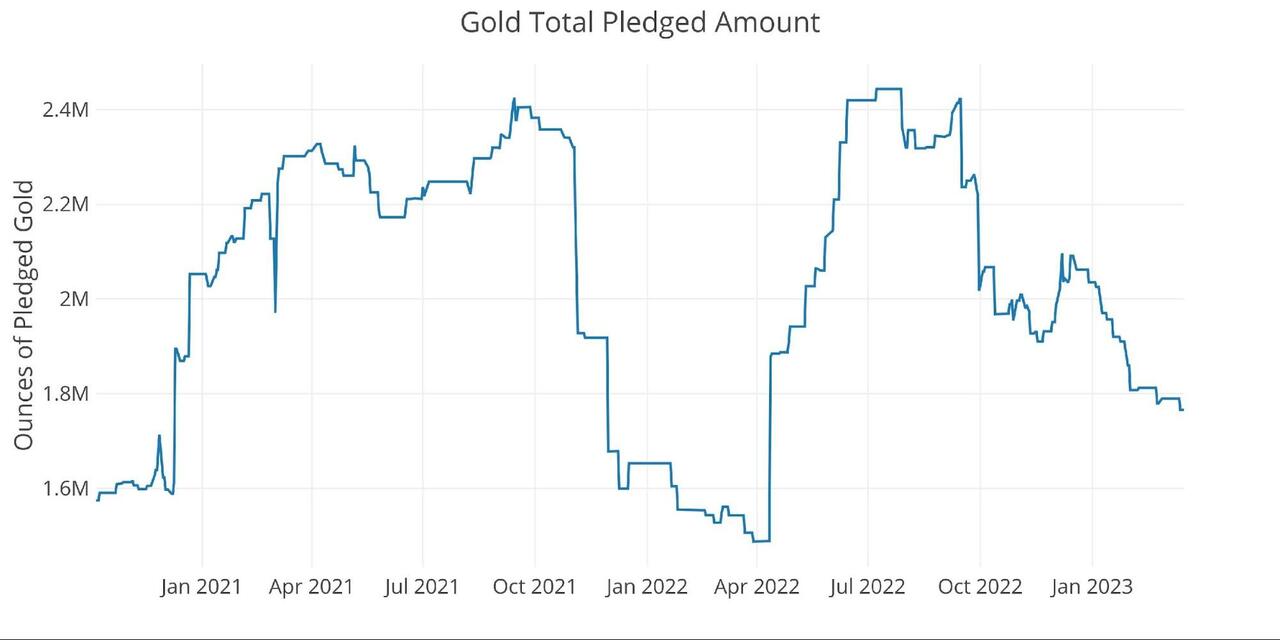

Pledged gold continues to decline, but similar to the inventory at large, the drop has been slowing.

Figure: 3 Gold Pledged Holdings

Silver

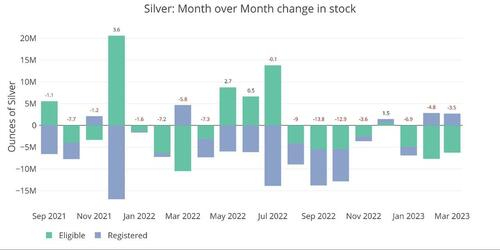

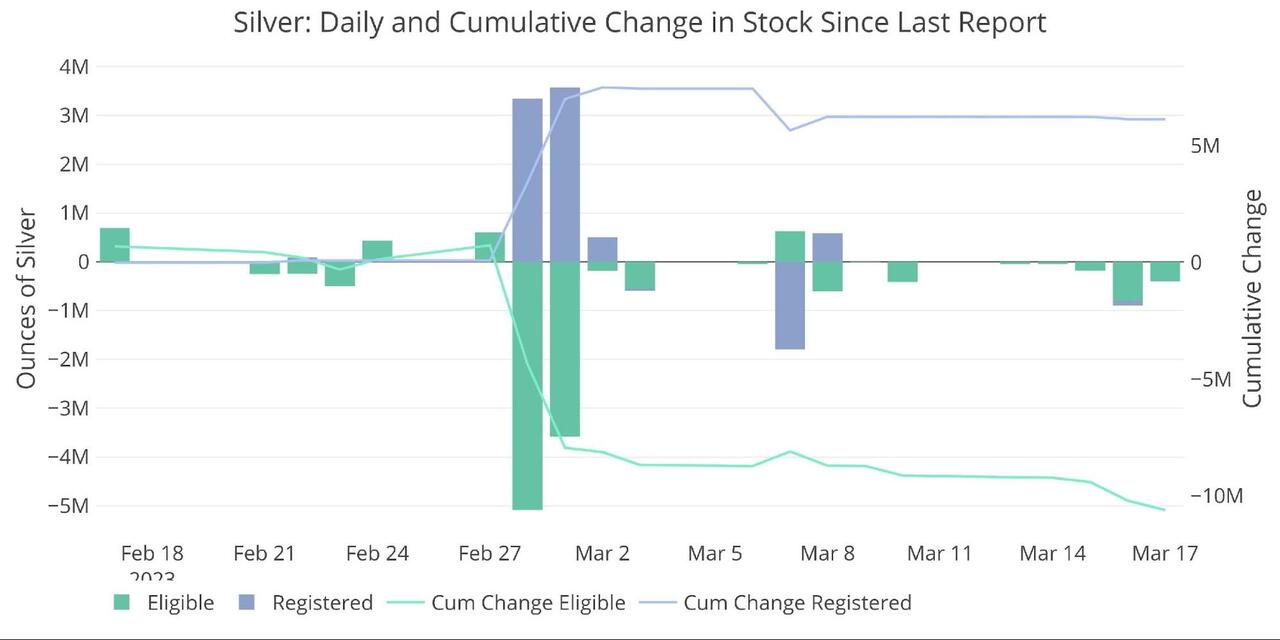

Outflows in silver continue at a strong pace, seeing 3.5M ounces in outflows MTD. Registered is actually seeing inflows for the second month in a row, most likely because inventory of Registered had reached dangerously low levels. As mentioned previously, the real floor is not actually zero but somewhere higher. This is for optics to keep confidence in the fractional reserve silver trade.

Figure: 4 Recent Monthly Stock Change

Unlike gold, the outflows slowed this week. The big moves into Registered occurred just as the March silver contract started its delivery. If Registered silver was not getting close to the bottom, why did the Comex have to move 7M ounces of silver into the Registered category to handle the March delivery volume? This metal was moved specifically to handle that demand which indicates available silver stocks are getting dangerously low.

Interestingly, the metal has not flowed back into Eligible as it typically does after delivery. The data shows that it was none other than JP Morgan taking the majority of the delivery at 5.2M ounces. Perhaps JP decided to obtain silver specifically for the purpose of keeping it in Registered to inflate the numbers. This move increased JP Morgan’s total allocation of Registered from 32% to 41.6%. This means almost half of all Registered silver now sits in JP Morgan vaults… most likely for optics.

Figure: 5 Recent Monthly Stock Change

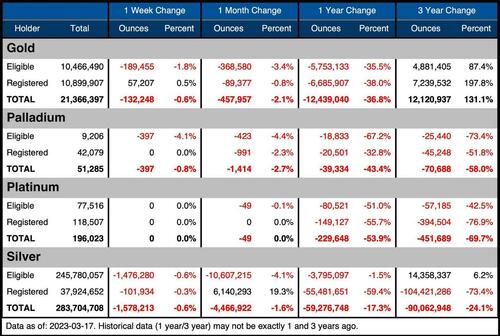

The table below summarizes the movement activity over several time periods to better demonstrate the magnitude of the current move.

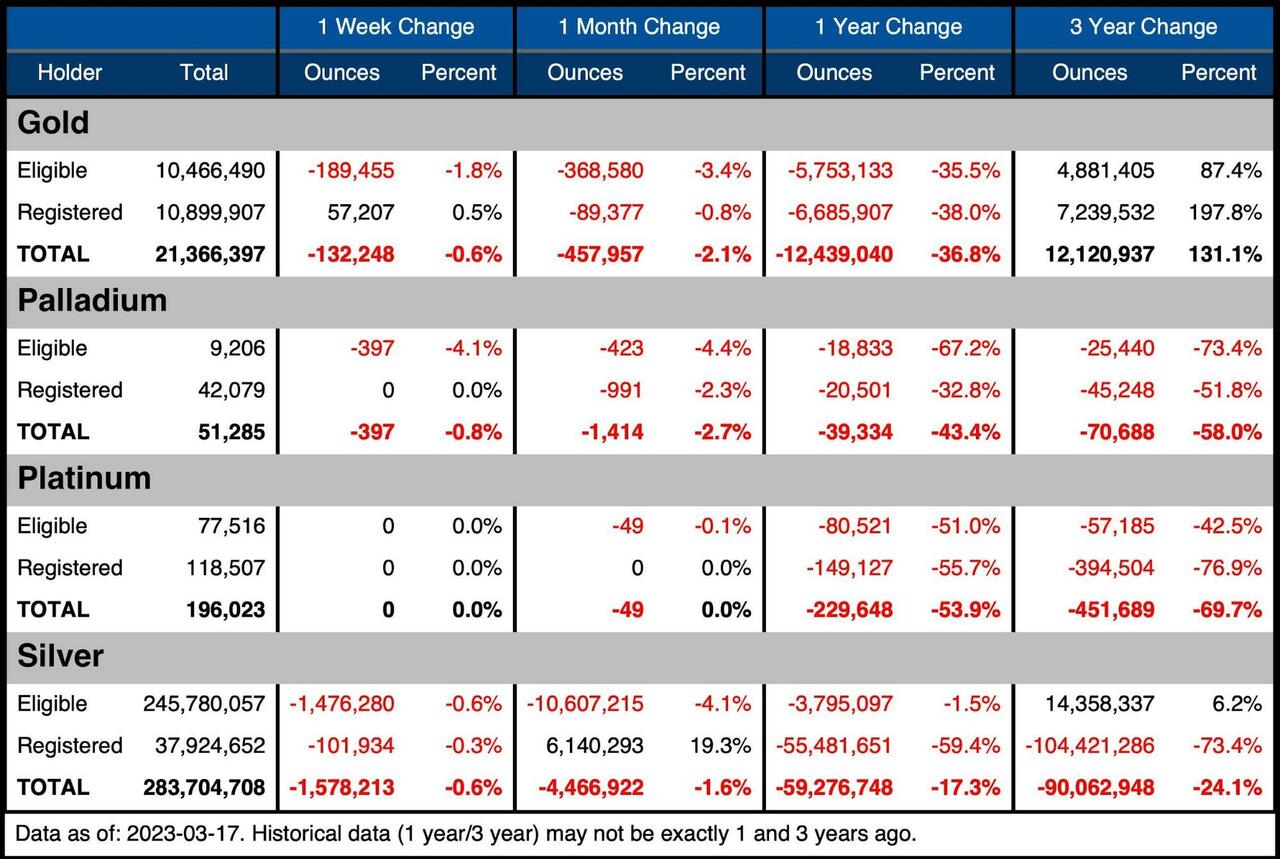

Gold

- Over the last month, gold saw inventories fall by 2.1%

- Registered remains a bit higher than Eligible

- Since last year, total gold holdings have fallen by 36.8% or 12.4M ounces

Silver

- Registered has increased 19.3% in the last month

- Total Registered remains below 40M ounces and has still seen a drop of 55M ounces in the last year

Palladium/Platinum

Palladium and platinum are much smaller markets but it’s possible that is where the market breaks first.

- Palladium saw a drop of 2.7% during its delivery month

- Platinum was very quiet during the month

Platinum is heading towards its next delivery month in April. In January, Platinum looked like it could break the Comex. At the time, we highlighted they had only bought a few months. Well, we are now close to where inventory will be put to the test once again.

Figure: 6 Stock Change Summary

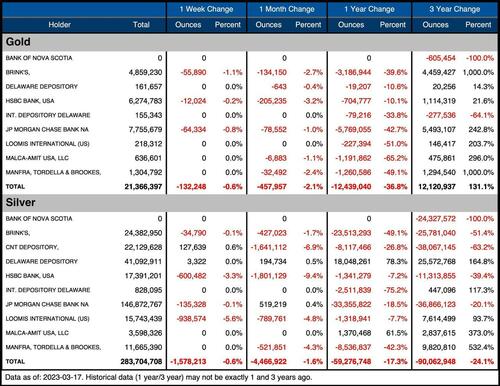

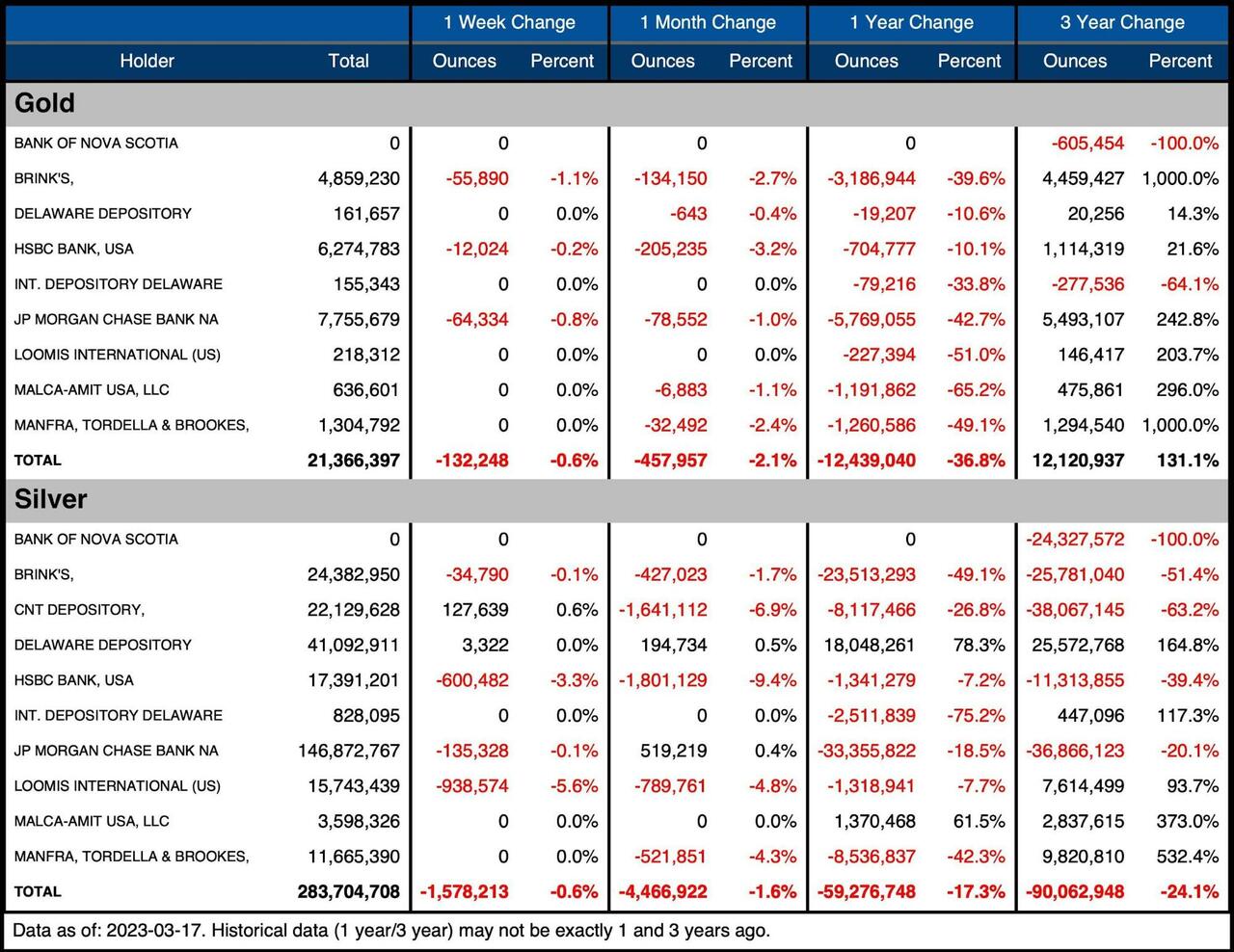

The next table shows the activity by bank/Holder. It details the numbers above to see the movement specific to vaults.

Gold

- 6 vaults lost gold over the month while none added

- Outflows were evenly distributed across all vaults

Silver

- JP Morgan only shows a net gain of 520k ounces, but as noted above, Registered inventories increased more than 5M ounces

- This indicates JP Morgan was moving the metal from within its own vaults

- CNT, HSBC, and Manfra all saw fairly large declines in their inventory

Figure: 7 Stock Change Detail

Historical Perspective

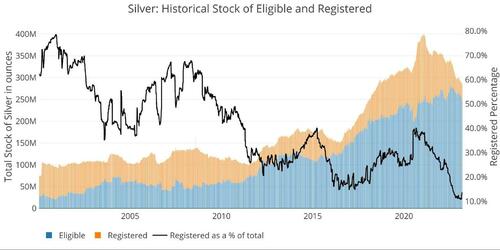

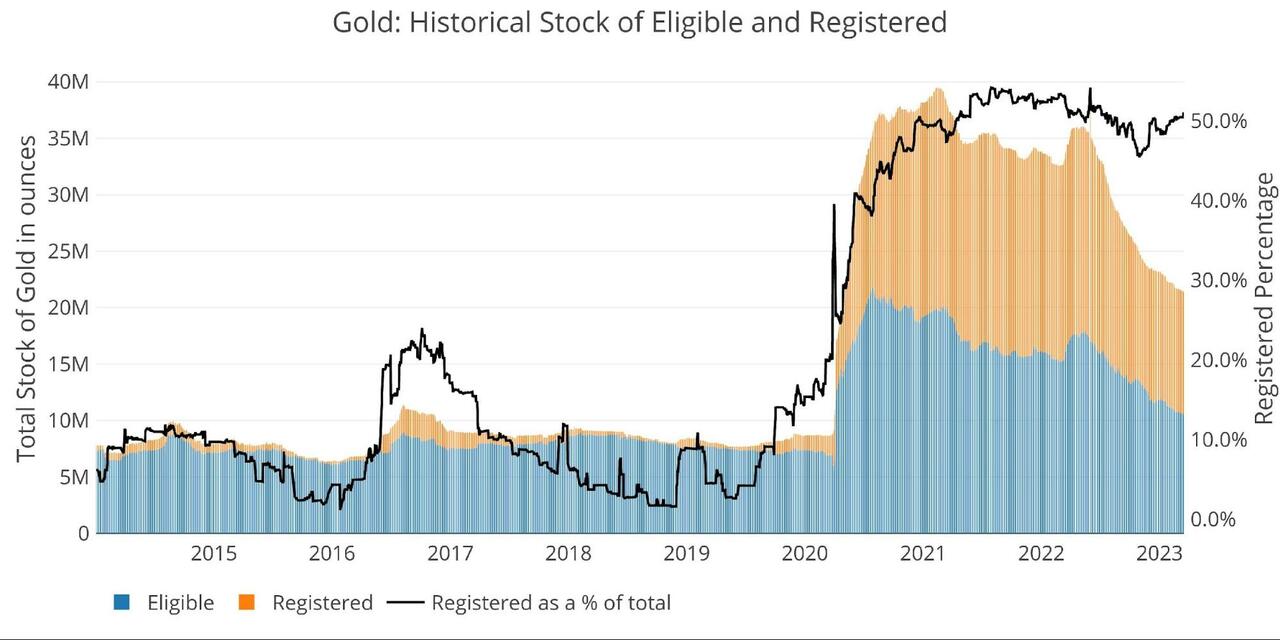

Zooming out and looking at the inventory for gold and silver shows just how massive the current moves have been. The black line shows Registered as a percent of total.

Inventories in gold have been falling evenly in both categories, which is why the black line has stayed relatively flat even while supplies have been crashing. It’s amazing how closely the ratio has stayed to the 50% mark. In October, the ratio reached 45%, but quickly rebounded to 50%.

In September 2019, all of the Registered stood for delivery, so it is likely this ratio is now being actively maintained to make sure confidence persists in the system. Given current market dynamics, this confidence could be put to the test.

Figure: 8 Historical Eligible and Registered

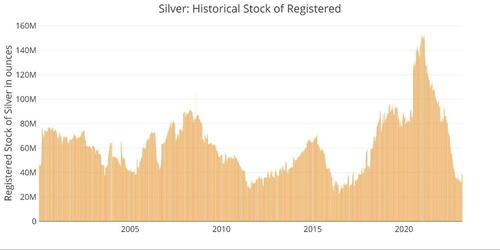

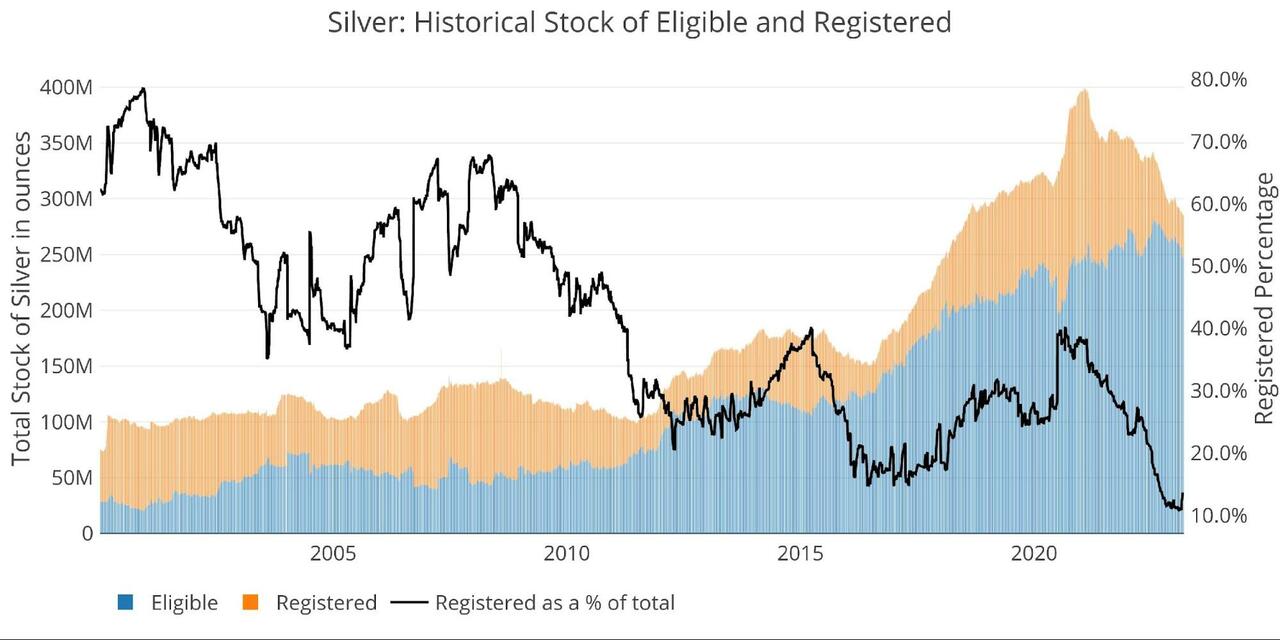

Silver has seen far more concentrated outflows from Registered, getting as low as 10.9% of total inventory in February. With the move by JP Morgan, the ratio has since recovered to 13.3%, but this is still at historically low levels compared to history.

Figure: 9 Historical Eligible and Registered

The recent “spike” can be seen on the far right side of the chart above. From this perspective, the moves by JP Morgan seem much smaller. A similar spike-up happened in March 2022 which quickly reversed as metal started flowing back out of Registered immediately after. Will 2023 see a similar pattern?

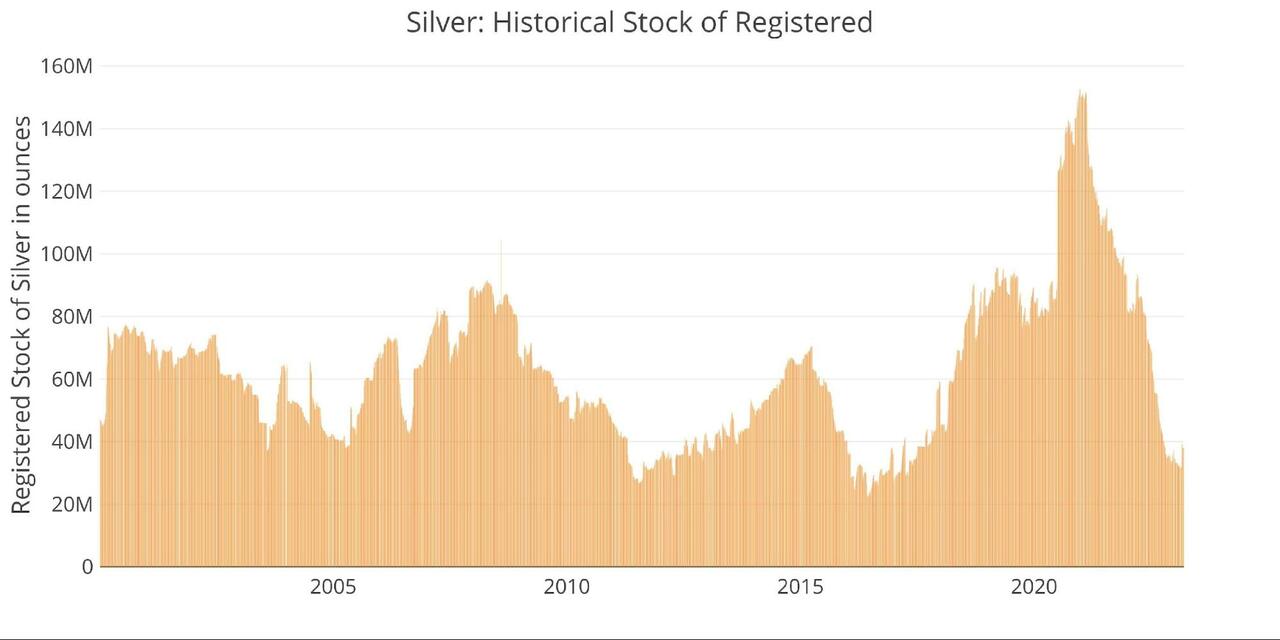

Figure: 10 Historical Registered

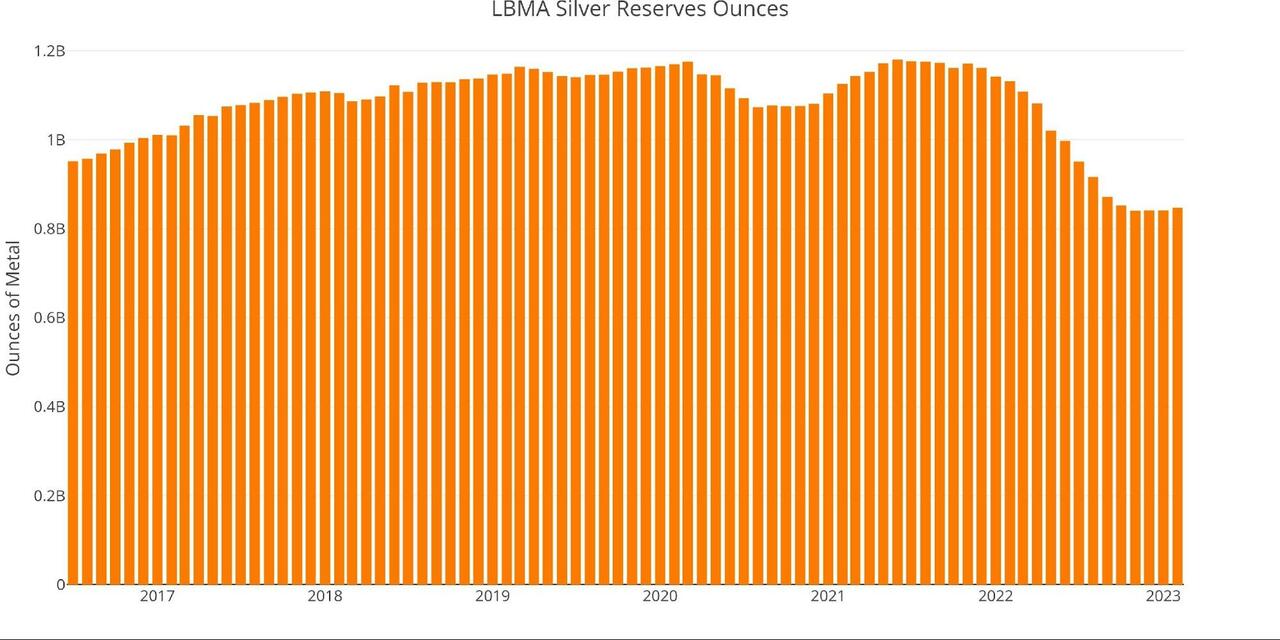

The LBMA had been seeing similar outflows of silver from their vault, but that appears to have stopped for now.

Figure: 11 LBMA Holdings of Silver

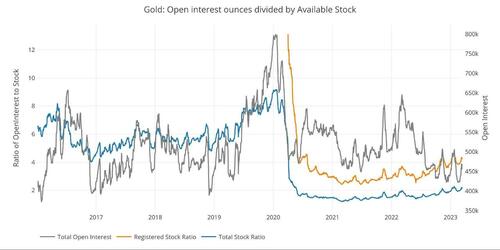

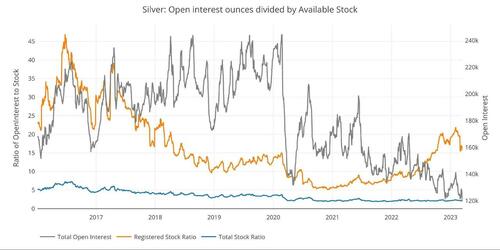

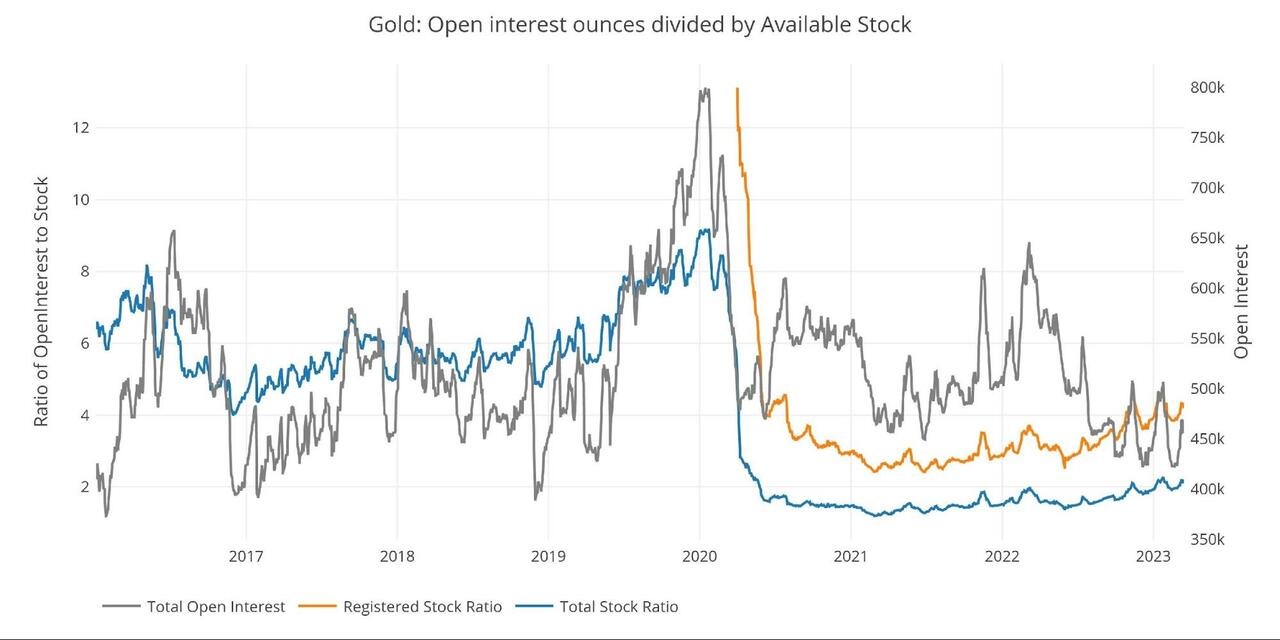

Available supply for potential demand

Coverage on the Comex continues to deteriorate. On Jan 26, before the recent sell-off in gold, the amount of paper gold for each Registered physical ounce was 4.6. That is the highest level since July 2020, right before all the new supply was added. The ratio now sits at 4.2, but the drop has mainly been driven by a fall in Open Interest rather than a surge in inventory.

Figure: 12 Open Interest/Stock Ratio

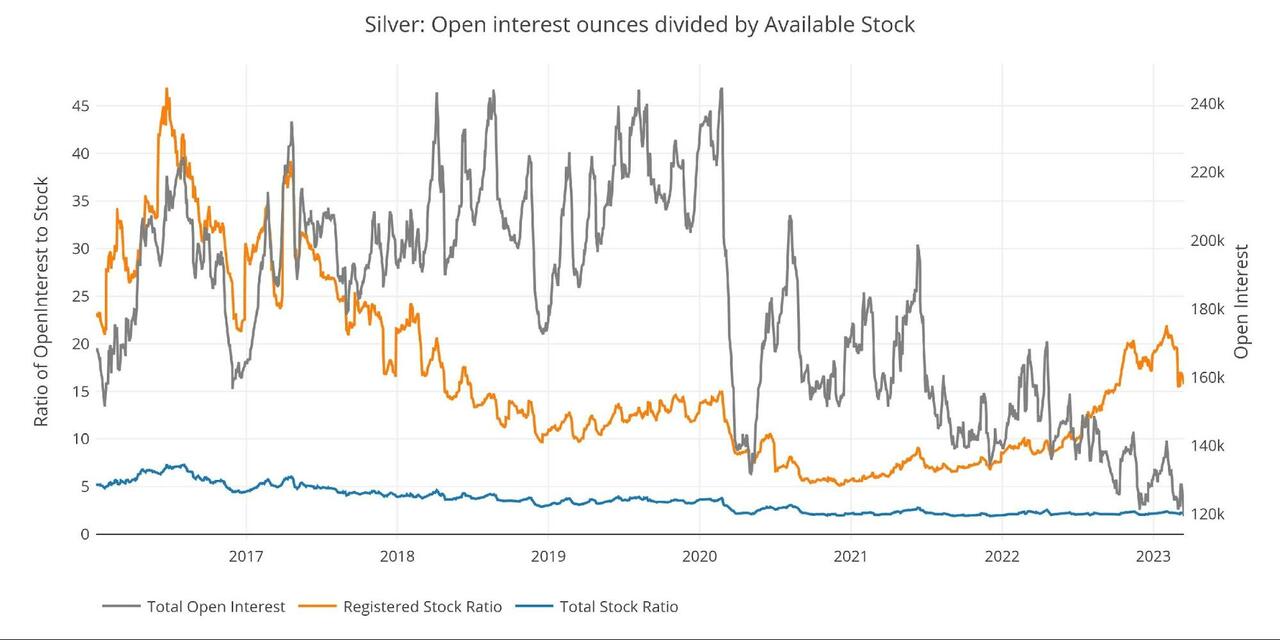

Coverage in silver is far worse than gold. The paper to Registered physical ratio reached 22 ounces on Feb 2nd. It had drifted lower to 19.5 and then after JP Morgan stepped in, the ratio dropped to 15.4.

This means that after the move by JP Morgan, there are still 15 paper contracts for every physical ounce of metal available.

Figure: 13 Open Interest/Stock Ratio

Wrapping Up

See above!

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

A MUST READ…….

EGON VON GREYERZ

THIS IS IT! – THE FINANCIAL SYSTEM IS TERMINALLY BROKEN

Egon von Greyerz

March 19, 2023

The financial system is terminally broken, toast, kaput!

Anyone who doesn’t see what is happening will soon lose a major part of their assets either through bank failure, currency debasement or the collapse of all bubble assets like stocks, property and bonds by 75-100%. Many bonds will become worthless.

Wealth preservation in physical gold is now absolutely critical. Obviously it must be stored outside a broken financial system. More later in this article.

The solidity of the banking system is based on confidence. With the fractional banking system, highly leveraged banks only have a fraction of the money available if all depositors ask for their money back. So when confidence evaporates, so do the balance sheets of the banks and depositors realise that the whole system is just a black hole.

And this is exactly what is about to happen.

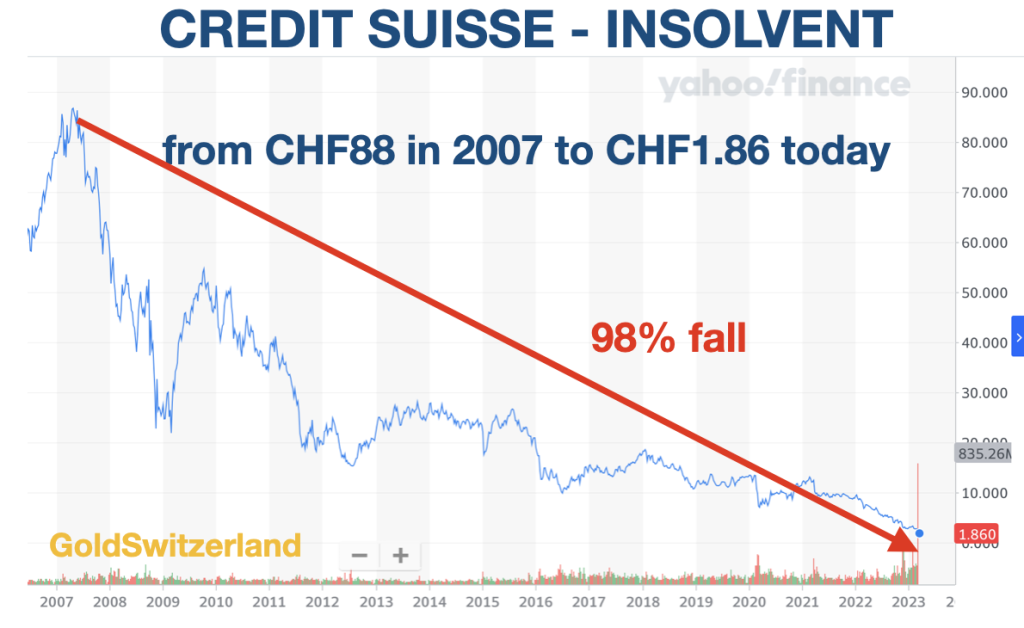

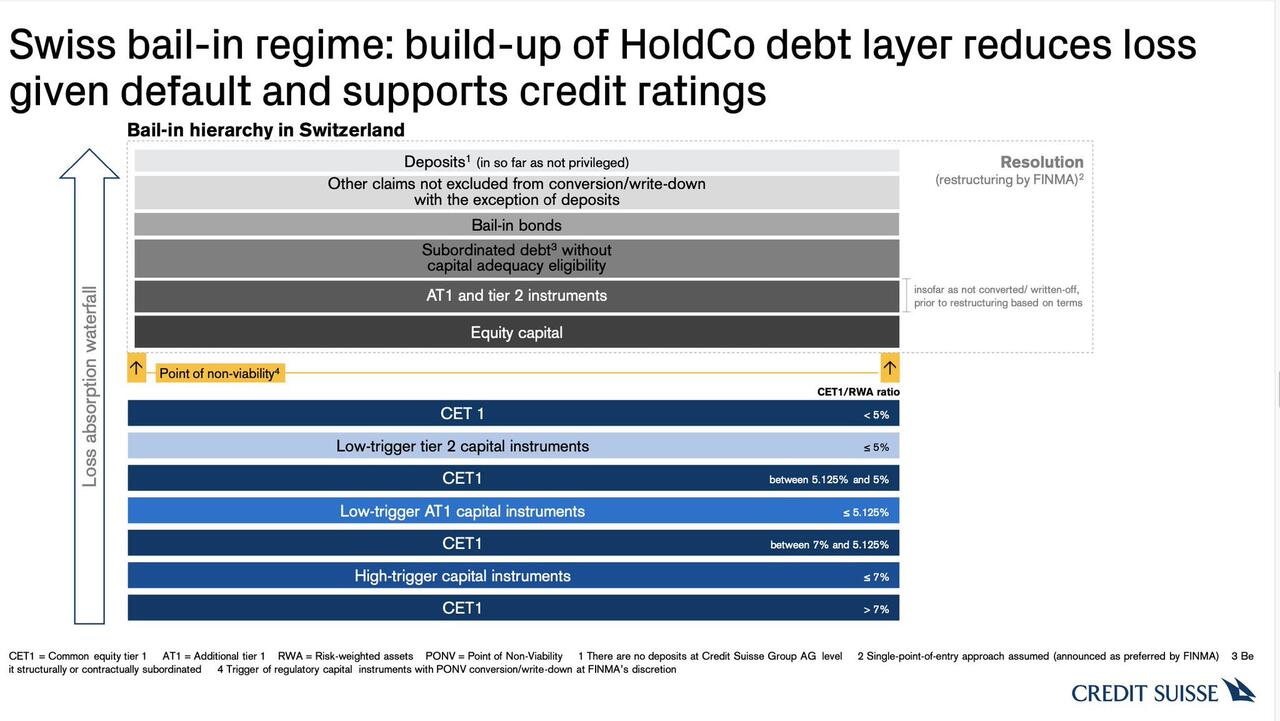

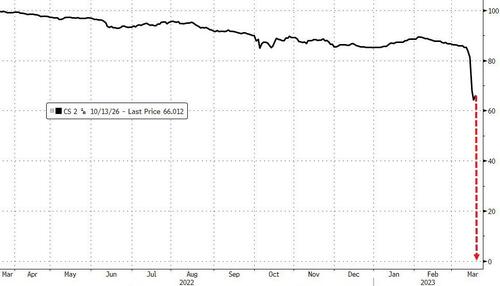

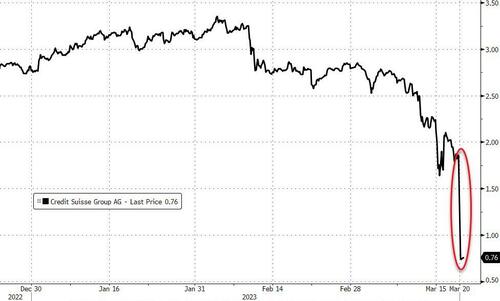

For anyone who believes that this is just a problem with a few smaller US banks and one big one (Credit Suisse), they must think again.

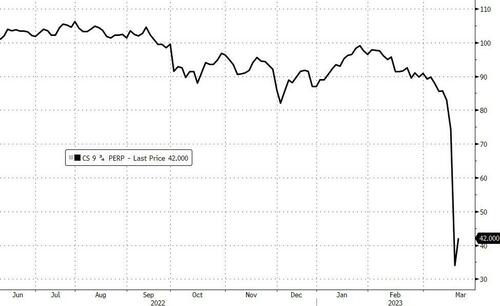

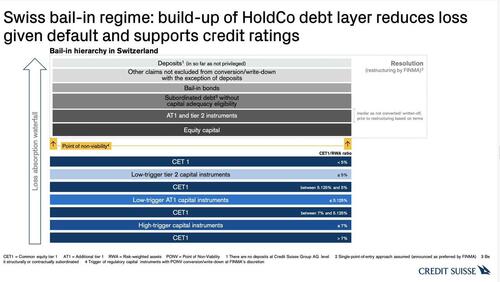

RE CREDIT SUISSE SEE ‘STOP PRESS’ AT THE END OF THE ARTICLE.

THE BANKS ARE FALLING LIKE DOMINOS, INCLUDING CREDIT SUISSE TONIGHT

Yes, Silicon Valley Bank (16th biggest US bank) is gone after an idiotic and irresponsible policy to invest short term customer deposits in long term US Treasuries at the bottom of the interest rate cycle. Even worse, they then valued the bonds at maturity rather than market, to avoid taking a loss. Clearly a management that didn’t have a clue about risk. SVB’s demise is the second biggest failure of a US bank.

Yes, Signature Bank (29th biggest) is gone due to a run on deposits.

And yes, First Republic Bank had to be supported by US lenders and the Fed by a $30 billion loan due to a run on deposits. But this won’t stop the rot as depositors attack the next bank and the next one and the next one……….

And yes, the Swiss second largest bank Credit Suisse (CS) is terminally ill after a number of poor investments over the years combined with poor management that has come and gone virtually every year.. I wrote an important article about the coming demise of CS 2 years ago here: “ARCHEGOS & CREDIT SUISSE – TIP OF THE ICEBERG.”

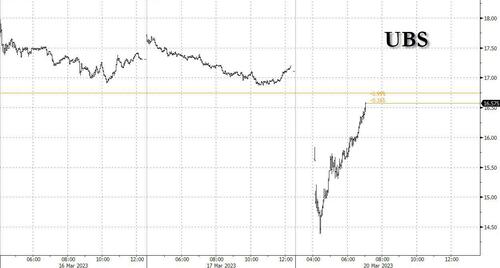

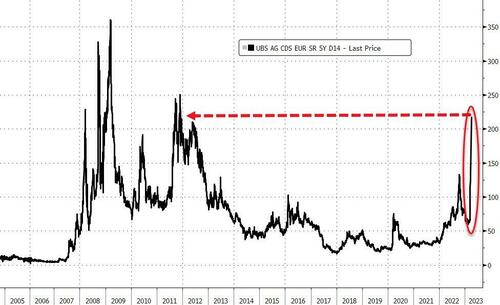

The situation at CS is so dire that a solution needs to be found before Monday’s (March 20) opening. The bank cannot survive in its present form. A failure for Credit Suisse would not just rock the Swiss financial system but have severe global repercussions. A merger with UBS is one solution. But UBS had to be bailed out in 2008 and doesn’t want to be weakened again by Credit Suisse without state guarantees and support from the Swiss National Bank (SNB). The SNB injected CHF50 billion into CS last week but the share price still went to a new low.

No one should believe that a state subsidised takeover of Credit Suisse by UBS will solve the problem. No, it will just be rearranging the deck chairs on the titanic and making the problem bigger rather than smaller. So rather than a lifebuoy, UBS will have a massive lead weight to carry which will guarantee its demise as the banking system collapses. And the Swiss government will take on assets which will be unrealisable.

Still, it is likely that by the end of the present weekend a deal will be announced with UBS being offered a deal they can’t refuse by taking over the good assets and the SNB/Government nurturing the bad assets of Credit Suisse in a rescue vehicle.

The SNB is of course in a mess itself, having lost $143 billion in 2022. The SNB balance sheet is bigger than Swiss GDP and consists of currency speculation and US tech stocks. This central bank is the world’s biggest hedge fund and the least successful.

Just to put a balanced view on Switzerland. It has the best political system in the world with direct democracy. It also has low Federal debt and normally no budget deficits. It is also the safest country in the world.

SWISS BANKING SYSTEM TOO BIG TO SAVE

But the Swiss banking system is very unsound, just like the rest of the world’s. A central bank which is bigger than the country’s GDP is extremely unsound. And a banking system which is 5x Swiss GDP makes it too big to save.

Although the Fed and ECB are much smaller in relation to their countries’ GDP than the SNB, these two central banks will soon discover that their assets of around $8 trillion each are grossly overvalued.

With a global banking system on the verge of a systemic failure, Central Bankers and bankers have been working around the clock this weekend to temporarily avoid the inevitable collapse of the bankrupt financial system.

BIGGEST MONEY PRINTING IN HISTORY COMING

As I pointed out above, the main Central Banks would also be bankrupt if they valued their assets honestly. But they have a wonderful source of money that they will tap to save the system.

Yes, I am of course talking about money printing.

We will in coming months and years see the most massive avalanche of money printing that has ever hit the world.

For anyone who believes that we are just seeing another bank run that will quickly evaporate, they will need to take a shower in ice cold Alpine water.

What we are witnessing is not just a temporary drama that will be sorted out by “the all powerful and resourceful” central banks.

THE DEATH OF MONEY

No, instead what we are seeing is the end phase of this financial era which started with the formation of the Fed in 1913 and in the next few years, or much sooner, will end with the death of money.

But the Death of Money doesn’t just mean that the dollar (and most currencies) will make their final move to ZERO, having already declined 98% since 1971.

Currency debasement is not the cause but the effect of the banking Cabal taking control of the money for their own benefit. As Mayer Amschel Rothschild said in the late 1700s: “Let me issue and control a nation’s money and I care not who makes the laws”.

Sadly, as this Cassandra (me) has written about since the beginning of the century, the Death of Money is not just all currencies going to ZERO as they have throughout history.

No, the Death of Money means a total and final collapse of this financial system.

Cassandra was a priestess in Greek mythology who was given the gift of predicting major events accurately but also given the curse that no one would believe her predictions.

No depositor must believe that the FDIC (Federal Deposit Insurance Corp) in the US or similar vehicles in other countries will save their deposits. All these organisations are massively undercapitalised and in the end it will be the governments in all countries which step in.

We know of course, that the government has no money. They just print whatever they need. That leaves ordinary people taking the final burden of all this money printing.

But ordinary people will have no money either. Yes a few rich people will be taxed heavily to cover bank deficits and losses. Still, that will be a drop in the ocean. Instead ordinary people will be impoverished with little income, no government handouts, no pension and money which is worthless.

The above is sadly the cycle that all economic eras go through. The issue this time is that the problem is global and of a magnitude never seen before in history.

Regrettably a rotten and bankrupt financial system needs to go through a cleansing period which the world will now experience. There cannot be sound growth and sound values until the current corrupt and debt infested system implodes. Only then can the world grow soundly again.

The transition will sadly be dramatic with a lot of suffering for most people. But there is no other way. We won’t just see poverty, famine but also many human tragedies. The risk of social unrest or civil war is very high plus the risk of a global war.

Central banks had of course hoped that their Digital Currencies (CBDC) would be ready to save them (but not the world) from the present debacle by totally controlling people’s spending. But in my view they will be too late. And since CBDCs are just another form of Fiat money, it would just exacerbate the problem with an even more severe outcome at the end. Still, it won’t prevent them from trying.

MARKET VALUE OF US BANKING ASSETS $2 TRILLION LOWER THAN BOOK VALUE

A paper issued by 4 US academics in finance, illustrates the $2 trillion black hole in the US banking system:

“Monetary Tightening and U.S. Bank Fragility in 2023: Mark-to-Market Losses and Uninsured Depositor Runs?”

March 13, 2023

Erica Jiang, Gregor Matvos, Tomasz Piskorski, and Amit Seru

CONCLUSION

“We provide a simple analysis of U.S. banks’ asset exposure to a recent rise in the interest rates with implications for financial stability. The U.S. banking system’s market value of assets is $2 trillion lower than suggested by their book value of assets. We show that these losses, combined with a large share of uninsured deposits at some U.S. banks can impair their stability. Even if only half of uninsured depositors decide to withdraw, almost 190 banks are at a potential risk of impairment to even insured depositors, with potentially $300 billion of insured deposits at risk. If uninsured deposit withdrawals cause even small fire sales, substantially more banks are at risk. Overall, these calculations suggest that recent declines in bank asset values significantly increased the fragility of the US banking system to uninsured depositors runs.”

What is crucial to understand is that the $2 trillion “loss” is only due to higher interest rates. When the US economy comes under pressure, the loan books of the banks will deteriorate dramatically and bad debts increase exponentially. With total assets of US commercial banks at $23 trillion, I would be surprised if 50% is repaid or recoverable in the coming crisis.

The above risks are just for the US financial system. The global system will be no better with the EU under massive pressure partly due to US led sanctions of Russia. Virtually every major economy in the world is in a dire position.

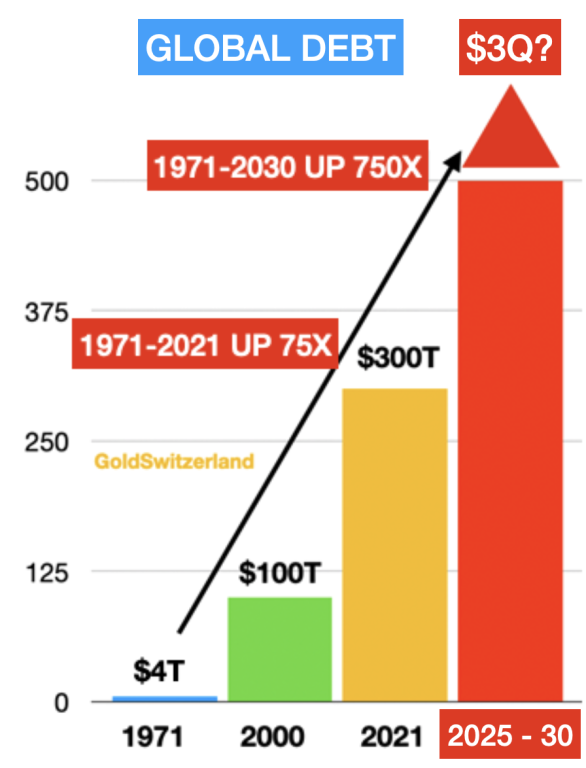

Let’s just look at the debt pyramid which I have discussed in many articles.

In 1971, when Nixon closed the gold window, global debt was $4 trillion. With gold backing no currency, this became a free for all to print unlimited amounts of money. And thus by 2000 debt had grown 25x to $100t. In 2006, when the Great Financial Crisis started, global debt was $120 trillion. By 2021 it had grown 75x from 1971 to $300 trillion.

The red column shows global debt at $3 quadrillion sometime between 2025 and 2030.

This assumes that the shadow banking system plus outstanding derivatives of currently probably around $2 quadrillion will need to be saved by central banks in a money printing bonanza. This will obviously lead to hyperinflation and thereafter to a depressionary implosion.

I know this sounds sensational but still a very likely scenario at the end of the biggest credit bubble in history.

GOLD – CRITICAL WEALTH PRESERVATION

I have been standing on a soapbox for over 20 years, warning the world about the coming financial crisis and the importance of physical gold for wealth preservation purposes. In 2002 we invested important funds into physical gold with the purpose of holding it for the foreseeable future.

Between 2002 and 2011 gold went from $300 to $1,900. Since then gold corrected and then went sideways as stocks and the asset markets surged backed by massive credit expansion.

With gold currently around $1990, there is not much gain since 2011. Still since 2002 gold is up 7x. Due to the temporarily stronger dollar, gold’s gains measured in dollars are much smaller than in Euros, Pounds or Yen. But that will soon change.

In the final section of the article “WILL NUCLEAR WAR, DEBT COLLAPSE OR ENERGY DEPLETION FINISH THE WORLD?”, I outlined the importance of owning physical gold to store it in a safe jurisdiction away from kleptocratic governments.

“2023 is likely to be the year of gold. Both fundamentally and technically gold looks like it will make major up moves this year.”

And at the end of this article, I explain the importance of how and where gold should be held:“PREPARE FOR 10 YEARS OF GLOBAL DESTRUCTION.”

“So my own preference would be to own physical gold and silver that only I have direct control of and can withdraw or sell with very short notice.

It is also important to deal with a company that can move your metals at very short notice if the security or geopolitical situation would necessitate it.”

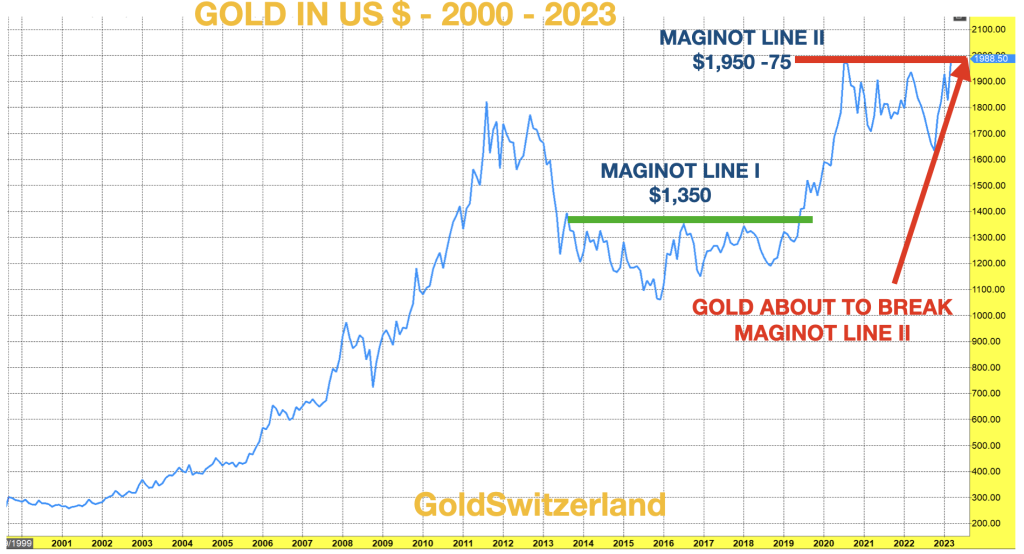

In February 2019 I wrote about what I called the Gold Maginot Line which had held for 6 years below $1,350. This is typical for gold. Having gone from $250 in 1999 to $1,900 in 2011, it then spent 8 years in a correction. At the time I forecast that the Maginot Line would soon break which it did and swiftly moved to $2,000 by August 2020. We have now had another period of consolidation since then and the next move above $2,000 and towards $3,000 is imminent.

Just to remind ourselves what happens to your money and gold during a hyperinflationary period, here is a photo from China’s hyperinflation in 1949 as people try to get their 40 grammes (just over one ounce) that they were allocated by the government. At some point in the next few years, there will be a panic in the West to buy gold at any price.

So as I have been urging investors for over 20 years, please get your gold NOW while it is still available.

STOP PRESS

Intense discussions are right now going on here in Switzerland between UBS, Credit Suisse, the regulator FINMA, the Swiss National Bank – SNB – and the Swiss Government. The Fed, the Bank of England and the ECB are also involved.

The latest rumour is that UBS will buy Credit Suisse for CHF900 million ($1 billion). The shares of CS closed at a market cap of CHF8 billion on Friday. The deal would clearly involve backing from the SNB and the Swiss government which would have to take on major liabilities.

The December 2022 book value of CS was CHF42 billion, as with all banks massively overstated.

The deal isn’t done at this point, 5.30pm Swiss time, but the whole banking world knows that without a deal, there will be global contagion starting tomorrow Monday the 20th.

Even if a provisional deal will be done by Monday’s open, the financial system has now been permanently injured with an open wound which won’t heal.

The problem will just move on to the next bank, and the next and the next….

Hold on to your seats but buy gold first.

END

23-03-18 19:40Section: Daily Dispatches

From The Telegraph, London

Sunday, March 19, 2023

https://www.telegraph.co.uk/opinion/2023/03/18/central-banks-have-pushed-us-precipice/

After the collapse of California’s Silicon Valley Bank left Prime Minister Rishi Sunak promising reporters a week ago there was “no systemic contagion risk,” here we are again.

Now the threat is even closer to home, with UBS in talks to take over all or part of Credit Suisse, in a deal brokered by a desperate Swiss government.

The sudden run on deposits at SVB was bad enough. It was the biggest U.S. lender to fail in more than a decade. Credit Suisse is in a different league altogether — one of only 30 banks worldwide classed as systemically important.

Already, there are warning signs that the move could threaten thousands of City jobs in London.

UBS has also made it clear it does not want to take on the full liabilities of Credit Suisse, asking the Swiss government for a backstop guarantee. The problem, of course, is that the combined balance sheet of the merged Swiss group would be much larger than Switzerland’s GDP — not a good place for a small country in the early stages of another global storm.

The fault for this slow-moving crisis is not hard to identify. Overconfident central banks and regulators, convinced of their godlike power to manage the world’s economy and keep it from danger, have once again pushed us to the precipice.

While individual banks deserve to face the consequences of their investment decisions, and directors, shareholders, and bondholders are ultimately responsible, it would be too easy to focus on their errors alone. The arrogance of financial regulatory authorities has helped to make the situation worse.

The immediate cause for the banks’ distress is a recent spate of interest rate hikes. The Federal Reserve in America runs annual stress tests on the banking sector to keep participants behaving responsibly. It emerged last week that, for the past decade, these tests have not assessed how banks would cope after a sudden, sharp rise in interest rates. False assurance in the system’s robustness came from the top down.

The impact of these hikes was then worsened by a regulatory system that assured financial institutions that government bonds such as U.S. Treasuries were the safest possible bet. Bond prices fall when rates rise, leaving any institution that swallowed the guidance nursing huge paper losses. That can be fine, unless these investments suddenly need to be turned into real money.

SVB appears an extreme example of where that advice could lead.

The interest rate rises that are now causing such havoc are themselves the result of earlier errors. Central banks decided that they had no choice but to act after inflation suddenly raged out of control last year, after decades of moderation.

Yes, Putin’s war of aggression in Ukraine played some role in this economic shock. But the greatest culprit was once again a bout of desperate ingenuity from the center. This time it was the extraordinary fiscal stimulus unleashed during the Covid pandemic. Worldwide, nearly $11 trillion was pumped into the system: a staggering 10% of global GDP.

Little wonder that our systems struggled to adjust in its aftermath.

Nor is this the beginning of the story. We have been living in the Alice-in-Wonderland world of easy money since 2008, or, arguably, since Alan Greenspan’s time at the Fed.

Quantitative easing and near-zero interest rates have kept the global economy on life support for a decade and a half. In this crisis too the ratings agencies proved asleep at the wheel. How can so few have realised the obvious: Interest rates that fall can also rise, and rise very quickly? Since when had the laws of finance and economics been repealed?

False confidence from regulators breeds instability. Interest rates need to be allowed to normalise from their artificially low levels so they can play their proper coordinating role in a free economy.

Yet in the brittle, artificial situation the gods of the central banks have created, every crisis produces more action and every action produces another crisis.

At some point we need to break the chain of failed interventions and acknowledge the limits to the power of central banks.

END

UBS offers to buy Credit Suisse for a pittance, nearly wiping out shareholders

Submitted by admin on Sun, 2023-03-19 09:08Section: Daily Dispatches

By Arash Massoudi, Stephen Morris, James Fontanella-Khan,

Laura Noonan and Owen Walker

Financial Times, London

Sunday, March 19, 2023

UBS has offered to buy Credit Suisse for up to $1bn, with Swiss authorities planning to change the country’s laws to bypass a shareholder vote on the transaction as they rush to finalise a deal before Monday.

The all-share deal between Switzerland’s two biggest banks is set to be signed as soon as this evening and will be priced at a fraction of Credit Suisse’s closing price on Friday, all but wiping out the target’s shareholders, four people with direct knowledge of the situation said.

The offer was communicated this morning with a price of SFr 0.25 a share to be paid in UBS stock, far below Credit Suisse’s closing price of SFr 1.86 Friday, the people said. UBS has also insisted on a material adverse change that voids the deal if its credit default spreads jump by 100 basis points or more, they added. …

… For the remainder of the report:

https://www.ft.com/content/ec4be743-052a-4381-a923-c2fbd7ea9cfd

END

By doubling bid, UBS gets Credit Suisse and huge government credit line

Submitted by admin on Sun, 2023-03-19 13:53Section: Daily Dispatches

By Arash Massoudi, Stephen Morris, James Fontanella-Khan,

Laura Noonan, and Owen Walker

Financial Times, London

Sunday, March 19, 2023

UBS has agreed to buy Credit Suisse after increasing its offer to more than $2 billion, with Swiss authorities poised to change the country’s laws to bypass a shareholder vote as they rush to announce a deal before Monday.

The all-share deal between Switzerland’s two biggest banks is set to be announced as soon as this evening and will be priced at a fraction of Credit Suisse’s closing price on Friday, all but wiping out the target’s shareholders, three people with direct knowledge of the situation said.

UBS will now pay more than SFr 0.50 a share in its own stock, up from a bid of SFr 0.25 earlier today worth around $1 billion that was rejected by the Credit Suisse board, the people said.

But the price remains far below Credit Suisse’s closing price of SFr 1.86 on Friday.

The Swiss National Bank has agreed to offer a $100 billion liquidity line to UBS as part of the deal, according to two people familiar with the matter. …

… For the remainder of the report:

https://www.ft.com/content/ec4be743-052a-4381-a923-c2fbd7ea9cfd

end

Tanzania and India prepare to eliminate the uSA dollar in their bilateral trade

(Business Insider/Africa)//GATA

Tanzania and India prepare to eliminate U.S. dollar from their bilateral trade

Submitted by admin on Sun, 2023-03-19 09:44Section: Daily Dispatches

By Chinedu Okafor

Business Insider Africa

Lagos, Nigeria

Sunday, March 19, 2023

Tanzania and India have reached an agreement that will make the U.S. dollar no longer required for trade between the two nations.

Tanzania and India are able to conduct business using their respective currencies, the Tanzanian shilling and the Indian rupee, thanks to a bilateral trade settlement agreement.

According to data from the Indian High Commission in Dar es Salaam, the value of trade between the two countries was $4.5 billion (roughly Sh 10.4 trillion) in the year ending March 2022. India is one of Tanzania’s largest trading partners.

According to Binaya Pradhan, the Indian high commissioner to Tanzania, between April 2021 and March 2022 India’s exports to Tanzania totaled $2.3 billion (or about Sh 5.3 trillion), while its imports from the East African country were estimated to be $2.2 billion (about Sh 5.1 trillion).

He claimed that Tanzanian businesses and banks have the chance to fully utilize the new framework to enable seamless payment in local currencies. …

… For the remainder of the report:

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

END

5.IMPORTANT COMMENTARIES ON COMMODITIES:

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

end

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//MONDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 6.8795

OFFSHORE YUAN: 6.8802

SHANGHAI CLOSED DOWN 15.64 PTS OR 0.48%

HANG SENG CLOSED DOWN 517.88 PTS OR 2.65 %

2. Nikkei closed DOWN 388.12 PTS OR 1.42%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 103.09 Euro RISES TO 1.0707 UP 54 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.217!!(Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 131.02/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.0585%***/Italian 10 Yr bond yield FALLS to 4.003%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.180…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.056//

3j Gold at $1985,00//silver at: 22.48 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 16/100 roubles/dollar; ROUBLE AT 76.90//

3m oil into the 65 dollar handle for WTI and 72 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 132.56/10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .217% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9270– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9926well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc. CREDIT SUISSE IN TROUBLE

USA 10 YR BOND YIELD: 3.380% DOWN 2 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.609 UP 1 BASIS PTS//INVERTED TO THE 10 YEAR!!

USA 2 YR BOND YIELD: 3.753 DOWN 9 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.02…

GREAT BRITAIN/10 YEAR YIELD: 3.271% DOWN 1 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Reverse Overnight Plunge As European Banks Stabilize From Historic Rout

MONDAY, MAR 20, 2023 – 08:03 AM

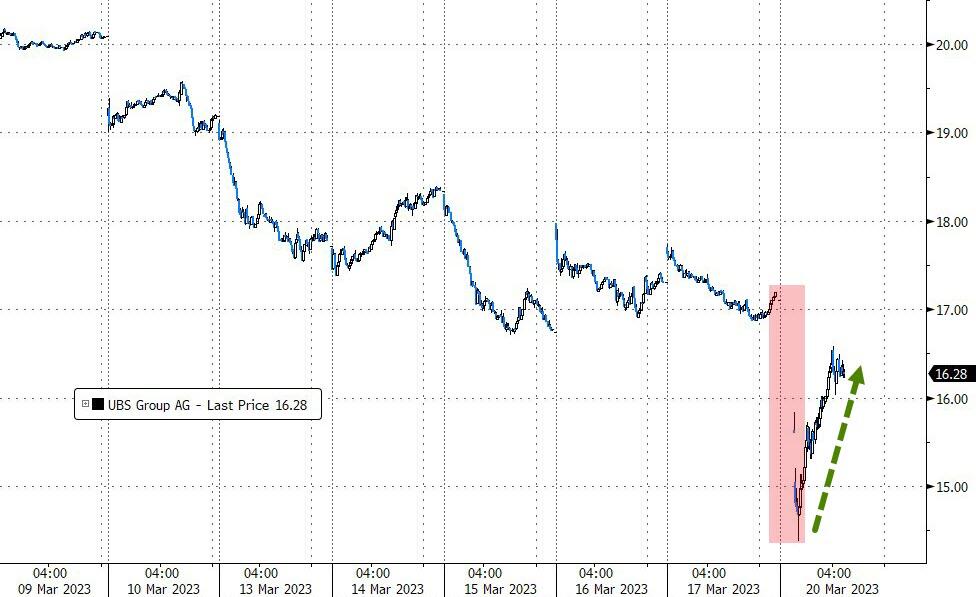

US equity futures, global markets and European bank stocks have stabilized, rebounding off worst levels which saw Europe’s brand new banking megagiant UBS plunge as much as 16% before recouping most of the losses…

… as investors digested UBS’s agreement to buy Credit Suisse as well as central bank moves to boost dollar liquidity in an effort to restore confidence in the global financial system. Futures contracts on the S&P 500 were little changed at 7:30 a.m. ET after tumbling 1% earlier. The Stoxx Europe 600 index was modestly higher, with banks and financial services still the sharpest fallers. UBS shares sank as much as 16%, while Credit Suisse sank 60%. European bank stocks pared losses with the Stoxx Europe 600 Banks Index down less than 1%, after after dropping as much as 6%. A gauge of Asian shares fell by more than 1%.

In premarket trading, First Republic Bank was poised to extend last week’s record loss as the US lender’s shares plunged 19% after S&P cut its credit rating again. Wells Fargo and Citigroup trimmed US premarket declines. Gold-mining stocks rallied in premarket trading on Monday, after a $3.2 billion deal between UBS and troubled lender Credit Suisse failed to calm nerves in the banking industry, knocking risk appetite. Newmont, the biggest US-listed gold miner, gains as much as 2.6%; Harmony Gold Mining +5.6%, Gold Fields +2.2%, New Gold +3.4%, Wheaton Precious Metals +1.5%, First Majestic Silver +2%, Pan American Silver +0.7%. The price of gold rose above $2,000 an ounce for the first time in a year amid safe-haven appeal. Here are some other notable premarket movers:

- Cryptocurrency-exposed stocks rise after Bitcoin extended its gains for a fifth consecutive session, with the digital asset reaching levels not seen in about nine months. Marathon Digital (MARA US) +5.6%, Riot Platforms (RIOT US) +8% and Coinbase (COIN US) +4.2%

- Energy stocks decline as investors’ concern about the banking system spur broad risk aversion and drag crude prices lower. Exxon Mobil (XOM US) slid 1.3%, Chevron (CVX US) -1.1%, Occidental Petroleum (OXY US) -1.1%.

For those who were lucky enough to be away from their computers this weekend, this is what you missed:

- Credit Suisse shareholders will receive 1 share in UBS (UBSN SW) for 22.48 shares in Credit Suisse which reflects a merger consideration of CHF 3bln and that FINMA determined that Credit Suisse’s additional tier 1 capital in the aggregate nominal amount of around CHF 16bln will be written off. Credit Suisse also told staff in a memo that the details of the transaction are being worked through and no disruption to client services is expected, while it told staff there will be no changes to payroll arrangements and bonuses will still be paid on March 24th.

- UBS said the company will suspend share buybacks and that they did not initiate the discussions but believe the transaction is financially attractive to UBS shareholders and are planning to de-risk and downsize Credit Suisse’s investment banking operations. UBS also noted its strategy is unchanged in US and APAC and said that Credit Suisse is quite complementary to the wealth business in Southeast Asia. Furthermore, Colm Kelleher will be Chairman and Ralph Hamers will be Group CEO of the combined entity, while the transaction is not subject to shareholder approval and there is a material adverse change clause on the Credit Suisse deal.

- SNB said it is providing substantial liquidity assistance to support the UBS takeover of Credit Suisse and the takeover was made possible with the support of the Swiss federal government, FINMA and SNB, while it added that both banks have unrestricted access to the SNB’s existing facilities. There were also comments from the Swiss Finance Minister that this is a commercial solution and not a bailout, while she noted the cost of bankruptcy to the Swiss economy would have been huge.

- ECB said it welcomes the swift actions and decisions taken by Swiss authorities and noted that the Euro area banking sector is resilient with strong capital and liquidity positions. ECB’s Lagarde also stated that the ECB’s policy toolkit is fully equipped to provide liquidity support to the euro area financial system if needed.

- BoE said it welcomes the comprehensive actions by the Swiss authorities to merge UBS and Credit Suisse, while it has been engaging with international counterparts throughout preparations for the announcement. Furthermore, it stated that the UK banking system remains safe and sound and is well-capitalised and funded.

- Fed Chairman Powell and US Treasury Secretary Yellen said they welcome the announcements by Swiss authorities to support financial stability and noted the capital and liquidity positions of the US banking system are strong and US financial system resilience is strong. Furthermore, they have been in close contact with international counterparts to support their implementation.

- At least two major banks in Europe are examining scenarios of contagion potentially spreading across Europe’s banking sector and looking to the Fed and ECB to step in with stronger signals of support, according to Reuters citing executives with knowledge of the deliberations.

- Banking stocks and bonds plummeted after UBS Group sealed a state-backed takeover of troubled peer Credit Suisse, a deal that was shoved down Credit Suisse investors’ throats – literally – in an attempt to restore confidence in a battered sector.

- The Federal Reserve and five other central banks announced coordinated action on Sunday to boost liquidity in US dollar swap arrangements. The Fed’s next policy decision is due later this week, with market attention on whether it may slow or pause interest-rate hikes.

- UBS emerged as Switzerland’s one and only global bank, a risky bet that makes the Swiss economy more dependent on a single lender. Credit Suisse told staff its wealth assets are operationally separate from UBS for now, but once they merged clients might want to consider moving some assets to another bank if concentration was a concern.

- The rudest shock in the rushed deal was reserved for the holders of Credit Suisse’s riskiest tranche of bonds. UBS is salvaging the most value from the wreckage, says Breakingviews columnist Liam Proud.

- Hedge fund managers and other large investors believe it is far too soon to call an all-clear on turmoil in the global financial sector.

Amid the endless turmoil, the KBW Bank Index plunged 28% over the past two weeks, with financials rattled by concerns over Credit Suisse as well the recent failures of Silicon Valley Bank and two other US lenders. Gains in tech stocks have helped support the overall market, however, as investors look for a safe haven.

“The turmoil still has at least a couple of days to play out, and only the Fed can come in and calm that,” Chris Beauchamp, chief market analyst at IG Group Holdings Plc, said on Bloomberg Television. He expects the US central bank to hike rates by 25 basis points as a pause would be interpreted by markets as a sign that the stress in banks is bigger than initially thought.

“Assuming these banking stresses do not evolve into something more serious, the European Central Bank and the Fed may perceive that they are at or near their objectives with current policy,” said Brad Tank, chief investment officer for fixed income at Neuberger Berman. “The Fed, in particular, is further along in its tightening cycle and should have more flexibility to pause — and markets are indeed pricing for 2023 fed funds rate cuts once again.”

Meanwhile, one day after he revealed his shock that stocks remain resilient and just under 4,000 despite calling for a crah for the past 3 months, Morgan Stanley’s Michael Wilson said the stress in the banking system marks what’s likely to be the beginning of a painful and “vicious” end to the bear market in US stocks, adding that the risk of a credit crunch has increased materially. The S&P 500 will remain unattractive until equity risk premium climbs to as high as 400 basis points from the current 230 level, according to the bearish strategist who two weeks ago flip-flopped briefly to bullish before getting rugpulled by the banking crisis.

European stocks are higher after reversing the negative knee-jerk reaction to the terms of the UBS takeover of Credit Suisse. The Stoxx 600 is up 0.6% as gains in utilities, miners and consumer products outweigh declines in bank stocks. European oil stocks declined as investors’ concern about the potential for a global banking crisis spur broad risk aversion and drag crude prices lower. The Stoxx Europe 600 Energy index slid 1%; among oil majors, Shell declined 1.5%, TotalEnergies -1.3%, and BP -0.6%. Smaller producers also dropped with Harbour Energy falling 5.7% and Tullow Oil -7.7%. Here are the biggest European movers:

- UBS shares drop as much as 16%, the most in eight years, after a government-brokered deal for it to buy rival Credit Suisse prompted a slew of downgrades

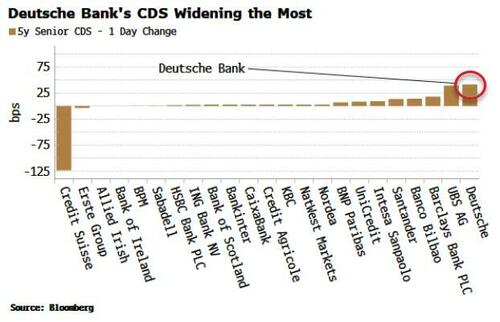

- Deutsche Bank declines 11%, ING -9.6%, Commerzbank -9.6%, Standard Chartered -8.7%, BNP Paribas -9% following UBS’s agreement to buy Credit Suisse

- El.En shares slide as much as 9.6% after Berenberg downgrades the laser- equipment maker to hold from buy, saying the company has a “tough year ahead”

- JM AB falls as much as 7.7% after DNB Markets gave the Swedish construction and building management company its sole sell rating in reinstated coverage

- Centamin shares rise as much as 6.6%, Endeavour Mining up as much as 7.2% and Fresnillo rises as much as 4.1% as gold gains owing to haven demand amid banking concerns