MARCH 21//RAID!!//GOLD CLOSED DOWN $39.70 TO $1938.60//SILVER CLOSED DOWN $.24 TO $22.29//PLATINUM CLOSED DOWN $15.45 TO $974.05//PLATINUM CLOSED DOWN $31.60 TO $1391.80//COVID UPDATES//DR PAUL ALEXANDER/VACCINE IMPACT//SLAY NEWS//CO CO BOND YIELDS SKYROCKET TO 15% AS THESE ARE SHUNNED//UKRAINE VS RUSSIA//USA SENDS 350 MILLION DOLLARS FOR AID TO UKRAINE//UK TO PROVIDE ARMOUR PIERCING BULLETS AND URANIUM DEPLETED (RADIOACTIVE)//SWAMP STORIES FOR YOU TONIGHT///

435 H SCOTIA CAPITAL 47 624 H BOFA SECURITIES 146 657 C MORGAN STANLEY 10 661 C JP MORGAN 65 12 661 H JP MORGAN 100 732 C RBC CAP MARKETS 6 737 C ADVANTAGE 11 5 880 C CITIGROUP 50 905 C ADM 1 13

TOTAL: 233 233

JPMORGAN stopped 12/233 contracts

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR MAR/2023. CONTRACT: 233 NOTICES FOR 23300 OZ or 0.7247 TONNES

total notices so far: 4973 contracts for 497300 oz (15.868 tonnes)

SILVER NOTICES: 4 NOTICE(S) FILED FOR 20,000 OZ/

total number of notices filed so far this month : 3091 for 15,455,000 oz

END

GLD

WITH GOLD DOWN $38.70

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD:////// ANOTHER MASSIVE DEPOSIT OF 3.40 TONNES OF GOLD INTO THE GLD//

INVENTORY RESTS AT 924.55TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 24 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF OF 0.781 MILLION OZ FROM THE SLV: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 458.566. MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL SIZED 189 CONTRACTS TO 120,906 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS SMALL SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.15 GAININ SILVER PRICING AT THE COMEX ON MONDAY. WE ARE NOW RECORDING FOR PROSPERITY OUR NEW LOW COMEX OI SILVER SET AT 119,412 CONTRACTS , MARCH 17/2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.15). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A HUGE GAIN ON OUR TWO EXCHANGES 1126 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 1 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD: A VERY STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS( 845 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.58 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE JUMP TO LONDON OF 5,000 OZ//NEW STANDING: 15.575 MILLION OZ + THE 1.0 MILLION OZ OF EXCHANGE FOR RISK//THUS TOTAL NEW STANDING 16.575 MILLION OZ/ //// V) HUGE SIZED COMEX OI GAIN/ STRONG SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –92 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTRACTS for 15 days, total 12,074 contracts: OR 60.370 MILLION OZ . (804 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 60.370 MILLION OZ

.

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 60.370MILLION OZ//INITIAL//ON PAR WITH LAST MONTH

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 189 CONTRACTS WITH OUR $0.15 GAIN IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A VERY STRONG SIZED EFP ISSUANCE CONTRACTS: 845 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAR OF 15.58 MILLION OZ//FIRST DAY NOTICE// FOLLOWED BY TODAY’S 5,000 OZ QUEUE JUMP TO LONDON (WHICH INCREASES THE AMOUNT OF SILVER STANDING) + 1.0 MILLION OF EXCHANGE FOR RISK ISSUED EARLY IN MARCH (INCREASES THE AMOUNT OF SILVER STANDING) //NEW STANDING 16.575 MILLION OZ .. WE HAVE A HUGE SIZED GAIN OF 1034OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 4 NOTICE(S) FILED TODAY FOR 20,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 4408 CONTRACTS TO 480,136 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -1677 CONTRACTS.

.

WE HAD A HUGE SIZED INCREASE IN COMEX OI ( 12,454CONTRACTS) WITH OUR $9.60 GAIN IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR MAR. AT 4.9953 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 35,500OZ (1.104 TONNES) //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London).

YET ALL OF..THIS HAPPENED WITH OUR $9.60 GAIN IN PRICEWITH RESPECT TO MONDAY’S TRADING

WE HAD A HUGE SIZED GAIN OF 12,454 OI CONTRACTS (38.737 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A VERY STRONG SIZED 8046 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 480,136

IN ESSENCE WE HAVE A HUGE SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 12,454 CONTRACTS WITH 4408CONTRACTS INCREASED AT THE COMEX AND 8046 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 12,454 CONTRACTS OR 38.737 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A VERY STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (8046 CONTRACTS) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (4408) TOTAL GAIN IN THE TWO EXCHANGES 12,454 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR MAR. AT 4.9953 TONNES FOLLOWED BY TODAY’S 35,500 OZ QUEUE JUMP//NEW STANDING 16.0747 TONNES // ///3) ZERO LONG LIQUIDATION //4) STRONG SIZED COMEX OPEN INTEREST GAIN// 5) VERY STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

TOTAL EFP CONTRACTS ISSUED: 68,370 CONTRACTS OR 6,837,000 OZ OR 212.65 TONNES IN 15 TRADING DAY(S) AND THUS AVERAGING: 4558 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15TRADING DAY(S) IN TONNES 212.65 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 212.65/3550 x 100% TONNES 5.97% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 212.65 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A SMALL SIZED 189 CONTRACTS OI TO 120,906 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A RECORD LOW OF 119,412 CONTRACTS THIS PAST WEEK, MARCH 17/2022

EFP ISSUANCE 845 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 845 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 845 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 189CONTRACTS AND ADD TO THE 845 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE GAIN OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1054 CONTRACTS.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES //5.170 MILLION OZ

OCCURRED DESPITE OUR $0.15 GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED UP 20.74 PTS OR 0.64% //Hang Seng CLOSED UP 238.05 PTS OR 1.36% /The Nikkei closed //Australia’s all ordinaries CLOSED UP 0.81% /Chinese yuan (ONSHORE) closed UP 6.8722//OFFSHORE CHINESE YUAN UP TO 6.8719// /Oil UP TO 67,79 dollars per barrel for WTI and BRENT AT 74,24 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 4408 CONTRACTS UP TO 480,136 WITH OUR GAIN IN PRICE OF $9.60 ON MONDAY

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAR… THE CME REPORTS THAT THE BANKERS ISSUED A VERY STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 8046 EFP CONTRACTS WERE ISSUED: : APRIL 8046 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 8046 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A HUGE TOTAL OF 12,454 CONTRACTS IN THAT 8046LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED GAIN OF 4408 COMEX CONTRACTS..AND THIS HUGE GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $9.60. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAR (16.047) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 16.0747 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $9.60) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR HUGE SIZED GAIN OF 12,454 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 38.737 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAR. (4.9953 TONNES) FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 35,500OZ (1.104 TONNES)… ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $9.60

WE HAD -1677 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 12,454 CONTRACTS OR 1,245,400 OZ OR 38.737 TONNES

TONNES

Estimated gold comex today 290,606// //fair

final gold volumes/yesterday 415,048///extremely strong

Total monthly oz gold served (contracts) so far this month

4973 notices 497,300 15.868 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 1

i) out of BRINKS: 6,430.200 oz (200 kilobars)

total withdrawals: 6430.200 oz

in tonnes: 0.20000 tonnes

Adjustments; 1

out of JPM: 12,117.720 oz adjusted out of dealer into customer account

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of MARCH we have an oi of 428 contracts having GAINED 75 contracts. We had 280 notices filed on MONDAY so we

gained A HUGE 355 contracts or an additional 35,500 oz will stand for metal at the comex

April LOST A SMALL 12,726 contracts DOWN to 168,783 contracts. It is here that our banker friends have to worry as many will try and take delivery in this upcoming delivery month.

May GAINED 91 contracts to stand at 377

We had 233 notice(s) filed today for 23300 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 65 notices were issued from their client or customer account. The total of all issuance by all participants equate to 233 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 12 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAR. /2023. contract month,

we take the total number of notices filed so far for the month (4,973 x 100 oz ), to which we add the difference between the open interest for the front month of (MAR. 428 CONTRACTS) minus the number of notices served upon today 233 x 100 oz per contract equals 516,800 OZ OR 16.0747 TONNES the number of TONNES standing in this active month of MARCH.

thus the INITIAL standings for gold for the MAR contract month:

No of notices filed so far (4,973 x 100 oz+ 428 OI for the front month minus the number of notices served upon today (233)x 100 oz} which equals 516,800 oz standing OR 16.0747 TONNES in this active delivery month of MARCH..

TOTAL COMEX GOLD STANDING: 16.0747 TONNES WHICH IS HUGE FOR AN INACTIVE DELIVERY MONTH.

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 3091 x 5,000 oz = 15,455,000 oz

to which we add the difference between the open interest for the front month of MAR(28) and the number of notices served upon today 4 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAR./2023 contract month: 3091 (notices served so far) x 5000 oz + OI for the front month of MAR (28) – number of notices served upon today (4) x 500 oz of silver standing for the MAR. contract month equates 15.575 million oz +the 1.0 million oz of exchange for risk//new total standing 16.575 million oz

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

MARCH 15/THE IDES OF MARCH: WITH GOLD UP $18.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 913.27 TONNES

MARCH 14/WITH GOLD DOWN $4.75 TODAY: HUGE CHANGES: A MONSTER DEPOSIT OF 11.85 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 913.27 TONNES

MARCH 13/WITH GOLD UP $48.85 TODAY: VERY STRANGE HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY REST AT 901.42 TONNES

MARCH 10//WITH GOLD UP $31.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 903.15 TONNES

MARCH 9/WITH GOLD UP $16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 906.62 TONNES

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

FEB 28/WITH GOLD UP $12.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 917.61 TONNES

FEB 27/WITH GOLD UP $6.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.32 TONNES

FEB 24/WITH GOLD DOWN $9.10 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 917.32 TONNES

FEB 23/WITH GOLD DOWN $13.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 919.92 TONNES

FEB 22/WITH GOLD DOWN 22 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 919.92 TONNES

FEB 21/WITH GOLD DOWN $7.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 919.92 TONNES

FEB 17/WITH GOLD DOWN $1.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 921.08 TONNES

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

GLD INVENTORY: 924.55 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

MARCH 17/WITH SILVER UP 79 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE WITHDRAWAL OF 10.478 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 462.748 MILLION OZ//

MARCH 16/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 5.009 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 473.226 MILLION OZ//

MARCH 15/WITH SILVER DOWN 7 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 643,000 OZ INTO THE SLV//INVENTORY RESTS AT 478.235 MILLION OZ/

MARCH 14/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.287 MILLION OZ FROM THE SLV////INVENTORY REST AT 477.592 MILLION OZ//

MARCH 13/WITH SILVER UP $1.35 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ//

MARCH 10.WITH SILVER UP 36 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ…

MARCH 9/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.979 MILLION OZ

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWALOF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

FEB 28/WITH SILVER UP 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.241 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.188

FEB 27/WITH SILVER DOWN 15 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.471 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 482.429 MILLION OZ

FEB 24/WITH SILVER DOWN 46 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.172 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.900 MILLION OZ//

FEB 23/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.379 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.072 MILLION OZ//

FEB 22/WITH SILVER DOWN 22 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ FROM THE SLV////INVENTORY RESTS AT 485.693 MILLION OZ

FEB 21/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.5363 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 486.382 MILLION OZ//

FEB 17/WITH SILVER UP 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 827,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.819 MILLION OZ/

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 458.566MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

Peter Schiff: Americans Will Pay For These Bank Bailouts

Peter Schiff appeared on the Capitol Report on NTD News to talk about the bank bailouts and the possible ramifications. He said that no matter what President Joe Biden and others tell you, Americans are going to pay for this.

The interview started with a clip of Treasury Secretary Janet Yellen assuring Congrees that the banking system is safe. So, should we feel confident in our banking system?

Peter said, “not at all!”

In fact, that comment is as accurate as her earlier comments that inflation was transitory or the comments in the days leading up to the ‘08 financial crisis when she and everybody else at the Fed was saying not to worry about subprime because it was contained.”

Peter noted that Yellen kept interest rates at zero for virtually her entire term as Federal Reserve chair.

That’s the reason that we had such a big bubble. Those low interest rates and quantitative easing, and she was part of that, that’s why all these banks are loaded up with now underwater long-term Treasuries and mortgage-backed securities so the banking system is a house of cards. It couldn’t be less sound, and partially, Janet Yellen is to blame for the current state of affairs.”

The host noted the falling CPI and asked what that said about the state of the US economy.

The economy is literally a house of cards. It’s imploding. But inflation is going to get much worse because the Fed has already returned to quantitative easing, whether they admit it or not. The way they are bailing out all the banks is by printing new money and adding it into the economy and taking on mortgages and government debt onto their already bloated balance sheet. So, the Fed’s balance sheet is going to go up. The money supply is going to go up. And that means consumer prices are going to go way up.”

Meanwhile, President Joe Biden keeps insisting that Americans aren’t going to have to pay the cost of these bailouts.

He’s lying. They’re going to pay the cost through higher prices. And when he says that everybody’s bank account is now safe, it’s not. It’s in more danger than ever before because your bank account is going to be eroded in value because of inflation. So, even if your bank doesn’t fail, and you don’t lose your money, your money is going to lose its value.”

Why exactly did SVB fail? Peter said it was due to the low interest rate and QE environment it operated in for a decade.

It was the Federal Reserve that created all these distortions by its artificial suppression of interest rates, and it caused financial institutions to take incredible risks in order to get a return.”

US government regulations also encouraged these banks to load up on Treasuries and mortgages through favorable accounting

So, this whole thing was a byproduct of bad monetary and fiscal policy.”

END

SVB And Signature Bank Were Just The Tip Of The Iceberg

The demise of Silicon Valley Bank and Signature Bank was just the tip of the iceberg. As it turns out, hundreds of banks are at risk. This explains why the Federal Reserve and US Treasury rushed to provide what is effectively a bailout for the entire banking system.

According to a Washington Post report, banks would face unprecedented losses if they were forced to liquidate their bond portfolios as SVB did.

According to the Post, the total capital buffer in the US banking system totals $2.2 trillion. Meanwhile, total unrealized losses in the system based on a pair of academic papers is between $1.7 and $2 trillion.

In other words, if banks were suddenly forced to liquidate their bond and loan portfolios, the losses would erase between 77 percent and 91 percent of their combined capital cushion. It follows that large numbers of banks are terrifyingly fragile.”

A second report by the Wall Street Journal cites a study from Stanford and Columbia Universities that found 186 US banks are in distress.

As economist Peter St. Onge put it, “In other words, we were already right up against the edge.”

This is precisely why the Fed had to create a way for banks to borrow against their devalued bond portfolio. If banks were put in a position where they had to sell those bonds to raise capital, they would have fallen like dominoes.

The Fed bailout may have plugged that hole in the dam, but there will almost certainly be more cracks in the future.

It’s because of the government that Silicon Valley Bank was in the position that it was. The reason it owned so many long-term, low-yielding US Treasuries and mortgage-backed securities was because the Fed kept interest rates at zero for so long. And the reason that it chose those assets was because bank regulators kind of pushed banks into Treasuries and mortgage-backed securities because they give them favorable accounting treatment. They don’t have to take any haircuts. They don’t have to mark them to market. So, the government created the problem.”

In short, while tech bros and loose bankers hog the headlines, what drives hundreds of banks to the edge is our crony banking system.

In this case, rapid Fed rate hikes crashed into a banking system that fractional reserve banking and the Fed’s “Lender of Last Resort” (LOLR) permanent bailout have driven to permanently drive as fast as possible, as close to the edge of the cliff as possible.

Together, the moral hazard has given a green light to those reckless tech bros, to those loose bankers who hand out millions—it turns out hundreds of billions. And it drives the entire banking industry to use opaque accounting tricks to hustle sleepy regulators and innocent taxpayers and dollar-holders who get stuck with the bill. The bankers themselves sleep like babies because they know you’ll cover their losses, but they keep their wins.

What turned this rigged casino into a crisis is in the past year the Fed hiked rates at the fastest pace in 50 years, from 0 percent last March to 4.5 percent to 4.75 percent today. They did this in a desperate bid to cancel the inflation they caused by financing $7 trillion in deficit spending and Covid lockdowns. Indeed, those of us who wondered why voters stood by meekly had only to look at the flood of money going out the door.

These reckless hikes savaged long bond prices, by far the most popular asset in bank vaults: Across the board, long bonds fell 20 percent, feeding an estimated 10 percent plunge in all bank asset values. In essence, the bank thought it had a dollar in the vault, but turns out it only had 90 or 80 cents. In the case of high-flyers like Silicon Valley and potentially hundreds more, it was more like 60 cents. Few banks can survive that.

So, what’s next?

St. Onge said probably “a lot of pain and a lot of inflation” caused by more bailouts even as the economy spirals into a recession.

In other words – stagflation.

We the People will survive—after all, the real assets don’t vanish: the food, cars, and electricity are all there. It’s a paper crisis, but unfortunately that paper crisis has sucked real Americans in, suckered them into putting their life savings into the care of a bunch of degenerate gamblers in expensive suits. And it can bring enormous collateral damage to the wider economy that, yes, provides that food, cars, and electricity if government steps in, as it usually does.”

Schiff sees a similar future.

This is going to cost Americans a lot of money, not because their taxes are going to be raised, but because the Federal Reserve is financing this massive bailout by creating even more inflation. So, Americans are going to pay for this at the supermarket, at the gas station. Their cost of living is going to go way up. If you thought inflation was bad last year, it’s about to get a whole lot worse.”

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

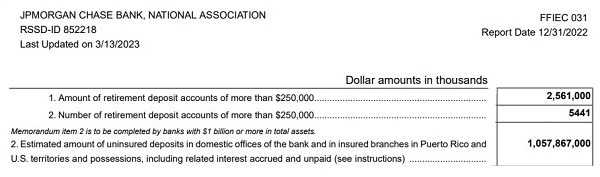

Jamie Dimon is the Chairman and CEO of JPMorgan Chase, the largest bank in the U.S., which is also ranked the riskiest global bank by its regulators. But instead of getting his own house in order in the midst of a banking crisis, Dimon has been peculiarly focused elsewhere.

Over the past five days, Jamie Dimon’s legions of publicists have been burning up the phone lines with reporters, pushing the narrative that Jamie Dimon is some kind of financial wizard who needs to have a seat at the table to save the regional bank, First Republic Bank. (Scroll down here to see the exhaustive public relations effort that has gone into this narrative.)

Last Thursday, news hit the wire services that Dimon had lined up 11 banks willing to place $30 billion in uninsured deposits into First Republic Bank. JPMorgan Chase, Bank of America, Citigroup and Wells Fargo each ponied up $5 billion – or two-thirds of the $30 billion. The Federal Deposit Insurance Corporation (FDIC) caps federal deposit insurance at $250,000 per depositor, per bank.

Taking $5 billion of your bank’s shareholders’ money and throwing it at a regional bank whose stock price is collapsing, was not viewed as the brightest of ideas by the stock market. Last Friday, the day after the deal was announced, shares of First Republic Bank dropped 32 percent. Yesterday, First Republic’s share price collapsed by another 47 percent. Over the weekend, S&P Global downgraded First Republic’s credit rating for a second time in a week to deeper junk status. Year-to-date, First Republic Bank has lost 90 percent of its market value. What exactly is there left to save?

We should also note that First Republic Bank’s Palm Beach, Florida branch is where Donald Trump’s hush money was wired to porn star Stormy Daniels by his attorney, Michael Cohen. (See our reporting here and the Wall Street Journal’s here.)

Today, a headline appears at Bloomberg News that provides a big clue as to what Jamie Dimon’s frantic obsession with First Republic Bank is really about, that is, use a collapsing regional bank to get Treasury Secretary Janet Yellen on board to push for a government guarantee on all deposits, insured and uninsured, at all FDIC banks. By framing this as coming to the rescue of regional banks, rather than another crony bailout of the unaccountable mega banks on Wall Street, Jamie Dimon doesn’t have to explain to his compromised Board of Directors why 69 percent of the bank’s deposits were uninsured at year end. (See: If You’re Baffled as to Why JPMorgan Chase’s Board Hasn’t Sacked Jamie Dimon as the Bank Racked Up 5 Felony Counts – Here’s Your Answer.)

Our scenario is supported by the following hard facts:

First Republic Bank’s regulatory filing for December 31, 2022 shows that it held $176.25 billion in deposits, of which $119.47 billion were uninsured, or 68 percent of all deposits. JPMorgan Chase’s same regulatory filing (FFIEC Call Report) for December 31, 2022 shows that at year-end it held $1.527 trillion in deposits of which an estimated $1.058 trillion were uninsured – or 69 percent.

3,Chris Powell of GATA provides to us very important physical commentaries

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

END

5.IMPORTANT COMMENTARIES ON COMMODITIES: LITHIUM

Even as global supply diminishes, lithium prices plummet by almost 50% as world demand sinks

(zerohedge0

Lithium Prices Plummet As Global Supply Concerns Diminish

TUESDAY, MAR 21, 2023 – 08:40 AM

The price of lithium has experienced a significant decline over recent months, resulting from a deceleration in electric vehicle sales and an increasing supply of the key ingredient used in battery packs.

Since November, the average price of battery-grade lithium carbonate in China has plunged from $84,500 per metric ton to $42,500, or about a 50% decline, according to Bloomberg data.

Vivek Chidambaram, the senior managing director for strategy at Accenture, a consulting firm, told NYT the plunge in lithium prices could be attributed to the slowdown in electric vehicle sales. He said tight supply last year, which resulted in skyrocketing prices, has shifted into surplus this year as suppliers are producing more battery-grade lithium carbonate than ever before.

“There was a time when people believed electric vehicles would grow very rapidly. Then the reality of how fast they were actually growing caught up.” He expects lithium prices to moderate over the next several years.

In the second half of 2022, EV demand slowed due to China’s ending of subsidies to stimulate sales in the world’s largest EV market. Then in the US, the world’s second-largest EV market, Tesla began discounting vehicles in December.

On Monday, Matty Zhao, an Asia Pacific basic materials analyst at Bank of America Securities, told CNBC that last year’s lithium shortfall, which sent prices soaring, could pivot into a surplus in 2023, with “a lot of supply coming out” from mines.

“We are expecting 38% lithium supply growth this year. That’s why 2023 is likely to turn into a surplus year for lithium,” Zhao said.

Cobalt, another crucial component in batteries, has seen prices plummet by over 50%. Meanwhile, copper, a key metal in electric motors and batteries, has experienced an 18% decline.

On a positive note, the decline in lithium prices could make EVs more affordable by lowering the cost of battery packs.

END

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

end

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 6.8722

OFFSHORE YUAN: 6.8719

SHANGHAI CLOSED UP 20.74 PTS OR 0.64%

HANG SENG CLOSED UP 238,05 PTS OR 1.36 %

2. Nikkei closed

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 102.69 Euro RISES TO 1.0779 UP 61 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.218!!(Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 132.21/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen XX CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.264%***/Italian 10 Yr bond yield RISES to 4.093%*** /SPAIN 10 YR BOND YIELD RISES TO 3.301…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.137//

3j Gold at $1961,90//silver at: 22.47 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 39/100 roubles/dollar; ROUBLE AT 76.78//

3m oil into the 67 dollar handle for WTI and 74 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 132.21/10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .217% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9242–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9968well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.541% up 6 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.707 UP 5 BASIS PTS//INVERTED TO THE 10 YEAR!!

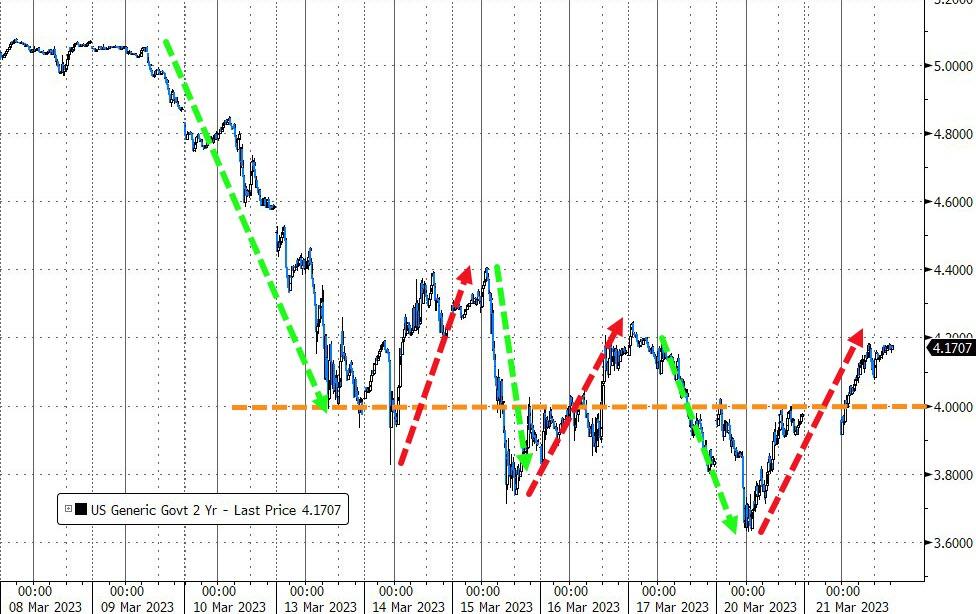

USA 2 YR BOND YIELD: 4.0949 UP 17 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.02…

GREAT BRITAIN/10 YEAR YIELD: 3.398% UP 9 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Surge Above 4,000 As Bank Crisis Fades Amid Growing Deposit Insurance Speculation

TUESDAY, MAR 21, 2023 – 08:05 AM

It’s only appropriate that the day after the weekly dose of doom and gloom from Marko Kolanovic and Mike Wilson, that stocks soar to the highest level in almost two weeks. S&P futures spiked above 4,000 on Tuesday as fears about turmoil in the global banking sector subsided, following a Bloomberg report that the Biden admin was considering insuring all deposits (unclear exactly how they will credibly insure all $18 trillion in deposits, some 75% of US GDP but whatever) followed by an FT article this morning previewing Janet Yellen’s speech at the American Bankers Association on Tuesday in which the Treasury Secretary will signal further US government backing for deposits at smaller American banks if needed, “a shift that seeks to protect parts of the country’s banking system struggling in the recent financial turmoil.”

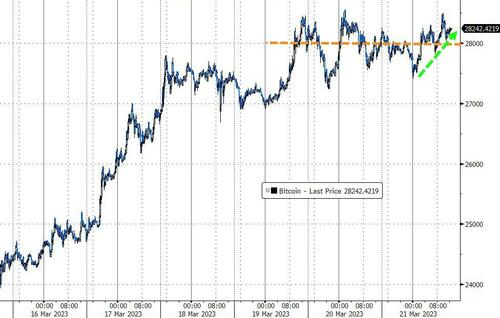

Contracts on the S&P 500 were up 0.8% by 7:45 a.m. ET paced by European shares with Estoxx50 +1.8% on the day as risk appetite has been stoked by report that US officials are studying ways to temporarily guarantee all bank deposits; Nasdaq 100 futures gained 0.7%. Both underlying indexes had risen on Monday. European and Asian markets were solidly in the green. As a result of the jump in risk sentiment, traders are also firming up bets on the Fed raising rates another 25bp on Wednesday with ~20bps currently priced in — versus less than 10bp at one stage on Monday.%. The Bloomberg Dollar Spot Index was down for the second day as treasury yields edged higher, mirroring moves in the UK and Europe. Gold fell and oil rose, while Bitcoin retreated for the first time in nearly a week.

Among notable movers in US premarket trading, First Republic Bank advanced more than 20%, rebounding from a slump to a record low as investors weighed a proposal from JPMorgan to help the struggling mid-size lender. Meta Platforms Inc. rose after Morgan Stanley raised its recommendation to overweight from equal-weight. Here are some of the other notable premarket movers:

First Republic Bank jumps as much as 27% in premarket trading, set to rebound after closing at a record low Monday, as investors digest a proposal from JPMorgan to help the struggling midsize lender. Shares in fellow regional banks also gain on Tuesday, with Western Alliance (WAL US) +3.9%, PacWest Bancorp (PACW US) +4.9%

Meta rises 2.5% after Morgan Stanley raised its recommendation to overweight from equal-weight, citing the social media giant’s pivot to increased efficiency.

First Majestic Silver drops 16% in US premarket trading after saying it’s temporarily suspending all mining activities and reducing its workforce at Jerritt Canyon effective immediately.

Keep an eye on Emerson Electric as it was upgraded to overweight from equal-weight at Morgan Stanley, which noted the drop in the US electrical-equipment maker’s stock after it announced its bid for National Instruments.

Investors are tiptoeing back into riskier assets, reversing the knee-jerk selloff early Monday that followed a government-brokered takeover of Credit Suisse Group AG at the weekend by Swiss rival UBS Group AG. Banks’ Additional Tier 1 bonds rebounded in Europe and Asia after euro-zone and UK regulators gave reassurances on the risky debt category, which seized up after Credit Suisse shareholders took precedence over the holders of over $16 billion of the AT1s. Appetite for risk is also being fueled by expectations that the Federal Reserve may adopt a more cautious policy approach when it decides on interest rates on Wednesday.

“The resolution to the Credit Suisse situation has managed to calm markets down, though in the US, all eyes remain on First Republic Bank and whether it needs another show of support from major banks,” said Joachim Klement, head of strategy, accounting and sustainability at Liberum Capital. “If the Fed can calm markets down tomorrow, a longer-lasting rally in equity markets is on the cards.”

“About 10 days ago we had a series of risks emerge and now one by one, those tail risks are diminishing,” said Erick Muller, head of investment strategy at asset manager Muzinich & Co. Ltd. “It seems like everything has been put in place to resolve any liquidity issues — which is reassuring.”

The latest BofA fund manager survey showed investors now view a systemic credit event as the biggest tail risk to markets, followed by elevated inflation and hawkish central banks. Strategist Michael Hartnett recommended selling the S&P 500 above 4,100 to 4,200 points — between 3.8% and 6.3% higher than current levels.

Money markets are wagering on a hike of around a quarter-point as the cracks that emerged in the global banking industry discourage more aggressive tightening. Swap traders now see the Fed’s benchmark rate ending the year around 4%, while two weeks ago investors were betting on rates peaking close to 6%.

“It is possible that some central bankers will see recent events as policy finally getting some traction and tightening financial conditions via forcing markets to price in greater credit risk,” Mizuho International Plc strategists including Evelyne Gomez-Liechti wrote in a note. “This would allow central bankers to do a little less with policy rates.”

European markets rise for a second day as concerns around the health of the banking sector ease and investors look ahead to this week’s central-bank rate decisions while the demise of Credit Suisse appears to be in the rear-view mirror for investors who have piled back into European bank stocks. The Stoxx Banks Index is up 4.5% as most lenders saw their AT1 notes rebound from Monday’s sharp sell off. The Stoxx 600 is up 1.5%, with banks and insurance stocks leading gains, while consumer staples trail. Here are some of the biggest European movers:

Kingfisher shares rise as much as 3.4% after the UK home- improvement retailer reported FY pretax profit that beat estimates and said it plans to announce a new buyback program

Santander gains as much as 4.8%, Deutsche Bank 4.6% and Commerzbank 7.2% as concerns around the banking system ease following UBS’s rescue deal for Credit Suisse

RWE climbs as much as 3.2% after the German energy company reported new guidance and a higher dividend ahead of estimates

Nordea shares rise as much as 3.6% after Barclays upgraded the bank to overweight, though is cautious given Nordic banks’ vulnerability to deposit outflows and funding costs

Axfood gains as much as 5.7%, the most since June 2022, as both DNB and Carnegie upgrade the Swedish food retailer and wholesaler to buy from hold

Thyssenkrupp climbs as much as 5.9% after a report that CVC is considering offering €1 for the German industrial firm’s steel unit

Rockwool bounces as much as 5.5% as DNB upgrades the Danish insulation supplier to buy from hold, saying it thinks the firm’s margin guidance is “overly cautious”

Earlier in the session, Asian stocks gained as concerns of an escalation in the banking crisis eased, with lenders helping drive the day’s advance. The MSCI Asia Pacific excluding Japan Index climbed as much as 1%, with Tencent, TSMC and AIA Group providing the biggest boosts among individual stocks. Japan was closed for a holiday. Financial stocks lent the most support among sub-indexes to the regional benchmark, which traded close to its 200-day moving average. Sentiment was helped by a rebound in riskier Additional Tier 1 bonds sold by banks in the region, along with news that US officials are studying ways to temporarily guarantee all bank deposits if the turmoil expands.

“Whenever there is bad news on individual banks, governments and big global banks are responding immediately, helping markets find a bottom,” analysts at Shinhan Investment Corp. wrote in a note. Benchmarks in Hong Kong and China advanced more than 1% to lead a regional rebound. The Hang Seng Tech Index gained 2.5% as Tencent climbed ahead of its earnings release. Korean stock gauges rose after China approved more foreign online game titles, fueling a rally among related stocks. Investors are waiting for the Fed’s monetary policy decision, due early Thursday in Asian hours, with expectations that the US central bank will refrain from an aggressive interest rate increase. Pershing Square’s Bill Ackman said the Fed shouldn’t raise its benchmark rate.

In Australia, the S&P/ASX 200 index rose 0.8% to close at 6,955.40, buoyed by a rebound in banks and mining shares. The rise comes following gains on Wall Street as immediate concerns over the global financial system dissipated. Australia’s central bank will consider pausing its policy tightening cycle next month, given that interest-rate settings are already restrictive and the economic outlook is uncertain, minutes of its March meeting showed. In New Zealand, the S&P/NZX 50 index fell 0.3% to 11,531.30.

Stocks in India rose, helped by a recovery in lenders who posted their biggest gains in two weeks as investors chose to look beyond the ongoing banking crisis and chase pockets of value. Tata Consultancy Services, the country’s biggest software exporter, slumped for a ninth straight session. This was the stock’s longest losing streak since November 2007, triggered by a surprise change in its top leadership. Meanwhile, the turmoil in US and European banks continued to dent the appeal for information technology service providers. The S&P BSE Sensex Index rose 0.8% to 58,074.68 in Mumbai, while the NSE Nifty 50 Index advanced 0.7%. The gauges have now risen for three of the last four sessions but slipped more than 4% over the last one month as global equities remained under pressure on concerns of slowing growth and higher rates. The 50-stock Nifty gauge is now trading at 17.3 times its members’ estimated earnings for the next 12 months – the lowest in one year – and near its 10-year average, according to data compiled by Bloomberg.

In FX, the Dollar Index is flat after a three-day fall. The New Zealand dollar is the weakest among G-10 currencies, followed by the Japanese yen. The euro advanced to the strongest level in five weeks and short-end German bonds extended a drop as concerns about contagion in the European banking sector eased further following the rescue deal of Credit Suisse Group AG over the weekend. EUR/USD rose as much as 0.5% to 1.0770, the highest since Feb. 14.

In rates, the improving market sentiment dented government bonds and treasuries extend declines led by the short-end as US stock futures gain and money markets add to Fed tightening wagers ahead of Wednesday’s policy decision. Losses across the curve are led by an aggressive bear-flattening move in bunds, with 2-year German yields nearly 21bp higher on the day to 2.57% as traders also bet the ECB will raise rates again in May. The US 2-year yield rises 11bps to 4.09% while its 10-year peer climbs 5bps to 3.54%, flattening the 2s10s curve 6bps to -56bps. Traders bet on 20bps of Fed hikes this week and add as much as 17bps to tightening expectations this year. The US session includes 20-year bond auction reopening at 1pm, while a $15b 10-year TIPS sale is slated for Thursday. WI 20-year yield near 3.875% is around 10bp richer than last month’s, which tailed by 0.2bp. Cash trading was closed in Tokyo for a Japanese holiday.

In commodities, crude futures rose for a second day with WTI rising 1.3% to trade near $68.50 after swinging in a $3-plus range on Monday. Traders are starting to return to risk markets after authorities stepped in to shore up the financial system. US officials are also studying ways they might temporarily expand protection for all deposits. Spot gold falls 0.6% to around $1,697. Bitcoin gains 0.4%.

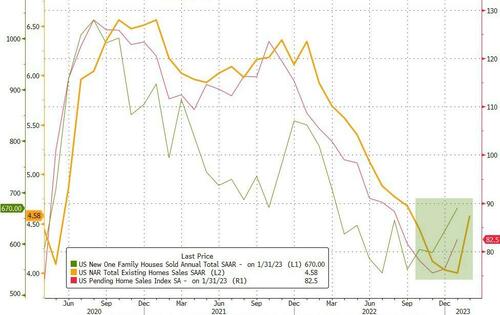

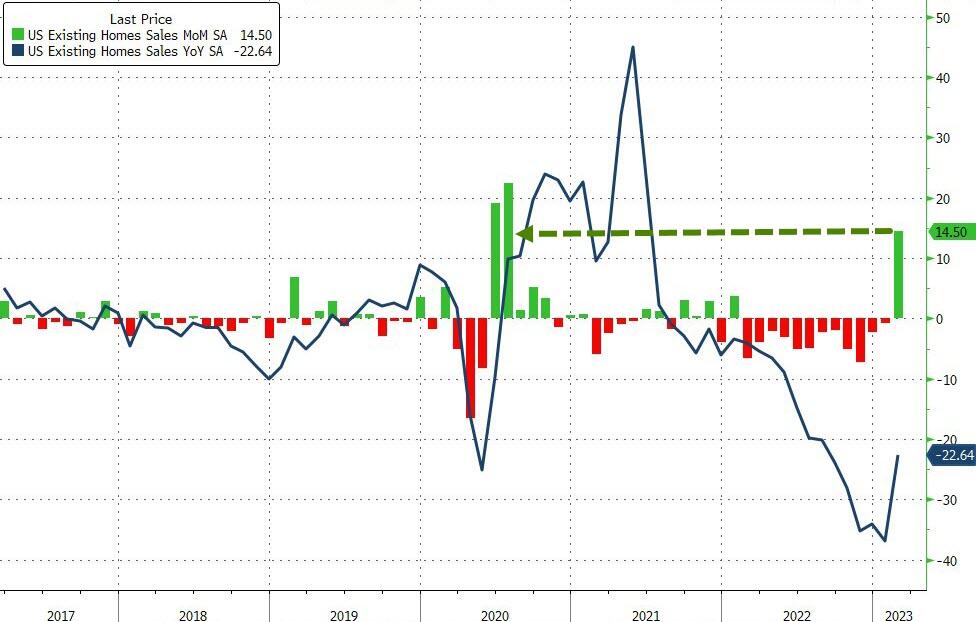

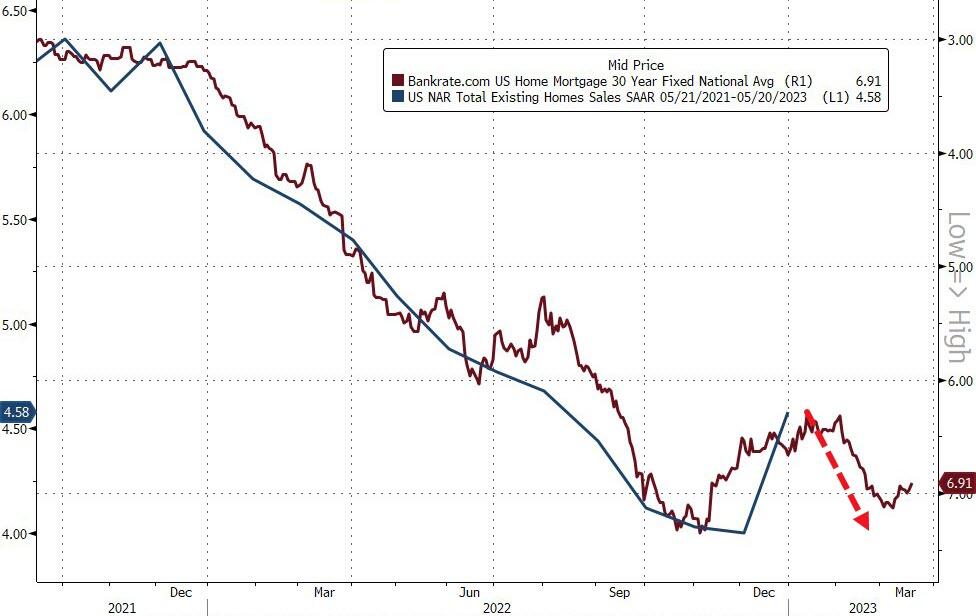

To the day ahead now, we get the US existing home sales for February and the latest Philly Fed non-mfg survey. From central banks, we’ll hear from the ECB’s Lagarde and Villeroy, whilst the two-day FOMC meeting will be getting underway ahead of tomorrow’s decision. Lastly, earnings releases include Nike.

Market Snapshot

Australia’s central bank will consider pausing its policy tightening cycle next month, given interest-rate settings are already restrictive and the economic outlook is uncertain, minutes of its March meeting showed. BBG

Vanguard will shut its remaining business in China after a partial retreat two years ago, people familiar said. It will shut the Shanghai unit and exit a robo-advisory joint venture with Ant Group. The reversal comes as rivals including BlackRock and Fidelity strive to build up local operations as China’s recovery and a pension reform brighten prospects. BBG

UBS relies more on AT1 bonds for its capital than any other major lender in Europe. AT1s are the equivalent of about 28% of its highest quality regulatory capital, Bloomberg calculations show, just slightly more than for Barclays. The average exposure among the 16 biggest banks in Europe is about 16%. BBG

Financial market turmoil may do some of the ECB’s work for it if it dampens demand and inflation, ECB President Christine Lagarde said on Monday. “Clearly financial stability tensions might have an impact on demand and might actually do part of the work that would otherwise be done by monetary policy and interest rate hikes,” Lagarde told European lawmakers. RTRS

The Federal Home Loan Bank System issued $304 billion in debt last week, according to a person familiar with the matter, who asked not to be identified discussing non-public data. That’s almost double the $165 billion that liquidity-hungry lenders tapped from the Federal Reserve. BBG

US officials are studying ways they might temporarily expand FDIC coverage to all deposits, a move sought by a coalition of banks arguing that it’s needed to head off a potential financial crisis. BBG

The jobs market may not be as robust as it seems as many job postings are “fake”, with the prospective employer having no intention of immediately filling the position in question. WSJ

US accounting rulemakers are being urged to rethink how banks should value their assets in financial statements, in the wake of the run on Silicon Valley Bank and pressure across the regional banking sector. Advocates of “fair value” accounting are urging the Financial Accounting Standards Board to force banks to recognize unrealized losses on securities such as those held by SVB, even when management insists they will never have to be sold. FT

Wall Street bank chief executives are trying to come up with a new plan for First Republic after a $30bn lifeline failed to arrest a sharp sell-off in the lender’s shares. The executives will discuss if anything more can be done for the California-based lender on the sidelines of a pre-planned gathering in Washington on Tuesday, which is being organized by the Financial Services Forum, one of the main industry lobby groups. FT

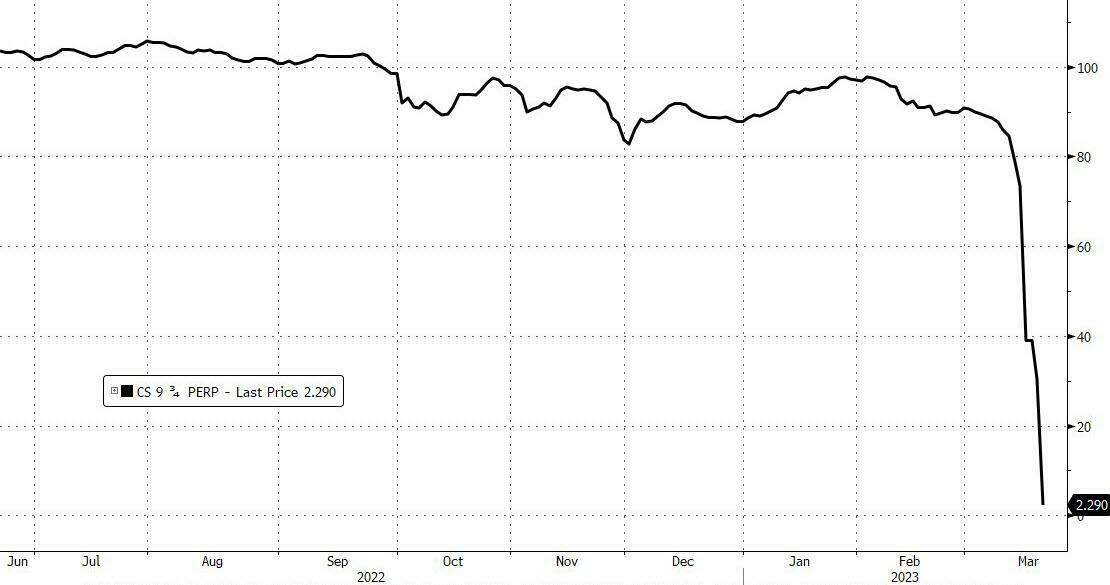

Pacific Investment Management Co. and Invesco Ltd. are among the largest holders of Credit Suisse’s so-called Additional Tier 1 bonds that have been wiped out after the bank’s takeover by UBS Group AG: BBG

First Republic Bank shares rallied in US premarket trading after falling to a record low Monday, as investors ponder what’s next for the struggling midsize lender following an offer of help from JPMorgan Chase & Co: BBG

Top Overnight News

S&P 500 futures up 0.9% to 4,018

MXAP up 0.5% to 156.40

MXAPJ up 1.0% to 504.24

Nikkei down 1.4% to 26,945.67

Topix down 1.5% to 1,929.30

Hang Seng Index up 1.4% to 19,258.76

Shanghai Composite up 0.6% to 3,255.65

Sensex up 0.7% to 58,035.99

Australia S&P/ASX 200 up 0.8% to 6,955.40

Kospi up 0.4% to 2,388.35

STOXX Europe 600 up 1.2% to 446.06

German 10Y yield little changed at 2.18%

Euro up 0.1% to $1.0734

Brent Futures up 0.7% to $74.28/bbl

Gold spot down 0.6% to $1,967.56

U.S. Dollar Index little changed at 103.35

A more detailed look at global markets

Asia-Pac stocks mostly tracked the gains on Wall St where some of the banking sector jitters dissipated following the Credit Suisse rescue and amid hopes FDIC’s deposit insurance amount could be increased. ASX 200 was led by outperformance in energy, financials and the mining-related sectors, while the RBA Minutes from the March meeting noted that the Board agreed to reconsider the case for pausing at the April meeting. Nikkei 225 was closed as Japanese participants observed the Vernal Equinox holiday. Hang Seng and Shanghai Comp. gained as Hong Kong benefitted from strength in consumer stocks and the mainland was buoyed by the PBoC’s liquidity injection albeit with upside capped on higher money market rates.

Top Asian News

China is giving chipmakers new powers to guide a recovery in the industry with a handful of China’s most successful chip companies to get easier access to subsidies and more control over state-backed research, according to FT.

RBA March Minutes said the Board agreed to reconsider the case for pausing at the April meeting and that a pause would allow time to reassess the outlook for the economy, while it added that further tightening of monetary policy is likely required to lower inflation. RBA noted monetary policy was in restrictive territory and the economic outlook was uncertain, while these considerations meant that it would be appropriate at some point to hold the cash rate steady to assess more fully the effect of the interest rate increases to date. Furthermore, it said inflation is too high, the labour market is tight, business surveys are solid and sluggish productivity could lead to more persistent inflation.

European bourses are firmer on the session, Euro Stoxx 50 +1.7%, as the region continues the positive APAC handover with specific banking-sector updates slim. Sectors are all in the green with Banking names the outperformer, SX7P +3.5%, and back at Friday’s best levels; albeit, the index has someway to go to recoup the pressure of recent days/weeks. Stateside, futures are similarly in the green though magnitudes are much more contained as participants await updates to First Republic (FRC) and the FDIC ahead of Wednesday’s FOMC, ES +0.6%.

Top European News

The Times shadow monetary policy committee urges the BoE to continue raising interest rates this week. Two members said the Bank should stick to 50bps, five said 25bps and one said unchanged.

ECB’s Kazaks said uncertainty in financial markets is high and it is not possible to say that we have stopped hiking, while he added that European banks are well capitalised and financial resources are available, according to Bloomberg.

ECB’s de Cos says he cannot validate the markets expectation of a 3.25% peak rate, via Expansion.

Swiss KOF: Inflation forecast at 2.6% (prev. 2.3%) and 1.5% (prev. 1.1%) in 2023 and 2024. Click here for more detail.

Bank headlines

US officials are examining ways to permit the FDIC to temporarily insure deposits beyond the current USD 250k cap on most accounts without the need for congressional approval, according to Bloomberg. There were also earlier reports that the House Freedom Caucus is against raising bank deposit guarantees.

US banking executives are to discuss at a Financial Services Forum event on Tuesday the next steps for First Republic (FRC), via FT citing sources.

Swiss Banking Association says Swiss banking credibility has not been destroyed by the Credit Suisse (CSGN SW) crisis, but the situation is not good.

ESMA Chair says reforms to make money market funds more resilient to economic shocks are needed sooner rather than later.

Australia’s prudential regulator has begun asking banks to declare their exposures to start-ups and crypto-focused ventures following the collapse of Silicon Valley Bank and volatility at global lenders, according to AFR.

FX

The DXY is underpressure as the risk tone takes a more constructive tilt, with the index at the low-end of 103.24-103.51 parameters.

Amidst this, the EUR is the marginal outperformer as the single currency extends above 1.07 though has seemingly paused for breath at 1.0750 with specific catalysts thin.

Next best is the CHF, though this is more a recuperation of recent depreciation than any concerted upward move vs the USD while EUR/CHF is essentially flat, given the EUR’s relative strength.

Antipodeans are at the bottom of the G10 pile following data and RBA minutes which suggested that a pause could occur in April, currently AUD/USD and NZD/USD are below 0.67 and 0.62.

Additionally, given the above, the JPY has pared back much of Monday’s haven allure with USD/JPY around 25pips shy of Monday’s 132.64 high at best.

PBoC set USD/CNY mid-point at 6.8763 vs exp. 6.8753 (prev. 6.8694)

Fixed Income

Bonds extend retreat from Monday’s lofty safe haven peaks as risk appetite continues to pick up amidst less financial sector stress.

Bunds down to 136.62 vs yesterday’s 140.30 Eurex best, Gilts to 104.65 from 107.33 and T-note 114-18+ compared to 116-24.

Solid 2053 DMO issuance provides UK debt with little support and 20 year US supply still to come.

Commodities

WTI and Brent are firmer in-fitting with the risk sentiment seen in European trade and with the complex attentive to commentary from Goldman Sachs, among others.

Specifically, the benchmarks are towards the top-end of USD 66.77-68.500/bbl and USD 72.82-7466/bbl parameters respectively.

Spot gold is softer given the relatively constructive tone with the yellow metal retreating further from Monday’s USD 2009/oz peak to USD 1963/oz at worst while base metals are benefitting from broader action and reports relating to China’s steel output.

Goldman Sachs’ Commodities Head Currie sees upside of USD 5-10/bbl for crude, saying a Fed pause would be bullish for oil.

Trafigura says they do not see major impact on industry from Credit Suisse (CSGN SW); current oil prices are not encouraging production. Still moving limited Russian refined products and considering whether to resume more Russian oil trade, CEO does not see much downside for oil at this point. Adds, that the existing LME Nickel contract is not fit for purpose.

Gunvor Co-head of trading says with all these new refineries coming on stream, we are not very bullish on refined products down the road; does not think oil price can go over USD 100/bbl by December.

Pierre Andurand of Andurand Capital sees oil price at USD 140/bbl at year end.

TotalEnergies (TTE GP) Normandy refinery (250k BPD) is to be shutdown amid strike action, according to a statement.

Norwegian oil production (Feb) 1.776mln BPD (vs. prev. M/M 1.754mln BPD), gas production 9.9bcm (vs. prev. M/M 11.1mln BPD).

China is reportedly considering cutting 2023 crude steel output by circa. 2.5%, via Reuters citing sources.

Geopolitics

Chinese President Xi said China will continue to play a constructive role in promoting a political settlement of the Ukraine crisis, while President Xi told Russian President Putin that ties with Russia are China’s strategic choice.

Chinese President Xi has invited Russia President Putin to visit China, via Ria. Subsequently, Russia’s Kremlin says Putin and Xi had a throughout exchange on Monday including on Chinese peace proposal for Ukraine, declined to give more details.

Iran is interested in developing peaceful nuclear and renewable energy cooperation with Russia, according to RIA.

Japanese PM Kishida said he will visit Kyiv and meet with Ukrainian President Zelensky, according to NHK. It was later reported that Japan’s Ministry of Foreign Affairs said Japan and Ukraine leaders will hold a summit today.

South Korea imposed sanctions on four individuals and six entities linked to North Korea’s weapons programmes, while it announced a watch list to ban the export of items related to North Korea’s satellite development, according to Reuters.

US Event Calendar

08:30: March Philadelphia Fed Non-Manufactu, prior 3.2

10:00: Feb. Existing Home Sales MoM, est. 5.0%, prior -0.7%

10:00: Feb. Home Resales with Condos, est. 4.2m, prior 4m

DB’s Jim Reid concludes the overnight wrap

Morning from what promises to be a very sunny warm day in Lisbon which makes a nice change from the rain in London as I left yesterday as we hit the first official day of spring. Like the seasons, it did feel like a new beginning for markets as they finally saw some positivity in the UBS-Credit Suisse deal after an open that felt like we might be in an ice age rather than starting to see green seasonal shoots.

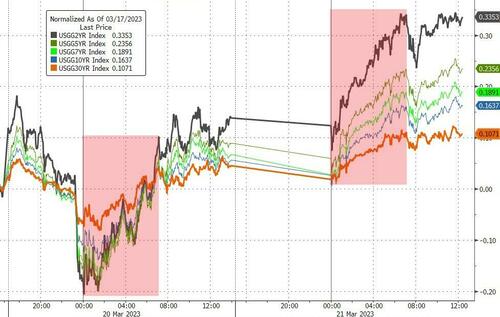

It’s worth looking at how bad the open was yesterday and why it turned around. The STOXX 600 fell by almost -2% within 20 minutes of the opening bell, whilst UBS was down almost -16% with European bank AT1s down around 10-15%. It was a similar story on the rates side too, since the 10yr Treasury yield hit its lowest intraday level in over 6 months, at just 3.286% (-14.3bps at that point).

It all turned when we got a statement from the European Banking Authority that explicitly set out that the EU’s practice was that “common equity instruments are the first ones to absorb losses”, and that “only after their full use would Additional Tier One be required to be written down”. A similar statement was then issued by the Bank of England, which said that the UK’s bank resolution framework “has a clear statutory order” as used in the case of SVB UK, which prioritised AT1 ahead of CET1. With that reassurance, AT1s recovered somewhat over the session and we saw a broader boost in bank stocks across the board.

In more detail, Euro Sub-Financial CDS was as much as +46bps wider on the open yesterday before closing -13bps tighter overall, while the senior index was +18bps wider just after the open before finishing -12bps tighter by the end of trading. The STOXX Banks index advanced +1.97% (from -6.61% at the early lows), as all 19 of the 23 members moved higher on the day.

This was an extremely important announcement as most financial investors felt very uncomfortable with the details of the Swiss merger and what it did for AT1 bondholders rights in the resolution pecking order. The EU/UK clarity was a very good move and net net probably helps the European economy longer-term as to permanently increase the cost of bank capital would be counterproductive. As we’ve shown for the last few days, CS was massively decoupled from the rest of the European banking sector in CDS terms over the last several months, so whilst harder times are to come economically, this announcement and the prior fairly stable European banking system outside of CS, should cut off contagion risks.

US banks have a few more issues to deal with still though and although the KBW Banks index was up +0.79% on the day, they were as much as +2.4% higher before selling off steadily after Europe went home.

This came as concerns continue to percolate regarding US bank First Republic, even after last week’s move by other US banks to deposit $30bn. S&P cut their credit rating to B+ from BB+ over the weekend and yesterday saw their shares end the day down -47.08%, which builds on a decline of more than -80% already over the previous two weeks. There was a short intraday rally after the Wall Street Journal reported that JPMorgan CEO Jamie Dimon was leading discussions with other CEOs to stabilise First Republic, which could involve some or all of the $30bn in deposits being converted into a capital infusion. Despite these headlines, the stock reverted lower to finish near the lows of the day.

Overnight, it was reported that US officials at the Treasury Department and FDIC were studying ways to temporarily expand their deposit coverages in case the current situation expands into a full-blown crisis of confidence. The White House was looking into whether federal regulators would be able to increase the $250k cap without an act of Congress as headlines suggest Republicans would oppose the move.

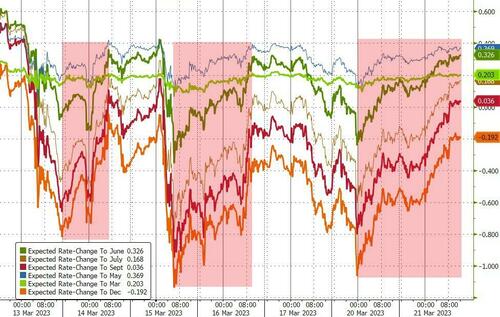

Aside from the First Republic issues, the more positive shift in sentiment saw investors put growing weight on the probability of the Fed hiking rates tomorrow. For instance, shortly after the European open when everything had slumped, just 9bps worth of hikes were being priced in by futures. But that bounced back over the rest of the session, and by the close a 17.8bps hike was priced in, which is equivalent to a 71.2% probability. So for the time being at least (and clearly things are subject to change in these conditions), it would still be a surprise relative to expectations if the Fed didn’t go ahead.

Last night, our own US economists published their preview of tomorrow’s Fed meeting (link here), and they agree with the view that the Fed will opt for 25bps. Our economists expect the Fed to follow the ECB’s lead and raise rates in line with expectations, do away with forward guidance, but signal a continued tightening bias. They do not expect much change to the dot plot or the SEP from December, and Powell will also likely emphasise the heightened uncertainty surrounding those forecasts in his press conference.

Those expectations of a Fed hike meant that yields posted a small increase yesterday, with the 10yr Treasury yield ending the day up +5.6bps at 3.485%. As with bank stocks though, that only came after a big turnaround earlier in the session, having recovered by nearly +20bps from their intraday low of 3.286%. It was much the same story in Europe too, with the 10yr bund yield up from a low of 1.91% after the open before closing at 2.125%, leaving it up by a net +1.7bps over the day.

For equities it was also a positive session, at least once we got past the European morning. By the close, the STOXX 600 had advanced +0.98%, capping off a turnaround of almost +3% on an intraday basis from the initial lows. And over in the US, the S&P 500 was up +0.89%, which now leaves it down by just -1.01% since its close on March 8 before the concerns about SVB really took hold. Tech stocks were the main underperformer yesterday, with Software (-0.8%) the worst-performing industry, but even so the NASDAQ still gained +0.39%.

This morning in Asia a cautious rally continues. As I check my screens, the Hang Seng (+0.33%), the KOSPI (+0.30%), the CSI (+0.42%) and the Shanghai Composite (+0.15%) are trading in positive territory. Elsewhere, markets in Japan are closed for a holiday with Treasuries not trading overnight.

In central bank news, the minutes from the Reserve Bank of Australia’s recent meeting were less hawkish as the central bank indicated a near-term pause in interest rate increases at its upcoming policy meeting scheduled on April 4th, as uncertainty surrounding the economic outlook persists. In response to the RBA meeting minutes, the Australian dollar rose to a high of 0.6726 versus the US dollar before settling at $0.6687 as we go to press. Meanwhile, 10yr government bonds rallied with yields dropping -4bps to 3.20% as I type.

Amidst all the financial news, one more positive story in the background for consumers (albeit for negative return reasons) has been the continued decline in commodity prices. For instance, European natural gas futures (-8.24%) closed at a 19-month low of €39.325 per megawatt-hour yesterday, which brings their decline over March so far to -15.73%. Oil prices were under pressure for most of the day before a late rally in the US left Brent crude up +1.12% to $73.79/bbl and WTI contracts were up +1.35% to $67.64/bbl. Both contracts reached their lowest level since December 2021 intraday. Overall the recent drop in energy prices will benefit consumers, as well as central banks since it’ll offer them a helpful tailwind on the inflation side. On the other hand, it’s worth noting that much of the decline is thanks to growing concerns about a recession, with oil traditionally being a more cyclical commodity in those circumstances.

To the day ahead now, and data releases include the German ZEW survey for March, Canada’s CPI for February, and US existing home sales for February. From central banks, we’ll hear from the ECB’s Lagarde and Villeroy, whilst the two-day FOMC meeting will be getting underway ahead of tomorrow’s decision. Lastly, earnings releases include Nike.

AND NOW NEWSQUAWK (EUROPE/REPORT)

Constructive APAC sentiment continues with focus on FRC, FDIC and FOMC – Newsquawk US Market Open

TUESDAY, MAR 21, 2023 – 06:57 AM

Sentiment remains constructive in Europe after a similar APAC handover with specific European-banking drivers limited.

Stateside, the tone is in-fitting but to a slightly lesser extent awaiting updates to First Republic and the FDIC before Wednesday’s FOMC.

DXY has been pressured by the tone, with JPY giving back Monday’s gains while the CHF attempts to recover.

EGBs & USTS continue to pullback from earlier haven-induced peaks with well-received UK supply having little impact

Commodities are, generally, benefitting from the risk tone; though, spot gold continues to retreat from Monday’s USD 2009/oz peak

Looking ahead, highlights include Canadian CPI, Retail Sales, US Existing Home Sales, Xi & Putin (2/3), Speeches from ECB’s Lagarde & Enria, Supply from the US.

Or why not try Newsquawk’s squawk box free for 7 days?

BANKS

US officials are examining ways to permit the FDIC to temporarily insure deposits beyond the current USD 250k cap on most accounts without the need for congressional approval, according to Bloomberg. There were also earlier reports that the House Freedom Caucus is against raising bank deposit guarantees.

US banking executives are to discuss at a Financial Services Forum event on Tuesday the next steps for First Republic (FRC), via FT citing sources.

Swiss Banking Association says Swiss banking credibility has not been destroyed by the Credit Suisse (CSGN SW) crisis, but the situation is not good.