March 22, 2023 · by harveyorgan · in Uncategorized · Leave a comment·Edit

Mar 23 2023 · by harveyorgan · in Uncategorized · Leave a comment·Edit

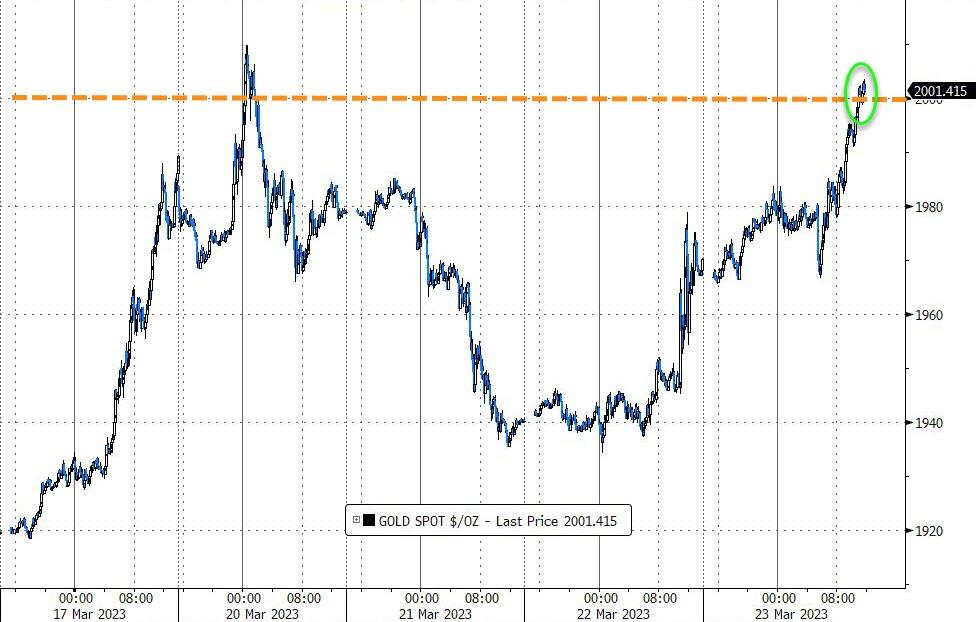

GOLD PRICE CLOSED: UP $47.70 at $1996,40

SILVER PRICE CLOSED: UP $0.62 to $23.11

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1993.70

Silver ACCESS CLOSE: 23.11

Bitcoin morning price:, $28,156 UP 9 Dollars

Bitcoin: afternoon price: $28,185 UP 38 dollars

Platinum price closing $982,60 UP $8.55

Palladium price; closing $1462.30 UP $70.50

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,732 50 UP 30 CDN dollars per oz (ALL TIME HIGH 2732.50

BRITISH GOLD: 1622,30 UP 18 pounds per oz//(ALL TIME HIGH//1629.84)

EURO GOLD: 1839,95 UP 27,83euros per oz //(ALL TIME HIGH//1860.82)

COMEX DATA EXCHANGE: COMEXEXCHANGE: COMEX

CONTRACT: MARCH 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,946.800000000 USD

INTENT DATE: 03/22/2023 DELIVERY DATE: 03/24/2023

FIRM ORG FIRM NAME ISSUED STOPPED

435 H SCOTIA CAPITAL 23

624 H BOFA SECURITIES 12

737 C ADVANTAGE 1 4

905 C ADM 38

TOTAL: 39 39

MONTH TO DATE: 5,192

JPMORGAN stopped 7/180 contracts

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR MAR/2023. CONTRACT: 39 NOTICES FOR 3900 OZ or 0.1213 TONNES

total notices so far: 5192 contracts for 519200 oz (16.149 tonnes)

SILVER NOTICES: 3 NOTICE(S) FILED FOR 15,000 OZ/

total number of notices filed so far this month : 3146 for 15,730000 oz

END

GLD

WITH GOLD UP $$47.70

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/SMALL CHANGES IN GOLD INVENTORY AT THE GLD:////// A SMALL DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD//

INVENTORY RESTS AT 925.42 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 62CENTS

AT THE SLV// SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF OF 0.919 MILLION OZ FROM THE SLV: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 459.485 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A FAIR SIZED 496 CONTRACTS TO 119,578 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.34 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. WITH TODAY’S READING AT THE COMEX, WE HAVE NOW SET ANOTHER RECORD LOW AT 119,126 CONTRACTS , MARCH 22.2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.34). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A HUGE GAIN ON OUR TWO EXCHANGES 1017 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 1 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS( 521 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.58 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S E<F>P>JUMP TO LONDON OF 180,000 OZ//NEW STANDING: 15.750 MILLION OZ + THE 1.0 MILLION OZ OF EXCHANGE FOR RISK//THUS TOTAL NEW STANDING 16.750MILLION OZ/ //// V) STRONG SIZED COMEX OI GAIN/ STRONG SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –44 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTRACTS for 17 days, total 13,274contracts: OR 66 370 MILLION OZ . (7980CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 66 370MILLION OZ

.

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 66.370 MILLION OZ//INITIAL//STRONG ISSUANCE BUT BELOW LAST MONTH

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 496 CONTRACTS WITH OUR $0.34 GAIN IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 521 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAR OF 15.58 MILLION OZ//FIRST DAY NOTICE// FOLLOWED BY TODAY’S 180,000 OZ EFP JUMP TO LONDON (WHICH INCREASES THE AMOUNT OF SILVER STANDING) + 1.0 MILLION OF EXCHANGE FOR RISK ISSUED EARLY IN MARCH (INCREASES THE AMOUNT OF SILVER STANDING) //NEW STANDING 16.750MILLION OZ .. WE HAVE A HUGE SIZED GAIN OF 1017OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 3 NOTICE(S) FILED TODAY FOR 15,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 554 CONTRACTS TO 470,428 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED-3517 CONTRACTS. (huge)

WE HAD A SMALL SIZED INCREASE IN COMEX OI ( 10,262 CONTRACTS) WITH OUR $10.10 GAIN IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR MAR. AT 4.9953 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 4300 OZ (0.133TONNES) //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London).

YET ALL OF..THIS HAPPENED WITH OUR $10.10 GAIN IN PRICE WITH RESPECT TO TUESDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 2698 OI CONTRACTS (8,3119 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2144 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 470,428

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2698 CONTRACTS WITH 6554 CONTRACTS INCREASED AT THE COMEX AND 2144 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2698 CONTRACTS OR 8 3919 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2144 CONTRACTS) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (554) TOTAL GAIN IN THE TWO EXCHANGES 2698 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR MAR. AT 4.9953 TONNES FOLLOWED BY TODAY’S 4300 OZ QUEUE JUMP//NEW STANDING 16.4199 TONNES // ///3) zero LONG LIQUIDATION //4) SMALL SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

TOTAL EFP CONTRACTS ISSUED: 73,936 CONTRACTS OR 7,393,600 OZ OR 229.97 TONNES IN 16 TRADING DAY(S) AND THUS AVERAGING: 4487 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES 229.27 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 229.26/3550 x 100% TONNES 6.82% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 229.82 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A STRONG SIZED 1496CONTRACTS OI TO 119,082 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 119,082 CONTRACTS TODAY, MARCH 22/2022

EFP ISSUANCE 521 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 521 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 521 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 496 CONTRACTS AND ADD TO THE 521 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE GAIN OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1017 CONTRACTS.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES //5.0855MILLION OZ

OCCURRED DESPITE OUR $0.15 GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

i)WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED UP 20.90 PTS OR 0.64% //Hang Seng CLOSED UP 162.12 PTS OR 2.95% /The Nikkei closed DOWN 47,08 PTS OR 0.17% //Australia’s all ordinaries CLOSED down 0.67% /Chinese yuan (ONSHORE) closed up 6.8189//OFFSHORE CHINESE YUAN up TO 6.8169/ /Oil UP TO 71.13 dollars per barrel for WTI and BRENT AT 76.84 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING BELOWLEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 554CONTRACTS UP TO 470,428 WITH OUR GAIN IN PRICE OF $10.10 ON TUESDAY

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAR… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2144 EFP CONTRACTS WERE ISSUED: : APRIL 2144 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2144 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR TOTAL OF 2,698 CONTRACTS IN THAT 2144 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED GAIN OF 554 COMEX CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $10.10. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A FAIR AMOUNT OF GOLD TONNAGE STANDING: MAR (16.1648) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 16.4199 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $10.10) //// AND WERE SUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD OUR FAIR SIZED GAIN OF 2698CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 8.319 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAR. (4.9953 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 4300 OZ (0.1227TONNES)… ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $38.70

WE HAD -3517 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 2698 CONTRACTS OR 269,800OZ OR 8.3919TONNES

TONNES

Estimated gold comex today 293,675// //fair

final gold volumes/yesterday 309,993///fair to good

//MARCH 23/ MARCH 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 64.30 oz Brinks 2 kilobars . |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 39 notice(s) 3,900OZ 0.1213TONNES |

| No of oz to be served (notices) | 48 contracts 4800 oz .149TONNES |

| Total monthly oz gold served (contracts) so far this month | 5192 notices 519200 16.149 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 1

i) out of BRINKS: 64.30 oz (2 kilobars)

total withdrawals: 64.30 oz

in tonnes: 0.0002 tonnes

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of MARCH we have an oi of 87 contracts having LOST 137 contracts. We had 180 notices filed on TUESDAY so we

gained 43 contracts or an additional 4300 oz will stand for metal at the comex

April LOST A CONSIDERABLE 10,121 contracts DOWN to 138,088 contracts. It is here that our banker friends have to worry as many will try and take delivery in this upcoming delivery month.

May GAINED 124 contracts to stand at 641

We had 39 notice(s) filed today for 3900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 180 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 7 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAR. /2023. contract month,

we take the total number of notices filed so far for the month (5,192 x 100 oz ), to which we add the difference between the open interest for the front month of (MAR. 87 CONTRACTS) minus the number of notices served upon today 39 x 100 oz per contract equals 527,900OZ OR 16.4199TONNES the number of TONNES standing in this active month of MARCH.

thus the INITIAL standings for gold for the MAR contract month:

No of notices filed so far (5,192x 100 oz+ 87 OI for the front month minus the number of notices served upon today (39)x 100 oz} which equals 527,900 oz standing OR 16.4199TONNES in this active delivery month of MARCH..

TOTAL COMEX GOLD STANDING: 16.4199 TONNES WHICH IS HUGE FOR AN INACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,753,544.746 OZ 54.54 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,357,630.556 OZ

TOTAL REGISTERED GOLD: 10,907,133.229 (339.25 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,450,400.876 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,153,544.746 OZ (REG GOLD- PLEDGED GOLD) 284.71 tonnes//

END

SILVER/COMEX

MAR 23/2023// THE MARCH 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 646,379.130 oz Brinks CNT JPMorgan . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 8,787,495oz Delaware |

| No of oz served today (contracts) | 3 CONTRACT(S) (15,000 OZ) |

| No of oz to be served (notices) | 22 contracts (110,000 oz) |

| Total monthly oz silver served (contracts) | 3146contracts (15,730,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i)Into Delaware: 8787.495 0z

Total deposits: 8787.495oz

JPMorgan has a total silver weight: 146.229 million oz/282.387million =51.69% of comex .//dropping fast

Comex withdrawals: 3

i) Out of CNT 20,329,880 oz

ii) Out of Brinks 1973.95 oz

iii) Out of JPMorgan; 646,379.130 oz

Total withdrawals; 646,379.130 oz

adjustments: 1 all dealer to customer

i) JPMorgan 594,561.900

the silver comex is in stress!

TOTAL REGISTERED SILVER: 36.669MILLION OZ (declining rapidly).TOTAL REG + ELIG. 282.387million oz

CALCULATION OF SILVER OZ STANDING FOR MAR

silver open interest data:

FRONT MONTH OF MAR/2023 OI: 26 CONTRACTS HAVING LOST 40 CONTRACT(S.) WE HAD 4 NOTICES FILED

YESTERDAY, SO WE LOST 36 CONTRACTS OR AN ADDITIONAL 180,000 OZ WILL NOT STAND FOR METAL ON THIS SIDE OF THE POND

April LOST 15 CONTRACTS TO STAND at 401.

May LOST 290CONTRACTS DOWN TO 95,803.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 3 for 15,000 oz

Comex volumes// est. volume today 58,091/ good//

Comex volume: confirmed yesterday: 59,885contracts ( good)

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 3146 x 5,000 oz = 15,730,000 oz

to which we add the difference between the open interest for the front month of MAR(26) and the number of notices served upon today 3x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAR./2023 contract month: 3146 (notices served so far) x 5000 oz + OI for the front month of MAR (26) – number of notices served upon today (3) x 500 oz of silver standing for the MAR. contract month equates 15.750million oz +the 1.0 million oz of exchange for risk//new total standing 16.750million oz

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

MARCH 15/THE IDES OF MARCH: WITH GOLD UP $18.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 913.27 TONNES

MARCH 14/WITH GOLD DOWN $4.75 TODAY: HUGE CHANGES: A MONSTER DEPOSIT OF 11.85 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 913.27 TONNES

MARCH 13/WITH GOLD UP $48.85 TODAY: VERY STRANGE HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY REST AT 901.42 TONNES

MARCH 10//WITH GOLD UP $31.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 903.15 TONNES

MARCH 9/WITH GOLD UP $16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 906.62 TONNES

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

FEB 28/WITH GOLD UP $12.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 917.61 TONNES

FEB 27/WITH GOLD UP $6.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.32 TONNES

FEB 24/WITH GOLD DOWN $9.10 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 917.32 TONNES

FEB 23/WITH GOLD DOWN $13.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 919.92 TONNES

FEB 22/WITH GOLD DOWN 22 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 919.92 TONNES

FEB 21/WITH GOLD DOWN $7.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 919.92 TONNES

FEB 17/WITH GOLD DOWN $1.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 921.08 TONNES

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

GLD INVENTORY: 925.42 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

MARCH 17/WITH SILVER UP 79 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE WITHDRAWAL OF 10.478 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 462.748 MILLION OZ//

MARCH 16/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 5.009 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 473.226 MILLION OZ//

MARCH 15/WITH SILVER DOWN 7 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 643,000 OZ INTO THE SLV//INVENTORY RESTS AT 478.235 MILLION OZ/

MARCH 14/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.287 MILLION OZ FROM THE SLV////INVENTORY REST AT 477.592 MILLION OZ//

MARCH 13/WITH SILVER UP $1.35 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ//

MARCH 10.WITH SILVER UP 36 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ…

MARCH 9/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.979 MILLION OZ

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWALOF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

FEB 28/WITH SILVER UP 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.241 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.188

FEB 27/WITH SILVER DOWN 15 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.471 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 482.429 MILLION OZ

FEB 24/WITH SILVER DOWN 46 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.172 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.900 MILLION OZ//

FEB 23/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.379 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.072 MILLION OZ//

FEB 22/WITH SILVER DOWN 22 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ FROM THE SLV////INVENTORY RESTS AT 485.693 MILLION OZ

FEB 21/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.5363 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 486.382 MILLION OZ//

FEB 17/WITH SILVER UP 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 827,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.819 MILLION OZ/

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 459.485MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

The Federal Reserve Is Walking A Tightrope In A Hurricane

THURSDAY, MAR 23, 2023 – 04:58 PM

Authored by Michael Maharrey via SchiffGold.com,

The Federal Reserve is trying to walk a tightrope — in a hurricane.

After rate hikes resulted in the collapse of Silicon Valley Bank and Signature Bank, the Federal Reserve and the US Treasury stepped in with a bailout. With that hole in the dam seemingly plugged for the time being, the Fed pushed forward and raised interest rates by another 25 basis points at its March meeting.

In effect, the bank bailout ended the inflation fight while allowing the Fed to continue the pretense of an inflation fight for a little while longer.

THE RATE HIKE

At its March meeting, the FOMC raised interest rates by another quarter percent. That brings the target range for the Fed funds rate to between 4.75 and 5%. It was the ninth consecutive rate increase.

The official FOMC statement asserted that the “US banking system is sound and resilient.”

It also noted that inflation “remains elevated.”

CPI came in at 6% in February. Although the CPI has ticked down in recent months, it remains closer to the 2022 highs than it does the 2% Fed target.

The FOMC statement indicated that “the Committee anticipates that some additional policy firming may be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.”

But it removed language from the statement saying the committee expects “ongoing increases” and replaced it with a line saying the committee “will closely monitor incoming information and assess the implications for monetary policy.”

This was widely viewed as a doveish indication that the Fed might be close to the end of rate hikes.

But the statement emphasized that “the Committee is strongly committed to returning inflation to its 2 percent objective.”

During the post-meeting press conference, Powell indicated that the banking crisis may actually help the Fed beat down inflation by tightening lending conditions.

Or maybe not.

It’s possible that these events will turn out to be very modest effects on the economy, in which case inflation will continue to be strong, in which case, you know, the path might look different. It’s also possible that this potential tightening will contribute significant tightening in credit conditions over time. And in principle, that means that monetary policy may have less work to do. We simply don’t know.”

The 25 basis point rate hike was widely anticipated. With price inflation still running far above the target, the Fed couldn’t plausibly pivot and end rate hikes. But make no mistake, the inflation fight ended the moment the central bank created the bank bailout program.

SOMETHING BROKE

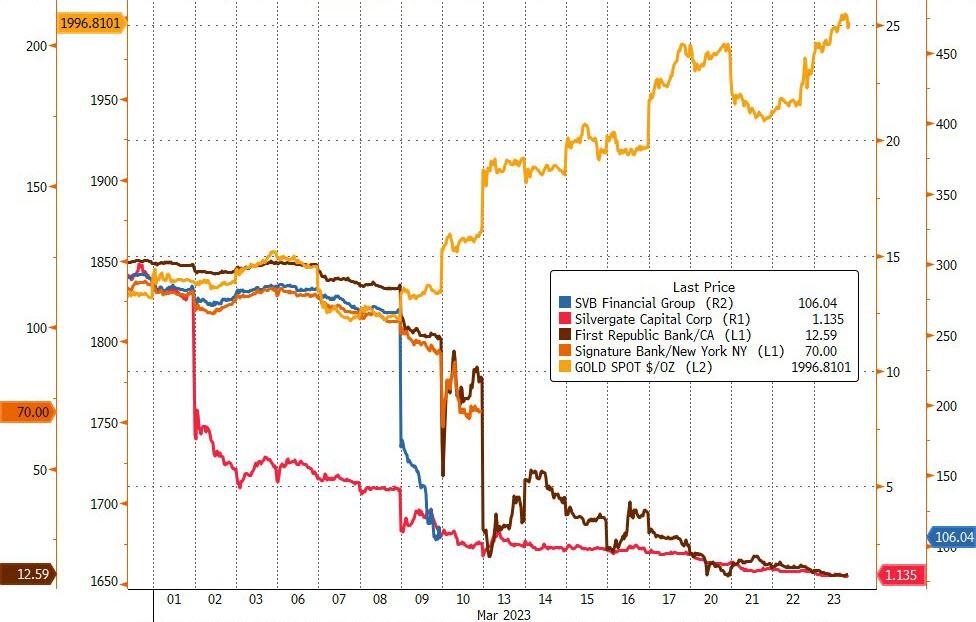

The collapse of SVB and Signature Bank were the first things to break as a result of Fed tightening.

They won’t be the last.

As I’ve been saying for months, this was inevitable. This bubble economy is built on artificially low interest rates and money creation. The Fed took some of that away when it started tightening monetary policy. In effect, the central bank has dug the foundation out from under the economy and the financial system. You can’t undermine a foundation without eventually causing the entire building to collapse.

During his post-FOMC meeting press conference, Powell tried the paint the collapse of SVB and Signature Bank as “an outlier.”

“These are not weaknesses that are at all broadly through the banking system,” Powell claimed.

This is simply false.

In fact, the collapse of SVB and Signature Bank was the tip of the iceberg. According to a Washington Post report, hundreds of banks are at risk because the Fed rate hikes have decimated the value of bonds held by these banks.

According to the Post, the capital buffer in the US banking system totals $2.2 trillion. Meanwhile, total unrealized losses in the system is between $1.7 and $2 trillion.

In other words, if banks were suddenly forced to liquidate their bond and loan portfolios, the losses would erase between 77 percent and 91 percent of their combined capital cushion. It follows that large numbers of banks are terrifyingly fragile.”

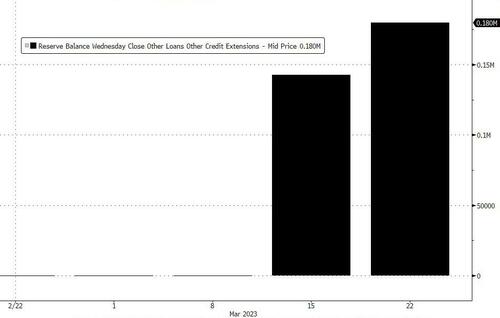

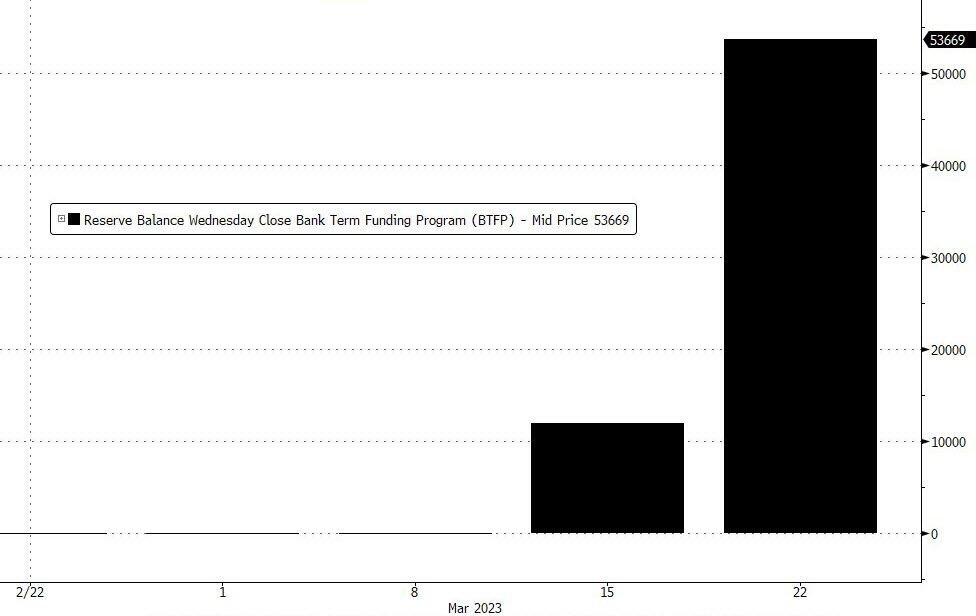

The fact that the Fed loaned banks some $300 billion in the first week of the bailout indicates the problem wasn’t “an outlier.”

KICK THE CAN DOWN THE ROAD

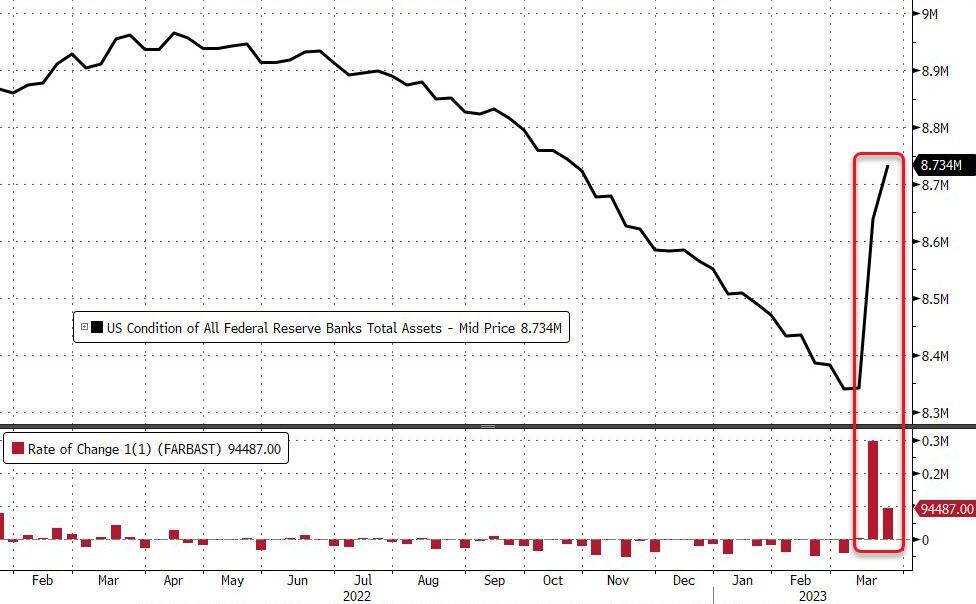

The Fed executed a shrewd move with its bank bailout. It created a way to mitigate the impact of interest rate hikes on bank balance sheets without having to lower interest rates more broadly.

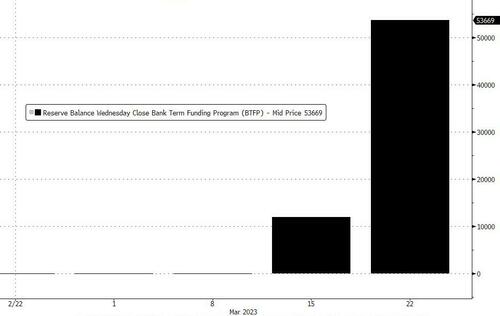

After the failure of Silicon Valley Bank, the Federal Reserve announced a loan program that will allow other banks to easily access capital “to help assure banks have the ability to meet the needs of all their depositors.”

The Bank Term Funding Program (BTFP) will offer loans of up to one year in length to banks, savings associations, credit unions, and other eligible depository institutions pledging US Treasuries, agency debt and mortgage-backed securities, and other qualifying assets as collateral. Banks will be able to borrow against their assets “at par” (face value).

According to a Federal Reserve statement, “the BTFP will be an additional source of liquidity against high-quality securities, eliminating an institution’s need to quickly sell those securities in times of stress.”

Keep in mind, banks are struggling precisely because the Fed raised interest rates so fast after holding them at zero for so long. As Peter Schiff noted, “It was the Federal Reserve that created all these distortions by its artificial suppression of interest rates, and it caused financial institutions to take incredible risks in order to get a return.”

With this loan program in place, banks can access capital based on their devalued bond holdings without selling their Treasuries and mortgage-backed securities into the market at a big loss (as SVB was forced to do). This provides some stability for both the banks and the bond markets.

This is how the Fed was able to raise interest rates and make a show of staying in the inflation fight. It can even keep shedding Treasuries and mortgage-backed securities from its balance sheet. Meanwhile, the banks can avoid the pain by accessing this crazy loan program. In effect, it can have its cake and eat it too – at least for a little while.

I think Powell and Company are hoping this loan boondoggle will buy them time to keep tightening for a while longer in the hope that CPI will drop enough in the next couple of months to claim victory over inflation and then pivot without losing face.

THE INFLATION FIGHT IS OVER

But make no mistake, no matter what Powell says, the inflation fight is over.

You don’t fight inflation by handing banks $300 billion of money created out of thin air. The purpose of monetary tightening is to squeeze liquidity out of the system. This loan program does the opposite. It injects liquidity into the system. It is the exact opposite of inflation fighting. It literally creates inflation.

Furthermore, it’s only a matter of time before something else breaks in the economy or the financial system. Banks aren’t the only things being impacted by increasing interest rates. Corporations are levered to the hilt. The federal government continues to borrow and spend, running up its debt. American consumers have buried themselves under record credit card debt. The entire economy is based on artificially low interest rates.

And the Fed just raised rates again.

The Fed may have managed to get a finger in one crack in the dam — for now — but it won’t be long before another hole appears. And then another. And then another.

It’s only a matter of time before the Fed has to abandon the pretense of an inflation fight, pivot, and start cutting rates.

In other words, inflation has won.

But for now, Powell and Company can continue to pretend to be tough on inflation. It can keep walking the tightrope. But tightrope walking in a hurricane is doomed to fail.

end

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards/John Rubino

A

3,Chris Powell of GATA provides to us very important physical commentaries

Craig Hemke at Sprott Money: Monetary madness endgame

Submitted by admin on Wed, 2023-03-22 14:57Section: Daily Dispatches

2:52p ET Wednesday, March 22, 2023

Dear Friend of GATA and Gold:

As the Federal Reserve slowly backs away from raising interest rates, the TF Metals Report’s Craig Hemke writes at Sprott Money today that the Keynesian era of monetary management is coming to an end in the long-expected uncontrolled inflation.

Hemke’s analysis is headlined “Monetary Madness Endgame” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/blog/Monetary-Madness-Endgame-2023-03-22

END

New York Sun: Louisiana congressman turns out to have been a prophet about the Fed

Submitted by admin on Wed, 2023-03-22 13:38Section: Daily Dispatches

From the New York Sun

Tuesday, March 21, 2023

https://www.nysun.com/article/the-federal-reserve-a-prophet-arises-from-louisiana

With the world beguiled by the predicament of the Federal Reserve — whether to raise interest rates to fight inflation or lower them to ease the banking crisis — this is a moment to reprise why Congress created the central bank in the first place. Monetary sage Edwin Vieira, Jr., reminds us that the Fed was formed at the acme of the Progressive Era to rationalize finance and prevent banking crises.

Just like the one we have today.

t was the Panic of 1907 — prompted by bank runs — that got the wheels spinning. The crisis, which sparked a global recession, was traced to “the handicap of an unscientific currency system,” as it was put by a founder of the Fed, Senator Glass. Never mind that under the gold standard America had a stable currency that allowed it to reach industrial dominance while holding inflation to an average of 0.1% a year.

Congress, advised by a monetary commission, in 1913 created the Fed to provide, as Mr. Vieira puts it, “so-called scientific management of currency and credit.” During the debate the Sun wrote that it was “difficult to discuss with any degree of patience this preposterous offspring of ignorance and unreason.” It described the proposed central bank as “an official board to exercise absolute control” of finance and as “covered all over with the slime of Bryanism.”

That was a reference to William Jennings Bryan, who, in the epic election of 1896, ran for free silver, which meant inflation, and lost to William McKinley, who stood for honest money. The Great Depression would soon put the lie to the Fed’s ability to ward off economic disaster.

“Scientific management didn’t work,” is how Mr. Vieira sums it up. He sees in the creation of the Fed the same statist impulses animating the New Deal.

The result, Mr. Vieira says, was to “cartelize” banking, with the Fed “at the top of the pyramid.”

Twenty years later FDR and his New Deal brain trust formed the National Recovery Administration, an attempt to manage American capitalism using the progressive euphemisms of systematizing and rationalizing. Yet when the NRA was struck down by a unanimous Supreme Court, the Fed, an anomaly, was left alone.

Congress had tried to prevent the resulting disaster by insisting, before it passed the Federal Reserve Act, that nothing in the law would authorize abrogating convertibility of the dollar under the Gold Standard Act of 1900. Congress also imposed on the Fed a 40% gold reserve requirement for paper money the central bank issued. “We have provided against inflation in almost every conceivable way,” Glass growled.

These pledges would ring hollow.

FDR devalued the dollar in 1933, and Congress forbade Americans from owning gold. After World War II, the Bretton Woods Agreement established a new value of the dollar. It required our government to redeem at a 35th of an ounce of gold dollars presented to it by foreign governments. That fell apart in the late 1960s and 1970s and we were precipitated into a 50-year experiment with fiat money.

The result has been not only inflation but quantitative easing and artificially low interest rates, culminating in today’s banking crisis. The central bank, freed from its responsibility to maintain the dollar’s fixed value in specie, has veered far from its legislated purpose. As have the other Bretton Woods institutions; even now, an effort is underway to shift the World Bank to a new mission, regulating the weather around the planet.

Which brings us back to the Fed, as it faces the dilemma of how to extricate America from the very crisis that the central bank has induced. It turns out that during the debate over creating the Fed, a congressman from Louisiana, James Walter Elder, uttered words that may yet make him a prophet: “If this bill becomes a law, someday the American people will have a memorable fight to unshackle themselves from this government bank.”

end

These twi readers are the top gun of the industry fraud in gold.silver trading

Former JPMorgan traders should get prison for spoofing, prosecution says

Submitted by admin on Wed, 2023-03-22 13:13Section: Daily Dispatches

By Steve Smith

Bloomberg News

Tuesday, March 21, 2023

The former head of the JPMorgan Chase & Co. precious-metals business and his top gold trader should get multiyear prison terms after they were convicted of spoofing the market for years, the U.S. government said in a court filing.

Michael Nowak, who ran the precious-metals desk, should get five years, and Gregg Smith, the top trader, should get six years, prosecutors said today in a sentencing memo to the federal judge in Chicago who presided over their trial. The recommendation was for longer terms than traders at other banks who have been convicted of spoofing.

The government said significant sentences are warranted because the two had spoofed for years and knew that what they were doing was prohibited.

At trial prosecutors presented evidence that included detailed trading records, chat logs, and testimony by former co-workers who “pulled back the curtain” on how Nowak and Smith moved precious-metals prices up and down for profit from 2008 to 2016. …

… For the remainder of the report:

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

END

5.IMPORTANT COMMENTARIES ON COMMODITIES: LITHIUM

END

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

end

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UPTO 6.8189

OFFSHORE YUAN: 6.8169

SHANGHAI CLOSED UP 20,90PTS OR 0.64%

HANG SENG CLOSED UP 458.21 PTS OR 2,34%

2. Nikkei closed DOWN47.04PTS OR 0.17%

3. Europe stocks SO FAR: MOSTLY GREEN

USA dollar INDEX DOWN TO 101,84 EURO RISES TO 1.0885 UP 16 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.312!(Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 131.06/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.2085%***/Italian 10 Yr bond yield FALLS to 4.058*** /SPAIN 10 YR BOND YIELD FALLS TO 3.253…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.135/

3j Gold at $1984.85/silver at: 23.07 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 1 AND 05/100 roubles/dollar; ROUBLE AT 76.00//

3m oil into the 71 dollar handle for WTI and 76 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 131.06 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .312% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9132 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9947well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

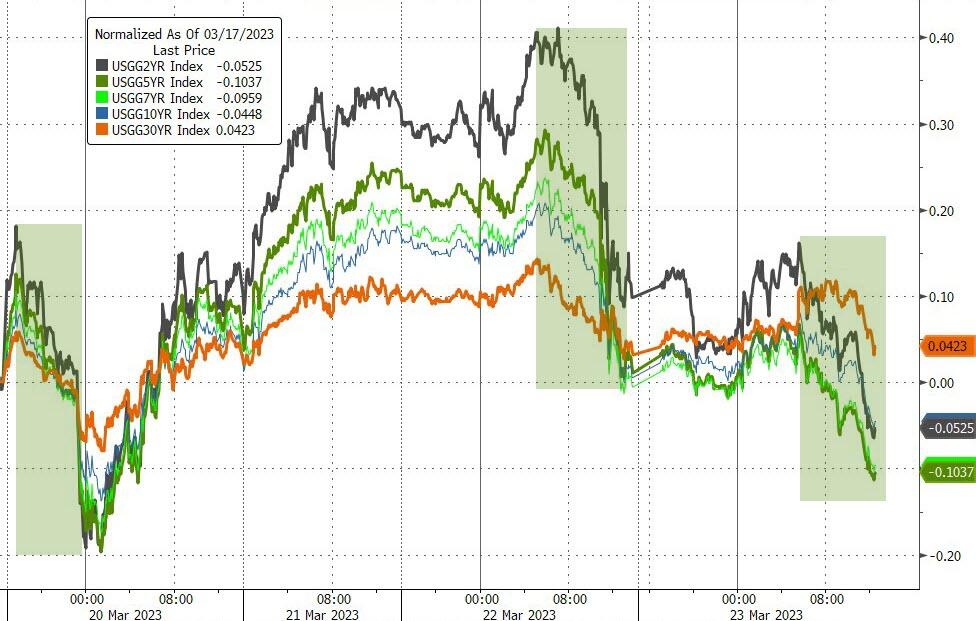

USA 10 YR BOND YIELD: 3.470% DOWN 3 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.734 UP 4BASIS PTS//I

USA 2 YR BOND YIELD: 4.058UP 12 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.05…

GREAT BRITAIN/10 YEAR YIELD: 3.404% DOWN 5 BASIS PTS

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Rebound After Yellen Torches Markets

THURSDAY, MAR 23, 2023 – 01:58 PM

After 76 year old treasury secretary Janet Yellen blew up the market yesterday with her post-FOMC comments that regulators aren’t looking to provide “blanket” deposit insurance to stabilize the US banking system, stock futures have rebounded modestly on Thursday, while paring some earlier gains. S&P 500 futures were up 0.5% at 3990 at 7:45 a.m. ET while Nasdaq 100 futures rose 0.9%. Both underlying indexes fell the most in two weeks yesterday. The tech-heavy Nasdaq index flirted with a bull market yesterday after briefly rising 20% from its December low. US government bond yields have edged up after falling sharply on Wednesday when the Fed raised rates 25bps but also opened the door to a pause, while WTI crude futures are down 0.6% in early US session. The Stoxx Europe 600 Index slid 0.8%, falling for the first time this week before a rates decision from the Bank of England.

In premarket trading, banking stocks were again the biggest laggards, following weakness in their US peers and as Citigroup Inc. slashed its outlook for the sector. Coinbase slumped after the largest US crypto exchange said it received a notice from the SEC formally declaring the securities regulator’s plans to bring an enforcement action against it. Analysts say the notice might be a precursor to the agency ultimately suing the company. Here are some other notable premarket movers:

- First Republic Bank shares rose on Thursday along with banking peers, set for a tentative rebound from yesterday’s losses following disappointment over comments from Treasury Secretary Janet Yellen over bank deposits.

- Cryptocurrency-exposed stocks rise as Bitcoin rebounds after snapping a six-session gaining streak on Wednesday. US equity futures also climbed, signaling a recovery following a tumultuous day of losses on Wall Street. Marathon Digital (MARA US) +5.1%, Riot Platforms (RIOT US) +4.7%.

- Chewy falls as much as 6.6% in US premarket trade after the online pet supplies retailer issued softer-than-expected FY23 guidance, with plans for international expansion likely to pressure margins. The company’s 4Q results also showed declining customer numbers, which Barclays says raises questions given that headwinds should have been abating.

- Phreesia Inc. shares dropped 3.3% in postmarket trading, after the application software company reported fourth-quarter results that beat expectations but gave a revenue outlook that KeyBanc sees as light.

Caution reigned in markets on Thursday following the Fed’s decision to proceed with a quarter-point rate hike, combined with Treasury Secretary Janet Yellen’s remarks on the health of the banking sector. While Fed Chair Jerome Powell assured that regulators’ actions demonstrated “all depositors’ savings are safe” as he raised rates by an expected quarter point, Yellen effectively contradicted him and sent stocks whipsawing, when she said regulators aren’t looking to provide “blanket” deposit insurance.

“Yellen’s comments were clearly the more important factor yesterday,” said Manish Kabra, US equity strategist at Société Générale. “Not securing all deposits risks more deposit runs, which means large banks’ outperformance versus regional banks is likely to continue. Overall, the US banks rally will continue to fade, at least until the yield curve is firmly positive.”

“It is well possible that the post-FOMC equity selloff quickly reverses, as falling yields are supportive of equity valuations — if financial stress is contained and economic data is not too bad,” said Ipek Ozkardeskaya, senior analyst at Swissquote Bank.

UBS strategists led by Mark Haefele believe that any rally would be unlikely to endure just yet however, noting that turning points usually rely on investors anticipating interest-rate cuts alongside a trough in economic activity and corporate earnings. “The Fed’s actions and analysis of the economy suggest these conditions are not yet fully in place,” they said in a note.

Separately, Goldman Sachs Group Inc. strategists say they expect US households to be net sellers of $750 billion worth of stocks in 2023 amid rising bond yields and declining personal savings. The team led by Cormac Conners says higher 10-year yields and lower savings rates tend to be associated with decreased net equity demand from households.

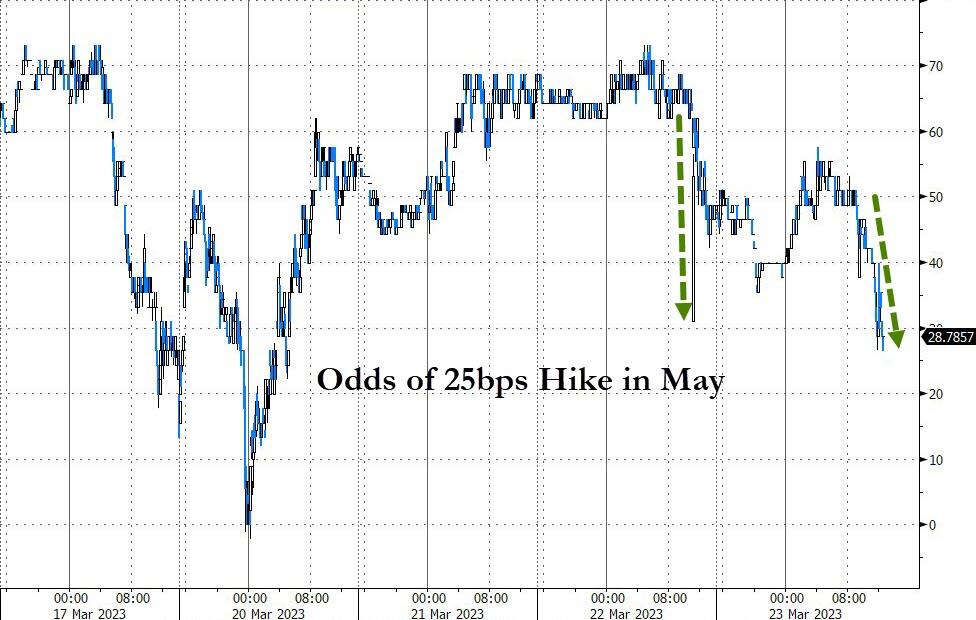

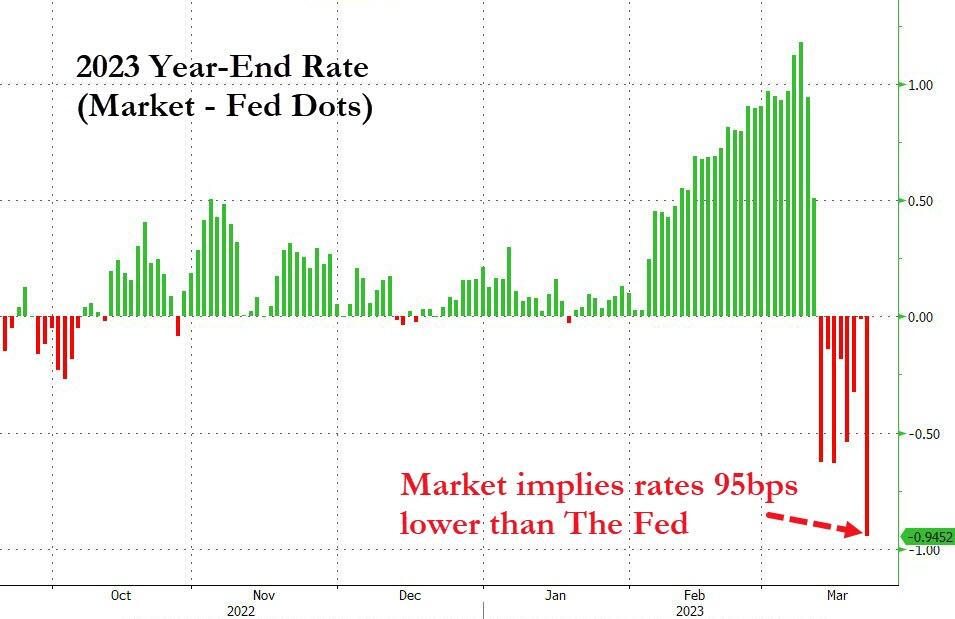

As a result of the ongoing bank crisis, the swap market shows investors are split on the chances that Fed officials will add another 25 basis points to their benchmark in May. Despite Powell’s guidance, expectations for cuts have deepened, with the market suggesting that the effective fed funds rate will drop to around 4.1% in December. “I would not expect the market to take these rate cuts out in the near term and could very well price in more cuts if the data deteriorates from here,” Matthew Hornbach, global head of macro strategy at Morgan Stanley, told Bloomberg Television. Powell himself, though, said in response to questioning that officials “just don’t” see cuts this year and that they will raise higher than expected if that is needed. “Rate cuts are not in our base case,” he said. He also didn’t see the bank crisis as recently as three weeks ago when he swore to Congress he would hike rates 50bps only to trigger the worst banking crisis since Lehman.

European stocks are on course to snap a three-day winning streak as banks underperform after US Treasury Secretary Janet Yellen warned they aren’t considering widespread insurance for bank deposits. The Stoxx 600 is down 1.0% while the Stoxx 600 Banks Index falls 2.5%. Here are some of the biggest European movers:

- HSBC shares drop as much as 3.3%, ING slides as much as 2.5% and ABN Amro tumbles as much as 3.7% after US peers fell on remarks that US lawmakers aren’t planning on widespread insurance for bank deposits

- Jeronimo Martins falls as much as 4.1%, curbing the stock’s rally since the start of the month, after 4Q earnings showed a further drop in the Portuguese retailer’s margins

- Rallye SA slumps as much as 10% after the company said the latest earnings from its French supermarket business make it difficult to finish debt restructuring

- Gym Group drops as much as 5.1% after Barclays downgrades the fitness operator to equal-weight from overweight, citing a “bleak” profit outlook

- Sanofi gains as much as 5.3%, the most since December, after releasing positive data from a phase 3 trial for its key drug Dupixent

- Scout24 climbs as much as 4.4%, reaching highest since mid-November, after the online classified advertising company announced a buyback

- Inwit rises as much as 4.8% to a record after Reuters reported that private equity firm Ardian is in the early stage of exploring a bid for the Italian tower operator

- Domino’s Pizza Group jumps as much as 4.3% after Barclays upgrades the pizza delivery chain to overweight from equal-weight, highlighting the increase in app usage

- Meyer Burger gains as much as 15% after the Swiss solar equipment manufacturer’s Ebitda and profitability beat expectations

- Nemetschek shares rise as much as 13% to their highest level since September. The German firm’s outlook for 2024 and 2025 was seen as solid

The BOE is likely to continue the quickest series of interest-rate increases in three decades, with its focus on combating inflation outweighing calls for a pause given recent turmoil in the banking system. The Swiss and Norwegian central banks both raised rates Thursday, as forecast, and flagged more hikes to come in their campaigns to tame rising consumer prices.

For the BOE, February UK CPI data have “removed any flexibility they may have thought they had and now markets are pricing in a higher terminal rate of around 4.5% as a result,” said Craig Erlam, a senior market analyst at Oanda Ltd. “This makes the language that accompanies the decision key,” he said, expecting policymakers to highlight an uncertain outlook and the need to be data-dependent.

Earlier in the session, Asian stocks rose as the region’s currencies strengthened against the dollar despite the Federal Reserve’s decision to raise US interest rates on Wednesday. The MSCI Asia Pacific Index climbed as much as 1.5%, rising for a third day, as most Asian currencies, including South Korea’s won and Thailand’s baht, gained. Hong Kong’s equity benchmarks were among the top performers, boosted by gains in Tencent after the firm reported better-than-expected revenue. Stock gauges in Japan and India underperformed. “Dollar reaction to the Fed hike looks to be muted, which can ease pressure on Asian currencies and fund flows,” said Marvin Chen, an analyst at Bloomberg Intelligence. “Focus should be on the dollar impact as peak Fed rates near.” The dollar slid as market expectations for rate cuts by the Fed deepened despite the central bank hiking its benchmark rate by a quarter-point and signaling that it expects more tightening after that.

A weaker greenback tends to be beneficial for Asian shares if it signals higher risk appetite and is seen as a positive for growth in the region’s emerging economies, many of which rely on imports priced in dollars. An index of Asian financial stocks headed for a three-day gain as a key technical indicator suggested the sector’s loss of more than 3% this month may have been excessive. US shares slumped Wednesday after comments from Treasury Secretary Janet Yellen rattled US bank shares and Fed Chairman Jerome Powell dashed hopes on rate cuts this year. Given expected slower US growth and the stresses in its banking system, it makes more sense to lean into the stronger growth recovery in China as well as Hong Kong and Thailand, said Sunil Koul, Asia Pacific equity strategist at Goldman Sachs, in a Bloomberg TV interview

Japanese equities fell, following US peers lower, after comments from Treasury Secretary Janet Yellen rattled US bank shares and Federal Reserve chief Jerome Powell said he was prepared to keep raising rates. The Topix Index fell 0.3% to 1,957.32 as of market close Tokyo time, while the Nikkei declined 0.2% to 27,419.61. Sony Group Corp. contributed the most to the Topix Index decline, decreasing 1.3%. Out of 2,159 stocks in the index, 1,256 rose and 781 fell, while 122 were unchanged. Yellen told US lawmakers that the government wasn’t considering “blanket” deposit insurance to stabilize the banking system while Powell said he was ready to keep raising rates until inflation shows signs of cooling. Japanese shares are falling after the comments, said Rina Oshimo, a senior strategist at Okasan Securities.

Australian stocks joined the selloff: the S&P/ASX 200 index fell 0.7% to close at 6,968.60, in a broad decline weighed by losses in mining shares and banks. The drop followed a slump on Wall Street as the Federal Reserve pushed back against bets for interest rate cuts this year. In New Zealand, the S&P/NZX 50 index was little changed at 11,594.94

Lastly, stocks in India were among the worst performers in Asia amid a mixed trend seen across global markets as investors remained concerned over the future course of central banks’ policy actions. The S&P BSE Sensex fell 0.5% to 57,925.28 in Mumbai, while the NSE Nifty 50 Index declined 0.4%. The gauge is now little changed this week after dropping for two out of the last four sessions. The benchmarks have slipped more than 4.5% each for the year. The underperformance in local equities compared with Asian and emerging market peers is a result of surging interest rates in the US – the Fed raised its main lending rate by another 25 bps on Wednesday to 5% – impacting flows from overseas investors. Index-heavy software exporters and banks came under pressure on increasing worries over global economic growth. Foreign investors have sold $2.8b of local shares this year through March 20 following inflows of about $11b over the preceding two quarters. Domestic investors have however remained buyers to the tune of $9b in 2023. Reliance Industries contributed the most to the Sensex’s decline, decreasing 1.3%. Out of 30 shares in the Sensex index, 13 rose, while 17 fell.

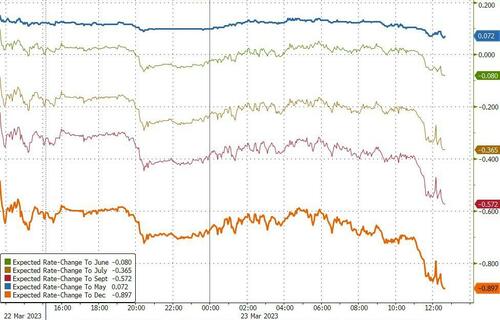

In FX, weakness in the dollar extended to a sixth day, with a gauge of the greenback falling to the lowest in more than a month as traders boosted bets for US interest-rate cuts, even after the Fed said more tightening may be needed. It has since rebounded fractionally from session lows.

- The Norwegian krone gained 1% versus the dollar after a hawkish 25bps hike from the Norges Bank. While there were expectations that Norges Bank would stand pat after hiking today, the central bank explicitly signaled another increase in May

- The pound and euro advanced, with the former climbing on leveraged demand amid expectations for the Bank of England to deliver a hawkish quarter-point rate increase on Thursday, according to a trader “With the banking sector concerns still fresh, the Fed was more dovish than just a while ago and that is dragging down bond yields and the dollar,” said Daisuke Uno, chief strategist at Sumitomo Mitsui Banking Corp. “I still think the Fed will raise the rate to tame inflation, which seems to remain stubborn”

- The Swiss franc struggled to hold gains after the SNB opted for a 50bps increase. The Dollar Index is little changed.

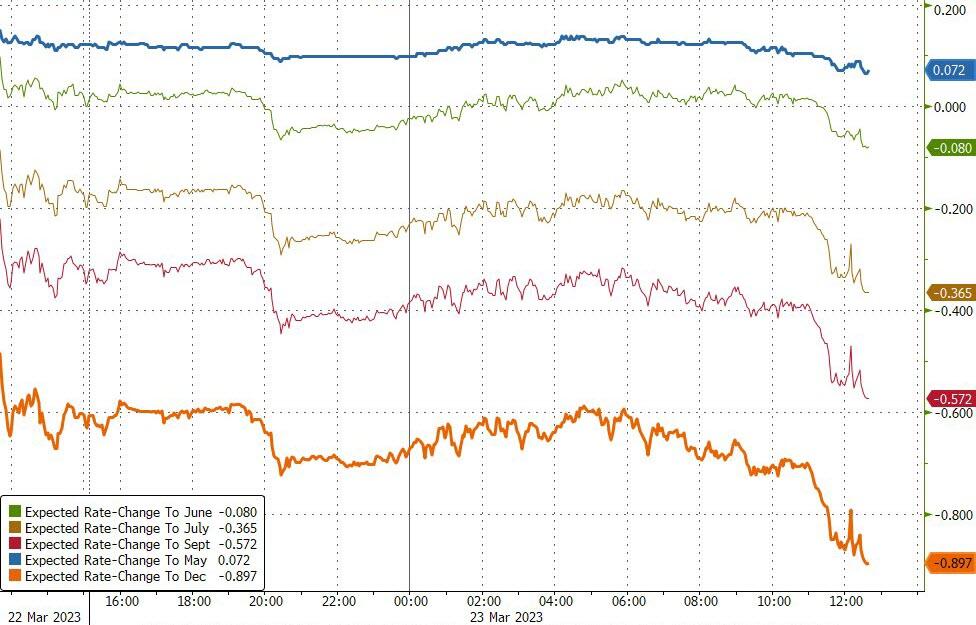

In rates, treasuries were cheaper across the curve, although futures remain near top of Wednesday’s range, a bull-steepening rally following Fed’s rate decision. US two-year yields are up ~2bps while UK two-year borrowing costs fall 9bps ahead of the Bank of England rate decision later today. Thursday’s losses are belly-led, cheapening 2s5s30s fly by ~3bp on the day. Bank of England rate decision at 8am New York time is expected to be a quarter-point rate increase. US yields cheaper by 3bp-5bp across the curve with 10-year around 3.48%, near low end of Wednesday’s 3.427%-3.642% range; on the curve, 2s10s spread is wider by ~1.5bp on the day, near Wednesday’s steepest levels, while 5s30s spread tightens ~1.5bp. Fed-dated OIS contracts price in around 13bp of rate hike premium for the May policy decision and then ~75bp of cuts by year-end.

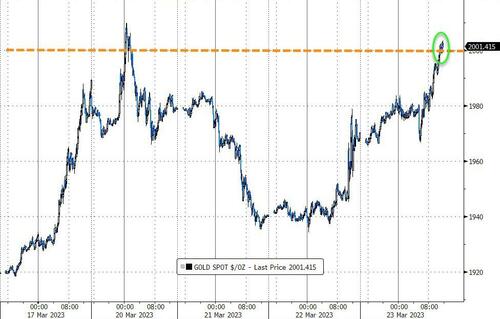

Crude futures decline with WTI falling 1.2% to trade near $70.05. Spot gold adds 0.5% to around $1,980. Bitcoin rises 1.2%.

Looking to the day ahead now, monetary policy decisions will include the Bank of England, the Swiss National Bank and the Norges Bank. Data releases include the US weekly initial jobless claims, February’s new home sales, the Kansas City Fed manufacturing activity for March, and the Q4 current account balance. Finally, EU leaders will gather in Brussels for a summit.

Market Snapshot

- S&P 500 futures up 0.5% to 3,989.00

- MXAP up 1.3% to 160.31

- MXAPJ up 1.5% to 517.51

- Nikkei down 0.2% to 27,419.61

- Topix down 0.3% to 1,957.32

- Hang Seng Index up 2.3% to 20,049.64

- Shanghai Composite up 0.6% to 3,286.65

- Sensex little changed at 58,181.18

- Australia S&P/ASX 200 down 0.7% to 6,968.61

- Kospi up 0.3% to 2,424.48

- STOXX Europe 600 down 0.4% to 445.25

- German 10Y yield little changed at 2.28%

- Euro up 0.4% to $1.0897

- Brent Futures down 0.2% to $76.52/bbl

- Gold spot up 0.4% to $1,977.01

- U.S. Dollar Index down 0.18% to 102.16

Top Overnight News from Bloomberg

- Hong Kong’s CPI for Feb falls short of expectations, coming in at +1.7% (down from +2.4% in Jan and below the St’s +2.4% forecast). Singapore’s inflation also comes in a bit below plan at +6.3% headline for Feb (down from +6.6% in Jan and below the St’s +6.4% forecast). BBG

- Blinken’s planned trip to China may be in the process of getting back on track after being derailed by the Chinese balloon incident. Blinken said China will be capable of invading Taiwan by 2027. SCMP

- The ECB will probably need to raise borrowing costs more, though the bulk of tightening is already done, according to Governing Council member Madis Muller. BBG

- Ukrainian troops, on the defensive for four months, will launch a long-awaited counterassault “very soon” now that Russia’s huge winter offensive is losing steam without taking Bakhmut, Ukraine’s top ground forces commander said on Thursday. RTRS

- Swiss financial regulator Finma has defended its decision to wipe out a huge swath of risky subordinated bonds as part of the CS rescue deal. In its first statement on the deal since the weekend, Finma said that all the contractual and legal obligations had been met for it to act unilaterally given the urgency of the situation. “On Sunday, a solution was found to protect clients, the financial centr and the markets,” said Finma’s chief executive Urban Angehrn. “In this context, it is important that Credit Suisse’s banking business continues to function smoothly and without interruption.” FT

- Following the Fed, the BOE will probably continue its quickest series of rate increases in three decades with a 25-bp hike to 4.25%. The SNB raised rates by 50 bps and signaled more to come as it resumed its inflation fight just days after the downfall of Credit Suisse. Norges Bank raised by 25 bps to 3%, as expected, and said it will tighten further in May. BBG

- Freight companies are dialing back expectations that demand will recover strongly in the second half of the year amid growing economic uncertainty and signs retailers are growing more guarded about placing big orders in 2023. WSJ

- OPEC+ is unlikely to take action on production despite the recent slump in prices as they attribute most of the volatility to financial speculation, not fundamentals. RTRS

- The SEC has told Coinbase that it plans to take enforcement action against the company, escalating its crackdown on digital-currency firms by targeting the biggest U.S. crypto exchange, Coinbase said Wednesday. WSJ

- The Swiss National Bank raised its interest rate by 50 basis points and signaled more to come as it resumed its inflation fight just days after the downfall of the country’s second- biggest bank became the epicenter of global financial turmoil: BBG

- Norway’s central bank raised its key interest rate to the highest level since 2009 and signaled further tightening after higher price pressure from a weaker-than-forecast krone outweighed concerns about global banking turbulence: BBG

- Wall Street banks and European rivals are undoing de facto hiring freezes after Credit Suisse’s emergency rescue by UBS, unable to resist the lure of top talent available at a discount: BBG

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded mixed with price action choppy as markets digested the FOMC where the Fed delivered a widely expected 25bps rate hike and maintained its terminal rate view but dropped its reference regarding expectations that ‘ongoing’ rate hikes will be appropriate. ASX 200 declined amid the uninspired mood across most industries with underperformance in tech and mining. Nikkei 225 was contained by weakness in financials and after Japan maintained the overall assessment of the economy but cut the assessment on corporate profits and production for the first time since April 2020. Hang Seng and Shanghai Comp. swung between gains and losses with optimism in Hong Kong following earnings releases from Orient Overseas International and Tencent whereby the advances in the latter inspired its tech peers, although participants also digested a rate hike by the HKMA which moved in lockstep with the Fed.

Top Asian News

- HKMA raised its base rate by 25bps to 5.25%, as expected, which is in lockstep with the Fed.

- RBNZ Chief Economist Conway said inflation is high and widespread because strong demand outstripped supply, while he added that they are incredibly determined to get inflation and inflation expectations back to the target. Furthermore, Conway expects monetary policy tightening to cause the New Zealand economy to enter a mild recession later this year as demand slows, as well as noted that the OCR is now comfortably above neutral and having the desired contractionary effect, according to Reuters.

European bourses began the session mixed/flat, but have since dipped more convincingly into negative territory with newsflow focused on hawkish Central Bank action post-Fed thus far. Once again, the FTSE 100 is lagging its peers as focus remains firmly on the upcoming BoE announcement, FTSE 100 -1.0%. Stateside, futures are firmer though remain shy of Wednesday’s best levels and have most recently eased off the sessions peak given the above action, ES +0.4%. Citi cuts their Stoxx 600 end-2023 forecast to 445 (prev. 475); FTSE 100 cut to 7600 (prev. 8000); downgrades Banks to Neutral (prev. Overweight).

Top European News

- ECB’s Muller says inflation is a bigger problem than the increase in borrowing costs. Lions share of hikes are behind us; ECB is likely to increase rates by a little.

- ECB’s Stournaras says should not commit to any rates in advance.

- Italy is reportedly preparing a new package of measures worth some EUR 5bln to aid firms and families cope with energy bills, and could be unveiled next week, according to Reuters sources.

Central bank decisions

- SNB hikes by 50bps to 1.50% vs exp. 1.50% (prev. 1.00%); does not rule out further hikes; reiterates language around price stability and FX intervention. Further increased its inflation forecasts, with CPI now not seen dropping back into the 0-2% target band until Q2-2023 (prev. Q4-2023). Click here for full details, reaction & analysis.

- Norges Bank hikes by 25bps to 3.00% vs exp. 3.00% (prev. 2.75%); the policy rate will be raised further in May; decision unanimous. Rate path now implies an end-2023 rate of 3.60% (prev. 3.08%). Click here for full details, reaction & analysis.

- Brazilian Central Bank maintained the Selic rate at 13.75%, as expected, while it will remain vigilant and will assess if the strategy of maintaining the Selic rate for a sufficiently long period of time will be enough to ensure the convergence of inflation. BCB added that inflation expectations have shown additional deterioration, especially at longer horizons and they will not hesitate to resume the tightening cycle if the disinflationary process does not proceed as expected.

FX

- The USD remains on the back-foot after Wednesday’s FOMC, though the DXY is back towards a 102.44 high after briefly printing a fresh March low of 101.91.

- Action which supports peers across the board and features antipodeans outperforming after recent pressure, NZD leading and cognisant of RBNZ’s Conway emphasising that inflation remains high and widespread; NZD/USD and AUD/USD testing 0.63 and 0.6750 respectively.

- GBP is next best ahead of the BoE, Cable at a fresh March peak of 1.2343 with 25bp fully priced and a peak of around 4.45% (current 4.00%) implied.

- The single currency, EUR, is underpinned by the USD but with EUR/GBP pressure preventing any further appreciation; EUR/USD holding sub-1.09 while EUR/GBP near the 0.8832 low.

- Finally, CHF benefitted from the SNB’s hawkish-hike while the NOK is back to pre-release levels as expectations for a 50bp hike unwind while the hawkish repo path adjustments are factored in.

Fixed Income

- EGBs are underpinned with yields softer across the curve post-Fed while Gilts are closer to the unchanged mark pre-BoE, though the morning’s hawkish action has sparked a pullback from best levels.

- Bunds hold around 136.00 and the 10yr yield now back above 2.25% after dipping to a 2.22% low; modest upside was seen in Bunds following Germany leaving its Q2 issuance calendar unrevised vs the prelim. FY release.

- Stateside, USTs continue to derive support from Wednesday’s announcements; though, the yield curve has lifted marginally from the mid-week trough, but does remain lower overall with action most pronounced in the belly.

- German Q2 issuance calendar sees no changes vs the prelim. annual release.

Commodities

- Commodities are mixed, with the crude benchmarks attempting to pare back some of their overnight losses while metals glean support from the USD’s downside.

- Specifically, WTI and Brent are towards the lower-end of USD 69.91-70.79/bbl and USD 75.76-76.66/bbl parameters, though the benchmarks are holding above USD 70 and USD 76 respectively.

- Both precious and base metals are benefitting from the softer dollar; spot gold towards the upper-end of USD 1964-1983/oz parameters, just shy of Wednesday’s USD 1985/oz best with base metals supported but off best given the broader risk tone.

- Iran’s Finance Minister said Iran achieved its highest level of oil exports for at least two years last month, according to FT.

- Goldman Sachs said gold remains the best safe-haven asset for financial risks and raised its gold target to USD 2050/oz from 1950/oz, while it added that Chinese demand continues to surge across the commodity complex with oil demand topping 16mln bpd and it remains very positive on commodity prices with 12-month forecasted returns of 27.9% for S&P GSCI.

Geopolitics

- China’s military said it monitored and drove away a US destroyer which entered the South China Sea Paracel Islands, although the US Navy later said that the Chinese military’s statement is false regarding a US destroyer being expelled from the South China Sea.

- Taiwan’s Foreign Minister said President Tsai’s meeting with the US House Speaker is still being arranged, according to Reuters.

- Saudi Arabia and Iran’s Foreign Ministers agreed to meet soon to pave the way for the reopening of embassies, according to the Saudi state news agency.

- Russian Foreign Ministry Lavrov is to hold discussions with Iran’s top diplomat on March 29th in Moscow, according to Tass.

- US mulls opening Pacific defense pact with Britain and Australia to more countries, according to Semafor.

- US reportedly plans to send aging A-10 attack planes to the Middle East while shifting newer jets to Asia and Europe, according to US officials cited by WSJ.

US Event Calendar

- 08:30: March Initial Jobless Claims, est. 197,000, prior 192,000

- March Continuing Claims, est. 1.69m, prior 1.68m

- 08:30: Feb. Chicago Fed Nat Activity Index, est. 0.10, prior 0.23

- 08:30: 4Q Current Account Balance, est. -$213.7b, prior -$217.1b

- 10:00: Feb. New Home Sales, est. 650,000, prior 670,000

- Feb. New Home Sales MoM, est. -3.1%, prior 7.2%

- 11:00: March Kansas City Fed Manf. Activity, est. -2, prior 0

DB’s Jim Ried concludes the overnight wrap

In an FOMC meeting that went to script but perhaps leaned dovish, Mr Powell’s press conference was overshadowed by his predecessor’s (Yellen) simultaneous comments that a blanket guarantee of deposits had not been discussed or considered. It seems highly unlikely the US would let depositors take losses but maybe such a move won’t be done pre-emptively and would require future stress first. The reaction to her comments also highlighted the nervousness and fragility underpinning a big 2-day rally. The remarks led to a late slump in equities (S&P 500 -1.65% – all post Yellen) and big rally in bonds (2yr -23bps – more than half after Yellen) and distracted from a relative uneventful FOMC, even if there were nuances worth discussing.