MARCH 24//GOLD CLOSED DOWN $15.10 TO $1981.30//SILVER CLOSED UP 3 CENTS TO $23.14//PLATINUM CLOSED DOWN 30 CENTS TO $982.30//PALLADIUM CLOSED DOWN $32.60 TO $1429.70//COVID AND VACCINE UPDATES//RUSSIAN VS UKRAINE UPDATES//BANKING CRISES INTENSIFIES//SWAMP STORIES//

435 H SCOTIA CAPITAL 4 624 H BOFA SECURITIES 2 737 C ADVANTAGE 6

TOTAL: 6 6

MONTH TO DATE: 5,198JPMORGAN stopped 7/180 contracts

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR MAR/2023. CONTRACT: 6 NOTICES FOR 600 OZ or 0.01866 TONNES

total notices so far: 5198 contracts for 519800 oz (16.1679 tonnes)

SILVER NOTICES: 0 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month : 3146 for 15,730000 oz

END

GLD

WITH GOLD UP $$47.70

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/SMALL CHANGES IN GOLD INVENTORY AT THE GLD:////// A SMALL DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD//

INVENTORY RESTS AT 925.42 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 62CENTS

AT THE SLV// SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF OF 0.919 MILLION OZ FROM THE SLV: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 459.485 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 1159 CONTRACTS TO 118,082 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.62 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. WITH TODAY’S READING AT THE COMEX, WE HAVE NOW SET ANOTHER RECORD LOW AT 118,082CONTRACTS , MARCH 23.2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.62). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A TINY GAIN ON OUR TWO EXCHANGES 46 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 1 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD: A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS( 1205 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.58 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S ZERO JUMP TO LONDON OF nil OZ//NEW STANDING: 15.750 MILLION OZ + THE 1.0 MILLION OZ OF EXCHANGE FOR RISK//THUS TOTAL NEW STANDING 16.750MILLION OZ/ //// V) STRONG SIZED COMEX OI GAIN/ STRONG SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –40 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTRACTS for 18 days, total 14,479contracts: OR 72.395 MILLION OZ . (8043CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 72.395MILLION OZ

.

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 72.395 MILLION OZ//INITIAL//STRONG ISSUANCE BUT BELOW LAST MONTH

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1199 CONTRACTS DESPITE OUR $0.62 GAIN IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 1205 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAR OF 15.58 MILLION OZ//FIRST DAY NOTICE// FOLLOWED BY TODAY’S 0 OZ EFP JUMP /QUEUE JUMP (WHICH INCREASES THE AMOUNT OF SILVER STANDING) + 1.0 MILLION OF EXCHANGE FOR RISK ISSUED EARLY IN MARCH (INCREASES THE AMOUNT OF SILVER STANDING) //NEW STANDING 16.750MILLION OZ .. WE HAVE A TINY SIZED GAIN OF 6 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 0 NOTICE(S) FILED TODAY FOR nil OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 10,317 CONTRACTS TO 480,174 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED-x847CONTRACTS.

WE HAD A STRONG SIZED INCREASE IN COMEX OI ( 11,164 CONTRACTS) WITH OUR $47.70 GAIN IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR MAR. AT 4.9953 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 400 OZ (0.133TONNES) //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London).

YET ALL OF..THIS HAPPENED WITH OUR $47,70 GAIN IN PRICEWITH RESPECT TO THURSDAY’S TRADING

WE HAD A HUGE SIZED GAIN OF 12,626 OI CONTRACTS (39,27PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2309 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 480,174

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 13,473CONTRACTS WITH 11,164 CONTRACTS INCREASED AT THE COMEX AND 2309 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2309 CONTRACTS OR 41,906 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2309CONTRACTS) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (10,317) TOTAL GAIN IN THE TWO EXCHANGES 2307 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR MAR. AT 4.9953 TONNES FOLLOWED BY TODAY’S 400 OZ QUEUE JUMP//NEW STANDING 16.310 TONNES // ///3) ZERO LONG LIQUIDATION //4) STRONG SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

TOTAL EFP CONTRACTS ISSUED: 76,245 CONTRACTS OR 7,624,500 OZ OR 237.15 TONNES IN 18 TRADING DAY(S) AND THUS AVERAGING: 4235 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18TRADING DAY(S) IN TONNES 237.15 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 237,15/3550 x 100% TONNES 6.82% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 237.15 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUGE SIZED 1199 CONTRACTS OI TO 118,082 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 118,122 CONTRACTS TODAY, MARCH 22/2022

EFP ISSUANCE 1205 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1205 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1205 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1199 CONTRACTS AND ADD TO THE 1205 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A TINY GAIN OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 6 CONTRACTS.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES //0.0300MILLION OZ

OCCURRED DESPITE OUR $0.62GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

i)FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED DOWN 20.99 PTS OR 0.64% //Hang Seng CLOSED DOWN 133.96 PTS OR 0.67% /The Nikkei closed DOWN 34.36 PTS OR 0.13% //Australia’s all ordinaries CLOSED down 0.15% /Chinese yuan (ONSHORE) closed up 6.8801//OFFSHORE CHINESE YUAN DOWN TO 6.8793/ /Oil UP TO 67.21 dollars per barrel for WTI and BRENT AT 73.13 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 10,317 CONTRACTS UP TO 480,174 WITH OUR GAIN IN PRICE OF $47.70 ON THURSDAY

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAR… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2307 EFP CONTRACTS WERE ISSUED: : APRIL 2307 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2307 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A HUGE TOTAL OF 12,626 CONTRACTS IN THAT 2309 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED GAIN OF 10,317 COMEX CONTRACTS..AND THIS STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GIGANTIC GAIN IN PRICE OF $47.70 WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAR (16.310) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 16.310 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $47.70) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR STRONG SIZED GAIN OF 12,626 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 41,906 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAR. (4.9953 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 400OZ (0.01244ONNES)… ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $47.70

WE HAD -847 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 12626 CONTRACTS OR 1,262,600OZ OR 39,27TONNES

Total monthly oz gold served (contracts) so far this month

5198 notices 519800 16.149 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 2

i)OUT OF DELAWARE 321.510 OZ 10 KILOBARS

II) OUT OF HSBC 64,302.000 OZ 2000 KILOBARS

total withdrawals: 64,623.510 oz

in tonnes: 2.010tonnes

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of MARCH we have an oi of 52 contracts having LOST 35 contracts. We had 39 notices filed on THURSDAY so we

gained 4 contracts or an additional 400 oz will stand for metal at the comex

April LOST A SMALL 5532 contracts DOWN to 132,,194 contracts. It is here that our banker friends have to worry as many will try and take delivery in this upcoming delivery month.

May GAINED 380 contracts to stand at 1006

We had 6 notice(s) filed today for 600 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 6 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAR. /2023. contract month,

we take the total number of notices filed so far for the month (5,198 x 100 oz ), to which we add the difference between the open interest for the front month of (MAR. 52 CONTRACTS) minus the number of notices served upon today 6 x 100 oz per contract equals 524,400OZ OR 16.310TONNES the number of TONNES standing in this active month of MARCH.

thus the INITIAL standings for gold for the MAR contract month:

No of notices filed so far (5,198x 100 oz+ xx OI for the front month minus the number of notices served upon today (6)x 100 oz} which equals 524400 oz standing OR 16.310TONNES in this active delivery month of MARCH..

TOTAL COMEX GOLD STANDING: 16.310 TONNES WHICH IS HUGE FOR AN INACTIVE DELIVERY MONTH.

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 3146 x 5,000 oz = 15,730,000 oz

to which we add the difference between the open interest for the front month of MAR(23) and the number of notices served upon today 0 (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAR./2023 contract month: 3146 (notices served so far) x 5000 oz + OI for the front month of MAR (23) – number of notices served upon today (0) x 500 oz of silver standing for the MAR. contract month equates 15.750million oz +the 1.0 million oz of exchange for risk//new total standing 16.750million oz

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

MARCH 15/THE IDES OF MARCH: WITH GOLD UP $18.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 913.27 TONNES

MARCH 14/WITH GOLD DOWN $4.75 TODAY: HUGE CHANGES: A MONSTER DEPOSIT OF 11.85 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 913.27 TONNES

MARCH 13/WITH GOLD UP $48.85 TODAY: VERY STRANGE HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY REST AT 901.42 TONNES

MARCH 10//WITH GOLD UP $31.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 903.15 TONNES

MARCH 9/WITH GOLD UP $16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 906.62 TONNES

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

FEB 28/WITH GOLD UP $12.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 917.61 TONNES

FEB 27/WITH GOLD UP $6.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.32 TONNES

FEB 24/WITH GOLD DOWN $9.10 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 917.32 TONNES

FEB 23/WITH GOLD DOWN $13.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 919.92 TONNES

FEB 22/WITH GOLD DOWN 22 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 919.92 TONNES

FEB 21/WITH GOLD DOWN $7.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 919.92 TONNES

FEB 17/WITH GOLD DOWN $1.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 921.08 TONNES

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

GLD INVENTORY: 925.42 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

MARCH 17/WITH SILVER UP 79 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE WITHDRAWAL OF 10.478 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 462.748 MILLION OZ//

MARCH 16/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 5.009 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 473.226 MILLION OZ//

MARCH 15/WITH SILVER DOWN 7 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 643,000 OZ INTO THE SLV//INVENTORY RESTS AT 478.235 MILLION OZ/

MARCH 14/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.287 MILLION OZ FROM THE SLV////INVENTORY REST AT 477.592 MILLION OZ//

MARCH 13/WITH SILVER UP $1.35 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ//

MARCH 10.WITH SILVER UP 36 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ…

MARCH 9/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.979 MILLION OZ

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWALOF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

FEB 28/WITH SILVER UP 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.241 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.188

FEB 27/WITH SILVER DOWN 15 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.471 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 482.429 MILLION OZ

FEB 24/WITH SILVER DOWN 46 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.172 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.900 MILLION OZ//

FEB 23/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.379 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.072 MILLION OZ//

FEB 22/WITH SILVER DOWN 22 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ FROM THE SLV////INVENTORY RESTS AT 485.693 MILLION OZ

FEB 21/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.5363 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 486.382 MILLION OZ//

FEB 17/WITH SILVER UP 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 827,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.819 MILLION OZ/

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 459.485MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

end

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards/John Rubino

A

3,Chris Powell of GATA provides to us very important physical commentaries

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

END

5.IMPORTANT COMMENTARIES ON COMMODITIES: LITHIUM

END

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

end

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 6.8801

OFFSHORE YUAN: 6.8793

SHANGHAI CLOSED DOWN20,99 PTS OR 0.64%

HANG SENG CLOSED DOWN133.96 PTS OR 0.67%

2. Nikkei closed DOWN34.36PTS OR 0.33%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 102.99 EURO FALLS TO 1.0718 DOWN 119 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.257(Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 129.13/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.2027%***/Italian 10 Yr bond yield FALLS to 3.951*** /SPAIN 10 YR BOND YIELD FALLS TO 3.103…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.014/

3j Gold at $1994.50 silver at: 23.14 nam est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 51/100 roubles/dollar; ROUBLE AT 76.51//

3m oil into the 67 dollar handle for WTI and 73 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 129.83 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .257% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9214as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9877well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

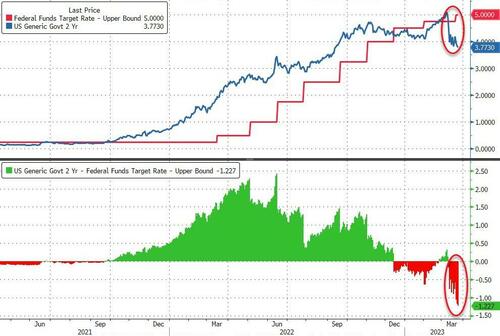

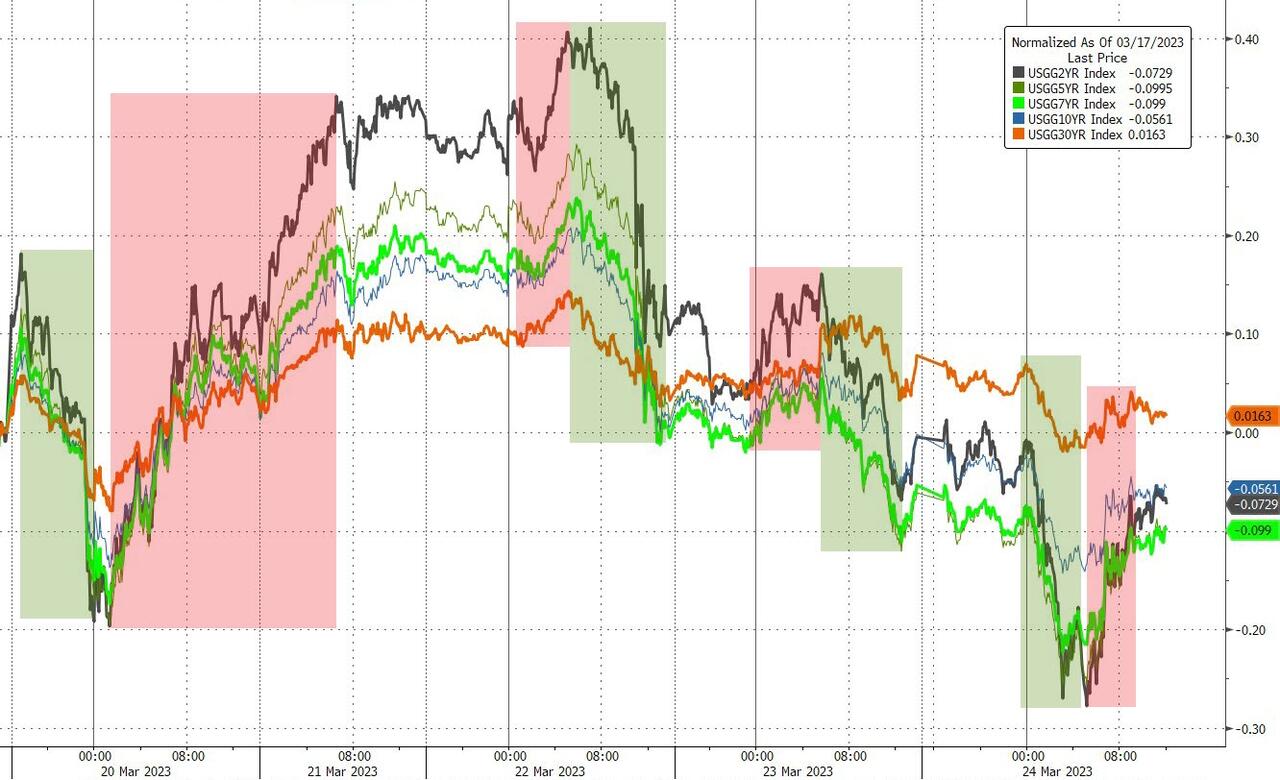

USA 10 YR BOND YIELD: 3.302 DOWN 10 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.6130 DOWN 7 BASIS PTS/

USA 2 YR BOND YIELD: 3.613DOWN 7 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.07…

GREAT BRITAIN/10 YEAR YIELD: 3.189% DOWN 57BASIS PTS

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

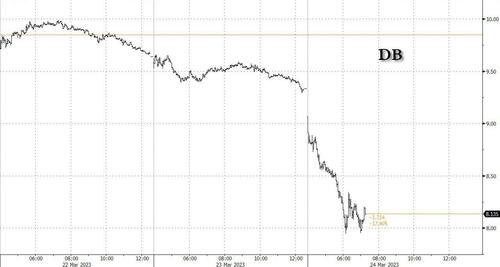

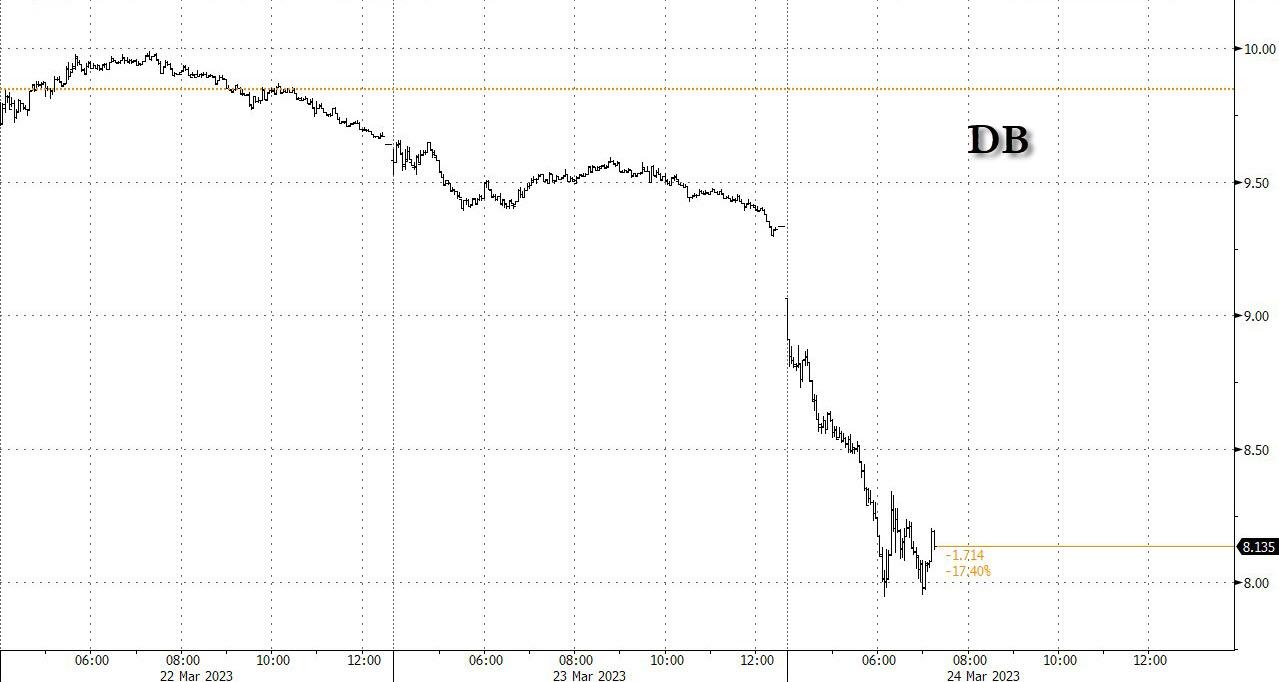

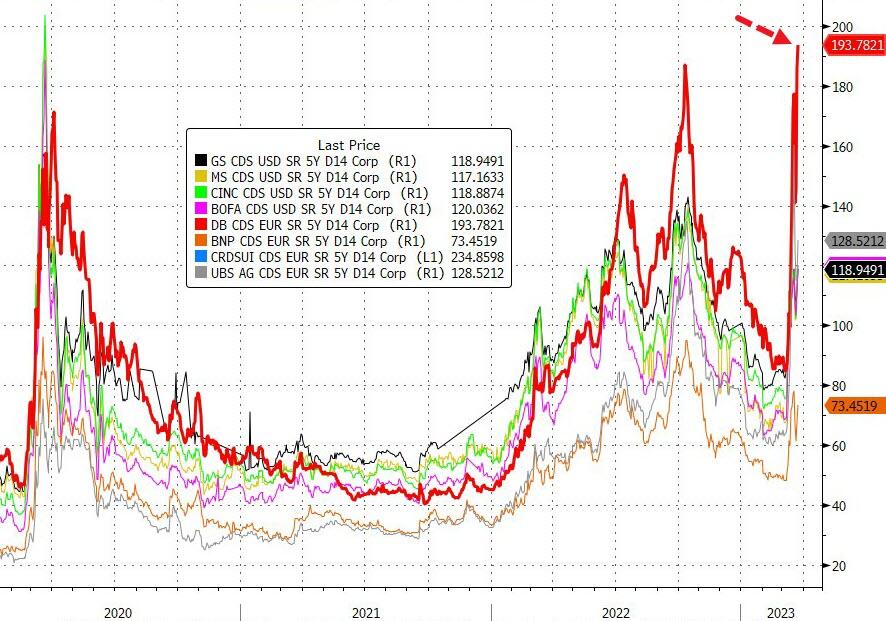

Futures Tumble, Treasuries And Rate Cut Odds Soar Amid Panic That Deutsche Bank Is The Next To Go

FRIDAY, MAR 24, 2023 – 03:09 PM

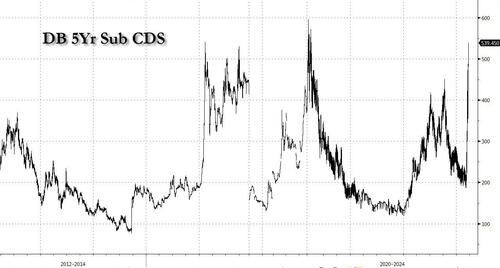

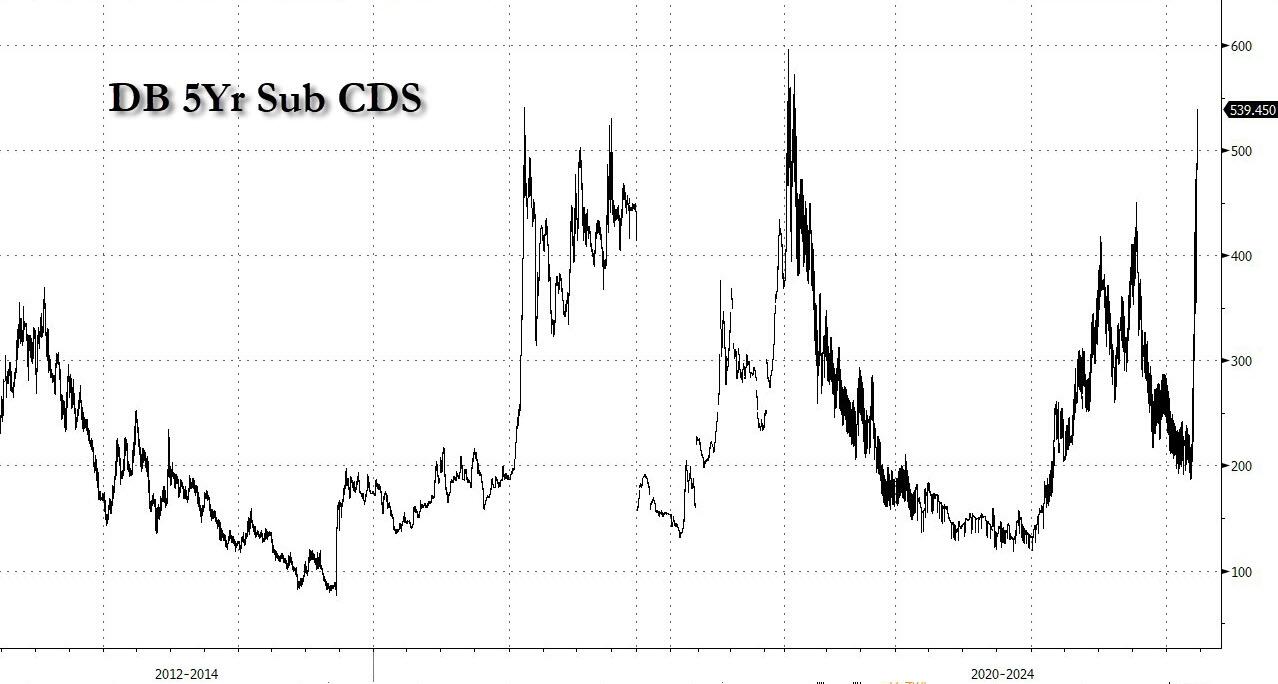

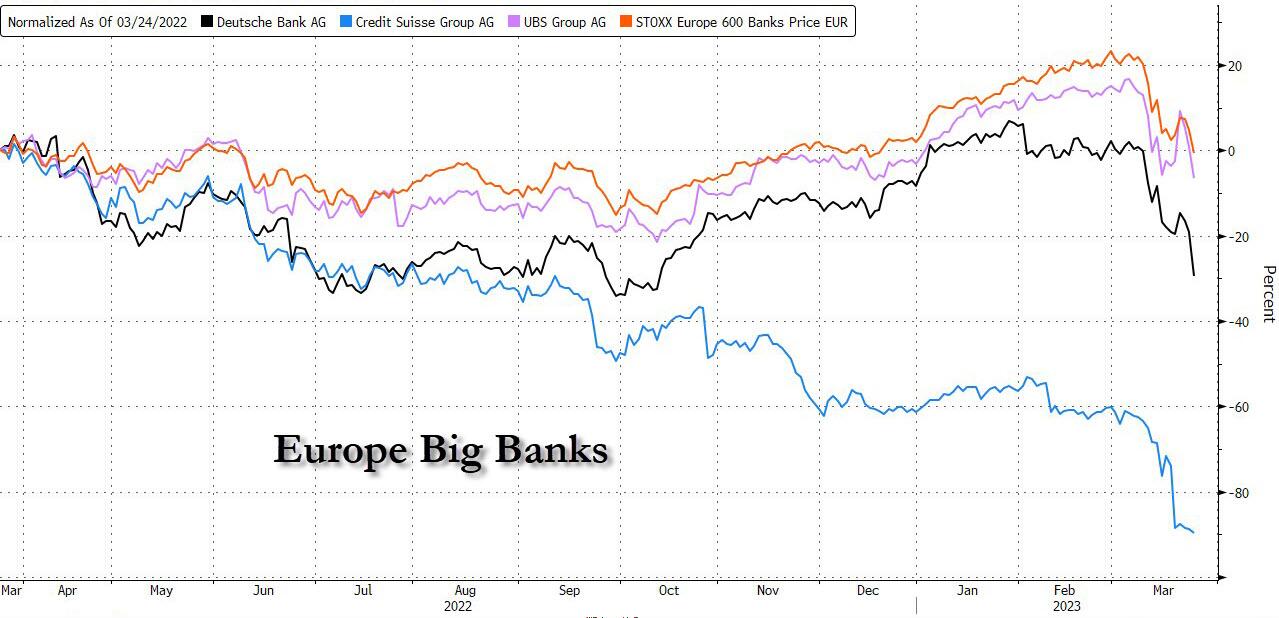

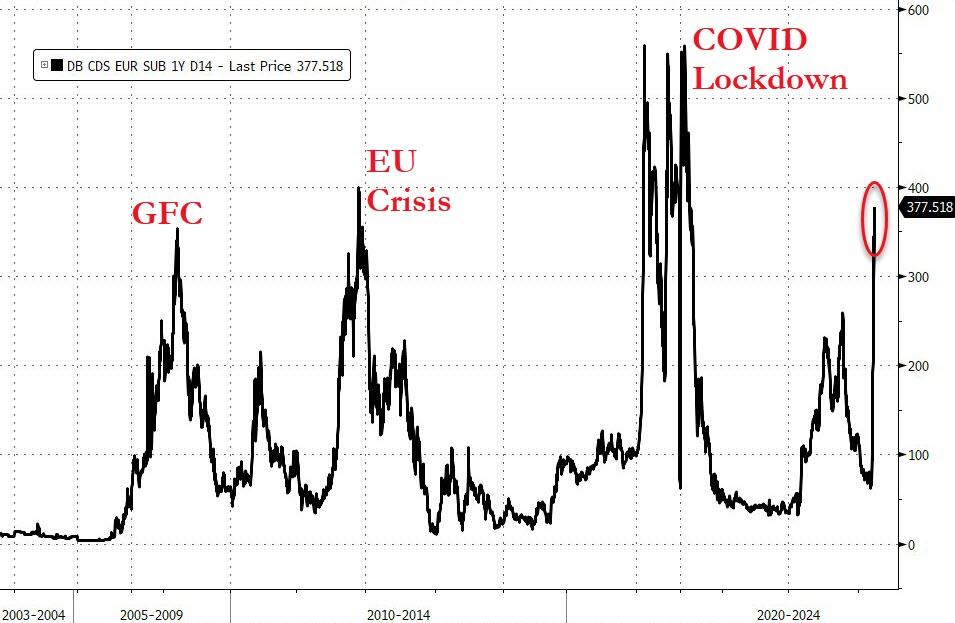

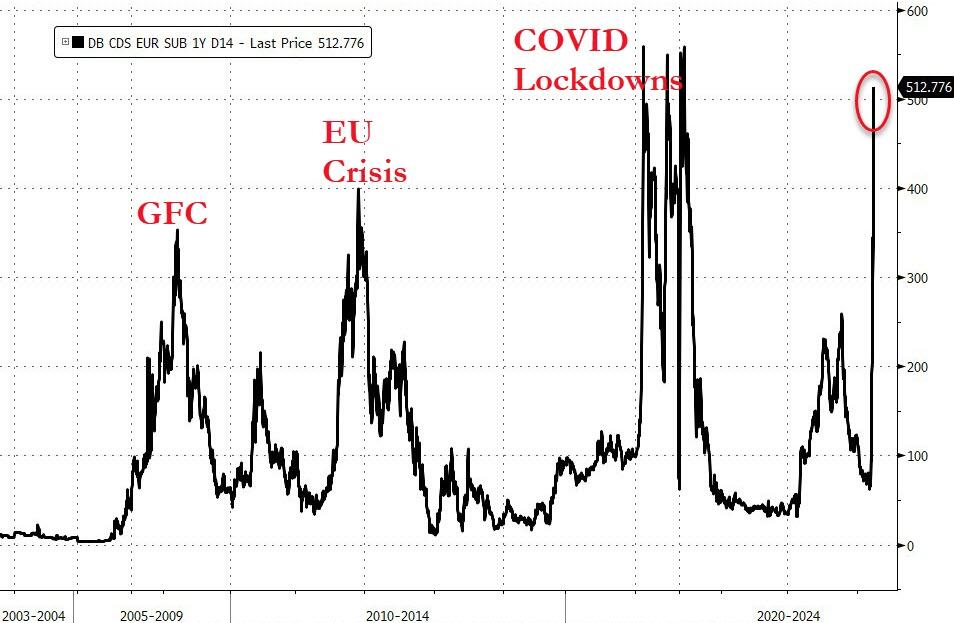

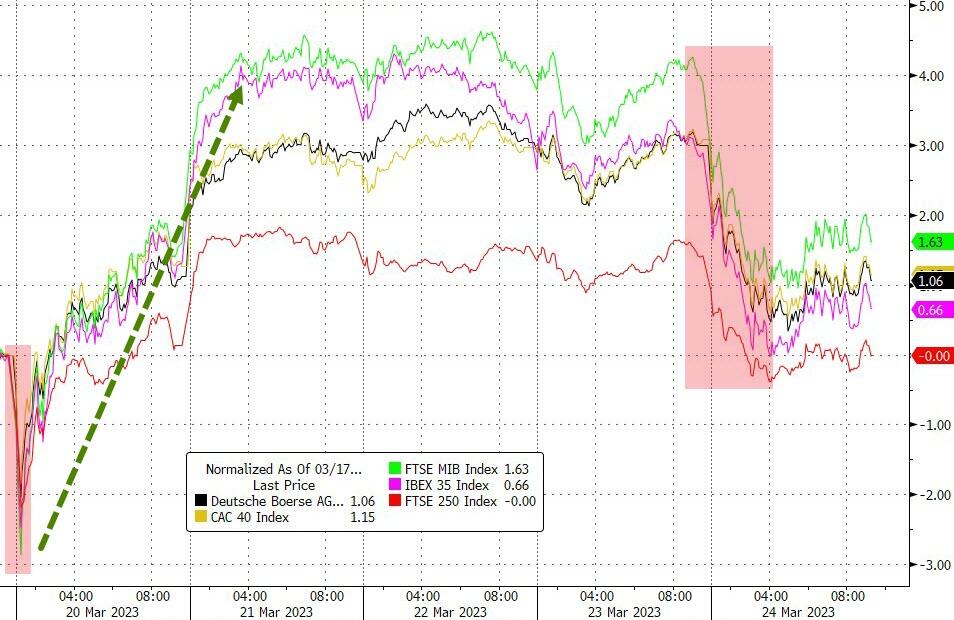

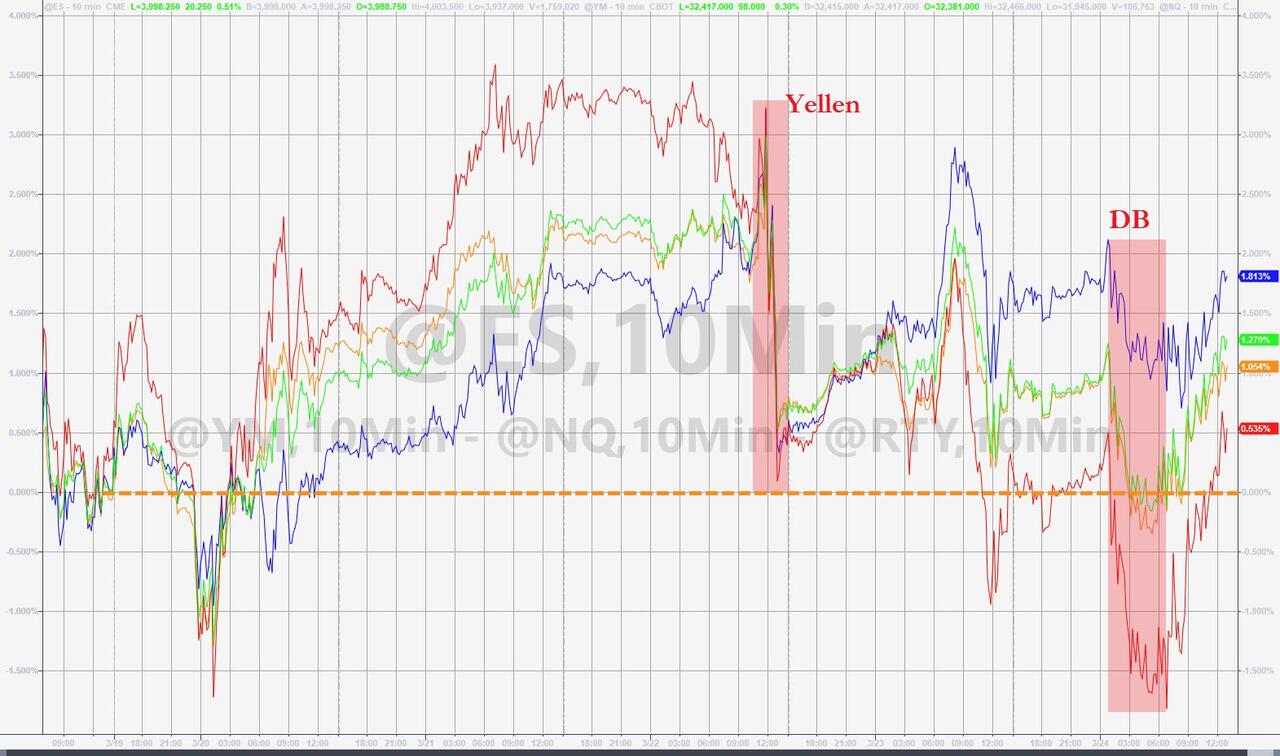

Yesterday, while attention was still focused on the US banking system and the ongoing botched response by the Fed and especially the Treasury’s senile Secretary, who more than two weeks after SIVB collapsed, have still not been able to stabilize confidence in banks – thereby assuring the US is about to slam head first into a brutal recession, just as Biden ordered to contain inflation, as US consumer spending is now in freefall – we pointed out that something bad was taking place in Europe: the credit default swaps of perpetually semi-solvent banking giant Deutsche Bank were quietly blowing out to multi-year highs.

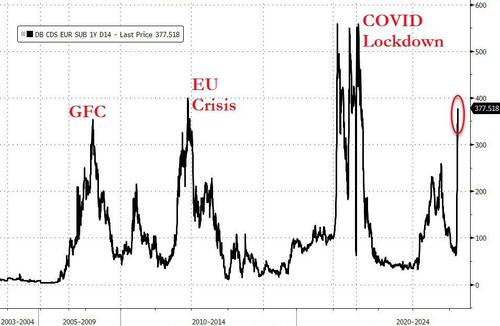

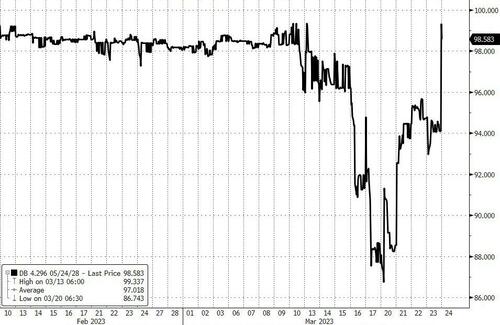

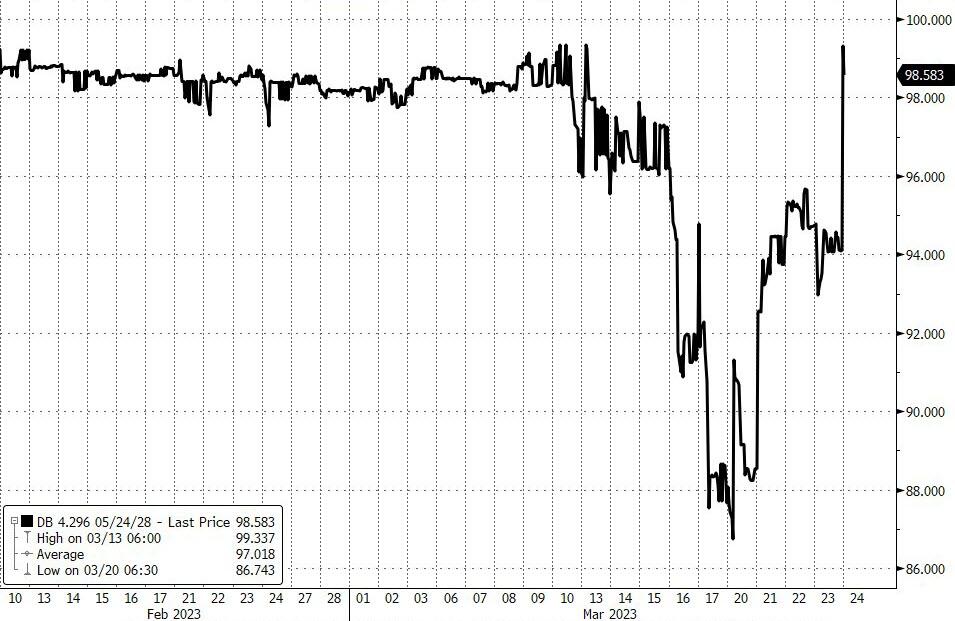

Well, we didn’t have long to wait before everyone else also noticed and this morning it’s official: the crisis has shifted to Germany’s and Europe’s largest TBTF bank, with even Bloomberg now writing that Deutsche Bank “has become the latest focus of the banking turmoil in Europe as ongoing concern about the industry sent its shares slumping the most in three years and the cost of insuring against default rising.” The bank – which has staged a recovery in recent years after a series of crises that nearly brought it down – said Friday it will redeem a tier 2 subordinated bond early. And while such moves are usually intended to give investors confidence in the strength of the balance sheet, though the share price reaction suggests the message isn’t getting through, and the stock plunged 13% in German trading…

… while DB’s CDS has exploded to level surpassing the bank’s near-collapse in 2016, and is about to take out the covid wides.

“It is a clear case of the market selling first and asking questions later,” said Paul de la Baume, senior market strategist at FlowBank SA. “Traders do not have the risk appetite to hold positions through the weekend, given the banking risk and what happened last week with Credit Suisse and regulators.”

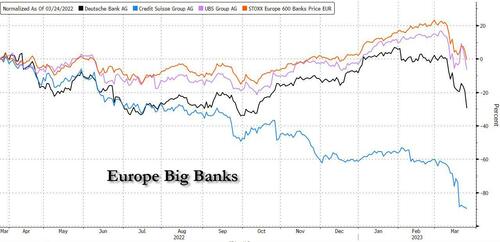

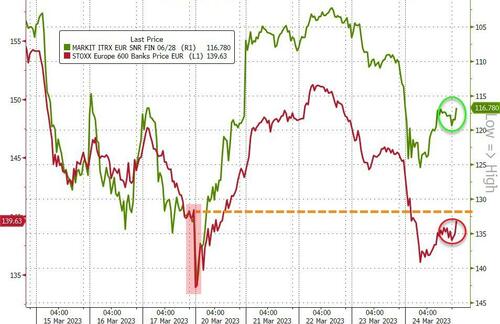

It wasn’t just Deutsche Bank: UBS Group AG shares also dropped as Bloomberg reported that it’s one of the banks under scrutiny in a US Justice Department probe into whether finncial professionals helped Russian oligarchs evade sanctions, according to people familiar with the matter. In any case, the sudden, violent spike in DB default risk which quickly carried over to all big European banks, and which will not reverse until first the ECB then the Fed both cut rates…

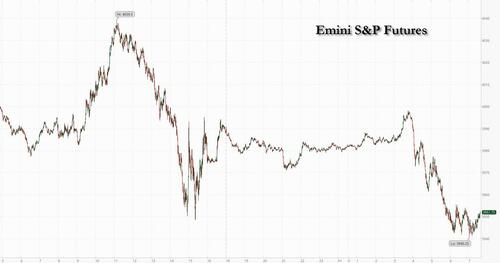

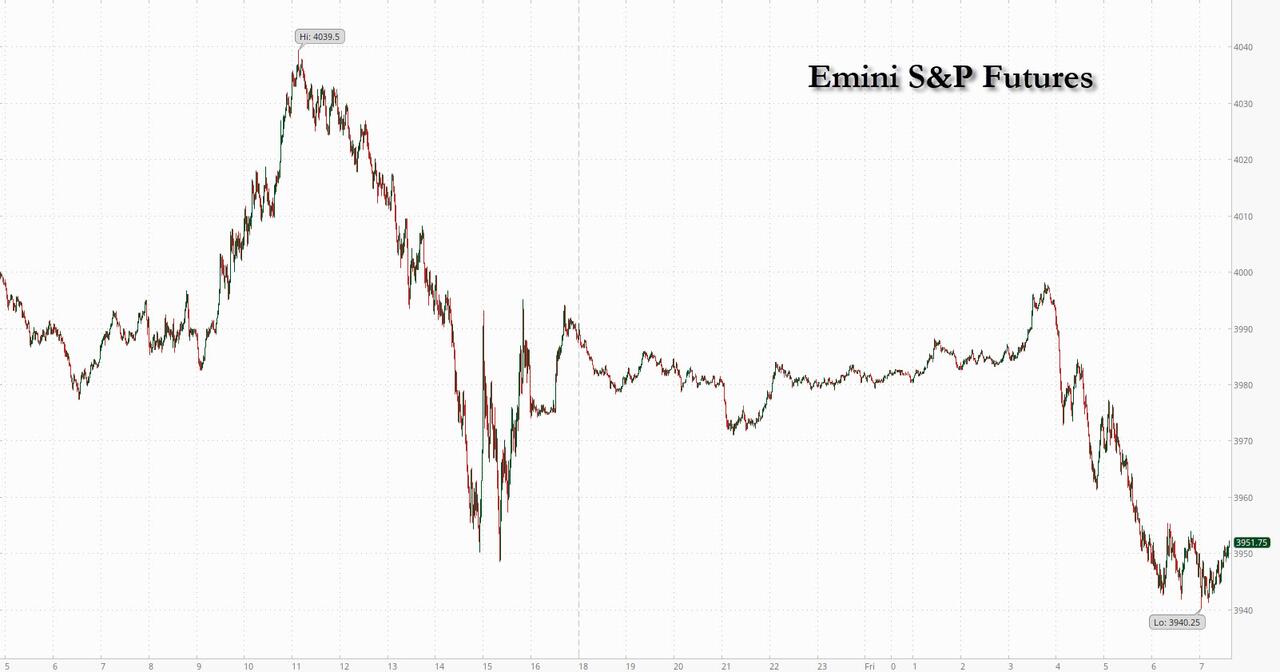

… sent broader risk sentiment reeling with S&P 500 futures at session lows, sliding 1% to 3940.

While there was no one big story setting off these moves. It could be a rush to havens heading into the weekend as traders wait for another shoe to drop — which has been a theme during recent weekends.

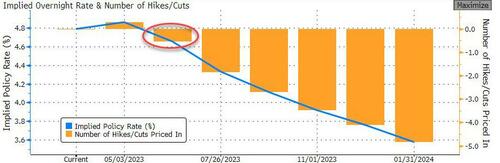

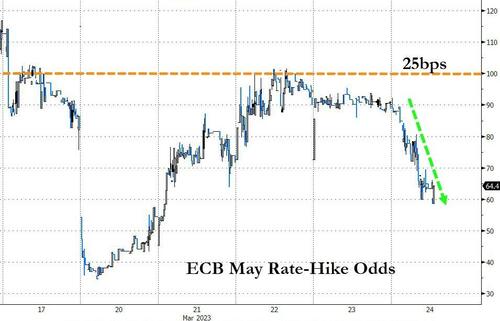

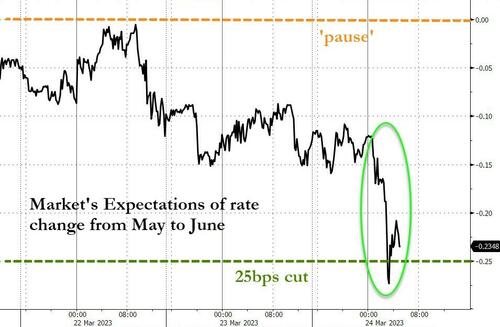

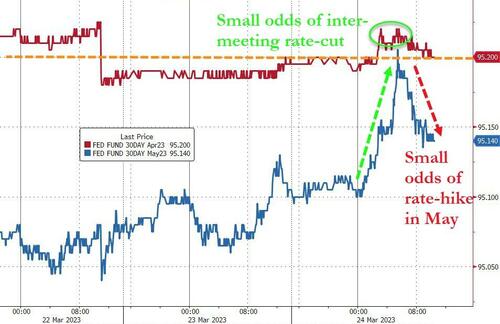

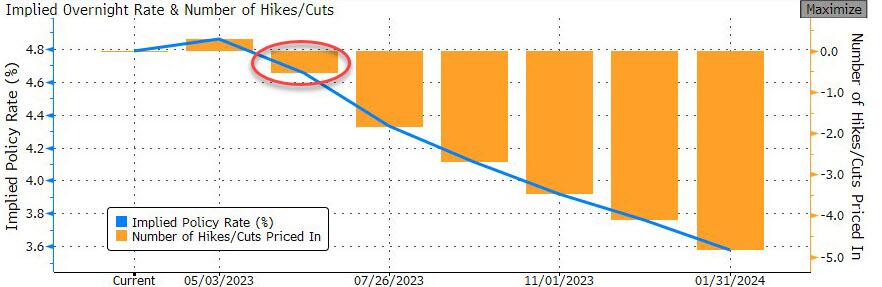

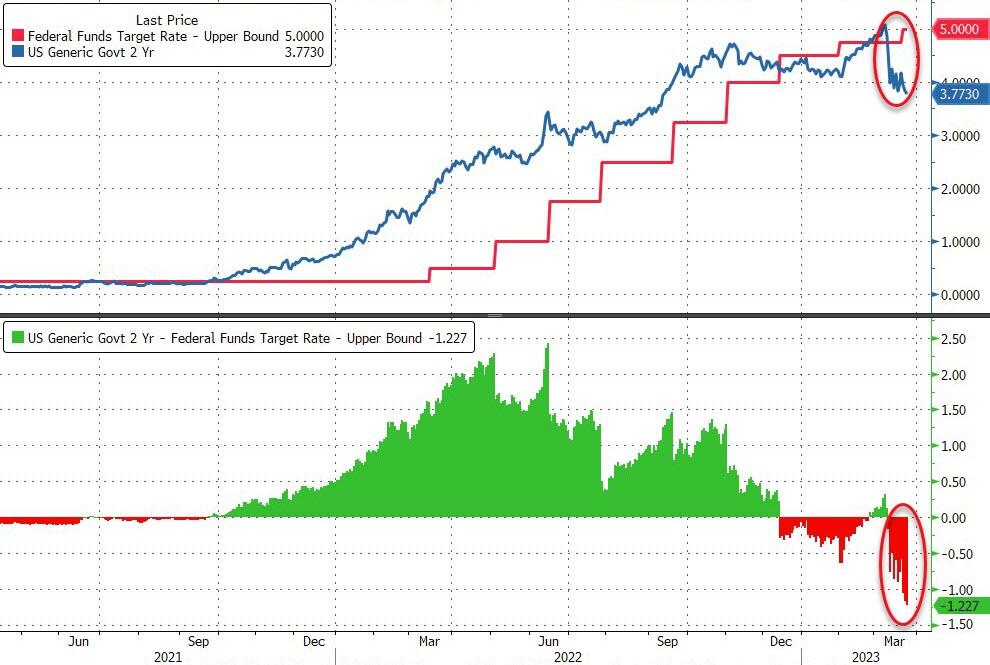

In any case, the latest global equity rout and bank crisis which is now spreading to TBTF banks has sent bond yields crashing with the 2-year US yield plumbing new session lows, breaking down as low as 3.55%, and the resulting shockwave has collapsed odds of another rate hike in May to just 28% while the odds of a rate cut in June have exploded to 83% as the Fed’s pivot finally arrives just on time: with the Fed having again broken the global financial system.

In premarket trading, First Republic Bank swung between gains and losses as investors digested Treasury Secretary Janet Yellen’s comments about regulators being prepared to take additional steps to guard bank deposits if warranted. Fellow regional banks and bigger lenders decline, and after a volatile session on Thursday took the stock’s March slump to 90%. Block fell another 5%, extending Thursday’s 15% plunge as it announced potential legal action against short seller Hindenburg Research for its report on the payment processor. Here are some other notable premarket movers:

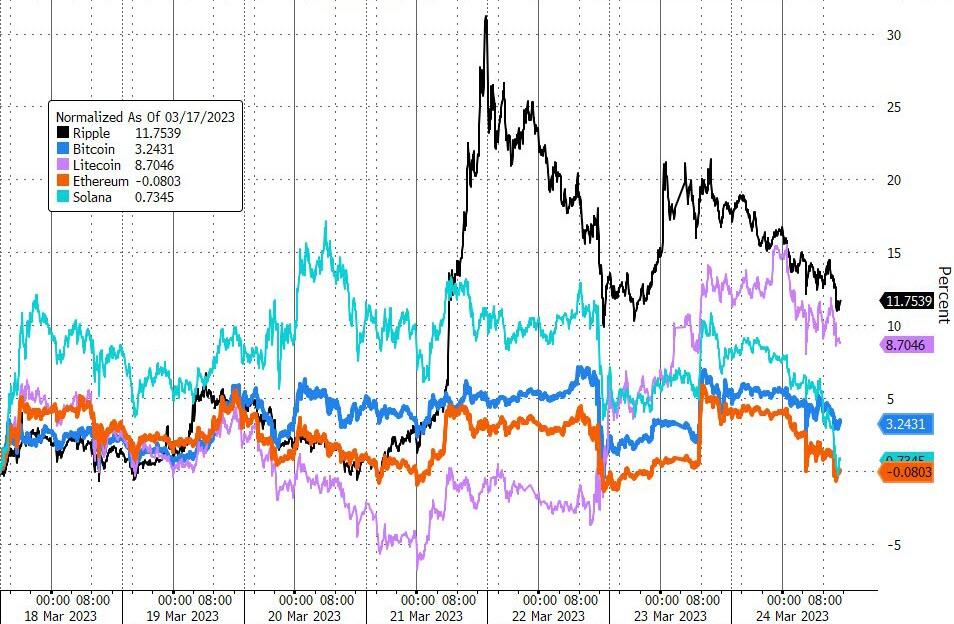

US cryptocurrency-exposed stocks decline, taking a pause from recent gains as the price of Bitcoin falls amid broader risk-off sentiment. Marathon Digital (MARA US) slid 0.9%, Hut 8 Mining Corp (HUT US) -1%, Coinbase (COIN US) -1.9%, Riot Platforms (RIOT US) -1.4%.

ReNew Energy Global gains 12% after Bloomberg reported, citing people familiar with the matter, that the Canada Pension Plan Investment Board is exploring buying the shares of the power producer that it doesn’t already own and taking the Nasdaq- listed firm private.

Joann slumped 6.2% in extended trading on Thursday after the fabric and crafts retailer reported adjusted earnings per share and Ebitda that missed the average analyst estimates, even as sales topped expectations.

Oxford Industries fell 5.5% in postmarket trading after the owner of Tommy Bahama and Lilly Pulitzer issued a forecast for net sales in the current quarter that trailed the average analyst estimate at the midpoint of the guidance range.

“Confidence is fragile, market volatility is likely to stay high, and policymakers may have to go further to make sure faith in the global financial system stays solid,” said Mark Haefele, chief investment officer at UBS Wealth Management. “Financial conditions are also likely to tighten, which increases the risk of a hard landing for the economy, even if central banks ease off on interest-rate hikes.”

“Credit and stock markets too greedy for rate cuts, not fearful enough of recession,” a team led by Michael Hartnett wrote in a note. The strategist, who was correctly bearish through last year, said investment-grade spreads and stocks will be taking a hit over the next three to six months. Global cash funds had inflows of nearly $143 billion, the largest since March 2020 in the week through Wednesday — adding up to more than $300 billion over the past four weeks, according to the note citing EPFR Global data.

European stocks are also plumbing lower, with European bank stocks sliding for a third day, and erasing weekly and yearly gains, as sentiment remains fragile on the sector. Deutsche Bank slumped nearly 15% as credit-default swaps surged amid wider concerns about the stability of the banking sector. The Stoxx 600 Banks Index is 5.3% lower as of 11:20am in London, erasing earlier weekly gains; the index is now -2.8% YTD. Meanwhile, UBS, which is not in the banking sector index, slumped as much as 8.4% as Jefferies cut its rating to hold from buy and it was among the banks under scrutiny in a US Justice Department probe into whether financial professionals helped Russian oligarchs evade sanctions. European oil stocks are also underperforming on Friday, dragging down the regional benchmark, as crude prices slump under pressure from a stronger dollar and concerns about the impact on growth of a fresh bout of stress facing the banking sector. The Energy sub-index slid as much as 4.3%, the most since March 15, while the Stoxx Europe 600 benchmark fell about 2%. Here are some other notable European movers:

Casino Guichard-Perrachon SA fell as much as 6% to a fresh record low after Moody’s cut its long-term debt rating on the company further into junk territory

Dino Polska drops as much as 5%, after its 4Q report showed that the Polish food supermarket chain is unable to maintain profitability amid inflation pressures

Smiths Group gains as much as 2.1%, after the industrial firm beat expectations on Ebita, while also surpassing projections on its full-year sales outlook

JD Wetherspoon jumps as much as 9.3% after the British pub operator posted a revenue beat for 1H, with Jefferies analysts noting resilience in like-for-like sales

Earlier in the session, Asia equities were set to snap a three-day rally as lingering concerns over the health of the banking sector pushed a gauge of the region’s financial shares lower. The MSCI Asia Pacific Index fell as much as 0.5% before trimming losses, with its 11 sectoral sub-gauges showing mixed moves. Most markets declined, led by Hong Kong’s Hang Seng Index, while Chinese tech shares extended their rally on the back of positive earnings. An index of Asian financial stocks dropped as much as 0.9%, tracking overnight declines in a measure of US financial heavyweights to the lowest since November 2020. Treasury Secretary Janet Yellen’s comments that authorities can take further steps to protect the banking system if needed failed to fully assuage concerns.

“The unease in the financial space will continue to weigh on the Asian financial sectors,” said Hebe Chen, an analyst at IG Markets Ltd. “The flip-flop in the market this week is seeing overwhelmed investors scratching their heads in the face of the mixed bag from Fed.” Even with Friday’s lackluster moves, the MSCI Asia benchmark was set to notch its best weekly performance in about two months. The shares rose earlier in the week thanks to assurances from regulators in the US and Europe over protecting the banking sector and the Federal Reserve’s dovish tilt. Meanwhile, a gauge of tech stocks in Hong Kong advanced for the fourth day close at its highest in a month. Lenovo led the gain, with JPMorgan lifting its recommendation on a bottoming of PC demand. “We like the internet sector, especially within China right now,” Marcella Chow, JPMorgan Asset Management’s global market strategist, said in an interview with Bloomberg TV. “China tech sector is attractive given improving regulatory outlook, leaner and more cost effective cost structure, improving margin.”

Japanese stocks Inched lower as worries linger over the financial sector while investors assess statements made by US Treasury Secretary Janet Yellen. The Topix Index fell 0.1% to 1,955.32 as of market close Tokyo time, while the Nikkei declined 0.1% to 27,385.25. Mitsubishi UFJ Financial Group Inc. contributed the most to the Topix Index decline, decreasing 1.1%. Out of 2,159 stocks in the index, 976 rose and 1,039 fell, while 144 were unchanged. “Assuming that the fallout from the US financial sector woes doesn’t spread significantly, Japanese stocks will likely stop its decline and pick up as the earnings period starts next month,” said Takeru Ogihara, a chief strategist at Asset Management One

Australian stocks slumped to post a seventh week of losses; the S&P/ASX 200 index fell 0.2% to close at 6,955.20, with financials the biggest drag, as the malaise hanging over the global banking sector continued to damp sentiment. The benchmark erased 0.6% for the week, the seventh straight decline, maintaining the longest losing streak since 2008. In New Zealand, the S&P/NZX 50 index fell 0.1% to 11,580.82.

Indian stocks declined for a third straight week in the longest losing streak since December spurred by a late selloff in key gauges amid risk-off sentiment in global equities. The Nifty 50 index ended just shy of entering a so-called technical correction given the index’s near 10% drop from its December peak. For the week, the Nifty 50 fell 0.9% while the Sensex declined 0.8%. The S&P BSE Sensex fell 0.7% to 57,527.10 as of 3:30 p.m. in Mumbai, while the NSE Nifty 50 Index declined 0.8% to 16,945.05. The selloff in small and mid cap counters contributed to the broader losses, with the Nifty Mid cap 100 and Nifty Small Cap 100 indexes ending nearly 2% lower each. Stocks of asset management companies were hammered after the government dropped the benefit of long-term capital gains tax for debt mutual funds in order to ensure parity in tax treatment with other such products. Shares of HDFC AMC dropped 4.1%, Aditya Birla AMC -2%, UTI AMC -4.8% and Nippon Life India AMC -1.2%. Reliance Industries contributed the most to the index decline, decreasing 2%. Out of 30 shares in the Sensex index, six rose and 24 fell

In FX, the dollar’s recent weakness, which had supported the outlook for the region’s currencies and other assets, also took a breather on Friday. The Bloomberg dollar index rose 0.3% after a six-day run of declines. The yen rallies to the highest in six weeks amid demand for haven assets due to concerns over the health of the global banking sector. The yen was the biggest gainer versus the greenback among the Group-of-10 currencies. Treasury yields continued to decline reflecting expectations for Federal Reserve rate cuts this year

“JPY’s strong performance we believe is driven by the return of its safe haven appeal, especially given that we see that Japanese banks are in a relatively better standing,” said Alan Lau, a strategist at Malayan Banking Bhd in Singapore. “Falling UST yields have also given the JPY support recently. Overall, we are positive on the yen and see the spot being on a downward trend this year with our year-end forecast at 122”

In rates, Treasuries front-end adds to Thursday’s gains, with 2-year yields richer by over 20bp on the day, as the yield continues to plumb new session lows, breaking as low as 3.55%, dropping below th 2023 lows, and steepening the curve as traders continue to price out rate-hike premium for the May meeting and start pricing for cuts as early as June. Yields were near lows of the day while rest of the curve is richer by 17bp across belly to 9bp out to long-end; front-end led gains steepens 2s10s, 5s30s by 10bp and 8bp on the day. SOFR white-pack futures surge higher, with gains led by Dec23 contract which rallied 27bp vs. Thursday close; Fed-dated OIS shows just 4bp of rate hike premium for the May policy meeting with almost a full cut then priced into the June policy meeting — around 120bp of rate hikes are then priced into year-end

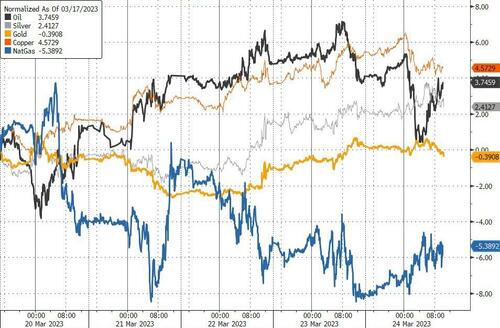

In commodities, oil slipped the most in over a week, with Brent below $75, tracking a slide in equity markets and feeling the effects of a stronger dollar. Aluminum and copper headed toward their biggest weekly gains in more than two months on increasing demand in China and bets on looser Federal Reserve policy. Uranium Energy is among the most active resources stocks in premarket trading, falling about 9%. Gold traded just shy of $2000 and is about to break solidly higher.

To the day ahead now, and data releases include the March flash PMIs from Europe and the US, along with UK retail sales for February, and the preliminary US durable goods orders for February. Otherwise from central banks, we’ll hear from the ECB’s De Cos, Nagel and Centeno, the Fed’s Bullard and the BoE’s Mann.

Market Snapshot

S&P 500 futures down 1% to 3,940

MXAP down 0.2% to 160.13

MXAPJ down 0.5% to 515.46

Nikkei down 0.1% to 27,385.25

Topix down 0.1% to 1,955.32

Hang Seng Index down 0.7% to 19,915.68

Shanghai Composite down 0.6% to 3,265.65

Sensex down 0.2% to 57,801.12

Australia S&P/ASX 200 down 0.2% to 6,955.24

Kospi down 0.4% to 2,414.96

STOXX Europe 600 down 0.7% to 443.10

German 10Y yield little changed at 2.11%

Euro down 0.4% to $1.0791

Brent Futures down 0.6% to $75.46/bbl

Gold spot down 0.3% to $1,987.17

U.S. Dollar Index up 0.30% to 102.84

Top Overnight News

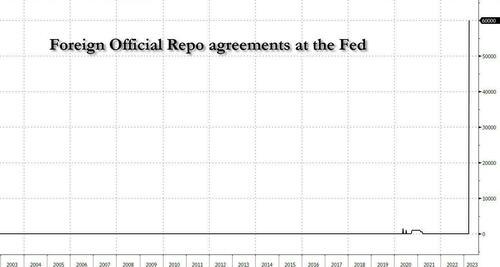

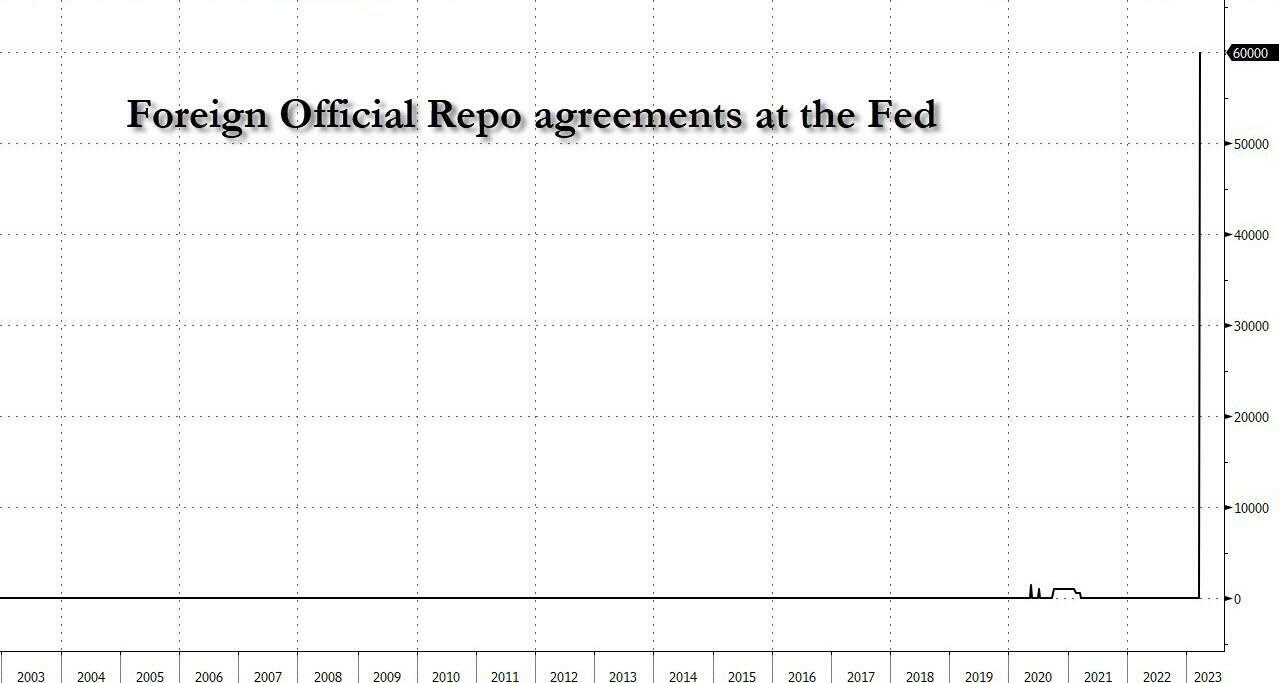

A Federal Reserve facility that gives foreign central banks access to dollar funding was tapped for a record $60 billion in the week through March 22: BBG

Deutsche Bank AG was at the center of another selloff in financial shares heading into the weekend: BBG

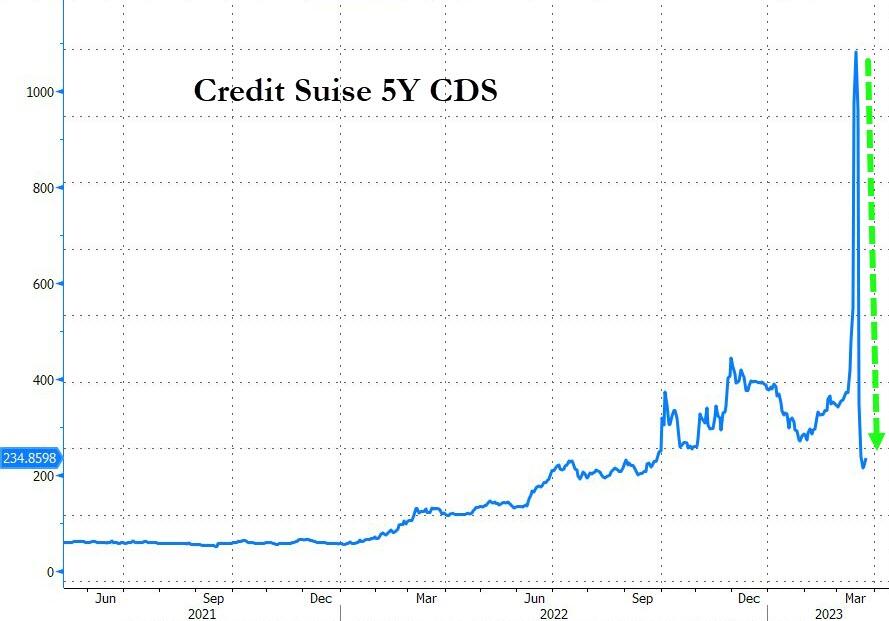

Credit Suisse Group AG and UBS Group AG are among banks under scrutiny in a US Justice Department probe into whether financial professionals helped Russian oligarchs evade sanctions, according to people familiar with the matter: BBG

Japan’s headline national CPI for Feb cools to +3.3% (down from +4.3% in Jan and inline w/the St) while core ticks higher to +3.5% (up from +3.2% in Jan and ahead of the St’s +3.4% forecast). RTRS

Copper prices will surge to a record high this year as a rebound in Chinese demand risks depleting already low stockpiles, the world’s largest private metals trader has forecast. Global inventories of the metal used in everything from power cables and electric cars to buildings have dropped rapidly in recent weeks to their lowest seasonal level since 2008, leaving little buffer if demand in China continues to pace ahead. FT

Authorities this week raided the Beijing offices of Mintz Group, detaining all five of the New York-based due diligence firm’s staff members in mainland China, the company said—an incident likely to unnerve global businesses operating in the country. WSJ

China’s top diplomat Wang Yi urged Europe to play a role in supporting peace talks for Russia’s war in Ukraine, though the US has warned Beijing’s proposals would effectively freeze the Kremlin’s territorial gains. BBG

Ukrainian troops, on the defensive for months, will soon counterattack as Russia’s offensive looks to be faltering, a commander said, but President Volodymyr Zelenskiy warned that without a faster supply of arms the war could last years. RTRS

Europe’s flash PMIs for March were mixed, with upside on services (55.6, up from 52.7 in Feb and ahead of the St’s 52.5 forecast) but downside on manufacturing (47.1, down from 48.5 in Feb and below the St’s 49 forecast). “Inflationary pressures have continued to moderate, with input prices falling sharply in manufacturing… overall input costs rose at the slowest rate since March 2021…the record easing of supply constraints marks a major reversal from the record delays seen during the pandemic” S&P

Deutsche Bank was at the center of another selloff in financials. The bank tumbled 11% in Frankfurt and default-swaps on its euro, senior debt surged to the highest since they were introduced in 2019, when Germany revamped its debt framework to introduce senior preferred notes. Other banks with high exposure to corporate lending also declined. Commerzbank slid 9% and Soc Gen 7%. BBG

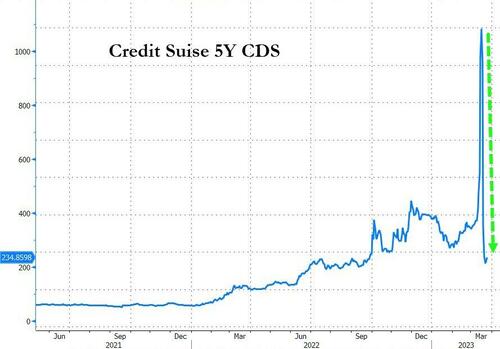

The Swiss authorities and UBS Group AG are racing to close the takeover of Credit Suisse Group AG within as little as a month, according to two sources with knowledge of the plans, to try to retain the lender’s clients and employees. RTRS

Citizens Financial is set to submit a bid for SVB’s private banking arm, Reuters reported. Customers Bancorp is also said to be exploring a deal for all or part of SVB. Carson Block said depositors at SVB and Signature Bank should have taken haircuts after regulators seized the firms. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly subdued after the recent bout of central bank rate hikes and choppy performance stateside where Wall Street just about closed higher amid a dovish market repricing of Fed rate expectations. ASX 200 was lower with risk appetite sapped by weak PMI data which returned to contraction territory. Nikkei 225 lacked conviction after the latest inflation data printed mostly in line with estimates. Hang Seng and Shanghai Comp. retreated after the central bank drained liquidity and as participants digest earnings releases, while it was also reported that the US added 14 Chinese entities to the red flag list.

Top Asian News

HKMA said Hong Kong has very little exposure to the European and US banking situation, while it needs to monitor the situation carefully for any further volatility but is not concerned about risks to the Hong Kong banking sector.

China is to extend some tax relief measures, according to local media.

Equities are back under marked pressure as banking sector concern re-intensifies within Europe, Euro Stoxx 50 -2.3% & ES -0.8%. Specifically, the European banking index SX7P -5.0% is the standout laggard amid broad-based pressure in banking names as CDS’ for the stocks continue to rise alongside focus on the redemption of notes by Deutsche Bank and Lloyds; currently, Deutsche Bank -12% is the Stoxx 600 laggard. Stateside, futures are pressured in tandem with the above price action though with the magnitude less pronounced ahead of the arrival of US players and as we await potential updates to the regions own banking names. Apple (AAPL) supplier Pegatron (4982 TW) is reportedly looking to open a second factory within India, to construct the latest iPhone models, via Reuters citing sources.

Top European News

ECB is likely to reassure EU leaders regarding bank stability on Friday and is to call for EU deposit insurance, according to Reuters.

ECB’s Nagel says it is necessary to increase policy rates to sufficiently restrictive levels, whilst the APP wind down should accelerate from Q3. Domestic price pressures are likely to last for longer, whilst underlying inflation is increasingly concerning. There are signs of second-round effects from inflation-induced higher wage increases.

ECB’s Nagel says there is often a bumpy road after similar instances in the banking sector, not surprising there have been market moves. On Deutsche Bank’s share slide, ECB’s Nagel will not comment.

BoE’s Bailey says rates will rise again if firms hike prices, via BBC; “If all prices try to beat inflation we will get higher inflation,”

Bank headlines

Deutsche Bank (DBK GY) announces a decision to redeem its USD 1.5bln fixed to fixed reset rate subordinated Tier 2 notes, due 2028. Lloyds (LLOY LN) has issued a notice of redemption for the entire outstanding principal amount of the USD 1bln 0.695% senior callable fixed-to-fixed rate notes due 2024. In terms of the accompanying risk-off price action, the desk notes the early redemption(s) can perhaps be taken as a negative if we assume the justification is that the bank(s) expect to see more dovishness/risk-off before the next fixed-to-fixed rate adjustment.

UBS Wealth Management head Khan offered a retention package to Credit Suisse’s Asia staff in Hong Kong town hall which focuses on stabilising the Credit Suisse Asia team and boosting banker confidence, according to sources.

Credit Suisse (CSGN SW) and UBS (UBSG SW) are among the banks facing a US Russia-sanctions probe.

Fed Balance Sheet: 8.784tln (prev. 8.689tln); Total factors supplying reserve funds 8.784tln (prev. 8.689tln); Loans 354.191bln (prev. 318.148bln); Bank Term Funding Program 53.669bln (prev. 11.943bln); Other credit extensions 179.8bln (prev. 142.8bln).

FX

The USD is benefitting from the marked risk-off move with the index surpassing 103.00 from a 102.50 base in short-order and extending further to a 132.25+ peak since.

Action which comes to the detriment of peers ex-JPY, as USD/JPY has been lower by roughly a full point at worse (best) given its haven allure and with JPY repatriation factoring.

Notably, CHF is outperforming its peers, ex-JPY, but is still softer overall as its proximity/exposure to the European banking situation continues to overshadow traditional haven status vs USD though it is markedly outperforming the EUR as the focus is on EZ banks this morning.

As such, EUR is the standout laggard with EUR/USD down to a 1.0722 trough vs initial 1.0830 best, antipodeans are similarly hampered given their high-beta status and after Thursdays firmer action.

Cable failed to see a lasting benefit from the morning’s retail data while the subsequent PMIs were slightly softer than expected; but, again, the action is very much USD-driven.

PBoC set USD/CNY mid-point at 6.8374 vs exp. 6.8367 (prev. 6.8709)

Fixed Income

Core benchmarks are experiencing a marked bid given the risk-off price action that we are seeing with an accompanying dovish re-pricing being seen for Central Banks.

Specifically, Bunds have surpassed 139.50 and USTs above 1.17 with the respective 10yr yields down to 2.02% and 3.29% with market pricing in favour of an unchanged outcome at the next ECB and Fed meetings as such.

Gilts are moving in tandem with EGB/UST peers and have eclipsed 107.00; BoE pricing is now heavily in favour of an unchanged outcome at the May meeting.

Commodities

Commodities diverge given the marked risk-off action with crude and base metals pressured while precious metals glean incremental support as the USD offsets the benefit of haven demand.

Specifically, WTI and Brent are under USD 68.00/bbl and USD 74.00/bbl respectively which places them at the mid/lower-end of the current WTD USD 64.12-71.67/bbl and USD 70.12-77.44/bbl parameters.

Spot gold is incrementally firmer though is yet to convincingly surpass USD 2k/oz while base metals are dented by the aforementioned tone with 3-month LME Copper slipping further below 9k to a USD 8940 low.

Russia could recommend a temporary halt to wheat and sunflower exports, via Vedomosti; due to the sharp decline in prices.

US base at North-east Syria’s Al-Omar oil field has been targeted in an attack, according to security sources cited by Reuters.

UBS maintains a positive outlook on Gold and targets USD 2050/oz by the end of the year.

Geopolitics

Ukraine’s top ground forces commander said Ukrainian troops are to launch a counterassault soon as Russia’s large winter offensive weakens without capturing the eastern city of Bakhmut, according to Reuters.

Russian Security Council Deputy Chairman Medvedev says cannot rule out that Russian forces will need to reach Kyiv or Lviv to ‘destroy the infection’, according to RIA.

US Pentagon said the US conducted air strikes in Syria which targeted an Iranian-backed group in response to a deadly UAV attack, according to Reuters and Wall Street Journal.

US Treasury Secretary Yellen said sanctions on Iran have created a real economic crisis in that country and the US is constantly looking at ways to strengthen Iran sanctions but added that sanctions may not be sufficient to change a country’s behaviour, according to Reuters.

China’s Defence Ministry said it monitored and drove away a US destroyer which entered the South China Sea Paracel Islands on Friday again and sternly demands the US to immediately stop such provocations, according to Reuters.

North Korea said it conducted an important weapon test and firing drill from March 21st-23rd, while it added that it conducted a new underwater attack system in which it tested a new nuclear underwater attack drone and launched strategic cruise missiles. Furthermore, North Korea said its leader Kim guided the military activities and that Kim seriously warned enemies to stop reckless anti-North Korea war drills, according to KCNA.

South Korean President Yoon said they will step up security cooperation with the US and Japan against North Korea’s nuclear and missile provocations, while he said they will make sure North Korea pays the price for its reckless provocations, according to Reuters.

US Event Calendar

08:30: Feb. Durable Goods Orders, est. 0.2%, prior -4.5%

08:30: Feb. -Less Transportation, est. 0.2%, prior 0.8%

08:30: Feb. Cap Goods Orders Nondef Ex Air, est. -0.2%, prior 0.8%

08:30: Feb. Cap Goods Ship Nondef Ex Air, est. 0.2%, prior 1.1%

09:45: March S&P Global US Manufacturing PM, est. 47.0, prior 47.3

09:45: March S&P Global US Services PMI, est. 50.2, prior 50.6

09:45: March S&P Global US Composite PMI, est. 49.5, prior 50.1

10:00: Revisions: Wholesale Inventories

11:00: March Kansas City Fed Services Activ, prior 1

DB’s Jim Reid concludes the overnight wrap

There’s a bad bout of conjunctivitis going round the school at the moment and every member of the family has now had it with the last hold out being me until yesterday. So my eyes are a bit blurry this morning looking at screens. One of the twins believes he has conjunctiv”eye-test” as he thinks it’s called. If he hadn’t given it to me I’d think he was quite sweet.

As I was looking at screens last night through weepy eyes, markets looked like they were trying to normalise. However late weakness in financials again was a big drag on the last couple of hours of US trading. Just after the European close, the S&P 500 was up over +1.2% and looked set to reverse a good portion of the previous day’s losses. However by the end of the session, further weakness in banks and cyclicals more broadly left the index only +0.30%, but having been down nearly half a percent with 30 minutes left in trading. The VIX, which intraday was near its lowest level (20.18) since the SVB issues became prominent, ended the day 0.35pts higher at 22.6. Today we’ll see if the flash PMIs around the world are impacted by the early part of the mini banking crisis we’ve seen in the last two weeks. So watch the European and US numbers carefully.

The renewed weakness in banks yesterday actually started in Europe with the STOXX Banks index down -2.27%. The STOXX 600 recovered from an intraday low of almost -1.0% to finish -0.21% lower overall. CDS markets highlighted the stress in European financials as the Subordinated Financial CDS index widened (+20bps) for the first time since last Friday – before the CS-UBS merger news – while the Senior CDS index was +9bps wider. In the US, the Regional bank ETF, KRE, was down -2.78% yesterday whilst the broader KBW Bank index was -1.73% lower as liquidity concerns of the smaller banks continue to permeate.

Staying with bank liquidity, after the US close last night, the Fed’s weekly balance sheet data showed that the use of the Fed’s discount window was down from $153bn to $110bn, while the credit deployed to SVB and Signature was up from 143bn to 180bn, and lastly the new emergency bank lending facility (BTFP) was up from $12bn to $54bn. So net of the two failed banks there was little change, indicating that banks were not finding it necessary to access cheap capital. The market should look favourably on that from a contagion standpoint. Overnight S&P and Nasdaq futures are both up around +0.2% and 2 and 10yr UST yields are both around -4.5bps lower as we go to press.

Far before that balance sheet data came out the S&P 500 opened much stronger, up +1.8% and stayed buoyant through the first three hours of trading, before the weakness in regional banks weighed on overall sentiment throughout the US afternoon. This was most pronounced with a bout of selling just before Treasury Secretary Yellen spoke in front of a House of Representatives subcommittee an hour or so before the US close. The selling might have been nervousness ahead of her remarks, given the negative market reaction to her comments before the Senate on Wednesday. Regardless, the S&P actually saw a +1.0% whipsaw move when Yellen said that the US government was “prepared for additional deposit action if warranted.” This was quickly faded, with the index continuing to trade between smaller gains and losses until it ended the day +0.30% higher.

Despite the weakness in banks and Energy (-1.4%) on the back of lower oil prices, the S&P finished in the green thanks to Tech stocks outperforming on the lower rate outlook. The FANG+ index surged by +2.53%, whilst the NASDAQ 100’s gains (+1.19%) mean it’s now up nearly 20% from its lows at the end of December, almost meeting the traditional definition of a bull market.

On the rates side, 10yr Treasury yields held up for the most part, with the 10yr yield -0.08bps to 3.427%. Short-dated rates were another story, with 2yr yields -10.4bps lower to 3.833% fully on the back of lower inflation expectations (-13.3bps), while 5yr rates were -7.2bps lower. This saw the 2s10s yield curve normalise a further +9.4bps yesterday to -41.3bps, which is the least inverted the curve has been in over 5 months. This drop in yields led by inflation expectations was also borne out in fed future pricing, where the market now only sees a 40% chance of a 25bp hike during the May meeting.

In Europe there was a sharp decline in longer dated yields that accelerated later in the session, with yields on 10yr bunds (-13.3bps), OATs (-12.3bps) and BTPs (-10.4bps) all moving lower. Furthermore, those moves came in spite of some of the ECB’s hawks calling for further tightening. For example, Austria’s Holzmann said that the ECB would “probably have to add” to its rate hikes at the next meeting in May. And the Netherlands’ Knot said that “I still think that we need to make another step in May, but I don’t know the size of that”.

Speaking of central banks, we had the Bank of England’s latest decision yesterday, who hiked rates by 25bps as expected. That takes the Bank Rate up to a post-2008 high of 4.25%, and 7 of the 9 MPC members were in support, with the other 2 preferring to remain on hold. Looking forward, the BoE said that they still expected inflation “to fall significantly” in Q2, aided by falling energy prices and the government’s move to extend the Energy Price Guarantee in last week’s budget. And when it comes to inflationary pressures, they said that if “there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required.”

In his review (link here), our UK economist writes that while he sees some upside to growth and pay, there are downsides to services CPI and credit conditions, making the next meeting in May a difficult decision to call. On balance, he sees more downside risks than upside, and holds onto his call for the Bank Rate to remain where it is at 4.25%, with the risks tilted to one further hike.

Whilst we’re on central banks, yesterday also saw the Swiss National Bank hike rates by 50bps, taking the policy rate up to 1.5%. There were a number of hawkish-leaning details, including an upgrade in their inflation forecast relative to December, and their statement said that inflation was “still clearly above the range the SNB equates with price stability.” In the meantime, SNB President Jordan said that a “Credit Suisse bankruptcy would have had serious consequences for national and international financial stability and for the Swiss economy” and that “taking this risk would have been irresponsible.”

This morning in Asia equity markets are lower with the KOSPI (-0.72%) the biggest underperformer with the Nikkei (-0.41%), the Shanghai Composite (-0.54%), the CSI (-0.27%) and the Hang Seng (-0.21%) trading in negative territory.

Data from Japan has shown that consumer price inflation (+3.3% y/y) slowed in line with forecasts but for the first time in 13 months in February, compared to a +4.3% increase in January, mainly due to the effect of government’s energy subsidy program. At the same time, core-core CPI (excluding both fresh food and fuel costs) advanced further to +3.5% y/y in February (v/s +3.4% expected), notching the fastest y-o-y gain since January 1982. It followed a +3.2% increase in January highlighting the underlying inflationary pressures. Staying with Japan, the preliminary estimate for manufacturing PMI showed that sector activity remained in contraction for the fifth consecutive month in March after the reading came in at 48.6, albeit up from the previous month’s final reading of 47.7 as output and new orders remained under pressure. On the contrary, activity in the services sector expanded for the seventh straight month in March as the PMI edged up to 54.2, recording the fastest pace since October 2013, against prior month’s reading of 54.0.

Elsewhere, manufacturing as well as services in Australia slipped into contractionary territory as the manufacturing PMI fell to 48.7 in March from 50.5 in February with the services PMI deteriorating to 48.2 from the prior print of 50.7.

When it came to yesterday’s data, the US weekly initial jobless claims came in at a 3-week low of 191k over the week ending March 18 (vs. 197k expected), pointing to continued strength in the labour market. Continuing claims saw a small increase to 1694k (1690k expected) and remains in a slight up-trend but not at a concerning level yet. Meanwhile, the new home sales data for February showed a modest rise to an annualised rate of 640k (vs. 650k expected), taking them up to a 6-month high. Over in the Euro Area, the European Commission’s preliminary consumer confidence data for March showed a decline to -19.2 (vs. -18.2 expected), marking a reduction after 5 consecutive monthly improvements.

To the day ahead now, and data releases include the March flash PMIs from Europe and the US, along with UK retail sales for February, and the preliminary US durable goods orders for February. Otherwise from central banks, we’ll hear from the ECB’s De Cos, Nagel and Centeno, the Fed’s Bullard and the BoE’s Mann.

AND 2 b) NOW NEWSQUAWK (EUROPE/REPORT)

Risk off returns as banking concerns re-intensify within Europe; Deutsche Bank -12% – Newsquawk US Market Open

FRIDAY, MAR 24, 2023 – 02:05 PM

Equities are back under marked pressure as banking sector concern re-intensifies within Europe, Euro Stoxx 50 -2.3% & ES -0.8%.

Specifically, the European banking index SX7P -5.0% is the standout laggard as CDS’ for the stocks continue to rise & focus on the redemption of notes by Deutsche Bank and Lloyds; DBK -12%.

USD and JPY benefit from the risk move with other G10 peers all succumbing to the USD’s upside, DXY above 103.25 at best.

Core fixed benchmarks are bid with yields lower and a marked dovish re-pricing been seen for Central Banks.

Commodities diverge given the marked risk-off action with crude and base metals pressured while precious metals glean incremental support as the USD offsets the benefit of haven demand.

Looking ahead, highlights include US Flash PMIs, US Durable Goods, Speeches from Fed’s Bullard & BoE’s Mann.

Or why not try Newsquawk’s squawk box free for 7 days?

BANKS

Deutsche Bank (DBK GY) announces a decision to redeem its USD 1.5bln fixed to fixed reset rate subordinated Tier 2 notes, due 2028. Lloyds (LLOY LN) has issued a notice of redemption for the entire outstanding principal amount of the USD 1bln 0.695% senior callable fixed-to-fixed rate notes due 2024. In terms of the accompanying risk-off price action, the desk notes the early redemption(s) can perhaps be taken as a negative if we assume the justification is that the bank(s) expect to see more dovishness/risk-off before the next fixed-to-fixed rate adjustment.

UBS Wealth Management head Khan offered a retention package to Credit Suisse’s Asia staff in Hong Kong town hall which focuses on stabilising the Credit Suisse Asia team and boosting banker confidence, according to sources.

Credit Suisse (CSGN SW) and UBS (UBSG SW) are among the banks facing a US Russia-sanctions probe.

Fed Balance Sheet: 8.784tln (prev. 8.689tln); Total factors supplying reserve funds 8.784tln (prev. 8.689tln); Loans 354.191bln (prev. 318.148bln); Bank Term Funding Program 53.669bln (prev. 11.943bln); Other credit extensions 179.8bln (prev. 142.8bln).

EUROPEAN TRADE

EQUITIES

Equities are back under marked pressure as banking sector concern re-intensifies within Europe, Euro Stoxx 50 -2.3% & ES -0.8%.

Specifically, the European banking index SX7P -5.0% is the standout laggard amid broad-based pressure in banking names as CDS’ for the stocks continue to rise alongside focus on the redemption of notes by Deutsche Bank and Lloyds; currently, Deutsche Bank -12% is the Stoxx 600 laggard.

Stateside, futures are pressured in tandem with the above price action though with the magnitude less pronounced ahead of the arrival of US players and as we await potential updates to the regions own banking names.

Apple (AAPL) supplier Pegatron (4982 TW) is reportedly looking to open a second factory within India, to construct the latest iPhone models, via Reuters citing sources.

The USD is benefitting from the marked risk-off move with the index surpassing 103.00 from a 102.50 base in short-order and extending further to a 132.25+ peak since.

Action which comes to the detriment of peers ex-JPY, as USD/JPY has been lower by roughly a full point at worse (best) given its haven allure and with JPY repatriation factoring.

Notably, CHF is outperforming its peers, ex-JPY, but is still softer overall as its proximity/exposure to the European banking situation continues to overshadow traditional haven status vs USD though it is markedly outperforming the EUR as the focus is on EZ banks this morning.

As such, EUR is the standout laggard with EUR/USD down to a 1.0722 trough vs initial 1.0830 best, antipodeans are similarly hampered given their high-beta status and after Thursdays firmer action.

Cable failed to see a lasting benefit from the morning’s retail data while the subsequent PMIs were slightly softer than expected; but, again, the action is very much USD-driven.

PBoC set USD/CNY mid-point at 6.8374 vs exp. 6.8367 (prev. 6.8709)

Core benchmarks are experiencing a marked bid given the risk-off price action that we are seeing with an accompanying dovish re-pricing being seen for Central Banks.

Specifically, Bunds have surpassed 139.50 and USTs above 1.17 with the respective 10yr yields down to 2.02% and 3.29% with market pricing in favour of an unchanged outcome at the next ECB and Fed meetings as such.

Gilts are moving in tandem with EGB/UST peers and have eclipsed 107.00; BoE pricing is now heavily in favour of an unchanged outcome at the May meeting.

Commodities diverge given the marked risk-off action with crude and base metals pressured while precious metals glean incremental support as the USD offsets the benefit of haven demand.

Specifically, WTI and Brent are under USD 68.00/bbl and USD 74.00/bbl respectively which places them at the mid/lower-end of the current WTD USD 64.12-71.67/bbl and USD 70.12-77.44/bbl parameters.

Spot gold is incrementally firmer though is yet to convincingly surpass USD 2k/oz while base metals are dented by the aforementioned tone with 3-month LME Copper slipping further below 9k to a USD 8940 low.

Russia could recommend a temporary halt to wheat and sunflower exports, via Vedomosti; due to the sharp decline in prices.

US base at North-east Syria’s Al-Omar oil field has been targeted in an attack, according to security sources cited by Reuters.

UBS maintains a positive outlook on Gold and targets USD 2050/oz by the end of the year.

ECB is likely to reassure EU leaders regarding bank stability on Friday and is to call for EU deposit insurance, according to Reuters.

ECB’s Nagel says it is necessary to increase policy rates to sufficiently restrictive levels, whilst the APP wind down should accelerate from Q3. Domestic price pressures are likely to last for longer, whilst underlying inflation is increasingly concerning. There are signs of second-round effects from inflation-induced higher wage increases.

ECB’s Nagel says there is often a bumpy road after similar instances in the banking sector, not surprising there have been market moves. On Deutsche Bank’s share slide, ECB’s Nagel will not comment.

BoE’s Bailey says rates will rise again if firms hike prices, via BBC; “If all prices try to beat inflation we will get higher inflation,”

DATA RECAP

UK GfK Consumer Confidence (Mar) -36 vs. Exp. -36.0 (Prev. -38.0)

UK Retail Sales MM (Feb) 1.2% vs. Exp. 0.2% (Prev. 0.5%); Ex-Fuel MM (Feb) 1.5% vs. Exp. 0.1% (Prev. 0.4%, Rev. 0.9%)

UK Retail Sales YY (Feb) 3.5% vs. Exp. -4.7% (Prev. -5.1%); Ex-Fuel YY (Feb) -3.3% vs. Exp. -4.7% (Prev. -5.3%, Rev. -5.4%)

UK Flash Services PMI (Mar) 52.8 vs. Exp. 53.0 (Prev. 53.5); Manufacturing PMI (Mar) 48.0 vs. Exp. 49.8 (Prev. 49.3)

UK Flash Composite PMI (Mar) 52.2 vs. Exp. 52.8 (Prev. 53.1)

EU S&P Global Composite Flash PMI (Mar) 54.1 vs. Exp. 51.9 (Prev. 52.0)

EU S&P Global Manufacturing Flash PMI (Mar) 47.1 vs. Exp. 49.0 (Prev. 48.5); Services Flash PMI (Mar) 55.6 vs. Exp. 52.5 (Prev. 52.7)

German S&P Global Composite Flash PMI (Mar) 52.6 vs. Exp. 51.0 (Prev. 50.7)

German S&P Global Manufacturing Flash PMI (Mar) 44.4 vs. Exp. 47.0 (Prev. 46.3); Services Flash PMI (Mar) 53.9 vs. Exp. 51.0 (Prev. 50.9)

French S&P Global Composite Flash PMI (Mar) 54.0 vs. Exp. 51.8 (Prev. 51.7)

French S&P Global Manufacturing Flash PMI (Mar) 47.7 vs. Exp. 48.0 (Prev. 47.4); Services Flash PMI (Mar) 55.5 vs. Exp. 52.5 (Prev. 53.1)

GEOPOLITICS

Ukraine’s top ground forces commander said Ukrainian troops are to launch a counterassault soon as Russia’s large winter offensive weakens without capturing the eastern city of Bakhmut, according to Reuters.

Russian Security Council Deputy Chairman Medvedev says cannot rule out that Russian forces will need to reach Kyiv or Lviv to ‘destroy the infection’, according to RIA.

US Pentagon said the US conducted air strikes in Syria which targeted an Iranian-backed group in response to a deadly UAV attack, according to Reuters and Wall Street Journal.

US Treasury Secretary Yellen said sanctions on Iran have created a real economic crisis in that country and the US is constantly looking at ways to strengthen Iran sanctions but added that sanctions may not be sufficient to change a country’s behaviour, according to Reuters.

China’s Defence Ministry said it monitored and drove away a US destroyer which entered the South China Sea Paracel Islands on Friday again and sternly demands the US to immediately stop such provocations, according to Reuters.

North Korea said it conducted an important weapon test and firing drill from March 21st-23rd, while it added that it conducted a new underwater attack system in which it tested a new nuclear underwater attack drone and launched strategic cruise missiles. Furthermore, North Korea said its leader Kim guided the military activities and that Kim seriously warned enemies to stop reckless anti-North Korea war drills, according to KCNA.

South Korean President Yoon said they will step up security cooperation with the US and Japan against North Korea’s nuclear and missile provocations, while he said they will make sure North Korea pays the price for its reckless provocations, according to Reuters.

CRYPTO

Bitcoin is softer on the session but within very confined sub USD 500 parameters as it remains somewhat detached from the broader risk-off action currently being seen.

APAC TRADE

APAC stocks were mostly subdued after the recent bout of central bank rate hikes and choppy performance stateside where Wall Street just about closed higher amid a dovish market repricing of Fed rate expectations.

ASX 200 was lower with risk appetite sapped by weak PMI data which returned to contraction territory.

Nikkei 225 lacked conviction after the latest inflation data printed mostly in line with estimates.

Hang Seng and Shanghai Comp. retreated after the central bank drained liquidity and as participants digest earnings releases, while it was also reported that the US added 14 Chinese entities to the red flag list.

NOTABLE ASIA-PAC HEADLINES

HKMA said Hong Kong has very little exposure to the European and US banking situation, while it needs to monitor the situation carefully for any further volatility but is not concerned about risks to the Hong Kong banking sector.

China is to extend some tax relief measures, according to local media.

DATA RECAP

Japanese National CPI YY (Feb) 3.3% vs. Exp. 3.3% (Prev. 4.3%); Ex. Fresh Food YY (Feb) 3.1% vs. Exp. 3.1% (Prev. 4.2%)

Japanese National CPI Ex. Fresh Food & Energy YY (Feb) 3.5% vs. Exp. 3.4% (Prev. 3.2%)

Australian Composite PMI (Mar P) 48.1 (Prev. 50.6)

2 c. ASIAN AFFAIRS

ASIAN AND AUSTRALIAN CLOSINGS//EUROPE OPENING TRADING:

FRIDAY MORNING/THURSDAY NIGHT